Independent Sponsor Deal Book (10 Sections, Day-1 Ready) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

I used to work in venture capital at Backed VC and Target Global, where I evaluated several hundred founder pitch decks a year. Now I run Peony, a data room platform. Over the last year I have watched hundreds of independent sponsor deal books move through our system, and the single clearest pattern is this: the sponsors who close are not the ones with the prettiest decks — they are the ones whose deal book is structured exactly the way capital partners actually read it.

A VC pitch deck and an independent sponsor deal book look similar from the outside. Both are trying to get capital from an investor. But the evaluation framework is completely different. A VC reads a deck to decide if a founder is worth a 30-minute first meeting. A capital partner reads an IS deal book to decide whether to commit $3M to $15M of equity into a specific company under a 90-day clock — while simultaneously evaluating the sponsor's process discipline, the company's financial quality, and the sector thesis. The deal book is not a pitch. It is the foundational diligence artifact for a dual-underwriting decision.

This guide breaks down the 10 sections that belong in every serious IS deal book, what capital partners open first (it is not the executive summary), what kills commitments in the first 5 minutes, and how to layer the book across three stages so partners see the right materials at the right time. For the companion pieces, see my Independent Sponsor Data Room Checklist (the 42 documents that live inside the deal book) and the Independent Sponsor LOI Playbook (the 90-day timeline the deal book powers).

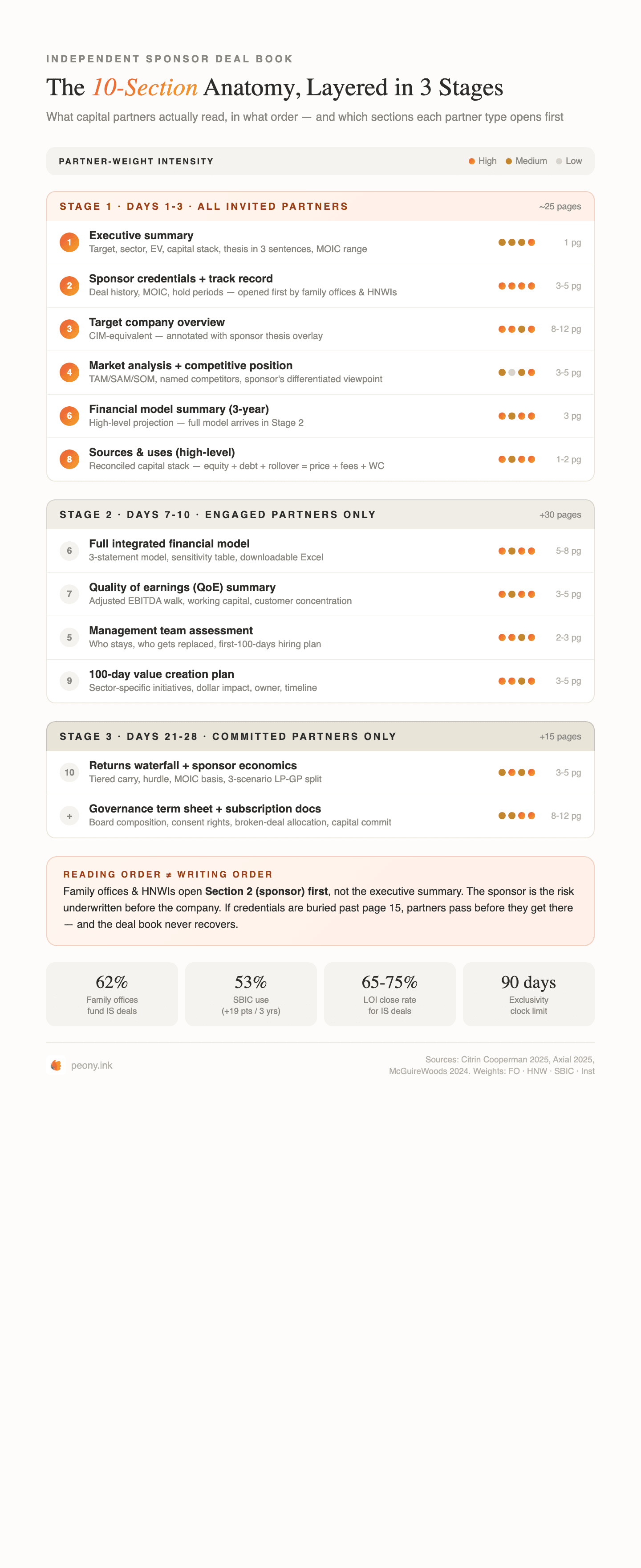

TL;DR: An independent sponsor deal book is the 40 to 70-page materials package capital partners read to evaluate both the deal and the sponsor simultaneously. Independent sponsors now close 27% of all deals on Axial — the highest buyer-type share (Axial 2025 IS Report). The deal book breaks into 10 sections layered across 3 stages: Stage 1 (6 sections, all invited partners, week 1), Stage 2 (detailed financials + QoE + value creation, engaged partners only, days 7-10), Stage 3 (returns waterfall + governance + subscription docs, committed partners only, days 21-28). Capital partners open the sponsor credentials section first, not the executive summary — because the sponsor is the risk underwritten before the company. 73% of M&A advisors say IS deals take longer to close than PE funds (Axial 2025), and deal book quality is the single most controllable variable in compressing that timeline. Family offices fund 62% of IS deals, HNWIs 55%, SBICs 53% (up 19 points in 3 years) (Citrin Cooperman 2025) — each capital partner type weights the 10 sections differently, and the deal book must reflect that.

Why an IS deal book is not a VC pitch deck

Three structural differences make an IS deal book fundamentally different from the fundraising materials VCs and PE funds use:

| Dimension | IS deal book | VC pitch deck | PE fund deck |

|---|---|---|---|

| What is being sold | A specific deal + the sponsor's process | A team's ability to build a breakout company | A fund strategy + a track record |

| What the reader buys | Equity in one company at a negotiated price | An option on future rounds at uncapped outcomes | LP interests in a blind-pool vehicle |

| Dual underwriting | Yes — company and sponsor evaluated simultaneously | No — the team is the only variable | No — the strategy is the only variable |

| Financial depth needed | 5-year integrated model + QoE + sources and uses + waterfall | Top-line and unit economics projections | Aggregate portfolio returns and DPI/TVPI |

| Timeline pressure | 90-day exclusivity clock | Months to close a round | 12-18 months for a fund close |

| Length | 40-70 pages layered in 3 stages | 10-15 slides | 60-100 pages in a private placement memo |

| Confidentiality | NDA gates before any section is visible; full watermarking | Usually unsigned with anti-forwarding links | Strict LP-only under non-disclosure |

The dual underwriting is the most important distinction. When a family office reads your deal book, they are running two independent evaluations in parallel: is this company worth buying at this price, and is this sponsor the right person to execute the thesis and protect our capital for the next 4 to 7 years? Most first-time sponsors write a deal book that answers only the first question. The sponsors who close — the ones in the 65 to 75% conversion band that Citrin Cooperman and McGuireWoods cite — answer both, and they structure the book so each question is answered by a specific section.

"We are not just evaluating the deal, we are evaluating the sponsor's process." — Grant Kornman, Partner at Align Collaborate (Citrin Cooperman)

The 10 sections every IS deal book needs

I have organized these in the order capital partners actually read them — not the order most sponsors write them. If your deal book leads with the target company and the thesis, you have buried the section that determines whether anyone reads the rest.

Section 1 — Executive summary (1 page, front cover)

What it is: A single page that names the target company, the sector, the enterprise value, the proposed capital structure, your sponsor fees, the thesis in three sentences, and the expected MOIC range.

Why it matters: This is the IC-meeting-prep page. The senior partner at a family office reads this 30 seconds before walking into a Monday morning pipeline review and decides whether the rest of the deal book goes into active diligence or the pass pile.

Common mistake: Sponsors write a narrative introduction here instead of a structured summary. A family office partner has 12 deals in their pipeline this month. Give them 8 bullet points, not 4 paragraphs.

Template elements: Target, sector, EV, proposed capital stack (sources and uses one-liner), sponsor economics (fee, carry, GP commit), thesis in 3 sentences, 3-scenario MOIC projection, projected hold period, key risks in one line.

Section 2 — Sponsor credentials and track record (3-5 pages)

What it is: Your deal history, role, entry multiples, hold periods, exit outcomes, realized IRR and MOIC — verifiable at the case-study level. If you have fewer than 3 completed transactions, include relevant operating roles, advisory engagements, and sector expertise with quantified impact.

Why it matters: This is the section capital partners open first, not the executive summary. The sponsor is the risk underwritten before the company. Family offices funded 62% of IS deals in 2025 and SBICs 53% — both groups make pass-or-advance decisions on the sponsor section within 5 minutes of opening the book (Citrin Cooperman 2025).

Common mistake: Generic career history instead of a structured track record. "10 years of PE experience" tells me nothing. "Led 4 platform acquisitions averaging $35M EV at previous fund, realized 3.2x average MOIC across 3 exits" tells me you can execute this deal. If you are first-time, be specific about relevant operating roles with dollar impact.

Template elements: 1-page sponsor bio, 1-2 pages of deal history table (date, target, EV, role, entry/exit multiple, MOIC, IRR, hold period, outcome), 1 page of sector-specific expertise with dollar impact, 1-page case study of most relevant prior deal.

For the deeper treatment of what to include in this section when you are first-time, see the sponsor credibility documents breakdown in the data room checklist.

Section 3 — Target company overview (8-12 pages)

What it is: The CIM-equivalent. Business description, products or services, customer segmentation, geographic footprint, competitive position, employee base, historical milestones, ownership structure, and founder or management compensation.

Why it matters: This is the section that answers "is the company worth buying at this price?" Most of your content here comes from the seller's CIM, but your job is to restructure and annotate it with your thesis overlay. Raw seller CIMs are written to maximize the sale price; your capital partners want your edited view of what is real versus what is sell-side marketing.

Common mistake: Sponsors copy the seller CIM wholesale. Capital partners have read 40 CIMs this quarter — they know the structure and they know the marketing layer. Annotate the CIM with your own observations: what you believe about customer quality, what you think is overstated, what you would change in the first 100 days.

Template elements: 1-page business summary, 1-page customer concentration table (top 10 customers by revenue and hold period), 1-page product or service line P&L (if meaningful), 2-3 pages of operational overview (locations, employees, systems), 1 page of ownership structure and seller rollover expectation.

Section 4 — Market analysis and competitive position (3-5 pages)

What it is: Total addressable market, market growth rate with cited source, competitive landscape with named competitors, barriers to entry, customer acquisition dynamics, and the specific positioning advantage of this target within the market.

Why it matters: Capital partners want to see you have a thesis beyond "good company at a fair price". The market section is where you differentiate from a sell-side intermediary running a broad auction. If your deal book market section reads like the seller's CIM chapter on market, you have not done the work.

Common mistake: Bloomberg-grade market statistics with no sponsor viewpoint. A family office can pull market size from IBISWorld. They cannot pull your specific view on why this company wins in its sector. Make that view explicit.

Template elements: 1-page TAM/SAM/SOM with cited sources (not Statista wave charts), 1-page competitor matrix (4-6 named competitors, revenue, positioning, key differences), 1-page market growth narrative, 1 page on the target's specific positioning advantage.

Section 5 — Management team assessment (2-3 pages)

What it is: CEO, CFO, and top 2-3 operators with background, tenure, equity, and a specific view on who stays post-close, who gets replaced, and what key hires are needed in the first 100 days.

Why it matters: Capital partners will not commit without a clear view of the management team they are inheriting. In LMM deals under $50M EV, the existing CEO frequently rolls equity and stays for 2 to 4 years. If you do not have a clear assessment, your capital partners will assume you have not done the work.

Common mistake: One-line bios with no assessment. "John has been CEO for 15 years" is useless. "John founded the company, has $8M personal net worth tied to the company, plans to roll 40% of his equity and step back from day-to-day in year 2 — his planned successor is the current COO who has 8 years with the company" gives partners a decision they can make.

Template elements: 1 page each on CEO and CFO (background, tenure, equity stake, post-close plan), 1 page on key operators, 1 page on management gaps and first-100-days hiring plan.

Section 6 — Integrated financial model summary (5-8 pages)

What it is: Three-statement financial model (income statement, balance sheet, cash flow) with 3 years historical, current year projection, and 3 to 5 years forward projection. Key assumptions listed on a single page. Adjusted EBITDA bridge with every adjustment labeled and sourced. For the full 7-tab model architecture, the $30M EV / $5M EBITDA worked sources and uses, the formula-driven waterfall cascade, and the five Excel mistakes that get models rejected, see our Independent Sponsor Financial Model: 2026 Template + Walkthrough — the deep dive on building the model file itself.

Why it matters: This is where you either earn the capital partner's trust or lose it permanently. If the three statements do not tie (cash flow reconciliation fails, balance sheet does not balance, or EBITDA bridge contains unsupported adjustments), you get a pass in week 1. According to Axial 2025, QoE EBITDA discrepancies were the second biggest reason LOIs broke at 21.3% — and unintegrated models compound that risk by signaling sloppy process.

Common mistake: Shipping a revenue-growth-and-EBITDA-margin projection without an integrated model. If your balance sheet does not project working capital, capex, debt paydown, and cash accumulation, sophisticated capital partners cannot evaluate the deal. Build the full model from day one.

Template elements: 1-page key assumptions (revenue growth, margin, capex, working capital, exit multiple), 1-page income statement (historical + projection), 1-page balance sheet, 1-page cash flow statement, 1-page EBITDA bridge with labeled adjustments, 1-page sensitivity table (base/upside/downside).

Section 7 — Quality of earnings summary (3-5 pages)

What it is: The quality of earnings report findings summarized for capital partner consumption. Adjusted EBITDA walk from reported to QoE-adjusted, normalized working capital, customer concentration, revenue quality (recurring versus project-based), and cost-of-goods structure.

Why it matters: A pre-LOI or early-post-LOI QoE compresses capital partner diligence by 1-2 weeks because partners can evaluate adjusted EBITDA from day one rather than waiting 3 to 4 weeks for the QoE to complete. Pre-LOI QoE reports cost $30,000 to $75,000 for typical IS deals in the $10M to $50M range — see the due diligence cost breakdown for the full picture. The cost is real, but the alternative is losing 2 weeks of your 90-day exclusivity clock.

Common mistake: Either no QoE at all (red flag for most family offices and all SBICs) or shipping the full 100-page QoE report without a summary. Include both: a 3 to 5-page summary in the deal book, and the full QoE as a Stage 2 appendix.

Template elements: 1-page executive summary of QoE findings, 1-page adjusted EBITDA walk, 1-page working capital normalization, 1-page revenue quality analysis, 1-page customer and vendor concentration.

Section 8 — Sources and uses + capital structure (2-3 pages)

What it is: Purchase price breakdown (cash, seller rollover, earnout), debt structure (senior, mezzanine, SBIC subordinated), equity structure (sponsor GP commit, lead capital partner, co-invest), transaction fees, and working capital adjustment. Everything ties to a single total.

Why it matters: This is the reconciliation page. If sources and uses do not balance — if equity plus debt plus seller rollover does not equal purchase price plus fees plus working capital — you have a sloppy deal book and capital partners will question every other number.

Common mistake: Missing the working capital adjustment line, forgetting to account for transaction fees, or not showing the SBIC 2-to-1 debenture leverage calculation for deals with SBIC capital. SBICs funded 53% of IS deals in 2025 and require specific structural disclosure (Citrin Cooperman 2025) — omitting it forces your SBIC partner to spend week 1 assembling basic eligibility data instead of evaluating the thesis.

Template elements: 1-page sources and uses table with full reconciliation, 1-page debt structure detail (tranches, pricing, covenants), 1 page on equity structure and investor allocation including GP commit.

Section 9 — 100-day value creation plan (3-5 pages)

What it is: The specific initiatives you will execute in the first 100 days post-close, with dollar impact estimates, responsible owner, and target completion date. Sector-specific operational levers, not generic consultant-speak.

Why it matters: This is the section that separates sponsors who win capital partner follow-on commitments from sponsors who close one deal and never raise again. Family offices and HNWIs especially want to see specific, quantified value creation initiatives — not "optimize operations" or "improve margins by 200 bps". A great 100-day plan is the foundation of the sponsor track record you will use to raise capital for deals 2, 3, and 4.

Common mistake: Generic bullet points lifted from a McKinsey playbook. "Implement lean operating model" is not a value creation initiative. "Migrate 40% of field technicians to route-based scheduling software to reduce windshield time by 18% and increase service capacity from 8 to 11 jobs per day per technician, generating $1.2M in incremental revenue by month 18" is.

Template elements: 1-page value creation framework overview, 1-2 pages of specific initiatives (5 to 10 initiatives, each with dollar estimate, owner, timeline), 1-page dashboard of KPIs you will track, 1-page year 1 through year 3 EBITDA walk showing how the initiatives compound.

Section 10 — Returns waterfall and sponsor economics (3-5 pages)

What it is: Tiered carry structure, hurdle rate, catch-up provision, IRR-versus-MOIC basis, and 3-scenario projection of LP-GP split at each outcome. Sponsor fees (closing, management, monitoring), GP commit, and co-invest rights for capital partners.

Why it matters: This is the economics page. Capital partners want to see you have thought about alignment — your GP commit matters, your carry structure matters, and whether your waterfall rewards you for 3x outcomes versus 5x outcomes matters. Citrin Cooperman 2025 found 64% of sponsors can earn 25%+ carry at max tiers (up from 37% in 2019), and 50% now use MOIC-based hurdles (up from 27%). The market has shifted toward absolute returns.

Common mistake: Over-engineered waterfall with 6+ tiers, complex European-style catch-up, and IRR-only triggers. Your family office partners want MOIC-based tiers, simple full catch-up, and a clear 8% preferred return. Institutional-grade but readable in 10 minutes.

Template elements: 1-page carry structure with tier breakdown, 1-page fee structure (closing, management, monitoring, GP commit), 1-page 3-scenario returns model (base, upside, downside), 1-page waterfall mechanics, 1-page LP-GP split summary.

How capital partners actually read the deal book

Different capital partner types weight the 10 sections differently. The book is the same, but the reading path is not. Knowing which section your target partner opens first changes how you sequence the pre-meeting share and the follow-up.

| Section | Family office weight | HNW individual weight | SBIC weight | Institutional co-invest weight |

|---|---|---|---|---|

| 1. Executive summary | Medium | Medium | Medium | High |

| 2. Sponsor credentials | Very high (opens first) | Very high | High | High |

| 3. Target company overview | High | High | Medium | Very high |

| 4. Market analysis | Medium | Low | Medium | High |

| 5. Management team | High | High | Medium | High |

| 6. Financial model | Very high | Medium | Very high | Very high |

| 7. Quality of earnings | Very high | Medium | Very high | Very high |

| 8. Sources and uses | High | Medium | Very high (SBIC compliance) | Very high |

| 9. 100-day value creation plan | Very high | Very high | Medium | High |

| 10. Returns waterfall | Medium | High | Medium | Very high |

For a family office capital partner, the reading path is typically: Section 2 (sponsor) → Section 9 (value creation) → Section 7 (QoE) → Section 6 (financial model) → Section 3 (company) → then everything else. If your deal book buries the value creation plan behind 40 pages of financial detail, family offices pass before they get to the section that would have convinced them.

Configure your data room so capital partners can navigate directly to the sections they care about most. Page-level analytics on Peony Business show which sections each partner actually opened and how long they spent — so after week 1 you know whether your SBIC partner finished the QoE, whether your family office reached the value creation plan, and which HNW partner stopped at the sponsor deck. That engagement signal is the difference between calling the right 2 partners back on Monday and wasting your follow-up budget on partners who never engaged.

The 3-stage release architecture

Do not share all 10 sections with all partners in week 1. Layer the release across three stages that mirror how capital partner diligence actually progresses:

Stage 1 — Days 1 to 3 (all invited partners, ~25 pages)

- Section 1: Executive summary

- Section 2: Sponsor credentials and track record

- Section 3: Target company overview (CIM summary, not full CIM)

- Section 4: Market analysis and competitive position

- Section 6: Financial model summary (3-year historical + projection, no full model)

- Section 8: Sources and uses (high-level, no tranche detail)

Purpose: Gives your 5 to 8 invited partners enough to decide whether to invest 3 to 4 weeks of diligence time. If a partner reads Stage 1 and passes, you have saved both sides weeks.

Stage 2 — Days 7 to 10 (serious partners only, +30 pages)

- Section 6: Full integrated financial model (downloadable Excel)

- Section 7: Quality of earnings report (summary + full report in appendix)

- Section 9: 100-day value creation plan

- Expanded Section 3: Customer concentration analysis, full CIM

- Expanded Section 5: Management team deep assessment

Purpose: The 3 to 5 partners who moved through Stage 1 now get the materials they need to complete their independent diligence. Stage 2 is where most partners decide to move to commitment discussions.

Stage 3 — Days 21 to 28 (committed partners only, +15 pages)

- Section 10: Full returns waterfall with governance mechanics

- Governance term sheet (board composition, consent rights, protective provisions)

- Subscription documents and capital commitment paperwork

- Capital partner reporting framework

- Broken-deal cost allocation agreement

Purpose: The 1 to 2 partners moving to commitment get the economics detail and legal paperwork. Stage 3 is where final negotiation and subscription happen — the materials here should not be visible to partners who are still in Stage 1 or Stage 2 review.

Use per-viewer staged access to expand each partner's permissions as they progress. Running three separate data rooms is operationally painful and creates version control risk. Peony Data Room at $52 per admin per month supports per-viewer staged folder access on a single data room — the core workflow IS sponsors need and the reason legacy VDR providers at $50,000 per deal are structurally broken for deal-by-deal IS economics.

For the underlying document list that populates these three stages, see the full independent sponsor data room checklist — 42 documents mapped by partner type. For the timing of when each stage releases within the 90-day exclusivity window, see the LOI playbook.

The 5 deal book mistakes that kill capital partner interest

These are the mistakes I see repeated across the hundreds of IS deal books I review each year on the platform. Fix all 5 before you send the book to a single capital partner.

1. Leading with the target company instead of the sponsor

If Section 2 (sponsor credentials) is buried at page 25, capital partners assume you do not have a track record worth showing. They pass before getting there. Sponsor credentials go in the first 5 pages, period.

2. Unintegrated financial model

If the three statements do not tie, the EBITDA bridge does not reconcile, or sources and uses does not balance, you get a pass in week 1 regardless of how good the deal is. Build the model in a way that every number traces to a source. Run tie-out checks before you ship.

3. Generic value creation plan

"Optimize operations" and "improve margins by 200 bps" are not value creation initiatives. Sector-specific, dollar-quantified, owner-assigned initiatives with target completion dates are. Family offices and HNWIs pass on generic plans because they cannot underwrite the sponsor's operational capability without specifics.

4. Over-engineered returns waterfall

Six-tier IRR-based waterfalls with European-style catch-up sound sophisticated and look like PE fund economics. They are not what family office capital partners want to evaluate. Simple MOIC-based tiers with full catch-up and 8% preferred return is the market standard — 64% of sponsors now operate this way per Citrin Cooperman 2025.

5. No capital partner-specific tailoring

Sending identical deal book versions to every partner type misses the signal that your SBIC needs different disclosures than your family office, and your HNW individuals need plain-English narrative that institutional co-invest teams can skip. Tailor the Stage 1 share by partner type using personalized sharing links that track each partner separately and let you customize which sections land first.

Protecting the deal book during the capital raise

Your deal book contains your purchase price, your sponsor economics, your QoE findings, and your thesis — all highly sensitive. When you share it with 5 to 8 capital partners simultaneously, you are creating 5 to 8 potential leak paths. Three controls matter:

NDA gates before any content is visible. Every capital partner signs an NDA before seeing a single page. Not a Dropbox folder "here is the link" — a gated access flow where the NDA signature happens inside the data room before the folder unlocks. This single control deters 90% of casual forwarding.

Dynamic watermarks with viewer identity. Every page the capital partner opens carries their email, IP address, and timestamp embedded in the watermark. If a screenshot appears on a competitor's desk, you know which partner's environment it came from. Peony's Data Room plan includes dynamic watermarking on all documents — Google Drive and Dropbox do not offer per-page dynamic watermarks on any plan.

Screenshot protection on sensitive pages. The returns waterfall, the QoE adjusted EBITDA bridge, and the sources and uses page are the sections competing bidders would most want to see. Block and log screenshot attempts on those specific folders. Legacy platforms and DocSend Advanced Data Rooms at $180 per month for three seats do not support screenshot detection outside their platform.

Deal books that leak compromise not just this deal but your next five. A family office that discovers your purchase price was forwarded to a competing bidder will never take your call again. For the full security framing for IS workflows, see the best data rooms for independent sponsors comparison, which tests 8 VDRs through the IS economic lens.

Templates and cost realities

You do not need to buy a deal book template. Every section I described above can be built in Excel for the model and PowerPoint or Google Slides for the narrative, and the entire package assembles in 3 to 5 days of focused work if your CIM and financial model are already in hand. What you cannot cheap out on:

- Quality of earnings report. $30,000 to $75,000 pre-LOI, roughly $50,000 to $125,000 post-LOI with full diligence scope. See the due diligence cost breakdown for the full deal cost stack.

- Financial model build or review. $5,000 to $25,000 if you commission it, 60-120 hours if you build it yourself.

- Legal review of governance terms. $15,000 to $40,000 for Stage 3 materials, typically done alongside the definitive agreement drafting.

The rest — the narrative, the structure, the design — is sweat equity. Sponsors who invest 40 to 80 hours structuring a tight 40-page deal book close at dramatically higher rates than sponsors who ship 120-page sprawling packages assembled in 2 days. See the data room folder structure guide for the folder architecture that holds the deal book plus supporting documents.

Why Peony for independent sponsor deal books

Peony for Private Equity, Peony for M&A, and Peony for Fundraising are all built for the workflow an independent sponsor runs: a seller-side diligence room receiving the seller's CIM and QoE, plus a capital-partner-side deal book room sharing your materials with 5 to 8 partners simultaneously — both running under a 90-day exclusivity clock.

Peony Data Room at $52 per admin per month includes every capability this workflow needs: NDA gates, dynamic watermarking, screenshot protection, page-level analytics per viewer, AI-powered Q&A with sponsor review, AI auto-indexing that organizes your uploaded deal book in under 3 minutes, AI redaction for sensitive pages, custom branding, and unlimited data rooms. Business at $30 per admin per month covers core sharing controls — screenshot protection, page-level analytics, and basic AI Q&A — for smaller deals, but Data Room is the tier IS workflows require because unlimited rooms, AI auto-indexing, AI room generation, and granular per-file permissions are what the deal-by-deal model depends on.

Compare that to Datasite at roughly $50,000 per deal and up, Firmex at approximately $7,800 per year minimum, or Ideals at $5,000 to $20,000 per month enterprise pricing. For an independent sponsor running 3 to 5 deals per year with $30M to $50M average enterprise value, the legacy VDR cost math does not work. Per-deal VDR pricing assumes the amortization math of a committed-capital PE fund — structurally broken for the deal-by-deal IS model. Peony's flat-rate unlimited data rooms is the economic architecture that matches IS workflow. Peony for Family Offices extends the same architecture to the capital partner side.

For deeper cluster reading: see the IS hub guide, the healthcare capital partners directory, the business services capital partners directory, and the 2026 IS conferences calendar.

Frequently Asked Questions

I am a first-time independent sponsor with a signed LOI on a $18M HVAC rollup — what goes in my deal book on day one and what can wait a week?

On day one you ship Stage 1: executive summary with the thesis in one page, sponsor credentials deck, CIM or teaser equivalent, a high-level sources and uses, and a 3-year financial summary. That is six sections, roughly 25 to 35 pages total, and it is what your capital partners need to decide whether to spend the next 3 to 4 weeks on diligence. Hold Stage 2 for days 7 to 10 — the full financial model, quality of earnings, customer concentration analysis, and 100-day value creation plan — and Stage 3 for days 21 to 28 when 1 to 2 partners move to commitment (returns waterfall, governance term sheet, subscription documents). First-time sponsors lose deals by dumping all 10 sections into week 1 and overwhelming partners who have not yet said yes to deeper diligence. Peony Data Room at $52 per admin per month lets you gate Stage 2 and Stage 3 folders separately with per-viewer permissions, so the $18M HVAC deal progresses partner by partner without creating three separate data rooms — something Dropbox and Google Drive cannot support without manual permissioning.

My family office reviews 8 to 12 independent sponsor deal books per month — which section do we open first and what makes us pass in 5 minutes?

Your team opens the sponsor credentials section first, not the executive summary. Family offices fund 62% of independent sponsor deals according to Citrin Cooperman 2025, and the sponsor is the risk you underwrite before the company. A pass in 5 minutes usually comes from three signals: no deal history or professional track record spelled out with entry multiples, hold periods, and MOIC; the 100-day value creation plan is generic consultant-speak without sector-specific levers; or the sources and uses does not reconcile — equity plus debt plus rollover does not equal purchase price plus fees plus working capital. On the other hand, a family office moves a deal book into its active pile when the sponsor section shows sector depth, the financial model is integrated (three statements tie), and the value creation plan names specific initiatives with dollar estimates. Peony page-level analytics show the sponsor exactly which sections your team spent time on versus which got a 30-second scroll, so the follow-up conversation focuses on your actual diligence questions — unlike Google Drive, which has no per-page engagement signal.

I spent 2 years at a PE fund before going independent and my deal book has 70 pages — is that too long for a $35M services deal?

Seventy pages for a $35M services deal is on the long end but not disqualifying if it is layered correctly. The rule I apply is that Stage 1 (what all invited capital partners see in week 1) should be 20 to 30 pages: 1-page executive summary, 5-page sponsor deck, 8 to 12-page CIM summary, 3-page financial summary, and 3-page thesis memo. Stage 2 (serious partners only) adds 25 to 40 pages of full financial model, QoE summary, customer analysis, and value creation plan. Stage 3 (committed partners) is 10 to 20 pages of governance, waterfall, and legal terms. If your 70 pages are well-layered across these three stages, that is fine. If all 70 pages land on partners in week 1, you will get passed on by 3 of 5 partners who do not have 90 minutes to triage. Use Peony's per-viewer staged access to expand each partner's permissions as they progress through diligence — something legacy VDRs at $50,000 per deal make economically impractical for a sponsor running 3 concurrent deals.

Our SBIC evaluates roughly 40 IS deal books per year — what capital structure detail do we need to see that generic PE memos usually miss?

Your SBIC team needs three pieces of capital structure detail that generic PE memos omit: the 2-to-1 debenture leverage calculation on the subordinated debt tranche, SBA size standard compliance confirming the target meets small business eligibility, and a debt service coverage ratio projection through the hold period that accounts for subordinated debt amortization. SBICs funded 53% of independent sponsor deals in 2025 according to Citrin Cooperman, up 19 percentage points over three years — and sponsors who ship deal books without the SBIC-specific disclosure force you to spend week 1 of diligence assembling basic eligibility data instead of evaluating the thesis. The sponsors who close fastest with SBIC capital include a dedicated 2 to 3 page SBIC compliance appendix covering leverage structure, eligibility verification, and debenture covenant compliance. Peony Data Room granular per-folder permissions let the sponsor gate SBIC-specific compliance materials separately from the core deal book, keeping the room clean for non-SBIC partners evaluating the same transaction — a workflow that Firmex at approximately $7,800 per year and Ideals at $5,000 to $20,000 per month charge enterprise add-ons to configure.

I signed my LOI last Friday on a $25M manufacturing deal and the first capital partner meeting is Wednesday — what is the minimum viable deal book I can have ready in 5 days?

For Wednesday you ship a 22-page Stage 1 deal book with these sections: 1-page executive summary with the investment thesis in three sentences, 4-page sponsor credentials deck, 6-page CIM summary (business overview, products, customers, competitive position), 3-page high-level financial summary (3-year historical, 3-year projection, adjusted EBITDA), 3-page sources and uses table, 3-page value creation plan outline, and 2-page risks and mitigants section. That is realistic to pull together in 5 days if you already have the CIM from the seller's advisor and a baseline financial model. What you do not ship on Wednesday: full QoE (commission it now for week 2 delivery), detailed financial model (Stage 2), returns waterfall, governance terms, customer concentration analysis. According to Axial 2025, QoE EBITDA discrepancies are the second biggest reason LOIs die at 21.3%, so get the QoE commissioned on Monday regardless. Peony AI auto-indexing organizes a 22-page deal book plus 40 seller diligence documents into a professional folder structure in under 3 minutes, so Tuesday evening you ship Wednesday-ready rather than pulling an all-nighter formatting folders.

We are a two-person IS firm targeting $15M to $40M deals and most of our capital partners are HNW individuals — do we need the same deal book structure as someone raising from institutional SBICs?

Your HNW capital partners want the same 10 sections but weighted differently. High-net-worth individuals fund 55% of IS deals according to Citrin Cooperman 2025 — second only to family offices — and they typically spend more time on the sponsor credentials section and the 100-day value creation plan, and less time on the formal capital structure waterfall and governance terms. For your $15M to $40M deals with HNW partners, prioritize: a sponsor deck that tells your story in plain English (not consultant-speak), a value creation plan with specific dollar-impact initiatives rather than generic 'operational improvements', a simple 1-page sources and uses instead of a 4-page capital stack diagram, and a returns section expressed as MOIC and hold period rather than IRR waterfall mechanics. HNWs who co-invest alongside institutional capital expect the institutional-grade materials to exist, but they make their decision on the plain-English story. Peony personalized sharing links track each HNW partner separately across the same data room, so you see who actually read the value creation plan versus who skimmed the executive summary — critical signal for a two-person firm deciding who to call back first.

I lost a $30M deal last month because my capital partner said the financial model 'did not tie' — what does that actually mean and how do I avoid it on the next one?

Your model did not tie means one of three things: the three financial statements (income statement, balance sheet, cash flow) did not reconcile so cash flow from operations plus investing and financing activities did not equal the change in cash on the balance sheet; the EBITDA bridge from reported to adjusted did not add up with all adjustments clearly labeled and sourced; or the sources and uses on the capital structure page did not equal purchase price plus transaction fees plus working capital adjustments. Capital partners reject on this signal because an unintegrated model suggests either inexperience or sloppiness, and 63% of buyers discover material financial discrepancies during diligence not apparent in initial disclosures according to industry research. The fix for your next deal: build the model in a way that every number traces to a source, run integrity checks (sum of capital sources = total uses, net income + depreciation - capex - working capital change = free cash flow), and include a 2-page financial model overview in the deal book that shows the tie-outs explicitly. Peony AI-powered Q&A lets capital partners ask 'does the sources and uses reconcile' and get a cited answer from the uploaded model in hours instead of the days it takes with email-based Q&A.

I am a former investment banker launching my first IS deal on a $45M industrial services target — what should the returns waterfall page actually show and what is the number one mistake sponsors make here?

Your returns waterfall page must show five things: the tiered carry structure (typically 10% carry to 1x-2x MOIC, 15% to 2x-3x, 20% to 3x-4x, 25% above 4x, per Citrin Cooperman 2025 which found 64% of sponsors earn 25%+ carry at max tiers), the hurdle rate (typically 8% to 9.9%, with 74% using full catch-up), whether carry is IRR-based or MOIC-based (50% now use MOIC, up from 27% in 2019), a 3-scenario model (base 3x, upside 5x, downside 1.5x), and a clear LP-GP split at each scenario. The number one mistake sponsors make is over-engineering the waterfall with 6+ tiers, complex European-style catch-up clauses, and IRR-only triggers — then wondering why family offices push back for 2 weeks on 'simplify the economics'. Your family office capital partners want to see MOIC-based tiers, simple full catch-up, and a straight 8% preferred return. Keep it institutional-grade but readable in 10 minutes. Peony Data Room lets you share the returns waterfall with dynamic watermarking embedding each capital partner's identity on every page, so sensitive economics stay confidential when shared with 5 to 8 potential partners simultaneously — unlike Google Drive, which has no per-page watermarking on any plan.

Our family office has committed to one IS deal per year and we want the deal book to be the single source of truth for our investment committee — what structure makes that possible?

Build the deal book with a clear 10-section structure that maps to your investment committee's decision tree: executive summary with thesis in 3 sentences, sponsor track record with verifiable deal history, target company overview with financial highlights, market and competitive position, management team assessment, integrated 5-year financial model with key assumptions listed on one page, quality of earnings summary with adjusted EBITDA reconciliation, sources and uses with capital structure detail, 100-day value creation plan with sector-specific initiatives, and returns waterfall with 3 scenarios. Number every page, include a 1-page executive summary at the front that your IC can read in 3 minutes, and include an appendix with supporting detail (full QoE, detailed customer analysis, legal structure) that your diligence team pulls from for deeper review. Family offices that treat the deal book as the IC source of truth move from first meeting to committee approval in 3 to 4 weeks instead of 6 to 8. Peony page-level analytics show the sponsor which IC members opened which sections, so the follow-up presentation can address the specific diligence questions your team actually has — a workflow that Dropbox cannot support at the page level.

I am running 3 concurrent IS deals and cannot rebuild the deal book from scratch each time — what is the right template structure that works across healthcare, services, and light manufacturing deals?

Your template should have the same 10 sections every time but with sector-specific content blocks inside each section. The structural sections stay constant: executive summary, sponsor credentials, target company, market analysis, management, financial model, QoE, sources and uses, value creation, returns waterfall. The sector-specific content that changes: in healthcare services, add a section on reimbursement risk and regulatory compliance; in business services, add a section on customer concentration and recurring revenue quality; in light manufacturing, add a section on supply chain dependencies and capital expenditure cycles. Maintain a master template folder in your data room platform with the 10-section skeleton, then customize the sector content in 4 to 6 hours instead of rebuilding from scratch. Sponsors running 3+ concurrent deals save 40 to 60 hours per deal with this approach. Peony Data Room includes unlimited data rooms at $52 per admin per month so you run all 3 deals from one account with separate viewer permissions for each, instead of paying $50,000 or more per deal at Datasite or managing 3 separate Dropbox folders with inconsistent security settings — unsustainable at any serious IS deal volume.

Related Resources

- What Is an Independent Sponsor? Complete Guide

- Independent Sponsor Data Room Checklist (42 Documents)

- Independent Sponsor LOI Playbook (90-Day Timeline)

- Independent Sponsor Capital Raising Playbook — pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall, and the five Excel mistakes that get models rejected

- Different Passwords for Different Investors — per-LP links, individual passwords, dynamic watermarks, and one-click revoke when sharing the deal book with 5-15 capital partners

- Best Data Rooms for Independent Sponsors

- 18 Independent Sponsor Conferences & Forums in 2026

- Top Healthcare Firms Backing Independent Sponsors

- Top Business Services Capital Partners for Independent Sponsors

- Due Diligence Cost Breakdown

- Data Room Folder Structure Guide

- M&A Data Room Guide

- Private Equity Data Rooms

- Fundraising Data Rooms

- Due Diligence Solutions

- Family Office Solutions

- Dynamic Watermarking

- Screenshot Protection

- Page-Level Analytics

You might also like

Apr 20, 2026

12 Manufacturing Capital Partners Funding Independent Sponsors in 2026

Apr 16, 2026

The 22 Independent Sponsor Conferences & Forums in 2026

Apr 16, 2026

Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026