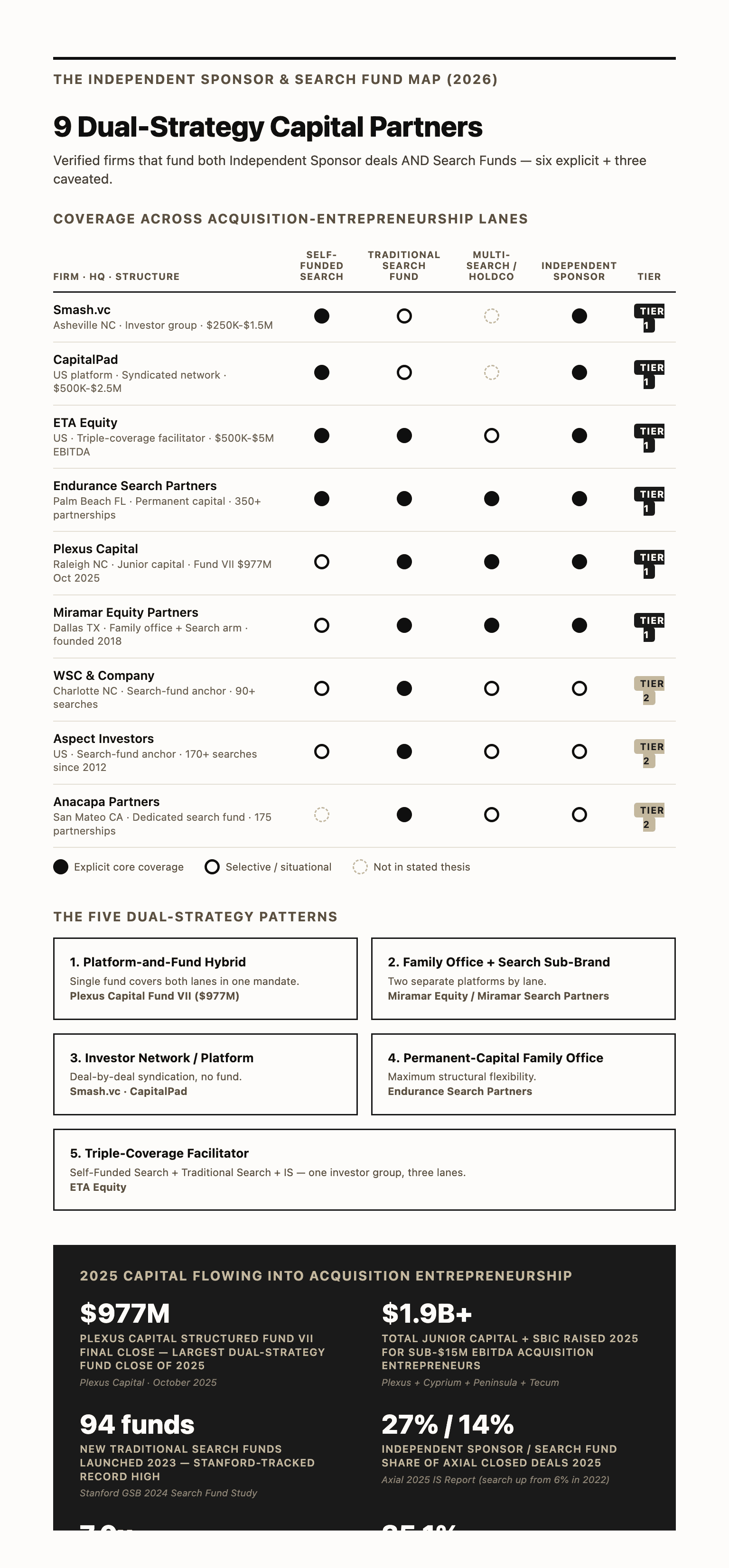

9 Dual-Strategy Capital Partners Funding Searchers + IS in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

Quick answer: Nine capital partners explicitly fund BOTH independent sponsor deals AND search funds in 2026 — six with core dual-strategy positioning (Smash.vc, CapitalPad, ETA Equity, Endurance Search Partners, Plexus Capital, Miramar Equity Partners) and three with caveated overlap (WSC and Company, Aspect Investors, Anacapa Partners). The cleanest dual-strategy stack for a second-time operator carrying a $3M-$8M EBITDA target on deal number two: Plexus Capital (junior capital $5M-$25M) plus Smash.vc or CapitalPad (minority co-invest $250K-$2.5M) plus Endurance Search Partners (permanent-capital family office). Pacific Lake Partners and Search Fund Partners are NOT on the dual-strategy list — they fund first-time MBA searchers under the original Stanford model and do not position for IS deals.

The single hardest question this post answers: which capital partners actually fund both independent sponsor AND search fund deals simultaneously, and how do I pitch each lane differently? Three personas pull this guide most often. First, the IS founder considering a second deal after a successful search-fund acquisition — needs continuity with the same investor group across the structural transition without rebuilding the relationship from cold. Second, the search-fund founder targeting an MBA-track first acquisition who may convert to IS economics on deal two — needs the firms with explicit triple coverage (self-funded + traditional + IS). Third, the family-office principal sizing a first allocation to acquisition entrepreneurship — needs to know which dual-strategy firms are co-invest takers versus full underwriters, so the allocation fits the office's diligence capacity. The 9-firm shortlist below is built specifically for these three reader pulls.

We run Peony, a data room platform. Searcher-and-independent-sponsor dual-strategy fundraising has quietly become one of our fastest-growing use cases in 2026 — driven by self-funded searchers running parallel pitches to 6-10 firms, second-time operators converting from search funds into independent sponsor structures, and capital partners themselves expanding from one lane into both. The single most-asked question on intro calls in Q1 2026: "Which capital partners actually fund both search funds and independent sponsor deals — and how do I pitch them differently?"

Most online resources answer the wrong question. Pacific Lake Partners, Search Fund Partners, Anacapa, and Relay Investments are excellent — they are the canonical search fund firms — but they do not position for independent sponsor deals. Conversely, the typical IS capital partner directories (which we have built for healthcare, manufacturing, tech/software, consumer, distribution/logistics, cleantech/energy, and business services) cover IS-only firms. The gap is the rare firm that does both — and there are real answers, not generic guidance. I spent years evaluating fund-versus-deal-by-deal economics at Backed VC and Target Global before founding Peony, and the dual-strategy firms below are the ones I would actually pitch if I were running a self-funded search today.

This guide maps 9 verified capital partners that explicitly fund both independent sponsors AND search funds in 2026 — six firms with explicit dual-strategy positioning (Smash.vc, CapitalPad, ETA Equity, Endurance Search Partners, Plexus Capital, Miramar Equity Partners), and three firms with strong but caveated overlap (WSC & Company, Aspect Investors, Anacapa Partners). For the foundational mechanics on how independent sponsors raise capital deal-by-deal, see our complete IS guide. For the full IS capital-raising playbook, see our capital raising stage-by-stage walkthrough.

TL;DR: Search funds and independent sponsors are converging in 2026 — driven by Stanford GSB 2024 Search Fund Study reporting a record 94 new searches launched in 2023, 681 cumulative first-time search funds since 1984, and 35.1% average IRR with 4.5x average ROI multiple (Stanford GSB 2024 Search Fund Study). On the IS side, independent sponsors reached 27% of all closed deals on Axial in 2025, the #1 buyer type ahead of PE funds at 20% (Axial 2025 Independent Sponsor Report), and roughly 1,500 active IS firms operate in the US per the H.I.G. Capital lender's-lens market view (H.I.G. Capital, July 2025). The largest dual-strategy fund close of 2025 was Plexus Capital Structured Capital Fund VII at $977 million in October 2025 — ahead of the $750M target — alongside Equity Fund II to total $1.3 billion raised in 5 months (Plexus Capital, October 2025). Plexus explicitly partners with both independent sponsors and search funds, the only fund of that size to position for both lanes. Below: 9 dual-strategy capital partners, their EBITDA criteria across both lanes, and how to pitch each. The market entry point for searchers and operators considering a first or second deal in 2026 is identifying which of these 9 firms fits your profile — most operators only need 3-5 in their rolodex.

Quick Reference Table — 9 Dual-Strategy Capital Partners (2026)

| # | Firm | HQ | Structure | Check Size | Min EBITDA | Dual-Strategy Coverage |

|---|---|---|---|---|---|---|

| 1 | Smash.vc | Asheville, NC | Investor group (deal-by-deal) | $250K-$1.5M | $750K (self-funded), $2M (IS) | Self-funded search + IS |

| 2 | CapitalPad | US-based platform | Investor network/syndication | $500K-$2.5M typical | $500K min, $1M+ preferred | Self-funded search + IS |

| 3 | ETA Equity | US | Facilitator/investor network | Not disclosed | $500K-$5M target | Self-funded + Traditional Search + IS (triple coverage) |

| 4 | Endurance Search Partners | Palm Beach, FL | Permanent-capital family office | Family-office (varies) | $10M-$30M EV target | Search funds + IS platforms + multi-search + holdco + De Novo |

| 5 | Plexus Capital | Raleigh, NC | Junior capital fund ($3.5B AUM) | $5M-$25M | $2M-$12M EBITDA, $10M-$100M revenue | Search funds + IS + PEGs + management teams |

| 6 | Miramar Equity Partners | Dallas, TX | Family office + Search Partners arm | $0.5M-$5M (search), $5M-$30M+ (PE) | $10M+ revenue | Traditional search funds (Miramar Search) + IS/PE (Miramar Equity) |

| 7 | WSC & Company | Charlotte, NC | Search fund-anchor LP, 90+ searches | Not disclosed | $2M-$6M EBITDA | Primarily search funds; opportunistic IS deals |

| 8 | Aspect Investors | US | Search fund-anchor, 170+ searches | Not disclosed | $5M-$50M revenue | Primarily search funds; ambiguous IS positioning |

| 9 | Anacapa Partners | San Mateo, CA | Dedicated search fund (175+ partnerships) | Pro-rata search | Search fund framework | Primarily search funds; flexible structures via principals |

How to read this table: firms 1-6 are the explicit dual-strategy core. Firms 7-9 anchor the search fund-side reference points and may participate in IS deals opportunistically. For pure search fund coverage without IS overlap, see the sidebar later: Pacific Lake Partners, Search Fund Partners, Footbridge Partners, Trilogy Search Partners, and Relay Investments are the canonical search fund-only firms.

What Is a "Dual-Strategy" Capital Partner and Why Does This Niche Exist in 2026?

A dual-strategy capital partner is a firm that explicitly funds both the search fund / self-funded search model (where an operator-CEO acquires and runs a single company they will own and operate) and the independent sponsor model (where a sponsor sources, negotiates, and signs an LOI on a target deal-by-deal, then raises specific capital from family offices, mezz, and SBICs to close). The two models look adjacent on paper — both are "acquisition entrepreneurship" structures targeting lower middle market businesses — but operate with materially different capital structures, investor expectations, and economic incentives.

Why the Lanes Are Merging in 2025-2026

Three structural forces converge in 2026 to make dual-strategy positioning a real category instead of a marketing label:

1. Searcher-to-IS career arc. Operators who close a first acquisition through a search fund or self-funded search structure increasingly want to do a second deal — but the second deal is rarely a fit for traditional search fund economics. The search fund model commits pre-search capital to a single operator-CEO who runs one company. A second deal is structurally an independent sponsor deal: deal-specific capital, no pre-search commitment, sponsor promote on the new transaction. Operators who succeeded in their first acquisition want continuity with the same investor group across this transition — not a fresh investor relationship. Dual-strategy firms like Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners explicitly support this arc.

2. Self-funded search bridges the gap. The fastest-growing acquisition-entrepreneurship structure in 2024-2025 is self-funded search — an operator with $50K-$500K personal capital who finances acquisitions primarily through SBA 7(a) loans (up to $5M) plus minority equity from outside investors. Self-funded search structurally blends search-fund-style operator focus with IS-style deal-by-deal capital. Smash.vc is built specifically for self-funded searchers ($750K+ EBITDA targets, $250K-$1.5M minority checks). The Self-Funded Search Association (selffundedsearch.org) has emerged as a distinct organization in 2024-2025, indicating the structure has reached scale.

3. LP capital flows toward junior capital partnering with both lanes. The single largest dual-strategy fund close of 2025 was Plexus Capital Structured Capital Fund VII at $977 million in October 2025 alongside Equity Fund II, totaling $1.3 billion raised in 5 months (Plexus, October 2025). Plexus's press release explicitly names search funds, independent sponsors, private equity groups, and management teams as eligible partner types. Add Cyprium Partners' SBIC I final close at $190 million in February 2025 (14+ IS-partnered deals as of August 2024) and Peninsula Capital Partners' Fund VIII at $400 million in September 2025 (70+ IS platforms historically), and the 2025 vintage of junior capital available to acquisition entrepreneurs hit a cycle high.

What Dual-Strategy Is NOT

It is important to distinguish dual-strategy capital partners from search fund firms that occasionally invest in an IS deal opportunistically (Pacific Lake Partners, Search Fund Partners, Anacapa Partners, Relay Investments) and from IS-only firms that occasionally back a self-funded searcher when the EBITDA is high enough (Cyprium, Centerfield, Peninsula, Tecum). A dual-strategy firm has both lanes as a stated core thesis, often with separate product lines, sub-brands, or fund mandates that explicitly cover each.

The 9 firms profiled below all clear that bar.

How Do Search Funds, Self-Funded Searches, and Independent Sponsors Actually Differ?

The three structures look adjacent but operate differently across capital structure, governance, and economics. The table below summarizes the differences using verified 2024-2025 benchmarks:

| Dimension | Traditional Search Fund | Self-Funded Search | Independent Sponsor |

|---|---|---|---|

| Operator capital | $0-$50K personal | $50K-$500K personal + SBA 7(a) | $0-$2M personal (typically PE/operator background) |

| Pre-search commitment | $400K-$500K committed by syndicate | None | None |

| Acquisition leverage | 50-65% senior debt typical | SBA 7(a) up to $5M (90% loan-to-value) | Senior + sub debt (3.5x-4.5x total leverage typical 2025) |

| Operator equity post-close | 25-30% with vesting (4-8 years) | 70-90% (operator owns) | 20-30% promote (no vesting on day 1) |

| Investor preferred return | 8% standard | Negotiated case-by-case | 8% standard |

| Target EBITDA range | $2M-$5M (Stanford median implies ~$2M) | $500K-$2M typical (Smash.vc floor: $750K) | $3M-$15M (some larger) |

| Median acquisition multiple | 7.0x EBITDA (Stanford 2024 study) | 4.5x-6x typical | below 6x for 54% of deals (McGuireWoods 2024) |

| Median enterprise value | $14.4M (Stanford 2024) | $5M-$10M | $25M-$100M |

| Investor governance | Heavy — board control, strategic input | Light — typical SBA + minority equity covenants | Sponsor-led with capital partner board seat |

| Hold period | 5-7 years typical | 5-10 years (operator-owned, less pressure to exit) | 4-6 years typical |

| Capital partner promote | None (investor-only economics) | None for SBA; minority equity gets pro-rata | 20-30% promote on deal performance |

The structural overlap that justifies the dual-strategy label is at the post-LOI minority co-investment slot. Whether you are a self-funded searcher with an SBA loan in hand or an independent sponsor with a signed LOI, you have the same need: a $250K-$5M minority equity check from a capital partner who will not run governance and will not displace your operator role. Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners write into exactly that slot regardless of which structural lane you are in. Plexus and Miramar play at higher EBITDA tiers but use the same logic: junior or minority co-investment, operator-led, deal-by-deal flexibility.

Who Are the 9 Capital Partners Writing Checks for Both Models in 2026?

Profiled in order of dual-strategy clarity — firms 1-6 explicitly market both lanes, firms 7-9 anchor the search fund side with selective IS overlap. Each profile covers HQ, structure, check size and EBITDA criteria, dual-strategy positioning, and a verified recent activity datapoint from primary sources only.

1. Smash.vc — The Canonical Self-Funded Search and IS Bridge

Website: smash.vc

Headquarters: Asheville, North Carolina

Founder: Travis Jamison — a 17-plus-year operator and investor who founded approximately 12 SaaS, ecommerce, and marketing companies prior to launching Smash.vc. (Note: Jim Cirigliano contributes editorial content on smash.vc but did not found the firm.)

Structure: A group of individual investors who co-invest deal-by-deal — explicitly not a fund, no LPs, no committed capital pool. Investments funded directly from the firm's principals.

Check size: $250,000 to $1.5 million per transaction.

EBITDA criteria:

- Self-funded searchers: ≥ $750K EBITDA

- Independent sponsors: ≥ $2M EBITDA

(Source: smash.vc/faq/)

Sectors: Home services, consumer services, healthcare services, manufacturing, agencies, B2B services. Industry-agnostic with a preference for durable, lower-disruption sectors.

Equity position: Minority co-investor — explicitly does not lead, does not take board control. Sits alongside the operator's lead capital source (SBA loan for self-funded; family office or mezz for IS).

Stage: From late diligence through post-close growth. Smash.vc joins after the searcher or sponsor has term sheet alignment with the lead capital source.

Unique value-add: Free in-house digital marketing agency for portfolio companies. Smash.vc owns a digital marketing operation (SEO, paid acquisition, content) that portfolio operators can use at no charge — designed to compress the typical 6-12 month post-close marketing rebuild.

Why operators pick them: Travis Jamison was an operator before he was an investor (12+ companies founded, mostly bootstrapped, exited multiple), so the firm pattern-matches on "operator who did it before" rather than "MBA who knows the playbook." For a self-funded searcher targeting a $1M-$2M EBITDA business — too small for traditional search fund firms, too small for most IS capital partners — Smash.vc is often the only credible minority co-investor option.

How to pitch: Lead with the deal economics and your operator profile. Skip the slick deck — Smash.vc's intake process is designed for direct-to-operator conversation, not investment committee review. Bring proof of LOI, SBA pre-qualification (for self-funded), and a 100-day operating plan.

2. CapitalPad — The Syndicated Dual-Strategy Network

Website: capitalpad.com

Headquarters: US-based platform (specific HQ not publicly disclosed)

Founders: Donza Worden and Travis Jamison (the same Travis Jamison who founded Smash.vc — CapitalPad and Smash.vc are related ventures by the same operator group, with overlapping but distinct positioning).

Structure: An investor network and syndication platform — accredited investors aggregate capital for specific deals on a deal-by-deal basis. Not a fund.

Check size:

- Network typical allocation: $1M-$2.5M per transaction

- Smaller allocations: from $500K

- Institutional partners: $750K+ minimum

EBITDA criteria: ≥ $500K EBITDA / SDE minimum, with strong preference for ≥ $1M EBITDA.

Deal size range: $5 million to $30 million enterprise value.

Equity position: Minority equity only, non-control. CapitalPad explicitly does not take majority positions.

Stage: Post-LOI for IS deals; both pre- and post-LOI for self-funded searchers.

Sectors: Founder-led, owner-operated lower middle market businesses in durable, lower-disruption sectors. The firm explicitly avoids ecommerce, cyclical industries, and high-tech-dependent businesses.

Dual-strategy explicit: Yes — CapitalPad's /raise/ page explicitly states they back acquisitions of established profitable lower middle market companies through both the independent sponsor and the self-funded search fund model. (Note: their /independent-sponsor-capital/ direct product line page states the IS-only product does not fund self-funded searchers — but the broader platform does. This nuance is worth understanding before pitching.)

Why operators pick them: The syndication structure means CapitalPad can write larger checks ($1M-$2.5M typical) than Smash.vc by aggregating multiple individual investors per deal. For a self-funded searcher running a $15M EV deal with $2M EBITDA, CapitalPad can take a $1.5M-$2M minority slot — too small for an institutional fund, too large for most individual angels.

How to pitch: Submit deal materials through capitalpad.com directly. The platform reviews deal-by-deal and circulates qualifying opportunities to its network. Expect 2-4 weeks of intake review before any allocation discussions.

3. ETA Equity — Triple-Coverage Facilitator (Self-Funded + Search Fund + IS)

Website: etaequity.com

Headquarters: Dallas, Texas

Founders: Matthew Zucker and Mark Sinatra (founded 2020). One principal is described as "actively invested in search funds and acquisitions since 2008, in over 90 search funds and 30+ acquired businesses."

Structure: A facilitator and investor model that gives accredited investors deal-by-deal access to ETA opportunities across all three structural lanes.

Check size: Not publicly disclosed — varies by deal and investor allocation.

EBITDA criteria: $500K to $5M EBITDA target companies.

Deal types backed: Self-funded search, traditional search fund, AND independent sponsor deals — all three explicitly. This is the most explicit triple coverage of any firm in this dataset.

Stage: Post-LOI for independent sponsors; both pre- and post-LOI for searchers.

Why operators pick them: ETA Equity's positioning is the cleanest "one investor group, three structures" option in 2026. For an operator who has not yet committed to a structure — self-funded search vs traditional search fund vs IS — ETA Equity can engage at any of the three. The triple-coverage framing also signals that the firm understands the structural transitions (search to IS, self-funded to IS) that traditional firms struggle with.

How to pitch: Engage through etaequity.com directly. Bring clarity on which structure your deal fits and why — ETA Equity is structurally agnostic but the diligence work is structure-specific.

4. Endurance Search Partners — Permanent Capital, Maximum Structural Flexibility

Website: endurancesearchpartners.com

Headquarters: Palm Beach, Florida

Founder: Rich Augustyn — Founder and Managing Partner with approximately 15 years of operating experience and 350+ search fund partnerships backed.

Founded year: 2009 (approximately 16-year track record as of April 2026).

Structure: A family office with capital sourced entirely from the firm's partners — permanent capital, no LP fund mechanics.

Fund size: Not publicly disclosed (family office structure).

EBITDA criteria / target size: Companies with $10M-$30M enterprise value.

Deal types backed: Search funds, independent sponsor platforms (explicitly named in firm materials), multi-search funds, due diligence funds, consolidation platforms, holding companies, and "De Novo Search to Start" structures.

Equity position: Minority co-investor.

Sectors: Industry-agnostic with a preference for recurring revenue and defensible competitive position.

Recent activity:

- Latest exit: Westwood (August 2024)

- Latest investment: Guadalimp Suministros (April 2025)

Portfolio examples: Pro Care Unlimited, EdFinMN, OptiMantra.

Why operators pick them: Permanent capital with no LP exit pressure means Endurance can hold investments longer than fund-vehicles and structure flexibly across the entire spectrum of acquisition-entrepreneurship models. The 350+ search fund partnership track record signals deep pattern recognition on operator quality. For a sophisticated operator considering an IS platform structure or a multi-search fund, Endurance's mandate is broader than almost any other firm in the market.

How to pitch: Engage through endurancesearchpartners.com. Bring clarity on which structural variant you are pursuing — Endurance evaluates each on its specific economics rather than fitting deals to a fund mandate.

5. Plexus Capital — The Largest 2025 Dual-Strategy Fund Close

Website: plexuscap.com

Headquarters: Raleigh, North Carolina (with offices in Charlotte)

Founded: 2005

AUM: $3.5 billion across 7 structured capital funds and 2 buyout funds.

Latest fund activity (October 2025): Plexus Capital closed Structured Capital Fund VII at $977 million — ahead of the $750M target — alongside Equity Fund II, totaling $1.3 billion raised in just 5 months (Plexus Capital, October 2025). This is the largest dual-strategy fund close of 2025 by a wide margin.

Check size: Not publicly disclosed per deal; $5M-$25M typical range based on fund size and target company parameters.

EBITDA criteria: $2M-$12M EBITDA, $10M-$100M revenue (Fund VII parameters).

Deal types backed: Independent sponsors, search funds, private equity groups, and management teams in recapitalizations or growth investments — all four named explicitly in the Fund VII press release.

Equity position: Junior capital — subordinated debt with equity ownership component (warrants, conversion features, preferred stock).

Sectors: Founder and family-owned businesses, profitable companies, broad sector coverage with no single-sector concentration.

Why operators pick them: Plexus's $977M Fund VII is the single strongest signal of LP capital flowing into dual-strategy junior capital structures. For an IS sponsor with a $4M-$8M EBITDA platform deal needing $5M-$15M of subordinated debt with equity component, or for a second-time searcher whose acquisition is too large for self-funded search but too small for traditional middle-market PE, Plexus is the canonical 2026 fit. The firm's North Carolina anchor and 7-fund track record gives credibility to LP committees that would otherwise be skeptical of dual-strategy positioning.

How to pitch: Plexus engages through investment bankers, financial intermediaries, and direct sponsor referral. Bring a complete capital structure proposal — Plexus prefers to evaluate deals where senior debt is already committed and the junior capital slot is the gap.

6. Miramar Equity Partners (and Miramar Search Partners)

Website: miramarequity.com and miramarequity.com/search-partners.php

Headquarters: Dallas, Texas

Founder: Kurt Leedy (co-founded Miramar Equity Partners in 2018; leads Miramar Search Partners as the search-side platform).

Founded year: 2018 (Miramar Equity Partners parent).

Structure: Dallas-based family office under Miramar Holdings parent. Two distinct platforms:

- Miramar Search Partners — explicit search fund investor

- Miramar Equity Partners — traditional PE / IS-style deals

Check size:

- Search funds: $0.5M to $5M (average $2.5M), 15-25% interest in cap table

- PE / IS deals: $5M to $30M+ per transaction

EBITDA criteria: Not specified explicitly; targets companies with $10M+ in revenue or bookings.

Sectors: Vertical software, healthcare, infrastructure (per the Smash.vc dual-strategy firm list).

Equity position: Both lanes — 15-25% in search funds; up to control in broader PE deals.

Stage: Both — search phase commitments to searchers (Miramar Search Partners) and post-LOI deals (Miramar Equity Partners).

Dual-strategy explicit: Yes — the two-platform structure is the cleanest "explicitly dual-strategy" model in the dataset. Miramar Search Partners is positioned exclusively for searchers; Miramar Equity Partners runs traditional PE / IS-style deals.

Why operators pick them: Dallas family office with deep Texas and Southwest network, plus the two-platform structure means a searcher who closes a deal through Miramar Search can transition into a Miramar Equity-led IS deal on a subsequent acquisition without changing investor relationships. Permanent capital horizon avoids the typical 5-year fund exit pressure.

How to pitch: Approach through miramarequity.com or miramarequity.com/search-partners.php depending on your structural lane. Miramar's investment committee evaluates separately for each platform — pitch the right one upfront.

7. WSC & Company — Search Fund-Anchor with Selective IS Overlap

Website: wscandcompany.com

Headquarters: Charlotte, North Carolina (per AUM 13F filings; not officially confirmed on firm website).

Co-founders: Badge Stone and Macon Carroll.

Funds:

- WSC Search & Acquire Fund I (older vintage)

- WSC Search & Acquire Fund II (2020 vintage per PitchBook)

Track record: 90+ search fund investments backed across both funds.

EBITDA criteria: $2M-$6M EBITDA targets.

Sectors: Business products, business services, family-owned transitions.

Deal types backed: Per the Smash.vc dual-strategy firm directory, WSC focuses on "traditional search fund model" — not explicitly dual-strategy. WSC may participate in IS deals opportunistically but is not positioned for it as a stated thesis.

Recent activity: YardWorks (residential landscape platform, Charleston SC) — formation of "Yard Alliance" platform.

Why operators pick them: 90+ search fund track record is a meaningful signal of pattern recognition on operator quality. For a searcher whose deal trajectory remains primarily traditional search fund, WSC is a credible mid-tier option (between the largest dedicated firms like Pacific Lake and SFP and the smaller dual-strategy networks like Smash.vc and CapitalPad).

How to pitch: Engage through wscandcompany.com. Be clear that you are running a traditional search fund or self-funded search structure — do not lead with IS framing.

8. Aspect Investors — Search Fund-Anchor with Ambiguous IS Positioning

Website: aspectinvestors.com

Headquarters: Not specified in publicly available materials.

Founder: Andy Love — Founder and Managing Partner. Founded Aspect Investors in 2012 after co-founding VantageCap Partners and Behavioral Health Group (his own search fund) earlier in his career.

Founded year: 2012.

Track record: Investor in 170+ search funds since 2012.

Structure: Traditional search fund focus per firm materials.

Revenue criteria: $5M-$50M target company revenue.

Recent activity: RescueStat acquired by Cardio Partner Resource (August 2025).

Dual-strategy positioning: Ambiguous. Smash.vc's dual-strategy directory does not list Aspect as a positioned dual-strategy firm; Aspect's firm materials emphasize traditional search fund deals. Aspect does fund operators who pursue various structural variants but does not explicitly market dual-strategy positioning.

Why operators pick them: Andy Love's background as a former searcher (he built Behavioral Health Group through his own search fund) means Aspect's diligence is operator-empathetic. The firm has a reputation for giving searcher-CEOs significant operating autonomy post-close — useful for operators who want to avoid heavy investor governance.

How to pitch: Engage through aspectinvestors.com. Lead with traditional search fund framing; if your structure later evolves toward IS, expect a structural conversation rather than automatic continuity.

9. Anacapa Partners — Dedicated Search Fund with Flexible Principal Engagement

Website: anacapapartners.com

Headquarters: San Mateo, California.

Founder: Jeff Stevens — Founder and Managing Partner. Stevens is one of the first generation of search fund entrepreneurs, having managed three funded searches between 1990 and 2005 before founding Anacapa.

Founded year: 2010.

Structure: Dedicated search fund investor.

Track record: 175 individuals or partnerships backed as of 2025; 60+ operating company investments over the past decade.

Sectors: B2B, B2C, energy, financial services, IT, industrials, SaaS, mobile and enterprise software.

Dual-strategy positioning: Per firm materials, focused exclusively on the search fund framework. NOT explicit dual-strategy. The firm invests in search fund principals who go on to pursue various structural variants (including occasional IS-adjacent deals) but does not market dual-strategy positioning.

Why operators pick them: Anacapa's 25-year track record across 175 partnerships gives it the deepest historical pattern recognition on first-time searchers in the US. For an MBA-track searcher running a traditional search fund process, Anacapa is one of the canonical first-tier investors.

How to pitch: Engage through anacapapartners.com. Anacapa's diligence process is rigorous and oriented around traditional search fund economics — do not pitch IS structure framing.

What Three Recent Dual-Strategy Moves Signal That the Lanes Are Merging in 2025-2026?

Three concrete 2024-2025 events show how the dual-strategy capital partner ecosystem is consolidating. Each is sourced to primary firm announcements or verified secondary sources.

Move 1: Plexus Capital Fund VII Closes at $977M with Search Funds Named in the Press Release (October 2025)

Plexus Capital announced the final close of Structured Capital Fund VII at $977 million in October 2025 — significantly above the $750 million target — alongside Equity Fund II, totaling $1.3 billion raised in 5 months (Plexus Capital announcement, October 2025; BusinessWire press release, October 14, 2025). The press release explicitly names independent sponsors, search funds, private equity groups, and management teams as eligible partner types — making Plexus the only sub-$15M EBITDA junior capital fund of that size to position for both the search fund and IS lanes simultaneously.

Why this matters: A $977M raise with explicit dual-strategy mandate signals that institutional LPs (pension funds, endowments, sovereign wealth) are now allocating dedicated capital to firms that can deploy across both search fund and IS deals. This is the strongest "the lanes are merging" data point of 2025.

Move 2: Endurance Search Partners' Guadalimp Suministros Investment (April 2025) Demonstrates Family-Office Multi-Structure Flexibility

Endurance Search Partners announced the Guadalimp Suministros investment in April 2025 — a target acquired through a structure that blends search fund principles (operator-CEO leading the company) with independent sponsor capital structuring (deal-by-deal capital, not pre-search committed capital). Endurance's portfolio includes both pure search fund deals (Pro Care Unlimited, EdFinMN, OptiMantra) and IS-style platform investments. The April 2025 Guadalimp deal demonstrates the firm actively deploying across both lanes simultaneously rather than as exception cases.

Why this matters: Permanent capital family offices with explicit multi-structure flexibility offer a meaningful alternative to traditional fund vehicles for operators whose deal economics do not fit standardized search fund or IS templates. Endurance's 350+ partnership history validates the model at scale.

Move 3: Aspect Investors' RescueStat → Cardio Partner Resource Sale (August 2025) Shows the Search Fund Exit Cycle Is Healthy

Aspect Investors' portfolio company RescueStat was acquired by Cardio Partner Resource in August 2025 — a successful search fund exit that validates the underlying acquisition-entrepreneurship model. Stanford GSB 2024 Search Fund Study reports an average IRR of 35.1% and ROI multiple of 4.5x for traditional search funds (with 42.9% IRR for exited deals). The continued flow of successful exits — RescueStat is one of dozens in 2024-2025 — sustains LP appetite for both search fund firms and dual-strategy expansions.

Why this matters: Successful exits in the search fund universe directly translate to LP capital available for dual-strategy firms to deploy on subsequent deals — including IS deals from operators who succeeded in search funds. The exit cycle is healthy enough to sustain Plexus's $977M raise and Endurance's continued portfolio expansion.

What Are the Five Dual-Strategy Patterns Capital Partners Follow?

Capital partners that fund both search funds and independent sponsors typically follow one of five structural patterns. Understanding which pattern each firm uses helps an operator pick the right capital partner for their specific structural lane.

Pattern 1: Platform-and-Fund Hybrids

A single fund with a mandate that explicitly covers both search funds and independent sponsors as eligible partner types. Plexus Capital Structured Capital Fund VII ($977M, October 2025) is the canonical example. The fund's investment committee evaluates each opportunity using a single set of criteria but accepts both structural lanes. Advantages: simplified fundraising mechanics, single LP base. Disadvantages: investment committee may pattern-match toward whichever lane has the strongest recent track record, leading to bias.

Pattern 2: Family Office with Search-Side Sub-Brand

A family office that runs traditional PE / IS-style deals as the primary business and operates a separate sub-brand or platform for search fund investments. Miramar Equity Partners (with Miramar Search Partners) is the cleanest example. The two platforms have separate websites, separate investment committees, and different deal-size targets. Advantages: clear lane separation, dedicated team per lane. Disadvantages: fewer cross-lane opportunities than a single-fund hybrid.

Pattern 3: Investor Network / Platform (Deal-by-Deal Syndication)

A network of accredited investors who aggregate capital deal-by-deal across both search fund and IS opportunities — explicitly not a fund. Smash.vc (Travis Jamison, Asheville NC) and CapitalPad (Travis Jamison and Donza Worden) are the canonical examples — both run by the same operator group with overlapping but distinct positioning. Advantages: maximum flexibility, no fund mechanics, fast decision cycles. Disadvantages: smaller individual checks, harder to scale to larger deals.

Pattern 4: Permanent Capital Family Office (Maximum Structural Flexibility)

A family office with permanent capital sourced from the firm's partners that explicitly supports multiple acquisition-entrepreneurship structures: search funds, multi-search funds, due diligence funds, IS platforms, holding companies, and "De Novo Search to Start" variants. Endurance Search Partners (Rich Augustyn, Palm Beach FL) is the canonical example with 350+ search fund partnerships. Advantages: longest hold periods, most structural flexibility, no LP exit pressure. Disadvantages: deal flow can be lumpy because investment committee is small.

Pattern 5: Triple-Coverage Facilitator

A facilitator or investor model that explicitly supports all three lanes — self-funded search, traditional search fund, and independent sponsor — with no preference for any. ETA Equity is the canonical example with explicit triple coverage in firm materials. Advantages: maximum operator optionality across structural transitions. Disadvantages: less specialization than firms that focus on one or two lanes.

Why Aren't Pacific Lake Partners and Search Fund Partners on the Dual-Strategy List?

The two largest dedicated search fund firms in the US — Pacific Lake Partners and Search Fund Partners — are not on this dual-strategy list because neither positions for independent sponsor deals as a stated thesis, despite often being the default starting point for operators considering acquisition entrepreneurship.

Pacific Lake Partners — The Search Fund Original Trail

Pacific Lake Partners (Boston with a Bay Area office) was founded in 2009 by Coley Andrews and Jim Southern. Jim Southern was the first search fund principal in 1984 under the mentorship of Irv Grousbeck (the search fund founder at HBS); Coley Andrews is a Stanford GSB MBA and Lecturer at Stanford GSB. Pacific Lake closed Fund IV at $175 million in 2019 with mostly returning investors — no public Fund V close announcement as of April 2026. The portfolio includes 30+ operating companies including Arizona College, Falcon Critical Care Transport, IS Logistica, Chronus, and Omatic. The firm's most recent acquisition was LabShares Newton (September 2023).

Pacific Lake's mission is anchored in the original Stanford / HBS search fund model. Their LP base, governance structure, and investment committee process is built around pre-search committed capital and traditional search fund economics — not deal-by-deal IS capital. Pacific Lake does not market for IS deals and does not position as dual-strategy.

Search Fund Partners (SFP) — The Palo Alto Anchor

Search Fund Partners (SFP) (Palo Alto) was founded in 2004 by Rich Kelley and David Carver. The firm has invested in 175+ searches, closed 100+ deals, and raised 6 funds. Recent investments include Paragon Legal (late 2018), Dr. Snip (July 2021), and Page Vault (September 2022).

SFP's mandate is similarly search-fund-only. The firm does not position for independent sponsor deals as a stated thesis.

Why Most Dedicated Search Fund Firms Don't Cross Into IS

Three structural reasons explain why the largest search fund firms stay search-fund-only:

-

LP base mismatch. Search fund LPs commit capital to pre-search vehicles with specific economic terms (pro-rata acquisition equity, sponsor promote with vesting, 8% pref). Independent sponsor LPs are typically family offices and high-net-worth individuals who underwrite each deal on its own merits. The LP fundraising mechanics, governance covenants, and reporting standards are different.

-

Investment committee orientation. A search fund firm's IC pattern-matches on operator quality, sector thesis, and deal trajectory toward a single target acquisition. An IS deal IC pattern-matches on the specific target's diligence package, capital structure, and exit thesis. Building both into one firm is operationally complex.

-

Mission lock. Firms like Pacific Lake and SFP are explicitly mission-driven around the original Stanford / HBS search fund model. Expanding into IS would dilute the mission and the LP narrative.

For operators who want exposure to both lanes through the same investor relationship, the dual-strategy firms profiled above (Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus, Miramar) are the right starting point. Pacific Lake and SFP remain canonical references for traditional search fund deals only.

Other Pure-Search-Fund Reference Firms (Not Dual-Strategy)

Beyond Pacific Lake and SFP, the following firms are canonical search fund-only investors and do not market dual-strategy positioning:

- Footbridge Partners (NY/SF; founded 2012 by Greg Geronemus and David Rosner; Footbridge Partners I 2012, Footbridge Partners II 2019)

- Trilogy Search Partners (Bellevue WA; founded 2014; 66 portfolio companies as of August 2024 with 18 acquisitions)

- Relay Investments (Boston; founded 2013 by Sandro Mina; $200M dedicated to search fund investments; 250+ search funds invested, 160+ acquisitions, 65+ exits)

For operators running pure traditional search fund processes with no plan to transition to IS, this set plus Pacific Lake, SFP, and Anacapa is the canonical reference.

How Do I Pick the Right Dual-Strategy Partner for My Searcher or IS Profile?

The decision framework below uses three primary variables — searcher capital available, target EBITDA range, and structural preference — to map operator profiles to the dual-strategy firms most likely to fit.

Decision Matrix

| Operator Profile | Recommended Partner Type | Best-Fit Firms (2026) |

|---|---|---|

| Pre-search MBA, no operating capital, target $2M-$5M EBITDA, 24-month search runway need | Traditional search fund investors (committed pre-search capital) | Pacific Lake Partners, Search Fund Partners, Anacapa Partners, Relay Investments |

| Mid-career operator, $50K-$500K personal capital, target $750K-$2M EBITDA, SBA 7(a) loan candidate | Self-funded search investors (dual-strategy minority co-investors) | Smash.vc, CapitalPad, ETA Equity, Endurance Search Partners |

| Experienced PE/operator, target $3M-$10M EBITDA, want minority IS structure with junior capital | IS-positioned junior capital (dual-strategy compatible) | Plexus Capital, Miramar Equity Partners (Equity side), Endurance, Cyprium |

| Searcher who closed first deal, want to convert to IS for second deal, EBITDA $3M-$8M | Dual-strategy continuity firms | Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus |

| IS sponsor needing $5M-$15M junior capital on $5M-$12M EBITDA platform deal | Junior capital with explicit dual-strategy mandate | Plexus Capital, Cyprium Partners, Peninsula Capital Partners |

| Operator pursuing search fund and IS holdco platform simultaneously (multi-search variant) | Permanent-capital family office with maximum flexibility | Endurance Search Partners, Miramar Equity Partners |

| Self-funded searcher targeting $5M-$15M EV with $750K-$1.5M EBITDA, needs $250K-$1M minority equity | Smallest-check dual-strategy network | Smash.vc (primary fit), CapitalPad (if larger check needed) |

How to Build a 5-Firm Dual-Strategy Rolodex

Most operators should build a rolodex of 3-5 dual-strategy firms that cover their structural lane and target EBITDA range. The minimum-viable rolodex for each profile:

Self-funded searcher, $750K-$1.5M EBITDA target: Smash.vc (primary), CapitalPad (larger check option), ETA Equity (triple coverage), Endurance Search Partners (permanent capital), one local family office.

Independent sponsor, $3M-$8M EBITDA target: Plexus Capital (largest junior capital fund), Miramar Equity (Equity side), Endurance Search Partners (platform structure), Smash.vc or CapitalPad (minority co-invest), one IS-specialist family office from your sector vertical.

Searcher transitioning to IS for second deal: Smash.vc, CapitalPad, ETA Equity, Endurance, Plexus — all five fit. Pick the 2-3 with the strongest fit for your specific second-deal EBITDA range.

For sector-specific IS capital partner directories beyond dual-strategy firms, see our detailed verticals:

- Healthcare IS capital partners

- Manufacturing IS capital partners

- Tech/Software IS capital partners

- Consumer IS capital partners

- Distribution/Logistics IS capital partners

- Cleantech/Energy IS capital partners

- Business Services IS capital partners

- SBIC for Independent Sponsors

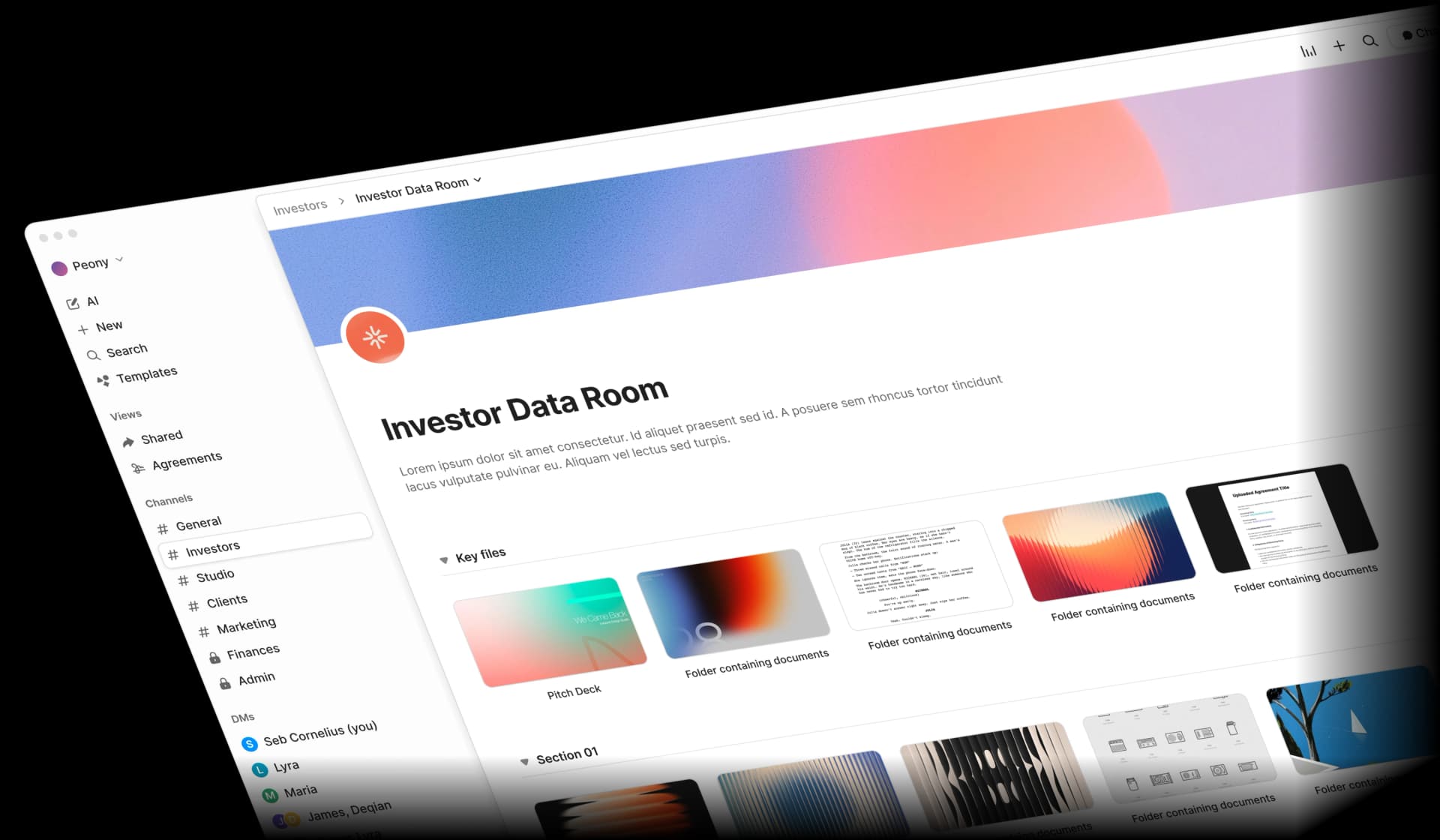

How Do I Securely Share a Data Room with Both Search Fund and IS Investors Simultaneously?

Self-funded searchers, second-time operators, and IS sponsors raising from dual-strategy firms typically pitch 6-12 capital partners simultaneously. The data room workflow has to handle two distinct review patterns at once — heavy lead-investor diligence and lighter minority co-investor review — without leaking sensitive customer concentration, vendor agreements, or financial detail to firms that have not signed an NDA.

What a Dual-Strategy Data Room Needs

| Capability | Why It Matters for Dual-Strategy Fundraising | Peony Data Room ($52/admin/month) | DocSend ($350/user/month) | Datasite ($25K-$30K/deal) |

|---|---|---|---|---|

| NDA-gated access per investor | Customer concentration, vendor rebate schedules, and target-specific identity must be hidden until each capital partner signs an NDA | Built-in NDA workflow per link | Not supported | $25K+ per deal to configure |

| Page-level analytics | Identify which capital partners spent 45 minutes on working capital normalization vs 8 minutes on the cover memo | Page-by-page view time per visitor | Page-level (cover only) | Available on enterprise tier |

| Dynamic watermarks | Embed each viewer's identity into every rendered page so any forwarded document traces back to source | Identity-bound watermarks on every page | Not available | Available on enterprise tier |

| Screenshot protection | Block and log unauthorized screen capture attempts during sensitive document review | Active screenshot blocking + audit log | Not available | Available on enterprise tier |

| Link expiry / instant revocation | Revoke access if a conversation goes cold without removing the room | Per-link expiry + one-click revocation | Available | Available |

| AI auto-indexing | Organize 50-100 documents into a professional folder structure in under 3 minutes | AI auto-indexing by document type | Not available | Manual setup ($5K+ services) |

| Smart Q&A | Route capital partner questions through AI-drafted answers with page citations before team approval | Built-in Smart Q&A workflow | Not available | Manual Q&A board |

The cost difference is structural: a self-funded searcher running 1-2 deals per year on Peony Data Room pays roughly $624 annually. A multi-deal independent sponsor running 4-6 deals per year still pays $624 annually on Peony Data Room — versus $100,000 to $180,000 on Datasite at $25K-$30K per deal across 4-6 deals.

Sharing a CIM with Pacific Lake, Smash.vc, ETA Equity, and CapitalPad simultaneously through a single Peony room (with separate NDA-gated links per firm) replaces 4 separate Dropbox folders and gives 4 independent engagement signals in real time. The follow-up call list ranks itself: the 2-3 firms with 30+ minutes on the deal materials are the genuine candidates worth chasing.

How Much Capital Actually Flowed Through Dual-Strategy and Acquisition-Entrepreneurship Firms in 2025-2026?

Verified 2025 capital flows across the dual-strategy and acquisition-entrepreneurship ecosystem:

| Firm / Source | 2025 Capital Event | Amount | Date | Source |

|---|---|---|---|---|

| Plexus Capital Fund VII | Final close (above $750M target) | $977 million | October 2025 | Plexus Capital |

| Plexus Equity Fund II | Final close (above $250M target, raised in 3 months) | $345 million | October 2025 | BusinessWire |

| Cyprium Partners SBIC I | Final close (14+ IS deals through Aug 2024) | $190 million | February 2025 | Cyprium Partners |

| Peninsula Capital Partners Fund VIII | Final close (70+ IS platforms historically) | $400 million | September 2025 | Dorsey Press |

| Tecum Capital SBIC IV | Final close | $325 million | July 2025 | Tecum Capital |

| Stanford 2024 Search Fund Study | New search funds launched in 2023 (record high) | 94 funds | Reported June 2024 | Stanford GSB |

| Stanford 2024 Search Fund Study | Cumulative first-time search funds since 1984 | 681 funds | Through Dec 31, 2023 | Stanford GSB |

| Stanford 2024 Search Fund Study | Median acquisition multiple | 7.0x EBITDA | Through 2023 | Stanford GSB |

| Stanford 2024 Search Fund Study | Average IRR | 35.1% | Through 2023 | Stanford GSB |

| Axial 2025 | Search funds share of closed deals (up from 6% in 2022) | 14% in 2025 | YTD 2025 | Axial |

| Axial 2025 | Independent sponsor share of closed deals (#1 buyer type) | 27% in 2025 | YTD 2025 | Axial 2025 IS Report |

| Citrin Cooperman 2025 IS Survey | IS deals closing at 4x-6x EBITDA | 54% of deals | 2025 | Citrin Cooperman |

| H.I.G. Capital July 2025 Lender's Lens | Active independent sponsor firms in US | ~1,500 | July 2025 | H.I.G. Capital |

The combined picture: $1.9+ billion of dedicated junior capital and SBIC capacity raised in 2025 alone for sub-$15M EBITDA acquisition-entrepreneurship deals (Plexus Fund VII + Equity Fund II + Cyprium SBIC I + Peninsula Fund VIII + Tecum SBIC IV), plus 94 new traditional search funds in 2023 (Stanford 2024 study), plus 14% search fund share of all Axial closed deals up from 6% in 2022. The dual-strategy infrastructure available to operators in 2026 is the largest in the cycle to date.

Frequently Asked Questions

I am a self-funded searcher with $750K of personal capital targeting a $1.5M EBITDA business — which capital partners back both self-funded searches and independent sponsor deals?

Self-funded searchers in the $500K-$2M EBITDA range looking for a partner who will also back later IS deals have a small but real shortlist in 2026. Smash.vc (Travis Jamison, Asheville NC) writes $250K-$1.5M minority checks against $750K+ EBITDA targets for self-funded searchers and steps up the EBITDA floor to $2M for true IS structures — same investor group, two product lines. CapitalPad (Travis Jamison and Donza Worden) operates a syndicated network with $500K-$2.5M typical allocations across $5M-$30M enterprise value targets in $500K+ EBITDA companies through self-funded search and IS structures alike. ETA Equity offers the most explicit triple coverage in the market: self-funded search, traditional search funds, and independent sponsors at $500K-$5M EBITDA targets. Endurance Search Partners (Rich Augustyn, Palm Beach FL) is a permanent-capital family office that backs search funds, multi-search funds, due diligence funds, holdco platforms, and explicitly named independent sponsor platforms across $10M-$30M enterprise value targets. For a $1.5M EBITDA target, Smash.vc or CapitalPad fits the check size cleanest. Peony at $30 per admin per month gives you a single data room you can share with all four through NDA-gated links — Google Drive folders give you zero tracking on who actually opened the customer concentration analysis, and DocSend has no NDA workflow at all.

I am a Stanford GSB MBA raising a traditional search fund for $400K of search capital — should I also pitch dual-strategy capital partners?

Traditional search fund investors like Pacific Lake Partners, Search Fund Partners, Anacapa Partners, and Relay Investments still write the largest committed pre-search checks for first-time searchers. Stanford GSB 2024 Search Fund Study tracked 681 cumulative first-time search funds since 1984 with 94 launched in 2023 alone — a record high — at a 35.1% average IRR and 4.5x ROI multiple. Pure-play search fund investors fund searchers across roughly 16 partnerships per cohort at $400K-$500K of search capital plus pro-rata acquisition equity. Dual-strategy firms like Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners write smaller minority co-investment checks alongside the lead search fund equity rather than committing pre-search capital. The cleanest path for a Stanford or HBS MBA raising $400K of search capital in 2026 is still the dedicated search fund universe (Pacific Lake, SFP, Anacapa, Relay, Trilogy Search Partners, Footbridge) for the lead investor slot — but adding 2-3 dual-strategy minority co-investors during deal close gives you optionality if you later want to do an independent sponsor deal post-acquisition. Peony page-level analytics show which investor partners spent 30 minutes on your industry thesis versus skimmed the cover letter, and which partners are genuine candidates to lead.

I closed my first search fund acquisition in 2024 and now want to do an IS deal in 2026 — which capital partners support that career arc?

Searchers who successfully close a first acquisition and want to do a second deal as an independent sponsor — keeping the operational role but raising deal-specific capital instead of committed pre-search capital — typically need a different capital partner stack the second time around. Pacific Lake Partners and Search Fund Partners are pure search fund firms; they commit pre-search capital to first-time searchers, not to second-time IS sponsors. Smash.vc and CapitalPad explicitly market to operators making this transition: minority co-investment for both self-funded searchers and post-LOI IS deals at $250K-$2.5M check sizes. ETA Equity's triple-coverage thesis lets you stay with the same investor group from search through IS. Plexus Capital's Structured Capital Fund VII (closed at $977M in October 2025, ahead of the $750M target) explicitly names search funds and independent sponsors as partner types — junior capital with equity at $5M-$25M for $2M-$12M EBITDA targets. Endurance Search Partners is a permanent-capital family office whose mandate explicitly covers both lanes. For a second-time operator with a closed first deal and $3M-$8M EBITDA target on deal #2, Plexus + Smash.vc or CapitalPad + Endurance is the canonical dual-strategy stack. Sharing your CIM, financials, and second-deal thesis through Peony at $30 per admin per month means each capital partner gets page-level analytics and dynamic watermarks — a workflow Datasite charges $25K+ per deal to configure.

How do search fund and independent sponsor capital structures actually differ — what does my data room need to look different for each?

Search funds raise committed pre-search capital from a syndicate of investors who cover the searcher's salary plus search expenses for ~24 months, then take pro-rata equity in the eventual acquisition with a stepped-up multiple (1.5x typically). The data room emphasizes the searcher (resume, references, search criteria, sector thesis, target list) more than any specific deal — you are pitching the operator before any company exists. Independent sponsors raise capital deal-by-deal post-LOI from family offices, mezz funds, SBICs, and dual-strategy firms — the data room emphasizes the specific target (full QofE, Q&A logs, customer concentration, vendor agreements, working capital normalization) and the sponsor's track record on prior deals. Self-funded searchers blend both: pre-LOI personal capital plus SBA 7(a) loan to ~$5M, then minority co-investors join post-LOI. For a self-funded searcher running a $5M EV deal with 90% SBA + 10% equity, the data room blends a search-style sponsor profile with IS-style target diligence. Peony AI auto-indexing organizes 50+ files into a professional folder structure in under 3 minutes, and Smart Q&A routes capital partner questions through AI-drafted answers with page citations before your team approves each response. At $52 per admin per month for Data Room tier, the cost is less than one DocSend seat at $350 per user per month while supporting both data room types.

I run a single-family office considering our first search fund or IS investment — how do dual-strategy firms structure equity differently for search vs IS deals?

Search fund equity is structured around the operator with three step-ups: pre-search capital pro-rata converts at acquisition, plus a sponsor promote (typically 25%-30% vested over 4-8 years tied to time, performance, and sale milestones), plus an investor preferred return. The Stanford GSB 2024 study reports a median 7.0x acquisition multiple on a $14.4M median purchase price — implying roughly $2M of EBITDA at the median. Independent sponsor equity is structured deal-by-deal with no pre-search commitment: sponsor receives 20-30% promote post-pref (8% standard), often with tiered breakpoints at 2x and 3x MOIC, plus management/transaction fees. Citrin Cooperman 2025 Independent Sponsor Report (172 respondents) notes 54% of IS deals close at 4x-6x EBITDA — meaningfully below traditional middle-market PE at 10.2x-14.9x. Dual-strategy firms like Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners write minority co-investment checks alongside the operator's primary capital source — they expect you to bring a lead investor (search fund firm or IS family office) and join as 15%-25% of the equity stack. For a single-family office allocating $5M-$15M to a first search or IS deal, the dual-strategy structure is the simplest entry point: you take a co-investment slot rather than running underwriting yourself. Peony at $30 per admin per month includes NDA-gated links so each capital partner signs before customer lists, vendor agreements, or specific target identity is visible.

I am sharing my searcher CIM and target deal materials with 8-12 capital partners simultaneously — what does a data room need to handle dual-strategy fundraising?

A dual-strategy data room needs to support two simultaneous workflows: lead-investor diligence (search fund investor or IS family office running full diligence) and minority co-investor diligence (dual-strategy firms reviewing summary materials and deciding whether to participate at the lead's pricing). Standard requirements include separate NDA gates per investor so customer concentration data is hidden until each capital partner signs, page-level analytics so you know which capital partners spent 45 minutes on the working capital normalization versus 8 minutes on the cover memo, dynamic watermarks with viewer identity embedded in every rendered page so any forwarded document traces back to the source, screenshot protection that blocks and logs unauthorized capture attempts, and link expiry with instant access revocation if a conversation goes cold. Peony at $52 per admin per month for Data Room tier includes all six features plus AI auto-indexing that organizes uploaded files in under 3 minutes — versus emailing loose PDFs through Dropbox where anyone can forward links without your knowledge. For a self-funded searcher running parallel pitches to Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners, a single Peony room with separate NDA-gated access links per firm replaces 4 separate Dropbox folders and gives you 4 independent engagement signals in real time.

Why aren't Pacific Lake Partners and Search Fund Partners on the dual-strategy list — they are the largest dedicated search fund investors?

Pacific Lake Partners (Boston/Bay Area, founded 2009 by Coley Andrews and Jim Southern) and Search Fund Partners (Palo Alto, founded 2004 by Rich Kelley and David Carver) are the two largest dedicated search fund firms in the US — Pacific Lake closed Fund IV at $175 million in 2019 with 30+ portfolio companies, SFP has invested in 175+ searches and closed 100+ deals across 6 funds — but neither positions for independent sponsor deals as a stated thesis. Pacific Lake's mission is to back first-time MBA-track searchers under the original Stanford/HBS search fund model pioneered by Irv Grousbeck (Jim Southern was Grousbeck's first protégé in 1984). Search Fund Partners has a similar mandate. Their LP base, governance, and investment committee process is built around pre-search committed capital and traditional search fund economics — not deal-by-deal IS capital. The dual-strategy firms in this post all explicitly market both lanes, often with separate product lines or platforms (Miramar Equity Partners runs Miramar Search Partners as a sub-brand, Plexus Fund VII names both partner types in the press release, ETA Equity offers triple coverage). For a searcher considering only traditional search fund firms, Pacific Lake and SFP remain the canonical references. For a searcher who might convert to IS later, dual-strategy firms are the better continuity choice. Peony page-level analytics work the same whether you are pitching Pacific Lake on a search fund deck or pitching Smash.vc on a self-funded search target.

What does the Plexus Capital Fund VII close at $977M signal for searchers and independent sponsors in 2026?

Plexus Capital's October 2025 close on Structured Capital Fund VII at $977 million — ahead of a $750M target — alongside Equity Fund II to total $1.3 billion raised in just 5 months is the single largest dual-strategy fund close of 2025 and one of the strongest signals that LPs are now allocating dedicated capital to firms that bridge search funds and independent sponsors. Plexus's own press release explicitly names both partner types: the firm partners with independent sponsors, search funds, private equity groups, and management teams pursuing recapitalizations or growth investments. Plexus targets $2M-$12M EBITDA companies with $10M-$100M revenue and writes junior capital (subordinated debt with equity ownership) of $5M-$25M typical. For a searcher who has closed a first acquisition and is now considering a second deal as an independent sponsor — or for an IS sponsor whose target is too small for a traditional control-buyout PE fund but too large for a self-funded search — Plexus Fund VII is the canonical 2026 fit. The fund is fully deployable now. Combined with Cyprium Partners' SBIC I final close at $190M in February 2025 (14+ IS-partnered deals through August 2024) and Peninsula Capital Partners' Fund VIII at $400M in September 2025 (70+ IS platforms historically), the 2025 vintage of junior capital for sub-$15M EBITDA acquisition entrepreneurs is the largest in the cycle to date. Peony at $30 per admin per month gives you a single data room you can share with all three firms simultaneously through NDA-gated links and page-level analytics.

I am a former operator considering my first acquisition deal — how do I pick between a self-funded search, a traditional search fund, and an independent sponsor structure?

The choice between self-funded search, traditional search fund, and independent sponsor depends on three things: your personal capital available, your target EBITDA range, and your tolerance for outside capital governance. Self-funded search works best for mid-career operators with $50K-$500K personal capital, $500K-$2M EBITDA targets, willingness to sign personally on an SBA 7(a) loan up to $5M, and preference for control (you operate, you own 70-90%, minority investors own 10-30%). Traditional search fund works best for first-time MBAs with no operating capital, a 24-month search runway need, $2M-$5M EBITDA targets, and willingness to give a syndicate of search fund investors 70-80% of the equity in exchange for committed pre-search capital and structured promote (Stanford 2024 study median: 7.0x multiple on $14.4M purchase, 35.1% average IRR). Independent sponsor works best for experienced PE/operator backgrounds with proprietary deal access, $3M-$15M EBITDA targets, capacity to raise 100% deal-by-deal capital from family offices and mezz, and acceptance of 20-30% promote with management fees. Smash.vc, CapitalPad, ETA Equity, and Endurance Search Partners support all three structures so you can stay with the same investor group across structural transitions. Smash.vc explicitly raises EBITDA criteria from $750K (self-funded) to $2M (IS) within the same product. Peony AI document extraction lets you reuse the same data room across all three structures — pivot the deck, keep the diligence package, save 2-3 weeks of room rebuild time.

How does Peony Data Room compare to legacy data rooms for searchers and independent sponsors who run multiple deals per year?

Legacy data rooms like Datasite charge $50,000+ per deal, which is structurally broken pricing for a self-funded searcher running 1-2 deals per year on $1M-$2M EBITDA targets or for a multi-deal independent sponsor running 3-6 deals per year with rotating capital partner stacks. DocSend at $350 per user per month has no NDA workflow at all — you cannot gate sensitive customer concentration or vendor rebate data behind a click-through NDA before sharing. Dropbox shared folders give you zero tracking on which capital partner opened which file or for how long. Peony at $52 per admin per month for Data Room tier includes AI auto-indexing, AI document extraction, Smart Q&A, NDA-gated links, dynamic watermarks, page-level analytics, screenshot protection, and link expiry — a feature stack that Datasite charges $25K+ per deal to configure. A multi-deal IS or searcher running 3 deals a year pays roughly $624 annually on Peony Data Room versus $150,000+ on legacy platforms. For a searcher pitching Pacific Lake, SFP, Smash.vc, CapitalPad, ETA Equity, and Plexus simultaneously, Peony's page-level analytics tell you within 24 hours which 2-3 partners are genuine candidates worth follow-up calls.

Related Resources

Independent Sponsor Cluster (16 sibling posts):

- What Is an Independent Sponsor? Complete 2026 Guide — pillar hub

- The Independent Sponsor Capital Raising Playbook (8 stages)

- The Independent Sponsor Financial Model Template + Walkthrough

- SBIC for Independent Sponsors: 8 Active SBIC IS Partners

- Independent Sponsor Deal Book: 10 Sections + 3-Stage Release

- Independent Sponsor Data Room Checklist (42 docs, 3 stages)

- Independent Sponsor LOI Playbook (90-day timeline)

- Best Data Rooms for Independent Sponsors (8 tested)

- 18 IS Conferences and Forums in 2026

- Healthcare Capital Partners for Independent Sponsors

- Business Services Capital Partners for Independent Sponsors

- Manufacturing Capital Partners for Independent Sponsors

- Tech/Software Capital Partners for Independent Sponsors

- Consumer Capital Partners for Independent Sponsors

- Distribution/Logistics Capital Partners for Independent Sponsors

- Cleantech/Energy Capital Partners for Independent Sponsors

You might also like

May 14, 2026

Small Business Due Diligence (2026): SBA 10% Rule + 5-Axis Intensity Grid

Apr 26, 2026

SBIC for Independent Sponsors: 2026 Leverage Playbook

Apr 25, 2026

The Independent Sponsor Capital Raising Playbook (2026)