Independent Sponsor Data Room Checklist (42 Documents, 3 Stages) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

I used to work in venture capital at Backed VC and Target Global. Now I run Peony, a data room platform. Over the past year, independent sponsors have become our fastest-growing user segment — and I have seen the same pattern repeat in almost every failed capital raise: the data room was missing half the story.

Standard M&A checklists cover company diligence. They list financials, legal documents, tax filings, customer contracts — the 174 document types that any buyer requests in any deal (see our complete due diligence checklist for the full list). But independent sponsor deals are not standard M&A. Capital partners evaluate both the deal and the sponsor simultaneously. When your data room only tells the deal story and omits the sponsor story, capital partners either pass or take weeks longer to commit.

This checklist covers the 42 documents that capital partners actually need to see in an IS data room — organized not by generic categories, but by the dual-diligence framework that mirrors how capital partners actually evaluate IS opportunities. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide.

TL;DR: Independent sponsors now account for 31% of all platform-sourced closed deals — the highest share of any buyer type (Axial 2026). Capital partners evaluate both the deal AND the sponsor in IS transactions — your data room must tell both stories. 42 documents across 3 categories (sponsor credibility, deal foundation, structure and economics), staged in 3 phases by capital partner type. 73% of M&A advisors say IS deals take longer to close than PE fund deals (Axial 2025). The #1 reason LOIs broke in 2025 was non-QoE diligence findings at 25.3% (Axial Dead Deal Report). A well-organized data room with staged access and fast Q&A is the single most controllable variable in compressing that timeline and preventing deal failure.

The Dual-Diligence Problem

In a traditional PE fund raise, LPs evaluate the team and strategy — not a specific deal. In sell-side M&A, buyers evaluate only the target company. In independent sponsor deals, capital partners evaluate both simultaneously:

- The deal: Company financials, market position, competitive landscape, management quality, growth potential, risk factors

- The sponsor: Track record, operational capability, sector expertise, process discipline, trustworthiness

- The thesis: Why this deal, why now, and why this sponsor is uniquely positioned to execute

"We are not just evaluating the deal, we are evaluating the sponsor's process." — Grant Kornman, Partner at Align Collaborate (Citrin Cooperman)

This means every IS data room must answer two questions from the first click: Is this a good company to buy? and Is this a good sponsor to back? Most data rooms answer only the first question. The sponsors who close capital fastest answer both — in the folder structure itself.

Repeat capital partner relationships account for 59% of IS deals (Citrin Cooperman 2025). First impressions in the data room are how those repeat relationships start.

The 12 Documents Standard M&A Checklists Miss

These documents are unique to independent sponsor transactions. You will not find them in Bloomberg Law's 174-item DD checklist, in any generic data room template, or in most VDR provider folder structures. They exist because capital partners need to underwrite the sponsor — not just the company.

1. Sponsor Track Record Deck

What it is: A structured summary of your deal history — entry multiples, hold periods, exit outcomes, and realized returns (IRR and MOIC). If you have fewer than 3 completed transactions, include your professional track record: relevant operating roles, advisory engagements, board seats, and sector-specific experience.

Why capital partners need it: Family offices and SBICs will not commit capital to a sponsor they cannot underwrite. This is the first document most capital partners open. According to Citrin Cooperman, 74% of IS report returns of 3x or more to investors and 37% achieve 5x or more — but capital partners need to verify your specific numbers, not industry averages.

2. 100-Day Value Creation Roadmap

What it is: A post-close operating plan with specific milestones — revenue initiatives, cost optimization, management upgrades, technology investments, and add-on acquisition targets — mapped to a 100-day timeline with measurable KPIs.

Why capital partners need it: This document proves you have an operational thesis, not just a financial one. "Buy it cheap and hope it grows" is not a plan. Capital partners want to see exactly what changes on Day 1, Day 30, Day 60, and Day 100.

3. Capital Structure Proposal

What it is: The complete capital stack breakdown — senior debt, mezzanine, SBIC subordinated debt, sponsor equity, capital partner equity, seller paper, and earn-out components. Includes sources and uses, leverage ratios, and debt service coverage.

Why capital partners need it: Capital partners need to understand their position in the stack before committing. A family office writing a $5M equity check evaluates the deal differently when senior debt is 3x EBITDA versus 4.5x. SBICs need to see how their 2-to-1 debenture leverage fits within the overall structure.

4. Governance Term Sheet

What it is: Board composition (who gets seats), protective provisions (what requires capital partner approval), consent rights (major decisions requiring sign-off), information rights (what gets reported and when), and removal/replacement mechanics.

Why capital partners need it: Governance terms determine whether capital partners are partners or passengers. 72% of IS are required to contribute personal equity alongside capital partners (Citrin Cooperman 2025), but the governance framework determines how that alignment actually works in practice.

5. Promote and Carry Schedule

What it is: The tiered carried interest structure with hurdle benchmarks. Typical structures: 10% carry after 1-2x MOIC, increasing to 15-20% after 2-3x, and 25%+ above 3-4x. Include whether hurdles are MOIC-based (now preferred by 50% of IS, up from 27% in 2019) or IRR-based.

Why capital partners need it: Economics alignment is the #1 negotiation point between sponsors and capital partners. 53% of experienced IS say negotiating economics is easier now versus 3-5 years ago (Citrin Cooperman 2025), but that does not mean capital partners will accept whatever you propose. Having the schedule in the data room from day one signals transparency.

6. Broken-Deal Fee Agreement

What it is: The cost allocation framework if the transaction does not close. Specifies who pays for legal fees, QofE costs, travel, and other broken-deal expenses. May include a pre-negotiated cap or a staged allocation (sponsor covers costs before partnership formation; capital partner covers costs after).

Why capital partners need it: 32% of IS cover broken-deal costs themselves (Citrin Cooperman 2025). The remaining 68% share costs with capital partners in various structures. Having this documented upfront prevents disputes that sour relationships — especially important when 59% of deals come from repeat partnerships.

7. Co-Investment Term Sheet

What it is: The subscription agreement template or term sheet governing the capital partner's investment — commitment amount, funding mechanics, closing conditions, representations, and transfer restrictions.

Why capital partners need it: Capital partners need their legal counsel to review terms before committing. Delays from negotiating subscription terms after verbal commitment are one of the most common timeline killers in IS deals.

8. Capital Partner Reporting Framework

What it is: The reporting cadence (monthly, quarterly), format (financial statements, KPI dashboards, narrative updates), and distribution method you will use post-close.

Why capital partners need it: Capital partners are investing in a specific deal with a specific sponsor — they expect regular, professional reporting. This document signals operational maturity. Sponsors who cannot articulate their reporting process rarely maintain the discipline post-close.

Additional IS-Specific Documents

- Prior deal case studies (2-3 completed transactions with entry thesis, execution, and outcome)

- Personal financial commitment disclosure (GP commit amount, fee rollover structure, vesting terms)

- Professional network and advisor bench (legal counsel, accounting firm, operational consultants)

- Exit strategy framework (target hold period, exit scenarios, projected return ranges)

The Complete IS Data Room Checklist: 42 Documents

Organized by the dual-diligence framework — sponsor credibility first, then deal foundation, then deal structure and economics. This mirrors how capital partners actually evaluate IS opportunities.

For the comprehensive 174-document M&A diligence list, see our due diligence data room checklist. For healthcare-specific documents, see our healthcare IS capital partners guide. For business services-specific documents, see our business services IS capital partners guide.

Section A: Sponsor Credibility (8 Documents)

These documents answer: Is this a good sponsor to back?

- Sponsor track record deck (deal history, entry/exit multiples, hold periods, realized returns)

- Team biographies and organizational chart (operating partners, advisors, functional experts)

- Prior deal case studies (2-3 transactions with entry thesis, execution narrative, and outcome)

- Capital partner references (prior co-investors willing to be contacted)

- Personal financial commitment structure (GP commit amount, fee rollover, vesting schedule)

- 100-day value creation roadmap (post-close operating plan with measurable milestones)

- Capital partner reporting framework (cadence, format, KPIs, distribution method)

- Professional network and advisor bench (legal, accounting, operational consultants)

First-time sponsors: If you do not have prior deal exits, substitute the track record deck with a professional experience summary emphasizing relevant operating roles, advisory engagements, and sector-specific expertise. The 100-day plan and reporting framework become even more important — they are the primary evidence of your process discipline.

Section B: Deal Foundation (20 Documents)

These documents answer: Is this a good company to buy?

Investment Thesis:

- Confidential Information Memorandum (CIM) or investment memo

- Executive summary (1-2 page deal overview for initial screening)

- Market and industry analysis with addressable market sizing and competitive landscape

Financial:

- Historical financial statements (3-5 years, audited if available)

- Monthly or quarterly financials (trailing 24 months minimum)

- Quality of earnings analysis (see QofE timing guidance in FAQ below)

- Financial model with assumptions and downside scenarios

- Working capital analysis with normalization adjustments

- Accounts receivable aging by customer

Commercial:

- Customer concentration analysis (top 10 customers by revenue percentage)

- Contract portfolio with renewal dates, terms, and change-of-control provisions

- Pipeline or backlog data (if applicable)

- Management team presentations and individual bios

Legal:

- Material contracts (vendor, customer, lease, and partnership agreements)

- IP portfolio, assignments, and protection status

- Litigation history and pending matters

- Regulatory compliance status and industry-specific certifications

Operational:

- Organizational chart with headcount by department

- Key employee agreements, retention terms, and non-compete status

- Technology stack and systems overview

Note: This is the IS-prioritized subset. The full 174-document list in our due diligence checklist covers additional items across 10 categories including tax (see our tax due diligence checklist), HR, security, and operations in granular detail.

Section C: Deal Structure and Economics (14 Documents)

These documents answer: How is this deal structured and what are my economics?

- Capital structure proposal (equity, senior debt, mezzanine, seller paper, earn-out breakdown)

- Sources and uses statement

- Governance term sheet (board composition, consent rights, protective provisions, information rights)

- Promote and carry schedule with hurdle tiers (MOIC or IRR benchmarks)

- Management fee structure and calculation basis

- Closing fee disclosure and rollover terms

- Broken-deal fee agreement (cost allocation framework)

- Co-investment term sheet or subscription agreement template

- Side letter terms (for capital partners requesting custom provisions)

- Debt term sheet or commitment letter (if financing secured or in progress)

- Seller transition agreement (employment terms, non-compete, earn-out structure)

- Insurance coverage summary (D&O, reps and warranties, key person)

- Tax structure analysis (entity structuring, QSBS eligibility under Section 1202 — the July 2025 One Big Beautiful Bill Act expanded QSBS with a tiered holding period of 3/4/5 years, raised the asset threshold from $50M to $75M, and increased the per-issuer gain exclusion from $10M to $15M)

- Exit strategy framework (target hold period, exit scenarios, projected return ranges)

How to Think About Staging Your IS Data Room

Not every IS deal requires the same data room structure. The right staging approach depends on your capital partner count, relationship depth, and deal complexity.

If you have 1-2 repeat capital partners who have backed your prior deals: Combine Stage 1 and Stage 2. Your repeat partners do not need the staged screening process — they already trust your process discipline. Gate only Stage 3 (governance terms, subscription documents, promote schedules) until they express commitment.

If you are running a competitive process with 5 or more capital partners: Use full 3-stage gating. Stage 1 screens for genuine interest. Stage 2 separates serious partners from browsers. Stage 3 protects sensitive economics from partners who will not proceed. Track engagement with page-level analytics to identify which partners are genuinely diligencing versus passively reviewing.

If your lead capital partner is an SBIC: Add an SBIC regulatory layer to Stage 2 — SBA licensing documentation, small business eligibility verification, leverage structure analysis showing the 2-to-1 debenture ratio. SBICs are now the fastest-growing IS capital partner type, funding 53% of IS deals in 2025, up 19 percentage points over three years (Citrin Cooperman 2025). Note: the SEC's March 2025 no-action letter eased Rule 506(c) accredited investor verification — issuers can now rely on minimum investment amounts ($200K for individuals, $1M for entities) as a reasonable verification step, simplifying the capital partner onboarding process.

If you are a first-time sponsor: Over-index on sponsor credibility documents in Stage 1. Your track record deck, 100-day plan, and governance framework are more important than a polished CIM when you do not have prior deal exits to point to. Capital partners evaluating first-time sponsors scrutinize process discipline more heavily than financial model assumptions.

If your deal is in healthcare: Add sector-specific documents (payer mix analysis, CPOM compliance, HIPAA documentation, provider credentialing). See our healthcare IS capital partners guide for the complete healthcare overlay.

If your deal is in business services: Add sector-specific documents (customer concentration by contract type, employee classification review, recurring vs. project revenue split). See our business services IS capital partners guide for the complete business services overlay.

The 3-Stage Capital Partner Diligence Playbook

Capital partners typically need 3 to 4 weeks for proper diligence. The staged approach below protects sensitive information while keeping serious partners moving. This staging is specific to IS capital partner diligence — for generic M&A staged disclosure, see the staged disclosure framework in our due diligence checklist.

Stage 1: Initial Risk Scan (Days 1-7)

Who sees this: All capital partners who sign the NDA.

Documents shared:

- Sponsor track record deck and team bios (Section A)

- CIM, executive summary, and market analysis (Section B — Investment Thesis)

- High-level financials: trailing 12-month revenue, EBITDA, and growth trend (Section B — Financial)

- Capital structure proposal and sources and uses (Section C)

- 100-day value creation roadmap (Section A)

Purpose: Capital partners determine if the opportunity fits their thesis and if the sponsor is credible. Most partners who will ultimately pass do so after Stage 1. A clean, professional Stage 1 experience — organized folders, named documents, immediate NDA-gated access — signals the process discipline that capital partners reward with faster Stage 2 commitment.

Capital partner actions: Review materials, schedule initial call with sponsor, decide whether to proceed to deep dive.

Stage 2: Deep Dive (Days 7-21)

Who sees this: The 3-5 capital partners who express serious interest after Stage 1.

Additional documents shared:

- Quality of earnings analysis (Section B — Financial)

- Detailed financial model with assumptions (Section B — Financial)

- Working capital analysis and AR aging (Section B — Financial)

- Customer concentration and contract portfolio (Section B — Commercial)

- Management presentations (Section B — Commercial)

- Material contracts and legal documents (Section B — Legal)

- Key employee agreements and org chart (Section B — Operational)

- Governance term sheet preview (Section C)

Purpose: Capital partners conduct substantive diligence on the company and begin evaluating deal terms. This is where most capital partner questions arise. A well-organized Stage 2 with fast Q&A turnaround compresses this from 14 days to 7-10 days.

Capital partner actions: Schedule management meeting, review financials in detail, engage legal counsel, submit diligence questions.

Stage 3: Commitment (Days 21-28)

Who sees this: The 1-2 capital partners moving to commitment.

Additional documents shared:

- Promote and carry schedule with hurdle tiers (Section C)

- Closing fee and management fee structure (Section C)

- Co-investment term sheet and subscription agreement (Section C)

- Side letter terms (Section C)

- Broken-deal fee agreement (Section C)

- Debt term sheet or commitment letter (Section C)

- Exit strategy framework (Section C)

- Tax structure analysis (Section C)

- Insurance coverage summary (Section C)

- Seller transition agreement (Section C)

Purpose: Final economics, governance, and legal terms for capital partners and their counsel to review. Gating these documents until Stage 3 prevents capital partners who will not proceed from accessing sensitive sponsor economics.

Capital-Partner-Type Access Matrix

Different capital partner types diligence differently. Family offices prioritize sponsor evaluation. SBICs need regulatory documentation. PE co-investors diligence like buyers. Understanding these differences lets you customize the data room experience by partner type.

| Document Category | Family Office | SBIC | PE Co-Investor | HNWI |

|---|---|---|---|---|

| Sponsor credibility | Stage 1 (first priority) | Stage 1 | Stage 1 | Stage 1 (primary focus) |

| Investment thesis | Stage 1 | Stage 1 | Stage 1 | Stage 1 |

| High-level financials | Stage 1 | Stage 1 | Stage 1 (deep from day 1) | Stage 2 (simplified) |

| Detailed financials and QofE | Stage 2 | Stage 2 | Stage 1 (they diligence like a buyer) | Stage 2 (summary) |

| Legal and contracts | Stage 2 | Stage 2 | Stage 2 | Stage 3 (counsel-led) |

| SBA regulatory documents | N/A | Stage 2 (required) | N/A | N/A |

| Governance and economics | Stage 3 | Stage 3 | Stage 2 (they negotiate early) | Stage 3 |

| Subscription documents | Stage 3 | Stage 3 | Stage 3 | Stage 3 |

Family offices (62% of IS deals) evaluate the sponsor first. If the track record and 100-day plan are compelling, they move fast — some commit within 2 weeks. If sponsor credibility documents are missing, they assume you are hiding a weak record.

SBICs (53% of IS deals, fastest-growing) need everything family offices need plus SBA-compliant documentation. Factor an extra 3-5 days for their regulatory review. SBICs provide unique value through 2-to-1 leverage on SBA debentures, but the documentation requirements are real. The SBA finalized SBIC regulatory reforms effective February 2, 2026 — streamlined licensing for subsequent funds, critical industry incentives, and removed obsolete provisions. SBIC applications surged to 127 in fiscal year 2024 (3.5x the prior five-year average), signaling growing capital availability for IS deals.

PE co-investors diligence like buyers, not like LPs. They want full financials and the QofE in Stage 1, not Stage 2. They evaluate governance terms earlier in the process and negotiate harder on promote structures. Expect more detailed questions on the financial model.

High-net-worth individuals (55% of IS deals) typically rely more on the sponsor relationship and simplified materials. Full financial detail is less important than a clear thesis and strong governance protections. Their legal counsel handles the deep review in Stage 3.

Multi-Capital-Partner Q&A Management

The hardest operational challenge in IS capital raises is managing questions from 5-20 capital partners simultaneously during a 3-4 week diligence window. Every day lost to slow Q&A response is a day off the exclusivity clock.

Why Email Fails

When capital partners email questions individually, you get:

- 10 separate threads with overlapping questions

- Inconsistent answers when you respond to the same question differently at different times

- No audit trail for who asked what and when

- Hours of duplicate work answering "What was trailing EBITDA?" for the fifth time

The Centralized Q&A Workflow

The best practice is a single Q&A channel where:

- Capital partners submit questions through the data room

- All questions appear in one dashboard with partner attribution

- Approved answers become visible to all authorized partners at that stage

- The Q&A library grows with each question — subsequent partners find answers without asking

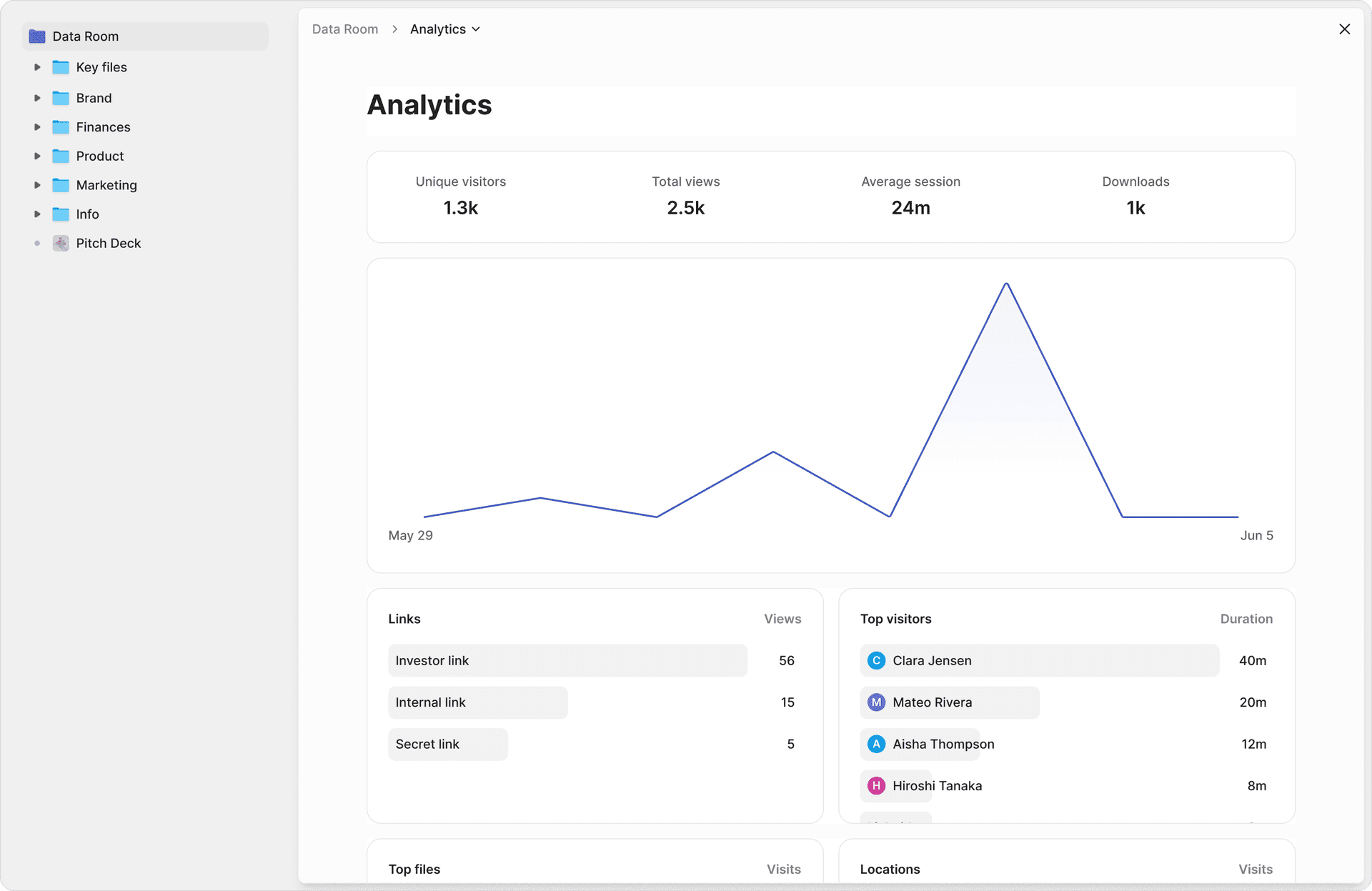

Peony Smart Q&A on the Data Room plan adds an AI layer: capital partners submit a question, AI drafts an answer using your uploaded documents with exact page citations, you review and approve before anything is sent. The approved answer library eliminates 60-80% of repetitive questions from new capital partners entering the process.

For the direct extraction mode on Data Room, capital partners query the document set themselves — "What was 2025 adjusted EBITDA?" returns "$4.2M — Quality of Earnings report, page 7." Objective financial facts surfaced instantly, no sponsor bottleneck.

5 Data Room Mistakes That Lose Capital Partner Interest

Axial's 2025 Dead Deal Report analyzed 75 broken LOIs and found that non-QoE diligence findings killed 25.3% of deals — more than doubling QoE EBITDA discrepancies at 21.3%. Renegotiation challenges accounted for 14.7%, and seller decisions for 13.3%. Many of these failures trace back to data room problems: missing documents that surface late, disorganized materials that slow diligence, and poor Q&A processes that erode capital partner confidence.

1. Missing Sponsor Credibility Documents

When a capital partner opens your data room and finds only company financials — no track record deck, no 100-day plan, no governance framework — they assume you are either a first-time sponsor who does not understand the process or a sponsor who is hiding a weak record. This is the most common mistake, and it happens because sponsors build data rooms from generic M&A templates that do not include sponsor-evaluation documents.

2. Flat Access (No Staged Disclosure)

Giving every capital partner access to everything — including promote terms, governance details, and subscription agreements — before they have expressed serious interest is operationally wasteful and strategically harmful. Partners who ultimately pass now know your economics. Use staged folder permissions to gate sensitive documents behind commitment milestones.

3. Stale Financials

Monthly financials more than 60 days old signal that the sponsor is not actively managing the diligence process. Capital partners evaluating a $30M deal expect trailing financials current within 30 days. If your monthly close takes 3 weeks, adjust your timeline expectations — do not upload stale numbers hoping nobody notices.

4. No Q&A Workflow

Managing capital partner questions through email creates chaos at exactly the moment when you need precision. A missing or slow Q&A process is the second most common reason diligence timelines extend beyond the exclusivity window.

5. Missing Governance and Economics Documents

Capital partners should not have to ask for the promote schedule, governance terms, or broken-deal fee framework. If these documents are absent from the data room (even in gated Stage 3 access), capital partners assume the terms are not yet defined — which signals either inexperience or an attempt to negotiate under time pressure.

Setting Up Your IS Data Room

A well-structured IS data room should be operational in hours, not days. The setup process:

- Upload all available documents — AI auto-indexing organizes uploads into a professional folder structure in under 3 minutes

- Create 3 folder groups matching the staging framework (Stage 1 / Stage 2 / Stage 3)

- Set per-folder permissions so capital partners start with Stage 1 access only

- Generate personalized sharing links for each capital partner with NDA gates requiring signature before access

- Enable Smart Q&A so capital partners can submit questions through the platform

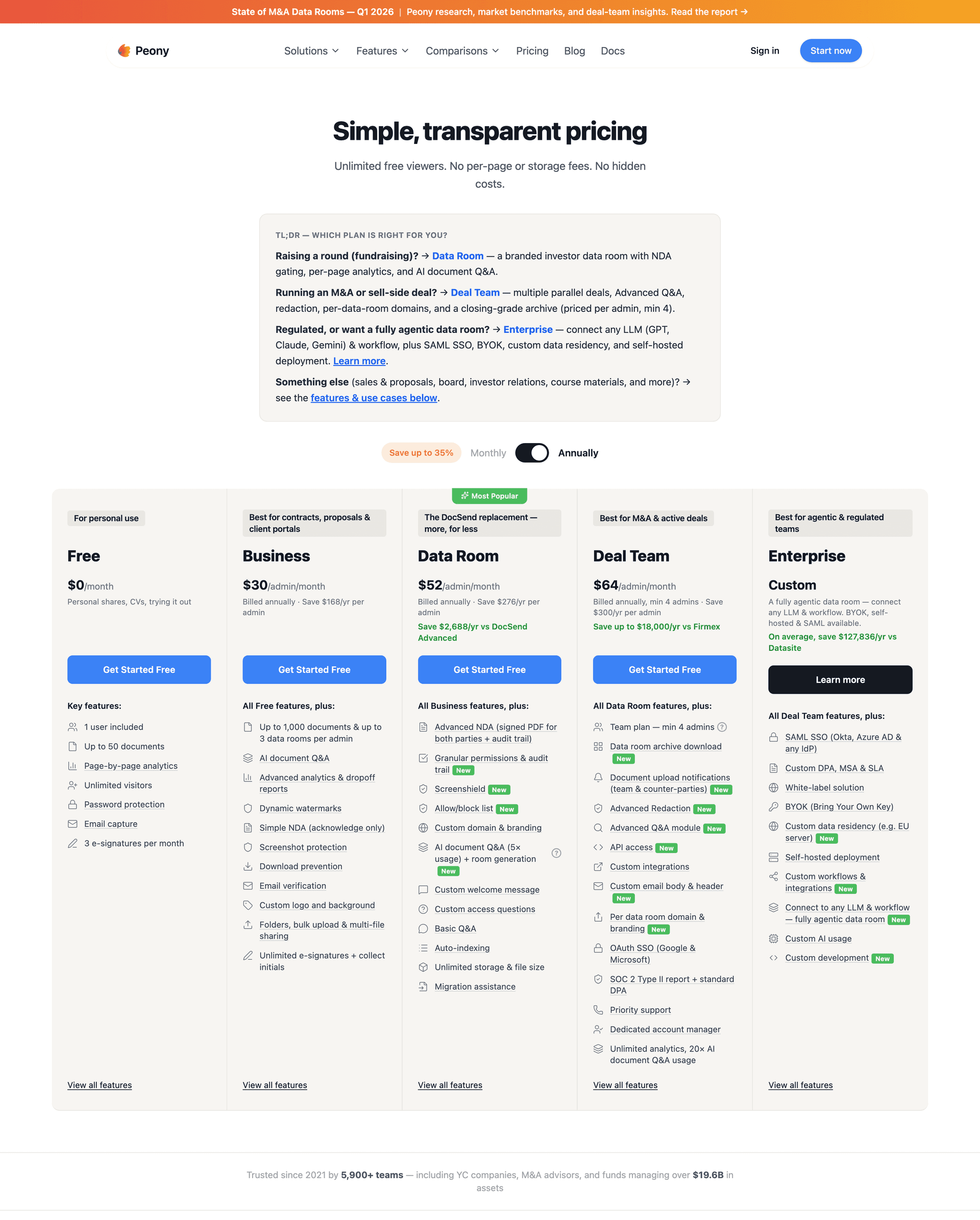

Active IS (3 or more deals per year): Peony Data Room at $52/month per admin includes everything in the staging playbook above — AI auto-indexing, Smart Q&A with human-in-the-loop, NDA gates, dynamic watermarks, screenshot protection, and page-level analytics. This replaces $15,000-$50,000/deal legacy VDR contracts while giving capital partners a faster, more professional diligence experience. Business at $30/month per admin covers core data room functionality with personalized links and analytics for sponsors running fewer concurrent deals.

Emerging IS (first or second deal): Start with Peony's free tier to get your first data room live. Upload your documents, share with capital partners, and upgrade to Business when you need AI-powered Q&A, screenshot protection, and staged access controls.

Set up your first independent sponsor data room in under 5 minutes — get started.

FAQ

I am a first-time independent sponsor raising $5M equity for a services acquisition — how many documents should my data room have?

A well-prepared independent sponsor data room contains 40 to 50 documents across three categories: sponsor credibility, deal foundation, and deal structure and economics. For a $5M equity raise on a services company, your capital partners will expect all three categories from day one. First-time sponsors often under-prepare sponsor credibility documents because standard M&A checklists do not include them. Even without prior deal exits, you should include your professional track record showing relevant operating or advisory experience, a detailed 100-day value creation plan, your capital partner reporting framework, and your governance term sheet. Capital partners evaluating first-time sponsors scrutinize process discipline more heavily than repeat sponsors with established track records. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes your uploaded documents into a professional folder structure in under 3 minutes — something Dropbox and Google Drive cannot do because they have no document classification layer.

Our family office co-invests on independent sponsor deals — what do we look at first in a data room?

Family offices typically evaluate sponsor credibility documents first before reviewing deal financials. The sponsor track record deck and prior deal case studies tell you whether this sponsor has the operational capability to execute the thesis. Family offices funded 62% of all independent sponsor transactions in 2025 according to Citrin Cooperman, and repeat relationships account for 59% of capital partner deals. After clearing the sponsor, family offices focus on the quality of earnings report, customer concentration analysis, and the 100-day value creation roadmap. Peony page-level analytics on the Data Room plan show sponsors exactly which pages you spent the most time on and for how long — something Dropbox and Google Drive cannot track at the document-page level. A well-organized data room with clear sponsor credibility materials up front signals professionalism before you even schedule a management meeting.

How do I stage data room access when I have 8 capital partners looking at the same $30M deal?

Use three-stage gating with per-partner tracking. Stage 1 shares the investment thesis, sponsor deck, and high-level financials with all 8 partners through NDA-gated links. Stage 2 opens detailed financials, quality of earnings, and legal documents to the 3 to 5 partners who express serious interest after 5 to 7 days. Stage 3 releases governance terms, promote schedules, and subscription documents only to the 1 to 2 partners moving to commitment. This staged approach protects your sensitive deal economics from partners who may not proceed while keeping serious partners moving through diligence efficiently. On Peony Data Room at $52 per admin per month, personalized sharing links track each of your 8 capital partners separately and you expand their access stage by stage without creating separate data rooms — something Google Drive and Dropbox cannot do because they have no per-user staged permissions or engagement tracking.

I am building my first IS data room for a $25M manufacturing acquisition — what documents should I include that a standard M&A checklist will not?

Standard M&A checklists miss approximately 12 documents that your capital partners will expect in a $25M manufacturing IS deal. These include the sponsor track record deck with deal history and returns, 100-day value creation roadmap, capital structure proposal showing the debt equity and seller paper breakdown, governance term sheet specifying board composition and consent rights, promote and carry schedule with hurdle tiers, broken-deal fee agreement, co-investment term sheet, and capital partner reporting framework. These documents exist because your capital partners evaluate both the deal and the sponsor simultaneously — which is fundamentally different from traditional M&A where the buyer evaluates only the company. On Peony Data Room, you can structure your data room to separate sponsor credibility documents from deal documents so capital partners navigate the dual-diligence process intuitively — generic VDR providers like Datasite use sell-side M&A folder templates that do not account for sponsor-evaluation documents.

We signed the LOI on a $40M services company and have 90 days of exclusivity — how long should capital partner diligence take and what compresses the timeline?

Capital partners typically need 3 to 4 weeks for proper diligence including management meetings, market assessment, and financial review. For a $40M services deal with 90 days of exclusivity, that means your capital partners need to complete their work in under a quarter of your total runway. The most effective timeline compression comes from data room organization and Q&A speed, not from cutting corners on diligence itself. According to Axial, 73% of M&A advisors say independent sponsors take longer to close than PE funds, primarily due to post-LOI capital assembly. A professionally structured data room with staged access and fast Q&A response times can compress the capital partner decision from 4 weeks to 2 to 3 weeks. Peony AI-powered Q&A on the Data Room plan lets capital partners ask questions against your uploaded documents and get cited answers with exact page numbers — compared to Datasite where Q&A workflows require manual document searching and cost $15,000 or more per deal.

I am an SBIC evaluating a $15M independent sponsor deal — what additional documents do I need beyond standard diligence?

For your $15M deal, you will need SBA-compliant documentation that other capital partner types do not require. Beyond the standard IS data room checklist, request the SBA licensing and regulatory compliance documentation, leverage structure analysis showing the 2-to-1 debenture ratio, small business eligibility verification confirming the target meets SBA size standards, and the proposed debt structure showing how your SBIC subordinated debt fits within the capital stack. SBICs funded 53% of IS deals in 2025, up 19 percentage points over three years according to Citrin Cooperman, making them the fastest-growing capital partner type. Peony Data Room per-folder permissions let the sponsor gate your SBIC-specific regulatory documents separately from the main diligence materials, keeping the data room clean for non-SBIC partners reviewing the same deal — compared to legacy platforms where creating separate permission groups typically requires enterprise pricing and multi-day configuration.

We are pursuing a $35M services acquisition and our lead capital partner wants a QofE — should I commission it before or after signing the LOI?

Commission the quality of earnings before signing the LOI if your deal budget allows it. QoE EBITDA discrepancies were the number 2 reason LOIs broke in 2025 at 21.3% according to the Axial Dead Deal Report, more than doubling from 10.6% in 2023 — and 63% of buyers discover material financial discrepancies during diligence not apparent in initial disclosures. Pre-LOI QofE reports cost $30,000 to $75,000 for typical IS deals in the $10M to $50M enterprise value range, but they dramatically accelerate capital partner diligence because partners can evaluate adjusted EBITDA from day one rather than waiting 3 to 4 weeks for the report to be completed during the exclusivity window. Sponsors who enter diligence with a QofE already uploaded to the data room signal process discipline that capital partners reward with faster commitments. If budget constraints force a post-LOI QofE, upload preliminary financial analysis and management-prepared adjustments to Stage 1 so capital partners can begin their assessment while the formal report is underway. Peony AI document extraction lets capital partners query the QofE directly and get cited answers with page numbers, reducing follow-up questions that slow the process.

I lost a capital partner on my last deal and think my data room was the problem — what is the most common mistake that kills capital partner interest?

The most common mistake is missing sponsor credibility documents. When a capital partner opens your data room and finds only company financials — with no sponsor track record, no 100-day plan, no governance framework, and no capital structure proposal — they assume you are either a first-time sponsor who does not understand the process or a sponsor who is hiding a weak track record. Either perception kills interest. Capital partners evaluate both the deal and the sponsor simultaneously, according to Grant Kornman of Align Collaborate, and the data room is the first evidence of your process discipline. The second most common mistake is flat access where every partner sees everything including sensitive promote terms and governance details before expressing serious interest. Peony NDA gates and staged folder permissions prevent both mistakes by enforcing structured disclosure from day one.

How do I handle capital partner Q&A when 10 partners are reviewing my data room at the same time?

Centralize all Q&A through a single workflow rather than managing 10 separate email threads. When your capital partners email questions individually, you lose version control, risk inconsistent answers, and spend hours repeating the same information. The most effective approach for your deal is a structured Q&A system where partners submit questions through the data room platform, you see all questions in one dashboard, and approved answers become visible to all your authorized partners. This eliminates duplicate questions and ensures every partner receives the same vetted information. Peony Smart Q&A on the Data Room plan lets your capital partners submit questions directly in the data room, AI drafts answers using your uploaded documents with exact page citations, you review and approve before anything is sent, and the approved answer library grows with each question so subsequent partners find answers without asking — replacing the email chaos that Dropbox and Google Drive force you into because they have no built-in Q&A workflow.

I run 3 to 4 IS deals per year in the $15M to $50M range — what is the best data room for deal-by-deal acquisitions?

Peony is purpose-built for independent sponsor deal flow. Legacy data rooms like Datasite charge $15,000 to $50,000 per deal, which is disproportionate for sponsors targeting $10M to $75M enterprise value companies who cannot amortize VDR costs across a committed fund. Peony Data Room at $52 per admin per month includes AI auto-indexing, Smart Q&A with human-in-the-loop, NDA gates, dynamic watermarks, screenshot protection, and page-level analytics. Business at $30 per admin per month covers core data room functionality. Setup takes under 5 minutes versus days or weeks for legacy platforms. The AI-powered Q&A workflow lets capital partners submit diligence questions, AI surfaces relevant document sections with exact page citations, and the sponsor reviews before responses are sent. Page-level analytics show which capital partners are genuinely engaged, and personalized sharing links track each partner separately across the same data room.

Related Resources

- Oil and Gas Data Room Checklist — 42 documents across 12 canonical folders, FEED-to-FID file mass, and 4-tier farm-out access matrix

- What Is an Independent Sponsor? Complete Guide — IS mechanics, economics, capital assembly, exclusivity windows

- Independent Sponsor Deal Book (10 Sections) — the capital partner deal book these 42 documents populate

- Independent Sponsor LOI Playbook — 90-day timeline governing when each document releases

- Independent Sponsor Capital Raising Playbook — pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall, and the five Excel mistakes that get models rejected

- Different Passwords for Different Investors — per-LP personalized links, individual passwords, dynamic watermarks, and one-click revoke across 5-15 capital partner shares with forensic attribution per leaked page

- Due Diligence Checklist (174 Documents) — comprehensive M&A diligence across 10 categories

- Healthcare IS Capital Partners — 17 healthcare firms with sector-specific data room overlay

- Business Services IS Capital Partners — 15 business services firms with sector-specific data room overlay

- Tax Due Diligence Checklist — 8-pillar tax DD framework

- Investment Due Diligence Checklist — buyer-side 7-pillar framework

- Data Room Folder Structure Guide — organizing documents for any deal type

- Best Data Rooms for Private Equity — VDR platform comparison

- Peony for Private Equity — PE-specific data room features

- Peony for M&A — M&A data room solutions

- Peony for Due Diligence — diligence workflow tools

You might also like

Apr 16, 2026

Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026

Apr 1, 2026

What Is an Independent Sponsor? Complete Guide (27% of All Deals) in 2026

Apr 26, 2026

SBIC for Independent Sponsors: 2026 Leverage Playbook