VC Fund Data Room Checklist (What LPs Actually Diligence) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: March 2026

I've helped hundreds of GPs set up LP data rooms through Peony—from first-time managers running a $30M debut fund to established firms raising Fund IV north of $500M. The pattern is always the same: the GPs who close faster are the ones whose data rooms answer every LP question before it gets asked.

A VC fund data room is a structured, access-controlled digital library that gives prospective limited partners everything they need to evaluate your firm, strategy, track record, operations, and terms. It is the single artifact that turns LP curiosity into conviction—and a sloppy one adds months to your fundraising timeline.

TL;DR: A best-practice LP data room contains 60 to 90 documents across 12 to 14 ILPA-aligned folders, covers everything from your one-pager to side-letter templates, and uses tiered access controls so sensitive materials stay locked until the right moment. This guide gives you the complete folder-by-folder checklist, the rationale behind every document LPs request, and the access-control setup that institutional allocators expect in 2026.

By the Numbers

- $161.4 billion — Global venture capital fundraising reached $161.4 billion in 2024, down from 2021 peaks but still well above pre-pandemic norms, intensifying competition for LP allocations. (PitchBook Global Fund Performance Report, 2025)

- 73% — Nearly three quarters of institutional LPs begin their diligence by reviewing the data room before taking a first GP meeting. (ILPA Due Diligence Best Practices, 2024)

- 90 days — The median time from first LP meeting to first close for emerging managers is roughly 90 days, though poorly organized data rooms can extend that timeline by months. (Preqin Fundraising Benchmarks, 2024)

- 60 to 90 documents — A fully institutional-grade LP data room typically contains between 60 and 90 documents, covering everything from the fund deck to cybersecurity policies. (ILPA Model Data Room Guidelines)

- 12 to 14 folders — Best-practice fund data rooms organize those documents into 12 to 14 ILPA-aligned folders so LPs can navigate using the same structure they see across every manager they diligence. (ILPA Due Diligence Questionnaire)

- 92% — Ninety-two percent of institutional LPs say reporting quality and transparency directly influence their re-up decisions for subsequent funds. (Preqin Investor Survey, 2024)

- 45 days — The SEC proposed that fund advisers deliver quarterly LP statements within 45 days of quarter-end; the Fifth Circuit vacated the rule, but most institutional LPs still benchmark against that timeline. (SEC Private Fund Adviser Rules, 2023)

- Under 3 minutes — Peony's AI auto-indexing organizes an entire fund data room in under 3 minutes, sorting uploaded files into the correct ILPA-aligned folder structure without manual drag-and-drop. (Peony Features)

- $3.2 trillion — Total global private capital dry powder reached $3.2 trillion at the end of 2024, meaning LP capital is available but GPs must compete harder on process and transparency to win allocations. (Bain Global Private Equity Report, 2025)

This post is specifically for GPs raising capital from LPs. If you are a startup founder raising from VCs, see our startup data room checklist. If you need to report to existing LPs after the close, see our LP reporting guide. For continuation vehicle structures, see the continuation vehicle data room guide.

How LPs Actually Use Your Data Room

Understanding the LP review process helps you organize materials in the order they will be consumed.

First pass (10 to 15 minutes): The LP skims your summary, deck, and team bios to decide if deeper diligence is worth the time. If your room is disorganized or missing basics, you lose them here.

Core diligence (days to weeks): They scrutinize strategy, track record integrity, portfolio construction, process consistency, and terms—then benchmark everything against ILPA standards. This is where page-level analytics become invaluable: you can see exactly which sections each LP spent real time on and tailor your follow-up accordingly.

Confirm and close: The LP validates reporting readiness, checks references, reviews legal documents, negotiates side letters, and submits subscription paperwork. A room with built-in e-signatures and NDA gating keeps this phase tight instead of scattered across email threads.

The Complete Folder-by-Folder Checklist

Use a numbered structure that mirrors the way LPs review managers. It keeps version control clean and signals you understand institutional workflows. The structure below aligns with the ILPA Due Diligence Questionnaire and current SEC disclosure requirements.

Folder 00 — Fund Overview and Terms

| Document | Why LPs Ask |

|---|---|

| One-page summary (strategy, target size, target return, fees/carry, geography and stage focus) | Rapid orientation before deeper dives |

| Key terms sheet (management fee, carry, hurdle, preferred return, recycling, key man, term, extensions) | Anchors expectations to the LPA. ILPA Principles highlight transparency on economics and governance |

| Fund deck (economics, pipeline, reserves, governance) | Visual summary for investment committee presentations |

| Contact matrix (IR lead, ops, legal) | Speeds diligence coordination |

Prep note: Your one-pager should be the single document you would send if an LP gave you 60 seconds. Lead with thesis and edge, not biography.

Folder 01 — Firm and Team

| Document | Why LPs Ask |

|---|---|

| Team bios (prior roles, functional strengths, time allocation, conflicts disclosure) | LPs underwrite people first. The ILPA DDQ asks for structured team information |

| Org chart (management company, GP entities, advisory committees) | Maps decision authority and identifies key-person risk |

| Time series of headcount and hiring plan tied to fund size | Verifies execution capacity scales with AUM |

| Key-person plan and succession provisions | Addresses bus-factor risk |

| Compensation and carry overview (vesting, clawback, GP commit) | Alignment of interest check |

Prep note: If partners carry deals from prior firms, prepare an attribution policy (see Folder 03) that clearly delineates pre-firm versus current-firm track record.

Folder 02 — Strategy and Edge

| Document | Why LPs Ask |

|---|---|

| Investment memo on strategy (problem, sourcing, selection, value creation, reserves, exits) | Tests whether the thesis is coherent and differentiated |

| Market maps and theses (where you win and why now) | Validates sector expertise |

| Sourcing funnel data (last 12 to 24 months) | Proves repeatability. Consistency with the ILPA DDQ helps LPs benchmark your pipeline against peers |

| Investment process overview (IC flow, decision rights, conflicts handling) | Governance check |

Prep note: Include both a qualitative strategy memo and a quantitative funnel breakdown. LPs want to see that your sourcing is a system, not a network of warm introductions.

Folder 03 — Track Record and Attribution

| Document | Why LPs Ask |

|---|---|

| Deal-level ledger (gross and net cash flows per deal, TVPI/DPI/IRR, write-ups and write-downs, date stamps) | Core performance evaluation. ILPA reporting conventions set the expected format |

| Attribution policy (who led what, how co-leads are handled, pre-firm deals) | Prevents inflated credit claims |

| Third-party verification or administrator extracts | Independent validation of self-reported numbers |

| Case studies (3 to 6 high-signal narratives: sourcing, decision, value add, exit) | Demonstrates repeatable process, not lucky outcomes |

Prep note: For emerging managers without audited fund-level returns, focus on deal-level attribution with clear methodology footnotes. The SEC Marketing Rule governs how you present performance—coordinate language with counsel.

Folder 04 — Performance Methodology

| Document | Why LPs Ask |

|---|---|

| Methodology memo (calculation methods, benchmark choices, treatment of fees and expenses, cash versus NAV timing) | Comparability across managers |

| Fair value policy (ASC 820 alignment with level hierarchy examples) | Valuation discipline. ASC 820 is the framework auditors and administrators rely on |

Prep note: If you show gross returns without paired net figures, make sure your approach complies with the March 2025 SEC Marketing Rule FAQ updates on extracted and position-level performance.

Folder 05 — Portfolio Construction and Pipeline

| Document | Why LPs Ask |

|---|---|

| Portfolio construction model (target number of names, initial check sizes, ownership, reserve ratios, loss assumptions) | Verifies strategy aligns with fund size and team bandwidth |

| Portfolio summary (company, stage, thesis fit, check size, ownership) | Current exposure snapshot |

| Reserves model and follow-on policy | Capital allocation discipline |

| Pipeline list (illustrative, with stage and thesis fit) | Forward-looking deal flow quality |

| IC memos for select deals (redacted) | Decision-making rigor |

Folder 06 — Operations and Service Providers

| Document | Why LPs Ask |

|---|---|

| Service provider roster (auditor, fund admin, tax, legal counsel, compliance consultant, banking) | Institutional infrastructure check. ILPA calls for clarity on who does what |

| Engagement letters (key providers) | Proves relationships are formalized |

| Management company financials or operating budget | Economic viability of the GP entity |

| Expense allocation policy (fund versus management company) | Fee and expense transparency—one of ILPA's core concerns |

Prep note: LPs will cross-reference your service providers against peers. Naming a Big Four or well-known fund administrator signals operational maturity even for a debut fund.

Folder 07 — Compliance and Regulatory

| Document | Why LPs Ask |

|---|---|

| Form ADV Parts 1 and 2A (and 2B supplements) — current versions | Baseline SEC adviser disclosure. SEC guidance covers content and delivery standards |

| Form CRS (if applicable to your client base) | Required for advisers with retail clients |

| Code of Ethics and Compliance Manual | Controls check |

| Policies for gifts and entertainment, political contributions, personal trading, MNPI handling | Operational controls |

| Marketing compliance memo (SEC Marketing Rule approach) | Performance presentation controls |

| Form D and blue-sky filings | Offering compliance |

AML/KYC note (2026 update): FinCEN adopted an AML program rule for investment advisers but proposed delaying the effective date to January 1, 2028. LPs still expect to see your draft AML policy and vendor approach. Include a readiness plan even if obligations are deferred. View the Federal Register notice.

Private Fund Adviser Rule note: The Fifth Circuit vacated the SEC's private-fund adviser rule on quarterly statements in 2024, and the SEC did not seek review. LPs still broadly expect ILPA-style transparency—use the ILPA templates to meet the spirit without the now-void rule.

Folder 08 — Legal and Offering Documents

| Document | Why LPs Ask |

|---|---|

| Private Placement Memorandum (PPM) or Offering Memo | Primary legal disclosure document |

| Limited Partnership Agreement (clean draft) | LPs compare terms to ILPA's model LPA and Principles 3.0 |

| Subscription package (sub agreement, investor questionnaire, FATCA/CRS forms, wiring instructions). ILPA's model subscription is a useful reference | Closing mechanics |

| GP and ManagementCo org documents (formation certificates, operating agreements) | Entity structure verification |

| Carry waterfall summary (European versus deal-by-deal, hurdles, catch-up) | Economics clarity |

| Key policies referenced in LPA (recycling, key person, conflicts) | Governance cross-check |

Prep note: Foreign and U.S. withholding/reporting obligations under FATCA often surface during subscription. Make sure your package and admin workflow anticipate this.

Folder 09 — Valuation and Audits

| Document | Why LPs Ask |

|---|---|

| Audited financial statements for prior funds (if any) | Independent verification |

| Management company financials (optional but appreciated) | GP economic health |

| Valuation committee charter | Governance around marks |

| Sample valuation memos | Demonstrates adherence to ASC 820 and independent checks |

Folder 10 — Reporting Samples and Readiness

| Document | Why LPs Ask |

|---|---|

| Sample quarterly report (portfolio updates, valuations, fees and expenses) | Reporting quality preview |

| Capital call and distribution notice samples — map to ILPA templates | LPs prefer standardized formats that feed their systems |

| ILPA Reporting Template v2.0 and Performance Template samples | Signals Day 1 operational maturity |

Prep note: Having ILPA-formatted samples ready before your first close is one of the strongest operational signals a GP can send. Many emerging managers skip this and pay for it in longer diligence cycles.

Folder 11 — Responsible Investment (ESG and DEI)

| Document | Why LPs Ask |

|---|---|

| Responsible Investment policy and governance (who owns it, how integrated) | LP mandates increasingly require ESG diligence |

| ESG reporting approach (metrics tracked, cadence). PRI/LP ESG DDQ if applicable | Standardized assessment |

| DEI metrics and initiatives (align with ILPA diversity template) | Growing LP allocation criteria |

| SFDR classification (Article 6/8/9) if marketing in Europe. View SFDR regulation | EU regulatory compliance |

Prep note: Even if you are a small, U.S.-only fund, the market expectation is that you address ESG and DEI. A two-page policy is far better than an empty folder.

Folder 12 — Cybersecurity and Risk

| Document | Why LPs Ask |

|---|---|

| Information security policy (access controls, encryption, incident response, vendor risk) | Even small firms handle sensitive data—LPs care about leak and outage risk |

| Business continuity and disaster recovery plan | Operational resilience |

| D&O and E&O insurance certificates | Risk transfer verification |

| Data room controls note (NDA gating, watermarking, access logs) | Meta-security: how the diligence process itself is protected |

Folder 13 — Side Letters and MFN (Gated)

| Document | Why LPs Ask |

|---|---|

| Pro forma side letter (typical clauses and constraints) | Sets negotiation expectations |

| MFN process description (timelines, scope, carve-outs) | Transparent MFN is now best practice. ILPA analysis provides context |

Prep note: Keep this folder behind a stricter access tier. Only LPs who have signed an NDA and are in active negotiation should see side-letter terms. In Peony, you can set per-folder NDA gates and password protection so this folder stays locked while the rest of the room is open.

Folder 14 — Q&A and RFI Tracker

| Document | Why LPs Ask |

|---|---|

| Central log of LP questions and responses (with dates and versions) | Prevents divergent answers and speeds closes |

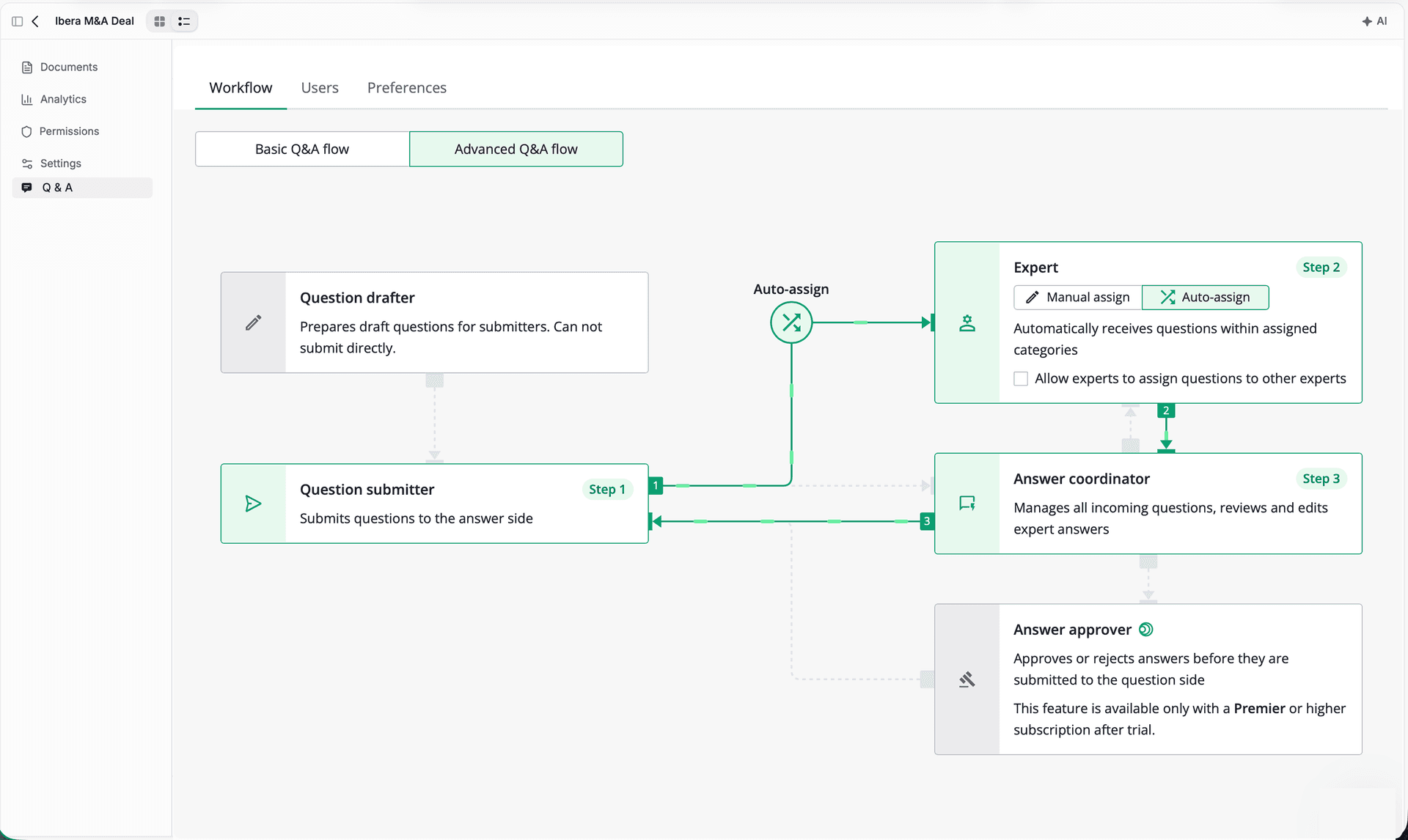

Prep note: A live Q&A tracker is one of the most underrated operational signals. It tells LPs you are organized, responsive, and treating all investors fairly. Peony's advanced Q&A workflow automates this: incoming LP questions are routed to AI for an initial draft, your team reviews and approves, and the finalized answer is sent back with a complete audit trail.

Optional but Frequently Requested

- Advisory committee charter and minutes template — governance depth for larger funds

- ERISA memo (if accepting plan assets): approach to the Plan Asset Regulation and VCOC exception, plus a management-rights letter template for portfolio companies

- References (referenceable LPs and founder references with contact protocol) — typically released late-stage as a closing lever

Fund I vs. Fund II and Beyond — What Changes

The folder structure stays the same. The emphasis shifts.

Fund I managers lean heavier on team narrative, sourcing process evidence, case studies from relevant prior roles, and reference lists because there is no audited multi-year track record yet. Spend extra time on the Strategy and Edge folder and include more granular funnel data.

Later funds lean heavier on net performance tables, ILPA-formatted reporting samples, audited financials, and evidence of LP communication discipline. Your track record folder becomes the centerpiece.

Access Control — Who Sees What During Fundraising

Not every LP should see everything at once. Staged disclosure is standard practice and protects both you and your investors.

Tier 1 — Teaser access (pre-NDA): Fund overview, deck, team bios, strategy summary. Enough to decide if full diligence is warranted.

Tier 2 — Full diligence (post-NDA): Everything in Folders 00 through 12 plus the Q&A tracker. This is the core room most LPs work through.

Tier 3 — Negotiation (post-NDA, qualified only): Side letters, MFN schedules, subscription documents, carry waterfall details. Restrict to LPs who are actively moving toward commitment.

In Peony, you implement this with multi-level access gating: layer NDA gates before Tier 2, add password protection and email verification for Tier 3, and use two-factor authentication for the most sensitive materials. You can adjust permissions per folder or per individual document, and revoke access instantly if a relationship stalls.

Red Flags That Slow or Kill an LP Commitment

After watching hundreds of fundraising processes, these are the patterns that consistently add months to a timeline or lose LPs entirely:

- Track-record math that does not reconcile with fees, offsets, or attribution policy

- No valuation policy or unexplained deviations from ASC 820

- Missing ILPA templates — LPs assume reporting pain after the close

- Security theater — no real cybersecurity or BCP detail

- Side-letter chaos — no standard template, no log, no MFN process

- Stale documents — date stamps from six or more months ago with no changelog

Version discipline matters. Use ISO-style file names (YYYY-MM-DD_Title_v1.2.pdf) and maintain a changelog at the root of your room. In Peony, you can update files after sending the link so your LP always sees the current version without needing a new URL.

Why Leading GPs Build Their Data Rooms in Peony

We built Peony because existing data room tools were either overpriced enterprise software designed for M&A bankers or consumer file-sharing tools with no real security. GP fundraising needs something different: fast setup, institutional-grade access controls, and actionable intelligence on LP engagement.

Set up in minutes, not weeks. Upload your documents and Peony's AI auto-indexing creates the folder structure automatically — sorting, labeling, and organizing 60-plus files in under 3 minutes. No more weekend spent dragging files into folders.

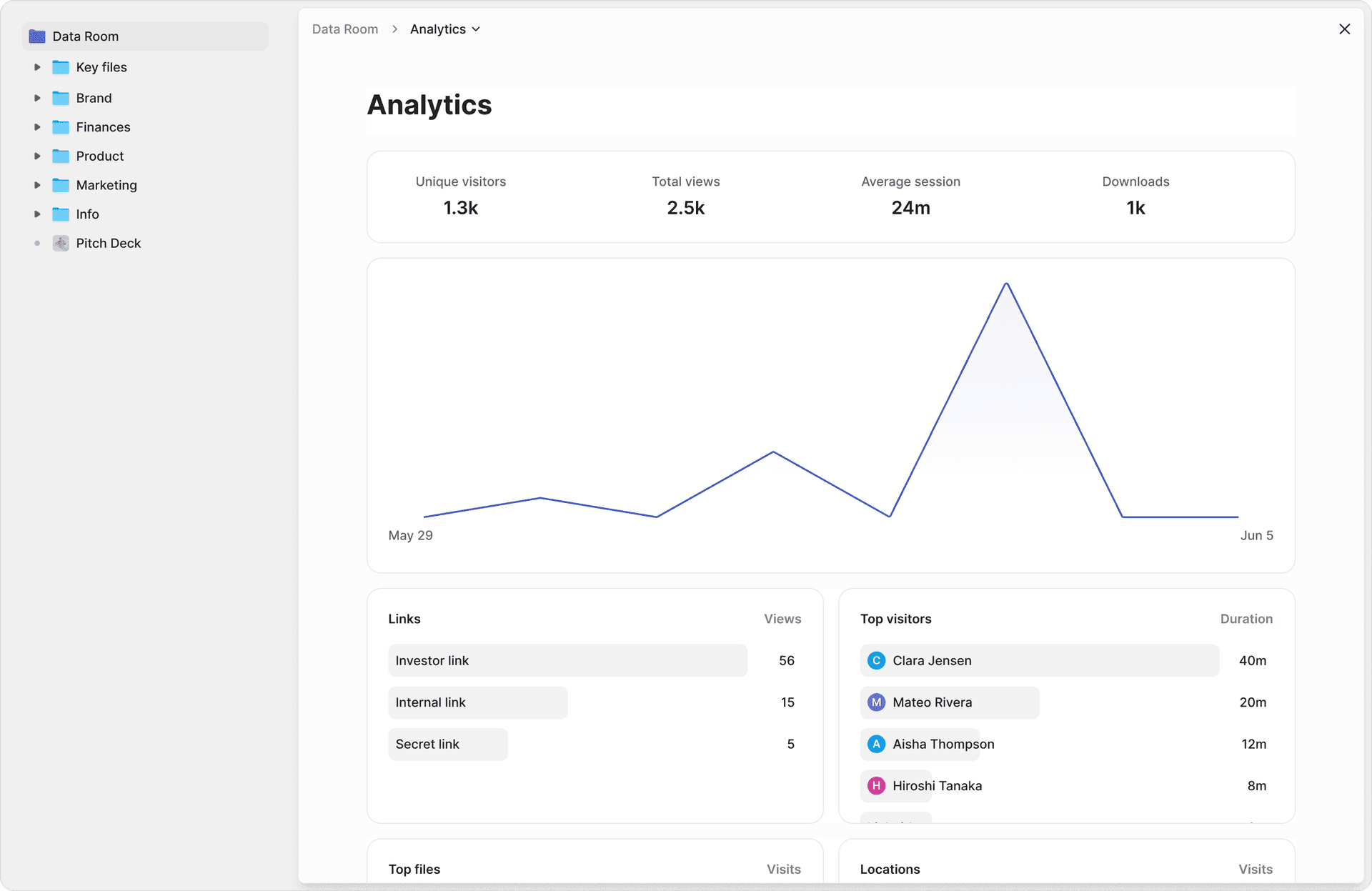

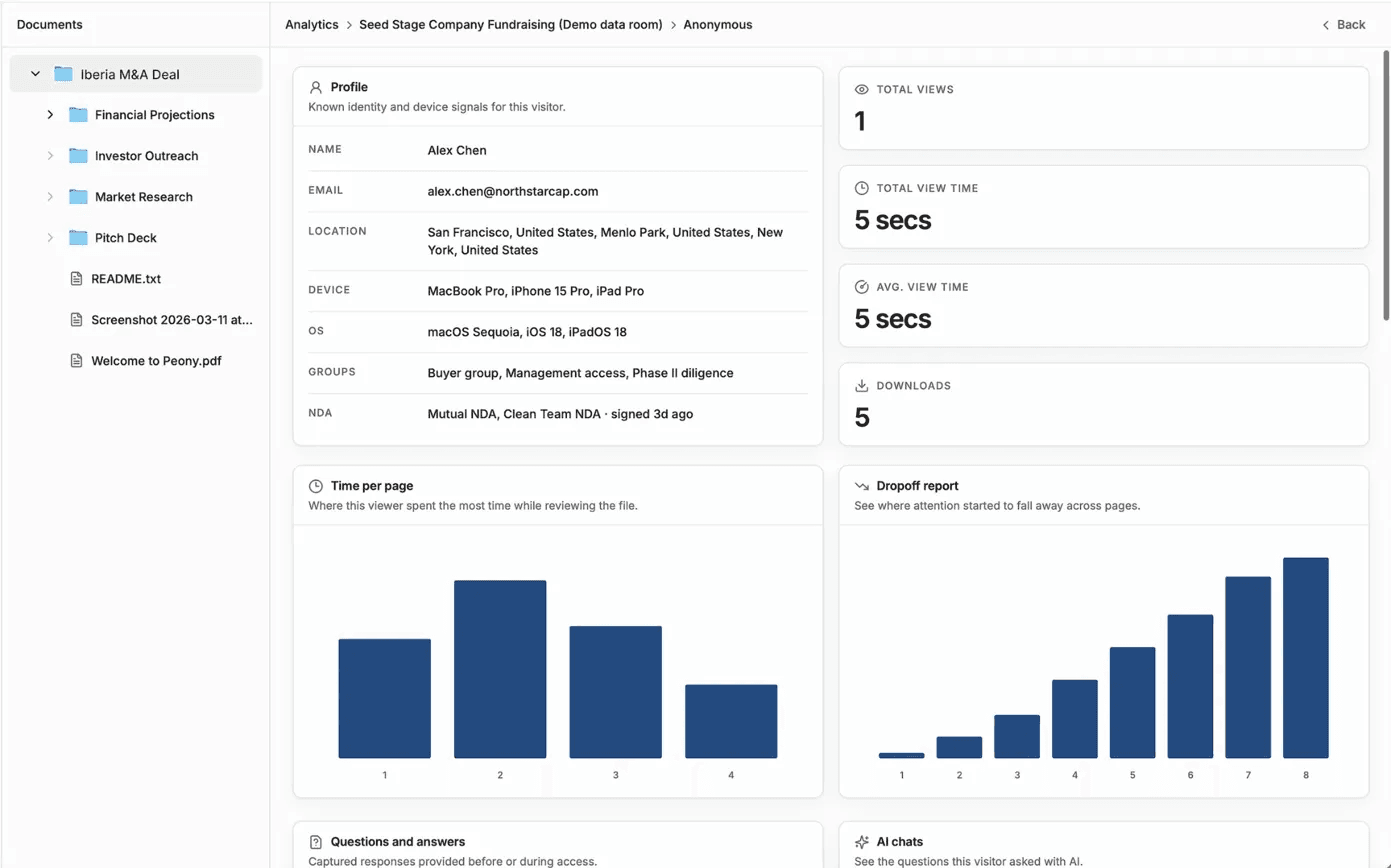

Know what your LPs actually care about. Page-level analytics show which pages each LP read and for how long. You will know if an LP spent 40 minutes on your track record and skipped your ESG policy — or vice versa. That intelligence transforms your follow-up from guesswork to precision.

Security that LPs respect. Screenshot protection blocks and logs capture attempts. Dynamic watermarks embed viewer identity into every rendered frame. NDA gates require a signed agreement before access. This is the level of protection institutional LPs expect for confidential fund materials.

AI-powered LP communication. Peony's Q&A workflow routes incoming LP questions to AI for a draft response, your team reviews and edits, and the approved answer is sent back with a full audit trail. No more conflicting answers across different email threads.

| Feature | Peony | iDeals | Datasite | Firmex |

|---|---|---|---|---|

| Starting price | Free ($0) | ~$500/mo | Custom ($2,500+/mo) | ~$500/mo |

| AI auto-indexing | Yes (under 3 min) | No | Yes (limited) | No |

| Page-level analytics | Yes | Basic | Yes | Basic |

| Screenshot protection | Yes (blocks + logs) | No | Yes | No |

| Dynamic watermarks | Yes (viewer identity) | Yes | Yes | Yes |

| NDA gate before access | Yes | No | Yes | Yes |

| Built-in e-signatures | Yes (AI field detection) | No | No | No |

| Q&A workflow with AI | Yes (4-step approval) | Yes (manual only) | Yes (manual only) | Yes (manual only) |

| Setup time | Under 5 minutes | Hours to days | Days to weeks | Hours to days |

Bottom line: For GP fundraising data rooms, Peony provides the fastest setup, deepest LP engagement analytics, and most complete security stack in the category — starting free. iDeals and Firmex are solid mid-market options if your placement agent already has a relationship. Datasite is purpose-built for mega-fund raises where the brand name matters to sovereign LPs.

One honest caveat. If your anchor LP is a sovereign wealth fund or mega-endowment that has used the same legacy VDR provider for 15 years and mandates it by name in their side letter, Peony's brand won't satisfy that requirement yet. For every other LP — and that covers the vast majority of institutional allocators — Peony matches or exceeds legacy providers on security, analytics, and speed at a fraction of the cost.

Built-in e-signatures. Handle NDA execution, subscription documents, and side letters with Peony's integrated e-signatures — AI-powered field detection means you are not manually placing signature blocks across dozens of documents.

Ask your documents anything. Peony's AI document extraction lets you query across every file in your room with natural language and get cited answers with exact page numbers. When an LP asks about a specific clause in your LPA, you find it in seconds.

AI-powered redaction identifies PII, financial data, and sensitive terms before you share, so you can redact confidential information without manually reviewing every page.

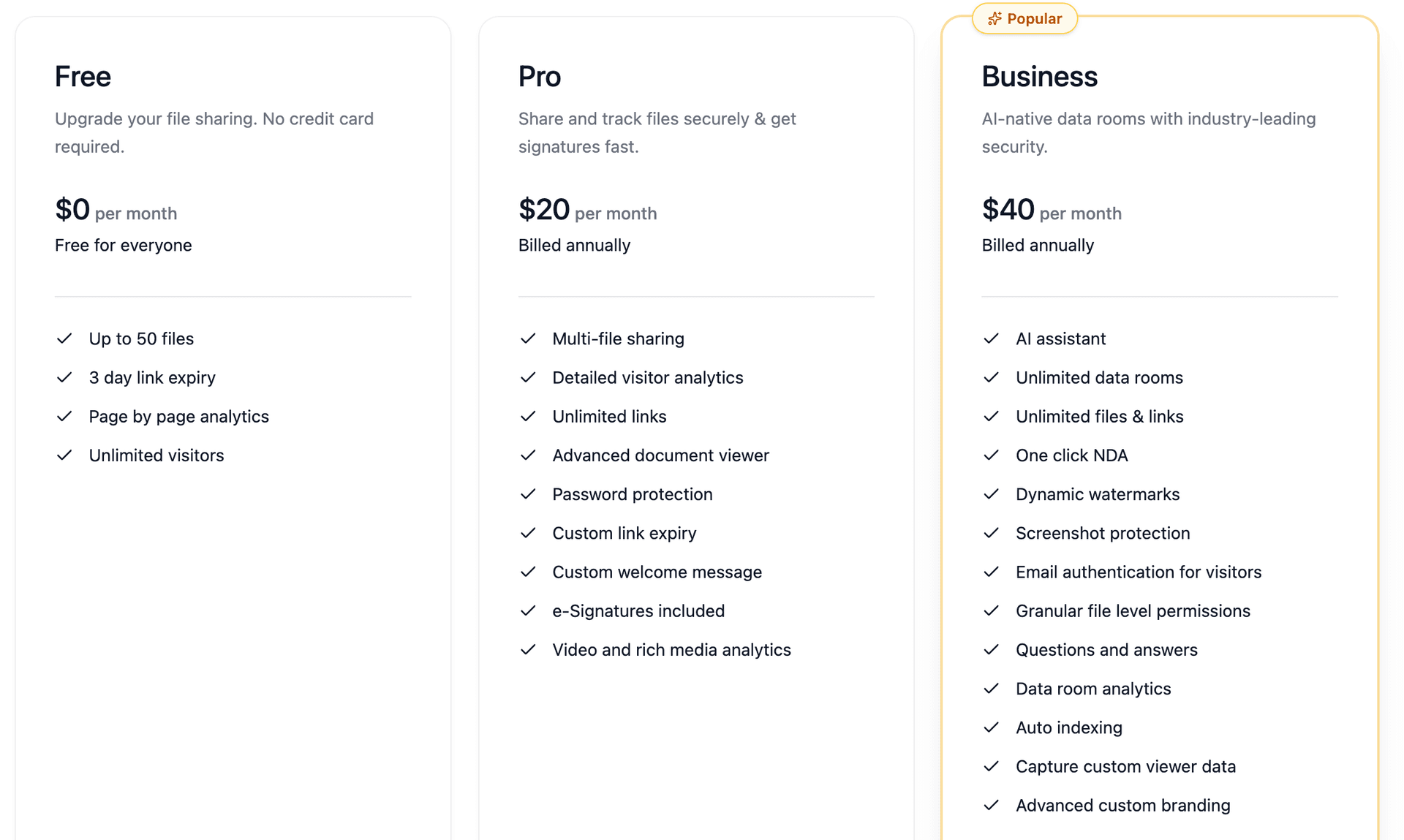

Pricing that works for emerging managers. Peony offers a free tier to get started, Business at $30/admin/month, and Data Room at $52/admin/month. Compare that to legacy VDR providers that charge thousands per month with per-page fees. See full pricing details.

Quick Setup Checklist — 90 Minutes to a Complete Room

- Copy the 14-folder structure above into Peony (or upload everything and let AI auto-indexing do it — see our folder structure guide for cross-deal templates)

- Drop in your one-pager, deck, and team bios (Folder 00 and 01)

- Upload strategy memo, market maps, and funnel data (Folder 02)

- Add performance tables with methodology footnotes and case studies (Folders 03 and 04)

- Load portfolio summary, pipeline list, and reserves model (Folder 05)

- Upload legal drafts — PPM, LPA, subscription package, policies (Folders 07 and 08)

- Add valuation documents and audited financials (Folder 09)

- Complete ILPA Reporting Template v2.0 and Performance Template samples (Folder 10)

- Finish ESG/DEI section with ILPA DDQ and Diversity Metrics Template (Folder 11)

- Set access tiers — enable NDA gating, watermarking, and access logs

- Publish your index and changelog, share the link, and start tracking engagement

The Bottom Line

If you are raising a fund in 2026, your data room is your first product. LPs are not looking for perfection — they are looking for clarity, consistency, and control. A room that mirrors ILPA standards, answers questions before they are asked, and provides institutional-grade security will close your fund faster than a beautifully designed pitch deck ever could.

For emerging managers (Fund I): Start with Peony's free tier. Upload everything, let the AI organize it, and focus your time on the strategy memo and case studies that actually win commitments. Get started here.

For established GPs (Fund II and beyond): Use Peony's Data Room plan ($52/admin/month) for advanced analytics, multi-level gating, and Q&A workflow. Your track record will do the heavy lifting — the data room just needs to present it cleanly and securely. See pricing. If you're running a fundraising or PE fund process, Peony scales with you.

For fund administrators and placement agents: Peony's workspace collaboration lets you manage multiple fund rooms from a single dashboard with consistent branding and security policies. Explore solutions.

Frequently Asked Questions

How many documents does a VC fund data room typically need?

Most GP data rooms contain 60 to 90 documents spread across 12 to 14 folders covering fund overview, legal, track record, operations, compliance, and ESG. Peony's AI auto-indexing sorts and labels uploaded files in under 3 minutes, so you can go from a pile of PDFs to a structured room without spending a weekend on manual organization.

What is the ILPA DDQ and why do LPs expect it?

The ILPA Due Diligence Questionnaire is a standardized template from the Institutional Limited Partners Association that covers strategy, governance, performance, operations, ESG, and DEI. Most institutional LPs use it as their diligence backbone because it makes cross-fund comparison efficient. Peony's page-level analytics let you see exactly which DDQ sections each LP spends the most time on, so you can tailor follow-up conversations to their actual concerns.

Should I gate sensitive documents behind an NDA?

Yes. Side letters, MFN schedules, carried-interest waterfalls, and any documents containing LP personally identifiable information should sit behind a separate access tier with an NDA requirement. Peony supports multi-level gating where you can layer NDA signatures, password protection, email verification, and two-factor authentication per folder or per document, so sensitive materials stay locked until the LP has signed.

How do I track which LPs are actively reviewing my fund materials?

Use a data room platform with page-level engagement analytics rather than simple open-or-not tracking. Peony shows which pages each LP read, how long they spent on every page, and which sections they revisited, giving you a real-time signal of who is doing deep diligence versus casual browsing.

What is the best folder structure for a VC fund data room?

A numbered 12-to-14-folder structure aligned with the ILPA DDQ sections works best: fund overview, team, strategy, track record, performance methodology, portfolio and pipeline, operations, compliance, legal and offering docs, valuation, reporting samples, ESG, cybersecurity, and a gated side-letter folder. Peony's AI auto-indexing can generate this structure automatically from your uploaded files, saving hours of manual sorting.

Do first-time fund managers need the same data room as established GPs?

The folder structure is the same, but the emphasis shifts. Fund I managers lean heavier on team narrative, sourcing process evidence, case studies from prior roles, and reference lists because there is no audited track record yet. Peony's built-in e-signatures with AI-powered field detection let even first-time GPs handle NDA execution and subscription documents inside the same room without bolting on a separate signing tool.

How should I handle LP questions during fund due diligence?

Maintain a centralized Q&A tracker so every LP gets consistent answers and nothing falls through the cracks. Peony's advanced Q&A workflow routes incoming LP questions to an AI that drafts initial responses, your team reviews and approves them, and the finalized answers are sent back with a full audit trail. This prevents conflicting responses and cuts turnaround time significantly.

What security features should a VC fund data room have?

At minimum you need NDA gating, dynamic watermarks, access logs, and the ability to revoke access instantly. Peony goes further with screenshot protection that blocks and logs capture attempts, dynamic watermarks that embed viewer identity into every rendered frame, and enterprise-grade encryption, so even if a document is forwarded, you know exactly who leaked it.

Related Resources

- Data Room for Emerging Managers — The Fund I LP-Tier Stack — anchor for emerging-manager Fund I/II/III LP distribution (Asymmetric Leak Risk Pyramid + 4-Layer EM Confidentiality Stack)

- 5 Pitch Deck Leaks Every Emerging Manager Should Study (2022-2026) — case-study companion: a16z Sept 2025 / Stability AI / Bolt / OpenAI Sutskever / FTX

- Startup Data Room Checklist (for Founders Raising from VCs)

- VC LP Reporting Guide

- Data Room for Investors

- Seed Funding Guide

- Best Data Rooms for Startups

- Continuation Vehicle Data Room Guide

- Startup Fundraising Strategy

- Startup Due Diligence Guide

- Due Diligence Data Room Checklist