Top RWA & Stablecoin Investors in 2026 (Tokenization + Dollar-on-Chain)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

I'm Sean, co-founder of Peony and a former VC at Backed VC and Target Global. Six quarters ago, "crypto investors" and "real-world asset investors" barely overlapped. In 2026, they do — and they do in a specific way that this post is about.

Three things converged: BlackRock's $2B BUIDL fund proved TradFi firms will underwrite tokenized Treasuries at institutional scale; Ethena's USDe stablecoin hit a $6B market cap by being a yield-bearing stablecoin backed by RWA-like basis-trade collateral; and the total stablecoin market crossed $312B in March 2026, making stablecoins the largest on-chain "product" in history. Tokenized treasuries (RWA) and yield-bearing stablecoins are literally the same balance-sheet product with different regulatory wrappers. The investors backing each overlap heavily.

That's why this post covers both. If you are a founder raising for a tokenized-asset protocol, a yield-bearing stablecoin, or an RWA-infrastructure company, these are the 15 investors actually writing checks in 2026 — grouped by what they underwrite on.

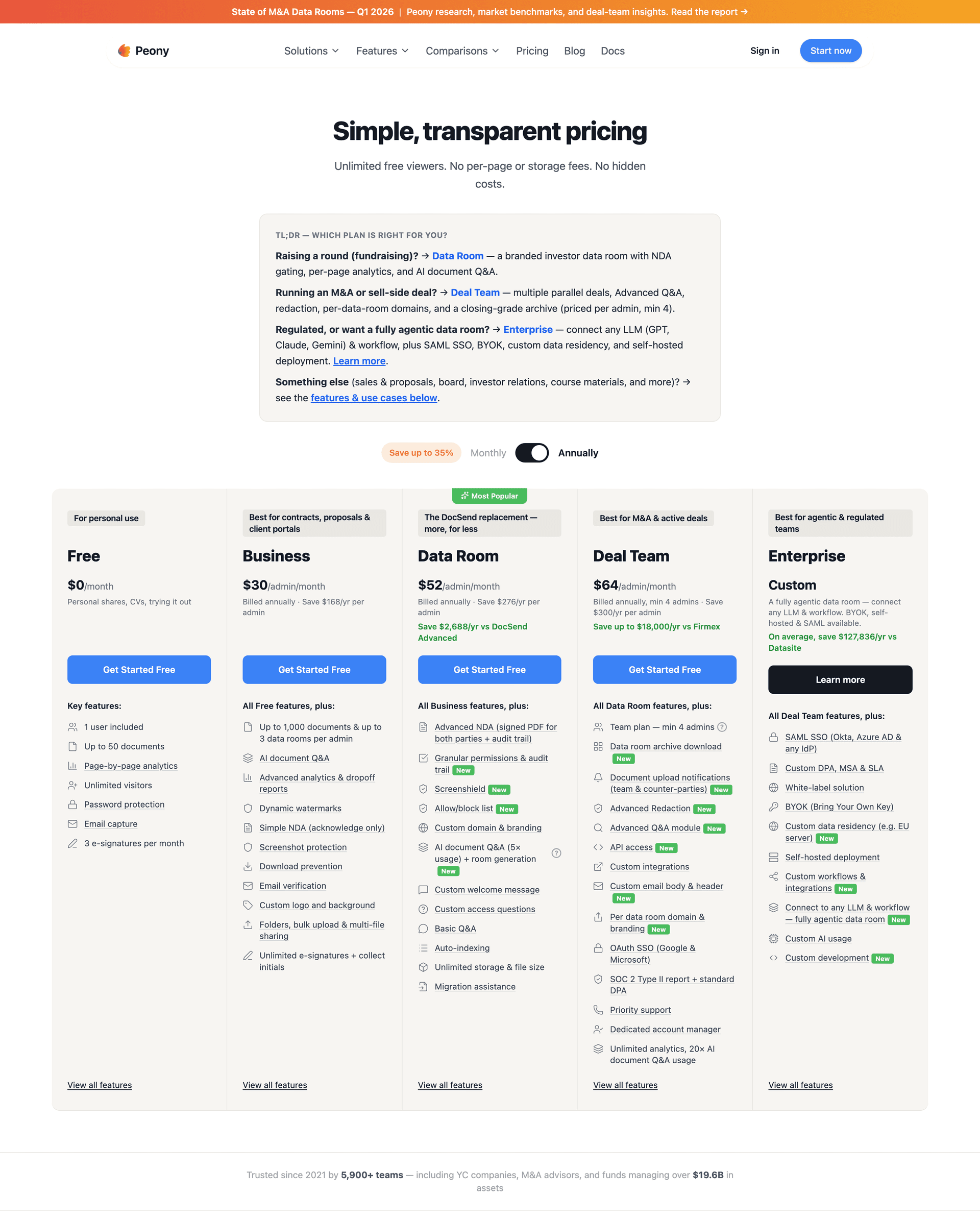

TL;DR: On-chain RWA market stands at $26.4B as of March 2026, up from ~$5B in 2022 — a 380% increase in three years. Tokenized US Treasuries alone grew from $380M in Q1 2023 to $14B in Q1 2026 — a 37x surge. Stablecoins: total market cap is $312B in March 2026, up ~50% YoY. Circle IPO'd in June 2025 at +168% on day one, raising $1.1B with $2.7B FY2025 revenue. The investor landscape divides into four archetypes: TradFi institutional (BlackRock, Franklin Templeton, WisdomTree, Apollo, KKR via Securitize), crypto-native VCs with strong RWA theses (a16z crypto, Paradigm, Dragonfly, Pantera, Haun, Polychain), stablecoin-specialist VCs (Castle Island, Coinbase Ventures, Multicoin, Hack VC), and fintech crossover investors (Flourish, QED, Ribbit). Per Peony's 2026 VDR pricing research, 47% of data room vendors hide pricing entirely — a real tax on RWA founders who need predictable cost structures when running bifurcated TradFi + crypto diligence processes.

Quick guide — match the investor to your stage and profile:

- TradFi-adjacent RWA (tokenized treasuries, regulated yield)? — start with TradFi institutional investors

- Crypto-native RWA (protocol design, tokenomics, on-chain credit)? — crypto-native VCs with RWA theses

- Yield-bearing stablecoin or payments rail? — stablecoin-specialist VCs

- Fintech-crypto crossover (on/off-ramps, wallets, neobanking)? — fintech-crossover investors

- Need the full archetype matrix? — The RWA & Stablecoin Investor Archetype Matrix

Above: the bifurcated RWA + Stablecoin data room workflow — TradFi DD on the left, crypto-native DD on the right, one Peony room, per-folder NDA gates.

Why are we covering RWA and Stablecoins together?

Because tokenized treasuries and yield-bearing stablecoins are the same balance-sheet product with different labels. BlackRock BUIDL, Franklin Templeton FOBXX, and WisdomTree WTGXX are yield-bearing stablecoins wrapped as regulated money-market funds. Ethena USDe, Mountain Protocol USDM, and Superstate USTB are RWA-backed stablecoins wrapped as crypto-native yield tokens. Same underlying cash flow (Treasuries + basis trades), different regulatory posture.

The investor overlap is structural, not coincidental. Franklin Templeton led Ethena's $100M round (a TradFi giant backing a crypto-native stablecoin). Paradigm backs both Circle (USDC issuer) and RWA protocols. Coinbase Ventures holds equity in Circle AND backs Ondo Finance (tokenized Treasuries). A founder building in one category will almost certainly raise from investors active in the other — unless they're in denial about where the market is actually going.

If you were planning to pitch only "pure crypto VCs" or only "TradFi institutions," you're leaving half the addressable capital on the table. The serious funds in 2026 play both sides. (If you're just mapping your broader fundraising sequence, my startup fundraising strategy guide sits upstream of this post and covers the Seed → Series C arc you'll need before you write the first cold email.)

Who are the most active institutional RWA investors in 2026?

The five largest institutional RWA investors in 2026 are BlackRock (BUIDL — $2B AUM), Franklin Templeton (BENJI + FOBXX — ~$700M combined), WisdomTree (WTGXX on-chain), Apollo Global (private credit via Securitize), and the KKR + Hamilton Lane tokenized-PE partnership with Securitize. These are TradFi giants with regulated wrappers — they don't write seed checks; they deploy at the infrastructure layer or as strategic LPs.

1. BlackRock (BUIDL — tokenized Treasury leader)

What they are: BlackRock is the world's largest asset manager ($10T+ AUM). Their on-chain product is the BlackRock USD Institutional Digital Liquidity Fund (BUIDL), tokenized by Securitize.

Current scale: $2 billion AUM as of March 2026, a tenfold increase from the $200M launch AUM in March 2024. Peaked at ~$2.9 billion mid-2025, holding 40%+ of the tokenized Treasury market. Live on Ethereum, Solana, Polygon, Avalanche, Aptos, Arbitrum, Optimism, and BNB Chain — one of the most chain-distributed tokenized products in existence.

How they invest: BlackRock doesn't lead Series A or Series B rounds for RWA startups. They operate at the distribution layer — take BUIDL as a given, and design your protocol to be BUIDL-compatible or BUIDL-competitive. The interesting signal: Circle partnered with BlackRock to move the $10B tokenized Treasury market around BUIDL's mechanical limits — meaning Circle and Ondo and Superstate are now the natural DeFi-native competitors to BUIDL itself.

Who should pitch: Infrastructure providers (custody, compliance, integration) and distribution partners (DEX listings, cross-chain bridges). Not a target for pure-protocol seed rounds.

2. Franklin Templeton (BENJI + FOBXX)

What they are: Franklin Templeton is a $1.6T+ asset manager. Their on-chain product is the Franklin OnChain U.S. Government Money Fund (FOBXX), launched in April 2021 — one of the earliest regulated tokenized Treasury funds. They also operate BENJI ($700M AUM in tokenized Treasury assets).

Current scale: FOBXX has $671M AUM across Stellar, Polygon, Avalanche, Arbitrum, Base, Aptos, and Solana — 8 blockchain platforms total. BENJI adds another $700M.

How they invest: Franklin Templeton made news by co-investing in Ethena Labs's $100M round — a TradFi giant backing a crypto-native yield-bearing stablecoin. This signals Franklin will write strategic checks into protocols that are adjacent to (or competitive with) their own tokenized products.

Who should pitch: Yield-bearing stablecoin protocols, tokenization-infrastructure companies, and cross-chain bridge providers.

3. WisdomTree (WTGXX)

What they are: A $100B+ AUM ETF issuer. Their on-chain product is the WisdomTree Government Money Market Digital Fund (WTGXX), launched in 2023.

How they invest: Similar posture to Franklin Templeton — strategic checks into tokenization infrastructure and DeFi protocols that complement WTGXX distribution. WisdomTree has been outspoken about digital-asset product expansion and has a digital-asset operating subsidiary, WisdomTree Prime.

4. Apollo Global Management (private credit via Securitize)

What they are: Apollo is a $700B+ AUM alternative-asset manager. On-chain, they operate through Securitize — tokenizing slices of their private credit funds for qualified investors.

How they invest: Strategic capital into RWA protocols and tokenization infrastructure, particularly those adjacent to private credit (Centrifuge, Maple Finance, Clearpool). Not a seed-stage investor.

5. KKR + Hamilton Lane (tokenized PE via Securitize and Figure)

What they are: KKR ($600B+ AUM) and Hamilton Lane ($950B+ AUM) have both tokenized portions of their private equity funds via Securitize and Figure Technologies. Hamilton Lane's Senior Credit Opportunities Fund is tokenized and accessible through secondary markets on-chain.

How they invest: Strategic capital into tokenization-platform operators and institutional custody providers. For founders, this is distribution, not seed capital.

Who are the top crypto-native VCs backing RWA and stablecoin protocols?

The top crypto-native VCs actively deploying into RWA and stablecoin protocols in 2026 are a16z crypto (Fund IV $4.5B), Paradigm, Dragonfly Capital (Fund IV $650M, February 2026), Pantera Capital, Haun Ventures ($1.5B), Polychain Capital, and CoinFund. These firms write seed-through-Series-B checks ($1M–$25M) and underwrite on protocol elegance, token economics, and distribution moats. Several of these funds (a16z, Paradigm, Pantera) also show up heavily in my AI investors map — the crypto-AI overlap is real in 2026, and founders pitching AI-powered RWA or on-chain agent infrastructure will want to pressure-test both lists.

1. a16z crypto ($4.5B Crypto Fund IV)

Fund scale: a16z crypto's Crypto Fund IV at $4.5B is the largest dedicated crypto fund ever raised, deployed across seed through growth stages.

RWA + stablecoin portfolio: Ondo Finance, Centrifuge, Maple Finance, Superstate (Robert Leshner's post-Compound venture), and active coverage of the tokenized-Treasury infrastructure stack. Historically backed Coinbase, MakerDAO, Uniswap, and many protocol plays that are now adjacent to RWA.

Stage + check size: Seed through Series B. Check sizes $1M (seed) through $50M+ (growth). They co-lead and lead with equal frequency.

How to pitch: Show protocol elegance first, distribution second, regulatory story third. a16z crypto evaluates founders like technical co-founders — expect hard questions on tokenomics and mechanism design.

2. Paradigm

Fund scale: Paradigm's Fund III is $850M, dedicated to early-stage crypto. Concentrated portfolio strategy — fewer but larger bets per fund.

RWA + stablecoin portfolio: Circle (long-time backer), Ethena (follow-on participant), Ondo-adjacent infrastructure, and multiple RWA protocols. Paradigm's Matt Huang has publicly framed stablecoins as "the killer app" of crypto in 2025-2026.

Stage + check size: Seed and Series A. Check sizes $3M-$25M. They care about technical credibility above all.

How to pitch: Deep technical credibility is the entry point. Come with a working prototype, a clear protocol-level innovation, and a team that has shipped production infrastructure before.

3. Dragonfly Capital ($650M Fund IV, February 2026)

Fund scale: Dragonfly Fund IV closed at $650M in February 2026. Their portfolio has 19 unicorns including Ethena.

RWA + stablecoin portfolio: Led Ethena's seed round ($6M, July 2023) and strategic round ($14M, February 2024) — the canonical "what a crypto-native RWA bet looks like" outcome. Also active in Polymarket, infrastructure plays.

Stage + check size: Seed through Series B. Check sizes $3M-$30M. They have explicit global posture — strong for non-US founders.

How to pitch: Dragonfly leads with conviction when they see structural innovation. Show why your mechanism is better than what exists — and be prepared to defend it technically for an hour.

4. Pantera Capital

Fund scale: Pantera has been investing in crypto since 2013 with multiple fund vehicles — venture fund, liquid fund, and a specialty RWA fund launched in 2023.

RWA + stablecoin portfolio: Ondo Finance (large position), Circle (historical), and multi-stage exposure across tokenization infrastructure, stablecoin protocols, and DeFi primitives.

Stage + check size: Seed through growth. Pantera writes everything from $500K seed checks through $50M growth checks depending on vehicle.

5. Haun Ventures ($1.5B)

Fund scale: Haun Ventures launched with $1.5B — $500M early-stage + $1B acceleration. Founded by former a16z partner and federal prosecutor Katie Haun.

RWA + stablecoin portfolio: Active in RWA infrastructure and stablecoin plays. Katie Haun's regulatory background is a particular asset for RWA founders navigating SEC registration and securities law.

6. Polychain Capital + CoinFund

Polychain: Fund IV first-closed at $200M with multi-billion AUM. Active backer of Maple Finance, Centrifuge, and infrastructure layer. Olaf Carlson-Wee's firm is protocol-focused.

CoinFund: Backed Superstate (Robert Leshner's new protocol), Distributed Global positions in infrastructure. Smaller vehicle but active in the seed-to-Series-A RWA layer.

Who are the stablecoin-specialist VCs in 2026?

The stablecoin-specialist VCs in 2026 — firms where stablecoin thesis is a core conviction, not a secondary bet — are Castle Island Ventures (Nic Carter's fund, thesis-heavy stablecoin research), Coinbase Ventures (Circle equity + USDC ecosystem bets), Multicoin Capital (stablecoin DeFi + on/off-ramps since 2019), and Hack VC (stablecoin infra + RWA). These firms write $1M-$15M checks at seed and Series A and evaluate on payments-stack economics, not pure tokenomics.

1. Castle Island Ventures (Nic Carter — deepest public stablecoin thesis)

Fund scale: Castle Island Ventures III raised hundreds of millions in 2025 — exact figure undisclosed. Previous funds: Fund II at $50M, Fund III is a meaningful step-up.

Stablecoin thesis: Castle Island co-authored the Artemis "Stablecoin Payments from the Ground Up" report in June 2025 — the most-cited institutional research on stablecoin payments rails. Nic Carter has the deepest public writing track record on stablecoin infrastructure, regulation, and payments economics.

Stage + check size: Seed and Series A. $1M-$10M checks. Infrastructure-first — they back public-blockchain infrastructure, stablecoin issuers, and stablecoin-adjacent payment rails.

How to pitch: Come with a payments-stack argument, not a tokenomics pitch. Castle Island evaluates stablecoins as monetary infrastructure, not speculative assets. If you can't articulate unit economics (cost per transaction, interchange dynamics, FX margin), don't bother.

2. Coinbase Ventures (Circle equity + USDC ecosystem)

Fund scale: Coinbase Ventures operates as Coinbase's corporate venture arm, with hundreds of portfolio companies. Coinbase itself holds significant equity in Circle (USDC issuer) and generates a large portion of its revenue from USDC-related yield sharing.

Stablecoin + RWA portfolio: Ondo Finance, Centrifuge (co-invested), countless stablecoin-adjacent bets. The strategic angle: Coinbase wants USDC to win, so they back USDC-complement infrastructure and distribution.

Stage + check size: Pre-seed through Series B. Check sizes $500K (pre-seed) through $10M+ (Series B). Strategic conviction matters — they back ecosystem fits, not just returns.

How to pitch: Articulate how your protocol grows the USDC ecosystem OR creates meaningful optionality around USDC distribution. Coinbase listing pathway can be implicit upside if the fit is right.

3. Multicoin Capital

Fund scale: Multicoin deploys from a $422M venture fund plus a multi-billion liquid/hedge fund. Kyle Samani and Tushar Jain co-founders.

Stablecoin + RWA portfolio: Early backer of Solana-native stablecoin infrastructure, stablecoin on/off-ramps, and multiple DeFi primitives. Strong Solana thesis means they're the first call for Solana-native stablecoin or RWA plays.

Stage + check size: Seed through Series B. Check sizes $2M-$20M. Thesis-driven — they'll pass on great teams that don't fit the thesis map.

4. Hack VC

Fund scale: Hack VC's Fund IV is ~$150M, deployed actively across crypto infrastructure, DePIN, and RWA layers. Ed Roman runs it.

Stablecoin + RWA portfolio: Active in stablecoin infrastructure, cross-chain bridges, and tokenization-adjacent DePIN plays. Chain-agnostic.

Stage + check size: Seed. Check sizes $500K-$3M. Lead investor in many rounds.

How to pitch: Hack VC likes technical founders with real infrastructure experience. Articulate why you're building infrastructure (not an app) and how it becomes a data or liquidity moat.

Who are the fintech-crossover investors backing stablecoin payments?

The fintech-crossover investors active in 2026 stablecoin-payments deals are Flourish Ventures (fintech+RWA overlap, backed by the Omidyar Network), QED Investors (fintech + stablecoin crossover), and Ribbit Capital (fintech + crypto hybrid). These firms bring payments-industry operating knowledge — interchange, FX settlement, correspondent banking — that pure crypto VCs don't have. If your pitch leans more fintech-forward than crypto-native, you'll also want to pressure-test your list against the broader fintech investor universe — many stablecoin-payments founders end up raising a blended round with 2-3 fintech-only checks alongside the crypto-native lead.

Flourish Ventures: Global fintech-focused, strong financial-inclusion thesis. Backed RWA-adjacent fintech across emerging markets. Check sizes $2M-$10M at seed/Series A.

QED Investors: Fintech-focused venture firm founded by ex-Capital One operators. Write $5M-$25M checks into payments infrastructure including stablecoin rails. QED's operator network spans banks, card networks, and PayTech — rare in crypto-native funds.

Ribbit Capital: Long-running fintech fund that has crossed into crypto with Robinhood, Coinbase backing. Hybrid fintech-crypto conviction — writes $5M-$50M checks.

The RWA and Stablecoin Investor Archetype Matrix (Peony 2026 framework)

When a founder asks "who should I pitch first?", the honest answer depends on what they're building and what they underwrite on. This matrix — built from my experience advising 8 RWA and stablecoin founders through their 2025-2026 fundraises — maps the four archetypes against check size, underwriting lens, stage, and diligence process.

| Archetype | Typical Check | Underwrites On | Stage | Example Investors | Example Portfolio | Diligence Length |

|---|---|---|---|---|---|---|

| TradFi institutional | $10M-$100M+ | Regulated yield + distribution reach | Late-stage / strategic | BlackRock (BUIDL), Franklin Templeton (BENJI/FOBXX), WisdomTree (WTGXX), Apollo, KKR | Ondo (Apollo-backed), Superstate (WisdomTree-adjacent), Securitize | 8-12 weeks |

| Crypto-native VC | $1M-$30M | Protocol elegance + token economics | Seed through Series B | a16z crypto, Paradigm, Dragonfly, Pantera, Haun, Polychain, CoinFund | Ethena (Dragonfly), Ondo (a16z), Centrifuge (Paradigm), Maple (Polychain) | 4-8 weeks |

| Stablecoin-specialist | $1M-$15M | Payments economics + infrastructure moats | Seed and Series A | Castle Island, Coinbase Ventures, Multicoin, Hack VC | Stablecoin-adjacent infra, on/off-ramps, Solana-native stablecoins | 4-6 weeks |

| Fintech crossover | $2M-$25M | Payments rails + regulatory posture | Series A/B | Flourish, QED, Ribbit | Emerging-market stablecoins, fintech-crypto hybrids, card-network integrations | 6-10 weeks |

Hands-on observation from 8 RWA and stablecoin founders I've advised through 2025-2026 raises: the median diligence data room contains 40-page legal opinions on securities classification (usually jurisdiction-specific: SEC, MAS, DFSA), regulatory memos per operating geography, token/share structure docs, custody architecture and wallet-infrastructure diagrams, auditor reports (Big 4 preferred), on-chain analytics dashboards, and competitive benchmarks. The average founder raises from at least two archetypes simultaneously — which means the data room must serve both audiences without cross-contamination.

Per Peony's 2026 VDR pricing research, 47% of VDR vendors hide pricing — and neither Datasite (institutional-default, $25K+ per deal) nor Dropbox (crypto-default, zero regulatory controls) handles the bifurcated TradFi + crypto-native workflow. This is precisely what Peony's NDA gates on Data Room ($52/admin/month) solve: TradFi investors see a signed-NDA view of legal opinions and compliance memos, crypto-native VCs see on-chain metrics and tokenomics frictionlessly, and the founder gets per-investor page-level analytics on who actually read what.

How do I actually pitch these investors as an RWA or stablecoin founder? (5 tactical tips)

Lead with regulatory posture first, not protocol elegance. Crypto-native VCs will forgive a rough prototype but not a hand-wavy SEC opinion. TradFi institutions will forgive a novel mechanism but not a missing custody architecture. The five tips below are what separates a funded round from a polite pass.

1. Pick your archetype lead first, then sequence

For each round, identify which archetype will lead: TradFi institutional, crypto-native VC, stablecoin specialist, or fintech crossover. That choice determines your narrative arc. A seed round led by Dragonfly Capital sounds different from a seed round led by QED — same company, very different pitch.

2. Bifurcate your data room by audience

Your legal opinion on securities classification belongs behind an NDA gate. Your on-chain metrics can be public inside the data room (crypto-native VCs dislike friction). Peony Data Room ($52/admin/month) gives you per-folder NDA gates so you can have one room serving both audiences without leaking regulatory exposure to crypto Twitter.

3. Show unit economics, not TVL vanity metrics

TVL is a starting point but not an argument. Show margin per dollar of TVL, revenue per token holder, and path to sustainable yield spreads. This is where Castle Island's Artemis stablecoin payments research becomes your reference text — investors expect you to understand payments economics at that depth.

4. Be explicit about which chains and why

Chain choice is distribution, not religion. BUIDL is live on 8 chains. Ondo is multi-chain. Your chain strategy signals how seriously you've thought about distribution — and investors evaluate accordingly.

5. Prove you can pass institutional DD

Even if you're raising from crypto-native VCs first, your architecture should pass an institutional DD cycle. That means Big 4 auditor, Chainalysis compliance, SOC 2 Type II roadmap, and a clear path to qualified-custodian integration. Investors check for this even at seed — because they know your next round will require it.

What's driving the 2026 RWA and stablecoin deployment wave?

Three converging trends: (1) regulatory clarity in the US (the 2025 CLARITY Act created a workable stablecoin framework), (2) TradFi distribution infrastructure catching up (BUIDL on Uniswap, Securitize on BNB), and (3) yield differentials between TradFi and DeFi compressing — meaning a tokenized 5.2% Treasury is suddenly more attractive than a 6% DeFi yield with 10x the risk.

The net result: tokenized Treasuries grew 37x from Q1 2023 to Q1 2026, stablecoin market cap crossed $312B, and Circle went public at +168% on day one with $2.7B FY2025 revenue. If the Centrifuge COO's projection of $100B+ RWA TVL by end of 2026 is even half-right, 2026 will be the year RWA becomes the dominant use case for crypto infrastructure.

That's why these 15 investors matter more now than ever. The window to raise a meaningful round as an RWA or stablecoin founder is widest right now — and it will narrow as category leaders emerge.

The bottom line: which investors do I actually pitch first?

| Your profile | First-priority investors | Rationale |

|---|---|---|

| Tokenized-treasury protocol (seed, $5M-$10M) | Dragonfly, a16z crypto, CoinFund, Pantera | Crypto-native with deep Treasury-layer thesis; Dragonfly led Ethena twice |

| Yield-bearing stablecoin (seed, $5M-$8M) | Dragonfly (Ethena playbook), Paradigm (Circle/Ethena), Castle Island, Hack VC | Technical-mechanism underwriting; fast DD cycles |

| Stablecoin payments rail (Series A, $10M-$20M) | Castle Island, QED, Flourish, Coinbase Ventures | Payments economics + fintech-stack operating knowledge |

| Real-estate RWA (Series A, $10M-$15M) | Ribbit, Flourish, Hack VC, Multicoin | Fintech overlap; chain-agnostic |

| Institutional tokenization infrastructure (growth, $25M+) | Apollo (via Securitize), BlackRock (strategic), KKR, Paradigm | Distribution partners, not seed capital |

| Emerging-market stablecoin (Series A, $5M-$10M) | Dragonfly (global), Multicoin, Pantera, Hack VC | Global posture; understand non-US regulatory diversity |

| Chain-infrastructure RWA (Series B, $15M-$30M) | a16z crypto, Paradigm, Pantera, Polychain | Scale capital for infrastructure plays |

Every one of these conversations runs more smoothly with a bifurcated Peony data room — per-folder NDA gates for TradFi LPs, frictionless access for crypto-native VCs, and per-investor analytics telling you who's actually reading your legal opinions versus just opening the deck. Data Room at $52/admin/month with unlimited data rooms, or Business at $30/admin/month if you only need a room or two per concurrent raise. Details in the pricing guide.

Frequently asked questions

I'm building a tokenized-treasury protocol — should I pitch BlackRock BUIDL's team, Ondo Finance's backers, or crypto-native VCs first?

Pitch crypto-native VCs (a16z crypto, Paradigm, Dragonfly) and RWA specialists (Castle Island, Hack VC) first — they evaluate protocol elegance and token economics at Seed and Series A, writing $3M-$15M checks. BlackRock's team doesn't lead seed rounds; they come in later as strategic capital or distribution partners. Ondo Finance's own backers (Founders Fund, Pantera, Coinbase Ventures) are the closest playbook — they back tokenized-treasury infrastructure at the growth stage. For a founder raising $8M at a $40M valuation, a Peony data room on Data Room ($52/admin/month) with page-level analytics, NDA gates, and AI auto-indexing lets you run TradFi diligence (40-page legal opinions, custody memos) and crypto diligence (on-chain analytics, tokenomics) in parallel — something Dropbox and Google Drive cannot separate by audience.

I'm a yield-bearing stablecoin founder — should I pitch Paradigm (who led Ethena USDe), Castle Island, or traditional RWA investors?

All three, sequenced by check size and conviction profile. Dragonfly led Ethena's initial rounds (seed $6M July 2023, strategic $14M February 2024) and followed with a $100M later round that brought in Franklin Templeton and Fidelity Ventures — so Dragonfly is the obvious warm-intro target for a USDe-style protocol. Castle Island's Nic Carter has the deepest stablecoin thesis in venture; pitch them on payments-rail economics and on/off-ramp unit economics. Traditional RWA investors (Apollo, Hamilton Lane, KKR via Securitize) care about the regulated wrapper. With Peony Business ($30/admin/month), you can gate the legal opinion on securities classification behind an NDA for TradFi investors while letting crypto VCs see the on-chain metrics freely — a bifurcated workflow Dropbox cannot support.

I'm an asset manager exploring tokenization — which RWA infrastructure providers (Ondo, Centrifuge, Securitize, Superstate) are actually VC-backed vs bootstrapped?

All four are VC-backed with substantial rounds. Ondo Finance is backed by Founders Fund, Pantera, Coinbase Ventures, and Tiger Global — their TVL crossed $2.5B in January 2026. Centrifuge is backed by BlueYard Capital, IOSG Ventures, and Coinbase Ventures; TVL on real-world credit. Securitize is backed by Morgan Stanley, BlackRock (strategic — BlackRock's BUIDL is tokenized by Securitize), and Sony Ventures; they power BUIDL's $2B AUM. Superstate (Robert Leshner's post-Compound venture) is backed by CoinFund and Distributed Global. If you're an asset manager vetting infrastructure, the VC backing signals commercial viability but isn't sufficient — regulatory posture and chain coverage matter more. Peony's data room gives you a single workspace to evaluate vendor diligence packages side-by-side.

I'm raising $8M Series A for a tokenized-real-estate platform — which RWA investors lead at that stage?

Hack VC, CoinFund, Multicoin Capital, and Dragonfly lead Series A rounds in the $5M-$15M range for infrastructure-heavy RWA plays. a16z crypto co-leads at the same stage with their $4.5B Crypto Fund IV. Castle Island Ventures Fund III (~$250M+ range, 2025 close) backs thesis-aligned stablecoin and RWA infrastructure at seed and Series A. For real-estate-specific RWA, the warm-intro path runs through Ribbit Capital (fintech overlap) and Flourish Ventures. A well-organized data room matters more for real-estate RWA than pure-crypto because investors want to see jurisdiction-specific SEC opinions, title-chain tokenization architecture, and cap-table clarity in one place. Peony's AI auto-indexing on Data Room ($52/admin/month) organizes 300+ diligence documents in under 3 minutes — something DocSend does not do at any tier.

I'm a fintech founder pivoting to stablecoin payments — which investors actually understand on/off-ramp unit economics?

Three camps: fintech-crypto crossover VCs, payments-native funds, and stablecoin specialists. Flourish Ventures and QED Investors have the deepest fintech knowledge and understand interchange, FX, and settlement economics from traditional payments — they evaluate stablecoin plays as payments-stack upgrades. Ribbit Capital backs both fintech and crypto with hybrid conviction. For pure stablecoin thesis, Castle Island Ventures (Nic Carter's thesis work) and Paradigm (Circle backer, Ethena lead) are the sharpest. Dragonfly Fund IV ($650M, closed February 2026) explicitly includes stablecoin and RWA infrastructure. Multicoin Capital has backed stablecoin DeFi and on/off-ramps since 2019. Peony's NDA gate on Data Room ($52/admin/month) lets you share jurisdiction-specific banking partnership agreements with investors under signed confidentiality — a control Google Drive cannot enforce.

I'm a crypto VC analyst evaluating RWA deal flow — how do I separate hype from institutional-grade opportunities?

Three filters: (1) real-world asset quality — are the underlying assets actually creditworthy, audited, and legally assignable? (2) tokenization wrapper integrity — is the issuer SEC-registered, audited by Big 4, with Chainalysis-level compliance? (3) distribution — is there actual institutional demand, or is this a retail play with institutional marketing? BlackRock BUIDL's $2B AUM is real demand. Many "institutional" projects have $10M TVL from five crypto hedge funds and no real institutional investors. Use Peony's data room to organize your internal memos and benchmark data when you're pitching LPs on your RWA thesis — page-level analytics show which LP spent time on your institutional-distribution section vs skimming the deck.

I'm an emerging-markets stablecoin issuer in Latam or Southeast Asia — who backs non-US stablecoin plays?

Dragonfly Capital explicitly has global posture and backs emerging-market plays. Multicoin Capital backs global stablecoin on/off-ramps. Pantera Capital invests internationally with multi-stage exposure. In Latin America specifically, Kaszek Ventures and Valor Capital are fintech+crypto hybrids that understand local payment rails. In Southeast Asia, Hack VC and Global Founders Capital have backed regional crypto infrastructure. For African stablecoin founders, Hack VC and Castle Island Ventures have both deployed into Africa-focused crypto infrastructure. The regulatory story differs per jurisdiction — use Peony Data Room ($52/admin/month) to bucket jurisdiction-specific regulatory memos into separate folders with different NDA gates per investor geography, which lets you avoid sharing Singapore MAS opinions with US-focused VCs who don't need them.

I'm a family office allocating to RWA — what's the realistic due diligence timeline with these 15 firms?

Expect 4-12 weeks depending on whether you're allocating to a fund (crypto-native VC) or direct into a protocol (tokenized treasury, real estate RWA). Crypto-native VCs have faster DD cycles (4-6 weeks for a fund commitment) but they require you to understand tokenomics and on-chain metrics fluently. TradFi-backed RWA funds (BUIDL, BENJI) have TradFi DD timelines (8-12 weeks with compliance, legal, and custody reviews). For family offices new to RWA, the hardest gate is custody — who holds the private keys and under what regulatory wrapper. A Peony data room on Business ($30/admin/month) lets the manager package all of these diligence artifacts into one NDA-gated room; Dropbox cannot enforce the NDA acceptance step that institutional DD programs typically require.

I'm building on Solana rather than Ethereum — which RWA and stablecoin investors are chain-agnostic?

Most top-tier RWA and stablecoin investors are chain-agnostic in 2026 — BlackRock BUIDL is live on Ethereum, Solana, Polygon, Avalanche, Aptos, Arbitrum, and Optimism via Securitize. Franklin Templeton FOBXX is on Stellar, Polygon, Avalanche, and others. For Solana-specific expertise, Multicoin Capital has the deepest Solana thesis and has backed Solana-native stablecoin infrastructure heavily since 2020. a16z crypto backs both chains. Paradigm is Ethereum-leaning but has Solana exposure. Hack VC is chain-agnostic with strong Solana DePIN and RWA bets. Castle Island Ventures is infrastructure-focused and chain-agnostic. Use your Peony data room to share chain-architecture diagrams, validator-economics memos, and MEV-risk docs in one structured location — investors evaluate chain choice as a distribution decision, not a philosophy.

I'm raising from both BlackRock-type institutional investors AND a16z crypto at the same time — how do I manage the two different diligence processes?

You need a bifurcated data room: one NDA-gated section for regulatory, legal, and custody artifacts (what TradFi cares about) and one for on-chain metrics, tokenomics, and protocol architecture (what crypto-native VCs care about). Peony's Data Room plan ($52/admin/month) handles this with per-folder NDA gates, per-link access controls, and personalized tracking links — so BlackRock gets a signed-NDA view of your legal opinion on securities classification, a16z crypto gets a frictionless view of your on-chain analytics, and you see per-investor analytics on who reviewed what. DocSend has no NDA gating at any tier, and Google Drive can't differentiate audiences within one share. This bifurcation is the single biggest workflow challenge for RWA founders — and it's what the Peony data room was built for.

Related resources

- Best Data Rooms for Startups

- Startup Data Room Checklist

- How to Send a Pitch Deck to Investors

- How to Require an NDA on a Pitch Deck

- Different Passwords for Different Investors (IS Playbook)

- Virtual Data Room Cost Guide (Peony 2026 Pricing Research)

- Top B2B SaaS Investors

- AI Investors

- Fintech Investors

- Startup Fundraising Strategy

- Data Rooms for Fundraising

- Venture Capital Data Rooms

- NDA Feature

- Page-Level Analytics

- AI Auto-Indexing

- Peony Pricing

You might also like

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026