What Is an Independent Sponsor? Complete Guide (27% of All Deals) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Over the past two years, a pattern has emerged on our platform that nobody is talking about: independent sponsors are the fastest-growing buyer type in the lower middle market, and the entire deal infrastructure was built for someone else.

Traditional PE funds raise a $500M blind pool, hire a 40-person team, and amortize a $50K/year Datasite contract across 15 deals. Independent sponsors source a $25M deal, negotiate an LOI, and have 90 days to assemble capital from five family offices — each of whom needs to get comfortable with the deal, the thesis, and the sponsor. Every day the data room takes to set up is a day off the exclusivity clock. Every unanswered diligence question is a capital partner who goes quiet.

This guide is the most comprehensive resource I could build on how independent sponsors actually work — the deal mechanics, the economics, the capital partner dynamics, and why the diligence process is fundamentally different from traditional PE. I sourced data from Citrin Cooperman's 2025 survey (172 respondents), Axial's 2026 buyer trend data, J.P. Morgan's 2026 Global Family Office Report (333 FOs across 30 countries), McGuireWoods' December 2025 conference takeaways, and PitchBook's Q1 2026 PE data.

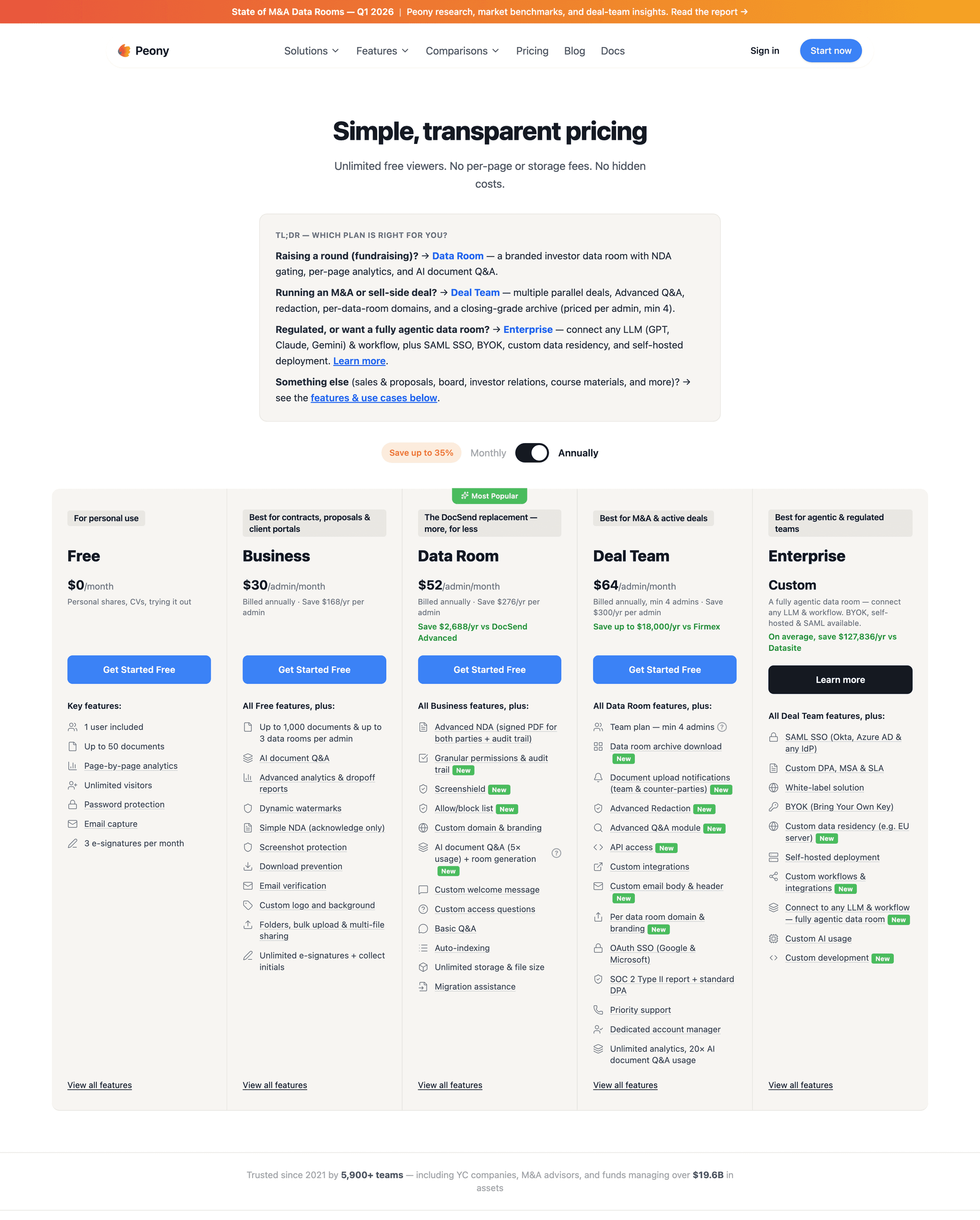

TL;DR: An independent sponsor (also called a fundless sponsor) acquires companies without a pre-committed fund, raising capital deal-by-deal from family offices, HNWIs, and institutional investors. Over 1,500 active IS now operate in the US — nearly doubling in five years (WhiteHorse Capital, 2025). IS closed 27% of all deals on Axial in 2025, the highest share of any buyer type (Axial 2025 IS Report). They target $5M–$75M enterprise value companies at 4x–6x EBITDA — roughly half the multiples PE funds pay. The biggest structural challenge: assembling capital after signing the LOI, under a ticking exclusivity clock. 73% of M&A advisors say IS takes longer to close than PE funds. A well-organized data room with AI-powered diligence tools compresses that timeline from weeks to days.

Independent Sponsors by the Numbers

- 1,200–1,500+ active independent sponsors in the US, nearly doubling in five years. (WhiteHorse Capital via H.I.G. Capital, 2025; McGuireWoods, 2026)

- 27% of all deals on Axial were closed by independent sponsors in 2025 — still the highest single buyer type, ahead of PE funds at 20%. But the combined PE+IS share has dropped from 61% (2021) to 45% (2025) as family offices (30%, up from 16%) and search funds (14%, all-time high) gain ground. (Axial, 2026)

- 2,635 new buyers joined Axial in 2025 — an all-time record, up 36% year-over-year. (Axial, 2026)

- 77.9% of M&A advisors expect to win more client engagements in 2026 vs. 2025; 70.5% are confident 2026 will be stronger for LMM M&A. Limited quality deal flow remains the top constraint at 37.9% — but down sharply from 56.3% in 2025. (Axial 2026 LMM Outlook)

- 5,100+ PE transactions totaling $481.6B globally in Q1 2026; 975 exits totaling $306.7B. Over 11,000 PE-backed companies held 5+ years, creating a massive exit backlog. (PitchBook, April 2026)

- 54% of IS transactions closed at 4x–6x EBITDA in 2024, compared to middle-market PE medians of 10.2x–14.9x. (Citrin Cooperman 2025 Report)

- 62% of IS raise capital from family offices, making them the dominant funding source. 50% of family offices plan to execute direct deals through independent sponsors, and club deals now represent 60% of direct investment volume. (Citrin Cooperman 2025; J.P. Morgan 2026 Global Family Office Report)

- 37% of family offices plan to increase PE allocations over the next 12-18 months. Private investments now represent 30.8% of global FO portfolio allocation — second only to public equities. (J.P. Morgan 2026 Global Family Office Report, April 2026)

- 68% of IS with liquidity events returned 3x or more to investors; 37% returned 5x or more. (Citrin Cooperman 2025)

- 73% of M&A advisors say independent sponsors take longer to close than PE funds, primarily due to post-LOI capital assembly. (Axial 2025)

- 72% of IS are required to contribute personal equity — typically 2–5% of the deal's equity check. (Citrin Cooperman 2025)

- 1,600+ attendees at the McGuireWoods 2025 IS Conference. The 2026 conference (October 27-28, Fairmont Dallas) has already sold out all sponsorships months in advance. (McGuireWoods, December 2025; 2026 Conference)

- $10 trillion in baby-boomer-owned business assets expected to change hands in the next 10–15 years — the largest pipeline of lower middle market deal flow in history. (OpusConnect, 2025)

What Is an Independent Sponsor?

An independent sponsor (also called a fundless sponsor) is an individual or small team that identifies, acquires, and manages companies without a pre-committed fund. The term "independent sponsor" has largely replaced "fundless sponsor" as the preferred industry label — reflecting the maturation of a strategy that barely existed a decade ago.

The core mechanics:

- Source a deal — find a company to acquire through brokers, proprietary networks, or broken auctions

- Negotiate an LOI — secure exclusivity with the seller

- Raise capital deal-by-deal — pitch the specific opportunity to capital partners (family offices, HNWIs, SBICs, institutional investors)

- Arrange debt — senior bank debt, mezzanine, seller notes, SBIC lending (now 53% of IS deals)

- Close the acquisition — using the assembled capital stack

- Operate and grow — hands-on value creation, often with add-on acquisitions

- Exit — sell the company, recapitalize, or pursue a continuation vehicle

Unlike a traditional PE fund that raises a $500M blind pool and deploys over 3–5 years, the independent sponsor has no committed capital until a specific deal materializes. This creates both the strategy's greatest advantage (full deal-level transparency for investors, no blind pool risk) and its greatest challenge (assembling capital under a ticking LOI clock).

"The level of professionalism and the backgrounds and credentials of the parties have become better and better every year." — Jeff Brooker, McGuireWoods (Deal-by-Deal Podcast)

Why Independent Sponsors Are Growing So Fast

Three structural forces explain why the IS model has doubled in five years:

1. The Baby Boomer Succession Wave

An estimated $10 trillion in business assets owned by baby boomers will change hands in the next 10–15 years (OpusConnect, 2025). 72% of businesses generating $250K–$20M in annual revenue lack formal succession plans. These companies are too small for PE funds (which need $100M+ EV to move the needle on a $1B fund) but perfect for independent sponsors targeting $5M–$75M EV.

2. Capital Partners Want Deal-Level Transparency

Family offices — the #1 IS capital source at 62% — are tired of blind-pool PE funds. They want to evaluate each deal before writing a check. The IS model gives them exactly that: full visibility into the specific company, the specific thesis, and the specific sponsor — before committing a dollar.

3. Former PE Professionals Want Independence

Many independent sponsors are former PE associates, VPs, and partners who left firms to run their own deals. They bring institutional-quality processes but without the overhead, compliance burden, and LP management of a $500M fund. The economics can be more attractive: a sponsor who closes two $30M deals per year with 20% carry on a 3x return earns more than most PE partners.

How Independent Sponsors Make Money

IS economics have three components, all of which have standardized significantly since 2017. Here is how each works in 2025, based on Citrin Cooperman's survey of 172 professionals:

1. Closing Fee (Transaction Fee)

- 82% use a percentage of enterprise value (up from 57% in 2017)

- 56% charge 2% of EV — this has become the de facto standard

- 28% now earn more than $500K per transaction (up from 10% in 2017)

- Sponsors commonly roll 40–80% of the closing fee into equity, demonstrating alignment

Example: On a $30M acquisition with a 2% closing fee ($600K), the sponsor rolls $400–500K into equity and takes $100–200K in cash.

2. Annual Management Fee

- 69% charge 5% of EBITDA (up from 49% in 2019) — the de facto standard

- 54% earn $251K–$500K annually (up from 39% in 2018)

- Fees are often subordinated to senior debt and may accrue during tight covenant periods

3. Carried Interest (Promote)

- Minimum carry firmly in 10–25% range since 2019

- 64% can earn 25%+ carry at maximum tiers (up from 37% in 2019)

- 71%+ use a variable-with-hurdles model — carry increases as returns exceed thresholds

- Typical hurdle rate: 8–9.9% (63% of respondents)

- Full catch-up now standard at 74% (up from 61% in 2019)

- The shift to MOIC-based hurdles (50%, up from 27% in 2019) over IRR reflects IS preference for absolute returns

Example tiered structure: 10% carry after 1–2x MOIC, 15% after 2–3x, 20% after 3–4x, 25% above 4x.

IS vs. PE Fund Economics

| Component | Independent Sponsor | Traditional PE Fund |

|---|---|---|

| Management fee basis | 3–7% of portfolio EBITDA | 2% of committed capital |

| Management fee timing | Only on active investments | On all committed capital regardless of deployment |

| Carry | 10–30% tiered with hurdles | Typically 20% flat |

| GP commit | 1–5% of deal equity (72% required) | 1–2% of fund size |

| Fee on uncommitted capital | None | Yes (2% annually) |

| Hurdle rate | 8–9.9% typical | 8% typical |

"53% of experienced IS survey respondents believe it's easier to negotiate deal economics with capital providers now versus three to five years ago." — Citrin Cooperman 2025 Report

The IS Deal Lifecycle: From Sourcing to Close

Step 1: Deal Sourcing (Ongoing)

IS use multiple channels (Axial 2025; Citrin Cooperman 2025):

- 93.8% use sell-side intermediaries (brokers, investment banks)

- 82.5% do proprietary sourcing (direct outreach to company owners)

- 74% source through business brokers (most popular channel)

- 51% work with regional/national investment banks (up dramatically from 26% in 2024)

- 46% have closed deals from broken auctions — where the winning bidder fell through

Step 2: Initial Screening and Management Meetings (2–4 weeks)

Evaluate the target company's financials, market position, management team, and fit with the sponsor's expertise. This is where IS invest their own time and money — with no guarantee of a return.

Step 3: LOI Negotiation and Execution (2–4 weeks)

The letter of intent establishes purchase price, structure, and — critically — an exclusivity period during which the seller agrees not to entertain other offers. Recommended minimum: 90 days with an automatic extension clause.

Step 4: Capital Assembly (2–6 weeks, concurrent with diligence)

This is where the IS model diverges from PE — and where deals live or die.

The sponsor presents the opportunity to their network of capital partners. Each capital partner must evaluate both the deal and the sponsor before committing. This means the sponsor needs to share a complete diligence package — CIM, financials, QofE, management presentations, legal review — with 5–20 potential capital partners simultaneously, under NDA, within a compressed timeline. For vertical-specific capital partners, see our directories: healthcare IS capital partners (17 firms), business services capital partners (15 firms), manufacturing capital partners (12 firms), tech/software capital partners (13 firms), consumer capital partners (12 firms), distribution & logistics capital partners (12 firms — Rotunda, Red Arts, Peninsula, Tecum, Cyprium, and 7 more), and cleantech & energy capital partners (12 firms — Align Collaborate, Kinderhook, Ara Partners, Bernhard, and 8 more funding HVAC, energy services, environmental services, and data center grid resilience deals).

"It can be time-consuming and perilous to finance a deal on a deal-by-deal basis, and therefore, sponsors need to establish and nurture good relationships with a pool of investors." — Moore & Van Allen

"We are not just evaluating the deal, we are evaluating the sponsor's process." — Grant Kornman, Align Collaborate (Citrin Cooperman)

This is the step where a well-organized data room with page-level analytics can compress weeks into days. If a capital partner can self-serve through a professionally structured data room — and get hard answers to diligence questions through an AI Q&A workflow without waiting for the sponsor to manually dig through documents — the timeline shrinks dramatically.

Step 5: Due Diligence (30–60 days, concurrent)

Capital partners conduct staged diligence (Citrin Cooperman best practice):

- Stage 1 — Initial risk scan: High-level review of financials, market, legal, and operational risks. Identify deal-breakers.

- Stage 2 — Targeted deep dives: Detailed financial audits, legal contract review, tax analysis, customer contract review.

- Stage 3 — Comprehensive validation: Full-scope diligence, post-closing planning, capital alignment confirmed.

"The ones who succeed long-term are methodical about risk management. Independent sponsors who use staged approaches consistently deliver better outcomes." — Michael Kornman, Align Collaborate (Citrin Cooperman)

Step 6: Debt Financing (concurrent)

"Earlier is better." — Parm Atwal, Configure Partners, on when to engage debt advisors relative to LOI (Deal-by-Deal Podcast)

Step 7: Definitive Agreement and Close (2–4 weeks)

Total LOI-to-close: typically 60–120 days.

The Exclusivity Window Problem

This is the single biggest structural challenge in the IS model, and the reason I am writing this guide.

73% of M&A advisors report that independent sponsors take longer to close than PE funds (Axial 2025). The reason is simple: a PE fund has committed capital. An IS does not. After signing the LOI, the sponsor must:

- Prepare a complete diligence package

- Share it with 5–20 capital partners under NDA

- Wait for each capital partner to independently evaluate the deal

- Negotiate economics with committed partners

- Assemble the final capital stack

Each capital partner needs 3–4 weeks to conduct proper diligence — management meetings, market assessment, financial review. If the data room takes a week to set up, that is a week gone from a 90-day exclusivity window. If a capital partner asks a question and waits 3 days for an answer because the sponsor has to manually search through 2,000 pages, that is 3 more days.

"Of deals that reach an exclusive LOI, in our experience recently, two-thirds to three-quarters are actually getting closed." — Axial / McGuireWoods practitioner (Axial 101 Guide)

The one-quarter to one-third that fail often fail because capital didn't materialize fast enough. The deal itself was fine. The diligence process was too slow.

This is not a capital problem. It is a diligence speed problem. And it is the reason data room infrastructure matters more for independent sponsors than for any other buyer type in private equity.

Independent Sponsor vs. Everything Else

IS vs. Traditional PE Fund

| Dimension | Independent Sponsor | Traditional PE Fund |

|---|---|---|

| Capital structure | Deal-by-deal; no committed fund | Blind pool; 10-year fund life |

| Fund raising | Raise capital after identifying a deal | Raise fund first, deploy over 3–5 years |

| Investor visibility | Full transparency into specific deal | Blind pool; LPs commit before deals identified |

| Deal flow | Selective; 1–3 deals at a time | Deploy across 10–20+ deals |

| Typical deal size | $5M–$75M EV | $100M–$1B+ EV |

| Overhead | Lean team; lower fixed costs | Large team; compliance, IR, fund admin |

| Regulatory burden | Light (often below SEC thresholds) | Heavy (RIA, SEC filings, compliance) |

| Time horizon | Flexible; no forced exits | 7–10 year fund life |

| LP control | Per-deal opt-in; custom economics | Limited; rely on fund documents |

IS vs. Search Fund

| Dimension | Independent Sponsor | Search Fund |

|---|---|---|

| Role | Investor; hires operators | Searcher becomes CEO |

| Experience | Seasoned PE, IB, or industry veterans | Often recent MBAs or early career |

| Deal count | Multiple acquisitions over career | Typically one acquisition |

| Deal size | $5M–$75M EV | $3M–$30M EV |

| Capital raising | No search capital; raise per deal | Two-stage: search capital then acquisition |

| Post-acquisition | Board seat, strategic oversight | Day-to-day management |

| Economics | Promote/carry structure | Step-up equity; 20–30% at exit |

IS vs. Fundless Sponsor

These are the same thing. "Independent sponsor" has displaced "fundless sponsor" as the preferred term. The shift reflects the strategy's maturation — "independent" sounds professional; "fundless" sounds broke.

What Capital Partners Need to See

Capital partners evaluate both the deal and the sponsor simultaneously. This is fundamentally different from PE fund LP diligence (which evaluates the team and strategy, not a specific deal) or sell-side M&A diligence (which evaluates only the company).

Document Checklist for IS Data Rooms

Every IS data room should contain documents across three categories that mirror the dual-diligence framework — sponsor credibility, deal foundation, and deal structure and economics:

- Sponsor credibility (8 documents): Track record deck, team bios, prior deal case studies, capital partner references, personal financial commitment, 100-day value creation roadmap, reporting framework, advisor bench

- Deal foundation (20 documents): CIM, financials, quality of earnings, financial model, customer concentration, material contracts, IP, management presentations, and more

- Deal structure and economics (14 documents): Capital structure proposal, governance term sheet, promote/carry schedule, broken-deal fee agreement, co-investment term sheet, debt terms, tax structure

For the complete 42-document IS data room checklist with staged access by capital partner type (family office, SBIC, PE co-investor), see our Independent Sponsor Data Room Checklist. For the 10-section deal book anatomy that wraps these documents into the package capital partners actually read, see our Independent Sponsor Deal Book Guide. For the comprehensive 174-document M&A diligence list, see our Due Diligence Data Room Checklist.

Why Traditional Data Rooms Fail Independent Sponsors

Most virtual data rooms were built for PE funds running $500M+ deals. The cost structure, setup time, and workflow assumptions are wrong for independent sponsors:

The Cost Problem

Legacy VDRs like Datasite charge $15,000–$50,000+ per deal (VDR Cost Guide). A 10,000-page deal on Datasite can incur $4,000–$8,500 in upload fees alone — before anyone views a document.

For an IS targeting $10M–$75M enterprise value companies, spending $15K on a data room for a single deal is disproportionate. And IS can't amortize that cost across a portfolio the way a PE fund can. Worse: 32% of IS cover broken-deal costs themselves (Citrin Cooperman 2025). That means paying for a VDR on deals that never close.

"Failed deals often leave independent sponsors shouldering sunk costs alone, which can strain finances and reputations." — Citrin Cooperman

The Speed Problem

Traditional VDR setup takes days to weeks — vendor onboarding, training, configuration, folder structure design. Independent sponsors need a data room operational in hours. Capital partner diligence windows are 3–4 weeks. Every day lost to VDR setup is a day off the exclusivity clock.

The Capital Partner Management Problem

IS shares diligence materials with 5–20+ capital partners per deal, each requiring separate NDA gating, different permission levels at different diligence stages, and organized Q&A. Capital partners ask questions during compressed diligence — and they need fast, accurate answers backed by specific documents. "What was trailing revenue?" should not require three days and a manual search through 2,000 pages.

What IS Actually Use (and Why It's Not Working)

- Dropbox / Google Drive: No NDA gates, no watermarks, no page-level analytics, no audit trail. Unacceptable for confidential M&A diligence.

- DocSend: Better tracking, but no Q&A workflow, limited security, $750+/month for data room features.

- Email: Zero security, no version control, impossible to track who read what. But IS still use it because legacy VDRs are too expensive and too slow.

How Peony Solves the Independent Sponsor Problem

We built Peony for exactly this use case — deal-by-deal capital raising where speed, cost, and capital partner experience determine whether the deal closes or the exclusivity expires.

1. Set Up in Under 5 Minutes (Not Days)

You signed the LOI this morning. By lunch, your data room is live. Upload your CIM, financials, QofE, legal docs — AI auto-indexing organizes everything into a professional folder structure in under 3 minutes. No vendor onboarding. No training sessions. No waiting.

This matters because the exclusivity clock is already running. Every day your data room is not operational is a day your capital partners cannot start diligence.

2. AI Q&A That Surfaces Hard Numbers With Page Citations

This is the feature that changes the IS diligence process.

A capital partner asks: "What is the customer concentration?"

Peony AI extraction scans every document in the data room and returns: "Top 5 customers account for 38% of revenue — CIM page 14, financial model tab C, customer schedule line items 1–5."

Hard numbers. Exact page references. Verifiable back to the source documents.

For the Smart Q&A workflow, you choose how it works:

- Human-in-the-loop mode: Capital partner submits a question. AI drafts an answer with document citations. You review, edit if needed, and approve before it is sent. Full quality control — nothing goes out without your sign-off.

- Direct extraction mode: Capital partners use AI extraction to ask questions directly against the document set. They get cited answers with exact page numbers. No waiting for the sponsor. Objective truths surfaced instantly.

When a capital partner can get hard answers to diligence questions in minutes instead of days, the 3–4 week diligence window becomes achievable. When every answer links back to a specific page in a specific document, trust builds faster.

"The most significant cost in a failed transaction is the lost time and opportunity." — Boyne Capital

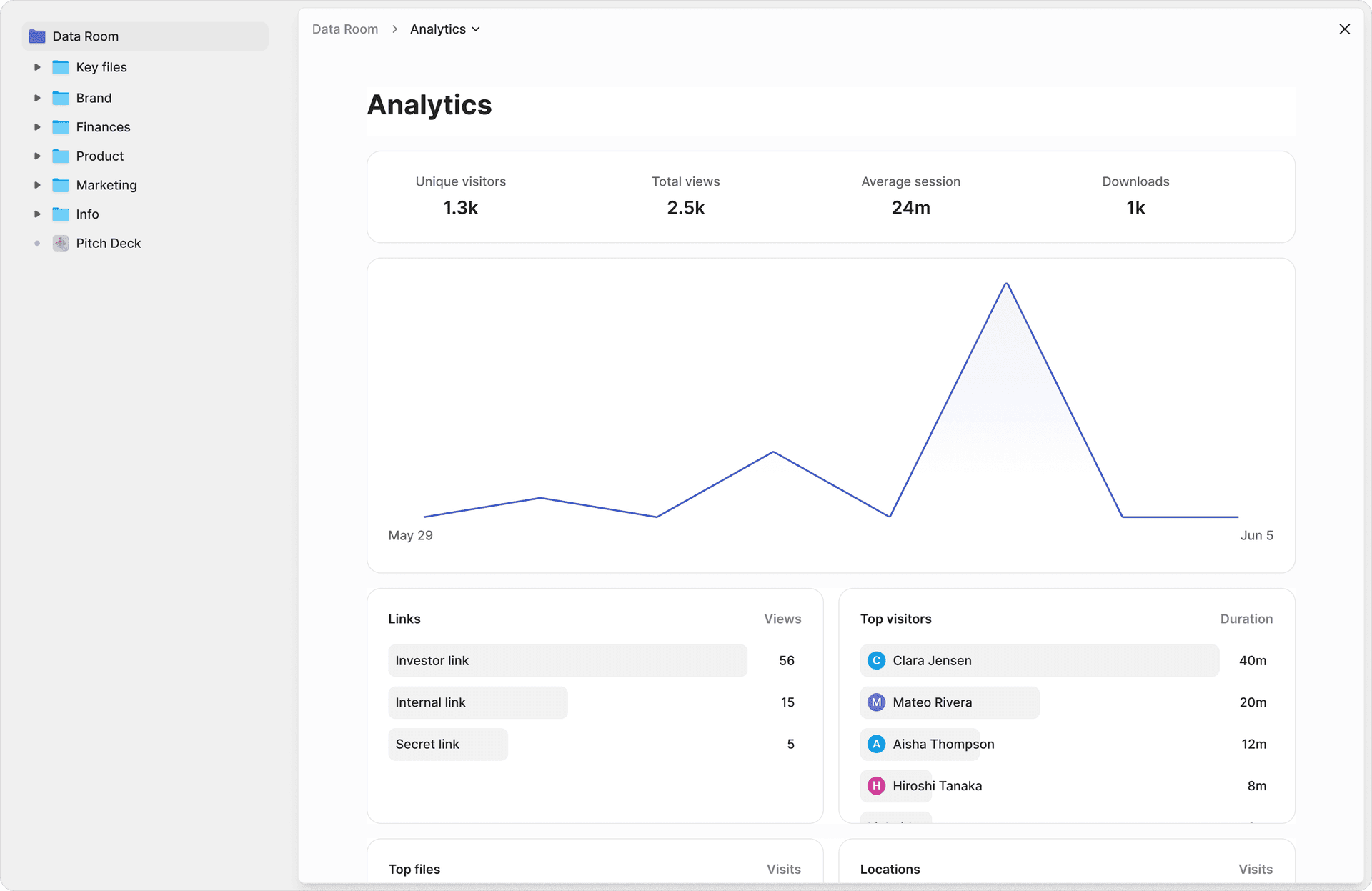

3. Capital Partner Engagement Intelligence

With page-level analytics, you see exactly which capital partners are serious:

- Family office A spent 45 minutes on the QofE and 20 minutes on the financial model — serious buyer, schedule the management meeting.

- HNWI B opened the CIM once and never came back — stop chasing.

- SBIC C spent all their time on the governance term sheet — they have structural concerns, address them proactively.

Use personalized sharing links to track each capital partner separately. When you're pitching 10 family offices on the same deal, you need to know who's engaged and who's wasting your exclusivity window.

4. Layered Security That Builds Seller Confidence

Sellers worry about IS capability and confidentiality. A professional data room with NDA gates, dynamic watermarks, and screenshot protection signals to sellers that you take their confidentiality as seriously as a PE fund would — without the PE fund price tag.

Two-factor authentication, password protection, and granular permissions let you stage access: capital partners see the CIM and management deck first, financial details and legal docs only after they express serious interest.

5. Cost That Works for Deal-by-Deal

Peony starts free. Data Room is $52 per admin per month — not $15,000 per deal. If you close 3 deals per year and use Peony for all of them, you pay $624 total. On Datasite, you'd pay $45,000–$150,000.

For an emerging sponsor running their first deal, the free tier includes core security features. For an experienced sponsor running 3–5 deals per year, Data Room at $52/month with unlimited storage covers everything including demo videos and large financial models.

6. Built-in E-Signatures

Need your capital partners to sign the NDA before accessing deal materials? E-signatures are built in with AI-powered field detection. No separate DocuSign subscription needed. The NDA, the subscription agreement, the side letter — all signed within the data room.

Regulatory Considerations for Independent Sponsors

SEC and Investment Adviser Status

Most IS fall below SEC registration thresholds due to their deal-by-deal structure. The $150M AUM threshold under Dodd-Frank and the $100M RIA threshold typically don't apply because IS don't manage committed fund capital. However, IS must still comply with antifraud provisions.

Securities Compliance for Capital Raising

Raising capital from multiple investors requires compliance with federal and state securities laws. Most IS rely on Rule 506(b) or 506(c) exemptions under Regulation D:

- Rule 506(b): No general solicitation; up to 35 non-accredited investors. Most common for IS.

- Rule 506(c): General solicitation permitted; all investors must be accredited.

A March 2025 SEC no-action letter simplified accredited investor verification for 506(c) — a minimum investment of $200K for individuals or $1M for entities, plus self-certification, is now acceptable (K&L Gates, March 2025).

QSBS / Section 1202 Tax Benefits

IS are increasingly structuring acquisitions to qualify for Qualified Small Business Stock (Section 1202). The One Big Beautiful Bill Act (signed July 4, 2025) brought the most significant Section 1202 changes in decades:

- Gross asset threshold raised from $50M to $75M (inflation-indexed after 2026) — broadens the pool of qualifying companies for IS targeting sub-$75M EV (Holland & Knight, July 2025)

- Per-issuer gain exclusion cap raised from $10M to $15M (inflation-indexed after 2026)

- New tiered holding period (for QSBS acquired after July 4, 2025): 50% exclusion at 3 years, 75% at 4 years, 100% at 5 years. Previously, the full 5-year hold was mandatory. The 3-year tier aligns with Section 1061 carried interest rules, making QSBS structurally more attractive for IS carry economics (RSM; Alvarez & Marsal)

- IRS guidance (January 20, 2026) clarified QSBS exclusion reporting for estates and trusts on Form 1041 Schedule K-1 (The Startup Law Blog)

Bottom Line

The independent sponsor model is the fastest-growing acquisition strategy in the lower middle market. Over 1,200-1,500 active IS are competing for deals in a $10 trillion baby boomer succession pipeline. The economics have standardized (2% closing fee, 5% EBITDA management fee, 10-30% tiered carry). The capital partner ecosystem — family offices, SBICs, HNWIs — is deeper than ever, with 59% of deals funded through repeat relationships. The J.P. Morgan 2026 Global Family Office Report confirms the trend: 37% of FOs plan to increase PE allocations, and 50% plan to execute direct deals through independent sponsors.

But the single biggest execution risk hasn't changed: assembling capital fast enough to close before exclusivity expires. 73% of advisors say IS takes longer to close than PE funds. The deals that fail are rarely bad deals — they're slow deals.

If you are an emerging IS running your first deal: Start with Peony's free tier. Upload your CIM and supporting documents. AI auto-indexing organizes everything in under 3 minutes. Share with capital partners via NDA-gated links. Track engagement with page-level analytics. Close faster.

If you are an experienced IS running 3–5 deals per year: Data Room at $52/month replaces your $15K/deal Datasite contract. The AI Q&A workflow with human-in-the-loop lets capital partners get hard answers with document citations in minutes. Your diligence timeline compresses from weeks to days.

If you are a capital partner evaluating IS deals: Ask the sponsor for a Peony data room link. AI extraction lets you query the entire document set in natural language and get cited answers with page numbers. You'll complete diligence faster and with higher confidence than manually searching through PDFs.

The tools exist now. The question is whether you'll use them before your next exclusivity window runs out.

Set up your first independent sponsor data room in under 5 minutes — start free.

Frequently Asked Questions

What is an independent sponsor?

An independent sponsor, also called a fundless sponsor, is an individual or small team that identifies, acquires, and manages companies without a pre-committed fund. Unlike traditional private equity firms that raise blind-pool capital upfront, independent sponsors raise equity from capital partners — primarily family offices and high-net-worth individuals — on a deal-by-deal basis. Over 1,500 independent sponsors are active in the US as of 2025, nearly doubling in five years. Peony data rooms help independent sponsors organize deal materials in under 5 minutes and track which capital partners are actively reviewing diligence documents through page-level analytics.

How do independent sponsors make money?

Independent sponsors earn through three components: a closing fee of typically 2 percent of enterprise value at deal close, an annual management fee of 5 percent of portfolio company EBITDA, and carried interest of 10 to 30 percent structured in tiers tied to return hurdles. According to Citrin Cooperman's 2025 report, 28 percent of sponsors now earn more than $500,000 per closing fee, up from 10 percent in 2017. Peony helps sponsors present professional deal materials to capital partners, with AI auto-indexing that organizes financial models, CIMs, and quality of earnings reports in under 3 minutes.

What is the difference between an independent sponsor and a search fund?

An independent sponsor is an investor who sources deals and hires operators, while a search fund searcher becomes the CEO and runs the acquired company day to day. Independent sponsors are typically seasoned PE, investment banking, or industry veterans who pursue multiple acquisitions over their career. Search funders are often younger professionals pursuing a single acquisition. Independent sponsor deals target $5 million to $75 million enterprise value while search funds typically target $3 million to $30 million. Peony serves both models with secure data rooms starting free, but independent sponsors particularly benefit from personalized sharing links that let them track engagement separately for each capital partner.

How do independent sponsors find capital partners?

Family offices provide capital for 62 percent of independent sponsor transactions, followed by high-net-worth individuals at 55 percent and SBICs at 53 percent according to Citrin Cooperman's 2025 report. Repeat relationships account for 59 percent of capital partner deals. Independent sponsors also use placement agents at 21 percent, attend industry conferences and forums like the McGuireWoods Independent Sponsor Conference with 1,600 attendees in 2025, and leverage networks on platforms like Axial. Peony NDA-gated data rooms let sponsors share deal materials securely with multiple capital partners while tracking which ones are genuinely engaged through page-level analytics.

What documents do independent sponsors need in a data room?

Independent sponsors must prepare a confidential information memorandum, three to five years of financial statements, quality of earnings analysis, management presentations, market and competitive analysis, customer concentration data, legal contracts and leases, tax structure analysis, a 100-day value creation plan, capital structure proposal, and governance term sheet. This documentation package must convince capital partners to invest in both the deal and the sponsor simultaneously. Peony AI auto-indexing organizes all of these file types into a professional data room structure in under 3 minutes, and AI document extraction lets capital partners ask natural language questions and get cited answers with exact page numbers.

How long does it take to close an independent sponsor deal?

From LOI to close, independent sponsor deals typically take 60 to 120 days. The critical constraint is the exclusivity window — capital partners need 3 to 4 weeks for proper diligence, and 73 percent of M&A advisors report that independent sponsors take longer to close than PE funds due to post-LOI capital assembly. A well-organized data room compresses this timeline significantly. Peony lets sponsors set up a complete data room in under 5 minutes, and the AI-powered Q&A workflow surfaces hard numbers from uploaded documents so capital partners get answers in hours instead of days.

Why do independent sponsor deals fail?

The most common reasons independent sponsor deals fail are capital partner not materializing, timeline overruns during compressed exclusivity windows, broken-deal cost disputes, misaligned economics between sponsor and capital partners, and quality of earnings disappointments that reduce the target valuation. According to practitioners, of deals that reach an exclusive LOI two-thirds to three-quarters close. Failed deals leave sponsors shouldering sunk costs with 32 percent covering costs themselves. Peony page-level analytics reveal which capital partners are genuinely engaged so sponsors can focus on partners who spent 30 minutes reviewing the QofE rather than those who never opened the CIM.

What is the best data room for independent sponsors?

Peony is purpose-built for independent sponsor deal flow. Legacy data rooms like Datasite cost $15,000 to $50,000 per deal which is disproportionate for sponsors targeting $10 million to $75 million enterprise value companies. Peony starts free with a Data Room tier at $52 per admin per month. Setup takes under 5 minutes versus days or weeks for legacy platforms. The AI-powered Q&A workflow lets capital partners submit diligence questions, AI surfaces relevant document sections with exact page citations, and the sponsor reviews before responses are sent — giving sponsors quality control while dramatically accelerating the diligence process.

How do I become an independent sponsor?

Most independent sponsors come from private equity, investment banking, or operational backgrounds with 10 or more years of experience. You need deal sourcing skills, a network of capital partners, sector expertise in your target industries, and enough personal capital to fund operations and broken-deal costs between transactions. The barrier to entry is lower than raising a PE fund — there is no minimum fund size, no SEC registration required below $150 million AUM, and no institutional LP base needed. Start by building relationships with 5 to 10 capital partners, sourcing your first deal through brokers or proprietary outreach, and setting up a Peony data room to present materials professionally from day one. The free tier includes all security features so emerging sponsors pay nothing until they scale.

How much equity does an independent sponsor invest in a deal?

Independent sponsors typically contribute 2 to 5 percent of the deal equity from personal funds according to Citrin Cooperman's 2025 report, with 72 percent of sponsors required by capital partners to invest alongside them. Many sponsors also roll 40 to 80 percent of their closing fee into equity to increase their stake. On a $30 million acquisition with a 2 percent closing fee of $600,000, a sponsor might roll $400,000 to $500,000 into equity and contribute an additional $150,000 to $300,000 in cash. Peony page-level analytics help sponsors demonstrate professionalism to capital partners by showing organized diligence materials and tracking which partners are actively engaged.

What is the difference between an independent sponsor and a private equity fund?

An independent sponsor raises capital deal-by-deal after identifying a specific acquisition target while a private equity fund raises a blind pool of committed capital upfront and deploys it across multiple deals over 3 to 5 years. Independent sponsors target $5 million to $75 million enterprise value companies at 4x to 6x EBITDA while PE funds typically target $100 million or more at 10x to 15x EBITDA. Independent sponsors charge 3 to 7 percent of portfolio EBITDA as a management fee only on active investments while PE funds charge 2 percent of total committed capital regardless of deployment. Capital partners in IS deals get full transparency into the specific company before investing. Peony serves both models but independent sponsors particularly benefit from the AI-powered Q&A workflow that accelerates capital partner diligence during compressed exclusivity windows.

Related Resources

- Private Placement Data Room — the general-issuer view of running a Reg D offering: gate the PPM, preserve the exemption, prove what each investor saw

- Independent Sponsor Data Room Checklist — 42-document checklist staged by capital partner type

- Independent Sponsor Deal Book: 10 Sections — anatomy of the deal book capital partners actually read, layered in 3 stages

- Independent Sponsor Conferences & Forums 2026 — full 2026 calendar of 18 IS events (MWISC, DealMAX, iGlobal, SBIA ISF)

- Best Data Rooms for Independent Sponsors — 8 VDRs tested through the IS economic lens

- Independent Sponsor LOI Playbook — 90-day timeline from LOI to close

- Independent Sponsor Capital Raising Playbook — pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- SBIC for Independent Sponsors — 2-to-1 debenture math, $175M/$350M caps, 8 active IS-partner SBICs (Tecum, Cyprium, Argosy, Centerfield, Plexus, Abacus), and $35M EV worked example

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall cascade, and the five Excel mistakes that get models rejected

- Healthcare Capital Partners — 17 firms funding healthcare IS deals

- Business Services Capital Partners — 15 firms funding services IS roll-ups

- Manufacturing Capital Partners — 12 firms funding manufacturing IS deals

- Tech/Software Capital Partners — 13 firms funding SaaS and MSP IS deals

- Consumer Capital Partners — 12 firms funding consumer and CPG IS deals

- Distribution & Logistics Capital Partners — 12 firms funding wholesale, 3PL, cold chain, and specialty distribution IS deals

- Cleantech & Energy Capital Partners — 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Capital Partners Funding Both IS and Search Funds — 9 dual-strategy firms (Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus Fund VII $977M, Miramar) for self-funded searchers, traditional search funds, and IS deals

- Different Passwords for Different Investors — per-LP personalized links, individual passwords, dynamic watermarks, NDA gates, and one-click revoke across 5-15 capital partner shares with forensic attribution when a leak happens

- Due Diligence Data Room Checklist — 174-document checklist across 10 categories

- Best Data Rooms for Private Equity — platform comparison for PE professionals

- M&A Process Guide — 8-phase lifecycle from strategy to integration

- Acquisition Integration Guide — post-close PMI playbook

- Tax Due Diligence Checklist — 8-pillar M&A tax DD framework

- Investment Due Diligence Checklist — 7-pillar buyer-side DD framework

- Vendor Due Diligence Checklist — 6-domain framework for sell-side preparation

- Virtual Data Room Cost Guide — pricing breakdown for every major VDR

- What Is a Virtual Data Room? — comprehensive VDR explainer

- Top 10 Virtual Data Room Providers — scored comparison of 10 platforms

- Data Room for Investors — what investors expect when they open your data room

- Startup NDA Guide — NDA best practices for confidential deal materials

- Seed Funding Guide — fundraising mechanics for first-time capital raisers

- Peony for Private Equity — PE-specific data room features

- Peony for M&A — M&A data room solutions

- Peony for Due Diligence — diligence workflow tools

You might also like

Apr 16, 2026

Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026

Apr 20, 2026

12 Manufacturing Capital Partners Funding Independent Sponsors in 2026

Apr 17, 2026

Independent Sponsor Deal Book (10 Sections, Day-1 Ready) in 2026