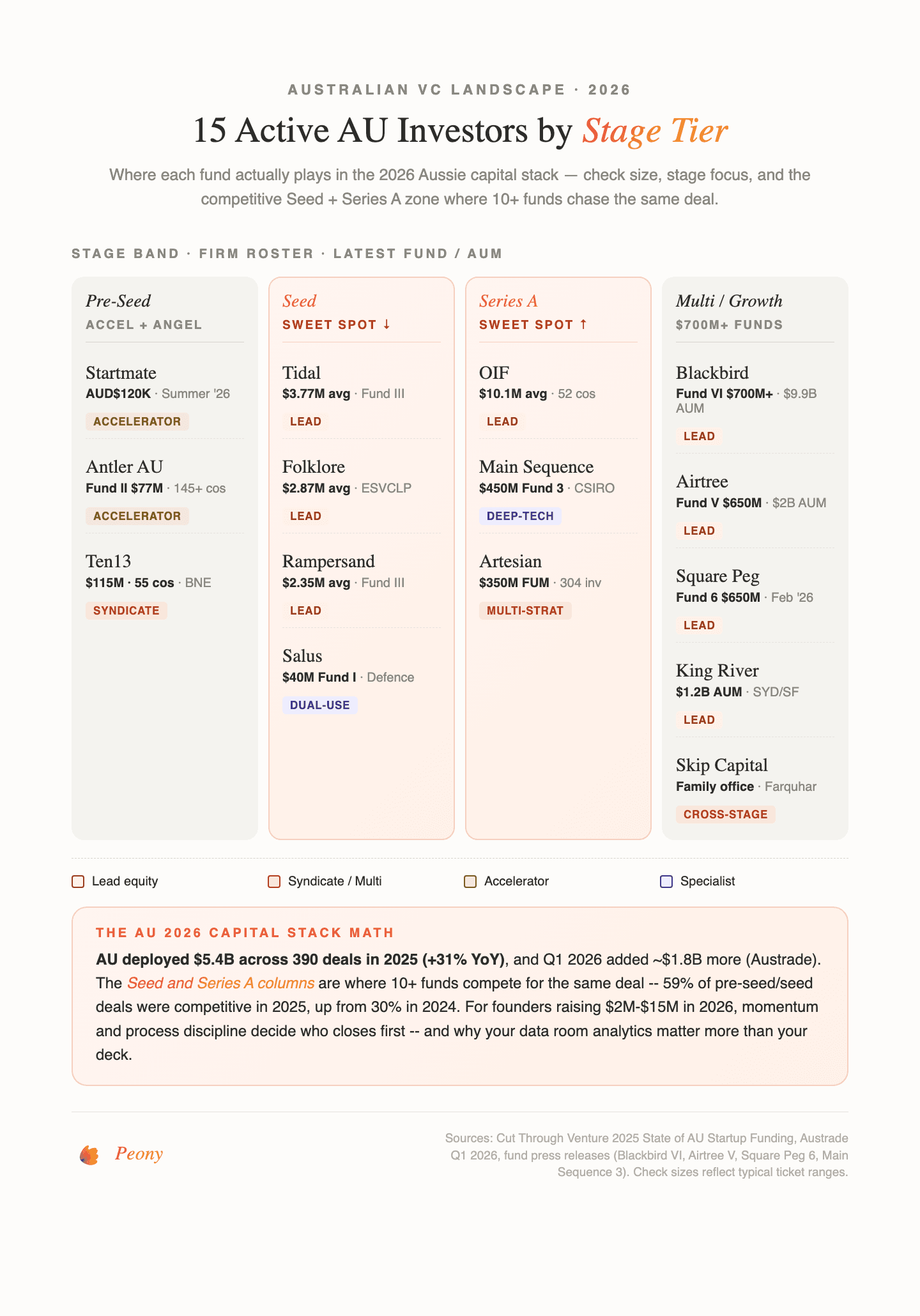

15 Active Australian Investors in 2026 (Check Sizes + Intro Paths)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

TL;DR -- Australian VC in 2026: Firmus closed a $505M raise at ~$5.5B valuation in April 2026 (Aussie AI-data-centre unicorn). Halter closed a $220M Series E in March 2026 with Blackbird participation. Canva hit a $42B valuation in August 2025. Q1 2026 saw ~$1.8B deployed across AU VC per Austrade data. Blackbird's Fund VI first close of $700M+ in August 2025 sets the dry-powder ceiling, Square Peg's Fund 6 plus Opportunities 3 first close of $650M in February 2026 is active, Main Sequence's Fund 3 at $450M did 13 investments in 2025 plus 7 more in Q1 2026, and Airtree's Fund V $650M covers both seed ($250M) and growth ($400M). In 2025, Australia deployed $5.4B across 390 deals (+31% YoY) -- the third-largest year on record -- with AI, fintech, and biotech/medtech topping sector flow. If you are raising in Australia in 2026, the capital is real -- but selectivity is too.

Last updated: April 2026

I spent two years at Backed VC and Target Global watching ANZ rounds close (or stall) across every stage -- from Startmate's AUD$120K cohort cheques up through Blackbird and Square Peg's growth participation in Eucalyptus's $190M round and Airwallex's $498M Series G. Aussie founders underestimate how quickly the ecosystem now moves: Blackbird's Fund VI first close in August 2025, Square Peg's Fund 6 first close in February 2026, Main Sequence's 7 Q1 2026 investments, and Firmus's $505M raise in April 2026 all happened inside 9 months. The founders who raise cleanly always do the same thing -- they build a target list of 12-20 genuinely matched funds, run a tight process, and show up with materials ready.

This guide is for that group. These are the 15 AU investors actually writing checks in 2026 -- covering pre-seed, seed, Series A, growth, and dual-use/defence -- with current fund sizes, typical check bands, 2025-2026 portfolio signals, and how to pitch each one. No filler firms, no inactive funds, no generic "ANZ VCs."

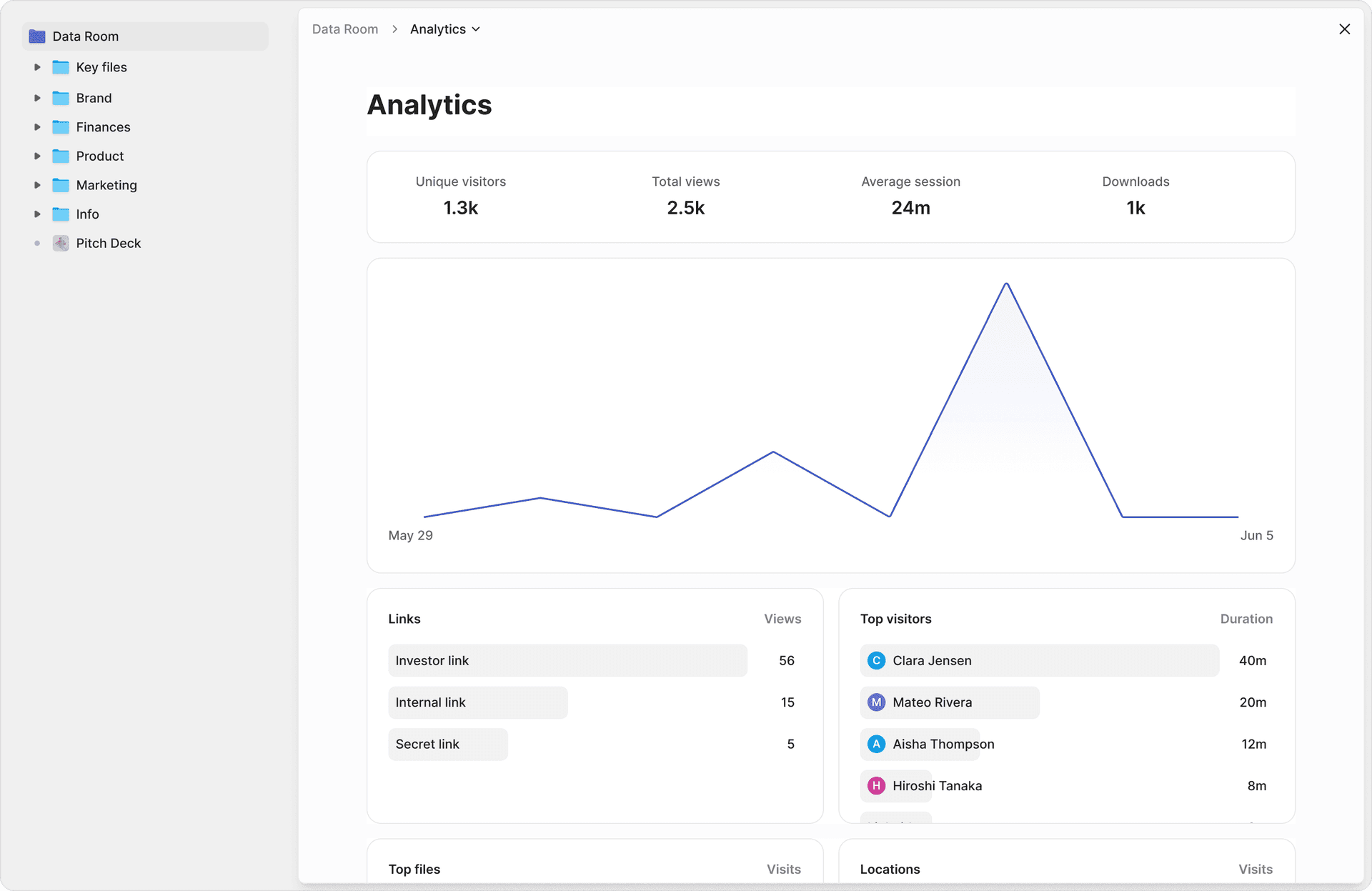

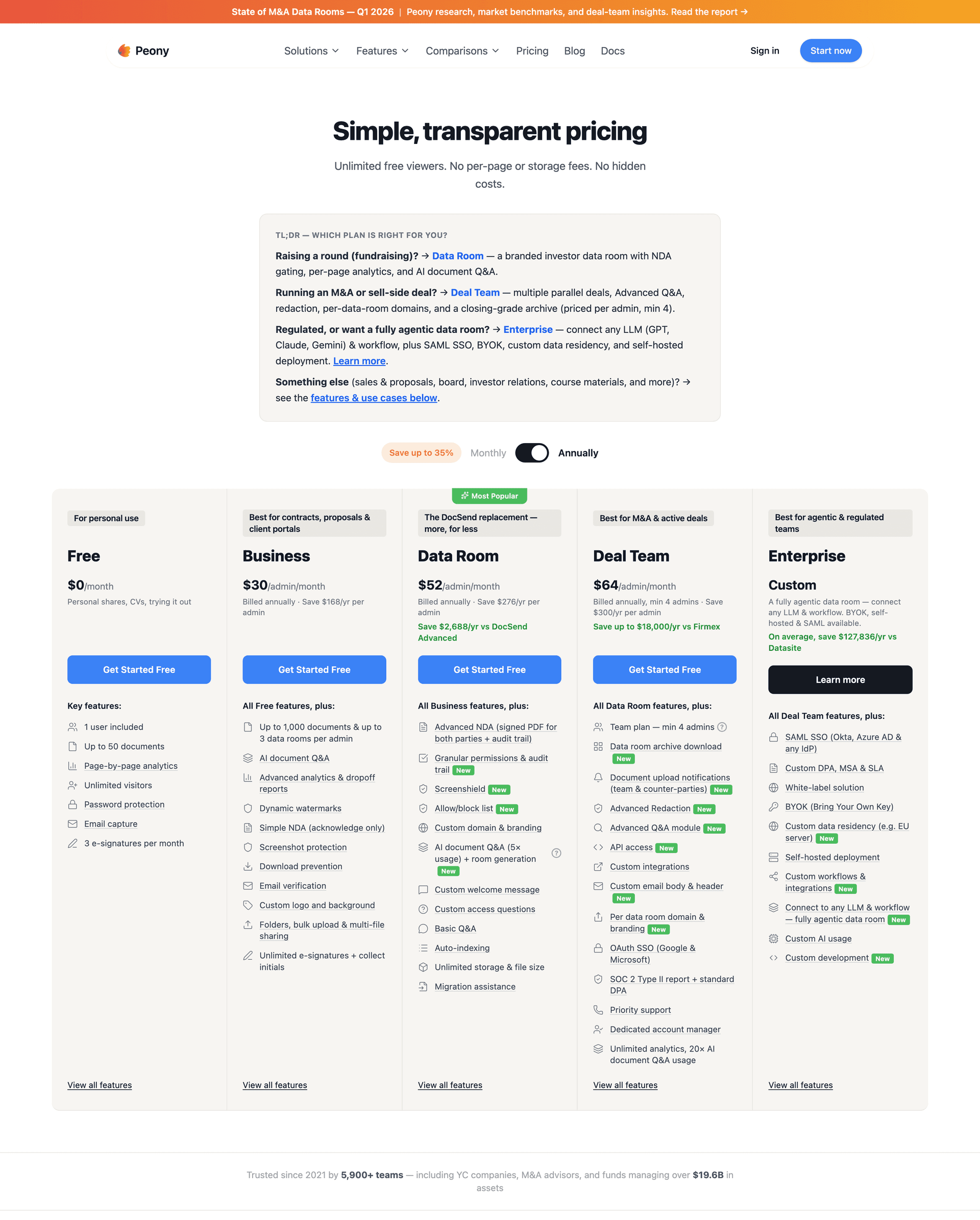

Before you start outreach, have your data room ready. AU seed rounds now close in 4-8 weeks when momentum is real, and Cut Through Venture's 2025 data shows 59% of pre-seed/seed deals were competitive (up from 30% in 2024). That means speed and signal matter. Peony Data Room at $52/admin/month gives you everything an Aussie raise actually needs: NDA gates on every fund link, dynamic watermarks tied to each partner's email, page-level analytics showing which partners read your financials versus skipped them, screenshot protection for sensitive valuation data, AI-powered Q&A that drafts answers with page citations, and AI auto-indexing that organises a Series A room in under 3 minutes. Unlike Datasite or Intralinks which charge $15K-$50K per deal, Peony scales from a simple deck share to a full Series A process without switching platforms.

1. How to pick the right AU VC in 2026

A. Decide what stage you are actually at (be honest)

In Australia in 2026, the stage bands map to:

- Angel + Pre-Seed (AUD $200K-$1.5M): Startmate, Antler, Ten13 syndicate, Tidal Seed Fund III, angel groups

- Seed (AUD $2M-$5M): Folklore, Tidal, OIF, Blackbird seed, Airtree seed ($250M pool), Rampersand, Skip early

- Series A (AUD $5M-$20M): Airtree, Square Peg, Blackbird, Main Sequence, King River, Artesian, Skip

- Series B and beyond (AUD $20M+): Square Peg Opportunities 3, Blackbird Follow-On, Airtree growth ($400M sleeve), Skip, crossover funds

Cut Through Venture reports 2025 median deal sizes: Angel + Pre-Seed $1.0M, Seed $2.5M, Series A $11.0M, Series B+ $30.0M. If your target check does not match an investor's sweet spot, you will fight their IC, which almost never ends well.

B. Match the fund's native habitat

Do not just ask "do they invest in my sector?" Ask:

- Do they win in your business model (SaaS, marketplace, deep tech, fintech, physical AI)?

- Do they have a real edge for you (AI infrastructure, fintech partnerships, CSIRO/research linkage, dual-use)?

- Are they set up to support your geography (Sydney/Melbourne/Brisbane/Perth + trans-Tasman + US expansion)?

C. Pick by sector fit

| Sector | Your strongest 2026 AU fits |

|---|---|

| B2B SaaS / vertical software | Blackbird, Airtree, Square Peg, Folklore, Tidal |

| AI / deep learning infrastructure | Blackbird, Airtree, Main Sequence, King River, Skip |

| Fintech / payments | Square Peg, Airtree, Skip, Ten13, King River |

| Climate / agtech / food tech | Main Sequence, Artesian, Blackbird, Giant Leap (cautious) |

| Medtech / biotech / deep-tech health | Main Sequence, Artesian, Airtree, Blackbird |

| Defence / dual-use / national resilience | Salus, Main Sequence, Blackbird |

| Consumer / marketplace / brand | Airtree, Folklore, Skip, Ten13 |

| Hardware / robotics / physical AI | Main Sequence, Blackbird, OIF |

D. Signal compounds in AU -- get your anchor right

Blackbird, Airtree, Square Peg, and Main Sequence are most often used as anchor credibility for AU rounds. The right anchor can 3x your close rate with follow-on participants and make trans-Tasman or US conversations dramatically easier. Skip's family-office halo (Canva, SafetyCulture, Airwallex co-investor track record) also functions as a strong anchor signal for later-stage rounds.

E. Use a simple scoring rubric

Score each investor 1-5 on:

- Stage fit

- Sector / thesis fit

- Check size + follow-on ability

- Your "unfair advantage" with them (warm intros, shared operators, alumni network)

- Evidence they are active right now (2025-2026 deployments, recent fund closes, visible momentum)

Which AU investor fits your stage/sector? (if/then)

| If you are... | Then your first 3 calls should be... | Why |

|---|---|---|

| A Sydney B2B SaaS founder at seed (AUD $3M) | Blackbird + Airtree + Folklore | Active seed leads with Series A follow-on ability |

| A Melbourne climate-tech founder at Series A (AUD $10M) | Main Sequence + Artesian + Blackbird | Deep-tech anchor + climate thesis + growth reach |

| A Sydney AI founder raising Series A | Blackbird + Airtree + Square Peg | Three highest-visibility AI allocators in AU |

| A Brisbane medtech founder at seed (AUD $4M) | Main Sequence + Artesian + Ten13 | CSIRO linkage + medtech thematic + Brisbane syndicate |

| A Sydney fintech founder at Series A post-Airwallex | Square Peg + Airtree + Skip | Airwallex-trained fintech muscle memory |

| A Perth or Adelaide founder with national ambition | Blackbird + Main Sequence + Artesian | Geography-agnostic AU allocators |

| A trans-Tasman founder (AU + NZ) | Blackbird + Airtree + (NZ: Icehouse or Pacific Channel) | Dedicated trans-Tasman mandates |

| A Sydney defence/dual-use founder | Salus + Main Sequence + Blackbird | Purpose-built defence VC + CSIRO dual-use |

| A solo pre-seed founder pre-team | Antler + Startmate | Co-founder matching + accelerator path |

| A post-Startmate founder raising $1.5M pre-seed | Blackbird (follow-on) + Airtree + Tidal | Graduation pattern with Blackbird LP stake |

2. The 15 AU investors actually writing checks in 2026

1. Blackbird Ventures (Sydney) -- the category-defining ANZ fund

Why they matter: Blackbird is the single most consequential ANZ fund in 2026. They closed Fund VI first close at $700M+ in August 2025 (the largest early-stage AU fund raised to date), with Future Fund, AustralianSuper, Hostplus, HESTA, and Aware Super as cornerstone LPs. Their portfolio is worth roughly USD$9.9B with a net IRR of 36.09% across all funds.

2025-2026 signal: Did 6 deals in Q1 2026, participated in Halter's $220M Series E in March 2026, backed Eucalyptus's $190M round in November 2025, and backed Kimia in early 2026. 51 investments in 2025 from 1,900 applications and 423 meetings.

Check size: Pre-seed to Series A/B via main fund; growth participation via Follow-On Fund. Typical entry $500K-$15M.

Best for: Wild Hearts -- founders attacking massive categories with speed and conviction. AU unicorn pipeline companies (Canva, SafetyCulture, Zoox alumni) came through Blackbird first.

How to approach: Warm intro via portfolio founders or Startmate. Blackbird runs Sunrise conferences and visible Twitter/LinkedIn surfaces -- partners answer cold inbound when the wedge is sharp.

Peony callout: Use Peony Data Room AI auto-indexing to organise Blackbird's diligence request into a professional folder structure in under 3 minutes -- versus the days it takes to manually structure a Dropbox folder.

2. Airtree Ventures (Sydney) -- the B2B-heavy ANZ heavyweight

Why they matter: Airtree runs Fund V at $650M split between a $250M seed fund and $400M growth fund -- structurally built for founders who want one partner from seed through Series B. Portfolio includes Canva (as co-investors), Culture Amp, Employment Hero, Linktree, and Go1.

2025-2026 signal: Led Eucalyptus's $190M growth round in November 2025, led Human Health in October 2025, did 3 deals in Q1 2026. Partners active at Sunrise and Antler events.

Check size: Seed $1M-$5M, Series A/B $5M-$25M.

Best for: B2B SaaS founders with global ambition from day one and a repeatable pipeline motion. Airtree wants operators with real customer conviction, not theoretical markets.

How to approach: Warm intro via portfolio CEO or Airtree partner content (they publish deep thematic posts). Fastest path is a 2-paragraph memo with traction numbers, not a 20-slide deck.

Peony callout: Page-level analytics show you which Airtree partner spent 30 minutes on your Q-of-E model versus 90 seconds on the team slide -- the signal you need to time follow-ups, something DocSend caps on lower tiers.

3. Square Peg Capital (Sydney/Melbourne) -- the fintech-capable Series A lead

Why they matter: Square Peg closed Fund 6 plus Opportunities 3 first close at $650M in February 2026. They led Airwallex's Series F at $232M in May 2025 at $6.2B and participated in the Series G at $498M in late 2025 at $12B. Track record includes Canva, Tyro, Fiverr, and Rokt. Offices in Sydney, Melbourne, Singapore, and Tel Aviv.

2025-2026 signal: Highly visible in fintech and AI. Opportunities 3 is specifically designed for follow-on into existing portfolio breakouts.

Check size: Series A $5M-$15M initial, Opportunities fund $15M-$50M growth checks.

Best for: Fintech, B2B SaaS, and applied AI founders with enterprise traction and international ambition. Their fintech muscle memory is unmatched in AU -- post-Airwallex, they are the default fintech Series A lead.

How to approach: Warm intro is strongly preferred. Partners speak at SXSW Sydney and Sunrise. Opportunities fund access is usually reserved for existing Square Peg portfolio follow-on.

Peony callout: NDA gates on every share link let you send Square Peg a different access level than co-investors in the same round -- per-fund access control Dropbox cannot provide.

4. Main Sequence Ventures (Sydney) -- the CSIRO-linked deep-tech anchor

Why they matter: Main Sequence is the CSIRO-linked deep-tech VC covering agri-food, industrials, space, quantum, and health. Fund 3 is $450M, making it one of the largest dedicated deep-tech funds in APAC. Portfolio includes Samsara Eco (enzymatic plastic recycling), Q-CTRL (quantum control), Advanced Navigation, Loam Bio, and v2food.

2025-2026 signal: Did 13 investments in 2025 plus 7 in Q1 2026. Participated in Advanced Navigation on March 17, 2026. Their 2025 pace made them one of the most active deep-tech allocators globally.

Check size: Seed to Series B, typical $2M-$20M.

Best for: Deep-tech founders with CSIRO or university commercialisation linkage, strong IP, and a de-risking plan tied to clear milestones. Climate, agri, space, quantum, and health are their native habitats.

How to approach: CSIRO ON program is the internal pipeline. External intros via university TTOs, Main Sequence Summits, and portfolio CEO references.

Peony callout: AI redaction auto-flags ITAR-sensitive content, unredacted patient data, and proprietary technical specs in your technical appendix before Main Sequence partners see it -- a capability Google Drive has zero support for.

5. Folklore Ventures (Sydney) -- "first cheque to forever" seed lead

Why they matter: Folklore is a Sydney-based seed specialist with a "first cheque to forever" positioning -- meaning they commit to follow-on through a company's life. Seed average $2.87M, Series A average $14.2M. Portfolio includes Linktree, Mr Yum (exit), Phocas, and Deputy.

2025-2026 signal: Led Hullbot's $16M Series A in November 2025. Consistent Q1 2026 deployment though specific deals less publicly visible than Blackbird/Airtree.

Check size: Seed $1.5M-$4M, follow-on through Series B+.

Best for: Founders who want one committed lead rather than a syndicate and who value long-term relationship over rolling term-sheet optionality.

How to approach: Warm intros through portfolio CEO references. Partners are direct communicators -- a 3-sentence memo plus clean metrics gets a fast yes-or-no.

Peony callout: Dynamic watermarks tie every page view to the specific investor who opened it -- if a Folklore partner forwards your financial model to a co-investor, the forwarded copy carries the original partner's name, which Dropbox simply cannot do.

6. OIF Ventures (Sydney) -- Opportunity Fund for technical founders

Why they matter: OIF Ventures is a Sydney-based early-stage VC with an Opportunity Fund of $55M launched in 2024 and 52 portfolio companies at time of writing. Strong on technical founders and deep software.

2025-2026 signal: Led Starboard Maritime Systems Series A of USD$13.6M in September 2025 and backed Omniscient on January 16, 2026. Active across technical verticals.

Check size: Seed $1M-$3M, Series A participation $3M-$8M.

Best for: Technical founders in maritime, defence-adjacent, and deep B2B software where a generalist fund would not have pattern recognition.

How to approach: Warm intro via Sydney tech ecosystem or portfolio CEOs.

Peony callout: Smart Q&A drafts investor answers with page citations automatically -- so when OIF sends you 40 diligence questions on your technical architecture, Peony generates first-draft answers tied to your uploaded docs, a workflow Datasite charges $15K+ per deal for.

7. Tidal Ventures (Sydney/NY) -- cross-border seed operator

Why they matter: Tidal Ventures runs Tidal Seed Fund III (launched 2023) and has 32 portfolio companies with seed average $3.77M. Dual-HQ Sydney and New York gives them credible cross-Pacific reach.

2025-2026 signal: Backed Vinyl in 2025, Start My Tomorrow in 2026, and Operata in 2026. Consistent seed deployment.

Check size: Seed $1M-$4M.

Best for: Founders planning a US expansion and wanting a seed lead with pattern recognition on the Sydney-to-NYC path. Tidal's NY presence opens US customer and follow-on doors.

How to approach: Warm intro via Sydney ecosystem or US operators in their network.

Peony callout: Screenshot protection blocks AND logs capture attempts on your pitch deck -- essential when Tidal partners review sensitive material across Sydney and NY offices, a capability DocSend flat-out lacks.

8. Ten13 (Brisbane) -- the syndicate powerhouse

Why they matter: Ten13 is a Brisbane-based syndicate platform with 550+ members who have collectively deployed $115M across 55 companies. Syndicate model gives founders access to operator capital faster than a traditional VC process.

2025-2026 signal: Participated in AutoGrab's $80M round in early 2026, backed Atrium's pre-seed in 2026. Track record includes Go1, Clipchamp (acquired by Microsoft), and Mr Yum (exit).

Check size: Syndicate rounds $500K-$5M aggregate.

Best for: Brisbane-founded or regionally distributed founders who want syndicate velocity plus operator mentorship. Ten13 is especially strong for early B2B SaaS, marketplaces, and fintech.

How to approach: Apply via ten13.vc or warm intro through portfolio CEO references. Brisbane's regional ecosystem is tight -- intros compound fast.

Peony callout: Page-level analytics show you which of Ten13's 550 members actually opened your deck versus skimmed it -- so you know which angels to prioritise for follow-up, something Google Drive cannot detect.

9. Rampersand (Melbourne) -- operator-led Melbourne seed

Why they matter: Rampersand is a Melbourne-based seed fund with Fund III deploying now. Operator-led team with deep Melbourne ecosystem density. Portfolio has included Mr Yum, Tixel, and Relevance AI.

2025-2026 signal: Backed Cuttable follow-on on March 24, 2026 and led Keeyu's $2.3M pre-seed in 2026. Seed average $2.35M.

Check size: Seed $1M-$3M.

Best for: Melbourne-based founders or any AU founder who wants hands-on operator mentorship rather than a hands-off check. Rampersand partners take board seats and engage with weekly cadence.

How to approach: Warm intro via Melbourne ecosystem (YBF, SXSW Sydney, Startmate Melbourne cohort).

Peony callout: Auto-indexing organises your full data room in under 3 minutes -- so when Rampersand asks for the usual seed diligence set (deck, model, cap table, incorporation, customer contracts), you share a clean folder structure, not a Dropbox mess.

10. Artesian VC (Sydney) -- multi-thematic $350M FUM specialist

Why they matter: Artesian is a Sydney-based multi-thematic VC with $350M FUM across 304 investments. Distinct sleeves for agri-food, medtech, clean energy, female-founder, and generalist strategies. High portfolio density gives them cross-sector pattern recognition.

2025-2026 signal: Backed Coherence in November 2025. Active across all sleeves.

Check size: Variable by sleeve, typically $500K-$3M at seed with follow-on capacity.

Best for: Founders whose sector aligns with one of Artesian's specific sleeves (agri-food, medtech, clean energy, female-led). Harder fit for pure software plays where Blackbird, Airtree, or Square Peg have stronger brand pull.

How to approach: Apply via artesianvc.com or warm intro via Sydney/Melbourne ecosystem.

Peony callout: NDA gates let you gate medtech clinical-trial data behind a tighter NDA than general fundraising materials -- per-document NDA layering Dropbox fundamentally cannot provide.

11. King River Capital (Sydney/SF) -- $1.2B AUM cross-Pacific generalist

Why they matter: King River Capital is a Sydney/SF cross-border VC with $1.2B AUM covering Series A through growth. Long track record in enterprise software, fintech, and maritime tech.

2025-2026 signal: Led Starboard Maritime Series A in September 2025 (co-with OIF) and backed Block Earner on February 9, 2026.

Check size: Series A $3M-$10M, growth participation $10M-$25M.

Best for: Later-seed and Series A founders planning US expansion who want a cross-Pacific lead with real West Coast operator reach. King River's SF office opens US customer doors.

How to approach: Warm intro via portfolio CEOs or the US/AU cross-border operator network.

Peony callout: Dynamic watermarks embedded with each viewer's email are essential when King River partners share your material across Sydney and SF offices -- capability DocSend caps on lower tiers.

12. Skip Capital (Sydney) -- Kim Jackson + Scott Farquhar family office

Why they matter: Skip Capital is the Sydney family office of Kim Jackson and Scott Farquhar (Atlassian co-founder). Track record includes Canva, SafetyCulture, and Airwallex co-investor status. Family-office structure means patient capital with no LP timing pressure.

2025-2026 signal: Backed Visibuild's $6.6M in December 2024, Lorikeet's $9M extension in February 2025, and Adora on February 11, 2026.

Check size: Highly variable -- $500K angel cheques up to $10M+ follow-on in mature breakouts.

Best for: Founders who already have an institutional lead and want family-office ballast with long-term alignment. Skip adds signal without the process overhead of a new fund.

How to approach: Typically accessed via co-investor introductions (Blackbird, Airtree, or Square Peg portfolio founders). Skip does not run a standardised application process.

Peony callout: E-signatures with AI field detection speed up SAFE and convertible note execution -- so when Skip commits, you close in days not weeks, a workflow Datasite charges per-deal for.

13. Salus Ventures (Sydney) -- purpose-built defence + dual-use VC

Why they matter: Salus Ventures is Australia's purpose-built defence and national-resilience VC. Fund I is $40M with plans to deploy $250M+ over 5 years as AUKUS tailwinds and the 2024 Defence Strategic Review mobilise super-fund allocations into dual-use.

2025-2026 signal: Led ExoFlare's $5.3M round with In-Q-Tel co-investing (rare CIA-backed co-invest signal for an AU round) and backed Gega Elements on October 27, 2025.

Check size: Seed to Series A, typical $1M-$5M.

Best for: Defence, dual-use, national-resilience, sovereign capability, maritime autonomy, critical minerals, and space founders. Their In-Q-Tel co-invest opens US DoD and intelligence-community customer doors.

How to approach: Warm intro via defence industry networks (AIDN, Defence Connect, Australian Defence Export Office) or portfolio CEO references.

Peony callout: AI redaction auto-flags ITAR-sensitive content, export-controlled tech specs, and classified-adjacent material before external sharing -- a workflow Google Drive has zero capability for.

14. Startmate (Sydney) -- Blackbird-backed accelerator

Why they matter: Startmate is Australia's leading accelerator, backed by Blackbird and running twice-yearly cohorts with standard AUD$120K per company. Summer '26 cohort = 19 companies / 42 founders. Demo Day is April 30, 2026 at Carriageworks in Sydney.

2025-2026 signal: Consistent cohort quality. Graduates automatically get warm intros to Blackbird, Airtree, Tidal, Folklore, and Ten13 -- the accelerator-to-VC pipeline is the tightest in ANZ.

Check size: AUD$120K standard cheque, pro-rata rights on follow-on rounds.

Best for: Pre-seed founders (2-5 person teams, pre-product to early traction) who want a programmatic path into the Aussie VC ecosystem with Blackbird LP backing.

How to approach: Apply via startmate.com for each cohort. Mentor network intros help application quality.

Peony callout: Auto-indexing + page-level analytics give Startmate alumni an investor-grade data room from day one of Demo Day -- so Blackbird and Airtree partners land on a polished folder structure, not a Dropbox with 47 unnamed files.

15. Antler Australia (Sydney + Brisbane) -- pre-team co-founder matching

Why they matter: Antler Australia runs Fund II at $77M (2025) with a Queensland program launched in February 2025 and has backed 145+ AU startups across 12 cohorts. Unique model: they match co-founders inside the cohort, then write the first cheque post-matching.

2025-2026 signal: 12th cohort picks include Huddled, Fitflo, Balo, and others. Active in Sydney and Brisbane with occasional Melbourne overlap.

Check size: Standard pre-seed cheque per program terms (typically $150K-$300K for ~15% equity), follow-on to $1M+ for top cohort graduates.

Best for: Solo founders, pre-team founders, or repeat founders who want a structured co-founder matching environment plus guaranteed cheque on the other side. Antler's global cohort network (Singapore, London, Stockholm) also creates cross-border optionality.

How to approach: Apply via antler.co for each cohort. Brisbane and Sydney cohorts run separately.

Peony callout: Post-Antler Demo Day, graduates move to a Peony Business data room for the next $500K-$1.5M raise -- page-level analytics from the first pitch meeting, with dynamic watermarks on the Data Room plan ($52/admin/month), a signal Airtree and Blackbird partners notice.

3. Quick reference: AU VC table 2026

| Firm | HQ | Fund size | Check size | Stage | Sector focus |

|---|---|---|---|---|---|

| Blackbird Ventures | Sydney | $700M+ Fund VI first close (Aug 2025) | $500K-$15M | Pre-seed to Series B | Generalist, AI, deep tech |

| Airtree Ventures | Sydney | $650M Fund V ($250M seed + $400M growth) | $1M-$25M | Seed to Series B | B2B SaaS, consumer, fintech |

| Square Peg Capital | Sydney/Melbourne | $650M Fund 6 + Opps 3 (Feb 2026) | $5M-$50M | Series A to growth | Fintech, AI, B2B SaaS |

| Main Sequence Ventures | Sydney | $450M Fund 3 | $2M-$20M | Seed to Series B | Deep tech, CSIRO, climate |

| Folklore Ventures | Sydney | Seed specialist | $1.5M-$4M seed | Seed to Series A follow-on | B2B SaaS, marketplaces |

| OIF Ventures | Sydney | $55M Opportunity Fund | $1M-$8M | Seed to Series A | Technical founders, maritime |

| Tidal Ventures | Sydney/NY | Tidal Seed III | $1M-$4M | Seed | Cross-border SaaS, consumer |

| Ten13 | Brisbane | $115M deployed across 55 cos | $500K-$5M syndicate | Pre-seed to Series A | Syndicate generalist |

| Rampersand | Melbourne | Fund III | $1M-$3M | Seed | Melbourne-native, SaaS |

| Artesian VC | Sydney | $350M FUM, 304 investments | $500K-$3M | Seed to Series A | Agri-food, medtech, clean energy |

| King River Capital | Sydney/SF | $1.2B AUM | $3M-$25M | Series A to growth | Enterprise, fintech, maritime |

| Skip Capital | Sydney | Family office | $500K-$10M+ | Angel to growth | Generalist, follow-on |

| Salus Ventures | Sydney | $40M Fund I ($250M+ over 5yrs) | $1M-$5M | Seed to Series A | Defence, dual-use, sovereign |

| Startmate | Sydney | Blackbird-backed accelerator | AUD$120K standard | Pre-seed | Generalist cohort |

| Antler Australia | Sydney + Brisbane | $77M Fund II (2025) | $150K-$1M | Pre-seed | Generalist, pre-team |

4. How to approach AU VCs in 2026

A. Warm intros compound

Australia's VC ecosystem concentrates in Sydney and Melbourne. Partners at Blackbird, Airtree, Square Peg, and Main Sequence know each other, share notes, and attend the same events (Sunrise, SXSW Sydney, Startmate Demo Day). A bad first meeting at Blackbird can cool interest at Airtree within a week. Budget for warm intros via portfolio founders, Startmate mentor network, Antler alumni, or shared LPs.

B. Process speed matters in 2026

Cut Through Venture's 2025 data shows 59% of pre-seed/seed deals were competitive, up from 30% in 2024. That means multi-fund processes are the norm, and speed is now a founder signal. Seed rounds close in 4-8 weeks from first meeting for well-prepared teams. Series A stretches 8-16 weeks because of heavier diligence.

C. Trans-Tasman tips

If you are running an ANZ round covering Australia and New Zealand:

- Blackbird's dedicated NZ$75M NZ fund is the default trans-Tasman bridge

- Airtree invests across ANZ with no geographic mandate

- Pacific Channel's Australian Fund IV (launched 2025) is the NZ-side bridge into AU

- Icehouse Ventures (NZ$70M Seed Fund IV) has 17 international LPs including Australian participation

- See our NZ investors guide for the full trans-Tasman playbook

D. Super-fund tailwinds

AustralianSuper, Hostplus, HESTA, Aware Super, Telstra Super, NGS, and Future Fund are now cornerstone LPs in Blackbird Fund V and VI. APRA changes now permit up to 2% of default super portfolios in PE/VC -- a structural tailwind that means AU dry powder is rising, not falling, through 2026-2027.

E. Five quick tips for pitching AU VCs in 2026 (that actually work)

-

Lead with the round math. "Raising AUD $X on Y terms, already committed AUD $Z, using it for A/B/C milestones by Month N." AU partners appreciate crisp asks.

-

Make global ambition the default narrative. Even at seed: show your first wedge outside Australia OR show product built for global distribution from day one. AU's 26M home market does not sustain a venture-scale outcome on its own.

-

Cite 2025-2026 comparables specific to your sector.

- AI: Firmus $505M April 2026, Canva $42B August 2025

- Fintech: Airwallex Series G $498M at $12B late 2025

- Climate/agri: Halter $220M Series E March 2026

- Deep tech: Samsara Eco, Q-CTRL, Advanced Navigation

-

Name the specific partner thesis you match. The fastest "yes" is when the investor feels: "this is exactly what we are built to back." Blackbird wants Wild Hearts. Airtree wants B2B SaaS with global category potential. Main Sequence wants deep tech with CSIRO or university linkage. Square Peg wants fintech or AI with enterprise traction.

-

Treat intros like product distribution. Do not ask "for an intro to the firm." Ask for: a specific partner + a specific reason + a specific timing window. Make it easy for the intro-giver to forward your 3-sentence blurb.

5. AU market by the numbers (2025-2026)

From Cut Through Venture's 2025 State of Australian Startup Funding report plus Austrade Q1 2026 data:

- $5.4B deployed across 390 deals in 2025 -- up 31% YoY, the third-largest year on record for AU VC

- Q4 2025 alone saw $2B+ deployed (Airwallex's $498M Series G was a single-deal driver)

- Q1 2026 tracked ~$1.8B per Austrade preliminary data -- momentum continues

- 2025 median deal sizes: Angel + Pre-Seed $1.0M, Seed $2.5M, Series A $11.0M, Series B+ $30.0M

- 59% of pre-seed and seed deals were competitive in 2025 -- up from 30% in 2024, meaning multi-fund processes are now standard

- One new unicorn minted in 2025: Firmus (AI data centres) -- which then raised $505M in April 2026 at ~$5.5B

- Top 2025 sectors by funding: AI at $1.0B, Fintech at $868M, Biotech/Medtech at $829M

- Super-fund structural tailwind: APRA now permits up to 2% of default super portfolios in PE/VC, with AustralianSuper, Hostplus, HESTA, Aware Super, Telstra Super, NGS, and Future Fund backing Blackbird Fund V and Fund VI

The 2025-2026 signals all point to the same conclusion: AU founders no longer need to move to the US to raise institutional capital. Blackbird's Fund VI, Square Peg's Fund 6, Main Sequence's Fund 3, Airtree's Fund V, and rising super-fund allocations create enough dry powder to fund AU's Series A through C in-country through 2027.

Why professional data rooms matter for AU fundraising

Australia's VC ecosystem is tight-knit, high-signal, and increasingly competitive. Partners at Blackbird, Airtree, Square Peg, Main Sequence, and Skip share notes. Deal flow moves through Sunrise, SXSW Sydney, Startmate, Antler Demo Days, and tight WhatsApp groups. How you present your materials in the first meeting sets the ceiling for the entire process.

Peony helps AU founders create investor-ready data rooms in minutes. AI auto-indexing organises your cap table, financial model, customer contracts, technical documentation, and IP into a professional folder structure that reads the same to a Blackbird partner as it does to a Square Peg growth-fund lead or a US co-investor at Sequoia.

Key capabilities:

- Page-level analytics show which documents each investor read and for how long -- so you know who is genuinely engaged across your 15-VC outreach list

- Dynamic watermarks embed each viewer's identity on every page, deterring forwarded leaks in a relationship-driven ecosystem

- Screenshot protection blocks AND logs capture attempts on sensitive pitch materials

- NDA gates require acceptance before the first page loads -- essential when you are sharing competitive commercials with Blackbird, Airtree, and Square Peg in parallel

- AI-powered Q&A drafts answers to investor questions with page citations, then routes through your team for approval

- E-signatures with AI field detection for SAFEs, convertible notes, and NDAs

- AI Redaction identifies PII, ITAR-sensitive content, and confidential financial data before external sharing

- Custom branding lets you present a polished founder-brand surface across every investor interaction

Transparent pricing: Peony Data Room at $52/admin/month (full fundraise toolkit) with Business at $30/admin/month for earliest-stage founders. For a 4-person AU founding team running 12 parallel VC conversations, that is $208/month -- versus $15,000-$50,000 per deal for Datasite or Intralinks on an AU seed or Series A.

Bottom line

Raising in Australia in 2026 requires matching your stage, sector, geography, and international ambition to the right investors. The 15 on this list are actively deploying capital -- but they are selective.

At pre-seed: Startmate, Antler, and Ten13 are your structured accelerator-to-VC trio. At seed: Blackbird, Airtree, Folklore, Tidal, Rampersand, and OIF lead or co-lead for B2B SaaS and technical founders; Main Sequence, Artesian, and Salus cover deep-tech and defence. At Series A: Airtree, Square Peg, Blackbird, Main Sequence, and King River write $5M-$15M leads. At growth: Square Peg Opportunities 3, Blackbird Follow-On, Airtree's $400M growth sleeve, and Skip Capital anchor $20M+ rounds. Trans-Tasman: Blackbird, Airtree, and Pacific Channel cover both sides.

The 2025-2026 signals -- Firmus's $505M April 2026 raise, Halter's $220M Series E March 2026, Canva's $42B valuation, Airwallex's $498M Series G, Blackbird's Fund VI first close at $700M+, and Square Peg's Fund 6 first close at $650M -- all point to the same conclusion: AU founders no longer need to move offshore to raise institutional capital.

Bring round math, "why this wins from Australia" narratives, stage-appropriate traction, and a clean Peony data room to every pitch. In a relationship-driven ecosystem, process discipline is a signal -- and signals compound.

Ready to pitch Australian investors? Set up your Peony data room in under 5 minutes with AI auto-indexing, NDA gates, dynamic watermarks, and page-level analytics. See Peony pricing here.

FAQ

I am a B2B SaaS founder in Sydney raising a $3M seed round in 2026 — which Australian VCs lead at this check size?

For a $3M AUD seed round in Sydney B2B SaaS in 2026, your strongest leads are Blackbird Ventures (Fund VI first close $700M+ August 2025, 6 deals in Q1 2026), Airtree Ventures (Fund V $650M with $250M dedicated to seed), Folklore Ventures (Sydney, seed average $2.87M, led Hullbot's $16M Series A November 2025), and Tidal Ventures (Sydney/NY, Tidal Seed Fund III with 32 portfolio companies and $3.77M seed average). Square Peg typically comes in at Series A but will lead high-conviction seeds. For a 4-person Sydney SaaS team at $20K MRR, Blackbird + Airtree co-lead with Folklore participation is the cleanest 2026 pattern. Upload your pitch deck, financial model, and cohort retention data into a Peony Business data room at $30/admin/month with page-level analytics showing exactly how much time each partner at Blackbird or Airtree spent on your retention slide versus the team slide -- a 30-minute-on-financials signal Dropbox cannot track on any plan.

I am a climate-tech founder in Melbourne raising a $10M Series A in 2026 — which AU deep-tech VCs are actively deploying?

For a $10M AUD Series A climate-tech round in Melbourne, your sharpest fits are Main Sequence Ventures (CSIRO-linked, Fund 3 at $450M, 13 investments 2025 plus 7 in Q1 2026, backed Samsara Eco and Q-CTRL), Blackbird Ventures (Eucalyptus $190M November 2025 shows $190M+ growth participation is live), Artesian VC ($350M FUM across 304 investments with multi-thematic clean-energy sleeve), and Square Peg (Fund 6 plus Opportunities 3 first close $650M February 2026). For Series A specifically Main Sequence is the deep-tech anchor Australia does not have a replacement for -- they announced Advanced Navigation participation March 17 2026. Your diligence set needs validated technical data, carbon-impact modelling, grant history, and a credible path to scale. Peony Data Room AI redaction auto-flags sensitive IP and unredacted customer data in your technical appendix before you share with Main Sequence partners -- a workflow Datasite charges $25K+ per deal for while you get it at $52/admin/month.

I am an AI-powered founder pitching Blackbird or Airtree in 2026 — what do Australian VCs actually expect in a data room this year?

For an AI-powered pitch to Blackbird or Airtree in 2026, your data room needs a tight pitch deck, financial model with 18-24 months runway, unit economics with CAC payback under 18 months, cohort retention data, cap table, incorporation documents, key customer contracts, technical architecture overview, and evidence of AI moat (proprietary data, model differentiation, or distribution edge). Blackbird saw 51 investments in 2025 from 1,900 applications, so clarity wins. Airtree led Eucalyptus's $190M November 2025 round and Human Health in October 2025 -- they pressure-test founder quality, category size, and real retention. For a 5-person Sydney AI founding team targeting a $6M seed, Peony Data Room at $52/admin/month gives you Smart Q&A that drafts investor answers with page citations -- a task junior analysts spend 2-3 hours per room on at legacy platforms like Datasite which charges $15K-$50K per deal. Unlike DocSend which caps analytics on lower tiers, Peony delivers full page-level analytics across unlimited share links.

I am a fintech founder raising a Series A in 2026 post-Airwallex's $498M Series G — which Australian fintech VCs are actively writing checks?

Post-Airwallex's $498M Series G at $12B late 2025 (Square Peg participated), the AU fintech VC ecosystem is highly active. Your sharpest 2026 targets are Square Peg Capital (Fund 6 plus Opportunities 3 first close $650M February 2026, led Airwallex Series F at $232M May 2025 at $6.2B), Airtree Ventures (Fund V $650M, broad fintech mandate), Ten13 (Brisbane syndicate with 550+ members, $115M deployed across 55 companies), and Skip Capital (Sydney family office, Adora February 11 2026, strong on fintech follow-on). King River Capital ($1.2B AUM) backs Block Earner in the crypto-fintech lane (February 9 2026 participation). For a 6-person Sydney fintech team at $500K ARR targeting $15M Series A, Square Peg lead with Airtree and Skip participation is the 2026 template. Peony Data Room at $52/admin/month gives you NDA gates per fund so regulatory and financial documents stay access-controlled by firm -- per-fund access control Dropbox fundamentally cannot provide.

I am a medtech founder in Brisbane raising a $4M seed — which Australian investors specialise in medtech and deep-tech health?

For a Brisbane medtech $4M AUD seed in 2026, the most sector-explicit AU investors are Main Sequence Ventures (CSIRO-linked, health/biotech in Fund 3 $450M, deep-tech anchor for AU), Artesian VC (medtech is one of their named thematic verticals across $350M FUM and 304 investments, Coherence November 2025), Airtree Ventures (Human Health October 2025), and Blackbird Ventures (broad but health-capable across Fund VI). Ten13 brings Brisbane-native syndicate reach with 550+ members and $115M deployed. For an Aussie medtech team you usually pair one sector-specialist lead (Main Sequence) with a generalist (Blackbird or Airtree) plus non-dilutive via MRFF, Biomedical Translation Bridge, or Advance Queensland. Upload clinical trial data and provisional patent filings into a Peony Data Room where dynamic watermarks embed each viewer's identity into every rendered page -- so if a partner forwards your IP appendix to a co-investor, the forwarded copy carries the original partner's name, something DocSend can do at entry tier but with zero screenshot protection.

I am a trans-Tasman founder raising an ANZ round across Australia and New Zealand — which funds cover both sides in 2026?

For a trans-Tasman round in 2026, your strongest bridges are Blackbird Ventures (dedicated NZ$75M NZ fund plus ANZ growth fund, 51 investments in 2025 across ANZ), Airtree Ventures (broad ANZ mandate, invested in Halter when it was NZ-only), Square Peg (Fund 6 covers ANZ plus Southeast Asia), and Folklore Ventures (regular trans-Tasman co-investor). On the NZ side, Icehouse Ventures (NZ$70M Seed Fund IV) and Pacific Channel (NZ$125M+ AUM with a new Australian Fund IV launched 2025) anchor ANZ cap tables alongside AU leads. For a trans-Tasman SaaS or deep-tech team raising $6M AUD, Blackbird + Airtree lead with Icehouse or Pacific Channel participation is the default pattern. See our guide to NZ investors for the sibling breakdown. Run one Peony Data Room with separate NDA-gated share links per fund so Auckland, Sydney, and Melbourne partners each get individually tracked access -- page-level analytics tell you which partner spent 20 minutes on your cohort chart versus 30 seconds, in a capability Google Drive simply lacks.

I am a pre-seed founder in Australia applying to Startmate or Antler in 2026 — how does the accelerator-to-VC path actually work?

For pre-seed founders in 2026, Startmate (Blackbird-backed, AUD$120K standard, Summer '26 cohort = 19 companies/42 founders, Demo Day April 30 2026 at Carriageworks in Sydney) and Antler Australia (Fund II $77M 2025, QLD program launched February 2025, 145+ AU startups across 12 cohorts) are the two most active accelerator doors. Startmate gives you direct exposure to Blackbird and Airtree partners plus an automatic warm-intro network into Tidal, Folklore, and Ten13 for follow-on rounds. Antler's model is pre-team -- they match co-founders inside the cohort then write the first check. After Demo Day most Startmate graduates close a $500K-$1.5M pre-seed within 90 days. For a solo founder or 2-person Sydney team pre-product, applying to both is rational since the selection rates differ. Once you are in the programs, maintain a Peony Business data room from day one with screenshot protection that blocks AND logs capture attempts on your financial projections -- so when a partner at Airtree or Skip starts circling, you can see exactly what they read, something Dropbox flat-out cannot track.

I am an Australian founder deciding between an ASX IPO path and a US IPO path in 2026 — which VCs support each route?

For an Aussie founder weighing ASX versus US IPO in 2026, the fund choice shapes the path. ASX-friendly investors like Main Sequence Ventures (CSIRO-linked, $450M Fund 3, deep-tech/industrials often IPO locally), Blackbird Ventures (Halter participated in $220M Series E March 2026, ASX-credible network), and Skip Capital (Canva alumni via founders -- Canva itself is US IPO-track at $42B August 2025) all maintain relationships with both sides of the ocean. Square Peg's US-heavy portfolio (Canva, Airwallex, Tyro) and NY co-investors tilts US. Airtree plays both. Growth-stage AU rounds in 2025-2026 -- Halter $220M, Eucalyptus $190M, Airwallex $498M, Canva $42B -- span ASX-credible and US-IPO-bound categories. For a 12-person Sydney team at $5M ARR weighing paths, your data room needs to present clean unit economics, audit-ready financials, and regulatory comfort for both venues. Peony Data Room at $52/admin/month gives you e-signatures with AI field detection for SAFEs, convertible notes, and NDAs -- so diligence runs as cleanly for an ASX listing sponsor as a US underwriter, a workflow Datasite charges per-deal for.

I am a defence or national-resilience founder in Australia raising in 2026 — which AU investors back dual-use tech?

For defence and dual-use tech founders in 2026, the explicit AU specialist is Salus Ventures (Sydney, Fund I $40M with plans to deploy $250M+ over 5 years, led ExoFlare's $5.3M round with In-Q-Tel co-investing, backed Gega Elements October 27 2025). Main Sequence Ventures (CSIRO-linked, $450M Fund 3) covers dual-use sovereign capability including Advanced Navigation (March 17 2026) which serves defence and autonomy. Blackbird Ventures backs defence-adjacent via AI and space (Fleet Space, Gilmour Space alumni). Artesian VC carries a defence-adjacent industrials sleeve across its 304 investments. AUKUS tailwinds and the 2024 Defence Strategic Review mean dual-use capital is increasingly mobilised from super funds through direct and fund-of-fund allocations. For a 5-person Sydney dual-use founding team raising $5M seed, Salus lead with Main Sequence and Blackbird participation is the cleanest 2026 template. Upload your classified-adjacent technical documents into a Peony Data Room where AI redaction auto-flags ITAR-sensitive content, export-controlled tech specs, and PII before sharing externally -- a workflow Google Drive simply has no capability for.

I am comparing DocSend and Peony for my 2026 AU fundraise — which data room actually works best for Australian founders?

For Australian founders raising in 2026 you need a data room that handles ANZ-specific fundraising dynamics: competitive seed markets (59% of pre-seed/seed deals were competitive in 2025 per Cut Through Venture, up from 30% in 2024), parallel multi-fund processes, and trans-Tasman information flow. Peony Data Room at $52/admin/month sets up a complete investor data room in under 5 minutes with AI auto-indexing organising your pitch deck, financials, milestone plans, and IP into a professional folder structure in under 3 minutes. Page-level analytics show which documents each partner at Blackbird, Airtree, Square Peg, or Main Sequence reviewed and for how long, dynamic watermarks embed viewer identity into every page, screenshot protection blocks and logs capture attempts, and NDA gates control access before first page load. For a 4-person Sydney team, that is $208/month total -- versus $15,000-$50,000 per deal for Datasite or Intralinks. DocSend offers link tracking but caps analytics on lower tiers, lacks watermarking at its entry tier, has no screenshot protection, and has no AI organisation. Google Drive and Dropbox offer zero fundraising intelligence. For the full comparison see our AU VC guide.

Related Resources

- 12 Active New Zealand Investors in 2026

- 13 Active Canada Investors in 2026

- 10 Active Slovenia Investors in 2026

- 15 Active Dubai Investors in 2026

- Investor Outreach Plan 2026

- Why Startups Need Data Rooms for Fundraising Success

- What Makes a Data Room Investor Ready

- How to Send Pitch Deck to Investors

- Startup Fundraising Strategy Complete Guide

- The Rise of AI-Powered Data Rooms

- Fundraising Data Rooms

- Venture Capital Data Rooms

- Startup Data Rooms

- Peony Pricing

You might also like

Apr 20, 2026

12 Active New Zealand Investors in 2026 (Check Sizes + Intro Paths)

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026

Apr 29, 2026

Top 8 Boston Investors in 2026: The Founder's Complete Guide to Raising in Boston & Cambridge