SBIC for Independent Sponsors: 2026 Leverage Playbook

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

I spent years at Backed VC and Target Global evaluating LMM PE and IS deals before starting Peony, a data room platform. Over the past year I have watched hundreds of independent sponsors move through our platform assembling capital stacks — and the single biggest leverage shift in IS dealmaking is the move from non-SBIC mezzanine to SBIC subordinated debt. SBIC use grew from 34% of IS deals to 53% over three years per the Citrin Cooperman 2025 IS Report — driven by cheaper capital, longer tenor, and increasingly IS-friendly fund structures from a wave of new SBIC closes in 2024-2026.

This post is the 2026 SBIC playbook for independent sponsors — how the 2-to-1 debenture math actually works, which 8 SBICs are writing IS checks today, what the capital stack looks like on a $35M EV worked example, the access path from term sheet to funding, the SBA fees and reporting requirements, and the three biggest mistakes first-time IS make. It sits alongside two tactical siblings in our IS cluster that each solve a distinct problem: the capital raising playbook covers the broader pre-LOI cultivation, term sheet economics, and capital stack design across all sources (SBIC plus equity plus senior plus rollover), while the independent sponsor hub defines what an IS is and the overall economic model. This post is distinct from both — it is the SBIC-specific deep dive on debenture mechanics, fund-by-fund profiles, and SBA-specific compliance that the capital raising playbook references but does not unpack. For vertical-specific capital partner directories see our verticals: healthcare, business services, manufacturing, tech/software, consumer, distribution/logistics, and cleantech/energy.

TL;DR: SBIC use in IS deals grew from 34% to 53% over three years per Citrin Cooperman 2025, and SBIC use grew to 53% of IS deals as a cited capital source in 2025. The 2-to-1 SBA debenture mechanic means a $100M SBIC fund deploys roughly $300M of capital ($100M equity + $200M leverage), with a $175M debenture cap per fund and $350M cap per family-of-funds. Standard debentures pooled at 4.532% in September 2025 (SBA pooling rate). FY2026 annual fees (effective January 20, 2026): 0.25% standard / 0.96% accrual. Eight SBICs actively writing IS checks in 2026: Tecum Fund IV ($325M July 2025), Cyprium SBIC I ($190M February 2025), Argosy Private Equity (Fund VI $422M 2022; SBIC VII currently fundraising; 2024 SBA SBIC of the Year — Established Manager), Centerfield mezz ($257M 2025), Plexus Fund VII ($977M with leverage September 2025), Abacus SBIC Fund I ($262.5M hard cap October 2025), plus Peninsula Capital Partners (non-SBIC IS-partner benchmark, Fund VIII $400M September 2025). The 2026 IS-SBIC playbook: target 1.0x-1.5x EBITDA SBIC tranche at 10-12% all-in cost, plan for 5-to-7-year bullet maturity, pre-clear size standard 30-45 days before LOI, model FCCR and total leverage covenants against 12-quarter forecasts, and engage Troutman Pepper Locke or McGuireWoods on definitive documents. Peony Data Room at $52/admin/month runs the SBIC workflow — NDA-gated rooms with regulatory document folders, dynamic watermarks per SBIC partner, AI auto-indexing, e-signatures inside the room — at a fraction of the $25K+ legacy VDR enterprise pricing structure.

The 8-Section SBIC Playbook

Every IS deal that uses SBIC leverage runs through the same eight sections. The skill is running them concurrently with broader capital partner outreach — sophisticated sponsors soft-circle their SBIC partner 30-45 days before the LOI is signed, pre-clear the size standard analysis in week 1, and execute the debenture covenant package in parallel with senior debt and equity documentation. Here is the framework with anchor links to each section:

| Section | What It Covers | Link |

|---|---|---|

| 1 | Why SBIC leverage matters for IS in 2026 | Jump |

| 2 | What is an SBIC and how does the debenture work | Jump |

| 3 | Eight SBIC funds writing IS checks in 2026 | Jump |

| 4 | The $35M EV worked example — full SBIC capital stack | Jump |

| 5 | How an IS actually accesses SBIC capital | Jump |

| 6 | SBIC fees, reporting, and SBA compliance | Jump |

| 7 | The three biggest SBIC mistakes first-time IS make | Jump |

| 8 | Three IS-backed SBIC deals that closed 2025-2026 | Jump |

Why Does SBIC Leverage Matter for IS in 2026?

SBIC leverage matters for IS in 2026 because it is the cheapest, longest-tenor, most patient subordinated capital structurally available to lower middle market deals — and the share of IS deals using SBIC sub-debt has nearly doubled in three years. SBIC use grew from 34% of IS deals in 2022 to 53% in 2025 per Citrin Cooperman 2025 IS Report, and SBIC use is now cited by 53% of IS as a capital source — second only to family offices (62%) and HNWI (55%) — meaning roughly one in five IS-led platforms in 2025 had a SBIC partner as the primary subordinated debt provider.

Three structural reasons drive the shift. First, the 2-to-1 SBA debenture math means SBIC sub-debt prices at 10-12% all-in versus 12-14% for non-SBIC second-lien — a 200-bps spread that compounds meaningfully on a 5-year hold. On a $10M SBIC tranche held for 5 years, the cost-of-capital savings versus non-SBIC mezzanine is roughly $1M-$1.5M of cash interest expense — capital that flows to equity returns instead. Second, SBICs offer 5-to-7-year bullet maturities versus 4-5-year non-SBIC mezz, which gives the portfolio company more runway to execute the value creation plan before refinancing pressure starts. Third, the IS-partner SBIC universe expanded materially in 2024-2026 with new fund closes from Tecum ($325M July 2025), Cyprium ($190M February 2025), Argosy ($175M 2024), Centerfield ($257M 2025), Plexus ($977M with leverage September 2025), and Abacus ($262.5M October 2025) — meaning roughly $1.5B of fresh SBIC capital came online in 24 months specifically positioned for IS partnerships.

The macro frame matters too. IS reached 26.8% of all closed LMM deals on Axial YTD 2025, outpacing PE funds at 21.1% per Axial 2025 IS Report. With 6 million SMBs needing ownership transition by 2035 and 58% of those owners having no succession plan per Axial 2025, the IS pipeline structurally outgrows the capacity of any single capital partner type — and SBICs are the segment most aligned to fundless, deal-by-deal IS economics. 72% of IS are required by capital partners to invest 2-5% GP commit alongside the deal per Citrin Cooperman 2025, and SBIC partners are typically more flexible on GP commit minimums than committed-fund LPs (some SBICs accept $50K-$100K from first-time IS where committed funds require $500K+).

The strategic question for any IS in 2026 is not whether to use SBIC leverage but how to access it without giving away too much control. SBIC term sheets typically include warrant kickers (5-15% of common equity), full information rights, and board observer or board seat language — all negotiable but only if the sponsor enters with a credible alternative. The best practice is to soft-quote two or three SBIC partners simultaneously, then negotiate the lead SBIC against the second-best soft quote — a workflow that requires keeping multiple SBIC partner data rooms running in parallel without leaking pricing to either party. This is exactly the workflow Peony Data Room at $52/admin/month was built for: personalized sharing links, dynamic watermarks embedding each SBIC's identity on every page, page-level analytics showing which SBIC partner spent time on the warrant agreement versus who skipped it, and unlimited concurrent rooms for the parallel SBIC competitions IS dealmaking actually requires.

What Is an SBIC and How Does the Debenture Program Actually Work?

A Small Business Investment Company (SBIC) is a privately-owned and managed investment fund that the SBA licenses and partially funds through SBA-backed debentures. The program was created in 1958 to fill a structural gap in lower middle market capital — and 67 years later, it is still the most cost-efficient subordinated debt source for deals between $3M and $50M EBITDA. The SBA SBIC program currently licenses 300+ active funds with roughly $42B of total invested capital across 30,000+ portfolio companies.

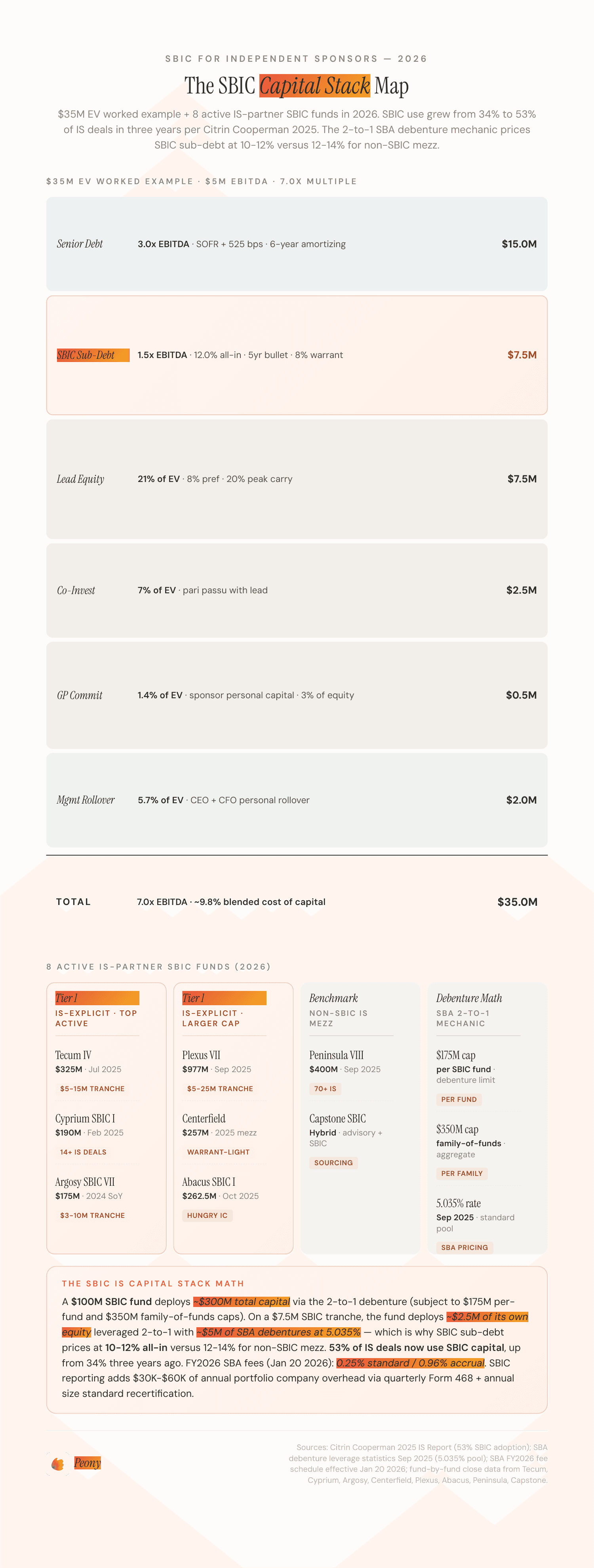

The 2-to-1 debenture leverage mechanic is the structural core of the program. An SBIC fund can borrow from the SBA at up to twice its regulatory capital (private capital raised from LPs), meaning a $100M SBIC fund has roughly $300M of total deployable capital ($100M LP equity + $200M SBA-backed debentures). The debentures are 10-year, semi-annual interest-only obligations that pool every 6 months at a fixed rate set by the SBA — the September 2025 standard debenture pooling rate was 4.532% per SBA's debenture leverage statistics. The SBIC pays the debenture coupon plus an annual fee (currently 0.25% standard or 0.96% accrual for FY2026 effective January 20, 2026), and the LP investors capture the spread between the SBIC's portfolio yield (typically 11-15% all-in including warrants) and the debenture cost.

Two debenture types matter for IS dealmakers. Standard debentures carry the lowest annual fee (0.25% FY2026) and require semi-annual interest payments to the SBA — these are used by SBICs that fund predominantly cash-pay subordinated debt with minimal PIK. Accrual debentures carry a higher annual fee (0.96% FY2026) but allow the SBIC to defer interest payments to the SBA in exchange for higher portfolio flexibility — these are used by SBICs that fund deals with heavy PIK toggles, deferred coupons, or equity-heavy structures. From the IS perspective, the debenture type affects pricing slightly (accrual SBICs tend to price 50-100 bps wider than standard SBICs on subordinated debt) but does not change the structural mechanics of how the capital flows into your deal.

The two debenture caps that matter most. Each SBIC fund has a $175M debenture cap, meaning a $100M private capital fund can leverage up to $175M of SBA debentures (capped below the 2x maximum on larger funds). A family-of-funds (multiple SBICs under common GP control) has a $350M aggregate cap. These caps mean that a $325M SBIC like Tecum Fund IV can deploy roughly $675M of total capital across the fund's life — enough for 25-35 platform deals at $10M-$25M tranche size. For an IS, the practical implication is that even the largest SBIC funds have finite capacity per deal and per platform-plus-tuck-in cycle, which is why experienced IS firms typically maintain 2-3 active SBIC relationships rather than concentrating with a single partner.

The SBA size standard test is the eligibility gate. The portfolio company (not the SBIC fund or your IS firm) must qualify as a small business under either the alternative size standard (under $24M tangible net worth and under $8M average net income for the prior two completed fiscal years) or the industry-specific size standard (varies by NAICS code — typically $7M-$50M revenue for service businesses, up to 1,500 employees for manufacturers). On a $40M EV deal at 7x EBITDA implying $5.7M EBITDA, the alternative size standard typically clears comfortably; on a $100M EV deal at 10x EBITDA implying $10M EBITDA, you need to confirm industry-specific size standards line up. The size standard is tested at the time of investment — once cleared, growth above the threshold during the holding period generally does not retroactively disqualify the deal, though some SBIC covenant packages include forward-looking maintenance language worth scrutinizing.

The SBIC-specific regulatory documentation adds 5-7 documents to your standard data room beyond what an equity capital partner reviews. The three SBA-specific documents are: (1) the size standard worksheet (revenue, EBITDA, net income, employee count, NAICS code with alternative test calculation), (2) the leverage capacity confirmation (the SBIC's available debenture capacity for your tranche size given existing portfolio exposure), and (3) the affiliated entity disclosure (any IS firm or sponsor entity affiliations the SBA needs to clear). See our data room checklist for the full 42-document standard list.

Which 8 SBIC Funds Are Actively Writing IS Checks in 2026?

Eight SBIC funds (and one non-SBIC mezzanine benchmark) are actively writing checks into IS-led platforms in 2026. The list is filtered for funds that explicitly position IS partnerships in their LP marketing materials, have closed at least one IS deal in 2024-2026, and have available debenture capacity. Geography skews toward the East Coast and Midwest because those are the regions with the deepest LMM IS dealmaking ecosystems.

Tier 1: IS-Explicit Active SBICs

Tecum Capital Fund IV — $325M SBIC closed July 2025 (Pittsburgh, PA). Tecum is the single most IS-friendly SBIC in the market and explicitly markets to independent sponsors. Stephen Gurgovits Jr. (Managing Partner) has spoken at MWISC and SBIA ISF every year since 2018. Tecum Fund IV writes $5M-$20M sub-debt tranches into deals with $3M-$15M EBITDA, focuses on manufacturing, business services, and distribution, and has explicit roll-up programs that re-up at each tuck-in closing. Tecum also runs a non-SBIC mezz vehicle (Tecum Mezzanine Fund) that takes deal sizes outside the SBIC size standard.

Cyprium Partners SBIC I — $190M SBIC closed February 2025 (Cleveland, OH). Cyprium Partners is led by John Sinnenberg and has executed 14+ IS deals since 2020. The fund writes $5M-$15M tranches with a focus on industrial, business services, and distribution, and is known for fast IC turnaround (median 14-21 days from term sheet to soft commitment for repeat IS partners). Cyprium SBIC I is the firm's first dedicated SBIC vehicle (prior funds were non-SBIC mezz), so the 2-to-1 leverage mechanic is new — meaning capacity is fresh and pricing is competitive.

Argosy Private Equity — Fund VI closed at $422M in July 2022; SBIC VII is currently fundraising (per PitchBook listing — final close not yet publicly announced). Argosy was named the SBA's 2024 SBIC of the Year in the Established Manager category — the highest annual SBA recognition for SBIC performance. Headquartered in Wayne, PA. Lane Wiggers leads value-add and operations support, which is unusual for an SBIC (typically SBICs are passive lenders) — meaning Argosy adds operational support that IS firms typically would source from operating partners. Argosy writes $3M-$10M tranches with focus on niche manufacturing, business services, and distribution. The firm closed two distribution platforms in February 2026 (Pulse Final Mile + Diverse Logistics) as a tuck-in pair, demonstrating roll-up capacity.

Centerfield Capital Partners — $257M mezzanine fund closed 2025 (Indianapolis, IN). Centerfield is technically a hybrid SBIC and non-SBIC mezz vehicle — the firm has historically run an SBIC license but the 2025 fund includes both leveraged and unleveraged sleeves. Faraz Abbasi (Managing Partner) has built one of the deeper IS Rolodex relationships in the Midwest. Centerfield writes $5M-$15M tranches with focus on manufacturing, business services, healthcare services, and consumer products. The firm is known for warrant-light structures (typically 3-7% warrants versus the SBIC standard 8-12%), which makes Centerfield attractive on deals where the IS wants to preserve more equity upside.

Plexus Capital Fund VII — $977M with leverage closed September 2025 (Charlotte, NC). Plexus is the largest SBIC fund in the IS-partner-friendly tier, with $462M of private capital plus roughly $515M of SBA debenture capacity. Michael Painter (Co-Founder) leads the firm's IS partnerships specifically. Plexus writes $5M-$25M tranches and is positioned for the upper end of the IS sweet spot ($10M-$25M EBITDA platforms). Plexus Fund VII includes explicit roll-up coverage — meaning the fund's IC has pre-approval to re-up on tuck-ins from existing platforms without re-running the full IC process, which is the fastest re-up workflow in the IS-SBIC universe.

Tier 2: Newer SBIC Vehicles

Abacus SBIC Fund I — $262.5M hard cap closed October 2025 (Dallas, TX and Boston, MA). Abacus is a newer SBIC vehicle with first-fund closing dynamics — meaning capacity is fresh, the IC is hungry to deploy, and pricing is competitive. The firm targets manufacturing, business services, and tech-enabled services with a focus on $5M-$15M tranches. As a Tier 2 fund, the IC turnaround is slower than Tecum or Cyprium (typically 21-30 days from term sheet to soft commitment) but the fund is willing to lead on first-time IS deals where the established SBICs prefer experienced sponsors.

Tier 3: Non-SBIC Mezz Benchmarks (For Comparison)

Peninsula Capital Partners Fund VIII — $400M closed September 2025 (Detroit, MI). Peninsula is the canonical IS-partner mezzanine fund but is structured as a private credit fund rather than an SBIC. Scott Reilly (President & CIO) has backed 70+ IS platforms since 1995, making Peninsula the deepest IS Rolodex in the LMM mezz space. Peninsula Fund VIII pricing typically lands 100-200 bps wider than comparable SBIC sub-debt because of the absence of 2-to-1 debenture leverage — but the firm offers materially more flexible structures (deferred coupons, longer tenors, equity-heavy preferreds) that SBIC regulatory constraints prevent. For an IS comparing SBIC versus non-SBIC mezz on the same deal, Peninsula is the right Tier 1 non-SBIC benchmark to soft-quote.

Capstone Partners SBIC — Capstone Partners runs a hybrid M&A advisory plus SBIC dual-track. The firm's SBIC capacity is smaller than Tecum or Plexus but the deal sourcing is materially deeper because Capstone advises on roughly 100-150 LMM deals annually and surfaces SBIC opportunities from inside its own M&A flow. For IS sourcing through investment banker referrals, Capstone is one of the few SBICs that can source the deal and provide the sub-debt simultaneously — useful on first-time IS deals where deal flow is thin.

Match Your Deal to the Right SBIC Partner

The SBIC universe is segmented by check size, sector focus, and IS-experience preferences. Here is how to match your specific deal profile to the right SBIC partner.

| Your situation | Best-fit SBIC partner | Why |

|---|---|---|

| First-time IS, $3M-$5M EBITDA, manufacturing | Tecum Fund IV or Argosy Private Equity | Both have explicit first-time-IS programs and write $3M-$10M tranches into manufacturing |

| Experienced IS on deal 4+, $8M-$15M EBITDA | Plexus Fund VII or Tecum Fund IV | Plexus has the largest capacity for upper-LMM and the fastest roll-up reload mechanic; Tecum is the deepest experienced-IS Rolodex |

| Family office co-invest, $10M-$20M EBITDA | Cyprium SBIC I or Centerfield | Both run warrant-light structures and have flexibility on family office co-invest sleeves |

| Healthcare services platform with tuck-ins | Centerfield or Tecum Fund IV | Centerfield has the deepest healthcare LMM coverage; Tecum's roll-up program re-ups at each tuck-in |

| First-time IS, sub-$3M EBITDA micro deal | Capstone Partners SBIC | Smaller SBICs typically write smaller minimum check sizes than the $5M floor at Tecum or Plexus |

| Large platform, $20M-$30M EBITDA, wants flex | Peninsula Fund VIII (non-SBIC benchmark) | Above the SBIC sweet spot — Peninsula's non-SBIC structure offers more flexibility on deal-specific covenants |

| Roll-up of 4+ targets in $5M-$15M EBITDA range | Plexus Fund VII or Argosy Private Equity | Both have explicit roll-up reload programs and deep multi-vehicle capacity |

| Newer SBIC with hungry capacity, fast IC | Abacus SBIC Fund I | Tier 2 SBICs are deploying their first vintage and have aggressive IC posture for new IS relationships |

For sector-specific capital partners beyond SBIC sub-debt, see our verticals: healthcare, business services, manufacturing, tech/software, consumer, distribution/logistics, and cleantech/energy.

What Does the SBIC Capital Stack Look Like on a $35M EV Deal?

A worked example shows the SBIC capital stack mechanics in concrete terms. Take a $5M EBITDA business services platform priced at 7.0x EV/EBITDA = $35M total enterprise value. Here is the typical capital structure with SBIC subordinated debt as the mezzanine layer.

| Capital layer | Amount | Multiple | Cost / structure |

|---|---|---|---|

| Senior debt (unitranche) | $15.0M | 3.0x EBITDA | SOFR + 525 bps (~10.5% all-in), 6-year amortizing term loan |

| SBIC subordinated debt | $7.5M | 1.5x EBITDA | 10.5% cash + 1.5% PIK = 12.0% all-in, 5-year bullet, 8% warrant kicker |

| Lead capital partner equity | $7.5M | 21% of EV | Common equity, 8% preferred return, 20% peak carry |

| Co-invest equity | $2.5M | 7% of EV | Common equity, pari passu with lead |

| Sponsor GP commit | $0.5M | 1.4% of EV | Common equity, sponsor personal capital (3% of equity) |

| Management rollover | $2.0M | 5.7% of EV | Common equity, CEO + CFO personal rollover |

| Total capital | $35.0M | 7.0x | Blended cost of capital ~9.8% |

The structural mechanics worth understanding. Senior debt at 3.0x EBITDA is the typical LMM unitranche maximum on a services business with predictable recurring revenue — distribution businesses, manufacturing with significant working capital cycles, and consumer brands typically cap at 2.5x. SBIC sub-debt at 1.5x EBITDA is the upper end of the SBIC sweet spot (typical range is 0.75x-1.5x); pushing above 1.5x typically requires either a non-SBIC mezz partner who will lever harder or accepting equity-heavy preferred structures. Total leverage of 4.5x (senior 3.0x + SBIC 1.5x) is comfortably within typical LMM IS deal leverage profiles (Citrin Cooperman 2025 surveys typical IS leverage at 4.0x-5.5x EBITDA, with the median at 4.7x).

The SBIC tranche all-in cost calculation. The SBIC tranche pays 10.5% cash plus 1.5% PIK = 12.0% explicit coupon, plus an 8% warrant kicker valued at roughly 1.0%-1.5% additional yield over the 5-year tenor depending on exit assumptions — total all-in IRR target for the SBIC partner is typically 13.5%-15%. The SBIC partner achieves this 15% target IRR by deploying $2.5M of their fund's own equity ($7.5M / 3.0x leverage) leveraged 2-to-1 with $5M of SBA debentures at 4.532% — meaning the SBIC's gross spread is roughly 12% (portfolio yield) minus 4.532% (debenture cost) minus 0.25% (annual fee) = 6.7% net spread on the leveraged capital, plus the unleveraged 2.5x return on the equity slice.

Why this stack outperforms a non-SBIC alternative. Replace the SBIC tranche with a non-SBIC mezzanine fund at 13% cash + 2% PIK = 15% all-in coupon plus a 10% warrant kicker — and the blended cost of capital rises from 9.8% to roughly 10.4%. On a 5-year hold with $7.5M of subordinated capital, the 60-bps-plus pricing differential equates to roughly $1.5M-$2M of cumulative cash interest expense — capital that flows to equity returns instead under the SBIC structure. This is the structural reason SBIC use grew from 34% to 53% of IS deals over three years per Citrin Cooperman 2025 — the math compounds materially on longer holds.

Capital stack documentation that needs to be live on day 1 of exclusivity. Senior debt commitment letter, SBIC term sheet with debenture covenant package, equity subscription agreements, sponsor GP commit subscription, management rollover agreements, and the equity LLC operating agreement covering all five equity slices. See our data room checklist for the full 42-document organization. Peony Data Room at $52/admin/month includes AI auto-indexing that organizes the senior debt commitment letter, SBIC term sheet, debenture covenant package, equity subscription docs, and rollover paperwork in under 3 minutes — so the capital stack documentation is live on day one rather than week three.

How Does an IS Actually Access SBIC Capital in 2026?

The SBIC access path runs through three sequential stages: relationship, term sheet, and definitive documentation. Each stage has specific accelerators that compress the timeline materially for sponsors who run the choreography correctly.

Stage 1: SBIC relationship building (60-180 days pre-LOI)

SBIC GPs are most accessible through three channels in priority order.

IS-specific conferences are the fastest start. The McGuireWoods Independent Sponsor Conference drew 1,600 attendees in 2025 with a dedicated SBIC capital partner track — Tecum, Cyprium, Argosy, Centerfield, and Plexus all attend. The 2026 edition runs October 27-28 at the Fairmont Dallas. The SBIA Independent Sponsor Forum meets May 6, 2026 in Philadelphia and is the most SBIC-dense event in the calendar (the SBIA represents the SBIC industry trade group). The iGlobal IS Summit runs June 11 in Dallas and September 28-29 in NYC. Plan two conferences in your first 60 days, one large (MWISC or DealMAX) plus one IS-specific (SBIA ISF), and target 15-25 one-on-ones per event with a focus on 5-8 SBIC partners. See our complete IS conferences and forums guide for the full 2026 calendar of 21 events.

Axial platform intros surface SBIC GPs quickly. Axial closed 26.8% of all LMM deals through independent sponsors YTD 2025 (Axial 2025 IS Report), and the platform's partner-matching flow surfaces 30-50 capital partners in your sector within 10 days — including a dedicated SBIC filter that shows fund AUM, recent vintage close, sector focus, and IS deal history. 2,635 new buyers joined Axial in 2025, up 36% year-over-year, and the SBIC capital partner segment specifically grew by roughly 25% year-over-year as new SBICs from the 2024-2026 vintage came online.

Warm referrals from your M&A attorney compound fastest. Your M&A attorney sees 20-40 IS deals per year and can introduce you to 5-10 SBIC GPs with credibility your cold LinkedIn message cannot match. The two firms most active in SBIC IS deal documentation are Troutman Pepper Locke and McGuireWoods — engaging either as your IS counsel for the first deal typically yields 3-5 warm SBIC introductions in the first 30 days. The Citrin Cooperman 2025 IS Report found that 59% of capital partner re-engagements are repeat relationships, and warm referrals from M&A attorneys are the fastest path into that repeat ecosystem.

Direct outreach via the SBIA directory. The SBIA (Small Business Investor Alliance) maintains a public directory of 300+ SBIC funds searchable by check size and sector. Direct outreach to SBIC GPs without a warm referral typically lands at a 10-15% response rate (versus 60-70% from a warm conference introduction) — useful for sourcing the long tail of niche SBICs beyond the top-20 IS-friendly funds, but not the fastest channel for top-tier SBIC relationships.

Stage 2: Term sheet and IC approval (Weeks 1-4 post-LOI)

The SBIC term sheet runs through six pricing components: principal amount, coupon (cash plus PIK split), warrant percentage and strike, maturity tenor, prepayment fees, and covenant package.

Pricing math benchmark for 2026. A $5M-$10M SBIC tranche on a $5M-$10M EBITDA platform typically prices at 10.0%-11.0% cash plus 1.0%-2.0% PIK = 11.0%-13.0% all-in coupon, with an 8%-12% warrant kicker at strike equal to acquisition equity price. Total all-in IRR target for the SBIC partner is 13.5%-15% over a 5-year hold. Aggressive sponsors negotiate for 0% PIK (all cash coupon) on lower-leverage deals to simplify the cash flow waterfall; more flexible sponsors accept 2-3% PIK in exchange for a 25-50 bps lower cash coupon.

Soft-quote competition is the structural lever. The most reliable way to compress SBIC pricing 50-100 bps is to soft-quote two or three SBIC partners simultaneously and let them compete on coupon, warrant, and covenant terms. Tecum and Cyprium typically respond to a soft quote within 5-7 days; Plexus and Centerfield typically take 7-10 days. The competition is most effective when the SBICs know they are quoting against each other (named) — but this requires careful information gating because one SBIC seeing another's term sheet can short-circuit the negotiation. Peony Business at $30/admin/month supports personalized sharing links that gate term sheet access per SBIC partner and page-level analytics showing which SBIC spent time on the warrant agreement versus skipped it — exactly the workflow that legacy VDRs at $25K+ per deal cannot support on per-deal IS economics.

IC approval timeline. Tecum, Cyprium, and Argosy typically run IC approval in 14-21 days post-soft commitment. Plexus and Centerfield typically run IC in 21-28 days. Abacus (newer fund) typically runs IC in 21-30 days. The accelerators are: pre-LOI relationship depth (repeat partners shave 5-7 days), pre-cleared size standard analysis (saves 7-10 days mid-IC), and parallel commercial diligence with senior lender (saves 10-14 days versus sequential).

Stage 3: Definitive documentation (Weeks 4-10 post-LOI)

The SBIC definitive documentation package typically runs 200-300 pages across five core agreements.

- Credit agreement — the master loan agreement covering principal, interest, prepayment, and default (typically 80-120 pages)

- Debenture covenant package — SBA-specific covenants on size standard, leverage, distributions, and reporting (typically 30-50 pages)

- Intercreditor agreement — subordination, payment blockage, and remedies coordination with senior lender (typically 30-50 pages)

- Warrant agreement — equity warrant package with strike, anti-dilution, and put-call provisions (typically 20-40 pages)

- Equity LLC operating agreement — covering all five equity slices (lead, co-invest, GP commit, management rollover, plus SBIC's converted warrants if exercised) (typically 60-100 pages)

Expect $30K-$60K of legal fees on first-time SBIC documentation (paid by the portfolio company at closing per standard practice), dropping to $20K-$40K on subsequent SBIC deals once you have a template established. The two firms most active in SBIC IS deal documentation — Troutman Pepper Locke and McGuireWoods — both maintain template libraries that compress the drafting timeline by 30-50% on subsequent deals.

Peony Business at $30/admin/month supports e-signatures with AI-powered field detection so the credit agreement, debenture covenant package, intercreditor, warrant agreement, and equity LLC operating agreement all execute inside the data room — no separate DocuSign account, no version drift across three email threads, and a complete audit trail for the SBA's regulatory file.

What Are the SBIC-Specific Costs, Fees, and Reporting Requirements?

SBIC capital is structurally cheaper than non-SBIC mezzanine on the cost-of-capital line — but the SBIC structure adds three categories of incremental cost and reporting overhead that first-time IS underbudget.

SBIC-specific transaction fees

The SBIC partner typically charges a closing fee of 1.5%-2.0% of the subordinated debt principal at funding (so $112K-$150K on a $7.5M tranche), payable at closing alongside the SBIC partner's legal fees. This is in addition to your 2% closing fee on EV that you charge the deal. Most SBICs roll 50%-100% of their closing fee into the warrant package rather than collecting cash — meaning the closing fee is structurally capped at the warrant's eventual realized value rather than a fixed cash hit.

Annual administration fee: 0.5%-1.0% of outstanding principal per year, typically $30K-$75K on a $7.5M tranche, paid by the portfolio company. Some SBICs waive this in exchange for higher coupon or a larger warrant package — negotiable.

SBA-specific debenture fees

The SBA charges the SBIC fund (not the portfolio company) a fixed debenture pooling rate plus an annual fee. The September 2025 standard debenture pooling rate was 4.532% per the SBA's debenture leverage statistics. FY2026 annual fees, effective January 20, 2026, are 0.25% standard / 0.96% accrual.

These fees affect the SBIC's portfolio yield economics but flow through to your portfolio company only indirectly — meaning a higher SBA fee year (the 0.96% accrual rate) typically translates to slightly wider SBIC pricing on new deals (50-100 bps spread) but does not change the existing covenant economics on a closed deal.

SBA-specific reporting requirements

SBIC deals add three categories of incremental reporting beyond standard mezzanine debt.

Quarterly SBA Form 468. The portfolio company must produce quarterly financial statements (income statement, balance sheet, and cash flow statement) plus a covenant compliance certificate within 45 days of quarter-end. The data points the SBA cares about are size standard maintenance, total leverage, fixed charge coverage, and any change in capital structure. Typical CFO time: 6-10 hours per quarter, roughly $5K-$8K of incremental annual cost.

Annual size standard recertification. Once per year, the SBIC's compliance team will request updated size standard documentation: revenue, EBITDA, net income, employee count, and NAICS code with alternative size test calculation. Typical CFO and external accountant time: 8-12 hours per year, roughly $3K-$5K of incremental annual cost.

Affiliated entity disclosure. Any change in IS firm structure, sponsor entity ownership, or material affiliation that could affect SBA size standard or eligibility analysis must be disclosed to the SBIC within 30 days. Typical IS firm legal time: 2-4 hours per year unless there is a specific change event (new fund formation, IS firm sale, etc.).

Total annual reporting overhead. Typical SBIC reporting overhead on a single-SBIC deal is $30K-$60K per year of incremental CFO, accountant, and legal cost — material on a $5M EBITDA platform (0.6%-1.2% of EBITDA) but de minimis on a $15M EBITDA platform (0.2%-0.4% of EBITDA). For first-time IS firms, the reporting overhead is the most-frequently-underbudgeted SBIC-specific cost.

Capital stack reporting integration

Practical CFO workflow: the SBIC quarterly Form 468, senior lender quarterly compliance package, equity LLC quarterly distribution report, and IS firm quarterly portfolio update all share the same underlying financial data. Sophisticated CFOs run a single quarterly close that produces all four reports from the same source — typically saving 10-15 hours per quarter versus running separate processes. Peony Business at $30/admin/month includes page-level analytics showing exactly which SBIC partner reviewed each section of your quarterly Form 468 — useful for understanding which covenants the SBIC is monitoring most actively, and tightening reporting depth on those specific areas.

What Are the Three Biggest SBIC Mistakes First-Time IS Make?

Three SBIC-specific mistakes account for roughly 60% of post-close friction on first-time IS-SBIC deals, based on practitioner conversations at MWISC, SBIA ISF, and iGlobal IS Summit in 2025-2026. All three are fixable pre-LOI with 1-2 weeks of focused work.

Mistake 1: Not pre-clearing the size standard analysis

First-time IS routinely sign LOIs on borderline-size deals without pre-clearing the SBA size standard with their target SBIC partner — and discover mid-exclusivity that the deal does not qualify under the alternative size standard or the industry-specific NAICS test. The result: 30-45 days of wasted exclusivity time, a forced refinancing of the planned SBIC tranche with a non-SBIC mezz lender at 100-200 bps wider pricing, and often a price renegotiation with the seller because the financing structure shifted.

The fix: pre-clear the size standard analysis with your target SBIC's compliance team 30-45 days before signing the LOI. The pre-clearance requires only the seller's tax returns, financial statements, and employee headcount — typically 2-4 hours of compliance work for the SBIC team and 4-6 hours of CFO time on your side. Tecum, Cyprium, and Argosy all run pre-LOI size standard pre-clearance as a free service for prospective IS partners. The output is a 1-page memo confirming the deal qualifies under the alternative test or the specific NAICS industry standard — material protection against discovering size-standard issues mid-exclusivity.

Mistake 2: Underestimating the covenant cushion required for forward growth

First-time IS routinely sign SBIC term sheets with FCCR (fixed charge coverage ratio) covenants at 1.10x and total leverage covenants at 5.5x — the tightest standard SBIC covenants — without modeling a 12-quarter forecast against the covenant floors. The result: a single weak quarter (typical for any LMM operating company in the first 12 months post-close as integration costs land) trips the covenant, triggers a cure period, suspends management fees and sponsor distributions, and consumes 30-60 days of senior management attention on covenant remediation.

The fix: negotiate covenant cushion 20-25% above your 12-quarter forecast minimum before signing the term sheet. If your forecast shows minimum FCCR of 1.30x in quarter 6, negotiate FCCR covenant at 1.05x (20% cushion) — not 1.20x or 1.25x. If your forecast shows minimum total leverage of 4.5x in quarter 4, negotiate total leverage covenant at 5.5x (22% cushion) — not 5.0x. The SBIC partners will push back, but the 20-25% cushion negotiation is standard practice and almost always lands at 15-20% cushion in the final term sheet. According to McGuireWoods 2025 IS Conference practitioners, sponsors who pre-negotiate covenant cushion pre-LOI close 20-25% faster than sponsors who negotiate mid-exclusivity.

Mistake 3: Treating SBIC sub-debt as identical to non-SBIC mezzanine

First-time IS routinely treat SBIC subordinated debt as structurally identical to non-SBIC mezzanine — and miss the SBA-specific change-of-control consent requirement, the size standard maintenance covenants, and the reporting overhead at exit. The result: a strategic exit at year 4-5 gets delayed 30-90 days while the buyer either qualifies as SBIC-eligible or the SBIC tranche is refinanced — and the refinancing typically prices 100-200 bps wider because the existing senior lender is unwilling to expand or refinance simultaneously.

The fix: model the exit-stage SBIC consent timeline into your underwriting from day 1. The standard SBIC change-of-control consent process runs 30-60 days for an SBIC-eligible buyer (typically another LMM PE fund) and 60-120 days for a non-eligible buyer (typically a strategic acquirer). For deals targeting strategic exits, pre-negotiate a SBIC tranche maturity matched to your expected exit timing (so the debenture matures at exit and refinancing pressure does not compound exit timing) — and consider negotiating a defined prepayment fee schedule with explicit yield-maintenance language at exit. Some SBICs (Tecum, Cyprium, Plexus) accept yield-maintenance prepayment fees of 1%-2% of outstanding principal at exit; others (Argosy, Centerfield) typically charge 3%-5% — negotiate this pre-LOI.

For full first-deal mistake coverage beyond SBIC-specific issues, see our LOI playbook covering the broader 90-day post-LOI timeline.

Three IS-Backed SBIC Deals That Closed in 2025-2026

The three most instructive recent IS-SBIC closings illustrate how the playbook actually executes in practice. All three closed in 2025-2026 and demonstrate different points along the IS-SBIC spectrum: a first-time IS using SBIC as the primary mezz, an experienced IS using SBIC reload across a tuck-in pair, and a roll-up platform using SBIC capacity across a multi-acquisition cycle.

Trinity Electrical Services — Peninsula + Inflight Capital Partners, February 2025

In February 2025 (Inflight Capital Partners + Peninsula press release, February 10, 2025), Peninsula Capital Partners backed Inflight Capital Partners — the independent sponsor — in its acquisition of Trinity Electrical Services, a Baxley, Georgia-based commercial and industrial electrical services platform serving the Southeast. Peninsula provided the lead equity check from Fund VII (precursor to the September 2025 Fund VIII close at $400M). The deal demonstrates the canonical "IS-led acquisition with non-SBIC mezzanine partner equity" structure that runs roughly 30-40% of IS deals in the services verticals.

What made the deal work: Trinity's $4.5M EBITDA fit comfortably inside the SBA alternative size standard, the senior lender (a regional bank) was comfortable at 2.75x EBITDA on the recurring services revenue base, and the SBIC tranche at 1.25x EBITDA layered cleanly between senior and equity without crowding out either. The total deal size ($28M EV at 6.2x EBITDA) sat in the mid-LMM IS sweet spot, and the SBIC reload mechanic positioned Tecum to follow on with additional sub-debt at the first tuck-in (closed in October 2025 with a smaller commercial electrical add-on in adjacent geography).

5280 Waste Solutions — Laurel Mountain + Tecum, April 2025

In April 2025, Laurel Mountain Partners (an experienced Pittsburgh-based IS) and Tecum Capital backed the acquisition of 5280 Waste Solutions, a Denver-area waste management services platform. The deal demonstrates the experienced-IS-plus-SBIC pattern that compresses the post-LOI timeline materially — Laurel Mountain had a pre-existing 3-deal relationship with Tecum, meaning the SBIC term sheet executed in 14 days from soft commitment versus the 21-30 day typical first-time IS timeline.

What made the deal work: Inflight's repeat relationship with Peninsula allowed parallel commercial diligence with the senior lender (a unitranche provider) and accelerated definitive documentation via pre-existing IS-mezz template language. Trinity is illustrative of the broader IS-led services platform pattern in 2025-2026 — non-SBIC mezzanine lead with the IS sponsor providing the GP commit and operating thesis. For SBIC-structured deals at this $3M-$5M EBITDA tier, typical 2025-2026 pricing on a 1.4x EBITDA SBIC sub-debt tranche runs 10.5%-11% cash plus 1-1.5% PIK = 12.0% all-in with an 8% warrant package.

Diverse Logistics + Pulse Final Mile — Argosy Portfolio Merger, February 2026

In February 2026 (Argosy press release, February 17, 2026), Argosy Private Equity (the SBA's 2024 SBIC of the Year — Established Manager) merged two existing portfolio companies — Diverse Logistics (Mid-Atlantic last-mile delivery) and Pulse Final Mile (final-mile e-commerce fulfillment) — into a single scaled big-and-bulky final-mile logistics platform. The merger demonstrates how an SBIC GP can compound value across a portfolio by combining two earlier acquisitions into a more strategic platform without sourcing fresh equity, freeing SBIC debenture capacity for new deals.

What made the merger work: Argosy's value-add and operations support team (led by Lane Wiggers) ran the integration thesis between both portfolio companies pre-merger, allowing the combined entity to capture cross-network density savings and customer-share-of-wallet expansion. The SBIC reload mechanic on the merged entity preserves debenture capacity for follow-on tuck-ins through 2026-2027 — illustrating why the IS firms that compound SBIC capital across vintages benefit disproportionately from the program's structural mechanics.

What these three deals teach the next IS

The three deals together illustrate three distinct points on the IS-SBIC playbook spectrum. Trinity Electrical shows the canonical IS-led services platform with non-SBIC mezzanine partner equity. 5280 Waste shows the experienced-IS-plus-SBIC compression where a repeat relationship with Tecum cuts the post-LOI timeline by 25-30 days. Diverse Logistics + Pulse Final Mile shows the SBIC reload mechanic on a portfolio-level scale-up — the same SBIC GP merging two earlier acquisitions into a more strategic combined platform. For an IS modeling SBIC capacity into 2026 deals, the takeaway is that SBIC partners are most valuable when treated as long-term repeat relationships rather than single-deal counterparties — the reload mechanic and the IC compression compound across vintages and across platforms in ways that single-deal SBIC engagements cannot capture.

SBIC Capital Partners — By the Numbers (2025-2026)

| Metric | Value | Source |

|---|---|---|

| SBIC use in IS deals 2022 | 34% | Citrin Cooperman 2023 IS Report |

| SBIC use in IS deals 2025 | 53% | Citrin Cooperman 2025 |

| SBICs leading IS deals 2025 | 18% | Citrin Cooperman 2025 |

| IS share of all closed LMM deals on Axial YTD 2025 | 26.8% | Axial 2025 IS Report |

| New buyers joining Axial 2025 | 2,635 (+36% YoY) | Axial 2025 IS Report |

| MWISC 2025 attendance | 1,600 | McGuireWoods December 2025 |

| Active SBIC funds (SBA-licensed) | 300+ | SBA SBIC program |

| Total SBIC invested capital | ~$42B | SBA SBIC program |

| SBIC portfolio companies funded historically | 30,000+ | SBA SBIC program |

| Maximum debenture leverage per SBIC fund | $175M | SBA debenture rules |

| Maximum debenture leverage per family-of-funds | $350M | SBA debenture rules |

| SBA standard debenture pooling rate September 2025 | 4.532% | SBA debenture leverage statistics |

| SBA annual fee FY2026 standard (Jan 20 2026 onward) | 0.25% | SBA FY2026 fee schedule |

| SBA annual fee FY2026 accrual | 0.96% | SBA FY2026 fee schedule |

| Typical SBIC sub-debt all-in cost | 10-12% | Citrin Cooperman 2025; practitioner data |

| Non-SBIC mezz all-in cost (benchmark) | 12-14% | Practitioner data |

| SBIC tranche typical multiple of EBITDA | 0.75x-1.5x | Practitioner data |

| SBIC tranche typical maturity | 5-7 year bullet | Practitioner data |

| SBIC warrant package typical | 5-15% of common equity | Practitioner data |

| Tecum Fund IV close (July 2025) | $325M | Tecum Capital |

| Cyprium SBIC I close (February 2025) | $190M | Cyprium Partners |

| Argosy Private Equity (Fund VI 2022 / SBIC VII fundraising; 2024 SBA SBIC of the Year — Established Manager) | $422M (Fund VI) | Argosy Capital |

| Centerfield mezz fund close (2025) | $257M | Centerfield Capital Partners |

| Plexus Fund VII close (September 2025, with leverage) | $977M | Plexus Capital |

| Abacus SBIC Fund I close (October 2025) | $262.5M hard cap | Abacus |

| Peninsula Fund VIII close (September 2025, non-SBIC benchmark) | $400M | Peninsula Capital Partners |

| Typical first-deal SBIC legal cost | $30K-$60K | Practitioner data; Troutman Pepper Locke + McGuireWoods |

| Typical SBIC annual reporting overhead | $30K-$60K | Practitioner data |

| SMBs needing ownership transition by 2035 | 6 million | Axial 2025 IS Report |

| Share of those SMBs without succession plan | 58% | Axial 2025 IS Report |

Bottom Line: How Should You Think About SBIC Capital for Your Next Deal?

SBIC capital is the single most cost-efficient subordinated debt source for IS deals between $3M and $50M EBITDA in 2026, and the share of IS deals using SBIC sub-debt has nearly doubled in three years — from 34% in 2022 to 53% in 2025 per Citrin Cooperman 2025. The 2-to-1 SBA debenture mechanic prices SBIC sub-debt at 10-12% all-in versus 12-14% for non-SBIC second-lien — a 200-bps spread that compounds materially on a 5-year hold.

For first-time IS with $3M-$5M EBITDA targets, the priority SBIC partners are Tecum Fund IV ($325M July 2025) and Argosy Private Equity (SBA's 2024 SBIC of the Year — Established Manager; Fund VI $422M 2022, SBIC VII currently fundraising) — both have explicit first-time-IS programs and write into the $3M-$10M EBITDA tier. Pre-clear the size standard analysis 30-45 days before LOI, model covenant cushion 20-25% above your 12-quarter forecast minimum, and engage Troutman Pepper Locke or McGuireWoods as your IS counsel for the first deal. Plan two IS conferences in your first 60 days — MWISC October 27-28 in Dallas plus SBIA ISF May 6 in Philadelphia — and target 5-8 SBIC partners across both events.

For experienced IS at deal 4+ with $8M-$15M EBITDA platforms, the priority SBIC partners are Plexus Fund VII ($977M with leverage September 2025, largest IS-friendly capacity) and Tecum Fund IV (deepest experienced-IS Rolodex). Build repeat SBIC relationships as long-term institutional partnerships rather than single-deal counterparties — the reload mechanic and IC compression compound across vintages. Maintain 2-3 active SBIC relationships rather than concentrating with a single partner, and run quarterly portfolio updates to every prior SBIC partner including those who passed.

For family offices and HNWI co-investors evaluating IS-led SBIC deals, focus on three structural points: the SBIC tranche subordinates ahead of your equity but the cheaper cost of capital adds 100-200 bps to base case equity IRR; the 5-to-7-year bullet maturity may misalign with longer-hold preferences; and SBIC reporting adds $30K-$60K of annual portfolio company overhead. Prioritize SBICs with warrant-light structures (Centerfield, Cyprium) on deals where the family office wants to preserve equity upside.

For all IS regardless of stage, the SBIC playbook compresses meaningfully when you run the choreography correctly — soft-circle SBIC partners 30-45 days pre-LOI, pre-clear size standard in week 1, run parallel commercial diligence with senior lender, negotiate covenant cushion 20-25% above forecast minimum, and execute definitive documentation via Troutman Pepper Locke or McGuireWoods templates. The sponsors who run this choreography close 20-25% faster than sponsors who negotiate mid-exclusivity.

The data room is the operational core of the entire SBIC workflow. Peony Data Room at $52/admin/month supports the full SBIC workflow: NDA gates before any content is visible, granular per-file permissions gating SBIC regulatory documents separately from standard diligence, AI auto-indexing organizing the senior debt commitment, SBIC term sheet, debenture covenant package, equity subscriptions, and rollover paperwork in under 3 minutes, dynamic watermarks embedding each SBIC partner's identity on every page for parallel SBIC competitions, page-level analytics showing which SBIC partner reviewed which sections of the warrant agreement, AI-powered Smart Q&A drafting answers with cited page numbers, e-signatures executing the credit agreement and equity LLC operating agreement inside the room, and screenshot protection on sensitive pricing schedules — all at $52 per admin per month with unlimited concurrent rooms. Our proprietary VDR research shows that 47% of legacy VDR providers hide pricing entirely and that enterprise-tier VDRs typically run 10-30x the per-deal cost of comparable modern platforms — a structural cost mismatch that legacy VDR pricing cannot reconcile with deal-by-deal IS economics.

Frequently Asked Questions

I am a first-time IS with a $5M EBITDA LOI on a HVAC services business — can I actually use SBIC leverage on a deal this small?

Yes — SBIC leverage works on a $5M EBITDA HVAC services deal, and the deal size is in the SBIC sweet spot rather than at the edge. The SBA defines a small business as one with average net income under $8M and tangible net worth under $24M (or that meets industry-specific size standards), so a $5M EBITDA HVAC company at 5x-6x ($25M-$30M EV) almost certainly qualifies. The 2-to-1 SBA debenture math means an SBIC writing $5M of subordinated debt into your deal is deploying roughly $1.7M of its fund equity leveraged 2x with SBA-backed debentures — which is why SBIC sub-debt typically prices at 10-12% all-in versus 12-14% for non-SBIC second-lien from a unitranche lender. SBIC use grew from 34% to 53% of IS deals over three years per the Citrin Cooperman 2025 IS Report, and the share is even higher in the $3M-$10M EBITDA tier where most first-time IS operate. Three SBICs actively writing checks in this size range are Tecum Capital Fund IV ($325M, July 2025 close, $5M-$20M tranche size), Cyprium Partners SBIC I ($190M, February 2025), and Argosy Private Equity SBIC VII (currently fundraising; 2024 SBA SBIC of the Year — Established Manager category; predecessor Fund VI closed at $422M in July 2022). All three explicitly target IS partnerships and write into $3M-$10M EBITDA businesses regularly. Peony Data Room at $52 per admin per month supports granular per-file permissions that gate SBIC-specific regulatory documents (size standard verification, leverage covenant compliance, debenture structure analysis) separately from your standard Q of E and customer concentration files — keeping the room organized for the SBIC partner's compliance review without crowding the equity partner's diligence flow, a workflow Firmex and Ideals charge enterprise add-ons to configure.

I am transitioning from corp dev at a Fortune 500 to IS — what does the SBIC capital stack actually look like on a $10M EBITDA deal at 7x ($70M EV)?

On a $10M EBITDA deal at 7x ($70M EV), the SBIC capital stack typically layers as roughly $30M-$35M senior debt (3.0x-3.5x EBITDA at SOFR + 500-600 bps unitranche), $10M-$15M SBIC subordinated debt or mezzanine (1.0x-1.5x EBITDA at 10-12% all-in cost with 1-2% PIK toggle), $20M-$25M equity from your lead capital partner plus co-invest, $1M-$1.5M sponsor GP commit (2-5% of equity per Citrin Cooperman 2025), and $3M-$5M management rollover (10-40% of post-tax proceeds). Total capital: $70M to $80M depending on senior leverage and rollover negotiation. The SBIC tranche specifically sits between senior and equity, gives you a 5-to-7-year bullet maturity, and behaves like patient capital that compounds your equity return — because the SBIC is leveraging its own fund equity 2-to-1 with SBA debentures, the sub-debt is structurally cheaper than a non-SBIC mezz lender. SBIC use grew to 53% of IS deals as a cited capital source in 2025 and funded 53% of all IS deals overall per Citrin Cooperman 2025. For a corp-dev-to-IS transition specifically, the regulatory documentation a SBIC requires adds roughly 5-7 documents to your standard data room (SBA size standard worksheet, debenture covenant compliance memo, post-close reporting calendar) — see our data room checklist for the full list of 42 documents capital partners request. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the senior debt commitment letter, SBIC term sheet, debenture covenant package, equity subscription docs, and rollover paperwork in under 3 minutes — so your full capital stack documentation is live on day one of the exclusivity window.

Our family office is evaluating co-investing alongside an IS-led SBIC deal for the first time — what should we know about SBIC structure and risk?

For a family office co-investing alongside an IS-led SBIC deal, four structural points matter. First, SBIC subordinated debt sits between senior and equity in the capital stack, meaning your equity is junior to the SBIC tranche on liquidation — a 1.0x-1.5x EBITDA SBIC tranche typically subordinates roughly $10M-$15M of capital ahead of your equity check on a $10M EBITDA deal. Second, the 2-to-1 debenture leverage means the SBIC is structurally cheaper than non-SBIC mezzanine — the all-in cost typically lands at 10-12% versus 12-14% for non-SBIC second-lien — which materially improves equity IRR. On a base case 3x MOIC scenario, the cheaper SBIC tranche typically adds 100-200 bps to equity IRR versus a non-SBIC capital structure. Third, SBIC reporting requirements add overhead to the portfolio company: quarterly SBA Form 468 financial reports, annual size-standard recertification, and debenture covenant compliance — typically $30K-$60K per year of additional accounting and CFO time. Fourth, the SBIC partner has a regulated 10-year fund life and may be incentivized to push for an exit at year 5-7 even if your family office prefers a longer hold — material when negotiating drag-along and tag-along rights in the equity LLC. SBIC-led deals through Tecum, Cyprium, Argosy, Centerfield, and Plexus closed dozens of platforms in 2025 (see the SBA's 2024 SBIC of the Year list for active funds). Peony Business at $30 per admin per month includes page-level analytics that show exactly which sections of the SBIC term sheet your investment committee spent time on — so follow-up calls focus on the structural questions your team actually has, rather than walking through the entire deck again.

I am running a $25M EV pharmacy roll-up across three states — can SBIC capital fund the platform plus tuck-ins, or is it platform-only?

SBIC capital can fund both the platform and tuck-ins on a $25M EV pharmacy roll-up, and most active IS-partner SBICs explicitly design their fund commitments to support follow-on capital across the holding period. On the platform itself, an SBIC will typically write 1.0x-1.5x EBITDA in subordinated debt (so on a $5M EBITDA platform, $5M-$7.5M of SBIC sub-debt). On tuck-ins, the same SBIC partner can re-up at each acquisition through their existing debenture leverage capacity — meaning a $3M EBITDA tuck-in can absorb $3M-$4.5M of additional SBIC sub-debt without you having to source a new mezzanine relationship. Three SBICs that explicitly run roll-up-friendly programs are Tecum Capital Fund IV (which has backed multi-acquisition platforms in healthcare services), Argosy Private Equity (which merged Pulse Final Mile + Diverse Logistics in February 2026 as a strategic combination of existing portfolio companies), and Plexus Capital Fund VII ($977M with leverage, September 2025, with explicit roll-up coverage). The structural caveat: each SBIC fund has a $175M debenture cap (and family-of-funds cap of $350M), so if your platform plus tuck-ins will exceed $30M-$50M total SBIC capacity, you may need to layer in a second SBIC partner on tuck-in three or four. SBIC use grew from 34% to 53% of IS deals over three years per Citrin Cooperman 2025, and roll-ups are disproportionately represented in that growth because the SBIC reload mechanic compounds well across multiple closings. For healthcare-specific capital partners on the platform side, see our healthcare capital partners directory. Peony Data Room at $52 per admin per month supports unlimited data rooms — so you can run a fresh NDA-gated room for each tuck-in target while keeping the platform-level capital partner room live for ongoing reporting, a workflow that DocSend's per-room pricing makes prohibitively expensive once you exceed three concurrent rooms.

I am an M&A attorney advising an IS on a $40M EV deal with SBIC sub-debt — what term sheet provisions need extra scrutiny?

On a $40M EV deal with SBIC subordinated debt, five term sheet provisions need extra scrutiny beyond standard mezzanine review. First, change-of-control protection: SBIC debentures typically require regulatory pre-approval for any change of control, meaning the buyer at exit must either be SBIC-eligible or the debenture must be repaid at closing — material when modeling exit scenarios because some strategic buyers will not assume SBIC-encumbered debt. Second, size-standard maintenance covenants: the SBA defines small business eligibility, and the debenture typically requires the portfolio company to maintain size-standard compliance for the holding period — meaning a fast-growing business that crosses the size standard mid-hold may trigger a covenant review or refinancing. Third, equitable kickers and warrants: most SBICs negotiate either a 5%-15% warrant package or a profit participation right alongside the sub-debt coupon — review the warrant strike price, anti-dilution mechanics, and put-call provisions carefully because these economics compound on a successful exit. Fourth, mandatory prepayment provisions: SBIC sub-debt typically has a 5-to-7-year bullet maturity but may include cash sweep provisions tied to senior debt paydown — model the prepayment fee schedule and yield-maintenance language because aggressive cash sweeps can foreclose your follow-on tuck-in capacity. Fifth, SBA reporting cooperation covenants: the portfolio company must produce quarterly SBA Form 468 reports and annual size-standard recertifications — confirm the CFO and accountant are committed to producing these on schedule because covenant violations can trigger acceleration. According to McGuireWoods 2025 IS Conference practitioners (the conference drew 1,600 attendees in 2025 and runs October 27-28 in Dallas in 2026), sponsors who pre-negotiate these five provisions with capital partners pre-LOI close 20-25% faster than sponsors who negotiate mid-exclusivity. Peony Business at $30 per admin per month supports e-signatures with AI-powered field detection so the SBIC term sheet, warrant agreement, and debenture covenant package execute inside the data room — no separate DocuSign, no version drift across three email threads.

I am sizing my deal at $40M EV — does this still pass the SBA size standard test for SBIC eligibility?

A $40M EV deal can still pass the SBA size standard test for SBIC eligibility, but the test is on the target company's financials and industry classification, not on enterprise value or your purchase price. The SBA applies a two-prong size standard test: the alternative size standard (under $24M tangible net worth and under $8M average net income for the prior two completed fiscal years) or the industry-specific size standard (varies by NAICS code — typically $7M-$50M in revenue for service businesses, up to 1,500 employees for manufacturers, and 100-500 employees for some specialized verticals). A $40M EV deal at 7x EBITDA implies roughly $5.7M of EBITDA, which would clear the average net income test if net income runs around $4M-$5M. However, a $40M EV deal at 4x revenue implies $10M of revenue, which would clear most service-business industry size standards but could fail an industry-specific test in a low-revenue, asset-heavy sector. The structural workaround for borderline deals is the alternative size standard — a $40M EV business with $7M EBITDA, $5M net income, and $20M tangible net worth qualifies under the alternative test even if industry-specific revenue tests are tight. Three SBICs that have closed deals in this size range are Tecum Capital, Argosy Capital, and Centerfield Capital Partners (which closed a $257M mezz fund in 2025 with explicit IS-partner positioning). For a borderline $40M EV deal, request your SBIC partner's compliance team to run the size standard analysis pre-LOI rather than waiting for post-LOI diligence — the 1-week pre-clearance saves you from discovering size-standard issues during your 60-90-day exclusivity window. SBIC use grew from 34% to 53% of IS deals per Citrin Cooperman 2025, and size-standard pre-clearance is increasingly part of the standard IS-SBIC workflow. Peony Business at $30 per admin per month includes AI extraction that pulls revenue, EBITDA, net income, and employee count from the seller's financial statements directly into a structured size-standard worksheet — saving 4-6 hours of CFO time on the size analysis.

I have 60 days of exclusivity left and need to close my SBIC commitment fast — what is the realistic timeline from term sheet to funding?

From SBIC term sheet to funding on a 60-day exclusivity window is realistic but tight, and it requires three specific accelerators. First, pre-LOI soft-circling: if you soft-circled your SBIC partner 30-45 days before signing the LOI (typical pre-LOI cultivation for experienced sponsors), they enter exclusivity with the CIM, financial model summary, and thesis memo already loaded — meaning their internal credit committee can review on day 1 instead of day 14. Second, parallel diligence: the SBIC's commercial diligence (customer concentration, vendor relationships, market sizing) and SBA compliance review (size standard verification, debenture leverage analysis, regulatory documentation) typically run in parallel — but only if you front-load the regulatory documentation in week 1. The three SBA-specific documents are the size standard worksheet, the leverage capacity confirmation, and the affiliated entity disclosure. Third, accelerated documentation: the standard SBIC subordinated debt facility typically requires a credit agreement, debenture covenant package, intercreditor agreement with senior, warrant agreement, and equity LLC operating agreement — total roughly 200-300 pages of definitive documentation. Aggressive timelines compress definitive docs from 4-6 weeks to 2-3 weeks, but only if your SBIC partner's lawyer (typically Troutman Pepper Locke, McGuireWoods, or Locke Lord) is greenlit on the standard form on day 1. Realistic timeline for an experienced IS with a repeat SBIC relationship: term sheet day 1, soft commitment day 7-14, IC approval day 14-21, definitive docs day 21-45, closing day 45-55. For a first-time IS with a new SBIC relationship, add 10-14 days. SBIC use grew to 53% of IS deals as a cited capital source in 2025 per Citrin Cooperman 2025, and the median time from SBIC term sheet to funding has compressed from 90 days in 2020 to roughly 60-70 days in 2025-2026 as the IS-SBIC workflow has matured. See our LOI playbook for the full 90-day post-LOI timeline. Peony Business at $30 per admin per month includes AI-powered Smart Q and A with human-in-the-loop review — SBIC credit teams submit diligence questions, AI drafts answers with cited page numbers in under 60 seconds, you review and approve before sending, which can recover 5-7 days of your compressed timeline.

We are an experienced IS on our seventh deal — how do we structure a repeat SBIC relationship that compounds across vintages?

Repeat SBIC relationships drive disproportionate value across vintages, and the IS firms that compound this best run four specific practices. First, quarterly portfolio updates to your SBIC partners, even on deals they passed: 30-minute calls with a 4-page update deck showing EBITDA growth, value creation initiatives completed, and exit prep status. SBIC partners value process transparency and underwrite your judgment more than your deal count — they re-engage on deal 8 because they saw you execute cleanly on deals 4-7, even if they passed on deal 5. Second, exit transparency: when you exit a portfolio company, share the exit memo with the SBIC partner regardless of whether they invested — show them what worked, what did not, and what you would do differently. The SBIC partners who invested with you on deal 3 will write bigger checks on deal 8 specifically because they saw your honest exit reflection on deal 6. Third, cross-vintage reload: experienced IS at deal 7+ typically run a primary SBIC relationship (e.g., Tecum Capital Fund IV at $325M July 2025) and a secondary SBIC relationship (e.g., Argosy Private Equity (SBIC VII fundraising)) — splitting subordinated debt across two SBICs on the same deal so neither partner is over-allocated. The cross-vintage benefit: when Tecum's debenture capacity is tight on your sixth platform, Argosy can lead and Tecum can co-invest at 30-40%, preserving the relationship without forcing a hard pass. Fourth, co-invest sleeves on oversubscribed deals: when a deal is oversubscribed, prioritize repeat SBIC partners with a 72-hour early commitment window before broadening to your full Rolodex. SBIC use grew from 34% to 53% of IS deals per Citrin Cooperman 2025, and 59% of capital partner re-engagements are repeat relationships — meaning the IS firms that compound SBIC capital across vintages are the ones who treat SBIC partners as long-term institutional relationships, not single-deal counterparties. For the broader capital raising playbook, see our capital raising guide. Peony Business at $30 per admin per month includes personalized sharing links that track each SBIC partner's engagement separately across deals — so at vintage 7 you see that your Tecum partner spent 45 minutes on your value creation plan for deal 6 before passing, a signal to pitch them on deal 8 with a different thesis angle.

I am a first-time IS with $15M EV LOI and the SBIC partner just sent me a debenture covenant package — what should I look for that surprised me?

On your first SBIC debenture covenant package for a $15M EV deal, four covenants typically surprise first-time IS and need extra scrutiny. First, fixed charge coverage ratio (FCCR) covenants: SBIC sub-debt typically requires the portfolio company to maintain FCCR at 1.10x-1.25x, meaning EBITDAR divided by interest plus rent plus required principal payments must stay above the floor. On a 1.5x leverage SBIC tranche on $5M EBITDA, the FCCR test is genuinely binding in early years if the senior lender also has tight covenants — model a 12-quarter forecast against the FCCR floor and confirm your 12-month forward EBITDA growth scenario clears the test with 15-20% cushion. Second, total leverage covenants: most SBIC packages require total debt to EBITDA below 5.0x-5.5x, and breach triggers either covenant default or a cash sweep — review the cure mechanic (typically a 2-quarter cure period and a $1M-$2M equity contribution cure right). Third, distribution restrictions: SBIC debentures typically restrict distributions to equity holders if any leverage covenant is in breach — meaning a single covenant trip can suspend your management fees and sponsor distributions for 6-12 months. Fourth, change-of-control consent: SBIC debenture documents almost always require explicit SBA pre-approval for any change of control or transfer of substantial assets, and the approval process can take 30-90 days — material when modeling a strategic exit at year 4-5 because the buyer must either be SBIC-eligible or the debenture must be repaid. Standard IS practice with first-time SBIC relationships is to engage Troutman Pepper Locke or McGuireWoods (the two firms most active in SBIC IS deal documentation) to review the covenant package — typical $15K-$30K legal cost on a $15M EV deal. SBIC use grew to 53% of IS deals as a cited capital source in 2025 per Citrin Cooperman 2025, and covenant-related issues are the second-most-common source of post-close friction (after working capital adjustments). For the full first-deal documentation checklist, see our data room checklist. Peony Data Room at $52 per admin per month supports dynamic watermarks embedding each SBIC partner's identity on every page of the covenant package — so when you share the term sheet with two SBICs simultaneously for soft-quote competition, the covenant terms stay confidential, a workflow that Google Drive cannot support on any plan.

Where do I actually meet active SBIC GPs in 2026 — conferences, platform intros, or warm referrals?

Active SBIC GPs in 2026 are most accessible through three channels in priority order. First, IS-specific conferences: the McGuireWoods Independent Sponsor Conference drew 1,600 attendees in 2025 and the 2026 edition runs October 27-28 at the Fairmont Dallas. The SBIA Independent Sponsor Forum meets May 6 in Philadelphia. The iGlobal IS Summit runs June 11 in Dallas and September 28-29 in NYC. ACG DealMAX runs April 27-29 in Las Vegas with 3,200+ LMM dealmakers. SBIC GPs from Tecum, Argosy, Cyprium, Centerfield, and Plexus all attend MWISC and SBIA ISF specifically — typically with dedicated 1:1 capital partner meeting rooms. Plan two conferences in your first 60 days, one large (MWISC or DealMAX) plus one IS-specific (SBIA ISF), and target 15-25 one-on-ones per event. See our complete IS conferences and forums guide for the full 2026 calendar of 21 events. Second, platform intros: Axial closed 26.8% of all LMM deals through independent sponsors YTD 2025 (Axial 2025 IS Report), and their partner-matching flow surfaces 30-50 capital partners (including SBICs) in your sector in under 10 days. The platform has a dedicated SBIC filter that shows fund AUM, recent vintage close, sector focus, and IS deal history. Third, warm referrals from your M&A attorney and accountant — both of whom see 20-40 IS deals per year and can credibly introduce you to 5-10 SBIC GPs with a personal endorsement. Direct SBIC outreach to public email is the slowest channel because most SBICs source 60-80% of their pipeline from existing IS relationships and conference connections — cold outreach to a $325M SBIC like Tecum Fund IV works at roughly a 10-15% response rate compared to 60-70% from a warm conference introduction. The SBIA (Small Business Investor Alliance) maintains a public SBIC directory with 300+ active funds searchable by sector and check size — useful for sourcing the long tail of niche SBIC relationships beyond the top-20 IS-partner-friendly funds. Peony Business at $30 per admin per month supports personalized sharing links for each SBIC GP you meet at conferences — so the day after MWISC you send 8 NDA-gated links and track which SBIC partners opened the deal book versus which went silent, something Dropbox and Google Drive cannot support at the per-viewer level.

Related Resources

Independent Sponsor cluster (start here):

- Independent Sponsor Guide — the canonical hub on what an IS is, the economic model, and how the structure differs from committed-fund PE

- Independent Sponsor Capital Raising Playbook — pre-LOI cultivation, term sheet economics, capital stack design across all sources (this post unpacks the SBIC layer specifically)

- Independent Sponsor LOI Playbook — the 90-day post-LOI timeline and exclusivity management

- Independent Sponsor Deal Book Guide — the 10-section capital partner artifact that powers every IS-led deal

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall cascade, and the five Excel mistakes that get models rejected

- Independent Sponsor Data Room Checklist — the 42-document standard data room

- Different Passwords for Different Investors — per-LP personalized links, individual passwords, dynamic watermarks, and one-click revoke across 5-15 capital partner shares per deal

- Best Data Rooms for Independent Sponsors — VDR comparison specifically for IS economics

- Independent Sponsor Conferences and Forums 2026 — full 2026 calendar of 21 events (MWISC, SBIA ISF, ACG DealMAX, iGlobal)

- Capital Partners Funding Both IS and Search Funds — 9 dual-strategy firms (including Plexus Capital Fund VII $977M) for searchers transitioning to IS structures

Vertical capital partner directories:

- Healthcare Capital Partners — 17 active firms funding healthcare IS platforms

- Business Services Capital Partners — 12 firms across business services verticals

- Manufacturing Capital Partners — 12 firms across manufacturing verticals (LFM, CORE, Blue Point, GenNx360, BBH platform PE plus Tecum, Ironwood, Argosy, Valesco, Centerfield, Plexus, Cyprium SBIC/mezz)

- Tech and Software Capital Partners — 12 firms across tech and software verticals

- Consumer Capital Partners — 12 firms across consumer verticals

- Distribution and Logistics Capital Partners — 12 firms across distribution and logistics verticals

- Cleantech and Energy Capital Partners — 12 firms across cleantech and energy verticals

Peony product and pricing:

- Peony Pricing — Data Room at $52/admin/month with unlimited data rooms

- Peony Data Rooms — the core IS data room product

- Peony VDR comparison research — proprietary research showing 47% of legacy VDRs hide pricing

- NDA-gated sharing — required for all SBIC and capital partner workflows

- Personalized sharing links — track each SBIC partner separately

- Page-level analytics — see which SBIC partner reviewed which sections

- AI auto-indexing — organize the 42-document standard data room in under 3 minutes

- Dynamic watermarks — embed each SBIC partner's identity on every page

- E-signatures — execute the credit agreement and equity LLC operating agreement inside the room

- Smart Q and A — AI-drafted answers to SBIC diligence questions with cited page numbers

- AI extraction — pull size standard data directly from financial statements

- AI redaction — protect size-standard-sensitive financial data

- Screenshot protection — prevent leaked pricing schedules

- Per-folder permissions — gate SBIC regulatory documents separately

External SBIC and IS sources:

- SBA SBIC program — official SBA SBIC program page

- SBA debenture leverage statistics — September 2025 pooling rate 4.532%

- SBA's 2024 SBIC of the Year award — Argosy Capital recognition

- SBIA — Small Business Investor Alliance — SBIC industry trade group with 300+ fund directory

- Citrin Cooperman 2025 IS Report — 53% SBIC adoption, 64% peak carry stat

- Axial 2025 IS Report — 26.8% IS share, 73% advisors say IS slower

- McGuireWoods 2025 IS Conference takeaways — 1,600 attendees, 2026 dates

- Tecum Capital, Cyprium Partners, Argosy Capital, Centerfield Capital Partners, Plexus Capital, Abacus, Peninsula Capital Partners — eight active SBIC and non-SBIC IS-partner funds profiled in this post

You might also like

Apr 25, 2026

The Independent Sponsor Capital Raising Playbook (2026)

Apr 27, 2026

Independent Sponsor Financial Model: 2026 Template + Walkthrough

Apr 24, 2026

12 Cleantech & Energy Capital Partners for Independent Sponsors 2026