12 Best Boutique M&A Advisors in Miami for $5M-$200M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

Over the past year I've fielded data-room questions from LatAm cross-border sellers running Brazilian / Mexican / Argentine in-country regulatory documents in parallel with US strategic-buyer diligence, migratory-family-office buyers deployed across the Brickell ecosystem (Citadel / Apollo / Blackstone Miami / Microsoft LatAm), Brickell PE associates running first-mandate sell-sides, Miami healthcare-services founders at the Bloom-Organization archetype, and Coconut Grove and Coral Gables founder-led sellers at the Cassel Salpeter / Cross Keys decision-tree fork. Miami sits structurally apart from every other US M&A metro: it's the only US metro where a record $4.7 billion in cross-border M&A involving Latin American buyers closed in 2025 (per SunBridge M&A Advisors' 2026 Miami Report), the densest US migratory family-office buyer pool (245 verified Florida-based family offices with 30+ in Miami metro per Altss Q1 2025 family office data), the anchor city for the Brickell financial-hub crystallization (Citadel/Ken Griffin's $2.5 billion HQ at 1201 Brickell Bay, plus Microsoft LatAm HQ, plus Blackstone Miami expansion, plus Apollo Brickell), and the metro where the LatAm cross-border seller pool meets the migratory family-office buyer pool at a density no other US city carries. The single hardest Miami question -- which Miami boutique runs LatAm cross-border on a $4.7B annual deal volume -- breaks on sub-vertical specialty (LatAm cross-border vs. generalist mid-market vs. healthcare-services vs. hospitality investment-sales vs. bank-owned-boutique tier), not firm-name brand. I run Peony, a data room platform for M&A and private equity, and Miami is one of the nine US metros (San Francisco, NYC, LA, Boston, Seattle, Dallas, Chicago, Atlanta, and Houston being the others) where we see the most boutique M&A advisor deal flow on the platform. Building this Miami guide as part of our city series -- see also our SF/Bay guide, NYC guide, LA guide, Boston guide, Seattle guide, Dallas guide, Chicago guide, Atlanta guide, Houston guide, Washington DC guide, Philadelphia guide, and Phoenix guide -- the DC guide covers the federal-services rollup buyer pool (KippsDeSanto, The McLean Group, Renaissance Strategic Advisors, Houlihan Lokey ADG, FOCUS Investment Banking) where the buyer set is dominated by GovCon strategics and Defense Industrial Base PE platforms rather than Miami's LatAm cross-border seller pool meeting the migratory family-office buyer pool -- the structurally distinct counterpart for Miami founders whose buyer set extends to federal-IT, cleared, or NIH-proximity targets rather than LatAm or Brickell strategic capital.

This guide maps 12 verified Miami-headquartered or Miami-led boutique M&A advisory firms (with explicit South Florida regional and NYC-HQ caveats where applicable) active in the $5M-$200M EV deal range as of May 2026. Every firm has been verified for Miami-area presence, deal size band, and recent transaction activity. Bulge-bracket banks (Goldman Sachs Miami, Morgan Stanley Miami, JPMorgan Miami) and elite-boutique upper-tier specialists are excluded by design -- their structural sweet spot is $200M+ deals, and a $25M-$200M sell-side at any of those firms is a B-team engagement. Generalist boutiques whose primary book is below $5M EV (true business-broker shops) are also excluded.

Quick answer: The best Miami M&A advisors for $5M-$200M deals as of May 2026 split across the 5-axis decision matrix: Cassel Salpeter & Co and Cross Keys Capital (generalist mid-market and South Florida regional), BroadSpan Capital, Latam Investment Banking (LatamIB), Atlantico Capital Partners, Antarctica Advisors, Vaupen Financial Advisors (LatAm cross-border specialty), Houlihan Lokey Miami, Solomon Partners Miami, Lincoln International Miami (bank-owned-boutique tier), The Bloom Organization Miami (healthcare services), and JLL Hotels & Hospitality Miami (hospitality investment-sales).

TL;DR: Miami sits at the intersection of LatAm cross-border M&A (BroadSpan Capital's Boa Praca/Wrist Ship Supply close December 19, 2024, BroadSpan's Grupo IMSA/NovaScott to Scott Bader Brazil June 2024, Atlantico Capital Partners' Grupo Exito to Grupo Calleja February 2024), generalist Miami mid-market (Cassel Salpeter's Sunbelt Health to UHS March 27, 2025, Cassel Salpeter's Nicklaus Companies $35.7M Chapter 11 sale March 9, 2026), healthcare services (The Bloom Organization Miami's Evolved Science to Formula Wellness November 2025, Bloom Miami's Royal Senior Care to Welltower April 2025), and hospitality consolidation (JLL Hotels' EAST Miami to Blackstone September 10, 2025, JLL's Diplomat Beach Resort $600M refinancing May 6, 2026). Cross-border M&A involving LatAm buyers reached a record $4.7 billion in the Miami metro in 2025 per SunBridge M&A Advisors' 2026 Miami Report. Miami metro fintech raised $1.8 billion in 2025 (30% of all Miami VC) per Refresh Miami. The Brickell financial-hub crystallization (Citadel $2.5B HQ at 1201 Brickell Bay, Microsoft LatAm HQ, Apollo Brickell, Blackstone Miami) anchors a deeper Miami buyer-side institutional footprint than at any prior point. For Miami founders selling between $5M and $200M, the right answer is almost always a Miami specialty boutique: BroadSpan, LatamIB, Atlantico, Antarctica, Vaupen (LatAm cross-border); Cassel Salpeter, Cross Keys (generalist mid-market); Houlihan Lokey, Solomon Partners, Lincoln International (bank-owned-boutique tier); The Bloom Organization Miami (healthcare services); JLL Hotels & Hospitality Miami (hospitality investment-sales). Below: the firms, deal-size bands, fees, and five recent verified Miami-tied closes that show how the metro's market actually works.

How Did I Verify This List?

Every firm on this list passes four filters:

- Miami-area headquarters or principal Miami office -- Miami, Coconut Grove, Brickell, Coral Gables, Doral, Aventura, or the broader Miami-Dade and South Florida regional corridor; Fort Lauderdale-anchored South Florida regional inclusion (Cross Keys Capital) is explicitly framed as such; not a satellite branch staffed by a single analyst

- Verifiable transaction record -- closed at least 5 transactions in the $5M-$200M EV range in the last 36 months, sourced from press releases, BusinessWire and PR Newswire announcements, SEC EDGAR filings, LatAm financial press, or firm transaction walls

- Active 2024-2026 deal activity -- not a legacy firm coasting on pre-2020 relationships

- Lower-middle-market core -- modal deal size in the $5M-$200M EV band; firms whose primary book is below $5M EV (true Main-Street brokers) or above $300M EV (where geography stops mattering and bulge-bracket banks dominate) are excluded

I cross-referenced firm websites against TTR Data's Latin American M&A reports, SunBridge M&A Advisors' 2026 Miami Report, Refresh Miami startup and venture coverage, the South Florida Business Journal, BusinessWire and PR Newswire announcements, and individual firm press releases for verified 2024-2026 transaction history. Where a firm claimed Miami leadership but the senior team was actually based elsewhere, I framed the geographic caveat explicitly rather than dropping the firm. Bulge-bracket Miami offices (Goldman Sachs, Morgan Stanley, JPMorgan, Citi, BofA) and elite-boutique upper-MM specialists are excluded by design -- their structural sweet spot is $200M+ deals and the $25-200M EV Miami seller is a B-team client at those firms.

Five caveats on the Miami specialty bench:

First, Houlihan Lokey Miami is included with explicit framing as a bank-owned-boutique-tier firm rather than a true independent. The structural caveat parallels the one we applied to Cain Brothers in the Boston guide, KBCM in the Seattle guide, and Houlihan Lokey in the LA and NYC guides -- the firm earns a place because the senior team and franchise depth are real, but the parent-firm ownership and global compliance overhead shape the deal-team experience.

Second, Solomon Partners' Miami office is NYC-headquartered (independently-run Natixis affiliate, part of Groupe BPCE). The Miami office at 3350 Virginia Street operates with documented Miami-area presence but the firm's senior bench is anchored in NYC, and engagement-letter terms reflect the parent-Natixis compliance overlay rather than pure-independent Miami flexibility. We include Solomon Partners on this list as the cross-coast bank-owned-boutique-tier option for Miami founders comparing local versus NYC-tier advisors.

Third, Cross Keys Capital's headquarters is Fort Lauderdale, not Miami (200 S Andrews Avenue, Suite 602, Fort Lauderdale, FL 33301; Chicago secondary office). We include Cross Keys on this list as the South Florida regional, Fort Lauderdale-anchored generalist option for South Florida founders comparing pure-Miami versus broader-region advisors. The firm has 20+ professionals and approximately $3 billion+ in closed transactions across its history -- founders evaluating Cross Keys should evaluate the firm on the depth and continuity of the current senior bench rather than founding-team pedigree alone.

Fourth, The Bloom Organization is a Florida-rooted boutique with HQ in Hallandale Beach, FL (30+ years of practice; 200+ closed transactions; approximately $15 billion aggregate value); the Miami office is led by Steven Weiss (MD; ex-Ardent Investors and H.I.G. Capital's Advantage U.S. Buyout Fund) with Henry Bloom, Robert Goettling, and Tyler Biscaha on the senior team. We include Bloom's Miami office on this list as the healthcare-services specialty boutique with a verified Miami-led 2025 close cadence -- not as a Miami-headquartered firm.

Fifth, JLL Hotels & Hospitality is a global firm, not a boutique. We include JLL Hotels on this list as the Miami investment-sales specialty option for hospitality sellers, framed explicitly as a global-firm Miami specialty rather than as a true mid-market boutique. The firm ranks #1 globally for hotel investment advisory with $9.2 billion in 2024 deal volume, approximately $2.4 billion Americas, 14% Americas market share, and approximately 25% global market share. Hyde Park Capital is excluded because the firm is Tampa-headquartered, not Miami; Capstone Partners is excluded because the firm is Boston-headquartered with no public Miami office verified; Stout Risius Ross is excluded because the firm is Chicago-headquartered; Allegiance Capital is excluded because the firm is Dallas-headquartered; and Eastdil Secured (Miami office at 1001 Brickell Bay; acquired by Savills on March 12, 2026 for $1.1 billion) is mentioned only as Miami hotel-sales market context, not as an M&A-advisor list entry.

Deqian Jia, my co-founder, adds the technical readiness lens here:

"Across the Miami-area data rooms we host, the gap between advisors who consistently close in 6 months and those who run 12-month processes is preparation. The fast advisors arrive at engagement with the QofE already drafted, the data room indexed by AI, and the management team rehearsed for buyer presentations. The slow ones spend the first six weeks on cleanup work that should have happened pre-engagement. Miami's structural distinguishing feature is the cross-border layer -- the same data room often hosts US-strategic-buyer documents and Brazilian-or-Mexican-or-Argentine in-country regulatory documents, and the data room has to support both English and Portuguese or Spanish reading orders, plus dual-jurisdiction tax-structuring memos. When you're picking a Miami advisor, ask to see a sample data room from a recent cross-border close -- not a pitch deck. The folder structure tells you everything." -- Deqian Jia, Peony co-founder

Quick Comparison Table

| Firm | Deal Size (EV) | Sectors | Fee Model | Best For |

|---|---|---|---|---|

| Cassel Salpeter & Co | $20M-$300M | Generalist mid-market: aerospace and defense, consumer, financial services, healthcare, technology, electronics, industrials | Lehman + retainer | Miami's 15-year generalist anchor; senior-MD-led; Coconut Grove since February 1, 2026 |

| BroadSpan Capital | $20M-$200M | LatAm and Caribbean cross-border M&A | Lehman + retainer | LatAm cross-border specialty with Brazilian, Mexican, Caribbean in-country MD bench |

| Latam Investment Banking (LatamIB) | $20M-$200M | LatAm M&A and capital raising (multi-sector) | Lehman + retainer | Pure-play LatAm boutique with Violy Byorum founder pedigree and 150+ mandates |

| Houlihan Lokey Miami | $50M-$1B+ | Financial services, REIT and mortgage finance, asset management, Capital Solutions | Lehman + retainer | Bank-owned-boutique-tier financial-services anchor |

| Lincoln International Miami | $40M-$500M | TMT (technology, media, telecom): software, fintech, consumer tech, communications | Lehman + retainer | TMT specialty with Spurrier Capital DNA and Lincoln parent's cross-coast reach |

| The Bloom Organization (Miami office) | $20M-$200M | Healthcare services: physician practices, ACOs, senior care, home health, behavioral health | Lehman + retainer | Healthcare-services specialty with verified 2025 Miami-led close cadence |

| Antarctica Advisors | $10M-$100M | Niche cross-border (seafood, food, agribusiness) | Lehman + retainer | Seafood-industry M&A specialty rare in IB; 25+ year founder pedigree |

| Vaupen Financial Advisors | $5M-$50M | Lower-middle-market US plus LatAm and Caribbean (multi-sector) | Lehman + retainer | LMM US-LatAm-Caribbean specialty with 35-year founder pedigree |

| Atlantico Capital Partners | $20M-$200M | Hispanic-market cross-border M&A plus structured and project finance | Lehman + retainer | Madrid-Miami-Mexico City cross-border boutique with EU and Hispanic markets focus |

| JLL Hotels & Hospitality (Miami) | $30M-$1B+ | Hotel investment sales advisory | Standard JLL fee structure | Global hotel-investment advisor with Miami specialty team |

| Cross Keys Capital | $15M-$200M | South Florida regional generalist mid-market (multi-sector) | Lehman + retainer | Fort Lauderdale-anchored South Florida regional with 20+ professionals |

| Solomon Partners (Miami office) | $50M-$500M+ | Bank-owned-boutique-tier multi-sector (FIG strength); Natixis affiliate | Lehman + retainer | NYC-HQ bank-owned-boutique tier with Miami office at 3350 Virginia Street |

Why Is Miami the M&A Capital for LatAm Cross-Border, Migratory Family-Office Buyers, and Hospitality Consolidation?

Miami's M&A market is structurally distinct from every other US metro in five ways, and each one shows up in the deal-size bands and advisor specialty mix.

First, the LatAm cross-border seller pool is unmatched in the US. Cross-border M&A activity involving Latin American buyers reached a record $4.7 billion in the Miami metro in 2025 per SunBridge M&A Advisors' 2026 Miami Report. Latin America recorded 2,118 M&A transactions in the first 9 months of 2025 with $78.1 billion in aggregate value (4% volume decline but 24% value increase YoY -- a fewer-but-larger deal pattern); Brazil alone closed approximately 1,142 transactions through August 2025 (33% volume increase YoY); Mexico capital mobilized surged 70%+ YoY to approximately $28 billion in 2025. SaaS led tech M&A activity in LatAm in September 2025 (44% of transactions), with fintech at 18%. The Miami-anchored LatAm cross-border specialty bench (BroadSpan Capital, LatamIB, Atlantico Capital Partners, Antarctica Advisors, Vaupen Financial Advisors) is structurally deeper than any other US metro on this axis -- no NYC, SF, LA, Boston, Houston, Chicago, Atlanta, Dallas, or Seattle equivalent has 30+ year LatAm M&A specialty depth at the boutique tier.

Second, the migratory family-office buyer pool has crystallized in Miami. Florida recorded 178,674 net international migrants from July 2024 to July 2025 (highest of any US state); Miami-Dade alone attracted 123,835 of those migrants. As of Q1 2025, 245 verified Florida-based family offices include 30+ in Miami metro per Altss Q1 2025 family office data. International buyers acquired 49% of all new luxury units in South Florida through June 2025, of whom approximately 86% were Latin American (i.e., approximately 42% of new luxury units were sold to Latin American buyers specifically). Banco Bradesco's Florida wealth-under-custody doubled to $4 billion since 2019, and Itau Unibanco's Miami WUM climbed 10% YoY in 2025 to approximately $24 billion. The migratory wealth converts directly into M&A buy-side activity: a Miami-anchored family office that ten years ago would have funneled deal flow through Sao Paulo or Mexico City now allocates directly to Miami-based deal teams, structurally shifting the geography of LatAm-adjacent buy-side activity into Miami.

Third, the Brickell financial-hub crystallization compresses the gap between Miami sell-side advisory and bulge-bracket capital sources. Citadel/Ken Griffin's $2.5 billion HQ at 1201 Brickell Bay Drive (54-story, 1.7 million square foot tower, redesign confirmed April 2026) anchors the new Miami financial center. Microsoft consolidated its LatAm HQ in Brickell in 2024. Blackstone significantly expanded Miami investment and real-estate operations in 2024. Apollo Global signed a Brickell lease in 2021. The direct M&A consequence: buyer-side institutional investor footprint in Miami is materially deeper than at any prior point in the city's history. A Miami sell-side advisor pitching in 2026 should be able to name the relevant Citadel strategic-investment, Apollo Hybrid Value, or Blackstone Tactical Opportunities team contact deployed in Miami specifically rather than referring generically to NYC headquarters.

Fourth, the hospitality and REIT consolidation engine runs through Miami at top-4 US scale. Miami was a top-4 US hotel market with $1.03 billion trading in 2024; hotel investment climbed 17.5% YoY to $24 billion in 2025 per JLL. The EAST Miami sale to Blackstone (Trinity + Certares as sellers, closed September 10, 2025; 352-room lifestyle hotel in Brickell) anchors the trend, and the Diplomat Beach Resort $600 million refinancing (May 6, 2026; Trinity Investments + UBS Asset Management as JV borrower; resort located in Hollywood, FL within the broader South Florida hospitality corridor) extends it. Eastdil Secured led the national US hotel investment-sales league table in 2024 with approximately 43.8% market share and $4.43 billion in 2024 hotel sales (up 62% YoY) -- a national leadership position that anchors its Miami hotel-sales presence rather than a Miami-only stat. The Miami real-estate cycle is increasingly a hospitality-REIT take-private flywheel, and the JLL Hotels & Hospitality Miami investment-sales team plus Eastdil Secured Miami office anchor the advisor side of that flywheel.

Fifth, the Miami fintech ecosystem post-FTX recovery and crypto M&A reset is the strongest of any US metro. Miami metro fintech raised $1.8 billion in 2025 (30% of all Miami VC) per Refresh Miami coverage; 614 fintech firms operate in the Miami metro. Crypto M&A globally surged in 2025 -- approximately $8.6 billion across 267 deals tracked by Galaxy / Architect Partners across full-year 2025 (approximately 3x full-year 2024 deal value), including Stripe-Bridge $1.1 billion, Robinhood-Bitstamp, Coinbase-Deribit $2.9 billion (closed August 14, 2025), and Ripple-Hidden Road $1.25 billion. Local Miami-anchored fintech players include Milo (crypto mortgages) and Ledn (Bitcoin-backed mortgage product launched 2024 following its $70 million Series B round in December 2021). For Miami fintech and crypto founders, the M&A backdrop is structurally favorable, and the right advisor selection turns on whether the buyer pool is concentrated in Miami's Brickell ecosystem (Lincoln International Miami's TMT specialty wins) or extends globally (NYC-tier fintech specialty firms like FT Partners win).

The structural takeaway: Miami is the only US metro where the LatAm cross-border seller pool meets the migratory family-office buyer pool at this density, and the right advisor for a Miami sell-side is structurally different from the right advisor for a NYC, Boston, SF, LA, Seattle, or Charlotte mandate -- Charlotte runs a LatAm-cross-border-light playbook anchored on Truist Insurance Holdings and select Bank of America LatAm wealth flows that complements Miami's heavy cross-border specialty without competing on the same deals. Miami is also the metro where the Brickell financial-hub buyer-side concentration compresses the structural gap between local boutiques and bulge-bracket capital sources -- favoring senior-MD-led Miami-anchored boutiques over NYC-flown-in bulge-bracket teams at the $25M-$200M LMM band.

What Should I Look For in a Miami M&A Advisor?

Five filters that matter more in Miami than in other US metros:

- LatAm in-country deal-team density (when relevant) -- if your buyer pool, seller pool, or strategic-acquirer set spans Brazil, Mexico, Colombia, Argentina, Peru, Chile, or Caribbean jurisdictions, the right advisor has named in-country MDs (BroadSpan's Negrao in Sao Paulo, Camarena in Mexico City; LatamIB's Mazzanti and Sanchez with Violy Byorum DNA; Atlantico's Toro in Mexico City; Antarctica's seafood and food in-country contacts) rather than a US-only senior bench coordinating cross-border work through unnamed local partners. Ask the pitching senior banker to name the in-country MD on your prospective deal and the last three deals they personally led from that jurisdiction.

- Brickell-deployed strategic-buyer relationship density -- the Brickell financial-hub crystallization (Citadel, Microsoft, Apollo, Blackstone, plus 245 Florida-based family offices) means the right Miami advisor names current Brickell-deployed buyer contacts rather than NYC-headquartered firm-level generalities. Ask the pitching firm to walk through their last three Brickell-buyer interactions and tell you which buyers they would call first for your deal.

- Senior-banker engagement -- the Miami LMM band ($25M-$200M EV) requires senior bankers personally on every buyer call. Boutiques like Cassel Salpeter, BroadSpan, LatamIB, Atlantico, Antarctica, Vaupen, Cross Keys, and The Bloom Organization Miami all run senior-banker models structurally. Bank-owned-tier firms (Houlihan Lokey, Solomon Partners, Lincoln International) sometimes delegate to VPs and analysts because the parent-firm cost structure spreads MD time across multiple mandates.

- Sub-vertical specialty depth -- 'Miami generalist' is not enough when your deal turns on healthcare-services PE-platform buyer relationships, hospitality-REIT corp-dev cycles, or a specific cross-border tax-structuring requirement. The right advisor names five recent buyers in your specific sub-vertical without having to look them up. Single-vertical Miami specialty firms include The Bloom Organization Miami (healthcare services), Antarctica Advisors (seafood and food), JLL Hotels (hospitality), and Lincoln International Miami (TMT).

- Engagement-letter-term flexibility -- Miami true-independents (Cassel Salpeter, BroadSpan, LatamIB, Atlantico, Antarctica, Vaupen, Cross Keys, The Bloom Organization) all run engagement-letter terms that can be negotiated without head-office sign-off. The bank-owned-tier firms (Houlihan Lokey, Solomon Partners, Lincoln International) and the global firms (JLL Hotels) structurally do not. For a Miami founder with strong leverage on retainer credit, tail-period exclusions, and minimum-fee floors, the structural fit is usually a true independent.

For pricing comparisons across data room platforms, our pricing guide covers what Miami specialty boutiques typically charge and how that compares to bulge-bracket alternatives. For confidentiality and watermarking specifically, Peony embeds buyer email plus exact view timestamp into every page of every CIM.

Which Miami M&A Advisors Anchor the Generalist Mid-Market and South Florida Regional Band ($15M-$300M EV)?

For Miami-area generalist sellers in consumer products, business services, industrial, financial services, and multi-sector situations, two firms anchor the band: Cassel Salpeter & Co (Coconut Grove since February 1, 2026; 15-year continuous Miami M&A practice with 50+ assignments completed in 2025 alone) and Cross Keys Capital (Fort Lauderdale-anchored South Florida regional; 20+ professionals; approximately $3 billion+ closed transactions across firm history). The first call splits structurally on geography preference (pure Miami-anchored versus broader South Florida regional) and on senior-banker continuity preference.

1. Cassel Salpeter & Co

HQ: 3250 Mary Street, Suite 410, Miami, FL 33133 (Coconut Grove) -- relocated February 1, 2026 from Brickell Avenue after 15 continuous years Founded: 2010 by James S. Cassel (Chairman and co-founder; attorney and dealmaker; University of Miami Law JD 1979) and Scott Salpeter (President and co-founder). Both Cassel and Salpeter previously co-founded Capitalink (sold to Ladenburg Thalmann), and the Cassel Salpeter founding consolidated their LMM Miami M&A practice into the current independent firm. Senior team: James S. Cassel (Chairman) and Scott Salpeter (President) anchor the senior bench; the firm has built out additional Managing Director and Director coverage across its specialty sectors. Track record: 50+ M&A, capital-raising, and restructuring assignments completed in 2025; 69 cumulative deals (58 M&A and 11 funding rounds) as of January 2026 Deal size sweet spot: $20M-$300M generalist middle-market M&A Sectors: Aerospace and defense, consumer products and services, financial services, healthcare, technology, electronics, industrials Verified 2024-2026 transactions:

- Sunbelt Health sold to Unified Health Services (UHS, Reynolda Equity Partners portfolio company) on March 27, 2025 -- Cassel Salpeter exclusive financial advisor to Sunbelt Health

- Nicklaus Companies LLC Chapter 11 sold to 20 Majors LLC (Nicklaus Brown & Co. -- Rory Brown and Gary Nicklaus) -- bankruptcy auction price $35.7 million; sale approved March 9, 2026 -- Cassel Salpeter advisor on the Chapter 11 sale process

- PLANTA restaurant chain Chapter 11 (2025) -- Cassel Salpeter advisor

Distinguishing factor: Cassel Salpeter is the deepest-rooted Miami-headquartered generalist M&A boutique with 15+ years of continuous focus, a 50+ assignment 2025 cadence, and the only Miami-anchored independent boutique with a verified Chapter 11 senior-banker bench (Nicklaus Companies, PLANTA). The February 1, 2026 relocation to Coconut Grove (3250 Mary Street, Suite 410) marked a generational milestone after 15 years on Brickell Avenue and signals continued Miami-anchored commitment. The firm runs a true-independent senior-MD-led model with no parent-firm approval layer.

Best for: Founder-owned and PE-backed Miami and South Florida sellers with $5M-$30M EBITDA in consumer, services, healthcare, technology, electronics, industrials, financial services, or aerospace and defense -- particularly those preparing for a senior-banker-led process where engagement-letter-term flexibility matters. Best contact: James S. Cassel (Chairman) or Scott Salpeter (President).

2. Cross Keys Capital

HQ: 200 S Andrews Avenue, Suite 602, Fort Lauderdale, FL 33301 (Chicago secondary office) -- South Florida regional, Fort Lauderdale-anchored, not pure Miami Founded: Founded by three investment bankers with ex-Goldman Sachs, Morgan Stanley, and Lehman Brothers pedigree (specific founding-team detail is best confirmed directly via the firm's leadership page; founders are not surfaced in third-party press at the same density as Cassel Salpeter's named co-founders). Senior team: 20+ professionals across the Fort Lauderdale and Chicago offices; senior bench detail is best verified directly via the firm at ckcap.com. Track record: Approximately $3 billion+ in closed transactions across firm history Deal size sweet spot: $15M-$200M South Florida regional generalist middle-market M&A Sectors: Multi-sector South Florida regional generalist -- consumer, business services, industrial, healthcare, technology Recent activity: Cross Keys' 2024-2026 specific deal disclosure is best verified directly via the firm's transactions page at ckcap.com -- the firm's South Florida regional generalist practice anchors a steady pipeline of Fort Lauderdale, Miami-Dade, Palm Beach, and broader Southeast founder-owned mid-market sellers rather than recent named deals at the public-press density of Cassel Salpeter.

Distinguishing factor: Cross Keys is the deepest-rooted Fort Lauderdale-anchored South Florida regional generalist boutique with 20+ professionals and approximately $3 billion+ in aggregate closed transactions. The Goldman Sachs, Morgan Stanley, and Lehman Brothers founding-team pedigree gives the senior bench cross-coast bulge-bracket-tier execution standards while keeping the engagement model independent. For South Florida founders whose deal sits across the Fort Lauderdale-Miami corridor (manufacturing, distribution, services, multi-sector situations), Cross Keys is the structural alternative to Miami-pure boutiques.

Best for: Founder-owned South Florida regional businesses with $5M-$30M EBITDA in consumer, business services, industrial, healthcare, or technology preparing for a senior-banker-led process where the deal-team's geographic footprint extends beyond pure Miami. Best contact: senior partners (best verified directly via ckcap.com).

Which Miami M&A Advisors Anchor the LatAm Cross-Border Specialty Band ($10M-$200M EV)?

For Miami-area sellers, buyers, or strategic-acquirers operating across Latin America and the Caribbean, five firms anchor the band: BroadSpan Capital (Brickell; founded 2001; 53 facilitated deals as of April 2026), Latam Investment Banking (LatamIB) (Miami; founded 2011; 150+ mandates with $10 billion+ aggregate), Atlantico Capital Partners (Miami + Madrid + Mexico City; founded 2015), Antarctica Advisors (Miami; niche seafood and food specialty), and Vaupen Financial Advisors (Miami; founded 2001; 35+ year founder pedigree). The first call splits structurally on jurisdiction (Brazil and broader Latin America versus Mexico versus Hispanic-EU-Latin America versus seafood and food versus US-LatAm-Caribbean LMM).

3. BroadSpan Capital

HQ: 1450 Brickell Avenue, Suite 2620, Miami, FL 33131 (plus offices in Rio de Janeiro, Sao Paulo, Mexico City, and Medellin) Founded: 2001 Senior team: Mark Rosen (Senior Advisor + Vice Chair of the Advisory Board; joined September 2023; former US Executive Director at the IMF until January 2021; former Chairman and CEO of BAML's Latin American Investment Banking Division until August 2018), Fabricio Negrao (Managing Director, Sao Paulo; joined January 2025; 18+ years Brazilian and LatAm M&A experience), Luis Camarena (Managing Director and Head of Mexico, Mexico City), and Mario Espinosa (Mexico team). Track record: 53 facilitated deals as of April 2026 Deal size sweet spot: $20M-$200M LatAm and Caribbean cross-border M&A Sectors: Cross-border M&A across Latin America and the Caribbean -- consumer, industrial, services, technology, agribusiness, energy Verified 2024-2025 transactions:

- Boa Praca sold to Wrist Ship Supply (Danish maritime supplies) -- closed December 19, 2024 -- BroadSpan Capital advisor on the Brazilian sell-side

- Grupo IMSA / NovaScott (50% sale of gelcoats manufacturer) sold to Scott Bader Brazil -- closed June 2024 -- BroadSpan Capital advisor; co-advised by EFIC Partners

- AGS acquisition of 55% of Omni Transloading & Logistics -- closed February 2024 -- BroadSpan Capital advisor

Distinguishing factor: BroadSpan is the deepest-rooted Miami-headquartered LatAm and Caribbean cross-border M&A boutique with 25 years of continuous focus, named in-country MDs across Sao Paulo, Mexico City, and Medellin, and a 53-deal track record across complex cross-border situations. Mark Rosen's IMF and BAML LatAm IB pedigree anchors the senior advisory bench. The firm's January 2025 addition of Fabricio Negrao to lead the Sao Paulo MD bench plus Luis Camarena's Mexico City MD position give Miami-anchored sellers the deepest in-country deal-team density of any boutique on this list.

Best for: LatAm and Caribbean sell-side, buy-side, or cross-border founders with $10M-$50M EBITDA preparing for a strategic acquirer or PE-platform exit where the in-country deal-team work (Brazilian, Mexican, or Caribbean regulatory diligence, dual-jurisdiction tax structuring, language-coordinated buyer outreach) matters as much as the US sell-side process. Best contact: Mark Rosen (Senior Advisor) or Fabricio Negrao (Sao Paulo MD) for Brazilian mandates; Luis Camarena (Mexico Head) for Mexican mandates.

4. Latam Investment Banking (LatamIB)

HQ: Miami Founded: 2011 Senior team: Alessio Mazzanti (Managing Director and Founder; previously Pan American Finance Director, Valorem (Santo Domingo family office), and Vice President at Violy Byorum & Partners (NY) 1996-2001) and Roberto Sanchez (Managing Director and Founder; previously Vice President at Violy Byorum & Partners 1997-2003). Track record: 150+ advisory mandates over the firm's history; approximately $10 billion+ in aggregate closed transaction value Deal size sweet spot: $20M-$200M LatAm M&A and capital raising Sectors: Multi-sector LatAm M&A -- consumer, industrial, services, technology, financial services, agribusiness, energy Recent activity: LatamIB's per-deal disclosure is more limited than BroadSpan's or Atlantico's public profile; the firm's track record is anchored in aggregate volume (150+ mandates, $10 billion+ aggregate) rather than recent named deals at the public-press density of BroadSpan. Founders evaluating LatamIB should request the firm's full transaction sheet directly and verify with senior-team references.

Distinguishing factor: LatamIB is the pure-play Miami-headquartered LatAm M&A boutique with 150+ mandate aggregate volume and the founder-pair Violy Byorum & Partners DNA -- both Mazzanti and Sanchez served as VPs at Violy Byorum (NY) in the late 1990s and early 2000s, when Violy Byorum was the leading LatAm M&A boutique on Wall Street. The LatamIB founder pedigree is rare in Miami and gives the firm direct Wall-Street-tier LatAm-cross-border execution standards in a Miami-anchored independent.

Best for: Cross-border founders, family offices, and PE platforms operating across Latin America preparing for a US strategic-acquirer or LatAm-strategic-acquirer exit at $20M-$200M EV where the founder-pair Violy Byorum DNA earns its tier. Best contact: Alessio Mazzanti or Roberto Sanchez (founder-tier).

5. Antarctica Advisors

HQ: Miami Founded: Founded by Ignacio J. Kleiman (Managing Partner) with co-founder Birgir Brynjolfsson (Partner) Senior team: Ignacio J. Kleiman (Managing Partner; 25+ years; J.P. Morgan M&A 1991; 10+ years Bankers Trust + Deutsche Bank in IB and PE; 6 years Rabobank International (NY) MD M&A Food; previously CEO of Glacier Securities) and Birgir Brynjolfsson (Partner; ex-Glacier Securities) Deal size sweet spot: $10M-$100M niche cross-border M&A Sectors: Niche seafood-industry M&A specialty; food and agribusiness cross-border generalist Recent activity: Antarctica's recent named deal disclosure is more limited than BroadSpan's; the firm's track record is anchored in seafood-industry M&A specialty depth (rare in IB) and the founder's long Wall-Street-LatAm pedigree (J.P. Morgan, Bankers Trust, Deutsche Bank, Rabobank International). Founders evaluating Antarctica should request the firm's transaction sheet directly and verify with senior-team references for sub-vertical-specific 2024-2026 closes.

Distinguishing factor: Antarctica Advisors is the only Miami-headquartered M&A boutique with a niche seafood-industry M&A specialty -- Kleiman's six years at Rabobank International (NY) as MD M&A Food gives the senior bench direct visibility into seafood, aquaculture, and broader food and agribusiness strategics worldwide. The seafood specialty is rare in IB and structurally differentiated from generalist Miami boutiques. The cross-border food and agribusiness practice extends the seafood specialty into adjacent verticals.

Best for: Seafood, aquaculture, food, and agribusiness founders and family-owned businesses with $5M-$25M EBITDA preparing for a strategic acquirer or PE-platform exit -- particularly those with cross-border buyer pools spanning North America, Europe, Latin America, or Asia. Best contact: Ignacio J. Kleiman (Managing Partner).

6. Vaupen Financial Advisors

HQ: Miami Founded: 2001 by Hy Vaupen (Founder and Managing Partner; 35+ years experience). Prior career: Ernst & Whinney CPAs, Beverage Canners International, GB Group, Kellstrom Industries. University of Florida Fisher School graduate; Florida CPA since 1979. Senior team: Hy Vaupen anchors the senior bench; specific MD and Director coverage detail is best verified directly via the firm at vaupenfinancial.com. Deal size sweet spot: $5M-$50M lower-middle-market US plus LatAm and Caribbean M&A Sectors: Multi-sector lower-middle-market generalist -- revenue $10M-$100M, deals $5M+ enterprise value Recent activity: Vaupen's per-deal public disclosure is limited (PitchBook tracks 3 deals); the firm's track record is anchored in aggregate practice depth (35+ years) and Hy Vaupen's combined CPA-and-IB pedigree (Ernst & Whinney CPAs, Beverage Canners, GB Group, Kellstrom Industries). Founders evaluating Vaupen should request the firm's full transaction sheet directly rather than relying on third-party tracking.

Distinguishing factor: Vaupen is the longest-operating Miami-headquartered lower-middle-market US-plus-LatAm-and-Caribbean specialty boutique anchored by Hy Vaupen's 35+ year combined CPA, corporate finance, and IB pedigree. The combination of Florida CPA practice (since 1979) plus Miami-anchored M&A practice (since 2001) gives the senior bench unusual depth on the financial-due-diligence and tax-structuring side of LMM cross-border deals.

Best for: Lower-middle-market US-anchored, LatAm-anchored, or Caribbean-anchored founders with $5M-$15M EBITDA preparing for a strategic acquirer or smaller PE-platform exit where the financial-due-diligence-plus-IB integrated capability earns its tier. Best contact: Hy Vaupen (Founder and Managing Partner).

7. Atlantico Capital Partners

HQ: Miami (founded 2015) + Madrid + Mexico City Founded: 2015 Senior team: Miguel Bermejo (Founder and Managing Partner; 20+ years M&A and structured-and-project-finance experience; relocated from Miami to Madrid in September 2024) and Juan Francisco Toro (leads Atlantico Mexico, Mexico City). Deal size sweet spot: $20M-$200M Hispanic-market cross-border M&A plus structured and project finance Sectors: Cross-border M&A and capital raising across Spain, Latin America (Mexico, Colombia, Peru, Chile, Dominican Republic), and the US Hispanic market; structured and project finance Verified 2024-2025 transactions:

- Grupo Exito sale to Grupo Calleja -- closed February 2024 -- Atlantico Capital Partners advised on the Casino/GPA seller side of the transaction

- IBT Health Piura + Chimbote hospital PPPs (Peru) -- ongoing 2024-2025 -- Atlantico Capital Partners advisor

- Renewable energy deals across Chile, Colombia, and the Dominican Republic -- Atlantico Capital Partners advisor

Distinguishing factor: Atlantico is the only Miami-headquartered M&A boutique with a Madrid-Mexico City-Miami three-office structure giving the senior bench direct EU and Hispanic-market reach in addition to Latin American coverage. Bermejo's September 2024 relocation from Miami to Madrid extends the firm's EU footprint at the senior-MD level. The structured-and-project-finance specialty (Peruvian hospital PPPs, Chilean and Colombian renewable energy) is rare among Miami-anchored boutiques and gives the firm advisor capability on infrastructure-tier transactions that pure M&A boutiques cannot match.

Best for: Cross-border founders, family offices, sovereign-sponsored entities, and PE platforms operating across Spain, Mexico, Colombia, Peru, Chile, the Dominican Republic, or the US Hispanic market -- particularly those with infrastructure, renewable energy, or healthcare-PPP deal profiles. Best contact: Miguel Bermejo (Madrid) or Juan Francisco Toro (Mexico City).

Which Miami M&A Advisors Anchor the Bank-Owned-Boutique Tier ($40M-$1B EV)?

For Miami-area founders and PE platforms whose deal turns on parent-firm balance-sheet capability, NYC-style execution standards, or sub-vertical financial-services and TMT depth, three firms anchor the band: Houlihan Lokey Miami (3390 Mary Street, Suite 116; bank-owned-boutique-tier with global parent), Solomon Partners Miami (3350 Virginia Street, Coconut Grove area; NYC-HQ Natixis affiliate), and Lincoln International Miami (Miami office opened October 2022, anchored by Spurrier Capital DNA in TMT). The first call splits structurally on sub-vertical (financial services and REIT versus multi-sector NYC-HQ versus pure TMT) and on parent-firm reach preferences.

8. Houlihan Lokey Miami

HQ: 3390 Mary Street, Suite 116, Miami, FL 33133 (Coconut Grove area); broader Houlihan Lokey parent firm is global Senior team: Jeffrey Levine (Managing Director, Global Co-Head Financial Services Group + Management Committee; joined Houlihan Lokey via the 2012 acquisition of Milestone Advisors), Michael McMahon (Managing Director, Head of Asset Management practice; 30+ years), and Kevin Ryan (Managing Director, Capital Solutions Group; joined July 2025 from CFO of Better Home & Finance Holding plus 20 years at Morgan Stanley). Deal size sweet spot: $50M-$1B+ financial services, REIT and mortgage finance, asset management, and Capital Solutions M&A Sectors: Financial services, REIT and mortgage finance, asset management, Capital Solutions (parent-firm-driven private placements and structured-finance advisory) Recent activity: Houlihan Lokey's parent-firm M&A activity is the broadest of any global mid-market firm; specific Miami-led deal disclosure is best verified directly via the firm's transactions page at hl.com. Kevin Ryan's July 2025 hire to the Miami Capital Solutions Group expanded the office's structured-finance bench.

Distinguishing factor: Houlihan Lokey Miami is the deepest financial-services, REIT and mortgage finance, and asset-management M&A bench in Miami, anchored by Jeffrey Levine's Global Co-Head FS Group position plus Management Committee membership. The Capital Solutions Group (Kevin Ryan, joined July 2025) extends the office's reach into structured-finance and private-placement advisory beyond pure M&A. Frame Houlihan Lokey Miami as a global-firm bank-owned-boutique-tier office rather than as a true-independent boutique -- the parent ownership shapes engagement-letter terms and senior-banker autonomy in the same way KBCM in Seattle and Cain Brothers in Boston do for their respective metros.

Best for: Financial services, REIT, mortgage finance, asset management, and complex Capital Solutions mandates with $50M+ EV where the parent-firm capability (global research, structured-finance distribution, syndicated debt placement) earns its tier. For Miami founders specifically, Houlihan Lokey Miami is the structural alternative to true-independent specialty boutiques when the deal envisions a complex capital stack at close or a buyer pool that requires staple financing. Note that the same Houlihan Lokey parent firm operates a separate Aerospace, Defense and Government Services (ADG) practice -- the Washington DC ADG bench covers the cleared-defense, federal-IT, and GovCon buyer pool (Leidos, GDIT, SAIC, Booz Allen, plus federal-services PE platforms Veritas, AE Industrial, Arlington Capital) that Miami's LatAm cross-border seller pool and Brickell migratory family-office buyer pool structurally do not reach.

9. Solomon Partners (Miami office)

HQ: Miami office at 3350 Virginia Street, Miami, FL 33133 (Coconut Grove area); firm headquarters in New York City (independently-run affiliate of Natixis, part of Groupe BPCE); other US offices in Chicago and Miami Senior team: Solomon Partners has been the firm's brand since its 2020 spin-off and 2022 rebrand from PJ SOLOMON; the senior bench is anchored at the NYC headquarters with named MDs across sectors including consumer, industrial, business services, financial services (FIG group expanded February 2025), and healthcare. Specific Miami-resident senior bankers should be confirmed directly with the firm before engagement-letter discussions. Track record: Solomon Partners' record M&A year was 2025; the firm operates as an independently-run affiliate of Natixis with documented Miami office presence Deal size sweet spot: $50M-$500M+ multi-sector middle-market M&A with FIG strength Sectors: Multi-sector NYC-tier middle-market M&A -- consumer, industrial, business services, financial services (FIG group expanded February 2025), healthcare Recent activity: Solomon Partners' 2025 record M&A year and February 2025 FIG group expansion were anchored by the NYC core practice; Miami-led 2024-2026 deal disclosure is best verified directly via the firm's transactions page at solomonpartners.com.

Distinguishing factor: Solomon Partners Miami is the bank-owned-boutique-tier NYC-HQ option for Miami founders evaluating local-versus-out-of-region cross-coast advisor selection. The Natixis-affiliate structure (Groupe BPCE parent) gives the senior bench European reach in addition to the NYC core practice, and the FIG group's February 2025 expansion deepens the firm's financial-services M&A coverage. The Miami office at 3350 Virginia Street operates with documented Miami-area presence.

Best for: Miami founders evaluating bank-owned-boutique-tier execution with NYC-style standards plus European reach -- particularly those with cross-Atlantic strategic-buyer pools or financial-services targets where the Natixis parent's European footprint earns its tier. Email pattern: [first].[last]@solomonpartners.com -- the firm uses the full-first-name-dot-last-name pattern, not [first_initial][last]@. Use the correct address pattern; the wrong one bounces.

10. Lincoln International Miami

Office: Miami, opened October 2022 -- anchored by Clark Spurrier (Managing Director and Chairman of the firm's TMT Group; US Management Committee member). Lincoln International is a global mid-market firm with 1,000+ professionals across 26 offices. History: Spurrier Capital Partners (NYC-founded 2009 by Clark Spurrier) was acquired by Lincoln International in March 2022; the Miami office launched October 2022 to extend the Spurrier Capital DNA into the Miami-anchored TMT specialty practice. Clark Spurrier brings 30+ years of tech investment-banking experience and 200+ M&A, IPO, and private-placement transactions across his career. Senior team: Clark Spurrier (MD, Chairman TMT Group; US Management Committee) anchors the Miami office. Additional Lincoln International parent-firm senior bench detail is best verified directly via the firm at lincolninternational.com. Deal size sweet spot: $40M-$500M TMT (technology, media, telecom) M&A Sectors: TMT specialty -- software, fintech, consumer tech, communications, broader technology and media Recent activity: Lincoln International's parent firm closed 360+ deals in 2024 across all offices; specific Miami-led 2024-2026 deal disclosure is best verified directly via the firm's transactions page at lincolninternational.com.

Distinguishing factor: Lincoln International Miami is the only Miami-anchored bank-owned-boutique-tier TMT specialty office -- Clark Spurrier's 30+ year tech IB pedigree (anchored by the 2022 Spurrier Capital acquisition) plus Lincoln International parent's global mid-market reach combine to support sub-vertical TMT specialty depth that pure-Miami generalist boutiques do not match. The Miami office launched October 2022 and extends Lincoln's broader US Management Committee bench into the Miami-anchored Brickell ecosystem.

Best for: TMT, software, fintech, consumer tech, and communications founders with $20M-$200M ARR or $40M-$500M EV preparing for a strategic acquirer or PE-platform exit where the Spurrier Capital DNA plus Lincoln International global parent's cross-coast reach matter. For Miami fintech founders specifically, Lincoln Miami is the structural local alternative to flying in NYC FT Partners. Best contact: Clark Spurrier (Chairman TMT Group; Miami office lead).

Which Miami M&A Advisors Anchor the Healthcare Services and Hospitality Specialty Bands?

For Miami-area healthcare-services and hospitality founders, two firms anchor the specialty bands: The Bloom Organization (Miami office) for healthcare services (physician practices, ACOs, senior care, home health, behavioral health) and JLL Hotels & Hospitality (Miami investment-sales team) for hospitality investment-sales advisory. Each is the structural default for its specialty axis; the two specialties rarely overlap on a single mandate.

11. The Bloom Organization (Miami office)

HQ (firm-wide): Hallandale Beach, FL (Florida-rooted); firm operates 30+ years with 200+ closed transactions and approximately $15 billion aggregate value across healthcare services Miami office leadership: Steven Weiss, MBA, CPA (Managing Director; leads Miami office; prior Ardent Investors LMM PE plus H.I.G. Capital's Advantage U.S. Buyout Fund), Henry Bloom (firm leadership), Robert Goettling (firm leadership), and Tyler Biscaha (Miami team) Deal size sweet spot: $20M-$200M healthcare-services M&A Sectors: Pure healthcare services -- physician practices, ACOs, senior care, home health, behavioral health, dental services, healthcare IT Verified 2025 transactions:

- Evolved Science sold to Formula Wellness (Trive Capital portfolio company) -- November 2025 -- Bloom Miami advisor; deal team led by Steven Weiss + Tyler Biscaha

- Next ACO of Nature Coast sold to Palm Beach ACO -- August 2025 -- Bloom Miami advisor; deal team led by Robert Goettling + Steven Weiss

- Royal Senior Care / Oakmonte Village sold to Welltower -- April 2025 -- Bloom Miami advisor; deal team led by Henry Bloom + Steven Weiss

Distinguishing factor: The Bloom Organization's Miami office is the deepest healthcare-services M&A bench with verified 2025 Miami-led close cadence across three named deals (Evolved Science / Formula Wellness, Next ACO / Palm Beach ACO, Royal Senior Care / Welltower). Steven Weiss's PE-buy-side pedigree (Ardent, H.I.G. Advantage) gives the senior bench direct visibility into which PE platforms, payer-aligned strategics, and senior-care REITs are filling pipeline gaps in physician services, ACOs, senior care, and home health. The firm-wide single-vertical depth (healthcare services and senior care; 200+ closed transactions; $15 billion aggregate) is structurally rare on the Miami bench. Frame Bloom Miami as 'Miami office of a Florida-headquartered (Hallandale Beach) healthcare-services boutique' rather than as a Miami-Brickell-headquartered firm.

Best for: Healthcare-services founders with $5M-$25M EBITDA in physician practices, ACOs, senior care, home health, behavioral health, dental services, or healthcare IT preparing for a strategic acquirer or PE-platform exit. Best contact: Steven Weiss (Miami office lead) for any Miami-led mandate.

12. JLL Hotels & Hospitality (Miami investment-sales team)

Office: Miami investment-sales advisory team (expanded materially in 2025 around named hospitality transactions) Firm-wide: JLL ranks #1 globally for hotel investment advisory in 2024 with $9.2 billion in deal volume, approximately $2.4 billion Americas, 14% Americas market share, and approximately 25% global market share Senior team: JLL's Miami Hotels & Hospitality team is anchored by named hospitality MDs whose specific roster is best verified directly via the firm at jll.com -- the team expanded in 2025 around named Miami transactions. Deal size sweet spot: $30M-$1B+ hotel investment-sales advisory Sectors: Hotel investment sales advisory -- limited-service, full-service, lifestyle, resort, condo-hotel mixed-use, hospitality REIT take-privates Verified 2024-2026 transactions:

- EAST Miami sold to Blackstone (Trinity Investments + Certares as sellers) -- closed September 10, 2025 -- JLL Hotels Miami advisor; 352-room lifestyle hotel in Brickell

- JW Marriott Marquis Miami $79.3 million refinancing -- JLL Hotels Miami advisor

- Diplomat Beach Resort (Hollywood, FL) $600 million refinancing -- May 6, 2026 -- JLL Hotels Miami advisor; Trinity Investments + UBS Asset Management JV borrower (note: resort is located in Hollywood, FL within the broader South Florida hospitality corridor, not Miami-Dade)

Distinguishing factor: JLL Hotels & Hospitality is the global #1 hotel investment-sales advisor with the deepest relationship density across hospitality REITs (Pebblebrook, Sunstone, RLJ, Ashford, Park Hotels, Hersha, DiamondRock), private-equity hospitality funds (Blackstone Real Estate, Starwood Capital, KSL Capital, Trinity Investments, Certares Hospitality), and global hospitality strategics (Marriott, Hilton, Hyatt, IHG, Accor). The Miami investment-sales team's 2024-2026 close cadence (EAST Miami / Blackstone, JW Marriott Marquis Miami refi, Diplomat Beach Resort refi) demonstrates the team's structural reach in the Miami top-4 US hotel market ($1.03 billion 2024 trading; $24 billion 2025 US hotel investment per JLL). Frame JLL Hotels Miami as a global-firm Miami specialty rather than as a true-independent boutique -- engagement terms reflect global-firm structure and the JLL parent's hospitality investment-management arm.

Best for: Hotel asset, resort, condo-hotel mixed-use, and hospitality-REIT founders, family offices, and PE hospitality fund GPs with $30M+ EV preparing for a strategic-buyer or take-private exit where the JLL parent's hospitality relationship density translates into pricing tension. For pure hotel-asset sales specifically, JLL Hotels Miami and Eastdil Secured Miami (1001 Brickell Bay; acquired by Savills on March 12, 2026 for $1.1 billion; 43.8% national US hotel-sales market share in 2024) are the two structural defaults.

What Recent Miami-Area M&A Deals Show How These Advisors Actually Work?

Five recent verified Miami-tied closes that illustrate the deal-size band, the buyer-pool composition, and the structural advantage each advisor brings.

Sunbelt Health to Unified Health Services (March 27, 2025; Cassel Salpeter & Co)

Cassel Salpeter served as exclusive financial advisor to Sunbelt Health on the March 27, 2025 sale to Unified Health Services (a Reynolda Equity Partners portfolio company). Sunbelt Health is a healthcare-services target; UHS is a Reynolda-backed PE platform. The deal demonstrates Cassel Salpeter's structural reach into the Florida-anchored healthcare-services PE-platform buyer pool and the firm's senior-MD-led model -- the engagement was structurally consistent with the firm's 50+ assignment 2025 cadence and the Miami-anchored independent-boutique senior-banker engagement standard. The buyer-pool composition of regional PE platforms with healthcare-services thesis is exactly the buyer set Cassel Salpeter designs around in Florida mid-market healthcare situations.

Boa Praca to Wrist Ship Supply (December 19, 2024; BroadSpan Capital)

BroadSpan Capital served as advisor on the December 19, 2024 sale of Boa Praca to Wrist Ship Supply (Danish maritime supplies). Boa Praca is a Brazilian maritime-supplies target; Wrist Ship Supply is a Danish strategic acquirer. The deal demonstrates BroadSpan's structural reach into the cross-border Brazilian sell-side plus EU strategic-buyer pool and the firm's named in-country MD bench (Sao Paulo, plus broader LatAm coverage). For Miami-anchored sellers specifically, the Boa Praca / Wrist deal is a direct data point on how BroadSpan's 25-year LatAm specialty depth and named in-country MDs translate into actual cross-border close.

Royal Senior Care / Oakmonte Village to Welltower (April 2025; The Bloom Organization Miami)

The Bloom Organization Miami served as advisor on the April 2025 sale of Royal Senior Care / Oakmonte Village to Welltower (one of the largest healthcare REITs globally). The deal team included Henry Bloom + Steven Weiss. The deal demonstrates Bloom Miami's structural reach into the senior-care REIT buyer pool and the firm's senior-MD-led healthcare-services specialty model -- Welltower is the senior-care REIT category leader, and the Bloom Miami senior-team relationship density across senior-care REITs (Welltower, Ventas, Healthpeak, Brookdale Senior Living) is the structural advantage the firm brings into Florida senior-care mandates.

Grupo Exito to Grupo Calleja (February 2024; Atlantico Capital Partners)

Atlantico Capital Partners served as advisor on the seller side (Casino/GPA) of the February 2024 sale of Grupo Exito to Grupo Calleja. Grupo Exito is a major Colombian retail conglomerate; Grupo Calleja is a Salvadoran strategic acquirer; Casino/GPA were the historic Brazilian-French sellers. The deal demonstrates Atlantico's structural reach into the cross-border LatAm sell-side plus EU-Latin American strategic-buyer pool and the firm's Madrid-Miami-Mexico City three-office structure. For Miami-anchored Hispanic-market founders specifically, the Grupo Exito / Grupo Calleja deal is a direct data point on how Atlantico's structured-and-project-finance specialty plus EU footprint translate into actual cross-border close.

EAST Miami to Blackstone (September 10, 2025; JLL Hotels & Hospitality Miami)

JLL Hotels & Hospitality Miami served as advisor on the September 10, 2025 sale of EAST Miami to Blackstone (Trinity Investments + Certares as sellers). EAST Miami is a 352-room lifestyle hotel in Brickell. The deal demonstrates JLL Hotels Miami's structural reach into the global hospitality-REIT and PE-hospitality-fund buyer pool, including Blackstone Real Estate as the buyer of record, plus the firm's Miami-team capability on top-4 US hotel-market transactions ($1.03 billion Miami trading in 2024; $24 billion US hotel investment in 2025 per JLL). For Miami hospitality founders specifically, the EAST Miami / Blackstone deal anchors the JLL-tier benchmark for boutique-hotel and lifestyle-hotel sell-side processes.

How Do I Pick the Right Miami M&A Advisor for My Situation?

The decision framework comes down to deal size + sub-vertical + ownership structure + buyer-pool geography + cross-border axis.

For $20M-$300M EV generalist Miami mid-market sales (consumer, services, healthcare, technology, financial services, aerospace and defense, electronics, industrials) -- Cassel Salpeter & Co is the Miami-default first call with 15+ years of continuous Miami practice, a 50+ assignment 2025 cadence, and the only Miami-anchored independent boutique with verified Chapter 11 senior-banker bench (Coconut Grove since February 1, 2026).

For $15M-$200M EV South Florida regional generalist (Fort Lauderdale-Miami-Palm Beach corridor) -- Cross Keys Capital brings 20+ professionals and approximately $3 billion+ in aggregate closed transactions with Goldman, Morgan Stanley, and Lehman pedigree founding-team DNA (Fort Lauderdale-anchored, not pure Miami).

For $20M-$200M EV LatAm cross-border M&A (Brazil, Mexico, Caribbean) -- BroadSpan Capital is the Brickell-anchored LatAm cross-border specialty default with named in-country MDs in Sao Paulo (Negrao) and Mexico City (Camarena), plus Mark Rosen's IMF and BAML LatAm IB Senior Advisor pedigree.

For $20M-$200M EV LatAm M&A with Wall-Street-tier execution standards -- Latam Investment Banking (LatamIB) is the founder-pair Violy Byorum DNA boutique with 150+ aggregate mandates and approximately $10 billion+ in closed transaction value (Mazzanti and Sanchez founder-tier).

For $20M-$200M EV Hispanic-market cross-border M&A across Spain, Mexico, Colombia, Peru, Chile, and the Dominican Republic plus structured-and-project-finance -- Atlantico Capital Partners brings the Madrid-Miami-Mexico City three-office structure with Bermejo (Madrid since September 2024) and Toro (Mexico City).

For $10M-$100M EV niche seafood, food, and agribusiness cross-border M&A -- Antarctica Advisors is the Miami-anchored seafood-industry M&A specialty boutique with Kleiman's J.P. Morgan / Bankers Trust / Deutsche Bank / Rabobank International M&A Food MD pedigree.

For $5M-$50M EV lower-middle-market US-plus-LatAm-and-Caribbean -- Vaupen Financial Advisors brings 35+ year founder-led practice with Hy Vaupen's combined Florida CPA (since 1979) plus Miami M&A (since 2001) integrated capability.

For $50M-$1B+ EV financial services, REIT and mortgage finance, asset management, and Capital Solutions deals -- Houlihan Lokey Miami (3390 Mary Street) is the bank-owned-boutique-tier global-firm anchor with Levine (Global Co-Head FS Group + Management Committee), McMahon (Asset Management head), and Ryan (Capital Solutions, joined July 2025).

For $40M-$500M EV TMT (software, fintech, consumer tech, communications) deals -- Lincoln International Miami brings Spurrier Capital DNA (Clark Spurrier as Chairman TMT Group + US Management Committee) plus Lincoln International parent's global mid-market reach.

For $50M-$500M+ EV multi-sector mandates with FIG strength and NYC-style execution standards plus European reach -- Solomon Partners Miami (3350 Virginia Street) is the NYC-HQ Natixis-affiliate Miami office with February 2025 FIG group expansion.

For $20M-$200M EV healthcare-services rollups (physician practices, ACOs, senior care, home health, behavioral health, dental) -- The Bloom Organization (Miami office) brings Steven Weiss's PE-buy-side pedigree plus the firm-wide single-vertical depth across 30+ years and 200+ closed transactions.

For $30M-$1B+ EV hospitality investment-sales advisory (boutique hotels, lifestyle hotels, resorts, condo-hotel mixed-use, hospitality REIT take-privates) -- JLL Hotels & Hospitality Miami is the global #1 hotel investment-sales advisor with the deepest hospitality-REIT and PE-hospitality-fund relationship density.

For framework comparisons with related frameworks, see our M&A data room guide, which covers what Miami advisors expect to see by Week 1 of the engagement.

What Data Room Capabilities Do Miami Advisors Demand?

Miami-area cross-border, generalist mid-market, healthcare-services, TMT, and hospitality sellers face structurally distinct confidentiality and workflow environments depending on which axis they sit on. The Miami advisors who run consistently confidential cross-border processes all rely on specific data room capabilities. Six capabilities matter most:

- Click-through NDA gates -- buyer-side users sign the NDA inside the data room before viewing any content, eliminating the email-attachment-NDA chain-of-custody problem that lets CIMs leak before signature; particularly critical for cross-border processes where Brazilian, Mexican, or Argentine buyer-side signatories need a clear and enforceable NDA chain

- Per-investor watermarks -- buyer email plus exact view timestamp embedded into every page so a leaked CIM has a forensic audit trail back to the specific buyer; the structural answer to Miami's overlapping-family-office and cross-border buyer-pool confidentiality risk

- Page-level analytics -- senior banker can see at a glance which buyer is reading the financials versus which is reading the legal section once and skipping the rest, which informs the LOI follow-up sequence; particularly useful for cross-border processes where buyer-side engagement signal timing differs across jurisdictions

- Visitor groups for buyer tiering -- US strategic acquirers, LatAm strategic acquirers, NYC PE platforms, and Brickell-deployed family offices each see different document sets; particularly useful for healthcare-services rollups where competitor-tier buyers should be blocked from physician-roster details and patient-volume tables until LOI signed

- Screenshot protection -- blocks and logs unauthorized capture attempts, deterring competitors from harvesting customer concentration tables, physician-roster details, and hotel-asset operating metrics during data room visits

- Auto-indexing -- compresses Weeks 1-3 of the engagement timeline because buyers can search across the entire data room (English, Portuguese, Spanish documents alongside US-side regulatory materials) instead of chasing folder paths; especially useful for cross-border data rooms with dual-language document sets

For Miami cross-border specifically, the smart Q&A feature centralizes buyer questions so the senior banker (or cross-border deal-team coordinator) can answer once and surface the answer to every approved buyer rather than repeating the same answer across 15 separate email threads in three languages. For solutions specifically targeted at M&A and private equity buyer-side workflows, Peony's M&A solution and PE solution pages cover the structural data room patterns most Miami advisors use. Custom domain means the data room URL reads as the seller's domain rather than a vendor URL -- a small detail that matters when Brickell-deployed strategic acquirers' corp-dev teams forward links internally.

How Do Miami M&A Advisor Fees Work?

Miami-area specialty boutiques typically run a Lehman-style success fee scale plus retainer:

| Deal Size (EV) | Typical Retainer | Lehman Success Fee Math (Standard 5/4/3/2/1 Scale) | Modified Fee Alternative | Typical Tail |

|---|---|---|---|---|

| $5M-$15M | $25K-$50K | 5/4/3/2/1 = approx 5-8% blended | Flat 4-5% on small deals | 12-24 months |

| $15M-$30M | $50K-$75K | 5/4/3/2/1 = approx 2.5-4% blended | 1.5-2% flat alternative on $20-30M | 12-24 months |

| $30M-$50M | $75K-$100K | 5/4/3/2/1 = approx 1.7-2.5% blended | 1.5% flat alternative; tiered with flat tail above $20M | 12-24 months |

| $50M-$100M | $100K-$150K | 5/4/3/2/1 = approx 1.2-1.7% blended | Tiered structure with flat tail above $50M | 12-24 months |

| $100M-$200M | $150K | 5/4/3/2/1 = approx 1.0-1.2% blended | Modified Lehman with higher first-tier and flat tail | 12-24 months |

Sub-vertical-specialty firms (BroadSpan and LatamIB and Atlantico on LatAm cross-border, The Bloom Organization Miami on healthcare services, Antarctica on seafood and food, Lincoln International Miami on TMT, JLL Hotels Miami on hospitality) sometimes charge at the higher end of the band given the buyer-relationship density they bring. Cross-border mandates often carry a small premium (10-25 basis points blended) over single-country Florida mandates because the senior team has to coordinate Brazilian, Mexican, Colombian, or Argentine in-country language, regulatory, and tax-structuring work alongside the US sell-side process. Bank-owned-tier firms (Houlihan Lokey, Solomon Partners, Lincoln International) typically run standard Lehman with a higher retainer floor ($75K-$150K) given the parent-firm cost structure. Pure generalist Miami boutiques (Cassel Salpeter, Cross Keys, Vaupen) typically run standard Lehman without the specialty premium. Bulge-bracket Miami offices (Goldman Sachs, Morgan Stanley) at $30M EV typically demand $250K+ retainer plus a $750K+ minimum success fee floor regardless of deal value -- structurally inefficient at the LMM band.

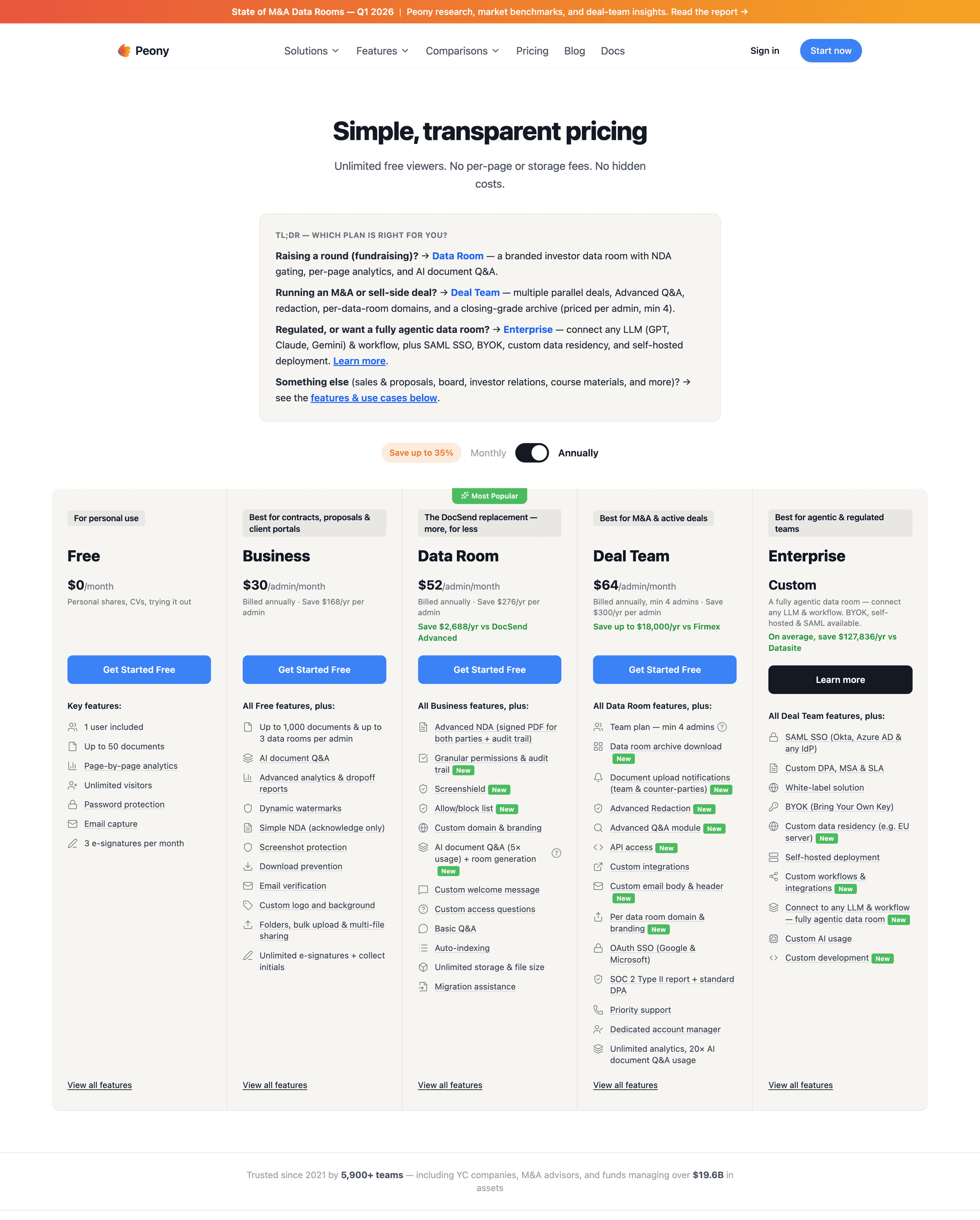

For full pricing detail on data room costs, Peony Data Room at $52 per admin per month replaces the $15K-$50K per-deal data room cost most Miami boutiques used to bill as expense reimbursement -- the platform fee shows up in the seller's expense column rather than the advisor's pass-through column. Peony Business at $30 per admin per month is a lower-tier option for smaller engagements with per-investor watermarks, page analytics, and screenshot protection; Data Room is the standard tier for active sell-side mandates given the visitor-group document isolation, granular per-file permissions, and unlimited rooms most Miami advisors require.

Miami M&A Advisor FAQs

What's the difference between a Miami M&A boutique and a bulge-bracket bank like Goldman or Morgan Stanley for a $50M deal?

For Miami-area sellers between $5M and $200M EV, the difference is structural: bulge-bracket banks are built around $200M+ engagements where senior MD time is allocated to the largest fee-payers, while specialty boutiques are built around the lower-middle-market band where senior bankers run buyer calls personally. A $50M EV Miami sell-side at Goldman or Morgan Stanley is staffed by a VP-and-analyst team, with the sector MD showing up for the pitch and the management presentation, then disappearing -- everything else routes through staff. Most Miami boutiques compete for the $25M-$200M EV band by structural design: Cassel Salpeter and Cross Keys on generalist mid-market; BroadSpan, LatamIB, Atlantico, Antarctica, and Vaupen on LatAm cross-border; The Bloom Organization Miami on healthcare services; Lincoln International Miami on TMT. Three firms operate as bank-owned-boutique-tier platforms (Houlihan Lokey Miami, Solomon Partners Miami, Lincoln International Miami). One specialty operator earns inclusion on the hospitality-specific side (JLL Hotels & Hospitality Miami). The structural test: ask any bulge-bracket pitcher to commit in writing to which senior banker (MD or above) will be on every buyer call. Most won't.

Should I hire BroadSpan Capital or Latam Investment Banking for an $80M Brazilian company sale to a US strategic acquirer?

For an $80M Brazilian company selling to a US strategic acquirer, the BroadSpan vs LatamIB choice breaks on three structural factors: in-country deal-team density, US strategic-buyer relationship pedigree, and aggregate cross-border volume. BroadSpan (Brickell; founded 2001; 53 facilitated deals) anchors the LatAm and Caribbean cross-border specialty bench with named in-country MDs in Sao Paulo (Negrao) and Mexico City (Camarena), plus Mark Rosen's IMF and BAML LatAm IB Senior Advisor pedigree. Verified closes include Boa Praca / Wrist Ship Supply (December 19, 2024), Grupo IMSA / NovaScott to Scott Bader Brazil (June 2024), and AGS / Omni Transloading (February 2024). LatamIB (Miami; founded 2011) is a pure-play LatAm M&A and capital-raising boutique built around Alessio Mazzanti and Roberto Sanchez (Founders and Managing Directors with shared Violy Byorum & Partners NY pedigree from the late 1990s through 2003). The firm has executed 150+ advisory mandates with approximately $10 billion in aggregate closed transaction value. The structural decision tree: BroadSpan goes deeper on Brazil and Mexico with named in-country MDs; LatamIB goes deeper on aggregate volume and the founder-pair Violy Byorum DNA. For an $80M Brazilian sell-side specifically, pitch both and ask each to walk through buyer-pool composition, senior-banker time allocation, and the co-advisory option.

How does the Brickell financial-hub crystallization (Citadel + Microsoft + Apollo + Blackstone) affect Miami M&A advisory selection?

The Brickell financial-hub crystallization of 2024-2026 -- Citadel's $2.5 billion HQ at 1201 Brickell Bay Drive, Microsoft's LatAm HQ in Brickell (2024), Blackstone's significant Miami expansion (2024), and Apollo's Brickell lease (2021) -- changes Miami M&A advisor selection in three structural ways. First, the buyer-side institutional investor footprint inside Miami is materially deeper than at any prior point in the city's history; a Miami sell-side advisor pitching in 2026 should name actual Miami-deployed Citadel, Apollo, Blackstone, and Microsoft contacts rather than generic NYC headquarters references. Second, the structural compression between Miami sell-side advisory and bulge-bracket capital sources means a $50M-$200M Miami sell-side no longer requires flying in NYC senior bankers -- the senior buy-side dealmakers are increasingly in Miami already. Third, the migratory family-office buyer pool has crystallized concurrently: 245 verified Florida-based family offices, 30+ in Miami metro per Altss Q1 2025 family office data, with Banco Bradesco's Florida WUC doubling to $4 billion since 2019 and Itau Unibanco's Miami WUM at approximately $24 billion in 2025. The right Miami advisor names current relationships across the Brickell strategic-buyer set plus the migratory family-office buy-side rather than the longest list of historical NYC-PE-platform contacts.

Should I hire Cassel Salpeter or Houlihan Lokey Miami for a $50M Florida mid-market sale?

For a $50M Florida mid-market sale, the Cassel Salpeter vs Houlihan Lokey Miami choice breaks on balance-sheet need, comms protocol, and senior-banker autonomy. Cassel Salpeter (Coconut Grove since February 1, 2026; founded 2010 by James S. Cassel and Scott Salpeter) closed 50+ assignments in 2025 and 69 cumulative deals through January 2026 across aerospace, consumer, financial services, healthcare, technology, electronics, and industrials. Recent closes include Sunbelt Health to UHS (March 27, 2025) and Nicklaus Companies $35.7M Chapter 11 sale (March 9, 2026). The firm runs a true-independent senior-MD-led model. Houlihan Lokey Miami (3390 Mary Street) anchors the bank-owned-boutique tier with depth in financial services (Levine), asset management (McMahon), and Capital Solutions (Ryan, July 2025). The cost is comms protocol -- HL-mandated review chains and global-firm compliance can slow the senior banker's response cycle. For a $50M Florida generalist mid-market sale with no balance-sheet financing dependency, Cassel Salpeter is structurally better. For a $50M-$200M financial services or asset management mandate, Houlihan Lokey Miami is the right call.

What's a reasonable success fee for a $50M Miami M&A sell-side mandate?

Miami M&A advisors at the $50M EV mid-market band typically charge 1.5-2.5% blended success fee plus a $50K-$150K retainer credited against the success fee at close, with tail period of 12-24 months standard. The standard Lehman scale (5/4/3/2/1) on $50M produces approximately $700K of success fees -- about 1.4% blended. Sub-vertical-specialty firms (BroadSpan, LatamIB, Atlantico, Antarctica on cross-border; Bloom Miami on healthcare services; Lincoln Miami on TMT) sometimes negotiate modified-Lehman alternatives. Bank-owned-tier firms (Houlihan Lokey, Solomon Partners, Lincoln) typically run standard Lehman with a higher retainer floor ($75K-$150K). Cross-border mandates often carry a small premium (10-25 basis points blended) over single-country Florida mandates. Bulge-bracket Miami offices at this deal size typically demand $250K+ retainer plus $750K minimum success fee floor regardless of deal value -- structurally inefficient at the $50M EV band.

How do I evaluate a Miami M&A advisor's 2024-2025 cross-border track record?

Verify cross-border track record through three independent sources: the firm's transaction wall cross-checked against PR Newswire, BusinessWire, the buyer's SEC 8-K filings if publicly traded, and major LatAm financial press (Valor Economico Brazil, El Financiero Mexico, La Republica Colombia, Cronista Argentina); third-party research including TTR Data's Latin American M&A reports (2,118 LatAm deals in 9-month 2025 with $78.1B aggregate), SunBridge M&A's 2026 Miami Report ($4.7B Miami metro cross-border 2025), and Refresh Miami startup coverage; and direct seller references for two CEOs from cross-border closes in the last 12 months. The single highest-signal question: ask for engagement letter date and close date on the last three closed cross-border deals -- 9-12 months is typical for cross-border given dual-jurisdiction diligence, 15+ months a warning sign.

The Bloom Organization Miami office vs Cain Brothers vs Cassel Salpeter for a $30M Florida physician practice rollup -- how do I choose?

The Bloom Miami vs Cain Brothers vs Cassel Salpeter choice breaks on sub-vertical depth and senior-team continuity. Bloom (firm-wide Florida-rooted, Hallandale Beach HQ, with 30+ years and 200+ deals across $15B aggregate) anchors its Miami office around Steven Weiss (MD; ex-Ardent Investors and H.I.G. Advantage), with verified 2025 Miami-led closes (Evolved Science / Formula Wellness November 2025, Next ACO / Palm Beach ACO August 2025, Royal Senior Care / Welltower April 2025). Cain Brothers (a division of KeyBanc Capital Markets) anchors the bank-owned-boutique-tier alternative with KBCM parent's full debt and equity capital markets capability. Cassel Salpeter (Coconut Grove) anchors the Miami generalist alternative on senior-banker-engagement strength rather than sub-vertical buyer-relationship density. The structural decision tree: pure healthcare-services rollup with senior-care REIT and ACO buyer-pool relationships goes to Bloom Miami; healthcare-services rollup with parent-bank-capability dependency goes to Cain Brothers; mixed Florida-anchored mid-market deal goes to Cassel Salpeter. For a $30M Florida physician practice rollup specifically, Bloom Miami is structurally the strongest first call.

Lincoln International Miami's Spurrier Capital DNA -- is it the right fit for a $40M Miami fintech exit, or should I fly in NYC FT Partners?

For a $40M Miami fintech exit, the Lincoln Miami vs FT Partners NYC choice breaks on deal-size sweet spot, senior-banker engagement, and Miami fintech-ecosystem face-time access. Lincoln International Miami (opened October 2022; led by Clark Spurrier, MD and Chairman TMT Group plus US Management Committee member; anchored by Lincoln's 2022 acquisition of Spurrier Capital Partners) brings 30+ years of Spurrier's tech IB experience plus Lincoln parent's global reach (1,000+ professionals across 26 offices). For Miami-anchored fintech founders, local face-time access matters: Lincoln Miami can convene meetings at Citadel Brickell, Microsoft Brickell, Blackstone Miami, or Apollo Brickell on short notice. FT Partners (NYC; founded 2001 by Steve McLaughlin) is the global fintech specialty boutique with the deepest aggregate fintech deal volume of any independent firm. Structural decision tree: $40M fintech exit with primary buyer-pool inside the Miami Brickell ecosystem goes to Lincoln Miami; $40M fintech exit with primary buyer-pool outside Miami goes to FT Partners NYC. Miami metro fintech raised $1.8 billion in 2025 (30% of Miami VC) per Refresh Miami; global crypto M&A surged in 2025 -- approximately $8.6 billion across 267 deals tracked by Galaxy / Architect Partners across full-year 2025.

Should I run an EAST-Miami-style hospitality sale through JLL Hotels & Hospitality, or hire a generalist M&A boutique?