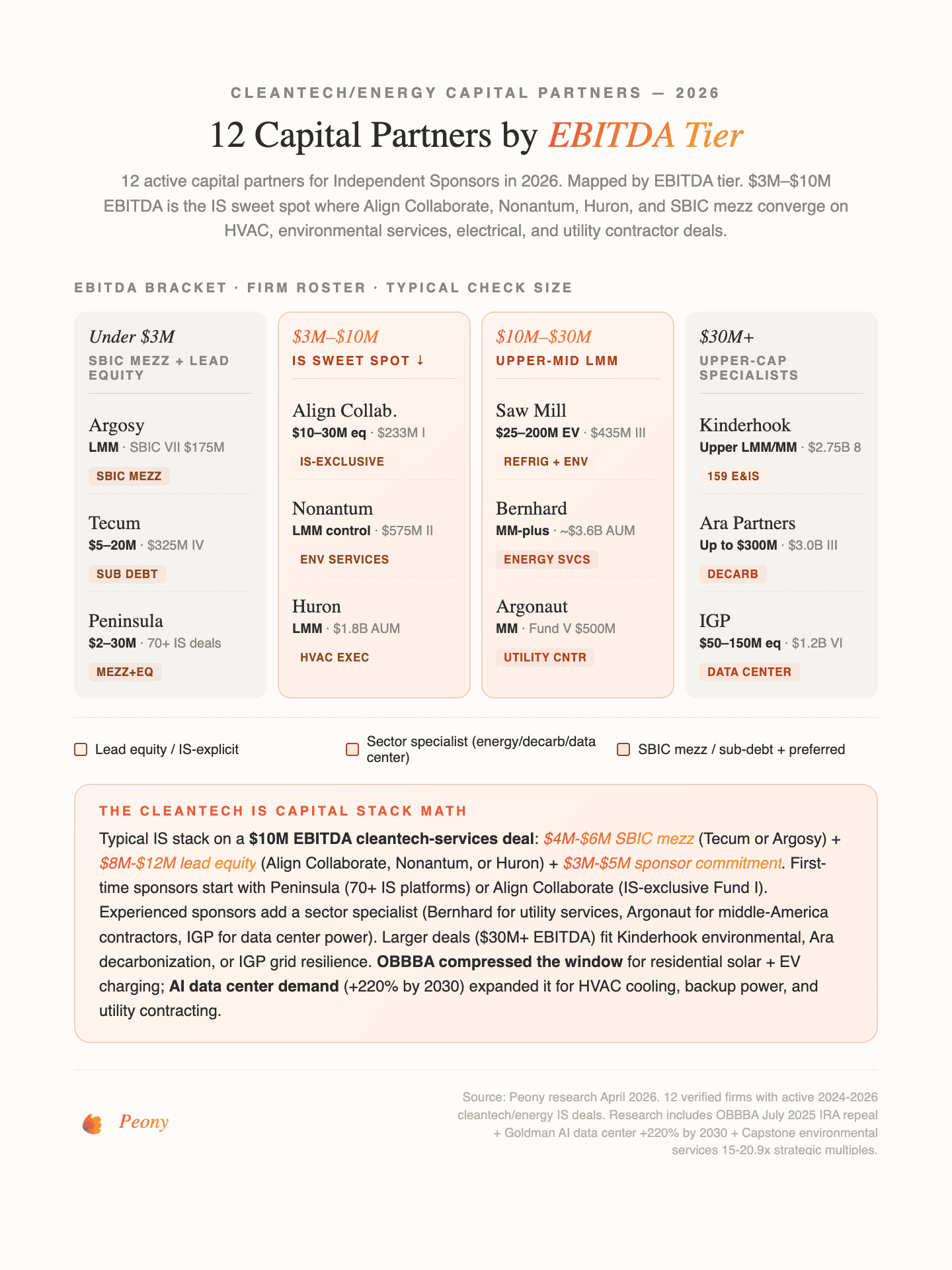

12 Cleantech & Energy Capital Partners for Independent Sponsors 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Cleantech and energy independent sponsor deals have moved from a niche slice of our IS pipeline to one of the three fastest-growing verticals on the platform over the past 12 months -- behind manufacturing and distribution/logistics but ahead of consumer in active rooms created during Q1 2026. The reason is structural and legislative: OBBBA's July 4, 2025 partial IRA repeal compressed the M&A window for several cleantech sub-sectors while AI data center electricity demand (up 220% by 2030 per Goldman Sachs) and the biggest strategic-deal multiple expansion of any sector in 2025 (environmental services at 15.0x-20.9x per Capstone) have created the richest sub-sector spread in any IS vertical.

The challenge is that most "generalist" LMM PE firms are not the right cleantech partner. You are not pitching a SaaS rollup. You are pitching a $7M-EBITDA family-owned commercial HVAC contractor in Ohio with 140 field technicians, 22% revenue from three large utility customers, $4M of service-truck fleet, 18 open warranty claims, a journeyman licensure stack across four states, NETA certifications on half the crew, and an owner who is 64 and wants to retire in nine months. Or a $5M-EBITDA environmental services operator in Louisiana with RCRA hazardous waste handler permits, DOT hazmat compliance files, Phase II ESA exposure on two legacy yards, and a municipal customer concentration issue. The capital partner has to underwrite utility or municipal customer concentration, warranty exposure on prior project work, OBBBA tax credit eligibility, NERC/FERC compliance, environmental liability, and licensure stack simultaneously. Generic PE firms that back tech-services rollups are not the right partner here.

This guide maps 12 verified capital partners actively funding cleantech and energy IS deals in 2026 -- IS-explicit equity partners, sector-specialist PE, and SBICs that write checks for environmental services, HVAC, electrical contracting, utility services, industrial decarbonization, and energy efficiency acquisitions. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide. I spent years evaluating cleantech, energy, and industrial deals at Backed VC and Target Global before starting Peony, and the cleantech IS diligence stack below is the one I would run on my own capital.

TL;DR: Cleantech and energy is the #5 vertical for independent sponsors in 2026 by deal volume (behind manufacturing, healthcare, tech/software, and distribution) but arguably has the most legislatively compressed window of any vertical. Energy, natural resources, and chemicals M&A hit $333.7 billion in 2025 -- up 31.3% YoY (KPMG Energy M&A 2025). Waste and recycling posted 202 transactions worth $5.7 billion disclosed in 2025, and environmental services saw 89 transactions YTD up 28.1% YoY with strategic deals running 15.0x-20.9x median -- the biggest multiple expansion of any sector (Capstone 2025). HVAC equipment 2025 median ran 10.9x EV/EBITDA and HVAC residential services hit 12.6x median in Q1 2025 with Blackstone paying 18.5x for the $2.5B Champions Group deal. Tax credit transfer market exceeded $20 billion in H1 2025 alone (2x H1 2024 pace) (Crux 2025 Mid-Year Market Intelligence) -- §45X and §48C transferability survived OBBBA intact. Goldman Sachs projects global data center power demand up 220% by 2030 vs 2023 with ~$720 billion in grid spending through 2030 (Goldman Sachs, 2026) -- the single biggest bullish driver for backup power, grid services, utility contracting, HVAC cooling, battery backup, and ESCO IS deals. Independent sponsors reached 26.8% of all closed deals on Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 IS Report). Below: 12 capital partners funding these deals, sub-sector multiples, OBBBA impact by sub-sector, and what cleantech capital partners actually need in your data room.

Why Is Cleantech & Energy Growing for Independent Sponsors in 2026?

Four structural forces converge in 2026 to make cleantech and energy one of the most legislatively compressed and structurally tailwind-heavy IS target sectors in the lower middle market -- and arguably the most sub-sector-sensitive, because the same "cleantech" label covers everything from terminated EV credits to preserved §45X tax credit transferability to AI-data-center-driven electrical services demand.

OBBBA's Partial IRA Repeal Creates a Compressed M&A Window

The One Big Beautiful Bill Act, signed July 4, 2025, executed a partial repeal of the Inflation Reduction Act with highly uneven sub-sector impact. EV credits §25E, §30D, and §45W terminated September 30, 2025 -- degrading economics for EV charging installers and fleet conversion businesses. Residential solar §25D expired December 31, 2025 -- compressing the M&A window for residential solar installers and driving a distressed-divestiture wave in 2026. §48E wind and solar construction credits are ineligible if construction begins after July 4, 2026 -- any platform with a project backlog needs a clean construction-start audit. §45X (advanced manufacturing production credit) phases down starting 2029 with wind components ineligible after 2027. But the survival clauses matter as much as the repeal clauses: §45X and §48C transferability SURVIVED OBBBA intact -- preserving the tax credit transfer market that cleared more than $20 billion in H1 2025 alone (2x H1 2024 pace per Crux Climate 2025 Mid-Year Market Intelligence) with projected full-year 2025 volume of $33-$40 billion. FEOC restrictions block Chinese-controlled supply chains and have driven reshoring plus US-supplier M&A. 100% bonus depreciation was reinstated, subsidizing capital-intensive infrastructure and incentivizing corporates to acquire operating renewables for tax-shield purposes. For an IS sourcing cleantech and energy deals, sub-sector selection is more important in 2026 than in any other vertical because OBBBA rewrote the pro forma for several sub-sectors in real time.

AI Data Center Electricity Demand Is the Dominant Bullish Driver

Goldman Sachs projects global data center power demand up 220% by 2030 versus 2023 -- an absolute demand curve step-change that flows downstream to backup power, grid services, utility contracting, HVAC cooling, battery backup, and ESCO businesses. US power demand is projected up 197% 2025-2030 to 95 GW capacity. Grid spending is projected at ~$720 billion through 2030, with the IEA base case showing global data center consumption doubling to ~945 TWh by 2030. This demand is non-discretionary: hyperscalers need backup diesel generators, battery energy storage, utility-scale transformers, ruggedized power conditioners (Industrial Growth Partners' SENS platform is the March 2025 reference), chilled-water HVAC systems, electrical contracting for DCE-tier buildouts, and utility-coordination services. Conventional thermal power M&A has resurged in parallel (Constellation/Calpine, Vistra/Cogentrix, Talen/PJM baseload transactions in 2024-2025) as hyperscalers contract directly with existing power generation. For an IS sourcing cleantech and energy deals in 2026, the AI data center tailwind is the single strongest end-market narrative -- and it is measurable in real deal activity at firms like Industrial Growth Partners, Bernhard Capital Partners, Argonaut, and Huron Capital.

Environmental Services Multiple Expansion Is the Biggest of Any Sector

Environmental services strategic deals in 2025 ran 15.0x to 20.9x EBITDA median per Capstone -- the biggest multiple expansion of any sector in 2025. Combined with 202 waste transactions worth $5.7 billion disclosed and 89 environmental services transactions YTD up 28.1% YoY, waste and environmental services is the single hottest LMM PE sub-sector in 2025-2026. Kinderhook Industries -- self-described as "an independent sponsor in the environmental services space" with 159 environmental and infrastructure services acquisitions since inception -- closed the $1.0 billion Ecowaste Solutions combination (Live Oak + CARDS Recycling) on January 16, 2026 (Goldman + Apollo S3 co-underwrote the transaction), $300M revenue, 400K customers, 600+ fleet. Nonantum Capital Partners' Momentum Environmental platform (Northeast/Mid-Atlantic non-discretionary waste, industrial cleaning, emergency response) added The Environmental Service Group in May 2025. For an IS targeting a $15M-$40M environmental services or waste platform, the multiple expansion is the upside case that generalist LMM PE cannot underwrite.

Critical Minerals and Supply Chain Services Gained a Government Backstop in 2025

The Pentagon became the largest shareholder of MP Materials in 2025 via a $1.4 billion public-private rare earth supply chain partnership -- $620M federal loan + $50M Commerce + $550M private. This is a new structural tailwind for critical minerals extraction, rare earth processing, battery material supply chains, and specialty metals distribution. Combined with FEOC restrictions blocking Chinese-controlled supply chains and reshoring-linked demand for domestic specialty chemical and industrial gas distribution, critical minerals and supply chain services is an emerging IS sub-sector with $500B+ in cumulative private capital catalyzed by transferable tax credits since 2022. For an IS sourcing a specialty chemical, industrial gas, or critical minerals services deal, capital partners with energy services fluency (Bernhard Capital Partners, Argonaut Private Equity) or industrial decarbonization fluency (Ara Partners) are the right sector fit.

Which 12 Capital Partners Fund Cleantech/Energy IS Deals in 2026?

Twelve capital partners actively fund cleantech and energy independent sponsor deals in 2026 across three roles: IS-explicit equity partners (Align Collaborate, Peninsula, Kinderhook, Nonantum), sector-specialist equity (Ara Partners, Bernhard Capital Partners, Argonaut Private Equity, Industrial Growth Partners), vertical adjacencies with deep HVAC/refrigeration/specialty distribution portfolios (Huron Capital, Saw Mill Capital), and SBIC/mezzanine providers (Tecum Capital, Argosy Private Equity). Every firm has been verified against 2024-2026 deal activity and check-size guidance. For data room setup ahead of capital partner outreach, Peony Data Room at $52/admin/month handles the cleantech-specific document mix (utility customer contracts, PPA schedules, tax credit transfer documentation, NERC/FERC compliance, Phase I and Phase II ESAs, NETA/NECA certifications, warranty exposure analyses) out of the box.

| Firm | Website | Check Size / EV | Fund (size, vintage) | Cleantech/Energy Focus |

|---|---|---|---|---|

| Align Collaborate | aligncollab.com | $10M-$30M equity | Fund I $233M (March 2025) | IS-EXCLUSIVE vehicle; Teague Electric, Right Angle |

| Peninsula Capital Partners | peninsulafunds.com | $2M-$30M | Fund VIII $400M (Sep 2025) | Junior capital, Trinity Electrical (Jan 2025) |

| Tecum Capital Partners | tecum.com | $5M-$20M | Fund IV $325M SBIC (Jul 2025) | Energy brokerage, waste mgmt (TPI, 5280) |

| Argosy Private Equity | argosycapital.com | LMM | SBIC VII $175M (2024 SBIC of Year) | Joliet Electric, Groome Industrial |

| Kinderhook Industries | kinderhook.com | Upper LMM / MM | Fund 8 $2.75B (Jun 2024) | 159 E&IS acquisitions; Ecowaste $1.0B Jan 2026 |

| Nonantum Capital Partners | nonantumcapital.com | LMM control | Fund II $575M (Jan 2022) | Momentum Environmental platform |

| Huron Capital | huroncapital.com | LMM | $1.8B AUM | HVAC ExecFactor (Exigent, Pueblo, Smith-Boughan) |

| Saw Mill Capital | sawmillcapital.com | $25M-$200M EV | Fund III $435M (Nov 2024) | Climate Pros, refrigeration, ARCXIS |

| Bernhard Capital Partners | bernhardcapital.com | MM-plus | Fund III + $530M Infra Fund | Pure-play energy services; SMSI, TechServ |

| Argonaut Private Equity | argonautpe.com | MM | Fund V $500M (Dec 2023) | Middle-America utility/energy contractors |

| Ara Partners | arapartners.com | Up to $300M equity | Fund III ~$3.0B + $800M Infra | Industrial decarbonization, >60% GHG reduction |

| Industrial Growth Partners | igpequity.com | $50M-$150M equity | Fund VI $1.2B (Aug 2022) | SENS (ruggedized power for data centers, grid) |

Tier 1 -- IS-Explicit Equity Partners with Active Cleantech/Energy Deals

These firms publicly position as IS partners, have IS-origin culture, or explicitly label themselves as independent sponsors in their sector positioning. Each has a verified 2024-2026 track record deploying capital into cleantech, environmental services, HVAC, electrical, or utility-services acquisitions in the lower middle market.

Align Collaborate

Website: aligncollab.com | Fund I: $233M final close March 26, 2025 (oversubscribed vs. $150M target) | HQ: Cleveland, OH + Dallas, TX

Align Collaborate runs an IS-exclusive investment vehicle -- Fund I closed at $233 million in March 2025, oversubscribed versus a $150 million target (Align Collaborate press, March 26, 2025). The firm publicly positions itself as wanting to be "Independent Sponsors' First Call" -- no other firm on this list is this explicit about IS-dedicated capital. Align writes $10M-$30M equity checks into targets with $2M-$15M EBITDA. 2024-2025 cleantech/energy deals include Teague Electric (2025 growth investment with IX Capital Partners as IS), Right Angle Partners Fire Protection (electrical + fire protection services), and the Rewind Restoration Platform (with LP First Capital as IS, acquired Icon Restoration).

Why it matters for IS: Align Collaborate is the single most IS-dedicated equity partner on this list. There is no fund mandate ambiguity -- Fund I exists to partner with independent sponsors. For a first-time or emerging IS sourcing a cleantech services, electrical, fire protection, or facility services deal at $5M-$15M EBITDA, Align Collaborate should be a first-call equity partner. The Cleveland + Dallas dual-hub structure gives them strong Midwest and Sun Belt sourcing coverage where most LMM cleantech deal flow originates.

Peninsula Capital Partners

Website: peninsulafunds.com | Fund VIII: $400M (closed September 2025) | Lifetime: $2.4B raised across 8 partnerships, 70+ IS platforms since 1995 | HQ: Southfield, MI

Peninsula Capital Partners is "the architect of a pioneering and unique investment program which focuses on providing mezzanine capital to non- and independently-sponsored transactions" per the firm's own positioning. Peninsula has backed 70+ independent sponsor platforms since 1995 -- the single deepest IS track record of any firm on this list. Fund VIII closed at $400 million in September 2025. Peninsula provides $2M-$30M checks in flexible junior capital -- mezzanine debt, preferred equity, and minority common equity -- with a $3M+ EBITDA minimum. January 2025 cleantech/energy deal: Trinity Electrical Services -- specialty electrical contracting IS buyout with Peninsula providing subordinated debt + common equity to the IS sponsor.

Why it matters for IS: Peninsula is the single most open-to-first-time-IS firm on this list. The firm's explicit IS-partner positioning and 70+ platform track record mean your cleantech services, electrical contracting, or utility services deal will not be the first IS transaction Peninsula has underwritten. For a first-time IS sourcing a $3M-$7M EBITDA cleantech or energy services deal, Peninsula is arguably the single most repeatable junior-capital source in the US lower middle market.

Kinderhook Industries

Website: kinderhook.com | Fund 8: $2.75B final close June 2024 (oversubscribed vs. $2.0B target) | Lifetime: 159 environmental and infrastructure services acquisitions since inception | HQ: New York, NY

Kinderhook Industries publicly self-describes as "an independent sponsor in the environmental services space" -- language used in the firm's own communications. Fund 8 closed at $2.75 billion in June 2024, oversubscribed versus a $2.0 billion target. Kinderhook has completed 159 environmental and infrastructure services acquisitions since inception, making it one of the most active E&IS consolidators in the US middle market. January 16, 2026 reference deal: Ecowaste Solutions $1.0 billion combination of Live Oak Environmental and CARDS Recycling -- $300M revenue, 400K customers, 600+ fleet vehicles, with Goldman Sachs and Apollo S3 co-underwriting the transaction.

Why it matters for IS: Kinderhook is the reference point for upper-LMM environmental and infrastructure services roll-ups. The Ecowaste Solutions transaction validates the waste and environmental services multiple-expansion thesis at scale, and the IS-style language in Kinderhook's own positioning signals cultural openness to sponsor partnerships on sub-platform deals. For an IS sourcing a $25M-$75M enterprise value environmental services, waste, or recycling platform, Kinderhook is either a co-invest partner or a reference exit target.

Nonantum Capital Partners

Website: nonantumcapital.com | Fund II: $575M (closed January 2022 at hard cap) | HQ: Boston, MA

Nonantum Capital Partners closed Fund II at $575 million in January 2022 at hard cap -- a specialist LMM buyout fund with explicit environmental services focus. Nonantum's flagship environmental services platform is Momentum Environmental -- a Northeast and Mid-Atlantic non-discretionary waste, industrial cleaning, and emergency response operator. May 2025 add-on: Momentum Environmental acquired The Environmental Service Group, extending the platform's industrial cleaning and emergency response footprint.

Why it matters for IS: Nonantum's Momentum Environmental platform is one of the most actively-expanded LMM environmental services roll-ups in the Northeast. For an IS sourcing a $15M-$40M environmental services or industrial cleaning deal in the Northeast, Mid-Atlantic, or Southeast US, Nonantum's operating depth and existing platform make them a credible co-invest or exit partner. The January 2022 Fund II hard-cap close signals disciplined deployment pace rather than opportunistic capital deployment -- a positive signal for IS partners who value follow-through on 3-to-4-year hold commitments.

Tier 2 -- Sector-Specialist Equity with Energy, Decarbonization, and Grid Fluency

These four firms are notable for pure-play or deep-vertical cleantech and energy specialization. Each has fund economics explicitly organized around cleantech, industrial decarbonization, energy services, or the AI-data-center-driven grid-spending tailwind.

Ara Partners

Website: arapartners.com | Fund III: ~$3.0B | Infrastructure Fund: $800M (final close May 2025, oversubscribed vs. $500M target) | AUM: $6.0B | HQ: Houston, TX + Dublin, Ireland

Ara Partners is the leading LMM industrial decarbonization specialist -- the firm targets assets delivering >60% greenhouse gas reduction versus incumbent alternatives and has built a concentrated portfolio of industrial decarbonization platforms. Fund III closed at approximately $3.0 billion and the $800 million Infrastructure Fund final-closed in May 2025, oversubscribed versus a $500 million target. Combined AUM reaches $6.0 billion. 2025-2026 deals include Microtec Development (glass-waste-to-pozzolan cement replacement -- direct decarbonization play on a hard-to-abate sector) and Sedron Technologies ($500M waste upcycling investment April 2026). Ara's check sizes can run up to $300M equity with Infrastructure Fund co-invest capacity.

Why it matters for IS: Ara is best as a follow-on equity partner for IS-sourced industrial decarbonization deals rather than a first-call IS partner -- Fund III is a large committed fund and Ara's typical platform size exceeds the IS sweet spot. But for an IS targeting an industrial decarbonization deal with >60% GHG-reduction economics (glass waste, concrete alternatives, hydrogen-adjacent, biogas, waste upcycling), Ara is the highest-fluency follow-on capital partner in the US LMM and a credible exit target at the platform-scale stage.

Bernhard Capital Partners

Website: bernhardcapital.com | Fund III: 2022 vintage | Infrastructure Fund: $530M | Gross AUM: ~$3.6B | HQ: Baton Rouge, LA

Bernhard Capital Partners is the only pure-play energy services private equity firm on this list. Combined gross AUM reaches ~$3.6 billion across Fund III (2022 vintage) and a $530M Infrastructure Fund. Bernhard operates a DOE technical consulting platform and has been highly active in utility and nuclear services. 2024-2025 deals include SMSI (nuclear/DOE services platform), TechServ (utility services platform, June 2025), and -- per late-2025 reporting -- advanced talks on Cleco Power (the reported transaction structure explicitly cites data center electricity demand, with Stonepeak as a co-investor in the Cleco Power conversation). Bernhard's LA + Gulf Coast + utility-sector sourcing network is uniquely dense.

Why it matters for IS: Bernhard's pure-play energy services positioning means their deal teams live and breathe utility contracting economics -- they underwrite utility customer concentration, NERC/FERC compliance, DOE prime contracting exposure, and nuclear technical services as core competencies rather than add-on expertise. For an IS sourcing a $20M-$75M utility services, nuclear services, or DOE-adjacent technical services platform, Bernhard reads teasers with sector fluency that generalist LMM firms cannot match. The Cleco Power + data center demand narrative is the cleanest example of AI-data-center-driven energy services M&A on this list.

Argonaut Private Equity

Website: argonautpe.com | Fund V: $500M (closed December 2023, above $400M target) | HQ: Tulsa, OK

Argonaut Private Equity runs a middle-America energy services and utility contractor portfolio with Fund V closed at $500 million in December 2023 above its $400M target. The Fund V portfolio explicitly concentrates on energy services and utility contracting: Bandera Utility Contractors (utility construction), Miller Contracting Services (utility services), Petroplex Acidizing (oil/gas services), Allstream Services & Rental (rental services), and Chemoil Energy Services (energy services).

Why it matters for IS: Argonaut is the single best capital partner fit for middle-America utility and energy services IS deals -- particularly utility construction contractors, specialty utility services, and energy services in Oklahoma, Texas, Louisiana, Kansas, and the broader Mid-Continent. For an IS sourcing a $10M-$30M EBITDA utility contractor, pipeline services, or energy services deal in Fund V's geographic wheelhouse, Argonaut is a credible lead or co-invest partner with deep local sourcing networks.

Industrial Growth Partners

Website: igpequity.com | Fund VI: $1.2B (August 2022) | Typical Check: $50M-$150M equity per platform | HQ: San Francisco, CA

Industrial Growth Partners closed Fund VI at $1.2 billion in August 2022 and deploys $50M-$150M typical platform equity. The March 2025 platform SENS -- the sixth Fund VI platform -- is the cleanest AI-data-center + grid-resilience play of any firm on this list. SENS makes ruggedized battery chargers and integrated power systems for data centers, hospitals, utilities, and telecom -- directly addressing the Goldman Sachs +220% data center power demand narrative.

Why it matters for IS: IGP's platform-size minimum ($50M+ equity) puts most IS deals outside their fund mandate, but the SENS platform explicitly targets the data center and grid-resilience sub-sector that is the strongest bullish narrative in cleantech 2026. For an IS sourcing a ruggedized power, backup generation, battery storage, or grid-services deal at $30M+ EBITDA, IGP's SENS platform is a reference exit target and IGP itself is a credible follow-on capital partner at the platform-scale stage.

Tier 3 -- Vertical Adjacencies: HVAC, Refrigeration, Specialty Services

These two firms have deep portfolios in HVAC, refrigeration, and specialty services -- vertical-adjacent to cleantech and energy and directly exposed to the AI-data-center HVAC-cooling tailwind and the environmental services multiple expansion.

Huron Capital

Website: huroncapital.com | AUM: $1.8B | HQ: Detroit, MI

Huron Capital manages $1.8 billion AUM through a Flex Equity strategy and its ExecFactor® operating-partner model. Huron's HVAC and energy efficiency services platforms include The Exigent Group (commercial HVAC/mechanical services, 2022 platform), Pueblo Mechanical (HVAC services, 2017 platform), and Smith-Boughan Mechanical + Premier Mechanical add-ons (2024-2025). The ExecFactor model pairs operating-partner executives with portfolio platforms to drive operational transformation.

Why it matters for IS: Huron's HVAC and mechanical services portfolio depth is the strongest of any firm on this list -- and the AI-data-center HVAC-cooling tailwind is one of the clearest structural narratives in cleantech 2026. For an IS sourcing a $10M-$30M commercial HVAC, mechanical services, or energy efficiency services platform, Huron's operating-partner model and platform consolidation track record make them a credible co-invest or exit partner. The ExecFactor cultural fit is strong for operator-led IS sponsors who want an institutional partner that values operational execution over financial engineering.

Saw Mill Capital

Website: sawmillcapital.com | Fund III: $435M (closed November 4, 2024, oversubscribed) | HQ: Briarcliff Manor, NY

Saw Mill Capital closed Fund III at $435 million in November 2024, oversubscribed (PR Newswire, November 4, 2024). The firm's cleantech and energy-adjacent platforms include Climate Pros (commercial refrigeration and HVAC services -- directly exposed to grocery, cold chain, and data-center-adjacent HVAC-cooling demand), Industrial Refrigeration Pros (ammonia and CO2 cold-chain decarbonization services), and ARCXIS (environmental test equipment and waste services). Saw Mill takes control equity positions with enterprise values of $25M-$200M.

Why it matters for IS: Saw Mill's specialty refrigeration and environmental services depth is directly adjacent to two of the four structural tailwinds in this guide -- AI data center HVAC-cooling demand (Climate Pros) and cold-chain decarbonization (Industrial Refrigeration Pros). Fund III's oversubscription in late 2024 signals aggressive 2025-2026 deployment appetite. For an IS sourcing a $10M-$25M EBITDA commercial refrigeration, HVAC/mechanical, or environmental test equipment platform, Saw Mill is a credible lead equity co-invest partner with vertical-specific underwriting fluency.

Tier 4 -- SBIC / Mezz / Sub-Debt with Cleantech and Energy Allocation

SBICs and mezzanine providers fill the debt side of cleantech IS capital stacks. Two of the most cleantech-active SBIC and mezzanine capital partners -- both with verified 2025 cleantech/energy IS deals.

Tecum Capital Partners

Website: tecum.com | Fund IV: $325M SBIC (SBA approval July 2025 -- fourth SBIC license) | HQ: Pittsburgh, PA

Tecum Capital's fourth SBIC fund received SBA approval in July 2025 at $325 million+ (PR Newswire, July 2025). The firm provides mezzanine debt and minority equity of $5M-$20M in businesses with EBITDA greater than $3M. Tecum's IS posture is explicit: the firm "partners with independent sponsors, family offices, committed funds, business owners seeking succession plans" and has "witnessed the rapid expansion of independent sponsors" with ongoing partnership activity. Two confirmed 2025 cleantech/energy IS deals: (1) TPI Efficiency (April 8, 2025) -- Cleveland-based energy brokerage and sustainability consulting platform, Tecum partnered with ScaleCo Capital; TPI subsequently acquired The Utilities Group. (2) 5280 Waste Solutions (April 9, 2025) -- Denver waste management majority recap, Tecum partnered with Laurel Mountain Partners (the Kendall Family Office) plus Comerica providing senior. Tecum is a McGuireWoods Independent Sponsor Conference sponsor.

Why it matters for IS: Tecum's IS-partner positioning, McGuireWoods IS sponsorship, and two confirmed April 2025 cleantech/energy IS deals make them a first-call mezz partner for cleantech IS sponsors. The $3M+ EBITDA target matches the IS sweet spot perfectly, and the fresh Fund IV SBA approval in July 2025 signals elevated 2025-2026 deployment capacity. For an IS sourcing a $15M-$30M energy services, waste management, environmental services, or utility services deal, Tecum is the reference mezz partner with cleantech-specific underwriting experience.

Argosy Private Equity

Website: argosycapital.com | SBIC VII: $175M (active, 2024 SBA SBIC of the Year -- Established Manager) | Firm AUM: $3.4B | HQ: Wayne, PA

Argosy Private Equity is the 2024 SBA SBIC of the Year (Established Manager) (SBIA, May 2024) and deploys SBIC VII at $175M. The firm manages $1.2B+ AUM across 7 SBIC funds and has completed 140+ platform investments since inception. Energy services exits 2024-2025 include Joliet Electric Motors (sold to Hitachi -- the platform pivoted to electric fracking during the hold, a reference example of energy-transition value creation) and Groome Industrial (natural gas power generation and refineries services -- delivered 900%+ EBITDA growth during the Argosy hold).

Why it matters for IS: Argosy's SBIC VII plus 140+ platform track record plus the Joliet Electric (Hitachi exit) and Groome Industrial (900%+ EBITDA growth) references make them a credible SBIC partner for cleantech and energy IS deals with energy-transition upside. Argosy's 2024 SBIC of the Year designation is industry-wide validation of underwriting quality. For an IS sourcing a $10M-$30M EBITDA specialty electrical, energy services, or power-services platform, Argosy is a reference SBIC partner with documented energy-transition value creation.

How Are Cleantech & Energy IS Deals Priced in 2026?

Cleantech and energy multiples vary more than any other IS sector because the category spans environmental services (multiple expansion at 15.0x-20.9x strategic), HVAC (10.9x-18.5x for Blackstone's Champions Group deal), solar services (compressed window before §25D and §48E cliffs), utility contracting, industrial decarbonization, and OBBBA-impacted sub-sectors. The 2025-2026 ranges we see on Peony data rooms and in published market data:

| Sub-sector | Revenue multiple | EBITDA multiple |

|---|---|---|

| Environmental services strategic deals (2025) | -- | 15.0x-20.9x EBITDA (Capstone 2025 -- biggest multiple expansion of any sector) |

| HVAC equipment median 2025 | -- | 10.9x EV/EBITDA (up from 9.0x in 2024) |

| HVAC residential services (Q1 2025) | -- | 12.6x median; Blackstone paid 18.5x for $2.5B Champions Group |

| Tuck-in HVAC add-ons | -- | 3x-8x (multiple-arbitrage) |

| Waste and recycling LMM platforms | -- | 7x-11x EBITDA (202 transactions, $5.7B disclosed 2025) |

| Solar installation services (OBBBA window) | -- | 6x-8x EBITDA (vs. 8x-12x+ for operational assets) |

| Utility services and electrical contracting | -- | 7x-10x EBITDA |

| Nuclear services / DOE technical consulting | -- | 8x-12x EBITDA |

| Industrial decarbonization platforms | -- | 10x-14x EBITDA (proven assets) |

| Backup power / grid resilience / data center | -- | 9x-13x EBITDA (IGP's SENS reference) |

| EV charging installer (degraded post-OBBBA) | -- | 5x-7x EBITDA (down from 8x-10x pre-OBBBA) |

| Overall energy/natural resources M&A value 2025 | -- | $333.7B total (+31.3% YoY per KPMG) |

Roll-up math for HVAC and environmental services platforms: Acquire add-ons at 3x-8x EBITDA for tuck-in scale, integrate into a regional platform, exit at 10.9x-20.9x EBITDA as a strategic target. This is the arbitrage that drives HVAC and environmental services consolidation in 2025-2026 and the 3x-to-18.5x multiple expansion band (Blackstone's Champions Group 18.5x deal is the reference ceiling) is the core value creation lever for IS sponsors.

Warranty exposure is the single biggest price-chip source in cleantech services diligence. Cleantech services targets with prior installation work (solar, HVAC, electrical, mechanical) carry warranty reserves that can move 3-7% of enterprise value. Capital partners expect 24 months of rolling warranty claim data, an explicit reserve for open claims, and a clear separation between warranty exposure and operational service obligations. For a $25M enterprise value deal, a $1.5M warranty reserve miss is 6% of EV.

OBBBA tax credit eligibility is the new diligence axis. Any target with exposure to §25E, §30D, §45W, §25D, §48E, §45X, or §48C needs documented construction-start dates, FEOC compliance attestations, and tax credit transfer documentation. An IS sourcing a residential solar platform needs to model the §25D cliff (December 31, 2025 expiration) and any §48E exposure (construction-start cutoff July 4, 2026) in the pro forma. Missing this analysis is a deal-killer in 2026.

Three IS-Backed Cleantech & Energy Deals That Closed in 2025-2026 (Reference Case Studies)

Three recent closed deals illustrate how cleantech and energy IS capital stacks get assembled in practice. Each pairs a specific sponsor with specific capital partners and specific deal economics -- useful reference architecture for IS sponsors planning their own capital raises.

Deal 1: Independent Sponsor Acquires Trinity Electrical Services (January 2025)

In January 2025, an independent sponsor acquired Trinity Electrical Services -- a specialty electrical contractor in rural Georgia. The capital stack: Peninsula Capital Partners provided subordinated debt plus common equity to the IS sponsor. This is a canonical IS-origin stack for specialty electrical contracting in 2026 -- Peninsula's 70+ IS platforms since 1995 is the single deepest IS track record in the LMM, and specialty electrical contracting sits at the intersection of the grid-spending tailwind ($720B through 2030) and the compressed post-OBBBA M&A window. Trinity's rural Georgia geography is representative of middle-America founder-led electrical services deals -- the highest-probability proprietary sourcing pool in 2026.

Deal 2: Laurel Mountain Partners (Kendall Family Office IS) Acquires 5280 Waste Solutions (April 9, 2025)

On April 9, 2025, Laurel Mountain Partners (the Kendall Family Office running IS deals) closed a majority recap of 5280 Waste Solutions -- a Denver waste management operator. The capital stack: Laurel Mountain Partners as sponsor + Tecum Capital Partners providing mezzanine + Comerica providing senior cash-flow lending. This transaction is a template for family-office-backed IS deals in environmental services -- the sector with the biggest multiple expansion of any in 2025 (15.0x-20.9x strategic). Tecum's Fund IV SBIC approval in July 2025 added fresh capacity for more deals like this one, and the Laurel Mountain structure (family office operating as IS) is one of the most common IS structures for cleantech and energy deals.

Deal 3: Kinderhook Industries Closes Ecowaste Solutions $1.0 Billion Combination (January 16, 2026)

On January 16, 2026, Kinderhook Industries closed the $1.0 billion Ecowaste Solutions combination of Live Oak Environmental and CARDS Recycling -- $300M revenue, 400K customers, 600+ fleet vehicles across the combined platform. Goldman Sachs and Apollo S3 co-underwrote the transaction. Kinderhook publicly describes itself as "an independent sponsor in the environmental services space" and has completed 159 environmental and infrastructure services acquisitions since inception. This transaction is a reference scale-up example -- Ecowaste Solutions is now one of the largest non-municipal integrated waste and recycling platforms in the US, and the $1.0B deal size validates the strategic-multiple-expansion thesis at scale.

Pattern recognition across all three deals: (1) each stack paired an IS or IS-style sponsor with 1-2 institutional capital partners plus a senior or subordinate lender; (2) each targeted a cleantech or energy services business in a defined sub-sector (specialty electrical, waste management, environmental services); (3) each closed within a 13-month window signaling real 2025-2026 deal velocity; (4) capital partners involved in these deals (Peninsula, Tecum, Kinderhook) are all on the 12-firm list above with verified IS-partnership track records.

What Due Diligence Do Cleantech Capital Partners Expect in 2026?

Cleantech and energy diligence is structurally different from manufacturing or distribution diligence because the assets are licenses, certifications, utility contracts, warranty exposure, and tax credit eligibility -- and the risks are utility and municipal customer concentration, warranty claims, NERC/FERC compliance, environmental liability, and OBBBA sub-sector exposure. Based on hosting hundreds of cleantech IS data rooms on Peony, here is what 2026 capital partners expect -- organized for the staged diligence approach in our complete IS guide and IS data room checklist. Set up your data room on day one of the exclusivity window.

Customer Concentration with Utility/Municipal/Commercial/Industrial Breakdown

Top-20 customer concentration with utility, municipal, commercial, and industrial buckets is the single most scrutinized schedule in cleantech services diligence. Capital partners expect the customer name (even under NDA), revenue share across trailing 3 fiscal years, contract term and remaining tenor, change-of-control language, RFP renewal cycle, and assignability provisions. Utility and municipal customers have materially different concentration risk profiles than commercial customers -- long-term contracts with predictable renewal windows versus shorter-term discretionary commercial spend. Any single customer above 20% of revenue is a material concentration issue; above 15% requires mitigation.

Tax Credit Eligibility and Transferability Documentation

OBBBA's partial IRA repeal makes tax credit documentation the new diligence axis. Capital partners expect documented eligibility letters for §45X (advanced manufacturing production credit, surviving transferability), §48C (advanced energy project credit, surviving transferability), §48E (wind/solar construction credit, construction-start cutoff July 4, 2026), and where applicable §25D (expired December 31, 2025 -- distressed-divestiture exposure), §25E/§30D/§45W (terminated September 30, 2025 -- degraded EV economics). Any platform with construction backlog exposure to §48E needs a clean construction-start audit. FEOC (Foreign Entity of Concern) compliance attestations are required post-OBBBA. Tax credit transfer documentation (Crux-cleared or bilateral) with counterparty identities and pricing is expected.

Warranty Exposure Analysis

Warranty exposure is often the largest working-capital adjustment in cleantech services diligence. Capital partners expect 24 months of rolling warranty claim data, an explicit reserve for open claims organized by product/project, a walk-forward of the warranty reserve from opening to closing balance, root-cause analysis for any repeated failure modes, and a clear separation between warranty exposure and ongoing service/maintenance obligations. For solar installation, HVAC mechanical, and electrical contracting targets, the warranty reserve can move 3-7% of enterprise value.

NERC/FERC Compliance and Utility Coordination

For any target with generation, transmission, or distribution-adjacent operations, capital partners expect NERC (North American Electric Reliability Corporation) compliance records, FERC (Federal Energy Regulatory Commission) filings where applicable, interconnection agreements for any generation assets, PPA (power purchase agreement) schedules with remaining term, escalators, and curtailment history, and utility coordination audit records. For ESCO (energy service company) targets, capital partners also expect measurement and verification (M&V) protocols, performance guarantee documentation, and savings attribution methodologies.

Licensure and Certification Stack

Cleantech services targets carry a stack of trade licenses, specialty certifications, and regulatory registrations that must be documented. Capital partners expect journeyman and master electrician licenses by state, HVAC mechanical licenses by state, plumbing licenses where applicable, NETA (National Electrical Testing Association) certifications for electrical testing and commissioning work, NECA (National Electrical Contractors Association) affiliations, NFPA (National Fire Protection Association) certifications for fire protection work, EPA 608 universal certifications for HVAC refrigerant handling, and EPA RCRA (Resource Conservation and Recovery Act) handler permits for any hazardous waste operator. Missing or expired certifications surface in diligence and require cure before close.

Environmental and Compliance

Cleantech services facilities -- particularly those with legacy fuel storage, battery storage, chemical inventory, or outdoor waste operations -- face environmental exposure. Capital partners expect Phase I ESAs on every owned facility and Phase II where Phase I flags (soil, groundwater, UST, AST). Logistics targets face DOT compliance, driver qualification files, hours-of-service audits, and CSA scores. Hazardous waste operators face RCRA, CERCLA, and DOT hazmat compliance. Any prior OSHA recordables, workers-comp claims, or EPA enforcement actions surface in diligence and require remediation disclosure.

For the complete due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes all of these cleantech-specific documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is utility customer concentration by contract term?" or "Which top-20 vendors have change-of-control provisions?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. The AI redaction feature identifies utility customer names, PPA pricing, EPC subcontract terms, and tax credit transfer pricing across uploaded documents before you share with capital partners, a workflow that Datasite charges $25K+ per deal to configure manually.

Where Do Cleantech/Energy IS Sponsors Meet Capital Partners in 2026?

Cleantech and energy IS outreach has a different rhythm than tech or distribution. The best sourcing happens at a mix of IS-specific conferences and cleantech/energy-operator events where targets (family-owned HVAC operators, environmental services operators, utility contractors) congregate alongside capital partners. Events happening AFTER April 24, 2026:

| Event | Date | Location | Organizer |

|---|---|---|---|

| ACG DealMAX (InterGrowth rebrand) | April 27-29, 2026 | Las Vegas | ACG Global |

| SBIA Independent Sponsor Forum | May 6, 2026 | Sheraton Philadelphia Downtown | SBIA |

| WasteExpo | May 2026 | Las Vegas | Waste360 |

| iGlobal Independent Sponsor Summit Dallas | June 11, 2026 | Dallas | iGlobal Forum |

| DistribuTECH International | Q1/Q2 2026 | Dallas (TBC) | Clarion |

| RE+ (Solar + Storage + Smart Energy Week) | September 2026 | Las Vegas | SEIA / SEPA |

| iGlobal Independent Sponsor Summit NYC | September 28-29, 2026 | New York | iGlobal Forum |

| AHR Expo | TBC 2026 | TBC | AHRI + ASHRAE |

| McGuireWoods Independent Sponsor Conference | October 27-28, 2026 | Fairmont Dallas (1,600+ attendees) | McGuireWoods |

| iGlobal IS Summit West Coast | October 29-30, 2026 | Los Angeles | iGlobal Forum |

For cleantech and energy IS sponsors specifically, the two highest-leverage events are ACG DealMAX (April 27-29) -- the largest LMM dealmaking conference anchoring Q2 capital partner meetings -- and the McGuireWoods Independent Sponsor Conference (October 27-28) -- the single largest dedicated IS event with 1,600+ attendees and strong cleantech/energy capital-partner representation. RE+ is the most concentrated target-source event for utility-scale solar, storage, and smart energy operators (founders, project developers, EPCs all congregate). WasteExpo is the most concentrated event for environmental services, waste management, and recycling operator sourcing. AHR Expo is the most concentrated event for HVAC operator relationships. DistribuTECH is the most concentrated event for utility contractor and grid services sourcing. For our full IS conferences and forums guide covering 21 events in 2026, see the cluster.

Axial-platform IS deal flow: Independent sponsors closed 26.8% of all deals on Axial YTD 2025. Repeat capital partner relationships account for 59% of IS deals according to Citrin Cooperman 2025. For an IS building a 5-to-10 firm capital partner rolodex focused on cleantech and energy, the fastest path is one IS-explicit equity partner (Align Collaborate, Peninsula, or Kinderhook) + one sector-specialist (Ara Partners for decarbonization, Bernhard for pure-play energy services, or Huron for HVAC) + one SBIC (Tecum or Argosy) + one vertical adjacency (Saw Mill for refrigeration or Nonantum for environmental services).

Use Peony's page-level analytics to track which capital partners are reading the utility customer concentration analysis and tax credit eligibility documentation versus skimming the CIM. The ones who spend 20+ minutes on the Q of E and warranty exposure analysis are the ones worth second meetings. Use personalized sharing links so every capital partner gets a distinct tracking URL, and NDA gates so nobody sees confidential utility customer lists or PPA pricing until they sign -- something DocSend cannot detect on any plan.

Cleantech & Energy IS Deals By the Numbers

- Energy, natural resources, and chemicals M&A 2025: $333.7 billion in deal value, up 31.3% year-over-year with 1,029 transactions (-9.7% YoY) (KPMG Energy M&A 2025)

- Waste and recycling 2025: 202 transactions, $5.7 billion disclosed value, 54 PE add-ons (Capstone 2025)

- Environmental services 2025: 89 transactions YTD, up 28.1% YoY, with strategic deals running 15.0x-20.9x median -- the biggest multiple expansion of any sector (Capstone 2025)

- Solar 2025: $22.2 billion corporate funding, $3.5 billion VC + PE across 75 deals (Mercom Capital 2025)

- Climate tech VC 2025: $42.2 billion deployed globally (flat YoY) (PitchBook Climate Tech 2025)

- HVAC equipment 2025 median: 10.9x EV/EBITDA (up from 9.0x in 2024) (Capstone 2025)

- HVAC residential services Q1 2025: 12.6x median with Blackstone paying 18.5x for the $2.5 billion Champions Group deal

- Tuck-in HVAC: 3x-8x EBITDA (multiple-arbitrage plays)

- Tax credit transfer market H1 2025: more than $20 billion (2x H1 2024 pace); projected full-year 2025: $33-$40 billion (Crux 2025 Mid-Year Market Intelligence)

- Cumulative private capital catalyzed by transferable tax credits since 2022: $500 billion+

- Global data center power demand projected up 220% by 2030 versus 2023 (1,350 TWh); US up 197% 2025-2030 to 95 GW capacity; grid spending ~$720 billion through 2030 (Goldman Sachs, 2026)

- IEA base case: global data center consumption doubles to ~945 TWh by 2030

- Pentagon became largest shareholder of MP Materials in 2025 via $1.4 billion public-private rare earth supply chain partnership ($620M federal loan + $50M Commerce + $550M private)

- 54% of IS transactions closed at 4x-6x EBITDA in 2024-2025 (Citrin Cooperman 2025 IS Report)

- 59% of IS capital partner deals come from repeat relationships (Citrin Cooperman 2025)

- Independent sponsors reached 26.8% of all closed deals on Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 Independent Sponsor Report)

- PE dry powder sits at approximately $3.7 trillion globally at the start of 2026 (S&P Global, December 2025)

- PE-backed add-ons reached 75.9% of all buyouts in Q2 2025 (PitchBook Q2 2025 US PE Breakdown)

How Peony Fits the Cleantech/Energy IS Workflow

Peony is a data room platform purpose-built for the exact workflow cleantech and energy IS sponsors run: multiple simultaneous deals during roll-up phases, heavy document diligence (utility customer contracts, PPA schedules, tax credit transfer documentation, NERC/FERC compliance records, Phase I and Phase II ESAs, NETA/NECA certifications, warranty exposure analyses), and capital partner engagement tracking. Peony Data Room at $52/admin/month is the plan cleantech IS sponsors use.

AI auto-indexing organizes utility contracts, PPA agreements, tax credit transfer documentation, NERC/FERC compliance files, Phase I ESAs, licensure records, and warranty exposure schedules into a professional folder structure in under 3 minutes. Junior analysts spend 2-3 hours on this same workflow in Datasite.

Page-level analytics tell you which capital partner spent 30 minutes on the Q of E versus skimmed the CIM, and which one lingered on the tax credit eligibility analysis versus flipped through it. DocSend gives you deck-level views; Peony gives you page-by-page engagement so you know who is genuinely diligencing versus pattern-matching.

Smart Q&A lets counterparties submit diligence questions where AI drafts answers by surfacing the exact document sections and page citations. Your team approves every response before it ships, and every Q&A exchange is audit-trailed. For cleantech diligence where questions like "What is utility customer concentration by contract term?" or "Which projects have §48E construction-start exposure?" come in from every capital partner, this workflow compounds across 3-to-6 simultaneous deals.

AI redaction identifies utility customer names, PPA pricing schedules, EPC subcontract terms, and tax credit transfer pricing across uploaded documents before capital partners see them -- a feature Datasite charges $25K+ per deal to configure manually.

Screenshot protection blocks and logs screen-capture attempts on sensitive files. Dynamic watermarks embed viewer identity on every frame of every document, which cleantech capital partners require before reviewing utility customer lists, PPA pricing schedules, or confidential EPC subcontract terms.

NDA gates require signature before any materials are visible -- DocSend cannot detect this on any plan. AI document extraction lets capital partners ask "What is gross margin by service line?" and get a cited answer. E-signatures close the loop after conference introductions -- capital partners sign the NDA and access materials in a single workflow.

Unlimited data rooms on Peony Data Room mean an IS running 4-to-8 simultaneous cleantech deals during a roll-up phase does not pay per-deal licensing. An IS running three cleantech deals per year pays roughly $624 annually on Peony Data Room versus $45,000-$150,000 on legacy platforms. The free tier is the entry point; Peony Data Room at $52/admin/month is where serious IS workflows run.

For deeper context on private equity co-investment structures, M&A deal process, due diligence expectations, and fundraising best practices, see our dedicated solutions guides.

Quick Guide: Match Your Situation to the Right Capital Partner

| Situation | Best CP Fit | Why |

|---|---|---|

| First-time IS, $15M EV specialty electrical contractor, $2.5M EBITDA | Peninsula Capital Partners + Tecum (mezz) | Peninsula's 70+ IS-platform track record and Trinity Electrical reference; Tecum's value-add focus + SBIC Fund IV fresh capacity |

| First-time IS, $18M EV environmental services operator, $3M EBITDA | Nonantum Capital Partners + Peninsula (mezz) | Nonantum's Momentum Environmental platform template; Peninsula's first-time-IS openness and junior-capital depth |

| Experienced IS, $35M EV HVAC roll-up platform, $5M EBITDA | Huron Capital + Tecum (mezz) | Huron's ExecFactor HVAC platforms (Exigent, Pueblo, Smith-Boughan); Tecum's cleantech IS track record |

| Operating-partner IS, $50M EV commercial refrigeration platform, $8M EBITDA | Saw Mill Capital + Argosy (mezz) | Saw Mill's Climate Pros + Industrial Refrigeration Pros depth; Argosy SBIC VII with energy-services track record |

| First-time IS, $12M EV fire protection + electrical services, $3M EBITDA | Align Collaborate + Peninsula (mezz) | Align's IS-exclusive Fund I + Right Angle Partners Fire Protection reference; Peninsula's flexible junior capital |

| Experienced IS, $75M EV waste management platform, $10M EBITDA | Kinderhook Industries (exit target) + Tecum (mezz) | Kinderhook's Ecowaste Solutions $1.0B template as exit target; Tecum's 5280 Waste Solutions April 2025 reference |

| Operating-partner IS, $40M EV utility services platform, $6M EBITDA | Argonaut Private Equity + Tecum (mezz) | Argonaut's Bandera Utility Contractors + Miller Contracting Services portfolio; Tecum's value-add mezz |

| Experienced IS, $60M EV nuclear/DOE technical services, $8M EBITDA | Bernhard Capital Partners + Peninsula (mezz) | Bernhard's SMSI platform + pure-play energy services fluency; Peninsula's flexible junior capital |

| First-time IS, $10M EV energy efficiency services, $2M EBITDA (pre-LMM) | Align Collaborate + Peninsula (mezz) | Align's IS-exclusive mandate; Peninsula's first-time-IS openness |

| Experienced IS, $100M+ EV industrial decarbonization platform, $15M+ EBITDA | Ara Partners (follow-on) + Kinderhook | Ara's Fund III + $800M Infrastructure Fund industrial-decarbonization mandate; Kinderhook's environmental services depth |

| First-time IS, $18M EV commercial HVAC/mechanical, $3M EBITDA | Huron Capital + Argosy (mezz) | Huron's ExecFactor HVAC platform consolidation track record; Argosy's 2024 SBIC of the Year mezz |

| Operating-partner IS, $30M EV data center backup power platform, $4M EBITDA | Industrial Growth Partners (co-invest) + Tecum | IGP's SENS platform (ruggedized power for data centers, grid, utilities, telecom -- the cleanest AI-data-center play); Tecum's cleantech IS track record |

Bottom Line

Cleantech and energy is the #5 IS sector in 2026 behind manufacturing, healthcare, tech/software, and distribution -- but arguably has the most legislatively compressed and structurally sub-sector-sensitive M&A window of any vertical given OBBBA's July 2025 partial IRA repeal, AI data center electricity demand driving $720B in grid spending through 2030, and the biggest strategic-deal multiple expansion of any sector in 2025 (environmental services at 15.0x-20.9x per Capstone). Sub-sector selection matters more here than in any other IS vertical because OBBBA rewrote the pro forma for residential solar, EV charging, and wind/solar construction in real time while leaving §45X and §48C transferability intact.

If you are targeting environmental services, waste, or recycling: Kinderhook Industries (Fund 8 $2.75B with 159 E&IS acquisitions and the Ecowaste Solutions $1.0B January 2026 reference), Nonantum Capital Partners (Momentum Environmental platform), and Saw Mill Capital (ARCXIS environmental test equipment) are the most active equity co-invest partners. Expect multiple expansion to continue through 2026 -- the 15.0x-20.9x strategic medians set a high ceiling.

If you are targeting HVAC, commercial refrigeration, or energy efficiency services: Huron Capital (ExecFactor platforms including The Exigent Group, Pueblo Mechanical, Smith-Boughan Mechanical, Premier Mechanical) and Saw Mill Capital (Climate Pros, Industrial Refrigeration Pros) are the most active equity partners. The AI-data-center HVAC-cooling tailwind plus 12.6x median residential services multiples (Blackstone paid 18.5x for Champions Group) set the upside case.

If you are targeting electrical contracting, utility services, or grid resilience: Align Collaborate (Teague Electric, Right Angle Partners Fire Protection -- IS-exclusive Fund I $233M), Bernhard Capital Partners (pure-play energy services with SMSI and TechServ), Argonaut Private Equity (middle-America utility contractors), and Industrial Growth Partners (SENS platform -- the cleanest AI-data-center play) are the most sector-fluent partners. Grid spending of $720B through 2030 is the strongest structural tailwind in cleantech 2026.

If you are targeting industrial decarbonization: Ara Partners is the leading LMM specialist (Fund III ~$3.0B + $800M Infrastructure Fund May 2025, >60% GHG-reduction mandate, Microtec and Sedron references). Most Ara deals exceed the IS sweet spot, but they are a credible follow-on partner or exit target at platform scale.

If you need mezzanine or subordinated debt: Peninsula Capital Partners (Fund VIII $400M September 2025, 70+ IS platforms since 1995 -- the deepest IS track record on this list, Trinity Electrical January 2025 reference) and Tecum Capital Partners (Fund IV $325M SBIC July 2025, two confirmed April 2025 cleantech IS deals -- TPI Efficiency and 5280 Waste Solutions) provide flexible capital structures tailored to cleantech IS stacks. Argosy Private Equity (SBIC VII, 2024 SBA SBIC of the Year, Joliet Electric Hitachi exit + Groome Industrial 900%+ EBITDA growth) is the reference SBIC for energy-transition value creation. Peninsula is the single most open-to-first-time-IS firm on this list -- if you are running your first cleantech deal, make Peninsula your first call.

For every cleantech IS deal: Set up your data room on day one of the exclusivity window. Cleantech diligence is license-heavy and tax-credit-sensitive (top-20 utility/municipal/commercial/industrial customer breakdown, tax credit eligibility documentation for §45X/§48C/§48E, FEOC compliance attestations, NERC/FERC compliance records, Phase I and Phase II ESAs, licensure stack across journeyman/master electrician/HVAC/plumbing, NETA/NECA/NFPA/EPA 608/RCRA certifications, and 24 months of warranty claim data) -- capital partners expect the data room to be organized and complete at Week 1 of exclusivity. You cannot afford to lose days to VDR setup. Peony lets you build a complete cleantech IS data room in under 5 minutes, with page-level analytics that show which capital partners are reading the tax credit eligibility analysis versus skimming the CIM, AI-powered Smart Q&A that surfaces hard answers with page citations so capital partners complete diligence faster, and NDA gates that prevent any capital partner from seeing utility customer lists or PPA pricing before signing.

Peony Data Room at $52/admin/month includes AI auto-indexing, AI-powered Smart Q&A, AI redaction, dynamic watermarks, screenshot protection, NDA gates, page-level analytics, AI document extraction, and e-signatures. An IS running three cleantech deals per year pays roughly $624 annually versus $45,000-$150,000 on legacy platforms. When your exclusivity clock is ticking and five capital partners need to get comfortable with the cleantech deal simultaneously, every hour matters.

Set up your first cleantech or energy IS data room -- see plans and pricing.

Frequently Asked Questions

I am a first-time IS with a signed LOI on a $10M EBITDA cleantech services platform -- which capital partners fund cleantech/energy independent sponsor deals?

Cleantech and energy independent sponsor deals are funded by three capital partner types: IS-explicit equity funds like Align Collaborate (IS-exclusive Fund I, $233M final close March 2025), Kinderhook Industries (self-described "independent sponsor in the environmental services space," Fund 8 $2.75B June 2024), Peninsula Capital Partners (70+ IS platforms since 1995, Fund VIII $400M September 2025), and Nonantum Capital Partners (Fund II $575M January 2022); sector-specialist equity like Ara Partners (industrial decarbonization, Fund III $3.0B + $800M Infrastructure Fund May 2025), Bernhard Capital Partners (pure-play energy services, ~$3.6B gross AUM), Argonaut Private Equity (middle-America energy services, Fund V $500M December 2023), Industrial Growth Partners (ruggedized power + data center backup, Fund VI $1.2B August 2022), and vertical adjacencies Huron Capital (HVAC/ExecFactor platforms, $1.8B AUM) plus Saw Mill Capital (commercial refrigeration, Fund III $435M November 2024); and SBIC or mezzanine providers including Tecum Capital (Fund IV $325M SBIC July 2025) and Argosy Private Equity (SBIC VII $175M, 2024 SBA SBIC of the Year). For a first-time IS on a $10M EBITDA cleantech services platform, a $4M-$6M check from Tecum or Argosy plus a lead equity partner like Align Collaborate, Nonantum, or Huron is the typical stack. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the top-20 utility customer contracts, PPA agreements, EPC subcontracts, tax credit transfer documentation, and Phase I ESAs in under 3 minutes -- so the data room is ready before the first capital partner call.

I run corp dev at a mid-market PE firm -- what EBITDA multiples do cleantech/energy IS deals trade at in 2026?

Cleantech and energy IS deals in 2026 trade across a wide range by sub-sector: HVAC equipment 2025 median runs at 10.9x EV/EBITDA (up from 9.0x in 2024 per Capstone), HVAC residential services Q1 2025 median hit 12.6x EBITDA (Blackstone paid 18.5x for the $2.5B Champions Group deal), tuck-in HVAC runs 3x to 8x for multiple-arbitrage plays, environmental services strategic deals in 2025 ran 15.0x to 20.9x median (the biggest multiple expansion of any sector per Capstone), solar installation services trade at 6x to 8x EBITDA versus 8x to 12x+ for operational assets, utility and electrical services platforms trade at 7x to 10x EBITDA, waste and recycling LMM platforms run 7x to 11x EBITDA (with 202 transactions and $5.7B disclosed value in 2025 per Capstone), energy and natural resources M&A totaled $333.7B in 2025 up 31.3% YoY per KPMG, and industrial decarbonization buyouts in the Ara Partners profile command 10x to 14x for proven assets. For a corp dev lead evaluating a $20M-$40M environmental services or HVAC platform, the spread between tuck-in and platform multiples plus the strategic-multiple-expansion premium is the core value creation mechanism. Peony Data Room at $52 per admin per month includes AI document extraction that lets capital partners ask What is revenue by utility customer or What is the gross margin by sub-service line across uploaded financials and get cited answers with exact page numbers, a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first cleantech IS deal -- why is cleantech/energy growing for independent sponsors in 2026?

Cleantech and energy is growing for independent sponsors because four structural forces converge in 2026: OBBBA (the One Big Beautiful Bill Act signed July 4, 2025) executed a partial IRA repeal that terminated EV credits §25E/§30D/§45W on September 30, 2025, expired residential solar §25D on December 31, 2025, and made §48E wind/solar ineligible if construction begins after July 4, 2026 -- but §45X and §48C transferability SURVIVED, generating a compressed M&A window before cliff dates and distressed divestiture tailwinds; AI data center electricity demand is the dominant bullish driver with Goldman Sachs projecting global data center power demand up 220 percent by 2030 versus 2023, US up 197 percent to 95 GW capacity, ~$720 billion in grid spending through 2030, and IEA's base case of global data center consumption doubling to ~945 TWh by 2030; environmental services multiple expansion hit 15.0x to 20.9x median strategic in 2025 per Capstone, the biggest multiple expansion of any sector; and critical minerals supply chain got a massive government backstop in 2025 with the Pentagon becoming the largest shareholder of MP Materials via a $1.4 billion public-private rare earth supply chain partnership ($620M federal loan plus $50M Commerce plus $550M private). For a family office allocating $5M-$15M equity to its first cleantech IS deal, focus on founder-led HVAC, electrical services, utility contractors, or environmental services platforms with $3M-$10M EBITDA that benefit from either the AI data center tailwind (backup power, grid services, HVAC cooling, ESCO) or the OBBBA compressed window (residential solar installers, EV infrastructure contractors). Peony Data Room at $52 per admin per month includes page-level analytics that show which capital partners spent 30 minutes on the utility customer concentration analysis versus skimmed the CIM, so you can prioritize follow-ups with genuinely engaged partners.

I am a corp dev analyst building my first cleantech data room -- what documents do capital partners need?

Cleantech and energy capital partners require standard M&A diligence plus sector-specific materials: top-20 customer concentration with utility, municipal, commercial, and industrial breakdown and contract terms, top-20 vendor and EPC subcontractor concentration with performance bonds and change-of-control provisions, PPA (power purchase agreement) schedules with remaining term, escalators, and curtailment history for any generation assets, interconnection agreements and utility coordination records, tax credit transfer documentation and §45X/§48C/§48E eligibility letters, NERC/FERC compliance records for any transmission- or generation-adjacent assets, Phase I and Phase II ESAs for every owned facility with particular attention to legacy fuel, chemical, or battery storage sites, cold chain or temperature-controlled compliance records for any HVAC/refrigeration targets, DOT compliance for service fleet, OSHA recordables and workers-comp history, driver qualification files for any last-mile or service-truck fleet, lease schedules for warehouses, yards, and substations with remaining term and renewal options, fleet lists with age and replacement timing for service-truck-heavy businesses, NETA/NECA/NFPA certifications for electrical work, EPA RCRA compliance for hazardous waste handlers, licensure records for HVAC, electrical, plumbing journeymen, and specialty subcontractors, and warranty exposure analysis for any installation or project work. For a corp dev analyst running point on a $25M-$50M cleantech services deal, these are the documents that kill or close the transaction. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes all of these in under 3 minutes into a professional folder structure, and Smart Q and A that routes capital partner questions through AI-drafted answers with page citations before your team approves each response.

Our IS targets data center and grid resilience -- which capital partners fit that sub-sector?

Data center and grid resilience IS deals sit at the intersection of two of the strongest end-market tailwinds in cleantech 2026 -- AI data center electricity demand and grid modernization spending -- and capital partner fit is sub-sector-specific. Industrial Growth Partners closed its March 2025 platform SENS (the sixth platform in Fund VI) specifically targeting ruggedized battery chargers and integrated power systems for data centers, hospitals, utilities, and telecom -- a direct AI data center plus grid-resilience play. Bernhard Capital Partners is the only pure-play energy services PE firm on this list, runs a DOE technical consulting platform, closed on SMSI (nuclear/DOE services) and TechServ (utility services June 2025), and was reported in advanced talks on Cleco Power (specifically citing data center electricity demand with Stonepeak) in late 2025. Argonaut Private Equity operates a portfolio heavy with utility contractors (Bandera Utility Contractors, Miller Contracting Services) through Fund V ($500M December 2023). Huron Capital's ExecFactor® platforms in HVAC and energy efficiency services (The Exigent Group, Pueblo Mechanical, Smith-Boughan Mechanical, Premier Mechanical) address the HVAC-cooling end of the data center supply chain. Align Collaborate's Teague Electric deal (2025, with IX Capital Partners IS) and Right Angle Partners Fire Protection directly target the electrical and fire-protection services that data center construction and retrofit demand. For a specialized IS targeting a $20M-$40M electrical services platform with utility or data center customer concentration, the stack typically pairs a sector-specialist equity lead with SBIC mezzanine from Tecum or Argosy. Peony Data Room at $52 per admin per month includes dynamic watermarks with viewer identity embedded in every frame and NDA gates so capital partners sign before any utility customer list, PPA pricing schedule, or EPC subcontract terms are visible.

Our IS is running three to six cleantech deals per year -- how much does a data room cost for cleantech/energy IS deals?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 3 to 25 million dollar EBITDA cleantech and energy services businesses. Cleantech deals also require extensive utility contract uploads, PPA and interconnection agreements, tax credit transfer documentation, NERC/FERC compliance files, Phase I and Phase II ESAs, NETA/NECA certifications, warranty exposure analyses, and EPC subcontract schedules, meaning sponsors often need four to six active data rooms simultaneously during a roll-up phase -- a dynamic structurally broken on per-deal pricing. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing, AI document extraction, Smart Q and A, AI redaction, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. An IS running three cleantech deals per year pays roughly 624 dollars annually on Peony Data Room versus 45,000 to 150,000 dollars on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure.

I am a capital-partner PE principal diligencing an environmental services deal -- what cleantech sub-sectors have the most IS activity in 2026?

The most active cleantech and energy sub-sectors for independent sponsor deals in 2025-2026 are environmental services and waste management (202 waste transactions and $5.7B disclosed in 2025 plus 89 environmental services transactions YTD up 28.1 percent YoY per Capstone, with strategic medians running 15.0x-20.9x EBITDA -- the biggest multiple expansion of any sector), HVAC and energy efficiency services (HVAC equipment 2025 median 10.9x EV/EBITDA, residential services 12.6x median in Q1 2025, with Blackstone paying 18.5x for the $2.5B Champions Group deal), electrical contracting and utility services (driven by AI data center demand + $720B grid spending through 2030 per Goldman), specialty chemical and industrial decarbonization (Ara Partners closed Fund III $3.0B plus $800M Infrastructure Fund May 2025 targeting >60% GHG-reduction assets), solar and storage installation services (compressed window before §25D expired December 31, 2025 plus §48E construction-start cliff on July 4, 2026), critical minerals and rare earth services (Pentagon's $1.4B MP Materials public-private partnership 2025 is the template), and nuclear and DOE technical services (Bernhard Capital's SMSI platform is the reference). For a capital-partner PE principal diligencing a $30M-$50M environmental services platform, expect customer concentration (municipal and industrial breakdown), change-of-control provisions in utility contracts, and warranty exposure on prior installation work to be the three biggest diligence issues. Peony Data Room at 52 dollars per admin per month includes AI-powered Smart Q and A that lets capital partners submit diligence questions where AI surfaces relevant document sections with exact page citations, something DocSend cannot detect on any plan.

I am an M&A attorney advising a first-time IS -- how do cleantech capital partners expect deal books to be structured?

Cleantech and energy capital partners expect deal books organized in a standard 3-stage diligence flow: Stage 1 initial risk scan including the CIM, top-20 customer and vendor concentration with utility/municipal/commercial/industrial breakdown, gross margin by service line, tax credit eligibility and transfer documentation if applicable (§45X/§48C/§48E), and Phase I environmental screening on any owned facility; Stage 2 deep dive with Q of E and working capital normalization, EPC subcontract and bonding audit, PPA and interconnection agreement review where applicable, NERC/FERC compliance records, licensure records for all journeymen and specialty trades, warranty exposure analysis on prior project work, fleet appraisal and replacement schedule for service-truck-heavy businesses, DOT and safety compliance records for service fleet, and OBBBA impact modeling for any EV, residential solar, or wind/solar construction exposure; Stage 3 comprehensive validation covering Phase II ESAs, OSHA audits, integration plan for field service management and dispatch systems, and 100-day route and crew-deployment optimization plan. For an M&A attorney advising a first-time IS running a $25M enterprise value environmental services or HVAC deal, the warranty exposure analysis alone can move 5-10 percent of enterprise value and capital partners will pressure-test every open warranty claim. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing that organizes documents into a professional folder structure in under 3 minutes, and personalized sharing links that track each capital partner separately so you know who is engaged before you draft the capital call.

Our IS is running a $25M roll-up of HVAC and energy services -- how do OBBBA and IRA changes affect deal economics?

OBBBA's July 4, 2025 partial IRA repeal changes deal economics materially by sub-sector: EV credits §25E/§30D/§45W terminated September 30, 2025 meaning EV charging installer and fleet conversion deal economics are degraded and private capital pace has slowed accordingly; residential solar §25D expired December 31, 2025 which compressed the installer M&A window before the cliff and is driving a wave of distressed sales in 2026; §48E wind/solar is ineligible if construction begins after July 4, 2026 meaning any platform with a project backlog needs a clean construction-start audit; §45X (advanced manufacturing production credit) phases down starting 2029 with wind components ineligible after 2027 -- but §45X and §48C TRANSFERABILITY SURVIVED OBBBA intact, which preserves the tax credit transfer market (more than $20 billion in H1 2025 alone per Crux, 2x H1 2024 pace, projected full-year $33-$40 billion); FEOC restrictions block Chinese-controlled supply chains post-OBBBA, which has driven reshoring and US-supplier M&A activity; and 100% bonus depreciation was reinstated, which subsidizes capital-intensive infrastructure and incentivizes corporates to acquire operating renewables for tax-shield purposes. For an IS running a $25M roll-up of HVAC and energy services, the clean sub-sectors are commercial HVAC (where data center cooling demand is accelerating), energy efficiency retrofits (preserved ESCO economics), electrical contracting (grid spending tailwind), and environmental services (multiple expansion); the sub-sectors requiring careful underwriting are residential solar (compressed window, pending cliff), EV charging (terminated credits), and wind component manufacturing (phased-out §45X). Document tax credit eligibility letters, the construction-start timeline for any §48E project, and FEOC compliance attestations in your data room. Peony Data Room at 52 dollars per admin per month includes AI redaction that identifies pricing and tax-credit transfer data across uploaded utility and EPC files, and NDA gates that prevent any capital partner from seeing confidential pricing schedules before signing, a workflow that Datasite charges $25K+ per deal to configure.

I am a first-time IS building a capital partner network -- where do cleantech/energy independent sponsors meet capital partners in 2026?

Cleantech and energy independent sponsors meet capital partners at the McGuireWoods Independent Sponsor Conference with 1,600 attendees in 2025 and the 2026 event on October 27-28 in Dallas, the ACG DealMAX conference on April 27-29 in Las Vegas (the InterGrowth rebrand anchoring the spring LMM calendar), the SBIA Independent Sponsor Forum on May 6 at the Sheraton Philadelphia Downtown, RE+ 2026 in Las Vegas for utility-scale solar and storage operator relationships, WasteExpo in Las Vegas for environmental services and waste operator sourcing, AHR Expo for HVAC operator relationships, DistribuTECH for utility contractor and grid services sourcing, the iGlobal Independent Sponsor Summit Dallas on June 11 and NYC on September 28-29, and through platforms like Axial where independent sponsors reached 26.8 percent of all closed deals YTD 2025. Repeat relationships account for 59 percent of capital partner deals according to Citrin Cooperman. For an IS building a 5-to-10 firm capital partner rolodex focused on cleantech and energy, starting with an IS-explicit equity partner like Align Collaborate, Peninsula, or Kinderhook plus one sector-specialist (Ara Partners for decarbonization, Bernhard for pure-play energy services, or Huron for HVAC) plus one SBIC like Tecum or Argosy is the fastest path. Peony Data Room at 52 dollars per admin per month includes NDA-gated data rooms with built-in e-signatures so capital partners can sign and access materials in a single workflow after conference introductions.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- SBIC for Independent Sponsors -- 2-to-1 debenture math, $175M/$350M caps, 8 active IS-partner SBICs (Tecum, Argosy, Centerfield, Plexus on cleantech/energy services), $35M EV stack example

- Independent Sponsor Manufacturing Capital Partners -- 12 firms funding manufacturing IS deals

- Independent Sponsor Tech/Software Capital Partners -- 13 firms funding tech/software IS deals

- Independent Sponsor Consumer Capital Partners -- 12 firms funding consumer IS deals

- Independent Sponsor Distribution & Logistics Capital Partners -- 12 firms funding distribution/logistics IS deals

- Independent Sponsor Healthcare Capital Partners -- 17 firms funding healthcare IS deals