M&A Process Explained (8 Phases, Real Deliverables) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

M&A Process Explained: 8 Phases, Real Deliverables

TL;DR: The global M&A market hit $4.8 trillion in 2025, up 43% year-over-year (Bain M&A Report 2026). Gen AI is compressing timelines by 30 to 50% and reducing costs by roughly 20% (McKinsey, Feb 2025). Yet 53% of acquirers still discover critical cybersecurity issues during diligence (Forescout), and Verizon's Yahoo acquisition saw a $350 million price reduction after undisclosed breaches. This guide walks through the 8 phases every M&A deal follows, the deliverables each phase produces, and the mistakes that kill transactions.

Last updated: March 2026

Why I wrote this

We run Peony, a data room company. Over the past two years I have supported M&A transactions from both sides of the table — founders selling their companies, corporate development teams running acquisitions, and PE firms executing platform buildups. Some of these deals closed in under six weeks. Others stretched past a year with multiple regulatory jurisdictions, working capital disputes, and last-minute earnout renegotiations.

The lesson I keep relearning: deals do not fail because the strategy was wrong. They fail because the process broke down somewhere between the investment thesis and the wire transfer. A phase got skipped, a deliverable was incomplete, or a stakeholder lost confidence because the deal infrastructure was disorganized.

This guide maps the full M&A lifecycle — all 8 phases, the actual deliverables each one produces, and where deals most commonly stall. I have intentionally kept the due diligence and integration sections concise because those topics each deserve (and have) their own deep-dive guides. The phases that other guides skim — strategy, targeting, LOI negotiation, valuation structure, signing mechanics — are where I go deepest here.

The 8 Phases at a Glance

- Strategy and deal thesis — Define why you are acquiring and what the target profile looks like.

- Target identification and sourcing — Build a long list, screen it, and rank candidates.

- First contact, NDA, and initial information — Engage the target, execute confidentiality, and exchange preliminary data.

- IOI or LOI — Submit a non-binding indication of interest or a binding letter of intent with exclusivity.

- Due diligence — Validate every assumption in the thesis through structured investigation.

- Valuation and deal structure — Finalize purchase price, working capital, earnouts, tax structure, and risk allocation.

- Signing and closing — Execute the definitive agreement, satisfy closing conditions, and wire funds.

- Post-merger integration — Capture the value the deal thesis promised.

The phases are sequential in theory. In practice, phases 4 through 7 overlap significantly, and smart deal teams begin integration planning during diligence rather than waiting for closing.

Phase 1: Strategy and Deal Thesis

Timeline: 1 to 6 months (ongoing for serial acquirers) Key deliverable: Written deal thesis and acquisition criteria document

This is the phase most acquirers rush through, and it is the single biggest predictor of whether the deal creates value. According to Bain's analysis of over 2,500 transactions, acquirers who define a clear deal thesis before sourcing targets generate returns 14 percentage points higher than those who pursue opportunistic deals.

Building the thesis

A deal thesis is not "we want to grow faster" or "the board wants us to do M&A." A thesis is a written hypothesis with testable assumptions:

- Strategic rationale. Are you buying revenue (customer base), capability (technology, talent), market position (geographic expansion, regulatory license), or cost synergies (duplicate functions, supply chain consolidation)?

- Financial parameters. What EBITDA multiples are acceptable? What revenue range? What growth profile? What margin floor?

- Integration assumptions. How much overlap exists? What is the realistic synergy capture timeline — 6 months, 18 months, 3 years? What does "done" look like?

- Risk appetite. How much customer concentration can you tolerate? Do you have bandwidth for cross-border regulatory complexity? Will the board approve deals with earn-out structures?

Write these down. The thesis becomes the scorecard for every subsequent phase. When due diligence surfaces a finding that contradicts a thesis assumption, you either adjust the price, restructure the deal, or walk away. Without a written thesis, there is no framework for that decision, and sunk-cost bias takes over.

The acquisition criteria document

Translate the thesis into a screening tool. A good criteria document includes:

- Industry and vertical — SaaS infrastructure, specialty chemicals, healthcare services, etc.

- Revenue range — $5M to $50M ARR, $20M to $200M revenue, etc.

- Geography — Domestic only, specific international markets, or global

- Growth profile — Minimum revenue growth rate, minimum gross margin

- Deal type — Platform acquisition, bolt-on, carve-out, acqui-hire, distressed

- Valuation guardrails — Maximum EV/EBITDA, EV/Revenue, or total enterprise value

- Non-starters — Customer concentration above a threshold, pending litigation, specific regulatory exposures

Serial acquirers (private equity platforms, corporate M&A teams running buildups) maintain living criteria documents that evolve with each completed deal. First-time acquirers should build this document before making a single outreach.

Deliverables exiting Phase 1

| Document | Purpose |

|---|---|

| Written deal thesis (1 to 3 pages) | Defines strategic rationale and testable assumptions |

| Acquisition criteria document | Screening tool for target identification |

| Board or IC authorization memo | Formal approval to pursue acquisitions |

| Budget allocation | Estimated total deal cost including advisory fees |

Phase 2: Target Identification and Sourcing

Timeline: 2 to 6 months (ongoing for active programs) Key deliverable: Prioritized target list with tier rankings

Building the long list

Most acquirers start with 50 to 200 companies on a long list. Sources include:

- Investment banks and M&A advisors. Sell-side bankers bring marketed processes; buy-side advisors source proprietary deal flow. Expect to pay 1% to 2% of deal value (Lehman formula or modified versions) for intermediary services.

- Industry databases. PitchBook, Capital IQ, Crunchbase, CB Insights, and sector-specific databases generate initial candidate lists based on financial and operational criteria.

- Proprietary sourcing. Direct outreach to companies that are not for sale — management teams, founders, investors. This is where the best deals often come from, because there is no competitive auction pressure.

- Inbound from networks. Board members, portfolio company executives, industry events, and professional networks surface targets that databases miss.

Screening and tiering

The long list gets screened against the acquisition criteria document from Phase 1. A typical screening cadence:

- Desktop screen — Public financials, headcount trends, product positioning, customer reviews, IP filings. Eliminate companies that clearly miss criteria.

- Preliminary financial analysis — Revenue estimates, growth trajectory, margin profile, comparable transaction multiples. Move survivors to Tier 1 (strong fit), Tier 2 (conditional fit), or Tier 3 (watch list).

- Management assessment — For Tier 1 targets, begin informal intelligence gathering: conference presentations, podcast appearances, LinkedIn profiles of leadership, Glassdoor sentiment. You are assessing whether the management team will be a retention priority or a replacement target.

The target one-pager

For each Tier 1 candidate, prepare a one-page profile:

- Company overview and founding story

- Revenue, growth, margin estimates

- Key customers and market position

- Strategic fit against thesis assumptions

- Estimated valuation range

- Known risks and open questions

- Recommended approach (intermediary introduction, direct CEO outreach, investor referral)

Deliverables exiting Phase 2

| Document | Purpose |

|---|---|

| Prioritized target list (50 to 200 names) | Universe of candidates ranked by fit |

| Tier 1 target profiles (one-pagers) | Investment committee review material |

| Sourcing channel tracker | Tracks how each target was identified |

| Comparable transactions analysis | Validates valuation expectations |

Phase 3: First Contact, NDA, and Initial Information Exchange

Timeline: 2 to 8 weeks per target Key deliverable: Executed NDA, CIM, and preliminary data room access

This is where the deal moves from abstract to tangible. The approach strategy matters — getting the first meeting wrong can permanently close a door.

Making first contact

The outreach method depends on whether the target is in a marketed process (bank-led auction) or a proprietary approach:

Marketed process: The sell-side advisor distributes a teaser (anonymous, 1 to 2 pages describing the company without identifying it). Interested buyers sign an NDA to receive the Confidential Information Memorandum (CIM). The process is structured, competitive, and timeline-driven.

Proprietary approach: The buyer (or their advisor) contacts the target's CEO, founder, or majority shareholder directly. This requires more nuance — you are pitching the idea of a transaction to someone who may not be actively considering one. Lead with strategic vision, not price. The best proprietary approaches explain why the combination creates value for the target's customers, employees, and shareholders.

The NDA

The non-disclosure agreement is the first legal document in any deal. It seems routine, but terms matter:

- Scope. What constitutes confidential information? Both parties' data, or only the target's?

- Duration. Standard is 2 to 3 years. Sellers want longer; buyers want shorter.

- Non-solicitation. Does the NDA include a non-solicit of the target's employees? Sellers insist on this; buyers resist because it constrains talent planning.

- Standstill. In public company deals, does the NDA include a standstill provision preventing hostile moves?

- Permitted disclosures. Can the buyer share information with financing sources, co-investors, or portfolio company management?

Peony's NDA gating feature enforces this digitally: recipients cannot access any data room documents until they have executed the NDA directly within the platform. This eliminates the common failure mode where a signed NDA sits in someone's inbox while deal materials are already being forwarded.

The CIM and preliminary data exchange

Once the NDA is executed, the sell-side shares the Confidential Information Memorandum — typically 40 to 80 pages covering:

- Executive summary and investment thesis

- Business overview and history

- Products and services

- Market and competitive landscape

- Financial summary (3 to 5 years historical, 2 to 3 years projected)

- Management team bios

- Growth opportunities and risks

Smart sellers also open a preliminary data room at this stage with high-level documents — corporate structure, summary financials, product overview — gated behind the NDA. This accomplishes two things: it signals professionalism, and it gives the seller page-level analytics showing which buyers are actually engaging with the materials versus which signed the NDA and never looked.

Management presentations

For serious bidders, the seller arranges management presentations — typically 2 to 3 hour sessions where the target's leadership team presents the business and answers questions. These are the buyer's best opportunity to assess:

- Quality of the management team (depth, clarity, credibility)

- Cultural fit with the buyer's organization

- Whether the founder or CEO will stay post-close (critical for earnout structures)

- Red flags that do not appear in written materials

Deliverables exiting Phase 3

| Document | Purpose |

|---|---|

| Executed NDA | Legal framework for information sharing |

| CIM / Information Memorandum | Comprehensive business overview |

| Preliminary data room access | High-level documents for initial evaluation |

| Management presentation materials | Deep dive on business and leadership |

| Process letter (if auction) | Timeline, bid procedures, evaluation criteria |

Phase 4: Indication of Interest and Letter of Intent

Timeline: 2 to 6 weeks Key deliverable: Executed LOI with exclusivity

This is the phase where economics get real. The buyer submits either a non-binding Indication of Interest (IOI) or proceeds directly to a Letter of Intent (LOI), depending on the process structure.

IOI versus LOI

| Element | IOI | LOI |

|---|---|---|

| Binding? | Non-binding | Partially binding (exclusivity, confidentiality, costs) |

| Valuation | Range (e.g., $80M to $100M enterprise value) | Specific price or formula |

| Deal structure | High-level (cash, stock, or combination) | Detailed (working capital mechanism, earnout terms, escrow) |

| Exclusivity | None | 60 to 90 days typically |

| Due diligence scope | Not specified | Outlined with timeline |

| Typical length | 2 to 5 pages | 8 to 20 pages |

In a competitive auction, the sell-side advisor collects IOIs first to shortlist bidders (typically narrowing 5 to 10 IOIs down to 2 to 4 finalists), then invites the finalists to submit binding LOIs after a second round of management access and data room review.

In a proprietary deal, the IOI stage is often skipped. The buyer and seller negotiate the LOI directly.

Key LOI terms to negotiate

Purchase price. Cash at close, stock consideration, rollover equity, seller notes. The headline number matters less than the composition — a $100M all-cash offer is not the same as a $100M offer with $20M in earnouts and $15M in escrow holdback.

Working capital mechanism. The LOI should specify whether closing working capital will be based on a peg (target amount), a true-up (adjusted post-close), or a locked-box (fixed at a historical date with no adjustment). This single term causes more post-close disputes than any other.

Earnout structure. If the buyer is bridging a valuation gap with contingent payments, define the earnout metrics (revenue, EBITDA, customer retention), measurement period (12 to 36 months), and accounting methodology in the LOI — not the purchase agreement. Leaving earnout details to later stages is the single most predictable source of post-close litigation.

Exclusivity period. Sellers want 30 to 45 days. Buyers want 90 to 120 days. Standard is 60 to 90 days with an extension mechanism if diligence is proceeding in good faith. Sellers should negotiate a reverse break fee — a penalty the buyer pays if they walk away without cause during exclusivity — to protect against buyers using exclusivity as a free option while market conditions change.

Conditions. Financing contingency (is the buyer's commitment to fund conditional?), board approval, regulatory approvals, material adverse change (MAC) clause definition.

The exclusivity clock

Once the LOI is signed, the exclusivity clock starts. Everything from this point — due diligence, valuation refinement, definitive agreement negotiation — must fit within this window. This is why data room infrastructure matters: sellers who take two weeks to set up a data room after LOI signing burn 15% to 25% of their exclusivity window on logistics instead of substance.

Peony data rooms go from empty to buyer-ready in under 5 minutes. AI auto-indexing sorts uploaded documents into standard due diligence categories in under 3 minutes. That means the data room can be populated and live within the first day of exclusivity, giving both sides the maximum window for substantive diligence.

Deliverables exiting Phase 4

| Document | Purpose |

|---|---|

| IOI (if auction process) | Non-binding preliminary offer to shortlist |

| Executed LOI | Key economic terms and exclusivity commitment |

| Exclusivity agreement | Formal no-shop period with defined expiration |

| Due diligence request list | Buyer's initial document requests by category |

| Preliminary integration thesis | Early view of post-close combination |

Phase 5: Due Diligence

Timeline: 1 to 6 months depending on deal size and complexity Key deliverable: DD findings report, purchase price adjustment recommendations

Due diligence is where the thesis meets reality. The buyer's team — financial, legal, tax, IP, HR, IT, commercial, and environmental specialists — investigates every material aspect of the target business.

I am intentionally keeping this section brief because I have written an entire 6-phase due diligence playbook and a 174-document due diligence checklist that cover this phase in depth. The short version: mid-market DD typically runs 1 to 2 months across 8 workstreams, large and cross-border deals run 3 to 6 months, and the most common failure mode is disorganized data rooms that exhaust buyer patience before diligence is complete.

For the data room setup — folder structure, document staging, security controls, Q&A workflow — see the dedicated M&A data room guide. Also review the VDR permissions model and redaction workflow before opening external access.

Phase 6: Valuation and Deal Structure

Timeline: Runs in parallel with Phase 5, finalized 2 to 4 weeks before signing Key deliverable: Definitive valuation model, deal structure term sheet, draft purchase agreement

This is the phase where investment bankers earn their fees. Valuation and structure are not a single calculation — they are an iterative negotiation informed by DD findings, tax optimization, risk allocation, and financing constraints.

Valuation methodologies

Most mid-market and large transactions use multiple methodologies in parallel:

Discounted cash flow (DCF). Projects free cash flows 5 to 10 years out and discounts them to present value. Sensitive to terminal growth rate and discount rate assumptions — a 1% change in WACC can move enterprise value by 15% to 20%.

Comparable company analysis (trading comps). Benchmarks the target against publicly traded peers on EV/EBITDA, EV/Revenue, P/E multiples. Useful for establishing a valuation range, but requires careful peer selection — a high-growth SaaS company and a mature services business in the same "industry" trade at vastly different multiples.

Precedent transactions (deal comps). Analyzes what acquirers have paid for similar companies in recent transactions. Includes a control premium (typically 20% to 40% above trading price for public companies) that trading comps miss.

Leveraged buyout analysis (for PE deals). Models the target under a leveraged capital structure to determine the maximum price a financial buyer can pay while achieving target returns (typically 20% to 25% gross IRR over a 3 to 5 year hold).

Working capital true-up

The working capital mechanism is the most technically complex and frequently disputed element of any deal. Here is how it works:

- Set the peg. Both parties agree on a "normal" level of working capital (typically the 12-month trailing average of current assets minus current liabilities, excluding cash and debt).

- Estimate at closing. The seller delivers an estimated closing balance sheet.

- True-up post-close. Within 60 to 90 days after closing, the buyer prepares a final closing balance sheet. If actual working capital exceeds the peg, the seller receives the difference. If it falls below, the buyer claws back the shortfall from escrow.

The disputes arise in the definitions — which line items are included, how reserves are calculated, whether deferred revenue counts. Get the definitions right in the purchase agreement, or plan on spending $200K to $500K in post-close arbitration.

Earnout structures

Earnouts bridge valuation gaps: the buyer pays a portion of the price contingent on the target hitting specified metrics post-close. They sound elegant, but they are litigation machines if not structured carefully.

Best practices for earnouts:

- Define metrics precisely — "EBITDA" means different things depending on add-backs, and "revenue" can include or exclude one-time contracts.

- Specify the measurement period (12, 24, or 36 months) and the accounting methodology.

- Include covenant language requiring the buyer to operate the business in a manner consistent with achieving the earnout — otherwise the buyer can gut the acquired business and argue the earnout was missed due to "market conditions."

- Cap the earnout at a percentage of total consideration (typically 10% to 30%).

Escrow and indemnification

The buyer holds back a portion of the purchase price (typically 5% to 15%) in escrow for 12 to 24 months to cover indemnification claims — breaches of representations, undisclosed liabilities, working capital shortfalls. The escrow amount, survival period, and claim thresholds (basket and cap) are among the most negotiated terms in any deal.

Representations and warranties insurance (RWI) has become standard in mid-market M&A. RWI shifts indemnification risk to an insurer, allowing sellers to receive more proceeds at closing and giving buyers a creditworthy counterparty for claims. Premiums typically run 2% to 4% of coverage limits.

Tax structure

The choice between an asset deal and a stock deal has significant tax consequences:

- Asset deal. The buyer gets a stepped-up tax basis in the acquired assets, generating future depreciation and amortization deductions. The seller faces potential double taxation (corporate-level gain plus shareholder-level gain for C-corps). Most PE buyers prefer asset deals for the tax step-up.

- Stock deal. The buyer inherits the target's existing tax basis and all historical liabilities. The seller typically receives more favorable capital gains treatment. A Section 338(h)(10) election can give asset-deal tax treatment in a stock-deal legal structure.

- Tax-free reorganization. In stock-for-stock deals meeting IRS requirements, sellers can defer gain recognition. These are common in public company strategic mergers.

International transactions add transfer pricing, permanent establishment risk, withholding taxes, and treaty benefits to the analysis. Cross-border deals routinely require 3 to 6 months of tax structuring alone.

Deliverables exiting Phase 6

| Document | Purpose |

|---|---|

| Valuation analysis (DCF, comps, precedents) | Supports and justifies purchase price |

| Deal structure term sheet | Cash/stock mix, earnout, escrow, working capital |

| Draft purchase agreement | Definitive legal document for negotiation |

| Tax structure memorandum | Optimizes after-tax proceeds for both parties |

| RWI policy application | Shifts indemnification risk to insurer |

Phase 7: Signing and Closing

Timeline: 1 to 6 months between signing and closing Key deliverable: Executed definitive agreement, funds transfer, legal entity transfer

In smaller deals, signing and closing happen simultaneously — both parties execute the purchase agreement and wire funds on the same day. In larger deals, especially those requiring regulatory approval, signing and closing are split by weeks or months.

The definitive agreement

The purchase agreement (SPA for share purchases, APA for asset purchases) is the definitive legal document. It typically runs 80 to 150 pages plus exhibits and disclosure schedules, and it covers:

- Purchase price and payment mechanics. Cash, stock, notes, earnout, escrow, working capital adjustment.

- Representations and warranties. 30 to 50 pages of representations about the target's business, finances, legal status, and compliance. Every statement is a potential indemnification claim if proven false.

- Covenants. Pre-closing operating covenants (seller operates the business in ordinary course), post-closing restrictive covenants (non-compete, non-solicit).

- Closing conditions. Regulatory approvals, third-party consents, material adverse change absence, accuracy of representations.

- Indemnification. Survival periods, basket and cap, escrow mechanics, special indemnities for known issues.

Regulatory approvals

Hart-Scott-Rodino (HSR). Transactions exceeding the HSR threshold ($119.5 million in 2025) require pre-merger notification to the FTC and DOJ. Standard waiting period is 30 days. The agencies can issue a "second request" for additional information, which effectively extends the review by 6 to 12 months. New FTC rules effective February 2025 add 68 to 121 hours per filing in compliance burden (FTC), with expanded requirements for narrative descriptions of competitive overlaps, transaction rationale, and labor market impacts.

CFIUS. Transactions involving foreign acquirers and US businesses in sensitive sectors (technology, infrastructure, personal data) may trigger review by the Committee on Foreign Investment in the United States. CFIUS reviews can add 45 to 90 days and result in conditions, divestiture requirements, or outright blocks.

Sector-specific regulators. Banking (OCC, FDIC, Fed), insurance (state regulators), healthcare (state attorney general, CMS), telecommunications (FCC), defense (DCSA), and energy (FERC) all have sector-specific merger review processes with their own timelines and requirements.

International. Cross-border deals may require filings in the EU (European Commission), UK (CMA), China (SAMR), and other jurisdictions — each with independent review timelines and substantive standards.

Third-party consents

Many contracts include change-of-control provisions requiring counterparty consent before the deal closes. Common consent requirements:

- Key customer contracts. Customers with change-of-control termination rights must affirmatively consent. Missing even one major customer consent can delay closing or trigger a MAC condition.

- Landlord consents. Commercial leases almost always require landlord approval for assignments.

- Lender consents. Existing debt instruments typically require payoff or lender consent.

- Government contracts. Federal contracts often require novation (formal transfer of contractor status).

- Licensing agreements. Software, IP, and regulatory licenses may require transferee qualification.

The closing checklist

A typical closing involves 50 to 200 individual deliverables, tracked in a closing checklist (also called a closing bible or closing set). The checklist includes:

- Executed purchase agreement and all ancillary agreements

- Officer certificates and good-standing certificates

- Board resolutions and shareholder approvals

- Payoff letters for existing debt

- Escrow agreements and escrow funding instructions

- Working capital estimate and supporting schedules

- FIRPTA certificates (for foreign sellers)

- Employment and retention agreements for key personnel

- Wire instructions and funds flow memo

Peony e-signatures with AI-powered field detection let deal teams execute closing documents — purchase agreements, employment agreements, escrow instructions, officer certificates — directly within the data room. No switching to a separate signing tool, no version confusion, and every executed document is automatically filed in the closing set with a complete audit trail.

Deliverables exiting Phase 7

| Document | Purpose |

|---|---|

| Executed definitive agreement | Legal transfer of ownership |

| Regulatory clearance letters | HSR, CFIUS, sector-specific approvals |

| Third-party consent package | Customer, landlord, lender approvals |

| Closing certificate and funds flow | Confirms conditions met, directs wire transfers |

| Closing bible / closing set | Complete record of all executed transaction documents |

Phase 8: Post-Merger Integration

Timeline: 100 days for initial stabilization, 12 to 24 months for full integration Key deliverable: Integration playbook, synergy tracking dashboard, Day 1 readiness plan

Integration is where the value promised in the deal thesis is either captured or lost. According to McKinsey, more than 60% of acquisitions fail to create the value projected at signing, and the primary culprit is poor integration execution — not poor deal selection.

I have written a complete post-merger integration playbook covering the 4 outcomes every integration must deliver, the pre-close planning phase, Day 1 stabilization, and the 100-day sprint. The key takeaway: begin integration planning during due diligence, not after closing. The best deal teams assign an integration lead before the LOI is signed.

Common Deal-Killers

Not every deal that enters Phase 3 reaches Phase 7. Based on deal data and my own experience, these are the issues that kill transactions most frequently:

Cybersecurity vulnerabilities. 53% of organizations discover critical cybersecurity issues during M&A due diligence (Forescout). The Verizon-Yahoo transaction saw a $350 million price reduction after Yahoo disclosed two massive data breaches post-LOI. Acquirers are now commissioning independent cybersecurity assessments as a standard DD workstream, not an optional add-on.

Customer concentration. When a single customer represents more than 20% of revenue, buyer anxiety spikes. The risk is not just revenue loss — it is negotiating leverage. A concentrated customer who learns about the acquisition can extract concessions (price reductions, extended terms) during the consent process.

IP ownership gaps. Startups frequently have incomplete IP assignment chains — contractors who built core technology without proper work-for-hire agreements, founders who developed IP before incorporation without assignment, open-source components embedded in proprietary products without compliance tracking. Any of these can derail a deal or force a significant price reduction.

Regulatory blockers. HSR second requests, CFIUS mitigation conditions, and sector-specific regulatory concerns can extend timelines past exclusivity windows or impose conditions that destroy the deal's economic rationale.

Working capital disputes. When the buyer and seller cannot agree on the working capital peg or the definitions of included line items, the deal stalls. This is entirely preventable with precise LOI language — but most LOIs defer the details.

Seller fatigue. Deals that drag past 9 to 12 months face increasing risk of seller fatigue. Management teams running a company while simultaneously supporting a demanding diligence process burn out. Organized, fast-moving data rooms with efficient Q&A workflows reduce this friction significantly.

By the Numbers: M&A in 2025 and 2026

| Metric | Value | Source |

|---|---|---|

| Global M&A deal value (2025) | $4.8 trillion, up 43% YoY | Bain M&A Report 2026 |

| Megadeals over $5B (2025) | 111, up 76% from 63 in 2024 | PwC |

| Critical cybersecurity issues found in M&A DD | 53% of organizations | Forescout |

| Gen AI impact on M&A costs | ~20% reduction, 30-50% faster cycles | McKinsey, Feb 2025 |

| Average mid-market DD duration | 1 to 2 months | Industry consensus |

| Average large-deal DD duration | 3 to 6+ months | Industry consensus |

| Verizon-Yahoo price reduction from breaches | $350 million | Public disclosure |

| New HSR filing compliance burden | 68 to 121 hours per filing | FTC, Feb 2025 |

| Acquisition failure rate (value destruction) | 60%+ fail to create projected value | McKinsey |

| RWI premium (typical) | 2% to 4% of coverage limits | Market data |

How Peony Supports the Full M&A Lifecycle

Most data room providers focus on a single phase — due diligence. Peony is built for the entire deal lifecycle, from NDA execution through closing and integration.

Phase 3: NDA and initial information exchange. Peony's NDA gating requires every recipient to execute a confidentiality agreement before accessing any document. No more tracking NDA status in a spreadsheet while deal materials circulate freely. Dynamic watermarks embed each viewer's identity into every rendered page, creating instant attribution if a teaser or CIM leaks.

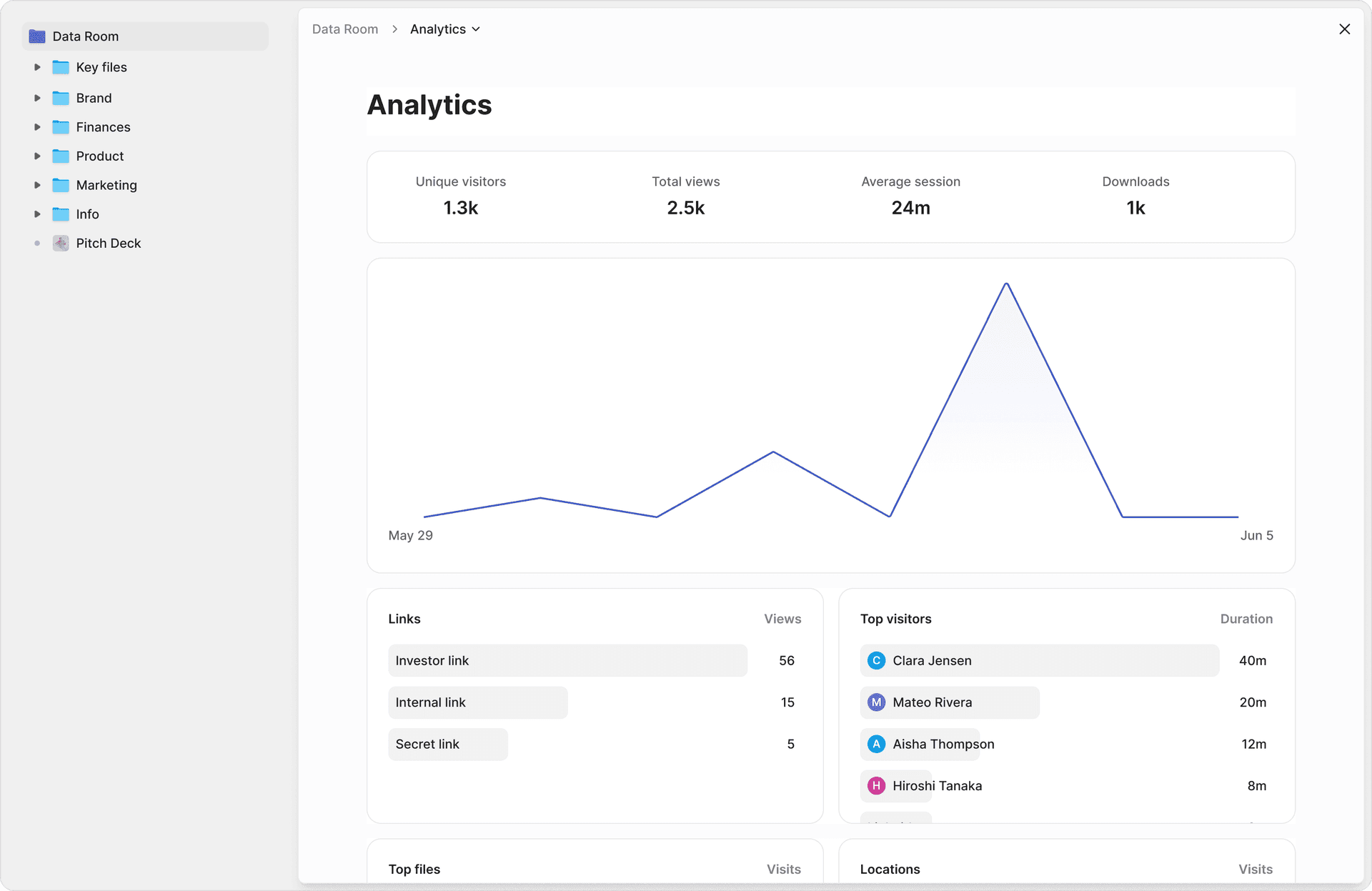

Phase 4: LOI and bid management. Multi-level access controls let sellers create separate permission groups per bidder in a competitive process. Each bidder sees only the documents staged for their access level. Page-level analytics show which bidders are seriously engaging — and which signed the NDA but never opened the CIM.

Phase 5: Due diligence. AI auto-indexing organizes thousands of documents into standard DD categories in under 3 minutes. AI-powered Q&A lets counterparties submit questions directly in the data room — AI drafts initial responses from uploaded documents, the deal team reviews and approves, and every exchange is logged with a complete audit trail. AI redaction identifies and masks PII, financial data, and sensitive terms before sharing.

Phase 6: Valuation support. AI extraction lets deal teams ask natural-language questions across every uploaded document and get cited answers with exact page numbers. Need to find every reference to "change of control" across 3,000 pages of contracts? Ask the question, get the citations. Screenshot protection blocks and logs capture attempts on valuation models and financial projections.

Phase 7: Signing and closing. Built-in e-signatures with AI-powered field detection let parties execute the purchase agreement, ancillary documents, and employment agreements directly within the data room. No switching tools, no version confusion. Every executed document is automatically filed in the closing set.

Phase 8: Integration. The same data room that hosted diligence becomes the integration document hub. Two-factor authentication and granular permissions ensure that integration teams only see what they need to see, and the full audit trail carries forward for regulatory filings and RWI claims.

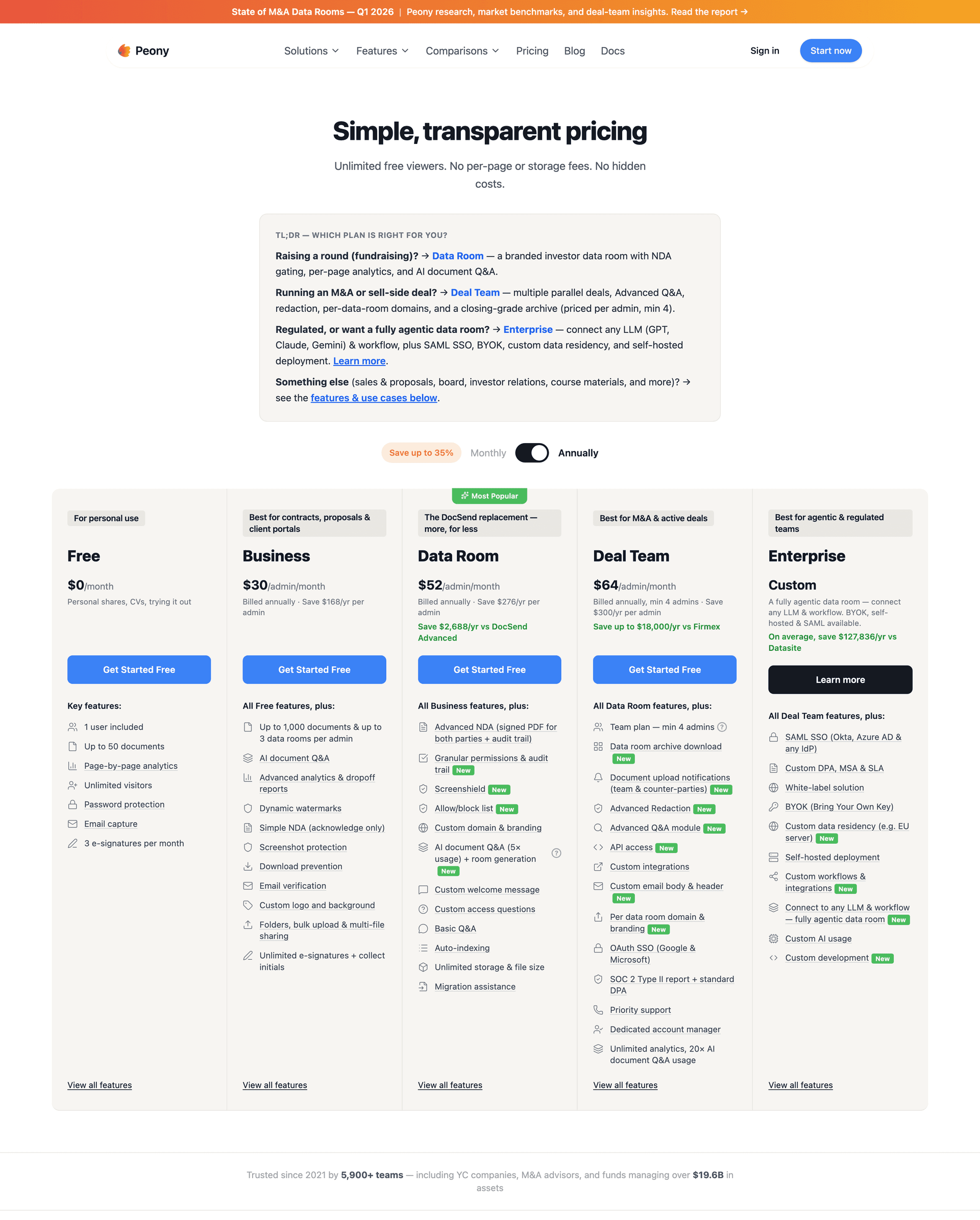

Pricing. Free tier includes per-page analytics and link expiry. Business at $30 per admin per month adds access revocation, screenshot protection, simple NDA gating, and basic AI document Q&A. Data Room at $52 per admin per month adds dynamic watermarking, AI auto-indexing, AI-powered rooms, threaded Q&A, granular per-file permissions, custom domain, and unlimited rooms and storage. No per-page fees, no storage overages. See full pricing.

For the M&A-specific setup guide, see M&A Data Rooms: What Deal Teams Get Wrong. For the full M&A solution overview, see the dedicated solution page.

Frequently Asked Questions

What are the 8 phases of the M&A process?

The 8 phases are: (1) Strategy and deal thesis, (2) Target identification and sourcing, (3) First contact, NDA, and initial information exchange, (4) Indication of interest or letter of intent, (5) Due diligence, (6) Valuation and deal structure, (7) Signing and closing, and (8) Post-merger integration. Peony data rooms support the entire lifecycle, starting with NDA-gated document sharing in Phase 3 and continuing through AI-powered due diligence rooms, e-signatures at signing, and secure integration document management.

How long does the M&A process take from start to finish?

The full M&A process typically takes 6 to 12 months for mid-market deals and 12 to 24 months for large or cross-border transactions. Strategy and sourcing consume 2 to 6 months, due diligence adds 1 to 6 months depending on complexity, and signing through closing adds 1 to 3 months for regulatory approvals. Peony AI auto-indexing organizes thousands of deal documents in under 3 minutes, compressing the data room setup phase from weeks to a single afternoon.

What is a deal thesis in M&A?

A deal thesis is a written hypothesis explaining why acquiring a specific company will create value. It typically includes the strategic rationale (revenue synergies, cost savings, capability gaps, geographic expansion), target financial profile, acceptable valuation range, and integration assumptions. The thesis becomes the scorecard against which every subsequent phase is measured. Peony page-level analytics help deal teams validate thesis assumptions by showing exactly which due diligence documents reviewers focused on and which sections raised concerns.

What is the difference between an IOI and an LOI in M&A?

An indication of interest (IOI) is a non-binding preliminary offer that states an estimated valuation range and high-level terms. A letter of intent (LOI) is a more detailed, partially binding document that includes a specific purchase price, deal structure, key conditions, and typically an exclusivity period of 60 to 90 days. The IOI is used to shortlist bidders in a competitive process; the LOI commits both parties to negotiate toward a definitive agreement. Peony dynamic watermarks embed each viewer's identity into every page of these sensitive documents, making it instantly traceable if a draft LOI leaks to competing bidders.

What kills M&A deals before closing?

The most common deal-killers are undisclosed cybersecurity vulnerabilities (53% of organizations hit critical issues per Forescout), customer concentration above 20% of revenue, unresolved IP ownership gaps, regulatory blockers such as HSR second requests, and valuation disagreements during confirmatory diligence. Slow or disorganized data rooms also kill deals indirectly by exhausting buyer patience. Peony screenshot protection blocks and logs capture attempts on sensitive deal documents, reducing the risk of confidential information leaking to competitors mid-process.

What is an exclusivity period in M&A?

An exclusivity period, also called a no-shop clause, is a contractual commitment by the seller not to solicit or negotiate with other buyers for a defined window, typically 60 to 90 days. It protects the buyer's investment in due diligence costs and management time. Sellers negotiate shorter exclusivity windows and reverse break fees as leverage. Peony AI-powered Q&A lets buyers submit questions directly in the data room, where AI drafts responses from uploaded documents and routes them through a team approval workflow, helping both sides resolve issues faster within tight exclusivity windows.

How much does the M&A process cost?

Total M&A transaction costs typically run 3% to 8% of deal value for mid-market transactions, covering investment banking fees (1% to 2%), legal counsel ($200K to $2M+), accounting and tax advisory ($100K to $500K+), and data room and technology costs. Legacy VDR providers charge $10,000 to $50,000 per month. Peony offers M&A data rooms starting free, with the Data Room plan at $52 per admin per month including AI auto-indexing, unlimited rooms, screenshot protection, and unlimited visitors, reducing technology costs by over 90% compared to legacy platforms.

What happens between signing and closing in an M&A deal?

Between signing and closing, the parties satisfy closing conditions: regulatory approvals (HSR, CFIUS, sector-specific), third-party consents from customers and landlords, financing commitments, material adverse change verification, and employee retention agreements. New FTC HSR rules effective February 2025 add 68 to 121 hours per filing. The gap typically lasts 30 to 90 days for domestic deals and up to 12 months for cross-border transactions with multiple regulatory jurisdictions. Peony built-in e-signatures with AI field detection let deal teams execute closing documents and ancillary agreements without switching to a separate signing tool.

Related Resources

- Best Home-Services M&A Advisors — the HVAC/plumbing/electrical sell-side bench, the consolidator map, and why the 2-week exploding offer is a pricing strategy

- Corporate Acquisition Strategy in 2026 — the layer above this process guide: programmatic M&A evidence, the 100→10→1 pipeline, and the machinery that makes acquisition #4 cheaper than #1

- How to Acquire a Company in 2026 — the first-time buyer's operating manual for $1M–$25M deals: SBA 7(a) under SOP 50 10 8, QoE, SDE add-backs, and the 75-day close

- Cross-Border M&A (2026) — what changes when the deal crosses a border: FDI screening, GDPR-safe diligence, locked-box mechanics, works councils

- Merger vs Acquisition: What's the Real Difference in 2026? — definitional, tax, antitrust, and PR-framing differential with 2026 deal examples (Capital One-Discover, HPE-Juniper, Pinnacle-Synovus, McCormick-Unilever RMT)

- Types of M&A Deals: Horizontal, Vertical, Conglomerate (2026 Examples + Antitrust by Type) — 5-type taxonomy with HSR Scrutiny Index, Synergy Realization Rate, DD Focus Shift, and Premium-Paid Pattern frames

- M&A Due Diligence Process: The 6-Phase Playbook

- M&A Data Rooms: What Deal Teams Get Wrong

- Due Diligence Checklist (174 Documents)

- Acquisition Integration Guide

- What Is a Virtual Data Room

- Due Diligence Cost Breakdown

- VDR Redaction Guide for Due Diligence

- VDR Permissions Guide for Due Diligence

- Best Data Rooms for Private Equity

- Top 10 Virtual Data Room Providers

- How to Structure an Earnout in an M&A Sale — the 2026 founder playbook including the 79% never-paid stat, Auris/Alexion case law, and the IRC §453A $5M trap

- M&A Solutions

- Due Diligence Solutions

- Private Equity Solutions