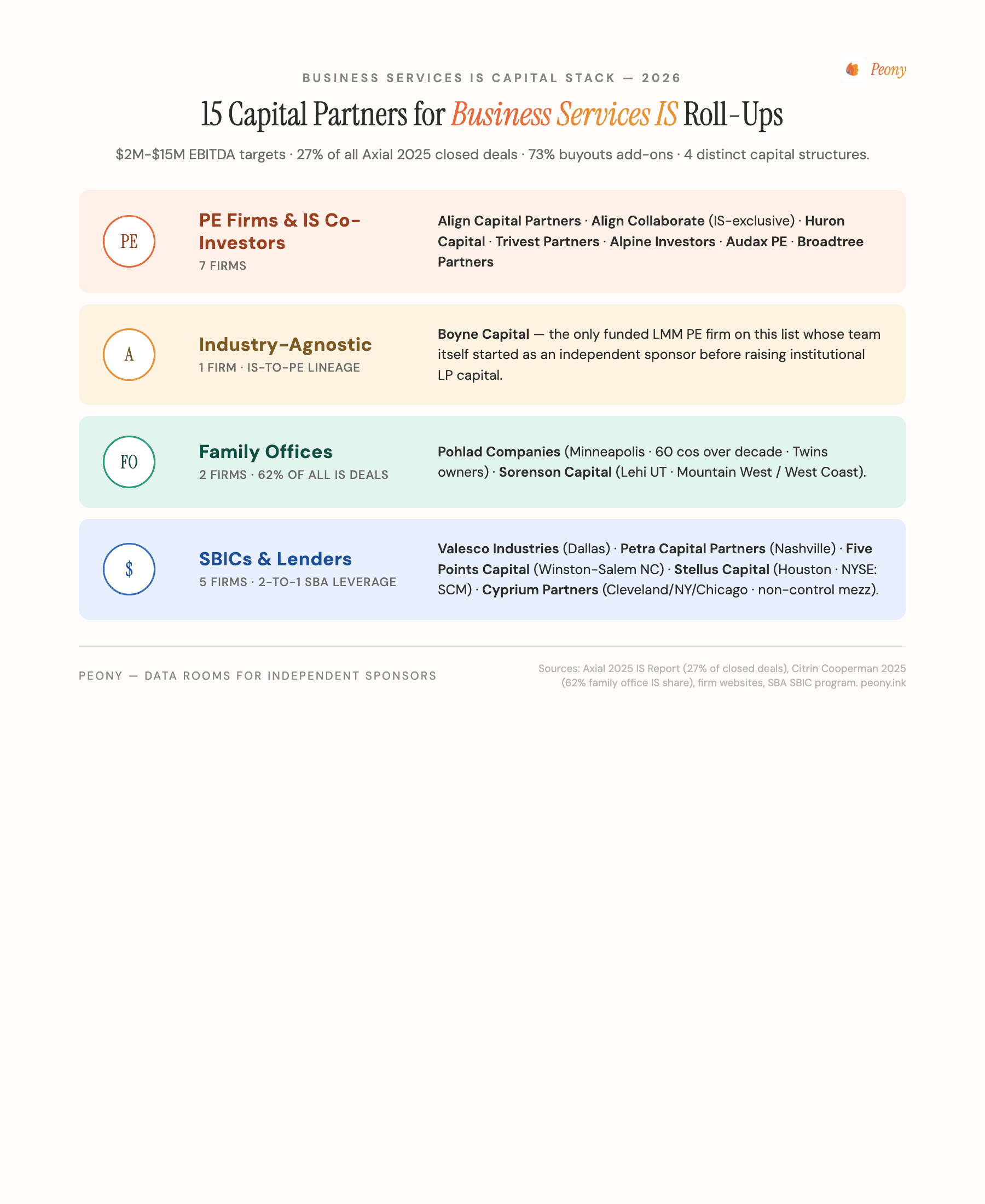

15 Business Services Capital Partners for IS Roll-Ups (4x-8x) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

We run Peony, a data room platform. Business services deals are the single largest category on our platform by deal count -- not healthcare, not manufacturing, not technology. The reason is straightforward: business services is the most common independent sponsor target sector in the lower middle market, and independent sponsors are our fastest-growing user segment.

The appeal is obvious. IT managed services companies, staffing firms, janitorial providers, accounting practices, HVAC operators, pest control businesses, landscaping companies -- these are recurring-revenue, low-capex, founder-operated businesses in massively fragmented markets where the owner is 62 years old and has no succession plan. Deal sizes of $2M-$15M EBITDA are too small for PE mega-funds but perfect for independent sponsors running roll-up strategies.

The challenge is finding capital partners who understand business services economics. A family office that backs biotech is not the right partner for a staffing firm roll-up where the due diligence centers on customer concentration, contract structure, and key person risk -- not IP portfolios or clinical trials. You need capital partners who have underwritten services businesses before.

This guide maps 15 verified capital partners actively funding business services IS deals in 2026 -- PE co-investors, family offices, and SBICs that write checks for IT services, staffing, facilities management, professional services, and field services acquisitions. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide. For healthcare-specific capital partners, see our healthcare IS capital partners directory.

TL;DR: Business services is the #1 independent sponsor target sector. PE deal value surpassed $1.2 trillion in 2025 — only the second time buyout activity crossed the trillion-dollar threshold — with add-ons representing 73% of all buyouts (Cherry Bekaert, February 2026). Q4 2025 saw 1,018 business services deals (RL Hulett, January 2026). MSP deals surged 20% in 2025 to 466 deals totaling $4.3B (Solganick, March 2026). CPA firm M&A is exploding: 31 deals in January 2026 alone — highest single month ever — with 52 deals in the first two months, on pace for 300+ in 2026 (CPA Trendlines, February 2026). Below: 15 capital partners funding these deals, sub-sector multiples, roll-up economics, and the data room documents business services capital partners actually need.

Why Business Services Is the Top Independent Sponsor Sector

Four structural forces make business services the most natural independent sponsor target:

Recurring Revenue and Low Capital Expenditure

Business services companies generate revenue through contracts, retainers, and ongoing service agreements -- not one-time product sales. An IT managed services provider with 100 monthly recurring revenue contracts has predictable cash flow that capital partners can underwrite. A janitorial company with multi-year facility contracts has built-in revenue visibility. Unlike manufacturing (which requires factory equipment) or healthcare (which requires licensed facilities and credentialed providers), most business services companies operate with minimal fixed assets. Cash flow goes to people and operations, not capital equipment.

Extreme Market Fragmentation

Every business services sub-sector has thousands of small operators. The US janitorial services market alone is an $80.4 billion industry with thousands of regional providers (Align BA). The IT managed services market is projected to reach $595 billion globally by the end of 2025 (Solganick). Pest control is a $26 billion US market (The Deal Sheet). This fragmentation creates natural roll-up opportunities where an IS can acquire a platform and bolt on add-ons at lower multiples, building scale that commands a premium at exit.

The Baby Boomer Succession Wave

An estimated 12 million boomer-owned businesses are approaching succession, and fewer than one-third have formal exit plans (Entrepreneur; Project Equity). With 10,000 boomers retiring daily, the pipeline of $2M-$15M EBITDA business services companies coming to market is accelerating every quarter. These founders built their businesses over 25-35 years and often have no internal successor -- their children chose different careers, and the management team cannot finance a buyout without outside capital. Independent sponsors are the natural buyer.

Validated by PE Deal Volume

PE deal value surpassed $1.2 trillion in 2025, with add-ons representing 73% of all buyouts and dry powder reaching close to $1.1 trillion (Cherry Bekaert, February 2026). Business services is one of the primary sectors driving that consolidation. Alpine Investors' Evergreen Services Group completed 47 acquisitions in 2025 (33 MSPs), closed 16 in Q4 2025 alone, and plans 30-40 acquisitions in 2026 with a $5B revenue target by 2030 (National Today, February 2026). Apex Service Partners now has 107 brands and 8,000+ field technicians. CPA firm M&A is the fastest-growing sub-sector: 31 deals in January 2026 (highest single month ever), 52 in Jan-Feb combined, on pace for 300+ in 2026 — up from 100+ in 2025, 65 in 2024, and just 22 in 2023 (CPA Trendlines, April 2026). MSP deals surged 20% in 2025 to 466 deals totaling $4.3B (Solganick, March 2026). The thesis is validated — the question is who funds the deals that are too small for institutional PE.

Business Services Independent Sponsor Capital Partners: Quick Reference

| Firm | Website | Check Size | Deal Size (EV) | Sub-Sector Focus |

|---|---|---|---|---|

| Align Capital Partners | aligncp.com | $10M-$75M equity | Up to $15M EBITDA | Professional business services, technology |

| Align Collaborate | aligncollaborate.com | $10M-$30M equity | $2M-$15M EBITDA | IS-exclusive, industry agnostic |

| Huron Capital | huroncapital.com | $50M+ equity | Lower-mid | Services, buy-and-build |

| Trivest Partners | trivest.com | $10M-$100M | Lower-mid to mid | Business services, consumer, distribution |

| Alpine Investors | alpineinvestors.com | $50M-$500M | Mid-market | IT services, HVAC, accounting, field services |

| Audax Private Equity | audaxprivateequity.com | $25M-$200M | Mid-market | Business services, buy-and-build |

| Broadtree Partners | broadtreepartners.com | $5M-$30M | $1M-$10M EBITDA | Services, technology, government |

| Boyne Capital | boynecapital.com | $10M-$50M | $3M-$15M EBITDA | Industry agnostic (institutional LP-backed) |

| Pohlad Companies | pohladcompanies.com | $10M-$50M | Lower-mid | Business services, consumer, specialty industrial |

| Sorenson Capital | sorensoncapital.com | $10M-$75M | $3M-$25M EBITDA | Business services, manufacturing, distribution |

| Valesco Industries | valescoind.com | $5M-$25M | $15M-$100M revenue | Business services, manufacturing (SBIC) |

| Petra Capital Partners | petracapital.com | Up to $25M | $10M-$75M EV | Business services, tech-enabled services (SBIC) |

| Five Points Capital | fivepointscapital.com | $5M-$30M | Lower-mid | Business and industrial services (SBIC) |

| Stellus Capital | stelluscapital.com | $5M-$50M | $5M-$50M EBITDA | Multi-sector including business services (BDC/SBIC) |

| Cyprium Partners | cyprium.com | $5M-$60M | $4M+ EBITDA | Business services, manufacturing, distribution |

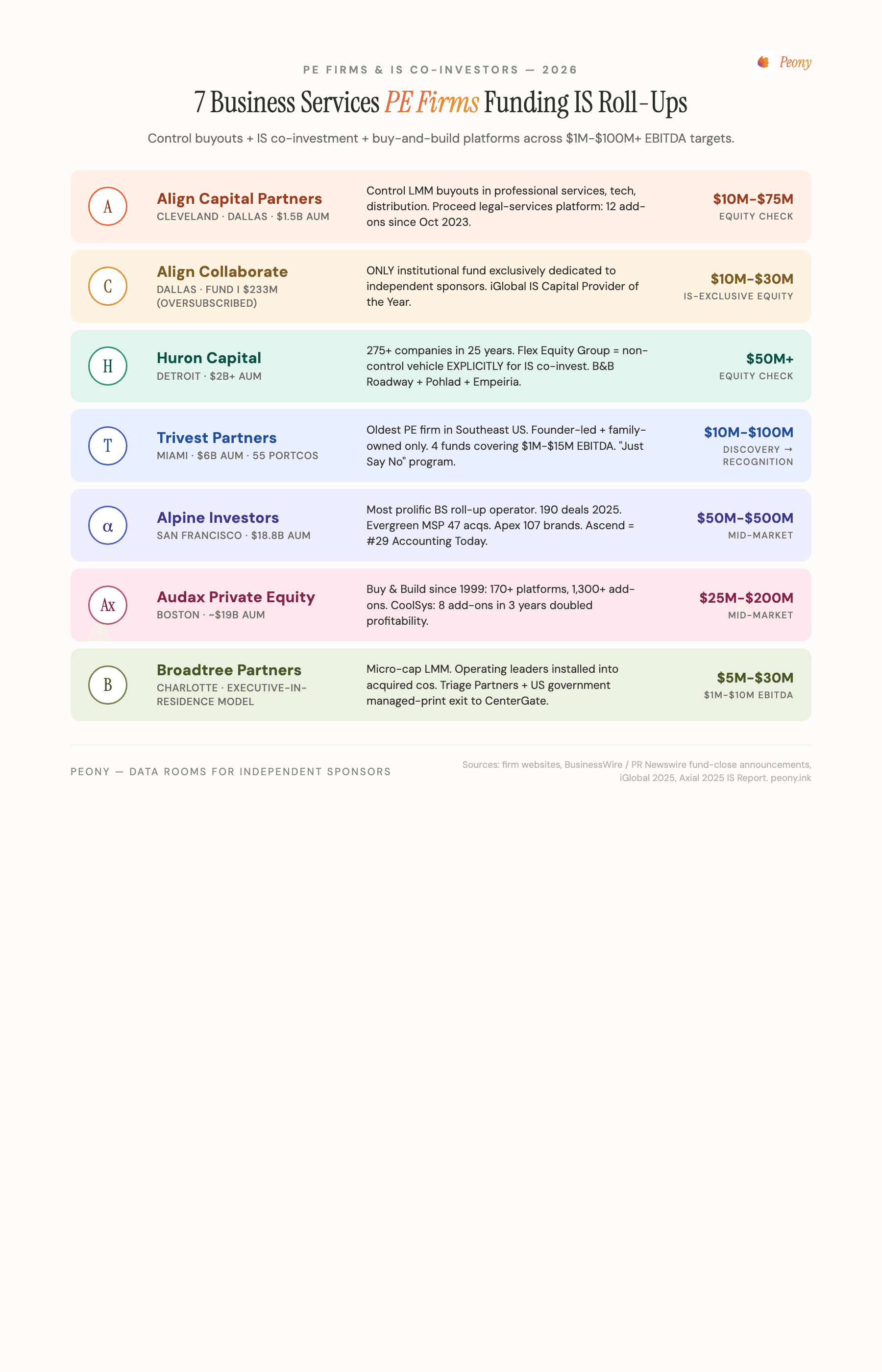

Business Services-Focused PE and Independent Sponsors

These firms actively co-invest in business services IS deals or operate as business services-focused platforms themselves. Each has a verified track record deploying capital into services company acquisitions and roll-ups.

Align Capital Partners

Website: aligncp.com | AUM: $1.5B committed | HQ: Cleveland and Dallas

Align Capital Partners makes control investments in lower-middle-market companies with up to $15M EBITDA across professional business services, technology, specialty manufacturing, and distribution. ACP's approach centers on accelerating growth through enhanced sales and marketing, pricing strategies, talent acquisition, geographic expansion, and greater technology adoption (Align Capital Partners). The firm was named to GCI Publishing's Top 50 PE Winners list.

Q1 2026: Closed a $405M single-asset continuation fund (CP EV Fund I, LP) for its legal services platform Proceed — which completed 12 add-on acquisitions since ACP acquired Counsel Press in October 2023 (April 1, 2026 — Kirkland & Ellis).

Why it matters for IS: Align's EBITDA target directly overlaps with the IS sweet spot. The Proceed continuation fund demonstrates the full lifecycle IS capital partners want to see: platform acquisition, add-on execution, and exit via continuation vehicle.

Align Collaborate

Website: aligncollaborate.com | Fund I: $233M (oversubscribed) | HQ: Dallas

Align Collaborate was purpose-built in 2023 as the only institutional equity investor designed exclusively for independent sponsors. Founded by Align Capital Partners and experienced IS investors Grant and Michael Kornman, the firm targets $10M-$30M equity investments in platform companies with $2M-$15M EBITDA. Fund I closed oversubscribed at $233M in March 2025, well above its $150M target (BusinessWire). Recent deals include a growth investment in Fire Protection Team alongside Right Angle Partners and Teague Electric alongside IX Capital Partners.

Why it matters for IS: Align Collaborate is the only institutional fund exclusively dedicated to independent sponsor transactions. If you are an IS sourcing business services deals in the $2M-$15M EBITDA range, they are the first call. They were named Capital Provider of the Year at iGlobal's Independent Sponsor Summit.

Huron Capital

Website: huroncapital.com | AUM: $2B+ | HQ: Detroit

Huron Capital brings a people-first, thematic buy-and-build approach to private equity investing in secularly relevant and fragmented services sectors. Over 25 years, Huron has acquired more than 275 companies through six control investment funds. Critically, Huron actively co-invests with independent sponsors through its non-control Flex Equity Group -- a recent example is the joint investment in B&B Roadway Security Solutions alongside the Pohlad family and independent sponsor Empeiria Capital (Huron Capital).

Why it matters for IS: Huron explicitly markets to independent sponsors because IS "find deals the firm doesn't" (Smart Business Dealmakers). Their Flex Equity Group is designed for IS co-investment. If you source a business services deal in their target sectors, Huron is a natural partner.

Trivest Partners

Website: trivest.com | AUM: ~$5.5B | HQ: Miami

Founded in 1981, Trivest is among the oldest PE firms in the Southeast US and focuses exclusively on founder-led and family-owned businesses. AUM now $6 billion across four unique funds with 55 portfolio companies as of January 2026 (BusinessWire, January 2026). Their fund structure includes Discovery Fund II ($600M, targeting $1M-$4M EBITDA), Mid-Market Fund VII ($950M, targeting $4M-$15M EBITDA), and Recognition Fund ($1.3B). Target sectors include business services, consumer, healthcare, distribution, and niche manufacturing.

Why it matters for IS: Trivest's "Just Say No" program eliminates typical pain points for founders, making their portfolio companies better acquisition targets for IS-led add-on strategies. Their Discovery Fund targets the fragmented, small-company segment where IS deal flow concentrates.

Alpine Investors

Website: alpineinvestors.com | AUM: $18.8B | HQ: San Francisco

Alpine is the most prolific business services roll-up operator in the market. In 2025 alone, Alpine launched five new platform companies and closed 190 deals across its portfolio. Key business services platforms and their 2026 trajectories:

- Evergreen Services Group: 47 acquisitions in 2025 (33 MSPs), 16 in Q4 alone. Plans 30-40 acquisitions in 2026 with a $5B revenue target by 2030 (National Today, February 2026)

- Apex Service Partners: Now 107 brands with 8,000+ field technicians (HVAC/plumbing/electrical)

- Ascend: 3+ CPA firm acquisitions in January 2026 alone (Gollob Morgan Peddy in TX, Gettleson Witzer in CA, Alexander Almand in GA). Now ranked No. 29 on Accounting Today's Top 100 with $315M revenue and 1,500 employees (CPA Practice Advisor, January 2026)

- Cobalt Service Partners: 17 total transactions

Alpine was ranked #1 in the 2025 HEC Paris-Dow Jones Upper Mid-Market Buyout Performance Ranking.

Why it matters for IS: Alpine demonstrates what business services roll-ups look like at scale. While Alpine operates its own platforms, their playbook validates the IS thesis in every sub-sector they touch. IS sponsors targeting IT services, HVAC, or accounting can use Alpine's track record when pitching capital partners.

Audax Private Equity

Website: audaxprivateequity.com | AUM: ~$19B | HQ: Boston

Audax's Buy & Build strategy has produced more than 170 platforms and 1,300 add-on acquisitions since 1999. Business services is a core specialization, with the firm seeking platforms that show resilience through economic cycles, provide mission-critical services, and operate in fragmented industries with actionable acquisition targets (Audax Private Equity). A notable example: Audax-backed CoolSys completed 8 add-on acquisitions in three years, more than doubling profitability and expanding into HVAC from its refrigeration base.

Why it matters for IS: Audax's 1,300+ add-on track record means they understand the bolt-on economics that drive IS roll-up strategies. Their business services specialization and appetite for mission-critical services align directly with IS deal flow.

Broadtree Partners

Website: broadtreepartners.com | AUM: Undisclosed | HQ: Charlotte

Broadtree Partners is a micro-cap and lower-middle-market PE firm that acquires companies with $1M-$10M EBITDA across business services, technology-enabled services, and government services. Broadtree's differentiator is its Executive-in-Residence model -- the firm installs its own operating leaders into acquired companies, giving founders a clean exit pathway while preserving business continuity (Broadtree Partners). Notable portfolio companies include Triage Partners (telecom and reverse logistics services) and a US government managed print services platform that Broadtree exited to CenterGate Capital in 2023.

Why it matters for IS: Broadtree's $1M-$10M EBITDA target sits at the smallest end of the IS deal spectrum, making them a natural co-investor for independent sponsors pursuing micro-cap business services acquisitions. Their operator-centric model means they bring management talent, not just capital.

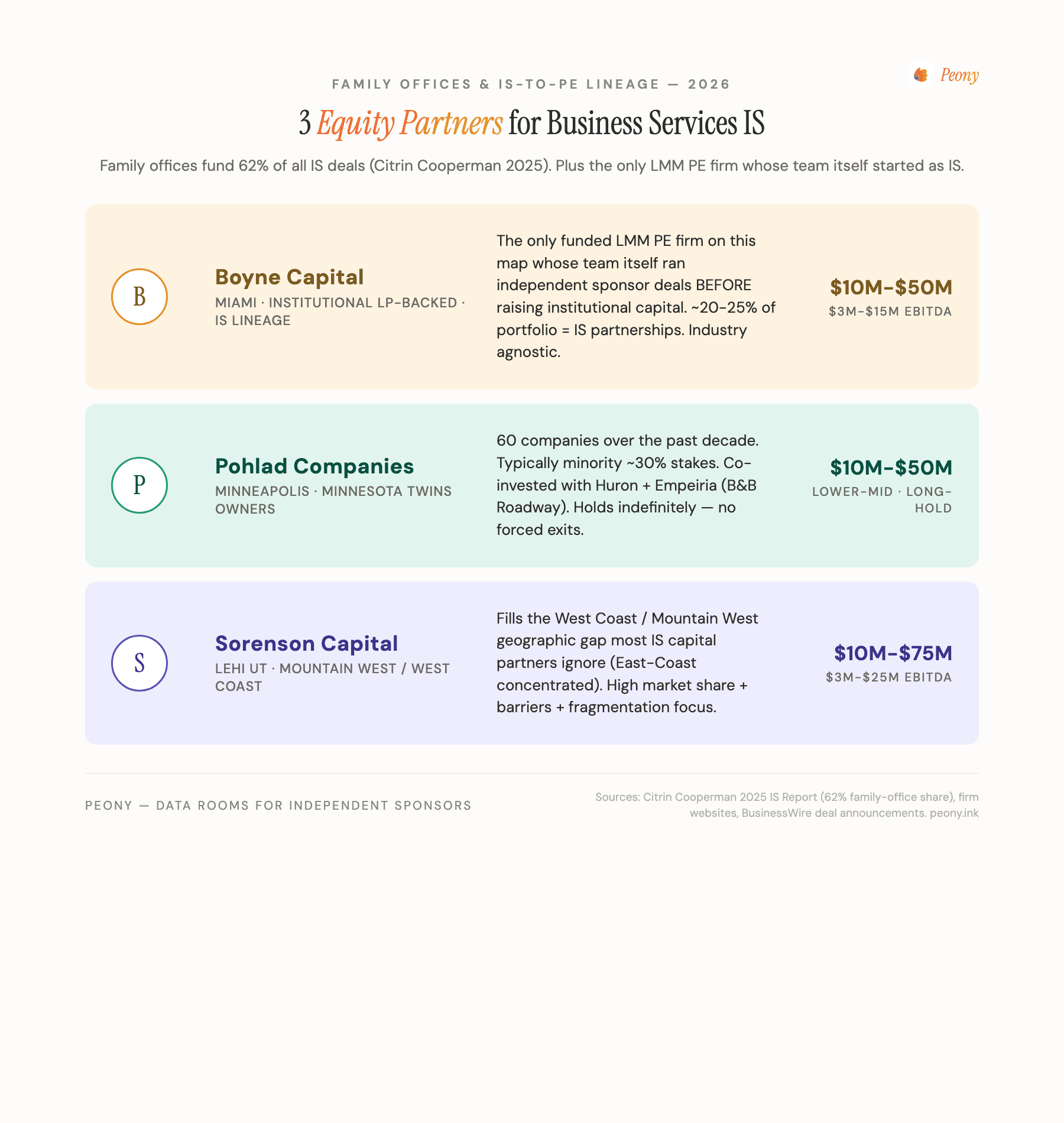

Industry-Agnostic Capital Partners Active in Independent Sponsor Deals

Not every active IS capital provider is sector-focused. A subset of lower middle market investment firms operate as industry-agnostic capital partners — evaluating opportunities across all sectors rather than narrowing to a vertical. They appear in a business services guide because they frequently back business services IS deals, but the fit is driven by deal characteristics (size, structure, sponsor quality), not sector specialization. The correction matters for independent sponsors: these firms are a genuine fit across verticals, not just the ones we happen to list.

Boyne Capital — The IS-to-PE Evolution Story

Website: boynecapital.com | HQ: Miami | Structure: Funded investment firm with institutional LP backing

The lineage that matters: Boyne Capital is one of the very few funded PE firms in the lower middle market whose team has actually sat in the independent sponsor seat. The firm started as an independent sponsor before raising institutional LP capital and evolving into a fully-funded investment firm. When you pitch Boyne, the partners across the table have personally run pre-LOI sponsor diligence, raised deal-by-deal capital, negotiated promote economics, and managed the cash-flow gap between LOI and close. Most "IS-friendly" capital partners learned IS deal mechanics from the outside. Boyne lived them — and that shows up in how they structure transactions, set diligence timelines, and treat the sponsor as a true counterparty rather than a service provider.

Boyne Capital is a funded investment firm with its own institutional LP capital that both executes its own deals and actively partners with independent sponsors. It is not a family office — the firm operates with external LPs and an active investment mandate, writing equity checks of $10M-$50M into companies with $3M-$15M EBITDA.

Sector focus: Industry agnostic. Boyne evaluates opportunities across all sectors and does not narrow to a vertical. Representative experience includes business services, environmental, government-related sectors, niche manufacturing, and infrastructure — but the firm does not limit itself to any specific industry. Independent sponsors in healthcare, consumer, industrials, and tech-enabled services are all in scope if the deal characteristics fit.

Geographic focus: North America — primarily the U.S., with selective activity in Canada and Mexico. No broader cross-border deals.

Independent sponsor activity: Approximately 20-25% of portfolio. Boyne is highly active in the independent sponsor ecosystem, with roughly one-fifth to one-quarter of its portfolio involving IS partnerships. The firm is currently diligencing new IS deals and — as noted in the callout above — operated as an independent sponsor itself before raising institutional LP capital. This is the differentiator that matters most for sponsors evaluating a capital partner.

Why it matters for IS: Boyne's IS-to-PE lineage translates directly into a sponsor-friendly approach across three concrete dimensions. (1) Structuring: the firm understands that promote economics, vesting cliffs, and post-close governance look different through the sponsor's lens than through a traditional PE underwriter's lens — and structures accordingly. (2) Diligence timelines: they know what a sponsor's exclusivity window actually feels like, and they don't burn weeks on questions a former IS partner would have pre-empted. (3) Deal execution: the cash-flow gap between LOI signing and equity close is a survival issue for first-time sponsors, and Boyne's team has personally bridged it. The $10M-$50M equity check and $3M-$15M EBITDA target match the IS sweet spot precisely, and the firm's institutional LP backing means committed capital (not subjective family-office timelines).

Positioning: Active capital partner and IS backer, not a passive family office. The only firm on this list whose team has personally run IS deals before raising the fund.

Family Offices Active in Business Services Independent Sponsor Deals

Family offices fund 62% of all independent sponsor transactions (Citrin Cooperman 2025), and business services is their most natural sector allocation. These companies are easy to understand -- everyone knows what a staffing firm or janitorial company does -- and the recurring revenue profiles match family office preference for predictable cash flow.

Pohlad Companies

Website: pohladcompanies.com | HQ: Minneapolis

The Pohlad family has invested in and built a diverse portfolio of businesses since the 1950s, including ownership of the Minnesota Twins. Their private investment arm has been involved with 60 companies over the past decade, typically taking minority stakes of approximately 30% in companies with predictable business models, strong management, and attractive valuations (Pohlad Companies). Investment focus areas include business services, consumer products, and specialty industrials. The Pohlad family co-invested with Huron Capital and independent sponsor Empeiria Capital in B&B Roadway Security Solutions.

Why it matters for IS: The Pohlad family's patience (they hold businesses indefinitely with no forced exits) and their proven IS co-investment track record make them an ideal capital partner for business services IS targeting long-term value creation over quick flips.

Sorenson Capital

Website: sorensoncapital.com | HQ: Lehi, Utah

Sorenson Capital invests in lower middle market companies with $3M-$25M EBITDA, targeting businesses with significant market share, high barriers to entry, fragmented industry competition, and sustainable profit margins (Sorenson Capital). Business services is a core sector alongside manufacturing and distribution. Their geographic preference for the Mountain West and West Coast provides coverage in a region underserved by the East Coast-concentrated IS capital partner ecosystem.

Why it matters for IS: Sorenson's Mountain West focus fills a geographic gap. Most IS capital partners cluster in New York, Miami, Chicago, and Dallas. If your business services deal is in Colorado, Utah, Arizona, or the Pacific Northwest, Sorenson understands the regional dynamics.

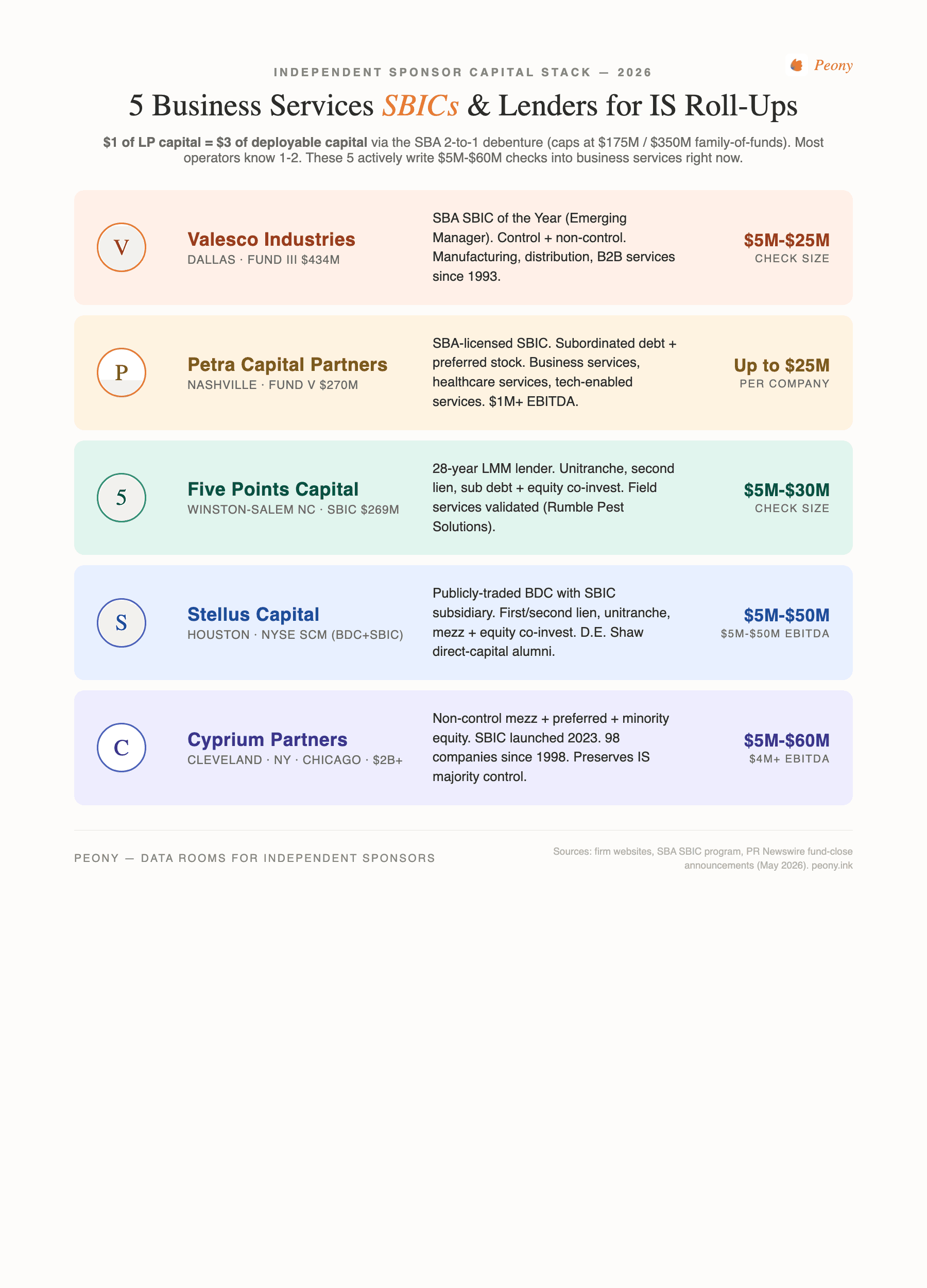

Business Services SBICs and Lenders

SBICs provide subordinated debt and equity that fill critical gaps in business services IS capital stacks. With SBA-leveraged capital, SBICs offer more flexible terms than traditional bank lenders -- particularly valuable for business services acquisitions where asset-light balance sheets limit senior debt capacity.

Valesco Industries (SBIC)

Website: valescoind.com | Fund III: $434M | HQ: Dallas

Valesco has invested in private and family-owned businesses since 1993, focusing on manufacturing, distribution, and business-to-business services. Fund III closed at $434M and received its SBIC license in Q4 2022. The firm makes control and non-control investments of $5M-$25M in companies with $15M-$100M revenue and at least $3M of cash flow (Valesco Industries). Valesco was awarded the SBA SBIC of the Year as an Emerging Manager.

Why it matters for IS: Valesco's SBIC structure, explicit business services focus, and Dallas base put them at the center of the lower middle market IS ecosystem. Their non-control investment option is particularly valuable for IS who want to retain majority ownership.

Petra Capital Partners (SBIC)

Website: petracapital.com | Fund V: $270M | HQ: Nashville

Petra Growth Fund V is an SBA-licensed SBIC targeting business services, healthcare services, and tech-enabled services companies. The fund invests up to $25M per company in equity or debt securities, focusing on companies with $10M-$75M enterprise value and EBITDA greater than $1M (PR Newswire). Petra provides subordinated debt and preferred stock for expansion, acquisition, buyout, or recapitalization.

Why it matters for IS: Petra's explicit business services focus and $10M-$75M EV target directly overlap with IS deal sizes. Their Nashville base, combined with SBIC leverage, provides flexible capital for IS-led business services acquisitions in the Southeast.

Five Points Capital (SBIC)

Website: fivepointscapital.com | Recent SBIC Funds: $269M | HQ: Winston-Salem, NC

Founded in 1997, Five Points provides flexible unitranche, second lien, and subordinated debt solutions with equity co-investment in support of PE investors, direct lending partners, and management teams. The firm serves business and industrial services, manufacturing, distribution, and healthcare services sectors (Five Points Capital). A recent deal: Five Points invested in Rumble Pest Solutions, demonstrating active deployment into the field services sub-sector.

Why it matters for IS: Five Points' 28-year track record in lower middle market lending, combined with their SBIC structure and explicit business services focus, makes them a natural mezzanine partner for IS capital stacks. Their Rumble Pest Solutions investment validates their appetite for field services roll-ups.

Stellus Capital (BDC/SBIC)

Website: stelluscapital.com | NYSE: SCM | HQ: Houston

Stellus Capital Investment Corporation is a publicly traded BDC with an SBIC subsidiary. The firm invests primarily in private middle-market companies with $5M-$50M EBITDA through first lien, second lien, unitranche, and mezzanine debt financing, often with equity co-investment (Stellus Capital). The management team previously led the D.E. Shaw group's direct capital business, bringing institutional credit underwriting to the lower middle market.

Why it matters for IS: Stellus's diverse financing structures mean business services IS can access multiple capital solutions from a single partner -- senior secured debt for the core capital stack plus equity co-investment for alignment.

Cyprium Partners (SBIC)

Website: cyprium.com | AUM: $2B+ invested | HQ: Cleveland, New York, Chicago

Cyprium provides non-controlling mezzanine debt, preferred stock, and minority equity investments in profitable middle market companies, investing $5M-$60M per transaction in companies with $4M+ EBITDA. The firm launched its first SBIC fund in 2023, extending its strategy to the lower middle market. Since 1998, Cyprium has invested over $2 billion in 98 companies across manufacturing, distribution, business services, healthcare, and technology (Cyprium Partners).

Why it matters for IS: Cyprium's non-control model preserves the IS's majority ownership and operating control. Their SBIC fund specifically targets lower middle market companies that IS typically source.

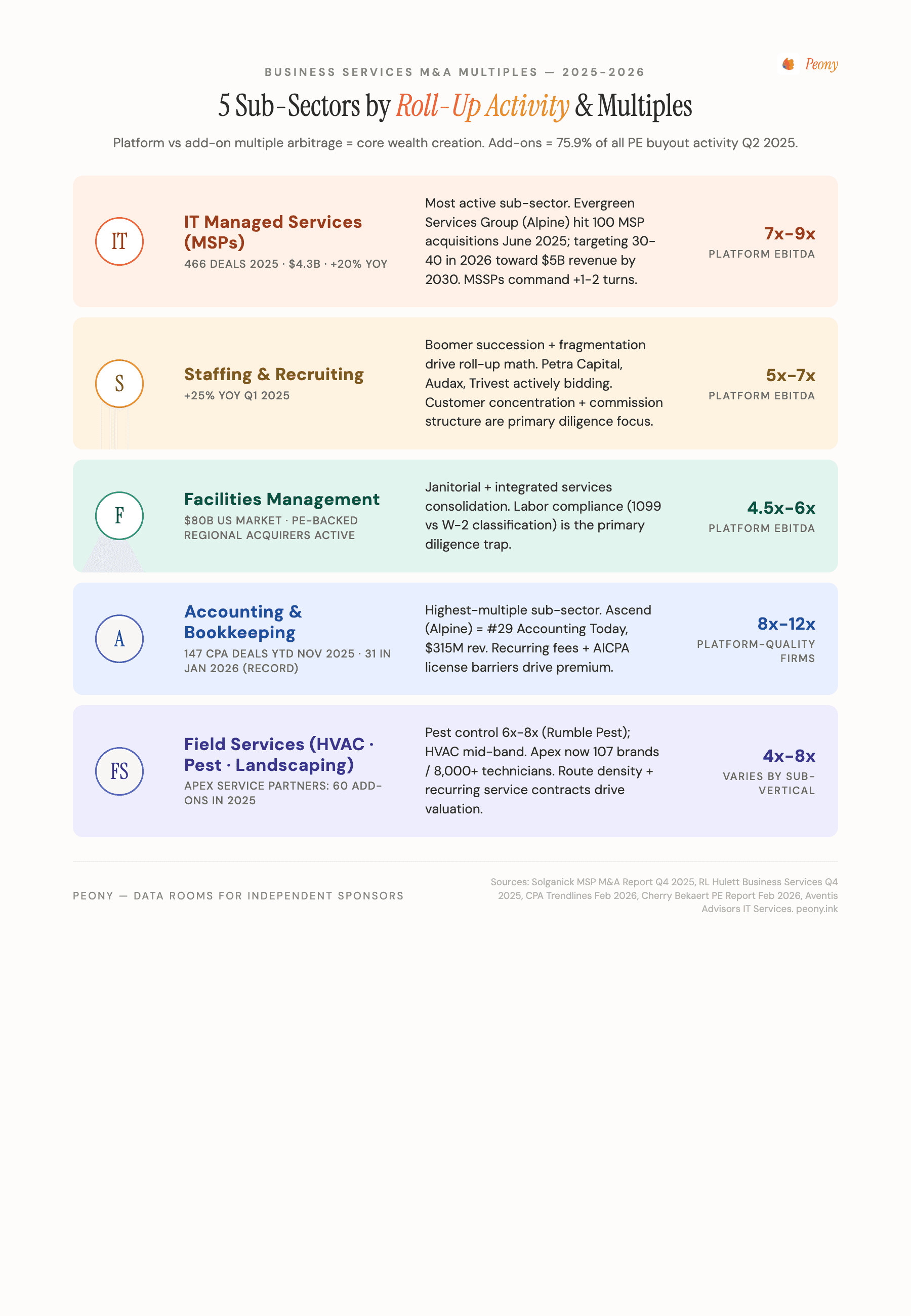

Business Services Sub-Sectors by Deal Activity

Not all business services sub-sectors carry the same deal dynamics. Here is where the deal flow is concentrated in 2025-2026, with verified EBITDA multiples and key dynamics for each.

IT Managed Services (MSPs)

Deal activity: The most active sub-sector by transaction count. Alpine's Evergreen Services Group completed 100 MSP acquisitions by June 2025 and closed 47 transactions in the calendar year, including 33 MSPs. The MSP M&A market saw a notable rise in deal activity in H1 2025, with April and May being particularly active (Solganick).

Multiples: Platform-quality MSPs at 7x-9x EBITDA; smaller MSPs with under $2M EBITDA at 4x-6x. Cybersecurity-focused MSSPs command premiums of 1-2 additional turns (Aventis Advisors).

IS opportunity: Acquire a regional MSP platform at 5x-7x, bolt on smaller MSPs at 3x-5x, centralize PSA/RMM tooling and NOC operations. Exit the consolidated platform at 8x-10x. The recurring monthly revenue model makes MSPs especially bankable.

Staffing and Recruiting

Deal activity: Q1 2025 saw a 25% year-over-year increase in staffing deal volume, the highest since Q4 2022. Analysts forecast 85-100 deals for the full year. PE add-ons remain a key driver, with 63% of recruitment platform deals involving a PE buyer (Griffin Financial Group; UHY).

Multiples: Light industrial/commercial staffing at 4x-4.5x EBITDA; professional staffing at 5x-6x; IT and healthcare staffing at 5.5x-7x. Deferred consideration (earn-outs, seller notes) historically represents about 50% of total consideration in staffing transactions.

IS opportunity: Staffing's high fragmentation and relationship-driven model reward IS who bring operational expertise. Platform acquisitions with diversified client bases and scalable recruiting teams command premiums. The key risk is revenue cyclicality -- contract staffing models trade higher than project-based placement.

Facilities Management and Janitorial

Deal activity: The US janitorial services market reached $80.4 billion in 2024 with a projected increase to $92.3 billion by 2029. PE-backed operators are actively acquiring regional providers to add geography and contracts. Imperial Dade (Advent International) and BradyIFS + Envoy Solutions have been particularly acquisitive (Align BA).

Multiples: Facilities management at 4.5x-6x EBITDA for well-established companies with recurring contracts; smaller regional operators at 4x-5x. Data center facility services command premiums due to growth in hyperscale computing.

IS opportunity: High recurring revenue, essential-service contracts, and massive fragmentation. Buy a regional facilities company at 4.5x, add three smaller janitorial operators at 3x-4x, cross-sell services across the combined customer base. The labor management challenge is real but creates a moat for operators who solve it.

Accounting and Bookkeeping

Deal activity: PE firms closed 147 CPA firm deals through November 2025 (CPA Trendlines). Alpine's Ascend platform completed 18 CPA firm acquisitions in 2025, including its largest deal -- Miami-based KSDT, a Top 200 Firm with 276 professionals (Ascend).

Multiples: Platform-quality CPA firms at 8x-12x EBITDA depending on service mix and client base; smaller practices at 5x-7x. Advisory and consulting-heavy practices command premiums over compliance-only firms.

IS opportunity: CPA firm succession is arguably the most acute of any business services sub-sector. The average CPA firm partner is over 55, and the profession faces a well-documented talent shortage. IS with accounting industry experience can build regional platforms by acquiring retiring partners' practices.

Field Services (HVAC, Pest Control, Landscaping)

Deal activity: Alpine's Apex Service Partners completed 60 HVAC add-on acquisitions across five regions in 2025. In pest control, PE add-on acquisitions surged 35% year-over-year, with PE firms accounting for approximately 60% of all pest control M&A deals (The Deal Sheet). Thompson Street Capital, Citation Capital, EQT, GTCR, and HCI Equity Partners are among the active PE investors in pest control. Five Points Capital invested in Rumble Pest Solutions.

Multiples: Pest control at 6x-8x EBITDA; HVAC at 5x-8x depending on commercial versus residential mix; landscaping at 4x-6x. The pest control market specifically reached $26 billion in 2025 and is projected to grow at a 6.1% CAGR through 2033.

IS opportunity: Field services businesses have the strongest recurring revenue characteristics of any business services sub-sector. Pest control and HVAC maintenance contracts create subscription-like economics. The key IS advantage: most field services companies are owner-operated with $1M-$5M EBITDA -- too small for institutional PE platforms but perfect for IS-led roll-ups.

Key Deal Considerations for Business Services Independent Sponsor Transactions

Business services deals do not carry the regulatory complexity of healthcare acquisitions (no CPOM, Stark Law, or HIPAA), but they have distinct risk factors that capital partners will scrutinize. Address these proactively in your data room.

Customer Concentration

Customer concentration is the #1 deal risk in business services. Capital partners typically require that no single customer exceeds 15-20% of revenue. If your target has a top client generating 30%+ of revenue, expect a purchase price reduction or an earn-out tied to customer retention. Document contract terms, renewal history, and multi-year relationship depth for every top-10 customer.

Mitigation strategy: The roll-up itself is a concentration remedy. Acquiring three add-on businesses with different customer bases immediately dilutes any single customer relationship at the platform level. Present your add-on pipeline as part of the concentration mitigation story.

Contract Structure: Recurring vs. Project-Based Revenue

Capital partners value recurring contractual revenue (monthly retainers, multi-year service agreements) at a significant premium over project-based revenue (one-time engagements, hourly billing). An MSP with 90% monthly recurring revenue trades 2-3 multiple turns higher than a consulting firm with 90% project-based billing.

What to document: Revenue breakdown by contract type, average contract duration, renewal rates, and automatic renewal provisions. If the target has a mix, show the trend -- capital partners want to see project-based revenue converting to contractual over time.

Key Person Risk

In professional services businesses, client relationships often follow individuals, not the company. If the founder personally manages the top five accounts, those relationships are at risk post-close. Capital partners will ask: "What happens to revenue if the founder leaves in 18 months?"

Mitigation strategy: Document management team depth, institutionalized sales processes, and account management structure. Show that client relationships have been transitioned to teams, not individuals. Retention bonuses and equity rollover structures for key employees signal commitment to capital partners.

Technology Enablement

Capital partners increasingly evaluate whether business services companies have adopted technology that creates operational leverage. An MSP using modern PSA/RMM platforms is more valuable than one running on spreadsheets. A staffing firm with an ATS and CRM is more scalable than one relying on the founder's Rolodex.

What to document: Technology stack inventory, automation metrics, and a post-close technology roadmap. The ability to deploy technology across add-on acquisitions (centralizing billing, implementing CRM, standardizing service delivery) is a key value creation lever in business services roll-ups.

Employee Classification and Labor Compliance

Business services companies often use a mix of W-2 employees and 1099 contractors. Misclassification risk is a material diligence issue -- the IRS and state labor departments are increasing enforcement, and reclassification liabilities can materially impact deal economics. Staffing firms, janitorial companies, and IT services providers are particularly exposed.

What to document: Employee vs. contractor classification methodology, any prior audit or inquiry history, and worker classification for every revenue-generating role. Use AI redaction to scrub sensitive employee compensation data before sharing with capital partners.

What Capital Partners Look For in a Business Services Data Room

Business services capital partner diligence moves faster than healthcare or real estate because there is less regulatory complexity -- but capital partners still expect a professionally organized data room from day one. Based on our experience hosting hundreds of business services IS data rooms, here is what capital partners expect -- organized for the staged diligence approach described in our independent sponsor guide.

Stage 1: Initial Risk Scan (Week 1-2)

- Confidential Information Memorandum with roll-up thesis

- Customer concentration analysis (top 10 clients by revenue)

- Revenue breakdown: recurring vs. project-based

- Trailing 12-month financial summary

- Sponsor track record and sector experience

- Add-on acquisition pipeline with target profiles

Stage 2: Deep Dive (Week 2-4)

- Quality of Earnings analysis with services-specific adjustments

- Employee and subcontractor roster with compensation data

- Key person dependency analysis

- Contract portfolio with renewal dates and terms

- Accounts receivable aging by client

- Technology stack assessment and automation metrics

- Insurance certificates and claims history

- Non-compete and non-solicitation agreements

Stage 3: Comprehensive Validation (Week 3-5)

- Post-close 100-day plan with add-on acquisition timeline

- Working capital analysis with services-specific adjustments

- Tax structure analysis (see our tax due diligence checklist)

- Employee classification review (W-2 vs. 1099)

- Customer satisfaction data and NPS scores

- Gross margin analysis by service line and customer

- Management transition plan for retiring founder

For the complete 174-document diligence checklist applicable across all deal types, see our due diligence data room checklist.

Peony AI auto-indexing organizes these documents into a professional folder structure in under 3 minutes. The AI-powered Q&A workflow lets capital partners ask questions like "What is the customer concentration?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. When capital partners can self-serve through diligence questions, the 3-4 week diligence window becomes achievable even when you are running multiple IS deals simultaneously.

Business Services Independent Sponsor Deals By the Numbers

- 75.9% of all PE buyout activity was add-on acquisitions in Q2 2025, with business services roll-ups a primary driver (Cherry Bekaert)

- 979 business services transactions in Q2 2025, up 3.6% year-over-year, with PE representing 42.4% of deal volume (RL Hulett / RSM)

- 12 million boomer-owned businesses approaching succession, with fewer than one-third having formal exit plans (Entrepreneur)

- 10,000 boomers retiring daily -- the largest ownership transfer in US history, estimated at $10 trillion in private business assets (Headway Business Advisors)

- 100 MSP acquisitions completed by Alpine's Evergreen Services Group by mid-2025 (Evergreen Services Group)

- 147 CPA firm deals closed by PE firms through November 2025 (CPA Trendlines)

- 60 HVAC add-on acquisitions by Alpine's Apex Service Partners in 2025 (Alpine Investors)

- $80.4 billion -- US janitorial services market size in 2024, projected to reach $92.3 billion by 2029 (Align BA)

- 62% of IS transactions funded by family offices, with business services their most common sector allocation (Citrin Cooperman 2025)

- $233M oversubscribed close for Align Collaborate Fund I, the first institutional fund exclusively for independent sponsor deals (BusinessWire)

Bottom Line

Business services is the independent sponsor's natural habitat. Recurring revenue, low capex, extreme fragmentation, boomer succession -- every structural force favors the IS roll-up playbook. The capital partner ecosystem for business services IS deals is deeper and more specialized than ever, with dedicated IS equity investors like Align Collaborate, services-focused PE co-investors like Huron Capital and Align Capital Partners, patient family offices like Pohlad Companies, and SBIC lenders like Valesco and Petra Capital.

If you are targeting IT managed services or accounting roll-ups: Alpine Investors' Evergreen and Ascend platforms validate the playbook. Align Capital Partners and Audax Private Equity have the deepest buy-and-build experience. MSP platforms trade at 7x-9x EBITDA; CPA firms at 8x-12x. The key differentiator is recurring revenue quality and technology adoption.

If you are targeting staffing, facilities management, or field services: Huron Capital and Trivest Partners have active deal flow in these sub-sectors, and Boyne Capital evaluates deals here as part of its industry-agnostic mandate. Platform multiples are lower (4x-7x) but add-on arbitrage is significant -- buy at 3x-4x, build to 6x-8x. Customer concentration and labor compliance are the primary diligence issues.

If you need mezzanine or subordinated debt: Valesco Industries (SBIC, business services-focused, Dallas-based), Petra Capital Partners (SBIC, $10M-$75M EV), Five Points Capital (SBIC, field services track record), and Stellus Capital (BDC/SBIC, Houston-based) all provide flexible capital structures tailored to business services M&A deal stacks. For deeper context on private equity co-investment structures and due diligence expectations, see our dedicated solutions guides.

For every business services IS deal: Set up your data room on day one of the exclusivity window. Business services diligence moves faster than healthcare because there is no regulatory gauntlet -- but that means capital partners expect answers faster. You cannot afford to lose days to VDR setup. Peony lets you build a complete business services data room in under 5 minutes, with page-level analytics that show which capital partners are reading the QofE versus skimming the CIM, and AI Q&A that surfaces hard answers with page citations so capital partners complete diligence faster.

Peony starts free. Business is $30/admin/month and Data Room is $52/admin/month -- not $15K per deal. Business includes AI document extraction and basic AI document Q&A, while Data Room adds unlimited rooms and the moderated AI Q&A workflow that multi-capital-partner IS deals demand. When your exclusivity clock is ticking and five capital partners need to get comfortable with the deal simultaneously, every hour matters.

Set up your first business services IS data room in under 5 minutes -- start free.

Frequently Asked Questions

Which capital partners fund business services independent sponsor deals?

Business services independent sponsor deals are funded by three main capital partner types: business services-focused PE firms that co-invest on a deal-by-deal basis such as Align Capital Partners, Huron Capital, and Trivest Partners; family offices with services sector allocations like Pohlad Companies; and SBICs such as Valesco Industries, Petra Capital Partners, and Five Points Capital that provide subordinated debt and equity for business services acquisitions. Family offices fund 62 percent of all IS transactions, and business services is the most common target sector due to recurring revenue and fragmented markets. Peony data rooms let independent sponsors share deal materials with multiple capital partners simultaneously through NDA-gated links while tracking which partners are actively reviewing the quality of earnings report through page-level analytics.

What EBITDA multiples do business services independent sponsor deals trade at?

Business services IS deals typically trade at 4x to 8x EBITDA for platform acquisitions and 3x to 5x for add-ons, compared to 10x to 15x for PE-backed platform transactions at scale. Sub-sector ranges in 2025-2026 include IT managed services at 7x to 9x, professional staffing at 5x to 7x, facilities management at 4.5x to 6x, pest control at 6x to 8x, and accounting and bookkeeping at 8x to 12x for platform-quality firms. The multiple arbitrage between add-on and platform valuations is the core wealth creation mechanism in business services roll-ups. Peony AI document extraction lets capital partners ask questions like What is the customer concentration across uploaded financials and get cited answers with exact page numbers, accelerating the valuation diligence that drives these multiples.

Why is business services the most common independent sponsor target sector?

Business services is the most common IS target sector because four forces converge: recurring or contractual revenue that provides cash flow predictability, low capital expenditure requirements compared to manufacturing or healthcare, extreme market fragmentation with thousands of small operators in every sub-sector, and a baby boomer succession wave with 12 million boomer-owned businesses approaching transition and fewer than one-third having formal succession plans. Deal sizes of 2 to 15 million dollars EBITDA sit in the sweet spot that PE mega-funds ignore but independent sponsors target. Add-on acquisitions accounted for 75.9 percent of all PE buyout activity in Q2 2025, and business services roll-ups are a primary driver of that trend. Peony page-level analytics show which capital partners are spending time on the quality of earnings versus skimming the CIM so sponsors can prioritize follow-ups with genuinely engaged partners.

What documents do business services capital partners need in a data room?

Business services capital partners require standard M&A diligence documents plus services-specific materials: customer concentration analysis showing revenue by client with contract terms and renewal rates, contract versus project-based revenue breakdown, employee and subcontractor roster with key person dependency analysis, technology stack and automation assessment, gross margin analysis by service line and customer, accounts receivable aging by client, insurance certificates and claims history, non-compete and non-solicitation agreements for key employees, and pipeline or backlog data for project-based businesses. Peony lets sponsors set up a complete business services data room in under 5 minutes with AI auto-indexing that organizes these documents into a professional folder structure, and the Smart Q&A workflow routes capital partner questions through AI-drafted answers with page citations before the sponsor approves each response.

How do independent sponsors handle customer concentration risk in business services deals?

Customer concentration is the number one deal-killer in business services IS transactions. Capital partners typically require that no single customer exceeds 15 to 20 percent of revenue, or they will demand a purchase price reduction or earn-out structure tied to customer retention. Independent sponsors mitigate this risk by documenting contract terms, renewal history, and relationship depth for top accounts, and by building a post-close add-on acquisition pipeline that diversifies the customer base through bolt-on acquisitions. The roll-up strategy itself is a concentration remedy because adding three to five acquisitions to a platform naturally dilutes any single customer relationship. Peony AI-powered Q&A lets capital partners ask What is the customer concentration and get cited answers with exact page numbers from the uploaded financials, so concentration risk is addressed in minutes rather than days of manual document review.

What business services sub-sectors have the most independent sponsor deal activity?

The most active business services sub-sectors for independent sponsor deals in 2025-2026 are IT managed services where Alpine Investors platform Evergreen Services Group completed its 100th MSP acquisition in 2025, staffing and recruiting with Q1 2025 deal volume up 25 percent year-over-year, facilities management and janitorial services in an 80 billion dollar US market with PE-backed operators actively acquiring regional providers, accounting and bookkeeping where PE firms closed 147 CPA firm deals through November 2025, and field services including HVAC pest control and landscaping where Apex Service Partners completed 60 add-on acquisitions in 2025 alone. Independent sponsors typically enter as platform acquirers at 4x to 6x EBITDA and build value through add-on acquisitions at 3x to 5x. Peony helps sponsors manage multi-party diligence across these deals with personalized sharing links that track each capital partner separately.

How much does a data room cost for a business services independent sponsor deal?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 2 to 15 million dollar EBITDA business services companies. Business services deals also require frequent data room access for add-on acquisitions during the roll-up phase, meaning sponsors may need four to eight active data rooms simultaneously. Peony starts free with Business at 30 dollars per admin per month and Data Room at 52 dollars per admin per month. Business includes AI document extraction, basic AI document Q&A and screenshot protection, while Data Room adds dynamic watermarks, unlimited data rooms, auto-indexing, and the moderated AI Q&A workflow. All paid plans include NDA gates, page-level analytics, and screenshot protection at no additional cost. An independent sponsor running three business services deals per year pays 360 to 624 dollars total on Peony versus 45,000 to 150,000 dollars on legacy platforms.

What is a business services roll-up and why do independent sponsors pursue them?

A business services roll-up is an acquisition strategy where an independent sponsor buys a platform company at 5x to 7x EBITDA and then acquires multiple smaller add-on businesses at 3x to 5x EBITDA, integrating them onto a single operating platform. The combined entity commands a higher exit multiple of 8x to 12x due to increased scale, diversified revenue, and operational efficiencies. Business services is ideal for roll-ups because sub-sectors like IT services staffing janitorial and field services have thousands of small fragmented operators. The baby boomer succession wave is accelerating supply with 10,000 boomers retiring daily and fewer than one-third of business owners having succession plans. Peony screenshot protection blocks and logs unauthorized capture attempts on sensitive financial projections and roll-up models while dynamic watermarks embed viewer identity into every rendered frame.

Where do business services independent sponsors meet capital partners?

Business services independent sponsors meet capital partners at the McGuireWoods Independent Sponsor Conference with 1,600 attendees in 2025 and the 2026 event on October 27-28 in Dallas, through business services-focused M&A advisors and intermediaries on platforms like Axial where independent sponsors closed 27 percent of all deals in 2025, and through repeat relationships which account for 59 percent of capital partner deals according to Citrin Cooperman. Sector-specific conferences like the Axial Concord conference and iGlobal Independent Sponsor Summit also facilitate introductions. Peony NDA-gated data rooms let sponsors share deal materials professionally after conference introductions with built-in e-signatures for NDAs so capital partners can sign and access materials in a single workflow.

What key person risk means in business services independent sponsor deals?

Key person risk is the risk that a business services company loses significant value if the founder or a small number of critical employees depart. This is especially acute in professional services firms where client relationships are tied to specific individuals rather than the company brand. Capital partners evaluate key person risk by reviewing employment agreements and non-compete terms, analyzing revenue concentration by relationship owner, and assessing whether the business has institutionalized its processes or remains dependent on founder relationships. Independent sponsors mitigate key person risk through retention bonuses, equity rollover structures, and post-close transition plans that shift client relationships from individuals to teams. Peony AI document extraction lets capital partners query employment agreements and non-compete clauses across the entire data room and get cited answers with exact page numbers, surfacing key person risk factors in minutes.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- SBIC for Independent Sponsors -- 2-to-1 debenture math, $175M/$350M caps, 8 active IS-partner SBICs (Tecum/Cyprium/Argosy/Centerfield/Plexus on services deals), $35M EV stack example

- Independent Sponsor Data Room Checklist -- 42-document checklist staged by capital partner type

- Independent Sponsor Healthcare Capital Partners -- 15 firms funding healthcare IS deals

- Independent Sponsor Distribution & Logistics Capital Partners -- 12 firms funding wholesale, 3PL, cold chain, and specialty distribution IS deals

- Independent Sponsor Cleantech & Energy Capital Partners -- 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Capital Partners Funding Both IS and Search Funds -- 9 dual-strategy firms (Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus, Miramar) for self-funded searchers, traditional search funds, and IS deals -- canonical option for $750K-$2M EBITDA business services targets

- Due Diligence Data Room Checklist -- 174-document checklist across 10 categories

- Best Data Rooms for Private Equity -- platform comparison for PE professionals

- M&A Process Guide -- 8-phase lifecycle from strategy to integration

- Tax Due Diligence Checklist -- 8-pillar M&A tax DD framework

- Vendor Due Diligence Checklist -- 6-domain sell-side preparation framework

- Virtual Data Room Redaction Guide -- AI redaction for M&A diligence

- Data Room for Investors -- what investors expect in your data room

- What Is a Virtual Data Room? -- comprehensive VDR explainer

- Peony for Private Equity -- PE-specific data room features

- Peony for M&A -- M&A data room solutions

- Peony for Due Diligence -- diligence workflow tools

You might also like

Apr 16, 2026

Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026

Apr 13, 2026

Independent Sponsor Data Room Checklist (42 Documents, 3 Stages) in 2026

Apr 2, 2026

17 Healthcare Capital Partners for Independent Sponsors ($4.4B) in 2026