Startup Due Diligence Guide (Both Sides of the Table) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Startup Due Diligence Guide (Both Sides of the Table) in 2026

Last updated: March 2026

We run Peony, a data room platform, and I have been through due diligence from both sides — raising capital for Peony and hosting hundreds of DD processes inside our data rooms. I have watched founders panic when an investor's counsel sends a 200-item document request on a Thursday afternoon. I have also seen the investor side: VCs skimming seven data rooms in a week, forming snap judgments about a company's maturity based on how the room is organized.

This guide covers the process of startup due diligence — what happens, why, and how to survive it — whether you are the founder preparing for scrutiny or the investor running the evaluation. If you are looking for the specific documents you need to assemble, see our companion piece: the startup data room checklist.

TL;DR: Startup DD is a structured investigation of your company's legal, financial, technical, and operational reality. Seed-stage DD runs 1 to 3 weeks; Series A takes 4 to 8 weeks; Series B and later can stretch 6 to 12 weeks. According to Carta, incomplete documentation is the #1 cause of deal delays. Deloitte research links poor DD preparation to 4 to 8 week delays and 10 to 15% valuation reductions. Peony (free tier available) gives you AI auto-indexing that organizes DD documents in under 5 minutes, page-level analytics that show which sections each investor actually reads, and enterprise security (screenshot protection, dynamic watermarks, NDA gates) to protect your most sensitive information during the process.

By the Numbers

- 4–8 weeks — average deal delay caused by incomplete or disorganized data rooms (Deloitte)

- 10–15% — valuation reduction linked to poor DD preparation (Deloitte M&A research)

- 73% of dealmakers would walk away from a deal with undisclosed cybersecurity issues (SRS Acquiom 2025 Study)

- 68% of data breaches involve a human element — forwarded links, screenshots, and permission errors (Verizon 2024 DBIR)

- Under 30% of seed-funded startups go on to raise a Series A (Crunchbase)

- $4.8 trillion — global M&A deal value in 2025, up 36% from 2024, making DD volume the highest in years (Bain & Company)

- 60 seconds — time before an experienced investor forms a first impression of your data room organization

- Under 5 minutes — setup time for AI-powered data rooms like Peony, vs. 20 to 40 hours for manual organization

What Startup Due Diligence Actually Is

Due diligence is the structured investigation an investor or acquirer conducts before committing capital. It is not a background check. It is not reading your pitch deck more carefully. It is a systematic examination of whether your company is what you say it is, where the risks are, and whether the team can execute.

For startups, DD answers three questions:

- Is this company real? — Do the financials match the narrative? Is the corporate structure clean? Does the IP belong to the company?

- Where are the risks? — Legal disputes, customer concentration, technical debt, regulatory exposure, cap table problems?

- Can this team execute? — Is the founder organized, honest, and in control of operations?

The depth scales with the stage. A seed investor might spend a weekend reviewing your data room. A Series B lead will assign a team of analysts for six weeks. But the three questions never change.

This guide is about the process — not the documents. For the specific files investors request at each stage, see our startup data room checklist. For how to build the room itself, see how to set up a data room.

The Founder's Perspective: Preparing for Due Diligence

Start 60 to 90 Days Before You Fundraise

The biggest mistake I see in Peony data rooms is founders who start DD preparation the week after a term sheet arrives. By then, you are already behind — scrambling to find documents while trying to run a company while your lawyer bills hourly.

One founder I worked with thought due diligence was "send them the deck and answer some questions." When the lead VC's counsel sent a 200-item document request three days after the term sheet, he went silent for a week. The VC almost pulled the deal.

What to do 60 to 90 days before raising:

- Clean the cap table. Every SAFE, note, option grant, and advisor share should be documented and reconciled. An investor once told me the number one red flag is an incomplete cap table — it signals the founder is not tracking equity carefully.

- Ensure IP assignments are signed. Every founder, employee, and contractor who touched the codebase needs a signed IP assignment. In one Series A I observed through Peony, an unsigned IP assignment from an early contractor took 5 weeks to resolve because the contractor had left the country.

- Reconcile your books. Your monthly P&L should tie to your bank statements. If you have been using a spreadsheet instead of accounting software, now is the time to fix that.

- Update your corporate minute book. Board consents for equity issuances, pivots, and major contracts should be documented. Investors check.

- Organize everything in a data room. Upload documents to a Peony data room — AI auto-indexing sorts files into standard DD categories in under 5 minutes. Enable NDA gates and password protection before sharing with anyone.

What Surprises Founders During DD

In my experience hosting hundreds of DD processes, these are the moments that catch founders off guard:

The volume of requests. Seed DD might involve 30 to 50 documents. Series A can hit 150 to 200. Series B and beyond can exceed 300. The jump from "show us your deck" to "we need three years of monthly P&Ls, every material contract, and an org chart with compensation bands" is jarring if you are not ready.

The timeline pressure. DD happens while you are still running the company. You cannot disappear for six weeks to assemble documents. The founders who survive DD with their sanity intact are the ones who prepared ahead and have a data room that is already 80% populated before the term sheet.

The personal questions. Investors will ask about founder vesting, personal guarantees, prior startup failures, and any legal issues. This is normal. They are not interrogating you — they are checking for surprises that could surface after they wire money.

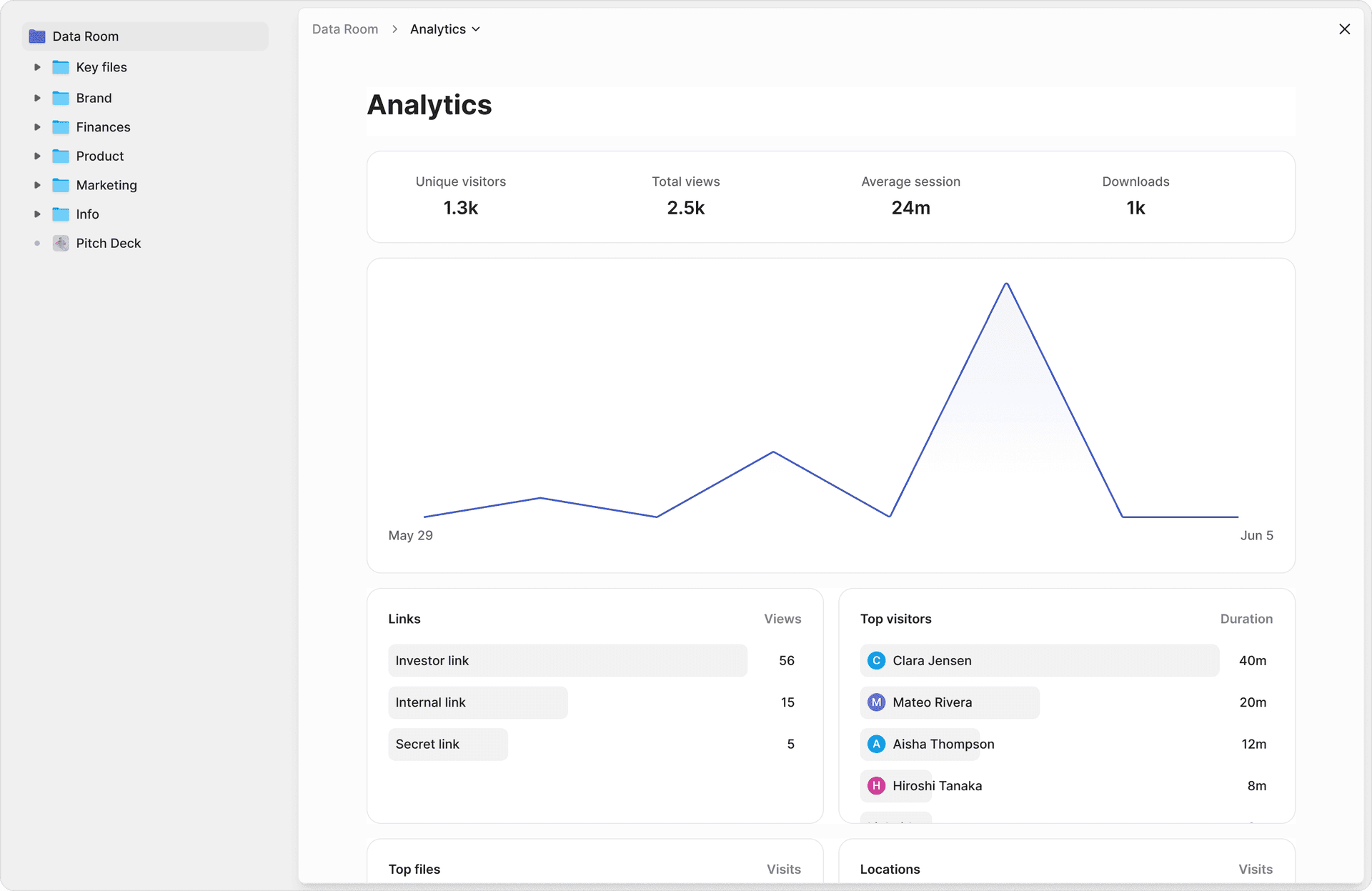

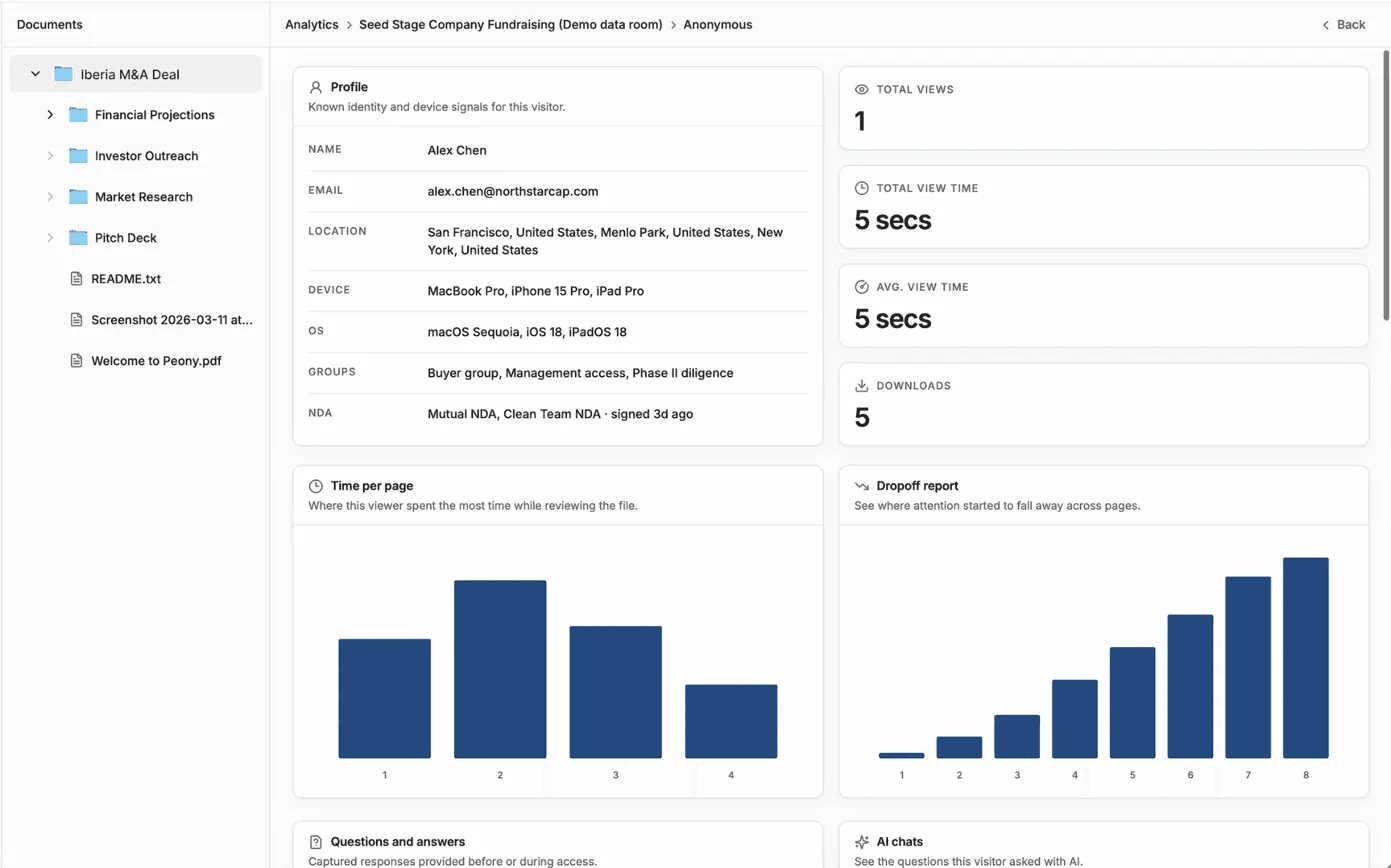

The silence. Investors go quiet for days during DD. It does not mean they are losing interest — it usually means the legal team is reviewing documents. But the silence is unnerving. Page-level analytics in Peony solve this: you can see that the investor's counsel spent 45 minutes in the legal folder yesterday even though nobody replied to your email.

Managing the Process Without Burning Out

DD is a project. Treat it like one.

- Assign internal owners. Finance handles financial requests. Your lawyer handles legal. Your CTO handles technical. Do not let every request land on the founder's desk.

- Use a Q&A workflow, not email threads. Questions and answers should live in one place with timestamps and audit trails. Peony's smart Q&A lets counterparties submit questions, AI drafts initial answers from your uploaded documents, your team reviews and edits, and approved responses go out — all with a complete record.

- Set expectations on response time. Tell the investor's team upfront: "We respond to DD requests within 48 hours. For items requiring legal review, 5 business days." Then stick to it.

- Flag issues proactively. If something is missing or imperfect, say so before they find it. "We have not yet completed our 409A valuation — here is the engagement letter with the provider, expected completion in 3 weeks." This builds trust. Hiding problems destroys it.

The Investor's Perspective: What They Are Really Looking For

I have talked to dozens of VCs and angel investors about what they actually prioritize during DD. The answer is simpler than most founders expect.

They Are Not Looking for Perfection

No seed-stage company has perfect books, a complete IP portfolio, and a spotless corporate record. Investors know this. What they are looking for is:

- Honesty about what is imperfect. Proactive disclosure of gaps builds trust. Discovering undisclosed issues destroys it.

- Evidence of organized thinking. A clean data room, consistent file naming, and prompt responses signal that the founder runs a tight operation. A messy Google Drive folder with 200 unsorted files signals the opposite.

- No deal-breakers. The handful of issues that actually kill deals — see red flags below.

The Red Flags That Kill Deals

Based on patterns I have seen across hundreds of DD processes in Peony data rooms:

| Red Flag | Why It Kills Deals | How Common |

|---|---|---|

| Unsigned IP assignments from founders or contractors | Investor cannot confirm the company owns its core asset | Very common at seed |

| Cap table inconsistencies (SAFEs, notes, options do not reconcile) | Signals founder is not tracking equity — a governance failure | Common |

| Financials that contradict the pitch deck | If MRR in the deck is $80K but the books show $55K, trust evaporates | More common than you think |

| Undisclosed related-party transactions | Paying a founder's spouse as a contractor without disclosure | Occasional, always serious |

| Customer concentration above 30% from one account | Revenue risk — if that customer churns, the business is in trouble | Common in early-stage B2B |

| Missing board consents for equity issuances | Suggests the board is either not meeting or not documenting decisions | Common at seed |

| Active or threatened litigation not disclosed | Legal risk the investor did not price into the valuation | Rare but deal-ending |

What Investors Check First

When an investor opens a data room, here is the typical reading order I see in Peony analytics — and with AI document extraction, they can ask natural-language questions across every file instead of hunting folder by folder:

- Cap table — Who owns what? Are there any surprises?

- Monthly financials — Does the revenue match the deck? What is the burn?

- Material contracts — Customer agreements, partnership deals, anything generating revenue

- IP and technology — Does the company actually own its product?

- Employment and founder agreements — Vesting, non-competes, key person risk

In one Series A process I watched unfold in Peony, analytics showed that 3 of 8 VCs read past the financials into the customer contracts and IP section. Those 3 became the term sheet offers. The other 5 never made it past the cap table and financials — a clear signal they had already decided to pass.

The Seven Areas of Startup Due Diligence

Every DD process, regardless of stage, covers the same seven areas. The depth increases as the round size grows. For the specific documents within each area, see our startup data room checklist.

1. Corporate and Cap Table

What gets examined: Articles of incorporation, bylaws, shareholder agreements, cap table, board minutes, equity grants, SAFEs, convertible notes, secondary transactions.

What investors are really looking for: Clean ownership. No orphaned equity. No verbal promises that are not documented. No side letters that contradict the main agreements.

Common findings: Missing board consents for option grants. SAFEs with conflicting terms from different rounds. Advisor shares that were never formally documented.

How to prepare: Export your cap table from Carta, Pulley, or your legal counsel. Ensure every equity event has a corresponding board consent. Upload everything to your Peony data room — AI auto-indexing sorts corporate documents into the right folder automatically.

2. Financial

What gets examined: Monthly P&L (12 to 24 months), balance sheet, cash flow statement, bank statements, revenue recognition methodology, burn rate, runway calculation, financial projections with assumptions.

What investors are really looking for: Consistency. Do the numbers in the data room match the pitch deck? Can the founder explain every line item? Is the projection model internally consistent?

Common findings: Revenue recognition that does not follow GAAP (pre-revenue startups counting LOIs as revenue). Burn rate that does not account for upcoming hires already committed. Projections disconnected from historical trends.

How to prepare: Reconcile your books monthly. Label estimates clearly. If you switched accounting methods, explain when and why. Your financial model should have an assumptions tab that an investor can modify.

3. Legal

What gets examined: Material contracts (customers, vendors, partners), IP assignments, employment agreements, NDAs, litigation history, regulatory filings, insurance policies.

What investors are really looking for: No pending lawsuits. No contracts with change-of-control provisions that would let customers walk after the round. Clean IP chain of title.

Common findings: Customer contracts with auto-renewal and 90-day termination clauses the founder forgot about. Missing IP assignments from early contractors. Expired D&O insurance.

How to prepare: Have your lawyer run a contract audit. Flag any change-of-control provisions. Ensure every person who contributed to the product has signed an IP assignment. Store sensitive legal documents in a Peony data room with dynamic watermarks and screenshot protection so confidential terms cannot be captured and shared.

4. Team and HR

What gets examined: Org chart, employment agreements, founder vesting schedules, key person dependencies, compensation bands, benefits, contractor classifications, workplace policies.

What investors are really looking for: Founder vesting that protects the company. No key-person risk where one departure kills the product. Contractor classification that passes IRS scrutiny.

Common findings: Founders with fully vested equity (investors will ask for re-vesting). Key engineers classified as contractors without proper agreements. No documentation of equity conversations with early employees.

How to prepare: Build a clean org chart. Verify that every employee and contractor has a signed agreement. Document compensation philosophy, even if it is simple.

5. Product and Technology

What gets examined: System architecture, tech stack, deployment pipeline, uptime history, security posture, technical debt assessment, AI model governance (if applicable), third-party dependencies, open-source licenses.

What investors are really looking for: Can this product scale without a rewrite? Is the security posture appropriate for the data being handled? Are there vendor lock-in risks?

Common findings: No staging environment. Secrets stored in code repositories. Open-source licenses that conflict with commercial use. AI features using customer data without clear consent flows.

How to prepare: Write a one-page architecture overview. Document your deployment process. Run a basic security audit. If you use AI, document model sources, training data provenance, and customer data flows. Share technical documentation through a Peony data room with screenshot protection — architecture diagrams and security docs should never be freely capturable.

6. Market and Competition

What gets examined: Total addressable market analysis, competitive landscape, market positioning, differentiation, win/loss analysis, pricing strategy.

What investors are really looking for: Does this team have a realistic view of the market? Is the TAM calculation bottom-up (credible) or top-down (aspirational hand-waving)? What is the actual competitive moat?

Common findings: TAM calculated as "X% of a $50B market" with no bottoms-up justification. Competitive analysis that omits the two strongest competitors. Pricing that does not match market reality.

How to prepare: Build a bottoms-up TAM model. Be honest about competitors — investors already know who they are. Document 5 to 10 recent win/loss stories with specifics.

7. Customers and Revenue

What gets examined: Customer list with ARR/MRR breakdown, logo and revenue churn, customer concentration, expansion revenue, pipeline, NPS or satisfaction data, case studies.

What investors are really looking for: Revenue quality. Is growth coming from new logos or expansion? Is churn manageable? Is there a customer who represents more than 25 to 30% of revenue (concentration risk)?

Common findings: Churn metrics that do not distinguish between logo churn and revenue churn. Revenue "growth" driven by a single large contract. Pipeline with no probability weighting.

How to prepare: Build a customer cohort analysis. Calculate net revenue retention. If you have concentration risk, acknowledge it and show the pipeline that will dilute it. Share customer data in a Peony data room with per-document permissions — not every investor needs to see individual customer names at the preliminary stage.

How DD Depth Changes by Stage

The same seven areas apply at every stage, but the depth and formality scale dramatically. This is the pattern I have observed across hundreds of processes in Peony:

| Dimension | Seed | Series A | Series B and Later |

|---|---|---|---|

| Typical timeline | 1–3 weeks | 4–8 weeks | 6–12 weeks |

| Document volume | 30–50 items | 150–200 items | 300+ items |

| Who conducts DD | Lead investor (partner level) | Associate team + legal counsel | Full deal team + external advisors |

| Financial depth | Monthly P&L, burn rate, projections | Audited financials, cohort analysis, unit economics | Multi-year audits, revenue recognition review, working capital analysis |

| Legal depth | Cap table, founder agreements, IP assignments | All material contracts, full IP audit, regulatory review | Third-party legal opinions, antitrust analysis, change-of-control review |

| Technical depth | Tech stack overview, team capabilities | Architecture review, security assessment, scalability analysis | Third-party code audit, pen testing, AI governance review |

| Customer depth | Top customers, general traction metrics | Full customer list with ARR, churn analysis, concentration | Customer reference calls, contract audits, revenue quality assessment |

| Common deal-breaker | Missing IP assignments | Financial inconsistencies | Regulatory exposure, technical debt |

Key insight: At seed, DD is about founder trust. At Series A, it shifts to business validation. At Series B and beyond, it becomes a full audit. Prepare accordingly.

Platform Comparison: Running DD on Different Tools

Not every founder uses a purpose-built data room. Here is what I have seen work — and fail — across different platforms, and why it matters for your DD process.

| Feature | Peony | Google Drive | Notion | Legacy VDR (Datasite, Intralinks) |

|---|---|---|---|---|

| Setup time | Under 5 minutes (AI auto-indexing) | 20–40 hours (manual folders) | 10–20 hours (manual pages) | 1–2 weeks (onboarding calls) |

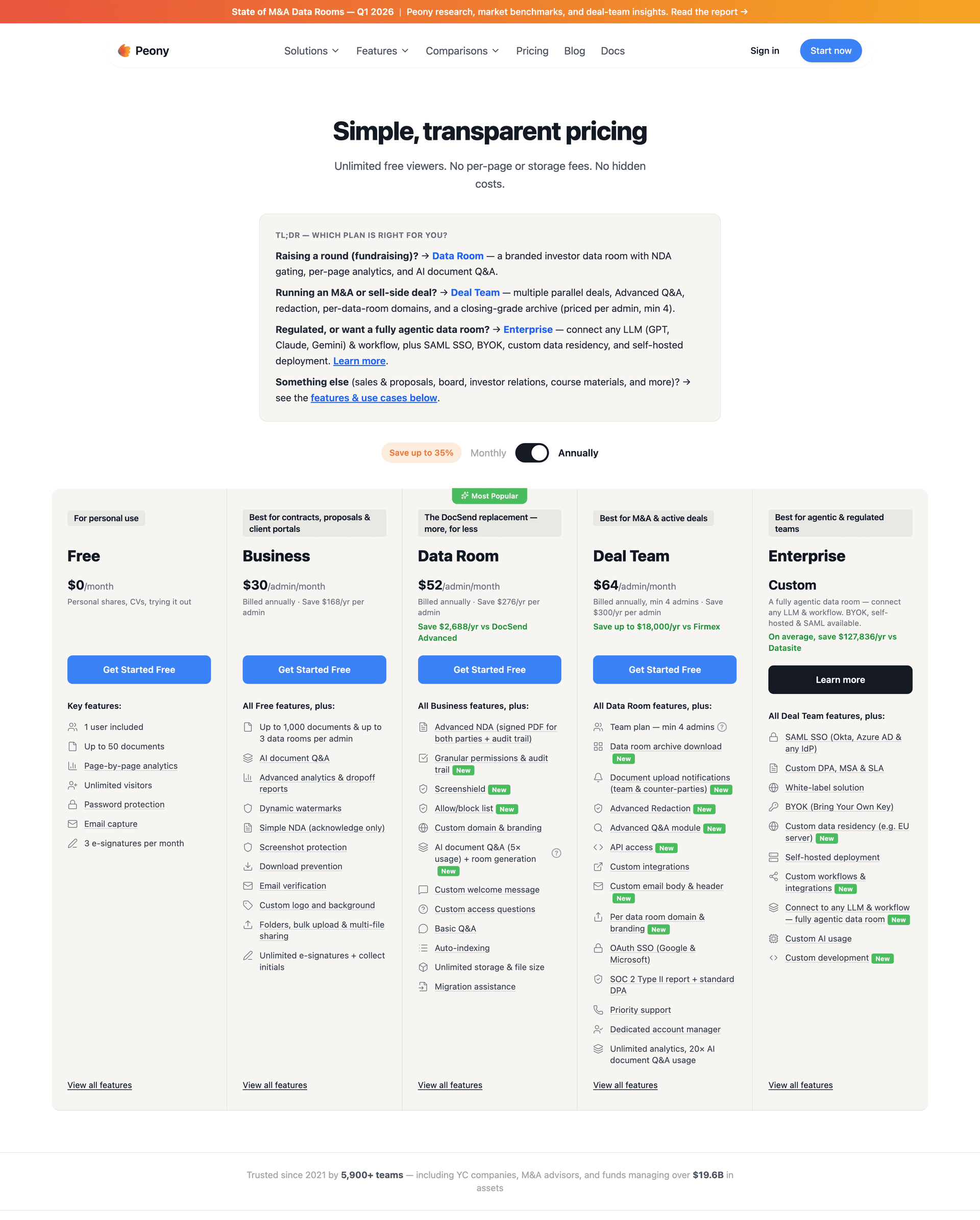

| Cost | Free tier; $52/admin/mo Data Room | Free | Free–$10/seat/mo | $500–$2,500+/mo |

| Page-level analytics | Yes — per-viewer, per-page | No | No | Basic (aggregate only) |

| Dynamic watermarks | Yes — viewer identity on every page | No | No | Yes (enterprise tier) |

| Screenshot protection | Yes — blocks and logs attempts | No | No | Varies by provider |

| NDA gates | Yes — built-in before access | No | No | Yes |

| AI auto-indexing | Yes — standard DD categories | No | No | Some providers, limited |

| Q&A workflow | Yes — AI-drafted answers, audit trail | No | Manual (comments) | Yes (manual) |

| E-signatures | Yes — built-in | No | No | Some providers |

| Mobile experience | Responsive, no plugins | Acceptable | Acceptable | Often poor (Java-based) |

| Impression on institutional VCs | Professional, signals maturity | Signals informality | Signals informality | Professional but slow |

One founder I worked with used a Google Drive folder for their Series A DD. An investor's associate spent 20 minutes trying to find the articles of incorporation buried in a subfolder called "Legal Stuff (old)." The investor flagged it in their IC memo as a sign of operational disorganization. The founder switched to Peony the next day.

A Google Drive or Notion folder might work for a pre-seed angel check. For anything with institutional investors, a purpose-built data room is not optional — it is infrastructure.

Common Mistakes (And What I Have Learned From Watching Hundreds of DD Processes)

Mistake 1: Treating DD as "Send Them the Deck"

The founder I mentioned earlier who was blindsided by a 200-item request is not unusual. Many first-time founders conflate investor meetings with due diligence. The meeting is where you pitch. DD is where they verify. These are completely different activities, and the document requirements are 10 to 50 times larger than what you shared in the pitch.

Mistake 2: Starting Preparation After the Term Sheet

By the time you have a term sheet, the clock is ticking. Most term sheets have exclusivity windows of 30 to 60 days. If you spend 3 weeks assembling documents, you have half the window left for the actual review, Q&A, and legal negotiation. Start 60 to 90 days before you plan to raise.

Mistake 3: Hiding Known Issues

Every company has issues. Missing a 409A valuation? Say so and share the engagement letter. Have a contractor IP assignment gap? Disclose it, explain the plan, and show that you have already engaged counsel. Investors expect imperfection at the startup stage. They do not tolerate concealment.

Mistake 4: Using the Wrong Tools

I have seen founders email cap tables as unprotected Excel files, share Google Drive folders with "anyone with the link" permissions, and send financials through Slack DMs. Each of these is a security failure and an organizational signal. Use a data room with dynamic watermarks, NDA gates, and access controls.

Mistake 5: Ignoring Engagement Signals

If 8 investors are in your data room and only 3 are reading past the cap table, that tells you something. Those 3 are your most serious prospects. Focus your energy on them. Without page-level analytics, you are flying blind — treating all 8 investors equally when the signal is already there.

Mistake 6: No Internal Ownership Structure

DD requests come in waves. If every question lands on the founder's desk, you will drown. Assign owners: CFO or finance lead handles financial requests, lawyer handles legal, CTO handles technical, head of sales handles customer data. Use Peony's smart Q&A to route questions to the right internal owner automatically.

Honest Limitations of Peony for DD

I recommend Peony because I built it and I believe it is the best option for startup due diligence. The one caveat: if your acquirer's counsel picks tools based on brand legacy rather than speed and capability, Peony may not be the right fit — and that is fine. For founders who care about how fast their data room is live, how much visibility they get into investor engagement, and how much they are paying — it is the best tool available.

The Bottom Line

Startup due diligence is not a surprise audit — it is a structured process that follows predictable patterns. The founders who survive it with their valuation and sanity intact are the ones who prepare early, organize methodically, disclose proactively, and use tools that give them visibility into how investors are engaging with their materials.

From the investor side, DD is about risk identification and trust calibration. A clean data room with prompt responses does more for investor confidence than a polished pitch deck ever will.

Whether you are a founder preparing for your first seed raise or a Series B veteran running your third DD process, the principles are the same: be organized, be honest, be responsive, and use infrastructure that matches the stakes.

Peony gives you AI auto-indexing that sets up your DD room in under 5 minutes, page-level analytics that show which investors are genuinely engaged, AI-powered Q&A that helps you respond to questions faster, and enterprise security (watermarks, screenshot protection, NDA gates, e-signatures) that protects your most sensitive information — all starting free at peony.ink/pricing.

Frequently Asked Questions

What is startup due diligence?

Startup due diligence is the structured investigation an investor conducts before wiring capital — verifying a company's financials, legal standing, technology, team, market position, and cap table. The process protects the investor from hidden risk and gives the founder a chance to demonstrate operational maturity. Peony's page-level analytics show founders exactly which DD documents each investor spends time on, so they can prioritize follow-ups with the most engaged parties instead of guessing.

How long does startup due diligence take at each stage?

Seed due diligence typically runs 1 to 3 weeks, Series A takes 4 to 8 weeks, and Series B or later can take 6 to 12 weeks as the scope expands to include detailed customer data, technology audits, and regulatory review. The biggest time drain is document requests — founders who have a Peony data room ready before the first investor meeting cut 2 to 4 weeks off the process because AI auto-indexing organizes everything into standard DD folders in under 5 minutes.

How do document requests change between seed and Series A due diligence?

Seed investors typically request 30 to 50 items focused on corporate formation, cap table, financial model, and IP assignments — they are checking for deal-breakers, not conducting a full audit. Series A due diligence expands to 150 to 200 items covering 24 months of detailed financials, all material contracts, employee agreements, a full IP portfolio audit, and technical architecture documentation. The jump in volume catches most founders off guard — it is the difference between a weekend review and a 6-week process. Peony's AI auto-indexing handles both scales, sorting documents into the standard folder structure whether you upload 40 files or 400.

What are the biggest red flags investors find during due diligence?

The top red flags are unsigned IP assignment agreements from founders or contractors, inconsistencies between the pitch deck financials and the actual books, missing board consents for major decisions, high customer concentration above 30 percent from a single account, and undisclosed related-party transactions. An investor once told me the number one deal-killer is an incomplete cap table — it signals that the founder does not track equity carefully. Peony's dynamic watermarking and screenshot protection help founders share sensitive cap table details securely during DD without worrying about leaks.

What legal and financial cleanup should founders do before due diligence?

The critical pre-DD cleanup items are reconciling your cap table so every SAFE, note, and option grant ties out, getting signed IP assignment agreements from every founder and contractor who touched the codebase, reconciling your monthly books with bank statements, updating your corporate minute book with board consents for all equity issuances, and resolving any pending or threatened disputes. This work typically takes 60 to 90 days and should start well before your first investor meeting. Peony's AI auto-indexing flags missing document categories when you upload, helping you spot gaps in your corporate records before investors do.

What is the difference between founder-side and investor-side due diligence?

Founder-side DD focuses on preparation and presentation — organizing documents, resolving known issues proactively, and managing the process without disrupting daily operations. Investor-side DD is about verification and risk assessment — confirming claims, stress-testing financials, and identifying deal-breakers. Peony serves both sides: founders use AI auto-indexing and page-level analytics to manage the process, while investors use the smart Q&A workflow to submit questions and receive structured answers with a full audit trail.

Can I use Google Drive or Notion for startup due diligence?

You can, but institutional investors notice. Google Drive and Notion lack dynamic watermarking, screenshot protection, NDA gates, page-level analytics, and per-document permissions — features that signal operational maturity. One founder I worked with lost three weeks because an investor could not find the articles of incorporation in a messy Google Drive folder with 200 files. Peony provides all of these VDR security features starting free, with AI auto-indexing that eliminates the folder-chaos problem entirely.

How do investors evaluate a startup's technology during due diligence?

Technical DD covers architecture documentation, codebase quality, deployment processes, security posture, uptime history, dependency risk, and AI model governance if applicable. Investors want to see that the product can scale without a rewrite. The depth increases at each stage — seed investors skim the tech stack, Series A investors review architecture, and Series B investors may run third-party code audits. Store sensitive technical documentation in a Peony data room with screenshot protection and dynamic watermarks so architecture diagrams cannot be captured and shared externally.

What happens if due diligence uncovers a problem?

It depends on severity. Minor issues like a missing 409A valuation or an expired NDA usually get resolved with a remediation plan and do not kill the deal. Major issues like undisclosed litigation, fraudulent financials, or contested IP ownership are deal-breakers. Middle-ground problems like unsigned contractor IP assignments typically cause delays of 3 to 6 weeks while lawyers draft retroactive agreements. Peony's audit trail logs every document view and download during DD, so both sides have a clear record of what was disclosed and when.

What does investor behavior in the data room reveal about their intent?

Investors who spend 20 or more minutes across multiple sessions, repeatedly return to the cap table and financial model, and share access with colleagues from their firm are advancing toward a decision. Investors who open the link once, skim the pitch deck, and never return have likely passed. In one Series A process I observed through Peony, 3 of 8 VCs read past the financials into customer contracts and IP — those 3 submitted term sheets. Peony's page-level analytics surface these behavioral patterns automatically, so founders can focus energy on investors showing genuine buying signals instead of chasing the ones who have already moved on.

Related Resources

- Startup Data Room Checklist — the specific documents you need for each DD category

- Best Data Rooms for Startups — platform comparison for fundraising and DD

- Seed Funding Guide — end-to-end guide to raising your seed round

- How to Send Your Pitch Deck to Investors — secure sharing before DD begins

- Data Room for Investors — what VCs actually want from your data room

- How to Set Up a Data Room — step-by-step setup instructions

- Small Business Due Diligence (2026): SBA 10% Rule + 5-Axis Grid — distinct topic: profitable Main Street businesses (SBA / search-fund), NOT pre-product VC-backed startups

- Cybersecurity Due Diligence (2026): The Bain Test + 5-Axis Breach Matrix — for SaaS-startup cyber posture

- Sell-Side Due Diligence (2026): VDD Scope Matrix — for founders preparing acquisition exits

- Due Diligence Data Room Checklist — the full 174-document M&A checklist

- M&A Due Diligence Process (The 6-Phase Playbook) — enterprise M&A DD end-to-end

- Peony for Startups — how Peony is built for startup fundraising

- Peony for Due Diligence — enterprise DD workflows