13 Tech/Software Capital Partners for Independent Sponsors in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Tech and software independent sponsor deals have been the fastest-growing use case on our platform over the past 12 months -- surpassing healthcare and manufacturing in active rooms created during Q1 2026. The reason is straightforward: 2025 posted a record 2,698 SaaS M&A transactions, up 28% year-over-year, with PE buyers accounting for 58% of activity (Software Equity Group, February 2026), and the lower middle market is where independent sponsors play while the mega-funds chase the Wiz, Confluent, and Armis-scale deals.

The challenge is that most tech and software capital partners look nothing like a healthcare PE firm or an industrial sponsor. You are not pitching a founder-owned CNC shop with a union workforce. You are pitching a $6M-ARR vertical SaaS company with 112% net revenue retention, a SOC 2 Type I audit in progress, two external contractors whose IP assignments never got signed, and an open-source dependency on an AGPL-licensed library that nobody noticed for three years. The capital partner has to underwrite code quality, customer concentration, cybersecurity posture, regulatory compliance, engineer retention, and product-market fit simultaneously. Generic "industry-agnostic" PE firms that back staffing or fabrication rollups are not the right partner here.

This guide maps 13 verified capital partners actively funding tech and software IS deals in 2026 -- software-focused PE co-investors, tech-enabled services specialists, and SBICs that write checks for vertical SaaS platforms, MSP roll-ups, MSSP acquisitions, IT services consolidations, and fintech-services deals in the lower middle market. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide. I spent years evaluating software deals at Backed VC and Target Global before starting Peony, and the tech IS diligence stack below is the one I would run on my own capital.

TL;DR: Tech and software is the fastest-growing IS sector in 2026 on the back of record SaaS M&A volume and MSP consolidation. 2025 SaaS M&A hit 2,698 transactions, an all-time high and up 28% YoY, with 58% PE buyer share (Software Equity Group, February 2026). Tech sector 2025 deal value hit $843.3B, up 67% YoY, representing 18% of all M&A (Chambers 2026 / Morrison Foerster). January 2026 tech M&A alone hit $43.2B, up 65% YoY, with 22 $10B+ tech deals closing in Q1 2026 (CNBC, February 2026 / FinancialContent, March 2026). PE was involved in 72% of MSP acquisitions in 2025 (Omdia / Solganick, 2025), and the top 20 PE-backed MSP platforms now control approximately 12% of the US market, up from 6% in 2022. PE dry powder sits at approximately $3.7 trillion globally at the start of 2026 (S&P Global, December 2025). PE-backed add-ons reached 75.9% share in Q2 2025, with tech roll-ups as the primary driver (PitchBook). 54% of IS transactions still close at 4x-6x EBITDA (Citrin Cooperman 2025 IS Report) -- lower than broader PE because IS targets sub-scale founder-led SaaS and MSPs. Below: 13 capital partners funding these deals, sub-sector multiples, the Evergreen/Alpine roll-up template, and what tech capital partners actually need in your data room.

Why Tech/Software Is the Fastest-Growing Vertical for Independent Sponsors in 2026

Four structural forces converge in 2026 to make tech and software the most compelling IS target sector in the lower middle market:

Record SaaS M&A Volume and PE Buyer Dominance

The 2025 SaaS M&A year was the busiest in recorded history. Software Equity Group counted 2,698 SaaS transactions in 2025, up 28% year-over-year and an all-time high, with PE buyers accounting for 58% of activity and AI positioning in 72% of deals (Software Equity Group, February 2026). Q3 2025 alone posted 746 SaaS transactions -- a single-quarter record. Tech sector M&A globally hit $843.3 billion in 2025 deal value, up 67% YoY, representing 18% of total M&A (Chambers 2026 / Morrison Foerster). Q1 2026 continued the cadence: January 2026 tech M&A hit $43.2B, up 65% YoY, with 22 $10B+ tech deals closing in Q1 2026 alone (CNBC, February 2026). Top 2026 mega-deals include Alphabet/Wiz at $32B, IBM/Confluent at $11B in December 2025, and ServiceNow/Armis at $7.75B. Sub-scale targets that the mega-funds ignore become the core IS deal flow.

MSP and Tech-Services Consolidation

The top 20 PE-backed MSP platforms now control approximately 12% of the US MSP market, up from 6% in 2022 (Omdia). PE was involved in 72% of MSP acquisitions in 2025 (Solganick, 2025). The roll-up math is one of the cleanest in PE: acquire an MSP add-on at 6x-8x EBITDA for $1M-$2M EBITDA, integrate, exit a platform at 10x-12x EBITDA (or 15x-20x for premium vertical software platforms). Evergreen Services Group closed 47 transactions in 2025 including its 100th MSP milestone; Lyra Technology Group hit $1B ARR in June 2025 with a target of $5B revenue by 2030. For IS sponsors, imitating this template at smaller scale with 3-to-6 add-ons per platform is the most repeatable tech thesis in the lower middle market.

Record PE Dry Powder Targeting Software

Private equity dry powder sits at approximately $3.7 trillion globally at the start of 2026 (S&P Global, December 2025). Tech-focused PE dry powder has grown by roughly $68 billion between 2021 and 2023 and remained sustained at elevated levels through 2026 according to McKinsey. PE-backed add-ons reached 75.9% of all buyouts in Q2 2025, with tech roll-ups as the primary driver (PitchBook). Translation: there is more capital chasing software platforms than there are attractive platforms to deploy it into. For an IS bringing a proprietary $3M-$10M ARR software deal, the capital partner side of the stack is not the constraint in 2026 -- deal sourcing and operational execution are.

AI Positioning Accelerates Multiples

AI positioning appeared in 72% of SaaS M&A deals in 2025 (Software Equity Group, February 2026). Vertical SaaS with genuine AI-enabled workflow embedding commands materially higher multiples than generic horizontal SaaS. Q3 2025 posted 54% vertical SaaS share, up from 43% year-over-year -- meaning more than half of all SaaS M&A is in vertical-specific platforms where defensible data moats and entrenched workflows drive premium multiples. For IS sponsors, vertical SaaS at Rule of 40 above 50 and NRR above 120% is the highest-multiple software category in the lower middle market.

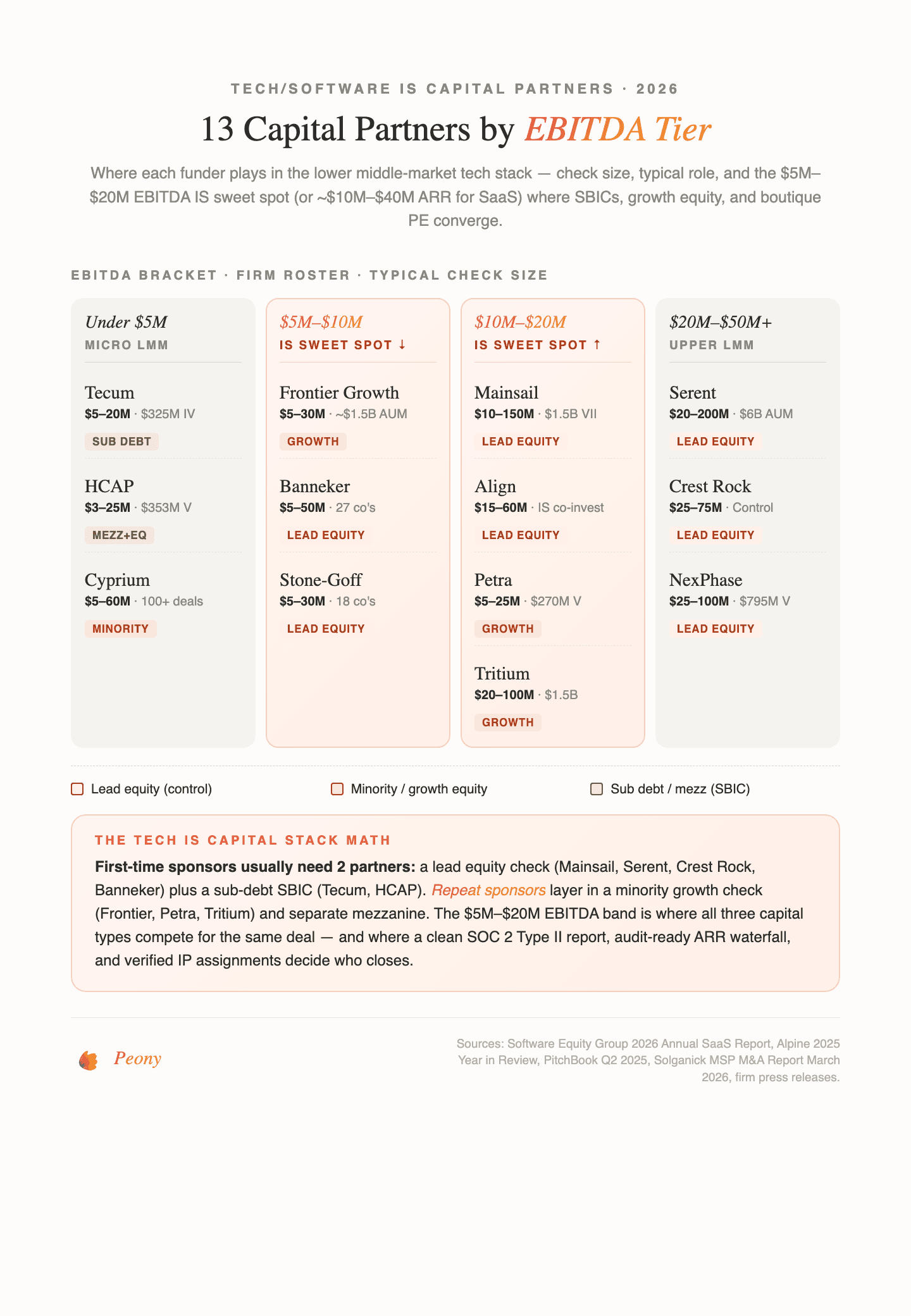

The 13 Capital Partners Funding Tech/Software Independent Sponsor Deals in 2026

Below is a quick-reference map of the 13 capital partners actively funding tech and software IS deals in 2026, organized by role (tech-focused PE, sub-sector specialists, and SBIC/mezzanine providers). Every firm has been verified against 2025-2026 deal activity and check-size guidance. For data room setup ahead of capital partner outreach, Peony Data Room at $52/admin/month handles the SaaS-specific document mix out of the box.

| Firm | Website | Check Size | Deal Size (EV / EBITDA / ARR) | Tech/Software Sub-Sector Focus |

|---|---|---|---|---|

| Mainsail Partners | mainsailpartners.com | $10M-$150M | $5M+ ARR | B2B software, capital-efficient founder-led |

| Serent Capital | serentcapital.com | $20M-$200M | $10M-$50M ARR | B2B software, growth and buyout equity |

| Crest Rock Partners | crestrockpartners.com | $25M-$100M | LMM control | Software, tech services, business services |

| NexPhase Capital | nexphase.com | Fund V $795M | LMM control / growth | Software, consumer, healthcare |

| Banneker Partners | bannekerpartners.com | $5M-$50M revenue tgts | Vertical enterprise SaaS | Public safety, higher ed, life sciences, OT cyber |

| Frontier Growth | frontiergrowth.com | $5M-$30M initial | $3M-$20M ARR, 25%+ growth | Pure vertical SaaS |

| Petra Capital Partners | petracapital.com | Up to $25M | Growth-stage | Tech-enabled services, healthtech |

| Align Capital Partners | aligncp.com | Control + IS co-inv | LMM + IS Collaborate Fund | Tech-enabled services, vertical software |

| Stone-Goff Partners | stonegoffpartners.com | $5M-$30M | LMM | Tech-driven B2B services |

| Tritium Partners | tritiumpartners.com | $20M-$100M | $5M-$75M revenue | Fintech, marketplaces, data analytics, tech-enabled |

| HCAP Partners | hcapfund.com | $3M-$25M | $10M-$100M revenue | Healthcare, software, services, manufacturing (SBIC) |

| Tecum Capital | tecum.com | $5M-$20M | $3M+ EBITDA | Tech services, ERP, IT modernization (SBIC) |

| Cyprium Partners | cyprium.com | $5M-$60M | $4M+ EBITDA | Tech, services, manufacturing (mezz + preferred) |

Tier 1 -- Tech-Focused PE That Co-Invests with Independent Sponsors

These firms actively co-invest in software and tech-services IS deals or operate as software-focused platforms. Each has a verified 2025-2026 track record deploying capital into vertical SaaS, B2B software, and tech-enabled services acquisitions in the lower middle market.

Mainsail Partners

Website: mainsailpartners.com | Fund VII: $1.535B (closed May 2025, oversubscribed) | HQ: San Francisco / Austin

Mainsail Partners closed Fund VII at $1.535 billion in May 2025, the largest fund in its 22-year history with oversubscribed demand, bringing total commitments to approximately $4 billion. The firm invests $10M-$150M in capital-efficient, founder-led B2B software companies with $5M+ ARR. Recent 2025-2026 deals include Pitstop (B2B productivity software, March 25, 2026), Steelhead Technologies Series C in December 2025 (ERP for metal finishing -- crossover tech + manufacturing thesis), and 2025 vertical SaaS platforms FieldFlo and CourtReserve. Mainsail typically takes lead or large minority growth equity positions.

Why it matters for IS: Mainsail's $5M+ ARR floor and capital-efficient founder-led mandate overlaps precisely with the IS sweet spot for vertical SaaS. Their Fund VII scale means they can write the lead equity check and leave room for an IS to retain sourcing and operating partnership on proprietary deals. For an IS bringing a founder-owned vertical SaaS at $5M-$15M ARR with Rule of 40 above 40, Mainsail is a first-call equity co-invest partner.

Serent Capital

Website: serentcapital.com | AUM: ~$6B | HQ: San Francisco / Nashville

Serent Capital manages approximately $6 billion AUM with Fund V closed at $1.1 billion. The firm invests $20M-$200M in B2B software companies with $10M-$50M ARR growing 20-100% annually. Recent 2026 deals include Autire (AI CPA audit software, March 3, 2026) and Coronado Dental (March 18, 2026). Serent takes both growth and buyout equity positions across B2B software verticals.

Why it matters for IS: Serent's dual focus on growth equity and buyout positions makes them flexible for IS sponsors running either a growth-capital thesis or a control buyout of a founder-owned vertical SaaS. The 20-100% growth range they underwrite is realistic for capital-efficient software businesses that do not rely on venture-scale burn -- the exact profile IS sponsors source proprietarily.

Crest Rock Partners

Website: crestrockpartners.com | Fund I: $400M (2020) | HQ: Denver

Crest Rock Partners manages four funds with Fund I at $400M (2020 vintage). The firm writes $25M-$75M checks (up to $100M for the right situation) for LMM control positions across software, tech, and business services. Recent deals include NexForm Technologies / Motus Fiber carve-out (March 2026), Opti9 Technologies' acquisition of Aptible PaaS (November 2025), and Pitcher (sales enablement). Crest Rock takes control equity positions.

Why it matters for IS: Crest Rock's LMM control mandate and blended software + tech-services + business-services focus makes them a natural fit for IS deals that sit at the tech / services boundary -- like ERP consulting platforms, managed hosting roll-ups, or vertical SaaS with professional-services revenue components. Their Denver base gives Midwest and Mountain West deal coverage under-penetrated by coastal software PE firms.

NexPhase Capital

Website: nexphase.com | Fund V: $795M (2024, oversubscribed, +45% vs Fund IV) | HQ: New York

NexPhase Capital closed Fund V at $795M in 2024, oversubscribed and 45% larger than Fund IV. The firm invests across software, consumer, and healthcare with LMM control and growth equity. Recent software deals include Magic Molecule (August 26, 2025), Insurance Systems (ISI) (P&C insurance vertical SaaS), and Aztec Software (education SaaS). NexPhase's software portfolio is concentrated in vertical SaaS with defensible niche positioning.

Why it matters for IS: NexPhase's explicit focus on vertical SaaS with niche positioning (P&C insurance, education, healthcare workflow) overlaps closely with the IS roll-up thesis in vertical-specific software. Fund V's 45% scale-up over Fund IV signals aggressive 2025-2026 deployment appetite. For an IS sourcing a $5M-$15M ARR vertical SaaS in a regulated industry, NexPhase is a credible lead equity co-invest partner.

Banneker Partners

Website: bannekerpartners.com | Fund I: $350M (March 2021) | HQ: San Francisco

Banneker Partners targets vertical enterprise software businesses in mission-critical verticals with 27 companies in the portfolio as of January 2026. The firm invests in companies with $5M-$50M revenue targets and takes both control and significant minority positions. Core sectors include public safety, higher education, life sciences, OT and ICS cybersecurity, and forestry. Recent deals include a strategic growth investment in Industrial Defender (OT/ICS cybersecurity, January 2026), Remsoft's acquisition of INFLOR (forest management vertical SaaS, February 2026), and Versaterm (public safety, added Permira as co-investor in 2025). Banneker explicitly invests in vertical enterprise software.

Why it matters for IS: Banneker's mission-critical vertical focus is one of the deepest in the software PE universe. OT/ICS cybersecurity (Industrial Defender), public safety (Versaterm), and forestry (Remsoft/INFLOR) are the sort of regulated, defensible vertical niches where IS sponsors can source proprietary deals that the generalist software funds never see. For an IS with a background in a specific regulated vertical, Banneker reads deal teasers with genuine sector fluency.

Frontier Growth

Website: frontiergrowth.com | AUM: ~$1.5B | HQ: Charlotte, NC

Frontier Growth manages approximately $1.5 billion AUM with Fund V currently active. The firm is purely vertical SaaS focused, targeting companies with $3M-$20M ARR growing 25%+ and writes $5M-$30M initial checks. Recent activity is extensive: Hauler Hero (February 10, 2026), Albiware Series B (August 2025), the NEOGOV exit to EQT at $3B (July 2025), and the AccessOne exit (September 4, 2025). Frontier Growth takes minority growth equity or buyout positions.

Why it matters for IS: Frontier Growth's pure vertical SaaS mandate and $3M-$20M ARR target is arguably the single closest match to the IS sweet spot in all of software PE. The NEOGOV exit to EQT at $3B and the AccessOne exit in the same year demonstrate active realization and a disciplined buy-and-build playbook. For a vertical SaaS IS deal in the $5M-$15M ARR band, Frontier Growth belongs in every first-call rolodex.

Petra Capital Partners

Website: petracapital.com | Fund V: $270M (January 2025, oversubscribed) | HQ: Nashville

Petra Capital Partners closed Fund V at $270 million in January 2025, oversubscribed. The firm invests up to $25M in equity or debt, focused on growth-stage tech-enabled services and healthtech companies. Recent deals include the Commence rebrand combining DOMA + Livanta + Advanta into an integrated healthcare tech platform (May 2025), RD Nutrition Consultants (February 28, 2026 with Conscious Capital Growth), and Pivot Point Consulting's combination with Innovative Consulting Group (February 17, 2026). Petra provides growth equity, subordinated debt, and preferred stock structures.

Why it matters for IS: Petra's flexible capital structure (equity, sub-debt, or preferred) lets IS sponsors build custom capital stacks on tech-enabled services deals where a pure equity check would over-dilute the sponsor. Nashville is an under-penetrated tech-services hub, and Petra's repeat activity through 2026 demonstrates real active deployment rather than a passive fund in harvest mode.

Align Capital Partners

Website: aligncp.com | Collaborate Fund I: $133M (April 2025, for IS co-invest) | HQ: Cleveland / Dallas

Align Capital Partners closed a $405M single-asset continuation fund for Proceed (tech-enabled legal services) in April 2026 -- one of the largest SAV vehicles in LMM tech-enabled services. More relevant for IS sponsors: Align Collaborate Fund I closed at $133M in April 2025 and is explicitly structured for IS deal-by-deal co-investment. Recent deals include Zcorum (IT Consulting, March 10, 2026), ClearSpeed Series D (June 26, 2025), and the Rewind Restoration platform with LP First Capital as independent sponsor in late 2025. Align takes control equity positions and co-invests with IS through the Collaborate vehicle.

Why it matters for IS: Align Capital's Collaborate Fund is one of the few dedicated pools of LP capital structured explicitly for IS deal-by-deal co-investment in tech-enabled services. For an IS sponsor sourcing a $15M-$40M tech-services deal who wants a capital partner with a committed fund behind them rather than ad-hoc family-office checks, Collaborate is the structural fit. The Rewind Restoration deal with LP First Capital validates the IS partnership model.

Tier 2 -- Sub-Sector Specialists (Tech-Enabled Services)

These firms specialize in tech-enabled services -- the category between pure software PE and generalist business-services PE where IT services, managed services, fintech services, marketplaces, and software-plus-services roll-ups live.

Stone-Goff Partners

Website: stonegoffpartners.com | Portfolio: 18 companies as of January 2026 | HQ: New York / Boston

Stone-Goff Partners focuses on tech-driven B2B service companies with an 18-company portfolio as of January 2026. Implied check sizes run $5M-$30M. Recent deals include Captivate Collective (February 12, 2026), the Walker Sands exit (October 7, 2025), and portfolio companies MojoTech (software engineering services), BigScoots (managed WordPress hosting), and Adar (outsourced IT). Stone-Goff takes control equity positions with management rollover.

Why it matters for IS: Stone-Goff's portfolio reads like a tech-IS target list: outsourced IT (Adar), managed hosting (BigScoots), software engineering services (MojoTech). The firm is one of a handful of LMM PE shops with genuine tech-services fluency rather than a hardware or staffing orientation. For an IS sourcing a $15M-$30M tech-enabled services deal, Stone-Goff's portfolio fit and management-rollover structure make them a credible co-invest or successor equity partner.

Tritium Partners

Website: tritiumpartners.com | Committed capital: ~$1.5B | HQ: Austin

Tritium Partners manages approximately $1.5 billion in committed capital and writes $20M-$100M checks in companies with $5M-$75M revenue. Core sectors include fintech, internet marketplaces, software and data analytics, and tech-enabled B2B services. Recent deals include the Loxo AI-powered recruiting SaaS investment at $115M in February 2025 and the Inova Payroll exit in December 2025. Tritium takes growth equity positions.

Why it matters for IS: Tritium's Austin base gives deep Texas and Southwest tech deal coverage, and their crossover fintech + marketplace + data-analytics mandate makes them a fit for IS deals where the target does not fit neatly in pure SaaS or pure services. The Loxo investment at $115M in 2025 demonstrates active large-check deployment in AI-powered vertical platforms -- directly aligned with the 72%-AI-positioned SaaS M&A backdrop.

Tier 3 -- SBIC / Mezz / Sub-Debt with Tech Allocation

SBICs and mezzanine providers fill the debt side of tech IS capital stacks. With SBA-leveraged capital, SBICs offer more flexible terms than traditional bank lenders -- particularly valuable for software acquisitions where senior lenders cap advance rates on ARR-backed borrowing bases. Three of the most tech-active SBIC and mezzanine capital partners:

HCAP Partners

Website: hcapfund.com | Fund V: $353M (including anticipated SBA leverage, 2021 vintage) | HQ: San Diego

HCAP Partners closed HCAP V at $353 million including anticipated SBA leverage (2021 vintage). The firm invests $3M-$25M in companies with $10M-$100M revenue across healthcare, software, services, and manufacturing. Recent deals include Core Analytics Lab & Radiology (January 13, 2026) and an investment activity announcement (January 4, 2026). HCAP provides mezzanine debt and private equity (non-control) structures.

Why it matters for IS: HCAP's explicit software and services sector focus (alongside healthcare and manufacturing) and $3M minimum check size are well-matched to tech IS deals at the small-to-mid end of the LMM range. Non-control structure preserves IS operating authority. For an IS on a $15M-$25M EV vertical SaaS or MSP deal, HCAP fills the mezz layer cleanly.

Tecum Capital

Website: tecum.com | Fund IV: $325M SBIC fund (February 2025) | HQ: Pittsburgh

Tecum Capital Partners IV launched in February 2025 at $325 million -- the firm's fourth SBIC-licensed fund (Tecum Capital, February 2025). Tecum provides mezzanine debt and minority equity of $5M-$20M in businesses with EBITDA greater than $3M. Tech-sector anchors include Custom Computer Specialists (IT services), Converged Security Solutions (CSS) (data solutions, security, and IT modernization), and Tier1 (ERP consulting, cloud, and managed services). Tecum is a McGuireWoods Independent Sponsor Conference sponsor.

Why it matters for IS: Tecum's tech-services portfolio (CCS, CSS, Tier1) and its explicit McGuireWoods IS sponsorship signal durable commitment to IS deal flow in the tech-services sub-sector. The $3M+ EBITDA target matches the IS sweet spot for MSPs and ERP consulting platforms. For an IS sourcing a $15M-$30M IT-services or managed-services deal, Tecum is a first-call mezz partner with proven sector fluency.

Cyprium Partners

Website: cyprium.com | AUM: $2B invested across 100+ companies since 1998 | HQ: Cleveland

Cyprium Partners has invested $2 billion across more than 100 companies since 1998. The firm provides non-controlling mezzanine debt, preferred stock, and minority equity of $5M-$60M in companies with $4M+ EBITDA (Cyprium Partners). Cyprium's most recent activity includes a Nucara pharmacy/HME investment on April 2, 2026 (very fresh) and the firm's 100th platform OneroRX. Tech is listed as a core sector alongside healthcare, manufacturing, and distribution.

Why it matters for IS: Cyprium's non-control model preserves IS operating authority across a wide $5M-$60M check range -- rare in the mezzanine universe. Their 100+ company track record and explicit tech sector focus make them a flexible capital partner across both small MSP add-ons and larger vertical SaaS platform deals.

Sub-Sector Multiples: How Tech IS Deals Are Priced in 2026

Tech and software multiples vary more than any other IS sector because the category spans pure SaaS, MSPs, MSSPs, IT services, and tech-enabled services -- each with distinct economic profiles. The 2025-2026 ranges we see on Peony data rooms and in published market data:

| Sub-sector | Revenue/ARR multiple | EBITDA multiple |

|---|---|---|

| Lower-mid SaaS ($5M-$50M EV) | 4.5x ARR median | 8-11x EBITDA |

| Vertical SaaS (Rule of 40 >50, NRR >120%) | 7-9x ARR | 15-20x+ EBITDA |

| PE platform SaaS (profitable) | 4-6x revenue | 12-15x EBITDA |

| Horizontal SaaS (undifferentiated) | 2-4x revenue | 6-10x EBITDA |

| MSP platform ($5M+ EBITDA) | -- | 12-14x EBITDA |

| MSP add-on ($1M-$2M EBITDA) | -- | 6-8x EBITDA |

| MSSP (MDR, tech-enabled) | 1-3x revenue | 5-8x EBITDA ($500M+ up to 11.2x) |

| IT Services Q1 2026 median | -- | 9.8x (Software Dev), 10.2x (IT Consulting) |

| Tech-enabled services (LMM) | 2-4x revenue | 6-10x EBITDA |

| Fintech services | 3-6x revenue | 8-13x EBITDA |

| Vertical healthtech software | 4-7x revenue | 10-14x EBITDA |

Roll-up math for MSP platforms: Acquire add-ons at 6x-8x EBITDA, integrate into a scaled platform, exit at 10x-12x EBITDA (or 15x-20x for a premium vertical-software-adjacent platform with genuine ARR underneath). This is the arbitrage that drove PE involvement in 72% of MSP acquisitions in 2025 (Omdia / Solganick) and the 6x-to-12x multiple expansion is the core value creation lever for IS sponsors.

Deferred revenue reconciliation is the single biggest price-chip source in SaaS diligence. According to SaaSCFO and Averi 2026, mismatches between GAAP deferred revenue and the ARR the seller represents are the most frequent working-capital adjustment that kills 5-10% of enterprise value at close. GRR of 90%+ is the healthy benchmark; NRR median compressed to 101% in 2026 from historical levels above 110% (Averi, 2026).

The Alpine / Evergreen Services Group Playbook (The Tech IS Roll-Up Template)

Evergreen Services Group (backed by Alpine Investors) is the single most instructive case study for tech and software independent sponsors in 2026. The data:

- Evergreen closed 47 transactions in 2025, including its 100th MSP milestone and its 10th Australia acquisition (REDD)

- Evergreen now operates across the US, Canada, UK, New Zealand, and Australia

- Three platform operating companies; Lyra Technology Group hit $1B ARR in June 2025

- Target: $5B revenue by 2030

- Platform vs add-on split: over $1M EBITDA = platform, under $1M = add-on

- Alpine has signaled continued aggressive acquisitions in 2026

For an IS sponsor, the Evergreen playbook is the closest thing to a reference architecture in tech roll-ups. Three durable principles:

1. Vertical focus over opportunistic breadth. Evergreen's MSP platforms are not generic tech-services roll-ups -- they are deliberately vertical (industry-specific MSPs, regional MSPs, cybersecurity-specific MSPs). An IS sourcing 3-to-6 add-ons in a single vertical or regional pocket beats one attempting cross-vertical roll-up on day one.

2. Platform economics before add-on velocity. The $1M-EBITDA platform threshold exists because anything smaller cannot absorb the operational infrastructure that makes add-on integration efficient. IS sponsors should close a platform at $2M+ EBITDA before aggressive add-on acquisition.

3. Multi-country expansion when capital is cheap. Evergreen's Australia, New Zealand, Canada, and UK expansion demonstrates that geographic roll-up unlocks deal flow when the US market becomes competitive. For an IS with operating experience in a second English-speaking market, geographic arbitrage is a real 2026 thesis.

IS sponsors cannot replicate Evergreen's scale in a single deal. But the 47-deals-in-2025 cadence validates that tech-services roll-ups are the highest-volume buy-and-build thesis in the lower middle market -- and the mechanics (platform + add-on math, vertical focus, disciplined integration) travel down-market. Our LOI playbook covers the capital-assembly mechanics that make this possible at IS scale.

Tech-Specific Due Diligence Requirements Capital Partners Expect in 2026

Tech and software diligence is structurally different from manufacturing or business services diligence because the assets are intangible (code, IP, customer contracts, engineering talent) and the risks are technical (security posture, open-source licensing, infrastructure dependency). Based on hosting hundreds of tech IS data rooms on Peony, here is what 2026 capital partners expect -- organized for the staged diligence approach in our complete IS guide and IS data room checklist. Set up your data room on day one of the exclusivity window.

SOC 2 Type II and ISO 27001

SOC 2 Type II is the de facto US enterprise vendor standard in 2026. Platform targets are expected to have a current SOC 2 Type II report, or at minimum a Type I report plus a remediation plan to complete Type II within 6-12 months post-close. ISO 27001:2022 has been restructured to 93 controls across four themes (Organizational, People, Physical, Technological) and is increasingly required for EU market access post-NIS2. Getting both SOC 2 Type II and ISO 27001 typically costs $30K-$150K and takes 12-24 months (Konfirmity, Venn). Targets without current audits face a material discount on exit multiple.

Cybersecurity Posture

Capital partners expect a complete cybersecurity package: third-party penetration test results from the last 12 months (external network, internal network, and web application), breach and incident history with disclosure dates and remediation documentation, SIEM and EDR tooling inventory, incident response playbook, and a current vulnerability management program. For MSSP and cybersecurity-adjacent targets, expect deep diligence on MDR offering quality, threat intelligence sources, and customer SLA performance. For targets with OT/ICS exposure (such as Banneker's January 2026 Industrial Defender investment), industrial control system security diligence is an additional layer.

Source Code Escrow and IP Assignments

Source code escrow is increasingly required by enterprise software customers and therefore material to diligence. Capital partners expect not just an escrow agreement but independent verification of deposit contents (Escode, Codekeeper). Agreements without verified deposits offer no actual protection. More critical: IP assignment agreements from every developer -- employees AND external contractors. External consultants and freelancers own their IP by default unless explicitly assigned in writing. Missing or unsigned IP assignments from external contractors are the most frequent M&A red flag in software deals (Travers Smith, 2026). Most founder-owned SaaS companies have this problem and fixing it pre-close requires signed amendments from every historical contractor.

Open-Source Software Bill of Materials

Capital partners expect an open-source SBOM with a full license scan. GPL and AGPL contamination is the most frequent kill-the-deal finding in tech diligence -- AGPL in particular is viral and can force the acquirer to open-source proprietary code that depends on contaminated libraries. Runs via tools like Black Duck, FOSSA, or Snyk should be in the data room before capital partner deep-dive Week 2.

ARR Waterfall and Deferred Revenue Reconciliation

ARR waterfall by vintage with logos named and dollar values disclosed, net revenue retention and gross revenue retention by cohort (ideally 3-year look-back), customer concentration with top 20 logos and contract terms, and a deferred revenue reconciliation to GAAP recognized revenue are non-negotiable. Deferred revenue mismatches are the single biggest source of price chips in SaaS diligence. Capital partners will model NRR against the 2026 101% median benchmark and chip multiples aggressively for any target below 95%.

Customer Contract Assignability

Enterprise software contracts frequently contain change-of-control and anti-assignment clauses that can trigger customer consents or outright termination rights on acquisition. Capital partners expect a complete audit of top-20 customer contracts with change-of-control, anti-assignment, and most-favored-nation clauses highlighted. For roll-up theses, this diligence layer compounds across every add-on.

Engineer Retention and Stay Bonus Pool

Engineer retention has been declining -- 75% of software companies reported declining retention in 2024 (Averi). Capital partners expect a proposed stay bonus pool of 3-5% of deal equity for key engineering talent, structured with cliff and vesting to bridge the first 12-24 months post-close. Targets without retention plans face post-close attrition risk that compresses expected value.

For the complete 174-document due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes all of these tech-specific documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is net revenue retention by cohort?" or "Are there any AGPL-licensed dependencies?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. The AI redaction feature identifies PHI, PII, source-code snippets, and customer names across uploaded documents before you share with capital partners, a workflow that Datasite charges $25K+ per deal to configure manually.

Where to Meet Tech/Software IS Capital Partners in 2026

Tech and software IS outreach has a different rhythm than manufacturing or healthcare. The best sourcing happens at a mix of IS-specific conferences and software-operator-and-founder conferences where targets (not just capital partners) congregate. Events happening AFTER April 20, 2026:

| Event | Date | Location | Organizer |

|---|---|---|---|

| ACG DealMAX (InterGrowth rebrand) | April 27-29, 2026 | Las Vegas | ACG Global |

| SBIA Independent Sponsor Forum | May 6, 2026 | Sheraton Philadelphia Downtown | SBIA |

| SaaStr Annual 2026 | May 12-14, 2026 | San Mateo County, CA | SaaStr |

| iGlobal Independent Sponsor Summit Dallas | June 11, 2026 | Dallas | iGlobal Forum |

| Black Hat USA 2026 | August 1-6, 2026 | Mandalay Bay, Las Vegas | Black Hat |

| iGlobal Independent Sponsor Summit NYC | September 28-29, 2026 | New York | iGlobal Forum |

| McGuireWoods Independent Sponsor Conference | October 27-28, 2026 | Fairmont Dallas (1,600+ attendees) | McGuireWoods |

| iGlobal IS Summit West Coast | October 29-30, 2026 | Los Angeles | iGlobal Forum |

For tech and software IS sponsors specifically, the two highest-leverage events are ACG DealMAX (April 27-29) -- the largest LMM dealmaking conference anchoring Q2 capital partner meetings -- and SaaStr Annual (May 12-14) -- where SaaS founders and operators congregate and proprietary vertical SaaS deals get sourced. Black Hat USA in August is the single best event for MSSP and cybersecurity services sourcing. The McGuireWoods IS Conference in October remains the largest dedicated IS event with 1,600+ attendees.

Axial-platform IS deal flow: Independent sponsors closed 27% of all deals on Axial in 2025. Repeat capital partner relationships account for 59% of IS deals according to Citrin Cooperman 2025. For an IS building a 5-to-10 firm capital partner rolodex focused on tech and software, the fastest path is one software-specialist (Mainsail or Frontier Growth) + one sub-sector specialist (Stone-Goff or Tritium) + one SBIC (HCAP or Tecum) + one flexible-capital partner (Petra or Align Collaborate).

Use Peony's page-level analytics to track which capital partners are reading the ARR waterfall and SOC 2 report versus skimming the CIM. The ones who spend 20+ minutes on the Q of E and cohort NRR are the ones worth second meetings. Use personalized sharing links so every capital partner gets a distinct tracking URL, and NDA gates so nobody sees confidential source-code documentation or customer lists until they sign -- something DocSend cannot detect on any plan.

Tech/Software Independent Sponsor Deals By the Numbers

- 2,698 SaaS transactions in 2025, up 28% YoY -- an all-time high -- with PE buyers at 58% share (Software Equity Group, February 2026)

- Q3 2025: 746 SaaS transactions, a single-quarter record (Software Equity Group)

- Tech sector 2025 deal value: $843.3B, up 67% YoY, 18% of total M&A (Chambers 2026 / Morrison Foerster)

- Q1 2026 tech M&A: $1.2T+ all M&A globally, deal values +26% YoY, January 2026 tech M&A alone at $43.2B (+65% YoY), 22 $10B+ tech deals in the quarter (CNBC, February 2026; FinancialContent, March 2026)

- PE dry powder: approximately $3.7T globally at the start of 2026 (S&P Global, December 2025)

- PE-backed add-on share: 75.9% in Q2 2025, with tech roll-ups as primary driver (PitchBook)

- Q3 2025 vertical SaaS share: 54%, up from 43% YoY (Software Equity Group)

- PE involvement in MSP acquisitions: 72% in 2025 (Omdia / Solganick)

- Top 20 PE-backed MSP platforms control approximately 12% of the US MSP market (up from 6% in 2022) (Omdia)

- AI positioning appeared in 72% of SaaS M&A deals in 2025 (Software Equity Group)

- Evergreen Services Group closed 47 transactions in 2025, 100th MSP milestone, Lyra Technology Group hit $1B ARR in June 2025 (Alpine Investors)

- 54% of IS transactions closed at 4x-6x EBITDA in 2024-2025 (Citrin Cooperman 2025 IS Report)

- 59% of IS capital partner deals come from repeat relationships (Citrin Cooperman 2025)

- Independent sponsors closed 27% of all Axial platform deals in 2025 (Axial)

How Peony Fits the Tech/Software IS Workflow

Peony is a data room platform purpose-built for the exact workflow tech and software IS sponsors run: multiple simultaneous deals during roll-up phases, heavy document diligence (SOC 2, pen test, IP assignments, source escrow, ARR cohorts), and capital partner engagement tracking. Peony Data Room at $52/admin/month is the plan tech IS sponsors use.

AI auto-indexing organizes ARR waterfalls, customer contracts, SOC 2 reports, pen test results, OSS SBOMs, and code escrow agreements into a professional folder structure in under 3 minutes. Junior analysts spend 2-3 hours on this same workflow in Datasite.

Page-level analytics tell you which capital partner spent 30 minutes on the Q of E versus skimmed the CIM, and which one lingered on the deferred revenue reconciliation versus flipped through it. DocSend gives you deck-level views; Peony gives you page-by-page engagement so you know who is genuinely diligencing versus pattern-matching.

Smart Q&A lets counterparties submit diligence questions where AI drafts answers by surfacing the exact document sections and page citations. Your team approves every response before it ships, and every Q&A exchange is audit-trailed. For SaaS diligence where questions like "What is NRR by cohort?" or "Is there any GPL-licensed code in the core product?" come in from every capital partner, this workflow compounds across 3-to-6 simultaneous deals.

AI redaction identifies PHI, PII, source-code snippets, and customer names across uploaded documents before capital partners see them -- a feature Datasite charges $25K+ per deal to configure manually.

Screenshot protection blocks and logs screen-capture attempts on sensitive files. Dynamic watermarks embed viewer identity on every frame of every document, which enterprise software and cybersecurity capital partners require before reviewing architecture diagrams, customer lists, or source-code documentation.

NDA gates require signature before any materials are visible -- DocSend cannot detect this on any plan. AI document extraction lets capital partners ask "What is ARR growth by vintage?" and get a cited answer. E-signatures close the loop after conference introductions -- capital partners sign the NDA and access materials in a single workflow.

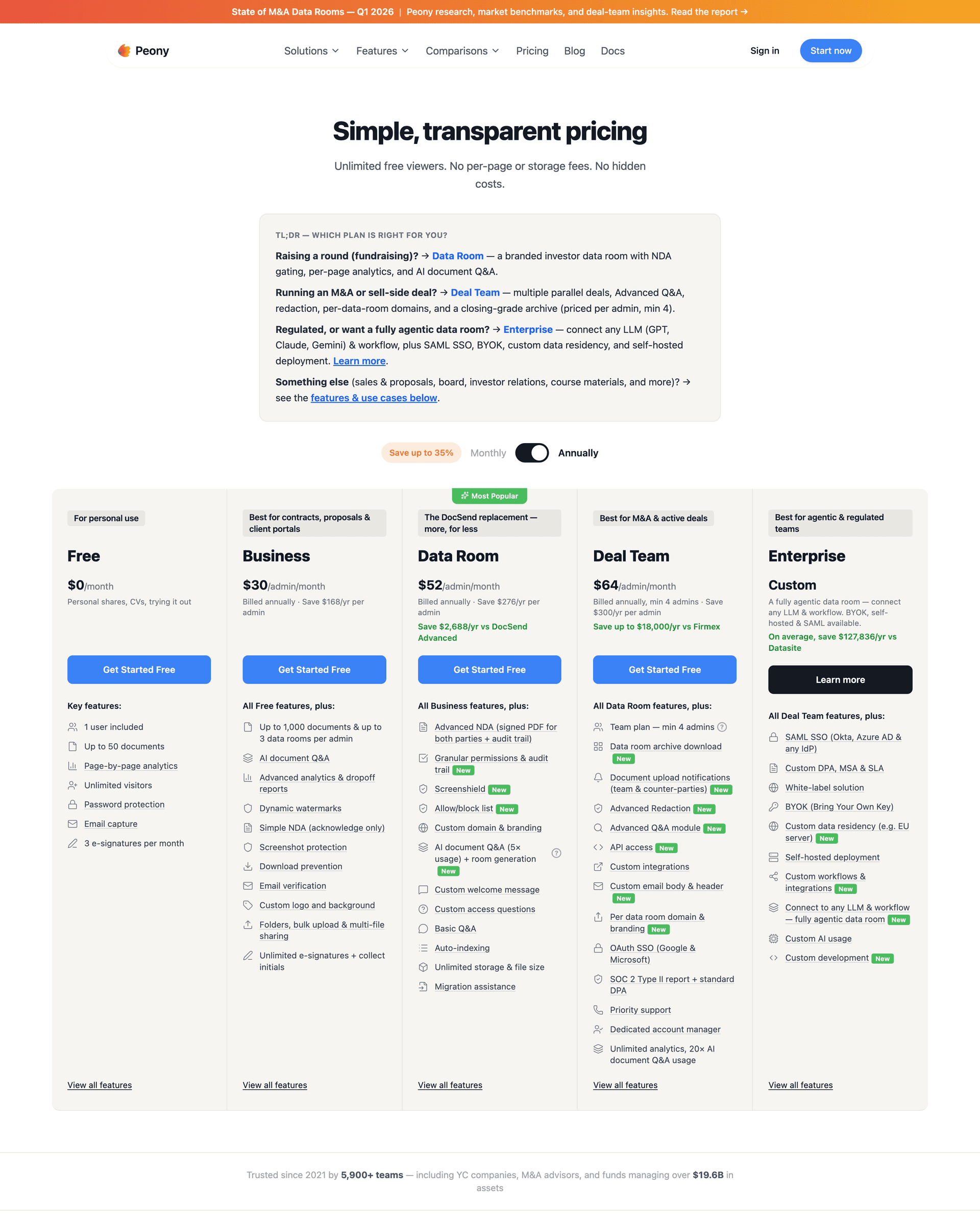

Unlimited data rooms on Peony Data Room mean an IS running 4-to-8 simultaneous deals during a roll-up phase does not pay per-deal licensing. An IS running three tech deals per year pays roughly $624 annually on Peony Data Room versus $45,000-$150,000 on Datasite. The free tier is the entry point; Peony Data Room at $52/admin/month is where serious IS workflows run.

For deeper context on private equity co-investment structures, M&A deal process, due diligence expectations, and fundraising best practices, see our dedicated solutions guides.

Quick Guide: Match Your Situation to the Right Capital Partner

| Situation | Best CP Fit | Why |

|---|---|---|

| First-time IS, $12M EV vertical SaaS, $3M ARR, 30% growth | Frontier Growth + HCAP Partners (mezz) | Frontier's $3M-$20M ARR sweet spot; HCAP's $3M check minimum with software sector focus |

| Experienced IS, $35M EV MSP platform, $4M EBITDA, regional focus | Stone-Goff Partners + Tecum Capital (mezz) | Stone-Goff portfolio (Adar, BigScoots); Tecum's McGuireWoods IS sponsorship + tech-services anchors |

| Operating-partner IS, $50M EV vertical SaaS roll-up, $8M ARR | Mainsail Partners + Align Collaborate (IS co-inv) | Mainsail's $5M+ ARR + Fund VII scale; Align Collaborate dedicated IS co-invest pool |

| First-time IS, $18M EV IT consulting, $3M EBITDA, Southeast | Crest Rock Partners + HCAP Partners | Crest Rock's blended software/services mandate; HCAP's software + services sector focus |

| Experienced IS, $75M EV cybersecurity services roll-up, $10M EBITDA | Banneker Partners + Cyprium (mezz) | Banneker's OT/ICS cyber depth (Industrial Defender); Cyprium's tech sector mezz |

| First-time IS, $22M EV vertical healthtech SaaS, $4M ARR, Rule of 40 above 50 | NexPhase Capital + Petra Capital Partners | NexPhase healthtech + vertical SaaS depth; Petra's healthtech + flexible capital structure |

| Operating-partner IS, $40M EV fintech services, $6M EBITDA, Texas-based | Tritium Partners + Tecum Capital (mezz) | Tritium's Austin base + fintech focus; Tecum tech-services mezz |

| Experienced IS, $100M+ EV MSP platform, $15M+ EBITDA | Serent Capital + Stone-Goff + Cyprium (mezz) | Serent scale; Stone-Goff tech-services fluency; Cyprium's $5M-$60M non-control mezz |

Bottom Line

Tech and software is the fastest-growing IS sector in 2026 because the structural forces are unusually well-aligned: record SaaS M&A volume (2,698 deals in 2025, all-time high), record PE dry powder ($3.7T globally), record add-on share (75.9% in Q2 2025), MSP consolidation driven by 72% PE buyer share, and AI positioning in 72% of deals accelerating multiples. The capital partner ecosystem for tech and software IS deals is wider and more specialized than manufacturing or healthcare, and the firms that show up are genuinely committed to the sector with purpose-built funds and 2025-2026 deployment track records.

If you are targeting vertical SaaS with defensible niche positioning: Mainsail Partners, Frontier Growth, Banneker Partners, and NexPhase Capital are the most active software-specialist equity co-investors. Platform acquisitions at 7x-9x ARR with Rule of 40 above 50 and NRR above 120% remain the premium profile. Deferred revenue reconciliation, cohort NRR, and customer contract assignability are the three diligence kill-switches.

If you are targeting MSP, MSSP, or tech-enabled services roll-ups: Stone-Goff Partners, Tritium Partners, Crest Rock Partners, and Align Capital Partners (via Collaborate Fund) have verified sub-sector deal flow. MSP add-ons at 6x-8x EBITDA exiting as platforms at 10x-12x is the proven arbitrage. Expect SOC 2 Type II, pen test, and customer contract assignability diligence to be mandatory.

If you need mezzanine or subordinated debt: HCAP Partners (Fund V at $353M, software as a core sector), Tecum Capital ($325M Fund IV, McGuireWoods IS sponsor with tech-services anchors), and Cyprium Partners ($2B invested, tech as core sector, non-control mezz + preferred equity) all provide flexible capital structures tailored to tech IS capital stacks. Pair one SBIC with one senior lender -- the debt side of the stack is not the bottleneck in 2026.

For every tech IS deal: Set up your data room on day one of the exclusivity window. Tech diligence is more document-heavy than manufacturing at the information-density level (SOC 2 reports, pen tests, cohort analyses, OSS SBOMs, IP assignments, source escrow, customer contracts) -- but the documents are digital, searchable, and auto-indexable, which means capital partners expect the data room to be organized and complete at Week 1. You cannot afford to lose days to VDR setup. Peony lets you build a complete tech IS data room in under 5 minutes, with page-level analytics that show which capital partners are reading the ARR waterfall versus skimming the CIM, AI-powered Smart Q&A that surfaces hard answers with page citations so capital partners complete diligence faster, and NDA gates that prevent any capital partner from seeing source-code architecture or customer lists before signing.

Peony Data Room at $52/admin/month includes AI auto-indexing, AI-powered Smart Q&A, dynamic watermarks, screenshot protection, NDA gates, page-level analytics, AI document extraction, and e-signatures. An IS running three tech deals per year pays roughly $624 annually versus $45,000-$150,000 on Datasite. When your exclusivity clock is ticking and five capital partners need to get comfortable with the SaaS deal simultaneously, every hour matters.

Set up your first tech or software IS data room -- see plans and pricing.

Frequently Asked Questions

I am a first-time IS with an LOI on a $12M vertical SaaS deal -- which capital partners fund tech/software independent sponsor deals?

Tech and software independent sponsor deals are funded by three capital partner types: software-focused PE firms that co-invest on a deal-by-deal basis such as Mainsail Partners, Serent Capital, Crest Rock Partners, Banneker Partners, NexPhase Capital, Frontier Growth, and Align Capital Partners; growth-equity specialists like Petra Capital Partners and Tritium Partners that take minority positions in tech-enabled services; and SBIC mezzanine providers such as HCAP Partners, Tecum Capital, and Cyprium Partners that fill the debt side of the capital stack. For a first-time IS on a $12M vertical SaaS deal, a $3M-$5M check from an SBIC like HCAP or Tecum plus a minority equity partner like Stone-Goff or Petra is the typical stack. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the ARR waterfall, customer contracts, SOC 2 report, pen test results, and code escrow agreement in under 3 minutes -- so the data room is ready before the first capital partner call.

I run corp dev at a mid-market PE firm -- what EBITDA multiples do tech/software IS deals trade at in 2026?

Tech and software IS deals in 2026 trade across a wide range by sub-sector: lower-mid SaaS platforms in the $5M-$50M enterprise value band trade at 4.5x ARR median and 8x to 11x EBITDA, vertical SaaS with Rule of 40 above 50 and NRR above 120 percent commands 7x to 9x ARR and 15x to 20x EBITDA, horizontal undifferentiated SaaS trades at 2x to 4x revenue and 6x to 10x EBITDA, MSP platform acquisitions with $5M+ EBITDA trade at 12x to 14x EBITDA while MSP add-ons with $1M-$2M EBITDA trade at 6x to 8x, MSSP tech-enabled services run 1x to 3x revenue and 5x to 8x EBITDA, and IT services medians in Q1 2026 hit 9.8x EBITDA for software development and 10.2x for IT consulting. For a corp dev lead evaluating a $25M-$50M vertical SaaS platform, the spread between add-on and platform multiples is the core value creation mechanism. Peony Business includes AI document extraction that lets capital partners ask What is net revenue retention by cohort or What is the ARR waterfall by vintage across uploaded financials and get cited answers with exact page numbers, a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first software IS deal -- why is tech/software growing for independent sponsors in 2026?

Tech and software is growing for independent sponsors because four structural forces converge in 2026: 2025 SaaS M&A posted 2,698 transactions at an all-time high, up 28 percent year-over-year with PE buyers accounting for 58 percent of activity according to Software Equity Group, private equity dry powder sits at approximately $3.7 trillion globally at the start of 2026 with tech-focused PE dry powder sustained at elevated levels, PE was involved in 72 percent of MSP acquisitions in 2025 driving roll-up consolidation where the top 20 PE-backed MSP platforms now control about 12 percent of the US market up from 6 percent in 2022, and Q1 2026 tech M&A hit $43.2 billion in January alone up 65 percent year-over-year with 22 tech deals exceeding $10 billion in the quarter. For a family office allocating $5M-$15M equity to its first software IS deal, focus on founder-led vertical SaaS businesses with $3M-$10M ARR in defensible niches or MSP platforms at $2M-$5M EBITDA in fragmented regional markets. Peony Business at $30 per admin per month includes page-level analytics that show which capital partners spent 30 minutes on the ARR waterfall versus skimmed the CIM, so you can prioritize follow-ups with genuinely engaged partners.

I am a corp dev analyst building my first tech data room -- what documents do capital partners need?

Tech and software capital partners require standard M&A diligence plus software-specific materials: ARR waterfall with logos by vintage, net revenue retention and gross revenue retention cohort analysis, customer concentration with top 20 logos and contract assignability language, deferred revenue reconciliation to GAAP recognized revenue, SOC 2 Type II report or Type I plus remediation plan, third-party penetration test results from the last 12 months, ISO 27001 certification if targeting EU customers, incident response playbook and breach history, open-source software bill of materials with license scan (GPL and AGPL flagged), IP assignment agreements from every employee and external contractor, source code escrow agreement with independent verification of deposit contents, engineer retention data and proposed stay bonus pool, and hosting infrastructure documentation (AWS, Azure, or GCP account structure). For a corp dev analyst running point on a $20M-$40M SaaS deal, these are the documents that kill or close the transaction. Peony Data Room auto-indexing organizes all of these in under 3 minutes into a professional folder structure, and Smart Q and A routes capital partner questions through AI-drafted answers with page citations before your team approves each response.

Our IS targets MSP roll-ups -- which capital partners fit sub-sector specialists?

MSP roll-up independent sponsors benefit from the Evergreen Services Group and Alpine Investors playbook backdrop, where Evergreen closed 47 transactions in 2025 including its 100th MSP milestone and Lyra Technology Group hit $1B ARR in June 2025 with a $5B revenue target by 2030. For IS sponsors imitating this template at smaller scale, the right capital partner mix depends on deal economics. Stone-Goff Partners is active in tech-driven B2B services including outsourced IT platforms like Adar and managed hosting like BigScoots. Tecum Capital is a McGuireWoods IS Conference sponsor with explicit tech-services exposure including Custom Computer Specialists, Converged Security Solutions, and Tier1 ERP consulting. HCAP Partners has Fund V at $353M with software and services as a core sector and check sizes of $3M-$25M. Cyprium Partners provides non-control mezzanine debt and preferred stock for $5M-$60M checks across tech and services. For a specialized IS targeting a $30M-$50M MSP platform with $4M+ EBITDA, the stack typically pairs a tech-services equity lead with SBIC mezzanine. Peony Business at $30 per admin per month includes NDA gates so capital partners sign before any customer list or technical architecture document is visible, and the Data Room plan at $52 per admin per month adds dynamic watermarks with viewer identity embedded in every frame.

Our IS is running three to six tech deals per year -- how much does a data room cost for tech/software IS deals?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 3 to 25 million dollar EBITDA software and tech-services businesses. Tech deals also require extensive technical document uploads, SOC 2 reports, penetration test results, source code escrow agreements, ARR and cohort analyses, customer contracts, and open-source license audits, meaning sponsors often need four to six active data rooms simultaneously during a roll-up phase. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing, AI document extraction, Smart Q and A, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. An IS running three tech deals per year pays roughly 624 dollars annually on Peony Data Room versus 45,000 to 150,000 dollars on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure.

I am a capital-partner PE principal diligencing a vertical SaaS deal -- what sub-sectors have the most IS activity in 2026?

The most active tech and software sub-sectors for independent sponsor deals in 2025-2026 are vertical SaaS which reached 54 percent of all SaaS transactions in Q3 2025 up from 43 percent year-over-year according to Software Equity Group, MSP and managed services roll-ups with 72 percent PE involvement in 2025 and the top 20 platforms controlling about 12 percent of the US market, cybersecurity services and MSSP platforms with multiples expanding on MDR and tech-enabled offerings, tech-enabled B2B services including outsourced IT, software development, and embedded engineering where Q1 2026 medians hit 9.8x to 10.2x EBITDA, fintech services and payments infrastructure, and vertical healthtech software where multiples run 10x to 14x EBITDA. For a capital-partner PE principal diligencing a $30M-$50M vertical SaaS platform, expect deferred revenue reconciliation, NRR cohort analysis, and customer contract assignability to be the three biggest diligence issues. Peony Data Room at 52 dollars per admin per month includes AI-powered Smart Q and A that lets capital partners submit diligence questions where AI surfaces relevant document sections with exact page citations, something DocSend cannot detect on any plan.

I am an M&A attorney advising a first-time IS -- how do tech capital partners expect deal books to be structured?

Tech and software capital partners expect deal books organized in a standard 3-stage diligence flow: Stage 1 initial risk scan including the CIM, ARR waterfall, customer concentration, SOC 2 Type II or Type I report, and preliminary open-source license scan; Stage 2 deep dive with Q of E and deferred revenue reconciliation, third-party penetration test, IP assignment audit covering employees and external contractors, source code escrow with independent deposit verification, cohort NRR and logo retention analysis, and customer contract assignability review; Stage 3 comprehensive validation covering incident response history, full OSS SBOM with GPL and AGPL screening, engineer retention and stay bonus plan, hosting infrastructure and third-party dependency mapping, and 100-day integration plan. For an M&A attorney advising a first-time IS running a $20M enterprise value deal, missing or unsigned IP assignment agreements from external contractors are the most frequent M&A red flag according to Travers Smith 2026. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing that organizes documents into a professional folder structure in under 3 minutes, and personalized sharing links that track each capital partner separately so you know who is engaged before you draft the capital call.

Our IS is running a $35M MSP roll-up -- how do we handle cybersecurity and SOC 2 diligence on a tech target?

MSP and software targets require a disciplined cybersecurity and compliance package in the data room: a current SOC 2 Type II report (or Type I plus a remediation plan to Type II within 6 to 12 months post-close), third-party penetration test results from the last 12 months, breach and incident history with disclosure dates and remediation documentation, SIEM and EDR tooling inventory, incident response playbook, ISO 27001:2022 certification for any targets with EU customers covering the 93 restructured controls across Organizational, People, Physical, and Technological themes, open-source software bill of materials with GPL and AGPL contamination flagged, and source code escrow agreement with independent verification of deposit contents. For an IS running a $35M MSP roll-up, SOC 2 Type II is the de facto US enterprise vendor standard and full certification costs $30K-$150K and takes 12-24 months. If the target is OT or ICS adjacent (as with Banneker's January 2026 Industrial Defender investment), add industrial control system diligence on top. Peony Business at 30 dollars per admin per month includes screenshot protection that blocks and logs screen capture attempts on sensitive files before capital partners see them, and Peony Deal Team adds advanced AI redaction that identifies PHI, PII, source code snippets, and customer data across uploaded documents, a workflow that Datasite charges $25K+ per deal to configure.

I am a first-time IS building a capital partner network -- where do tech/software independent sponsors meet capital partners in 2026?

Tech and software independent sponsors meet capital partners at ACG DealMAX on April 27-29 2026 in Las Vegas (the InterGrowth rebrand anchoring the spring LMM calendar), the SBIA Independent Sponsor Forum on May 6 2026 at the Sheraton Philadelphia Downtown, SaaStr Annual 2026 on May 12-14 in San Mateo County for SaaS founder and operator sourcing, the iGlobal Independent Sponsor Summit Dallas on June 11 2026, Black Hat USA on August 1-6 2026 at Mandalay Bay for cybersecurity and MSP targets, the iGlobal IS Summit NYC on September 28-29 2026, the McGuireWoods Independent Sponsor Conference on October 27-28 2026 at the Fairmont Dallas with 1,600+ attendees, the iGlobal IS Summit West Coast on October 29-30 2026 in Los Angeles, and through platforms like Axial where independent sponsors closed 27 percent of all deals in 2025. Repeat relationships account for 59 percent of capital partner deals according to Citrin Cooperman. For an IS building a 5-to-10 firm capital partner rolodex focused on tech and software, starting with a software-specialist like Mainsail or Frontier Growth plus one SBIC like HCAP or Tecum is the fastest path. Peony Data Room at 52 dollars per admin per month includes NDA-gated data rooms with built-in e-signatures so capital partners can sign and access materials in a single workflow after conference introductions.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- Independent Sponsor Manufacturing Capital Partners -- 12 firms funding manufacturing IS deals

- Independent Sponsor Consumer Capital Partners -- 12 firms funding consumer and CPG IS deals

- Independent Sponsor Distribution & Logistics Capital Partners -- 12 firms funding wholesale, 3PL, cold chain, and specialty distribution IS deals

- Independent Sponsor Cleantech & Energy Capital Partners -- 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Independent Sponsor Healthcare Capital Partners -- 17 firms funding healthcare IS deals

- Independent Sponsor Business Services Capital Partners -- 15 firms funding business services IS deals

- Independent Sponsor Data Room Checklist -- staged diligence checklist by capital partner type

- Independent Sponsor LOI Playbook -- post-LOI capital assembly and exclusivity management

- Independent Sponsor Deal Book -- what capital partners want to see in 2026

- Independent Sponsor Conferences and Forums -- 21 events mapped for IS dealmakers

- Best Data Rooms for Independent Sponsors -- platform comparison for IS workflows

- Due Diligence Data Room Checklist -- 174-document checklist across 10 categories

- M&A Data Room Guide -- M&A-specific data room setup

- Best Data Rooms for Startups -- stage-gated feature priority matrix

- Virtual Data Room Cost Guide -- budget calculator framework by deal profile

- Peony for Private Equity -- PE-specific data room features

- Peony for M&A -- M&A data room solutions

- Peony for Due Diligence -- diligence workflow tools

- Peony for Fundraising -- fundraising data room workflows