Tax Due Diligence Checklist (8 Pillars M&A Tax Advisors Miss) in 2026

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Tax Due Diligence Checklist (8 Pillars M&A Tax Advisors Miss) in 2026

Last updated: May 2026

I run Peony, a data room platform used in hundreds of M&A transactions. Over the past two years I have helped tax advisors, PE operating partners, and corporate development teams set up tax due diligence rooms for deals ranging from a single-entity domestic acquisition to a 14-jurisdiction cross-border carve-out with transfer pricing intercompany agreements stretching back a decade. The pattern is consistent: the financial DD team flags a few tax line items, the buyer assumes that covers it, and then a seven-figure sales tax exposure surfaces three months after closing.

Tax due diligence is not a subset of financial DD. It is a parallel workstream that asks fundamentally different questions about the same data. This post is the 8-pillar checklist I wish someone had handed me before my first deal.

TL;DR: Tax-related purchase price adjustments appear in 30 to 40% of mid-market M&A transactions (EY M&A Tax Survey, 2025). The average state sales tax audit assessment is $475,000 (Avalara, 2025). Over 50 jurisdictions have now enacted BEPS 2.0 Pillar Two rules imposing a 15% global minimum tax (OECD, 2026), and the OECD's January 2026 "side-by-side" package recognizes the U.S. as the only Qualified SbS Regime — creating asymmetric exposure for US-headquartered groups with significant offshore footprint. Yet most buyers still run tax DD as a financial DD add-on rather than a standalone workstream. Below is the 8-pillar framework that catches what generic checklists miss.

What M&A Tax Due Diligence Is and Why It Matters

At a high level, M&A tax due diligence has three jobs:

- Find historic exposures -- underpaid taxes, aggressive positions, open audits, missing filings, and unreported nexus.

- Understand the future tax profile -- how the target's tax footprint behaves once it sits under your ownership structure, including combined effective tax rate changes and attribute limitations.

- Inform deal structure and protection -- pricing adjustments, share versus asset elections, covenants, indemnities, escrows, and warranty and indemnity (W&I) insurance sizing.

If any one of those three jobs is skipped, the deal model is wrong. A purchase price that ignores a $2 million sales tax exposure is $2 million too high. A stock deal that assumes full NOL utilization without testing Section 382 limits may destroy $10 million in expected tax savings on day one.

Practitioners typically break the work into three deliverables:

- An information request list (the document checklist below)

- Management interviews with the target's tax team and external advisors

- Quantitative analysis and modeling of exposures, attributes, and deal structure alternatives

In 2026 you also have to overlay BEPS 2.0 Pillar Two minimum tax rules, rapidly changing enforcement environments in multiple jurisdictions, and the accelerating shift to AI-assisted tax compliance that changes how targets manage -- or fail to manage -- their tax functions.

Think of tax DD as a focused scan of the target's past and future tax life. Not a box-ticking exercise. The checklist below is organized into 8 pillars because that structure maps to how tax risk actually clusters in real deals.

The 8-Pillar Tax DD Framework

You can adapt this to any jurisdiction, but the logic stays the same across domestic, cross-border, PE, and strategic transactions.

Pillar 1: Corporate Income Tax

Start with the core compliance picture.

Federal and state income tax returns -- Obtain corporate income tax returns for at least the last 3 to 5 years for every entity, plus notices of assessment, payment records, and correspondence with tax authorities. For U.S. targets, this means federal returns and every state where the target files. For multinational targets, the equivalent filings in each jurisdiction.

Open audits and disputes -- Understand what periods are under examination, how material the issues are, and whether the positions taken are technically defensible. Request copies of audit correspondence, revenue agent reports, and any settlement proposals or litigation filings.

Uncertain tax positions (UTPs) -- Review ASC 740 / FIN 48 reserves, supporting technical memoranda, and any external opinions. Compare the reserve methodology against the actual positions to test whether reserves are adequate or overly optimistic.

Historic restructurings -- Mergers, spin-offs, debt restructurings, entity conversions, and changes in accounting methods that may have lingering tax effects. A Section 351 contribution from five years ago can still create problems if documentation was incomplete.

Effective tax rate reconciliation -- Walk the reported effective tax rate back to the statutory rate and understand every reconciling item. Permanent differences, credits, and rate changes between jurisdictions tell you where value creation opportunities and hidden risks sit.

Your goal: is the target broadly compliant, or are there skeletons -- non-filed returns, aggressive loss utilizations, or "creative" positions -- that could crystallize post-closing?

Pillar 2: Indirect Taxes

Indirect taxes are consistently where the most material surprises hide, particularly for targets that have grown quickly across state lines or international borders.

Sales tax nexus -- Where is the target registered for sales tax, and where should it be registered based on actual economic activity? Post-Wayfair, economic nexus thresholds (typically $100,000 in sales or 200 transactions) apply in most U.S. states. A SaaS company selling into 40 states but collecting tax in only 12 may have seven-figure exposure.

VAT and GST registrations -- For international targets, verify registration status in every jurisdiction where taxable supplies occur. Digital services rules in the EU, UK, Australia, and Canada have expanded registration requirements significantly since 2020.

Returns and reconciliations -- Review a sample of indirect tax returns and reconcile reported taxable base to revenue in the financial statements. Discrepancies often indicate misclassification of taxable versus exempt revenue.

Customs and duties -- For importers, review tariff classification, valuation methodology, country-of-origin declarations, and free trade agreement utilization. With U.S. Section 301 tariffs on Chinese goods still in effect and new trade enforcement expanding, customs exposure can be material for manufacturing and hardware targets.

Treatment of key revenue streams -- Cross-border digital services, marketplace facilitator obligations, and exempt-versus-taxable splits deserve line-by-line review against current rules in major jurisdictions.

A secure data room with granular permissions keeps indirect tax workpapers separated from the broader DD population so only the tax workstream accesses sensitive nexus analysis.

Pillar 3: Employment and Payroll Tax

Employment tax risk is growing as remote work, gig models, and equity compensation create classification and withholding complexity that did not exist a decade ago.

Payroll tax filings and payments -- Review payroll tax returns across all entities and jurisdictions for consistency. Look for late filings, underpayments, or unfiled returns in states where remote employees work.

Worker classification -- This is the single highest-risk item in employment tax DD for technology, staffing, and gig economy targets. Misclassifying employees as independent contractors triggers retroactive payroll taxes, penalties, and interest -- plus potential Department of Labor and state agency exposure. Request the target's classification methodology, any IRS SS-8 filings, and state audit correspondence.

Equity compensation -- Options, RSUs, phantom equity plans, and profits interests each have different income recognition and withholding rules. Verify that the target has correctly withheld and reported at exercise, vesting, and settlement. International equity comp adds country-by-country reporting obligations.

Mobile employees -- Executives and key staff working cross-border can trigger unexpected payroll tax and social security obligations in multiple jurisdictions. Request a mobility tracking log if one exists.

Benefits and retirement plans -- Deferred compensation arrangements under Section 409A, retirement plan compliance (Form 5500 filings), and post-employment benefit obligations that may transfer to the buyer.

Pillar 4: International Tax

For cross-border groups, this pillar can be the single largest risk driver and the most complex to analyze.

Group structure and intercompany flows -- Map the entire legal entity structure and trace the flow of intercompany financing, royalties, management fees, and supply chain payments. Every intercompany transaction is a potential transfer pricing issue and a potential withholding tax obligation.

Permanent establishment (PE) risk -- Where might the target's activities in a jurisdiction have created a taxable presence despite no local entity? Employees traveling to or working remotely in foreign jurisdictions, dependent agents signing contracts, and fixed places of business can all trigger PE under domestic law or treaty definitions. Post-COVID remote work has expanded PE risk significantly.

Transfer pricing -- Request the master file, local files, and country-by-country reports under BEPS Action 13. Review the target's transfer pricing policies, benchmarking studies, and any advance pricing agreements (APAs). Check for past TP audits, adjustments, or mutual agreement procedure (MAP) cases. Transfer pricing documentation gaps are the most common international tax DD finding.

Withholding taxes -- On dividends, interest, royalties, and service fees paid cross-border. Verify that the target has applied correct treaty rates and maintained beneficial ownership documentation. Treaty shopping risk in structures using holding companies in the Netherlands, Luxembourg, or Singapore should be tested.

BEPS 2.0 and Pillar Two -- From 2024 onward, jurisdictions representing over 90% of global GDP have begun implementing the OECD's Pillar Two rules. For M&A this means:

- Checking whether the combined post-deal group will be in scope (generally EUR 750 million or more in consolidated revenue)

- Calculating jurisdictional effective tax rates against the 15% minimum floor

- Quantifying potential top-up tax liabilities in low-tax jurisdictions

- Assessing new GloBE information return reporting obligations and data requirements

- Evaluating the Transitional CbCR Safe Harbour and whether the target currently qualifies

Over 50 jurisdictions have enacted domestic Pillar Two legislation by early 2026. In January 2026 the OECD released its "side-by-side" package establishing a Central Record of qualified regimes; as of January 5, 2026, the U.S. is the only country identified as meeting eligibility for the Qualified SbS Regime, and no jurisdiction has yet been recognized as a Qualified UPE Regime. The asymmetry between jurisdictions -- particularly the interaction between the U.S. GILTI/BEAT regime and the OECD framework -- creates deal-specific complexity that generic checklists miss entirely.

Peony AI extraction lets international tax advisors ask natural-language questions across uploaded transfer pricing studies, intercompany agreements, and CbCR filings -- and get cited answers with exact page numbers. This eliminates days of manual cross-referencing across hundreds of documents.

Pillar 5: Tax Attributes

Tax DD is not just about risk. It is also about identifying and protecting value.

Net operating losses (NOLs) -- Quantify federal and state NOL carryforwards, carryback availability, and expiry schedules. For pre-2018 NOLs, the 20-year carryforward limitation applies. For post-2017 NOLs, the 80% taxable income limitation and indefinite carryforward rules under TCJA apply.

Section 382 limitations -- This is the most commonly missed item in tax DD for stock acquisitions. An ownership change (more than 50 percentage points over a 3-year testing period) limits annual NOL utilization to the Section 382 amount: target equity value multiplied by the long-term tax-exempt rate. A $100 million target with $50 million in NOLs may see annual utilization capped at $4 to 5 million, dramatically changing the value of those losses.

- Has the target already undergone a prior ownership change?

- Will this transaction trigger a new ownership change?

- Are there built-in gains or losses that affect the limitation?

Tax credits -- R&D credits (Section 41), investment tax credits, state and local incentives, employment zone credits, and any credits subject to recapture. Verify documentation supports the credit claims and that ongoing qualification conditions will survive post-closing changes.

Step-up analysis -- In an asset deal or Section 338(h)(10) election, the buyer gets a stepped-up tax basis in acquired assets. Model the after-tax benefit of additional amortization and depreciation against the tax cost to the seller. This analysis often drives the share-versus-asset decision.

Tax holidays and incentive agreements -- For targets with negotiated tax holidays, development zone incentives, or government grants with clawback provisions, verify that deal-related changes (ownership, location, headcount) do not trigger termination or recapture.

Pillar 6: Transaction Structure

The findings from Pillars 1 through 5 feed directly into deal structuring. This pillar is where tax DD stops being a backward-looking exercise and starts shaping the economics of the deal.

Asset deal versus stock deal -- In an asset deal, the buyer acquires specific assets and assumes only specified liabilities, with a stepped-up basis for depreciation and amortization. In a stock deal, the buyer acquires the entity and inherits all historic liabilities -- known and unknown. The tax cost to the seller often differs materially between structures.

Section 338(h)(10) election -- Treats a stock acquisition as an asset acquisition for tax purposes. Both buyer and seller must consent. The buyer gets step-up without the legal complexity of transferring individual assets, but the seller bears the tax cost of a deemed asset sale. Model both scenarios.

Tax-free reorganizations -- Sections 368(a)(1)(A) through (G) provide for tax-deferred reorganizations when specific requirements (continuity of interest, continuity of business enterprise, business purpose) are met. If the target's shareholders want rollover equity or the deal involves a merger of equals, test whether a tax-free structure works.

Partnership and LLC structuring -- For targets organized as pass-throughs, Section 743(b) basis adjustments, Section 754 elections, and hot asset rules (Section 751) create a separate layer of complexity.

Earnout and deferred consideration -- Tax treatment of earnout payments depends on whether they are treated as purchase price adjustments, compensation, or contingent payments under Section 453. Mischaracterization creates problems for both parties.

A well-organized data room with AI-powered Q&A lets both buyer and seller tax teams collaborate on structure analysis without emailing sensitive models back and forth.

Pillar 7: Tax Agreements and Indemnities

Once the DD findings are quantified, they flow into the legal protections negotiated in the purchase agreement.

Tax representations and warranties -- Scope of reps covering compliance, no pending audits, no waivers of statute of limitations, and no tax sharing agreements. Negotiate specific reps for material items identified during DD (e.g., the target represents that it has no sales tax nexus outside of states X, Y, and Z).

Tax indemnities -- Allocation of pre-closing versus post-closing tax liability. Standard approach: seller indemnifies for all pre-closing taxes and buyer bears post-closing taxes, with a proration mechanism for straddle periods. Specific indemnities for identified exposures (nexus, TP adjustments, pending audits) sit on top.

Escrow and holdback -- Portion of purchase price held in escrow to cover identified or probable tax exposures. Size escrow based on DD findings, typically 5 to 15% of identified exposure with a cushion for unknown items.

W&I insurance -- Warranty and indemnity insurance has become standard in PE transactions. Understand what tax-specific exclusions the policy contains. Known tax issues identified in DD are typically carved out. Synthetic tax indemnity policies can cover specific exposures that sellers refuse to indemnify.

Tax sharing and allocation agreements -- If the target is part of a consolidated group, existing tax sharing agreements determine who bears the economic burden of taxes. Review termination provisions -- these agreements often survive closing and create ongoing obligations.

Historic SPA tax clauses -- Previous acquisition agreements may contain tax covenants, indemnities, or cooperation obligations that still bind the target. Review all prior deal documents.

Peony e-signatures with AI-powered field detection let deal teams execute tax indemnity agreements, escrow instructions, and SPA amendments directly in the data room without switching to a separate signing tool.

Pillar 8: Tax Processes and Controls

The final pillar assesses how tax is managed day-to-day. A clean compliance history means less if the underlying processes cannot sustain it under new ownership.

Tax function staffing -- Who is responsible for tax? Internal team, external advisors, or both? What is the experience level and bandwidth? If tax compliance depends on a single person who is leaving post-close, that is a material risk.

Compliance calendar and filing history -- Request the complete filing calendar across all jurisdictions and tax types. Verify that extensions are properly filed and that no jurisdictions have been missed. Late filings often correlate with other compliance issues.

Technology and automation -- What tax technology does the target use for provision, compliance, transfer pricing, and indirect tax? Is the data extraction process automated or manual? Targets still running tax compliance on spreadsheets represent both a risk (error-prone) and an opportunity (post-close modernization).

Internal controls -- How are tax positions reviewed and approved before filing? Is there a tax risk register? Are there documented policies for transfer pricing, sales tax collection, and worker classification? SOX-compliant targets should have documented tax-related internal controls.

Response to law changes -- How does the target track and implement legislative changes? The pace of tax law change -- BEPS 2.0, Pillar Two, state nexus expansion, digital services taxes -- means targets without a systematic tracking process are likely falling behind.

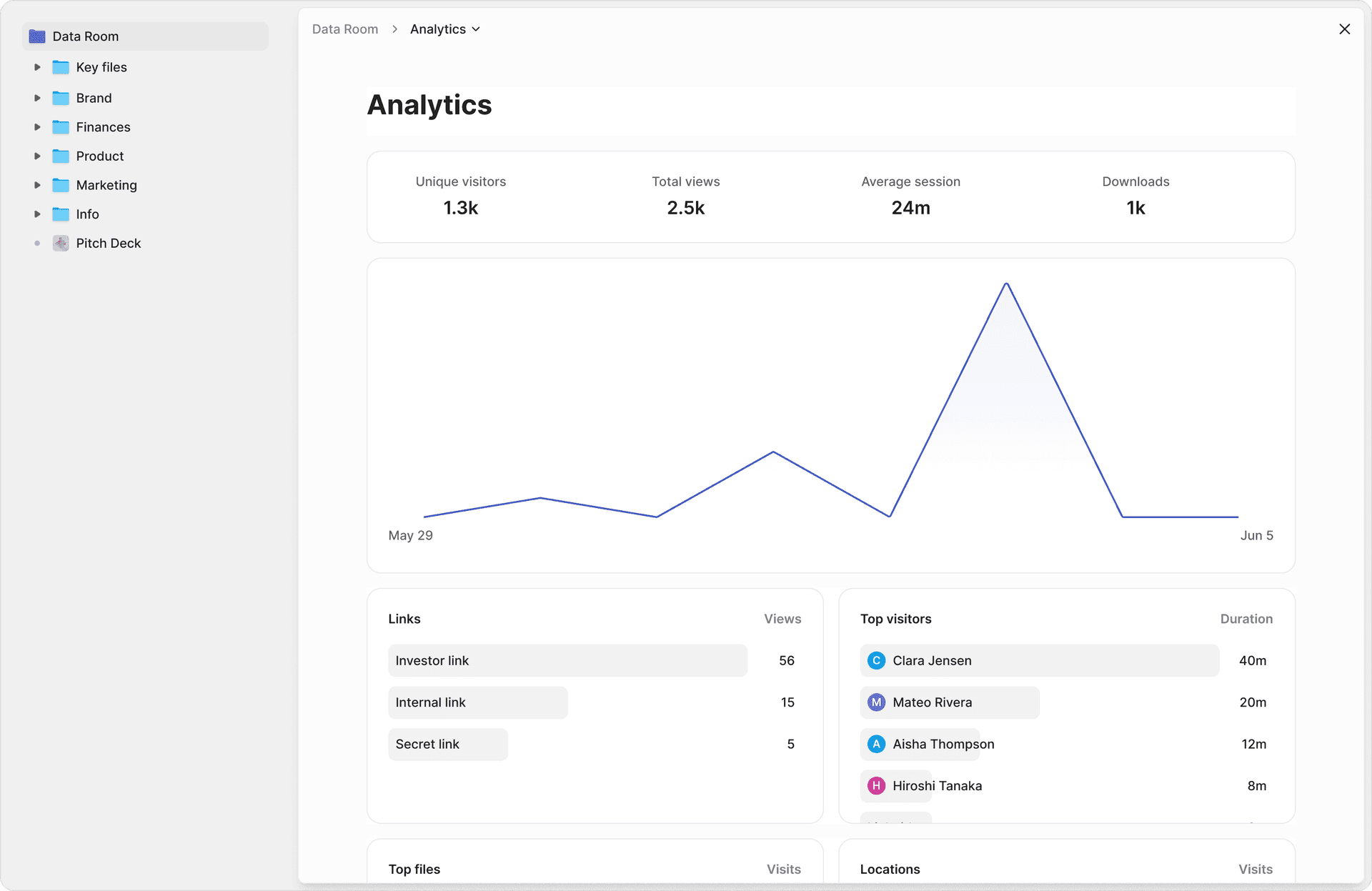

If governance is weak, even a "clean" historic file can deteriorate quickly post-closing. Peony's page-level analytics show deal leads exactly which sections of the tax process assessment each reviewer actually read, so nobody rubber-stamps the controls review.

Tax DD Document Checklist (Organized by Pillar)

This is the information request list I use as a starting template. Adapt it to the target's jurisdiction, size, and industry.

Corporate Income Tax (Pillar 1)

| # | Document | Years |

|---|---|---|

| 1 | Federal and state/provincial income tax returns | 3-5 |

| 2 | Notices of assessment and payment records | 3-5 |

| 3 | Tax authority correspondence and audit files | All open |

| 4 | ASC 740 / FIN 48 uncertain tax position schedules | 3-5 |

| 5 | Technical memoranda and external tax opinions | All |

| 6 | Effective tax rate reconciliations | 3-5 |

| 7 | Documentation for historic restructurings and entity changes | All |

Indirect Taxes (Pillar 2)

| # | Document | Years |

|---|---|---|

| 8 | Sales tax and use tax registrations by jurisdiction | Current |

| 9 | Sales tax returns and nexus analysis | 3-5 |

| 10 | VAT/GST registrations and returns | 3-5 |

| 11 | Customs classifications, valuations, and duty payments | 3-5 |

| 12 | Exemption certificates received from customers | Current |

| 13 | Taxability matrix for products and services | Current |

Employment and Payroll Tax (Pillar 3)

| # | Document | Years |

|---|---|---|

| 14 | Payroll tax returns by jurisdiction | 3-5 |

| 15 | Worker classification analysis and supporting documentation | All |

| 16 | IRS SS-8 filings or state classification rulings | All |

| 17 | Equity compensation plan documents and withholding records | All |

| 18 | Cross-border mobility tracking log | Current |

| 19 | Section 409A deferred compensation documentation | All |

| 20 | Form 5500 filings for retirement plans | 3-5 |

International Tax (Pillar 4)

| # | Document | Years |

|---|---|---|

| 21 | Legal entity structure chart with ownership percentages | Current |

| 22 | Intercompany agreements (loans, licenses, services, supply) | All |

| 23 | Transfer pricing master file and local files | 3 |

| 24 | Country-by-country reports (CbCR) | 3 |

| 25 | Advance pricing agreements (APAs) and MAP cases | All |

| 26 | Permanent establishment analysis by jurisdiction | Current |

| 27 | Withholding tax certificates and treaty position documentation | 3-5 |

| 28 | BEPS 2.0 Pillar Two impact assessment (if applicable) | Current |

| 29 | GloBE information return filings | All filed |

Tax Attributes (Pillar 5)

| # | Document | Years |

|---|---|---|

| 30 | NOL carryforward schedules by jurisdiction | All |

| 31 | Section 382 ownership change analysis | All |

| 32 | R&D credit studies and supporting documentation | 3-5 |

| 33 | Investment and employment tax credit certificates | All |

| 34 | Tax holiday and incentive agreements | All |

| 35 | Asset tax basis schedules | Current |

Transaction Structure (Pillar 6)

| # | Document | Years |

|---|---|---|

| 36 | Prior deal structuring memoranda | All |

| 37 | Section 338(h)(10) election analysis (if applicable) | Current |

| 38 | Tax-free reorganization opinion letters | All |

| 39 | Partnership and LLC agreement tax provisions | Current |

Tax Agreements and Indemnities (Pillar 7)

| # | Document | Years |

|---|---|---|

| 40 | Tax sharing and tax allocation agreements | All |

| 41 | Prior SPA tax clauses and indemnity provisions | All |

| 42 | Group relief and consolidation arrangements | Current |

| 43 | Existing tax indemnities given or received | All |

| 44 | W&I insurance policies with tax-specific terms | Current |

Tax Processes and Controls (Pillar 8)

| # | Document | Years |

|---|---|---|

| 45 | Tax compliance calendar by jurisdiction and tax type | Current |

| 46 | Tax function organizational chart | Current |

| 47 | External advisor engagement letters and scope | Current |

| 48 | Tax technology stack documentation | Current |

| 49 | Tax risk register and internal control documentation | Current |

| 50 | Tax policy manuals (TP, sales tax, classification) | Current |

Peony AI auto-indexing organizes all 50 document categories into a clean folder structure in under 3 minutes. Upload everything and let AI sort it rather than spending two days manually building the data room index.

How Tax DD Fits Alongside IT, Environmental, and Legal DD

Tax DD is one workstream within a broader DD operation. In 2026, sophisticated deal teams run four DD subtypes in parallel because the liability surfaces no longer overlap cleanly. Below is how the four compare and where they intersect.

| Workstream | Primary surface | 2026 escalation driver | Typical liability tail |

|---|---|---|---|

| Tax DD (this post) | Filing positions, nexus, attributes, structure | BEPS 2.0 Pillar Two; state nexus expansion | 3-10 years post-close |

| IT DD | Infrastructure, licenses, security, AI integration debt | Third-party breach involvement doubled to 30% (Verizon DBIR 2025) | Indefinite (decade+) |

| Environmental DD | Contamination, PFAS, CSDDD, BFPP defense | PFAS CERCLA designation reaffirmed September 2025 | Multi-decade |

| Legal DD | Contracts, litigation, regulatory, IP | EU AI Act enforcement; CSDDD value-chain obligations | 2-7 years post-close |

The intersections matter as much as the boundaries:

- Tax × IT: BEPS 2.0 effective tax rate calculations depend on IT system outputs. If the target's tax data lives in spreadsheets that the IT DD flagged as fragility-5, the Pillar Two calculation is built on sand.

- Tax × Environmental: Environmental remediation reserves create deferred tax assets. Indemnity payments for legacy contamination have specific tax characterization that affects both buyer and seller's deal economics.

- IT × Environmental: Climate-risk DD (now part of env DD since the SEC climate rule collapse) requires IT-system access to emissions and energy usage data. Targets without that infrastructure are fragility-4 on both axes.

The right framing: tax DD is a financial workstream with international and structural complexity. IT DD is an operational workstream with regulatory and integration complexity. Environmental DD is a liability workstream with multi-decade tail risk. None of the three is bolted onto financial DD — each is a parallel scope with its own information request list, its own specialist team, and its own findings register that feeds into the deal economics.

Common Tax DD Mistakes

After supporting dozens of tax DD processes, these are the mistakes I see most often.

Treating tax DD as a financial DD add-on. The financial DD team will flag tax provisions and maybe obvious exposures, but they are not testing filing positions, nexus questions, transfer pricing arm's-length standards, or Section 382 limitations. Tax DD needs its own workstream, its own information request list, and its own report.

Ignoring state and local tax. Buyers fixate on federal income tax and miss that the target has sales tax nexus in 35 states but only collects in 8. The average state sales tax audit assessment is $475,000 (Avalara, 2025), and that number climbs quickly for targets with high-volume e-commerce or multi-state SaaS revenue.

Assuming NOLs transfer at face value. A target with $50 million in NOLs looks attractive until you model Section 382. If the ownership change limits annual utilization to $4 million, and the NOLs expire in 15 years, the present value of those losses is a fraction of the headline number. Every stock acquisition should include a Section 382 analysis.

Skipping the BEPS 2.0 assessment. Even if the standalone target is below the EUR 750 million threshold, the combined post-deal group may be in scope. Buyers who wait until after closing to assess Pillar Two exposure can face unexpected top-up taxes and compliance obligations in multiple jurisdictions.

Not testing worker classification. A target with 500 contractors and no classification methodology is sitting on a payroll tax bomb. The IRS, Department of Labor, and state agencies are all increasing enforcement. The cost of reclassification -- retroactive taxes, penalties, interest, plus benefits catch-up -- can be material.

Under-sizing tax indemnities. Generic indemnity baskets and caps that were negotiated before tax DD is complete often prove insufficient when specific exposures are quantified. The indemnity structure should be informed by DD findings, not the other way around.

Neglecting the compliance calendar. If the target has a filing due three weeks after closing and there is no transition plan, the buyer may miss the deadline and incur penalties before even understanding the filing process. Request the complete compliance calendar during DD and build a transition timeline.

How Peony Supports Tax Due Diligence

I built Peony because I kept seeing the same infrastructure problem in every deal: tax advisors spending more time requesting, organizing, and searching for documents than actually analyzing them. A tax DD process that should take four weeks stretches to eight because the data room is disorganized, advisors cannot find documents, and Q&A rounds take days instead of hours.

Here is what Peony does differently for tax DD specifically.

AI-powered document extraction. Tax advisors upload the entire information request response -- hundreds of returns, schedules, agreements, and memos -- and Peony AI auto-indexes everything into a clean folder structure in under 3 minutes. Then advisors ask natural-language questions like "What is the NOL carryforward balance by jurisdiction as of December 2025?" and get cited answers with exact page numbers across every uploaded document. This eliminates the manual cross-referencing that consumes the first week of every tax DD engagement.

Smart Q&A workflow for tax questions. Counterparties submit tax DD questions directly in the Peony data room. AI drafts answers from uploaded documents. The target's tax team reviews the drafts, approves or edits, and sends the response -- with a full audit trail. No more email chains with 47 replies and three conflicting answers to the same transfer pricing question.

Page-level analytics for tax workstream management. Peony analytics show exactly which pages of each tax document every reviewer read and for how long. Tax DD leads can see whether the transfer pricing specialist actually reviewed the master file or just skimmed the executive summary. This is the difference between "we looked at the TP docs" and "we read every benchmarking study and found three intercompany transactions without documentation."

Security built for sensitive tax data. Tax DD documents contain the most sensitive financial information in any deal -- effective tax rates, uncertain positions, audit correspondence, and structuring analysis. Peony screenshot protection blocks and logs screenshot attempts. Dynamic watermarks embed viewer identity into every rendered frame. NDA gates require counterparties to sign before accessing any documents. AI-powered redaction identifies and removes PII, financial data, and sensitive terms before sharing with broader deal teams.

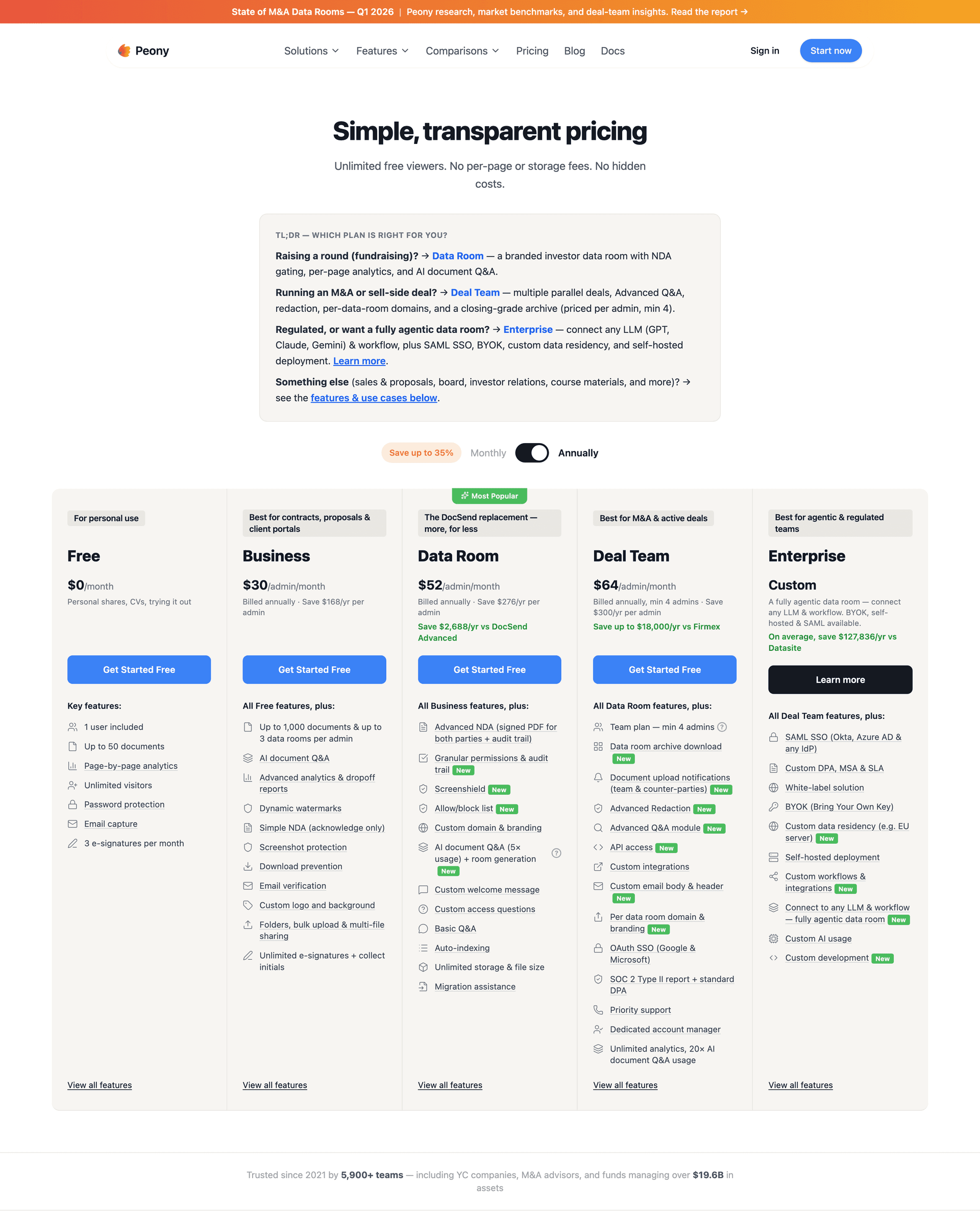

Cost that makes sense for mid-market tax DD. Legacy VDR providers charge $5,000 to $25,000 per month for a single deal room. Peony Business starts at $30 per admin per month with unlimited viewers, AI features, and no per-page fees. For a PE firm running tax DD on six portfolio acquisitions per year, the cost difference is six figures annually.

Bottom Line

Tax due diligence is not a box-ticking exercise bolted onto financial DD. It is a parallel workstream that tests filing positions, quantifies exposures, models attribute value, and directly shapes deal structure and legal protections. The 8-pillar framework above -- corporate income tax, indirect taxes, employment tax, international tax, tax attributes, transaction structure, tax agreements, and processes -- covers the full scope of what a thorough tax DD engagement should address.

The most consequential mistakes are not exotic. They are pedestrian: missing sales tax nexus, overvaluing NOLs, ignoring BEPS 2.0, and under-sizing indemnities. A structured checklist with the right data room infrastructure catches these issues before they become post-closing surprises.

If you are running tax DD on a live deal, start with the 50-item document checklist above, upload everything to a Peony data room with AI auto-indexing, and let your advisors spend their time analyzing rather than searching.

Frequently Asked Questions

What is tax due diligence in M&A?

Tax due diligence in M&A is a structured investigation into the target company's historic tax exposures, future tax profile, and deal structure implications across all tax types including corporate income tax, indirect taxes, employment taxes, international tax, and tax attributes. It goes beyond financial DD by testing filing positions, nexus risk, transfer pricing documentation, BEPS 2.0 exposure, and Section 382 limitations. Peony AI extraction lets tax advisors ask natural-language questions across thousands of uploaded tax documents and get cited answers with exact page numbers, eliminating days of manual document review.

What documents are needed for tax due diligence?

A comprehensive tax DD request list includes 40 or more document categories organized across 8 pillars: corporate income tax returns and assessments for 3 to 5 years, indirect tax registrations and filings, payroll tax records and worker classification analysis, transfer pricing documentation and intercompany agreements, NOL and credit schedules with Section 382 analysis, deal structure memoranda, tax sharing and indemnity agreements, and compliance calendars with internal control documentation. Peony AI auto-indexing organizes thousands of tax documents into review-ready folder structures in under 3 minutes, so advisors spend time analyzing rather than sorting.

How long does tax due diligence take?

Tax due diligence typically takes 3 to 6 weeks for domestic mid-market deals and 6 to 12 weeks for cross-border transactions with multiple jurisdictions, transfer pricing complexity, or BEPS 2.0 exposure. The timeline depends on the target's document readiness, number of entities, and whether open audits or controversies require deeper analysis. Peony page-level analytics show exactly which sections of the tax DD report each reviewer actually read and for how long, so deal leads can identify stalled workstreams before they blow the timeline.

What is the difference between tax DD and financial DD?

Financial DD examines historic financial statements, revenue quality, working capital, and debt for accuracy and sustainability. Tax DD uses overlapping data but asks different technical questions: are filing positions defensible, does nexus exist in unregistered jurisdictions, are transfer pricing policies arm's-length compliant, will NOLs survive a change of ownership under Section 382, and how does BEPS 2.0 Pillar Two affect the combined group's effective tax rate. Peony smart Q&A workflow lets tax and financial DD teams submit questions in the same data room, where AI drafts answers and routes them through a team approval process, keeping both workstreams coordinated.

What are the biggest tax risks in an acquisition?

The biggest tax risks in acquisitions are undisclosed sales tax nexus in multiple states, aggressive transfer pricing positions without adequate documentation, misclassified workers triggering retroactive payroll tax and penalties, NOLs that are limited or eliminated by Section 382 ownership change rules, and unrecorded indirect tax liabilities from rapid geographic expansion. For cross-border deals, permanent establishment risk and BEPS 2.0 top-up taxes add material exposure. Peony screenshot protection blocks and logs capture attempts on sensitive tax documents, preventing confidential exposure data from leaking to competing bidders.

How does BEPS 2.0 affect M&A tax due diligence?

BEPS 2.0 Pillar Two imposes a 15% global minimum effective tax on multinational groups with consolidated revenue above EUR 750 million. In M&A, this means tax DD must now assess whether the combined post-deal group triggers Pillar Two scope, calculate jurisdictional effective tax rates against the 15% floor, quantify potential top-up tax liabilities, and evaluate new compliance and reporting obligations. Over 50 jurisdictions have enacted Pillar Two rules as of early 2026, and the OECD's January 2026 side-by-side package recognizes the U.S. as the only Qualified SbS Regime. Peony dynamic watermarks embed each viewer's identity into every rendered frame of BEPS analysis documents, making attribution instant if sensitive cross-border tax data surfaces outside the data room.

Should I do tax DD on an asset deal or stock deal?

Yes, tax DD is critical for both deal types but the focus differs. In a stock deal, the buyer inherits all historic tax liabilities, making exposure identification the priority. In an asset deal, the buyer gets a stepped-up tax basis in acquired assets but must verify the seller's allocation, confirm no successor liability, and model the amortization and depreciation benefit. Section 338(h)(10) elections and tax-free reorganizations add further complexity. Peony NDA gates require counterparties to sign a non-disclosure agreement before accessing any deal structure documents in the data room, adding a legal control layer before sensitive asset versus stock analysis is shared.

What is the best data room for tax due diligence?

Peony is the best data room for tax due diligence in 2026. At $30 per admin per month on the Business plan, Peony includes AI-powered document extraction that lets tax advisors ask natural-language questions across all uploaded returns and get cited answers with exact page numbers, page-level analytics showing which sections each reviewer read, NDA gating, screenshot protection, dynamic watermarking, e-signatures for engagement letters, and setup in under 5 minutes. Legacy VDR providers charge $5,000 to $25,000 per month and take weeks to deploy.

Related Resources

- IT Due Diligence (2026): 6-Axis Fragility Audit — parallel workstream covering tech-stack risk

- Environmental Due Diligence (2026): PFAS, CSDDD, BFPP — for industrial and real estate targets

- AI Due Diligence (2026): 5-Layer Audit + EU AI Act Map — for AI-specific assets

- Due Diligence Data Room Checklist (174 Documents)

- M&A Due Diligence Process Guide

- Mergers and Acquisitions Process Guide (8 Phases)

- Vendor Due Diligence Checklist

- Virtual Data Room Redaction for M&A

- What Is a Virtual Data Room?

- Data Room Folder Structure Guide

- Investment Due Diligence Checklist — 7-pillar buyer-side DD framework

- Independent Sponsor Guide

- Real Estate Due Diligence Checklist

- Roll Equity in M&A: 2nd-Bite Math + OBBBA QSBS Trap — how seller rollover works in 2026 LMM deals, the OBBBA QSBS trap when rolling into partnership HoldCo, and the 11 founder pitfalls

- How to Structure an Earnout in an M&A Sale — the 2026 founder playbook including the 79% never-paid stat, Auris/Alexion case law, and the IRC §453A $5M trap

- M&A Data Rooms by Peony

- Due Diligence Solutions