Investment Due Diligence Checklist (7 Pillars, Buyer Side) in 2026

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Investment Due Diligence Checklist (7 Pillars, Buyer Side) in 2026

Last updated: April 2026

I run Peony, a data room platform used by 5,900+ customers. I see inside thousands of diligence processes every quarter -- the well-run ones that close on time and the messy ones that blow up at the eleventh hour. The difference is almost never the deal itself. It is the framework the investor uses to evaluate it.

This post is the buyer-side investment due diligence checklist -- what investors evaluate, why each area matters, and where deals actually die. If you are a founder or seller looking for the document upload list, head to the 174-document seller-side checklist. If you are raising a seed or Series A and want startup-specific guidance, see the startup due diligence guide.

TL;DR: Bain's 2025 Global Private Equity Report found that 42% of PE deals fail to meet underwriting expectations, most often because DD missed commercial or operational risks hiding in plain sight. The optimal DD duration is approximately 139 days -- deals at that length had the highest completion rates, lowest premiums (22%), and best 12-month shareholder returns (Bayes Business School, 900+ deals). Below is the 7-pillar investor-side framework I see the best deal teams use, with the 10 red flags that kill deals most often.

What Investment Due Diligence Means in 2026

Investment due diligence is a structured, buyer-side investigation into what you are buying, how it makes money, what could go wrong, and how you will eventually get your capital back. It is not the same as the seller's data room upload process -- that is the supply side. This checklist is the demand side: the analytical framework an investor applies to the materials.

Three regulatory pillars make this non-optional for institutional capital:

- SEC fiduciary standard. Registered investment advisers must conduct reasonable investigation and document the basis for every recommendation. The SEC has repeatedly sanctioned advisers who relied on offering documents alone without independent verification.

- ERISA prudent-investor rule. Pension fund fiduciaries must investigate investments with the care, skill, and diligence a prudent person would use. ERISA Section 404(a)(1)(B) is the statutory anchor, and DOL enforcement actions confirm that "we read the PPM" is not enough.

- Common-law duty of care. Even outside registered structures, GPs owe LPs a duty to investigate before deploying capital. Failure to conduct DD can create breach-of-fiduciary claims in Delaware Chancery Court, which handles the majority of LP-GP disputes.

In practical terms, DD protects you from three things:

- Regulatory exposure -- you did not do your homework, and a regulator or LP auditor notices.

- Financial loss -- you missed a material risk that was discoverable in the data room.

- Reputational damage -- your LP, board, or co-investors ask "how did you miss that?" and you have no documented answer.

The asymmetry is stark: thorough DD costs 1 to 3% of deal value in professional fees and internal time. A blown deal costs 100% of deployed capital plus opportunity cost, legal fees, and reputational fallout. The math always favors doing the work.

Before You Open the Data Room: Clarify Your Mandate

Before disappearing into a data room, get brutally clear on your own criteria:

- Target return profile. IRR, cash-on-cash multiple, DPI, and TVPI targets. A 3x MOIC target implies very different DD focus than a 15% net IRR target.

- Risk appetite and loss tolerance. What is the maximum acceptable loss on any single position? What is the portfolio-level drawdown limit?

- Time horizon and liquidity needs. A 10-year fund has different DD requirements than a family office with perpetual capital.

- Sector, stage, and geography focus. These constrain the universe and determine which expert networks and benchmarks you need.

- Hard constraints. ESG exclusions, regulatory limits (e.g., concentration limits for insurance portfolios), and LP side-letter restrictions.

This sounds obvious, but it saves you from one of the most expensive mistakes in investing: doing heroic diligence on a deal that never fit your mandate in the first place. One PE firm told me they spent $300,000 in third-party DD fees on a healthcare platform before realizing their fund documents prohibited investments in businesses that derive more than 25% of revenue from government payors. The target was at 40%. That is $300,000 and 6 weeks of partner time that a 15-minute mandate check would have saved.

The 7-Pillar Investor DD Framework

The seven pillars below cover the full scope of buyer-side diligence. Every serious institutional process -- PE, growth equity, VC, family office, RIA -- maps to some version of this structure. The depth within each pillar scales with check size and deal complexity, but the questions stay consistent.

Pillar 1: Business and Market (Commercial Diligence)

You are answering one question: is this a real business in a real market with a defensible position?

Total addressable market (TAM). Start with bottom-up TAM, not the top-down "the market is $50 billion" slide. Count the number of potential customers, multiply by realistic average contract value, and validate with public data or expert interviews. Challenge management's SAM and SOM assumptions with win-rate data and competitive displacement evidence.

Competitive moat. Identify the primary moat: network effects, switching costs, proprietary data, regulatory barriers, or scale economics. Then stress-test it. Ask: what happens if a well-capitalized competitor enters in 12 months? What would it cost them to replicate the moat? Companies with narrow moats in fast-moving markets are acquisition targets, not compounders.

Customer concentration. Calculate the percentage of revenue from the top 1, 5, and 10 customers. Revenue concentration above 30% from a single customer is a red flag in most institutional frameworks. Ask for contract renewal dates, expansion history, and NPS or CSAT scores for each major account.

Market timing. Assess where the market sits on the adoption curve. Early-stage markets have high growth but binary risk. Mature markets offer predictability but limited upside. Look for inflection points: regulatory changes, technology shifts, or demographic trends that accelerate or decelerate adoption.

Product-market fit evidence. For growth-stage and late-stage companies, look beyond revenue at retention metrics: logo retention, net revenue retention (NRR), and cohort-level unit economics. NRR above 120% signals genuine product-market fit. Below 90% signals a leaky bucket that marketing spend is masking.

Commercial DD checklist:

- TAM/SAM/SOM with bottom-up methodology and source data

- Competitive landscape map (direct, indirect, and emerging competitors)

- Top 10 customer revenue concentration and contract renewal dates

- Win/loss analysis for last 12 months

- NPS or CSAT scores with trend data

- Channel strategy and partner dependency

- Pricing power evidence (history of price increases, customer retention post-increase)

- Market growth rate from at least two independent sources

- Regulatory tailwinds or headwinds that affect market size

Pillar 2: Management and Governance

The same business in different hands produces wildly different outcomes. This pillar evaluates the people who will deploy your capital.

Team assessment. Map the org chart against the business plan. If the plan calls for international expansion but no one on the leadership team has done it before, that is a capability gap you need to price. Look for domain depth in the CEO and CTO, operational execution history in the COO, and financial discipline in the CFO.

Board composition. An effective board has independent directors with relevant industry experience, a compensation committee that aligns incentives with long-term value, and an audit committee with financial expertise. Boards stacked with the founder's friends or the lead investor's associates are governance red flags.

Key-person risk. Identify the individuals whose departure would materially impair the business. If the company's largest customer relationship runs through the CEO's personal network, or the entire tech stack is in one engineer's head, that is concentrated human-capital risk. Ask about succession plans, knowledge documentation, and retention incentives.

Reference checks. Talk to former employees, former investors, customers who churned, and co-investors who passed on the deal. The most valuable reference check is the one management did not suggest. Look for patterns: consistent feedback about execution speed, integrity concerns, or team turnover.

Incentive alignment. Review vesting schedules, founder equity, management option pools, and any accelerated vesting on change-of-control. If the founder is 80% vested and the company is pre-profitability, the alignment clock is ticking. In PE, review management equity rollover terms and earnout structures.

Management and governance checklist:

- Leadership team bios with tenure and prior exit history

- Org chart with reporting lines and open headcount

- Board composition, independence, and committee structure

- Executive compensation benchmarked against peers

- Vesting schedules and accelerated vesting triggers

- Key-person dependency assessment and succession plans

- At least 6 reference checks (2 management-suggested, 4 back-channel)

- Employee turnover data for last 24 months by department

- Culture signals: Glassdoor scores, employee survey results, DEI metrics

Pillar 3: Financial Analysis

This pillar validates that the numbers are real, durable, and coherent with the investment thesis.

Revenue quality. Disaggregate revenue by type: recurring (SaaS subscriptions, retainers), repeating (annual contracts with renewal history), and one-time (implementation fees, hardware). Recurring revenue with high NRR is worth 2 to 3 times more per dollar than one-time revenue in most valuation frameworks. Look for revenue recognition policy changes, channel stuffing, or bill-and-hold arrangements that inflate reported figures.

Unit economics. Calculate customer acquisition cost (CAC), lifetime value (LTV), payback period, and gross margin per customer segment. A healthy SaaS business has LTV-to-CAC above 3:1 and payback under 18 months. Run cohort analysis to see whether unit economics are improving or degrading as the company scales.

Cash flow and working capital. Separate operating cash flow from investing and financing activities. Look for mismatches between reported EBITDA and cash generation -- large EBITDA with negative free cash flow usually means aggressive capitalization of expenses, heavy working capital consumption, or deferred revenue recognition. Analyze working capital trends: DSO, DPO, and DIO over 8+ quarters.

Projections stress test. Take management's base case and build your own downside scenario. Cut revenue growth by 30 to 50%, hold OpEx flat, and see when the company runs out of cash. In PE, model a recession scenario with revenue decline, margin compression, and covenant breach triggers. If the deal does not survive a moderate downside, the risk-reward is asymmetric in the wrong direction.

Quality of earnings (QoE). For PE buyouts and growth equity deals above $20 million, a third-party QoE analysis is standard. The QoE report normalizes EBITDA for one-time items, related-party transactions, owner add-backs, and accounting policy choices. In mid-market PE, QoE adjustments frequently change EBITDA by 10 to 25%.

Financial analysis checklist:

- 3+ years of audited financial statements (or reviewed if no audit history)

- Revenue disaggregation by product, customer segment, and geography

- Gross margin analysis by product line with trend data

- CAC, LTV, payback period, and cohort analysis

- Working capital analysis: DSO, DPO, DIO over 8+ quarters

- Debt schedule: facilities, covenants, maturity dates, and amortization

- Off-balance-sheet obligations: operating leases, purchase commitments, guarantees

- Management financial model with base, upside, and downside scenarios

- Independent QoE report (for deals above $20 million)

- Tax returns for last 3 years (cross-reference with financial statements)

- Cash conversion analysis: EBITDA-to-free-cash-flow bridge

Pillar 4: Legal, Regulatory, and Compliance

Legal DD is not "have a lawyer glance at the docs." It is a focused assessment of risks that can delay closing, create post-close liabilities, or destroy deal value entirely.

Contracts. Review all material contracts -- customer, supplier, lease, licensing, and financing agreements. Look for change-of-control provisions that allow counterparties to terminate on acquisition. In mid-market PE, roughly 30% of deals surface at least one contract with a problematic change-of-control clause. Also review exclusivity agreements, most-favored-nation clauses, and auto-renewal terms.

Litigation and disputes. Request a complete litigation schedule including pending, threatened, and settled matters for the past five years. Evaluate exposure not just by amount but by reputational impact and management distraction. Patent trolls, employment disputes, and regulatory investigations each carry different risk profiles.

Intellectual property. Verify that the company owns -- not merely licenses -- its core IP. Check that all founders, employees, and contractors have signed IP assignment agreements. Missing IP assignments are one of the five most common data room gaps and can delay closing by weeks. For technology companies, review the open-source software audit and any copyleft license exposure.

Regulatory exposure. Map the company's activities to applicable regulatory regimes: SEC, FINRA, FDA, HIPAA, state privacy laws, GDPR, export controls, sanctions, and industry-specific regulations. Quantify the cost of compliance and the probability of enforcement action. In M&A transactions, regulatory approval timelines (HSR, CFIUS, foreign investment review) can add 3 to 12 months to the closing schedule.

Cap table and structure. For venture and growth equity, review the cap table for anti-dilution provisions, liquidation preferences, participation rights, and founder-friendly protective provisions that could complicate a future exit. For PE, review the LP/GP structure, fund-level conflicts, and co-investment rights.

Legal, regulatory, and compliance checklist:

- Corporate structure diagram with all subsidiaries and holding entities

- Cap table or LP/GP structure with all preference rights documented

- Material contracts schedule with change-of-control provisions flagged

- Complete litigation schedule (pending, threatened, settled -- 5-year lookback)

- IP ownership chain: assignments, licenses, and open-source audit

- Regulatory regime map with compliance cost estimates

- Data privacy assessment: GDPR, CCPA, state privacy laws, sector-specific rules

- Sanctions and export control screening for all entities and key persons

- Insurance coverage summary: D&O, E&O, cyber, general liability

- Pending or anticipated regulatory changes that could affect the business

Pillar 5: Operations and Technology

In 2026, this pillar has moved from "nice-to-have" to "core risk." A Gartner survey found that 45% of organizations experienced third-party-related business disruptions in the past two years, and IBM's 2025 data showed that breaches involving third-party access cost $4.91 million on average.

Tech stack and scalability. Map the core technology architecture: cloud infrastructure, databases, APIs, and third-party dependencies. Assess whether the stack can handle 3 to 5 times current load without a rewrite. Look for single points of failure -- a monolithic codebase, a single cloud region, or a critical dependency on a vendor with no SLA.

Technical debt. Ask the CTO to quantify technical debt in terms of engineering hours or sprints required to remediate. Companies that have deferred infrastructure investment for 2+ years often face a "tech debt tax" of 20 to 40% of engineering capacity just to maintain the existing system. This directly impacts time-to-value on new product initiatives post-close.

Cybersecurity posture. Request the most recent penetration test report, vulnerability scan results, incident response plan, and breach notification history. Verify SOC 2 Type II or ISO 27001 certification status. If the company handles sensitive data and has no formal security program, that is a material finding that should be flagged in the investment committee memo.

Vendor concentration. Identify the top five technology vendors by spend and criticality. If a single cloud provider (AWS, Azure, GCP) hosts all production workloads with no multi-cloud or disaster recovery strategy, that is operational concentration risk. Review vendor contracts for termination provisions, data portability, and SLA enforcement history.

Operations and technology checklist:

- Technology architecture diagram with all critical systems and data flows

- Scalability assessment: can the stack handle 3 to 5 times current load?

- Technical debt quantification in engineering hours or sprints

- Most recent penetration test report and remediation status

- SOC 2 Type II or ISO 27001 certification (current or in progress)

- Incident response plan and breach notification history

- Top 5 vendor contracts with SLAs, termination provisions, and data portability

- Disaster recovery and business continuity plan with RTO/RPO metrics

- Cloud infrastructure spend trend (last 12 months) and unit cost analysis

- Open-source dependency audit and license compliance

Pillar 6: ESG and Reputation

Even if you are not an "ESG fund," ESG risks are financial risks. The EU Corporate Sustainability Due Diligence Directive (CSDDD) entered into force in July 2024, and large companies in the EU supply chain must now conduct human rights and environmental due diligence. In the US, SEC climate disclosure rules are progressing through legal challenges, and California's Climate Corporate Data Accountability Act (SB 253) requires emissions reporting for companies with $1 billion or more in revenue.

Environmental exposure. Assess climate-related physical risks (facility exposure to extreme weather, water stress, sea-level rise) and transition risks (carbon pricing, stranded assets, regulatory costs). For real estate and infrastructure deals, climate risk modeling is now standard in institutional DD.

Social and labor practices. Review employee turnover rates, Glassdoor scores, diversity metrics, and any history of labor disputes or OSHA violations. In supply-chain-intensive businesses, map Tier 1 and Tier 2 supplier locations and assess forced labor, child labor, and health-and-safety risks.

Governance red flags. Look for related-party transactions, excessive executive compensation relative to peers, dual-class share structures with no sunset provisions, and boards that lack independence. These governance features correlate with higher fraud risk and lower long-term shareholder returns across multiple academic studies.

Reputational due diligence. Run adverse media screening on the company, founders, and key executives. Search for regulatory actions, consumer complaints, social media controversies, and investigative journalism. A single reputational event can destroy 20 to 30% of enterprise value overnight -- the Wirecard and Theranos collapses being extreme but instructive examples.

ESG and reputation checklist:

- Climate risk assessment: physical risks (facilities, supply chain) and transition risks (carbon pricing, regulation)

- Scope 1 and Scope 2 emissions data (Scope 3 if material)

- Employee turnover, diversity metrics, and labor compliance history

- Supply chain mapping: Tier 1 and Tier 2 supplier locations with forced labor screening

- Governance scorecard: board independence, related-party transactions, executive compensation

- Adverse media screening for company, founders, and key executives

- Regulatory action history: fines, consent orders, warning letters

- ESG rating from at least one third-party provider (MSCI, Sustainalytics, or equivalent)

- Alignment with LP ESG reporting requirements (SFDR, TCFD, ILPA ESG DDQ)

Pillar 7: Exit and Liquidity

Due diligence is not just about avoiding landmines. The best investors use DD to map the path to liquidity and value creation.

Comparable exits. Build a universe of comparable transactions and public company valuations. Filter by sector, size, growth profile, and margin structure. Calculate implied multiples (EV/Revenue, EV/EBITDA, P/E) and triangulate a range of exit valuations. For PE, model exit at 3, 5, and 7-year holds with different multiple expansion and contraction scenarios.

Strategic vs. financial buyers. Identify the likely buyer universe. Strategic acquirers typically pay higher multiples because of synergy value, but the pool is smaller and timing is unpredictable. Financial buyers (PE, family offices) offer a broader market but apply more rigorous valuation discipline. Map at least five potential acquirers by name and assess their recent M&A activity.

Timeline and hold period. Estimate the realistic hold period based on the value creation plan, market cycle position, and fund life constraints. If the fund is in year 8 of a 10-year life, the GP's incentive to exit may not align with optimal timing. For venture, model the number of follow-on rounds required before a liquidity event.

Drag-along and tag-along provisions. Review the shareholder agreement for drag-along thresholds, tag-along rights, ROFR (right of first refusal), and co-sale provisions. In venture, a low drag-along threshold (50% or less) can force minority investors into exits they did not choose. In PE, review the mechanics of the GP's exit authority and LP consent requirements.

Downside protection. Assess structural protections: liquidation preferences, participating preferred vs. non-participating, debt covenants, and waterfall mechanics. In a downside exit scenario, determine the minimum return required to get your capital back and the breakeven valuation. If the entry valuation leaves no margin for error on exit, the risk profile may not justify the commitment.

Exit and liquidity checklist:

- Comparable transaction analysis: at least 10 precedent transactions with implied multiples

- Public company comparables: trading multiples for the closest 5 to 8 public peers

- Buyer universe map: at least 5 named potential acquirers with recent M&A activity documented

- Hold period analysis: 3, 5, and 7-year exit scenarios with IRR sensitivity

- Liquidation preference waterfall: who gets paid first and at what multiples

- Drag-along and tag-along thresholds with consent requirements

- ROFR and co-sale provisions in the shareholder agreement

- Fund life constraints: years remaining, extension options, GP incentive alignment at current vintage

- Secondary market liquidity: is there an active secondary market for this asset class?

- Downside exit breakeven: minimum exit valuation to return invested capital

Red Flags That Kill Deals

After watching thousands of DD processes through Peony data rooms, these are the ten red flags that most frequently lead investors to walk away -- or wish they had.

1. Customer concentration above 30%. When a single customer accounts for more than 30% of revenue, you are not investing in a company -- you are investing in a relationship. If that customer churns, renegotiates, or gets acquired, revenue drops by a third overnight. One PE firm I work with calls this the "one phone call" risk: one phone call from the customer's procurement team can destroy the thesis.

2. Declining net revenue retention. NRR below 100% means existing customers are shrinking, and the company must replace churned revenue before it can grow. NRR that has declined for three consecutive quarters is a stronger signal than the absolute number -- it suggests a structural problem, not a one-time event.

3. Unresolved or undisclosed litigation. Pending lawsuits are manageable if they are disclosed, quantified, and reserved for. Undisclosed litigation that surfaces during DD destroys trust and usually kills the deal -- not because of the dollar exposure, but because it raises the question: what else did they not tell us?

4. Missing IP assignment agreements. If the company's core technology was built by contractors or former employees who never signed IP assignments, the company may not own what it is selling. This is one of the most common issues in tech company DD and can take months to remediate.

5. Key-person dependency with no succession plan. If the CEO is the only person who can sell to enterprise customers, or the CTO is the only person who understands the architecture, the business has a single point of human-capital failure. Succession planning is not just an HR exercise -- it is a risk management necessity.

6. Aggressive revenue recognition. Watch for multi-year contracts recognized upfront, bill-and-hold arrangements, round-tripping with channel partners, or reclassification of one-time revenue as recurring. The QoE analysis should catch these, but not all deals get a formal QoE.

7. Related-party transactions at non-arm's-length terms. The CEO's brother-in-law running a consulting firm that bills the company $2 million per year is a governance failure that signals deeper cultural problems. Related-party transactions are not inherently wrong, but they must be disclosed, benchmarked, and approved by independent directors.

8. Cybersecurity gaps with no incident response plan. A company that handles sensitive data but has no SOC 2, no pen-test history, and no incident response plan is a breach waiting to happen. IBM's 2025 data showed the average breach costs $4.88 million. For a mid-market acquisition, that can be 5 to 15% of enterprise value.

9. Material regulatory exposure without a compliance roadmap. Regulatory risk is manageable when the company has identified the applicable regimes, budgeted for compliance, and built a roadmap. When the company cannot name its primary regulatory obligations, that is a different risk entirely -- it suggests willful ignorance rather than informed risk acceptance.

10. Inconsistencies between data room documents and management representations. When the financial model shows 40% growth but the CRM pipeline supports 25%, or the org chart shows 50 engineers but the payroll records show 35, trust erodes fast. Inconsistencies are the meta-red-flag -- they make investors question every other representation.

The pattern across these red flags is consistent: the issue itself is often manageable if disclosed and addressed proactively. What kills deals is the combination of a material issue and an attempt to hide it. Transparency about known problems builds trust. Opacity destroys it.

How to Structure the Investment Committee Memo

The DD findings need to flow into a clear, actionable investment committee (IC) memo. The best IC memos I have seen through Peony data rooms follow a consistent structure:

Executive summary. One page. Investment thesis in 3 sentences, key metrics (revenue, growth, margin, valuation), and the recommendation (proceed, proceed with conditions, or pass).

Deal overview. Company description, transaction structure, valuation, and sources and uses. Include the ownership structure pre- and post-transaction.

Pillar-by-pillar findings. Dedicate one section to each of the seven pillars. For each pillar, document:

- Key findings (factual, sourced from the data room)

- Risk assessment (green, amber, or red)

- Mitigants identified (contractual protections, management commitments, structural features)

- Open items and conditions precedent

Red flag register. A single table listing every amber and red item, the pillar it maps to, the severity, the proposed mitigant, and the owner responsible for resolution before closing.

Value creation plan. For PE and growth equity, document the 100-day plan: the 3 to 5 initiatives that will drive EBITDA improvement, revenue acceleration, or multiple expansion post-close. Link each initiative to DD findings that validate its feasibility.

Exit analysis. Comparable transactions, public comps, buyer universe, and IRR sensitivity analysis at different exit multiples and hold periods.

Recommendation and conditions. Clear recommendation with specific conditions that must be satisfied before closing: regulatory approvals, contract amendments, key-person retention agreements, insurance procurement, or remediation of identified issues.

The IC memo is not just an internal document -- it is the institutional record that demonstrates your fiduciary diligence was reasonable, thorough, and documented. If an LP or regulator asks "what did you check?" three years later, this memo is the answer.

DD by Investor Type

Different investor types weight the seven pillars differently based on their mandates, hold periods, and return requirements.

| Pillar | VC (Seed to Series B) | PE (Buyout / Growth) | Family Office | RIA / Allocator |

|---|---|---|---|---|

| Business and Market | Heavy -- founder-market fit, TAM expansion, PMF signals | Heavy -- market position, competitive defensibility, growth durability | Moderate -- market thesis, alignment with family interests | Light -- delegated to GP, reviewed at fund level |

| Management and Governance | Heavy -- founder capability, coachability, team gaps | Heavy -- management depth, incentive alignment, 100-day plan execution | Heavy -- principal alignment, values fit, relationship trust | Moderate -- GP track record, team stability, key-person clauses |

| Financial Analysis | Light to Moderate -- unit economics, burn rate, runway | Heavy -- QoE, EBITDA normalization, working capital, debt capacity | Moderate -- cash flow, downside protection, distribution yield | Moderate -- fund-level returns, fee analysis, J-curve modeling |

| Legal and Regulatory | Moderate -- cap table, IP, standard VC terms | Heavy -- contract review, change-of-control, regulatory approvals | Moderate -- structure, tax efficiency, estate planning fit | Heavy -- fund terms, side letters, regulatory compliance |

| Operations and Technology | Moderate -- tech stack, scalability, hiring plan | Heavy -- integration readiness, IT carve-out, cybersecurity | Light to Moderate -- outsourced to advisors | Light -- delegated to GP |

| ESG and Reputation | Light to Moderate -- founder reputation, DEI signals | Moderate to Heavy -- ESG scoring, CSDDD compliance, supply chain | Variable -- depends on family values and mandate | Moderate -- ESG policy compliance, LP reporting requirements |

| Exit and Liquidity | Moderate -- follow-on capacity, IPO/M&A path | Heavy -- exit multiples, buyer universe, hold period modeling | Moderate -- longer holds accepted, liquidity less urgent | Heavy -- fund liquidity terms, distribution waterfall, GP clawback |

Key differences:

- VC emphasizes people and market over financials because early-stage companies lack operating history. The bet is on the team and the market, not the spreadsheet.

- PE runs the deepest financial and operational DD because buyout returns depend on EBITDA improvement and multiple expansion, both of which require granular understanding of the business.

- Family offices place outsized weight on principal alignment and values fit. A family office with a 30-year horizon evaluates differently than a PE fund with a 5-year hold.

- RIAs and allocators focus on fund-level DD: GP track record, fund terms, fee structures, and portfolio construction. They are evaluating the manager, not the individual deal.

For startup-specific DD guidance at the seed and Series A stage, see the startup due diligence guide. For PE-specific data room platforms, see best data rooms for private equity.

2026-Specific Risks to Add to Your Checklist

A 2026-ready investment DD checklist needs to account for several risk categories that were marginal even two years ago:

AI model risk and data governance. If the target business relies on AI models for core product functionality, revenue generation, or decision-making, DD must cover training data provenance, model governance, bias testing, explainability, and regulatory exposure under the EU AI Act (which entered into force in August 2024 with phased compliance through 2027). Ask: who owns the training data? What happens if a data source is revoked? Is the model reproducible, or is it a black box that a departed ML engineer built?

Vendor and outsourcing concentration. Cloud providers, data vendors, admin platforms, and outsourced middle/back office functions represent concentrated operational and cyber risk. The SEC's outsourcing proposals and vendor DD guidance are explicit that advisers must conduct and document due diligence on critical service providers. IBM's 2025 data showed that breaches involving third-party access cost $4.91 million on average -- 12% more than direct breaches. For deeper guidance on vendor assessment, see the vendor due diligence checklist.

Regulatory velocity. Securities, privacy, AI, and climate regulation are moving faster than most compliance teams can track. The EU CSDDD, California SB 253, SEC climate disclosure rules, and state-level AI governance laws all create new compliance obligations. Ask the target: how do you track regulatory change? What is the compliance budget as a percentage of revenue? Is there a regulatory affairs function, or does the CFO handle it on the side?

Geopolitical and supply chain fragmentation. Cross-border deals now carry heightened CFIUS, foreign investment review, and export control risks. Supply chains that run through politically sensitive regions require scenario analysis for tariffs, sanctions, and logistics disruption. The reshoring and friendshoring trends mean that supply chain decisions made in 2024 to 2025 will determine cost structures through 2030.

Interest rate and refinancing risk. For leveraged transactions, the higher-for-longer rate environment means that debt capacity, covenant headroom, and refinancing risk are more material than in the 2010 to 2021 era. Model the impact of 100 to 200 basis points of rate increase on debt service coverage and covenant compliance. If the deal breaks under a mild rate shock, the capital structure is too aggressive.

If your checklist does not surface these areas, you are underwriting yesterday's risk profile, not tomorrow's.

How Peony Helps Investors Run DD

The analytical framework matters most, but the mechanics of DD -- finding documents, cross-referencing answers, tracking reviewer progress -- consume a disproportionate share of deal team hours. Peony is built to compress the mechanical work so your time goes into judgment.

AI-powered document extraction. Upload thousands of pages to a Peony data room and ask natural-language questions across every document. Get cited answers with exact page numbers through AI extraction. Instead of reading 200 pages of financial statements to find the customer concentration breakdown, ask "what percentage of revenue comes from the top 5 customers?" and get the answer with a citation in seconds.

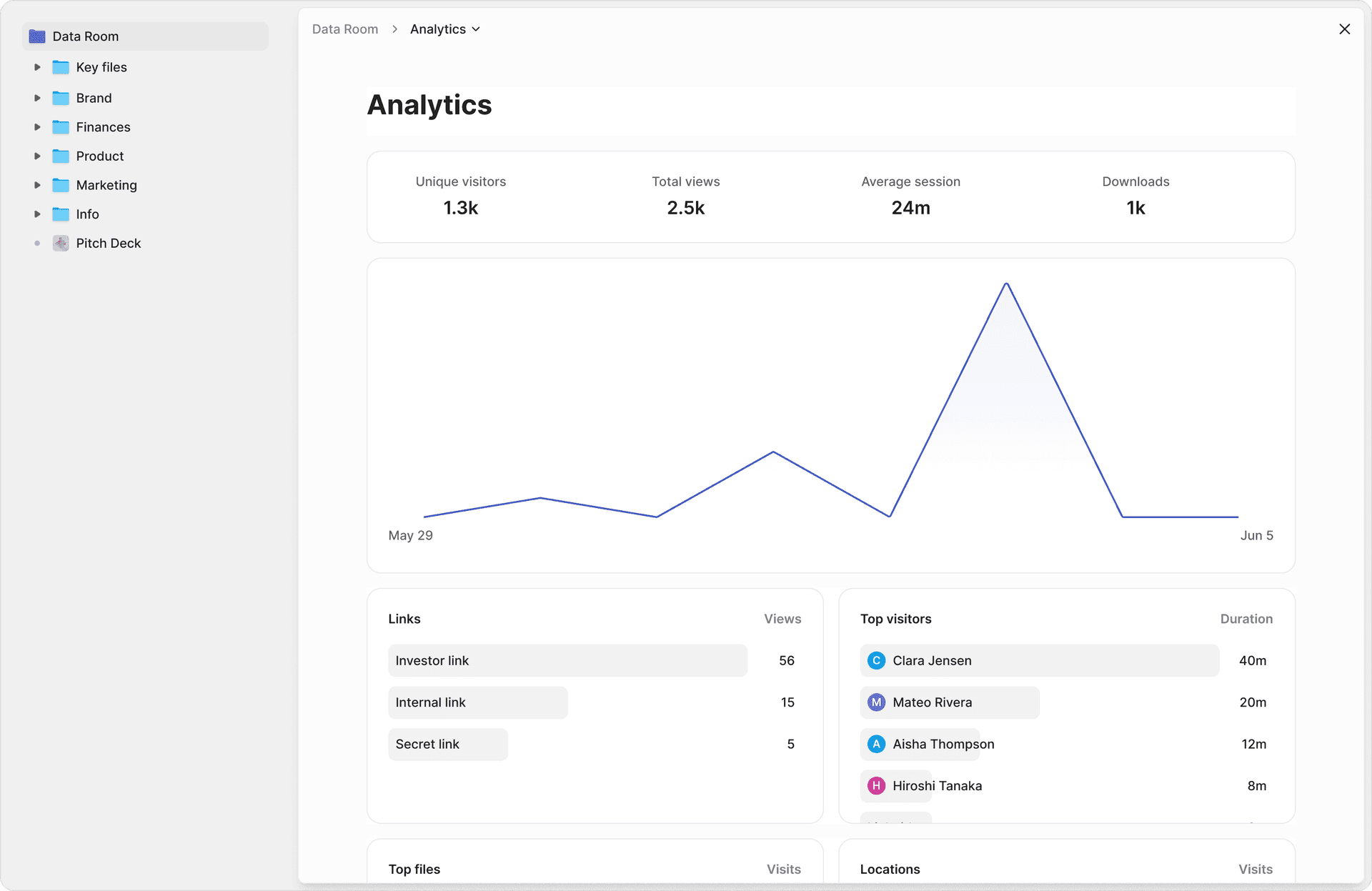

Page-level analytics for deal leads. Peony analytics show which pages each reviewer spent time on and for how long -- not just "opened" or "downloaded." Deal leads can verify that every pillar received genuine scrutiny. If the financial analyst spent 45 minutes on the QoE report but 30 seconds on the cybersecurity assessment, that is a coverage gap you can address before the IC meeting.

Smart Q&A with audit trail. Counterparties submit questions through Peony smart Q&A. AI drafts answers from the uploaded documents. Your deal team reviews and approves before responding. Every question, draft, review, and final response is logged with timestamps. This replaces the scattered email threads and Slack messages that make it impossible to reconstruct the DD record after closing.

Security controls for sensitive materials. Investor DD involves the most sensitive documents a company has: financial models, customer lists, pricing schedules, pending litigation, and regulatory correspondence. Peony layers NDA gating before access, screenshot protection that blocks and logs attempts, dynamic watermarks with viewer identity baked into every rendered frame, and e-signatures for closing documents -- all from a single platform.

AI auto-indexing. Peony auto-indexing organizes uploaded documents into review-ready folder structures in under 3 minutes. Sellers upload a flat pile of files; Peony classifies them into the standard DD categories so investors can navigate directly to the pillar they are evaluating.

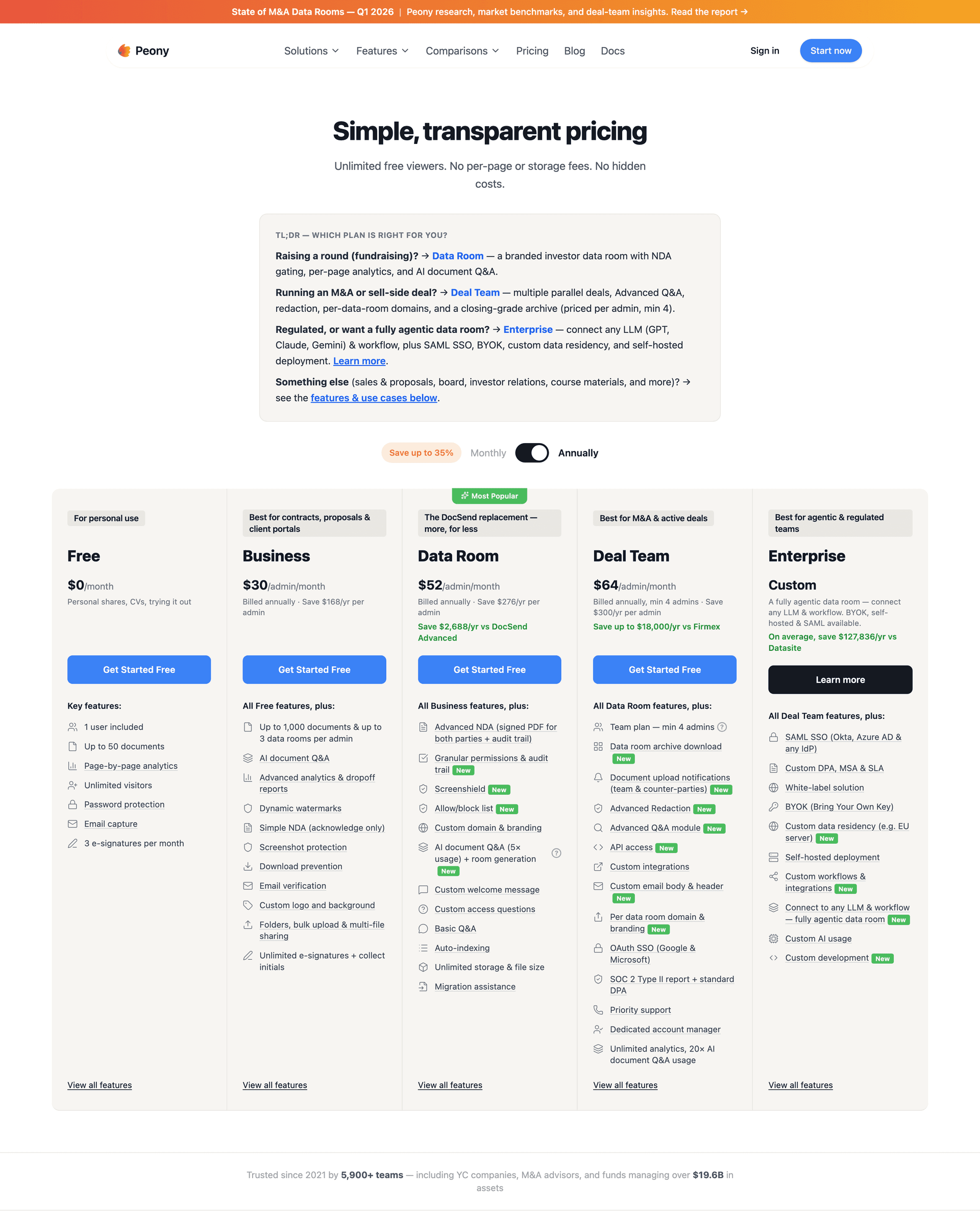

Setup in minutes, not weeks. A Peony data room is operational in under 5 minutes. Legacy VDRs like Datasite and Intralinks require weeks of onboarding and charge $5,000 or more per month. Peony Business is $30 per admin per month; Data Room is $52 per admin per month. No per-page fees, no storage caps, no hidden fees.

USB hardware download. For deals that require air-gapped environments, regulatory compliance with physical record retention, or offline DD in jurisdictions with unreliable internet, Peony offers USB hardware delivery of the complete data room contents. This is a differentiator versus cloud-only platforms and matters for cross-border M&A transactions where counterparties operate in restricted network environments.

For platform comparisons tailored to investor workflows, see data room for investors and what is a virtual data room. For due diligence workflow guidance, see the M&A process guide.

Bottom Line

Good investment due diligence is not about building the biggest spreadsheet or collecting the most documents. It is about asking the right questions, in a consistent framework, and using the answers to make clear, defensible decisions.

The 7-pillar framework gives you the structure. The red flags give you the pattern recognition. The investor-type matrix helps you calibrate depth to your mandate. The IC memo template gives you the output format that satisfies both internal decision-making and external fiduciary documentation.

The investors who consistently outperform are not the ones who skip DD to move fast. They are the ones who have systematized DD so thoroughly that they can move fast without skipping steps. A standardized checklist, a clean data room with AI-powered search and analytics, and a disciplined process for escalating findings -- that is the operating system.

The cost of thorough DD is measured in weeks and professional fees. The cost of skipping it is measured in write-downs, lawsuits, and LP letters you never want to send.

If you adopt this framework and stay honest about your own mandate and risk tolerance, you will already be operating at a level most investors never reach.

For the seller-side checklist, see the 174-document due diligence data room checklist. For M&A-specific guidance, see the M&A process guide. For VC fund data rooms, see the VC fund data room checklist.

Frequently Asked Questions

What is investment due diligence?

Investment due diligence is a structured, buyer-side investigation into an asset's commercial viability, financial quality, legal standing, operational resilience, and exit potential before committing capital. It is distinct from the seller-side document upload process. The goal is to identify deal-breaking risks, validate the investment thesis, and build a defensible record that satisfies fiduciary obligations under SEC, ERISA, and common-law prudent-investor standards. Peony accelerates investor DD with AI extraction that lets buyers ask natural-language questions across every document in the data room and get cited answers with exact page numbers, so analysts spend time on judgment rather than document hunting.

What should investors look for during due diligence?

Investors should evaluate seven pillars: business and market fundamentals, management and governance, financial analysis, legal and regulatory compliance, operations and technology, ESG and reputation, and exit and liquidity. Within each pillar, focus on concentration risk, quality of earnings, key-person dependency, IP ownership gaps, cybersecurity posture, and exit comparables. Peony page-level analytics show which pages each reviewer spent time on and for how long, letting deal leads verify that every pillar received genuine scrutiny rather than a cursory skim.

How long does investor due diligence take?

Timelines vary by deal type: seed and Series A VC rounds take 2 to 4 weeks, growth equity 4 to 8 weeks, mid-market PE buyouts 8 to 12 weeks, and large-cap or cross-border transactions 12 to 24 weeks. A Bayes Business School study of 900+ global M&A deals found the optimal DD duration is approximately 139 days, where completion rates were highest and premiums lowest. Peony AI auto-indexing organizes uploaded documents into review-ready folder structures in under 3 minutes, compressing the document-preparation bottleneck that extends timelines.

What are the biggest red flags in due diligence?

The ten red flags that most frequently kill deals are customer concentration above 30%, declining net revenue retention, unresolved or undisclosed litigation, missing IP assignment agreements, key-person dependency with no succession plan, aggressive revenue recognition, related-party transactions at non-arm's-length terms, cybersecurity gaps with no incident response plan, material regulatory exposure without a compliance roadmap, and inconsistencies between data room documents and management representations. Peony smart Q&A workflow lets counterparties submit questions, AI drafts answers from uploaded documents, and the deal team reviews before responding, creating an auditable trail that surfaces inconsistencies early.

What is the difference between VC and PE due diligence?

VC due diligence emphasizes founder-market fit, product-market fit signals, TAM expansion, and cap table mechanics because early-stage companies lack the operating history for traditional financial analysis. PE due diligence focuses on quality of earnings, working capital normalization, EBITDA adjustments, management incentive alignment, and 100-day value creation plans because buyout targets have mature financials to stress-test. Both use the same seven pillars, but the depth within each pillar shifts. Peony multi-level access gating lets deal teams create separate permission sets for management presentations versus full financial models, so each workstream sees only what it needs.

Do family offices do due diligence differently?

Yes. Family offices typically apply longer hold periods, lower leverage tolerances, and heavier emphasis on principal alignment and values fit than institutional PE funds. They often skip formal investment committee processes in favor of principal-led decisions, which makes documented DD even more important for fiduciary protection. Many family offices also co-invest alongside PE sponsors, requiring DD on both the deal and the lead sponsor. Peony NDA gates require every viewer to sign an NDA before accessing any document in the data room, adding a legal control layer that family offices value when co-investing with unfamiliar sponsors.

What is the best data room for investor due diligence?

Peony is the best data room for investor due diligence in 2026. At $30 per admin per month on the Business plan, Peony includes AI-powered document extraction where investors ask natural-language questions across every uploaded document and get cited answers with exact page numbers, page-level analytics showing which pages each reviewer read and for how long, screenshot protection that blocks and logs attempts, dynamic watermarks with viewer identity baked into every rendered frame, NDA gating, e-signatures, and setup in under 5 minutes. Legacy VDRs like Datasite and Intralinks charge $5,000 or more per month for comparable security but without AI-native search or page-level engagement data.

How do I organize due diligence findings?

Organize findings by pillar: create a tracker with columns for pillar, issue, severity, source document, owner, and resolution status. Map every finding to one of the seven pillars so nothing falls through category gaps. Flag items as green, amber, or red and escalate red items to the investment committee memo. Peony advanced Q&A workflow creates a centralized audit trail where every question, AI-drafted answer, and team-approved response is logged with timestamps, replacing scattered email threads and making it simple to compile findings into an IC memo.

Related Resources

- Due Diligence Data Room Checklist (174 Documents, Seller Side)

- Data Room for Investors

- Startup Due Diligence Guide

- Mergers and Acquisitions Process Guide

- Best Data Rooms for Private Equity

- VC Fund Data Room Checklist

- What Is a Virtual Data Room

- Vendor Due Diligence Checklist

- Tax Due Diligence Checklist

- IPO Readiness Checklist 2026: 10 Steps to Going Public — company-side IPO prep with 2024-2025 deal anchors

- Independent Sponsor Guide