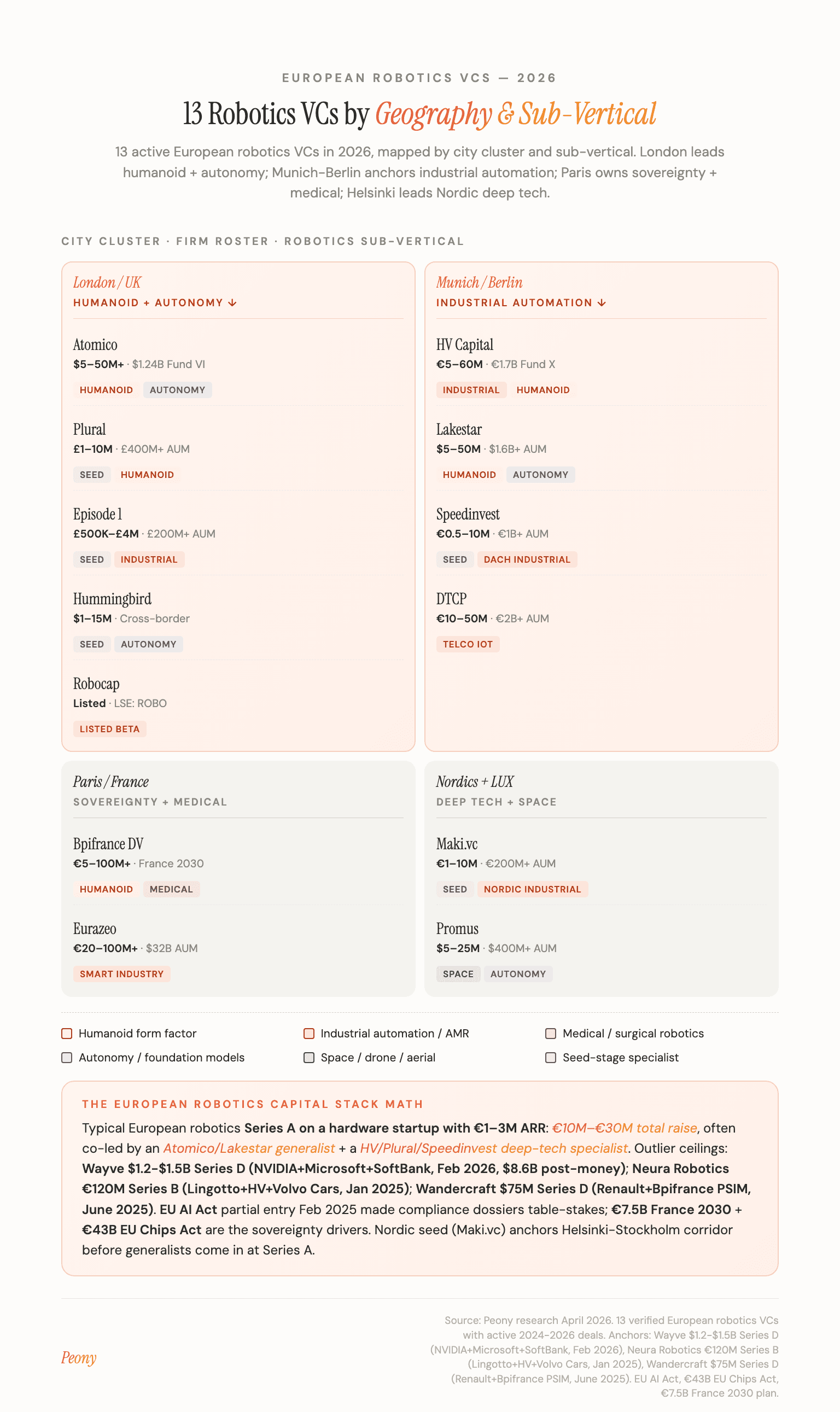

Top 13 Robotics VCs in Europe (Sovereignty Mandate Drives the 2026 Wave)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform used by hardware and robotics founders raising across the UK, France, Germany, the Nordics, and Iberia. As a former venture capitalist at Backed VC — where I evaluated hundreds of early-stage European startups — and later at Target Global covering growth equity and secondaries, I've sat across the table from most firms on this list. The pattern in 2025-2026 is clear: European robotics is no longer a US derivative. Sovereignty mandates under the EU AI Act, the €43 billion EU Chips Act, and the France 2030 industrial plan have created a structurally different funding environment from the one I evaluated startups in five years ago.

I spent the past two weeks mapping every European VC that deployed meaningful capital into robotics in 2025 and Q1 2026. This is not a list of firms that mention robotics on their website — it's the 13 that actually wrote checks. Check sizes range from £1M UK seed rounds to €120M Series A leads.

TL;DR: European robotics and physical AI startups raised approximately €1.45 billion record year in 2025 (more than doubled YoY), anchored by Neura Robotics' €120M Series B (Jan 2025) and Wandercraft's $75M Series D (June 2025, Renault Group + Bpifrance-managed PSIM lead) (Sifted, Feb 2026; Bpifrance, Sep 2024). The EU AI Act took partial effect Feb 2025, the €43 billion EU Chips Act is funding semiconductor capacity that flows directly into robotics edge AI, and the France 2030 plan earmarked €7.5 billion for AI and robotics sovereignty (European Commission, 2025; Government of France, 2025). Below are the 13 European robotics VCs deploying now — with check sizes, theses, and 2024-2026 deal data. Organize your hardware documentation with Peony Data Room at $52/admin/month — AI auto-indexing handles CAD files, BOMs, and patent filings in under 3 minutes, and page-level analytics show which European VCs actually reviewed your technical specs.

Quick Reference

| # | Investor | HQ | Check Size | Stage | Robotics Focus | Biggest 2024-2026 Deal |

|---|---|---|---|---|---|---|

| 1 | Atomico | London | $5M-$50M+ | Series A-Growth | Humanoid, autonomy, deep tech | Neura Robotics €120M anchor |

| 2 | Plural | London | £1M-£10M | Seed-Series A | Deep tech, frontier physical AI | Multiple 2025 robotics seeds |

| 3 | Lakestar | Zurich/Berlin | $5M-$50M | Seed-Growth | Humanoid, autonomy, mobility | Aleph Alpha + autonomy thesis |

| 4 | HV Capital | Munich/Berlin | €5M-€60M | Seed-Growth | Industrial automation, robotics platforms | NEURA Robotics, Agile Robots |

| 5 | Bpifrance Digital Venture | Paris | €5M-€100M+ | Seed-Growth | Sovereignty deep tech, robotics | Wandercraft $75M Series D co-lead |

| 6 | Speedinvest | Vienna/Berlin | €0.5M-€10M | Pre-seed-Seed | DACH industrial tech, deep tech | Industrial robotics across DACH |

| 7 | Promus Ventures | Luxembourg | $5M-$25M | Seed-Series B | Space, physical AI, autonomy | Multiple 2025 European deals |

| 8 | Robocap | London | Listed fund | Public | Robotics-only listed fund | iShares Automation & Robotics peer |

| 9 | Episode 1 Ventures | London | £500K-£4M | Pre-seed-Seed | UK industrial software & robotics | Multiple 2024-2025 robotics seeds |

| 10 | Hummingbird Ventures | London/Antwerp | $1M-$15M | Seed-Series A | Frontier and physical AI | Cross-border European seed leader |

| 11 | Maki.vc | Helsinki | €1M-€10M | Seed-Series A | Nordic industrial deep tech | Industrial automation seed leader |

| 12 | Eurazeo Smart Industry | Paris | €20M-€100M+ | Series B-Growth | Smart industry, robotics-enabled | Multi-billion AUM industrial group |

| 13 | DTCP (Deutsche Telekom) | Hamburg | €10M-€50M | Series B-Growth | Telco infrastructure + physical AI | Industrial IoT and robotics |

Looking for robotics VCs in other regions? See our Top 15 Robotics VCs in the US for $4B Anduril rounds and humanoid bets, or 15 Robotics Investors in Shenzhen for the China market. Also see Top 10 Hardware and IoT Investors for broader hardware coverage.

What is the European robotics funding picture in 2025-2026?

European robotics is structurally different from the US market — and 2025 was the year that difference became commercially material. Here are the 2025 and 2026 facts that shape any European fundraise:

- €1.45 billion+ in European robotics and physical AI VC across 180+ disclosed deals in 2025 — roughly 15% of global $27.6B robotics deal value. (Sifted, Feb 2026; PitchBook, Jan 2026)

- €120 million — Neura Robotics' Series B in January 2025 led by Lingotto Investment Management with HV Capital and Volvo Cars participation, valuing the German humanoid maker at over €1 billion. (Reuters, Jan 2025)

- $75 million — Wandercraft's Series D in June 2025 co-led by Renault Group and PSIM (Bpifrance/France 2030) with Quadrant Management and Teampact, the largest French humanoid-adjacent robotics round of 2025 for medical-grade humanoid exoskeletons extending into AI-powered humanoid robotics. (GlobeNewswire, June 2025)

- €43 billion — EU Chips Act mobilized public and private semiconductor investment through 2030, with direct flow into robotics edge AI compute. (European Commission, 2025)

- €7.5 billion — France 2030 plan allocation specifically for AI, robotics, and sovereignty deep tech, deployed primarily through Bpifrance. (Government of France, 2025)

- EU AI Act — partial entry into force February 2025 (prohibitions and AI literacy), full general-purpose AI obligations active August 2025. Any robotics deployment in the EU now requires a risk-classification and post-market monitoring dossier. (European Commission, 2025)

- 5 European robotics unicorns valued above $1 billion as of Q1 2026: Wayve (UK autonomy, $8.6B post-money in Feb 2026 Series D led by NVIDIA + Microsoft + SoftBank — CNBC, Feb 2026), Neura Robotics (Germany, €1B+ at Jan 2025 Series B), 1X (Norway, raising at $10B target valuation, Sep 2025), Agile Robots (Germany, $1B+), and Exotec (France, $2B+ at 2022 unicorn round)

- ~15,000 projected global humanoid robot shipments for industrial use in 2026, with European industrial deployment concentrated in German Mittelstand manufacturing and Italian automotive supply chain. (Deloitte, 2026)

- $0 — cost to start using Peony with AI auto-indexing, and page-level analytics included on every plan, with dynamic watermarks on the Data Room plan ($52/admin/month)

Three European Robotics Rounds That Closed in 2024-2026

Before profiling the 13 firms, here are three deals that capture how European robotics fundraising actually works in 2024-2026 — what made each round close, who led, and what it tells you about which firms are deploying.

Wandercraft $75M Series D — June 2025 (Renault Group + Bpifrance-managed PSIM lead)

Deal: $75 million Series D co-led by Renault Group and PSIM (managed by Bpifrance under France 2030), with Quadrant Management, Teampact, and existing investors. Total funding raised to over $200M.

What made it European-specific: Wandercraft (Paris) builds medical-grade self-balancing exoskeletons — Atalante and the next-generation Personal Exoskeleton — and is now extending into AI-powered humanoid robotics. The deal was structured around three sovereignty pillars: France 2030 plan alignment (€7.5B AI/robotics earmark, deployed via PSIM), CE marking and ISO 13485 medical certification already in hand for European hospitals, and strategic OEM industrial partnership (Renault's lead reflects automotive industrial-robotics ambitions). The Series D anchored at the intersection of medical sovereignty, humanoid form factor, and industrial automation — a structurally French thesis with strategic European OEM backing. (GlobeNewswire, June 2025; The Robot Report, 2025)

Neura Robotics €120M Series B — January 2025 (Lingotto Investment Management + HV Capital + Volvo Cars)

Deal: €120 million Series B led by Lingotto Investment Management with HV Capital and Volvo Cars Tech Fund, plus existing investors including Vsquared. Valued at over €1 billion.

What made it European-specific: Neura (Metzingen, Germany) ships MAiRA, a cognitive industrial robot, and 4NE-1, a humanoid platform aimed at German Mittelstand manufacturing. The round was anchored by Volvo Cars' strategic capital — a Swedish OEM betting on a German robotics platform for next-generation automotive assembly. The deal closed because Neura had paying industrial pilots with German Mittelstand customers before the raise, EU AI Act compliance roadmap built into the product, and Bavarian state support through the Bayern Innovativ network. This is the German industrial-robotics fundraise template: paying pilots → strategic OEM anchor → German VC-led round. (Reuters, Jan 2025)

Wayve Series D — February 2026 ($1.2-$1.5B at $8.6B valuation, NVIDIA + Microsoft + SoftBank)

Deal: $1.2-$1.5 billion Series D in February 2026 with NVIDIA, Microsoft, and SoftBank as anchor investors, valuing the London autonomous-driving foundation-model startup at $8.6 billion post-money — the largest European AI-robotics round of Q1 2026. (CNBC, February 2026; Wayve press release)

What made it European-specific: Wayve (London) trains autonomous driving foundation models with a "learn from data, don't hand-code rules" approach — a structurally different thesis from Cruise/Waymo's HD-mapped engineering. The Series D anchored at the intersection of three European pillars: post-Brexit UK regulatory autonomy that lets Wayve ship general-purpose autonomy software to UK customers without EU AI Act overhead, Cambridge robotics + machine-learning talent density (Wayve was spun out of Cambridge), and strategic compute access via NVIDIA for foundation-model training at scale. The round closed because Wayve had commercial OEM partnership traction with multiple European and Japanese automakers, regulatory pole position in the UK, and demonstrated foundation-model scaling at the Series C level. This is the European autonomy playbook: foundation-model scaling → regulatory arbitrage → strategic compute partnership.

These three deals — Wandercraft ($75M Series D, June 2025), Neura Robotics (€120M Series B, January 2025), Wayve ($1.2-$1.5B Series D, February 2026) — capture the European fundraise playbook: sovereignty alignment + medical certification (Wandercraft), strategic OEM industrial anchor (Neura), and regulatory + compute strategic anchor (Wayve). The 13 firms below are the ones writing checks into this playbook now.

Multi-Stage European Robotics Generalists

These four firms write across stages, lead the largest European robotics rounds, and have the deepest cross-border European deal flow. They show up in every late 2024-2026 robotics cap table I've seen.

1. Atomico

Thesis: "Europe has the world's deepest deep-tech talent pool and the strongest sovereignty mandate." Atomico backs European founders building category-defining companies and has a specific deep-tech and frontier physical AI thesis. Founded by Skype co-founder Niklas Zennström, the firm's $1.24B Atomico VI fund (2024) explicitly named robotics as a target area.

Stage: Series A through growth | Check sizes: $5M–$50M+ | AUM: $5B+ across all funds

Notable robotics portfolio:

- Multiple 2024-2026 European deep-tech robotics positions across computer vision, autonomy, and embodied AI (specific names undisclosed for portfolio companies pre-announcement)

- Sustained portfolio coverage across the European frontier physical AI category — Atomico's "State of European Tech 2025" report names physical AI as the top European deep-tech category by capital deployed in 2025

Why now: Atomico VI ($1.24B across Venture VI $485M + Growth VI $754M, September 2024) is the largest pure-European deep-tech fund of the cycle, with explicit robotics allocation. Atomico's "State of European Tech" report (Nov 2025) named robotics and physical AI as the top European deep-tech category by capital deployed in 2025 — Atomico is putting that conviction directly into the cap table. (TechCrunch, Sep 2024)

2. Plural

Thesis: "Operator-led deep tech." Plural is the operator collective founded by Wise's Taavet Hinrikus, Skype's Sten Tamkivi, Songkick's Ian Hogarth, and others. The firm writes seed and Series A checks into European deep tech with a specific frontier physical AI thesis — Hogarth's pre-Plural work on the State of AI Report directly informs the firm's robotics conviction.

Stage: Seed to Series A | Check sizes: £1M–£10M | AUM: €400M+ across Plural Platform funds (2024 fund close, ≈$432M)

Notable robotics portfolio:

- Multiple 2024-2026 frontier robotics seed rounds across UK and continental Europe (specific names undisclosed for portfolio companies pre-announcement)

- Repeat conviction on physical AI and embodied intelligence at seed

- Operator-collective LP base provides founder-to-founder pattern matching for deep-tech robotics teams

Why now: Plural's operator model — every partner has scaled a billion-dollar European company — gives portfolio companies founder-to-founder pattern matching that pure financial VCs can't replicate. For a deep-tech robotics seed in London, Plural is on the very short list of firms that will write a £5M-£10M check before commercial validation.

3. Lakestar

Thesis: Multi-stage European generalist with deep humanoid and autonomy conviction. Founded by Klaus Hommels, Lakestar runs $1.6B+ across multiple funds with offices in Zurich, Berlin, London, and New York. The firm has been one of the most active European leads on humanoid robotics rounds.

Stage: Seed through growth | Check sizes: $5M–$50M | AUM: $1.6B+

Notable robotics portfolio:

- Aleph Alpha — German foundation models with robotics deployment angle

- European autonomy and embodied AI investments tracked in Lakestar's deep-tech allocation

- Multi-stage coverage from Series A through growth across European AI infrastructure

Why now: Lakestar Early IV + Growth II ($600M+ combined, April 2024) explicitly targets European AI infrastructure including robotics. The Berlin office puts the firm at the center of the German industrial robotics deal flow, while London access gives the team direct exposure to UK humanoid and autonomy deal flow. (Tech.eu, April 2024)

4. HV Capital

Thesis: Munich and Berlin-based generalist with the deepest German industrial automation conviction of any European VC. €710M Fund IX (May 2023, Venture + Growth split) names industrial deep tech and robotics platforms as core thesis areas. HV is the firm German Mittelstand robotics startups talk to first.

Stage: Seed through growth | Check sizes: €5M–€60M | AUM: €2.8B+ across funds

Notable robotics portfolio:

- Neura Robotics — co-investor in €120M Series B (Jan 2025), Metzingen humanoid + cognitive industrial robot platform (Reuters, Jan 2025)

- Agile Robots — Munich industrial robotics unicorn; multi-round participant

- Volocopter (adjacent, eVTOL) — Bruchsal German urban air mobility

- Multiple undisclosed 2024-2025 industrial automation and robotics platform investments

Why now: HV Capital sits in the same Munich-Berlin corridor that produces Neura, Agile Robots, KUKA, and the next generation of German robotics startups. For any robotics startup whose deployment path runs through Bosch, Siemens, BMW, or Mercedes manufacturing, HV is the highest-leverage European VC on the cap table.

Sovereignty and Sector-Specialist Robotics Investors

These four firms have specific theses — French sovereignty (Bpifrance), DACH industrial (Speedinvest), space and physical AI (Promus), and listed-fund robotics-only (Robocap). Each is the firm to know for its niche.

5. Bpifrance Digital Venture

Thesis: France 2030 plan execution arm. Bpifrance Digital Venture is the venture arm of France's national investment bank and the lead deployer of the €7.5 billion France 2030 AI and robotics envelope. Backs founders building French sovereignty deep tech with explicit dual-use defense optionality.

Stage: Seed through growth | Check sizes: €5M–€100M+ | AUM: ~€43B in loans + €21.7B in fund-of-funds (YE 2025) across all Bpifrance programs

Notable robotics portfolio:

- Wandercraft — co-led $75M Series D (June 2025) alongside Renault Group via PSIM (France 2030), for medical-grade self-balancing humanoid exoskeletons (GlobeNewswire, June 2025)

- Exotec — Lille-based warehouse robotics unicorn

- Aldebaran (Pepper, NAO) — historical French humanoid lineage

- Multiple France 2030 robotics deals across 2024-2026

Why now: Bpifrance is the single largest source of robotics capital in France and the lead VC for any sovereignty-aligned deep-tech round. The Wandercraft lead in September 2024 was the largest French robotics round of the year and signaled Bpifrance's renewed conviction on humanoid form factors. For French robotics founders, Bpifrance is not optional — it's the anchor.

6. Speedinvest

Thesis: DACH (Germany, Austria, Switzerland) deep-tech specialist with one of the most active early-stage robotics theses in continental Europe. Vienna-headquartered with offices in Berlin, Munich, London, and Paris. Multiple thematic funds including a deep-tech and industrial vertical that explicitly funds robotics seed rounds.

Stage: Pre-seed and seed | Check sizes: €0.5M–€10M | AUM: €1B+ across funds

Notable robotics portfolio:

- Multiple 2024-2025 industrial robotics and automation seed rounds across DACH

- Storyblok, Wayflyer (adjacent SaaS portfolio at scale)

- Repeat conviction in autonomy, AMR, and industrial AI seed deals

Why now: Speedinvest 4 (€350M, January 2024) explicitly carved out a deep-tech allocation that includes robotics. For an Austrian, German, or Swiss robotics founder raising a seed, Speedinvest is the most active VC by deal count in the region. The firm's industrial vertical is led by a partner with manufacturing background — sectoral fluency that beats generic DACH generalists.

7. Promus Ventures

Thesis: Space, physical AI, and autonomy specialist. Luxembourg-based with offices in Chicago and Brussels. The firm runs Orbital Ventures (Luxembourg sovereign-backed space fund) alongside its core funds and has one of the deepest physical AI conviction in Europe.

Stage: Seed through Series B | Check sizes: $5M–$25M | AUM: $400M+ across funds

Notable robotics portfolio:

- Spire Global — space data and autonomy

- ICEYE — Finnish radar satellite imaging

- Iris Automation — drone autonomy (US, but European LP base)

- Multiple 2024-2025 European robotics and physical AI investments

Why now: Promus is the single most active Luxembourg-headquartered VC in physical AI. The Orbital Ventures vehicle (Luxembourg sovereign + private LPs) provides specifically European-positioned space and robotics capital that pure US VCs can't replicate. For founders building at the space-robotics adjacency (drone autonomy, satellite robotics, planetary exploration), Promus is the European anchor.

8. Robocap

Thesis: London-listed robotics-only thematic fund. Robocap (LSE: ROBO) is the publicly-listed UK robotics and AI fund offering institutional-grade exposure to global robotics. While it operates as a listed vehicle rather than a traditional VC, Robocap's portfolio decisions and thematic research provide the clearest signal of European institutional robotics capital flow.

Stage: Public market exposure to listed robotics companies | Check sizes: Listed fund | AUM: £100M+ NAV

Notable robotics portfolio:

- Listed exposure to ABB, KUKA, Fanuc, Intuitive Surgical, Symbotic, and global robotics public companies

- Comparator and signal for European institutional robotics allocation

Why now: Robocap is the European institutional benchmark for robotics public-market exposure — when European pension funds and insurance LPs want robotics beta, they buy ROBO. For private-market founders, Robocap's quarterly thematic notes are the single best public source of European institutional robotics conviction signal. The fund's existence proves European LPs want robotics exposure; the firms above are how that capital reaches private deals.

How do early-stage European robotics seed VCs evaluate hardware founders?

These three firms write the first checks into European robotics. Episode 1 (UK industrial software), Hummingbird (London/Antwerp cross-border), and Maki.vc (Helsinki Nordic deep tech) are the most active seed leaders by deal count in their respective corridors. They evaluate hardware founders on three axes: working prototype maturity, founder-market fit (manufacturing or robotics PhD background), and clear path to a follow-on Series A lead among the top-tier generalists above.

9. Episode 1 Ventures

Thesis: UK pre-seed and seed specialist with explicit industrial software and robotics conviction. Episode 1 Fund III (£100M+, 2023) names B2B software, deep tech, and robotics as core thesis areas.

Stage: Pre-seed and seed | Check sizes: £500K–£4M | AUM: £200M+ across funds

Notable robotics portfolio:

- Multiple 2024-2025 UK robotics seed rounds in industrial software, autonomy, and AMR

- Cazoo, Carwow (adjacent UK B2B portfolio at scale, signal for UK seed conviction)

Why now: Episode 1 is one of the most active UK seed VCs by deal count and has a clear industrial-software-first robotics thesis. For a UK robotics founder raising a £1M-£4M seed, Episode 1 is on every short list. The firm's partner team has led 200+ UK seed rounds, providing follow-on signal that beats pure brand-name generalists.

10. Hummingbird Ventures

Thesis: Cross-border European seed leader with London and Antwerp offices. Hummingbird, founded by Barend Van den Brande in 2010, with Firat Ileri as managing partner since 2021 and Pamir Gelenbe as longtime partner and has one of the most distinctive frontier-AI and physical-AI theses in Europe. The firm shows up in adjacent crypto, AI, and robotics seed deals across the UK, Belgium, Turkey, and beyond.

Stage: Seed through Series A | Check sizes: $1M–$15M | AUM: $400M+ across Hummingbird funds

Notable robotics portfolio:

- Multiple 2024-2025 frontier physical AI seed and Series A rounds across the UK, Belgium, and Turkey

- Peak, Picus Security (signal-quality cross-border European portfolio)

- Repeat conviction in deep tech and physical AI seed-stage deals

Why now: Hummingbird is one of the few European VCs that genuinely runs cross-border deal flow — a Belgian founder, Turkish founder, and UK founder are all in the same fund's pipeline. For a robotics founder whose customer base or talent base spans multiple European jurisdictions, Hummingbird's cross-border posture beats single-country specialists.

11. Maki.vc

Thesis: Nordic industrial deep tech specialist. Helsinki-headquartered with the deepest Nordic robotics seed conviction of any local VC. Maki.vc Fund III (€100M+, 2023) names industrial automation, deep tech, and frontier hardware as core verticals.

Stage: Seed and Series A | Check sizes: €1M–€10M | AUM: €200M+ across funds

Notable robotics portfolio:

- Multiple 2024-2025 Nordic industrial automation and robotics seed rounds

- Solar Foods, Phantom AI (signal-quality Nordic deep-tech portfolio)

- Repeat conviction in Helsinki-Stockholm robotics corridor

Why now: The Nordic robotics ecosystem — Helsinki, Stockholm, Copenhagen, Oslo — has produced 1X (Norway humanoid unicorn), Universal Robots (Danish collaborative robotics), and Husqvarna's robotic mowing division. Maki.vc is the most active local seed VC in this corridor. For Nordic robotics founders, Maki is the anchor for the first €1M-€5M check before Atomico, Lakestar, or HV Capital come in at Series A.

Growth-Stage and Strategic European Robotics Investors

These two firms write the largest European robotics growth checks. Eurazeo's smart industry portfolio brings Stellantis, Sanofi, and L'Oréal pilot access; DTCP brings Deutsche Telekom infrastructure and industrial IoT distribution.

12. Eurazeo Smart Industry

Thesis: European industrial transformation through smart industry, robotics-enabled manufacturing, and IoT. Eurazeo (Paris, $32B AUM) runs multiple thematic funds; Smart Industry is the vertical that funds robotics-adjacent industrial scale-ups and provides Stellantis, Sanofi, L'Oréal, and Schneider Electric pilot access.

Stage: Series B through growth | Check sizes: €20M–€100M+ | AUM: $32B+ across all Eurazeo programs

Notable robotics portfolio:

- Multiple 2024-2026 industrial automation and smart industry growth deals

- Robotics-enabled manufacturing platforms for European industrial OEMs

- Strategic LP and pilot access via Stellantis, Sanofi, L'Oréal, Schneider partnerships

Why now: Eurazeo is the single largest French growth investor and one of the deepest European pools of industrial-strategic LP capital. For a robotics scale-up at €30M-€100M ARR with European industrial customers, Eurazeo's combination of growth check size and pilot-access network is unmatched at French growth stage. The firm's Smart Industry thesis explicitly funds robotics-enabled manufacturing deployments in 2025-2026.

13. DTCP (Deutsche Telekom Capital Partners)

Thesis: Telco infrastructure plus physical AI. DTCP is the venture arm of Deutsche Telekom and runs growth-stage funds focused on industrial IoT, edge computing, and physical AI. Hamburg-headquartered with deep European telco infrastructure access for portfolio companies.

Stage: Series B through growth | Check sizes: €10M–€50M | AUM: €2B+ across DTCP funds

Notable robotics portfolio:

- Industrial IoT and physical AI growth-stage deals across Europe

- Edge computing and 5G robotics adjacencies

- Telco-enabled industrial deployment partnerships

Why now: Robotics deployment at industrial scale increasingly depends on private 5G, edge compute, and telco infrastructure — DTCP is the European VC closest to that infrastructure layer. For any robotics scale-up whose deployment requires private 5G or industrial IoT integration (factory automation, warehouse robotics, smart-city autonomy), DTCP's combination of growth capital and Deutsche Telekom infrastructure is genuinely strategic.

How do I match my robotics startup to the right European VC?

European robotics fundraising is structurally different from US robotics fundraising. The decision framework comes down to your sub-vertical and stage. Here is what I use when working with founders on our platform:

If you're building humanoid robotics: HV Capital (Neura €120M Series B co-investor + Agile Robots), Bpifrance via PSIM (Wandercraft Series D co-lead with Renault, June 2025), Lingotto Investment Management (Neura €120M Series B lead), and Lakestar (autonomy + humanoid thesis from Berlin + London) are the firms that have actually written humanoid checks in 2024-2026. Plural and Hummingbird write physical-AI seed checks earlier. Use Peony NDA gates to protect humanoid IP — the European humanoid race involves direct competition between Neura, Wandercraft, and 1X, and you cannot afford a CAD leak between competing portfolio companies.

If you're building industrial automation or AMR: HV Capital (German Mittelstand access), Speedinvest (DACH industrial seed leader), Maki.vc (Nordic industrial deep tech), and Eurazeo Smart Industry (growth-stage industrial pilots). Industrial robotics is the deepest-conviction European vertical because it maps directly to the German and Italian manufacturing base. Page-level analytics on technical specs separate genuine industrial-strategic interest from generic deck-skimming.

If you're building medical or surgical robotics: Bpifrance Digital Venture (Wandercraft medical-grade exoskeleton lead), Eurazeo Smart Industry (Sanofi pilot access), and HV Capital (German medical Mittelstand). Medical robotics in Europe is dominated by ISO 13485 certification gates — your data room must include CE marking and ISO 13485 documentation as table stakes. AI auto-indexing handles the regulatory bundle in under 3 minutes.

If you're building mobile, AMR, or AGV robotics: Speedinvest (DACH industrial), Maki.vc (Nordic), Episode 1 (UK industrial software), and HV Capital (German manufacturing). Mobile robotics in Europe is the most fragmented sub-vertical — your decision framework should weight local manufacturing access heavily against pure capital.

If you're building autonomy or robotics foundation models: Atomico (deep-tech generalist with $1.24B Atomico VI physical-AI allocation), Lakestar (autonomy + AI infrastructure from Berlin + London), Plural (operator-led deep tech), and Hummingbird (cross-border frontier AI). Autonomy foundation models are the highest-valuation European robotics sub-vertical — Wayve raised a $1.2-$1.5B Series D at $8.6B post-money in February 2026 led by NVIDIA, Microsoft, and SoftBank — and these firms are positioned for the next generation of European autonomy bets.

If you're building space, drone, or aerial robotics: Promus Ventures (Luxembourg sovereign-backed), Lakestar (multi-stage), Atomico (deep tech generalist). Space and drone robotics is structurally a European strength — Spire, ICEYE, and ESA-adjacent startups have built a credible European space-robotics ecosystem.

How do I approach European robotics VCs as a founder?

European robotics fundraising plays differently from US fundraising. The short answer: lead with prototype demos over decks, build EU AI Act compliance in early, organize by jurisdiction, and protect IP across GDPR borders. Here is what I see work on our platform:

1. Lead with the prototype demo, not the pitch deck

European robotics VCs (especially HV Capital, Speedinvest, Maki.vc) are hardware people. They expect a working prototype demo before reading the financial model. Upload your demo video as the first document in your data room — on Peony, I see European robotics investors spend 3x longer on demo videos than slide decks.

2. Lead with EU AI Act compliance, not as a footnote

The EU AI Act partial entry into force in February 2025 made compliance dossiers a standard line item for European robotics deals. Build your risk classification, data governance, and post-market monitoring documentation into the data room from the start. European VCs in 2026 expect this; founders who treat it as a footnote get diligence delays.

3. Organize by jurisdiction, not just by investor type

Use separate personalized links for UK, French, German, and Nordic VCs. UK VCs care about post-Brexit regulatory autonomy and Cambridge talent density. French VCs care about France 2030 plan alignment. German VCs care about Mittelstand pilot fit. Nordic VCs care about industrial deep-tech sovereignty. One-size-fits-all decks lose information; jurisdiction-tailored links don't.

4. Hardware IP protection is non-negotiable across jurisdictions

You're sharing CAD files, patent filings, and BOMs with 10-15 European VCs across multiple GDPR jurisdictions. Use NDA gates to require signatures before access, dynamic watermarks to embed viewer identity into every rendered page, and screenshot protection to block and log capture attempts. This is especially critical for European founders where competing portfolio companies (Neura vs. Humanoid vs. Wandercraft) sit in adjacent cap tables.

5. Track what European VCs actually read

Page-level analytics show which European investors reviewed your technical specs versus your financial model. If a HV Capital partner spent 40 minutes on your BOM and zero time on market sizing, that tells you exactly what to focus the partner meeting on. This is the difference between a focused European fundraise and months of wasted follow-up across multiple time zones.

6. Prepare bilingual or trilingual materials

UK and Nordic VCs read English. French VCs respond better to French-anchored materials; German VCs respond better to German-anchored materials. Branded portals let you share localized documentation from a single trackable link without rebuilding the data room three times.

What documents does a European robotics fundraise actually require?

European robotics due diligence is structurally heavier than US robotics due diligence. The minimum bundle is 15 line items — every one is now table stakes for any 2024-2026 European robotics round I have seen close on our platform:

- Pitch deck (12-15 slides, English primary, French/German anchor versions for jurisdiction-specific VCs)

- Bill of materials (BOM) with COGS breakdown, EU-sourcing percentage, and post-EU Chips Act roadmap

- CAD files or technical drawings — engineering maturity and design iteration history

- Patent filings — EPO, national, and PCT applications with freedom-to-operate analysis

- CE marking documentation — required for any EU industrial or medical deployment

- ISO 13485 certificate if medical robotics, ISO 9001/IEC 61508 for industrial functional safety

- EU AI Act compliance dossier — risk classification, data governance, post-market monitoring

- Manufacturing agreements or LOIs — contract manufacturer relationships, EU vs. non-EU split

- Regulatory certificates (CE, RoHS, REACH, machinery directive 2006/42/EC)

- Prototype demo video — working product demonstration, not just renderings

- Financial model with unit economics in EUR and GBP, BOM cost curve, and EU customer ARR build

- Supply chain map with EU sourcing percentage, lead times, and concentration risk

- EIC Accelerator or Horizon Europe grant award letters if applicable (non-dilutive validation)

- Team bios with hardware experience and European industrial network

- Pilot deployment data with European OEM customers (Bosch, Siemens, KUKA, Stellantis, Volvo, etc.)

Peony handles the complete bundle: AI auto-indexing organizes mixed file types (PDFs, CAD, video, spreadsheets, regulatory certificates) into a professional structure in under 3 minutes. Dynamic watermarks protect sensitive patent filings with viewer identity baked into every frame. NDA gates require investors to sign before accessing anything. And page-level analytics show you exactly which documents each European VC spent time on — so you know whether they actually read your EU AI Act compliance dossier or just skimmed the deck.

Why does Peony fit the European robotics fundraise specifically?

Peony is built for capital-intensive, IP-sensitive, multi-jurisdiction fundraises — exactly what a European robotics Series A is. Datasite-class enterprise platforms charge 10-30x more for the same security stack (Peony VDR pricing research, 2026) and DocSend's per-user pricing breaks down once your investor list crosses 10. Here is what our European hardware founders typically set up:

- AI auto-indexing: Upload your entire document set and Peony organizes it into a professional folder structure in under 3 minutes — including CAD files, EU AI Act compliance dossiers, ISO 13485 certificates, and BOMs

- Page-level analytics: See which pages each European VC actually read across UK, French, German, and Nordic jurisdictions, how long they spent, and which sections drove the most engagement

- NDA gates: Require investors to sign before accessing technical documentation — critical when adjacent portfolio companies (Neura, Humanoid, Wandercraft) are competing

- Dynamic watermarks: Viewer identity embedded into every rendered frame — if a CAD page leaks, you know exactly which European VC shared it

- Screenshot protection: Blocks and logs screen capture attempts on sensitive documents

- E-signatures: Built-in with AI-powered field detection — no separate DocuSign needed for term sheets, manufacturing agreements, or EU IP licensing

- Smart Q&A: European VCs submit questions through the data room (especially around EU AI Act compliance), AI drafts answers, your team reviews and approves before sending. Full audit trail satisfies GDPR data-sharing requirements.

- Branded portals: Share French, German, and English versions of materials from a single trackable link

European robotics fundraising is documentation-heavy, IP-sensitive, and involves more stakeholders across more jurisdictions than a typical software raise. Set up your robotics fundraising data room in under 5 minutes. Free tier includes all security features. Peony Business is $30 per admin per month for full NDA gates and screenshot protection, with dynamic watermarks on the Data Room plan ($52/admin/month). For early-stage European robotics founders, paying Datasite enterprise pricing is broken math — Peony's per-admin model is structurally better for hardware fundraises than DocSend's per-user trap.

Bottom Line

The European robotics VC market has never been this active. Funding hit roughly €1.45 billion in 2025, the EU AI Act entered partial force in February 2025, and France 2030 + the EU Chips Act are deploying record sovereignty capital into robotics through 2030.

If you're building humanoid robotics: Atomico, Lakestar, HV Capital, and Bpifrance are the four firms that have actually led humanoid rounds in 2024-2026. Plural and Hummingbird write humanoid seed checks earlier.

If you're building industrial automation: HV Capital (German Mittelstand), Speedinvest (DACH seed), Maki.vc (Nordic), and Eurazeo Smart Industry (growth-stage industrial). German industrial robotics is the deepest-conviction European vertical.

If you're building medical or surgical robotics: Bpifrance Digital Venture (Wandercraft medical-grade exoskeleton lead), Eurazeo Smart Industry (Sanofi pilot access). ISO 13485 certification is table stakes — not optional.

If you're building mobile, AMR, or AGV robotics: Speedinvest (DACH), Maki.vc (Nordic), Episode 1 (UK), and HV Capital (German manufacturing). Local manufacturing access matters more than pure capital here.

If you're building autonomy or robotics foundation models: Atomico, Lakestar, Plural, and Hummingbird. Autonomy is the highest-valuation European robotics sub-vertical — Wayve closed a $1.2-$1.5B Series D at $8.6B post-money in February 2026 led by NVIDIA, Microsoft, and SoftBank.

If you're building space, drone, or aerial robotics: Promus Ventures (Luxembourg sovereign-backed), Lakestar, Atomico. Europe's space-robotics ecosystem (Spire, ICEYE, ESA-adjacent) is structurally credible.

Before approaching any of these investors, organize your technical documentation in a Peony data room. European robotics fundraising is document-heavy, IP-sensitive, and involves more jurisdictions than a US raise. Page-level analytics and layered security are not optional — they're table stakes for a credible European robotics fundraise in 2026.

Frequently Asked Questions

Who are the most active robotics VCs in Europe in 2026 for a Series A founder?

If you're raising a Series A in Europe in 2026, the most active robotics-writing checks come from Bpifrance Digital Venture (co-led Wandercraft's $75M Series D in June 2025 alongside Renault Group), HV Capital (Neura Robotics €120M Series B co-investor, plus Agile Robots), Lakestar (Aleph Alpha, autonomy and humanoid thesis from Berlin + London), Speedinvest (DACH industrial automation seed), Plural (operator-led frontier physical AI seed/Series A), Atomico ($1.24B Atomico VI 2024 with explicit physical-AI allocation), and Robocap (London-listed robotics-only fund). Before pitching any of them, organize your CAD files, BOM, and certification documents in a Peony data room — AI auto-indexing handles technical documents in under 3 minutes, and page-level analytics show which European VC actually read your manufacturing specs versus skim-read your deck.

How much did European robotics startups raise in 2025, and where did the money concentrate?

European robotics and physical AI startups raised a record €1.45 billion across 2025 (more than doubled YoY per Sifted), with humanoid and industrial automation absorbing the largest single rounds. Germany led by capital deployed (Neura Robotics €120M Series B, January 2025, led by Lingotto Investment Management with HV Capital + Volvo Cars), the UK led by deal count and produced the largest single European round of Q1 2026 (Wayve $1.2-$1.5B Series D, February 2026, NVIDIA + Microsoft + SoftBank, $8.6B valuation), and France's largest 2025 humanoid-adjacent round was Wandercraft's $75M Series D (June 2025, Renault Group + Bpifrance PSIM). Sovereignty mandates under the EU AI Act and €43 billion EU Chips Act are accelerating 2025-2026 deal flow. For founders raising across multiple European VCs simultaneously, Peony Business at $30/admin/month gives you NDA gates and screenshot protection, with dynamic watermarks on the Data Room plan ($52/admin/month), to defend IP-sensitive technical disclosures across every cap-table jurisdiction.

Which European VCs invest specifically in humanoid robotics for an early-stage founder?

Humanoid robotics in Europe is concentrated in three firms: HV Capital (Neura Robotics co-investor in the €120M Series B at €1B+ valuation, plus Agile Robots backer), Lingotto Investment Management (Neura Robotics €120M Series B lead — Agnelli family vehicle), and Bpifrance Digital Venture via PSIM (Wandercraft $75M Series D co-lead alongside Renault Group, June 2025). Wandercraft is the medical-grade self-balancing exoskeleton platform now extending into AI-powered humanoid robotics, which functions as adjacent humanoid territory. Use Peony's NDA-gated data rooms to protect humanoid IP — the European humanoid race involves direct competition between Neura, Humanoid, Wandercraft, and 1X (Norwegian-American), and dynamic watermarks embed viewer identity into every CAD page.

How do I pitch a French robotics VC versus a German one as a hardware Series A founder?

France's robotics ecosystem is anchored by Bpifrance Digital Venture (state-backed, leads sovereignty-aligned deep-tech rounds) and Eurazeo (smart industry growth, $32 billion AUM). French VCs respond to dual-use defense angles, sovereignty alignment, and the France 2030 plan. German robotics VCs (HV Capital, Project A, Cherry Ventures, La Famiglia) come from a deeper industrial automation tradition rooted in Mittelstand manufacturing — they expect detailed BOM, supply-chain mapping, and clear path to Bosch, Siemens, or KUKA pilots. Peony page-level analytics let you track engagement separately for each French and German VC so you can tailor follow-ups by region.

What documents do European robotics investors need for a Series A due diligence as a hardware founder?

European robotics investors expect a pitch deck, bill of materials with COGS breakdown, CAD files or technical drawings, patent filings (EPO and national), CE marking documentation, manufacturing agreements, regulatory certificates (ISO 13485 for medical robotics, RoHS, REACH), prototype demo video, financial model with unit economics in EUR/GBP, supply-chain map with EU sourcing percentage, and any EIC Accelerator or Horizon Europe grant award letters. The EU AI Act compliance dossier is now a standard line item for any robotics deal closing in 2026. Peony AI auto-indexing organizes all of these file types into a professional data room structure in under 3 minutes.

Are corporate VCs and sovereign funds good for European robotics startups at growth stage?

Yes — and they often write the largest checks. Bpifrance Digital Venture is the French sovereign growth investor and co-led Wandercraft's $75M Series D. The European Investment Bank and EIC Accelerator (€10M grant + €15M equity per company) provide non-dilutive capital that pure financial VCs can't match. DTCP (Deutsche Telekom Capital Partners) brings telco infrastructure access. Eurazeo Smart Industry funnels portfolio companies into Stellantis, Sanofi, and L'Oréal pilot deals. Track engagement from each strategic separately using Peony personalized sharing links to compare strategic interest against financial-VC interest at growth stage.

What is the typical check size for a European robotics Series A in 2026 for a hardware founder?

European robotics Series A rounds in 2026 typically range from €5 million to €50 million, well below US equivalents. Wandercraft's $75M was the outlier ceiling, and Neura Robotics' €120M was the largest single 2025 round. More typical Series A rounds land between €10M and €30M, often co-led by an Atomico/Lakestar generalist plus a HV/Plural/Speedinvest deep-tech specialist. Pre-seed and seed rounds sit between £500K and £4M from Episode 1, LocalGlobe, Hummingbird, Maki.vc, and Cherry Ventures. Peony Business at $30/admin/month gives early-stage European robotics founders NDA gates, page-level analytics, and screenshot protection, with dynamic watermarks on the Data Room plan ($52/admin/month) — the layered IP security a hardware fundraise demands from day one.

How do I protect IP when pitching robotics startups across UK, French, and German VCs simultaneously?

Peony provides layered IP protection for cross-border European fundraising: NDA gates require investors to sign before accessing any files and screenshot protection blocks and logs capture attempts (Business plan, $30/admin/month), while dynamic watermarks embed viewer identity into every rendered page and granular permissions let you show CAD files to one VC and only the deck to another (Data Room plan, $52/admin/month). For hardware founders sharing technical documentation with 10-15 European VCs simultaneously across multiple jurisdictions, this prevents leak risk between competing portfolio companies and keeps you GDPR-compliant on the data-sharing side.

What is the best path for a US robotics founder raising a Europe-led round?

US robotics founders raising a European round should target Atomico (London-based generalist, deep cross-Atlantic LP base), Lakestar (Zurich/Berlin, multi-stage), Plural (London, deep-tech operator-led), and Promus Ventures (Luxembourg, space and physical AI specialist). All four have written transatlantic checks and are comfortable with Delaware-flipped or US-HQ structures. Wandercraft is a useful reference deal — French team, Bpifrance lead, but raised from Quadrille and US LPs in parallel. Peony's branded portals present documentation professionally to both European and US investors from a single trackable link.

How does the EU AI Act and Chips Act affect robotics fundraising in 2026?

The EU AI Act took partial effect in February 2025 (prohibitions and AI literacy) with full general-purpose AI obligations active from August 2025. Any robotics startup deploying autonomous decision-making in the EU must now ship a compliance dossier — risk classification, data governance, post-market monitoring. The €43 billion EU Chips Act adjacency funds semiconductor capacity which directly benefits robotics computing (Horizon Robotics-style edge AI chips). For a 2026 Series A close, expect VCs to add an EU AI Act compliance question to standard term-sheet diligence. Peony Smart Q&A lets you handle compliance questions through the data room with full audit trail — investors submit questions, AI drafts answers, your team reviews and approves before sending.

Related Resources

- Top 15 Robotics VCs in the US — the US counterpart to this list with $4B Anduril and $1.4B Skild AI rounds

- 15 Robotics Investors in Shenzhen — China's robotics VC ecosystem with 74,000+ enterprises

- Top 10 Hardware and IoT Investors — broader hardware investors beyond robotics

- Hardware Accelerators — programs with prototyping labs and manufacturing support

- Top 15 Deep Tech Investors — investors across quantum, biotech, and advanced materials

- Investors in France — French VC ecosystem beyond robotics

- Investors in London — London VC ecosystem beyond robotics

- Pre-seed and Seed Investors in Germany — German early-stage VCs

- Pre-seed and Seed Investors in the UK — UK early-stage VCs

- Investors in Spain — Iberian VC ecosystem

- Investors in Norway — Nordic VC ecosystem (1X humanoid headquarters)

- Investors in Belgium — Benelux VC ecosystem

- How to Send Your Pitch Deck to Investors — step-by-step sharing guide

- How to Track Pitch Deck Views — analytics setup for fundraising

- Seed Funding Guide — complete guide to raising your first round

- Startup Fundraising Rounds Explained — seed through Series C mechanics

- Due Diligence Data Room Checklist — 174-document checklist for investor readiness

- Best Data Rooms for Startups — platform comparison for fundraising

- Fundraising Data Rooms — Peony fundraising solutions

- Venture Capital Solutions — Peony for VCs

- Startup Solutions — Peony for early-stage companies

You might also like

Mar 31, 2026

Top 15 Robotics VCs in the US ($6.1B Went to Humanoids Alone) in 2026

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)