Real Estate Due Diligence Checklist (What Buyers Miss) in 2026

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Real Estate Due Diligence Checklist: What Buyers Actually Miss in 2026

Last updated: March 2026

I run Peony, a data room company, and real estate deals generate some of the largest document sets we see. A typical commercial acquisition data room holds 300 to 2,000+ pages across title reports, environmental assessments, rent rolls, lease abstracts, insurance policies, and zoning letters. The buyers who get burned are not the ones who skip due diligence entirely -- they are the ones who check 90% of the list and miss the 10% that matters most.

In 2026, that 10% increasingly lives in two places: insurance and climate risk (premiums doubling or coverage disappearing entirely) and regulatory shifts (new energy benchmarking laws, rent stabilization expansions, and short-term rental crackdowns). The traditional "inspect the roof and check the rent roll" approach leaves real money on the table.

This is the checklist I help clients organize inside Peony's commercial real estate data room -- 7 categories, every document type, with asset-type overlays and the 2026 updates that most guides still ignore.

TL;DR: This checklist covers 7 due diligence categories with 80+ document types across legal, physical, financial, tenant, market, insurance, and regulatory workstreams. 27% of commercial RE transactions encounter unexpected title issues (ALTA). Environmental remediation costs average $200,000+ per site (EPA). Insurance premiums in high-risk zones have risen 200-400% since 2020 in parts of Florida, Louisiana, and California. Peony (free tier available) uses AI auto-indexing to organize your entire RE document set in under 3 minutes, with page-level analytics showing which sections each buyer actually reviewed.

What Is Real Estate Due Diligence?

Real estate due diligence is the systematic investigation of every material aspect of a property -- legal ownership, physical condition, financial performance, environmental health, regulatory compliance, and market position -- before you commit capital. It is the bridge between a promising listing and an informed investment decision.

The process exists because real estate transactions involve information asymmetry. Sellers know more about the asset than buyers. Due diligence closes that gap by requiring documented verification of every seller claim. When done properly, it either confirms your investment thesis and gives you confidence to close, or it surfaces deal-breaking risks that save you from a costly mistake.

For a broader overview of due diligence across all transaction types, see our complete due diligence checklist covering 174 document types. For the M&A-specific process, see our M&A due diligence process guide.

By the Numbers: Real Estate Due Diligence in 2026

| Metric | Value | Source |

|---|---|---|

| U.S. commercial RE transaction volume (2024) | $374 billion | MSCI Real Assets |

| Transactions with unexpected title issues | 27% | ALTA (American Land Title Association) |

| Average Phase I ESA cost | $2,000-$6,000 | EPA Brownfields Program |

| Average environmental remediation cost per site | $200,000+ | EPA Brownfields Program |

| Properties in FEMA Special Flood Hazard Areas | 13 million+ structures | FEMA NFIP |

| Insurance premium increases in high-risk FL zones | 200-400% since 2020 | Insurance Information Institute |

| Commercial deals that fail during DD | 15-20% | National Association of Realtors |

| Average residential DD contingency period | 14-30 days | NAR Profile of Home Buyers and Sellers |

| Commercial DD timeline (mid-market) | 45-90 days | CCIM Institute |

| Properties with at least one material defect found during inspection | 86% | ASHI (American Society of Home Inspectors) |

The ALTA statistic deserves emphasis: more than one in four commercial transactions surfaces an unexpected title issue. These are not obscure edge cases -- they include unrecorded easements, mechanics' liens, boundary discrepancies, and judgment liens that can delay closing by weeks or kill a deal entirely. A thorough title review is not optional.

Category 1: Legal and Title Due Diligence

Legal and title verification answers the most fundamental question: do you actually own what you think you are buying, free of claims and encumbrances that could limit your use or expose you to liability?

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Preliminary title report / title commitment | All exceptions, liens, encumbrances, easements, and rights of way | Unresolved title defects can prevent transfer or create post-closing liability |

| Title insurance policy (owner's and lender's) | Coverage amount, exclusions, endorsed exceptions | Your financial backstop against title claims; gaps in coverage are gaps in protection |

| ALTA/NSPS survey | Boundaries, improvements, easements, encroachments, flood zone | Confirms physical reality matches legal description; required for most commercial lenders |

| Deed and chain of title | Ownership history, proper conveyance, authority of grantors | Gaps in chain of title can void your ownership claim |

| Entity verification (corporate seller) | Articles, operating agreement, certificate of good standing, signatory authority | If the seller's entity is not in good standing or the signer lacks authority, the sale may be voidable |

| HOA/condo documents (if applicable) | CC&Rs, bylaws, meeting minutes, budgets, reserves, pending assessments | Special assessments and litigation reserves can materially affect your cost basis |

| Easement agreements | Scope, location, benefited and burdened parties, maintenance obligations | Easements can restrict development plans or require ongoing maintenance costs |

| Pending or threatened litigation | Lawsuits, disputes, code enforcement actions | Active litigation can cloud title, delay closing, or create successor liability |

| Property tax records | Current assessed value, tax rate, payment history, appeal status | Reassessment after sale can dramatically increase annual tax burden |

For commercial deals valued above $1M, always obtain a current ALTA/NSPS survey rather than relying on an older survey. Boundary discrepancies and unrecorded easements are among the most expensive surprises in real estate.

Store all title and legal documents in a secure commercial real estate data room with NDA gates so counterparties execute confidentiality agreements before accessing sensitive ownership records.

Category 2: Physical and Environmental Condition

This category answers: what shape is the asset actually in, and what liabilities might be hiding in the soil, structure, or systems?

Physical Condition

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Property condition assessment (PCA) | Structure, roof, foundation, exterior envelope, drainage | Identifies deferred maintenance and near-term CapEx needs |

| Roof assessment | Age, remaining useful life, warranty status, leak history | Roof replacement is often the single largest CapEx item ($5-$30 per sq ft for commercial) |

| HVAC, plumbing, electrical systems | Age, condition, code compliance, energy efficiency | System replacement costs can exceed $100K+ on commercial properties |

| Elevator inspection reports | Compliance, maintenance history, modernization timeline | Elevator code violations can trigger immediate shutdown orders |

| Fire and life safety systems | Sprinklers, alarms, extinguishers, emergency lighting, ADA compliance | Non-compliance creates liability exposure and can void insurance coverage |

| CapEx history and schedule | Past 5 years of capital improvements, planned future projects | Reveals whether the seller has invested adequately or deferred maintenance |

| Certificates of occupancy | Current CO for all units and common areas | Missing or outdated COs can make the property legally non-occupiable |

| As-built drawings and floor plans | Accuracy of existing plans versus actual conditions | Discrepancies signal unpermitted work that may require remediation |

Environmental

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Phase I Environmental Site Assessment | Recognized environmental conditions (RECs), historical uses, regulatory database review | Required for CERCLA liability protection (the "innocent landowner" defense) |

| Phase II ESA (if Phase I flags issues) | Soil and groundwater sampling, contamination levels vs. regulatory thresholds | Determines actual remediation scope and cost, which often exceeds $200K |

| Asbestos, lead paint, and mold surveys | Presence, condition, and management plans | Remediation requirements vary by state; disclosure obligations are strict |

| Underground storage tank records | Tank inventory, removal/closure documentation, monitoring reports | UST leaks are among the most expensive environmental liabilities |

| Wetlands delineation (if applicable) | Jurisdictional boundaries, buffer zones, mitigation requirements | Wetlands encroachment can eliminate developable acreage |

2026 update: ASTM's Property Resilience Assessment standard (E3429-24) now integrates climate resilience into environmental due diligence, layering hazard identification and resilience planning on top of traditional Phase I assessments. Ask your environmental consultant whether they incorporate this standard.

For properties with complex environmental histories, use Peony's AI document extraction to ask natural-language questions across Phase I reports, remediation records, and regulatory correspondence -- and get cited answers with exact page numbers instead of reading hundreds of pages manually.

Category 3: Financial and Operational

For income-producing property, the financials determine whether the deal actually works. This is where the pro forma meets reality.

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Rent roll (current) | Tenant names, unit numbers, lease dates, rent amounts, escalations, deposits, arrears | The single most important financial document; verify against actual leases and bank deposits |

| Trailing 12-36 month operating statements (T-12, T-36) | Gross income, vacancy, operating expenses, NOI, trends | Reveals whether income is stable, growing, or declining; watch for one-time adjustments |

| Property tax bills (3-5 years) | Current assessed value, tax rate, exemptions, appeal history | Post-sale reassessment can increase taxes 20-50%+ depending on jurisdiction |

| Utility bills (12-24 months) | Water, electric, gas, waste, common area charges | Verify against seller representations; unusually low bills may signal deferred maintenance |

| Service contracts | Landscaping, security, cleaning, maintenance, elevator, waste removal | Identify contracts with auto-renewal, above-market pricing, or termination penalties |

| CapEx budget and reserve study | Planned improvements, reserve funding levels, timeline | Underfunded reserves mean the buyer inherits deferred capital needs |

| Insurance loss runs (5 years) | Claims history, frequency, severity, types | High claim frequency signals ongoing property issues and may affect insurability |

| Debt documents (if assuming financing) | Loan terms, prepayment penalties, due-on-sale clauses, reserve requirements | Assumption terms can materially change your cost of capital |

Key underwriting questions

- Are reported rents consistent with signed leases and bank deposit records?

- Are expenses artificially low because the owner performs unpaid management or defers maintenance?

- What is the realistic reassessed property tax after your purchase price is recorded?

- How will current interest rates, insurance trends, and utility cost inflation affect projected cash flow over your hold period?

The goal is not to make the pro forma attractive. The goal is to make it honest.

Category 4: Tenant Analysis (Commercial and Multifamily)

You are not just buying a building. You are buying a stream of cash flow that depends on tenants honoring their obligations.

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| All leases, amendments, and side agreements | Base rent, escalations, options, exclusives, co-tenancy clauses, CAM provisions | The lease is the legal foundation of your income stream; every provision affects value |

| Estoppel certificates | Tenant confirmation of lease terms, rent, deposits, defaults | Locks tenants into acknowledged terms and prevents post-closing disputes |

| Tenant financial statements (major tenants) | Revenue, profitability, creditworthiness | A lease is only as valuable as the tenant's ability to pay |

| Lease expiry schedule | Rollover timing, clustering, weighted average lease term (WALT) | Expiry cliffs where multiple leases end simultaneously create vacancy and re-leasing risk |

| Rent concession history | Free months, tenant improvement allowances, reduced rents | Concessions that mask true market rent inflate reported NOI |

| Tenant correspondence | Complaints, maintenance requests, renewal discussions | Reveals tenant satisfaction and likelihood of renewal |

| Rent control / stabilization status | Applicable regulations, current registered rents, permitted increases | In regulated markets, your ability to increase rents may be severely limited |

| Sublease and assignment records | Third-party occupants, consent requirements | Subletting can introduce unknown credit risk into your income stream |

Concentration risk: If a single tenant represents more than 40% of gross revenue, model the scenario where that tenant vacates. If the deal does not survive that scenario at your purchase price, you are underpricing tenant risk.

Track which lease documents each prospective buyer spends the most time reviewing using Peony's page-level analytics. If a buyer lingers on a specific tenant's lease, proactively prepare supplemental information about that tenant's financials and renewal prospects.

Category 5: Market and Zoning

Market context determines whether your assumptions about rent growth, vacancy, and exit value are realistic or aspirational.

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Zoning verification letter | Current zoning designation, permitted uses, density limits, parking requirements | Confirms your intended use is legal; nonconforming status limits future flexibility |

| Variance or special use permits | Conditions, expiration, transferability | Permits may not transfer to new owners or may have conditions you cannot meet |

| Entitlement status (development sites) | Approved plans, conditions of approval, timeline, community agreements | Entitlement risk is the single largest variable in development deals |

| Comparable rent analysis | Market rents for similar properties in the submarket | Determines whether current rents are above, at, or below market |

| Vacancy and absorption data | Submarket vacancy rates, absorption trends, historical patterns | High vacancy or negative absorption signals pricing pressure |

| New supply pipeline | Planned and under-construction competitive properties | New supply within a 1-3 mile radius directly competes for your tenants |

| Demographic and employment trends | Population growth, employer concentration, income trends | Long-term demand drivers determine exit value more than current cap rates |

| Historic district or landmark designation | Restrictions on modifications, facade requirements, tax incentives | Designation can limit renovations but may provide tax benefits |

2026 update on zoning: Many municipalities have adopted or are adopting new zoning codes that affect density, accessory dwelling units (ADUs), and mixed-use designations. Confirm the applicable zoning code version and check for pending amendments that could change permitted uses during your hold period.

Category 6: Insurance and Climate Risk

In many markets in 2026, the deal lives or dies on insurance. This category has moved from a back-of-checklist afterthought to a make-or-break analysis.

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Current insurance policies (all types) | Property, liability, flood, windstorm, earthquake, umbrella coverage amounts and exclusions | Understand exactly what is and is not covered before you inherit the risk |

| Insurance premium history (5 years) | Premium trajectory, carrier changes, coverage reductions | Rising premiums are a leading indicator of market-level risk repricing |

| Actual insurance quotes for your ownership | Binding quotes from 2-3 carriers for your intended use and entity | Never rely on the seller's premiums; your coverage needs and carrier options may differ significantly |

| FEMA flood zone determination | Flood zone designation, base flood elevation, community rating system class | FEMA designates 13 million+ structures in Special Flood Hazard Areas; zone changes can dramatically affect insurance costs and property value |

| Wildfire risk assessment | WUI (Wildland-Urban Interface) designation, defensible space, local fire history | California, Colorado, Oregon, and other Western states have seen carriers exit high-risk zones entirely |

| Wind and hurricane risk (coastal) | Wind zone designation, building code compliance, shutter/impact requirements | Coastal wind exclusions and named-storm deductibles (2-5% of insured value) are increasingly common |

| Climate risk score | First Street, ClimateCheck, or insurer-provided property-level risk data | A starting point for understanding flood, wildfire, heat, and storm exposure over your hold period |

| Resilience measures in place | Elevated equipment, fire-resistant materials, flood barriers, backup power | Existing resilience measures can reduce premiums and protect value; their absence is a CapEx liability |

| Loss run reports (5 years) | Claims history, type, frequency, severity | Frequent claims signal ongoing property issues and may limit future carrier options |

Why this category changed everything in 2026

The Insurance Information Institute reports that homeowners' insurance premiums increased an average of 33% nationally between 2020 and 2024, with much larger increases in climate-exposed markets. In parts of Florida, Louisiana, and California, premiums have risen 200-400%. Several major carriers have stopped writing new policies in high-risk zones entirely.

For buyers, the practical implication is that you cannot underwrite a deal using the seller's historical premiums. You must obtain binding quotes for your own entity and intended use, model premium escalation scenarios, and stress-test your returns against a 50-100% premium increase over your hold period.

For a detailed breakdown of due diligence costs including insurance assessment fees, see our due diligence cost breakdown guide.

Category 7: Regulatory and Compliance

Regulatory due diligence verifies that the property complies with all applicable laws and identifies upcoming regulatory changes that could affect operations or value.

| Document / Item | What to Check | Why It Matters |

|---|---|---|

| Certificates of occupancy (all units) | Current and valid for actual use | Operating without a valid CO is illegal in most jurisdictions and can void insurance |

| Building code compliance history | Violations, remediation, open permits | Unresolved violations transfer to the buyer and may require immediate remediation |

| ADA compliance assessment | Accessibility of common areas, parking, entries, restrooms | ADA lawsuits are common and expensive; proactive compliance is cheaper than reactive litigation |

| Fire code compliance | Sprinkler coverage, alarm systems, exit signage, fire department inspections | Fire code violations can trigger immediate closure orders |

| Energy benchmarking requirements | Local Law 97 (NYC), BERDO (Boston), or equivalent local mandates | Non-compliance penalties are growing; retrofitting for efficiency is a significant CapEx item |

| Rent control / rent stabilization | Applicable regulations, registered rents, tenant protections | In regulated markets, your income is capped by law regardless of market conditions |

| Short-term rental restrictions | Local ordinances, HOA rules, licensing requirements | If your business plan includes Airbnb or short-term rental income, verify it is legal |

| Environmental compliance orders | EPA, state DEQ, or local agency orders | Compliance orders create successor liability that survives the sale |

| Seismic retrofit requirements | Local seismic safety ordinances (especially CA, OR, WA, UT) | Soft-story retrofit mandates can cost $50,000-$200,000+ per building |

| Upcoming regulatory changes | Pending legislation, proposed zoning amendments, planned infrastructure | Changes during your hold period can dramatically affect value -- for better or worse |

2026 update: Energy benchmarking and building performance standards are expanding rapidly. New York's Local Law 97 began imposing carbon emission penalties in 2024. Boston's BERDO, Denver's Energize Denver, and Washington DC's BEPS all require commercial buildings to meet energy targets or face penalties. If your target property is in a jurisdiction with building performance standards, model the compliance cost into your CapEx budget.

Use Peony's AI redaction to identify and redact PII, financial data, and sensitive terms from regulatory documents before sharing them with counterparties during due diligence.

Asset-Type Variations: Adjusting the Checklist

Not every property type requires the same emphasis. Here is how to adjust the checklist by asset type.

Residential (Single-Family and Small Multifamily)

- Heavier emphasis on: Physical inspection, title, insurance, property tax reassessment, local landlord-tenant laws

- Lighter emphasis on: Tenant financial analysis (fewer tenants, shorter leases), commercial zoning complexities

- Unique considerations: HOA documents and special assessments, lead paint disclosure (pre-1978 construction), septic and well testing (rural properties), flood zone determination

- Typical DD timeline: 14-30 days

Commercial (Office, Retail, Mixed-Use)

- Heavier emphasis on: Tenant creditworthiness and lease analysis, WALT and rollover risk, CAM reconciliation, ADA compliance, energy benchmarking

- Lighter emphasis on: Single-unit physical inspection (PCA covers the whole asset)

- Unique considerations: Co-tenancy and exclusivity clauses, tenant improvement obligations, parking ratios and requirements, signage rights

- Typical DD timeline: 45-90 days

Industrial and Warehouse

- Heavier emphasis on: Environmental (Phase I always required, often Phase II), loading dock and clear height specifications, power capacity, floor load ratings

- Lighter emphasis on: Aesthetic condition, tenant mix complexity (often single-tenant)

- Unique considerations: Hazardous materials storage and handling permits, rail access and truck court dimensions, EPA compliance history, UST records

- Typical DD timeline: 45-75 days

Land and Development Sites

- Heavier emphasis on: Zoning and entitlement, survey and boundary, environmental (especially brownfield risk), utility availability, access and ingress/egress

- Lighter emphasis on: Physical condition (no existing structure), tenant analysis (no tenants), operating financials

- Unique considerations: Entitlement risk is dominant, wetlands and endangered species, impact fees and exactions, community opposition, phasing plans

- Typical DD timeline: 60-120+ days

For guidance on organizing due diligence documents for private equity real estate transactions specifically, see our best data rooms for private equity guide.

Specialized asset classes go deeper still — each inverts the checklist around its own dominant risk. For the asset-specific playbooks, see our data center data room (power, interconnection, and the hyperscale lease abstract), cell tower data room (the lease tape and the FCC/FAA/NEPA compliance file), and industrial data room (clear height, ESFR commodity classification, and IOS zoning) guides. Operating-asset classes go further still — the senior housing data room (license, operations transfer, RIDEA, census) and the skilled nursing facility data room (CHOW, F-tags, payor mix) re-order the entire checklist around the operation, not the building. More asset-specific checklists round out the set: the multifamily acquisition data room (reconciling the rent roll to leases without exposing resident PII), the net-lease data room (single-tenant NNN and sale-leaseback, where the tenant's credit is the asset), the medical office building data room (Stark/anti-kickback and fair-market-value lease compliance plus health-system credit), the note sale data room (buying or selling the CRE loan itself — the debt, where the chain of title to the note is the diligence), and the renewable energy data room (solar, wind, and BESS projects run on site control, interconnection, offtake, and tax-credit basis).

How to Organize Your Real Estate Data Room

A well-organized data room accelerates due diligence, reduces repetitive buyer questions, and signals professional preparation. Here is the folder structure I recommend based on hundreds of RE transactions.

Recommended folder structure

- Legal and Title -- deed, title commitment, survey, easements, entity documents, HOA records

- Physical and Environmental -- PCA, inspection reports, Phase I/II ESA, as-built drawings, CapEx history

- Financial and Operational -- rent roll, T-12/T-36 operating statements, tax bills, utility records, service contracts, debt documents

- Tenant Analysis -- leases, amendments, estoppel certificates, tenant financials, correspondence

- Market and Zoning -- zoning letter, comp analysis, supply pipeline data, demographic reports

- Insurance and Climate Risk -- current policies, premium history, flood determination, climate risk scores, loss runs

- Regulatory and Compliance -- certificates of occupancy, code compliance, ADA assessment, energy benchmarking, permits

Setting up with Peony

- Upload in bulk -- drag and drop your entire document set into a new Peony data room. AI auto-indexing categorizes files into the 7-folder structure in under 3 minutes.

- Set staged access -- use per-folder permissions so Phase 1 buyers see property overviews and market data, while detailed financials and tenant information unlock only for shortlisted bidders after NDA execution.

- Enable security -- activate dynamic watermarks (viewer identity embedded in every page), screenshot protection (blocks and logs attempts), and email verification for all visitors.

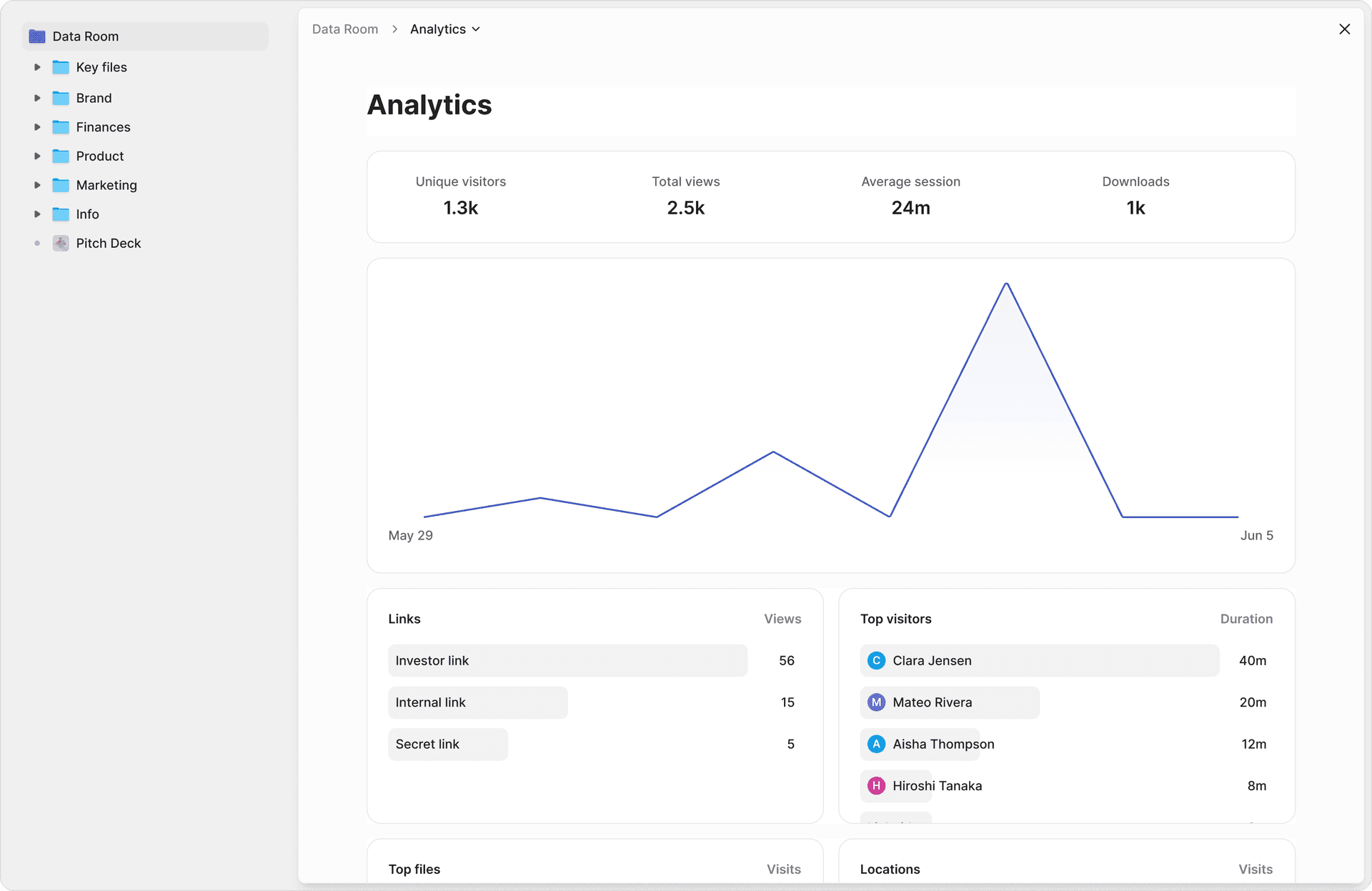

- Track engagement -- page-level analytics show exactly which documents each buyer reviewed, for how long, and in what order. If a buyer skips the environmental section entirely, that tells you something.

- Manage Q&A -- use Peony's structured Q&A workflow so buyer questions get routed to the right team member, AI drafts initial responses, and approved answers maintain a complete audit trail.

- Execute documents -- use built-in e-signatures for LOIs, PSAs, NDAs, and estoppel certificates without switching to a separate tool.

The entire setup takes under 5 minutes. Compare that to the days or weeks required to manually organize folders, set permissions, and configure security in legacy VDR platforms.

For a comprehensive guide to data room organization across all transaction types, see our complete guide to virtual data rooms.

The Bottom Line: Tiered Recommendations by Deal Type

Single-family or small multifamily (sub-$1M): Focus your energy on title, physical inspection, insurance quotes, property tax reassessment, and local landlord-tenant laws. A basic data room (even Peony's free tier) keeps everything organized and shareable.

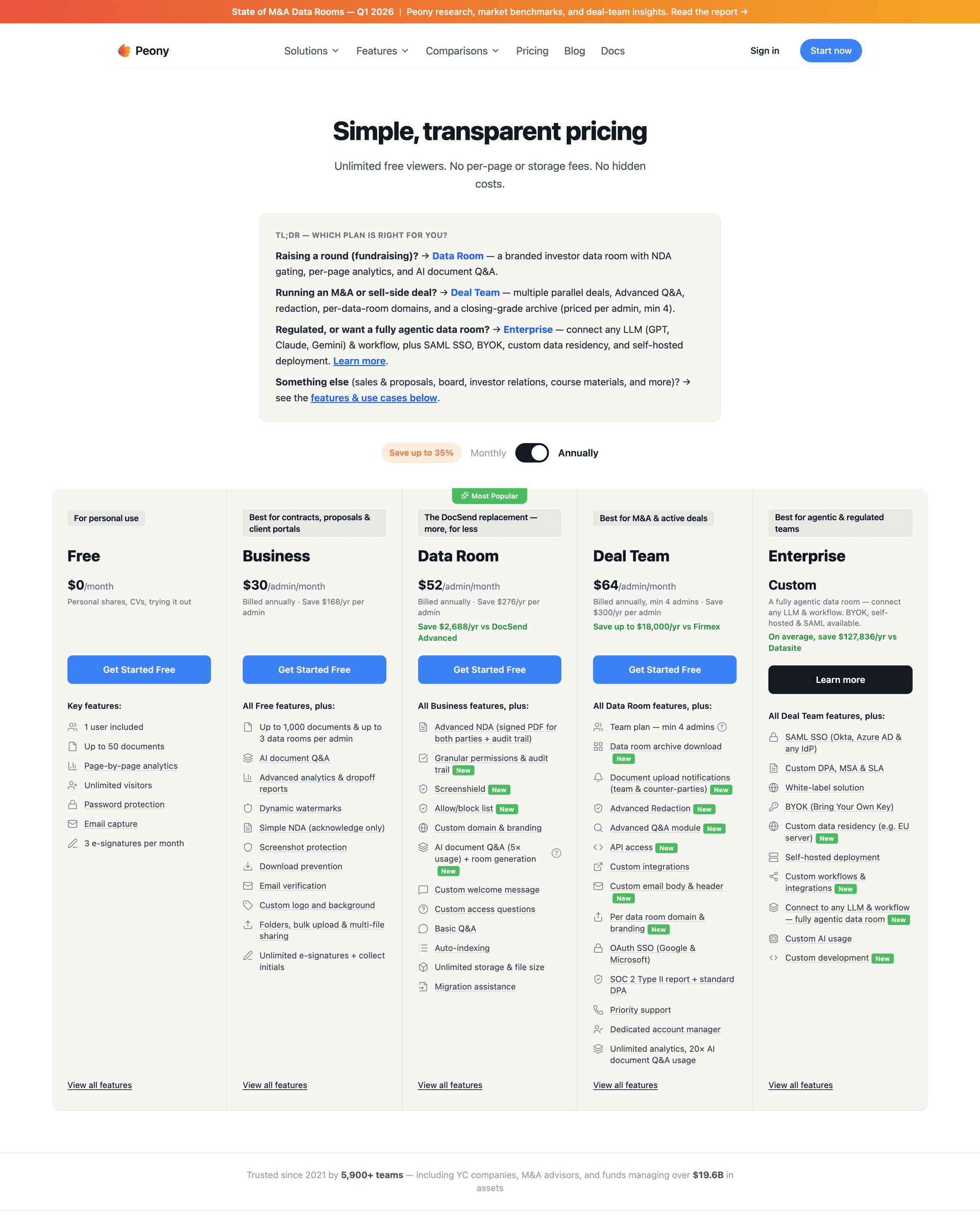

Mid-market commercial ($1M-$25M): Run the full 7-category checklist. Get an ALTA survey, Phase I ESA, property condition assessment, and actual insurance quotes. Use a data room with page-level analytics and NDA gating to manage multiple interested parties professionally. Peony's Data Room plan at $52/admin/month covers unlimited rooms and all security features.

Large commercial or portfolio ($25M+): Full checklist plus retained environmental counsel, independent market study, detailed tenant credit analysis, and climate resilience assessment. Your data room needs staged disclosure, structured Q&A, dynamic watermarking, and comprehensive audit trails. Consider whether institutional counterparties require a specific VDR provider -- some large pension funds and REITs mandate legacy platforms by policy, which is one area where Peony's newer brand can be a limitation despite superior features.

Land and development: Prioritize entitlement, zoning, environmental, and survey above all else. The absence of existing structures means physical inspection is minimal, but the regulatory and environmental workstreams are far more complex and uncertain.

Regardless of deal size, the pattern is the same: verify every seller claim with documentation, model the downside scenarios, and make sure the risks are priced into your offer. Walking away from a bad deal is not a failure of due diligence -- it is exactly what good due diligence is designed to produce.

FAQ

What is real estate due diligence?

Real estate due diligence is the systematic investigation of a property's legal, physical, financial, environmental, and regulatory condition before committing capital. The goal is to verify every seller claim and uncover hidden risks that could reduce value or create liability after closing. Peony's AI auto-indexing organizes hundreds of RE documents into proper due diligence categories in under 3 minutes, so buyers and sellers spend time analyzing documents instead of hunting for them.

How long does real estate due diligence take?

Residential due diligence typically takes 14 to 30 days, which is the standard inspection and contingency window in most purchase agreements. Commercial and multifamily transactions run 45 to 90 days depending on asset size, tenant complexity, and environmental risk. Large portfolio or industrial deals can exceed 120 days. Peony's page-level analytics show sellers exactly which sections each buyer reviewed and for how long, so they can identify stalled workstreams and push materials proactively before deadlines expire.

What documents are needed for real estate due diligence?

A comprehensive real estate due diligence package covers 7 categories: legal and title (deed, title commitment, survey, easements), physical and environmental (inspection reports, Phase I ESA, roof and structural assessments), financial and operational (rent roll, trailing 12-month P&L, tax bills, utility costs), tenant analysis (all leases, estoppel certificates, tenant financials), market and zoning (zoning letter, comp analysis, entitlement status), insurance and climate risk (current policies, loss history, flood zone determination, wildfire risk score), and regulatory and compliance (certificates of occupancy, ADA compliance, building code violations). Peony data rooms include AI-powered document extraction that lets buyers ask natural-language questions across every uploaded document and get cited answers with exact page numbers.

What is the most commonly missed item in real estate due diligence?

Insurance availability and premium trajectory is the most commonly missed item in 2026. Buyers model acquisition returns using historical premiums, then discover after closing that insurers have repriced the risk zone or exited entirely. FEMA flood zone reclassifications, wildfire risk reassessments, and coastal wind exclusions can increase annual insurance costs by 200% to 400% in affected areas. Peony's dynamic watermarking embeds each viewer's identity into every rendered page of insurance documents, so sellers can share sensitive loss-run data and premium histories without risking unauthorized distribution.

How do I organize a real estate data room for due diligence?

Organize your real estate data room into 7 top-level folders matching the standard due diligence categories: Legal and Title, Physical and Environmental, Financial and Operational, Tenant Analysis, Market and Zoning, Insurance and Climate Risk, and Regulatory and Compliance. Upload all documents in bulk, and Peony's AI auto-indexing sorts them into the correct folders in under 3 minutes. Then set staged permissions so sensitive financial data is only visible to shortlisted buyers, enable NDA gates before access, and share a single secure link instead of emailing attachments. The entire setup takes under 5 minutes.

What are the biggest red flags in real estate due diligence?

The biggest red flags are: unresolved title defects or boundary disputes, Phase I environmental contamination requiring remediation, deferred maintenance exceeding 15% of asset value, tenant concentration where a single tenant represents more than 40% of revenue, zoning nonconformity without grandfathering documentation, flood zone designation without adequate insurance, and operating expense ratios significantly below market norms which suggest deferred spending. Peony's screenshot protection blocks and logs capture attempts on sensitive due diligence documents, which is critical when sharing red-flag findings with investment committees reviewing off-market deals.

How much does real estate due diligence cost?

Real estate due diligence costs range from $2,000 to $5,000 for a single-family residential property up to $50,000 to $200,000 or more for large commercial or portfolio transactions. The largest line items are Phase I and Phase II environmental assessments ($2,000 to $50,000), ALTA surveys ($3,000 to $25,000), property condition assessments ($5,000 to $30,000), and legal review ($5,000 to $50,000). Data room costs add $0 to $25,000 depending on the provider. Peony offers real estate data rooms starting free, with the Data Room plan at $52 per admin per month including unlimited rooms, AI auto-indexing, e-signatures for LOIs and PSAs, and enterprise security.

What security features matter for real estate due diligence data rooms?

Real estate due diligence involves sharing highly sensitive documents including financial statements, tenant personal information, environmental reports, and insurance loss histories. Essential security features are NDA gates that require signature before any document access, dynamic watermarking that traces leaks to specific viewers, screenshot protection that blocks and logs capture attempts, granular per-folder permissions for staged disclosure, email verification for visitor identity, and complete audit trails. Peony's Free plan includes AES-256 encryption, 2FA, link expiry, and per-page analytics. The Business plan ($30/admin/month) adds NDA gates and screenshot protection, with dynamic watermarking on the Data Room plan ($52/admin/month) -- which matters for off-market deals where confidentiality is the seller's primary concern.

Related Resources

- The Office-Conversion Data Room — one evidence room for three audiences: buy the asset or the note, raise the LP equity, close the construction lender

- Commercial Property Due Diligence: How to Run It Against the Clock — the process companion to this checklist: the 30–90 day clock, contingencies, re-trades, and how the diligence is run across buyer, seller, and lender

- Due Diligence Checklist: 174 Documents Buyers Actually Request

- M&A Due Diligence Process: The 6-Phase Playbook

- Due Diligence Cost Breakdown

- What Is a Virtual Data Room? Complete Guide

- Real Estate Fund Data Room: The 3-Room Model — the fund-level layer above per-asset diligence (fundraising room + LP reporting portal)

- Real Estate Syndication Data Room — the sponsor-side raise where this buyer-DD checklist becomes the underwriting evidence LPs scrutinize

- Data Room for Real Estate: 5 VDR Archetypes

- Startup Due Diligence Guide

- Best Data Rooms for Private Equity

- Secure File Sharing Guide

- Peony for Real Estate

- Peony for Due Diligence

- Mobile Home Park Data Rooms — the MHC overlay for this checklist: park-owned home titles, well/septic records, and resident-notice clocks

You might also like

May 13, 2026

Environmental Due Diligence (2026): PFAS, CSDDD, BFPP Defense Stack

Aug 7, 2026

Best M&A Data Rooms (I Built One, Then Tested 6 More) in 2026

Jul 28, 2026

Carve-Out Data Room Guide (2026): Sale Perimeter, TSA Schedules, and Day-1 Separation