12 Manufacturing Capital Partners Funding Independent Sponsors in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Manufacturing independent sponsor deals have become one of the fastest-growing use cases on our platform over the past 12 months, trailing only healthcare and business services. The reason is straightforward: roughly $1.6 trillion in announced US manufacturing and industrial investment commitments are on the books since January 2025 (IndustrialSage Manufacturing Investment Tracker, April 2026), and the lower middle market is where independent sponsors play while the mega-funds chase the $500M+ deals.

The challenge is that most manufacturing capital partners look nothing like a healthcare PE firm. You are not pitching recurring-revenue SaaS economics. You are pitching a $4M-EBITDA CNC shop in Ohio with aging equipment, a union workforce, one Tier-1 OEM customer at 35% of revenue, and an owner who is 67 and wants out in nine months. The capital partner has to underwrite customer concentration, capex intensity, labor relations, environmental liability, and reshoring-driven demand simultaneously. Generic "industry-agnostic" PE firms that back staffing or accounting rollups are not the right partner here.

This guide maps 12 verified capital partners actively funding manufacturing IS deals in 2026 -- PE co-investors, family-office-style patient capital, and SBICs that write checks for precision machining, aerospace components, packaging, industrial services, and specialty manufacturing acquisitions. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide.

TL;DR: Manufacturing is the #3 IS sector behind healthcare and business services but is growing the fastest on reshoring tailwinds. Manufacturing multiples climbed from 10.2x to 11.1x between H1 2024 and H1 2025 driven by reshoring, supply chain diversification, and defense spending (Capstone Partners, 2025). Q4 2025 posted 1,949 industrial manufacturing deals with $156B in aggregate value, up 90% year-over-year (PMCF Industrial Manufacturing M&A Pulse Q4 2025). 54% of IS transactions still close at 4x-6x EBITDA (Citrin Cooperman 2025 IS Report) -- lower than broader PE because IS targets sub-scale founder-led manufacturing. Aerospace and defense hit a record PE year in 2025 with mid-teens to 20x multiples on sole-source IP businesses. The structural tailwind: approximately $1.6 trillion in announced US manufacturing investment is repricing lower-middle-market targets, and Monroe Capital closed a $6.1B private credit fund in January 2026 for sub-$35M EBITDA lower-middle-market lending, much of it earmarked for industrials. Below: 12 capital partners funding these deals, sub-sector multiples, roll-up economics, and what manufacturing capital partners actually need in your data room.

Why Manufacturing Is Growing for Independent Sponsors

Four structural forces converge in 2026 to make manufacturing a compelling IS target sector:

The Reshoring Wave

As of March 31, 2026, roughly $1.6 trillion in announced private-sector US manufacturing and industrial investment commitments are being tracked across 132 companies and 32 states -- covering reshoring, foreign direct investment, and domestic expansion projects of $50M or more since January 2025 (IndustrialSage). Federal reshoring and onshoring initiatives, growing US defense spending, aerospace production backlogs, supply chain security priorities, and the rapid expansion of AI and data center infrastructure are all increasing demand for certified, US-based precision manufacturers. For IS sponsors, this means Tier 2 and Tier 3 suppliers in precision machining, metal fabrication, and specialty components are seeing real demand acceleration -- not just valuation multiple expansion.

Baby Boomer Manufacturing Succession

More than 11,000 Americans turn 65 every day, and manufacturing is where the effect is most magnified because the sector built its strength on stability and long careers (ManufacturingTomorrow, February 2026). Manufacturing had 415,000 job vacancies in June 2025 according to the National Association of Manufacturers. Thousands of founder-owned manufacturing businesses in the $1M-$10M EBITDA range are coming to market with no internal successor -- the kids chose different careers, and the management team cannot finance a buyout. For an IS with manufacturing operating experience, this is the single largest deal flow catalyst in the lower middle market.

Fragmented Sub-Sectors and PE-Validated Thesis

Q4 2025 recorded 1,949 industrial manufacturing deals with $156B in aggregate value, up 90% year-over-year (PMCF Industrial Manufacturing M&A Pulse Q4 2025). CORE Industrial Partners alone closed at least 5 manufacturing platform and add-on deals in 2025 (IMMEC, Edwards Moving & Rigging, Superior Lithographics, Hudson Technologies, and Airway Aerospace). GenNx360 acquired Heartland Business Systems in October 2025 and has completed 118 transactions including 83 bolt-ons over its 19-year history (GenNx360 Capital Partners, October 2025). The thesis is validated -- the question is who funds the deals that are too small for institutional PE.

Debt Capital Supply

Monroe Capital closed on $6.1 billion in new investable capital in January 2026 for its private credit strategy targeting sub-$35M EBITDA lower-middle-market lending (Monroe Capital, January 2026). SBIC fund launches in 2025 added hundreds of millions of dollars in manufacturing-eligible debt capacity, including Tecum Capital Partners IV at $325M (Tecum Capital, February 2025) and Argosy's latest 2025 SBIC vintage at $175M. For IS sponsors, this means the debt side of the capital stack is not the constraint in 2026 -- sourcing proprietary deals and selecting the right equity co-invest partner is.

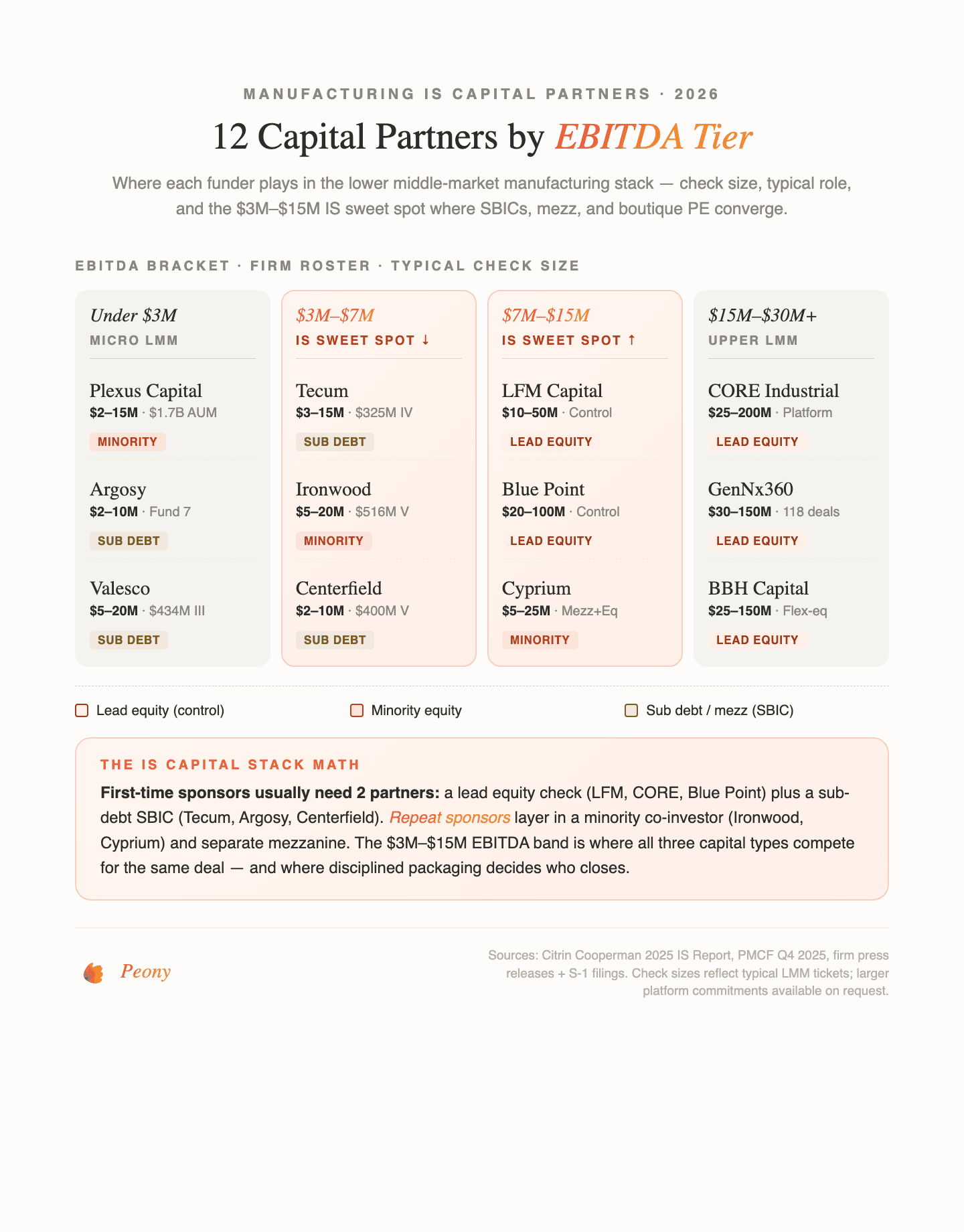

Manufacturing Independent Sponsor Capital Partners: Quick Reference

| Firm | Website | Check Size | Deal Size (EV / EBITDA) | Manufacturing Sub-Sector Focus |

|---|---|---|---|---|

| LFM Capital | lfmcapital.com | Control equity | $15M-$125M EV, $3M+ EBITDA | Manufacturing and industrial services |

| CORE Industrial Partners | coreipfund.com | $25M-$100M | Lower-mid to mid | Manufacturing, industrial tech, industrial svc |

| Blue Point Capital | bluepointcapital.com | $25M-$100M | $25M-$300M revenue | Industrial, business services, consumer |

| GenNx360 Capital Partners | gennx360.com | $25M-$150M | Middle market | Industrial services, niche mfg, packaging |

| BBH Capital Partners | bbh.com/us/en/what-we-do/capital-partners | $20M-$75M | Mid-market | Manufacturing, business products, consumer |

| Tecum Capital | tecum.com | $5M-$20M | $3M+ EBITDA | Manufacturing, value-added distribution (SBIC) |

| Ironwood Capital | ironwoodcap.com | $5M-$25M | Lower-mid | Aerospace/defense, mfg, industrial svc (SBIC) |

| Argosy Private Equity | argosycapital.com | $10M-$30M | Lower-mid | Niche manufacturing, B2B services (SBIC) |

| Valesco Industries | valescoind.com | $5M-$25M | $15M-$100M rev, $3M+ cash flow | Mfg, value-added distribution, B2B svc (SBIC) |

| Centerfield Capital | centerfieldcapital.com | $7M-$25M | $3M-$15M EBITDA | Manufacturing, B2B, distribution (SBIC) |

| Plexus Capital | plexuscap.com | $3M-$30M | $2M-$20M EBITDA | Mfg, distribution, B2B services (SBIC) |

| Cyprium Partners | cyprium.com | $5M-$60M | $4M+ EBITDA | Manufacturing, aerospace, packaging (SBIC) |

Manufacturing-Focused PE and Independent Sponsor Co-Investors

These firms actively co-invest in manufacturing IS deals or operate as manufacturing-focused platforms. Each has a verified track record deploying capital into fabrication, precision machining, aerospace components, and specialty manufacturing acquisitions in the lower middle market.

LFM Capital

Website: lfmcapital.com | Focus: Manufacturing and industrial services | HQ: Nashville

LFM Capital targets lead or control investments in US-based lower middle market manufacturing and industrial services companies with at least $3M of EBITDA and enterprise values from $15M to $125M (LFM Capital). In January 2025, LFM announced the sale of Accelevation LLC to Olympus Partners after partnering with Accelevation since August 2022 to support rapid growth (LFM Capital, January 2025).

Why it matters for IS: LFM's EBITDA target overlaps precisely with the IS sweet spot. Their Nashville base and manufacturing-only focus means they evaluate deals with operational fluency that generalist PE firms lack. For an IS bringing a proprietary manufacturing deal, LFM is a natural equity co-invest partner.

CORE Industrial Partners

Website: coreipfund.com | AUM: $1.58B+ capital commitments | HQ: Chicago

CORE Industrial Partners invests exclusively in lower middle market manufacturing, industrial technology, and industrial service businesses (CORE Industrial Partners). In 2025, CORE closed at least 5 deals across platforms and add-ons: IMMEC (August 2025), Edwards Moving & Rigging, Superior Lithographics, Hudson Technologies (metal stampings and diaphragms, July 2025), and Airway Aerospace via the AxioAero platform (January 2026 announcement — BusinessWire). CORE has now acquired 24 companies across its portfolio.

Why it matters for IS: CORE's exclusive manufacturing focus and active 2025-2026 deal cadence make them the most active manufacturing-specialist PE firm in the lower middle market. IS sponsors sourcing deals in aerospace MRO, precision machining, packaging, or industrial services should have CORE on the first-call list.

Blue Point Capital

Website: bluepointcapital.com | AUM: $1.8B+ committed | HQ: Cleveland

Blue Point invests equity capital in leading lower middle market industrial, business services, and consumer companies generating $25M-$300M in revenue (Blue Point Capital). Their industrial portfolio includes National Safety Apparel (PPE manufacturing), Brimar Industries (safety signs and labels), and Sylvan Industries (industrial pipe fabrication and millwright services). Blue Point-backed NSA and Bashlin Industries were positioned for continued growth as of July 2025 (BusinessWire, July 2025).

Why it matters for IS: Blue Point's four-office footprint (Cleveland, Charlotte, Seattle, Shanghai) gives manufacturing IS sponsors access to global supply-chain expertise -- critical for reshoring-adjacent deals where capital partners need to underwrite both domestic manufacturing economics and Asia-based component supply.

GenNx360 Capital Partners

Website: gennx360.com | AUM: $2.4B | HQ: New York

GenNx360 invests exclusively in North America-based business-to-business middle market industrial services and manufacturing companies in fragmented markets with structural tailwinds (GenNx360). Target industries include business and industrial services, automation and industrial technology, packaging products, equipment services, environmental services, niche manufacturing, and food ingredients and equipment. GenNx360 has completed 118 transactions including 83 bolt-ons over 19 years, with 29 platform companies. The firm was named to Inc.'s 2025 Founder-Friendly Investors List (BusinessWire, October 2025) and acquired Heartland Business Systems as a platform in October 2025.

Why it matters for IS: GenNx360's 83 bolt-on track record is one of the deepest buy-and-build records in lower middle market industrials. For an IS running a manufacturing roll-up thesis, GenNx360's operational playbook and founder-friendly posture make them a credible equity co-invest partner.

BBH Capital Partners

Website: bbh.com | Structure: Merchant banking arm of Brown Brothers Harriman | HQ: New York

BBH Capital Partners is the private equity arm of Brown Brothers Harriman, the oldest and largest private bank in the US. The firm seeks to invest across business products, business services, consumer products, manufacturing, and industrial sectors in North America (BBH Capital Partners). Manufacturing portfolio companies include 700 Valve Supply (industrial valve MRO distribution), American Spraytech (aerosol and bag-on-valve manufacturing), and Wolter Inc. (material handling equipment dealer). Their most recent investment was Salem Plumbing Supply on December 19, 2025.

Why it matters for IS: BBH's patient-capital positioning -- backed by a 200-year-old private bank -- makes them a natural partner for IS sponsors pursuing longer-hold manufacturing roll-ups where generalist PE funds want a 3-to-5-year exit. Their industrial portfolio depth signals genuine sector familiarity, not a tourist allocation.

Manufacturing SBICs and Mezzanine Providers

SBICs provide subordinated debt and equity that fill critical gaps in manufacturing IS capital stacks. With SBA-leveraged capital, SBICs offer more flexible terms than traditional bank lenders -- particularly valuable for capex-heavy manufacturing acquisitions where senior lenders cap advance rates on equipment-backed borrowing bases. Seven of the most active manufacturing SBIC capital partners:

Tecum Capital

Website: tecum.com | Fund IV: $325M SBIC fund | HQ: Pittsburgh

Tecum Capital Partners IV, L.P. launched in February 2025 at $325M and is the firm's fourth SBIC-licensed fund (Tecum Capital, February 2025). Tecum provides mezzanine debt and minority equity investments of $5M-$20M in businesses with EBITDA greater than $3M across manufacturing, value-added distribution, and business services. In November 2025, Tecum Equity Alpha Management and the Armstrong Group formed SupplyCo, an industrial supply platform for operationally essential products across industrial, manufacturing, and field service applications (Tecum Capital, November 2025). In September 2025, Cantilever Group made a strategic minority investment in Tecum itself, bolstering the firm's balance sheet for continued deployment.

Why it matters for IS: Tecum's $5M-$20M check size and $3M+ EBITDA target is the sweet spot for lower middle market manufacturing IS deals. The SupplyCo formation demonstrates Tecum's appetite for operational platforms, not just passive mezzanine lending. For an IS sourcing a $15M-$30M EV fabrication or distribution deal, Tecum is a first-call mezz partner.

Ironwood Capital

Website: ironwoodcap.com | Fund V: $516M | HQ: Avon, CT

Ironwood Capital provides non-control growth capital to middle market companies, investing $5M-$25M in subordinated debt and preferred stock across aerospace and defense, manufacturing, transportation and logistics, waste and environmental services, business services, facilities services, and healthcare (Ironwood Capital). Ironwood has deployed more than $1 billion across over 100 companies, operates through SBIC-licensed funds, and is currently investing from Ironwood Capital Partners V LP which closed at $516M in 2022.

Why it matters for IS: Ironwood's non-control preferred stock and subordinated debt structure preserves the IS's majority ownership and operating control. Their explicit aerospace and defense sector focus is rare among SBICs -- for an IS sourcing a Tier 2 or Tier 3 A&D supplier deal, Ironwood is one of a small number of non-control capital partners with genuine sector expertise.

Argosy Private Equity

Website: argosycapital.com | Latest SBIC: $175M (2025 vintage) | HQ: Wayne, PA

Argosy Private Equity was named the 2024 SBIC of the Year -- Established Manager by the SBA (SBIA, May 2024). Through six SBIC-licensed funds, Argosy has partnered with over 130 companies across 34 states since 1990, focusing on family-and-founder-led businesses in niche manufacturing and B2B services largely located outside urban and suburban areas -- including Low-or-Moderate-Income (LMI) areas and HUBZones. Argosy's 2025 vintage mezzanine fund totals $175M.

Why it matters for IS: Argosy's explicit focus on rural and underserved geography is a differentiator. For an IS with a proprietary deal in a tier 3 or tier 4 metro (think small-town Pennsylvania fabrication or rural Midwest foundries), Argosy understands the dynamics and will actually look at the deal. Most SBICs cluster deal flow in NY/Chicago/Dallas -- Argosy reaches into the 34 states where manufacturing founder-owners actually live.

Valesco Industries

Website: valescoind.com | Fund III: $434M | HQ: Dallas

Valesco has invested in private and family-owned businesses since 1993 focusing on manufacturing, value-added distribution, and business-to-business services. Fund III closed at $434M and received its SBIC license in Q4 2022 (Valesco Industries). The firm makes control and non-control investments of $5M-$25M in companies with $15M-$100M revenue and at least $3M of cash flow. Valesco was awarded the SBA SBIC of the Year as an Emerging Manager in 2022.

Why it matters for IS: Valesco's Dallas base puts them at the center of Texas and Southwest manufacturing deal flow. Their non-control investment option is particularly valuable for IS sponsors who want to retain majority ownership while accessing SBIC debt leverage. The firm's explicit manufacturing and distribution focus beats generalist SBICs for sector-informed diligence.

Centerfield Capital Partners

Website: centerfieldcapital.com | Fund V: $400M (SBIC + parallel) | HQ: Indianapolis

Centerfield holds a hard-cap close of its fifth fund, Centerfield Capital Partners V LP and CCP V-SBIC LP (together Fund V), with $400M of total capital. Centerfield invests $7M-$25M of subordinated debt and equity in US-based companies with revenue of $15M-$100M and EBITDA of $3M-$15M across business services, consumer products, healthcare services, manufacturing, and value-added distribution (Centerfield Capital Partners). The firm explicitly states it was "backing independent sponsors before the nomenclature existed" and structures transactions in partnership with private equity sponsors, independent sponsors, business owners, and management teams.

Why it matters for IS: Centerfield's institutional IS track record is the single strongest IS signal in the SBIC peer set. Their $3M-$15M EBITDA target matches the IS sweet spot, and their Indianapolis base gives deep Midwest manufacturing deal coverage. For an IS on a first deal, Centerfield's experience structuring IS transactions means less friction on term-sheet mechanics.

Plexus Capital

Website: plexuscap.com | AUM: $1.7B across 181 investments | HQ: Raleigh, NC

Plexus Capital meets SBA licensing criteria to provide subordinated debt and equity capital as an SBIC, and was previously named the nation's SBIC of the Year (Plexus Capital). Plexus invests $3M-$30M in companies with revenue up to $100M and EBITDA from $2M-$20M, targeting lower middle market businesses in the Mid-Atlantic and Southeast US. Target sectors include business services, consumer services, manufacturing, value-added distribution, and healthcare. Manufacturing accounts for approximately 9% of Plexus Capital's portfolio by sector.

Why it matters for IS: Plexus's $2M EBITDA minimum is one of the lowest in the SBIC universe, meaning they will actually look at micro-cap manufacturing deals that most SBICs reject. For an IS sourcing a $2M-$3M EBITDA family-owned manufacturer in North Carolina, Georgia, or Virginia, Plexus is one of the few SBICs that will take the first meeting.

Cyprium Partners

Website: cyprium.com | AUM: $2B+ invested | HQ: Cleveland

Cyprium provides non-controlling mezzanine debt, preferred stock, and minority equity investments in profitable middle market companies, investing $5M-$60M per transaction in companies with $4M+ EBITDA (Cyprium Partners). The firm launched its first SBIC fund in 2023. Cyprium's most recent manufacturing-sector activity includes a subordinated debt and preferred equity investment in Albers Aerospace in May 2025 to support strategic acquisitions and future growth (Cyprium Partners, May 2025), and a debt investment in T&R Recovery Group. Target sectors include food and beverage, aerospace, plastics and packaging, manufacturing, distribution, and building products.

Why it matters for IS: Cyprium's non-control model preserves the IS's majority ownership. The Albers Aerospace investment demonstrates active deployment into the aerospace sub-sector with a buy-and-build thesis -- directly aligned with IS roll-up economics.

How to Choose Your Manufacturing Capital Partner (Decision Framework)

Manufacturing is the most heterogeneous IS sector. A $3M-EBITDA CNC shop in Pennsylvania, a $20M-EBITDA aerospace components supplier, and a $12M-EBITDA industrial distribution platform all sit under "manufacturing" but fit different capital partner profiles. Use these branches to narrow your capital-partner shortlist before you send the CIM.

Branch 1: By Deal EBITDA

- Sub-$3M EBITDA: Plexus Capital ($2M minimum), Argosy (rural/LMI focus), Valesco (small-end mandate). Most manufacturing-specialist PE firms (LFM, CORE, GenNx360) will decline at this size.

- $3M-$7M EBITDA: Centerfield, Tecum, Plexus, Ironwood, Cyprium -- the SBIC sweet spot. LFM will consider the top end of this band.

- $7M-$15M EBITDA: LFM, Blue Point (lower end), Valesco, BBH (smaller positions), plus any SBIC mezzanine as part of the capital stack.

- $15M-$30M+ EBITDA: CORE Industrial Partners, GenNx360, Blue Point, BBH Capital Partners -- scaled manufacturing platforms. SBICs participate as mezzanine, not equity lead.

Branch 2: By Sub-Sector

- Aerospace and defense: Cyprium (Albers Aerospace track record), CORE (AxioAero platform), Ironwood (core sector), Blue Point (NSA electrical safety). Avoid generalist SBICs without A&D-specific deals -- the ITAR, export control, and FAA diligence will slow them to a crawl.

- Precision machining, metal fabrication, CNC: LFM Capital, CORE Industrial Partners, Tecum Capital, Centerfield. Look for firms with portfolio companies that read like your target.

- Industrial services and distribution: Tecum (SupplyCo platform), Blue Point (Sylvan), BBH (700 Valve Supply), Valesco. Recurring-revenue industrial distribution reads like business services and commands higher multiples.

- Specialty packaging and converting: GenNx360, CORE (Superior Lithographics in Momentium platform), Cyprium (plastics and packaging core sector). Reshoring-driven demand.

- Electrical equipment, utilities components: Blue Point (National Safety Apparel), BBH, Ironwood. Tied to grid modernization and AI data center buildout.

- Food and beverage equipment: GenNx360, Cyprium. Narrow pool, but structural tailwinds from food supply-chain reshoring.

Branch 3: By Capital Stack Role

- Need lead equity check (control or majority): LFM, CORE, Blue Point, GenNx360, BBH. These firms take the reins; the IS stays on as sourcing partner and board member.

- Need non-control minority equity: Ironwood, Cyprium, Centerfield, Plexus, Tecum -- the IS retains operating control and governance. This is the most common IS deal structure.

- Need subordinated debt to fill capital stack: Every SBIC on this list (Tecum, Argosy, Valesco, Centerfield, Plexus, Ironwood, Cyprium, HCAP indirectly). Pair one SBIC with one senior lender like Monroe Capital whose January 2026 $6.1B close signaled aggressive deployment appetite.

Branch 4: By Geography

- Northeast/Mid-Atlantic: Ironwood (Connecticut), BBH (New York), Argosy (Pennsylvania), Plexus (North Carolina).

- Midwest: CORE (Chicago), GenNx360 (also with Midwest exposure), Blue Point (Cleveland), Centerfield (Indianapolis), Cyprium (Cleveland).

- Southeast: Plexus (North Carolina Mid-Atlantic and Southeast footprint), LFM Capital (Nashville).

- Southwest/Texas: Valesco (Dallas). Surprisingly thin bench outside of Valesco for Texas-focused manufacturing IS deals.

- Rural/LMI/HUBZone: Argosy. If your deal is in a tier-3 or tier-4 metro, this is the SBIC that wants the deal.

Branch 5: By Sponsor Experience Level

- First-time IS (no closed deals yet): Lead with Centerfield (institutional IS specialist) and one manufacturing-specialist like LFM or CORE. Avoid firms that require a closed track record before engagement.

- Experienced IS (3+ closed deals): You can lead with equity specialists (LFM, CORE, GenNx360) and pull SBIC mezzanine in separately. Repeat relationships matter -- 59% of capital partner deals come from repeat IS relationships per Citrin Cooperman 2025.

- Operating-partner IS (former industry executive): Lean into firms that value operational experience -- BBH, Blue Point, GenNx360, LFM. Your operating credibility is worth more to these firms than a 2 percentage-point equity concession.

What Manufacturing Capital Partners Look For in a Data Room

Manufacturing diligence is more document-heavy than healthcare or business services because of physical assets, environmental exposure, and labor complexity. Based on our experience hosting manufacturing IS data rooms, here is what capital partners expect -- organized for the staged diligence approach in our complete IS guide. Set up your data room on day one of the exclusivity window.

Stage 1: Initial Risk Scan (Week 1-2)

- Confidential Information Memorandum with manufacturing thesis and sub-sector positioning

- Top-10 customer concentration with contract terms and renewal dates

- Trailing 5-year revenue, gross margin, and EBITDA by product line or plant

- Capex history (maintenance versus growth split) and forward 3-year capex plan

- Sub-sector context: reshoring exposure, OEM supplier tier, certification scope (ISO 9001, AS9100, IATF 16949, FDA, USDA)

- Sponsor track record, operating background, and industry network

Stage 2: Deep Dive (Week 2-4)

- Quality of Earnings with manufacturing normalization adjustments (inventory methods, capex, overhead absorption)

- Plant-level P&L with labor and overhead allocation

- Equipment list with age, condition, and estimated remaining useful life

- Third-party equipment appraisals (ASA-certified for capex-heavy targets)

- Customer contracts, purchase orders, LTA (long-term agreements) portfolio

- Union contracts, labor agreements, NLRB history, OSHA incident logs

- Environmental records: Phase I ESA, permits, spill history, RCRA and CERCLA exposure

Stage 3: Comprehensive Validation (Week 3-5)

- Phase II ESA (if triggered by Phase I findings)

- Working capital bridge with manufacturing-specific adjustments

- Supply chain stress-test: single-source components, reshoring dependencies, tariff exposure

- Tax structure analysis (see our tax due diligence checklist)

- 100-day integration plan with capex and operational efficiency milestones

- Add-on acquisition pipeline with target profiles (for roll-up IS theses)

- Insurance certificates: general liability, product liability, environmental, D&O

For the complete 174-document due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes these documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is the maintenance capex as a percent of revenue?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. The AI redaction feature identifies pricing, customer names, and sensitive terms across uploaded documents before you share with capital partners, a workflow that Datasite charges $25K+ per deal to configure manually.

Manufacturing IS Outreach Mechanics

Manufacturing capital partner outreach has a different rhythm than healthcare or business services. Three durable patterns:

1. Lead with the sub-sector, not "manufacturing." A blast message that says "I have a $20M manufacturing deal" gets a form response. A message that says "I have a $22M aerospace MRO deal with a sole-source OEM contract, AS9100 certification, and $4.2M EBITDA" gets a partner-level callback. Manufacturing-specialist PE firms filter hundreds of CIMs per year -- sub-sector specificity is the signal that separates proprietary sourcing from broker-broadcast deals.

2. Include the capex story up front. Every manufacturing capital partner opens the same question: "What is maintenance capex, what is growth capex, and how does that reconcile to the EBITDA you are representing?" If the CIM answers this on page 3 with a capex bridge table, you skip two weeks of back-and-forth. For a founder-owned target, pull 5 years of fixed-asset additions from the tax return and build the bridge yourself before the capital partner asks.

3. Preempt the customer concentration question. Manufacturing targets almost always have concentration -- a Tier 2 supplier with one OEM at 40% is normal. What kills deals is surprise concentration disclosed in Week 3. Lead with it in Week 1, explain the contract structure (LTA length, pricing mechanics, multi-year POs), and present the mitigation story (pipeline, cross-selling, product line expansion). This is the same playbook we recommend in our business services capital partners guide -- the principles travel.

Use Peony's page-level analytics to track which capital partners are reading the capex bridge and customer concentration tabs versus skimming the CIM. The ones who spend 20 minutes on the Q of E are the ones worth second meetings. Use personalized sharing links so every capital partner gets a distinct tracking URL, and NDA gates so nobody sees confidential documents until they sign -- something DocSend cannot detect on any plan.

Manufacturing Independent Sponsor Deals By the Numbers

- $1.6 trillion in announced US manufacturing investment tracked since January 2025 across 132 companies and 32 states (IndustrialSage Manufacturing Investment Tracker, April 2026)

- 1,949 industrial manufacturing deals in Q4 2025 with $156B in aggregate value, up 90% year-over-year (PMCF Industrial Manufacturing M&A Pulse Q4 2025)

- Manufacturing multiples climbed from 10.2x to 11.1x between H1 2024 and H1 2025 (Capstone Partners Middle Market M&A Valuations Index, 2025)

- $6.1 billion private credit fund closed by Monroe Capital in January 2026 for sub-$35M EBITDA lower-middle-market lending (Monroe Capital, January 2026)

- 415,000 manufacturing job vacancies reported by the National Association of Manufacturers in June 2025, underscoring labor constraints and succession urgency

- 54% of IS transactions closed at 4x-6x EBITDA in 2024-2025 (Citrin Cooperman 2025 IS Report)

- 62% of IS transactions funded by family offices, with manufacturing and industrials among their top three sector allocations (Citrin Cooperman 2025)

- CORE Industrial Partners closed 5+ manufacturing deals in 2025 across platforms and add-ons (CORE Industrial Partners news)

- 118 transactions including 83 bolt-ons completed by GenNx360 over 19-year history, validating buy-and-build in niche manufacturing (GenNx360, October 2025)

- Aerospace and defense delivered a record PE year in 2025 with multiples in the mid-teens to 20x for sole-source high-IP businesses (PE Hub, 2025)

Quick Guide: Match Your Situation to the Right Capital Partner

| Situation | Best CP Fit | Why |

|---|---|---|

| First-time IS, $8M EV CNC shop, $2.5M EBITDA, rural PA | Argosy Private Equity + Plexus Capital | LMI/rural focus (Argosy); $2M EBITDA minimum (Plexus) |

| Experienced IS, $30M EV aerospace MRO, $4M EBITDA, Tier 2 supplier | CORE Industrial Partners + Cyprium (mezz) | CORE's AxioAero platform; Cyprium's Albers Aerospace buy-and-build track record |

| Operating-partner IS, $50M EV industrial distribution, $8M EBITDA | Blue Point Capital + Tecum (mezz) | Blue Point 4-office footprint; Tecum's SupplyCo industrial distribution platform |

| First-time IS, $12M EV specialty packaging, $3M EBITDA, reshoring | GenNx360 + Centerfield (mezz) | GenNx360 packaging focus; Centerfield institutional IS specialist |

| Experienced IS, $75M EV precision machining roll-up, $12M EBITDA | LFM Capital + Ironwood (mezz) + Monroe (senior) | LFM manufacturing-only focus; Ironwood non-control; Monroe scale debt |

| Operating-partner IS, $25M EV family-owned fabrication, $4M EBITDA, TX | Valesco Industries + Centerfield (mezz) | Valesco Texas base; Centerfield IS structure experience |

| First-time IS, $18M EV electrical components, $3.5M EBITDA, Southeast | Plexus Capital + BBH (minority) | Plexus Mid-Atlantic/Southeast footprint; BBH patient capital for long-hold |

| Experienced IS, $100M+ EV industrial platform, $20M+ EBITDA | GenNx360 + Blue Point + Monroe Capital (senior) | Scale capital partners; Monroe's $6.1B January 2026 close for sub-$35M EBITDA targets |

Bottom Line

Manufacturing is the fastest-growing IS sector in 2026 because the structural forces are unusually well-aligned: a $1.6 trillion reshoring wave, a demographic succession cliff, validated PE deal volume through Q4 2025, and abundant SBIC + private credit capital for the debt side of the capital stack. The capital partner ecosystem for manufacturing IS deals is narrower and more specialized than healthcare or business services, but the firms that show up are seriously committed to the sector.

If you are targeting precision machining, fabrication, or industrial components: LFM Capital, CORE Industrial Partners, GenNx360, and Blue Point Capital are the most active manufacturing-specialist equity co-investors. Platform acquisitions at 5x-7x EBITDA with add-on bolt-ons at 3.5x-5x remain the proven playbook. Customer concentration, capex intensity, and labor relations are the three diligence kill-switches.

If you are targeting aerospace, defense, or sole-source IP businesses: CORE (AxioAero platform), Cyprium (Albers Aerospace), Ironwood Capital (core sector), and Blue Point (National Safety Apparel) have verified sub-sector deal flow. Multiples run 9x-14x or higher for the right profile. Expect ITAR, export control, and FAA/EASA certification diligence to add 2-4 weeks versus generic manufacturing.

If you need mezzanine or subordinated debt: Tecum Capital ($325M Fund IV, 2025 vintage), Argosy Private Equity ($175M 2025 vintage, 2024 SBIC of the Year), Valesco Industries ($434M Fund III, Dallas-based), Centerfield Capital Partners ($400M Fund V, institutional IS specialist), Plexus Capital ($2M EBITDA minimum), Ironwood Capital (non-control preferred stock), and Cyprium Partners (non-control mezz + preferred equity) all provide flexible capital structures tailored to manufacturing IS capital stacks. Pair one SBIC with one senior lender like Monroe Capital -- the M&A debt side of the stack is not the bottleneck in 2026.

For every manufacturing IS deal: Set up your data room on day one of the exclusivity window. Manufacturing diligence moves slower than business services because of physical asset review, equipment appraisals, and environmental reports -- but that means capital partners expect the data room to be organized and complete at Week 1. You cannot afford to lose days to VDR setup. Peony lets you build a complete manufacturing data room in under 5 minutes, with page-level analytics that show which capital partners are reading the capex bridge versus skimming the CIM, and AI-powered Smart Q&A that surfaces hard answers with page citations so capital partners complete diligence faster. For deeper context on private equity co-investment structures, M&A deal process, due diligence expectations, family office dynamics, and fundraising best practices, see our dedicated solutions guides.

Peony Data Room at $52/admin/month includes AI auto-indexing, AI-powered Smart Q&A, AI redaction, AI Rooms, dynamic watermarks, screenshot protection, NDA gates, custom domain, and aggregate analytics dashboard. An IS running three manufacturing deals per year pays roughly $624 annually versus $45,000-$150,000 on Datasite. When your exclusivity clock is ticking and five capital partners need to get comfortable with the deal simultaneously, every hour matters.

Set up your first manufacturing IS data room -- see plans and pricing.

Frequently Asked Questions

I am a first-time IS with a signed LOI on a $15M packaging deal -- which capital partners fund manufacturing independent sponsor deals?

Manufacturing independent sponsor deals are funded by three capital partner types: manufacturing-focused PE firms that co-invest on a deal-by-deal basis such as LFM Capital, CORE Industrial Partners, Blue Point Capital, and GenNx360; family-office and patient-capital firms like BBH Capital Partners that take minority positions; and SBIC debt-plus-equity providers such as Tecum Capital, Ironwood Capital, Argosy Private Equity, Valesco Industries, Centerfield Capital, Plexus Capital, Cyprium Partners, and HCAP Partners. For a first-time IS on a $15M packaging deal, a $3M-$5M check from an SBIC like Centerfield or Tecum plus a minority equity partner like Ironwood is the typical stack. Peony Business at $30 per admin per month lets you share deal materials with all of them through NDA-gated links while page-level analytics show which capital partner actually read the quality of earnings.

I run corp dev at a mid-market PE firm -- what EBITDA multiples do manufacturing independent sponsor deals trade at in 2026?

Manufacturing IS deals typically trade at 5x to 7x EBITDA for platform acquisitions and 3.5x to 5x for add-ons, compared to 8x to 10x for scaled PE-backed manufacturing platforms. Sub-sector ranges in 2025-2026 include asset-heavy commodity manufacturing at 5x to 7x, engineered specialty products at 7x to 9x, aerospace and defense at 9x to 14x for sole-source high-IP businesses, precision machining and CNC at 6x to 8x, and industrial services at 6x to 8x. For a corp dev lead evaluating a $25M-$50M family-owned fabrication business, the spread between add-on and platform multiples is the core value creation mechanism. Peony Business includes AI document extraction that lets capital partners ask What is the customer concentration or What is capex as a percent of sales across uploaded financials and get cited answers with exact page numbers, a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first manufacturing IS deal -- why is manufacturing growing for independent sponsors in 2026?

Manufacturing is growing for independent sponsors because four structural forces converge in 2026: the reshoring wave with roughly $1.6 trillion in announced US manufacturing and industrial investment commitments tracked since January 2025, aging founder-owners with manufacturing, logistics, and agriculture magnified in the baby boomer succession wave, fragmented sub-sectors where PE mega-funds ignore sub-$10M EBITDA targets, and PE-backed add-on activity that reached 73 percent of all buyouts in 2025. For a family office allocating $5M-$15M equity to its first IS deal, focus on founder-led businesses with $3M-$10M EBITDA in reshoring-adjacent sub-sectors like precision machining, aerospace MRO, or industrial services. Peony Business at $30 per admin per month includes page-level analytics that show which capital partners spent 30 minutes on the Q of E versus skimmed the CIM, so you can prioritize follow-ups with genuinely engaged partners.

I am a corp dev analyst building my first manufacturing data room -- what documents do capital partners need?

Manufacturing capital partners require standard M&A diligence plus manufacturing-specific materials: customer concentration analysis with top 10 revenue and contract terms, bill-of-materials and gross margin by SKU or product line, capex history and trailing 5-year maintenance-versus-growth split, plant-level P&L with labor-and-overhead absorption, equipment list with age and replacement cost, ISO and AS9100 quality certifications, environmental compliance records with Phase I and Phase II ESAs, OSHA incident logs and workers comp history, union contracts and labor relations files, and any reshoring-linked supplier or OEM contracts. For a corp dev analyst running point on a $20M-$40M fabrication deal, these are the documents that kill or close the transaction. Peony Data Room at $52 per admin per month includes auto-indexing that organizes all of these in under 3 minutes into a professional folder structure, and Smart Q and A that routes capital partner questions through AI-drafted answers with page citations before your team approves each response.

Our IS targets aerospace and defense -- which capital partners fit sub-sector specialists?

For aerospace and defense IS deals, the best capital partner fit depends on deal size and IP profile. Sole-source high-IP aerospace targets commanding 9x to 14x EBITDA fit firms like CORE Industrial Partners whose AxioAero platform acquired Airway Aerospace in January 2026, or Cyprium Partners which completed a subordinated debt and preferred equity investment in Albers Aerospace in May 2025 to support strategic acquisitions. Defense electronics and MRO fits Blue Point Capital and Ironwood Capital which lists aerospace and defense as a core sector. For a specialized IS targeting a $30M-$50M precision-machining business with Tier 2 OEM contracts, the stack usually pairs a manufacturing-focused equity check with SBIC debt from Tecum or Argosy. Peony Business at $30 per admin per month includes screenshot protection, which aerospace capital partners require before reviewing ITAR or export-controlled specs.

Our IS is running three to six manufacturing deals per year -- how much does a data room cost for a manufacturing independent sponsor deal?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 3 to 25 million dollar EBITDA manufacturing businesses. Manufacturing deals also require extensive technical document uploads, engineering drawings, equipment appraisals, environmental reports, and ISO certifications, meaning sponsors often need four to six active data rooms simultaneously during a roll-up phase. Peony Data Room at 52 dollars per admin per month includes unlimited data rooms, AI auto-indexing, AI document extraction, Smart Q and A, AI redaction, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. An IS running three manufacturing deals per year pays roughly 624 dollars annually on Peony Data Room versus 45,000 to 150,000 dollars on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure.

I am a capital-partner PE principal diligencing an industrial distribution deal -- what manufacturing sub-sectors have the most IS activity?

The most active manufacturing sub-sectors for independent sponsor deals in 2025-2026 are precision machining and metal fabrication where fragmented owner-operators dominate, aerospace MRO and defense electronics with 41 PE transactions in Q2 2025 alone, industrial services and supply where Tecum Equity and Armstrong Group formed SupplyCo in November 2025, specialty packaging and converting benefiting from reshoring of CPG supply chains, electrical products and utilities equipment tied to grid investment and AI data center buildout, and food and beverage equipment. For a capital-partner PE principal diligencing a $30M-$50M industrial distribution platform, expect customer concentration to be the single biggest diligence issue. Peony Data Room at 52 dollars per admin per month includes AI-powered Smart Q and A that lets capital partners submit diligence questions where AI surfaces relevant document sections with exact page citations, something DocSend cannot detect on any plan.

I am an M&A attorney advising a first-time IS -- how do manufacturing capital partners expect deal books to be structured?

Manufacturing capital partners expect deal books organized in a standard 3-stage diligence flow: Stage 1 initial risk scan including the CIM, customer concentration, capex history, and environmental screening; Stage 2 deep dive with Q of E, equipment appraisals, union and labor compliance, and customer contracts; Stage 3 comprehensive validation covering Phase I ESAs, OSHA audits, and 100-day integration plan. For an M&A attorney advising a first-time IS running a $20M enterprise value deal, the folder structure alone can cost you a capital partner if it looks amateurish. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing that organizes documents into a professional folder structure in under 3 minutes, and personalized sharing links that track each capital partner separately so you know who is engaged before you draft the capital call.

Our IS is running a $40M roll-up of CNC shops -- how do we handle capex-heavy due diligence on a manufacturing target?

Capex-heavy manufacturing targets require a disciplined split between maintenance capex and growth capex in the Q of E, with 5-year historical capex, a plant-by-plant equipment list showing age and remaining useful life, and a forward 3-year capex forecast that capital partners can stress-test. For an IS running a $40M roll-up of CNC shops, every dollar of understated maintenance capex is a dollar of overstated EBITDA, and every capital partner will model that sensitivity. Document equipment appraisals from a qualified third-party ASA appraiser, attach maintenance logs for mission-critical machines, and include warranty and service contracts. Peony Business at 30 dollars per admin per month includes AI redaction that identifies pricing and customer data across uploaded equipment and customer files, and NDA gates that prevent any capital partner from seeing confidential specs before signing, a workflow that Datasite charges $25K+ per deal to configure.

I am a first-time IS building a capital partner network -- where do manufacturing independent sponsors meet capital partners in 2026?

Manufacturing independent sponsors meet capital partners at the McGuireWoods Independent Sponsor Conference with 1,600 attendees in 2025 and the 2026 event on October 27-28 in Dallas, the ACG InterGrowth conference anchoring the spring LMM calendar, the SBIA Independent Sponsor Forum in Philadelphia, iGlobal Independent Sponsor Summit events, and through platforms like Axial where independent sponsors closed 27 percent of all deals in 2025. Repeat relationships account for 59 percent of capital partner deals according to Citrin Cooperman. For an IS building a 5-to-10 firm capital partner rolodex focused on manufacturing, starting with SBICs like Tecum and Argosy plus one manufacturing-specialist like LFM or CORE is the fastest path. Peony Business at 30 dollars per admin per month includes NDA-gated data rooms with built-in e-signatures so capital partners can sign and access materials in a single workflow after conference introductions.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- SBIC for Independent Sponsors -- 2-to-1 debenture math, $175M/$350M caps, 8 active IS-partner SBICs (including Tecum, Argosy, Centerfield, Plexus on manufacturing), and $35M EV worked example

- Independent Sponsor Healthcare Capital Partners -- 17 firms funding healthcare IS deals

- Independent Sponsor Business Services Capital Partners -- 15 firms funding business services IS deals

- Independent Sponsor Tech/Software Capital Partners -- 13 firms funding SaaS and MSP IS deals

- Independent Sponsor Consumer Capital Partners -- 12 firms funding consumer and CPG IS deals

- Independent Sponsor Distribution & Logistics Capital Partners -- 12 firms funding wholesale, 3PL, cold chain, and specialty distribution IS deals

- Independent Sponsor Cleantech & Energy Capital Partners -- 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Independent Sponsor Data Room Checklist -- staged diligence checklist by capital partner type

- Independent Sponsor LOI Playbook -- post-LOI capital assembly and exclusivity management

- Independent Sponsor Deal Book -- what capital partners want to see in 2026

- Independent Sponsor Conferences and Forums -- 21 events mapped for IS dealmakers

- Best Data Rooms for Independent Sponsors -- platform comparison for IS workflows

- Due Diligence Data Room Checklist -- 174-document checklist across 10 categories

- M&A Process Guide -- 8-phase lifecycle from strategy to integration

- Tax Due Diligence Checklist -- 8-pillar M&A tax DD framework

- Peony for Private Equity -- PE-specific data room features

- Peony for M&A -- M&A data room solutions

- Peony for Due Diligence -- diligence workflow tools

- Peony for Family Offices -- family office capital partner workflows

You might also like

Apr 17, 2026

Independent Sponsor Deal Book (10 Sections, Day-1 Ready) in 2026

Apr 16, 2026

The 22 Independent Sponsor Conferences & Forums in 2026

Apr 16, 2026

Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026