15 Sports Investors Actively Deploying in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Sports is one of the most partnership-dependent fundraising categories we host on our platform -- founders need teams, leagues, rights holders, and athletes to sign off on pilots, sponsorships, and media deals before a capital partner will even take a first call. That dynamic concentrates deal flow into a small universe of true sports-specialist investors who can unlock those relationships. Generic "industry-agnostic" VCs that occasionally do a sports deal are not the right partner here, no matter how famous the fund name.

This guide maps 15 sports-focused investors actively deploying capital in 2026 -- sports-specialist VCs at seed through Series B, franchise-ownership PE platforms, and sports-adjacent growth shops. Every firm listed has verified 2024-2026 deployment activity. I spent years evaluating consumer and tech deals at Target Global and Backed VC before starting Peony, and the sports-investor stack below is the one I would run for my own capital.

TL;DR: Sports is the most-capitalized year in VC + PE history outside of 2021, with four structural forces converging in 2026. The global sports industry is projected at $521.74B in 2026, up from $495.38B in 2025 (Research and Markets, 2026). Global sports-tech VC totaled $12.5B through October 2025, on pace for the second-largest year on record (SportsTech X Global Sports Tech VC Report 2025, November 2025). Private equity deal value in sports services hit an 8-year high of $6.33B in Q1-Q3 2025 (S&P Global Market Intelligence, October 2025). Global women's elite-sports revenue is projected at $2.35B in 2025, up 25% year-over-year from $1.88B in 2024 (Deloitte, March 2025). The Los Angeles Lakers sold at a $10 billion valuation (announced June 2025, closed October 2025) -- shattering the $6.1B record set earlier in 2025 by the Boston Celtics sale to a Sixth Street-led consortium (Sportico, October 2025). Apollo Sports Capital launched a $5B vehicle in September 2025 and closed its majority acquisition of Atlético de Madrid at €2.2B ($2.55B) on March 12, 2026 (Apollo, March 2026). The NFL opened to private equity in August 2024; four deals have closed to date including Ares/Dolphins at $8.1B, Arctos/Bills, Arctos/Chargers (8% stake May 2025), and Sixth Street/Patriots (November 2025) (Fortune, December 2024 / Sixth Street, November 2025). US sports betting reached $160-$170B in legal handle in 2025 across 38 states plus DC, with market projected to grow 11.02% CAGR to $27.42B by 2034 (IMARC Group, 2026). Below: 15 sports-specialist investors actively deploying, sub-sector breakdowns, the women's sports and NFL PE angles driving 2026, and what sports capital partners actually need in your data room.

How to Pick the Right Sports Investor (Fast, Practical)

Start With Your Sports Wedge

Investors in sports typically specialize in one or two of these wedges:

- Sportstech and fan engagement (collectibles, ticketing, creator and fan economy, AI-powered fan platforms)

- Athlete performance and health (wearables, rehab, mental performance, sports medicine, biomechanics)

- Sports media and content (rights-adjacent tech, distribution, analytics, broadcast AI)

- Sports betting and gambling tech (sportsbook infrastructure, prediction markets, personalization AI)

- Sports commerce (merch, marketplaces, retail innovation, collectibles)

- Emerging leagues and experiences (women's sports, TGL, Unrivaled, PWHL, new formats, venues)

- Franchise ownership and sports PE (minority stakes, liquidity solutions, structured capital)

If you are building athlete health software, a franchise-ownership PE firm is not your best first call -- even if they are famous.

Decide What You Need Beyond the Check

Sports startups are uniquely partnership-dependent. You want to know:

- Can this investor unlock teams, leagues, and pilots?

- Can they help with rights, distribution, sponsorship, or athlete networks?

- Do they understand sports-specific constraints (seasonality, regulations, league rules, CBA dynamics)?

Filter by Stage and Check Size

A clean stage match saves months. If you are at seed, pitching Arctos is a waste of both sides' time. If you are at Series B with $10M ARR, Stadia Ventures writing $100K is not moving the needle. The 15 firms below are mapped to stage and check size so you can compress your outreach list to the 5-7 firms that can realistically lead or fill your round.

The 15 Sports Investors Actively Deploying in 2026

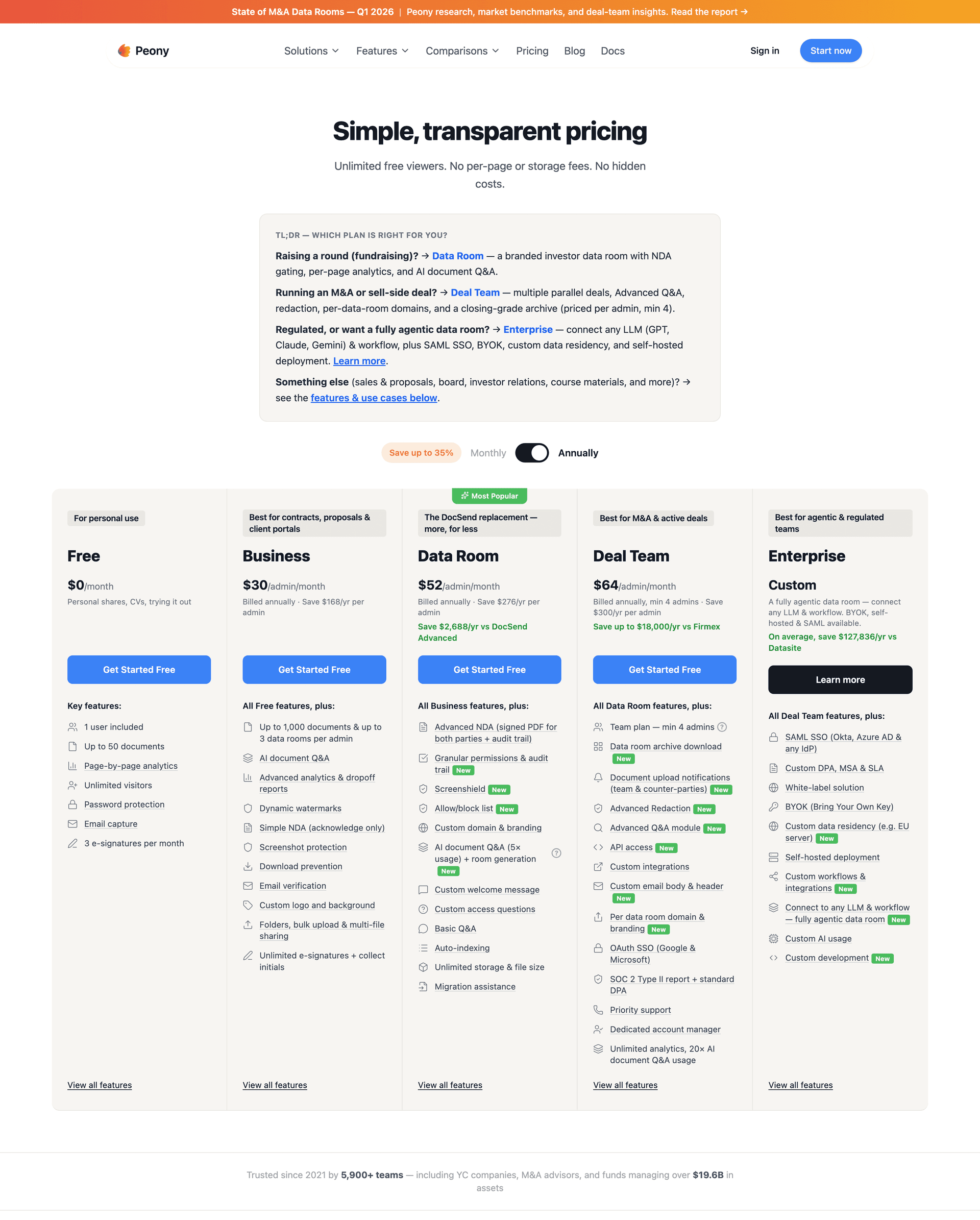

Organized by role: sports-specialist VCs at seed through Series B, franchise-ownership PE platforms, and sports-adjacent growth shops. Every firm listed has verified 2024-2026 deployment activity and check-size guidance. For data room setup ahead of investor outreach, Peony Business at $30/admin/month handles the sports-specific document mix out of the box.

| Firm | Website | Check Size | Stage | Sub-Sector Focus |

|---|---|---|---|---|

| Courtside Ventures | courtsidevc.com | $500K-$3M | Seed-Series A | Fan engagement, athlete, betting infra, collectibles |

| Will Ventures | willventures.com | $1M-$5M | Seed | Athlete health, consumer wellness, sports entertainment |

| 359 Capital (fka Sapphire) | 359capital.com | $2M-$10M | Series A-B | Sports, media, entertainment consumer |

| LEAD | lead.vc | $100K-$5M | Pre-seed-Series A | Sports tech + health tech, wearables, biomechanics |

| KB Partners | kbpartners.com | $1M-$3M initial | Seed | Sports tech first institutional check |

| SeventySix Capital | seventysixcapital.com | $500K-$3M | Seed-Series A | Sports betting, gaming, analytics, AI |

| Elysian Park Ventures | elysianpark.ventures | $500K-$100M | Stage-agnostic | Sports x health x commerce x culture x tech (Dodgers) |

| Arctos Partners | arctospartners.com | Up to 10% stakes | Franchise PE | NFL, NBA, MLB, European football, F1 minority stakes |

| RedBird Capital Partners | redbirdcap.com | $50M-$500M+ | Growth PE | AC Milan, sports rights, sports media |

| Sixth Street Partners | sixthstreet.com | Minority franchise | Large-cap PE | Celtics, Giants, Patriots, Spurs, Real Madrid, Barcelona |

| Ares Management | aresmgmt.com | Franchise + infra | Large-cap PE | Miami Dolphins, Inter Miami, McLaren, Atlético (partial) |

| Apollo Sports Capital | apollo.com | $5B vehicle | Large-cap PE | Atlético Madrid majority, Mutua Madrid Open, Miami Open |

| Bruin Capital | bruincptl.com | Platform-level | Middle-market PE | Box To Box Films, Full Swing, TGI Sport |

| Bluestone Equity Partners | bluestoneep.com | Growth | Growth PE | Players Health, athlete safety + sports insurance |

| Monarch Collective | monarchcollective.com | Minority franchise | Women's sports PE | Angel City FC, Boston Legacy, WNBA Cleveland, FC Viktoria Berlin |

Tier 1 -- Sports-Specialist VCs (Seed to Series B)

These firms are where sportstech founders raising their first institutional round should spend their outreach time. Each has verified 2024-2026 deployment.

Courtside Ventures

Website: courtsidevc.com | Fund IV: ~$100M target, launched late 2025 with Michael Jordan as LP | HQ: New York

Courtside Ventures is the leading brand-name early-stage sports VC with a 96-company portfolio split roughly evenly between sports tech (30+) and lifestyle (30+). Fund IV launched in late 2025 with a $100M target and Michael Jordan joining as an LP (Courtside, October 2025). The firm writes $500K-$3M seed and Series A checks, often as lead or co-lead. Recent 2025 deals include leading Fermat's $45M Series B (gaming and collectibles), participating in Jump's Series A (August 2025), and the Dibbs acquisition by Bastion (February 2025). Courtside's LP base includes athletes, team owners, and strategic brands -- a credibility unlock for founders selling into teams or leagues.

Why it matters for founders: If your product benefits from athlete endorsement or team pilot access, Courtside's LP network moves faster than cold outreach. Ideal for fan engagement, collectibles, athlete-adjacent consumer products, and sportstech at the $500K-$3M check size.

Will Ventures

Website: willventures.com | Fund II: $150M (closed October 2022, actively deploying through 2026) | HQ: Boston

Will Ventures closed Fund II at $150M in October 2022 and is still actively deploying with a deliberately slow and intentional 20-25 company portfolio construction (TechCrunch, October 2022). The firm writes $1M-$5M seed checks with a sports-plus-consumer thesis anchored by a research-driven investment process and a deep athlete-backed LP community. Portfolio includes Ness, Mighty Health, The Post, and Street FC. Will Ventures is seed-first with strong distribution and athlete-community support.

Why it matters for founders: Will Ventures's athlete-network LP base is uniquely valuable for founders whose product lifecycle depends on athlete endorsement or adoption. The firm's research-driven thesis means diligence is rigorous but the partnership is long-term and operationally involved.

359 Capital (formerly Sapphire Sport)

Website: 359capital.com | AUM: $300M total; $181M Fund II | HQ: New York

359 Capital spun out from Sapphire Ventures on November 10, 2025 and rebranded under Michael Spirito, bringing $300M AUM and a $181M Fund II with 30+ portfolio companies (TechCrunch, November 2025). The firm writes $2M-$10M checks at Series A-B with a consumer, sports, media, and entertainment thesis. The strategic LP base is the most valuable in the category -- City Football Group, adidas, AEG, Madison Square Garden, Sinclair, and dozens of team owners. Founders get both capital and genuine enterprise sports-and-media pilot introductions.

Why it matters for founders: 359 Capital is your highest-probability lead for a $5M-$10M Series A in sportstech or sports-media. No other Series A firm has comparable strategic-LP distribution across multiple leagues, broadcasters, and team owners.

LEAD

Website: lead.vc | AUM: ~$155M across fund family | HQ: Berlin / Lake Nona / global

LEAD runs the deepest sports-plus-health-tech franchise in the industry with a $155M AUM spread across four fund vehicles: LEAD ONE (pre-seed), Lake Nona Fund (seed), ADvantage ($50M Series A fund with OurCrowd), and Locker Room (athlete and leader co-invest) (LEAD, 2024). The firm writes $100K-$5M across 70+ portfolio companies. Core thesis is sports tech and health tech with explicit clinical and biomechanics validation capability -- uniquely important for wearables, rehab, and sports medicine startups. LP base includes pro teams, player associations, federations, and health systems.

Why it matters for founders: LEAD is one of only three sports specialists with a dedicated health and biomechanics thesis. For athlete performance, rehab, or sports medicine founders with clinical validation requirements, LEAD is the first call.

KB Partners

Website: kbpartners.com | Myriad Opportunity Fund I and II: active 2024-2025 | HQ: Chicago

KB Partners is a 25-year-old sports VC writing $1M-$3M initial checks (with similar reserved follow-on) at the first-institutional stage. The 71-company portfolio includes Club Champion, Phenix, Full Swing, Hammerhead, asensei, and ANGLR. The most recent 2024 investment was NIL FanBox (December 2024). KB specializes in the sports-plus-technology crossover and often writes the first institutional check for capital-efficient wedges.

Why it matters for founders: If you are a founder who has bootstrapped or raised angel rounds and need the first institutional check, KB Partners's first-check pattern recognition is valuable. Not a lead-at-any-stage fund, but a reliable seed partner.

SeventySix Capital

Website: seventysixcapital.com | Active deployment: 2024-2025 | HQ: Philadelphia

SeventySix Capital is the deepest sports-betting and gambling-tech specialist in the category. The firm co-led Lucra Sports' $10M Series A in 2024 and has active portfolio holdings in Diamond Kinetics (first smart baseball bat), Epoxy.ai (sportsbook personalization AI), and similar gambling-adjacent companies. SeventySix also operates an Athlete Venture Group chaired by Alejandro Bedoya with members including DeMarco Murray, James Develin, and Emmanuel Sanders.

Why it matters for founders: If you are building sports betting infrastructure, prediction markets, or gambling-tech personalization, SeventySix has the deepest sportsbook network of any sports-specialist VC. The Athlete Venture Group adds a promotional and distribution unlock that no other sports fund matches.

Tier 2 -- Sports PE and Ownership Platforms

These firms write $50M-$500M+ checks into sports franchises, franchise-adjacent businesses, sports media infrastructure, and sports rights. Relevant for late-stage founders at $10M+ ARR or for franchise-ownership finance questions.

Elysian Park Ventures

Website: elysianpark.ventures | Structure: Evergreen fund tied to LA Dodgers ownership group | HQ: Los Angeles

Elysian Park Ventures is the only major sports fund tied directly to an MLB ownership group -- the Los Angeles Dodgers. The evergreen structure allows stage-agnostic investing with checks from $500K to $100M across 70+ startups and 13 exits. Recent 2025-2026 activity includes leading International Dance League's $7M seed (2025) and an expected PrizePicks sale to Allwyn International for $1.6B in H1 2026 (Yahoo Finance, December 2025). Portfolio spans sports, health, commerce, culture, and tech. Elysian Park's SeatGeek investment remains the anchor comparable for sports-commerce exits.

Why it matters for founders: Elysian Park provides unique pilot-access to the Dodgers organization and the broader LA sports ecosystem. For fan-engagement, ticketing, or wellness founders, this is an unmatched distribution unlock.

Arctos Partners

Website: arctospartners.com | Sports-related AUM: ~$11.3B entering 2025 (Fund II at $4.1B + liquidity strategy $2.7B) | HQ: Dallas / New York

Arctos Partners is the largest institutional owner of North American sports equity, holding stakes in 25+ franchises globally. Entering 2025, Arctos managed approximately $11.3 billion in sports-related funds including Fund II at $4.1B (closed 2024) plus a $2.7B liquidity-provision strategy (Sportico, 2025). Arctos is the only PE firm holding multiple NFL stakes -- the Buffalo Bills (approved December 2024) and the LA Chargers (8% stake, May 2025) -- alongside NBA, MLB (Dodgers-adjacent, Giants), European football, and F1 (McLaren Racing) positions. In February 2026, KKR agreed to acquire Arctos outright (initially valued at $1.4 billion; roughly $15 billion AUM across 30+ team stakes) -- the clearest signal yet that sports equity has become core institutional infrastructure.

Why it matters for founders: Arctos is not a founder-check vehicle. For franchise-adjacent businesses, liquidity-provision transactions, or growth-stage companies where sports capital markets matter, Arctos is a benchmark partner with the deepest franchise relationships in the industry.

RedBird Capital Partners

Website: redbirdcap.com | AUM: $14B across 8 funds including RedBird Capital Fund IV | HQ: New York

RedBird Capital Partners runs a $14B AUM sports, media, and entertainment PE franchise under Gerry Cardinale. Portfolio anchors include AC Milan (acquired 2022, qualified for three consecutive Champions League editions), a Fenway Sports Group partnership, SpringHill (LeBron James's media company), and a $2B commitment to the Skydance-Paramount merger (the largest PE Hollywood studio investment in history). A Rajasthan Royals stake sold in March 2026 for $1.63B. RedBird is the deepest sports-rights and content-infrastructure PE firm globally.

Why it matters for founders: For growth-stage companies at $10M+ ARR in sports rights, media infrastructure, or sports content, RedBird is a top-3 dealmaker globally. Not a founder-seed-check firm but a realistic Series C-to-growth-stage partner.

Sixth Street Partners

Website: sixthstreet.com | Franchises: 7 pro-sports teams across 5 leagues | HQ: San Francisco

Sixth Street Partners is an NFL-approved PE fund (since summer 2024) with a diversified franchise portfolio spanning seven teams across five leagues. Recent activity includes co-investing in the Boston Celtics $6.1B acquisition (March 2025), buying a stake in the San Francisco Giants (2025), and closing a minority investment in the New England Patriots (November 2025) (Sixth Street, November 2025). Other franchise stakes include the San Antonio Spurs (20%), Real Madrid, FC Barcelona, and Bay FC (NWSL).

Why it matters for founders: Sixth Street's diversified franchise ownership across NFL, NBA, MLB, European soccer, and NWSL makes them a major capital partner for NFL-approved minority deals and for cross-sport franchise-adjacent businesses needing multi-league distribution.

Ares Management

Website: aresmgmt.com | First NFL PE deal closed: December 2024 | HQ: Los Angeles

Ares Management closed the first NFL PE deal in history in December 2024, acquiring 10% of the Miami Dolphins at an $8.1 billion valuation -- a transaction that also included Hard Rock Stadium and the F1 Miami Grand Prix (Fortune, December 2024). Portfolio includes Inter Miami FC, McLaren Racing, Atlético de Madrid (partial, now majority-owned by Apollo as of March 2026), and the Miami Dolphins. CEO Michael Arougheti is one of the most visible bulls on sports PE.

Why it matters for founders: For franchise-adjacent businesses and stadium-plus-live-events infrastructure, Ares's Dolphins-plus-Hard Rock Stadium-plus-F1 combination is unique. Not a founder-seed-check firm but a valuable capital partner at the infrastructure layer.

Apollo Sports Capital

Website: apollo.com | Fund: $5B vehicle launched September 2025 | HQ: New York

Apollo Sports Capital is the freshest mega-capital entrant in sports PE, launching a $5 billion vehicle on September 29, 2025 (Apollo, September 2025) and closing its majority acquisition of Atlético de Madrid at €2.2B ($2.55B) on March 12, 2026 (Apollo, March 2026). Additional holdings include stakes in Mutua Madrid Open and Miami Open (tennis). Apollo Sports Capital is open to hybrid and credit structures that pure-equity PE firms will not consider.

Why it matters for founders: Apollo's hybrid and credit flexibility opens structures (subordinated debt, preferred stock, revenue-share) that franchise-adjacent businesses can use to avoid dilution. The $5B fresh vehicle means active 2026-2027 deployment.

Bruin Capital

Website: bruincptl.com | Raise: $1B raise led by Josh Harris's 26North and TJC in 2026 | HQ: New York

Bruin Capital is the only global investment platform dedicated exclusively to middle-market sports service businesses -- a distinct positioning from franchise PE. In 2026, Bruin closed a $1B raise led by Josh Harris's 26North and TJC, bringing total capital raised to over $2B since 2015 (Sportico, 2026). Portfolio includes Box To Box Films (producer of Drive to Survive), Full Swing, PlayGreen, and TGI Sport.

Why it matters for founders: For middle-market sports services businesses at $5M-$25M EBITDA in data, technology, or premium production, Bruin is the dedicated capital partner. Not a franchise-ownership firm, but the right home for scaled sports service platforms.

Bluestone Equity Partners

Website: bluestoneep.com | Fund I: $300M oversubscribed, closed Q1 2023, deploying 2024-2025 | HQ: New York

Bluestone Equity Partners is the growth-PE arm of the sports-and-media specialist universe, led by former NBA executive Bobby Sharma. The inaugural fund closed oversubscribed at $300M in Q1 2023 with institutional-only LPs, explicitly targeting sports, media, and entertainment growth equity. Portfolio includes Players Health (athlete safety and sports insurance). Bluestone provides growth equity at the Series B-C stage.

Why it matters for founders: For growth-stage sports-tech founders at $5M+ ARR needing institutional PE capital with sports-industry depth, Bluestone's former-NBA-exec leadership and institutional-only LP base makes them a credible capital partner at Series B-C.

Monarch Collective

Website: monarchcollective.com | Fund: $250M total (raised fresh $100M to reach $250M in March 2025) | HQ: Los Angeles

Monarch Collective is the first and only dedicated women's sports PE fund, raising fresh $100M to reach $250M total in March 2025 with LPs including Pivotal Ventures (Melinda French Gates), Hello Sunshine, EY, and Rockefeller Foundation (CNBC, March 2025 / Sportico, March 2025). Portfolio includes Angel City FC, San Diego Wave FC, Boston Legacy FC, WNBA Cleveland expansion (first W team investment, February 2026), and FC Viktoria Berlin (first European investment, November 2025 -- 38% stake). Monarch is building "the Berkshire of women's sports."

Why it matters for founders: For women's sports franchise-adjacent businesses or minority-equity transactions, Monarch Collective is the only dedicated capital partner. The LP base (Pivotal Ventures, Hello Sunshine, Rockefeller) provides additional marketing and distribution unlocks that pure PE capital cannot match.

Sub-Sector Breakdown: Where 2026 Sports Capital Is Flowing

Sports capital deployment in 2026 is concentrated across six sub-sectors with distinct dynamics:

Fan Engagement and Creator-Fan Economy

AI-powered fan engagement is the hottest sportstech vertical in 2026. Genius Sports has raised $489.1M cumulatively and is the dominant infrastructure player. The English Premier League launched Microsoft Copilot-powered "Premier League Companion" trained on 30 seasons, 300K articles, and 9K videos in 2025. Fan-platform startups are crowding the seed-to-Series-A market. Courtside Ventures, 359 Capital, and Elysian Park are the most active investors here.

Athlete Performance and Sports Health

Wearables drive 42% of private sports-tech deals. Whoop raised a $575M Series G in Q1 2026 at a $10.1B valuation (Crunchbase News, March 2026). Teamworks raised $235M in June 2025, reaching unicorn status. LEAD and Will Ventures are the deepest specialist investors in this sub-sector; KB Partners writes first institutional checks for capital-efficient wedges.

Sports Betting and Gambling Tech

US sports betting handle hit $160-170B in 2025 across 38 states plus DC, representing $10.70B in operator revenue per IMARC Group. The market is projected to grow 11.02% CAGR to $27.42B by 2034. Novig raised a $75M Series B in Q1 2026 (sweepstakes prediction markets). Full 50-state legalization would add $1.6B in annual tax revenue. SeventySix Capital, Courtside Ventures, and 359 Capital lead deployment in this category.

Sports Media and Rights-Adjacent

The NBA's new 11-year, $76B media rights deal with ESPN/ABC, NBC, and Amazon Prime kicked in for the 2025-26 season -- a 2.8x rights-fee increase that lifted franchise valuations league-wide. 2025-26 NBA viewership averaged 1.78M across partners, up 16-35% YoY depending on network. RedBird Capital, Sixth Street, and Ares are the most active investors in rights-adjacent infrastructure.

Franchise Ownership and Sports PE

PE activity in US sports is at record levels: 18 of 30 MLB teams now have PE connections, with 10 direct investments per PitchBook. Franchise valuation records set in 2025 include the Lakers at $10B (June/October 2025) and the Celtics at $6.1B (March 2025). The NFL opened to PE in August 2024 and four deals have closed (Ares/Dolphins, Arctos/Bills, Arctos/Chargers, Sixth Street/Patriots). CVC Capital Partners formed a $13.6B Global Sport Group in September 2025 consolidating LaLiga, Ligue 1, WTA, Premiership Rugby, Six Nations, and Volleyball World. Arctos, Sixth Street, Ares, Apollo, and RedBird are the dominant franchise PE firms.

Women's Sports

The fastest-growing segment in sports investing. Global women's elite-sports revenue projected at $2.35B in 2025, up 25% YoY from $1.88B in 2024 and up 2.4x from $981M in 2023 per Deloitte. Commercial 54%, Broadcast 25%, Matchday 21% of revenue mix. NWSL average valuation +77% YoY (2024 to 2025), +179% from 2023. Angel City FC leads at $335M (#1, up 34% YoY). Denver NWSL expansion fee: $110M (September 2025) -- 2x prior record. Atlanta NWSL expansion fee: $165M (Arthur Blank, 2025). WNBA added three expansion teams at $250M fees each (Cleveland 2028, Detroit 2029, Philadelphia 2030), with Cleveland post-money at $290M and Detroit post-money at $325M. Unrivaled 3x3 basketball at $340M valuation after Bessemer-led Series B in September 2025. Monarch Collective is the only dedicated women's sports PE fund.

Sports-Specific Due Diligence Requirements Investors Expect in 2026

Sports diligence is structurally different from generic SaaS or consumer diligence because the assets are partnership rights, athlete relationships, and rights-adjacent IP, and the risks are mostly commercial (partnership loss, seasonality, regulatory exposure, league rule changes) rather than technical. Based on hosting hundreds of sports IS and sportstech data rooms on Peony, here is what 2026 capital partners expect.

Partnership Agreements and Pilot Results

Every sportstech capital partner will ask for partnership agreements with teams, leagues, or federations including change-of-control language, exclusivity clauses, term lengths, and renewal probability. Pilot results need to be documented with named KPIs, stakeholder sign-offs, and expansion pricing. For a $5M Series A, expect every capital partner to want to see at least two signed pilot agreements plus one reference call with a team or league counterparty.

Media Rights and NIL Endorsement Contracts

Media rights documentation, licensing agreements, and NIL endorsement contracts form the second diligence layer. Any athlete-endorsement product needs a full NIL contract audit with term lengths, renewal terms, morality clauses, and state-by-state NIL regulation compliance. For betting-adjacent products, add state-by-state regulatory compliance files covering all 38 legal states plus DC.

Seasonal Revenue and Off-Season Engagement

Sports businesses are uniquely seasonal, and capital partners want to understand off-season engagement or multi-sport expansion mechanics. Expect a seasonal revenue breakdown showing off-season revenue retention, athlete-dormancy adjustments, and multi-sport expansion pathways.

Stakeholder Map

Every sports diligence session starts with: who is your buyer? Team, league, brand, athlete, consumer, or sportsbook? Ambiguity kills sports deals faster than any other vertical. A one-page stakeholder map showing buyer, distribution partner, and revenue path is table stakes.

Competitive Positioning and Data Edge

Sports is a crowded market; the moat is usually data rights, data quality, or distribution -- not features. Capital partners expect a competitive positioning section showing your unique data asset or distribution lever.

For the complete due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes all of these sports-specific documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is the NIL contract renewal probability?" or "What is the pilot expansion pricing model?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. AI redaction identifies PII, athlete-contract dollar amounts, and team-confidential data across uploaded documents before you share with capital partners. NDA gates require signature before any sensitive media rights or athlete contract is visible -- something DocSend cannot detect on any plan.

Sports Investor Deals By the Numbers

- Global sports industry projected at $521.74B in 2026, up from $495.38B in 2025 (Research and Markets, 2026)

- Global sports-tech VC: $12.5B through October 2025 (pace = 2nd-largest year on record) (SportsTech X Global Sports Tech VC Report 2025)

- PE deal value in sports services: $6.33B in Q1-Q3 2025 (8-year high) (S&P Global Market Intelligence, October 2025)

- Global women's elite-sports revenue: $2.35B projected 2025, up 25% YoY from $1.88B in 2024 (Deloitte, March 2025)

- Women's sports revenue mix: Commercial 54%, Broadcast 25%, Matchday 21% (Deloitte)

- NWSL average valuation: +77% YoY (2024 to 2025), +179% from 2023 (Sportico, 2026)

- Angel City FC #1 NWSL valuation: $335M, up 34% YoY (Sportico, 2026)

- Denver NWSL expansion fee: $110M (September 2025, 2x prior record); Atlanta NWSL expansion fee: $165M (Sportico, 2025)

- WNBA expansion fees: $250M each (Cleveland 2028, Detroit 2029, Philadelphia 2030) (Sportico, June 2025)

- Unrivaled 3x3 basketball: $340M valuation after Series B (Bessemer-led, September 2025) (Unrivaled, September 2025)

- Los Angeles Lakers sale: $10B valuation (June 2025 announcement, closed October 2025) -- record (Sportico, October 2025)

- Boston Celtics sale: $6.1B (March 2025, Sixth Street-led consortium) (Sportico, March 2025)

- Apollo Sports Capital: $5B vehicle launched September 2025 (Apollo, September 2025)

- Apollo Sports Capital closed Atlético de Madrid majority at €2.2B ($2.55B) March 12, 2026 (Apollo, March 2026)

- CVC Global Sport Group: $13.6B formed September 2025 (Sportico, September 2025)

- NFL PE: 4 deals closed since August 2024 rule change (Ares/Dolphins $8.1B, Arctos/Bills, Arctos/Chargers 8% May 2025, Sixth Street/Patriots November 2025) (Fortune, December 2024 / Sixth Street, November 2025)

- US sports betting: $160-170B handle 2025, $10.70B operator revenue, projected 11.02% CAGR to $27.42B by 2034 (IMARC Group, 2026)

- NBA media rights: 11-year, $76B deal (ESPN/ABC, NBC, Amazon Prime) began 2025-26 season, 2.8x rights-fee increase (PitchBook, 2025)

- Whoop Series G: $575M at $10.1B valuation (Q1 2026) (Crunchbase News, March 2026)

- Teamworks: $235M raise June 2025 (unicorn status) (TechCrunch, 2025)

- Monarch Collective: $250M total AUM after fresh $100M raise March 2025 (CNBC, March 2025)

- 359 Capital: $300M total AUM, spun out from Sapphire Ventures November 10, 2025 (TechCrunch, November 2025)

- Arctos Partners: ~$11.3B in sports-related funds entering 2025 (Fund II $4.1B + $2.7B liquidity strategy) (Sportico, 2025)

- Bruin Capital: $1B raise led by Josh Harris's 26North + TJC (2026) (Sportico, 2026)

How Peony Fits the Sports Startup Fundraising Workflow

Peony is a data room platform purpose-built for the exact workflow sports founders run: multiple simultaneous investor conversations across 10-15 firms during fundraise, heavy partnership and rights documentation diligence, athlete-contract confidentiality, and sportsbook regulatory compliance tracking. Peony Data Room at $52/admin/month is the plan sports founders use.

AI auto-indexing organizes partnership agreements, media rights documentation, NIL endorsement contracts, pilot results, seasonal revenue breakdowns, and stakeholder maps into a professional folder structure in under 3 minutes. Junior analysts spend 2-3 hours on this same workflow in Datasite.

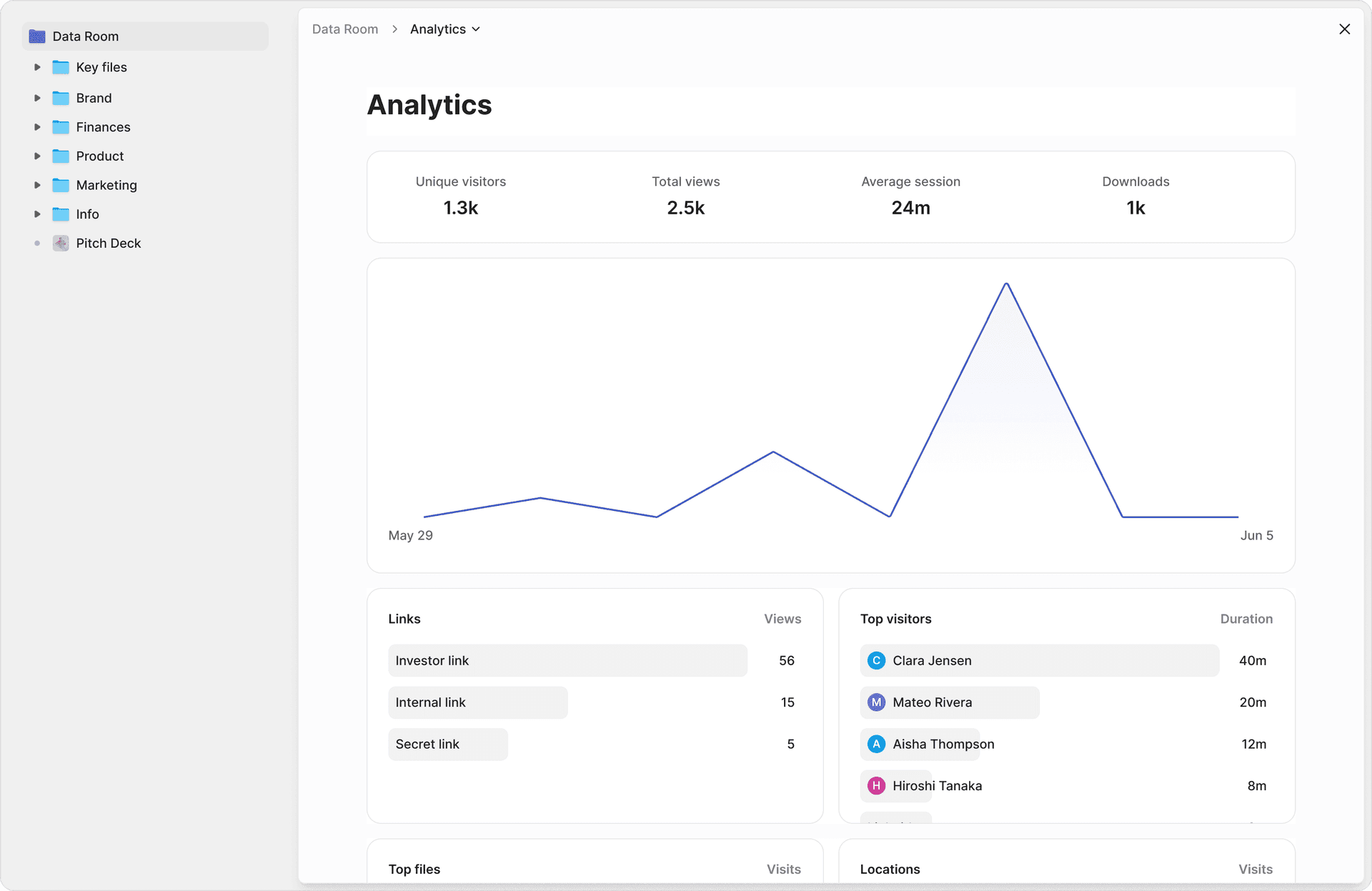

Page-level analytics tell you which investor spent 30 minutes on the partnership agreements versus skimmed the team slide, and which one lingered on the pilot results versus flipped through them. DocSend gives you deck-level views; Peony gives you page-by-page engagement so you know who is genuinely diligencing versus pattern-matching.

Smart Q&A lets counterparties submit diligence questions where AI drafts answers by surfacing the exact document sections and page citations. Your team approves every response before it ships, and every Q&A exchange is audit-trailed. For sports diligence where questions like "What is the NIL renewal probability?" or "What is off-season revenue retention?" come in from every capital partner, this workflow compounds across 10-15 simultaneous investor conversations.

AI redaction identifies PII, athlete-contract dollar amounts, team-confidential data, and regulatory-sensitive sportsbook data across uploaded documents before investors see them -- a feature Datasite charges $25K+ per deal to configure manually.

Screenshot protection blocks and logs screen-capture attempts on sensitive files. Dynamic watermarks embed viewer identity on every frame of every document, which sports investors like Elysian Park Ventures and RedBird Capital Partners require before reviewing partnership term sheets, league relationship data, or athlete contracts.

NDA gates require signature before any materials are visible -- DocSend cannot detect this on any plan. AI document extraction lets investors ask "What is the pilot expansion pricing model?" and get a cited answer. E-signatures close the loop after conference introductions -- investors sign the NDA and access materials in a single workflow.

Unlimited data rooms on Peony Data Room mean a sports founder running a Series A pitch across 15 investors and a strategic partnership conversation with two leagues simultaneously does not pay per-deal licensing. A sports founder running a Series A fundraise pays roughly $52 per month on Peony Data Room versus $15,000-$50,000 per deal on Datasite. The free tier is the entry point; Peony Data Room at $52/admin/month is where serious sports fundraises run.

For deeper context on startup fundraising, venture capital, and M&A deal processes, see our dedicated solutions guides.

Quick Guide: Match Your Situation to the Right Sports Investor

| Situation | Best Investor Fit | Why |

|---|---|---|

| Pre-seed sportstech founder, pre-product or pre-revenue | Stadia Ventures + LEAD ONE + Courtside Ventures | Stadia accelerator $100K + structured program; LEAD ONE pre-seed vehicle; Courtside Fund IV first check $500K |

| Seed athlete performance wearable, $3M-$5M raise, clinical validation required | LEAD + Will Ventures + Courtside Ventures | LEAD clinical depth; Will Ventures athlete network; Courtside Fund IV |

| Seed fan engagement or collectibles, $3M raise | Courtside Ventures + KB Partners + Will Ventures | Courtside Fermat co-lead; KB Partners first-institutional; Will Ventures consumer depth |

| Series A sportstech, $5M-$10M raise, need sports/media distribution | 359 Capital + Elysian Park Ventures | 359 Capital strategic LP base (CFG, adidas, MSG, AEG); Elysian Park Dodgers-ownership network |

| Seed sports betting or prediction markets, $3M-$5M raise | SeventySix Capital + Courtside Ventures | SeventySix deepest sportsbook network; Courtside gaming and betting infra thesis |

| Series A women's sports infrastructure or content, $5M-$10M raise | Monarch Collective + 359 Capital + Courtside Ventures | Monarch Collective only dedicated women's sports PE; 359 Capital strategic LPs; Courtside broader sports thesis |

| Series B-C sportstech, $15M-$50M raise, growth equity | 359 Capital + Bluestone Equity Partners + RedBird Capital | 359 Capital Series B tickets up to $10M; Bluestone institutional growth PE; RedBird at upper end |

| Franchise-adjacent business, $50M+ round | Arctos + Sixth Street + Apollo Sports Capital + RedBird | Arctos 25+ franchise stakes; Sixth Street 7 franchise network; Apollo $5B fresh; RedBird $14B AUM |

| Middle-market sports services ($5M-$25M EBITDA) | Bruin Capital + Bluestone Equity Partners | Bruin exclusive middle-market sports services mandate; Bluestone growth PE with sports depth |

| NFL franchise minority stake | Arctos + Sixth Street + Ares + Apollo + consortium (Dynasty, etc) | Arctos only firm with multiple NFL stakes; Sixth Street Patriots 2025; Ares first NFL deal 2024 |

Bottom Line

Sports in 2026 is the most-capitalized year in venture plus PE history outside of 2021, with four structural forces converging: a global sports industry projected at $521.74B (Research and Markets), PE sports-services deal value at an 8-year high of $6.33B in Q1-Q3 2025 (S&P Global), global sports-tech VC at $12.5B through October 2025 on pace for the second-largest year ever (SportsTech X), and women's sports revenue up 25% YoY to $2.35B (Deloitte). Franchise valuations hit records (Lakers $10B, Celtics $6.1B), NFL opened to PE with four deals closed, and fresh mega-vehicles (Apollo Sports Capital $5B, CVC Global Sport Group $13.6B, Monarch Collective $250M) signal sustained 2026-2027 deployment.

If you are a seed-stage sports founder: Courtside Ventures (Fund IV $100M target, Michael Jordan LP), LEAD ($155M AUM across 4 fund vehicles with pre-seed to Series A), Will Ventures (Fund II $150M, athlete network), KB Partners (first-institutional check specialist), and SeventySix Capital (sports betting depth) are the five first-call firms. Check sizes range $100K-$5M.

If you are a Series A-B sportstech founder: 359 Capital ($2M-$10M checks, strategic LP base of CFG, adidas, MSG, AEG, Sinclair), Elysian Park Ventures (Dodgers-ownership network, $500K-$100M checks), and Bluestone Equity Partners (institutional growth PE) are the realistic lead universe. For women's-sports-adjacent deals, add Monarch Collective.

If you are a growth-stage or franchise-adjacent business: RedBird Capital ($14B AUM), Sixth Street (7 franchises across 5 leagues), Arctos ($11.3B sports AUM, 25+ franchise stakes), Ares (first NFL PE deal), and Apollo Sports Capital ($5B fresh vehicle) are the realistic capital partners. Bruin Capital covers middle-market sports services specifically.

For every sports fundraise: Set up your data room on day one of your outreach process. Sports diligence is unusually document-heavy at the commercial-partnership level (team and league agreements, NIL contracts, media rights, pilot results, stakeholder maps, seasonal revenue analysis) -- and investors expect the data room to be organized and complete before the first deep-dive call. Peony lets you build a complete sports data room in under 5 minutes, with page-level analytics that show which investors are reading the partnership agreements versus skimming the team slide, AI-powered Smart Q&A that surfaces hard answers with page citations so investors complete diligence faster, and NDA gates that prevent any investor from seeing sensitive team partnership terms or athlete contracts before signing.

Peony Data Room at $52/admin/month includes AI auto-indexing, AI-powered Smart Q&A, AI redaction, dynamic watermarks, screenshot protection, NDA gates, page-level analytics, AI document extraction, and e-signatures. A sportstech founder running a Series A fundraise across 15 investors pays roughly $52 per month on Peony Data Room versus $15,000-$50,000 per deal on Datasite. When your fundraise clock is ticking and 15 investors need to get comfortable with the sports deal simultaneously, every hour matters.

Set up your first sports investor data room -- see plans and pricing.

Frequently Asked Questions

I am a seed-stage founder building athlete performance wearables -- which sports investors actually lead rounds in my category?

For athlete performance and sports health tech at seed stage, four investors are your highest-probability leads in 2026. LEAD manages approximately $155M AUM across pre-seed through Series A fund vehicles (LEAD ONE, Lake Nona Fund, ADvantage, Locker Room) with a published $100K-$5M ticket range, and maintains the deepest sports-plus-health-tech thesis in the category with clinical and biomechanics validation capability. Will Ventures is still deploying its $150M Fund II (closed 2022) with a seed-first sports and consumer thesis and deep athlete-network LP base. Courtside Ventures launched Fund IV with a $100M target in late 2025 including Michael Jordan as an LP, writing $500K-$3M seed checks with a 96-company portfolio spanning sports tech, lifestyle, and gaming. KB Partners writes $1M-$3M initial checks with similar reserved follow-on across a 71-company sports-tech portfolio. For a first-time wearables founder raising a $3M-$5M seed, LEAD plus Courtside as co-leads plus a Will Ventures or KB Partners fill is a realistic stack. Peony Business at $30 per admin per month gives you page-level analytics showing which partner reviewed your clinical data versus who skimmed the team slide -- something DocSend cannot detect on any plan.

I am raising a $5M-$10M Series A for a sportstech company -- what check sizes do the top sports investors write?

Sports investor check sizes in 2026 vary significantly by stage and fund type. At seed, LEAD publishes $100K-$5M across its fund family, Courtside Ventures writes $500K-$3M lead or co-lead positions, Will Ventures typically writes $1M-$5M, and KB Partners writes $1M-$3M initial. At Series A and B, 359 Capital (spun out from Sapphire Ventures on November 10, 2025 with $300M total AUM and a $181M Fund II) writes $2M-$10M checks and has the most strategic sports-and-media LP base in the category -- City Football Group, adidas, AEG, Madison Square Garden, Sinclair, and dozens of team owners. Elysian Park Ventures writes $500K-$100M across stages with Dodgers-ownership-group distribution. SeventySix Capital co-led Lucra Sports' $10M Series A in 2024 with sportsbook and gambling tech depth. For a $5M-$10M Series A in sportstech in 2026, 359 Capital is your highest-probability lead given their explicit Series A-B focus and unique LP base. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes partnership agreements, media rights documentation, athlete contracts, and pilot blueprints in under 3 minutes -- a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first sports venture commitment -- what is the state of sports investing in 2026?

Sports investing in 2026 is at record capital deployment: the global sports industry is projected at $521.74B in 2026 (up from $495.38B in 2025) per Research and Markets, private equity deal value in sports services hit an 8-year high of $6.33B in Q1-Q3 2025 per S&P Global Market Intelligence, and global sports-tech VC through October 2025 totaled $12.5B -- on pace for the second-largest year on record. Women's sports is the fastest-growing segment at $2.35B projected 2025 revenue, up 25% year-over-year from $1.88B in 2024 per Deloitte. The NBA's new 11-year $76B media rights deal (ESPN/ABC, NBC, Amazon Prime) kicked in for the 2025-26 season, driving a 2.8x rights-fee increase that pushed franchise valuations league-wide -- the Lakers sold at $10B in October 2025, shattering the $6.1B Celtics record set earlier in 2025. NFL opened to PE in August 2024 and four PE deals have closed (Ares/Dolphins at $8.1B, Arctos/Bills, Arctos/Chargers 8% stake May 2025, Sixth Street/Patriots November 2025). For a family office allocating $10M-$50M to sports in 2026, the highest-leverage entry points are women's sports franchise stakes via Monarch Collective ($250M dedicated fund), sports-tech Series A via 359 Capital, or co-invest alongside Arctos/Sixth Street/Apollo Sports Capital on NFL minority positions. Peony Business at $30 per admin per month includes page-level analytics showing which capital partners spent 30 minutes on the partnership agreements versus skimmed the team slide, so you can prioritize follow-ups with genuinely engaged partners.

I am a sportstech founder about to enter due diligence -- what documents do sports investors typically expect in a data room?

Sports investors dig into distribution access and stakeholder relationships more deeply than generalist VCs. Beyond standard financials and cap table, expect requests for partnership agreements with teams, leagues, or federations with change-of-control language and exclusivity clauses, media rights and licensing documentation, athlete contracts or NIL endorsement agreements with term lengths and renewal probability, sponsorship revenue breakdown and pipeline, pilot results with named KPIs and expansion metrics, seasonal revenue analysis showing off-season engagement or multi-sport expansion, competitive positioning showing your data edge or distribution moat, stakeholder map clarifying whether your buyer is the team, league, brand, athlete, consumer, or sportsbook, and for betting-adjacent products state-by-state regulatory compliance files covering all 38 legal states plus DC. 359 Capital evaluates category leadership potential and pathways into sport and media distribution given their strategic LP base. LEAD wants clinical or biomechanics validation on performance products. Arctos and Ares will underwrite franchise-adjacency and rights monetization mechanics. For a corp dev analyst running point on a $10M-$20M Series A sportstech deal, these documents kill or close the transaction. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes all of these in under 3 minutes and Smart Q&A that routes capital partner questions through AI-drafted answers with page citations before your team approves each response, something DocSend cannot detect on any plan.

Our startup is building women's sports infrastructure -- which investors back the category?

Women's sports is the fastest-growing vertical in sports investing in 2026: global women's elite-sports revenue projected at $2.35B in 2025 (up 25% YoY) per Deloitte, NWSL average team valuation up 77% YoY, and WNBA adding three expansion teams at $250M fees each (Cleveland 2028, Detroit 2029, Philadelphia 2030). Monarch Collective is the first and only dedicated women's-sports PE fund, raising fresh $100M to reach $250M total in March 2025 with LPs including Pivotal Ventures (Melinda French Gates), Hello Sunshine, EY, and Rockefeller Foundation -- portfolio includes Angel City FC, San Diego Wave FC, Boston Legacy FC, WNBA Cleveland expansion (February 2026), and FC Viktoria Berlin (first European investment, November 2025). Elysian Park Ventures backs women's-sports-adjacent deals via the Dodgers-ownership network. 359 Capital, Courtside Ventures, and Will Ventures all have women's-sports portfolio exposure. For a pre-seed to Series A women's-sports infrastructure founder, Monarch Collective plus one of the sports-tech generalists (Courtside, LEAD, Will Ventures) is the typical capital stack. Peony Business at $30 per admin per month includes NDA gates so capital partners sign before any league term sheets, broadcast partner discussions, or athlete roster documentation is visible, and the Data Room plan at $52 per admin per month adds dynamic watermarks with viewer identity embedded in every frame.

I am running a fundraise across 10 sports investors -- how much does a data room cost for sportstech deals?

Legacy data rooms like Datasite charge $15,000 to $50,000 per deal, which is disproportionate for sportstech founders raising $3M-$15M seed or Series A rounds. Sports deals also require extensive document uploads including partnership agreements with teams and leagues, media rights documentation, NIL endorsement contracts, pilot results with named KPIs, sponsorship pipelines, regulatory compliance files for betting-adjacent products, and stakeholder maps -- meaning sports founders often need two to four active data rooms simultaneously (current investors, new lead, strategic partners, potential acquirers). Peony Data Room at $52 per admin per month includes AI auto-indexing, AI document extraction, Smart Q&A, AI redaction, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. A sports founder running a Series A pitch across 15 investors pays roughly $52 per month on Peony Data Room versus $15,000-$50,000 per deal on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure manually.

I am building a sports betting analytics platform -- which investors specialize in the convergence of sports and gambling technology?

Sports betting and gambling technology is a $160-170B US handle market in 2025 with $10.70B operator revenue, projected to grow 11.02% CAGR to $27.42B by 2034 per IMARC Group -- and full 50-state legalization would add $1.6B in annual tax revenue. For founders in this category, four investors have explicit sportsbook, prediction-market, or gambling-tech portfolios. SeventySix Capital has the deepest network with Diamond Kinetics, Epoxy.ai (sportsbook personalization AI), and Lucra Sports ($10M Series A co-lead in 2024), plus an Athlete Venture Group chaired by Alejandro Bedoya. Courtside Ventures explicitly covers sports and adjacent categories including gaming and sports betting infrastructure with a sports-heavy LP base. 359 Capital invests across sports, media, and entertainment with betting-data convergence exposure. Elysian Park Ventures is on track to exit PrizePicks to Allwyn International for $1.6B in H1 2026 per Yahoo Finance December 2025 reporting. For a seed-to-Series B sports betting analytics founder, SeventySix plus Courtside or 359 Capital is the typical capital stack. Peony Business at $30 per admin per month includes AI redaction that identifies PII, state licensing data, and proprietary algorithms across uploaded documents before capital partners see them, and screenshot protection that blocks and logs screen capture attempts on sensitive compliance files -- something DocSend cannot detect on any plan.

Our team is raising from sports PE for a franchise-adjacent business -- who writes growth checks above $50M?

Sports PE above $50M in 2026 is concentrated in five firms actively deploying into franchise-adjacent businesses, franchise minority stakes, and sports-rights-adjacent infrastructure. Arctos Partners entered 2025 with approximately $11.3B AUM in sports-related funds (Fund II at $4.1B closed 2024, plus $2.7B liquidity-provision strategy) and holds stakes in 25+ franchises globally including NFL Bills and Chargers (8% stake, May 2025), NBA, MLB, European football, and McLaren F1. Sixth Street Partners co-invested in the Boston Celtics $6.1B acquisition March 2025, added stakes in the San Francisco Giants and New England Patriots (closed November 2025), and now holds interests in seven pro-sports franchises across NFL, NBA, MLB, European soccer, and NWSL. Ares Management closed the first NFL PE deal in December 2024 acquiring 10% of the Miami Dolphins at $8.1B valuation. Apollo Sports Capital launched its $5B vehicle in September 2025 and closed its majority acquisition of Atlético de Madrid at €2.2B ($2.55B) on March 12, 2026. RedBird Capital Partners manages $14B AUM across 8 funds, owns AC Milan, and committed $2B to the Skydance-Paramount merger. Bruin Capital closed a $1B raise led by Josh Harris's 26North and TJC in 2026 targeting middle-market sports service businesses. For a $50M-$500M franchise-adjacent growth round, Arctos plus Sixth Street plus Apollo Sports Capital is the realistic capital partner universe. Peony Business at $30 per admin per month includes NDA gates so capital partners sign before any team financials, league revenue allocation schedules, or media rights term sheets are visible, and the Data Room plan at $52 per admin per month adds dynamic watermarks with viewer identity embedded in every frame.

I am a pre-seed sportstech founder -- which accelerator or fund specializes in founders with no institutional backing yet?

For pre-seed sportstech founders without institutional backing, four paths exist in 2026. Stadia Ventures runs a 10-week accelerator program with a $100K equity investment, has invested since 2015, and has 76 portfolio companies including Teamworks which became a unicorn in 2025. LEAD ONE is the pre-seed arm of LEAD's $155M fund family explicitly targeting sports and health tech at the earliest stages. KB Partners frequently writes the first institutional check at the sports-tech intersection with $1M-$3M initial. Courtside Ventures at Fund IV with $100M target and Michael Jordan as LP (October 2025) will write $500K-$3M seed checks for pre-product or pre-revenue founders with unique distribution angles. For a pre-seed sports founder with a defensible data or distribution angle but no product-market fit yet, Stadia's structured accelerator plus LEAD ONE plus Courtside Ventures is the typical stack. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes pre-seed materials (founder backgrounds, market sizing, early pilot data, advisor roster) into a professional folder structure in under 3 minutes so your data room looks like a Series B founder's the day you start pitching.

I am raising capital for a sports startup -- what is a realistic fundraising timeline from first meeting to close in 2026?

Sports-focused fundraising in 2026 typically takes 10 to 16 weeks from first meeting to wire, though specialized investors can move faster when they see strong pilot data. A disciplined process looks like weeks 1-2 for 10 to 15 targeted first calls with sports specialists (Courtside, LEAD, Will Ventures, 359 Capital, KB Partners, SeventySix Capital for betting-adjacent), weeks 3-5 for deep dives with 5-8 interested firms including pilot blueprint review, weeks 6-8 for term sheet negotiation, and weeks 9-12 for legal and closing. LEAD and Courtside Ventures can move faster at seed stage if you show strong retention or engagement curves. 359 Capital targets Series A-B so their diligence process is more structured and may include LP consultations given their strategic sport and media brand base. Sports PE deals above $50M (Arctos, Sixth Street, Apollo Sports Capital, Ares) typically take 16-24 weeks given the league approval requirements and regulatory layering. Throughout this process, Peony Business at $30 per admin per month tracks which investors re-opened your data room after each update with page-level analytics, so you can prioritize follow-ups with genuinely engaged firms rather than chasing silent ones -- visibility that Dropbox and Google Drive cannot provide.

Related Resources

- Data room for a sports team minority-stake sale -- the seller-side process when a fund on this list buys into a franchise: league caps, approval gates, and walled diligence

- Best Data Rooms for Startups -- how to set up your sportstech data room for fundraising

- How to Send Pitch Deck to Investors -- the full deck-distribution workflow for sports founders

- Data Room for Investors -- what investors expect in your data room

- Startup Fundraising Strategy -- the broader fundraising playbook for sports and tech founders

- Consumer Investors -- consumer and DTC VCs active in 2026 (adjacent to sports commerce)

- Top Media Investors -- media specialists that overlap with sports rights

- Due Diligence Data Room Checklist -- 174 documents across all deal types

- Investor Outreach Plan -- 8-step fundraising outreach workflow

- Fundraising Data Rooms -- Peony for fundraising

- Venture Capital -- Peony for VCs and their portfolio companies

- Startup Data Rooms -- Peony for startup founders

You might also like

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026

Apr 29, 2026

Top 8 Boston Investors in 2026: The Founder's Complete Guide to Raising in Boston & Cambridge

Apr 29, 2026

Top 10 Active Investors in Italy (2026): Complete Founder Guide to Italian VC Firms