14 Best Boutique M&A Advisors in LA for $5M-$100M Deals (2026 Guide)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

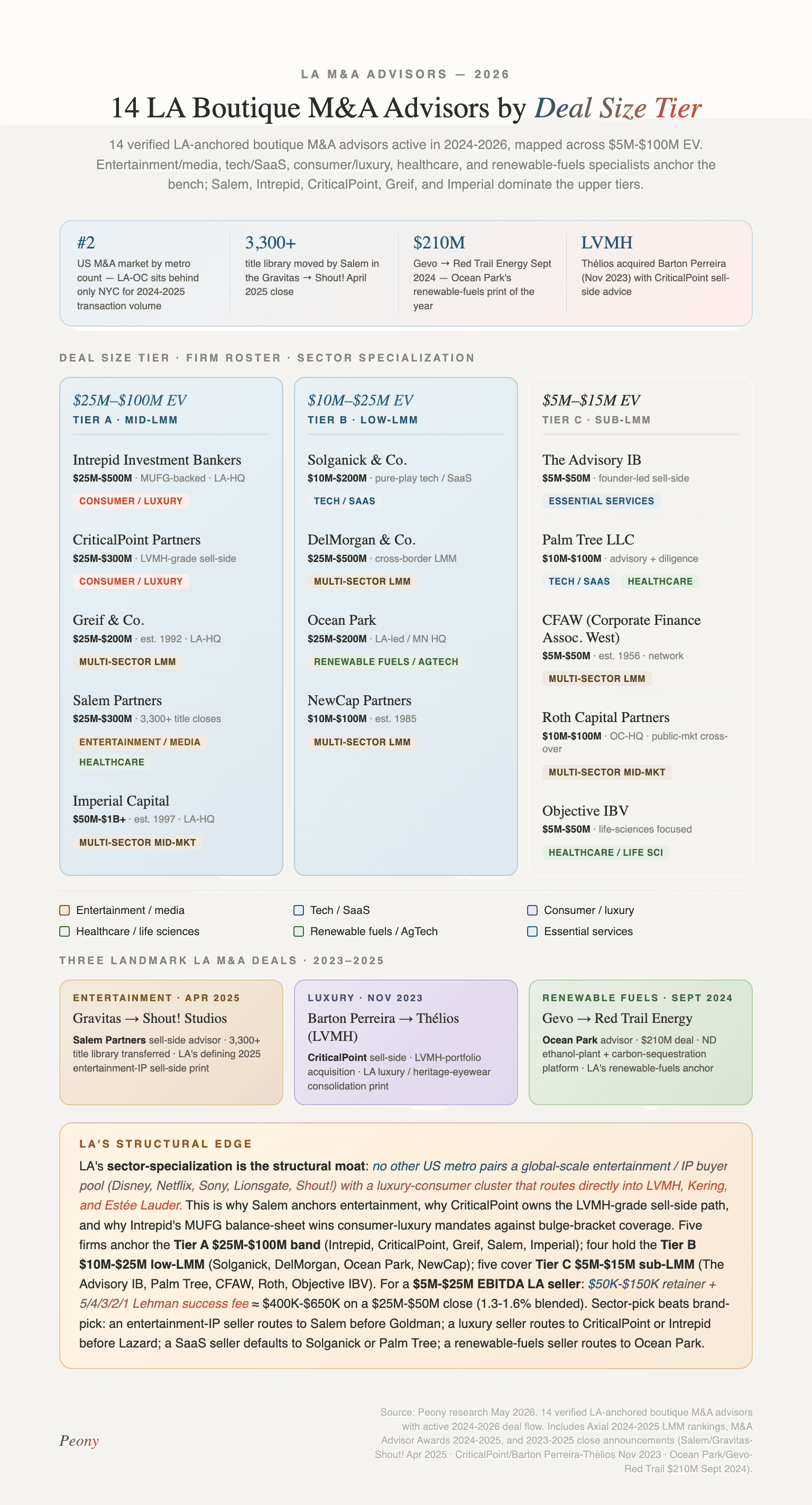

Quick answer: The best LA M&A advisors for $5M-$100M deals as of May 2026 are Intrepid Investment Bankers, CriticalPoint Partners, Greif & Co., Salem Partners, and Imperial Capital in the $25M-$100M Mid-LMM band; Solganick, DelMorgan & Co., Ocean Park Advisors, and NewCap Partners in the $10M-$25M Low-LMM band; and The Advisory IB, Palm Tree LLC, Corporate Finance Associates Worldwide, Roth Capital Partners, and Objective IBV in the $5M-$15M Sub-LMM band. The single hardest LA question -- who actually understands LA entertainment-tech + biotech crossover M&A -- breaks on sub-vertical specialty (media/entertainment vs. life sciences vs. consumer/luxury vs. renewable fuels), not firm-name brand.

Over the past year I've fielded data-room questions from Century City entertainment-tech sellers, biotech founders in Westwood and the UCLA/USC research triangle, Hollywood-media sponsors running agency-consolidation auctions (CAA/WME/UTA orbit), Beverly Hills luxury and Manhattan Beach DTC consumer founders, and Orange County tech-corridor CEOs (Newport Beach, Irvine, Costa Mesa). LA sits structurally apart from every other US M&A metro: it's the second-largest US M&A market by deal value, the global capital of entertainment and media M&A (Hollywood, agency consolidation, streaming-platform roll-ups), the anchor of West Coast healthcare and life sciences M&A (Cedars-Sinai, UCLA Health, the Westside biotech corridor), and the densest US market for consumer, beauty, and DTC brand exits (Beverly Hills luxury, Manhattan Beach and Newport Beach DTC, Pasadena consumer-brand incubators). I run Peony, a data room platform for M&A and private equity, and LA is one of the five US cities (Dallas, Chicago, Atlanta, Houston, and NYC being the others) where we see the most boutique M&A advisor deal flow on the platform. Building this LA guide as part of our city series -- see also our Dallas guide, Chicago guide, Atlanta guide, Houston guide, NYC guide, Washington DC guide, Philadelphia guide, and Phoenix guide -- LA aerospace and defense sellers in particular should triangulate the DC bench because Lincoln International's A&D co-heads in LA work the same buyer-pool axis as KippsDeSanto, Renaissance Strategic Advisors, and Houlihan Lokey ADG in DC.

This guide maps 14 verified LA-headquartered or LA-led boutique M&A advisory firms active in the $5M-$100M EV deal range as of May 2026. Every firm has been verified for LA presence, deal size band, and recent transaction activity. Bulge-bracket and elite-boutique upper-tier banks (Houlihan Lokey, Moelis & Co., Lazard) are excluded by design -- their structural sweet spot is $200M+ deals, and a $25M-$100M sell-side at any of those firms is a B-team engagement. PE platforms with in-house transaction-advisory desks (ClearLight Partners) are also excluded because their engagement model is not the same as a sell-side boutique. DC-headquartered or non-LA boutiques (FOCUS Investment Banking) are excluded even when they market into LA. Generalist boutiques whose primary book is below $5M EV (true business-broker shops) are also excluded, except where the firm's sub-LMM bench (NewCap, CFAW, Objective IBV) makes the cut on transaction volume and senior-advisor depth.

TL;DR: LA sits at the intersection of entertainment and media M&A (Salem Partners' Gravitas Ventures sale to Shout! Studios announced April 2025, FilmRise's merger with Oaktree Capital and Shout! Studios forming Radial Entertainment July 2025), consumer and luxury M&A (CriticalPoint Partners' Barton Perreira sale to Thelios (LVMH) announced November 2023, closed early 2024), and renewable energy and AgTech (Ocean Park Advisors' Gevo acquisition of Red Trail Energy $210M announced September 12 2024 and closed February 2025). Nationally, Axial recorded 12,856 lower-middle-market deals in 2025 (+17.1% YoY) -- a record high -- and LA boutiques anchor the upper end of that league table. For LA founders selling between $5M and $100M, the right answer is almost always an LA boutique: Intrepid Investment Bankers, CriticalPoint Partners, Greif & Co., Salem Partners, and Imperial Capital in the $25M-$100M Mid-LMM band; Solganick, DelMorgan & Co., Ocean Park Advisors, and NewCap Partners in the $10M-$25M Low-LMM band; and The Advisory IB, Palm Tree LLC, Corporate Finance Associates Worldwide, Roth Capital Partners, and Objective IBV in the $5M-$15M Sub-LMM band. Below: the firms, the deal-size bands, the fees, and three recent verified LA-tied closes that show how the metro's market actually works.

How I Verified This List

Every firm on this list passes four filters:

- LA metro headquarters or principal LA office -- Brentwood, West LA, Westwood, Beverly Hills, Century City, Santa Monica, Manhattan Beach, DTLA, Pasadena, Burbank, or Newport Beach / Orange County within the LA commuter shed; not a satellite branch staffed by a single analyst

- Verifiable transaction record -- closed at least 5 transactions in the $5M-$100M EV range in the last 36 months, sourced from press releases, Axial deal feeds, BusinessWire and PR Newswire announcements, or firm transaction walls

- Active 2024-2026 deal activity -- not a legacy firm coasting on pre-2020 relationships

- Lower-middle-market core -- modal deal size in the $5M-$100M EV band; firms whose primary book is below $5M EV (true Main-Street brokers) or above $300M EV (where geography stops mattering and bulge-bracket banks dominate) are excluded

I cross-referenced firm websites against Axial's 2024-2025 Top 100 LMM Investment Bank rankings, the Los Angeles Business Journal's annual Leaders of Influence: Investment Bankers list, the ACG Los Angeles chapter, and individual firm press releases for verified 2024-2026 transaction history. Where a firm claimed LA leadership but the senior team was actually based elsewhere, I dropped it. Houlihan Lokey (LA-headquartered but $200M+ structural sweet spot), Moelis & Co. (upper-LMM and middle market), and Lazard (institutional middle market) are excluded by design -- their structural sweet spot is $200M+ deals and the $25-100M EV LA seller is a B-team client at those firms. ClearLight Partners (PE platform, not a sell-side advisor) and FOCUS Investment Banking (DC-headquartered) are excluded by category.

One caveat on Ocean Park Advisors: the firm's corporate office is in Edina, Minnesota, not LA; however, its LA-led pure-play renewable-fuels/biofuels practice (Eric Ouyang LA-based, plus Frank Kim and Mark Fisler) is the only verified LA-led pure-play biofuels/AgTech boutique in the LMM landscape with 38+ biofuels transactions, so I've included Ocean Park as the LA-led specialty boutique in this category despite the Minnesota corporate HQ.

Deqian Jia, my co-founder, adds the technical readiness lens here:

"Across the LA data rooms we host, the gap between advisors who consistently close in 6 months and those who run 12-month processes is preparation. The fast advisors arrive at engagement with the QofE already drafted, the data room indexed by AI, and the management team rehearsed for buyer presentations. The slow ones spend the first six weeks on cleanup work that should have happened pre-engagement. LA's industry-leak risk is structurally higher than other US metros -- Hollywood production sets, Beverly Hills agency offices, and the Westside healthcare corridor all overlap socially, and a leaked CIM can reach a competitor's M&A desk by Monday morning. When you're picking an LA advisor, ask to see a sample data room from a recent close -- not a pitch deck. The folder structure tells you everything." -- Deqian Jia, Peony co-founder

Quick Comparison Table

| Firm | Deal Size (EV) | Sectors | Fee Model | Best For |

|---|---|---|---|---|

| Intrepid Investment Bankers | $25M-$300M | Consumer, FIG, food and beverage, beauty, healthcare, industrial | Lehman + retainer | Largest LA boutique by lifetime deal volume (152) |

| CriticalPoint Partners | $25M-$200M | Consumer, industrials, A and D, healthcare services, IT, media | Modified Lehman | LABJ Leader of Influence senior bench; PE Rolodex |

| Greif and Co. | $25M-$2B | Multi-sector consumer, packaging, services, security, RE | Lehman + retainer | Founder-led 33+ years; LA M and A icon Lloyd Greif |

| Salem Partners | $25M-$200M | Media and entertainment, life sciences, TMT, real estate | Lehman + retainer | LA's premier media and entertainment specialist |

| Imperial Capital | $25M-$500M | FIG, A and D, business services, consumer, energy, healthcare | Lehman + retainer | Full-service IB platform with restructuring practice |

| Solganick and Co. | $10M-$200M | Software, IT services, MSP/MSSP, cybersecurity, AI, healthcare IT | Lehman + retainer | Pure-play software / tech-services LA specialist |

| DelMorgan and Co. | $10M-$1B | Energy, tech, longevity / healthcare, optical, hostile takeovers | Lehman + retainer | Most globally oriented LA boutique; 80 countries |

| Ocean Park Advisors | $10M-$300M | Renewable fuels, AgTech, FIG, TMT, food and beverage | Lehman + retainer | LA-led renewable-fuels practice (38 biofuels deals); MN HQ |

| NewCap Partners | $5M-$50M | US Tech, California Tech, family-owned business, VC-backed | Lehman + retainer | Longest-running LA boutique (1987, 38 years) |

| The Advisory IB | $5M-$50M | HVAC, plumbing, electrical, restoration, fire, accounting | Modified Lehman | Pure-play essential services with Axial Top 5 status |

| Palm Tree LLC | $10M-$100M | Healthcare services, medical devices, biotech, PE buy-side DD | Hybrid advisory | Hybrid IB plus consulting plus interim CFO |

| Corporate Finance Associates (CFAW) | $5M-$50M | Multi-sector LMM owner-operator, healthcare practice expansion | Modified Lehman | Oldest firm (1956); 35-office global network |

| Roth Capital Partners | $10M-$200M | Business services, consumer, healthcare, industrial, sustainability | Lehman + retainer | Newport Beach 40-year track record; growth-company |

| Objective IBV | $5M-$100M | Healthcare and life sciences, business services, industrials | Lehman + retainer | Combined IB plus valuation; 500+ M and A engagements |

Why Is LA the M&A Advisor Capital for Entertainment, Healthcare, and Consumer?

LA in 2026 is the second-largest US M&A market by deal value and the dominant city for entertainment, media, healthcare-services, and consumer-brand deals. The math:

- Largest US entertainment and media M&A market by transaction count -- Hollywood film/TV production, agency consolidation (CAA, WME, UTA roll-ups across recent cycles), streaming-platform asset acquisitions (Netflix, Disney+, Paramount+, Peacock), and music-rights consolidation all anchor LA-resident advisor practices. Salem Partners' Gravitas / Shout! deal (April 2025) and the FilmRise / Oaktree / Shout! merger forming Radial Entertainment (July 2025) sit at the structural center of this market.

- Anchor of West Coast healthcare and life sciences M&A -- the Cedars-Sinai medical campus, the UCLA Health system, and the Westside biotech corridor (centered on the UCLA / USC research triangle) drive a $300B+ healthcare M&A pipeline annually. Salem Partners' Life Sciences practice (Co-Founder John Dyett raised $500M+ in equity and advised Adams Respiratory Therapeutics' $2.3B sale to Reckitt Benckiser and ZS Pharma's $2.7B sale to AstraZeneca), CriticalPoint's Los Angeles Reproductive Partners deal, Intrepid's Analyte Health to Brightstar (August 4, 2025), and Objective IBV's healthcare and life sciences specialty all operate from this corridor.

- Densest US consumer, luxury, and DTC market -- Beverly Hills luxury (Barton Perreira / Thelios LVMH eyewear), Manhattan Beach and Newport Beach DTC, Pasadena consumer-brand incubators, and the Glendale and Burbank consumer-products clusters drive a sub-vertical buyer pool no other US metro can match. Intrepid's MD Steve Davis Co-Heads Beauty/Personal Care/Wellness; CriticalPoint runs consumer and luxury mandates; Greif & Co. has historic positioning across Bristol Farms, Bumble Bee Seafoods, and beverage/spirits (Bacardi / Patron Tequila).

- Orange County tech corridor -- the OC tech ring (Newport Beach, Irvine, Costa Mesa, Aliso Viejo) anchors a software, fintech, and consumer-tech buyer pool that Roth Capital Partners (Newport Beach HQ), Solganick (Century City software / cybersecurity), and NewCap (LA + OC + Silicon Valley three-office Western footprint) all serve.

- Top-3 US LA County GDP -- LA County is consistently a top-3 US metro by GDP, anchoring a buyer pool of LA-resident PE platforms (Brentwood Associates, Aurora Capital Partners, Levine Leichtman Capital Partners, Marlin Equity, Platinum Equity, Leonard Green & Partners) and West-Coast strategic acquirers.

- Los Angeles Business Journal annual Leaders of Influence: Investment Bankers list -- editorially curated list that recognizes individual LA bankers; CriticalPoint MDs Diane Cabo and Nick Cipiti, Greif & Co. founder Lloyd Greif, and Solganick CEO Aaron Solganick all recur, signaling tier-leading dealmaker density in the metro's boutique bench.

- National Axial 2025 LMM deal count: 12,856 deals, +17.1% YoY -- a record high, with LA firms anchoring the top of the Top 100 LMM Investment Bank league table. The Advisory IB ranked Top 5 LMM Investment Bank Q1, Q2, and Q3 2025; Solganick and Ocean Park have recurring Axial league table appearances.

Why this matters for sellers: LA has the deepest specialty boutique bench of any US metro by entertainment, healthcare, and consumer sub-vertical. The media-and-entertainment dominance of Salem Partners, the consumer/beauty/wellness density of Intrepid (MD Steve Davis Co-Head), the luxury franchise of CriticalPoint (Barton Perreira / Thelios LVMH), the renewable-fuels specialty of Ocean Park (38 biofuels transactions, Gevo / Red Trail Energy $210M close February 2025), and the essential-services velocity of The Advisory IB (Axial Top 5 Q1-Q3 2025) are unique to LA.

The sectoral mix matters too. LA's entertainment and media depth produces a predictable buyer pool of studios, streaming platforms, and media-content strategic acquirers (Lionsgate, Sony Pictures Television, Warner Bros. Discovery, Disney corporate development, Paramount, Hachette, HarperCollins, Penguin Random House for adjacent publishing). The consumer cluster drives a defined set of PE consolidators (Brentwood Associates, Aurora Capital, Levine Leichtman, Marlin Equity) and luxury / DTC strategic acquirers (LVMH, Kering, Richemont, EssilorLuxottica). The healthcare base produces direct relationships between LA advisors and the West Coast PE healthcare-services platforms (Aurora Capital, Webster Equity Partners, Audax Group, ClearLight, InTandem Capital Partners), the academic-medical-center corporate development arms, and the public healthcare strategics.

What Should I Look For in an LA M&A Advisor?

Three filters matter more than firm prestige for $5M-$100M deals:

1. Sub-sector deal density. An LA advisor who has closed 10 entertainment, healthcare-services, beauty/wellness, software/MSP, renewable-fuels, or essential-services transactions in the last three years will run a tighter process than a generalist who has closed 50 deals across 15 sectors. Sub-sector density compounds: the advisor knows which LA PE platforms are active, which strategic acquirers are filling holes in their footprint, what working capital adjustments are standard, and what customer concentration thresholds will trigger an earnout. Ask any candidate LA advisor to name five recent buyers of comparable businesses in your sector. If they cannot, move on.

2. LA buyer Rolodex relevance. The right LA advisor maintains direct relationships with the 30-50 buyers most likely to acquire your specific business. For a $30M entertainment business, that means relationships with Lionsgate, Sony Pictures Television, Warner Bros. Discovery, Disney corporate development, Paramount, Endeavor, AMC Networks, and the LA-resident PE platforms (Sankaty Advisors, Comvest, Yucaipa, Vine Alternative Investments). For a $50M healthcare-services business, that means relationships with Aurora Capital Partners, Audax Group, Webster Equity Partners, InTandem Capital Partners, Frazier Healthcare, and the Cedars-Sinai / UCLA / USC corporate development arms. For a $25M consumer / beauty business, that means relationships with Brentwood Associates, Aurora Capital, Levine Leichtman Capital Partners, Castanea Partners, North Castle Partners, and the LVMH / Kering / Richemont strategic deal teams. For a $40M software / MSP business, that means relationships with Insight Partners, Vista Equity Partners, Thoma Bravo, Francisco Partners, the LA-resident growth equity firms (TPG Growth, Crescent Capital), and the public software strategics. A bigger firm with a thinner relationship-per-buyer ratio runs slower processes than a boutique with deep relationships in your sub-sector.

3. Process discipline. The fast LA advisors (Intrepid, CriticalPoint, Salem Partners, Greif, Solganick, Ocean Park, MidCap-equivalent service-focused operators, The Advisory IB) run 4-6 month processes from engagement to close. The slow ones run 9-12 month processes. The difference is preparation, not market conditions. Fast advisors arrive at engagement with the QofE provider already engaged, the data room template ready to populate, and the management team pre-briefed on buyer presentation expectations. Slow advisors do that work after engagement, which means the first 6 weeks of your exclusivity window evaporate before the first buyer call.

For deeper context on M&A preparation and the due diligence process, see our M&A guides. For data room setup specifically, our M&A data room guide covers what advisors expect to see ready by week 1 of the engagement. The companion Dallas, Chicago, Atlanta, Houston, Charlotte, and NYC city guides cover the same tier framework applied to other US metros -- LA's entertainment, agency, and DTC consumer specialty bench is structurally distinct from the banking-belt and healthcare-services depth that anchors the Charlotte playbook, and the two metros' specialty benches rarely overlap on the same mandate.

Which LA M&A Advisors Handle $25M-$100M Mid-LMM Deals?

For $25M-$100M EV mid-LMM deals out of LA, five firms anchor the band: Intrepid Investment Bankers (the largest by lifetime deal volume), CriticalPoint Partners (Manhattan Beach senior bench with PE Rolodex depth), Greif & Co. (Lloyd Greif's 33+ year founder-led independence), Salem Partners (LA's premier media and entertainment specialist), and Imperial Capital (full-service IB platform with restructuring capability). All five run senior-banker-led processes and have direct relationships with the strategic acquirers and PE platforms buying at this size.

1. Intrepid Investment Bankers, LLC

Headquarters: 11755 Wilshire Blvd. 22nd Floor, Los Angeles CA 90025 (Brentwood / West LA) Founded: 2010 by Ed Bagdasarian (ex-Barrington Associates Principal Partner), Adam Abramowitz, Jeremiah Mann, and W. Rosenberg; MUFG-owned since January 2019 Team: CEO Ed Bagdasarian; MD Lorie Beers Head of Special Situations (joined January 2023, 30+ years restructuring); MD Steve Davis Co-Head of Beauty / Personal Care / Wellness (joined 2011); MD Steven Nelson; senior bench across multiple verticals Deal size: $25M-$300M EV (some flex up to $500M) Sectors: Consumer products, financial institutions, food and beverage, distribution, industrial products, business services, healthcare, beauty / personal care / wellness, special situations Track record: 152 lifetime deals (117 M&A); largest LA boutique by transaction volume; MUFG cross-border access since the January 2019 acquisition

Intrepid Investment Bankers is the largest LA boutique by lifetime deal volume, founded 2010 by Ed Bagdasarian (ex-Barrington Associates Principal Partner) with co-founders Adam Abramowitz, Jeremiah Mann, and W. Rosenberg. Bagdasarian runs as CEO; the senior bench includes Lorie Beers (MD and Head of Special Situations, joined January 2023 with 30+ years of restructuring experience), Steve Davis (MD and Co-Head of Beauty / Personal Care / Wellness, joined 2011), and Steven Nelson (MD). The firm was acquired by MUFG (Mitsubishi UFJ Financial Group) in January 2019 and operates as MUFG's US middle-market M&A platform -- a structural advantage giving the firm Japanese cross-border buyer relationships that few LA peers can replicate. Sub-vertical depth: consumer products, financial institutions, food and beverage, distribution, industrial products, business services, healthcare, beauty / personal care / wellness, and special situations.

Recent closes: Analyte Health acquired by Brightstar Capital Partners (announced August 4, 2025, healthcare DTC platform); Cloudco Entertainment (owner of Care Bears IP and 30+ children's brands) acquired by IVEST Consumer Partners (2025, ~$100M, consumer IP); Snak King private-label snack producer investment from Falfurrias Management Partners (August 2024, food); i4cp PE round (April 8, 2025, business services / leadership development).

Best for: Sellers in $25M-$300M EV deals across consumer products, food and beverage, beauty and personal care, healthcare, financial institutions, and special situations who want the largest LA boutique by lifetime deal volume with MUFG cross-border buyer access. Intrepid's 152-deal lifetime track record (117 M&A) is the deepest of any LA boutique on this list.

Considerations: Intrepid runs multi-sector mandates by structural design. For pure-play media / entertainment, software / MSP, or renewable-fuels engagements, the sector specialists below are the closer fits.

2. CriticalPoint Partners, LLC

Headquarters: 1230 Rosecrans Avenue, Suite 170, Manhattan Beach CA 90266 Founded: 2012 by Matt Young (ex-Platinum Equity Principal, ex-Bear Stearns Tech IB) Team: Founder and CEO Matt Young; MD Diane Cabo (LABJ 2024 Leader of Influence, 2024 Banking and Finance Visionary, 2025 Dealmakers nominee); MD Nick Cipiti (LABJ 2024 Leader of Influence, 2024 Banking and Finance Visionary, 2025 Investment Banker of the Year finalist); MD Mike Vehaskari (LABJ 2025 Dealmakers nominee); Director Chris Kim Deal size: $25M-$200M EV Sectors: Consumer products and services, industrials, aerospace and defense, IT, media, communications, business services, healthcare services, transportation, distribution, manufacturing Track record: Hybrid IB plus private-capital arm; founder pedigree (ex-Platinum Equity Principal) gives PE-buyer Rolodex thicker than most LA peers their size

CriticalPoint Partners is a Manhattan Beach senior-bench boutique founded 2012 by Matt Young, who came out of Platinum Equity as a Principal after an earlier career at Bear Stearns Tech IB. The firm runs as a hybrid IB plus private-capital platform, with the private-capital arm taking principal positions alongside the M&A advisory practice. The senior bench is unusually decorated for a firm of this size: MD Diane Cabo (LABJ 2024 Leader of Influence, 2024 Banking and Finance Visionary, 2025 Dealmakers nominee), MD Nick Cipiti (LABJ 2024 Leader of Influence, 2024 Banking and Finance Visionary, 2025 Investment Banker of the Year finalist), and MD Mike Vehaskari (LABJ 2025 Dealmakers nominee) all carry editorially-curated LA Business Journal recognition. Sub-vertical depth: consumer products and services, industrials, aerospace and defense, IT, media, communications, business services, healthcare services, transportation, distribution, and manufacturing.

Recent closes: Barton Perreira acquired by Thelios (LVMH eyewear unit, announced November 2023, closed early 2024, ~$80M reportedly, luxury consumer); Los Angeles Reproductive Partners acquired by InTandem Capital Partners (healthcare services / fertility); VICI (e-commerce fashion); high-end multi-location pet retailer transaction.

Best for: Sellers in $25M-$200M EV consumer, luxury, healthcare-services, industrials, aerospace and defense, and IT deals who want a senior-MD-led boutique with editorially-curated LA Business Journal recognition and a PE-buyer Rolodex thicker than most LA peers their size. CriticalPoint's hybrid IB plus private-capital model is structurally distinct from any other Manhattan Beach or West LA peer. For LA aerospace and defense sellers whose buyer pool tilts toward cleared-services PE consolidators (Veritas Capital, Carlyle Aerospace & Defense, AE Industrial Partners, Sagewind Capital, Arlington Capital Partners) or Tier-1 strategic acquirers (SAIC, Leidos, CACI, Booz Allen Hamilton), our Washington DC M&A advisor guide covers the closest sibling specialty bench.

Considerations: CriticalPoint is a Manhattan Beach firm and its private-capital arm takes principal positions in select transactions -- ask in pitch whether your engagement is advisory-only or whether the firm intends to participate as a co-investor.

3. Greif & Co.

Headquarters: Downtown Los Angeles (US Bank Tower area, 633 W. 5th Street zone) Founded: 1992 by Lloyd Greif (ex-Vice Chairman of Sutro & Co., ~10 years) Team: Founder and CEO Lloyd Greif (LABJ 2025 M&A Industry Icon Award; LABJ 2024 Leaders of Influence: Investment Bankers honoree) Deal size: $25M-$2B EV (core LMM $25M-$200M) Sectors: Multi-sector -- consumer (Bristol Farms, Bumble Bee Seafoods), real estate brokerage, security services, packaging, footwear, water filtration Track record: Longest-running LA founder-led boutique (33+ years independent -- never sold); Lloyd Greif is the LA M&A icon

Greif & Co. positions itself as The Entrepreneur's Investment Bank and is the longest-running LA founder-led boutique -- 33+ years independent and never sold. Lloyd Greif founded the firm in 1992 after approximately 10 years as Vice Chairman of Sutro & Co., and continues to run the firm today. He received the LABJ 2025 M&A Industry Icon Award and is a recurring LABJ Leaders of Influence: Investment Bankers honoree. The firm runs entrepreneur-to-entrepreneur positioning -- the structural pitch is that founders selling their life's work want to talk to a founder, not a senior banker who left their last firm three years ago. Sub-vertical depth: multi-sector across consumer (Bristol Farms grocery, Bumble Bee Seafoods), real estate brokerage, security services, packaging, footwear, and water filtration.

Recent closes: Trinamix (Oracle Cloud / AI enterprise software) growth investment from AEA Elevate (announced March 23, 2026, "well into nine figures"); historic franchise includes CRH plc's $1.3B acquisition of C.R. Laurence Co., Bacardi's acquisition of Patron Tequila, the LBO of Pinkerton's Security, and the IPOs of Skechers, U.S. Filter, Smart and Final, and LA Gear.

Best for: Sellers in $25M-$2B EV multi-sector LA deals who want the longest-running LA founder-led boutique with entrepreneur-to-entrepreneur positioning and Lloyd Greif's 33+ year network. Greif & Co. is a default first-call for LA founders wanting to talk to the founder of the firm rather than a hired senior banker.

Considerations: Greif & Co. runs founder-led mandates with Lloyd Greif personally engaged on senior-banker work. Senior-bench depth below the founder is thinner than at Intrepid or CriticalPoint -- the engagement is by design Lloyd Greif-led. Ask in pitch about backup-banker depth and process-management staffing.

4. Salem Partners, LLC

Headquarters: 11111 Santa Monica Blvd, Suite 2250, Los Angeles CA 90025 (Westwood / West LA) Founded: 1997 by John Dyett (Life Sciences) and Stephen Prough (TMT) Team: Co-Founder and MD John Dyett (Head of Life Sciences; raised $500M+ equity; advised Adams Respiratory Therapeutics' $2.3B sale to Reckitt Benckiser and ZS Pharma's $2.7B sale to AstraZeneca); Co-Founder and CEO Stephen Prough (Head of TMT); MD Jeff Barcy (Real Estate, $20B+ raised); MD Brendan Houlihan (20+ year IB advisory, tech / media / entertainment); MD James Ratkovich (Real Estate, joined 2014); MD Ivar Combrinck (led the Gravitas / Shout! deal) Deal size: $25M-$200M+ EV Sectors: Media and entertainment (specialty -- film / TV / distribution), Life Sciences and Biotech, Technology / TMT, Real Estate Track record: Premier LA media and entertainment specialty boutique; Hollywood / film / TV / distribution focus unmatched among LA peers; Shout! Studios repeat-client signal of franchise quality

Salem Partners is LA's premier media and entertainment specialty boutique, founded in 1997 by John Dyett (Life Sciences) and Stephen Prough (TMT). The Westwood / West LA HQ sits at the structural center of LA's entertainment and life sciences corridors. Co-Founder and MD John Dyett runs Life Sciences and has raised $500M+ in equity, with anchor advisory roles on Adams Respiratory Therapeutics' $2.3B sale to Reckitt Benckiser and ZS Pharma's $2.7B sale to AstraZeneca. Co-Founder and CEO Stephen Prough runs TMT. Senior bench includes MD Jeff Barcy (Real Estate, $20B+ raised), MD Brendan Houlihan (20+ year IB advisory across tech / media / entertainment), MD James Ratkovich (Real Estate, joined 2014), and MD Ivar Combrinck (led the Gravitas / Shout! Studios deal). Sub-vertical depth: media and entertainment (film / TV / distribution specialty), Life Sciences and Biotech, Technology / TMT, and Real Estate.

Recent closes: Gravitas Ventures acquired by Shout! Studios (April 2025, MD Ivar Combrinck led, 3,300+ titles transferred); FilmRise acquired by Oaktree Capital Management plus Shout! Studios in a merger forming Radial Entertainment (July 2025, 70,000-title library); Bright North Studios acquired by Redbird IMI (2024); Fabric acquired by Xytech (2024, media / entertainment tech); Vine Alternative Investments premium content portfolio sale (2024); Shout! Studios buy-side acquisition of the Open Road catalog (2024).

Best for: Sellers in $25M-$200M+ EV media and entertainment, Life Sciences and Biotech, TMT, and Real Estate deals who want LA's premier media and entertainment specialty boutique. Salem Partners' Hollywood / film / TV / distribution franchise is unmatched among LA peers, and the Shout! Studios repeat-client relationship signals franchise quality on the buy-side as well as the sell-side.

Considerations: Salem Partners runs media / entertainment, Life Sciences, TMT, and Real Estate mandates by structural design. For pure-play consumer products, software / MSP, renewable-fuels, or essential-services engagements, other firms are the closer fits. For LA founders running pure-play biotech or life sciences sales where the strategic-buyer pool is concentrated in the Boston / Cambridge corridor (Pfizer, Eli Lilly, Bristol-Myers, Sanofi, Merck, Novartis), our Boston M&A advisor guide covers the East Coast biotech specialty bench (Aquilo Partners, Outcome Capital, Back Bay Life Science Advisors).

5. Imperial Capital, LLC

Headquarters: 10100 Santa Monica Blvd., Suite 2400, Los Angeles CA 90067 (Century City) Founded: 1997 Team: 150+ professionals across 12 industry verticals; senior team led by the firm's longstanding Century City partnership Deal size: $25M-$500M+ EV (borderline LMM / upper-mid; fits at upper edge of this tier) Sectors: 12 verticals including financial services / banking, aerospace and defense, business services, consumer, energy, gaming, healthcare, industrials, real estate, security, technology Track record: 447 lifetime deals; 204 deals tracked (129 M&A plus 75 funding rounds as of October 2025); $49.6M annual revenue 2025; full-service IB platform with capital markets plus restructuring plus M&A

Imperial Capital is a full-service Century City investment bank, founded 1997, with 150+ professionals across 12 industry verticals. The firm sits at the borderline between LMM boutique and upper-mid IB -- the $25M-$500M+ EV deal range overlaps with Tier A boutiques on the lower end but extends well into the upper-LMM band. Structural advantage: Imperial Capital runs a broader full-service platform than the pure-play M&A boutiques on this list, with capital markets, restructuring and recapitalization, and M&A advisory practices that compound across the firm's 12 industry verticals (financial services / banking, aerospace and defense, business services, consumer, energy, gaming, healthcare, industrials, real estate, security, technology).

Recent closes: SafeTrust $17.7M Series B financing (February 24, 2025, general financial advisor); 447 lifetime deals; 204 deals tracked across 129 M&A and 75 funding rounds as of October 2025; $49.6M annual revenue 2025.

Best for: Sellers in $25M-$500M+ EV financial services, aerospace and defense, business services, consumer, energy, gaming, healthcare, industrials, real estate, security, and technology deals who want a full-service Century City IB platform with capital markets and restructuring depth. Imperial Capital's restructuring / recapitalization arm is structurally distinct from any pure-play M&A boutique on this list.

Considerations: Imperial Capital straddles the boutique / IB tier -- the firm is at the upper edge of this list's deal-size band, and for sub-$25M EV mandates, the Tier B and Tier C boutiques are the closer fits. The firm's restructuring practice means some engagements involve capital markets or balance-sheet work alongside M&A; ask in pitch about the specific senior banker who will run a pure sell-side mandate. Several LA firms -- Imperial Capital, Roth Capital Partners, and Ocean Park among them -- run a full capital markets advisory practice alongside sell-side M&A, which changes both the fee math and when a bank beats a boutique; see our advisor-vs-bank guide and fee guide.

Which LA M&A Advisors Handle $10M-$25M Low-LMM Deals?

For $10M-$25M EV low-LMM deals, four LA firms own this band: Solganick & Co. (Century City pure-play software / tech-services specialist), DelMorgan & Co. (Santa Monica's most globally oriented boutique), Ocean Park Advisors (LA's renewable-fuels and AgTech specialty), and NewCap Partners (the longest-running LA boutique, 1987).

6. Solganick & Co.

Headquarters: 2029 Century Park East, Suite 400, Los Angeles CA 90067 (Century City) Founded: 2009 by Aaron Solganick (CEO and Founder; ~30-year tech IB experience; multi-year LABJ Leaders of Influence honoree) Team: CEO and Founder Aaron Solganick; MDs Frank Grant and Ramesh Menon; Texas MD additions in 2024 expansion Deal size: $10M-$200M EV (LMM core $20M-$100M) Sectors: Software, IT services and consulting, MSPs / MSSPs (managed service providers / managed security service providers), cybersecurity, AI, cloud computing, data analytics, healthcare IT, Snowflake / data partner ecosystem Track record: Pure-play software / tech-services LA specialist; founder-led ~$20B lifetime deals; 3 Snowflake partner sales trailing 24 months plus 4 additional data analytics firm sales

Solganick & Co. is LA's pure-play software and tech-services specialist, founded 2009 by Aaron Solganick (CEO and Founder) after ~30 years of tech IB experience. Solganick is a multi-year LA Business Journal Leaders of Influence: Investment Bankers honoree. The senior bench includes MDs Frank Grant and Ramesh Menon, with a 2024 Texas expansion adding additional senior bankers. Sub-vertical depth: software, IT services and consulting, MSPs / MSSPs, cybersecurity, AI, cloud computing, data analytics, healthcare IT, and the Snowflake / data partner ecosystem (3 Snowflake partner sales in the trailing 24 months plus 4 additional data analytics firm sales). The firm positions as an "AI-enabled and data-driven investment bank" and publishes quarterly market reports (cybersecurity Q2 2025, MSP / MSSP YTD 2025, technology services Q1-Q4 quarterly).

Recent closes: Columbia Advisory Group acquired by Complete (backed by Heritage Holding) -- announced December 26, 2025, closed Q2 2025, MSP / cybersecurity / GRC services, competitive process targeting PE-backed strategic buyers; 3 Snowflake partner sales in trailing 24 months; 4 additional data analytics firm sales.

Best for: Sellers in $10M-$200M EV software, IT services, MSP / MSSP, cybersecurity, AI, cloud computing, data analytics, and healthcare IT deals who want the most pure-play tech-services LA boutique with founder-led ~$20B lifetime deals. Solganick's Snowflake / data partner ecosystem relationships are structurally distinct from any other LA boutique.

Considerations: Solganick runs software and tech-services mandates by structural design. For media / entertainment, consumer, healthcare-services, renewable-fuels, or essential-services engagements, other firms are the closer fits.

7. DelMorgan & Co.

Headquarters: Santa Monica, CA Founded: 2011 by Neil Morganbesser (President and CEO) and Rob Delgado (Co-Founder and Chairman) Team: Founder and CEO Neil Morganbesser; Co-Founder and Chairman Rob Delgado Deal size: $10M-$1B+ EV (broad range; LMM core but firm has done multi-billion mandates internationally) Sectors: Multi-sector global -- energy, technology, longevity / healthcare, optical infrastructure, hostile shareholder takeovers, unsolicited acquisitions; serves companies, institutions, governments, and individuals across 80 countries Track record: Axial 3Q23 ranking: 6th of 571 IBs on Top 25 LMM League Table; $300B+ in transactions across 80 countries; historic clientele includes The Walt Disney Co., PayPal, AT&T (advisory roles)

DelMorgan & Co. is the most globally oriented LA boutique, founded 2011 by Neil Morganbesser (President and CEO) and Rob Delgado (Co-Founder and Chairman). The Santa Monica HQ runs cross-border and unconventional mandates -- energy, technology, longevity / healthcare, optical infrastructure, hostile shareholder takeovers, unsolicited acquisitions, and special-situations advisory across 80 countries. Structural advantage: DelMorgan specializes in fewer-but-bigger international engagements where most LA boutiques have no buyer relationships. The firm's historic advisory clientele includes The Walt Disney Co., PayPal, and AT&T, and the firm reports $300B+ in transactions across 80 countries. Axial ranked DelMorgan 6th of 571 IBs on the 3Q23 Top 25 LMM League Table.

Track record includes: Angry Chickz debt financing (2024 per Axial), historic mandates with Clearday (longevity healthcare 2022) and Laser Light Communications (optical infrastructure 2023), Mighty Pilates acquisition (per Axial), plus active 2024-2025 mandate book per Axial 3Q23 Top 25 LMM League Table ranking (6th of 571 IBs); SBR Energy financing engagement.

Best for: Sellers in $10M-$1B+ EV cross-border or unconventional mandates -- including hostile shareholder takeovers, unsolicited acquisitions, sovereign-level engagements, and longevity / healthcare deals -- where the buyer pool extends well beyond US-only relationships. DelMorgan's 80-country footprint and $300B+ lifetime transaction history are structurally distinct from any other LA boutique.

Considerations: DelMorgan runs cross-border and unconventional mandates by structural design. For US-only LMM sell-side processes in software, media, or essential services, other firms are the closer fits.

8. Ocean Park Advisors / Ocean Park Securities

Headquarters: Edina, Minnesota (corporate office, 7300 Metro Boulevard, Suite 305); active LA-led practice including MDs Eric Ouyang (LA-based, 20+yr IB) + Frank Kim + Mark Fisler Founded: 2004 Team: MD Eric Ouyang (LA-based, ~20-year IB; $50B+ in strategic advisory and capital raising); MD Frank Kim (16+ year IB and corporate development; $2B+ M&A; $500M+ capital raises); MD Mark Fisler (renewable-fuels / biofuels practice lead; led the Gevo deal) Deal size: $10M-$300M EV (LMM core; some larger renewables / AgTech mandates) Sectors: Renewable energy / fuels (biofuels, sustainable aviation fuel), agribusiness, agriculture technology (AgTech), financial institutions, technology / media / telecom, food and beverage; restructuring and crisis management Track record: 38+ biofuels transactions (most-active LA-led boutique in biofuels / SAF / AgTech); 80+ engagements lifetime; Ocean Park Securities subsidiary handles capital markets work alongside M&A

Ocean Park Advisors is the LA-led pure-play renewable-fuels and AgTech specialty boutique, founded 2004. The firm's corporate office is in Edina, Minnesota, with the LA bench anchoring the renewable-fuels and AgTech practice. Differentiator: LA-led pure-play renewable-fuels/biofuels practice (38+ biofuels transactions); firm corporate HQ in Edina MN with Eric Ouyang anchoring the LA bench. The senior bench includes MD Eric Ouyang (LA-based, ~20-year IB experience, $50B+ in strategic advisory and capital raising), MD Frank Kim (16+ year IB and corporate development, $2B+ M&A and $500M+ capital raises), and MD Mark Fisler (renewable-fuels / biofuels practice lead). Structural advantage: Ocean Park has executed 38+ biofuels transactions -- the most-active LA-led boutique in biofuels, sustainable aviation fuel (SAF), and AgTech -- and combines M&A advisory with restructuring and crisis management plus capital markets work through the Ocean Park Securities subsidiary. The firm's hybrid sector boutique positioning (energy plus AgTech) is distinctive in the LA bench. Sub-vertical depth: renewable energy / fuels, agribusiness, AgTech, financial institutions, TMT, food and beverage, and restructuring / crisis management.

Recent closes: Gevo's acquisition of Red Trail Energy ($210M, announced September 12, 2024, closed February 2025) -- exclusive financial advisor and sole lead arranger to Gevo on M&A and financing; arranged a $105M senior secured term loan facility from Orion Infrastructure Capital; the 65M-gallon-per-year ethanol plant plus carbon-capture-and-sequestration (CCS) assets in Richardton, ND, were renamed "Net-Zero North" -- Ocean Park's 38th biofuels transaction.

Best for: Sellers in $10M-$300M EV renewable-fuels (biofuels, SAF), AgTech, agribusiness, financial institutions, TMT, and food and beverage deals who want the most-active LA biofuels boutique with combined M&A plus restructuring plus capital markets capability. Ocean Park's 38+ biofuels deal track record is the deepest of any LA boutique on this list.

Considerations: Ocean Park runs renewable-fuels, AgTech, and adjacent mandates by structural design. For media / entertainment, consumer / luxury, software / MSP, healthcare-services, or essential-services engagements, other firms are the closer fits.

9. NewCap Partners, Inc.

Headquarters: Los Angeles, CA (offices in OC and Silicon Valley) Founded: 1987 (38+ years -- among the longest-tenured LA boutiques) Team: 6 senior team members and ~16 employees across North America and Asia Deal size: $5M-$50M EV (true LMM core; smaller Series A capital raises) Sectors: Multi-sector -- middle-market companies, entrepreneurs, family-owned businesses, and VC-backed firms; primarily US Tech and California Tech Track record: 32-55 lifetime deals; longest-running LA-founded boutique (1987); strong family-business / closely-held private company franchise

NewCap Partners is the longest-running LA-founded boutique, founded 1987 -- 38+ years of independent operation. The firm runs a three-office Western footprint (LA, OC, Silicon Valley) with 6 senior team members and ~16 employees across North America and Asia. Structural advantage: NewCap's smaller deal-size band ($5M-$50M EV) makes the firm a natural fit for sub-$25M EV mandates that mid-LMM firms (Intrepid, CriticalPoint, Greif, Salem) won't accept. The franchise is anchored on family-business and closely-held private company engagements, with sub-vertical depth in middle-market companies, entrepreneurs, family-owned businesses, and VC-backed firms (primarily US Tech and California Tech). Lifetime deals: 32-55 across the 38-year operating history.

Recent closes: Unified Teldata (general advisor 2025); active 2024-2026 mandate book across family-business, closely-held private company, and US Tech / California Tech engagements; firm structures lean toward smaller-deal-size discrete advisory mandates given the $5M-$50M EV core band.

Best for: Sellers in $5M-$50M EV family-owned businesses, closely-held private companies, US Tech, and California Tech who want the longest-running LA boutique (1987) with a three-office Western footprint and a $5M EV deal floor. NewCap's family-business franchise is the deepest of any LA boutique on this list.

Considerations: NewCap's specific 2024-2026 deal trail is lighter in public listings than Solganick or Ocean Park because the firm runs a confidential family-business engagement model. Ask for closed-deal references during the pitch process.

Which LA M&A Advisors Handle $5M-$15M Sub-LMM Deals?

For $5M-$15M EV sub-LMM deals, five LA firms own this band: The Advisory IB (the newest entrant -- 100% essential-services specialist with Axial Top 5 status), Palm Tree LLC (hybrid IB plus consulting plus interim CFO with PE buy-side franchise), Corporate Finance Associates Worldwide (CFAW) (the oldest firm at 70 years; 35-office global network), Roth Capital Partners (Newport Beach 40-year track record), and Objective IBV (combined IB plus valuation with healthcare and life sciences specialty).

10. The Advisory IB

Headquarters: Beverly Hills, CA Founded: 2024 (newest firm on this list) Team: FINRA-licensed senior team led by the firm's founder; AI-enabled buyer-targeting tool Deal size: $5M-$50M EV (clients $2M-$100M revenue, 5+ years operating history) Sectors: Pure-play essential services -- HVAC, plumbing, electrical, landscaping, restoration, fire and life safety, accounting, "real-world businesses" Track record: Axial "Top 5 Lower Middle Market Investment Bank" Q1, Q2, and Q3 2025; firm-stated 81 deals in 2025 with $630M+ in transaction volume; 4 closings reported December 2025 - February 2026 per Axial

The Advisory IB positions itself as The Investment Bank for Essential Services and is the newest firm on this list -- founded 2024 in Beverly Hills. Despite the short operating history, the firm captured Axial Top 5 Lower Middle Market Investment Bank rankings in Q1, Q2, and Q3 2025, with firm-stated metrics of 81 deals in 2025 and $630M+ in transaction volume (4 closings reported December 2025 - February 2026 per Axial). Structural advantage: 100% essential-services specialty captures the home-services rollup wave (HVAC, plumbing, electrical, landscaping, restoration, fire and life safety, accounting) that PE consolidators have driven hard since 2023 -- a mega-theme that legacy generalist boutiques have approached opportunistically rather than as a dedicated practice. The firm is FINRA-licensed and uses an AI-enabled buyer-targeting tool to map sub-vertical PE consolidators against essential-services sellers. Client profile: $2M-$100M revenue, 5+ years operating history.

Recent closes: Active 2024-2026 mandate book across HVAC, plumbing, electrical, landscaping, restoration, fire and life safety, and accounting essential-services engagements; 81 firm-stated 2025 deals with $630M+ aggregate transaction volume; 4 closings reported December 2025 - February 2026 per Axial.

Best for: Sellers in $5M-$50M EV essential-services deals -- HVAC, plumbing, electrical, landscaping, restoration, fire and life safety, accounting -- who want the most pure-play essential-services LA boutique with FINRA licensing, AI-enabled buyer-targeting, and Axial Top 5 LMM Investment Bank recognition across Q1, Q2, and Q3 2025. The Advisory IB captures the home-services rollup wave better than any LA generalist on this list.

Considerations: The Advisory IB is a newer firm (founded 2024). Ask for closed-deal references and the specific senior banker who will run the engagement -- the firm's volume-led model means deal-team staffing matters as much as the firm-name pitch.

11. Palm Tree LLC

Headquarters: Los Angeles, CA (offices in LA, Chicago, Detroit, and Dallas) Founded: 2010 Team: 134 employees across the four-office network; senior team supports investment banking, transaction support consulting, and interim CFO services Deal size: $10M-$100M EV (LMM core; firm functions across PE investment lifecycle) Sectors: Healthcare services, medical devices, biotech, plus diverse PE buy-side support across multiple sectors; hybrid model (investment banking plus consulting plus accounting plus financial due diligence) Track record: 32 total tracked deals; heavy PE buy-side franchise with financial due diligence as a core revenue line; multi-office footprint compounds buyer Rolodex

Palm Tree LLC is a hybrid LA boutique founded 2010 that runs investment banking alongside transaction support consulting and interim CFO services. The four-office network (LA, Chicago, Detroit, Dallas) compounds buyer Rolodex across the Midwest, Southwest, and West Coast PE platforms. Structural advantage: Palm Tree's hybrid model means the firm runs financial due diligence engagements as a core revenue line, which gives the firm direct visibility into which PE buyers are active across sub-verticals. Sub-vertical depth: healthcare services, medical devices, biotech, plus diverse PE buy-side support across multiple sectors. Total tracked deals: 32 across the firm's 134-employee footprint.

Recent closes: Palm Tree Securities advised Detroit Manufacturing Systems (DMS) on its buy-side acquisition of Android Industries and Avancez Assembly, forming Voltava LLC (closed December 12, 2025); active 2024-2026 mandate book across healthcare diligence engagements (PE buy-side, unnamed for confidentiality) and the firm's IB practice.

Best for: Sellers in $10M-$100M EV healthcare services, medical devices, biotech, and PE-rolodex-driven sectors who want a hybrid IB plus consulting platform with multi-office (LA / Chicago / Detroit / Dallas) buyer Rolodex and a heavy PE buy-side franchise. Palm Tree's interim CFO services make the firm a natural fit for sellers who need bench depth on the financial-controls work pre-engagement.

Considerations: Palm Tree's hybrid model means the firm balances PE buy-side engagements (financial DD) against sell-side mandates -- ask in pitch about the specific senior banker who will run a pure sell-side engagement and the engagement's economics relative to the firm's PE-rolodex-driven services.

12. Corporate Finance Associates Worldwide (CFAW)

Headquarters: Greater Los Angeles, CA (corporate office) -- 35 offices in Americas / Europe / Asia network Founded: 1956 in Columbia, South Carolina; corporate office now in greater LA -- ~70-year track record Team: Senior LA-based MDs Peter Heydenrych and Pablo Ocasio (LA / Orange County practice); Healthcare Practice Advisor Albert T. Kelley (joined LA November 2025) Deal size: $5M-$50M EV (true LMM / sub-LMM; founder / family-owned business focus) Sectors: Multi-sector LMM -- divestitures, mergers, acquisitions, recapitalizations for owner-operated businesses; healthcare practice expansion in LA Track record: Oldest firm on this list (founded 1956 -- 70 years); most distributed network model (35 offices globally with LA as corporate HQ); strong sub-$25M EV deal flow

Corporate Finance Associates Worldwide (CFAW) is the oldest firm on this list, founded 1956 in Columbia, South Carolina, with corporate office now in greater LA. The 70-year track record runs across 35 offices in the Americas, Europe, and Asia -- the most distributed network model among LA-anchored boutiques on this list. Senior LA-based MDs Peter Heydenrych and Pablo Ocasio anchor the LA / Orange County practice. Albert T. Kelley joined as Healthcare Practice Advisor in November 2025, expanding the firm's healthcare practice in LA. Structural advantage: CFAW's distributed-network model means the firm can run cross-border and cross-region engagements that single-office boutiques cannot. Sub-vertical depth: multi-sector LMM divestitures, mergers, acquisitions, and recapitalizations for owner-operated businesses, with healthcare practice expansion in LA from November 2025 forward.

Recent closes: IntuitiveCare investment from Arcadea Group (May 28, 2025) -- Brazilian healthcare RCM cross-border engagement led by CFAW Worldwide network; Gas Clip Technologies acquired by Chimney Rock Equity Partners (closed March 2026); active 2024-2026 mandate book across multi-sector LMM owner-operator engagements.

Best for: Sellers in $5M-$50M EV multi-sector LMM deals who want the oldest firm on this list (1956) with the most distributed network model (35 offices globally, LA corporate HQ). CFAW's owner-operated business franchise and healthcare practice expansion in LA from November 2025 are structurally distinct in the sub-LMM band.

Considerations: CFAW operates as a network model rather than a single LA bench -- service depth varies across the 35-office footprint. Ask in pitch which specific LA MD or healthcare practice advisor will run the engagement and request 2-3 closed-deal references from the past 18 months.

13. Roth Capital Partners, LLC

Headquarters: Newport Beach, CA (also offices in NY, Chicago, LA proper, SF, Austin, Boston, Miami Beach) Founded: 1984 (40+ years) Team: 235+ staff across 10 offices; senior bench across the Newport Beach HQ and 9 satellite offices Deal size: $10M-$200M+ EV Sectors: Business services, consumer, healthcare, industrial growth, resources, sustainability, technology and media -- growth companies Track record: Newport Beach 40-year track record; 400+ M&A and advisory assignments lifetime; 2,300+ deals lifetime; $100.5B+ raised; strong micro-cap and small-cap equity research and capital markets franchise

Roth Capital Partners is the Newport Beach Orange County M&A flagship, founded 1984 -- 40+ years of operating history. The firm runs 235+ staff across 10 offices (Newport Beach HQ plus NY, Chicago, LA proper, SF, Austin, Boston, Miami Beach), with a senior bench across the Newport Beach HQ and the 9 satellite offices. Structural advantage: Roth historically anchored micro-cap and small-cap equity research and capital markets, and the cross-office deal-flow advantage compounds the firm's growth-company franchise across business services, consumer, healthcare, industrial growth, resources, sustainability, and technology and media. Lifetime metrics: 2,300+ deals, 400+ M&A and advisory assignments, and $100.5B+ raised.

Recent closes: Active 2024-2026 mandate book across business services, consumer, healthcare, industrial growth, resources, sustainability, and technology and media engagements; 400+ M&A and advisory assignments lifetime sit alongside the firm's capital markets practice.

Best for: Sellers in $10M-$200M+ EV business services, consumer, healthcare, industrial growth, resources, sustainability, and technology and media deals who want the Orange County M&A flagship with a Newport Beach 40-year track record and a 10-office cross-regional footprint. Roth's micro-cap and small-cap equity research and capital markets franchise is structurally distinct from any pure-play LMM boutique on this list.

Considerations: Roth Capital Partners runs a broader full-service platform than the pure-play M&A boutiques on this list (capital markets, equity research, and M&A advisory across the 10-office footprint). For sellers wanting a pure-play LMM M&A boutique, Solganick (software / tech), Ocean Park (renewable fuels), or Salem Partners (media / entertainment) are the closer fits.

14. Objective, Investment Banking and Valuation (Objective IBV)

Headquarters: LA office plus San Diego HQ Founded: 2006 (formerly Objective Capital Partners; rebranded to Objective IBV) Team: Senior team executed 500+ M&A advisory engagements plus thousands of valuations Deal size: $5M-$100M EV (LMM core; valuation work spans wider) Sectors: Healthcare and life sciences (specialty), business services, essential services, industrials; valuation advisory Track record: Awards: Best Investment Bank and Valuation Firm 2025 USA, Corporate / Strategic Deal of The Year (Over $100MM) 2024, Cross-Border Deal of the Year ($100MM-$1B) 2024, Valuation Firm of The Year 2024

Objective, Investment Banking and Valuation (Objective IBV, formerly Objective Capital Partners) is a combined IB plus valuation boutique, founded 2006 with offices in LA and San Diego HQ. The senior team has executed 500+ M&A advisory engagements plus thousands of valuations, and the firm has captured an unusual concentration of awards: Best Investment Bank and Valuation Firm 2025 USA, Corporate / Strategic Deal of The Year (Over $100MM) 2024, Cross-Border Deal of the Year ($100MM-$1B) 2024, and Valuation Firm of The Year 2024. Structural advantage: the combined IB plus valuation practice gives Objective dual revenue streams and credible competitive positioning in healthcare and life sciences -- a sector where pre-engagement valuation work is structurally important. Sub-vertical depth: healthcare and life sciences (specialty), business services, essential services, industrials, and valuation advisory.

Track record includes: Awards-led pipeline anchored by Best Investment Bank and Valuation Firm 2025 USA, Corporate / Strategic Deal of The Year (Over $100MM) 2024, Cross-Border Deal of the Year ($100MM-$1B) 2024, and Valuation Firm of The Year 2024; active 2024-2025 mandate book across healthcare and life sciences, business services, essential services, and industrials engagements alongside the firm's valuation advisory practice.

Best for: Sellers in $5M-$100M EV healthcare and life sciences, business services, essential services, and industrials deals who want a combined IB plus valuation boutique with multi-award recognition across 2024-2025 and a senior team that has executed 500+ M&A advisory engagements. Objective IBV's healthcare and life sciences specialty in LA is credible competitive positioning.

Considerations: Objective IBV is split between LA office and San Diego HQ -- ask in pitch which office and which senior MD will run the engagement, and verify the senior banker has closed deals in your specific sub-sector in the last 18 months.

What Recent LA M&A Deals Show How These Advisors Actually Work?

Three closed LA-tied transactions from November 2023 through July 2025 show the spread of the metro's boutique M&A market across entertainment / media, consumer / luxury, and renewable energy / AgTech: Salem Partners' Gravitas Ventures sale to Shout! Studios (April 2025) plus the FilmRise / Oaktree / Shout! merger forming Radial Entertainment (July 2025), CriticalPoint Partners' Barton Perreira sale to Thelios (LVMH) (announced November 2023, closed early 2024), and Ocean Park Advisors' Gevo acquisition of Red Trail Energy ($210M, announced September 12, 2024 and closed February 2025). Each deal demonstrates why LA's middle-market boutique bench is competitive nationally on transactions where sub-vertical relationship density compresses the buyer pool from 200 generalists to 30-50 highly relevant strategic and PE-platform acquirers.

Deal 1 (Entertainment / Media): Salem Partners-Advised Gravitas / Shout! Sale plus FilmRise / Oaktree / Shout! Merger

Buyer (Deal A): Shout! Studios (LA-based independent media distributor with deep catalog ownership) Target (Deal A): Gravitas Ventures (independent film distribution platform with 3,300+ titles) Buyer (Deal B): Oaktree Capital Management plus Shout! Studios (combined ownership in the merger forming Radial Entertainment) Target (Deal B): FilmRise (independent media library with 70,000-title catalog) LA advisor: Salem Partners served as financial advisor on both transactions -- MD Ivar Combrinck led the Gravitas / Shout! deal Announced: Gravitas / Shout! April 2025; FilmRise / Oaktree / Shout! / Radial Entertainment July 2025

The Gravitas / Shout! transaction is a 3,300+ title independent film distribution catalog acquired by Shout! Studios, a LA-based independent media distributor with deep catalog ownership across cult and classic film and TV. MD Ivar Combrinck ran the sell-side mandate end-to-end. Three months later, Salem Partners advised on the FilmRise transaction in which Oaktree Capital Management acquired FilmRise's 70,000-title independent media library and merged it with Shout! Studios to form Radial Entertainment (announced July 2025) -- a structural consolidation that combined two LA-resident independent media platforms into a national-scale catalog franchise. The Salem Partners role on both transactions illustrates the firm's repeat-client franchise quality with Shout! Studios and the depth of relationships across LA's independent media and film distribution corridor.

Why this matters for LA sellers in the $5M-$100M range: Entertainment / media transactions concentrate disproportionately in LA advisor mandates because the information-and-content boutiques (Salem Partners' film / TV / distribution franchise, Greif & Co.'s historic media positioning) maintain direct relationships with the LA-resident strategic acquirers and PE platforms (Shout! Studios, Oaktree, Vine Alternative Investments, Yucaipa, Comvest) that anchor the buyer pool. For LA entertainment sellers in the lower-middle-market and middle-market, the Gravitas / Shout! and FilmRise / Oaktree / Shout! deals demonstrate the depth of strategic and PE-platform capital available through Salem Partners' Westwood-discreet engagement model and 28+ year sub-vertical Rolodex.

Deal 2 (Consumer / Luxury): CriticalPoint-Advised Barton Perreira Sale to Thelios (LVMH)

Buyer: Thelios (LVMH eyewear unit; LVMH is the world's largest luxury conglomerate) Target: Barton Perreira (LA-area luxury eyewear brand with premium-channel distribution and celebrity wear-list traction) LA advisor: CriticalPoint Partners served as financial advisor to Barton Perreira on the sale Announced: November 6, 2023; Closed: early 2024 Deal value: ~$80M reportedly

The Barton Perreira sale to Thelios is a premium-luxury eyewear consolidation in which Barton Perreira's LA-area brand and distribution were acquired by Thelios, the eyewear unit of LVMH -- the world's largest luxury conglomerate (parent of Louis Vuitton, Christian Dior, Bulgari, Tiffany, Tag Heuer, and Sephora, among others). CriticalPoint ran the sell-side mandate end-to-end as part of the firm's consumer / luxury franchise. The Thelios acquisition fits LVMH's structural pattern of acquiring premium-eyewear brands to feed Thelios' distribution and manufacturing capability -- adjacent to LVMH's earlier eyewear deals and the EssilorLuxottica / Kering eyewear-brand competitive landscape. The deal sits alongside CriticalPoint's other 2024-2025 mandate book including Los Angeles Reproductive Partners to InTandem Capital Partners (healthcare services / fertility), VICI (e-commerce fashion), and a high-end multi-location pet retailer transaction.

Why this matters for LA sellers in the $5M-$100M range: Consumer / luxury transactions concentrate in LA advisor mandates because LA is the densest US market for premium consumer brands (Beverly Hills luxury, Manhattan Beach and Newport Beach DTC, Pasadena consumer-brand incubators) and the buyer pool tilts toward global luxury conglomerates (LVMH, Kering, Richemont, EssilorLuxottica) and LA-resident PE consumer platforms (Brentwood Associates, Aurora Capital, Levine Leichtman, Castanea Partners, North Castle Partners). For LA consumer / beauty / luxury sellers in the lower-middle-market, the Barton Perreira / Thelios deal demonstrates the depth of strategic capital available through CriticalPoint's Manhattan Beach senior bench and PE-buyer Rolodex (founder Matt Young's Platinum Equity pedigree extends into the LA consumer-PE consolidator network).

Deal 3 (Renewable Energy / AgTech): Ocean Park-Advised Gevo Acquisition of Red Trail Energy ($210M)

Buyer: Gevo, Inc. (Nasdaq: GEVO; renewable-fuels and sustainable aviation fuel platform) Target: Red Trail Energy (65M-gallon-per-year ethanol plant plus carbon-capture-and-sequestration (CCS) assets in Richardton, North Dakota) LA advisor: Ocean Park Advisors served as exclusive financial advisor and sole lead arranger to Gevo on the M&A transaction and the related $105M senior secured term loan from Orion Infrastructure Capital Announced: September 12, 2024; Closed: February 2025 Deal value: $210M

The Gevo / Red Trail Energy transaction is a $210M acquisition in which Gevo, a Nasdaq-listed renewable-fuels and sustainable aviation fuel (SAF) platform, acquired Red Trail Energy's 65M-gallon-per-year ethanol plant plus carbon-capture-and-sequestration (CCS) assets in Richardton, North Dakota -- subsequently renamed Net-Zero North. Ocean Park Advisors served as exclusive financial advisor and sole lead arranger to Gevo on the M&A transaction and the related $105M senior secured term loan facility from Orion Infrastructure Capital. The deal was Ocean Park's 38th biofuels transaction and illustrates the firm's combined M&A plus capital markets capability -- the dual-mandate role (M&A advisor and lead arranger) is structurally rare among LMM boutiques and reflects the firm's senior team depth across MDs Eric Ouyang, Frank Kim, and Mark Fisler (who led the deal).

Why this matters for LA sellers in the $5M-$100M range: Renewable energy and AgTech transactions concentrate in Ocean Park's mandate book because the firm has executed 38+ biofuels transactions and maintains direct relationships with the strategic acquirers (Gevo, POET, Valero Renewable Fuels, Marathon Petroleum), the PE platforms (Orion Infrastructure Capital, Ridgewood Infrastructure, BlackRock Climate Infrastructure), and the AgTech buy-side ecosystem that anchor the buyer pool. For LA-resident renewable-fuels, AgTech, agribusiness, and food and beverage sellers in the lower-middle-market and middle-market, the Gevo / Red Trail Energy deal demonstrates the depth of strategic and PE-infrastructure capital available through Ocean Park's hybrid M&A plus capital markets engagement model.

How Should LA Sellers Choose an M&A Advisor by Deal Size and Sector?

Match the tier to the deal size first, then overlay sector specialization, then run a 4-6 week parallel pitch with three to five firms. The fast LA advisors (the ones who close in 4-6 months instead of 9-12) all expect the same preparation work to be done before the engagement letter is signed -- if you arrive ready with the QofE drafted and the data room populated, your process compresses by 6-8 weeks.

1. Match the tier to the deal size. A $25M EV business should not pitch Intrepid, Salem Partners, or Greif unless the sub-sector match is exceptional (Salem for entertainment / media or life sciences specifically; Intrepid for consumer / beauty / wellness; Greif for founder-led entrepreneur-to-entrepreneur engagements). A $75M EV business should not pitch The Advisory IB, NewCap, or Objective IBV -- those firms specialize in sub-$25M sales where the senior bench has deeper visibility into the buyer pool. The right match for a $25M consumer / DTC deal is Intrepid or CriticalPoint. The right match for a $40M software / MSP deal is Solganick. The right match for a $30M healthcare-services deal is CriticalPoint, Salem Partners, or Intrepid. The right match for a $20M renewable-fuels deal is Ocean Park. The right match for a $10M essential-services HVAC roll-up is The Advisory IB. Tier discipline compounds: an advisor working at the structural sweet spot for your deal size runs a tighter, more competitive process.

2. Sector overlay matters more than tier discipline alone. For entertainment / media / film / TV / distribution mandates, the right firms by deal size are Salem Partners ($25M-$200M+ EV with the deepest LA media franchise) and Greif & Co. ($25M-$2B EV with founder-led history). For consumer / beauty / luxury / DTC mandates, Intrepid ($25M-$300M EV with MD Steve Davis Co-Head Beauty / Personal Care / Wellness) and CriticalPoint ($25M-$200M EV with the Barton Perreira / Thelios LVMH deal) are the two pure-plays. For healthcare-services and HealthIT, CriticalPoint, Salem Partners (Co-Founder John Dyett's Life Sciences practice), Intrepid (Analyte Health to Brightstar August 2025), and Objective IBV (healthcare and life sciences specialty) are the LA pure-plays. For software / MSP / cybersecurity / AI / cloud / data analytics, Solganick is the LA pure-play. For renewable fuels / AgTech / biofuels / SAF / agribusiness, Ocean Park is the LA pure-play. For essential services (HVAC, plumbing, electrical, restoration, fire and life safety, accounting), The Advisory IB is the LA pure-play. For multi-sector LMM owner-operator transitions, NewCap (1987 family-business franchise) and CFAW (1956 70-year track record) are the closer fits. For full-service capital markets plus M&A plus restructuring, Imperial Capital is the LA platform.

3. Get the Quality of Earnings drafted before pitching advisors. A QofE from a credible accountant (not your tax CPA) is the single most valuable preparation document. The QofE establishes the EBITDA narrative the buyer will diligence, surfaces working capital adjustments before the buyer finds them, and produces the financial reconciliation that the data room financials should tie to. Allow 6-8 weeks for QofE prep. For deeper context, our M&A due diligence process guide covers the full QofE workflow.

4. Run a parallel pitch process with 3-5 advisors. Most LA sellers pick the first advisor who pitches well. The right approach is to run a 4-6 week parallel pitch with 3-5 firms (one Tier A specialist, two Tier B operators, two Tier C if your deal is $5M-$15M EV; two Tier A and two Tier B if your deal is above $25M EV). Compare track records in your specific sub-sector, ask for sample CIMs and data rooms from recent closes (not pitch decks), and verify the senior banker who will actually run your process.

5. Pre-clean the data room contents. Customer concentration tables, contract summaries, employee rosters with key person flags, AR aging by client, and AP aging by vendor should all be organized before the advisor sees them. Buyers will diligence all of this -- the question is whether they find it organized in week 1 or wait until week 8. For click-through NDA workflows that compress buyer onboarding from days to minutes, our M&A click-through NDA guide covers the full workflow.

For data room setup for M&A specifically, our M&A data room guide covers the 8-folder structure that LA advisors expect to see by week 1 of the engagement.

What Should LA Sellers Demand from a Data Room Before Going to Market?

Demand NDA-gated access, dynamic watermarks, page-level analytics, AI-powered Q&A, custom domain branding, and per-cohort permissions -- features that compress the first six weeks of advisor work into a single day of seller preparation. LA advisors are universally more enthusiastic about engagements where the seller arrives with an organized data room than ones where the advisor has to spend the first six weeks of the engagement on data room setup. The structural cost asymmetry shows up here: legacy VDR vendors charge $15K to $50K per deal for a single transaction-grade data room, and 47% of legacy VDR vendors hide pricing on their websites. For boutique LA advisors running 8-12 deals per year, that prices out the sub-$50M EV band before the engagement letter is signed.

Peony Business at $30 per admin per month replaces the per-deal economics with flat-rate pricing -- an LA boutique advisor running 12 deals per year pays $360 total on Peony versus $180K to $600K on legacy per-deal VDRs. The feature alignment matters as much as the cost:

- NDA-gated access with built-in click-through e-signatures -- LA entertainment producers and agency partners use Peony's NDA gates with allow-list link access to share CIM with pre-vetted strategic acquirers (Lionsgate, Sony Pictures, Warner Bros. Discovery, Disney corporate development) without rebuilding the room when the buyer pool expands -- an LA-Hollywood industry-leak risk that flat-priced legacy VDR tooling has historically struggled to handle at boutique advisor margins

- Dynamic watermarks -- viewer email and timestamp embedded in every rendered page, so a leaked CIM has a forensic audit trail back to the buyer; Manhattan Beach and Newport Beach DTC consumer-brand sellers use Peony's dynamic watermarks with timestamp to embed buyer email plus view time into every page rendered -- a forensic audit trail when sensitive customer-LTV data leaves the room and reaches a competitor's M&A desk

- Granular permissions via visitor groups -- separate the lender data room from the strategic-buyer data room from the management equity rollover folder; DTLA fintech and OC tech founders use Peony's visitor groups to separate the lender data room from the strategic-buyer data room from the PE management equity rollover folder, so each cohort sees only the documents relevant to their diligence path

- Page-level analytics -- shows which buyers spent time on the QofE versus skimming the CIM; Beverly Hills luxury and DTC consumer brand exits use Peony's per-page analytics to see which strategic acquirer's M&A team is reading the customer concentration tables (LTV / CAC / acquisition channel mix) versus skimming the brand-equity slide

- Screenshot protection -- blocks and logs unauthorized capture attempts on the Business plan

- AI-powered Smart Q&A -- handles repetitive buyer questions with cited answers; Westside healthcare and life sciences founders (Cedars-Sinai / UCLA Health corridor; Salem Partners' healthcare practice) use Peony's AI Smart Q&A to handle repetitive HIPAA, payor-mix, and FDA-compliance questions with cited answers from uploaded clinical and billing data -- exactly the lift PE healthcare-services buyers expect to see automated in 2026

- AI auto-indexing -- compresses data room setup to under 5 minutes by organizing every uploaded document into the standard M&A folder structure automatically

- Custom domain branding -- run your data room on a domain that matches your firm or transaction code name

LA boutiques running data rooms on Peony in 2026 include sub-LMM specialists in entertainment / media, healthcare technology, consumer / DTC / beauty, software / MSP / cybersecurity, renewable fuels / AgTech, and essential services -- the firms that need the cost structure to make sub-$50M EV economics work and the AI Smart Q&A workflow to handle the repetitive lift that diligence buyers expect to see automated.

For solo LA M&A advisors and sub-LMM specialists running 1-3 deals per year, Peony Business at $30 per admin per month covers data room hosting with NDA gates, page-level analytics, screenshot protection, and basic AI document Q&A. The Data Room tier at $52 per admin per month adds watermarks, AI auto-indexing, and unlimited data rooms -- which is what running middle-market and upper middle-market M&A processes actually requires.

Set up your first LA M&A data room in under 5 minutes -- start free.

What Do LA M&A Advisors Charge in 2026?

LA M&A advisors charge total fees of 5-8% blended on $5M-$15M deals, 1.7-3% blended on $15M-$50M deals, and 1-2% blended on $50M-$100M deals -- with retainers ranging from $25K (volume-led essential-services firms) to $150K credited against the success fee at close. Fee structures across the 14 firms collapse to three patterns by deal size:

| Deal Size (EV) | Retainer | Success Fee Structure | Approx. Total Fees |

|---|---|---|---|

| $5M-$15M | $25K-$50K | Modified Lehman: 8-10% on first $1M, 6% next $1M, 4% next $1M, then 2-3% above (or 8-15% flat for sub-$5M owner-operators) | 5-8% blended |

| $15M-$50M | $25K-$75K | Lehman 5/4/3/2/1 (5% first $1M, 4% next, 3% next, 2% next, 1% above) | 1.7-3% blended |

| $50M-$100M | $50K-$150K | Negotiated tiered (often 1.5-2.0% flat above $30M with retainer credit) | 1-2% blended |

Retainer credit: All 14 firms credit retainer against success fee at close. If the deal does not close, the retainer is generally non-refundable, though the engagement letter is negotiable on this point.

Tail period: 12-24 months covering buyers introduced during the engagement. Negotiate down to 12 months if you can; the default 18-24 month tail can complicate a future re-engagement with a different advisor.

Expense reimbursement: $25K-$50K cap is standard for travel, marketing, and CIM preparation. Above this, the seller pays direct.

Houlihan Lokey comparison: Houlihan Lokey is LA-headquartered and the largest US restructuring and middle-market bank. At $25-100M EV deals, Houlihan typically demands a $250K+ retainer plus a higher success fee minimum (often $750K floor regardless of deal value) -- structurally inefficient for the LMM band, which is why this guide excludes Houlihan and recommends boutique alternatives.

For deeper context on what to expect in the data room cost structure component of your M&A process, our cost guide covers VDR pricing across the 15 platforms most commonly used by LA advisors.

Frequently Asked Questions

Q: I'm running a sell-side for a $30M EV LA services business. Should I hire a boutique M&A advisor or a bulge-bracket bank like Houlihan Lokey?