12 Distribution/Logistics Capital Partners for Independent Sponsors 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Distribution and logistics independent sponsor deals have quietly become one of our fastest-growing use cases over the past 12 months -- trailing manufacturing, healthcare, and tech/software but ahead of consumer in active rooms created during Q1 2026. The reason is structural: wholesale distribution is one of the most fragmented major industries in the US -- the top 100 players control roughly 30% of their respective markets (Modern Distribution Management 2026 Top Distributors List), and the lower middle market is where independent sponsors play while the mega-funds chase the $1B+ Ferguson- and US Foods-scale platform deals.

The challenge is that most "industry-agnostic" LMM PE firms are not the right distribution partner. You are not pitching a vertical SaaS company with 112% net revenue retention. You are pitching a $6M-EBITDA family-owned industrial distributor in Ohio with 30,000 SKUs, three warehouses, a fleet of 12 trucks, one OEM supplier at 22% of COGS, two customers at 15% each, $14M of inventory that turns 4x, and an owner who is 68 and wants out in eight months. The capital partner has to underwrite customer AND vendor concentration, inventory working-capital normalization, fleet capex, warehouse lease renewals, and cyclical freight exposure simultaneously. Generic PE firms that back tech-services or staffing rollups are not the right partner here.

This guide maps 12 verified capital partners actively funding distribution and logistics IS deals in 2026 -- distribution-specialist PE co-investors, diversified LMM firms with deep distribution portfolios, and SBICs that write checks for wholesale distribution, 3PL, specialty distribution, cold chain, and last-mile acquisitions. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide. I spent years evaluating distribution and consumer deals at Backed VC and Target Global before starting Peony, and the distribution IS diligence stack below is the one I would run on my own capital.

TL;DR: Distribution and logistics is the #4 vertical for independent sponsors in 2026 by deal volume (behind manufacturing, healthcare, and tech/software) but arguably has the richest structural setup of any vertical. Q3 2025 US transportation and logistics M&A hit $144.6 billion in deal value -- up 709% year-over-year (PMCF Transportation and Logistics M&A Pulse Q3 2025). Wholesale distribution posted 60+ M&A deals worth over $5 billion in the first five months of 2025 alone (Distribution Strategy Group, 2025). Approximately 6 million US SMBs will face ownership transition by 2035, with 58% having no succession plan (McKinsey, 2025) -- distribution is one of the highest-owner-age verticals in the US economy. Independent sponsors reached 26.8% of all closed deals on Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 Independent Sponsor Report). 54% of IS transactions still close at 4x-6x EBITDA (Citrin Cooperman 2025 IS Report) -- lower than broader PE because IS targets sub-scale founder-led distributors. Sub-sector multiple spread is wider here than anywhere else: wholesale distribution trades at 6x-8x EBITDA, value-added distribution at 8x-12x, and cold chain premium deals hit 12x-14.5x (Frigo-Trans sold to UPS at 14.5x, Staci to bpost at 12.0x per MCF Logistics Insights Spring 2025). The structural tailwind: more than $3 trillion in reshoring and nearshoring FDI has been announced since 2025 (AFIMAC Nearshoring Position Paper 2025) pulling downstream warehousing, 3PL, and industrial distribution demand with it. Below: 12 capital partners funding these deals, sub-sector multiples, roll-up economics, and what distribution capital partners actually need in your data room.

Why Is Distribution & Logistics Growing for Independent Sponsors in 2026?

Four structural forces converge in 2026 to make distribution and logistics one of the most compelling IS target sectors in the lower middle market -- and arguably the most underpriced, because fewer PE firms have genuine sub-sector fluency than in tech or healthcare.

Baby Boomer Succession Is the Single Largest Source of Distribution Deal Flow

Distribution is one of the highest-family-ownership and highest-owner-age verticals in the US economy. Approximately 6 million US SMBs face ownership transition by 2035, with roughly 350,000 baby boomer owners selling companies each year and 58% having no succession plan (McKinsey Great Ownership Transfer, 2025). Gallup's 2025 Pathways to Wealth Survey shows 27% of employer firms with owners 55+ are unsure of long-term plans or intend to close. Distribution skews older than the US SMB average because many family-owned distributors were founded in the 1960s-1980s alongside the broader industrial supply chain. For IS sponsors, family-owned distributors with aging owners and no natural succession plan are the highest-probability proprietary deal sourcing pool in 2026. Many of these owners reject mega-fund buyers on principle (culture, legacy concerns, employee impact) but respond to operator-led IS pitches that preserve management and community.

Reshoring Pulls Downstream Distribution Demand

More than $3 trillion in reshoring and nearshoring FDI has been announced since 2025, with 1.7 million cumulative manufacturing jobs reshored since 2010 (AFIMAC Global Nearshoring Position Paper, 2025). 81% of Bain Reshoring Survey respondents plan to move supply chains closer to market -- up 18 percentage points versus 2022. Every new US manufacturing plant needs local and regional distribution infrastructure: industrial supply distributors, packaging distributors, MRO distributors, specialty chemical distributors, and 3PLs to handle inbound and outbound. Nearshoring to Mexico is driving Gulf Coast and Texas warehousing demand materially above the US average. Prologis has been explicitly cited as the largest beneficiary of this trend. For an IS sourcing a distribution deal in a reshoring-adjacent sub-sector (industrial supply, specialty packaging, MRO, cold chain for food supply, last-mile for e-commerce consolidation), the end-market tailwind is the strongest of any IS vertical.

Record Wholesale Distribution Deal Flow and Strategic Consolidation at the Top

Wholesale distribution posted 60+ M&A and equity deals worth over $5 billion in the first five months of 2025 alone (Distribution Strategy Group, 2025). The electrical distribution market alone saw 14+ acquisitions in the past 18 months, with Sonepar leading at 7 acquisitions, and WESCO, Graybar, Rexel, CED, and QXO all aggressively rolling up (Electrical Wholesaling 2025 Top 100). Brad Jacobs's QXO specifically is running a specialty-distributor roll-up across dozens of targets. This consolidation at the top leaves hundreds of mid-tier regional distributors ($20M-$150M revenue, $3M-$12M EBITDA) squeezed and seeking IS or LMM PE partners to scale or exit -- the classic IS deal profile.

Cold Chain and Specialty Distribution Command Premium Multiples

Cold chain premium deals hit 12x-14.5x EBITDA in 2025 (Frigo-Trans sold to UPS at 14.5x, Staci to bpost at 12.0x per MCF Logistics Insights Spring 2025). The US cold storage market is growing from $39.6 billion in 2025 to $91.4 billion by 2032 at a 12.7% CAGR. Value-added distribution -- kitting, light assembly, private-label manufacturing, technical sales support -- trades at 8x-12x EBITDA. Wholesale distribution at the broadline end trades at 6x-8x EBITDA, and trucking/asset-based logistics at 3x-5x EBITDA. The multiple spread across distribution sub-sectors is wider than in any other IS vertical -- which means sub-sector selection is arguably the single most important decision an IS makes in distribution.

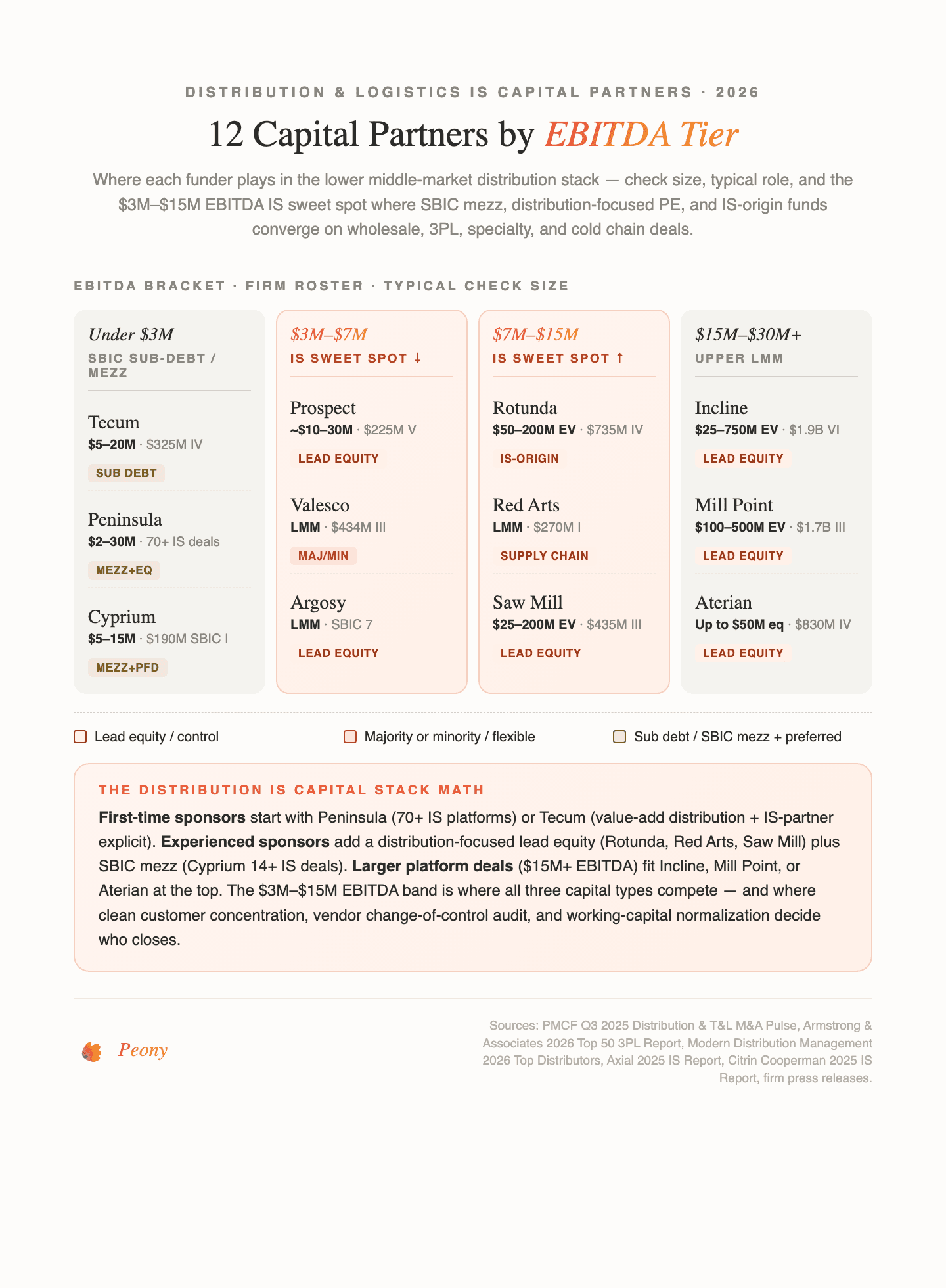

Which 12 Capital Partners Fund Distribution/Logistics IS Deals in 2026?

Twelve capital partners actively fund distribution and logistics independent sponsor deals in 2026 across three roles: distribution-focused PE co-investors (Rotunda, Red Arts, Saw Mill, Incline, Mill Point, Aterian, Prospect), IS-origin or flexible-capital specialists (Valesco, Argosy), and SBIC/mezzanine providers (Peninsula, Tecum, Cyprium). Every firm has been verified against 2024-2026 deal activity and check-size guidance. For data room setup ahead of capital partner outreach, Peony Data Room at $52/admin/month handles the distribution-specific document mix (vendor contracts, customer concentration, warehouse leases, fleet lists, cold chain certifications) out of the box.

| Firm | Website | Check Size / EV | Fund (size, vintage) | Distribution/Logistics Focus |

|---|---|---|---|---|

| Rotunda Capital Partners | rotundacapital.com | $50M-$200M EV | Fund IV $735M (May 2025) | Value-added distribution, asset-light logistics |

| Red Arts Capital | redartscapital.com | LMM control | Fund I $270M+ (May 2023) | Pure-play supply chain, 3PL, co-manufacturing |

| Saw Mill Capital | sawmillcapital.com | $25M-$200M EV | Fund III $435M (Nov 2024) | Specialty distribution, facility services |

| Incline Equity Partners | inclineequity.com | $25M-$750M EV | Fund VI $1.9B + Ascent II $500M | Value-added distribution, services, light mfg |

| Mill Point Capital | millpoint.com | $100M-$500M EV | Fund III $1.7B (Oct 2024) | DSD distribution platform (GlacierPoint) |

| Aterian Investment Partners | aterianpartners.com | Up to $50M equity | Fund IV $830M+ (Oct 2021) | Distribution, manufacturing, chemicals |

| Prospect Partners | prospect-partners.com | Pre-LMM | Fund V $225M (Oct 2024) | Value-add distribution, specialty services, niche mfg |

| Valesco Industries | valescoind.com | LMM majority or minority | Fund III $434M (2023) | Value-add distribution, mfg, business services |

| Argosy Private Equity | argosycapital.com | LMM | SBIC 7 (active, 2021) | Big-and-bulky final-mile logistics (Diverse Logistics) |

| Peninsula Capital Partners | peninsulafunds.com | $2M-$30M | Fund VIII $400M (Sep 2025) | Junior capital (mezz + preferred), 70+ IS platforms |

| Tecum Capital | tecum.com | $5M-$20M | Fund IV $325M SBIC (Jul 2025) | Value-add distribution + business services (SBIC) |

| Cyprium Partners | cyprium.com | $5M-$15M | SBIC I $190M (Feb 2025) | Distribution core sector, 14+ IS-partnered deals |

Tier 1 -- Distribution-Focused PE That Co-Invests with Independent Sponsors

These firms actively co-invest in distribution and logistics IS deals or operate as distribution-focused platforms. Each has a verified 2024-2026 track record deploying capital into wholesale distribution, specialty distribution, 3PL, and value-added distribution acquisitions in the lower middle market.

Rotunda Capital Partners

Website: rotundacapital.com | Fund IV: $735M (closed May 2025, oversubscribed vs. $550M target) | AUM: $1.6B across four funds | HQ: Bethesda, MD

Rotunda Capital Partners was founded in 2009 as an independent sponsor and retains that IS-origin culture even though it now manages $1.6 billion AUM across four funds. Fund IV closed at $735 million in May 2025, oversubscribed versus a $550 million target (Business Wire, May 6, 2025). The firm explicitly names "value-added distribution; asset-light logistics; and industrial, business and residential services" as its three target verticals -- the only firm on this list with distribution and logistics called out as two of three pillars. Recent 2025 deals include Value Added Distributors, LLC (January 14, 2025 acquisition -- Shawano, WI distributor of hoses, tubes, seals and couplings to specialty-vehicle OEMs across 17 Midwest and Southern facilities) and National Fulfillment Services (Fund IV's first deal, tech-enabled logistics platform).

Why it matters for IS: Rotunda's IS-origin DNA is the most explicit of any firm on this list. Founding team grew the firm from a single deal-by-deal sponsor into an institutional fund, which means they genuinely understand the IS economics (exclusivity windows, capital assembly friction, deal-by-deal carry mechanics) that newer institutional firms paper over. For a first-time or emerging IS sourcing a value-added distribution or asset-light logistics deal at $8M-$15M EBITDA, Rotunda should be a first-call equity co-invest partner.

Red Arts Capital

Website: redartscapital.com | Fund I: $270M+ institutional (May 2023) | HQ: Chicago, IL

Red Arts Capital is the only pure-play supply chain and logistics LMM fund on this list. Fund I ($270M+) closed in May 2023 and the firm runs a concentrated portfolio focused entirely on distribution, warehousing, co-manufacturing, and contract packaging. The flagship platform Partners Warehouse acquired PSS Distribution Services (Jamesburg, NJ) in December 2024, extending the platform's footprint into East Coast 3PL with value-added services and creating a national network across Illinois, California, New Jersey, and Dallas with 2+ million square feet (Business Wire, December 12, 2024). Additional portfolio platforms include Radius Logistics (3PL integrating transport, warehousing, and parcel), BelPak (co-manufacturing and co-packing across 25+ US/Canada facilities), and CoRegistics (contract packaging).

Why it matters for IS: Red Arts is the highest-concentration sector-specialist on this list. Their deal teams live and breathe supply chain economics -- they underwrite warehouse square-foot utilization, customer concentration across 3PL contracts, and co-manufacturer capacity as core competencies rather than add-on expertise. For an IS sourcing a specialty 3PL, cold chain, or co-manufacturing platform at $15M-$40M enterprise value, Red Arts reads teasers with sector fluency that generalist LMM firms cannot match.

Saw Mill Capital

Website: sawmillcapital.com | Fund III: $435M (closed November 4, 2024, oversubscribed) | HQ: Briarcliff Manor, NY

Saw Mill Capital closed Fund III at $435 million in November 2024, oversubscribed (PR Newswire, November 4, 2024). The firm invests in "facility and industrial service, specialty distribution and manufacturing businesses" with enterprise values of $25M-$200M. Recent deals include Pro Max Fence Systems (June 2024, third Fund III investment -- specialty distribution of non-residential fencing and access control) and Climate Pros' acquisition of Market Mechanical (September 2024 -- refrigeration and HVAC distribution in the Twin Cities). Saw Mill takes control equity positions.

Why it matters for IS: Saw Mill's LMM specialty-distribution mandate and multi-decade track record make them a credible lead equity co-invest partner for IS sponsors sourcing $10M-$25M EBITDA specialty distribution platforms -- particularly facility services, HVAC/refrigeration distribution, building products distribution, and industrial services where the target combines product distribution with service revenue. Fund III's oversubscription in late 2024 signals aggressive 2025-2026 deployment appetite.

Incline Equity Partners

Website: inclineequity.com | Fund VI: $1.9B (October 2023) | Ascent II: $500M lower-middle-market extension fund (January 2025) | HQ: Pittsburgh, PA

Incline Equity Partners manages Fund VI at $1.9 billion (PR Newswire, October 2023) plus Ascent II at $500 million (PR Newswire, January 2025) for lower-middle-market deals. The firm invests across three core verticals explicitly named as "services, value-added distribution and specialized light manufacturing." Recent activity includes RKD Group acquired June 12, 2025; Accredited Labs (calibration-services roll-up with 8 add-ons across CA, MD, AZ, NV, IL, NC in 2025 plus a $300M single-asset continuation vehicle in October 2025); and Fond du Lac Cold Storage as an active portfolio company. Incline takes lead equity in buyouts and ownership transitions.

Why it matters for IS: Incline is the largest distribution-focused fund platform on this list at $2.4B+ in combined capacity. The Ascent II vehicle explicitly targets the $5M-$15M EBITDA lower-middle-market band where emerging IS sponsors source most deals, while Fund VI handles the upper LMM ($15M+ EBITDA, $25M-$750M EV). For an IS partnering across a 4-to-6-year hold cycle, Incline's dual-fund structure lets them participate in both the initial platform and follow-on add-ons without fund mismatch.

Mill Point Capital

Website: millpoint.com | Fund III: $1.7B (hard cap, oversubscribed, October 10, 2024 -- five months launch to final close) | HQ: New York, NY

Mill Point Capital closed Fund III at $1.7 billion in October 2024 in just five months from launch to final close (Business Wire, October 10, 2024). The firm invests in "Business Services, Industrials and IT Services" with enterprise values of $100M-$500M. The distribution thesis runs through the GlacierPoint Enterprises platform, which acquired Joe & Ross / J&R Dairy Service in June 2024 -- a Chicago-metro DSD distributor of frozen products and ice cream (GlacierPoint press, June 2024). The original E&M Logistics platform (2021, Nestlé frozen pizza and Häagen-Dazs ice-cream DSD distribution) serves as the operating anchor with Jim Schubauer as Executive Partner.

Why it matters for IS: Mill Point's DSD (direct-store-delivery) distribution expertise is uniquely deep -- there are only a handful of PE firms with genuine DSD operating chops, and Mill Point's executive-partner model with Jim Schubauer is one of them. For an IS sourcing a regional DSD distributor, specialty food distribution, or frozen/cold chain DSD platform at $25M-$80M enterprise value, Mill Point's GlacierPoint platform is either a natural exit partner (as strategic acquirer) or a co-invest reference for the operating complexity.

Aterian Investment Partners

Website: aterianpartners.com | Fund IV: $830M+ (October 2021) | Cumulative commitments: $2.0B+ since 2009 | HQ: New York / Miami

Aterian Investment Partners closed Fund IV at more than $830 million in October 2021 (Aterian press) and has deployed $2.0+ billion since 2009 across 40+ platform investments. The firm targets three sectors explicitly: Manufacturing, Distribution, and Chemicals & Commodities. Check sizes run up to $50M equity on revenues of $25M-$500M. Recent distribution-adjacent activity includes Outlook Group (November 4, 2024 -- B2B printing services with distribution component) and Rogers Building Solutions (sold August 2025 to GHK Capital as an exit). On Rogers, Aterian partnered with Craft Work Capital as an independent sponsor -- direct evidence of IS partnership capacity.

Why it matters for IS: Aterian's explicit distribution sector focus plus the Craft Work Capital / Rogers Building Solutions IS partnership reference make them a credible co-invest partner for distribution IS sponsors. Fund IV's scale ($830M+) allows lead equity checks up to $50M while preserving room for IS operating partnership.

Prospect Partners

Website: prospect-partners.com | Fund V: $225M (hard cap, October 2024) | HQ: Chicago, IL

Prospect Partners closed Fund V at its $225 million hard cap in October 2024 (Prospect Partners press). The firm is explicit about Fund V's focus: "specialty services, niche manufacturing, and value-add distribution sectors." Prospect targets pre-LMM companies below the typical LMM buyout band -- sub-$25M EBITDA targets with lead-control equity positions. Extera Building Solutions (March 2024 platform formation -- commercial re-roofing) is distribution-adjacent. Traditional fund sponsor, not IS-branded, but operates in the same deal territory.

Why it matters for IS: Prospect's pre-LMM focus on value-added distribution targets ($2M-$5M EBITDA) is precisely the band where first-time and emerging IS sponsors source proprietary deals. Fund V's 2024 hard-cap close signals disciplined deployment pace rather than opportunistic capital deployment -- a positive signal for IS partners who value follow-through on 3-to-4-year hold commitments.

Tier 2 -- IS-Origin Firms and Flexible-Capital Specialists

These two firms are notable for dedicated IS-partnership capacity or IS-origin culture -- each publicly states IS deal flow is a material source of their capital deployment.

Valesco Industries

Website: valescoind.com | Fund III: $434M (oversubscribed vs. $375M target, 2023 -- Fund III + SBIC structure) | HQ: Dallas, TX

Valesco Industries began as an independent sponsor and has since migrated to fund management with a $434M Fund III closed oversubscribed in 2023 versus a $375M target (Valesco press). The firm targets three sectors: "manufacturing, value-add distribution, and business services." Of Valesco's 8 platform investments in the current fund, 3 have been done to support independent sponsors (Valesco interview with Patrick Floeck). The firm runs majority or minority positions with flexible capital. Adams Flavors, Foods & Ingredients (distribution platform) has been the most active -- it acquired Goodman's Vanilla on September 29, 2024 and Johnny's Fine Foods on May 13, 2025.

Why it matters for IS: Valesco's IS-origin culture plus the 3-of-8-platform IS deployment track record puts them in the same IS-fluency tier as Rotunda and Peninsula. For an IS sourcing a value-add distribution or ingredient/specialty food distribution deal at $5M-$15M EBITDA, Valesco's Fund III capacity and SBIC leverage make them a credible co-invest or lead-equity partner.

Argosy Private Equity

Website: argosycapital.com | SBIC 7: Active (2021 licensed, current deployment) | Firm AUM: $3.4B | HQ: Wayne, PA

Argosy Private Equity is the 2024 SBA SBIC of the Year (Established Manager) (SBIA, May 2024) and deploys SBIC 7 (currently active). The most relevant platform for this guide is Diverse Logistics -- a non-asset-based big-and-bulky final-mile logistics company. In June 2025, Diverse Logistics acquired Massiano Logistics (Orlando white-glove furniture delivery and warehousing) (PR Newswire, June 20, 2025). In February 2026, Diverse Logistics merged with Pulse Final Mile to create a scaled national big-and-bulky final-mile platform operating from 111 customer DCs and 15 warehousing and cross-dock facilities with 850+ third-party contract carriers (Argosy press, February 2026).

Why it matters for IS: The Diverse Logistics platform is one of the most active big-and-bulky final-mile roll-up vehicles in the US -- and the Pulse Final Mile merger in February 2026 creates a reference exit target for IS sponsors scaling regional final-mile operators. Argosy's SBIC leverage plus the operating depth of the Diverse Logistics team make them a credible partner for last-mile IS deals at $15M-$40M enterprise value. Argosy's 2024 SBIC of the Year designation is industry-wide validation of underwriting quality.

Tier 3 -- SBIC / Mezz / Sub-Debt with Distribution Allocation

SBICs and mezzanine providers fill the debt side of distribution IS capital stacks. With SBA-leveraged capital, SBICs offer more flexible terms than traditional bank lenders -- particularly valuable for working-capital-intensive distribution acquisitions where senior lenders cap advance rates on inventory and accounts receivable. Three of the most distribution-active SBIC and mezzanine capital partners:

Peninsula Capital Partners

Website: peninsulafunds.com | Fund VIII: $400M (closed September 2025) | Lifetime: $2.4B raised across 8 partnerships, 70+ IS platforms since 1995 | HQ: Detroit, MI

Peninsula Capital Partners is "the architect of a pioneering and unique investment program which focuses on providing mezzanine capital to non- and independently-sponsored transactions" per the firm's own positioning. Peninsula has backed 70+ independent sponsor platforms since 1995 -- the single deepest IS track record of any firm on this list. Fund VIII closed at $400 million in September 2025 (PE Professional, December 2025), with total firm commitments reaching $2.4B across 8 partnerships. Peninsula provides $2M-$30M checks in flexible junior capital -- mezzanine debt, preferred equity, and minority common equity -- with a $3M+ EBITDA minimum. Recent IS-partnered deals include TapMango (December 2024 -- tech-enabled digital marketing IS majority recap) and Trinity Electrical Services (January 2025 -- specialty electrical contracting IS buyout with subdebt + common equity).

Why it matters for IS: Peninsula is the single most open-to-first-time-IS firm on this list. The firm's explicit IS-partner positioning and 70+ platform track record mean your deal will not be the first IS transaction they have underwritten, and the reference check value alone is worth the call. For a first-time IS sourcing a $3M-$7M EBITDA distribution or specialty-services deal, Peninsula is arguably the single most repeatable junior-capital source in the US lower middle market.

Tecum Capital

Website: tecum.com | Fund IV: $325M SBIC (SBA approval July 2025 -- fourth SBIC license) | HQ: Pittsburgh, PA

Tecum Capital's fourth SBIC fund received SBA approval in July 2025 at $325 million+ (PR Newswire, July 2025). The firm provides mezzanine debt and minority equity of $5M-$20M in businesses with EBITDA greater than $3M. Core sectors include "manufacturing, value-added distribution, and business services." Tecum's IS posture is explicit: the firm "partners with independent sponsors, family offices, committed funds, business owners seeking succession plans" and has "witnessed the rapid expansion of independent sponsors" with ongoing partnership activity. Recent distribution deal: Onward Capital's acquisition of Connecticut Electric in early 2025 -- circuit breakers and electrical distribution products, with Tecum providing subordinated debt + equity alongside Midwest Mezzanine Funds (Tecum press). Tecum is a McGuireWoods Independent Sponsor Conference sponsor.

Why it matters for IS: Tecum's value-added distribution focus, IS-partner positioning, and McGuireWoods IS sponsorship make them a first-call mezz partner for distribution IS sponsors. The $3M+ EBITDA target matches the IS sweet spot perfectly, and the fresh Fund IV SBA approval in July 2025 signals elevated 2025-2026 deployment capacity. For an IS sourcing a $15M-$30M electrical, plumbing, industrial supply, or specialty-distribution deal, Tecum is the reference mezz partner.

Cyprium Partners

Website: cyprium.com | SBIC I: $190M final close February 2025 (first SBIC license) | Lifetime: $2B+ invested across 100+ companies since 1998 | HQ: Cleveland, OH

Cyprium Partners completed final close on SBIC Fund I at more than $190 million in April 2025, marking the firm's first SBIC license (Cyprium press, April 2025). Cyprium has invested $2+ billion across more than 100 companies since 1998 and targets "founder, family, management, entrepreneur, and independent sponsor-owned companies." The firm provides non-controlling mezzanine debt, preferred stock, and minority common equity of $5M-$15M in companies with $4M+ EBITDA across manufacturing, distribution, and business services. Cyprium has completed 14+ IS-partnered deals (Cyprium SBIC press, August 2024). Recent distribution deal: Bochi Investments (Oregon-based IS) acquired Willamette Valley Meat Company in April 2025 -- a meat processor/distributor. This was Cyprium's 14th IS-partnered investment and the first from its debut SBIC fund.

Why it matters for IS: Cyprium's 14-IS-deal track record plus $2B+ lifetime deployment and non-control model preserve IS operating authority across a wide $5M-$15M check range. Distribution is explicitly one of three core sectors. For an IS sourcing a $15M-$30M food distribution, specialty chemical distribution, or wholesale distribution deal with $4M+ EBITDA, Cyprium fills the mezz layer cleanly with documented IS-partnership experience.

How Are Distribution & Logistics IS Deals Priced in 2026?

Distribution and logistics multiples vary more than any other IS sector because the category spans pure wholesale, 3PL, specialty, cold chain, last-mile, and trucking -- each with distinct economic profiles and capital intensity. The 2025-2026 ranges we see on Peony data rooms and in published market data:

| Sub-sector | Revenue multiple | EBITDA multiple |

|---|---|---|

| Broadline wholesale distribution (LMM platform) | -- | 6-8x EBITDA |

| Wholesale distribution add-on ($1M-$2M EBITDA) | -- | 4-5x EBITDA |

| Value-added / specialty distribution (MM) | -- | 8-12x EBITDA |

| Upper middle-market distribution | -- | 9-13x+ EBITDA |

| 3PL regional / freight brokerage | 0.5-1.5x revenue | 5-8x EBITDA (cyclical) |

| 3PL tech-enabled / asset-light | -- | 9-12x EBITDA (top freight brokerage 12-14x) |

| Cold chain / refrigerated 3PL | -- | Median 9.2x, premium deals 12-14.5x (Frigo-Trans UPS, Staci bpost) |

| Last-mile (strategic acquirers) | -- | 12-13x EBITDA (PE-backed 5-6x) |

| Specialty chemical distribution | -- | 8-11x EBITDA |

| For-hire trucking / asset-based | 0.3-0.8x revenue | 5-6x EBITDA average, 6-8x premium |

| Foodservice distribution | -- | 6-9x EBITDA |

| Industrial supply / MRO | -- | 6-9x EBITDA |

| Overall T&L median TEV/EBITDA | -- | 10.44x (2025 down from 11.46x prior year per PCE Q2 2025) |

Roll-up math for wholesale distribution platforms: Acquire add-ons at 4x-5x EBITDA for $1M-$2M EBITDA, integrate into a scaled platform, exit at 8x-12x EBITDA (or 12x-14x for a premium 3PL or specialty-distribution platform). This is the arbitrage that has driven distribution consolidation for two decades and the 4x-to-12x multiple expansion is the core value creation lever for IS sponsors.

Working capital normalization is the single biggest price-chip source in distribution diligence. Distributors carry material inventory and accounts receivable, and the working-capital peg at close can move 5-10% of enterprise value. Capital partners expect 24 months of rolling working-capital data normalized for seasonality, not an LTM snapshot. Inventory turns below 4x for broadline wholesale, below 6x for specialty, or declining over the trailing 36 months are consistent red flags in diligence.

Three IS-Backed Distribution Deals That Closed in 2024-2026 (Reference Case Studies)

Three recent closed deals illustrate how distribution IS capital stacks get assembled in practice. Each pairs a specific sponsor with specific capital partners and specific deal economics -- useful reference architecture for IS sponsors planning their own capital raises.

Deal 1: Onward Capital (IS) acquires Connecticut Electric (Q1 2025)

Onward Capital LLC -- a Chicago-based independent sponsor focused on LMM industrials -- acquired Connecticut Electric (Anderson, IN), a circuit breakers and electrical distribution products business, from Thompson Street Capital Partners in early 2025. The capital stack: senior debt from Byline Sponsor Finance (Byline Bank cash-flow lending); subordinated debt + equity from Tecum Capital + Midwest Mezzanine Funds; equity from Onward + family offices. This is the canonical electrical-distribution IS stack in 2026 -- senior cash-flow lender, two mezz partners, sponsor equity -- and Tecum Capital's involvement is consistent with their explicit value-added distribution mandate.

Deal 2: Bochi Investments (IS) acquires Willamette Valley Meat Company (April 2025)

Bochi Investments -- an Oregon-based IS -- acquired Willamette Valley Meat Company, a meat processor and regional food distributor. The junior capital came from Cyprium Partners (SBIC I) alongside two other SBIC funds -- making this Cyprium's 14th IS-partnered investment and the first from its debut SBIC fund (closed at $190M in April 2025). Food distribution and meat/protein distribution deals are a durable IS sub-sector because founder-led processors frequently sit at the intersection of supplier relationships (ranchers, slaughterhouses) and downstream foodservice/retailer customers that require capital to scale.

Deal 3: Partners Warehouse (Red Arts Capital portfolio) acquires PSS Distribution Services (December 2024)

Partners Warehouse, Red Arts Capital's flagship 3PL platform, acquired PSS Distribution Services (Jamesburg, NJ) in December 2024, extending the platform's footprint into East Coast 3PL with value-added services. The combined platform operates a national 3PL network across Illinois, California, New Jersey, and Dallas with 2+ million square feet -- a reference roll-up template for 3PL IS sponsors. While Red Arts is not itself a pure IS (it is a sector-specialist institutional fund), the Partners Warehouse platform structure is a direct analog for an IS-backed 3PL roll-up targeting $15M-$40M EV add-ons.

Pattern recognition across all three deals: (1) each stack paired an IS or IS-like sponsor with 1-2 institutional capital partners plus a senior lender; (2) each targeted a founder-owned or PE-owned distribution business in a defined sub-sector (electrical, food, 3PL); (3) each closed within a 13-month window signaling real 2024-2026 deal velocity; (4) capital partners involved in these deals (Tecum, Cyprium, Red Arts) are all on the 12-firm list above with verified IS-partnership track records.

What Due Diligence Do Distribution Capital Partners Expect in 2026?

Distribution and logistics diligence is structurally different from manufacturing or tech diligence because the assets are inventory, routes, customer relationships, vendor contracts, and working capital -- and the risks are customer concentration, vendor change-of-control, inventory carrying cost, and cyclical freight exposure. Based on hosting hundreds of distribution IS data rooms on Peony, here is what 2026 capital partners expect -- organized for the staged diligence approach in our complete IS guide and IS data room checklist. Set up your data room on day one of the exclusivity window.

Customer Concentration Analysis

Top-20 customer concentration with revenue share and contract terms is the single most scrutinized schedule in distribution diligence. Capital partners expect the customer name (even under NDA), revenue share across trailing 3 fiscal years, contract term and remaining tenor, change-of-control language, most-favored-nation clauses, and assignability provisions. Any single customer above 20% of revenue is a material concentration issue; above 15% requires mitigation (long-term contract, CoC-protected assignment, or customer interview diligence). In foodservice and medical distribution, top-5 customer concentration above 40% is typical but requires customer interview diligence to clear.

Vendor Concentration and Rebate Programs

Vendor concentration is under-appreciated but often more material than customer concentration in distribution. Capital partners expect top-20 vendor concentration by COGS, exclusivity arrangements, change-of-control provisions, rebate program structures (volume rebates, growth rebates, category rebates), and historical rebate recovery rates. A distributor that earns 300-500 bps of gross margin from vendor rebates has that margin at risk on every vendor CoC clause. Missing a CoC clause in a top-5 vendor contract is a deal-killer. Our due diligence checklist covers the full vendor audit template.

Working Capital Normalization

Distribution businesses carry material inventory and accounts receivable. The working-capital peg at close can move 5-10% of enterprise value. Capital partners expect 24 months of rolling inventory and AR data with seasonality patterns explicit, a peg that reflects normalized rather than LTM working capital, and explicit treatment of excess cash, aging inventory, slow-payer AR, and obsolete SKU reserves. For a $25M enterprise value deal, a $1.5M working-capital miss is 6% of EV -- and capital partners will pressure-test every assumption.

Warehouse, Fleet, and Route Economics

For asset-heavy targets (3PL, trucking, last-mile, cold chain), capital partners expect a complete operational data package: warehouse lease schedules with remaining term, renewal options, rent escalation, and square-foot economics; fleet lists with age, VIN, maintenance history, book value, and replacement timing; route-level profitability analysis for logistics targets; and DOT compliance and driver qualification files for any trucking or last-mile. Cold chain targets require temperature-controlled warehouse certification records, HACCP compliance, and FSMA audit documentation. Targets where the warehouse lease expires within 24 months without renewal flexibility face a material discount.

Environmental and Compliance

Distribution facilities -- particularly those with legacy fuel storage, paint, chemicals, or outdoor inventory -- face environmental exposure. Capital partners expect Phase I ESAs on every owned facility and Phase II where Phase I flags (soil, groundwater, UST, AST). Logistics targets face DOT compliance, driver qualification files, hours-of-service audits, and CSA scores. Cold chain and food-grade distribution face FSMA, USDA, and HACCP compliance. Any prior OSHA recordables, workers-comp claims, or EPA enforcement actions surface in diligence and require remediation disclosure.

ERP, WMS, and IT Systems

ERP and WMS (warehouse management system) maturity is a material value driver in distribution. Capital partners expect documentation of the current ERP (NetSuite, SAP, Epicor, Sage, Acumatica, Infor, Microsoft Dynamics), WMS integration, EDI capability with top-20 customers and vendors, cycle count vs. physical inventory variance, and system age and upgrade roadmap. Distributors still on QuickBooks or homegrown legacy systems at $20M+ revenue face a $500K-$2M post-close ERP replacement that every capital partner will quantify.

For the complete due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes all of these distribution-specific documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is customer concentration by vertical?" or "Which top-20 vendors have change-of-control provisions?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. Granular per-file permissions wall off customer names, vendor rebate schedules, route-level profitability data, and pricing across uploaded documents before you share with capital partners, a workflow that Datasite charges $25K+ per deal to configure manually.

Where Do Distribution/Logistics IS Sponsors Meet Capital Partners in 2026?

Distribution and logistics IS outreach has a different rhythm than tech or healthcare. The best sourcing happens at a mix of IS-specific conferences and distribution-operator events where targets (family-owned distributors, 3PL operators, wholesalers) congregate alongside capital partners. Events happening AFTER April 23, 2026:

| Event | Date | Location | Organizer |

|---|---|---|---|

| ACG DealMAX (InterGrowth rebrand) | April 27-29, 2026 | Las Vegas | ACG Global |

| SBIA Independent Sponsor Forum | May 6, 2026 | Sheraton Philadelphia Downtown | SBIA |

| NAW Executive Summit | June 2026 (TBC) | Washington DC | NAW |

| iGlobal Independent Sponsor Summit Dallas | June 11, 2026 | Dallas | iGlobal Forum |

| CSCMP EDGE 2026 | September 27-30, 2026 | Nashville | CSCMP |

| iGlobal Independent Sponsor Summit NYC | September 28-29, 2026 | New York | iGlobal Forum |

| MDM SHIFT Conference | TBC 2026 | TBC | MDM |

| McGuireWoods Independent Sponsor Conference | October 27-28, 2026 | Fairmont Dallas (1,600+ attendees) | McGuireWoods |

| iGlobal IS Summit West Coast | October 29-30, 2026 | Los Angeles | iGlobal Forum |

For distribution and logistics IS sponsors specifically, the two highest-leverage events are ACG DealMAX (April 27-29) -- the largest LMM dealmaking conference anchoring Q2 capital partner meetings -- and the McGuireWoods Independent Sponsor Conference (October 27-28) -- the single largest dedicated IS event with 1,600+ attendees and strong distribution capital-partner representation. NAW Executive Summit is the most concentrated target-source event for wholesale-distribution IS deal flow (founders, family-business owners, and operators all congregate). CSCMP EDGE is the most concentrated event for 3PL and contract logistics sourcing. For our full IS conferences and forums guide covering 21 events in 2026, see the cluster.

Axial-platform IS deal flow: Independent sponsors closed 27% of all deals on Axial in 2025. Repeat capital partner relationships account for 59% of IS deals according to Citrin Cooperman 2025. For an IS building a 5-to-10 firm capital partner rolodex focused on distribution and logistics, the fastest path is one distribution-specialist equity partner (Saw Mill or Incline) + one diversified LMM PE with distribution depth (Gauge or Wind Point) + one SBIC (Tecum or Centerfield) + one flexible-capital partner (Peninsula or Cyprium).

Use Peony's page-level analytics to track which capital partners are reading the customer concentration analysis and vendor rebate schedule versus skimming the CIM. The ones who spend 20+ minutes on the Q of E and working-capital normalization are the ones worth second meetings. Use personalized sharing links so every capital partner gets a distinct tracking URL, and NDA gates so nobody sees confidential customer lists or vendor rebate schedules until they sign -- something DocSend cannot detect on any plan.

Distribution & Logistics IS Deals By the Numbers

- Q3 2025 US transportation and logistics M&A hit $144.6 billion in deal value, up 709% year-over-year and up 110% quarter-over-quarter (PMCF Transportation and Logistics M&A Pulse Q3 2025)

- Wholesale distribution posted 60+ M&A and equity deals worth over $5 billion in the first five months of 2025 (Distribution Strategy Group, 2025)

- Global transportation and logistics M&A: $138.5 billion total in 2025 -- greater than the past three years combined (M&A Worldwide 2026 Outlook)

- Approximately 6 million US SMBs face ownership transition by 2035, with 58% having no succession plan (McKinsey Great Ownership Transfer, 2025)

- More than $3 trillion in reshoring and nearshoring FDI announced since 2025, with 1.7M cumulative manufacturing jobs reshored since 2010 (AFIMAC Nearshoring Position Paper, 2025)

- 81% of Bain Reshoring Survey respondents plan to move supply chains closer to market (+18 points versus 2022) ([Bain, 2025])

- PE-backed add-ons reached 75.9% of all buyouts in Q2 2025 (PitchBook Q2 2025 US PE Breakdown)

- PE dry powder sits at approximately $3.7 trillion globally at the start of 2026 (S&P Global, December 2025)

- Electrical distribution saw 14+ acquisitions in the past 18 months, with Sonepar leading at 7 acquisitions; WESCO, Graybar, Rexel, CED, and QXO all aggressively rolling up (Electrical Wholesaling 2025 Top 100)

- US cold storage market: $39.6 billion in 2025 growing to $91.4 billion by 2032 at 12.7% CAGR ([Persistence Market, 2025])

- Cold chain premium deals: Frigo-Trans sold to UPS at 14.5x EBITDA; Staci sold to bpost at 12.0x (MCF Logistics Insights Spring 2025)

- 54% of IS transactions closed at 4x-6x EBITDA in 2024-2025 (Citrin Cooperman 2025 IS Report)

- 59% of IS capital partner deals come from repeat relationships (Citrin Cooperman 2025)

- Independent sponsors reached 26.8% of all closed deals on Axial YTD 2025, outpacing PE funds at 21.1% (Axial 2025 Independent Sponsor Report)

- Distribution wholesale platform multiples: 6x-8x EBITDA; value-added distribution 8x-12x; upper MM distribution 9x-13x+; 3PL regional freight brokerage 5x-8x; 3PL tech-enabled premium 9x-12x (top freight brokerage 12x-14x); cold chain median 9.2x with premium deals at 14.5x; last-mile strategic 12x-13x; for-hire trucking 5x-6x average (PCE Q2 2025, KMCo Q1 2025, First Page Sage 2025)

How Peony Fits the Distribution/Logistics IS Workflow

Peony is a data room platform purpose-built for the exact workflow distribution and logistics IS sponsors run: multiple simultaneous deals during roll-up phases, heavy document diligence (customer contracts, vendor agreements, warehouse leases, fleet lists, DOT files, cold chain certifications), and capital partner engagement tracking. Peony Data Room at $52/admin/month is the plan distribution IS sponsors use.

AI auto-indexing organizes customer contracts, vendor agreements, warehouse leases, fleet lists, cycle count audits, and compliance records into a professional folder structure in under 3 minutes. Junior analysts spend 2-3 hours on this same workflow in Datasite.

Page-level analytics tell you which capital partner spent 30 minutes on the Q of E versus skimmed the CIM, and which one lingered on the customer concentration analysis versus flipped through it. DocSend gives you deck-level views; Peony gives you page-by-page engagement so you know who is genuinely diligencing versus pattern-matching.

Smart Q&A lets counterparties submit diligence questions where AI drafts answers by surfacing the exact document sections and page citations. Your team approves every response before it ships, and every Q&A exchange is audit-trailed. For distribution diligence where questions like "What is inventory turns by category?" or "Which top-20 customers have change-of-control clauses?" come in from every capital partner, this workflow compounds across 3-to-6 simultaneous deals.

Granular per-file permissions wall off customer names, vendor rebate schedules, route-level profitability data, and pricing across uploaded documents before capital partners see them -- a workflow Datasite charges $25K+ per deal to configure manually.

Screenshot protection blocks and logs screen-capture attempts on sensitive files. Dynamic watermarks embed viewer identity on every frame of every document, which distribution capital partners require before reviewing customer lists, vendor rebate schedules, or confidential pricing.

NDA gates require signature before any materials are visible -- DocSend cannot detect this on any plan. AI document extraction lets capital partners ask "What is gross margin by product category?" and get a cited answer. E-signatures close the loop after conference introductions -- capital partners sign the NDA and access materials in a single workflow.

Unlimited data rooms on Peony Data Room mean an IS running 4-to-8 simultaneous deals during a roll-up phase does not pay per-deal licensing. An IS running three distribution deals per year pays roughly $624 annually on Peony Data Room versus $45,000-$150,000 on Datasite. The free tier is the entry point; Peony Data Room at $52/admin/month is where serious IS workflows run.

For deeper context on private equity co-investment structures, M&A deal process, due diligence expectations, and fundraising best practices, see our dedicated solutions guides.

Quick Guide: Match Your Situation to the Right Capital Partner

| Situation | Best CP Fit | Why |

|---|---|---|

| First-time IS, $12M EV wholesale distributor, $2.5M EBITDA, Midwest | Peninsula Capital Partners + Tecum Capital (mezz) | Peninsula's 70+ IS-platform track record (the most first-time-IS-friendly firm on the list); Tecum's value-add distribution mandate + SBIC Fund IV fresh capacity |

| First-time IS, $20M EV food distributor, $3M EBITDA | Cyprium Partners (SBIC I mezz) + Peninsula | Cyprium's 14+ IS deals + Willamette Valley Meat reference; Peninsula's junior-capital depth |

| Experienced IS, $35M EV electrical distributor, $5M EBITDA | Rotunda Capital Partners + Tecum (mezz) | Rotunda's IS-origin + value-added distribution mandate; Tecum's Connecticut Electric reference deal |

| Operating-partner IS, $50M EV 3PL roll-up, $8M EBITDA | Red Arts Capital + Cyprium (mezz) | Red Arts pure-play supply chain + Partners Warehouse template; Cyprium's non-control distribution mezz |

| First-time IS, $15M EV specialty distribution (HVAC/refrigeration), $3M EBITDA | Saw Mill Capital + Peninsula (mezz) | Saw Mill's Climate Pros/Market Mechanical reference; Peninsula's first-time-IS track record |

| Experienced IS, $75M EV DSD food distribution roll-up, $10M EBITDA | Mill Point Capital (exit target) + Cyprium (mezz) | Mill Point's GlacierPoint DSD platform as exit target; Cyprium's food-distribution experience |

| Operating-partner IS, $40M EV last-mile logistics platform, $6M EBITDA | Argosy Private Equity + Peninsula (mezz) | Argosy's Diverse Logistics + Pulse Final Mile reference; Peninsula's flexible junior capital |

| Experienced IS, $60M EV industrial supply distribution platform, $8M EBITDA | Incline Equity Partners + Cyprium (mezz) | Incline's flagship value-add distribution focus (Fund VI + Ascent II); Cyprium's distribution core sector |

| First-time IS, $10M EV specialty value-add distribution, $2M EBITDA (pre-LMM) | Prospect Partners + Peninsula (mezz) | Prospect's pre-LMM value-add distribution mandate; Peninsula's first-time-IS openness |

| Experienced IS, $100M+ EV upper-LMM wholesale distribution platform, $15M+ EBITDA | Mill Point Capital + Aterian Investment Partners | Mill Point's upper-LMM control scale; Aterian's distribution + manufacturing + chemicals triangulation |

| First-time IS, $18M EV branded ingredient distributor, $3M EBITDA | Valesco Industries + Tecum (mezz) | Valesco's IS-origin + ingredient platform (Adams Flavors); Tecum value-add distribution mezz |

| Operating-partner IS, $30M EV cold chain 3PL platform, $4M EBITDA | Red Arts Capital + Cyprium (mezz) | Red Arts pure-play supply chain fluency; Cyprium's non-control mezz with distribution core sector focus |

Bottom Line

Distribution and logistics is the #4 IS sector in 2026 behind manufacturing, healthcare, and tech/software -- but arguably has the richest structural setup of any vertical given baby boomer succession concentration, reshoring tailwinds pulling downstream warehousing and 3PL demand, and wholesale consolidation at the top (Sonepar, WESCO, QXO) squeezing mid-tier distributors into IS-sized deal flow. Sub-sector selection matters more here than in any other IS vertical because multiples span 3x-5x for for-hire trucking versus 12x-14.5x for cold chain premium deals.

If you are targeting wholesale or value-added distribution: Rotunda Capital Partners (IS-origin + Fund IV $735M), Incline Equity Partners (Fund VI $1.9B + Ascent II $500M with explicit value-added distribution mandate), Saw Mill Capital (Fund III $435M specialty distribution), and Aterian Investment Partners (Fund IV $830M+ with distribution as one of three core sectors) are the most active equity co-invest partners. Expect customer concentration, vendor change-of-control, and working-capital normalization to be the three diligence kill-switches.

If you are targeting 3PL, cold chain, or specialty logistics: Red Arts Capital is the only pure-play supply-chain LMM fund on this list and the Partners Warehouse + PSS Distribution template is a reference roll-up architecture. Argosy Private Equity's Diverse Logistics + Pulse Final Mile merger in February 2026 creates a scaled national big-and-bulky final-mile platform that serves as both reference template and potential exit target. For cold chain specifically, the 12x-14.5x premium multiples that Frigo-Trans and Staci achieved in 2025 set the upside ceiling.

If you need mezzanine or subordinated debt: Peninsula Capital Partners (Fund VIII $400M September 2025, 70+ IS platforms since 1995 -- the deepest IS track record on this list), Tecum Capital (Fund IV $325M SBIC July 2025 with explicit value-added distribution focus and McGuireWoods IS sponsorship), and Cyprium Partners (SBIC I $190M February 2025 with 14+ IS-partnered deals) all provide flexible capital structures tailored to distribution IS stacks. Peninsula is the single most open-to-first-time-IS firm on this list -- if you are running your first deal, make Peninsula your first call.

For every distribution IS deal: Set up your data room on day one of the exclusivity window. Distribution diligence is working-capital-intensive (top-20 customer contracts, top-20 vendor agreements with rebate schedules, 24-month working-capital roll, warehouse lease schedules, DOT compliance for logistics, cold chain certifications where applicable, and ERP/WMS documentation) -- capital partners expect the data room to be organized and complete at Week 1 of exclusivity. You cannot afford to lose days to VDR setup. Peony lets you build a complete distribution IS data room in under 5 minutes, with page-level analytics that show which capital partners are reading the customer concentration analysis versus skimming the CIM, AI-powered Smart Q&A that surfaces hard answers with page citations so capital partners complete diligence faster, and NDA gates that prevent any capital partner from seeing customer lists or vendor rebate schedules before signing.

Peony Data Room at $52/admin/month includes unlimited data rooms, AI auto-indexing, AI-powered Smart Q&A, dynamic watermarks, screenshot protection, NDA gates, page-level analytics, AI document extraction, and e-signatures. An IS running three distribution deals per year pays roughly $624 annually versus $45,000-$150,000 on Datasite. When your exclusivity clock is ticking and five capital partners need to get comfortable with the distribution deal simultaneously, every hour matters.

Set up your first distribution or logistics IS data room -- see plans and pricing.

Frequently Asked Questions

I am a first-time IS with a signed LOI on a $10M EBITDA industrial distributor -- which capital partners fund distribution/logistics independent sponsor deals?

Distribution and logistics independent sponsor deals are funded by three capital partner types: distribution-focused PE firms that co-invest on a deal-by-deal basis such as Rotunda Capital Partners (founded AS an IS in 2009), Red Arts Capital (pure-play supply chain), Saw Mill Capital, Incline Equity Partners, Mill Point Capital, and Aterian Investment Partners; IS-origin and flexible LMM PE like Valesco Industries (also IS-origin), Prospect Partners, and Argosy Private Equity; and SBIC or mezzanine providers such as Peninsula Capital Partners (70+ IS platforms since 1995), Tecum Capital, and Cyprium Partners (14+ IS-partnered deals). For a first-time IS on a $10M EBITDA industrial distributor, a $4M-$6M check from an SBIC like Tecum or Cyprium plus a minority equity partner like Peninsula or a lead-equity partner like Rotunda is the typical stack. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the top-20 customer contracts, vendor agreements, warehouse leases, fleet lists, and route profitability analyses in under 3 minutes -- so the data room is ready before the first capital partner call.

I run corp dev at a mid-market PE firm -- what EBITDA multiples do distribution/logistics IS deals trade at in 2026?

Distribution and logistics IS deals in 2026 trade across a wide range by sub-sector: wholesale distribution (plumbing, electrical, industrial supply) trades at 6x to 8x EBITDA for LMM platforms and 4x to 5x for add-ons, specialty and value-added distribution commands 8x to 12x EBITDA, upper middle-market distribution reaches 9x to 13x EBITDA, 3PL regional and freight brokerage runs 5x to 8x EBITDA and is cyclical, 3PL tech-enabled and asset-light trades at 9x to 12x EBITDA (top freight brokerage 12x to 14x), cold chain median runs at 9.2x with premium deals hitting 14.5x (Frigo-Trans to UPS at 14.5x, Staci to bpost at 12.0x per MCF Logistics Insights Spring 2025), last-mile strategic acquirers pay 12x to 13x EBITDA while PE-backed last-mile trades at 5x to 6x, specialty chemical distribution runs 8x to 11x EBITDA, and for-hire trucking runs 5x to 6x EBITDA average. For a corp dev lead evaluating a $20M-$40M wholesale distribution platform, the spread between platform and add-on multiples plus sub-sector premia is the core value creation mechanism. Peony Business includes AI document extraction that lets capital partners ask What is customer concentration by vertical or What is the gross margin by product category across uploaded financials and get cited answers with exact page numbers, a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first distribution IS deal -- why is distribution/logistics growing for independent sponsors in 2026?

Distribution and logistics is growing for independent sponsors because four structural forces converge in 2026: the baby boomer succession wave hit the distribution industry hardest with approximately 6 million US SMBs facing ownership transition by 2035 and 58 percent having no succession plan according to McKinsey, more than $3 trillion in reshoring and nearshoring FDI has been announced since 2025 pulling downstream 3PL and wholesale distribution demand, wholesale M&A posted 60 or more deals worth over $5 billion in the first five months of 2025 alone according to Distribution Strategy Group, and Q3 2025 US transportation and logistics M&A deal value hit $144.6 billion up 709 percent year-over-year per PMCF. For a family office allocating $5M-$15M equity to its first distribution IS deal, focus on founder-led wholesale distributors with $3M-$10M EBITDA in defensible regional or vertical niches where the owner is over 60 and has no natural succession plan. Peony Business at $30 per admin per month includes page-level analytics that show which capital partners spent 30 minutes on the customer concentration analysis versus skimmed the CIM, so you can prioritize follow-ups with genuinely engaged partners.

I am a corp dev analyst building my first distribution data room -- what documents do capital partners need?

Distribution and logistics capital partners require standard M&A diligence plus distribution-specific materials: top-20 customer concentration with revenue share, contract terms, and assignability language, top-20 vendor concentration with exclusivity, rebate programs, and change-of-control provisions, gross margin analysis by product category and customer vertical, inventory turns and aging by SKU or category, warehouse lease schedules with remaining terms and renewal options, fleet list (if asset-heavy) with age, maintenance history, and replacement timing, route profitability analysis for logistics targets, cold chain certification records for cold storage or refrigerated distribution, DOT compliance records and driver qualification files for trucking or last-mile, Phase I and Phase II ESAs for any owned facility, OSHA and workers comp history, freight carrier agreements with rate schedules, EDI and ERP system documentation, and cycle count and physical inventory audit reports. For a corp dev analyst running point on a $25M-$50M distribution deal, these are the documents that kill or close the transaction. Peony Data Room auto-indexing organizes all of these in under 3 minutes into a professional folder structure, and Smart Q and A routes capital partner questions through AI-drafted answers with page citations before your team approves each response.

Our IS targets cold chain and specialty distribution -- which capital partners fit sub-sector specialists?

Cold chain and specialty distribution independent sponsor deals command the highest multiples in the distribution universe -- cold chain premium deals hit 12x to 14.5x EBITDA (Frigo-Trans sold to UPS at 14.5x, Staci sold to bpost at 12.0x per MCF Logistics Insights) versus 6x to 8x for broadline wholesale -- and capital partner fit is deeply sub-sector-specific. Red Arts Capital is the only pure-play supply-chain and logistics LMM fund on this list and operates Partners Warehouse (2M+ sqft 3PL including PSS Distribution acquired December 2024) and BelPak (25+ facility co-manufacturing and contract packaging). Saw Mill Capital explicitly lists specialty distribution as a core sector (Fund III $435M closed November 2024) and has backed Climate Pros (HVAC/refrigeration distribution). Peninsula Capital Partners has backed 70-plus IS platforms historically with distribution exposure and writes mezz and minority equity $2M-$30M checks on Fund VIII ($400M September 2025). Rotunda Capital Partners was founded AS an independent sponsor in 2009 and explicitly names value-added distribution and asset-light logistics in its mandate (Fund IV $735M May 2025). For a specialized IS targeting a $20M-$40M cold chain 3PL or a regional medical-supply distributor with $4M-$8M EBITDA, the stack typically pairs a distribution-focused equity lead with SBIC mezzanine from Tecum or Cyprium. Peony's Data Room plan at $52 per admin per month includes dynamic watermarks with viewer identity embedded in every frame, with NDA gates starting on the Business plan at $30 per admin per month so capital partners acknowledge before any customer list, vendor rebate schedule, or route profitability data is visible.

Our IS is running three to six distribution deals per year -- how much does a data room cost for distribution/logistics IS deals?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 3 to 25 million dollar EBITDA distribution and logistics businesses. Distribution deals also require extensive vendor and customer contract uploads, DOT compliance files, warehouse lease schedules, environmental reports, and rebate program documentation, meaning sponsors often need four to six active data rooms simultaneously during a roll-up phase -- a dynamic structurally broken on per-deal pricing. Peony Data Room at 52 dollars per admin per month includes unlimited data rooms, AI auto-indexing, AI document extraction, Smart Q and A, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. An IS running three distribution deals per year pays roughly 624 dollars annually on Peony Data Room versus 45,000 to 150,000 dollars on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure.

I am a capital-partner PE principal diligencing a wholesale distribution deal -- what distribution sub-sectors have the most IS activity in 2026?

The most active distribution and logistics sub-sectors for independent sponsor deals in 2025-2026 are industrial and MRO wholesale distribution where fragmented regional players dominate and reshoring-linked demand drives tailwinds, foodservice distribution where consolidation around regional specialty distributors continues post-Sysco and US Foods, jan/san and packaging distribution benefiting from institutional recovery, specialty medical and dental distribution at premium multiples due to recurring demand, cold chain 3PL and specialty warehousing with defensive economics driving 12x-14.5x EBITDA premium multiples in 2025 deals, last-mile and final-mile logistics driven by e-commerce consolidation in tier-2 and tier-3 metros (Argosy's Diverse Logistics + Pulse Final Mile merger in February 2026 is the reference template), and specialty chemicals and industrial gases distribution which trades at premium multiples on customer stickiness and regulatory barriers. For a capital-partner PE principal diligencing a $30M-$50M wholesale distribution platform, expect customer concentration, vendor change-of-control provisions, and inventory working-capital normalization to be the three biggest diligence issues. Peony Data Room at 52 dollars per admin per month includes AI-powered Smart Q and A that lets capital partners submit diligence questions where AI surfaces relevant document sections with exact page citations, something DocSend cannot detect on any plan.

I am an M&A attorney advising a first-time IS -- how do distribution capital partners expect deal books to be structured?

Distribution and logistics capital partners expect deal books organized in a standard 3-stage diligence flow: Stage 1 initial risk scan including the CIM, top-20 customer and vendor concentration analyses, gross margin by category, inventory turns, and environmental screening on any owned facility; Stage 2 deep dive with Q of E and working capital normalization, vendor change-of-control and rebate program audit, warehouse lease schedules and remaining terms, fleet appraisal and replacement schedule for asset-heavy targets, DOT and safety compliance records for logistics, and cold chain certification records where applicable; Stage 3 comprehensive validation covering Phase I and Phase II ESAs, OSHA audits, integration plan for ERP and WMS consolidation, and 100-day route and warehouse optimization plan. For an M&A attorney advising a first-time IS running a $25M enterprise value distribution deal, the working capital normalization alone can move 5-10 percent of enterprise value and capital partners will pressure-test the inventory and accounts receivable peg. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing that organizes documents into a professional folder structure in under 3 minutes, and personalized sharing links that track each capital partner separately so you know who is engaged before you draft the capital call.

Our IS is running a $35M roll-up of industrial distributors -- how do we handle working capital and vendor concentration due diligence?

Working capital-heavy distribution targets require a disciplined normalization calculation in the Q of E, with 24 months of rolling inventory and accounts receivable data, a peg that reflects normal seasonality rather than LTM snapshot, and explicit separation of operating working capital from excess cash. Vendor concentration requires a complete audit of top-20 vendors by COGS, change-of-control provisions and rebate program structures, exclusivity arrangements that transfer on sale, and historical rebate recovery rates. For an IS running a $35M roll-up of industrial distributors, every vendor rebate dollar is a dollar of gross margin that needs to flow through post-close, and every missed change-of-control clause is a potential vendor termination right. Document vendor contracts with change-of-control language highlighted, attach historical rebate statements for the trailing 36 months, and include a supplier concentration summary showing any vendor above 10 percent of COGS. Peony Data Room at 52 dollars per admin per month includes granular per-file permissions that wall off pricing and rebate data across uploaded vendor and customer files, and NDA gates that prevent any capital partner from seeing confidential vendor rebate schedules before signing, a workflow that Datasite charges $25K+ per deal to configure.

I am a first-time IS building a capital partner network -- where do distribution/logistics independent sponsors meet capital partners in 2026?

Distribution and logistics independent sponsors meet capital partners at the McGuireWoods Independent Sponsor Conference with 1,600 attendees in 2025 and the 2026 event on October 27-28 in Dallas, the ACG DealMAX conference on April 27-29 in Las Vegas (the InterGrowth rebrand anchoring the spring LMM calendar), the SBIA Independent Sponsor Forum on May 6 at the Sheraton Philadelphia Downtown, the NAW Executive Summit in Washington DC for wholesale distribution deal sourcing, CSCMP EDGE 2026 in Nashville for 3PL and supply chain operator relationships, the iGlobal Independent Sponsor Summit Dallas on June 11 and NYC on September 28-29, and through platforms like Axial where independent sponsors reached 26.8 percent of all closed deals YTD 2025. Repeat relationships account for 59 percent of capital partner deals according to Citrin Cooperman. For an IS building a 5-to-10 firm capital partner rolodex focused on distribution and logistics, starting with a distribution-specialist equity partner like Rotunda, Saw Mill, or Incline plus one SBIC like Tecum, Peninsula, or Cyprium is the fastest path. Peony Data Room at 52 dollars per admin per month includes NDA-gated data rooms with built-in e-signatures so capital partners can sign and access materials in a single workflow after conference introductions.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- SBIC for Independent Sponsors -- 2-to-1 debenture math, $175M/$350M caps, 8 active IS-partner SBICs (Tecum, Argosy, Plexus on distribution roll-ups including Pulse Final Mile + Diverse Logistics Feb 2026)

- Independent Sponsor Manufacturing Capital Partners -- 12 firms funding manufacturing IS deals

- Independent Sponsor Tech/Software Capital Partners -- 13 firms funding tech/software IS deals

- Independent Sponsor Consumer Capital Partners -- 12 firms funding consumer IS deals

- Independent Sponsor Healthcare Capital Partners -- 17 firms funding healthcare IS deals

- Independent Sponsor Business Services Capital Partners -- 15 firms funding business services IS deals

- Independent Sponsor Cleantech & Energy Capital Partners -- 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Independent Sponsor Data Room Checklist -- staged diligence checklist by capital partner type

- Independent Sponsor LOI Playbook -- post-LOI capital assembly and exclusivity management

- Independent Sponsor Deal Book -- what capital partners want to see in 2026

- Independent Sponsor Conferences and Forums -- 21 events mapped for IS dealmakers

- Best Data Rooms for Independent Sponsors -- platform comparison for IS workflows

- Due Diligence Data Room Checklist -- 174-document checklist across 10 categories

- M&A Data Room Guide -- M&A-specific data room setup

- Virtual Data Room Cost Guide -- budget calculator framework by deal profile

- Peony for Private Equity -- PE-specific data room features

- Peony for M&A -- M&A data room solutions

- Peony for Due Diligence -- diligence workflow tools

- Peony for Fundraising -- fundraising data room workflows