Seed Funding for Startups (What 200+ Data Rooms Taught Me) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Seed Funding for Startups in 2026 (What 200+ Data Rooms Taught Me)

Last updated: March 2026

We run Peony, a data room platform, and over the last two years I have helped hundreds of startups set up data rooms for their seed rounds. I have watched founders raise $500K pre-seed bridges and $5M seed rounds. I have seen what investors actually open first, which documents they spend the most time on, and where deals stall because materials were not ready.

This guide comes from that vantage point — not as a fundraising coach, but as someone who sees the inside of seed round data rooms every single day and knows exactly where founders lose momentum.

TL;DR: The median US seed round in 2026 is around $3 million, most raised on post-money SAFEs. Plan to spend 3 to 6 months fundraising. Build a target list of 50 to 80 investors, lead with warm introductions, and have your data room ready before your first meeting — not after. The founders who close fastest are the ones who never make an investor wait for a document. Peony (free tier available) gives you page-level analytics, AI auto-indexing, and e-signatures so you can track engagement and close without stitching together five different tools.

By the Numbers

- $3.1 million — median US seed round in 2025, up from $2.1 million in 2020 (Carta State of Startup Funding)

- 70%+ of US seed deals closed on SAFEs in 2025, with post-money SAFEs now the dominant instrument (Y Combinator SAFE data)

- 15–25% — typical founder dilution in a seed round, depending on valuation cap and instrument

- 3–6 months — average time from first investor meeting to wire transfer at the seed stage

- Under 30% of seed-funded startups go on to raise a Series A (Crunchbase Funding Report)

- 68% of data breaches involve a human element — forwarding a Google Drive link with your cap table is exactly the kind of mistake that causes them (Verizon 2024 DBIR)

What Is Seed Funding, Exactly?

Seed funding is the first significant external capital a startup raises after the idea stage. It sits between pre-seed (friends and family, small angels, your savings) and Series A (institutional venture capital at scale). The money is meant to get you from a working product to product-market fit — hiring your first engineers, acquiring your first paying customers, and building enough traction to prove the business works.

In 2026, seed funding is not just a dollar amount. It is a signal. When a credible seed investor writes a check, they are telling the market: "This team and this problem are worth betting on." That signal matters when you need to recruit, sign enterprise customers, or raise your Series A.

Where seed fits in the funding ladder:

| Stage | Typical Range | Primary Source | Goal |

|---|---|---|---|

| Pre-seed | $100K–$500K | Angels, friends and family, pre-seed funds | Build MVP, prove technical feasibility |

| Seed | $1.5M–$4M | Seed VCs, angel syndicates, accelerators | Validate product-market fit, build core team |

| Series A | $8M–$25M | Institutional VCs | Scale go-to-market, expand market position |

How Much Should You Raise?

This is the question I see founders get wrong most often — and I can tell because the financial model in their data room does not match the ask on their pitch deck.

The formula is simple: calculate your monthly burn rate for the next 18 months, then add a 20 percent buffer for things that will inevitably cost more than planned. That is your raise target.

Here is what the benchmarks look like in 2026:

- SaaS / B2B software: $2M–$4M (median $3M)

- Consumer apps: $1.5M–$3M (median $2M)

- Fintech: $3M–$5M (higher because of compliance costs)

- Biotech / deep tech: $4M–$8M (longer development timelines)

- Marketplace: $2M–$3.5M (need capital for both supply and demand sides)

Valuation expectations: Post-money valuations for seed rounds range from $8M to $25M depending on sector, traction, and geography. A SaaS company with $20K MRR and 20% month-over-month growth might justify a $15M post-money cap. A deep tech startup with strong IP but no revenue might land at $10M.

What investors actually check: When a VC opens your Peony data room, the financial model is almost always the second document they read (after the deck). They are looking for unit economics that make sense — customer acquisition cost, lifetime value, gross margins, and a path to profitability that does not require three more rounds. If your model says you need $3M but your burn assumptions only justify $1.5M, they will notice.

The Three Seed Instruments: SAFE, Convertible Note, Priced Equity

The legal instrument you choose determines your cap table structure, your dilution, and how much you spend on lawyers. Here is how each one works in practice.

SAFE (Simple Agreement for Future Equity)

A SAFE is a contract where an investor gives you money now in exchange for equity later — typically at your next priced round. No interest, no maturity date, no monthly payments. The investor gets shares when a triggering event happens (usually a Series A).

Post-money SAFEs (the Y Combinator standard) are now dominant. The key difference from pre-money SAFEs: your dilution is calculable from day one. If you sell $3M in post-money SAFEs with a $12M cap, investors own exactly 25% — regardless of how many SAFEs you issue.

When to use a SAFE:

- First seed round with multiple investors closing at different times

- You want to minimize legal costs (a SAFE is a 5-page document)

- Standard US seed deal structure — investors expect it

Watch out for: Stacking too many SAFEs at different caps. I have seen founders on Peony with four SAFEs at four different valuations, and the cap table becomes genuinely confusing before Series A. Keep it clean.

Convertible Note

A convertible note is debt that converts to equity later. Unlike a SAFE, it has an interest rate (typically 2–8%) and a maturity date (usually 18–24 months). If the note matures before a conversion event, you technically owe the money back — though in practice, most notes get extended or converted.

When to use a convertible note:

- Bridge round between major raises

- Investors who prefer debt structure (more common outside the US)

- Situations where a SAFE is not standard in your jurisdiction

Watch out for: Maturity date pressure. If you have not raised a priced round by maturity, you are in an uncomfortable negotiation with your note holders.

Priced Equity Round

A priced round means you are selling actual shares at a defined price per share. This requires a formal valuation, a lead investor to set terms, and significantly more legal work (expect $15K–$50K in legal fees versus $2K–$5K for a SAFE).

When to use a priced round:

- You have a strong lead investor who wants board governance

- Raising $4M+ where institutional terms make sense

- International investors who are unfamiliar with SAFEs

Watch out for: Over-engineering the governance for a seed stage company. You probably do not need three board seats, anti-dilution ratchets, and full drag-along rights at $3M.

How to Find Investors for Your Seed Round

The biggest mistake I see in the data rooms on Peony is not a bad financial model — it is a founder who pitched five investors over three months instead of fifty investors over six weeks. Seed fundraising is a parallel process, not a sequential one.

Build Your Target List (50–80 Investors)

Start by mapping the investor landscape to your specific stage and sector:

Seed venture capital firms — These are funds that write $250K–$2M checks into seed rounds. They run a process similar to Series A funds: partner meetings, investment committee votes, and formal due diligence. Examples include First Round Capital, Initialized Capital, Founder Collective, and Uncork Capital.

Angel investors — Individual investors writing $25K–$250K checks with faster decision timelines (1–3 weeks versus 4–8 weeks for funds). Find them through AngelList, angel groups, and warm introductions from other founders.

Accelerators — Y Combinator ($500K for 7%), Techstars ($120K for 6%), and 500 Global ($250K for 5%) combine capital with intensive programs. The equity cost is fixed regardless of your valuation, so the earlier you join, the more expensive it is in relative terms. Also see our guides to accelerators in San Francisco, Boston, healthcare, and worldwide.

Sector-specific funds — For fintech, look at funds like QED Investors and Ribbit Capital. For healthcare, check 7wire Ventures. For climate, Lowercarbon Capital. These investors bring domain expertise alongside capital. Browse our US seed investor directory for a curated list.

Prioritize Warm Introductions

Cold emails work about 2–5% of the time at seed stage. Warm introductions work 25–40% of the time. The math is obvious. For a template and delivery strategy that maximizes response rates, see our guide on how to send your pitch deck to investors.

Where warm intros come from:

- Other founders in the investor's portfolio

- Accelerator mentors and alumni

- Advisors, board members, and existing investors

- Customers who happen to know VCs (more common than you think)

Create Competitive Tension

Fundraising is a market. When multiple investors are interested simultaneously, terms improve, timelines compress, and FOMO works in your favor. This is why you launch outreach in waves — not one investor at a time.

The cadence I recommend:

- Weeks 1–2: Pitch your Tier 3 list (practice, refine, gather feedback)

- Weeks 3–4: Pitch your Tier 2 list (polished materials, sharper narrative)

- Weeks 5–6: Pitch your Tier 1 list (optimized pitch, social proof from Tier 2 interest)

- Ongoing: Maintain 15–20 active conversations at all times

How to Prepare Your Data Room

This is the part where I have the most direct insight — I watch founders set up fundraising data rooms every day on Peony, and the difference between a well-organized room and a messy one is measurable. Investors who get a clean data room move faster to term sheet. Investors who get a Google Drive folder full of unsorted PDFs stall.

What Goes in a Seed Data Room

Your seed data room is not your Series A data room. Investors at this stage are not doing a 200-document legal review. They want to validate that you are real, organized, and not hiding anything obvious.

Essential documents (have these ready before your first meeting):

- Pitch deck (10–12 slides, updated monthly)

- Executive summary (2-page overview for investors who want text, not slides)

- Financial model (24-month projections with clear assumptions)

- Cap table (current ownership, outstanding SAFEs, option pool)

- SAFE or term sheet template (so investors know what instrument you are using)

Due diligence documents (share when an investor moves to serious interest):

- Articles of incorporation and bylaws

- Founder agreements and vesting schedules

- IP assignment agreements (every employee and contractor)

- Key customer contracts or LOIs

- Product metrics (MRR, growth rate, retention, engagement)

- Team bios with LinkedIn links

- Bank statements (last 3–6 months)

Why a Purpose-Built Data Room Matters at Seed

I am biased, obviously — We built Peony. But here is what I have observed from thousands of rooms (and you can see how we compare in our best data rooms for startups breakdown):

The Google Drive problem: About 40% of the seed-stage founders I talk to start by sharing documents through Google Drive or Dropbox. The issues are predictable — no analytics (you have no idea if an investor actually read your model), no access controls (one forwarded link and your cap table is public), and no watermarking (leaked documents are untraceable). If you are weighing these tools against purpose-built alternatives, our DocSend alternatives review compares every serious platform.

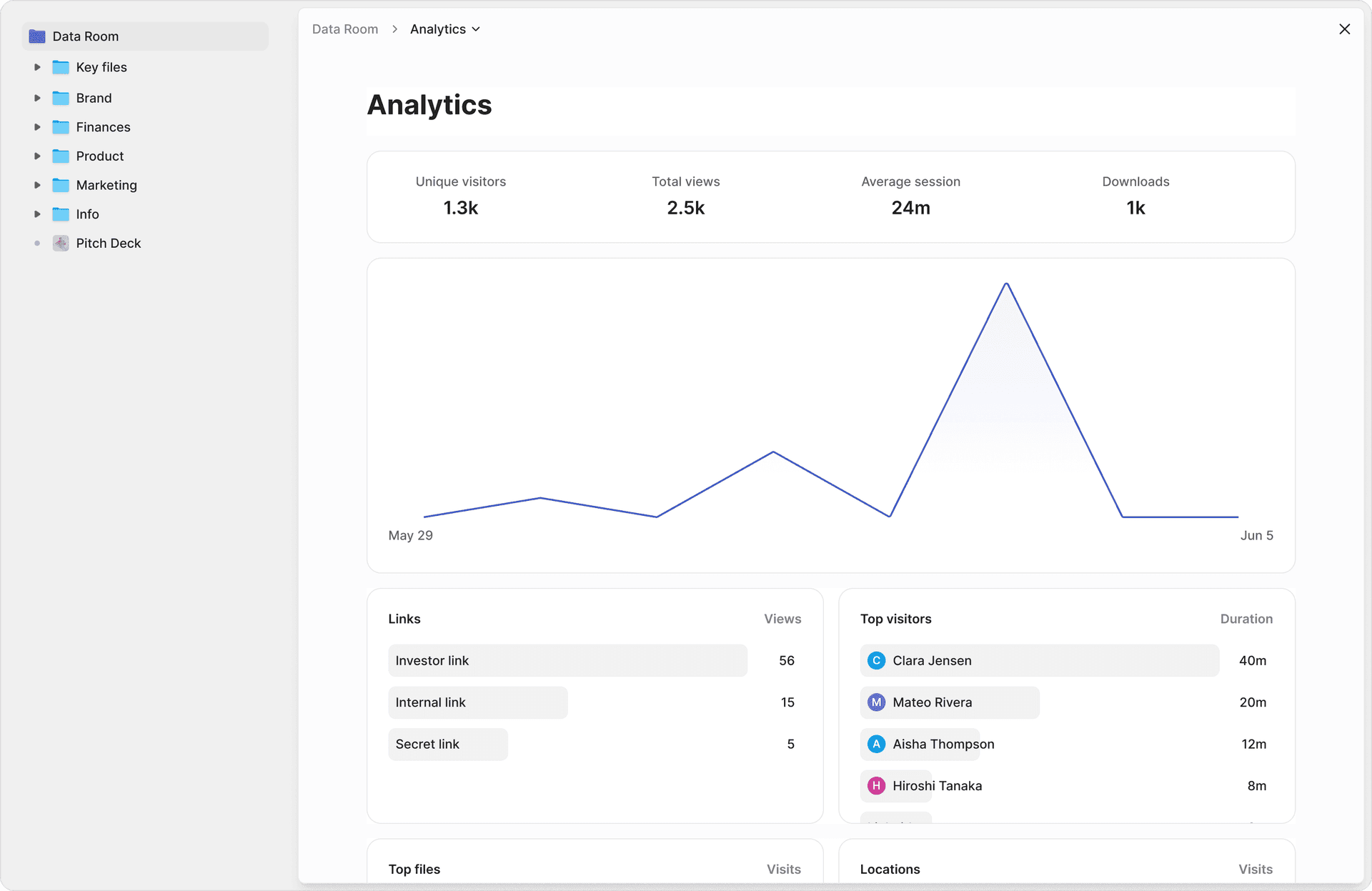

What Peony gives you that matters for seed:

- Page-level analytics — See which investors actually read your financial model versus which ones just opened the deck. This changes how you prioritize follow-ups.

- AI auto-indexing — Upload your documents and the AI creates the folder structure. I have watched founders spend 2 hours organizing a Google Drive versus 3 minutes on Peony.

- Dynamic watermarks — Every page renders with the viewer's email address. If your deck leaks, you know exactly who shared it.

- E-signatures — Close your SAFE agreements inside the same platform where you shared the deck. No switching to DocuSign.

- Link-level permissions — Share the pitch deck with 50 investors, but gate the financial model behind an NDA. Different access levels for different stages of the conversation.

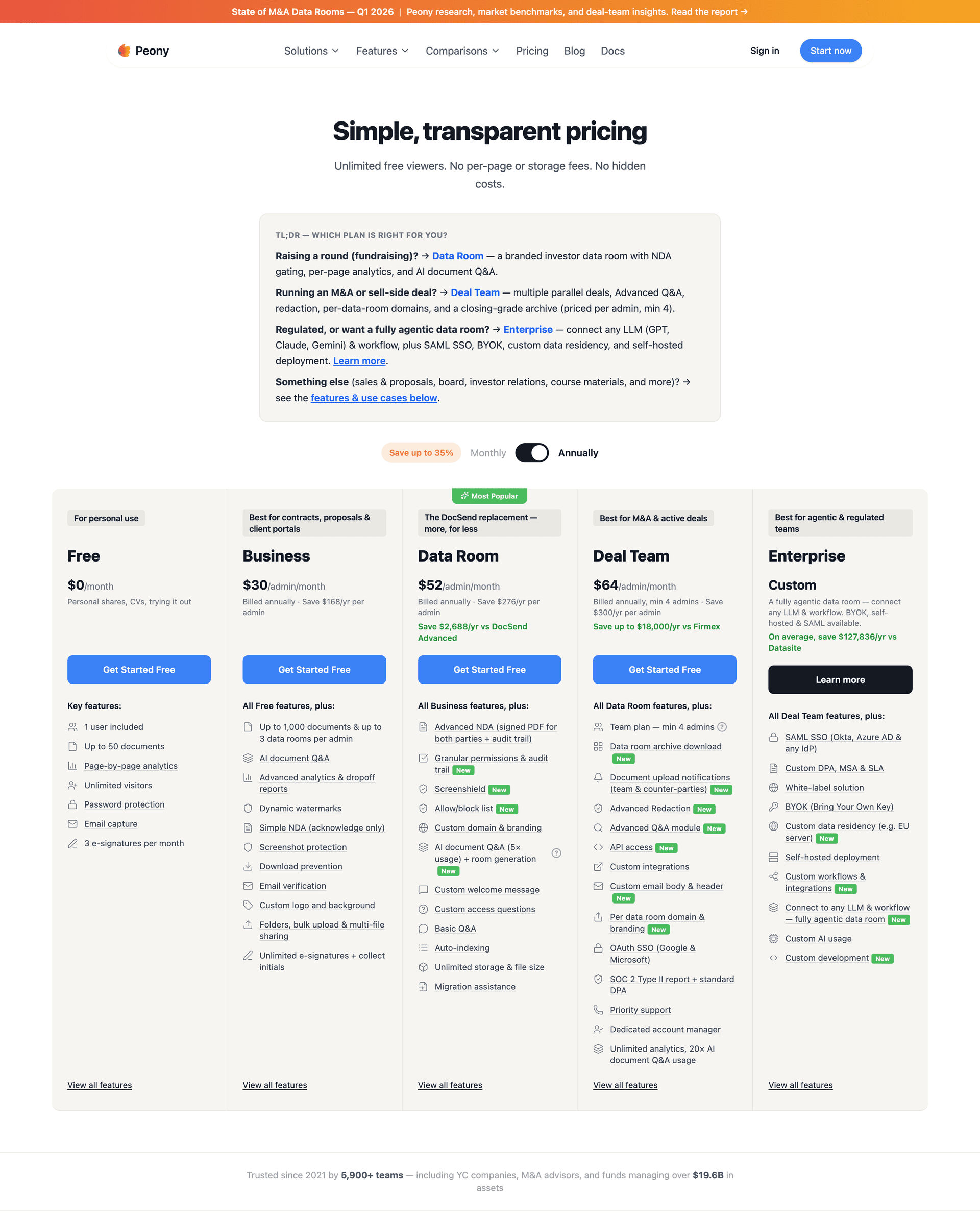

Pricing: Peony starts free. The Business plan at $30/admin/month includes page-level analytics and screenshot protection. The Data Room plan at $52/admin/month adds dynamic watermarks, unlimited data rooms, and AI auto-indexing. Most seed-stage founders start on Free and upgrade when they enter due diligence.

The Pitch Process: Step by Step

Here is the process as it actually works in 2026, based on what I see in investor engagement patterns through Peony's analytics.

Step 1: The Warm Intro or Cold Outreach

The first touch is a forwardable email — 3 to 5 sentences. Problem you are solving, why now, one traction metric, and an ask for 30 minutes. Attach nothing. If they are interested, they will reply.

Step 2: The First Meeting (30–45 Minutes)

This is a conversation, not a presentation. Walk through your deck, but spend most of the time on the problem, your insight, and your traction. Leave the detailed financials for the data room.

After the meeting: Send a follow-up email within 24 hours with a link to your Peony data room. This is when you will see the first real engagement data — did they open the deck? Did they look at the financials? Did they spend 12 minutes on your customer contracts or 30 seconds on the cover page?

Step 3: The Deep Dive (Partner Meeting or Second Call)

If an investor is serious, they will schedule a deeper session — often with a partner or the full investment team. This is where they probe your unit economics, competitive positioning, and team capability.

Before this meeting: Check your Peony analytics to see which documents they spent the most time on. If they focused on your customer contracts, expect questions about retention and churn. If they lingered on the cap table, expect questions about prior investors and dilution.

Step 4: Due Diligence

The investor has decided they want to invest, pending verification. They will request access to your full data room — corporate documents, IP filings, employment agreements, bank statements.

This is where preparation pays off. If your data room is already organized on Peony, you grant access with one click. If your documents are scattered across Google Drive, email attachments, and your lawyer's Dropbox, you lose 1–2 weeks gathering materials — and momentum dies.

Step 5: Term Sheet and Closing

The lead investor sends a term sheet. You negotiate (more on this below). Once terms are agreed, your lawyer drafts the definitive agreements, and you execute through e-signatures inside your data room. Wire transfer follows.

Total timeline: 4 to 12 weeks from first meeting to close, depending on investor type and deal complexity. Angels move faster (1–3 weeks). Institutional seed funds move slower (6–12 weeks).

Seven Mistakes That Kill Seed Rounds

These are not theoretical — I have watched each one play out through the data rooms on Peony.

1. Starting Outreach Before Your Materials Are Ready

What happens: An investor says "send me your deck," and you spend 3 days frantically building a financial model. By the time you send it, the investor has moved on. The engagement data in your Peony analytics shows they opened the link 4 days later and spent 90 seconds before closing.

The fix: Have your data room loaded and tested before you send your first outreach email. Period.

2. Pitching Investors Sequentially

What happens: You pitch one investor, wait 3 weeks for a response, pitch the next one. Six months later, you have talked to 12 investors and have no term sheet.

The fix: Run a parallel process. Launch outreach to 15–20 investors in the same 2-week window. Create urgency through legitimate competitive interest.

3. Raising Too Much or Too Little

What happens: Raise too little and you are fundraising again in 8 months. Raise too much at a high valuation and you set a bar you cannot clear for Series A.

The fix: Model 18 months of runway with a 20% buffer. Be honest about your burn rate in the financial model that sits in your data room.

4. Ignoring the Cap Table

What happens: You stack four SAFEs at different caps, add an advisor with 3% equity, and by the time Series A comes around, you own 45% of your company and the math does not work for institutional VCs.

The fix: Maintain a clean, updated cap table in your data room. Model future dilution before accepting any new investment.

5. Obsessing Over Valuation

What happens: You spend 6 weeks negotiating a $15M cap versus a $12M cap while your best investors lose patience and move on.

The fix: Evaluate the full term sheet — not just valuation. Board seats, pro-rata rights, information rights, and investor reputation matter as much as the number on the cap.

6. Sharing Documents Without Security

What happens: You email your cap table and financial model as PDF attachments. They get forwarded. Your competitor sees your margins. Your current employer sees your moonlighting project. This is more common than founders think — our guide on how to protect your pitch deck covers every prevention method.

The fix: Use a platform with dynamic watermarking, access controls, and screenshot protection. See our full guide on how to protect your pitch deck. Every document shared through Peony is traceable to the specific viewer.

7. Losing Track of Investor Engagement

What happens: You send your data room link to 40 investors and have no idea who actually looked at it. You follow up with everyone equally, wasting time on investors who never opened the link. See our full guide on tracking pitch deck engagement for the analytics framework I use.

The fix: Use page-level analytics to prioritize. The investor who spent 20 minutes in your financial model is a warmer lead than the one who spent 30 seconds on the deck cover.

Negotiating Your Term Sheet

When a lead investor sends a term sheet, here is what to focus on — in order of importance for seed stage:

Valuation Cap (for SAFEs) or Pre-Money Valuation

This determines your dilution. Post-money SAFE caps make the math simple: divide your raise by the cap to get the percentage sold. A $3M raise on a $12M post-money cap is 25% dilution.

Option Pool

Investors will typically ask for a 15–20% option pool carved out before their investment. This means the dilution comes from your shares, not theirs. Negotiate the pool size based on your actual 18-month hiring plan — do not accept 20% if you only need 12%.

Pro-Rata Rights

These give investors the right to maintain their ownership percentage in future rounds. Standard at seed. Generally fine to grant — it means your investors want to keep backing you.

Board Composition

At seed, most startups have a 3-person board: 2 founders and 1 investor. Some SAFEs come with no board seat at all. Be cautious about giving up board control this early — you are a long way from needing formal governance.

Information Rights

Investors will want quarterly financial updates and annual audited statements. This is reasonable. What to push back on: weekly reporting obligations, unlimited data room access, or consent rights over routine business decisions.

After the Wire: What Comes Next

Closing the round is not the finish line — it is the starting gun.

Deploy Capital Strategically

A typical seed allocation in 2026:

- Product and engineering (35–40%): Hire your first 3–5 engineers, build core features

- Go-to-market (25–30%): Sales team, marketing experiments, customer success

- Team (20–25%): Key hires across product, design, operations

- Operations and overhead (10–15%): Legal, accounting, office, tools

Communicate with Investors

Set a monthly update cadence from day one. Use a template: key metrics, wins, challenges, asks. The founders who keep investors informed get faster responses when they need introductions, advice, or bridge capital.

Keep your Peony data room active as an ongoing investor portal. Upload quarterly financials, board decks, and KPI dashboards so your investors always have access to current materials — and you can track who is actually reading them.

Start Preparing for Series A on Day One

Fewer than 30% of seed-funded startups raise a Series A. The ones that do share common traits:

- $1M+ ARR or strong equivalent traction

- 100%+ year-over-year growth

- Positive unit economics (or a clear path within 6 months)

- Clean data room with 18+ months of organized financials

Start building your Series A data room inside Peony the moment your seed round closes. Twelve months of well-organized financial history, board minutes, and customer metrics will make your next raise dramatically faster.

Bottom Line

Seed fundraising in 2026 is not fundamentally different from any other year — you need a strong team, a real problem, early traction, and a compelling pitch. What has changed is the tooling. You no longer need to spend $500/month on an enterprise VDR to present professionally, and you no longer need to guess which investors are actually interested. For a full comparison of what those tools cost, see our virtual data room cost guide.

Here is my honest recommendation:

- If you are pre-revenue or very early: Focus on the SAFE instrument, target angels and accelerators, and use Peony Free to share your deck with tracking.

- If you have $10K–$50K MRR: Target seed VCs, run a parallel process with 50+ investors, and use Peony Data Room ($52/admin/month) for full data room capabilities with unlimited rooms, AI auto-indexing, and page-level analytics.

- If you are raising $4M+: Consider a priced round with a lead investor, engage a startup attorney, and use your Peony data room for the full due diligence process — AI auto-indexing, watermarking, NDA gates, and audit trails.

The founders who close fastest are never the ones with the best pitch. They are the ones who never make an investor wait for a document.

Frequently Asked Questions

How much seed funding should a startup raise in 2026?

The median seed round in 2026 is around $3 million, but the right number depends on your 18-month plan. Calculate your monthly burn rate, multiply by 18, and add a 20 percent buffer. Most founders I work with on Peony raise between $1.5 million and $4 million. Use a Peony data room to organize your financial model, burn projections, and cap table so investors can verify your numbers during due diligence.

What is a SAFE note and how does it work for seed funding?

A SAFE (Simple Agreement for Future Equity) is a contract where an investor gives you money now in exchange for equity later — typically at your next priced round. It is the most common seed instrument in 2026, used in roughly 70 percent of US seed deals. When founders set up their Peony data room for a seed raise, the SAFE agreement and cap table are usually the first documents investors request.

How do I find angel investors for my seed round?

Start with warm introductions through your network, accelerator alumni, and existing advisors. Platforms like AngelList, LinkedIn, and accelerator demo days are strong channels. Build a target list of 50 to 80 investors matched to your stage and sector. Then set up a Peony data room with your pitch deck, financials, and team bios so you can share a secure link the moment an investor expresses interest.

What documents should be in a seed round data room?

A seed data room should include your pitch deck, executive summary, financial model with 24-month projections, cap table, SAFE or term sheet template, articles of incorporation, founder agreements, IP assignments, key customer contracts, and product metrics dashboard. Peony's AI auto-indexing organizes all of these into a standard folder structure automatically — upload everything and the system sorts it in under 5 minutes.

How long does it take to close a seed round in 2026?

Plan for 3 to 6 months from first outreach to wire transfer. Hot deals with strong traction can close in 4 to 6 weeks, but that is the exception. The founders who close fastest on Peony are the ones who have their data room ready before the first investor meeting — no scrambling to find documents when due diligence starts.

Should I use a SAFE or convertible note for my seed round?

In 2026, SAFEs dominate seed rounds because they are simpler, cheaper to execute, and have no maturity date or interest accrual. Convertible notes still make sense for bridge rounds or when investors insist on debt structure. Either way, store the executed agreements in a Peony data room so your cap table stays clean and every investor can access their documents through a secure, trackable link.

What metrics do seed investors look for in 2026?

Seed investors want to see product-market fit signals: monthly recurring revenue of $10,000 to $50,000, month-over-month growth of 15 to 20 percent, strong retention, and a clear path to unit economics. Present these in a metrics dashboard inside your Peony data room — page-level analytics will show you which sections each investor spends the most time on, so you know what resonates.

How do I prepare for investor due diligence during a seed round?

Organize your corporate documents, financials, legal agreements, IP filings, and product metrics before you start outreach. Use a Peony data room with granular permissions so you can control exactly who sees what — share the pitch deck broadly, but gate sensitive financials and cap table details behind NDA requirements. Peony's audit trail logs every view, download, and access event for your records.

What are the biggest mistakes founders make during seed fundraising?

The three most common mistakes I see through Peony data rooms: starting outreach before materials are ready, pitching investors sequentially instead of in parallel, and obsessing over valuation while ignoring governance terms. Founders who set up their Peony data room first — with financials, deck, cap table, and team bios organized — consistently close faster because investors never have to wait for documents.

How much equity should I give away in a seed round?

Most seed rounds in 2026 dilute founders by 15 to 25 percent, depending on the instrument and valuation. Post-money SAFEs make dilution math straightforward — a $3 million raise on a $12 million post-money cap means exactly 25 percent dilution. Keep your cap table updated in a Peony data room so both you and your investors have a single source of truth throughout the round.

Related Resources

- Q1 2026 Startup Fundraising Benchmarks — fresh seed and Series A medians, dilution, sector and city velocity

- Startup Data Room Checklist — Everything that belongs in your data room, organized by stage

- Startup Fundraising Strategy — Complete fundraising guide from seed to Series C

- AI-Powered Pitch Deck Creation Guide — Build a compelling deck faster

- Top US Seed Investors — Curated directory of active seed funds

- Best Data Room for Investors — What VCs actually want to see in a data room

- Startup Due Diligence Guide — What investors check and how to prepare

- How to Send Your Pitch Deck to Investors — The right way to share your deck without losing control

- Best Data Rooms for Startups — Side-by-side comparison of platforms built for fundraising

- How to Protect Your Pitch Deck — Watermarking, access controls, and leak prevention

- How to Track Pitch Deck Engagement — See who opened your deck and which slides they read

- Digital Sales Room Guide — How to build data rooms that accelerate sales cycles

- VC Fund Data Room Checklist — What GPs need when raising from LPs

- Startup Fundraising Rounds Guide — Pre-seed through IPO, stage by stage

- Series A Data Room — the next round, where your data room gets graded against benchmarks

- Due Diligence Data Room Guide — Complete guide to due diligence rooms

- Secure File Sharing Guide — Protect sensitive documents in transit

- Notion Data Room Guide — Why Notion falls short for investor sharing

- Peony Pricing