Startup Fundraising Rounds Explained (Seed to Series C) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Startup Fundraising Rounds Explained (Seed to Series C) in 2026

Last updated: March 2026

I've watched hundreds of fundraising rounds close through Peony data rooms — from $300K pre-seed checks to $80M Series C raises. The pattern that surprises most first-time founders: the round label matters far less than the milestones behind it. A "seed" round in 2026 might be $1.5M or $5M depending on the sector. What stays constant is the underlying logic: each round converts a new set of risks into knowable facts, and the bar for proof escalates with each stage.

This guide breaks down what actually happens at each round — the terms, dilution math, check sizes, timelines, investor expectations, and how your data room requirements evolve from a 10-document folder to a 200-document war room.

TL;DR: Pre-seed rounds average $500K to $2M on SAFEs. Seed medians hit $3.1M in 2025 with 15-25% dilution. Series A medians sit near $10M at a $48M pre-money. Series B deals average $30M. Series C reaches $50M or more. Fewer than 30% of seeded startups reach Series A (the "Series A crunch"). The founders who close fastest have their materials organized before the first meeting. Peony (free tier available) lets you set up a data room in under 5 minutes, track investor engagement with page-level analytics, and scale from seed to Series C without switching platforms.

What Are Fundraising Rounds?

Fundraising rounds are staged capital raises where startups sell equity (or equity-like instruments) to investors in exchange for cash to grow the business. Each round has a label — pre-seed, seed, Series A, B, C — that roughly corresponds to the company's maturity and risk profile.

The labels are conventions, not legal categories. There is no regulator defining when a company is "Series A ready." But venture investors, founders, and lawyers have converged on expectations for each stage: what instruments you use, how much dilution is normal, what milestones you should have hit, and what documents investors will request in due diligence.

Understanding these expectations is the difference between running a clean process and scrambling to meet investor requests mid-round.

By the Numbers

- $3.1 million — median US seed round in 2025, up from $2.1M in 2020 (Carta State of Startup Funding)

- $48 million — median Series A pre-money valuation in Q1–Q2 2025 (Carta Series A data)

- $30 million — median US Series B deal size in 2024-2025 (KPMG Venture Pulse Q1 2025)

- $50 million+ — median US Series C deal size, with later rounds reaching $100M (KPMG Venture Pulse)

- Fewer than 30% of seed-funded startups go on to raise Series A (Crunchbase Funding Report)

- 70%+ of US pre-seed and seed deals close on SAFEs (Y Combinator SAFE data)

- 18–24 months — average gap between seed and Series A, up from 12–15 months in 2021 (Axios venture capital analysis)

- 2.5–3 years — median gap between Series A and Series B in 2025, requiring longer runways (PitchBook NVCA Venture Monitor)

- 15–25% — typical founder dilution per round at seed and Series A

- 68% of data breaches involve a human element — unsecured document sharing is exactly the kind of mistake that causes them (Verizon 2024 DBIR)

The Instruments: SAFEs, Notes, and Priced Rounds

Before diving into each round, here is a quick primer on the three instruments you will encounter.

SAFE (Simple Agreement for Future Equity): An investor gives you money now in exchange for equity later — typically at your next priced round. No interest, no maturity date. Post-money SAFEs (the Y Combinator standard) make dilution calculable from day one. SAFEs dominate pre-seed and seed.

Convertible note: Debt that converts to equity in a future round. Comes with interest (usually 4-8%), a maturity date (12-24 months), and a conversion discount or valuation cap. Still used for bridge rounds and when investors prefer debt structure.

Priced equity round: Investors purchase preferred stock at a negotiated valuation. Comes with formal governance: board seats, liquidation preferences, anti-dilution protections, and protective provisions. Standard from Series A onward.

| Feature | SAFE | Convertible Note | Priced Round |

|---|---|---|---|

| Legal cost | $0–$2K | $5–$15K | $25–$50K+ |

| Dilution timing | Deferred | Deferred | Immediate |

| Interest | None | 4–8% | N/A |

| Maturity date | None | 12–24 months | N/A |

| Board seat | Rare | Rare | Standard |

| When used | Pre-seed, seed | Bridges, some seeds | Series A onward |

Pre-Seed: From Idea to First Proof

Purpose: Show the problem is real, the wedge is sharp, and users will try it.

Typical raise: $250K to $2M, with most rounds under $1M.

Valuation: SAFEs with caps between $5M and $10M. Carta reports a $7.5M median cap for sub-$250K pre-seed checks in 2025.

Instrument: SAFE in roughly 90% of cases. Some angels still use convertible notes.

Dilution: 10-15% is typical, though with uncapped SAFEs (rare in 2026) dilution is unknown until conversion.

Timeline: 1-3 months to close. Pre-seed investors often make decisions in 1-2 meetings.

What investors expect to see:

- A working prototype or MVP — not just slides

- 10-30 direct user conversations or early pilots

- A clear 90-day plan with a binary success criterion ("We will have X paying users by Y date")

- A 12-18 month budget that maps to the ask

- Founder-market fit: why this team for this problem

Data room requirements: Minimal. A pitch deck, financial model, founder bios, and incorporation documents. Most founders share these via email at this stage — but even a basic Peony data room gives you analytics on which investors actually read your deck versus those who just opened the link.

Common pitfall: Counting sign-ups as traction. Ten thousand sign-ups with 2% activation means 200 real users. Investors have seen this pattern enough to discount vanity metrics entirely.

Seed: From Promise to Repeatable Traction

Purpose: Prove users stay and there is a repeatable path to revenue or durable engagement.

Seed is where most founders encounter their first real fundraising process — multiple investor meetings, due diligence requests, and negotiation on terms. The median US seed round hit $3.1M in 2025, and competition for quality deals is intense.

I have covered the seed stage in depth — SAFEs versus notes, finding angels, data room setup, and closing mechanics — in our seed funding guide. Here is the summary relevant to understanding how seed fits in the overall funding ladder.

Typical raise: $1.5M to $5M, with $3M as the median.

Valuation: $12M to $20M pre-money, with $14.8-16M as the 2025 median on Carta.

Dilution: 15-25%, depending on instrument and valuation cap.

Timeline: 3-6 months from first outreach to wire.

Key milestones: Retention cohorts that flatten (not decay), early renewals or expansion revenue, a clear ideal customer profile, and a repeatable top-of-funnel. For SaaS, $10K-$50K MRR with 15-20% month-over-month growth is a common benchmark.

Data room requirements: Pitch deck, cap table, financial model with 24-month projections, SAFE or term sheet template, articles of incorporation, founder agreements, IP assignments, key customer contracts, and a product metrics dashboard.

For the full breakdown — including SAFE mechanics, valuation negotiation, and a complete seed data room checklist — see our seed funding guide.

Series A: From Traction to a Scalable Engine

Purpose: Demonstrate a repeatable go-to-market engine with reliable unit economics. This is the round where most institutional venture capital firms enter.

Typical raise: $5M to $20M, with a median near $10M (Carta reports approximately $7.9M in Q1 2025, though this varies by sector).

Valuation: $30M to $70M pre-money, with a median near $48M in Q1-Q2 2025.

Instrument: Priced equity round with preferred stock. This is where term sheets get detailed — liquidation preferences, anti-dilution protections, board seats, and protective provisions all come into play.

Dilution: 15-25%. A $10M raise at a $40M pre-money valuation means 20% dilution.

Timeline: 4-8 months. Series A diligence is significantly more thorough than seed — expect 3-6 weeks of diligence after a term sheet.

What investors expect to see:

- Revenue: $1M to $3M ARR is common for SaaS (not a hard rule, but a frequent benchmark operators cite — SaaStr)

- Retention: Cohorts that settle high, early net revenue retention signal above 100%

- Efficiency: Improving payback period, clear contribution margin after variable costs, and first sales productivity metrics (ramp curves, win rates)

- Pipeline quality: Stage-to-stage conversion that matches the forecast, with 3-4x qualified coverage on near-term targets

- Team: First key hires beyond founders — head of sales, head of engineering, early customer success

Data room requirements: Everything from seed plus: audited or reviewed financials, detailed customer metrics (cohort analyses, churn breakdowns), organizational chart, sales pipeline data, legal summary of all material contracts, employee agreements and equity incentive plan, insurance policies, and any regulatory filings. Expect 30-60 documents across 8-12 folders.

At this stage, a disorganized Google Drive folder signals to investors that your operations are sloppy. A structured Peony data room with auto-indexing and granular access permissions tells a different story. Prepare with our startup data room checklist and VC data room checklist.

Common pitfall: Top-line growth while efficiency deteriorates. Investors in 2026 care about growth and improving unit economics — not one or the other.

The Series A crunch: Fewer than 30% of seed-funded startups successfully raise a Series A. The gap between seed and Series A has stretched to 18-24 months. Many startups run bridge rounds to reach A-level proof. Plan your seed runway accordingly — budget for 18 months minimum, not 12.

Series B: From Engine to Repeatable Scale

Purpose: Prove the system scales — people, process, and product — without breaking economics.

Typical raise: $20M to $50M, with a US median around $30M.

Valuation: $80M to $200M pre-money for most sectors. AI companies skew higher — Carta reports a $143M median pre-money for AI Series B rounds in 2024.

Instrument: Priced equity round. Term sheet complexity increases with additional investor rights, information rights, and sometimes pay-to-play provisions.

Dilution: 10-20%. Larger rounds at higher valuations mean percentage dilution often decreases even as dollar amounts increase.

Timeline: 3-6 months once the process starts, but many Series B companies spend 6-12 months preparing before launching the raise. The A-to-B gap now stretches to 2.5-3 years in many cases.

What investors expect to see:

- Management depth: VP/Director layer with hiring and enablement plans — not just founders doing everything

- Multi-channel GTM: ROI by segment and channel, with disciplined pruning where returns decay

- Operational rigor: Forecast accuracy within 10-15%, stable release cadence, customer success SLAs being met

- Financial maturity: A credible multi-year model with scenarios and a believable path to profitability at scale

- Market expansion: Evidence that the core product can extend into adjacent segments or geographies

Data room requirements: Everything from Series A plus: multi-year financial projections with scenario analyses, detailed organizational chart with hiring plan, customer concentration analysis, competitive landscape documentation, IP portfolio summary, compliance certifications (SOC 2, ISO 27001 if applicable), board meeting minutes, and cap table with full waterfall analysis. Expect 80-150 documents.

Common pitfall: Expanding product lines before core retention is durable. Investors want to see that your existing customers are not churning before you chase new markets.

Series C and Beyond: Toward Category Leadership

Purpose: Demonstrate durable market leadership, efficient deployment of large capital, and governance readiness for an eventual exit.

Typical raise: $50M or more at Series C, with later rounds (D, E) reaching $100M+.

Valuation: High-hundreds-of-millions to $1B+ pre-money. Wide dispersion by sector — AI and fintech command premiums.

Instrument: Priced equity round, sometimes with structured terms (participating preferred, ratchets, IPO-contingent provisions) as valuations get large and downside protection becomes a negotiation point.

Dilution: 5-15%. At this stage, dilution per round is lower because valuations are high.

Timeline: 3-6 months. Diligence at this stage resembles what an acquirer or IPO underwriter would request.

What investors expect to see:

- Board-quality reporting: Consistent metric definitions, reconciled financials, and quarterly board packages

- Margin shape and operating leverage: Durable gross margin (65%+ for SaaS) and improving cash conversion

- Compliance and risk: Security and privacy governance, completed audits, regulatory readiness

- Strategic pipeline: M&A, partnerships, or international expansion with integration discipline

- Path to liquidity: A credible IPO timeline or strategic acquisition thesis

Data room requirements: The most extensive — 150 to 300 documents across 15-20 folders. Audited financials (2-3 years), tax returns, all material contracts, regulatory filings, board and committee minutes, detailed IP portfolio, employee roster and equity grants, insurance coverage summary, customer and revenue detail, and any M&A integration materials. Multiple parties (lead investor, co-investors, legal counsel, accounting firms) need different permission levels on different documents.

For companies at this stage, a Peony data room with NDA gates, dynamic watermarks, and screenshot protection ensures that even with 20+ parties in the room, every document view is tracked and attributed. Built-in e-signatures with AI field detection let you close without switching to a separate signing tool.

Common pitfall: Using M&A to mask organic softness. Separate organic versus inorganic performance clearly — investors at this stage will demand it.

Comparison: Fundraising Rounds Side by Side

| Pre-Seed | Seed | Series A | Series B | Series C+ | |

|---|---|---|---|---|---|

| Typical raise | $250K–$2M | $1.5M–$5M | $5M–$20M | $20M–$50M | $50M+ |

| Median valuation | $5M–$10M cap | $12M–$20M | $30M–$70M | $80M–$200M | $500M–$1B+ |

| Dilution | 10–15% | 15–25% | 15–25% | 10–20% | 5–15% |

| Instrument | SAFE | SAFE or priced | Priced equity | Priced equity | Priced equity |

| Timeline to close | 1–3 months | 3–6 months | 4–8 months | 3–6 months | 3–6 months |

| Investors | Angels, pre-seed funds | Seed VCs, syndicates | Institutional VCs | Growth VCs | Late-stage, crossover |

| Key milestone | Prototype + user validation | Product-market fit signals | Scalable GTM + $1-3M ARR | Multi-channel scale | Category leadership |

| Data room docs | 5–10 | 10–20 | 30–60 | 80–150 | 150–300 |

| Board seat | None | Rare | Standard (1) | Standard (1–2) | Standard (2+) |

How Data Room Requirements Evolve

One of the clearest patterns I see through Peony: the complexity of your data room roughly doubles with each fundraising round. Here is what that looks like in practice.

Pre-Seed: The Basics

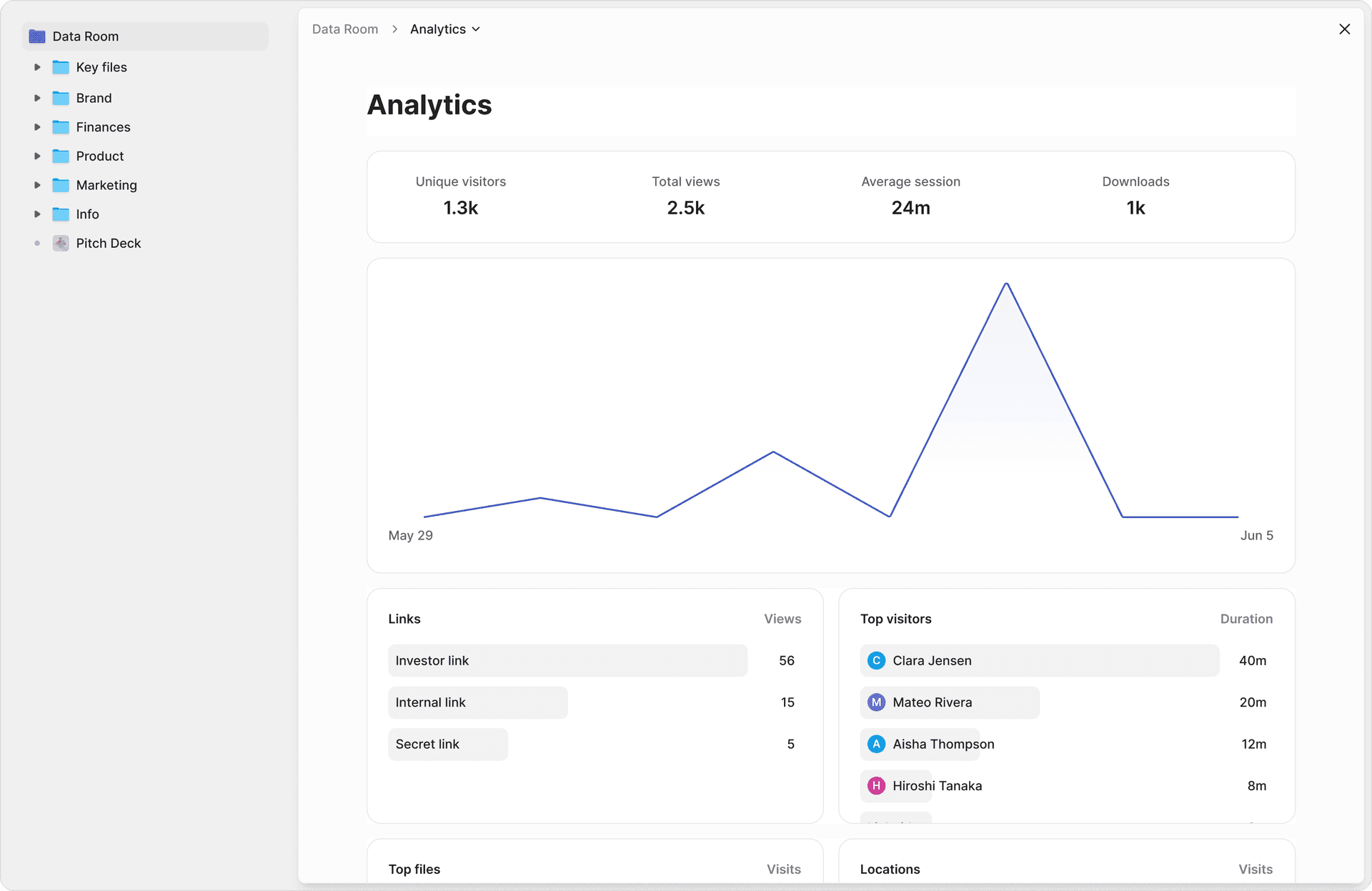

Five to ten documents. Pitch deck, financial model, founder LinkedIn profiles or bios, articles of incorporation, and maybe an early product demo video. Most founders share these as email attachments or a Google Drive link. Even at this stage, a Peony data room gives you an edge — you can see exactly which slides each angel investor spent time on through page-level analytics, and that tells you what resonates before the follow-up call.

Seed: The First Real Room

Ten to twenty documents shared with five to ten investors. You need a cap table, SAFE templates, IP assignments, customer contracts, and product metrics alongside your deck and model. This is where disorganized sharing starts costing you — if an investor asks for your cap table and you take two days to find the latest version, that is a signal. Peony's AI auto-indexing sorts uploaded documents into standard folders in under 3 minutes.

Series A: Institutional Standards

Thirty to sixty documents shared with ten to fifteen firms. Audited financials, cohort analyses, pipeline data, org charts, legal summaries — the bar is institutional. Investors expect a structured index, not a flat file dump. Granular permissions matter here: your lead investor might get full access while other firms only see the pitch deck and summary financials until they sign a term sheet.

Series B: Multi-Stakeholder Complexity

Eighty to one hundred fifty documents. Multiple workstreams happening in parallel — financial diligence, legal diligence, commercial diligence, and technical diligence, each with different teams needing different documents. NDA gates before access become essential. The Smart Q&A workflow — where counterparties submit questions, AI drafts answers, and your team reviews before sending — saves dozens of hours compared to managing questions over email.

Series C+: IPO-Grade Documentation

One hundred fifty to three hundred documents with twenty or more parties. At this level, you need an audit trail that would satisfy a regulator. Every view, download, and print must be logged and attributable. Dynamic watermarks with viewer identity baked into every rendered frame prevent leaks. Screenshot protection blocks and logs capture attempts. This is the level of control that Peony's security stack was built for.

Term Sheet Concepts to Understand Before You Sign

Starting at Series A, you will negotiate term sheets with concepts that directly affect your economics as a founder. Here are the ones that matter most.

Liquidation preference (1x non-participating vs. participating): Determines who gets paid first if the company is sold. The venture standard is 1x non-participating preferred — investors get their money back or convert to common (whichever is higher). Participating preferred means investors get their money back AND their pro rata share of what remains. The difference can be millions in a moderate exit.

Anti-dilution protection: Adjusts investor share price if a future round happens at a lower valuation (a "down round"). Weighted-average is standard and fair. Full ratchet is harsh on founders — avoid if possible.

Pro rata rights: The right to invest in future rounds to maintain ownership percentage. Standard for lead investors.

Protective provisions: Actions that require investor consent — issuing new equity classes, selling the company, changing the charter, or taking on debt above a threshold.

Board composition: Who gets board seats and how many. At Series A, a common structure is 2 founders + 1 investor + 1 or 2 independents.

Run the math on every term sheet scenario — especially what happens in a moderate exit (2-3x the last round valuation), not just the home-run case. Use your Peony data room to share term sheet drafts securely with your legal counsel using manage links with expiration dates.

How Peony Supports Every Fundraising Stage

Running a successful fundraise at any stage requires more than strong metrics — you need to present materials professionally and maintain control over who sees what.

Peony is built for this. Set up a data room in under 5 minutes, and it scales with you from pre-seed to Series C without switching platforms.

- AI auto-indexing sorts your documents into standard folders in under 3 minutes — no manual organization

- Page-level analytics show which pages each investor read and for how long, so you know who is seriously engaged

- AI document extraction lets investors ask natural language questions across your entire data room and get cited answers with page numbers

- Smart Q&A manages counterparty questions: AI drafts answers, your team reviews, approved responses go out with a full audit trail

- Screenshot protection blocks and logs capture attempts on sensitive documents

- Dynamic watermarks embed viewer identity into every rendered frame

- NDA gates require signed non-disclosure before document access

- Built-in e-signatures with AI-powered field detection — close without switching to a separate tool

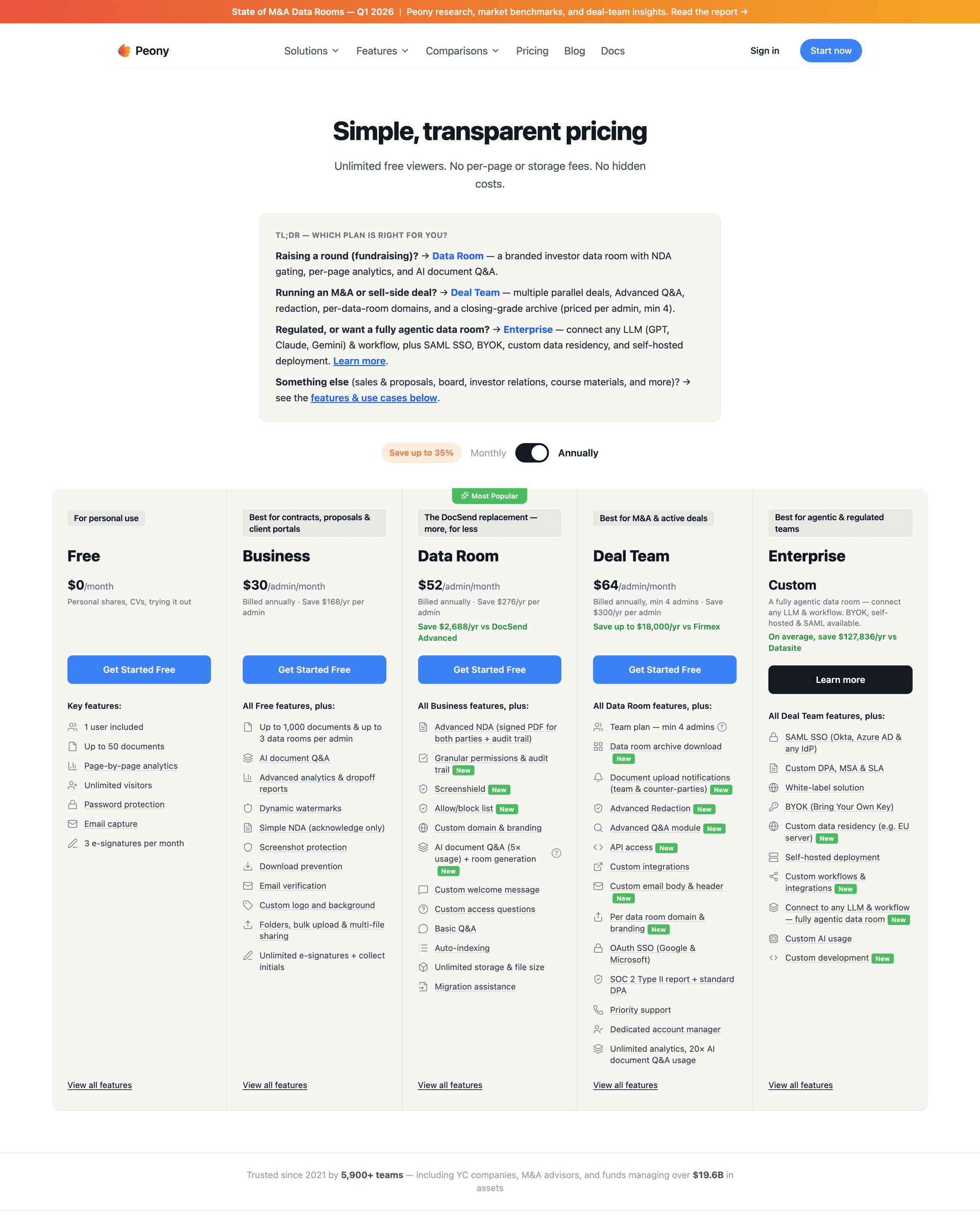

Free tier available. Business at $30/admin/month and Data Room at $52/admin/month. No enterprise sales calls required.

One honest caveat: if you are raising a Series C from a mega-fund whose LPs require a legacy vendor like Datasite or Intralinks by name, you may encounter brand preference. For everyone else — pre-seed through Series B and most Series C rounds — Peony does everything the legacy platforms do at a fraction of the cost, with a modern interface built in 2023, not 2008.

The Bottom Line

Fundraising rounds are not an obstacle course — they are milestones in risk reduction. Each round, you convert uncertainty into proof, and investors underwrite the next leap.

If you are pre-seed or seed: Focus on building proof, not perfecting your process. A SAFE, a clean data room, and a clear 90-day plan is enough. Read our seed funding guide and fundraising strategy guide for the details.

If you are approaching Series A: This is where preparation separates companies that raise from those that stall. Build your data room 3-6 months before you start outreach. Use our startup data room checklist and track pitch deck engagement to refine your materials.

If you are Series B or beyond: Your data room is now a reflection of your operational maturity. Investors will judge your company partly by how organized your diligence materials are. Invest in proper security controls and document management.

At every stage, the founders who close fastest are the ones who never make an investor wait for a document. That is what Peony is built for.

What are the typical startup fundraising rounds in order?

The typical order is pre-seed, seed, Series A, Series B, and Series C, though many startups also raise bridge rounds between stages. Pre-seed covers the idea-to-prototype phase, seed funds the path to product-market fit, Series A scales a proven go-to-market, Series B expands into new channels and markets, and Series C prepares for category leadership or IPO. At every stage, a Peony data room helps you organize and share materials in under 5 minutes with AI auto-indexing that categorizes your documents automatically.

How much dilution should founders expect per fundraising round?

Founders typically give up 10 to 15 percent at pre-seed, 15 to 25 percent at seed, 15 to 25 percent at Series A, 10 to 20 percent at Series B, and 5 to 15 percent at Series C. Cumulative dilution means a founder who raises through Series C may retain 25 to 40 percent of the company. Track your cap table in a Peony data room so every investor and advisor can access the latest version through a secure, trackable link with page-level analytics showing exactly who reviewed it.

How long does each fundraising round take to close?

Pre-seed rounds typically close in 1 to 3 months, seed rounds in 3 to 6 months, Series A in 4 to 8 months, and Series B and C rounds in 3 to 6 months once the process starts. The founders who close fastest are the ones with their Peony data room ready before the first meeting — page-level analytics show which investors are actually engaged so you can prioritize follow-ups instead of guessing.

What is the difference between a SAFE, convertible note, and priced round?

A SAFE is a simple contract where investors fund you now for equity later with no interest or maturity date. A convertible note is debt that converts to equity with interest and a maturity date. A priced round means investors buy preferred stock at a negotiated valuation with formal governance rights. SAFEs dominate pre-seed and seed, while Series A and beyond are almost always priced rounds. Store executed agreements of any type in a Peony data room with screenshot protection and dynamic watermarks so terms stay confidential.

What documents do investors expect in a data room at each fundraising stage?

Pre-seed investors expect a pitch deck, financial model, and founder bios. Seed adds a cap table, SAFE or term sheet, IP assignments, and early metrics. Series A requires audited financials, customer contracts, org chart, and detailed unit economics. Series B and C add compliance certifications, board materials, and multi-year projections. Peony's AI auto-indexing sorts all documents into the right folders in under 3 minutes, so your data room scales from a 10-document seed room to a 200-document Series C room without manual reorganization.

What milestones do investors expect before each fundraising round?

Pre-seed investors want a working prototype and early user validation. Seed investors want product-market fit signals like flattening retention cohorts. Series A investors want $1 million to $3 million in ARR with improving unit economics. Series B investors want a VP-level team and multi-channel go-to-market with proven ROI. Series C investors want board-quality reporting and a clear path to profitability. At every stage, Peony's AI document extraction lets investors ask natural language questions across your data room and get cited answers with exact page numbers, which accelerates diligence.

How do data room requirements change from seed to Series C?

Data room complexity roughly doubles with each round. A seed data room might hold 10 to 20 documents shared with 5 investors. A Series A room holds 30 to 60 documents shared with 10 to 15 firms. A Series C room can hold 150 to 300 documents with 20 or more parties needing different permission levels. Peony handles this with granular folder-level permissions, NDA gates before access, and built-in e-signatures with AI field detection — so you manage one platform from first raise to IPO prep.

What is the Series A crunch and how can startups prepare for it?

The Series A crunch refers to the fact that fewer than 30 percent of seed-funded startups successfully raise a Series A. The gap between seed and Series A has stretched to 18 to 24 months, and investors now expect $1 million to $3 million in ARR with strong retention before writing a check. Startups that prepare early by building their Peony data room during the seed stage — tracking which metrics investors engage with through page-level analytics — enter Series A fundraising with a clear picture of what resonates and what needs work.

Related Resources

- Q1 2026 Startup Fundraising Benchmarks — current deal-size, valuation, dilution, and timeline data by stage and sector

- Seed Funding for Startups Guide

- Startup Fundraising Strategy Guide

- Startup Data Room Checklist

- VC Fund Data Room Checklist

- Data Room for Investors Guide

- Startup Due Diligence Guide

- How to Send Your Pitch Deck to Investors

- How to Track Pitch Deck Engagement

- Top US Seed Investors

- Series A Data Room: From Conviction to Verification — what changes in the room at the Series A step-change

- Venture Debt Data Room — the debt instrument that sits next to these equity rounds to extend runway

- Best Data Rooms for Startups