12 Best Boutique M&A Advisors in Seattle ($5M-$200M Deals 2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

Over the past year I've fielded data-room questions from cloud/SaaS founders running Microsoft / AWS strategic auctions at the OpenAI-Statsig $1.1B archetype, biotech sponsors at Fred Hutch and the Bothell biotech corridor, aerospace-supply-chain CEOs sized for the post-Boeing-Spirit consolidation cycle, Bellevue-anchored AI talent-capture sellers (engineer-as-asset structures), and PNW generalist founder-led sellers at the Exvere / Zachary Scott / Alexander Hutton tier. Seattle sits structurally apart from every other US M&A metro: it's the only US metro where two of the world's largest enterprise software acquirers are HQ-based within 25 miles of each other (Microsoft Redmond and Amazon South Lake Union), the Pacific Northwest's anchor city for software M&A (Bothell-headquartered Corum Group runs a 36-year software-only specialty boutique with $20B+ in aggregate seller wealth), the west-coast hub for aerospace supply-chain consolidation (Boeing's $8.3B Spirit AeroSystems reacquisition closed December 8, 2025, restructuring the entire PNW aerospace supplier landscape), and the metro where the AI strategic-acquirer dynamic is sharpest in 2025-2026 -- OpenAI's $1.1 billion all-stock acquisition of Bellevue-based Statsig in September 2025 (CEO Vijaye Raji moving to OpenAI as CTO of Applications) being the most-cited recent precedent. The single hardest Seattle question -- who covers Microsoft + AWS strategic-acquirer auctions for $50-200M SaaS sellers -- breaks on sub-vertical specialty (commercial SaaS vs. software pure-play vs. aerospace supply chain vs. PNW generalist), not firm-name brand. I run Peony, a data room platform for M&A and private equity, and Seattle is one of the eight US metros (San Francisco, NYC, LA, Boston, Dallas, Chicago, Atlanta, and Houston being the others) where we see the most boutique M&A advisor deal flow on the platform. Building this Seattle guide as part of our city series -- see also our SF/Bay guide, NYC guide, LA guide, Boston guide, Dallas guide, Chicago guide, Atlanta guide, Houston guide, Washington DC guide, Philadelphia guide, and Phoenix guide -- the DC guide is the Seattle-defense-aerospace analog where the strategic-acquirer concentration is dominated by GovCon primes (Leidos, GDIT, Booz Allen, SAIC, CACI, ManTech) and Defense Industrial Base PE platforms (Veritas Capital, AE Industrial, Arlington Capital) rather than Microsoft/AWS commercial enterprise corp-dev -- the structural buyer-pool analog when the Boeing-Spirit reacquisition and PNW aerospace supplier consolidation pivots into cleared-program work.

This guide maps 12 verified Seattle-headquartered or Seattle-led boutique M&A advisory firms active in the $5M-$200M EV deal range as of May 2026. Every firm has been verified for Seattle-area presence, deal size band, and recent transaction activity. Bulge-bracket banks (Goldman Sachs Seattle, Morgan Stanley Seattle, JPMorgan Seattle) and elite-boutique upper-tier specialists are excluded by design -- their structural sweet spot is $200M+ deals, and a $25M-$200M sell-side at any of those firms is a B-team engagement. Generalist boutiques whose primary book is below $5M EV (true business-broker shops) are also excluded.

Quick answer: The best Seattle M&A advisors for $5M-$200M deals as of May 2026 are Cascadia Capital (multi-vertical anchor with Cantwell SF tech-desk extension), Corum Group (36-year software pure-play), KeyBanc Capital Markets (the legacy Pacific Crest franchise; bank-owned-boutique tier), Madison Park Group (cross-coast software specialty; NYC-HQ caveat), Zachary Scott (PNW consumer / F&B / industrial generalist), Alexander Hutton (Oaklins US-member cross-border generalist), Liberty Ridge Advisors (Exvere-alumni founder-pedigree boutique), ACT Capital Advisors (Mercer Island light-industrial), Exvere (longest-running PNW generalist), Chinook Capital Advisors (Kirkland lower-mid-market), Tullius Partners (44-year founder-led services specialty), and CLA Meridian Capital (post-April 2026 accounting + IB integrated platform). The Seattle-distinguishing decision driver is the Microsoft/AWS strategic-acquirer pool concentration -- the OpenAI-Statsig $1.1B AI talent-capture acquisition in September 2025 is the most-cited recent precedent.

TL;DR: Seattle sits at the intersection of strategic-acquirer SaaS M&A (OpenAI's $1.1B Statsig acquisition September 2025, KBCM's AtScale strategic-investment from Snowflake December 2025, KBCM's FluentStream sale to Ooma December 1 2025), software M&A pure-play (Corum Group's 36-year focus and $20B+ aggregate seller wealth), aerospace supply-chain consolidation (Boeing's $8.3B Spirit AeroSystems reacquisition closed December 8, 2025), engineering-services rollups (CLA Meridian's M/E Engineering and FA Engineering sales to Salas O'Brien 2025), industrial supply chain (Zachary Scott's Bellingham Cold Storage sale to Lineage Logistics June 2025), and PE take-privates absorbing public-market depth (Smartsheet's $8.4B take-private by Vista Equity Partners and Blackstone closed early 2025; Auth0's $6.5B sale to Okta as the watershed precedent). Greater Seattle's tech ecosystem holds approximately $90.8B in value with $33.3B in 2024 exits, implying the next 24 months will be PE-driven consolidation rather than IPO-driven. For Seattle founders selling between $5M and $200M, the right answer is almost always a Seattle specialty boutique: Cascadia Capital and Corum Group as the SaaS / software anchors; Zachary Scott, Alexander Hutton, ACT Capital Advisors, Liberty Ridge, Chinook Capital, Tullius Partners, and Exvere in the PNW Generalist band; CLA Meridian Capital for industrial / engineering with accounting integration post-April 2026; Madison Park Group as the cross-coast software specialty option (NYC-HQ caveat); and KBCM (the legacy Pacific Crest franchise) as the bank-owned-boutique-tier anchor. Below: the firms, the deal-size bands, the fees, and five recent verified Seattle-tied closes that show how the metro's market actually works.

How Did I Verify This List?

Every firm on this list passes four filters:

- Seattle-area headquarters or principal Seattle office -- Seattle, Bellevue, Bothell, Kirkland, Mercer Island, Redmond, Tacoma, or the broader Puget Sound corridor; not a satellite branch staffed by a single analyst

- Verifiable transaction record -- closed at least 5 transactions in the $5M-$200M EV range in the last 36 months, sourced from press releases, BusinessWire and PR Newswire announcements, SEC EDGAR filings, or firm transaction walls

- Active 2024-2026 deal activity -- not a legacy firm coasting on pre-2020 relationships

- Lower-middle-market core -- modal deal size in the $5M-$200M EV band; firms whose primary book is below $5M EV (true Main-Street brokers) or above $300M EV (where geography stops mattering and bulge-bracket banks dominate) are excluded

I cross-referenced firm websites against Axial's 2024-2025 Top 100 LMM Investment Bank rankings, GeekWire and Puget Sound Business Journal deal coverage, BusinessWire and PR Newswire announcements, the Washington Technology Industry Association deal coverage, and individual firm press releases for verified 2024-2026 transaction history. Where a firm claimed Seattle leadership but the senior team was actually based elsewhere, I framed the geographic caveat explicitly rather than dropping the firm. Bulge-bracket Seattle offices and elite-boutique upper-MM specialists are excluded by design -- their structural sweet spot is $200M+ deals and the $25-200M EV Seattle seller is a B-team client at those firms.

Three caveats on the Seattle specialty bench:

First, KeyBanc Capital Markets is included with explicit framing as a bank-owned-boutique-tier firm rather than a true independent. KBCM's Seattle technology team carries the legacy Pacific Crest Securities franchise (Pacific Crest founded in the 1980s, acquired by KeyCorp in July 2014, fully integrated into KBCM in 2015 -- the brand is retired but the senior-team continuity is real). The structural caveat parallels the one we applied to Cain Brothers in the Boston guide and Houlihan Lokey in the LA and NYC guides -- the firm earns a place because the senior team and franchise depth are real, but the parent-bank ownership shapes the deal-team experience.

Second, CLA Meridian Capital is included with explicit framing as a bank-owned-platform tier with accounting integration. The legacy Meridian Capital independent boutique joined CLA (CliftonLarsonAllen LLP) on April 1, 2026, now going to market as 'CLA Meridian Capital.' The integration produces accounting plus IB integrated workflow capability that pure-IB independent boutiques do not offer, at the cost of CLA-mandated review chains and conflict checks. Brian Murphy and Patrick Ringland anchor the post-integration Seattle bench.

Third, Madison Park Group is included with explicit NYC-headquartered caveat. Founder Jonathan B. Adler is NYC-based, the firm is structurally a NYC software boutique with documented Bellevue and Seattle deal presence -- not a Seattle-based firm. We include Madison Park on this list as the cross-coast software specialty option for Seattle founders comparing local versus out-of-region advisors. Pacific Crest Securities is no longer included as a standalone firm because the brand was retired in 2015 after KeyCorp's full integration into KBCM -- the Seattle-native franchise is referenced in past tense in the KBCM profile below. Vincent Stone Capital, McAdams Wright Ragen (merged into Baird in 2014), and the D.A. Davidson Seattle office (David Wright departed for Oppenheimer in August 2025) are excluded for the reasons noted.

Deqian Jia, my co-founder, adds the technical readiness lens here:

"Across the Seattle-area data rooms we host, the gap between advisors who consistently close in 6 months and those who run 12-month processes is preparation. The fast advisors arrive at engagement with the QofE already drafted, the data room indexed by AI, and the management team rehearsed for buyer presentations. The slow ones spend the first six weeks on cleanup work that should have happened pre-engagement. Seattle's structural distinguishing feature is the strategic-acquirer concentration -- Microsoft 15 minutes from downtown, Amazon 5 minutes, plus AWS strategic team and the broader Puget Sound enterprise software buyer set. When the deal turns on a Microsoft or AWS strategic call, the data room has to be ready for corp-dev diligence within 48 hours of the first scientific or product conversation, not after a 6-week tidy-up. When you're picking a Seattle advisor, ask to see a sample data room from a recent close -- not a pitch deck. The folder structure tells you everything." -- Deqian Jia, Peony co-founder

Quick Comparison Table

| Firm | Deal Size (EV) | Sectors | Fee Model | Best For |

|---|---|---|---|---|

| Cascadia Capital | $25M-$500M+ | Multi-vertical: software, F&B, healthcare, industrial, consumer, business services | Lehman + retainer | Seattle multi-vertical anchor with SF tech-desk extension |

| Corum Group | $10M-$300M | Software and IT M&A pure-play (30+ sub-categories) | Modified Lehman | Software-only specialty with 36-year focus |

| KBCM (Pacific Crest legacy) | $50M-$1B+ | Technology (SaaS, internet, communications, IT services), industrial, healthcare, fintech | Lehman + retainer | Bank-owned-boutique-tier technology anchor |

| Zachary Scott | $20M-$150M | Consumer products, F&B, industrial manufacturing, specialty distribution, business services | Lehman + retainer | Seattle generalist for consumer / F&B / industrial founder mandates |

| Alexander Hutton | $15M-$150M | Generalist mid-market with Oaklins international cross-border reach | Lehman + retainer | Cross-border PNW generalist with Oaklins US-member channel |

| Madison Park Group | $20M-$200M | Software and tech-services (NYC-HQ; documented Bellevue/Seattle deal presence) | Modified Lehman | Cross-coast software specialty for Seattle founders comparing local vs out-of-region |

| Liberty Ridge Advisors | $10M-$75M | PNW founder-led mid-market (manufacturing, distribution, services, tech) | Lehman + retainer | Exvere-alumni founder pedigree at smaller-boutique scale |

| ACT Capital Advisors | $10M-$100M | Lower-middle-market generalist with technology specialty | Lehman + retainer | Mercer Island generalist with light-industrial precision-mfg depth |

| Exvere | $10M-$100M | PNW generalist (1991-present; 150+ assignments / $3B+ closed) | Lehman + retainer | Longest-running PNW generalist boutique with low marketing profile |

| CLA Meridian Capital | $20M-$300M | Industrial, engineering, consumer, technology (accounting + IB integrated post-April 2026) | Lehman + retainer | Bank-owned-platform tier with CLA accounting integration |

| Chinook Capital Advisors | $5M-$50M | PNW lower-middle-market (industrial, services, distribution, tech services) | Lehman + retainer | Kirkland lower-mid-market for $10-30M revenue founder mandates |

| Tullius Partners | $5M-$50M | Founder-led services: pest control, security, landscape, healthcare services, water | Lehman + retainer | 40+ year specialty in founder-led services succession planning |

Why Is Seattle the M&A Capital for Strategic-Acquirer SaaS, Software Pure-Play, and Aerospace Supply-Chain Deals?

Seattle's M&A market is structurally distinct from every other US metro in five ways, and each one shows up in the deal-size bands and advisor specialty mix.

First, the Microsoft/AWS strategic-acquirer pool is the densest in any US metro. Seattle is the only city where both giants are HQ-based -- Microsoft Redmond, Amazon South Lake Union -- which produces structurally different buyer-relationship density for Seattle SaaS founders than any other metro. The OpenAI-Statsig $1.1 billion all-stock acquisition announced September 2, 2025 is the headline AI talent-capture acquisition precedent: Statsig was Bellevue-based, founder Vijaye Raji moved to OpenAI as CTO of Applications, and Statsig continued operating from Bellevue with all 155 employees. The deal both highlighted Seattle's enterprise SaaS depth and confirmed that AI hyperscalers are buying Seattle product-engineering talent at scale -- the Microsoft/AWS strategic-acquirer pool extends to the AI-hyperscaler tier (OpenAI, Anthropic, Cohere) where the buyer-side rationale is talent-capture as much as product-capture. Microsoft's strategic-tuck portfolio (Nuance Communications, GitHub, Activision Blizzard, LinkedIn historic precedents) and AWS's continued infrastructure buy-side activity create a robust strategic bid for Seattle SaaS founders evaluating $30M-$300M exits.

Second, the software M&A pure-play specialty is uniquely deep in Seattle. Bothell-headquartered Corum Group has run a software-only M&A practice continuously since 1985 -- 36+ years and $20B+ in aggregate seller wealth across 36 years of operation. No other US metro has a comparable software-only boutique with the same depth of focus. Corum's privacy-first marketing posture (the firm intentionally does not publish per-deal values, citing client confidentiality) means the firm's track record is anchored in aggregate transaction volume and Bruce Milne's published research. Milne's March 2026 Corum thought-piece included the quoted observation that 'tech M&A is thriving, deal values are up, and opportunity is everywhere' -- a reading consistent with Corum's 30+ deal annual baseline.

Third, the Boeing-Spirit AeroSystems $8.3B reacquisition closed December 8, 2025 restructures aerospace supply chain across the entire Pacific Northwest. Boeing's reacquisition of Spirit AeroSystems creates downstream M&A pressure across PNW aerospace supply chain (machined-parts shops, MRO services, composites, tier-2 and tier-3 suppliers) -- and that pressure flows through to Seattle-area boutiques like ACT Capital Advisors (Mercer Island; light-industrial precision-manufacturing depth, recent Hawkins Precision sale to TriggerTech July 2025), CLA Meridian Capital (engineering-services rollups via M/E Engineering and FA Engineering sales to Salas O'Brien), and Cascadia Capital's industrials practice. The buyer pool for Seattle aerospace suppliers is structurally deeper today than it was in 2023 because PE platforms specializing in aerospace and defense (HEICO, TransDigm, Heico Defense, Astronics, Loar Group, AAR Corp, Carlyle aerospace funds, AE Industrial Partners) have accelerated their consolidation activity.

Fourth, the PE take-private wave has absorbed Seattle's public-market software depth. Smartsheet's $8.4 billion take-private by Vista Equity Partners and Blackstone (announced September 2024 and closed early 2025) removed Seattle's largest public SaaS pure-play from the public market, alongside Auth0's earlier $6.5 billion sale to Okta as the watershed precedent. Greater Seattle tech ecosystem value sits at approximately $90.8 billion with $33.3 billion in 2024 exits per CB Insights and GeekWire deal coverage, implying the next 24 months of Seattle tech M&A will be PE-driven consolidation rather than IPO-driven. For a Seattle SaaS founder evaluating exit options, the structural reality is that the IPO path is materially narrower than at any prior point this decade.

Fifth, the Pfizer-Seagen biotech aftermath continues to ripple through the Bothell life-sciences corridor with layoffs, spinouts, and capital-pressured therapeutics founders creating sell-side activity. Pfizer's 2023 acquisition of Seagen for $43 billion was the watershed event for Seattle biotech M&A; combined with the Washington-state biotech IPO drought (1 Washington-state IPO in 2025), the default exit narrative for clinical-stage Seattle biotech has flipped to M&A-first. Seattle's biotech bench is materially smaller than Boston's Cambridge and Kendall Square corridor, but the M&A-vs-IPO pivot is structurally the same.

The structural takeaway: Seattle is the only US metro where the Microsoft/AWS strategic-acquirer pool plus the AI-hyperscaler buy side (anchored by OpenAI's recent Statsig precedent) dominates SaaS M&A at the LMM band -- and the right advisor for a Seattle SaaS sell-side is structurally different from the right advisor for a NYC, Boston, SF, LA, or Charlotte mandate -- the latter's banking-fintech and healthcare-services specialty bench has no Microsoft/AWS-equivalent hyperscaler anchor and runs a structurally distinct buyer pool. Seattle is also the metro where Boeing/Spirit reacquisition supply-chain consolidation pressure post-December 2025 and engineering-services rollup activity (CLA Meridian's 2025 Salas O'Brien deals) produce a parallel non-tech M&A surge that intersects with multiple Seattle boutiques across ACT Capital, CLA Meridian, Cascadia industrials, Liberty Ridge, and Chinook.

What Should I Look For in a Seattle M&A Advisor?

Five filters that matter more in Seattle than in other US metros:

- Strategic-acquirer relationship density -- Microsoft and AWS corp-dev teams have a different rhythm and cadence than NYC PE platform buyers. The right Seattle advisor names five recent Microsoft, Amazon, Salesforce, ServiceNow, Snowflake, or Adobe corp-dev contacts without checking notes -- and explains how each contact is best engaged structurally (warm intro vs cold reach, product-led vs financial-led framing, US-vs-international team coordination).

- Senior-banker engagement -- the Seattle LMM band ($25M-$200M EV) requires senior bankers personally on every buyer call. Boutiques like Cascadia Capital, Corum Group, Madison Park Group, Zachary Scott, Alexander Hutton, ACT Capital, and Tullius Partners run senior-banker models structurally. Bank-owned-tier firms (KBCM, CLA Meridian) sometimes delegate to VPs and analysts because the parent-bank or parent-firm cost structure spreads MD time across multiple mandates.

- Sub-vertical specialty depth -- 'PNW generalist' is not enough when your deal turns on Microsoft's specific corp-dev priorities or on a Boeing-tier aerospace supplier's customer-concentration profile. The right advisor names five recent buyers in your specific sub-vertical without having to look them up.

- Cross-coast capability when the buyer pool requires it -- if your buyer pool spans Microsoft Seattle plus Salesforce SF plus an NYC-headquartered PE platform, the right advisor has either cross-coast desk presence (Cascadia's SF tech desk via Cantwell, KBCM's national bank-owned franchise, Madison Park's NYC-HQ practice) or established relationships across coasts that the senior MD personally manages.

- Engagement-letter-term flexibility -- Seattle independents (Cascadia, Corum, Zachary Scott, Alexander Hutton, Liberty Ridge, ACT, Exvere, Chinook, Tullius) all run engagement-letter terms that can be negotiated without head-office sign-off. The bank-owned-tier firms (KBCM, CLA Meridian) structurally do not. For a Seattle founder with strong leverage on retainer credit, tail-period exclusions, and minimum-fee floors, the structural fit is usually a true independent.

For pricing comparisons across data room platforms, our pricing guide covers what Seattle specialty boutiques typically charge and how that compares to bulge-bracket alternatives. For confidentiality and watermarking specifically, Peony embeds buyer email plus exact view timestamp into every page of every CIM.

Which Seattle M&A Advisors Anchor the SaaS, Software, and Strategic-Acquirer Tech Band ($25M-$500M EV)?

For Seattle-area SaaS, software, and strategic-acquirer-bound tech founders, four firms anchor the band: Cascadia Capital (Seattle 1000 2nd Avenue; multi-vertical platform with deep tech specialty extended via the 2025 Cantwell SF-desk hire), Corum Group (Bothell; software pure-play with 36 years of focus), KeyBanc Capital Markets (700 Fifth Avenue, 49th floor; bank-owned-boutique-tier; legacy Pacific Crest Securities franchise), and Madison Park Group (NYC-HQ with documented Bellevue/Seattle deal presence; cross-coast software specialty option). The first call splits structurally on sub-vertical, deal size, and ownership-structure preferences.

1. Cascadia Capital

HQ: 1000 2nd Avenue, Suite 1200, Seattle, WA 98104 (additional offices in Silicon Valley, LA, Nashville, Atlanta, Chicago, NYC, Minneapolis) Founded: 1999 by Michael Butler and Kevin Cable Senior team: Michael Butler (Chairman & CEO; Seattle), Kevin Cable (Co-founder, Vice Chairman; Seattle), Christian Schiller (Vice Chairman, Market Development; Seattle), Jonathan Cantwell (Managing Director and Head of Technology Investment Banking; Silicon Valley; joined October 2025 from GP Bullhound where he was Partner and Head of Software and previously advised Peak on its sale to UiPath and Compendium on its sale to Oracle), Bryan Jaffe (COO of Investment Banking and Managing Director, Food, Beverage and Agribusiness; LA), Vitaliy Marchenko (Managing Director, Healthcare; Nashville), and Carle Felton (Managing Director, Capital Markets Advisory; Atlanta). Track record: $35B+ in closed M&A transaction value across firm history; 1,200+ clients Deal size sweet spot: $25M-$500M+ multi-vertical M&A Sectors: Technology and SaaS, Food and Beverage, Healthcare, Industrials, Consumer, Business Services, Real Estate, Energy and Sustainability, Financial Sponsor coverage Verified 2024-2026 transactions:

- Bouncie automotive SaaS growth recapitalization by Nova Street Partners (2025) -- Cascadia exclusive financial advisor to Bouncie

- HGS BioScience and NutriAg engagement (October 2025) -- Cascadia advisor

- Willamette Valley Meat Co. transaction (March 2025) -- Cascadia advisor

- Blue Pacific Flavors transaction (September 2025) -- Cascadia advisor

- Vertical Raise sold to Arbiter (April 2026) -- Cascadia advisor

- Modes Corwik sold to MASSiv (November 2025) -- Cascadia advisor

- Enviromatic acquired by Wind Point Partners (December 2025) -- Cascadia advisor

Distinguishing factor: Cascadia is Seattle's only multi-vertical national-tier boutique with a Seattle headquarters and seven additional offices, the deepest in-region face-time access to Microsoft Redmond and Amazon South Lake Union corp-dev teams of any boutique on this list, and the 2025 addition of Jonathan Cantwell from GP Bullhound to anchor an SF software and AI desk meaningfully extends the firm's tech specialty. Cantwell's prior advisory work on PeakAI to UiPath and Compendium to Oracle gives the senior bench direct visibility into AI-hyperscaler buyer behavior.

Best for: Seattle SaaS, food and beverage, healthcare, industrial, or consumer founders with $5M-$50M EBITDA preparing for a strategic-acquirer or PE-platform exit at the $25M-$500M+ EV band where a multi-vertical platform with a Seattle headquarters and an SF software desk is the structural fit. Best contact: Michael Butler (Chairman & CEO) for cross-vertical situations; Jonathan Cantwell for software and AI specifically; Bryan Jaffe for food, beverage and agribusiness; Kevin Cable as Co-founder and Vice Chairman across the senior bench.

2. Corum Group

HQ: 19805 N. Creek Parkway, Bothell, WA 98011 Founded: 1985 by Bruce Milne (still CEO and Chairman) Senior team: Bruce Milne (Founder, CEO, Chairman), Rob Schram, Tomoki Yasuda (research and insights), Allan Wilson (Regional VP, Pacific Northwest), plus international VPs across EMEA and APAC Track record: $20B+ aggregate seller wealth across 36+ years; longest software M&A track record of any specialist Deal size sweet spot: $10M-$300M software and IT M&A Sectors: Software and IT exclusively -- 30+ sub-categories Recent activity and thought leadership: Corum's privacy-first marketing posture means individual transaction values are intentionally not published. The firm leans on aggregate track record and Bruce Milne's published research. The March 2026 Corum thought-piece 'Private Equity Tech M&A: Growth in 2025' includes Milne's quoted observation that 'tech M&A is thriving, deal values are up, and opportunity is everywhere.' Corum's 30+ deal annual baseline is consistent across the firm's 36 years of operation.

Distinguishing factor: Corum is the longest-operating software-only M&A boutique in any US metro -- 36+ years of focus, $20B+ in aggregate seller wealth, and a privacy-first marketing posture that is itself a competitive feature for founders who want their deal terms not appearing in BusinessWire. The Bothell headquarters is a 25-minute drive from Microsoft Redmond, putting senior bankers within reasonable face-time distance of Microsoft corp-dev when the buyer pool requires it. The international VP network (EMEA and APAC) gives Corum cross-border reach into European and Asian software acquirers that Seattle-only boutiques do not match.

Best for: Seattle software and IT founders with $10M-$50M ARR preparing for a strategic acquirer where the sub-vertical specialty depth and the privacy-first deal terms matter more than multi-vertical platform breadth. Best contact: Bruce Milne (founder) for senior-engagement situations; Allan Wilson for Pacific Northwest regional outreach.

Note on track record evaluation: Avoid relying on per-deal published values for Corum -- the firm intentionally does not publish them. The right structural test is to ask Corum to walk through the engagement letter date and close date on the last three closed software deals, plus to walk through aggregate sub-vertical depth (vertical SaaS, horizontal SaaS, infrastructure software, security software, fintech software, healthtech software).

3. KeyBanc Capital Markets (the legacy Pacific Crest Securities franchise)

HQ: Cleveland (KBCM parent); Seattle office at 700 Fifth Avenue, 49th Floor, Seattle, WA 98104 History: Pacific Crest Securities was founded in the 1980s as a Seattle-native technology investment-banking franchise. KeyCorp acquired Pacific Crest in July 2014, and the firm was fully integrated into KeyBanc Capital Markets in 2015. The Pacific Crest brand was retired but the Seattle technology M&A team is the legacy anchor of KBCM Technology Group, with senior-team continuity from the Pacific Crest era. The structural framing for Seattle founders evaluating KBCM is bank-owned-boutique-tier with the Pacific Crest legacy underwriting the senior team's Seattle and Pacific Northwest tech relationships. Senior team: Timothy Monnin (Managing Director and Head of FinTech Investment Banking), Andrew Schmidt (Managing Director, Equity Research, FinTech), Sunil Abraham (added 2024-25), Matt Brischetto (Managing Director). The senior team is Seattle-anchored with broader KBCM Technology Group support nationally. Deal size sweet spot: $50M-$1B+ technology and multi-sector M&A Sectors: Technology (Software and SaaS, Internet, Communications, IT Services), Industrial, Consumer, Healthcare, FinTech, Energy Verified 2025 KBCM Technology deals:

- Hasgrove Limited / Interact employee experience software majority investment from Castik Capital (December 2025) -- KBCM advisor

- AtScale strategic investment from Snowflake (December 2025) -- KBCM advisor

- FluentStream Corp sold to Ooma, Inc. (December 1, 2025) -- KBCM advisor

Distinguishing factor: KBCM brings KeyBanc's debt capital markets, syndicated lending, and equity capital markets capability under one roof, which matters if the buyer set includes PE platforms requiring staple financing or a complex capital stack at close. The Pacific Crest legacy gives the Seattle senior team a multi-decade buyer-relationship density into the Pacific Northwest software ecosystem that pure-bulge-bracket competitors do not match. Frame KBCM as 'KeyBanc Capital Markets technology division anchored by the legacy Pacific Crest franchise' rather than 'Pacific Crest Securities' (retired since 2015) -- accuracy matters.

Best for: Seattle software, SaaS, fintech, or HCIT founders with $25M+ revenue who want a technology-specialty senior team plus a balance-sheet-capable parent. For Seattle founders specifically, KBCM is the bank-owned-boutique-tier alternative to true independents like Cascadia, Corum, or Madison Park. The trade-off is parent-bank compliance overhead on engagement-letter terms and obvious cross-sell incentives.

4. Madison Park Group

HQ: New York City (Founder Jonathan B. Adler is NYC-based per his LinkedIn and The Org leadership pages); documented Bellevue and Seattle deal presence through cross-coast travel and PNW software ecosystem relationships built over time Founded: 2004 by Jonathan B. Adler Senior team: Jonathan Adler (Founder and Managing Director); 8-10 senior team members operating from NYC primarily Deal size sweet spot: $20M-$200M software and tech-services M&A Sectors: Software, technology-enabled services, divestitures, financings Verified 2023-2025 transactions:

- DevonWay sold to Ideagen (September 2023; operations and quality management software) -- Madison Park advisor

- MCN Solutions sold to Ntracts (September 2025; compliance and workflow software) -- Madison Park advisor

Distinguishing factor: Madison Park's software-only specialty depth produces a denser buyer-pool understanding than a multi-vertical Seattle-based generalist for software-specific mandates, and the firm's NYC headquarters gives senior bankers direct access to NYC-headquartered software strategics and PE platforms that Seattle-local boutiques access primarily through cross-coast travel or video. The trade-off is geography: a Seattle or Bellevue founder evaluating Madison Park is structurally choosing cross-coast software specialty over Seattle-local face-time access to Microsoft Redmond and Amazon South Lake Union corp-dev teams.

Best for: Seattle and Bellevue software founders specifically comparing local versus out-of-region advisors who want a software-only specialty boutique with NYC-headquartered senior team and cross-coast travel for PNW deal coverage. Best contact: Jonathan Adler (founder).

Critical framing note: Madison Park Group is NYC-headquartered, not Seattle-based. The firm has documented Bellevue and Seattle deal presence through cross-coast travel and PNW software ecosystem relationships, but the senior team operates from NYC primarily. Seattle founders should evaluate Madison Park on the structural choice of cross-coast software specialty, with the geographic caveat made explicit rather than buried.

Which Seattle M&A Advisors Anchor the PNW Generalist Band ($5M-$150M EV)?

For Seattle-area generalist sellers in consumer products, food and beverage, industrial, business services, manufacturing, and multi-sector founder-led situations, six firms anchor the LMM band: Zachary Scott (Seattle, Lower Queen Anne; founded 1991), Alexander Hutton (Seattle, Westlake; founded 1986; Oaklins US member), Liberty Ridge Advisors (Seattle, Belltown; founded around 2014 by Exvere alumni), ACT Capital Advisors (Mercer Island; founded 1986), Exvere (downtown Seattle; founded 1991; 30+ years of PNW practice), and Chinook Capital Advisors (Kirkland, Carillon Point; founded 2017). The first call breaks on size, sub-vertical, founder-pedigree preferences, and cross-border reach.

5. Zachary Scott

HQ: 600 University Street, Suite 1300, Seattle, WA 98101 (Lower Queen Anne metro) Founded: 1991 by Jay Hanneman and Tom Working Senior team: Jay Hanneman (Co-founder, Chairman), Tom Working (Co-founder), Liz Brown, Ben Brockman Deal size sweet spot: $20M-$150M generalist middle-market M&A Sectors: Consumer Products, Food and Beverage, Industrial Manufacturing, Specialty Distribution, Business Services Verified 2025 transactions:

- Bellingham Cold Storage sold to Lineage Logistics (June 2025) -- Zachary Scott advisor; significant PNW industrial-services consolidation deal

- Multiple sell-side mandates in PNW family-owned and founder-owned consumer and industrial brackets (firm transaction wall at zacharyscott.com)

Distinguishing factor: Zachary Scott is one of the longest-operating Seattle-headquartered consumer and industrial generalist boutiques with 34 years of continuous PNW M&A practice and a verified 2025 close in PNW industrial-services consolidation (Bellingham Cold Storage to Lineage Logistics in June 2025). The firm's structural focus on PNW family-owned and founder-owned consumer, F&B, and industrial businesses means every banker on staff has direct visibility into which regional consolidators, PE platforms, and strategic acquirers are filling pipeline gaps in the PNW middle market.

Best for: PNW family-owned and founder-owned consumer, food and beverage, industrial, or business-services sellers with $5M-$25M EBITDA preparing for a strategic acquirer or PE-platform exit at the $20M-$150M EV band. Best contact: Jay Hanneman (Co-founder, Chairman) or Tom Working (Co-founder).

6. Alexander Hutton

HQ: 1700 Seventh Avenue, Suite 2100, Seattle, WA 98101 (Westlake metro) Founded: 1986 Closed transactions: 220+ Sectors: Generalist mid-market -- distribution, manufacturing, consumer, healthcare services, technology services Network: Oaklins United States member, providing cross-border deal access through Oaklins' 850+ professional network across 45 countries Recent activity: 18 deals tracked via Tracxn as of September 2025; the Oaklins channel produces cross-border M&A flow that Seattle-only boutiques without an international network do not access. Specific 2025 deal closes are limited in public reporting; the firm's 220+ closed transactions across 39 years of practice anchor the senior bench.

Distinguishing factor: Alexander Hutton is the Seattle generalist with the deepest cross-border reach because of the Oaklins US membership. For Seattle founders whose buyer pool includes Asian, European, or Canadian acquirers, the Oaklins network provides structural access to international corp-dev teams that domestic-only PNW boutiques do not match. The 220+ closed transactions across 39 years of PNW practice anchor the senior bench across multiple sub-verticals (distribution, manufacturing, consumer, healthcare services, technology services).

Best for: PNW family-owned and founder-owned generalist sellers with $5M-$15M EBITDA preparing for a strategic acquirer or PE-platform exit at the $15M-$150M EV band -- particularly where the buyer pool includes international acquirers requiring Oaklins network access. Best contact: senior team via firm directory.

7. Liberty Ridge Advisors

HQ: Seattle (Belltown / 2nd Avenue corridor) Founded: Around 2014 by Leif Johnson (formerly nine-year Managing Director at Exvere) and Michael Bennett (Exvere alum) Senior team: Leif Johnson (Co-founder), Michael Bennett (Co-founder) Deal size sweet spot: $10M-$75M lower-middle-market generalist M&A Sectors: Lower middle market generalist -- manufacturing, distribution, services, technology Verified 2024-2025 transactions:

- Silicon Forest Electronics sale to IIB (2021) -- Liberty Ridge advisor

- IDAX sold to Helix (2025) -- Liberty Ridge advisor

Distinguishing factor: Liberty Ridge is the structural choice for PNW founders who specifically want the Exvere-alumni founder pedigree applied to a smaller-boutique team. Leif Johnson's nine years as Managing Director at Exvere built a multi-decade Seattle generalist track record, and the founder-led structure at Liberty Ridge means senior MDs personally run every engagement. The smaller scale (compared to Cascadia or Alexander Hutton) is structurally aligned with $10M-$50M EV mandates where senior-banker time allocation is the primary structural input.

Best for: PNW founder-owned generalist sellers with $3M-$15M EBITDA preparing for a strategic acquirer or PE-platform exit at the $10M-$75M EV band where senior-MD time allocation matters more than multi-vertical breadth. Best contact: Leif Johnson (Co-founder) for senior-MD direct engagement.

8. ACT Capital Advisors

HQ: 7900 SE 28th Street, Suite 412, Mercer Island, WA 98040 Founded: 1986 Senior team: Robert Hild (Chairman and CEO) anchors the senior bench. The firm's leadership page at actcapitaladvisors.com lists the broader senior team. Deal size sweet spot: $10M-$100M lower-middle-market generalist with technology specialty Sectors: Lower-middle-market generalist with technology specialty layer -- manufacturing, distribution, services, healthcare services, light-industrial precision manufacturing Verified 2025 transactions:

- Hawkins Precision sold to TriggerTech (July 2025) -- ACT Capital advisor; light-industrial precision-manufacturing close

- Derotic sold to Amerit (September 2025) -- ACT Capital advisor

- Green Clean Commercial general advisory engagement (2026) -- ACT Capital advisor

Distinguishing factor: ACT Capital is the Mercer Island-headquartered lower-middle-market generalist with 39 years of continuous practice and a technology-specialty layer that pure-generalist PNW boutiques do not carry. Robert Hild (Chairman and CEO) anchors the senior bench across the lower-middle-market mandate book. The Mercer Island location is convenient for Eastside-PNW founders (Bellevue, Kirkland, Redmond, Issaquah) who prefer not to commute downtown for engagement meetings. The verified 2025 closes (Hawkins Precision in July 2025, Derotic in September 2025) demonstrate the firm's structural reach into PE-platform and strategic-acquirer buyer pools at the lower-middle-market band.

Best for: PNW founder-owned and family-owned manufacturing, distribution, services, healthcare-services, or light-industrial precision-manufacturing sellers with $3M-$15M EBITDA preparing for a strategic-acquirer or PE-platform exit at the $10M-$100M EV band. Best contact: Robert Hild (Chairman and CEO). Seattle aerospace-supplier, DOD-tier, or cleared-program founders whose buyer pool extends to GovCon strategics (Leidos, GDIT, SAIC, Booz Allen, CACI) and Defense Industrial Base PE platforms (Veritas Capital, AE Industrial, Arlington Capital) should also evaluate the DC ADG bench -- Houlihan Lokey ADG, KippsDeSanto, and Renaissance Strategic Advisors carry the senior-banker depth ACT Capital and Cascadia structurally do not specialize in for cleared-deal handling.

Critical framing note: ACT Capital Advisors is anchored by Robert Hild as Chairman and CEO -- not David Atterbury. David Atterbury is associated with Whetstone Capital Advisors, a different firm.

9. Exvere

HQ: Downtown Seattle Founded: 1991 Track record: 150+ assignments and $3B+ in aggregate transaction value across 30+ years of PNW middle-market practice Sectors: PNW generalist middle-market; sub-vertical depth detailed at exvere.com Recent activity: Public deal-list disclosure is limited because Exvere does not heavily PR each close. The notable alumni network includes the founders of Liberty Ridge Advisors (Leif Johnson, Michael Bennett), demonstrating the senior-bench depth Exvere has produced over time.

Distinguishing factor: Exvere is the longest-operating PNW generalist boutique with 30+ years of continuous Seattle-area middle-market practice and a low-profile marketing posture that itself appeals to founders who prefer not to see their deal terms in BusinessWire. The 150+ assignments and $3B+ aggregate transaction value across the firm's history, combined with the alumni network producing Liberty Ridge Advisors and other Seattle-area boutiques, anchors a structural depth that newer firms cannot replicate.

Best for: PNW founder-owned generalist sellers with $3M-$10M EBITDA preparing for a strategic-acquirer or PE-platform exit at the $10M-$100M EV band where the senior-bench depth and the low-marketing-profile structural posture are the primary inputs.

Note on founder identity: Exvere was founded in 1991 with 30+ years of PNW middle-market practice. We frame Exvere on this list around the firm's 150+ assignments and $3B+ aggregate transaction value, the alumni network that produced Liberty Ridge Advisors, and the low-marketing-profile structural posture rather than naming a specific founder.

10. Chinook Capital Advisors

HQ: 5145 Carillon Point, Building 5000, Kirkland, WA 98033 Founded: 2017 by John O'Dore and Ed Kirk Senior team: John O'Dore (Co-founder), Ed Kirk (Co-founder) Deal size sweet spot: $5M-$50M lower-middle-market PNW generalist M&A Sectors: Lower-middle-market PNW generalist -- typical client revenues $10M-$100M; sub-verticals include industrial, services, distribution, manufacturing, technology services Verified 2025 transactions:

- Sno Valley sold to ACI (January 2025) -- Chinook advisor

- Axis Surveying and Mapping sell-side advisory -- Chinook advisor

Distinguishing factor: Chinook is the Kirkland-headquartered lower-middle-market boutique built specifically for the smaller-end of PNW founder-led mandates -- typical client revenues $10M-$100M, which is below the modal client size at Cascadia, Zachary Scott, Alexander Hutton, or ACT Capital. The Carillon Point location on the Kirkland waterfront is convenient for Eastside founders who prefer not to commute downtown. The 2017 founding by John O'Dore and Ed Kirk anchors a focused senior-bench engagement model where co-founders personally run every mandate. The verified January 2025 close (Sno Valley to ACI) demonstrates the firm's PE-platform buyer-pool reach at the lower-middle-market band.

Best for: Eastside and PNW founder-owned generalist sellers with $1M-$8M EBITDA preparing for a strategic-acquirer or PE-platform exit at the $5M-$50M EV band where senior-MD time allocation and Eastside geographic convenience matter. Best contact: John O'Dore or Ed Kirk (co-founders) for senior-MD direct engagement.

Critical framing note: Chinook Capital Advisors was founded in 2017 by John O'Dore and Ed Kirk -- not by Wally Chinook or Manny Padda.

11. Tullius Partners

HQ: Seattle (Westlake / Belltown corridor) Founded: 1981 by Larry Tullius Senior team: Larry Tullius (Founder) anchors the senior bench across the firm's specialty mix Deal size sweet spot: $5M-$50M founder-led services M&A and succession planning Sectors: Pest control, security services, landscape installation and maintenance, healthcare services, bottled water, building services Track record: 70% successful close rate across 40+ year history; longest-running Seattle boutique by years-in-market Recent activity: Public deal-press is limited because the firm's value to founders is succession planning, valuation, and capital raise rather than deal-tombstone marketing. The 40+ year track record under Larry Tullius and the published 70% close rate (materially higher than typical industry close rates for sub-$20M EBITDA founder-led mandates) anchor the senior bench's structural depth in services-sector M&A.

Distinguishing factor: Tullius Partners is the longest-running Seattle-area boutique by years in market (44+ years since 1981) and the only Seattle firm with a structural specialty in founder-led services sub-sectors -- pest control, security services, landscape, healthcare services, bottled water, building services. The 70% close rate across 40+ years reflects deep buyer-pool relationships in regional consolidators, PE platforms specifically focused on services-rollup strategies, and strategic acquirers in adjacent service categories. For a Seattle founder approaching succession in any of those sub-verticals, Tullius is the structural specialty fit.

Best for: PNW founder-led services sellers with $1M-$8M EBITDA approaching succession or Boomer-retirement in pest control, security services, landscape, healthcare services, bottled water, or building services preparing for a strategic-acquirer or PE-platform exit at the $5M-$50M EV band. Best contact: Larry Tullius (Founder) for senior-MD direct engagement.

Critical framing note: Tullius Partners was founded in 1981 by Larry Tullius -- not by Phil Tullius.

Which Seattle Boutique Covers Industrial / Engineering with Accounting Integration?

For Seattle-area industrial, engineering, consumer, and technology founders where the QofE workstream is heavy and the buyer pool requires tighter financial-diligence coordination, one firm anchors the band: CLA Meridian Capital (former Meridian Capital, joined CLA on April 1, 2026).

12. CLA Meridian Capital

HQ (former): Seattle. Now: part of CLA (CliftonLarsonAllen LLP) following the April 1, 2026 integration. Goes to market as 'CLA Meridian Capital.' Founded (legacy): Meridian Capital -- the legacy independent boutique whose investment-banking practice joined CLA on April 1, 2026 Senior team post-integration: Brian Murphy (former CEO and Managing Director of Meridian; now Managing Principal of Investment Banking for CLA) and Patrick Ringland (former Meridian President) anchor the post-integration Seattle bench Track record: 203+ deals across the legacy Meridian Capital history Deal size sweet spot: $20M-$300M industrial, engineering, consumer, technology M&A Sectors: Industrial, Engineering, Consumer, Technology -- family-owned, founder-owned, entrepreneur-owned middle-market focus Verified 2025 transactions (under legacy Meridian Capital branding):

- M/E Engineering sold to Salas O'Brien (October 2025) -- legacy Meridian Capital advisor; engineering-services consolidation close

- FA Engineering sold to Salas O'Brien (February 2025) -- legacy Meridian Capital advisor; engineering-services consolidation close

Distinguishing factor: CLA Meridian Capital is the only Seattle-area boutique post-April 2026 with full integrated accounting plus IB workflow capability. CLA's national accounting and tax footprint produces structurally tighter coordination between QofE workstreams, tax due diligence, and sell-side advisory work -- which compresses the typical 8-12 week QofE window and reduces buyer-side surprise findings during diligence. The legacy Meridian Capital senior team continuity (Brian Murphy, Patrick Ringland) and 203+ deal track record anchor the post-integration Seattle bench across industrial, engineering, consumer, and technology mandates. The two 2025 Salas O'Brien deals (M/E Engineering October 2025, FA Engineering February 2025) demonstrate engineering-services consolidation depth.

Best for: Seattle and PNW family-owned, founder-owned, and entrepreneur-owned industrial, engineering, consumer, or technology sellers with $5M-$30M EBITDA preparing for a PE-platform or strategic-acquirer exit at the $20M-$300M EV band where QofE is heavy and integrated accounting plus IB workflow capability is the structural fit. Best contact: Brian Murphy (Managing Principal of Investment Banking for CLA) or Patrick Ringland.

Email migration note: Email addresses may be transitioning from @meridianib.com to @claconnect.com for senior bankers post-integration; confirm the current address before sending engagement-letter discussions.

What Recent Seattle-Area M&A Deals Show How These Advisors Actually Work?

Five recent verified Seattle-tied closes that illustrate the deal-size band, the buyer-pool composition, and the structural advantage each advisor brings.

Statsig Acquired by OpenAI (September 2, 2025; AI-Hyperscaler Strategic Precedent)

OpenAI's $1.1 billion all-stock acquisition of Bellevue-based Statsig announced September 2, 2025 is the headline AI-hyperscaler precedent for Seattle SaaS founders. Statsig was a feature-flagging and experimentation platform serving enterprise customers; OpenAI is the leading large-language-model and AI-applications provider. Statsig founder and CEO Vijaye Raji moved to OpenAI as CTO of Applications, with Statsig continuing to operate from Bellevue with all 155 employees post-close. The deal demonstrates the structural buyer-relationship dynamic that distinguishes Seattle SaaS M&A from every other US metro -- AI hyperscalers buying Seattle product-engineering talent at scale, with retention packages and strategic-integration scope built into the deal terms. For Seattle SaaS founders evaluating Cascadia Capital, Corum Group, KBCM, or Madison Park Group, the Statsig precedent is the most-cited recent data point on AI-hyperscaler buyer behavior.

Bellingham Cold Storage Sold to Lineage Logistics (June 2025; Zachary Scott)

Zachary Scott served as advisor to Bellingham Cold Storage on the June 2025 sale to Lineage Logistics. Bellingham Cold Storage is a PNW industrial-services company in cold-chain logistics; Lineage Logistics is a PE-backed cold-storage rollup platform. The deal demonstrates Zachary Scott's structural depth in PNW industrial-services consolidation and the firm's relationship density with PE-platform buyers running rollup strategies in the cold-storage and logistics sub-sector. For PNW family-owned and founder-owned industrial-services founders evaluating Zachary Scott, the Bellingham Cold Storage deal is a direct data point on how the firm's senior bench engages with PE-platform buyers during competitive sale processes.

Hawkins Precision Sold to TriggerTech (July 2025; ACT Capital Advisors)

ACT Capital Advisors served as advisor to Hawkins Precision on the July 2025 sale to TriggerTech. Hawkins Precision is a PNW light-industrial precision-manufacturing company; TriggerTech is a manufacturing-platform consolidator. The deal demonstrates ACT Capital's structural reach into the PE-platform and strategic-acquirer buyer pools at the lower-middle-market band, plus the firm's technology-specialty layer that anchors the senior bench under Robert Hild (Chairman and CEO). For PNW founders evaluating ACT Capital, the Hawkins Precision deal is a direct data point on how the firm's senior bench engages with PE-platform buyers in light-industrial precision manufacturing.

M/E Engineering and FA Engineering Sold to Salas O'Brien (2025; CLA Meridian Capital under legacy Meridian branding)

The legacy Meridian Capital served as advisor on the M/E Engineering sale to Salas O'Brien (October 2025) and the FA Engineering sale to Salas O'Brien (February 2025). Both deals are engineering-services consolidation closes where Salas O'Brien is the consolidator buyer. These deals demonstrate the engineering-services M&A depth of the senior team that now anchors CLA Meridian Capital post-April 2026 integration. Brian Murphy (former CEO and MD of Meridian, now Managing Principal of Investment Banking for CLA) and Patrick Ringland (former Meridian President) ran the engagements, demonstrating the senior-team continuity that carries forward into the CLA-integrated practice.

Sno Valley Sold to ACI (January 2025; Chinook Capital Advisors)

Chinook Capital Advisors served as advisor to Sno Valley on the January 2025 sale to ACI. The deal demonstrates Chinook's structural reach into PE-platform buyer pools at the lower end of the PNW middle-market band ($10M-$100M typical client revenue). John O'Dore and Ed Kirk (co-founders) ran the engagement, consistent with the firm's senior-MD-led process design. For Eastside and PNW founders with $1M-$8M EBITDA evaluating Chinook, the Sno Valley deal is a direct data point on how the firm's co-founders engage with PE-platform buyers during competitive sale processes at the smaller end of the LMM band.

How Do I Pick the Right Seattle M&A Advisor for My Situation?

The decision framework is a four-axis decision matrix: deal size + sub-vertical + ownership structure + buyer-pool geography. For Seattle specifically, the Microsoft/AWS strategic-acquirer pool concentration shifts the buyer-pool-geography axis weight higher than in any other US metro -- a $50M Seattle SaaS founder with deep Microsoft corp-dev relationships almost always picks a different advisor than a $50M NYC financial-services founder or a $50M Boston biotech founder where the buyer-pool is Sanofi, Eli Lilly, and Pfizer rather than Microsoft and Amazon.

For $25M-$500M EV multi-vertical Seattle SaaS, F&B, healthcare, industrial, or consumer with strategic-acquirer-tier buyer pool needing in-region face-time access to Microsoft Redmond and Amazon South Lake Union → Cascadia Capital is the Seattle-default first-call with $35B+ in lifetime closes, seven additional offices, and the 2025 Cantwell SF tech-desk extension.

For $10M-$300M EV software and IT M&A where 36-year sub-vertical specialty depth and privacy-first marketing posture matter → Corum Group runs the Bothell-headquartered software pure-play with $20B+ aggregate seller wealth and Bruce Milne's continuous senior leadership since 1985.

For $50M-$1B+ EV technology and multi-sector M&A where balance-sheet financing capability and the legacy Pacific Crest research-bench depth matter → KeyBanc Capital Markets (KBCM) brings the bank-owned-boutique-tier with the Pacific Crest legacy underwriting Seattle and Pacific Northwest tech relationships.

For $20M-$200M EV software and tech-services M&A where cross-coast specialty boutique with NYC-headquartered senior team is the structural fit → Madison Park Group is the cross-coast software specialty option for Seattle and Bellevue founders comparing local versus out-of-region advisors.

For $20M-$150M EV PNW family-owned and founder-owned consumer products, F&B, industrial, or business-services sellers → Zachary Scott runs Seattle's longest-tenured consumer / F&B / industrial generalist boutique with 34 years of continuous PNW practice and the verified June 2025 Bellingham Cold Storage close.

For $15M-$150M EV PNW generalist mandates with cross-border Asian, European, or Canadian acquirer buyer-pool needs → Alexander Hutton runs the Seattle generalist with the deepest cross-border reach via Oaklins United States membership and the 850+ professional network across 45 countries.

For $10M-$75M EV PNW founder-owned generalist sellers wanting Exvere-alumni founder pedigree at smaller-boutique scale → Liberty Ridge Advisors runs the Belltown founder-led boutique with co-founders Leif Johnson and Michael Bennett.

For $10M-$100M EV PNW lower-middle-market generalist with technology-specialty layer and Eastside / Mercer Island geographic preference → ACT Capital Advisors runs the Mercer Island generalist anchored by Robert Hild (Chairman and CEO) with verified 2025 closes (Hawkins Precision in July 2025, Derotic in September 2025).

For $10M-$100M EV PNW generalist sellers wanting longest-running PNW boutique with low-marketing-profile structural posture → Exvere runs the downtown Seattle generalist with 150+ assignments and $3B+ aggregate transaction value across 30+ years.

For $20M-$300M EV industrial, engineering, consumer, or technology sellers where QofE is heavy and integrated accounting plus IB workflow capability matters → CLA Meridian Capital is the only Seattle-area firm post-April 2026 with full CLA accounting integration anchored by Brian Murphy and Patrick Ringland.

For $5M-$50M EV PNW lower-middle-market generalist sellers at the smaller end of the LMM band with Eastside / Kirkland geographic preference → Chinook Capital Advisors runs the Carillon Point boutique founded 2017 by John O'Dore and Ed Kirk.

For $5M-$50M EV PNW founder-led services sellers in pest control, security services, landscape, healthcare services, bottled water, or building services approaching succession or Boomer-retirement → Tullius Partners is the 44-year specialty boutique anchored by Larry Tullius with a 70% close rate across the firm's history.

For framework comparisons with related frameworks, see our M&A data room guide, which covers what Seattle advisors expect to see by week 1 of the engagement.

What Data Room Capabilities Do Seattle Advisors Demand?

Seattle advisors demand five data room capabilities because the Microsoft/AWS strategic-acquirer pool concentration compresses the corp-dev diligence timeline below 48 hours: click-through NDA gates, per-investor watermarks, page-level analytics, visitor-group buyer tiering, and screenshot protection. When Microsoft and AWS corp-dev teams are 15-25 minutes from the seller's office, the data room has to be ready for corp-dev diligence within 48 hours of the first scientific or product conversation, not after a 6-week tidy-up. The Seattle advisors who run consistently confidential and fast processes all rely on the same five capabilities -- the same five that Boston biotech advisors demand for Cambridge-leak-prone confidentiality and NYC PE deal teams demand for sponsor-side parallel-process rigor:

- Click-through NDA gates -- buyer-side users sign the NDA inside the data room before viewing any content, eliminating the email-attachment-NDA chain-of-custody problem that lets CIMs leak before signature; particularly critical for Seattle SaaS where leaked CIMs translate into competitor product-strategy reverse-engineering within 72 hours

- Per-investor watermarks -- buyer email plus exact view timestamp embedded into every page so a leaked CIM has a forensic audit trail back to the specific buyer; the structural answer to Seattle's overlapping-investor and overlapping-engineering-talent confidentiality risk

- Page-level analytics -- senior banker can see at a glance which buyer is reading the financials versus which is reading the legal section once and skipping the rest, which informs the LOI follow-up sequence and identifies which Microsoft, Amazon, or strategic team is genuinely engaged versus just taking the pitch meeting

- Visitor groups for buyer tiering -- strategic acquirers, PE platform buyers, and competitor-adjacent buyers each see different document sets, with competitor-tier buyers blocked from product-strategy tables, customer-concentration tables, or unit-economics detail until LOI signed

- Screenshot protection -- blocks and logs unauthorized capture attempts on Business plan rooms, deterring competitors from harvesting customer lists, product-roadmap pages, and financial tables during data room visits

For Seattle SaaS specifically, the auto-indexing feature compresses Weeks 1-3 of the engagement timeline because Microsoft, Amazon, and other strategic buyers can search across the entire data room instead of chasing folder paths -- a meaningful benefit when the data room contains thousands of pages of customer agreements, product documentation, and engineering artifacts. For solutions specifically targeted at M&A and private equity buyer-side workflows, Peony's M&A solution and PE solution pages cover the structural data room patterns most Seattle advisors use. Custom domain means the data room URL reads as the seller's domain rather than a vendor URL -- a small detail that matters when strategic acquirers' corp-dev teams forward links internally. Smart Q&A centralizes buyer questions so the senior banker (or CFO) can answer once and surface the answer to every approved buyer rather than repeating the same answer across 15 separate email threads.

How Do Seattle M&A Advisor Fees Work?

Seattle-area specialty boutiques typically run a Lehman-style success fee scale plus retainer:

| Deal Size (EV) | Typical Retainer | Lehman Success Fee Math (Standard 5/4/3/2/1 Scale) | Modified Fee Alternative | Typical Tail |

|---|---|---|---|---|

| $5M-$15M | $25K-$50K | 5/4/3/2/1 = roughly 5-8 percent blended | Flat 4-5 percent on small deals | 12-24 months |

| $15M-$30M | $50K-$75K | 5/4/3/2/1 = roughly 2.5-4 percent blended | 1.5-2 percent flat alternative on $20M-$30M | 12-24 months |

| $30M-$50M | $75K-$100K | 5/4/3/2/1 = roughly 1.7-2.5 percent blended | 1.5 percent flat alternative; tiered with flat tail above $20M | 12-24 months |

| $50M-$100M | $100K-$150K | 5/4/3/2/1 = roughly 1.2-1.7 percent blended | Tiered structure with flat tail above $50M | 12-24 months |

| $100M-$200M | $150K | 5/4/3/2/1 = roughly 1.0-1.2 percent blended | Modified Lehman with higher first-tier and flat tail | 12-24 months |

Sub-vertical-specialty firms (Corum Group on software, Cascadia Capital on multi-vertical with software desk, Madison Park Group on software and tech-services, Tullius Partners on founder-led services) sometimes charge at the higher end of the band given the buyer-relationship density they bring. Bank-owned-tier firms (KBCM, CLA Meridian) typically run standard Lehman with a higher retainer floor ($75K-$150K) given the parent-bank or parent-firm cost structure. Pure generalist boutiques (Zachary Scott, Alexander Hutton, Liberty Ridge, ACT Capital, Exvere, Chinook) typically run standard Lehman without the specialty premium. Bulge-bracket Seattle offices (Goldman Sachs, Morgan Stanley, JPMorgan) at $30M EV typically demand $250K+ retainer plus a $750K+ minimum success fee floor regardless of deal value -- structurally inefficient at the LMM band.

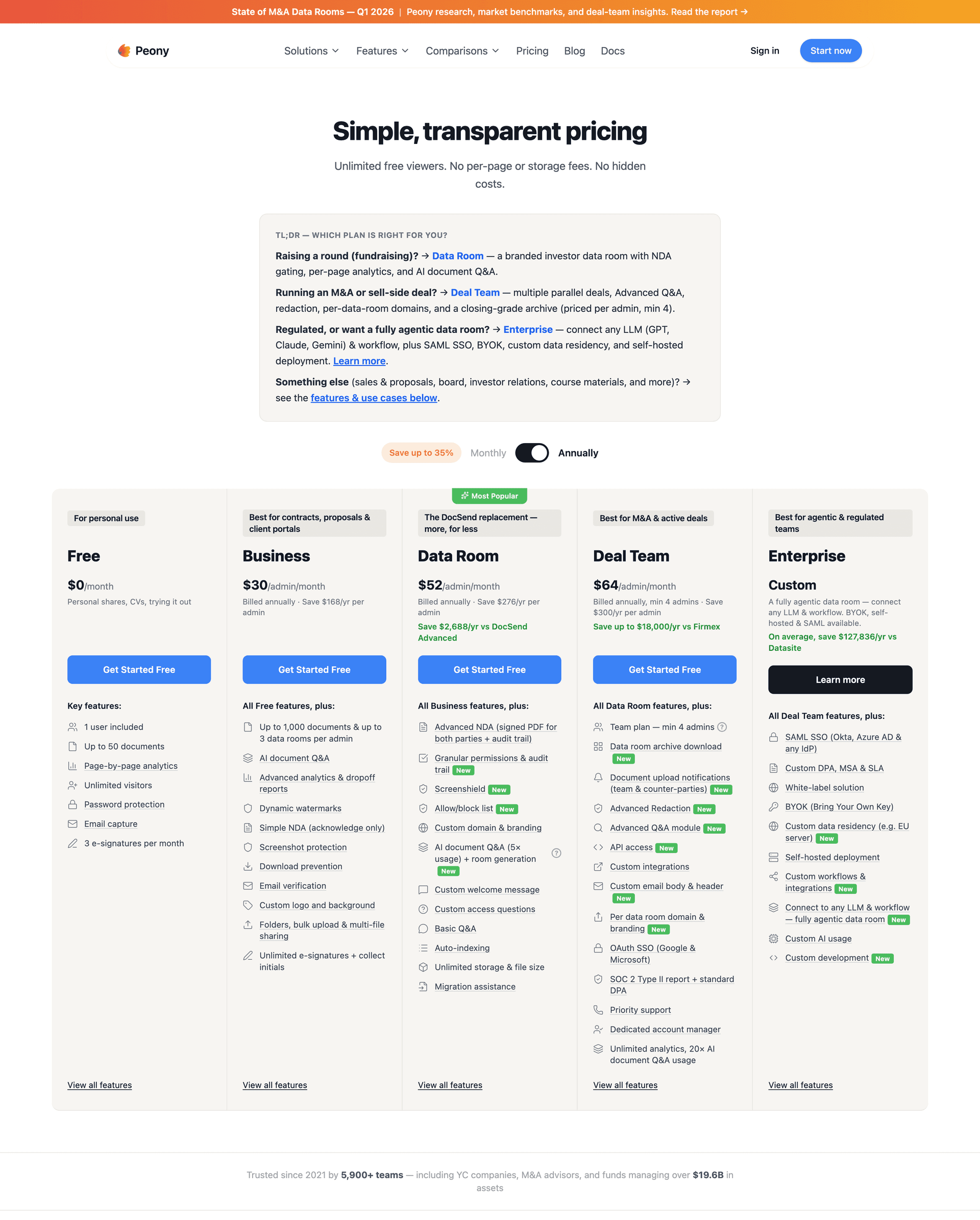

For full pricing detail on data room costs, Peony Business at $30 per admin per month replaces the $15K-$50K per-deal data room cost most Seattle boutiques used to bill as expense reimbursement -- the platform fee shows up in the seller's expense column rather than the advisor's pass-through column, which the senior banker can use as an argument for a slightly lower success-fee floor. Business covers the core data-room functionality (NDA gates, basic analytics) for deal teams who do not need the full enterprise-tier feature set, while Peony Data Room at $52 per admin per month adds dynamic watermarks, unlimited storage with no per-file cap, unlimited rooms, custom domain, and granular per-file permissions.

Seattle M&A Advisor FAQs

What's the difference between a Seattle M&A boutique and a bulge-bracket bank like Goldman or Morgan Stanley for a $50M deal?

For Seattle-area sellers between $5M and $200M EV, the difference is structural: bulge-bracket banks are built around $200M+ engagements where senior MD time is allocated to the largest fee-payers, while specialty boutiques are built around the lower-middle-market band where senior bankers run buyer calls personally. A $50M EV Seattle SaaS sell-side at Goldman or Morgan Stanley is staffed by a VP-and-analyst team, with the sector MD showing up for the pitch and the management presentation, then disappearing -- everything else routes through staff. Most Seattle boutiques compete for the $25M-$200M EV band by structural design with senior-banker-led models, sub-vertical specialty depth, and minimum-fee floors aligned to the LMM band. Two firms operate as bank-owned-tier platforms (KBCM as the legacy Pacific Crest franchise; CLA Meridian as a CLA accounting-firm-owned IB practice post-April 2026). The structural test: ask any bulge-bracket pitcher to commit in writing to which senior banker (MD or above) will be on every buyer call. Most won't.

Cascadia Capital vs Corum Group for a $50M Seattle SaaS exit -- how do I choose?

Cascadia Capital is multi-vertical with a Seattle headquarters and a 2025 Cantwell SF tech-desk extension; Corum Group is software-only with 36 years of focus and a privacy-first marketing posture. For a $30M-$80M ARR Seattle SaaS where the buyer pool is concentrated among software strategics and PE platforms, Corum's single-vertical depth produces a denser buyer outreach. For a $50M-$300M Seattle SaaS where the buyer pool spans Microsoft, Amazon, Google, Salesforce strategics plus PE platforms plus possible international acquirers, Cascadia's multi-vertical platform plus Cantwell's SF tech-desk reach produces broader buyer coverage. The structural test: ask each pitching firm to name five recent buyers in your specific sub-vertical without checking their notes.

Should I sell my Seattle SaaS to Microsoft or AWS as a strategic acquirer, or run a broader process?

This is the Seattle-distinguishing exit question of 2025-2026 because Seattle is the only US metro where two of the world's largest enterprise software acquirers are HQ-based within 25 miles of each other. The OpenAI-Statsig $1.1 billion all-stock acquisition announced September 2, 2025 is the most-cited recent precedent: Statsig founder and CEO Vijaye Raji moved to OpenAI as CTO of Applications, with Statsig continuing to operate from Bellevue. Three structural inputs decide: buyer-relationship density (if Microsoft M12 or AWS strategic team has been in active product-integration dialogue for 6+ months, the strategic call shapes the floor and a broader process risks burning the relationship), talent-retention structure (multi-year retention tied to founding-team employment can produce a different realized purchase price than the headline number), and regulatory backdrop (FTC and DOJ scrutiny on large-tech acquisitions has increased close-timeline risk for SaaS targets above $500M EV). The structural recommendation: hire a senior banker before you take the second strategic call, and have the banker run a 4-6 firm parallel outreach to build deal-floor optionality.

How does the Boeing-Spirit AeroSystems reacquisition affect Seattle aerospace supply-chain founders considering a sale?

Boeing's $8.3 billion reacquisition of Spirit AeroSystems closed on December 8, 2025 and reorders the M&A pressure across the entire Pacific Northwest aerospace supply chain. For a Seattle-area machined-parts shop, composites manufacturer, MRO services firm, or tier-2/tier-3 supplier with $15M-$100M revenue, four downstream effects shape exit timing: consolidation pressure pushes downstream (single-customer Boeing concentration above 60% structurally lowers valuations); PE platform M&A activity in aerospace and defense (HEICO, TransDigm, Astronics, Loar Group, AAR Corp, Carlyle aerospace funds, AE Industrial Partners) has accelerated through 2025; non-Boeing aerospace primes (Lockheed, RTX, Northrop, GE Aerospace) and large tier-1 suppliers (Howmet Aerospace, TransDigm, HEICO) have increased buy-side activity to lock in alternative supplier capacity; and timing matters -- founders running a process in 2026 capture the consolidation-arbitrage premium while it's at peak. Seattle advisors with aerospace-supply-chain depth include ACT Capital (Mercer Island; light-industrial precision-manufacturing), CLA Meridian (engineering-services rollup depth via Salas O'Brien deals), and Cascadia Capital industrials.

What's a reasonable success fee for a $50M Seattle M&A sell-side mandate?

Seattle M&A advisors at the $50M EV band typically charge 1.5-2.5 percent blended success fee plus a $50K-$150K retainer credited against the success fee at close, with tail period of 12-24 months standard. The standard Lehman scale (5/4/3/2/1) on $50M produces approximately $700K of success fees -- about 1.4 percent blended. Specialty firms with deeper buyer relationships sometimes charge at the higher end. Bank-owned-tier firms (KBCM, CLA Meridian) typically run standard Lehman with a higher retainer floor. Bulge-bracket Seattle offices at this deal size typically demand a $250K+ retainer plus a $750K minimum success fee floor regardless of deal value -- structurally inefficient at the $50M EV band.

How do I evaluate a Seattle boutique M&A advisor's 2024-2025 track record?

Verify the track record through three independent sources: the firm's transaction wall cross-checked against PR Newswire, BusinessWire, GeekWire, Puget Sound Business Journal, and the buyer's own SEC 8-K filings; Axial league tables, CB Insights and GeekWire deal coverage, and Washington Technology Industry Association data; and direct seller references for two CEOs from closes in the last 12 months. The single highest-signal question: ask for the engagement letter date and close date on the last three closed deals -- 6-9 months is typical, 12+ months a warning sign. Seattle advisors with verified 2025 closes include Cascadia Capital (multiple multi-vertical closes including Bouncie growth recap and Vertical Raise to Arbiter April 2026), KBCM (AtScale to Snowflake December 2025, FluentStream to Ooma December 1 2025, Hasgrove to Castik December 2025), Zachary Scott (Bellingham Cold Storage to Lineage Logistics June 2025), ACT Capital (Hawkins Precision to TriggerTech July 2025, Derotic to Amerit September 2025), CLA Meridian under legacy Meridian branding (M/E Engineering to Salas O'Brien October 2025, FA Engineering to Salas O'Brien February 2025), and Chinook Capital (Sno Valley to ACI January 2025). For Corum Group, the privacy-first marketing posture means individual deal verification is best done through the firm directly rather than public sources.

Should I hire a Seattle boutique or KBCM/Pacific Crest for a $100M tech mandate with public-market overlap?

For a $100M Seattle tech mandate with public-market overlap, the choice between a Seattle independent (Cascadia, Corum, Madison Park) and KBCM (the legacy Pacific Crest franchise) breaks on three factors: balance-sheet need, public-equity buyer-pool overlap, and senior-banker autonomy. KBCM brings KeyBanc's debt capital markets, syndicated lending, and equity capital markets capability under one roof -- relevant if the buyer set includes PE platforms requiring staple financing. The cost is comms protocol: KeyBanc-mandated review chains and Fortune-500 compliance overhead can slow the senior banker's response cycle. By contrast, Cascadia, Corum, and Madison Park all run pure independent boutiques with no parent-bank approval layer. For a $100M Seattle SaaS with no balance-sheet financing dependency and a strategic-acquirer-only buyer pool, the independent boutique is structurally better. For a $100M-$500M Seattle SaaS with a PE platform in the buyer set or where the buyer pool overlaps with the public-equity research universe KBCM covers (former Pacific Crest research analysts now staffing KBCM's equity-research bench), KBCM's parent-bank capability earns its tier.

Madison Park Group is NYC-headquartered -- should I still hire them for a Seattle software exit?

Madison Park Group is a NYC-headquartered software and tech-services M&A boutique with documented Bellevue and Seattle deal presence -- not a Seattle-based firm. For a Seattle software founder evaluating Madison Park, the structural choice depends on three inputs: sub-vertical specialty depth (Madison Park's software-only focus produces a denser buyer-pool understanding than a multi-vertical Seattle-based generalist), senior-MD time allocation (Seattle engagements with NYC-headquartered firms require either Seattle visits scheduled in advance or video calls), and regional buyer-relationship density (if your buyer pool includes Microsoft and AWS strategic teams primarily, a Seattle-based firm has structurally higher in-region face-time access). The structural test: ask Madison Park to walk through the last five Seattle and Bellevue deals where the senior MD was personally on every buyer call. Three or more of five and the cross-coast practice has the in-region density to compete with Seattle alternatives. Recent verified transactions include DevonWay sold to Ideagen (September 2023; operations and quality management software) and MCN Solutions sold to Ntracts in September 2025 (compliance and workflow software).

Should I sell my Bothell biotech now or wait for the IPO market to reopen post-Pfizer/Seagen?

For a Bothell or Bellevue biotech founder, the M&A-now-versus-IPO-later decision is sharper than in any prior cycle because the Washington-state biotech IPO market is essentially closed (1 Washington-state IPO in 2025) and the Pfizer-Seagen aftermath continues to ripple through the Bothell life-sciences corridor with layoffs, spinouts, and capital-pressured therapeutics founders creating sustained sell-side activity. Five structural inputs decide: cash runway (18-24 months extends the IPO option; 9-12 months pushes toward a sale), strategic-buyer pipeline interest (Eli Lilly, Pfizer, Sanofi, Novartis, Merck, Bristol-Myers Squibb continue to fill pipeline gaps via M&A), clinical-data inflection point timing, the Bothell talent-retention dynamic (post-Seagen layoffs produce a stronger local clinical-development talent pool available to acquirers), and lab real-estate cost structure. The structural recommendation: hire the same advisor for both options and ask them to model the M&A outcome at three valuation breakpoints alongside the IPO scenario at two pricing breakpoints. For Seattle-area healthcare and life-sciences mandates specifically, Cascadia Capital's healthcare-services bench (Felton in Atlanta with Seattle senior support), ACT Capital, and cross-coast Boston biotech specialists (Provident Healthcare Partners for healthcare services, Outcome Capital for medtech, Aquilo Partners for biopharma) are the structural alternatives.

How does CLA Meridian Capital's April 2026 integration with CLA affect deal-team experience for Seattle founders?

CLA Meridian Capital is the Seattle-based Meridian Capital investment-banking practice that joined CLA on April 1, 2026, now going to market as 'CLA Meridian Capital.' The integration creates three deal-team experience differences: accounting plus IB integrated workflow (CLA's national accounting and tax footprint produces tighter coordination between QofE workstreams, tax due diligence, and sell-side advisory work, compressing the typical 8-12 week QofE window); senior-team continuity (Brian Murphy, former CEO of Meridian, now Managing Principal of Investment Banking for CLA; Patrick Ringland, former Meridian President -- both anchor the post-integration Seattle bench); and parent-firm comms protocol (CLA-mandated review chains around engagement-letter terms and conflict checks may add friction the legacy independent boutique did not carry). The trade-off mirrors Capstone Partners' Huntington Bancshares ownership in Boston -- structural buyer-pool reach extension at the cost of some engagement-letter-term flexibility. For mandates where QofE is light and the buyer pool is concentrated with strategic acquirers requiring no staple financing, an independent Seattle boutique may run faster. For mandates where QofE is heavy and the buyer pool includes PE platforms requiring tighter financial-diligence coordination, CLA Meridian's integrated workflow earns its tier.

Bottom Line

For Seattle-area founders selling between $5M and $200M EV, the structural answer is almost always a sub-vertical specialty boutique built around the LMM band, not a bulge-bracket bank built around $200M+ engagements. The 12 firms covered here are the verified active 2025-2026 Seattle-area bench: Cascadia Capital and Corum Group for the SaaS / Software anchor band; KeyBanc Capital Markets (the legacy Pacific Crest franchise) for the bank-owned-boutique-tier technology anchor; Madison Park Group for the cross-coast software specialty option (NYC-HQ caveat); Zachary Scott, Alexander Hutton, Liberty Ridge Advisors, ACT Capital Advisors, Exvere, and Chinook Capital Advisors for the PNW Generalist band; Tullius Partners for the founder-led services succession-planning specialty; and CLA Meridian Capital for the bank-owned-platform tier with CLA accounting integration post-April 2026.

The structural decision tree: pick the firm whose sub-vertical specialty matches your sub-sector, whose deal-size sweet spot matches your EV band, and whose ownership structure (true-independent vs bank-owned-tier vs accounting-integrated platform) aligns with your balance-sheet-financing needs and engagement-letter-term flexibility preferences. Then ask the firm to name the specific senior banker who will personally run your process from CIM to close, and require it in writing in the engagement letter. Seattle's structural distinguishing feature -- Microsoft 15 minutes from downtown, Amazon 5 minutes, AWS strategic team and the broader Puget Sound enterprise software buyer set, plus the Boeing-Spirit aerospace supply-chain consolidation pressure post-December 2025, plus the OpenAI-Statsig $1.1B precedent in September 2025, plus the CLA Meridian April 2026 accounting-integrated platform tier -- means the right advisor pick at the right deal size band is as load-bearing as any decision in the founder's exit. And the strategic-acquirer dominance dynamic for Seattle SaaS specifically (Microsoft, Amazon, plus AI hyperscalers like OpenAI buying enterprise SaaS at scale) means the M&A path with a Seattle-local senior banker on every Microsoft, Amazon, or AWS corp-dev call is structurally more important than a cross-coast bulge-bracket alternative for $25M-$200M EV mandates.