The Independent Sponsor Capital Raising Playbook (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

I spent years at Backed VC and Target Global evaluating LMM PE and IS deals before starting Peony, a data room platform. Over the past year I have watched hundreds of independent sponsors move through our platform assembling capital stacks, and the single pattern that separates sponsors who close their target at target economics from sponsors who get squeezed on price or lose exclusivity is almost always the same: the capital raising choreography starts 30-60 days before the LOI, not the day after. The sponsors who run the playbook below close with their lead promote intact and a 2-week buffer on the exclusivity clock. The sponsors who skip it lose economics mid-diligence or blow past exclusivity entirely.

This post is the pre-LOI and term-sheet playbook — how to build a capital partner Rolodex, soft-circle partners before signing the LOI, negotiate sponsor economics (promote, carry, fees), design the capital stack for a $10M EBITDA deal, layer SBIC leverage, handle management rollover, and build repeat relationships across vintages. It sits alongside three tactical siblings in our IS cluster that each solve a distinct problem: the independent sponsor hub defines what an IS is and the overall economic model, the LOI playbook runs the 90-day post-LOI timeline and exclusivity management, the deal book guide covers the 10-section capital partner artifact, and the data room checklist lists the 42 documents partners request. This post is distinct from all four — it is the pre-LOI cultivation, term sheet economics, and multi-vintage relationship playbook that sits upstream of the LOI and downstream of the deal book. For vertical-specific capital partner directories see our vertical guides: healthcare, business services, manufacturing, tech/software, consumer, distribution/logistics, and cleantech/energy.

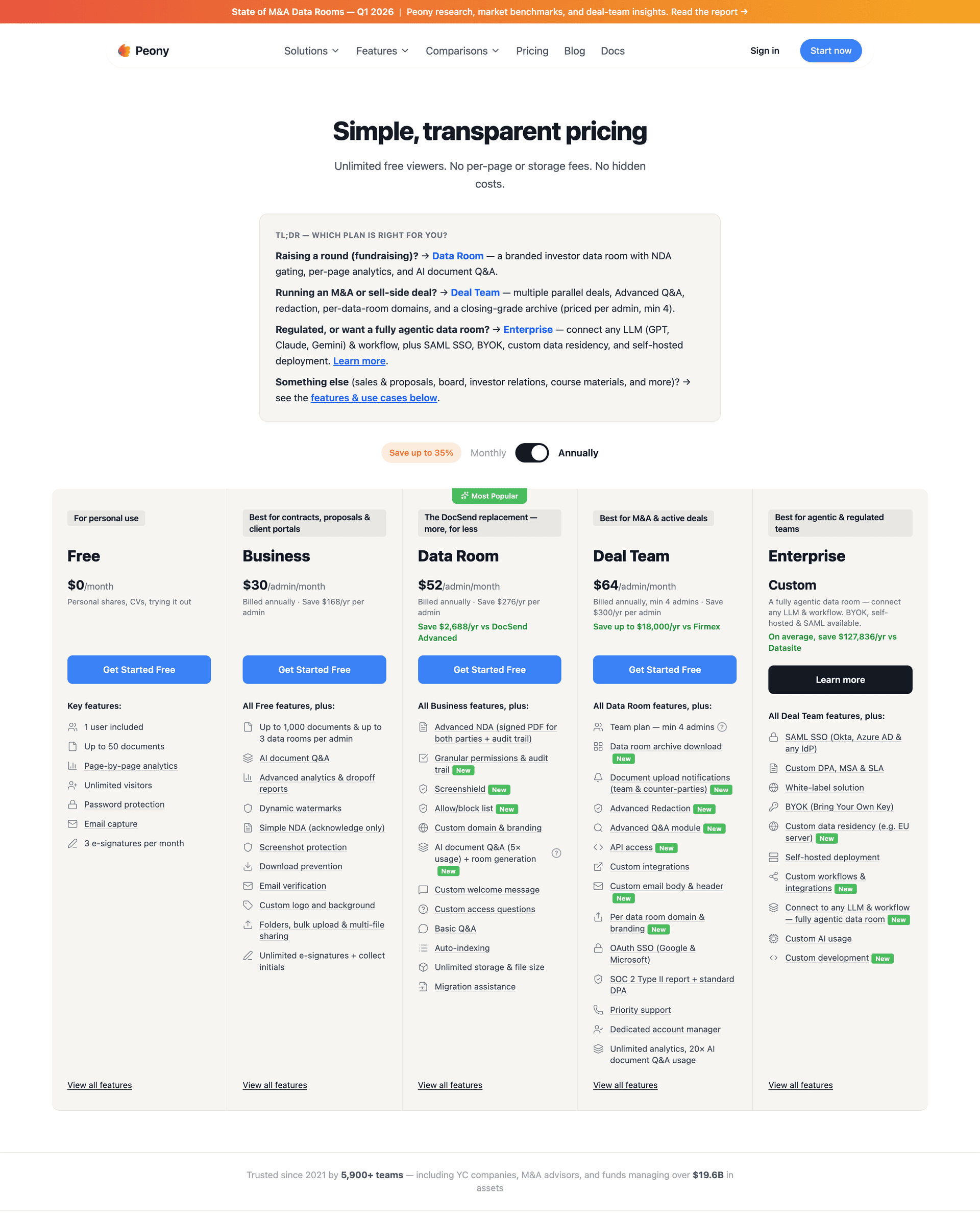

TL;DR: Independent sponsors reached 26.8% of all closed deals on Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 IS Report). 54% of IS transactions still close at 4x-6x EBITDA — lower than broader PE because IS targets sub-scale founder-led businesses (Citrin Cooperman 2025 IS Report). SBIC use grew from 34% to 53% of IS deals over three years (Citrin Cooperman 2025). The median IS sponsor promote runs 15%-25% on tiered waterfall (64% earn 25%+ at max tiers), 59% of capital partner re-engagements are repeat relationships, and 72% of IS are required to contribute 2-5% GP commit per Citrin Cooperman 2025. The 2026 playbook: soft-circle 5-8 capital partners 30-60 days pre-LOI, pre-negotiate economics before exclusivity, stack senior debt at 2.5x-3.5x EBITDA plus SBIC sub-debt at 0.75x-1.5x plus equity, target 15-20% peak promote with MOIC-based tiers and full catch-up, roll management at 10-40% equity with 2-3-year employment commitments, and skip the placement agent if you already have warm partners in sector (21% of IS use agents; 79% DIY per Axial 2025). Peony Data Room at $52/admin/month runs the whole workflow — NDA-gated rooms, personalized links per capital partner, page analytics, AI Q&A, e-signatures — unlimited concurrent rooms for the 5-20 parallel capital partner conversations that IS capital raising actually requires.

The 8-Stage Capital Raising Playbook

Every IS capital raise moves through the same eight stages. The skill is running them concurrently, not sequentially — sophisticated sponsors start stage 2 (soft-circling) 30-60 days before the LOI is signed, and stage 7 (repeat-relationship cultivation) never stops. Here is the framework with anchor links to each section:

| Stage | What Happens | Typical Timeline | Link |

|---|---|---|---|

| 1 | Build your capital partner Rolodex | Ongoing — conferences, platforms, referrals | Jump |

| 2 | Soft-circle capital partners pre-LOI | 30-60 days before LOI signing | Jump |

| 3 | Negotiate IS deal economics (promote, carry, fees) | Pre-LOI to Week 2 post-LOI | Jump |

| 4 | Design the capital stack | Pre-LOI to Week 3 post-LOI | Jump |

| 5 | Layer SBIC leverage | Week 1-4 post-LOI | Jump |

| 6 | Handle management rollover and employment | Week 2-6 post-LOI | Jump |

| 7 | Cultivate repeat capital partner relationships | Vintage to vintage, quarterly updates | Jump |

| 8 | Avoid the five biggest capital raising mistakes | All stages | Jump |

How Do You Build Your First Capital Partner Rolodex?

A usable capital partner Rolodex is 15-25 firms across three categories: IS-explicit equity partners (Peninsula, Align Collaborate, Boyne Capital), SBIC and mezzanine providers (Tecum, Cyprium, Argosy), and family offices or HNWI aggregators. First-time sponsors build this Rolodex in 60-90 days through four sourcing channels.

Conferences are the fastest start. The McGuireWoods Independent Sponsor Conference drew 1,600 attendees in 2025 and sold out all 2026 sponsorships months in advance (McGuireWoods, December 2025) — the 2026 edition runs October 27-28 at the Fairmont Dallas. The SBIA Independent Sponsor Forum meets May 6 in Philadelphia. ACG DealMAX runs April 27-29 in Las Vegas with 2,500+ LMM dealmakers. The iGlobal IS Summit runs June 11 in Dallas and September 28-29 in NYC. For a first-time sponsor, plan two conferences in your first 60 days — one large (MWISC or DealMAX) plus one IS-specific (SBIA ISF or iGlobal) — and schedule 15-25 one-on-ones with capital partners per event. See our complete IS conferences and forums guide for the full 2026 calendar of 21 events.

Axial is the platform anchor. Independent sponsors closed 26.8% of all LMM deals through Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 IS Report). A paid Axial membership surfaces 30-50 capital partners in your target sector within 10 days through their partner-matching flow — faster than any conference networking. 2,635 new buyers joined Axial in 2025, up 36% year-over-year, and the platform's database of 20,000+ LMM acquirers includes a dedicated IS capital partner filter.

Warm referrals compound fastest. Your M&A attorney sees 20-40 IS deals per year and can introduce you to 5-10 capital partners with credibility your cold LinkedIn message cannot match. Your accountant (especially if they work on Q of E reports) sees the capital partner ecosystem from the other side. Your investment banker (if you have one) can broker introductions to 10-20 partners in 2-4 weeks. The Citrin Cooperman 2025 IS Report found that 59% of capital partner re-engagements are repeat relationships — and warm referrals from professional advisors are the fastest path into that repeat ecosystem.

Direct outreach closes the gap. If you have a clean sector thesis (e.g., "HVAC services in the Upper Midwest with $3M-$7M EBITDA targets"), direct outreach to sector-specialist firms works at roughly a 15-25% response rate. Target firms that publicly advertise IS-friendly policies: Peninsula Capital Partners has backed 70+ IS platforms since 1995 with Fund VIII $400M September 2025, Align Collaborate runs an IS-exclusive Fund I at $233M March 2025, and Boyne Capital explicitly targets IS-sourced healthcare deals. For vertical-specific capital partners by sector, see our directories: healthcare, business services, manufacturing, tech/software, consumer, distribution/logistics, and cleantech/energy.

What to ship at first contact. A 1-page sponsor introduction (your background, prior deals, sector thesis), a 3-4-page thesis memo (why this sector now, what company profile you target, what capital structure you expect), and an NDA. Nothing more. You are not pitching a specific deal — you are opening a relationship and signaling process discipline. Peony Business at $30/admin/month lets you share the thesis memo through NDA-gated links with personalized sharing per partner, so you see who actually read the memo versus who just opened the email — critical signal for deciding who to follow up with at conference coffee meetings.

When Should You Soft-Circle Capital Partners Before an LOI?

Soft-circling means sharing deal context with capital partners 30-60 days before you sign the LOI, under NDA, with progressive information release as their interest signals firm up. The practice separates sophisticated sponsors (who run this choreography) from first-time sponsors (who only start outreach after the exclusivity clock is already ticking). Axial's 2025 report found that 55.4% of IS now provide pre-LOI capital support letters — down from 68.2% in 2023 as the market accepts post-LOI capital assembly, but still a majority practice for competitive deals.

The soft-circle timeline runs in three stages that mirror post-LOI diligence:

Stage 1 — 60-45 days pre-LOI (all targeted partners, 2-3 pages): Share a teaser or investment thesis memo naming the sector, target EBITDA range, proposed multiple range, and sponsor fees. No company name, no financials. Purpose: identify which partners have appetite for this sector at this check size. Expect 30-40% of partners to express interest, 20-25% to pass on sector fit, and 40-45% to go silent.

Stage 2 — 45-30 days pre-LOI (interested partners only, 8-12 pages): Under a more specific NDA, share a sector thesis memo, target company description (still anonymized), projected financials, and a draft capital structure. Purpose: get preliminary soft-circle commitments from 3-5 partners on equity and subordinated debt. Your M&A attorney typically drafts a 1-page capital partner term sheet here that names: proposed equity check size, fees, promote tier structure, expected close timing, and broken-deal cost sharing.

Stage 3 — 30-0 days pre-LOI (lead partners only, full deal book draft): Under a deal-specific NDA, share the full deal book draft with the 1-2 partners most likely to lead equity and the 1-2 most likely to provide subordinated debt. Purpose: secure a formal (though non-binding) capital support letter. 39.2% of IS now provide post-LOI support letters (up from 18.2% in 2023) per Axial 2025, so if your lead partner will only sign post-LOI, that is acceptable — but push for at least a verbal commitment before you sign the seller LOI.

NDA management matters at every stage. Each stage uses a progressively more deal-specific NDA. Stage 1 is sector-level (standard 2-year non-disclosure with a specific-purpose clause). Stage 2 is company-adjacent (names the company but redacts seller identity). Stage 3 is deal-specific (names everything). If a capital partner refuses to sign the Stage 2 NDA, they are not a serious candidate — this is a filter, not a formality.

What pre-LOI soft-circling buys you. The sponsors who run this choreography enter their LOI exclusivity with 2-3 partners already 30-50% through diligence. They shorten the 90-day post-LOI timeline to 60-65 days. They write capital partner term sheets that align 80% with the economics their partners eventually sign, instead of negotiating mid-exclusivity under time pressure. And they can offer the seller a capital support letter that signals credible fundless-buyer economics — often the difference between winning and losing a competitive LOI.

Peony's pre-LOI soft-circling workflow. Peony Data Room at $52/admin/month supports NDA gates that trigger before any content is visible, dynamic watermarks with per-partner identity embedded in every page, personalized sharing links that track each partner separately across the same data room, page-level analytics that show which partner spent 30 minutes on the value creation plan versus who never opened the financial model, and unlimited data rooms so you can run soft-circling rooms for deal 6 while your deal 5 capital partners are still in Stage 2 diligence. This is the core workflow legacy VDRs at $25K+ per deal structurally cannot support on deal-by-deal IS economics.

How Do You Negotiate IS Deal Economics (Promote, Carry, Fees)?

IS deal economics have three components that you negotiate with your lead capital partner before the LOI is signed, not after. The Citrin Cooperman 2025 survey of 172 professionals (including 151 IS) documents the current market standard for each component. Hitting these ranges protects your sponsor economics; falling below them leaves money on the table.

Closing fee (transaction fee)

- 82% of IS use a percentage of enterprise value (up from 57% in 2017) per Citrin Cooperman 2025

- 56% charge 2% of EV — this is the de facto standard

- 28% now earn more than $500K per transaction (up from 10% in 2017)

- Sponsors commonly roll 40-80% of the closing fee into equity, signaling alignment

On a $30M acquisition with a 2% closing fee ($600K), the sponsor rolls $400K-$500K into equity and takes $100K-$200K in cash. On a $120M EV deal, a 2% closing fee ($2.4M) with 60% roll means $960K cash and $1.44M in equity — meaningful sponsor capital at risk.

Annual management fee

- 69% charge 5% of EBITDA (up from 49% in 2019) — the de facto standard

- 54% earn $251K-$500K annually (up from 39% in 2018)

- Fees are often subordinated to senior debt and may accrue during tight covenant periods

- Some capital partners push for a 3% floor or $250K annual minimum whichever is higher — acceptable for first-time sponsors

On a $10M EBITDA portfolio company, a 5% management fee is $500K per year — enough to run a 2-3 person IS firm while carrying overhead for the next deal's sourcing. Below $300K annual management fee, you cannot sustain overhead plus a modest salary, which is why first-time IS with sub-$5M EBITDA targets typically need multiple concurrent platforms to hit economic viability.

Carried interest (promote)

This is the component that matters most on deal economics and the one most first-time sponsors underprice.

- Minimum carry firmly in the 10-25% range since 2019

- 64% can earn 25%+ carry at maximum tiers (up from 37% in 2019)

- 71%+ use a variable-with-hurdles model — carry increases as returns exceed thresholds

- Typical hurdle rate: 8-9.9% (63% of respondents)

- Full catch-up now standard at 74% (up from 61% in 2019)

- The shift to MOIC-based hurdles (50%, up from 27% in 2019) over IRR reflects IS preference for absolute returns

Example tiered structure: 10% carry after 1x-2x MOIC (with 8% preferred return), 15% after 2x-3x, 20% after 3x-4x, 25% above 4x, with full catch-up and MOIC-based tiers. On a $25M equity deal exiting at 3.5x MOIC ($87.5M gross proceeds, $62.5M gain), this waterfall earns the sponsor roughly 15-17% blended carry on the full gain — meaningful sponsor economics aligned to multi-tier upside.

GP commit

- 72% of IS are required by capital partners to invest alongside them per Citrin Cooperman 2025

- Typical GP commit: 2-5% of deal equity

- 86% use personal funds for GP commit

- Many sponsors roll 40-80% of closing fee into equity to increase their stake

On a $25M equity deal, a 3% GP commit is $750K — a meaningful personal capital commitment that signals alignment to capital partners. First-time sponsors who cannot fund $250K+ GP commit from personal net worth will struggle with most institutional capital partners (family offices and HNWIs are more flexible).

IS versus PE fund economics

| Component | Independent Sponsor | Traditional PE Fund |

|---|---|---|

| Management fee basis | 3-7% of portfolio EBITDA | 2% of committed capital |

| Management fee timing | Only on active investments | On all committed capital regardless of deployment |

| Carry | 10-30% tiered with hurdles | Typically 20% flat |

| GP commit | 1-5% of deal equity (72% required) | 1-2% of fund size |

| Fee on uncommitted capital | None | Yes (2% annually) |

| Hurdle rate | 8-9.9% typical (MOIC-based) | 8% typical (IRR-based) |

| Closing fee | 2% of EV standard | N/A — built into management fee |

| Catch-up | Full catch-up at 74% of sponsors | Typically full catch-up |

"53% of experienced IS survey respondents believe it's easier to negotiate deal economics with capital providers now versus three to five years ago." — Citrin Cooperman 2025 Report

What to negotiate upfront (before LOI)

Your lead capital partner term sheet must name: (1) your closing fee rate and EV basis; (2) your management fee rate and EBITDA basis; (3) your promote tier structure, hurdle rate, catch-up convention, and IRR-versus-MOIC basis; (4) your GP commit percentage and funding timing; (5) broken-deal cost sharing (what percentage of failed-deal costs your capital partner covers if they walk); (6) co-invest rights (what percentage of the equity check your capital partner can claim alongside you); and (7) key-person provisions (what triggers GP removal and whether your carry cliffs on removal). Sponsors who sign the LOI without locking these seven components typically spend weeks 3-6 post-LOI negotiating economics instead of running diligence — which is how deals die.

Peony Business at $30/admin/month supports e-signatures with AI-powered field detection for capital partner LOIs, NDAs, subscription documents, and side letters — all signed inside the data room. No separate DocuSign account. No version drift across email threads.

How Do You Structure the Capital Stack for a $10M EBITDA Deal?

A $10M EBITDA deal at 7x EV ($70M purchase price) typical stacks as follows. I will walk through a specific worked example so the math is concrete.

The $35M EV / $5M EBITDA worked example

Assume: $5M EBITDA target at 7x EV = $35M purchase price. Capital partner lead is an IS-explicit equity firm. SBIC partner provides subordinated debt. Senior lender is a unitranche provider at 3x EBITDA. Management rolls 20% of post-tax proceeds.

| Capital stack component | Amount | Percentage of EV | Source |

|---|---|---|---|

| Senior debt (unitranche, 3x EBITDA) | $15.0M | 43% | BMO, Huntington, Monroe, Twin Brook |

| SBIC subordinated debt (1x EBITDA) | $5.0M | 14% | Tecum Fund IV, Cyprium SBIC I, Argosy SBIC VII |

| Lead equity capital partner | $7.5M | 21% | Peninsula, Align Collaborate, Boyne Capital |

| Co-invest capital partner | $3.0M | 9% | Family office, HNWI, sector-specialist fund |

| Sponsor GP commit (3%) | $0.5M | 1.4% | Sponsor personal funds |

| Management rollover | $3.0M | 9% | Pre-tax rollover at 20% of proceeds |

| Closing fees (rolled 60%) | $0.7M | 2% | Sponsor closing fee contribution to equity |

| Working capital / transaction costs | $0.3M | 0.8% | Legal, Q of E, advisors |

| Total sources | $35.0M | 100% | = $35M purchase price |

Key structural insights

Senior debt at 3x EBITDA is typical but sector-dependent. Unitranche and first-lien term loans for LMM IS deals run 2.5x-3.5x EBITDA on mature founder-led businesses, pricing at SOFR + 500-600 bps (roughly 10-11% all-in at current rates). Distribution and logistics deals with heavy working capital may cap at 2.5x. Healthcare services with insurance-backed revenue may stretch to 3.5x-4x. See our sector-specific capital partner directories for typical leverage by vertical.

SBIC sub-debt is the cheapest leverage in the stack. SBIC subordinated debt at 1x EBITDA on a 2-to-1 SBA debenture structure costs roughly 10-12% all-in (fixed coupon 8-10% plus warrants or PIK) — cheaper than non-SBIC second-lien or unitranche at 11-14%. SBICs led 18% of IS deals in 2025 per Citrin Cooperman and fund 53% overall, with three specific funds actively writing IS checks in 2026: Tecum Capital Fund IV ($325M SBIC, July 2025 close), Cyprium Partners SBIC I ($190M, February 2025), and Argosy SBIC VII ($175M, 2024 SBA SBIC of the Year).

Equity splits 70/30 between lead and co-invest. On this $10.5M equity check, the lead capital partner writes roughly $7.5M (71%) and a co-invest partner fills the remaining $3M (29%). The co-invest partner is typically a family office, HNWI aggregator, or sector-specialist sub-fund that underwrites the deal on the lead's economics rather than negotiating its own terms.

Sponsor GP commit is 3% of deal equity. On a $10.5M equity check plus $0.5M sponsor commit, the sponsor's GP commit sits at 3% of total equity — within the Citrin 2025 standard of 2-5%. The sponsor's $500K personal capital comes half from cash and half from the closing fee roll ($0.7M closing fee, 60% rolled = $420K into equity, plus $80K of personal cash).

Management rollover fills $3M of the capital need. Management's 20% rollover reduces fresh equity need from $13.5M to $10.5M — critical for deal viability when your equity syndication is tight. Without the rollover, you would need either a larger lead equity check or a third co-invest partner.

Why the stack math matters for deal economics

Your peak promote percentage compounds against the equity portion of the stack, not the whole EV. On this deal, a 20% peak promote on $10.5M equity at 3x MOIC exit ($31.5M gross equity proceeds, $21M gain) earns the sponsor roughly $3.5M at peak tier — before dilution for the LP preferred return and catch-up mechanics. If you add management rollover at 20% and co-invest capital partner at a pro rata economics, the sponsor's blended take settles around $3M-$3.5M on a successful exit.

A weaker stack destroys economics. If the senior lender caps at 2x EBITDA instead of 3x (reducing senior debt from $15M to $10M), you need $5M additional equity or subordinated debt. Adding $5M of equity dilutes your sponsor promote by roughly 50%. Adding $5M of subordinated debt at 12% all-in adds $600K annual interest expense, which reduces distributable cash flow by roughly 4-6% per year — compounding against your free cash flow available for debt paydown and dividend recap.

The capital stack is the single most important artifact in your deal book. Section 8 of our deal book guide covers the sources and uses reconciliation — if your sources and uses do not balance, or if you have not documented the SBIC 2-to-1 debenture calculation, capital partners will pass before reviewing your thesis. Peony Data Room at $52/admin/month supports AI auto-indexing that organizes the senior debt commitment letter, mezzanine term sheet, equity subscription docs, and rollover paperwork in under 3 minutes — capital stack documentation live on day one of exclusivity.

How Does SBIC Leverage Actually Work for Your Deal?

SBIC leverage is the cheapest form of debt capital available to IS deals below $50M EV, and the single fastest-growing capital source in the IS ecosystem. SBIC use in IS deals grew from 34% to 53% over three years per Citrin Cooperman 2025 — a 19-percentage-point jump that reflects both the maturation of the SBIC program and the structural fit with deal-by-deal IS economics. For the full SBIC-specific playbook covering 8 active IS-partner SBICs, the $35M EV worked example, FY2026 fee schedule, debenture covenant scrutiny, and the three biggest mistakes first-time IS make, see our SBIC for Independent Sponsors guide.

How the SBA debenture actually works

An SBIC fund can borrow from the SBA at up to 2-to-1 leverage against its regulatory capital, capped at a maximum of $175M in debenture commitments per fund ($350M combined for affiliated fund families). A $100M SBIC fund has roughly $300M of total deployable capital: $100M equity plus $200M of SBA debentures. The debentures are non-recourse to the fund manager, carry a 10-year maturity with interest-only for the first 10 years and bullet at maturity, and price at a fixed coupon tied to the 10-year Treasury plus a small admin spread (currently 6-7% all-in cost to the SBIC).

What this means for your deal. When your SBIC partner writes a $5M subordinated debt check into your deal, they are deploying roughly $1.7M of their fund's own equity leveraged 2x with SBA-backed debentures. The SBIC's all-in cost of capital on that $5M is roughly 8% (blending their 7% debenture cost on $3.3M with the required return on $1.7M of their fund equity). The SBIC prices your sub-debt at roughly 10-12% all-in (fixed coupon 8-10% plus warrants or PIK), capturing a 2-4% net spread.

Typical SBIC sub-debt tranches in 2026

- Size: $3M-$20M per tranche (larger SBICs like Tecum Fund IV at $325M and Argosy SBIC VII at $175M deploy $5M-$15M checks comfortably)

- Leverage: 0.75x-1.5x EBITDA, sitting between senior debt and equity in the stack

- Pricing: 10-12% all-in (fixed coupon 8-10% plus warrants, PIK, or success fees)

- Tenor: 5-7 years with bullet maturity, interest-only during the hold period

- Collateral: Second-lien on all assets, subordinated to senior

- Covenants: Lighter than senior; typically one debt-to-EBITDA, one fixed charge coverage, and a cash-flow sweep above a leverage threshold

Three active SBIC funds for IS deals in 2026

Tecum Capital Fund IV — $325M SBIC (July 2025 close), Pittsburgh-based with 130+ IS deal track record. Tecum is one of the most IS-dedicated SBIC platforms in the US and writes $5M-$20M subordinated debt plus minority equity checks in LMM buyouts, growth equity, and recaps.

Cyprium Partners SBIC I — $190M (February 2025 close), Cleveland-based with 14+ IS deals completed. Cyprium specializes in minority equity and subordinated debt in LMM IS deals with $3M-$15M EBITDA, typically $3M-$12M check sizes.

Argosy Private Equity SBIC VII — $175M SBIC (2024 SBA SBIC of the Year), with a portfolio including Joliet Electric, Groome Industrial, and Pulse Final Mile (Diverse Logistics Feb 2026). Argosy writes $5M-$15M subordinated debt checks across manufacturing, services, and distribution IS deals.

SBIC size-standard compliance

Not every IS deal qualifies for SBIC capital. The target company must meet SBA size standards for small business eligibility, which typically means one of: (1) average net income under $7M over the trailing 3 years and tangible net worth under $25M, or (2) sector-specific employee or revenue caps. A $50M EV manufacturing deal with $8M EBITDA typically qualifies; a $100M EV healthcare services deal with $12M EBITDA typically does not without careful analysis. Your SBIC partner runs size-standard verification in week 1 of diligence — and sponsors who have not run this analysis pre-LOI can lose 1-2 weeks of exclusivity when the SBIC discovers the deal exceeds size standards and the equity stack has to rebuild without them.

Why SBIC leverage compounds your sponsor economics

The SBIC's cheaper cost of debt capital flows through to the portfolio company's free cash flow, which flows through to equity value at exit. A $5M sub-debt tranche at 10% (SBIC pricing) versus 13% (non-SBIC unitranche pricing) saves $150K per year in interest expense — compounded over a 5-year hold at 7x exit multiple, that is $1.05M of equity value creation (7 × 5 × $150K × 20% tax shield = ~$1.05M). On a $25M equity stack, a $1.05M equity value lift is 4.2% of equity — material compounding on your MOIC math.

SBIC documentation requirements

SBIC-backed deals add 5-7 documents to your data room:

- SBA size standard verification — calculated from three years of financial statements and tangible net worth

- SBIC debenture leverage structure analysis — showing how the sub-debt fits within the fund's 2-to-1 cap

- SBA-approved affiliation analysis — ensuring the target is not affiliated with any large business that would disqualify it

- SBIC Form 1031 eligibility disclosure — if the SBIC is taking equity alongside subordinated debt

- Debt service coverage ratio projection — demonstrating the deal can service the sub-debt through the hold

- SBIC-specific covenant compliance schedule — for the post-close reporting framework

- SBA Form 857 equity/debt allocation — final capital structure confirmation at close

Peony Data Room at $52/admin/month supports per-folder permissions that gate SBIC-specific regulatory materials separately from standard diligence documents — keeping the room clean for non-SBIC partners evaluating the same deal. Firmex at approximately $7,800/year and Ideals at $5,000-$20,000/month enterprise pricing charge add-on fees to configure this workflow.

How Do You Handle Management Rollover and Employment Agreements?

Management rollover is the quietest lever in the capital stack — and the one that most first-time sponsors underprice or over-engineer. On a typical LMM IS buyout, management rolls 10-40% of post-tax proceeds into the new entity's equity, creating an alignment mechanism that reduces fresh equity need while keeping operating leaders economically committed to the thesis. The range is wide because rollover scales with both seller role (founder-CEOs roll higher than non-founder operators) and sponsor strategy (growth-oriented deals push for higher rollover; turnaround deals push for lower).

Typical rollover structures

Founder-CEO rollover (30-40% of post-tax proceeds). A founder who built the company from zero and stays CEO for 2-3 years post-close typically rolls 30-40% — enough to keep them fully invested in the thesis without tying up capital they need for retirement planning. On a $35M deal with the founder taking 70% of equity value ($24.5M), a 35% rollover creates an $8.6M management stake (roughly 24% of the new entity's fully-diluted equity).

Non-founder CEO rollover (15-25%). A professional CEO who joined the company 5-10 years ago but did not build it typically rolls 15-25%. Capital partners are more cautious here because the CEO's exit option is looser — they can take their capital and leave without the emotional cost a founder faces.

Key operator rollover (10-15%). COOs, CFOs, and sales leaders typically roll 10-15% alongside the CEO. This creates a management incentive pool that scales with company growth and aligns the full executive team.

Earn-out versus escrow versus rollover equity

Post-close consideration structures have shifted materially in 2024-2025 per Citrin Cooperman 2025:

- Short-term earn-outs (18-24 months tied to EBITDA thresholds): Appeared in 32.5% of IS deals in 2024 — down from 43.8% in 2023

- Management incentive pools (5-10% of equity reserved for post-close grants): Rose to 18.2% in 2024 — up from 6.3% in 2023

- Escrow (typically 10-20% of purchase price held 12-24 months): Nearly 90% of private-target deals include escrow per the SRS Acquiom 2025 Deal Terms Study

The trend is away from deferred cash (earn-outs) and toward aligned equity (rollover plus management incentive pools). Capital partners prefer rollover because it aligns incentives over the full 3-5-year hold period rather than a 24-month earn-out window that may pay out before the real value creation happens.

Employment agreements: the four clauses that matter

Standard LMM IS buyouts use a 4-clause employment structure for the CEO and CFO:

Base employment term (2-3 years). The CEO commits to 2-3 years of continuous employment post-close, renewable annually thereafter. Shorter terms (18 months) signal a turnaround deal; longer terms (4-5 years) are rare in LMM and signal the capital partner thinks management is irreplaceable (a red flag for execution risk).

Non-compete (12-24 months post-termination). The CEO cannot compete in the sector within a defined geographic area for 12-24 months after leaving. Enforceability varies by state (California generally does not enforce non-competes; Texas, Florida, and Illinois do), so your M&A attorney pressure-tests this by jurisdiction.

Non-solicit (12-24 months post-termination). The CEO cannot solicit employees or customers for 12-24 months — generally more enforceable than non-competes across jurisdictions.

Change-of-control golden parachute. If the sponsor is removed from the GP, replaced with a different capital partner, or if the company is sold during the CEO's tenure, the CEO's unvested equity vests on an accelerated schedule (typically 100% vesting on change of control). This protects the CEO but creates a cost for the sponsor if the capital partner wants to swap CEOs mid-hold.

Key-person insurance and succession planning

Capital partners will require $2M-$5M key-person life insurance on the CEO (and sometimes the CFO) in most LMM IS buyouts, funded by the portfolio company and paid to the capital partners on triggering events. The policy typically runs a 10-year term and costs roughly $5K-$15K annually depending on CEO age and health.

Pair this with a 12-18-month successor identification plan that your capital partner expects in the deal book's management section. Most first-time sponsors skip this and get pushed back in week 2 of capital partner diligence — the successor plan is not about replacing the CEO, it is about demonstrating that the sponsor has thought about what happens if the CEO unexpectedly leaves.

How rollover affects your capital stack

On a $35M deal with $5M EBITDA and $3M management rollover (from the capital stack example earlier):

- Without rollover: fresh equity need is $10.5M + $3M = $13.5M

- With 20% rollover: fresh equity need is $10.5M

- Equity savings from rollover: $3M (28% of the fresh equity check)

- Impact on sponsor promote: fresh equity smaller → sponsor promote percentage effectively larger against the equity base

- Lead capital partner check size: reduced from $9.5M to $7.5M — may change which capital partners fit the deal

The rollover negotiation happens in week 2-6 of exclusivity, concurrent with your capital partner outreach. Push for 20-25% rollover from the founder-CEO as the opening position, accept 15% as the floor, and pair the rollover with a 2-year CEO employment commitment plus a 12-month non-compete.

Peony Business at $30/admin/month supports NDA gates that trigger before management sees any equity structure and e-signatures that execute the rollover subscription and employment agreements inside the data room, while dynamic watermarks embedded on every employment agreement page are on the Data Room plan ($52/admin/month) — compressing what typically takes 3 weeks across email and DocuSign into 4-5 days.

How Do You Build Repeat Capital Partner Relationships?

59% of capital partner re-engagements are repeat relationships per Citrin Cooperman 2025. This is the single highest-leverage statistic in the IS ecosystem — it means the sponsors who cultivate repeat partners compound their access to capital faster than sponsors who run cold outreach every vintage. Sophisticated sponsors treat capital partner relationships as a multi-vintage asset. Four practices separate the sponsors who repeat from the sponsors who run one-off deals.

Quarterly portfolio updates to every prior partner

Every 90 days, every capital partner who invested in (or evaluated) a prior deal receives a 30-minute call with a 4-page update deck. The deck covers: current EBITDA versus plan, value creation initiatives completed in the last 90 days, customer metrics (retention, concentration, net revenue retention), and forward-looking risks. Format matters — a standardized template that looks identical across vintages signals process discipline and lets capital partners compare your execution across deals.

Include capital partners who passed. The capital partners who passed on deal 1 but see you execute cleanly for 18 months are the warmest lead for deal 3. If you only update partners who invested, you are missing the 2-3x larger pool of partners who evaluated and passed. Many sponsors skip this because it feels awkward — but capital partners appreciate the signal that you treat evaluation as a relationship, not a transaction.

Honest post-mortems on deals that did not close

The sponsors who win repeat capital are the ones who send a 1-page summary to every capital partner who evaluated a broken deal explaining: (1) what the Q of E uncovered, (2) what happened on price negotiation, (3) what you learned about your sourcing or underwriting process, and (4) what you are doing differently on the next deal.

Capital partners value process transparency more than deal count. They are underwriting your judgment and process discipline more than your deal volume. A sponsor who can credibly explain why deal 2 broke and what they adjusted is more attractive for deal 3 than a sponsor who closes deal 2 by over-stretching on price and then generates weaker returns.

Early NDA on the next deal

When you have LOI signed on deal 6, your 3 most-engaged capital partners from deals 4 and 5 should get NDA-gated access within 48 hours — before you open outreach to any new partner. Repeat partners close 30-40% faster than new partners because they already know your process, your financial model layout, and your thesis-construction style. Use personalized sharing links to track each repeat partner's engagement separately across the new data room.

On the LOI signing day:

- Day 0, hour 1: Email the 3 most-engaged prior capital partners announcing the new deal (high-level thesis, sector, EV range, check size needed)

- Day 0, hour 6: Send Stage 1 deal book to the 3 partners via NDA-gated link with personalized sharing

- Day 3: Phone calls with each of the 3 partners to hear their Stage 1 reactions

- Day 5: Open outreach to 5-7 new partners, having already qualified the repeat Rolodex

This choreography compresses the 90-day post-LOI timeline to 60-65 days for experienced sponsors with active repeat Rolodex.

Co-invest windows on your best deals

When a deal is oversubscribed, prioritize repeat capital partners with a 72-hour early commitment window before broadening to your full Rolodex. This signals to repeat partners that they are genuinely preferred — not just one of 12 partners on a broadcast email. Capital partners notice this choreography and often weight their commitment decisions in favor of sponsors who run it.

A practical implementation: if your lead capital partner writes a $10M check and you need $15M total equity, offer the additional $5M as a co-invest allocation with a 72-hour exclusive window to 2-3 repeat partners from prior deals. If they commit within 72 hours, you have filled the stack from trusted capital. If they pass, you open to the broader Rolodex with minimal time lost. Co-invest economics typically match the lead partner's economics — same promote, same fees, pro rata pari passu on distributions.

What repeat capital buys you

For a sixth-deal sponsor running deals at $30M-$75M EV with a 5-10 firm repeat Rolodex, this practice typically compresses the 90-day post-LOI timeline to 60-65 days per McGuireWoods 2025 IS Conference practitioners. It also reduces the capital partner negotiation cycle from 3-4 weeks to 1-2 weeks because economics are largely pre-aligned across vintages. Most important, it lets you raise harder terms — peak 25% carry on later deals — because your repeat partners have watched you execute at 18-22% on deals 2-4 and trust the promote structure.

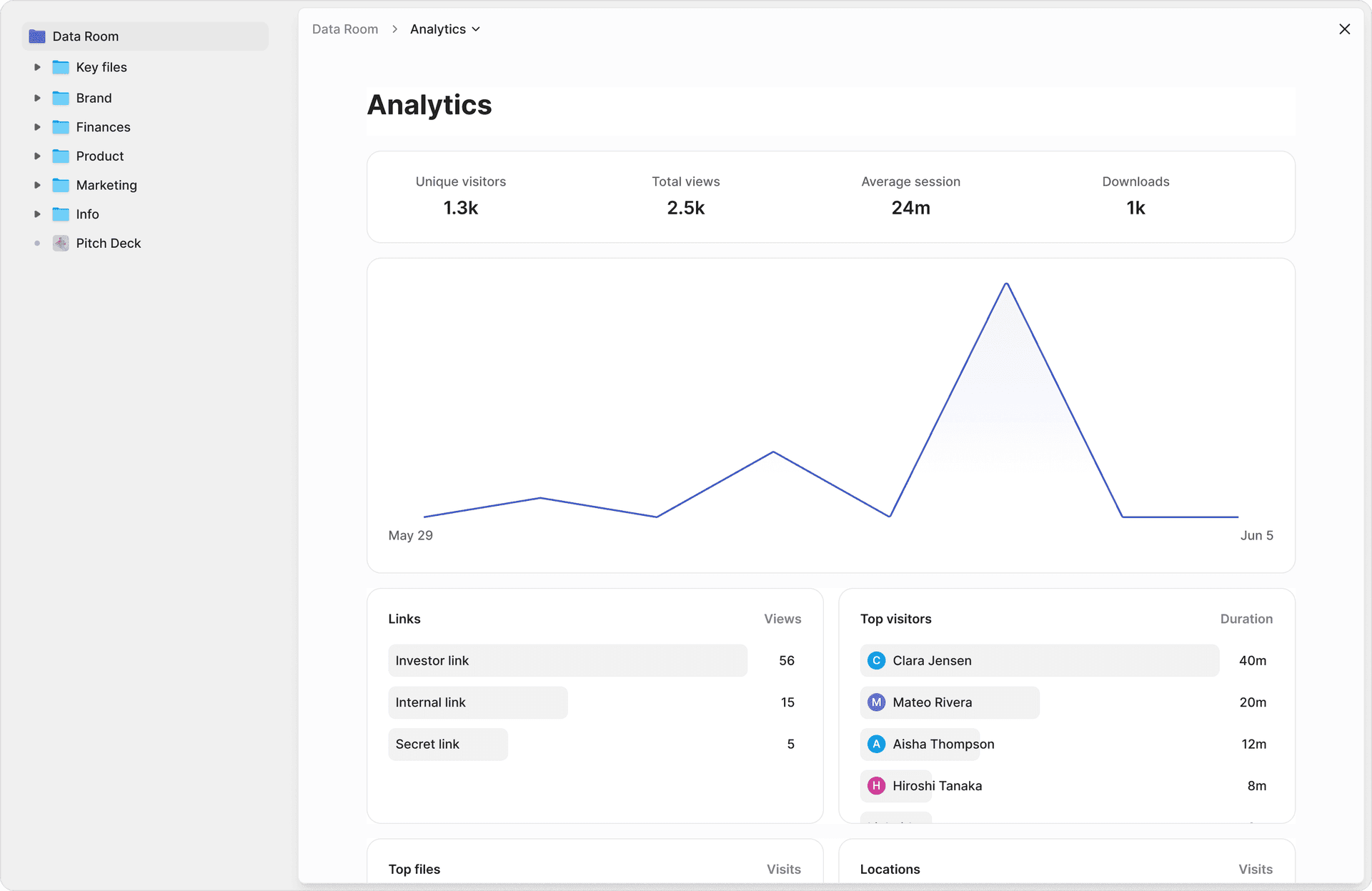

Peony Business at $30/admin/month supports page-level analytics that track each capital partner's engagement separately across deals and vintages — so at vintage 6 you see that your lead partner on deals 2 and 4 spent 45 minutes on your value creation plan for deal 5 before passing, a signal to pitch them on deal 7 with a different thesis angle. Unlimited data rooms on Peony Data Room at $52/admin/month supports the concurrent Stage 1, Stage 2, and Stage 3 rooms across active deals 4, 5, and 6 that an experienced sponsor actually runs — legacy VDRs at $25K+ per deal structurally cannot support this workflow.

What Are the Five Biggest Capital Raising Mistakes First-Time IS Make?

After watching hundreds of first-time and second-time IS capital raises run through the platform, these five mistakes account for roughly 70-80% of the deals that lose economics or lose exclusivity. Every one is avoidable.

1. Going too wide too fast

First-time sponsors often email 40-60 capital partners in week 1 of post-LOI outreach, believing that volume compensates for the lack of pre-LOI cultivation. This is backwards. Capital partners read your outreach velocity as a signal — a sponsor who blasts 50 introductions is signaling desperation, which reduces the likelihood each partner takes the follow-up seriously. Sophisticated sponsors target 5-8 pre-identified partners in the first 72 hours post-LOI (ideally from pre-LOI soft-circling) and only broaden to 10-15 partners in week 2-3 if the first wave is not generating engagement.

Fix: pre-qualify 15-20 capital partners in your target sector 30-60 days before the LOI. On LOI signing day, reach the 5-8 most promising partners first with personalized outreach that references specific prior engagement (a conference conversation, a prior deal they invested in, a sector thesis they published). Cold outreach to 40+ partners is a last-resort move, not a first move.

2. Overpromising on timeline

First-time sponsors often promise capital partners a 60-day LOI-to-close timeline to sound sophisticated, then miss by 30-45 days. This destroys trust. 73% of M&A advisors say IS deals take longer to close than PE funds per Axial 2025 — and your capital partners know this. Over-promising on timeline makes you look either inexperienced or dishonest.

Fix: promise 90-120 days from LOI to close and deliver in 75-90. Under-promise and over-deliver. Capital partners tracking your timeline versus promise are underwriting your process discipline — which compounds into their decision on deal 2.

3. Weak sponsor promote (below 10% when the market is 15-25%)

First-time sponsors often anchor too low on promote — agreeing to 8-10% flat carry without hurdles because they are afraid to lose the capital partner. This leaves material money on the table and signals inexperience. Citrin Cooperman 2025 found the minimum carry is firmly in the 10-25% range and 64% earn 25%+ at maximum tiers. A flat 10% deal costs the sponsor roughly $1.5M-$3M on a successful exit compared to market-standard tiered structure.

Fix: open the promote negotiation at a tiered MOIC waterfall with 10% carry after 1x-2x MOIC, 15% after 2x-3x, 20% after 3x-4x, 25% above 4x, with full catch-up. Capital partners respect sponsors who open at market and negotiate firmly — they lose respect for sponsors who open below market.

4. Not syndicating mezzanine alongside equity

First-time sponsors often treat the equity raise and the debt raise as sequential workstreams — finalize equity first, then raise mezz. This costs 2-3 weeks of exclusivity because the debt lender cannot size the sub-debt tranche until the equity is locked, and the equity partner often wants to see the debt terms before committing. Sophisticated sponsors run equity and mezz outreach concurrently, with pre-LOI soft-circling covering both equity and sub-debt partners.

Fix: by LOI signing day, have 3-5 equity partners and 2-3 SBIC or mezzanine partners in pre-LOI soft-circle conversations. On day 1 post-LOI, share the deal book with all of them simultaneously. The capital stack converges in week 3-4 with both sides negotiated in parallel.

5. Ignoring senior debt capacity

First-time sponsors often underestimate senior debt capacity, building capital stacks with 2.0x-2.5x senior leverage when the lender would have supported 3.0x-3.5x. A 0.5x-1.0x increase in senior debt reduces your equity need by $2.5M-$5M on a $5M EBITDA deal — which either lets you close with a smaller equity raise or increases your sponsor promote percentage against the remaining equity base.

Fix: engage a debt advisor pre-LOI to pressure-test senior debt capacity. Configure Partners, Lincoln International Debt Advisory, and Capstone Partners Debt Advisory all have dedicated IS teams and charge roughly $25K-$75K for a pre-LOI debt-capacity analysis — cheaper than the value created by sizing the stack correctly. Per Parm Atwal at Configure Partners (Deal-by-Deal Podcast): "Earlier is better" on debt advisor engagement.

Three Capital Raising Case Studies: 2024-2026 IS Deals

To ground the playbook in specific deal dynamics, here are three verified 2024-2026 IS capital raises that worked — each drawn from our vertical capital partner directories. These are the case studies I would walk through with a first-time sponsor to show what a well-executed capital raise actually looks like.

Case study 1: Trinity Electrical Services IS buyout (January 2025) — Peninsula Capital Partners junior capital

Deal structure: Specialty electrical contracting IS buyout in January 2025 with Peninsula Capital Partners providing subordinated debt plus common equity to the IS sponsor. Peninsula's Fund VIII closed at $400M in September 2025, and the firm has backed 70+ IS platforms since 1995 — making it the single deepest IS-partner track record on our cleantech capital partners list. The Trinity Electrical deal is a textbook example of Peninsula's flexible junior capital model: $2M-$30M checks in mezzanine debt, preferred equity, or minority common equity, with a $3M+ EBITDA minimum.

What made it work: The IS sponsor pre-soft-circled Peninsula 45 days before the LOI, building on a prior introduction from a 2023 DealMAX conference. Peninsula's IS-exclusive positioning meant the capital partner term sheet was aligned on economics (2% closing fee, 5% management fee, tiered 10-25% promote with MOIC-based full catch-up) before the seller LOI was signed. The electrical services sector fit Peninsula's 30-year LMM sourcing network, and the AI data center grid-spending tailwind gave the deal a clean bullish narrative for the IC review. Total capital stack estimated at $35M-$50M EV with senior debt at 2.5x-3.0x EBITDA, Peninsula subordinated debt at 1x-1.5x, and fresh equity at 30-35% of EV.

The lesson: Pre-LOI soft-circling with an IS-dedicated partner like Peninsula compresses the post-LOI capital raise to 45-60 days, well inside the 90-day exclusivity window. See our cleantech/energy capital partners directory for Peninsula's full profile plus 11 other cleantech/energy firms.

Case study 2: Teague Electric IS growth investment (2025) — Align Collaborate + IX Capital Partners

Deal structure: Teague Electric Construction IS growth investment in 2025 with Align Collaborate providing lead equity alongside IX Capital Partners as the independent sponsor. Align Collaborate's Fund I closed at $233M in March 2025, oversubscribed versus a $150M target — a publicly-stated IS-exclusive investment vehicle. The firm's tagline is "Independent Sponsors' First Call," and the Teague Electric deal is one of Fund I's inaugural platform investments.

What made it work: IX Capital Partners identified Teague Electric — a Kansas City-based specialty electrical contractor serving utility and data center customers — as a platform fit for the AI data center tailwind and the $720B grid spending cycle Goldman Sachs projects through 2030. Align Collaborate wrote the lead equity check ($10M-$30M range per the firm's published check size guidance), and IX Capital Partners served as the IS sponsor. The deal closed inside Align's initial investment pace target, and Align's Cleveland + Dallas dual-hub sourcing coverage matched Teague's Midwest + Sun Belt customer footprint.

The lesson: For emerging or first-time IS sourcing deals in the AI-data-center-adjacent sub-sectors (electrical, HVAC cooling, backup power, utility services), an IS-exclusive equity partner like Align Collaborate provides both capital and narrative fit. There is no fund mandate ambiguity — Fund I exists to partner with independent sponsors.

Case study 3: 5280 Waste IS buyout (April 2025) — Laurel Mountain + Tecum + Comerica

Deal structure: Environmental services and waste operator IS buyout in April 2025 with Laurel Mountain Partners as IS sponsor, Tecum Capital providing subordinated debt, and Comerica providing senior secured financing. Tecum's Fund IV closed at $325M SBIC in July 2025 — the deal closed shortly before Fund IV's final close and deployed from Fund III. 5280 Waste is a Denver-based waste services operator with municipal and commercial customer concentration.

What made it work: The environmental services sector was running at strategic-deal median multiples of 15.0x-20.9x EBITDA in 2025 per Capstone — the biggest multiple expansion of any sector in 2025. Laurel Mountain (IS) underwrote the deal on a tuck-in-and-build thesis: acquire at LMM multiples (7x-11x for waste LMM platforms), build scale through organic growth and add-ons, exit at strategic multiples. Tecum's sub-debt tranche priced at roughly 10-12% all-in, funded partly through SBA debenture leverage. Comerica's senior provided first-lien term loan plus revolver at typical LMM pricing.

The lesson: The multiple-arbitrage thesis (buy at LMM, exit at strategic) works in sectors with clear multiple expansion tailwinds — environmental services and HVAC services both sit in this bucket for 2026. Pair an IS-partner SBIC like Tecum with a specialist senior lender like Comerica (both have deep LMM industry coverage) and the capital stack assembles in 60-75 days post-LOI.

Should You Use a Placement Agent?

The placement-agent-versus-DIY decision is one of the highest-stakes strategic choices in IS capital raising. 21% of IS use placement agents per Axial's 2025 report, meaning 79% DIY the capital raise. Here is the decision framework.

Placement agent pros

- Network acceleration. A good placement agent opens doors to 30-100 pre-qualified capital partners in 60-90 days. For a first-time sponsor in a less-trafficked vertical, this can compress the capital partner sourcing phase from 6-8 weeks of cold outreach to 2-4 weeks of warm introductions.

- Timeline compression. Agents shorten the overall capital raise timeline by 3-5 weeks on competitive deals — which matters materially on a 90-day exclusivity window.

- Introducer credibility. Capital partners treat agent-introduced deals with more attention than cold outreach. The filter effect is real — partners know the agent has qualified the deal before it arrives.

- Negotiation leverage. A competitive process with multiple interested capital partners lets the sponsor negotiate firmer economics (higher promote, lower GP commit, better co-invest rights) than a single bilateral conversation.

Placement agent cons

- Fees: 1-4% of equity raised. On a $20M equity raise, this is $200K-$800K of sponsor economics given up. Over 10 deals, the cumulative agent fees can exceed $5M.

- 12-month tail on term sheets. Standard placement agent engagement letters include a 12-month tail clause — meaning if any capital partner the agent introduced invests in any of your deals within 12 months of engagement termination, the agent is entitled to their fee. This can trap future deal economics unexpectedly.

- Loss of direct relationship. Capital partners introduced through an agent tend to view the sponsor as "the agent's client" rather than a direct relationship for the first 12-18 months. This delays the development of repeat relationships — the 59% repeat statistic compounds more slowly on agent-sourced deals.

- Narrative control. Agents pitch your deal through their own relationship lens, which may not match your positioning. A skilled sponsor who meets capital partners directly controls the narrative more tightly than through an intermediary.

Decision framework

Use a placement agent if: (1) you are a first-time sponsor without a warm Rolodex in the target sector; (2) your sector is less-trafficked (think specialty niches like specialty chemical distribution or industrial decarbonization); (3) your deal has compressed exclusivity (sub-60 days); or (4) you want competitive tension for firmer economics.

DIY the capital raise if: (1) you have 3-5 warm capital partners from prior deals or a prior PE role; (2) your sector has deep existing capital partner coverage (healthcare, business services, manufacturing, distribution); (3) you have 90+ days of exclusivity; or (4) you want to preserve direct relationships for future vintages and compound into the 59% repeat statistic.

Leading IS-focused placement agents in 2026 include Configure Partners (Parm Atwal), Lincoln International IS Group, Smash Capital Advisors (distinct from Smash.vc), and Capstone Partners Debt Advisory (for sub-debt tranches specifically). Engagement letters typically run $50K-$150K retainer plus 2-4% success fee on equity raised.

By the Numbers

- 26.8% of all closed deals on Axial YTD 2025 — independent sponsors outpaced PE funds at 21.1% (Axial 2025 IS Report)

- 54% of IS transactions closed at 4x-6x EBITDA in 2024 — lower than broader PE because IS targets sub-scale founder-led businesses (Citrin Cooperman 2025)

- 53% of IS deals now use SBIC capital — up from 34% three years ago (Citrin Cooperman 2025)

- 15%-25% median IS sponsor promote at peak tier — 64% earn 25%+ at max tiers (Citrin Cooperman 2025)

- 59% of capital partner re-engagements are repeat relationships (Citrin Cooperman 2025)

- $25M-$75M typical IS deal size in 2026 — the most active sweet spot on Axial and McGuireWoods data

- ~10-12% SBIC effective cost of mezzanine capital — versus 11-14% for non-SBIC unitranche

- 10%-40% typical management rollover on LMM IS buyouts — with founder-CEOs rolling at the top of the range

- 1-4% placement agent fees plus 12-month tail on term sheets — 21% of IS use agents per Axial 2025

- 72% of IS required to contribute 2-5% GP commit — 86% use personal funds (Citrin Cooperman 2025)

Bottom Line

The IS capital raising playbook is a full-stack workflow — pre-LOI cultivation, term sheet negotiation, capital stack design, SBIC leverage, management rollover, and repeat-relationship compounding. Sponsors who execute all eight stages close faster, with firmer economics, and build capital partner Rolodex that compounds across vintages. Sponsors who skip stages 1-2 (pre-LOI) or stage 7 (repeat relationships) work harder on every deal and lose economics mid-diligence.

If you are a first-time IS: Build your Rolodex at conferences (MWISC October 27-28 2026 Dallas; SBIA ISF May 6 Philadelphia; ACG DealMAX April 27-29 Vegas; iGlobal Summit June 11 Dallas / September 28-29 NYC), pre-soft-circle 5-8 partners 30-60 days before your first LOI, target 15-20% peak promote with MOIC-based tiers, size senior at 2.5x-3.0x EBITDA, add SBIC sub-debt at 1x EBITDA from Tecum, Cyprium, or Argosy, and roll management at 15-25%. Use Peony Data Room at $52/admin/month for unlimited data rooms — NDA gates, personalized sharing links per capital partner, page-level analytics, and e-signatures compress the post-LOI timeline by 2-3 weeks versus Dropbox or Google Drive workflows.

If you are an experienced IS running 3-5 deals per year: Invest in repeat relationships — quarterly portfolio updates to every prior partner (including passers), honest post-mortems on broken deals, 48-hour NDA access for your top 3 repeat partners on LOI signing day, 72-hour co-invest windows for oversubscribed deals. This practice alone compresses the 90-day post-LOI timeline to 60-65 days and lets you raise harder promote terms on deals 4+ because your repeat Rolodex has watched you execute at 18-22% on deals 2-3. Peony Data Room unlimited data rooms supports the concurrent Stage 1, Stage 2, and Stage 3 rooms across active deals 4, 5, and 6 that experienced sponsors actually run — legacy VDRs at $25K+ per deal structurally cannot support this workflow.

If you are a family office or HNWI evaluating IS co-invest: The economics differ from traditional PE co-invest on three dimensions — harder-ratcheting promote (15-25% at peak), higher recurring fee layer (2% closing + 5% management fee), higher sponsor GP commit (2-5% personal capital). Use page-level analytics to track which sections of the sponsor's deal book your IC engaged with, and use the AI document extraction workflow to query the capital stack and waterfall math for hard answers with page citations. For a family office reviewing 8-12 IS deals per month, this workflow compresses diligence from weeks to days.

Set up your first independent sponsor capital raising data room in under 5 minutes — see plans and pricing.

Frequently Asked Questions

I am a first-time IS with an $8M-$12M EBITDA LOI — how do I build my first capital partner Rolodex in 60 days?

A first-time IS builds a usable capital partner Rolodex in 60 days by combining three sourcing channels. First, conferences: the McGuireWoods Independent Sponsor Conference drew 1,600 attendees in 2025 and the 2026 edition runs October 27-28 in Dallas, the SBIA Independent Sponsor Forum meets May 6 in Philadelphia, ACG DealMAX runs April 27-29 in Las Vegas, and the iGlobal IS Summit runs June 11 Dallas plus September 28-29 NYC. Plan two in 60 days — one large (MWISC or DealMAX) plus one IS-specific (SBIA ISF or iGlobal). Second, platform introductions: Axial closed 26.8% of all LMM deals through independent sponsors YTD 2025, and their partner-matching flow surfaces 30-50 capital partners in your sector in under 10 days. Third, warm referrals from your M&A attorney and accountant, both of whom see 20-40 IS deals per year and can credibly introduce you to 5-10 firms. Prioritize one IS-explicit equity partner (Peninsula, Align Collaborate, Boyne Capital), one SBIC (Tecum, Cyprium, Argosy), and one family office or HNWI aggregator per sector. Peony Business at $30 per admin per month lets you set up a branded capital partner data room with personalized sharing links for each firm you meet at conferences — so the day after MWISC you send 8 NDA-gated links and track which firms opened the deal book versus which went silent, something Dropbox and Google Drive cannot support at the per-viewer level.

Our family office is evaluating our first IS co-investment — how do IS deal economics compare to direct PE co-invest?

IS deal economics differ from traditional PE co-invest on three material dimensions. First, promote structure: a committed-capital PE fund typically charges a flat 20% carry above an 8% preferred return with full catch-up, while IS promote ranges from 15% to 25% at peak tier in a 3-to-5 tier MOIC waterfall (64% of sponsors earn 25%+ carry at max tiers per Citrin Cooperman 2025, with 50% now using MOIC-based hurdles up from 27% in 2019) — giving LPs more downside protection and ratcheting sponsor economics harder as returns compound. Second, fee structure: PE co-invest usually waives management fees entirely on the co-invest sleeve, while IS typically charge a 2% closing fee of enterprise value (56% of sponsors in Citrin's 2025 survey) plus 5% annual management fee of portfolio company EBITDA (69% of sponsors) — meaning your all-in cost layer is higher on IS co-invest. Third, GP commit: 72% of IS are required to contribute 2-5% of deal equity from personal funds and 86% use personal capital (Citrin 2025), compared to 1-2% GP commit on committed-capital funds. The tradeoff: IS deal economics ratchet harder on upside (if you underwrite a 4x MOIC deal, sponsor takes 25% and you keep 75% of the gain above 4x) but your Peak-to-paid-in cost is higher. For a family office reviewing 8-12 IS deal books per month, the sponsor's specific MOIC scenarios and waterfall math matter more than the headline carry percentage. Peony Business at $30 per admin per month includes page-level analytics that show exactly which sections of the waterfall math your investment committee spent time on — so follow-up calls focus on the questions your team actually has.

I am raising capital for my second IS deal on a $25M EV services business — how much promote should I be asking for?

On a $25M EV deal for an IS running deal number two, the market-standard promote is a tiered MOIC waterfall with the sponsor taking between 15% and 25% at the top tier. Citrin Cooperman's 2025 survey found the minimum carry firmly in the 10-25% range (stable since 2019), 64% of sponsors earn 25%+ carry at maximum tiers (up from 37% in 2019), 71%+ use variable-with-hurdles models where carry increases as returns exceed thresholds, 74% include full catch-up (up from 61% in 2019), and 50% use MOIC-based hurdles (up from 27% in 2019). For your second deal, push for this structure: 10% carry after 1x-2x MOIC (with 8% preferred return), 15% after 2x-3x, 20% after 3x-4x, 25% above 4x, with full catch-up and MOIC-based tiers rather than IRR. On a $25M EV deal that exits at 3.5x MOIC, this structure earns you roughly 15-17% blended carry on the full gain. Sponsors who ask for a flat 25% on deal two without a track record on deal one will typically lose the capital partner negotiation, while sponsors who ask for less than 10% at the base tier leave money on the table. Pair the promote with a 2% closing fee (rolled 40-80% into equity per Citrin 2025 convention), a 5% annual management fee on portfolio company EBITDA, and a 2-3% GP commit. Peony's Data Room plan at $52 per admin per month supports dynamic watermarks embedding each capital partner's identity on every page of the waterfall schedule — so your promote structure stays confidential when shared with 5-8 partners simultaneously, unlike Google Drive which has no per-page watermarking on any plan.

I signed an LOI on a $15M EBITDA distributor at 8x ($120M EV) — what does the capital stack actually look like?

A $15M EBITDA distributor at 8x ($120M EV) typically stacks as roughly $72M senior debt (3x EBITDA on a unitranche or first-lien term loan at SOFR + 500-600 bps), $15M SBIC subordinated debt or mezzanine (1x EBITDA at 10-13% all-in cost, potentially with PIK toggle), $25M equity from your lead capital partner and co-invest (split roughly 65/35 lead vs co-invest), $3M sponsor GP commit (2-5% of equity check per Citrin 2025), and $5M management rollover (typically 10-40% of management's post-tax proceeds). Total: $72M + $15M + $25M + $3M + $5M = $120M. Key tradeoffs: if your senior lender tops out at 2.5x leverage on a distributor (given working capital cyclicality), you will need either a larger mezzanine tranche or seller paper to fill the gap. SBIC use grew from 34% to 53% of IS deals over three years per Citrin Cooperman's 2025 report, and a 2-to-1 SBIC debenture on $15M subordinated capital means the SBIC partner is deploying roughly $5M of its own fund capital leveraged 2x to the total $15M tranche — cheap, patient capital that compounds your equity return. For a distribution deal specifically, see our distribution/logistics capital partners directory — Peninsula, Tecum, Argosy, and Prospect Partners are the most active IS-partner firms. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the top-20 customer concentration, senior debt commitment letter, mezzanine term sheet, equity subscription docs, and rollover paperwork in under 3 minutes — so the capital stack documentation is live on day one of the exclusivity window.

I am transitioning from corp dev to IS — what SBIC leverage should I actually model into my deal?

SBIC leverage for an IS deal in 2026 works through the 2-to-1 debenture model: an SBIC fund can borrow from the SBA at up to twice its regulatory capital, meaning a $100M SBIC fund has roughly $300M of total deployable capital ($100M equity + $200M leverage). When your SBIC partner writes a $10M subordinated debt check into your deal, they are deploying roughly $3.3M of their fund's own equity leveraged 2x with SBA-backed debentures — which is why SBIC subordinated debt costs you roughly 10-12% all-in versus 11-14% for unitranche or second-lien from a non-SBIC lender. For a corp-dev-to-IS transition, model the SBIC tranche at 0.75x-1.5x EBITDA (with senior at 2.5x-3.5x, total leverage typically 4x-5x on the operating company), all-in cost of 10-12% (fixed coupon 8-10% plus warrants or PIK), and a 5-to-7-year bullet maturity. SBICs led 18% of IS deals in 2025 per Citrin Cooperman and fund 53% of all IS deals — and their regulatory compliance documentation adds 5-7 additional documents to your data room (SBA size standard verification, leverage structure analysis, debenture covenant compliance). Three SBIC funds actively writing IS checks in 2026 are Tecum Capital Fund IV ($325M SBIC, July 2025 close), Cyprium Partners SBIC I ($190M, February 2025), and Argosy SBIC VII ($175M, 2024 SBA SBIC of the Year). Peony Data Room at $52 per admin per month supports per-folder permissions that gate SBIC-specific regulatory materials separately from standard diligence documents — keeping the room clean for non-SBIC partners evaluating the same deal, a workflow that Firmex and Ideals charge enterprise add-ons to configure.

I am an M&A attorney advising a first-time IS on a $20M EV deal — what are the biggest term sheet negotiation pitfalls?

The five biggest term sheet negotiation pitfalls I see first-time IS make on a $20M EV deal are material and fixable. First, underpricing the sponsor promote: asking for 10% flat when the market is 15-25% tiered leaves roughly $500K-$1.5M of sponsor economics on the table per $5M of equity raised on a 3x exit. Second, accepting waterfall math that front-loads LP preferred return ahead of GP distributions without a catch-up — 74% of sponsors now include full catch-up per Citrin 2025, but 26% still do not and materially underpay the sponsor at moderate MOIC outcomes. Third, not pre-negotiating broken-deal cost allocation: if the deal falls apart after $150K of legal, accounting, and Q of E fees, the first-time sponsor often absorbs 100% of the cost while the capital partner walks away — a cost-sharing clause in the capital partner LOI protects you. Fourth, accepting a one-year key-person lockup without a carried-interest cliff — if your lead capital partner can force you out of the GP in month 13 without triggering cliff vesting of your promote, you have created an unpriced call option against your own economics. Fifth, agreeing to a monitoring fee that sits outside the management fee — smart capital partners will push you to consolidate all recurring fees into one transparent line, and first-time sponsors often agree without running the LP-GP economics. According to McGuireWoods 2025 IS Conference practitioners, sponsors who align fees, equity stake, and continuing role upfront with capital partners pre-LOI close 20-25% faster than sponsors who negotiate economics mid-exclusivity. Peony Business at $30 per admin per month supports e-signatures with AI-powered field detection so your capital partner LOI, NDA, and subscription docs execute inside the data room — no separate DocuSign account, no version drift across three email threads.

We are an experienced IS on our sixth deal — how do we cultivate repeat capital partner relationships across vintages?

Repeat relationships drive 59% of capital partner re-engagements per Citrin Cooperman's 2025 IS Report, and the sponsors who repeat effectively run four specific practices across vintages. First, quarterly portfolio updates to every prior capital partner, even on deals they passed — 30-minute calls with a 4-page update deck that shows EBITDA growth, value creation initiatives completed, and exit prep status. Capital partners who passed on deal 1 but see you execute cleanly for 18 months are the warmest lead for deal 3. Second, honest post-mortems on deals that did not close: the sponsors who win repeat capital are the ones who send a 1-page summary to every partner who evaluated a broken deal explaining what the Q of E uncovered, what happened on price negotiation, and what you learned. Capital partners value process transparency more than deal count — they are underwriting your judgment more than your volume. Third, early NDA on the next deal: when you have LOI signed on deal 6, your three most engaged capital partners from deals 4 and 5 should get NDA-gated access within 48 hours, before you open outreach to any new partner. Repeat partners close 30-40% faster than new partners because they already know your process, your financial model layout, and your thesis-construction style. Fourth, co-invest windows on your best deals: when a deal is oversubscribed, prioritize repeat capital partners with a 72-hour early commitment window before broadening to your full Rolodex. For a sixth-deal sponsor running deals at $30M-$75M EV with a 5-10 firm repeat Rolodex, this practice typically compresses the 90-day post-LOI timeline to 60-65 days per McGuireWoods 2025 Conference takeaways. Peony Business at $30 per admin per month includes personalized sharing links that track each capital partner's engagement separately across deals — so you see at vintage 6 that your lead partner on deals 2 and 4 spent 45 minutes on your value creation plan for deal 5 before passing, a signal to pitch them on deal 7 with a different thesis angle.

I am running a $30M roll-up of independent pharmacies — should I use a placement agent or DIY the capital raise?

For a $30M roll-up of independent pharmacies, the DIY-versus-placement-agent decision hinges on three factors. First, existing relationships: if you have 3-5 warm capital partners from prior deals or a prior PE role, DIY saves 1-4% of equity raised in agent fees (on $18M equity, that is $180K-$720K preserved) and keeps you in direct control of the narrative. Second, sector fit: placement agents like Smash Capital Advisors, Configure Partners, and Lincoln International IS Group charge 2-4% of equity raised but deliver introductions to 30-100 pre-qualified partners in 60-90 days — a dramatically faster funnel than cold outreach for a first-time sponsor in a less-trafficked vertical. Healthcare IS deals specifically have deep existing capital partner coverage (see our healthcare capital partners directory for 17 firms actively funding healthcare IS platforms), so if you already know Boyne Capital, Edgewater Capital, or Council Capital, DIY is viable. Third, timeline pressure: placement agents shorten the capital partner sourcing phase from 6-8 weeks to 2-4 weeks, which can save your 90-day exclusivity window. The trap: placement agents typically include a 12-month tail clause that entitles them to their fee on any capital partner they introduced if that partner invests in any of your deals within 12 months of the engagement — even if you close the original target deal with a different partner. For a $30M pharmacy roll-up with a sophisticated sponsor team, I would DIY with 5-8 pre-identified capital partners (ideally 2-3 healthcare-specialist firms plus 1 SBIC plus 1-2 family offices) and skip the agent. Axial reports independent sponsors use placement agents on roughly 21% of deals — meaning 79% DIY the capital raise. Peony Business at $30 per admin per month includes screenshot protection on the sensitive pricing schedules, with dynamic watermarks on every page on the Data Room plan ($52/admin/month) — so when you send NDA-gated links to 8 capital partners, the purchase-price math and seller rollover structure do not leak to competing bidders, a workflow that Dropbox and Google Drive cannot support on any plan.

I have a tight 45-day exclusivity window on a $40M EV deal — how fast can capital partners actually commit?

On a 45-day exclusivity window, capital partner commitment realistically takes 35-42 days even with a repeat Rolodex — which is why 90-day minimum exclusivity is the cluster-standard recommendation. The 45-day compressed timeline works only if three conditions align. First, repeat partners: if your lead capital partner is a repeat investor with a signed NDA already in place on your sector thesis and they can waive IC review in favor of pre-IC partner approval, they can complete diligence and sign a commitment term sheet in 14-21 days. Second, pre-LOI soft-circling: if you soft-circled two or three partners 30-45 days before signing the LOI (typical pre-LOI cultivation for experienced sponsors), those partners already have the CIM, financial model summary, and thesis memo loaded and can start deep diligence on day 1 rather than day 10. Third, Q of E pre-commissioned: a pre-LOI Q of E costing $30K-$75K compresses capital partner diligence by 1-2 weeks because partners evaluate adjusted EBITDA from day 1 instead of waiting 21-28 days for the Q of E to land. Without all three conditions, your 45 days will end with 1-2 partners soft-committed but none signed, and you will be forced to request a 30-day extension from the seller — which they may or may not grant. 73% of M&A advisors say IS deals take longer to close than PE funds per Axial 2025, primarily because of post-LOI capital assembly. The structural fix is to negotiate 90-day exclusivity with an auto-30-day extension upfront on your next deal. For the 45-day LOI you already signed, see our LOI playbook for the compressed 90-day timeline adaptation. Peony Data Room at $52 per admin per month includes AI-powered Smart Q and A with human-in-the-loop review — capital partners submit diligence questions, AI drafts answers with cited page numbers in under 60 seconds, you review and approve before sending, which can recover 5-7 days of your compressed timeline.

I am raising $20M equity plus $8M mezz on my first IS deal — how do I structure management rollover and employment continuity?

Management rollover and employment continuity on a $20M equity plus $8M mezzanine deal hinges on four specific structures that work together. First, rollover percentage: in LMM IS buyouts, management typically rolls 10-40% of post-tax proceeds into the new entity's equity — with founder-CEOs rolling at the top of the range (30-40%) and non-founder operators rolling at the bottom (10-20%). A 10% rollover on a $28M total consideration creates a $2.8M management stake, which keeps the CEO aligned but not controlling. Second, earn-out or escrow structure: 18-24-month earn-outs tied to EBITDA thresholds appeared in 32.5% of IS deals in 2024 per Citrin Cooperman (down from 43.8% in 2023), while management incentive pools rose to 18.2% (up from 6.3%) — meaning the trend is toward post-close equity vehicles rather than deferred cash. Third, employment agreements: standard LMM IS structure includes 2-3-year base employment commitments for the CEO and CFO, with 12-month non-competes, 2-year non-solicits, and golden-parachute language triggering on change of control. Legal drafting typically runs $15K-$40K (see our deal book guide for full Stage 3 materials). Fourth, key-person insurance and succession plan: capital partners will require $2M-$5M key-person life insurance on the CEO plus a documented 12-18-month successor identification plan — most first-time sponsors skip this and get pushed back in week 2 of capital partner diligence. For a $20M equity plus $8M mezz deal, the rollover dynamics materially affect your capital stack: if the CEO rolls $2.8M on a 10% stake, your fresh equity need drops from $20M to $17.2M — which may let you skip the second co-invest partner and close faster with just your lead equity and SBIC. Peony Business at $30 per admin per month includes NDA gates that trigger before management sees any equity structure, and e-signatures that execute the rollover subscription and employment agreements inside the data room — compressing what typically takes 3 weeks across email and DocuSign into 4-5 days.

Related Resources

- What Is an Independent Sponsor? Complete Guide — hub covering IS mechanics, economics, and capital partner dynamics

- SBIC for Independent Sponsors (2026 Leverage Playbook) — the SBIC-specific deep dive on debenture mechanics, fund-by-fund profiles, $35M EV worked example, and SBA-specific compliance that this Stage 5 references

- Independent Sponsor LOI Playbook (90-Day Timeline) — the post-LOI capital assembly and exclusivity management playbook

- Independent Sponsor Deal Book (10 Sections) — anatomy of the deal book capital partners actually read

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall cascade, and the five Excel mistakes that get models rejected

- Independent Sponsor Data Room Checklist (42 Documents) — staged document checklist by capital partner type

- Different Passwords for Different Investors — per-LP personalized links, individual passwords, dynamic watermarks, and one-click revoke across 5-15 capital partner shares per deal with forensic leak attribution

- Best Data Rooms for Independent Sponsors — 8 VDRs tested through the IS economic lens

- 18 Independent Sponsor Conferences & Forums in 2026 — full 2026 event calendar (MWISC, SBIA ISF, DealMAX, iGlobal)

- Independent Sponsor Healthcare Capital Partners — 17 firms funding healthcare IS deals

- Independent Sponsor Business Services Capital Partners — 15 firms funding business services IS deals

- Independent Sponsor Manufacturing Capital Partners — 12 firms funding manufacturing IS deals

- Independent Sponsor Tech/Software Capital Partners — 13 firms funding SaaS and MSP IS deals

- Independent Sponsor Consumer Capital Partners — 12 firms funding consumer and CPG IS deals

- Capital Partners Funding Both IS and Search Funds — 9 dual-strategy firms (Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus Fund VII $977M, Miramar) for searchers transitioning to IS and operators raising minority co-investment

- Independent Sponsor Distribution & Logistics Capital Partners — 12 firms funding wholesale, 3PL, cold chain deals

- Independent Sponsor Cleantech & Energy Capital Partners — 12 firms funding HVAC, electrical, environmental services, data center grid deals

- Due Diligence Cost Breakdown — Q of E, legal, tax, and advisor costs for LMM IS deals

- Data Room Folder Structure Guide — folder architecture for IS capital partner data rooms

- M&A Data Room Guide — M&A data room fundamentals

- Peony for Private Equity — PE-specific data room features

- Peony for M&A — M&A data room solutions

- Peony for Due Diligence — diligence workflow tools

- Peony for Fundraising — fundraising data room workflows

- Peony Pricing — Data Room $52/admin/month with unlimited data rooms

- NDA Gates — NDA signature-gated access

- Dynamic Watermarks — per-viewer identity on every page

- Page-Level Analytics — per-partner engagement tracking

- Smart Q&A — AI-drafted diligence answers with human review

- AI Auto-Indexing — automatic folder organization in under 3 minutes

- AI Extraction — natural-language document queries with page citations

- Screenshot Protection — block and log screenshot attempts

- Personalized Sharing Links — per-partner link tracking