13 Active Canada Investors in 2026 (Check Sizes + Sector Fit + Intro Paths)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

TL;DR — Canadian VC in 2026: Cohere raised $500M at $6.8B in August 2025 led by Radical + Inovia, extended to $7B in September 2025. Waabi closed a $1B raise in January 2026 (the largest in Canadian history) co-led by Khosla + G2 with $250M milestone from Uber. Radical Ventures closed a $650M USD Fund 4 in October 2025 — the biggest early-stage AI fund raised in Canada. Georgian manages $5.9B AUM and is raising a fresh $1B fund. OMERS Ventures refocused on Canada in 2025 with $5M-$25M tickets from Fund IV. SR&ED's enhanced 35% ITC threshold jumped to $4.5M and capital expenditures are eligible again. Canada now has 33 unicorns (Feb 2026, Tracxn) with AI/FinTech/HealthTech capturing 75% of VC funding. If you are raising from Canada in 2026, the capital is real — but selectivity is too.

Last updated: April 2026

I spent two years at Backed VC and Target Global watching CEE and cross-Atlantic founders raise — including from Toronto, Montreal, Vancouver, and Waterloo. Canada is weirdly underrated: world-class technical talent, Vector Institute and Mila feeding AI founders directly into Radical and Inovia, a weak CAD that makes engineering costs structurally lower than US equivalents, and a capital stack that ranges from government-backed BDC all the way to globally competitive firms like Georgian and OMERS.

The catch: the best Canadian investors are highly pattern-driven and very picky about fit — so targeting matters more than blasting your deck. In 2026, the signal is clearer than ever. Cohere's $500M Series D at $6.8B (led by Radical and Inovia in August 2025, extended to $7B in September) and Waabi's $1B round in January 2026 (the largest raise in Canadian history, co-led by Khosla Ventures and G2 Venture Partners with Uber commitment) both show what Canadian founders can build — and who is writing the checks when they do.

This guide is for founders who want to actually close rounds, not window-shop the ecosystem. It covers the 13 Canadian investors writing real checks in 2026, what they look for, how to pitch them, and how to run the fundraise itself so you do not burn 6 months getting ghosted.

Before you start outreach, build a proper data room. Canadian VCs move fast when convinced — how you run your fundraise is a direct signal of how you run the company. Peony Business at $30/admin/month gives you NDA gates on every share link, page-level analytics showing which partners actually read your financials, and basic AI document Q&A. Step up to Peony Data Room at $52/admin/month when you want dynamic watermarks tied to each investor's email and the moderated Q&A workflow that drafts answers with page citations. Legacy platforms like Intralinks charge $5K-$20K per deal for these capabilities. Peony delivers the same intelligence at transparent pricing for the $1M-$500M deal range that covers almost every Canadian seed and Series A round.

1. How to pick the right Canadian investor (the fast filter)

A. Start with stage (and be honest about it)

Canadian funds can be very stage-specific in 2026:

- Pre-seed (first cheque, CAD $500K-$2M): Garage Capital, Panache Ventures, Real Ventures (early), BDC Seed Venture Fund

- Seed (first institutional round, CAD $2M-$8M): Golden Ventures, Real Ventures, Version One Ventures, Radical Ventures (AI), Inovia Capital (early tickets)

- Series A (CAD $5M-$20M): Inovia Capital, Relay Ventures, Vanedge Capital, BDC Capital, Radical (AI)

- Series B and beyond (CAD $15M+): Georgian, OMERS Ventures, Portage Ventures (fintech), Inovia Capital (growth), BDC Capital Growth

If you pitch "Series A" when you're pre-seed, you'll get polite pass energy (and you'll waste your best intros).

B. Match the fund's "native habitat"

Don't just ask "do they invest in my sector?" Ask:

- Do they win in my business model (SaaS, marketplace, deep tech, fintech infra, AI)?

- Do they have a real edge for me (Toronto-Waterloo AI talent, hiring network, US enterprise intros, follow-ons)?

- Are they set up to support my geography (Toronto/Montreal/Vancouver/Waterloo/Calgary + US expansion)?

C. Optimize for "follow-on capacity"

In Canada, follow-on matters a lot in 2026 because:

- CVCA data shows Canadian VC trended to fewer, larger financings in 2025 — and that pattern continued into Q1 2026

- Your best outcome is often: Canadian lead + strong US co-investor (Cohere's $6.8B round had Radical + Inovia leading with AMD Ventures, NVIDIA, and Salesforce Ventures participating)

- The $1B government commitment to VC starting 2026 flows mostly through existing funds (BDC, Inovia, Radical, Georgian) — so you want those firms as LP-advantaged anchors

So look for firms that can credibly support you through the next round (or have a history of bringing in the right syndicate).

D. Know the Canada-specific deal dynamics in 2026

A few practical realities:

- BDC Capital is a major player and often shows up across the ecosystem via direct VC AND as a fund-of-funds LP in Inovia, Radical, and others

- SR&ED (Scientific Research and Experimental Development) is back on the table: 2026 enhanced ITC threshold raised from $3M to $4.5M and capital expenditure eligibility restored. BC also modernized its provincial SR&ED in Budget 2026

- The weak Canadian dollar (CAD ~1.40/USD) means your USD-invoice revenue looks oversized relative to CAD-denominated costs — a real advantage when pitching US-based growth investors

- Many top Canadian funds invest across North America but still have a strong "Canada-first" sourcing advantage (especially at seed)

E. Use a simple scoring rubric (steal this)

Score each investor 1–5 on:

- Stage fit

- Sector / thesis fit

- Check size + follow-on ability

- Your "unfair advantage" with them (warm intros, shared operators, alumni network)

- Evidence they're active right now (recent deployments, new funds, visible 2025-2026 momentum)

Which Canadian investor fits your stage/sector? (if/then)

| If you are... | Then your first 3 calls should be... | Why |

|---|---|---|

| A Toronto SaaS founder at pre-seed (CAD $500K-$1.5M) | Panache → Golden → BDC Seed | Fast stackable pre-seed with government-backed co-investor |

| A Toronto B2B SaaS founder at seed (CAD $3M-$6M) | Golden → Inovia → Real Ventures | Active seed leads with growth-stage follow-on ability |

| A Toronto AI founder raising Series A | Radical → Inovia → Georgian | Cohere template: Radical + Inovia co-lead |

| A Waterloo technical/dev-tools founder at pre-seed | Garage Capital → Panache → BDC Seed | Garage is operator-led with deep University of Waterloo ties |

| A Montreal AI/deep-tech founder | Real Ventures → Inovia → Radical (if AI) | Montreal's AI gravity (Mila) + Real's Montreal roots |

| A Vancouver B2B SaaS or deep tech founder | Vanedge → Version One → Inovia | Vanedge leads Series A, Version One leads seed |

| A Calgary climate or energy tech founder | BDC Capital + Golden Ventures + US co-leads | BDC's cleantech mandate + Golden's climate thesis |

| A US founder wanting Toronto-Waterloo AI talent | Radical → Inovia → Golden | All three invest cross-border and value Toronto-Waterloo density |

| A fintech founder at Series A ($10M-$25M) | Portage → Relay → Inovia | Portage's $5.7B fintech specialization |

| A Series B-plus growth founder | OMERS → Georgian → Inovia (growth) | Three largest Canadian growth checks |

2. The 13 Canadian investors actually writing checks in 2026

1) BDC Capital

Why they're top-tier: BDC Capital is Canada's backbone VC investor — direct VC across all stages AND the largest LP in the Canadian VC fund-of-funds universe. They've been invested in Inovia's Funds II, III, IV, V, and Growth Fund I, and are top investors in the Inovia portfolio with 11 companies. In 2025 they co-led Cohere's $500M Series D alongside Radical and other institutional backers.

Recent activity: BDC's Seed Venture Fund remains one of the most active pre-seed vehicles in Canada. BDC Capital's direct VC teams cover deep tech, cleantech, women-led and diverse founder funds, and late-stage growth. The $1B additional Canadian government VC commitment starting 2026 flows significantly through BDC's fund-of-funds arm.

Stage: Seed through growth. Direct investment sizes vary from ~$250K (seed) to $5M-$20M (Series B+).

Sectors: Deep tech, cleantech, fintech, enterprise SaaS, life sciences, AI.

How to approach: Direct application via bdc.ca, or (much better) via warm intro through an existing BDC portfolio CEO or an LP partner at Inovia/Radical/Golden.

Founder angle: If you're building in Canada and want a credible anchor with longevity plus access to the broader LP network, BDC is an ecosystem "gravity well."

2) Inovia Capital

Why they're top-tier: Inovia is the most institutional Canadian early-to-growth VC platform with $2.5B USD / $3.5B CAD AUM and clear 2026 deployment momentum. They co-led Cohere's $500M Series D in August 2025, one of the largest Canadian rounds of the year. In 2025 they launched a $416M CAD continuation fund to stick with winners through IPO, and are raising Fund VI in 2026 with a similar size/strategy to Fund V and a clear AI focus.

Recent activity: In 2024 they deployed $194M across 55 investments. Promoted two principals to partner in early 2026 ahead of the Fund VI raise. Active across pre-seed, seed, Series A, and growth with continuation vehicle support for mature companies.

Stage: Pre-seed to growth. Initial checks $500K-$15M; follow-on to exit via continuation fund.

Sectors: Enterprise software, AI, fintech, marketplaces, consumer, cybersecurity.

How to approach: Warm intro via portfolio founders is the fastest path. Partners are highly visible on LinkedIn and at TechTO events.

Founder angle: Inovia is the default "Canadian lead + global support" VC for software founders who want to build from Canada but compete globally. Cohere, Lightspeed, Clio, and Top Hat all went through Inovia.

3) Radical Ventures

Why they're top-tier: Radical is the single most globally visible Canadian firm in AI in 2026 — they closed a $650M USD early-stage AI Fund 4 in October 2025 (their largest to date), co-led Cohere's Series D, and have 6 unicorns in their portfolio including Cohere, Waabi, and Xanadu. They invested in 76 companies as of December 2025 with 12 new investments in the trailing 12 months.

Recent activity: Fund 4 is their fourth dedicated early-stage AI vehicle and sixth overall. They maintain offices in Toronto, London, and San Francisco — transatlantic by design but deeply rooted in the Toronto AI ecosystem. CPP Investments is a major LP.

Stage: Seed and Series A (with growth follow-on through later funds).

Sectors: AI only — science, infrastructure, enterprise, consumer AI applications, defense AI.

How to approach: Warm intros through existing portfolio founders or through the Vector Institute / University of Toronto AI networks. Cold inbound on strong technical teams does get read.

Founder angle: If you're AI and legit, Radical is a "signal investor" that upgrades your entire round. Their brand pulls US institutional capital into Canadian rounds.

4) Georgian

Why they're top-tier: Georgian is the largest growth-stage Canadian software VC at $5.9B AUM (as of Dec 31, 2025), with 80+ portfolio companies and a dedicated AI Lab. In 2025 they led Replit's $400M Series D and are actively raising a new $1B fund with $100M strategic investment from Navigator Global Investments (March 2026, 4.5% passive equity stake in Georgian itself).

Recent activity: Currently deploying from Growth Fund VI and Alignment Fund II. Published 2025 AI Adoption Benchmarks Report with 32% of surveyed enterprises reporting AI deployment and 48% of growth-stage respondents reporting ROI gains.

Stage: Series B through late growth. Initial checks $10M-$50M+ (up to $100M+ for platform bets like Replit).

Sectors: B2B software, applied AI, trust/security platforms, data infrastructure.

How to approach: Warm intro through portfolio CEOs is best. Georgian also runs founder events and AI Lab content that gets read by their IC.

Founder angle: Georgian is the Canadian VC you want on your cap table for Series B and beyond. Their AI Lab is a genuine value-add, not marketing.

5) Golden Ventures

Why they're top-tier: Toronto-based, seed-focused, and very active. Golden publicly lists pre-seed/seed focus, initial cheques $500K-$3M, and closed Fund V at over $100M in 2024 targeting high-potential founders in AI, climate, blockchain, and quantum. They are one of the most founder-recommended seed leads in Canada.

Recent activity: Fund V is actively deploying in 2026. Notable portfolio includes Ada, Hopper (now a unicorn), Wealthsimple, and Shopify Pay partners.

Stage: Pre-seed and seed (seed-plus in select cases).

Sectors: Sector-agnostic — they respond to team quality and wedge clarity. Strong representation in AI, climate, blockchain, and quantum.

How to approach: Warm intros through existing founders. Golden's associate team is reachable via LinkedIn and responsive to clear, specific pitches.

Founder angle: Great if you want a seed lead that's founder-friendly, pattern-rich, and can bridge you toward an Inovia or US Series A.

6) Panache Ventures

Why they're top-tier: Panache positions itself as Canada's pre-seed fund with first cheques up to $1.5M from a $100M Fund II. They have done 250+ investments since 2017 and continue to invest in 2026 (most recent documented investment: Canada Rocket Company seed round in January 2026). Montreal-headquartered with strong French-Canadian founder network.

Recent activity: Fund II is actively deploying. They frequently co-invest with BDC Seed, Real Ventures, and Golden.

Stage: Pre-seed (dominant) and first-money seed.

Sectors: Broad Canadian pre-seed — SaaS, marketplaces, fintech, climate, consumer.

How to approach: Direct via panache.vc or warm intros through Montreal/Toronto ecosystem.

Founder angle: If you're truly early (idea stage to first traction), Panache is one of the cleanest fits in Canada.

7) Real Ventures

Why they're top-tier: Real Ventures is one of the most founder-recognized early-stage firms in Canada, with deep Montreal roots and a strong AI thesis powered by proximity to Mila. They explicitly position themselves as a leading Canadian early-stage VC that leans into founder development.

Recent activity: Still actively investing in 2026 though they have not publicly announced a new fund close recently — deployment is more measured than during their 2018-2021 peak years.

Stage: Pre-seed to seed-plus (typical checks $500K-$2M).

Sectors: AI (Montreal/Mila-anchored), software, consumer, and founder-driven stories.

How to approach: Warm intros through Montreal startup community (Mila, OSMO, Startupfest).

Founder angle: If you want an investor who leans in early and supports the human side of scaling — especially as a Montreal or Quebec founder — Real is built for that.

8) OMERS Ventures

Why they're top-tier: OMERS Ventures is the VC arm of one of Canada's largest pension funds — effectively giving it deep pockets, long time horizons, and patient institutional weight. In 2025 they strategically refocused on Canada after a period of aggressive global expansion. Fund IV is a $750M vintage deploying now.

Recent activity: Published VC Predictions for 2026 highlighting a return to discipline and physical AI opportunities at UofT, Waterloo, McGill, and UBC. Active in enterprise software, fintech, AI/infra, and vertical SaaS.

Stage: Series A through growth ($5M-$25M initial tickets, larger for co-leads).

Sectors: Fintech, vertical software, enterprise SaaS, AI/infrastructure, physical AI/robotics.

How to approach: Warm intros through existing Canadian angels, portfolio CEOs, or growth-stage operators. OMERS is plugged into the Toronto growth-stage network.

Founder angle: Strong intros from Canadian angels, growth funds, or founders help a lot. Best fit if you're past traction-proving and ready to scale with a patient institutional lead.

9) Vanedge Capital

Why they're top-tier: Vancouver-based early-growth VC with over $500M AUM and a long-running practice in technical-heavy software — data, AI, security, interactive tech. Vanedge has led and co-led Series A rounds in Canada for over a decade and is the default Vancouver Series A lead.

Recent activity: Continuing to deploy from their most recent fund. Portfolio spans data infrastructure, AI, cybersecurity, and interactive technology.

Stage: Series A (with seed-plus and Series B selectively). Typical checks $2M-$8M.

Sectors: Technical B2B software, AI infrastructure, data platforms, security, interactive tech.

How to approach: Warm intros through Vancouver tech ecosystem (UBC, BCTech Summit, Innovate BC).

Founder angle: Vanedge is a strong option if your company is more "deep tech / deep software" than GTM-first SaaS, and you want a Canadian lead comfortable with longer technical roadmaps.

10) Garage Capital

Why they're top-tier: Waterloo-based pre-seed/seed fund founded by operators, with strong roots in the University of Waterloo ecosystem and a "built by founders" identity. Garage is the go-to pre-seed check for Waterloo technical founders — they know the ecosystem cold.

Recent activity: Actively deploying from their most recent fund. Portfolio includes dev-tools, vertical SaaS, and AI-infrastructure startups emerging from the Toronto-Waterloo corridor.

Stage: Pre-seed and seed. Typical checks $200K-$750K.

Sectors: B2B software, dev tools, AI tools, technical products — especially Toronto-Waterloo corridor companies.

How to approach: Direct outreach or warm intros through University of Waterloo alumni network and Velocity.

Founder angle: Garage is a great first institutional check if you're early, technical, and want hands-on feedback from investors who've built and scaled companies themselves.

11) Portage Ventures

Why they're top-tier: A major fintech platform within Sagard with $5.7B AUM and global fintech focus across stages — insurance, consumer/SMB finance, wealth/asset management, and fintech enablers. In January 2026 they took over select assets from Point72 Ventures' fintech portfolio via a $280M continuation vehicle (PPCVI) backed by Goldman Sachs Alternatives.

Recent activity: Actively deploying Portage Ventures IV and Portage Capital Solutions. Consolidating fintech leadership across North America via the Point72 acquisition. 115+ portfolio companies.

Stage: Seed through Series C.

Sectors: Fintech only — insurance, consumer and SMB finance, wealth management, asset management, fintech infrastructure.

How to approach: Warm intros through portfolio fintech CEOs or Sagard's network.

Founder angle: If you're fintech and want a specialist with real industry network, Portage is a serious contender.

12) Relay Ventures

Why they're top-tier: Long-running Canadian firm with a clear early-stage entry point — Relay publicly highlights pre-seed + seed entry and ongoing founder support across stages with a current deploying fund. Toronto-based with meaningful Silicon Valley connectivity.

Recent activity: Continuing to deploy in 2026. Mobile, marketplace, and vertical software focus. Not as loud publicly as Inovia or Golden but consistently writing checks.

Stage: Pre-seed, seed, and Series A (typical checks $500K-$5M).

Sectors: Early-stage software, mobile, vertical SaaS, marketplaces.

How to approach: Warm intros through portfolio founders.

Founder angle: Relay can be a great early believer if you're building something that needs sharp go-to-market execution and value operator-heavy feedback.

13) Version One Ventures

Why they're top-tier: Vancouver-based early-stage fund that stays visibly active and publishes recent investments. Their thesis leans toward mission-driven founders with modern internet/software DNA — often crypto/fintech-adjacent themes. Founded by Boris Wertz (former CEO of AbeBooks) with strong West Coast networks.

Recent activity: Active through 2025-2026 with pre-seed and seed deals. Strong in Vancouver but invests across North America.

Stage: Pre-seed and seed (typical checks $250K-$1.5M).

Sectors: Software, mission-driven consumer internet, crypto/web3, marketplaces, climate.

How to approach: Warm intros through Vancouver ecosystem and portfolio CEOs. Boris is active on Twitter.

Founder angle: Version One is a strong option if you want early conviction with a West Coast/global mindset and value mission alignment.

3. What Cohere and Waabi tell you about 2026 Canadian fundraising

Two rounds define the 2026 Canadian landscape:

Cohere's $500M Series D at $6.8B (August 2025, extended to $7B in September 2025) — led by Radical Ventures and Inovia Capital with participation from AMD Ventures, NVIDIA, PSP Investments, Salesforce Ventures, HOOPP, and Cisco. The takeaway: Canadian-led institutional rounds pull global strategic capital when the technical quality is there. Cohere did not need to move to the US to raise $500M.

Waabi's $1B raise (January 2026) — $750M Series C co-led by Khosla Ventures and G2 Venture Partners with a $250M milestone commitment from Uber, plus strategic participation from NVentures (NVIDIA), Volvo Group Venture Capital, and Porsche Automobil Holding SE. The largest fundraise in Canadian history. Uber will exclusively deploy at least 25,000 Waabi autonomous vehicles on its ridehail platform. The takeaway: physical AI and deep tech from Canada is now attractive to global growth investors when the team quality and applied research depth is there.

Both rounds had Radical Ventures anchoring or backing — a direct signal that Radical is the single most consequential Canadian VC in 2026 for AI-driven companies.

4. Cross-border pitch tips for US founders raising from Canadian VCs in 2026

If you are a US founder considering raising from Canadian investors — or building in Canada to access Toronto-Waterloo AI talent — the dynamics shift:

-

Pick the cross-border-friendly funds first. Radical (offices in Toronto, London, SF), Inovia (Montreal-Toronto-New York), Golden (North America-wide), and Relay (Toronto + SF) explicitly invest cross-border. BDC is Canada-only by mandate.

-

Lead with the Canadian structural advantage. Don't apologize for being US-based — show why a Canadian investor gives you a structural edge: Toronto-Waterloo AI talent density (3x lower cost than SF equivalent engineers for 2026 CAD weakness), Vector Institute / Mila research ties, SR&ED 35% refundable tax credit on Canadian R&D spend, and customer proximity in the Toronto-Waterloo-Montreal corridor.

-

De-risk the "Canada discount." Some Canadian VCs historically valued companies slightly lower than US equivalents. Proactively show your US expansion plan, US hiring plan, and revenue diversification to unlock US-comparable valuations.

-

Use the CAD weakness to your advantage. With CAD ~1.40/USD in early 2026, USD-invoiced revenue looks oversized relative to CAD-denominated engineering costs. This is a real, sustained gross margin advantage over US-only competitors.

-

Send a Peony Business data room link, not a PDF. Cross-border rounds compound information control challenges — NDA gates, and dynamic watermarks on the Data Room plan ($52/admin/month), matter more when investors span multiple jurisdictions.

5. Five quick tips for pitching Canadian VCs in 2026 (that actually work)

-

Lead with "why this wins from Canada." Even if you're going global, show how your team/location is an advantage (Toronto-Waterloo AI talent, Mila research ties, SR&ED runway extension, cost structure from CAD weakness, customer proximity).

-

Make your ask match the stage. Pre-seed: prove insight + velocity. Seed: prove traction + repeatability. Series A: prove growth engine + retention + scaling plan.

-

Cite 2025-2026 comparables specific to your sector.

- AI: Cohere Series D ($6.8B, Radical + Inovia), Waabi Series C ($1B, Khosla + G2)

- Fintech: Portage's Point72 takeover ($280M continuation vehicle)

- Growth SaaS: Replit Series D ($400M, Georgian-led)

-

Name the specific partner thesis you match. The fastest "yes" is when the investor feels like: "this is exactly what we're built to back." Inovia wants software/AI global category leaders. Radical wants AI-only, technically deep teams. Golden wants founder quality and wedge clarity. Georgian wants growth-stage B2B with applied AI.

-

Treat intros like product distribution. Don't ask for "an intro to the firm." Ask for:

- a specific partner

- a specific reason

- a specific timing window …and make it easy for the intro-giver to forward your 3-sentence blurb. Use a professional data room like Peony to organize materials with AI-powered organization and track investor engagement with page-level analytics.

6. Quick guide: which Canadian investor matches your situation

| Your situation | Best first calls | Why |

|---|---|---|

| CAD $500K-$1.5M pre-seed, Toronto SaaS | Panache + Golden + BDC Seed | Fast, stackable, government-backed co-invest |

| CAD $500K pre-seed, Waterloo technical | Garage + Panache + angel syndicate | Garage's UWaterloo native edge |

| CAD $2M-$5M seed, Toronto or Montreal | Golden + Real Ventures + Inovia early | Founder-friendly, Montreal AI proximity |

| CAD $3M-$8M Series A, AI-focused | Radical + Inovia + Georgian (if B2B) | Cohere template — AI-first Canadian lead |

| CAD $5M-$15M Series A, B2B SaaS | Inovia + BDC Capital + US co-lead | Canadian lead + US strategic |

| CAD $10M-$25M Series A, fintech | Portage + Inovia + Relay | Portage is the fintech specialist at $5.7B AUM |

| CAD $15M+ Series B, growth software | Georgian + OMERS + Inovia growth | Three largest Canadian growth checks |

| Vancouver B2B SaaS or deep tech | Vanedge + Version One + Inovia | Vanedge = Vancouver Series A default |

| Physical AI / robotics | Radical + Inovia + international (Khosla, Waabi template) | Waabi + Cohere precedent |

| US founder targeting Toronto-Waterloo AI talent | Radical + Inovia + Golden | All three cross-border + AI-capable |

Why professional data rooms matter for Canadian fundraising

Canadian startups compete for global capital in 2026 — especially at Series A and beyond, where Inovia, OMERS, Georgian, and Portage run institutional-grade diligence cycles. How you present your materials in the first meeting sets the ceiling for the entire process.

Peony helps Canadian founders create investor-ready data rooms in minutes. AI auto-indexing organizes your cap table, financial model, customer contracts, and product documentation into a professional folder structure that reads the same to a partner at Inovia as it does to a growth-stage investor at Georgian or a US co-lead at Khosla.

Key capabilities:

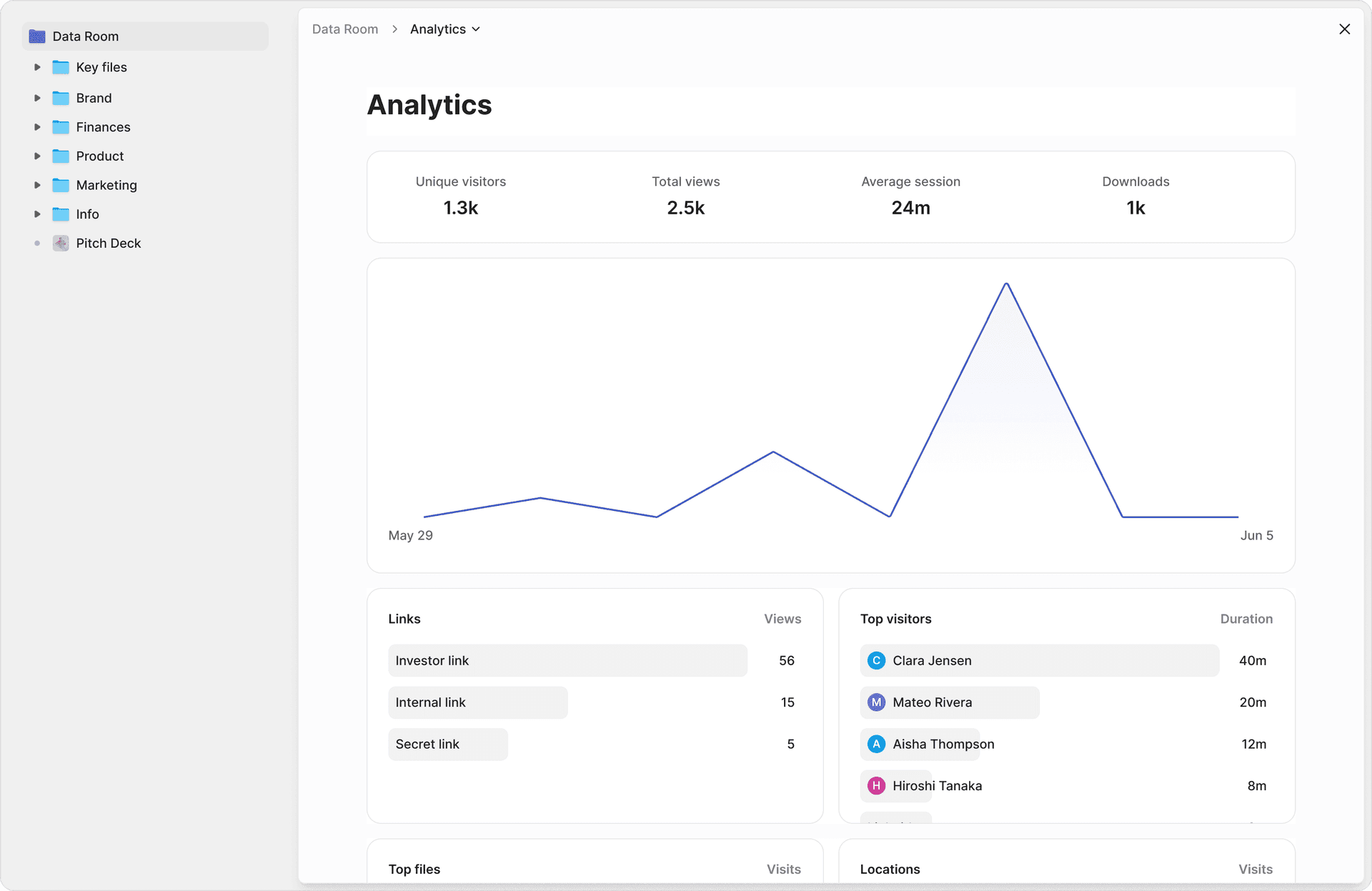

- Page-level analytics show which documents each investor read and for how long — so you know who is genuinely engaged across your 15-VC outreach list

- Dynamic watermarks embed each viewer's identity on every page, deterring forwarded leaks in a relationship-driven ecosystem where Canadian VCs share notes

- Screenshot protection blocks AND logs capture attempts

- NDA gates require acceptance before the first page loads

- AI-powered Q&A drafts answers to investor questions with page citations, then routes through your team for approval

- E-signatures with AI field detection for SAFEs, convertible notes, and NDAs

- AI Redaction identifies PII and sensitive financial data before external sharing

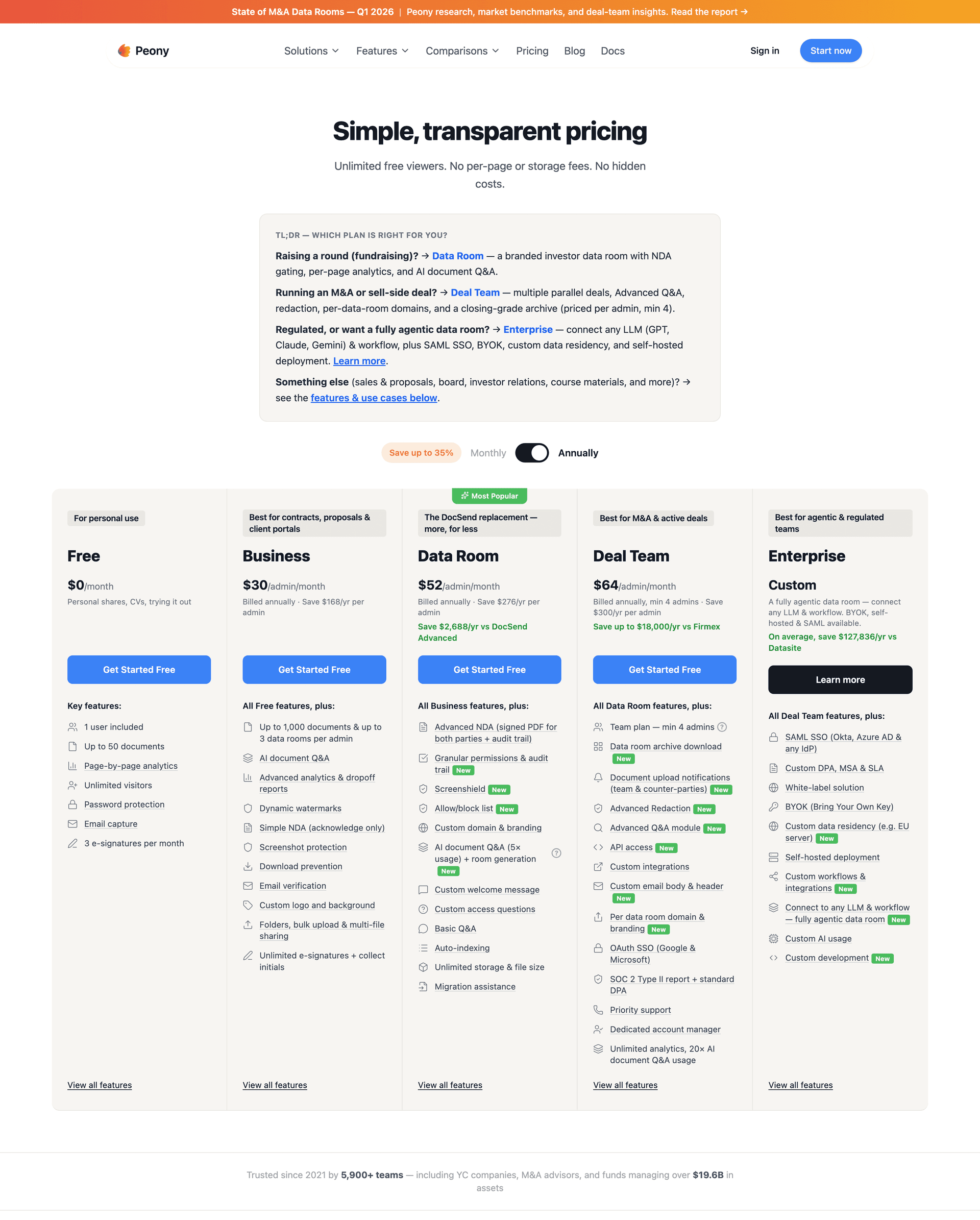

Transparent pricing: Peony Business at $30/admin/month (full fundraise toolkit) with Peony Data Room at $52/admin/month when you want unlimited rooms, AI room generation, and the moderated Q&A workflow. For a 3-person Canadian founding team, that is $90-$156/month — vs. $5K-$20K per deal for Intralinks or Datasite on a $1M-$500M deal range.

Bottom line

Raising in Canada in 2026 requires matching your stage, sector, geography, and international ambition to the right investors. The 13 on this list are actively deploying capital — but they are selective.

At pre-seed: Panache, Garage, and BDC Seed are your stackable Canadian trio. At seed: Golden, Real, and Version One for software; Radical for AI. At Series A: Inovia, BDC Capital, Relay, and Vanedge lead or co-lead rounds; Radical anchors AI rounds. At Series B and beyond: Georgian, OMERS, Portage (fintech), and Inovia's growth fund are the four largest Canadian growth checks. Cross-border: Radical, Inovia, and Golden all invest across North America.

The 2025-2026 ecosystem signals — Cohere's $7B valuation, Waabi's $1B raise, Radical's $650M USD Fund 4, Georgian's $1B fundraise in progress, and Canada's 33 unicorns — all point to the same conclusion: Canadian founders no longer need to move to the US to raise institutional capital.

Bring round math, "why this wins from Canada" narratives, stage-appropriate traction, and a clean Peony data room to every pitch. In a relationship-driven ecosystem, process discipline is a signal — and signals compound.

Ready to pitch Canadian investors? Set up your Peony data room in under 5 minutes with AI auto-indexing, NDA gates, dynamic watermarks, and page-level analytics. See Peony pricing here.

FAQ

I am a SaaS founder in Toronto raising a $5M Series A in 2026 — which Canadian VCs actually lead at this stage and check size?

For a $5M Series A in Canadian SaaS in 2026, your strongest leads are Inovia Capital, which manages $2.5B USD ($3.5B CAD) AUM and is raising Fund VI in 2026 with a software/AI focus; BDC Capital, Canada's largest and most active VC investor which co-led Cohere's $500M Series D at $6.8B in August 2025; and Georgian, a growth-stage investor with $5.9B AUM that led Replit's $400M Series D and is raising a new $1B fund. Golden Ventures writes initial cheques of $500K to $3M from its $100M Fund V and could co-lead or bridge you to A. OMERS Ventures refocused on Canada in 2025 and writes $5M to $25M tickets from Fund IV ($750M vintage). For a 6-person Toronto B2B SaaS team at $1M ARR targeting a $5M Series A, Inovia + OMERS co-lead with BDC participation is the cleanest 2026 pattern. Organize your metrics and financial model in a Peony Business data room at $30 per admin per month — page-level analytics show you which partners at BDC or Inovia actually read your retention charts versus skimmed the deck, something Google Drive or Dropbox cannot detect on any plan.

I'm raising across multiple stages from Panache pre-seed to Inovia growth — what check sizes do Canadian VCs actually write in 2026?

Canadian VC check sizes in 2026 span a wide range. At pre-seed, Panache Ventures writes first cheques up to $1.5M and Garage Capital writes $200K to $750K from Waterloo. At seed, Golden Ventures writes $500K to $3M from Fund V, Real Ventures writes $500K to $2M, and Version One Ventures writes $250K to $1.5M. At Series A, Relay Ventures writes $1M to $5M, Vanedge Capital writes $2M to $8M from over $500M AUM, and Inovia Capital writes $3M to $15M. At growth-stage and Series B-plus, OMERS Ventures writes $5M to $25M per round, Georgian writes $10M to $50M-plus from $5.9B AUM, and Portage Ventures writes fintech growth checks from $5.7B AUM. Radical Ventures deploys from its $650M USD Fund 4 (closed October 2025) at seed and Series A for AI companies, with tickets typically $2M to $15M. When you are comparing term sheets from multiple Canadian firms, you want a Peony Business data room where page-level analytics show which investors spent the most time reviewing your financial model versus skimming the executive summary — DocSend gives you open-or-not tracking at best, and Google Drive gives you nothing at all.

I am a US-based founder considering raising from Canadian VCs to access Toronto-Waterloo AI talent in 2026 — how do I approach cross-border fundraising?

Several top Canadian VCs actively invest across North America in 2026 and the weak Canadian dollar (roughly 1.40 CAD/USD) makes Canadian engineering talent structurally cheaper than US equivalents. Radical Ventures runs offices in Toronto, London, and San Francisco and has 6 unicorns in portfolio including Cohere, Waabi, and Xanadu. Golden Ventures explicitly invests pre-seed through seed-plus across North America. Inovia Capital positions itself as a full-stack venture firm anchored in Canada that backs founders scaling globally. Version One Ventures in Vancouver backs early-stage mission-driven founders with a global mindset. Your pitch should lead with why a Canadian investor gives you a structural advantage — Toronto-Waterloo AI talent density, research ties to Vector Institute or Mila, cost structure from CAD weakness, or customer proximity in the Toronto-Waterloo-Montreal corridor. De-risk the Canada discount by proactively showing your US expansion plan. Peony Business at $30 per admin per month gives you NDA-gated links so you can share sensitive legal and financial documents across jurisdictions with identity verification for each viewer, and dynamic watermarks embed the viewer's name on every page so leaked copies are traceable. Google Drive or Dropbox shared folders offer no identity verification or leak tracing.

What do Canadian VCs look for in a startup data room before moving to partner meeting in 2026?

Canadian VCs are highly pattern-driven and stage-specific in 2026. At pre-seed they want insight plus velocity. At seed they want traction plus repeatability. At Series A they want a growth engine plus retention plus a scaling plan. Across all stages, investors pressure-test five areas: a clear why-this-wins-from-Canada narrative, unit economics with CAC payback, cohort retention data, a financial model with 18 to 24 months of runway, and a cap table showing ownership structure (SR&ED-backed runway extension counts — the 2026 enhanced ITC threshold raised to $4.5M and capital expenditures restored). BDC Capital looks for big markets and defensible tech. Inovia wants scalable software with global outcome potential. Georgian needs real revenue scale and strong retention plus AI-first product design. Radical wants technical AI differentiation. For a 7-person Toronto team preparing Series A diligence with three VCs in parallel, Peony Data Room AI auto-indexing organizes your uploads into a professional folder structure in under 3 minutes, and the Smart Q&A workflow lets partners submit diligence questions that get AI-drafted answers with cited page numbers — a task junior analysts spend 2 to 3 hours on per room at legacy platforms like Datasite.

I am raising a $2M seed round for a climate tech startup in Vancouver in 2026 — how do I share my pitch materials securely with fifteen investors?

Create individual share links with different permission levels for each investor rather than emailing PDF attachments. Version One Ventures in Vancouver backs mission-driven founders and is actively writing pre-seed to early seed checks. Vanedge Capital (over $500M AUM) is the Vancouver-based Series A lead for technical founders. Real Ventures supports founders from day one. Panache Ventures positions itself as Canada's pre-seed fund with first cheques up to $1.5M. With Peony Business at $30 per admin per month, you generate NDA-gated links that require each investor to verify their identity before viewing, and dynamic watermarks on the Data Room plan ($52 per admin per month) embed the viewer's name on every page so leaked copies are traceable. Screenshot protection blocks and logs any capture attempts. You can revoke access instantly if a conversation goes cold. For a 3-person Vancouver climate tech founding team running 15 parallel angel and VC conversations, that is $90 per month total versus the $5,000-plus per-deal minimums on legacy platforms like Datasite or Intralinks. Sending your deck as a plain PDF through email or DocSend means you lose all control the moment someone forwards it.

How long does a typical seed or Series A fundraise take in Canada in 2026 and how can I compress the timeline?

A well-run Canadian seed process in 2026 typically takes 6 to 10 weeks from first meeting to wire, while Series A can stretch 8 to 16 weeks because of heavier diligence and partner meeting cycles. CVCA data shows Canadian VC has trended to fewer, larger deals in 2025, so controlling your timeline matters more than spraying pitch decks. The biggest time sinks are follow-up document requests and scheduling partner meetings with firms like Inovia, BDC, Georgian, and OMERS. For a 5-person Toronto founder running your first institutional seed with 12 parallel VC conversations, you compress the process by having your data room fully loaded before first meetings so investors can self-serve diligence materials on their own schedule. Peony Business page-level analytics show you in real time which investors are actively reviewing documents — so you can time your follow-ups to land right after a partner finishes your financial model versus guessing blindly. Founders who treat intros like product distribution and run tight processes with organized data rooms consistently close faster than those emailing PDFs, something Google Drive and Dropbox cannot track.

Which Canadian VCs specialize in AI, fintech, or deep tech sectors in 2026?

For AI in 2026, Radical Ventures is your top target with a clear AI-only identity, $650M USD Fund 4 (closed October 2025), and 6 unicorns in portfolio including Cohere, Waabi, and Xanadu. Georgian focuses on growth-stage B2B software where AI, trust, and security themes matter and runs its own AI Lab — they led Replit's $400M Series D in 2025. Inovia's Fund VI (fundraising 2026) is explicitly software/AI-focused. For fintech, Portage Ventures manages $5.7B AUM with global fintech focus from seed to Series C (they took over Point72 Ventures' fintech portfolio in January 2026 via a $280M continuation vehicle). For deep tech and physical AI, Vanedge Capital in Vancouver backs technical software, data, AI infrastructure, security, and interactive tech with over $500M AUM. For a 4-person Toronto AI founding team at $500K ARR raising a $5M Series A, Radical + Inovia co-lead with Georgian participation is the cleanest 2026 pattern. When sharing proprietary technical documentation or financial models with specialized investors, Peony Data Room AI redaction identifies sensitive information before you share externally, and identity-bound access ensures only verified viewers can open your data room — a gap Google Drive fundamentally cannot close.

I am choosing between legacy platforms and newer tools for my Canadian fundraise — what is the best data room for a startup raising under $10M in 2026?

For Canadian startups raising under $10M in 2026, legacy platforms like Datasite and Intralinks charge $5,000 to $20,000 per deal and are built for $500M-plus M&A transactions. Sharing documents through Google Drive or Dropbox gives you zero analytics and no security beyond a basic password. Peony Business at $30 per admin per month is built for the $1M to $500M deal range that covers most Canadian seed and Series A rounds, with page-level analytics showing which pages each reviewer read and for how long, screenshot protection that blocks and logs capture attempts, dynamic watermarks with viewer identity, and NDA gates. Setup takes under 5 minutes versus weeks for legacy platforms. For a 5-person Waterloo team at $500K ARR running a $4M seed with Golden Ventures, Garage Capital, and BDC in parallel, that is $150 per month total — the page-level analytics alone justify the switch because you will know exactly which investors at BDC Capital or Inovia are doing real diligence versus kicking tires. Google Drive and Dropbox offer zero fundraising intelligence. DocSend charges per user and lacks screenshot protection and AI auto-indexing on its entry tier.

I am a Waterloo technical founder raising pre-seed from Garage Capital and Panache in 2026 — what check sizes and terms should I expect?

For a Waterloo technical founder at pre-seed in 2026, Garage Capital (Fund IV deploying now, headquartered in Waterloo with deep University of Waterloo ties) writes typical first cheques of $200K to $750K on SAFE or convertible note terms with founder-friendly post-money caps. Panache Ventures writes first cheques up to $1.5M with similar SAFE structures from their Montreal headquarters. BDC Seed Venture Fund is a credible co-investor for Canadian pre-seed with government-backed LP credibility. For a 2-person Waterloo dev tools founding team pre-revenue with strong technical credentials and early design partners, stacking Garage ($500K) + Panache ($750K) + 2-3 angel checks is a realistic $1.5M pre-seed. Expect 4 to 8 weeks from first meeting to wire — Garage moves fast when the technical quality is clear. Peony Business at $30 per admin per month gives you a pre-seed-ready data room with NDA gates per investor and page-level analytics — unlike DocSend or Google Drive, you see exactly which angels spent 15 minutes on your technical architecture versus 30 seconds on the team slide. That signal tells you who to prioritize for follow-up.

Related Resources

- Top Venture Capital Firms in Dublin

- Top Venture Capital Firms in Rome

- 12 Top France Investors in 2026

- 10 Active Slovenia Investors in 2026

- 18 Pre-Seed Investors in Germany

- Top Venture Capital Firms in Finland

- 10 Best Investors in Poland

- Top Investors in Dubai

- Why Startups Need Data Rooms for Fundraising Success

- What Makes a Data Room Investor Ready

- Startup Fundraising Strategy: Complete Guide

- How to Send Pitch Deck to Investors

- The Rise of AI-Powered Data Rooms

- Fundraising Data Rooms

- Venture Capital Data Rooms

- Startup Data Rooms

You might also like

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026

Apr 29, 2026

Top 8 Boston Investors in 2026: The Founder's Complete Guide to Raising in Boston & Cambridge

Apr 29, 2026

Top 10 Active Investors in Italy (2026): Complete Founder Guide to Italian VC Firms