SaaS M&A Data Room 2026: The Re-Pivot Window Playbook

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Quick answer: Yes -- if you're a late-stage SaaS company in 2026, M&A is the realistic exit path, not IPO. The IPO window slammed shut after Anthropic's January 12 launch of Claude Cowork triggered a $1 trillion repricing of public SaaS comps; zero VC-backed SaaS unicorns have filed to go public YTD 2026 per Crunchbase. But Q1 2026 was the most active software M&A quarter since 2021 -- Google/Wiz $32B, Palo Alto/CyberArk $25B, IBM/Confluent $11B closed in 60 days. Whether you're talking to a strategic acquirer or a PE take-private buyer, your data room readiness will compress or expand your multiple by 1-2x ARR.

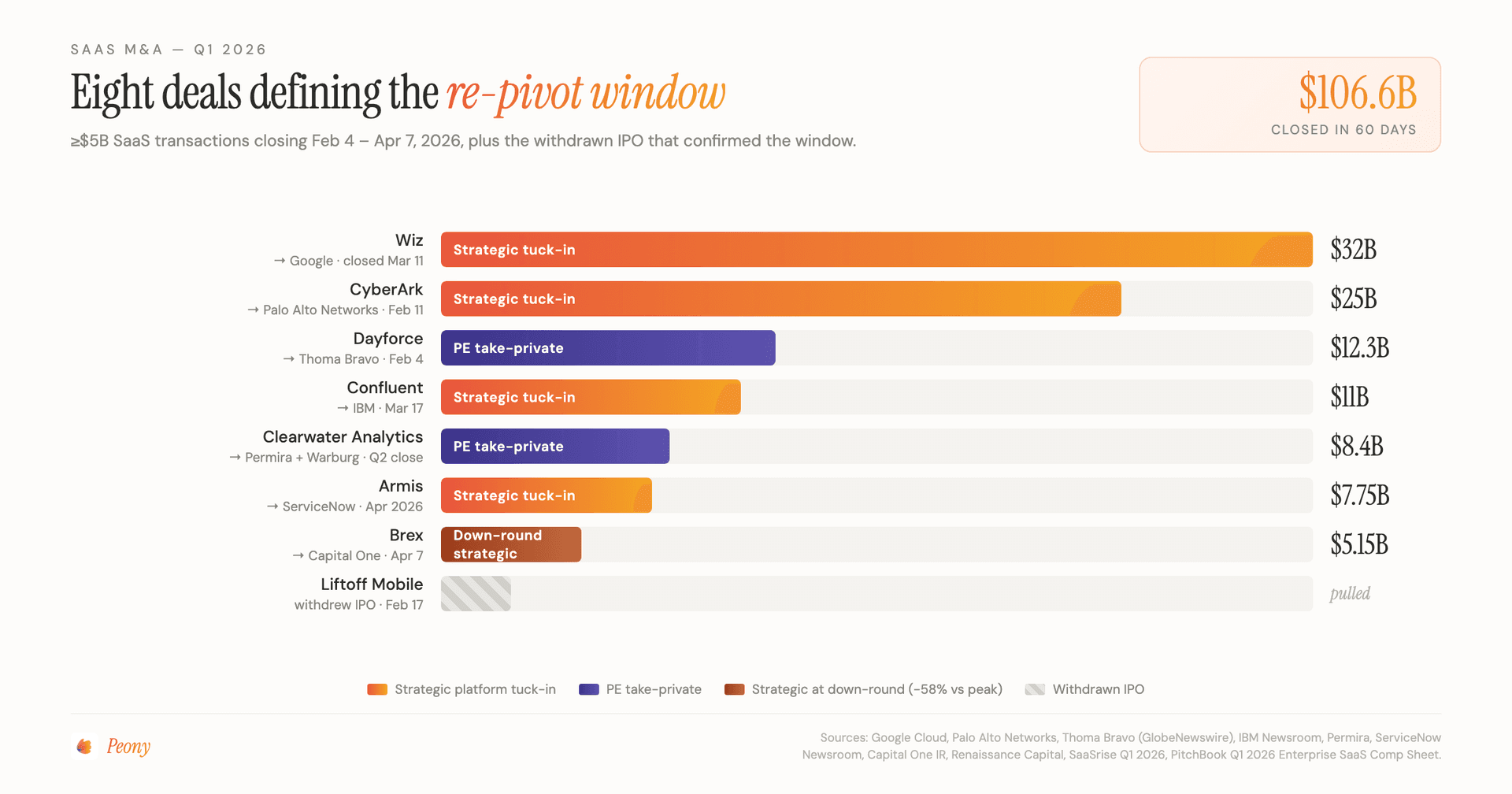

TL;DR: The SaaS M&A re-pivot window is open and active. Q1 2026 had 620+ SaaS transactions worth $95B+ aggregate per SaaSrise, the most active software-M&A quarter since 2021, with eight ≥$5B SaaS strategic and PE deals closing in 60 days: Google/Wiz $32B (Mar 11), Palo Alto/CyberArk $25B (Feb 11), Thoma Bravo/Dayforce $12.3B (Feb 4), IBM/Confluent $11B (Mar 17), Permira+Warburg+Francisco+Temasek/Clearwater $8.4B (Q2 2026 close), ServiceNow/Armis $7.75B (Apr 2026), and Capital One/Brex $5.15B (Apr 7). Median public SaaS EV/TTM-revenue compressed to 3.3x at Mar 31 2026 from 4.9x YE 2025 and 6.2x YE 2024 per PitchBook. The 4-tier SaaS data room readiness ladder (Tier 1 raw -> Tier 2 organized -> Tier 3 AI-defensible -> Tier 4 auction-grade) is the structural diagnostic: ~60% of late-stage unicorns sit at Tier 1, ~5% at Tier 4. Tier 4 sellers achieve Wiz-style premiums; Tier 1 sellers absorb Brex-style 58% discounts. Below: the deal landscape, the readiness ladder, the buyer-segmentation playbook, and the advisor-selection map.

Last updated: May 2026

I run Peony, a data room platform for M&A and private equity. I wrote this for four SaaS-specific sell-side personas the generic M&A data room guide does not address: the SaaS founder at $5-100M ARR running a sell-side after the Liftoff withdrawal killed the IPO option, the PE platform corp-dev associate underwriting a SaaS take-private bolt-on against the new 3.3x EV/revenue floor, the SaaS CFO preparing diligence packs that need to defend AI-feature-attribution to NRR cohort-by-cohort, and the growth-equity associate underwriting a SaaS minority-recap or secondary at the post-SaaSpocalypse comp. The single hardest question every one of them brings to me: what's actually different about a SaaS data room versus a generic M&A data room — ARR cohort builds, gross-vs-net retention by acquisition vintage, customer-concentration above the 10% threshold, ETR construction with stock-based comp roll-back, and the GAAP-vs-cash-revenue reconciliation that bridges deferred revenue to billings. None of that exists in the 174-document generic M&A baseline.

I co-founded Peony after eight years on the investor side -- venture at Backed VC, growth equity at Target Global covering late-stage and secondary deals, and a brief earlier stint in M&A at Nomura. Across those roles I evaluated hundreds of SaaS deals from the buyer's chair, and I now field SaaS-specific room questions every week from sellers staring down the 12-month SaaS M&A re-pivot window.

This guide is the SaaS-vertical sibling to the generic M&A data room playbook — that anchor frames the 11-folder corporate baseline; this post layers the SaaS-specific stack on top: the eight closed ≥$5B deals that define the active window, the 4-tier SaaS data room readiness ladder that determines whether you get a Wiz-style premium or a Brex-style 58% discount, and the AI-defensibility evidence pack that maps directly to a multiple uplift in 2026 SaaS diligence. Advisor cross-references against the NYC, SF/Bay, LA, Boston, Miami, and Seattle M&A guides; platform comparisons in the top 10 VDR providers review and virtual data room cost guide.

What triggered the SaaS M&A re-pivot window in 2026?

Three triggers stacked Q1 2026 to slam the SaaS IPO window shut and open the M&A window in parallel: Anthropic's Claude Cowork launch repriced per-seat SaaS, public SaaS comps compressed nearly 50% in 15 months, and Liftoff Mobile pulled its $711M IPO on February 17, 2026 to set the withdrawn-IPO precedent every other unicorn followed.

This is the SaaS M&A re-pivot window in its clearest form: a finite period (~12-18 months from the closure event) where strategic acquirers and PE platforms are aggressively buying SaaS at compressed multiples while the IPO market is structurally unavailable. We're inside it now, and the deal-clock starts from the Liftoff withdrawal.

Trigger 1: AI-agent threat repricing

Anthropic launched Claude Cowork on January 12, 2026 and expanded it to 11 plugins on January 30, 2026. In the three weeks between those two events, public SaaS comps lost approximately $1 trillion in market capitalization. Bloomberg's February 4, 2026 piece "What's Behind the SaaSpocalypse Plunge in Software Stocks" crystallized the framing in mainstream financial media. TechCrunch followed on March 1, 2026 with "SaaS in, SaaS out: Here's what's driving the SaaSpocalypse", and Salesforce CEO Marc Benioff's February 25, 2026 response ("This isn't our first SaaSpocalypse") gave every SaaS executive the public talking-point cover for the rerating.

The structural thesis behind the rerating: per-seat SaaS pricing assumes humans buying licenses to operate a software workflow. Agentic workflows -- where an AI agent orchestrates the same workflow without per-seat human licenses -- compress the seat count by 5-20x in many use cases. Public investors repriced that risk into multiples. Strategic acquirers and PE buyers also repriced it, but they have a workaround: buy the SaaS at the new multiple, integrate it into their own AI-orchestration stack, and capture the value differential. That's the bid that's still active.

Trigger 2: Multiple compression

Median EV/TTM-revenue for tracked public SaaS comps fell to 3.3x as of March 31, 2026, down from 4.9x at year-end 2025 and 6.2x at year-end 2024 per PitchBook's Q1 2026 Enterprise SaaS Public Comp Sheet and Valuation Guide. That's a 47% drop in 15 months. A 2021-vintage unicorn priced at 30x ARR cannot file an IPO at 3.3x without re-anchoring the entire cap table to a 90% haircut. So they don't file; they sell.

The math is unforgiving. A $300M ARR SaaS that was worth $9B at 30x in 2021 is worth ~$1B at 3.3x today. The CFO's job is no longer to maximize the IPO peak; it's to maximize the realistic-cash exit inside the SaaS M&A re-pivot window. The virtual data room cost guide covers the operational side of getting buyer-ready inside that window without burning $50K+ on legacy VDR pricing.

Trigger 3: Withdrawn-IPO precedent

Blackstone-backed Liftoff Mobile filed its $711M IPO on January 13, 2026 per Renaissance Capital. Bloomberg reported on February 5, 2026 that Liftoff was postponing the IPO on the software rout. On February 17, 2026, Liftoff officially withdrew the filing per Bloomberg and the SEC.

The market read the withdrawal as a precedent rather than a one-off. Crunchbase News reported on February 25, 2026 that zero VC-backed SaaS unicorn IPO filings have hit the market YTD 2026 -- a stark contrast to the 20+ filings in a comparable 2021 period. Crunchbase's stalled-unicorn coverage further documented that 517 global / 45 US SaaS unicorns haven't raised since 2021. The IPO window is not slowly closing; it is structurally shut, and the cohort with no recent funding round is exactly the cohort being pushed toward M&A by their boards.

Which deals define the active SaaS M&A window?

Eight named ≥$5B SaaS strategic and PE deals closed in the 60 days between February 4 and April 7, 2026. The pattern across the eight is what makes the SaaS M&A re-pivot window real and operational rather than narrative.

Quick comparison table -- 8 SaaS deals defining Q1 2026

| Target | Acquirer | Value | Announced | Closed | Acquirer advisor | Target advisor |

|---|---|---|---|---|---|---|

| Wiz | Google (Alphabet) | $32B | Mar 18 2025 | Mar 11 2026 | BofA Securities | Goldman Sachs |

| CyberArk | Palo Alto Networks | $25B | Jul 28 2025 | Feb 11 2026 | Not disclosed | Not disclosed |

| Dayforce | Thoma Bravo (take-private) | $12.3B | Aug 21 2025 | Feb 4 2026 | Goldman + J.P. Morgan | Evercore |

| Confluent | IBM | $11B | Aug 2025 | Mar 17 2026 | Not disclosed | Not disclosed |

| Clearwater Analytics | Permira + Warburg consortium | $8.4B | Dec 21 2025 | Q2 2026 (pending FIRB) | Not disclosed | Not disclosed |

| Armis | ServiceNow | $7.75B | Dec 23 2025 | Apr 2026 | Tidal Partners + JPM + Barclays | Not disclosed |

| Brex | Capital One | $5.15B | Jan 22 2026 | Apr 7 2026 | BofA Securities | Centerview Partners |

| Liftoff Mobile (counter-example) | n/a -- pulled $711M IPO | n/a | Filed Jan 13 | Withdrawn Feb 17 2026 | n/a | n/a |

Strategic platform tuck-ins

Four of the eight deals are strategic platform tuck-ins -- the highest-multiple archetype inside the window. Google's $32B Wiz acquisition closed March 11, 2026 per Google Cloud's press release and the Cleary Gottlieb advisory release. It is the largest acquisition in Google's history. BofA Securities advised Google; Goldman Sachs advised Wiz. The strategic logic: cloud-security platform consolidation across multi-cloud architecture that no competing strategic could replicate.

Palo Alto Networks' $25B CyberArk acquisition closed February 11, 2026 per Palo Alto Networks' press release, formally entering Identity Security as a platform pillar. IBM's $11B Confluent acquisition closed March 17, 2026 per the IBM Newsroom -- the strategic frame is agentic-AI data fabric anchored on data-in-motion infrastructure. ServiceNow's $7.75B Armis acquisition announced December 23, 2025 per the ServiceNow Newsroom and TechCrunch coverage, closed in April 2026 ahead of the original H2 2026 schedule. Tidal Partners led ServiceNow's advisory mandate with J.P. Morgan and Barclays as co-advisors -- a marquee boutique mandate against bulge-bracket competition.

PE take-privates

Two of the eight are PE take-privates that price off the new comp floor with strong free-cash-flow logic. Thoma Bravo's $12.3B Dayforce take-private closed February 4, 2026 per the GlobeNewswire / Thoma Bravo announcement and the Kirkland & Ellis advisory release. Goldman Sachs and J.P. Morgan advised Thoma Bravo; Evercore exclusively advised Dayforce. The Permira + Warburg Pincus consortium's $8.4B Clearwater Analytics take-private announced December 21, 2025 per Permira's release, closes Q2 2026 pending FIRB clearance. Francisco Partners is co-investor; Temasek is participating LP. The four-firm consortium signals scarcity of single-firm $8B+ checks for SaaS take-privates in the current environment.

Strategic at down-round

One of the eight is the cleanest down-round-to-prior-peak example. Capital One's $5.15B Brex acquisition closed April 7, 2026 per Capital One's IR release and the closing announcement. TechCrunch's coverage anchored the discount math: Brex's $5.15B sale price is approximately a 58% discount to its $12.3B 2022 peak private valuation. BofA Securities advised Capital One; Centerview Partners advised Brex. The deal is the structural illustration of "strategic at down-round" -- the buyer pays for capability rather than valuation peak, and the seller takes a real-cash exit at the new comp floor rather than waiting for IPO multiples to reflate.

Counter-example: the withdrawn IPO

Liftoff Mobile, Blackstone-backed, filed its $711M IPO on January 13, 2026 and withdrew it on February 17, 2026. The withdrawal is the single most useful counter-example for any board still deliberating IPO-vs-M&A: the IPO-market signal is no longer ambiguous. Renaissance Capital's tracking confirms zero VC-backed SaaS unicorn IPO filings YTD 2026.

What is the 4-tier SaaS data room readiness ladder?

The 4-tier SaaS data room readiness ladder is the diagnostic I use across Peony customer engagements to map a SaaS seller's data room maturity to the multiple they will achieve in the active window. The four tiers are stacked, not parallel: each tier subsumes the lower tier and adds specific artifacts that move you up the multiple curve.

Tier 1 -- Raw

A Drive folder with terms-of-service, ARR statement, and headcount roster. Approximately 60% of late-stage SaaS unicorns sit here as of May 2026 by my read of the customer pipeline. Strategic acquirers will walk on a Tier 1 room because the absence of organization signals absence of management discipline; PE buyers will use it as leverage to lowball at 2.5-3x EV/revenue, often below the 3.3x median floor. The structural problem with Tier 1 is not security; it's that the buyer has to do your work for you, and the buyer prices that work into the discount.

Tier 2 -- Organized

An indexed data room, basic Q&A log, and a folder structure following the standard M&A 11-category convention (00 Intro, 01 Corporate, 02 Financials, 03 Tax, 04 Legal, 05 HR, 06 IP, 07 Customers, 08 Sales, 09 Privacy, 10 Insurance, 99 Confirmatory). Tier 2 is acceptable for a take-private at the comp floor multiple but loses 1-2x EV/revenue versus Tier 3 in negotiation. Most legacy VDR platforms (Datasite, Intralinks, Firmex) get sellers to Tier 2 with substantial billable hours. The full sell-side template is in the M&A data room playbook.

Tier 3 -- AI-defensible

This is the multiple-defending tier in 2026. Tier 3 adds five specific artifact categories on top of Tier 2:

- Model architecture diagrams -- which foundation models you use, where they run, how you orchestrate them, what fallback paths exist if any single model partner deprecates an API or changes pricing.

- Training data rights documentation -- what proprietary training data you own, what you license, what the survival terms are, and what happens to the training-data asset if the licensor changes terms.

- Model drift monitoring evidence -- how you detect model performance degradation, what's your rollback protocol, what's your model-versioning practice, what's your customer-facing communication protocol when a model changes.

- Customer cohort retention with AI-feature attribution -- segment your retention and net-revenue-retention curves by whether the cohort uses your AI features. Show that AI-feature-using cohorts retain and expand at higher rates than legacy cohorts. If you cannot segment this way, the buyer assumes the worst.

- Claude Cowork / agentic-threat scenario analysis -- explicit scenario analysis of how your business survives if buyers shift to agent-on-agent workflows. Include pricing-architecture roadmap from per-seat to outcome-based or usage-based, customer-cohort migration evidence, and competitive-positioning analysis versus the agentic alternatives.

Tier 3 is the fastest single multiple-mover in 2026 SaaS M&A. Sellers at Tier 3 typically negotiate 1-2x EV/revenue above the 3.3x median floor in a competitive process; sellers at Tier 2 typically settle at the floor; sellers at Tier 1 typically settle below the floor with a 5-10% discount. The math compounds quickly at scale: on a $300M ARR business, the gap between Tier 2 and Tier 3 is approximately $300M-$600M of enterprise value.

Tier 4 -- Auction-grade

Tier 4 adds buyer-segmentation, traceability, and competitive-process discipline on top of Tier 3:

- Pre-built buyer-segmented data rooms -- a strategic-acquirer view emphasizing platform-fit, architecture, integrations, customer overlap, and technical depth, versus a PE-buyer view emphasizing unit economics, gross retention, FCF conversion, and opex roll-forward. Same data room, different visitor groups, different segments shown. Visitor groups handle this in Peony Data Room at $52 per admin per month.

- Screenshot-blocking for sensitive customer logos and pricing -- if your top 10 customer list is a competitive moat, you cannot let a competing portfolio company in a strategic acquirer's stable screenshot it. Screenshot-blocking + screenshot-attempt logging closes the leak path and gives you a defensible audit trail.

- NDA gates per buyer tier -- different bidders see different documents based on which stage of your process they have reached, with explicit NDA gating before each tier of access. This is required when running a competitive auction with bidder groups that include competing-portfolio-company conflicts.

- Page-level analytics -- which buyer reviewed which page for how long. This is the single most underrated diligence-period intelligence. If a strategic acquirer's deal team has spent 4 hours on your customer-concentration breakdown and keeps revisiting your top-10 customer detail, they are building a model. If another bidder has not opened anything beyond the executive summary after two weeks, they are not submitting a competitive bid. The deadline-extension decision should be informed by this signal, not by anecdotal sense from the banker.

- Per-investor watermarks -- every rendered page carries a dynamic watermark with the viewer's identity embedded. If a document leaks, you can trace the leak to the exact viewer. The Peony block-screenshots feature (shipping pending) hardens this protection further for the competitor-portfolio-company scenario.

Approximately 5% of late-stage SaaS sellers operate at Tier 4 today. Those are the sellers achieving Wiz-style premium-to-private multiples on competitive auction processes. The cost of operating at Tier 4 inside Peony Data Room is $52 per admin per month per pricing -- a rounding error against the multiple gap.

4-tier readiness ladder summary table

| Tier | Description | % of late-stage SaaS | Multiple impact | Peony equivalent |

|---|---|---|---|---|

| 1 (Raw) | Drive folder, ARR doc, headcount | ~60% | Below floor (3.3x), 5-10% discount | Pre-Peony |

| 2 (Organized) | Indexed room, basic Q&A, 11-cat structure | ~30% | At comp floor (3.3x) | Free / Business tier |

| 3 (AI-defensible) | Tier 2 + 5 AI-defensibility artifacts | ~5% | +1-2x above floor (4-5x) | Data Room $52/admin/mo |

| 4 (Auction-grade) | Tier 3 + buyer-segmentation, watermarks, page analytics | ~5% | Premium-to-comp (5-8x+) | Data Room $52/admin/mo + visitor groups + watermarks + page analytics |

How do I show AI-defensibility in due diligence?

You show three things in the data room and a 2026 strategic acquirer or PE buyer will price your AI-agent risk closer to the floor of their model rather than the ceiling: customer-cohort retention with AI-feature attribution, training-data and model-portability documentation, and pricing-architecture evidence.

Customer-cohort retention with AI-feature attribution

Segment your retention curves by whether the cohort uses your AI features. Show that AI-feature-using cohorts retain at higher rates and expand at higher net-revenue-retention than legacy cohorts. If you cannot segment cohorts this way, the buyer assumes the worst: that your legacy product is the floor, the AI feature is a non-defensible add-on, and your retention is at risk in the agentic-threat scenario.

The artifact: a cohort retention spreadsheet with three columns (legacy cohort, AI-feature-active cohort, AI-feature-attributable retention delta) over at least 12 months of data. Bonus points for segmenting by customer size, vertical, and geography. The Tier 3 rung specifically maps to this evidence.

Training-data and model-portability documentation

Explicitly document which foundation models you orchestrate (Anthropic, OpenAI, Google, Meta, Mistral, others), which proprietary training data you own versus license, what the survival terms are on the licensed data, and what your rollback protocol is if a foundation model partner deprecates an API or changes pricing.

The buyer is solving for the Claude-Cowork scenario where the foundation model partner becomes the competitor. Show that you have model-portability and that your defensibility is in your data and your workflow, not in any single foundation model. The artifact: a one-page architecture diagram plus a rights-and-portability matrix listing each model dependency, each training-data source, and the contractual survival terms.

Pricing-architecture evidence

If you are still pure per-seat, show a credible roadmap to outcome-based or usage-based pricing that survives the agent-on-agent workflow scenario. Bloomberg's February 4, 2026 "SaaSpocalypse" framing crystallized the per-seat-pricing repricing; if your pricing thesis assumes 100 per-seat licenses but the buyer's agentic-future model assumes 10 agent-orchestrators replacing those seats, you need to show the alternative pricing architecture explicitly.

The artifact: a pricing-evolution memo with three scenarios (status-quo per-seat, hybrid per-seat-plus-usage, fully outcome-based) and revenue-impact modeling for each. Cite TechCrunch's March 1, 2026 "SaaS in, SaaS out" explainer and Salesforce's Marc Benioff's February 25, 2026 "This isn't our first SaaSpocalypse" response to anchor your data room narrative in the same vocabulary the buyer is using internally.

How do I segment my data room for strategic acquirers vs PE buyers?

Strategic acquirers and PE take-private buyers consume different evidence to arrive at the same multiple. A strategic-acquirer-segmented view emphasizes platform-fit (architecture, integrations, customer overlap, technical depth, integration roadmap); a PE-buyer-segmented view emphasizes unit economics (LTV/CAC, gross retention, FCF conversion, opex roll-forward, debt-service coverage). Tier 4 of the 4-tier SaaS data room readiness ladder specifically supports both views inside one workspace via visitor groups -- the sell-side advisor toggles which buyer sees which segment without rebuilding the room.

Strategic-acquirer view (platform-fit emphasis)

Surface these documents to strategic-acquirer visitor groups:

- Product architecture documentation (services, dependencies, data schema, API surface, deployment topology)

- Integration matrix with named partner SaaS, hyperscaler dependencies, and proprietary integrations

- Customer overlap analysis with the strategic acquirer's existing customer base (synergy modeling)

- Technical depth evidence -- patents, proprietary algorithms, training-data assets, foundation-model orchestration architecture (Tier 3 artifacts surface here too)

- Integration roadmap with timing, dependencies, and risk

- Hire-the-team evidence -- which engineering and product leaders are foundational to ongoing roadmap

The strategic acquirer is solving for: does this asset close a stated platform gap, what's the integration cost, what's the synergy capture, what's the talent retention. Surface evidence aligned to those four questions.

PE-buyer view (unit-economics emphasis)

Surface these documents to PE-buyer visitor groups:

- LTV/CAC ratio with full unit-economics derivation (cohort lifetime, gross margin, fully loaded CAC by channel)

- Gross retention and net-revenue-retention curves with cohort segmentation

- Free-cash-flow conversion analysis and FCF margin trajectory

- Opex roll-forward with category detail (R&D, S&M, G&A) and headcount sensitivity

- Debt-service coverage modeling for take-private leverage scenarios

- Five-year operating model with multiple downside scenarios

- Founder/management equity rollover assumptions

The PE buyer is solving for: does this asset throw off enough free cash flow to support a 50%+ leveraged structure, what's the operational improvement plan, what's the unlevered IRR, what's the exit strategy in 4-7 years. Surface evidence aligned to those four questions.

Both views, same data room

The structural mistake sellers make is building two physical data rooms. Don't. Build one room with two visitor-group-driven views. The platform supports this natively in Peony Data Room via visitor groups at $52 per admin per month per pricing; legacy VDR platforms charge $5,000+ per month for equivalent functionality. The cost gap matters because a competitive process running 60-120 days easily multiplies into $50K+ on legacy platforms versus under $700 on Peony Data Room.

Which advisors are leading SaaS deals in 2026?

Three structural tiers of advisors are active in 2026 SaaS M&A, and they compete on different deal-size sweet spots: bulge-bracket banks anchor the $5B+ band, branded-boutique tech specialists anchor the $500M-$5B band, and generalist mid-market boutiques anchor the sub-$500M band.

Bulge-bracket: Goldman, Morgan Stanley, J.P. Morgan, Evercore, BofA, Centerview, Barclays, Citi

For deals above $5B, the bulge-bracket bench is unavoidable. Goldman Sachs advised Wiz on the $32B Google sale and advised Thoma Bravo on Dayforce alongside J.P. Morgan; Goldman ranked Q1 2026 #1 by deal value globally per the GlobalData Q1 2026 advisor league tables. Morgan Stanley ranked Q1 2026 #2 by deal value at $210.3B. J.P. Morgan co-advised Thoma Bravo on Dayforce and ServiceNow on Armis. Evercore was exclusive financial advisor to Dayforce on the $12.3B Thoma Bravo take-private; the firm has a deep tech bench across NYC and SF. BofA Securities advised Capital One on the $5.15B Brex acquisition and advised Google on the $32B Wiz acquisition. Centerview Partners advised Brex on the Capital One sale; the firm has a deep NYC and SF tech practice. Barclays co-advised ServiceNow on the Armis acquisition. Citi ranked Q1 2026 #5 by deal value at $112.8B.

The NYC M&A advisor guide covers all eight bulge-bracket firms with named senior bankers and recent deals. The SF/Bay Area M&A advisor guide covers the SF tech practices of Goldman, Morgan Stanley, J.P. Morgan, Evercore, BofA, and Centerview.

Branded-boutique tech specialists: Tidal Partners, Drake Star, AGC, Vista Point, Aquilo

For deals between $500M and $5B, the branded-boutique tech specialist bench is structurally advantaged. Tidal Partners is the most interesting cross-link for SaaS founders specifically. The firm was founded August 2022 by ex-Centerview Silicon Valley partners David Handler and David Neequaye, headquartered in Palo Alto, with offices in NYC and Miami. Tidal led the advisory mandate on ServiceNow's $7.75B Armis acquisition with J.P. Morgan and Barclays as co-advisors -- the kind of marquee boutique success against bulge-bracket competition that anchors a sector-cut advisor relationship. The boutique was founded into the 2022 SaaS-IPO-window-closing moment, the founders' Centerview Silicon Valley DNA travels through to senior-banker engagement on every deal, and the Armis lead-advisor mandate is a public proof point that branded boutiques are winning marquee strategic mandates.

Drake Star and AGC Partners are the two SF tech-specialty boutiques most active in the sub-$1B SaaS band; the SF M&A advisor guide covers both alongside Vista Point Advisors and the SF tech practices of bulge-bracket firms. AGC Partners also has a strong Boston bench positioned for biotech-SaaS overlap exits; the Boston M&A advisor guide covers AGC alongside Aquilo Partners as the two Boston anchors.

Generalist mid-market: Houlihan Lokey

Houlihan Lokey ranked Q1 2026 #1 by deal volume globally with 76 transactions per the GlobalData league tables -- the firm anchors the LA M&A advisor bench and is the elite middle-market choice for SaaS sellers in the $200M-$2B EV band where deal velocity matters more than absolute deal size.

For Miami-anchored SaaS sellers tapping the LatAm cross-border seller pool or the migratory family-office buyer pool, the Miami M&A advisor guide covers Tidal Partners' Miami office bridging the boutique tech-specialty bench into the South Florida ecosystem. For Seattle SaaS sellers benefiting from Microsoft and AWS strategic-acquirer face-time, the Seattle M&A advisor guide is the right cluster-anchor.

How long is the SaaS M&A re-pivot window open?

The SaaS M&A re-pivot window typically runs 12-18 months from the IPO market closure event before strategic acquirers fill up and PE multiples compress further. Counting from Liftoff Mobile's February 17, 2026 IPO withdrawal as the closure event, the window-fill point lands around February-August 2027.

Three structural mechanics drive the time horizon. First, strategic acquirer integration capacity: once Google has digested Wiz, IBM has digested Confluent, ServiceNow has digested Armis, and Palo Alto has digested CyberArk -- each of which is 12-24 months of integration lift -- those acquirers' next-deal appetite drops materially for the subsequent 18 months. Second, PE dry-powder constraints: once the 2026 dry powder allocated to SaaS take-privates is deployed (Thoma Bravo's $12.3B, the Permira + Warburg + Francisco + Temasek $8.4B, plus the next 4-6 deals likely to close in 2026), incremental SaaS take-privates compete with other PE strategies for marginal capital and the multiple-floor compresses further. Third, public-comp re-expansion path: if public SaaS multiples reflate from 3.3x toward the 5-7x range over 2027-2028, the IPO market reopens for marquee assets and the M&A bid weakens at the margin as sellers reach for IPO optionality.

The historical analogue: the post-2008 IPO closure window ran approximately through 2010, then compressed substantially through 2011 as both strategic and PE buyers digested. The 2022 SaaS IPO downturn was a closer comp; the current window inflected from "PE take-private dominant" early to "strategic acquirer dominant" by Q1 2026 with the Wiz, CyberArk, Confluent, and Armis closes within 60 days of each other.

For SaaS sellers operationally, the implication is clear: if you are reading this in May 2026 and you are 2021-vintage unicorn cohort, the optimal exit window is roughly the next 12 months. Standing up a Tier 3 buyer-grade data room now (Peony Data Room at $52/admin/mo) and running a competitive process in Q3-Q4 2026 lands you in the maximum-multiple band of the window. Waiting until 2027 means competing against tired strategic-acquirer deal teams whose 2026 budgets are spent and PE platforms whose 2026 dry powder is already deployed.

How does the SaaS M&A window compare to past M&A re-pivot windows?

The 2026 SaaS M&A re-pivot window is structurally similar to three prior windows -- post-2008 software, post-2015 ad-tech, and post-2022 fintech -- but distinct in the AI-agent threat repricing trigger.

The post-2008 software window ran approximately 18-24 months and produced strategic platform tuck-ins (Oracle/Sun $7.4B, IBM/Cognos, SAP/SuccessFactors at the front end of the window, then HP/Autonomy $11.7B and Microsoft/Skype $8.5B at the back end as multiples re-expanded). The post-2015 ad-tech window was shorter (~12 months) and produced consolidation across programmatic stacks. The post-2022 fintech window produced both strategic platform tuck-ins and PE take-privates in approximately equal volume, with multiple compression that anchored deals at 6-10x revenue rather than the 15-25x prior peaks.

The 2026 SaaS window is materially deeper than the 2022 fintech window because the AI-agent threat is structural rather than cyclical, and the multiple compression is sharper (3.3x median per PitchBook Q1 2026 versus 6-10x in the 2022 fintech window). The implication: 2026 SaaS sellers should not wait for multiple-reflation; the comparable historical data does not support it inside the 12-18 month window. The right move is to execute inside the window at the available premium rather than holding for IPO multiples that may not reflate before strategic appetite fills up.

What are the most common SaaS data room mistakes I see?

Five mistakes show up repeatedly across the late-stage SaaS sell-side mandates running on Peony.

Mistake 1: Treating the data room as a file dump rather than a buyer narrative. A data room is a buyer-side reading experience. The order of folders, the document naming conventions, and the cross-references between sections all signal management discipline -- or its absence. Tier 1 sellers dump files into top-level folders with inconsistent naming. Tier 4 sellers organize the room as a buyer-side reading order: executive summary, financial overview, AI-defensibility evidence, customer detail, technical architecture, legal, HR.

Mistake 2: One generic data room for all bidder groups. Strategic acquirers and PE buyers consume different evidence. Running one generic data room that mixes both views forces every buyer to wade through irrelevant detail and dilutes the platform-fit narrative for strategics or the FCF narrative for PE. The fix: visitor groups at the data room level. One room, two segmented views, no rebuilding cost.

Mistake 3: No page-level analytics. Without page-level analytics, the sell-side advisor is flying blind on buyer engagement. Time-on-page per buyer per document is the single highest-signal indicator of bidder seriousness; download counts and login counts are not. Legacy VDR analytics typically stop at logins and downloads. Peony's per-page heatmap shows exactly which buyer reviewed which page for how long.

Mistake 4: Sensitive customer logos and pricing in screenshot-able form. If your top 10 customer list is a competitive moat and a competing-portfolio-company in a strategic acquirer's stable can screenshot it, the leak path is open. Screenshot-blocking + screenshot-attempt logging closes the leak path. Per-investor watermarks on every rendered page give you traceability if a document does leak. The block-screenshots feature ships pending in Peony.

Mistake 5: Late-tier confirmatory documents leaking into early-tier access. Multi-stage gating with NDA-per-tier is the structural fix. Stage 1 bidders see executive summary, CIM, market overview. Stage 2 bidders unlock detailed financials, key contracts, customer data after signing the second-stage NDA. Stage 3 confirmatory access (employee-level compensation, pending litigation, disclosure schedules) opens for the final bidder only. Multi-level gating means the same data room serves all three stages through permission-level controls, with a single audit trail across the entire process. The M&A data room playbook covers the gating mechanics in full.

Bottom line

The SaaS M&A re-pivot window is open, finite, and operating at the most active software-deal-value pace since 2021. Eight ≥$5B SaaS deals closed in the 60 days between February 4 and April 7, 2026: Google/Wiz $32B, Palo Alto/CyberArk $25B, Thoma Bravo/Dayforce $12.3B, IBM/Confluent $11B, Permira+Warburg/Clearwater $8.4B, ServiceNow/Armis $7.75B, and Capital One/Brex $5.15B. Median public SaaS EV/TTM-revenue is at 3.3x as of March 31, 2026 -- a 47% drop from 6.2x at year-end 2024. Zero VC-backed SaaS unicorn IPO filings have hit the market YTD 2026. The window is real and the deal-clock is running.

The 4-tier SaaS data room readiness ladder -- Tier 1 raw, Tier 2 organized, Tier 3 AI-defensible, Tier 4 auction-grade -- is the structural diagnostic for whether you achieve a Wiz-style premium or absorb a Brex-style 58% discount. Approximately 60% of late-stage SaaS unicorns sit at Tier 1 today; approximately 5% at Tier 4. The gap between Tier 2 and Tier 3 is typically 1-2x EV/revenue, which compounds to $300M-$600M of enterprise value on a $300M ARR business.

For SaaS founders, CFOs, and boards inside the window, the operational decisions are: (1) stand up a Tier 3 data room now using Peony Data Room at $52/admin/mo with page-level analytics, visitor groups, and per-investor watermarks; (2) build the AI-defensibility evidence pack (cohort retention with AI-feature attribution, training-data and model-portability documentation, pricing-architecture roadmap); (3) select the right advisor for your deal size and category fit -- bulge-bracket above $5B, branded-boutique tech specialists like Tidal Partners between $500M-$5B, generalist mid-market like Houlihan Lokey below $500M; (4) run a competitive process in Q3-Q4 2026 to land in the maximum-multiple band of the window. The cross-coast advisor map sits across our NYC, SF, LA, Boston, Miami, and Seattle guides.

The IPO window will eventually reopen. The SaaS M&A re-pivot window is open now, with named buyers and active processes. Move inside the window at the available premium rather than holding for IPO multiples that may not reflate before strategic appetite fills up.

Related Resources

- Medical device M&A data room — the QMSR-era regulatory evidence room: staging the 510(k)/QMS file so device buyers confirm instead of discover

- The Best M&A Data Rooms of 2026 — anchor playbook with folder structure, document checklist, stage-gate permissions, and the head-to-head VDR platform comparison

- Top 10 Virtual Data Room Providers (2026) — full VDR platform comparison with Datasite, Intralinks, Firmex, iDeals, and Peony scored on M&A use cases

- Virtual Data Room Cost Guide (2026) — pricing transparency analysis across legacy and modern VDR platforms

- Best M&A Advisors in NYC (2026) — Goldman, Morgan Stanley, J.P. Morgan, Evercore, BofA, Centerview, and Tidal Partners NYC office

- Best M&A Advisors in SF/Bay Area (2026) — Tidal Partners HQ, Drake Star, Vista Point, AGC, plus SF tech practices of bulge-bracket firms

- Best M&A Advisors in LA (2026) — Houlihan Lokey HQ and middle-market tech bench

- Best M&A Advisors in Boston (2026) — AGC, Aquilo for biotech-SaaS overlap exits

- Best M&A Advisors in Miami (2026) — Tidal Partners Miami office, LatAm cross-border, Brickell ecosystem

- Best M&A Advisors in Seattle (2026) — Microsoft and AWS strategic-acquirer face-time

You might also like

Aug 7, 2026

Best M&A Data Rooms (I Built One, Then Tested 6 More) in 2026

Jul 30, 2026

Best M&A Data Rooms in 2026 (10 Ranked for Deal Teams)

Jul 28, 2026

Carve-Out Data Room Guide (2026): Sale Perimeter, TSA Schedules, and Day-1 Separation