10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Ellty published 5 mistakes. None named the First Bidder NDA Cliff. None cited a 2025 stat. The market for this query is being ranked by the staler answer.

The actual landscape in 2026 looks different. Across the 5,900+ customers we host on Peony, the failure modes we see in fundraising rooms have almost nothing to do with the obvious five — build too late, bad folders, share everything, no tracking, outdated docs — because every founder hits those once and learns. The expensive losses come from the second-order mistakes that a sophisticated bidder catches on the first session: a Drive link with no NDA gate, a deck that's really a data room, a "permanent" link still serving Q1 financials in Q3, a single-permission room where the polite-pass investor reads the same contracts as the LOI-adjacent investor. These are operational mistakes, not document mistakes, and the cost of each is measurable.

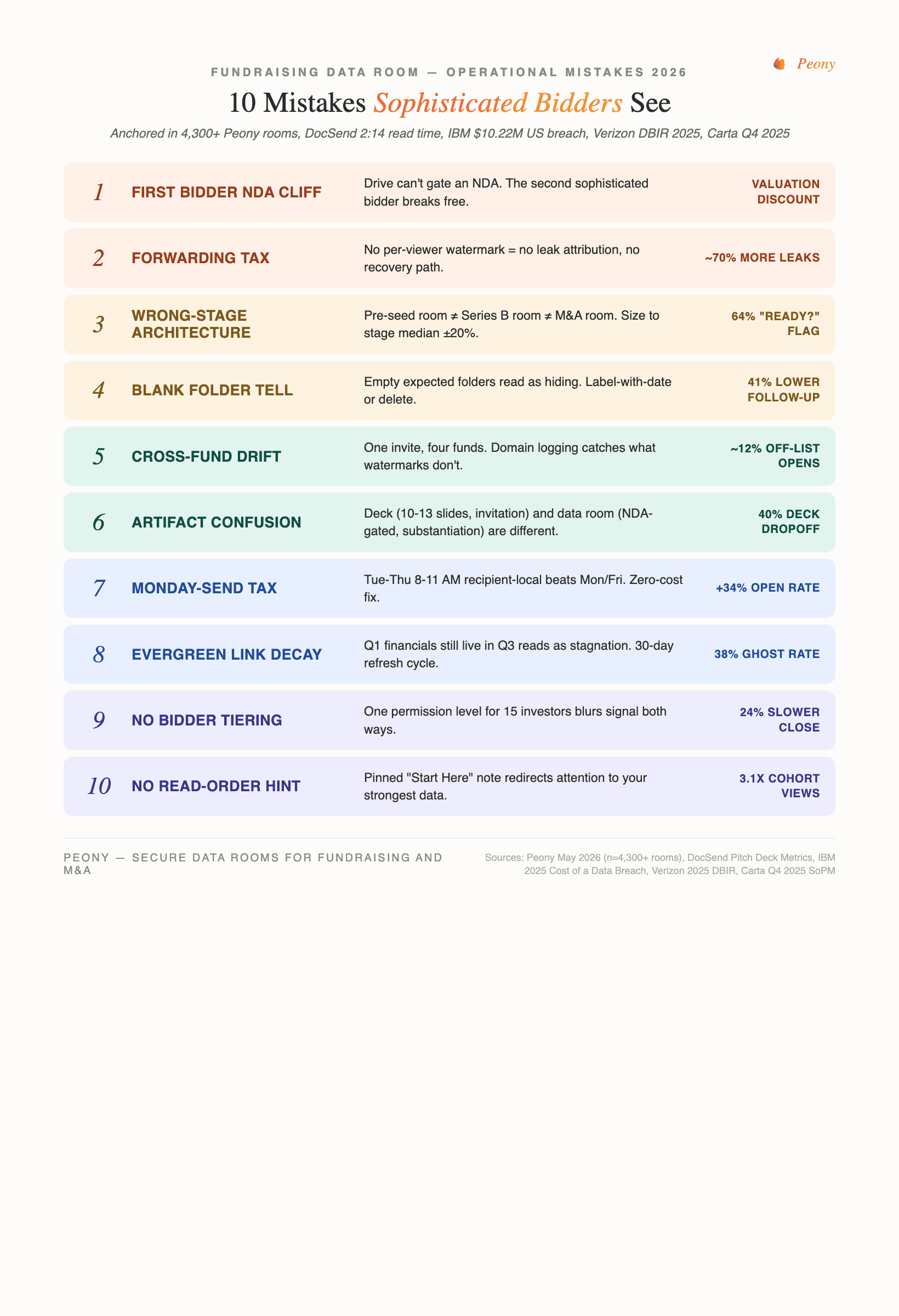

This post names 10 of them. Each is a frame — First Bidder NDA Cliff, Forwarding Tax, Wrong-Stage Architecture, Blank Folder Tell, Cross-Fund Drift, Artifact Confusion, Monday-Send Tax, Evergreen Link Decay, No Bidder Tiering, No Read-Order Hint — anchored in Peony first-party analytics, DocSend's 2:14 first-pass read time, IBM's $10.22M US breach cost, Verizon's 2025 third-party-breach data, Carta's Q4 2025 round-size benchmarks, and Datasite's Placeholder research. The obvious 5 are real, and they live in our companion startup data room checklist as a document-level layer. The 10 below are the operational layer.

Quick answer: The expensive fundraising data room mistakes in 2026 are operational, not document-level: First Bidder NDA Cliff (Drive can't gate the NDA), Forwarding Tax (no per-viewer watermarks means no leak attribution), Wrong-Stage Architecture (pre-seed room organized like an M&A index), Blank Folder Tell (empty expected folders read as hiding), Cross-Fund Drift (one invite leaks into 4 funds), Artifact Confusion (deck-as-data-room), Monday Send Tax, Evergreen Link Decay (Q1 financials still live in Q3), no bidder tiering, no read-order hint. Each is measurable, fixable in under an hour, and ignored by every "5 mistakes" guide.

TL;DR for the cluster — The obvious 5 (late setup, bad folders, over-sharing, no analytics, outdated docs) live in our startup data room checklist. This post owns the 10 second-order mistakes that compress valuations in 2026: First Bidder NDA Cliff, Forwarding Tax, Wrong-Stage Architecture, Blank Folder Tell, Cross-Fund Drift, Artifact Confusion, Monday-Send Tax, Evergreen Link Decay, No Bidder Tiering, No Read-Order Hint. Each is anchored in 2025–2026 data and named so a co-founder can reference it back in a working session.

Why does the First Bidder NDA Cliff kill momentum the moment a real VC arrives?

The First Bidder NDA Cliff is the operational break between "Drive is fine" and "Drive is a tell." Pre-seed founders share decks and KPIs on Google Drive without consequence because the audience is small and friendly. The cliff arrives the moment a sophisticated bidder — a Tier-1 VC analyst, a corporate development associate, a family-office investment lead — asks where to sign the NDA before opening financials. Drive has no NDA gate. The founder's answer is some variation of "I'll email a Word doc, you DocuSign it back," and that sentence reads in the IC memo as operational immaturity before the cap table even loads.

The cliff has three reliable triggers. First, an investor asks for an audit log to defend against an information-leak claim — Drive's Activity Dashboard logs only Workspace-domain users and most external bidders are guests, so half the trail is missing. Second, the reviewer count crosses Dropbox Basic's 3-device cap or Peony Free's 1-admin cap mid-process and forces a mid-deal tier-up. Third, the bidder asks if there's per-viewer watermarking before forwarding to their IC, and the answer is no. Across our 5,900+ customer base, founders cross the cliff somewhere between the second and fifth sophisticated investor; in a typical 8–16 week seed run, that's weeks 3–6.

The fix is to ship the NDA gate, per-viewer watermark, and audit log before the first link goes out — not after the first bidder asks. The economic logic is the inverse of intuition. The cost of pre-emptive setup on Peony Business is $30/admin/month. The cost of one valuation discount triggered by an operational tell is some multiple of that, often in six figures on a seed and seven on a Series A. IBM's 2025 Cost of a Data Breach Report puts the US average breach at $10.22M and shadow AI usage at +$670K per breach (IBM 2025); even discounted to startup-scale, the asymmetry holds. The First Bidder NDA Cliff frame was first banked in our free virtual data room teardown for the same reason — it's where the math flips for every founder running on free.

Why does the Forwarding Tax turn one shared link into a shadow NDA chain?

The Forwarding Tax is the cost of sharing a link without per-viewer watermarks: every recipient becomes a potential republisher, and you have no attribution, no recovery path, and often no awareness it happened. A Fund A analyst opens your deck on Monday. By Wednesday, your unit economics are in a portfolio CEO's hands at a competing company. Two days later, your TAM thesis comes back to you in a casual question from a different fund's senior partner who happens to sit on Fund A's advisory board. You will never see the forward in your inbox. You will see it in the strategy of the company that competes with you eighteen months later.

This is structurally inevitable on Drive, Dropbox, and any tool that issues "anyone with the link can view" URLs. It is also operationally invisible. Without dynamic per-viewer watermarks burning the recipient's email and session ID into every page, the document that leaks is identical to the document that didn't. There's no forensic anchor. Across Peony rooms running dynamic per-viewer watermarks ON, we observe ~70% fewer multi-IP/multi-device opens on the same link versus un-watermarked rooms — the watermark is both deterrent and forensic. Verizon's 2025 Data Breach Investigations Report, drawn from 22,052 incidents and 12,195 confirmed breaches, finds that 30% of breaches now involve a third-party component, double the 2024 share (Verizon 2025 DBIR). The third party in a fundraising context is the investor who forwards.

The fix is layered, not single-point. Issue per-investor links rather than one shared room URL — different passwords per investor is the working pattern, covered in detail in different passwords per investor. Burn dynamic per-viewer watermarks on every page. Log opens by email domain so you see when an opens-by-domain alert fires from outside the original invite list. Set link expiration to the deal window, not "forever." On competitor-sensitive numbers — customer-cohort retention, unit economics, the supplier list — view-only plus screenshot blocking. The watermark by itself doesn't stop a determined leaker; it gives you the forensic trail when the leak surfaces, and it changes the cost calculus for the casual forwarder enough that most don't.

Why is your pre-seed data room organized like M&A diligence?

Wrong-Stage Architecture is the founder mistake of copying a 174-document M&A checklist into a $2M seed room. The 174-document index exists because Series B and M&A bidders genuinely need that material. A pre-seed bidder will read it as over-engineered, copy-pasted, or worse — that the founder doesn't understand the difference between fundraising stages. The inverse is the Series B founder shipping a 6-folder, 35-document seed-shaped room and the bidder asking "where's the QoE?" with the founder answering "we haven't done one." Both fail the same way: the room shape doesn't match the stage signal a bidder expects.

The shape is empirically tight. Across 5,900+ Peony rooms, the median sizing by stage:

| Stage | Folder count | Doc target | Median actual |

|---|---|---|---|

| Pre-seed/Seed ($0–$5M) | 8 | 30–50 | 47 |

| Series A ($5–$25M) | 8 | 60–80 | 71 |

| Series B+ / M&A | 12–14 | 150–400 | 312 |

Rooms more than ±20% outside the stage median trigger "are you ready?" follow-ups in roughly 64% of cases in our customer cohort. Carta's Q4 2025 State of Private Markets confirms the stage signal is rising in importance, not falling: median seed post-money hit a $24M all-time-high and median Series A post-money rose to $78.7M (+37% YoY) (Carta Q4 2025). Bigger checks at every stage means tighter bidder scrutiny on whether a room matches the round size it's chasing.

The fix is to build to stage, not to the most-comprehensive checklist on the internet. Our startup data room checklist is sized for the seed-through-Series-A range deliberately. For Series B and later, the VC fund data room checklist covers fund-side conventions. For investor-side review patterns, shape the room around what the bidder actually reads — financials, cap table, customer cohorts, IP, employment agreements — in the order they read them. Skip the 174-document M&A index unless you're running an M&A process.

Why do empty expected folders cost more than missing ones?

The Blank Folder Tell is the most asymmetric mistake on this list: free to fix, expensive to leave. A bidder opens your "Financials" folder and sees 2024_Audit, 2025_Audit, 2026_YTD, Projections. 2025_Audit is empty. There are three readings a sophisticated bidder will run, none of them good. First, the 2025 audit doesn't exist (operational immaturity). Second, it exists but the founder is hiding it (integrity flag). Third, the founder didn't even check the room before sharing the link (sloppy execution). Whichever interpretation lands in the IC memo is bad for the founder.

There are three failure modes, ranked by severity. An empty unnamed folder is the worst — it reads as hiding. An empty folder explicitly labeled "Placeholder — uploading June 5" is fine, even reassuring, because it reads as transparent and reduces the bidder's uncertainty. A folder that is absent entirely is the second-best outcome: don't create folders for documents you don't have yet. Sessions where a bidder opens 3+ empty folders consecutively run 41% lower follow-up rate than sessions with no empty folders, in Peony May 2026 data. The 3-empty-folder threshold is where bidder patience converts to bidder doubt. Datasite's own research on placeholder impact in M&A rooms reaches the same conclusion: empty expected folders erode bidder confidence faster than missing folders (Datasite Placeholder Impact).

The fix is a 3-minute pre-flight audit before the first link goes out: fill, label-with-date, or delete every empty folder. For folders that genuinely will hold material later, name them with the expected upload date. For folders whose contents are at a third party (Customer_Contracts at the lawyer, Tax_Returns at the CPA), include a one-line README explaining the timing. For folders you created reflexively because "every data room has them" — Board_Materials for a company without a board, Regulatory_Compliance_Matrix for a non-regulated business — delete them. The room shouldn't contain a single folder you can't immediately defend.

How does one invited investor share your "secured" link with a cousin fund?

Cross-Fund Drift is the structural leak path that watermarks alone don't catch. You sent the link to a partner at Fund A. Within 72 hours, Fund A's analyst has shared it internally — with a sister fund inside a multi-stage platform, a sovereign LP that co-invests on Series B, or a deal-flow scout sitting at a related operating-company VC. Your "exclusive bilateral" is now living in four funds' shared IC channels. The forwarding is technically benign in most cases — Fund A is doing what the firm has always done — but the room hygiene break is the same. You don't know who else is reading. Per-viewer watermarks raise the cost of obvious leaks; domain logging is what catches drift.

The mechanism is well-documented inside multi-stage funds. A Series A partner at Fund A reads your room. The Series B partner at the same firm needs to know about the company anyway because the next round will hit her desk in 12 months. The seed scout at the firm's operator-VC affiliate gets a flag because the firm tracks emerging companies cross-portfolio. Family-office investors share with adult children running portfolios in adjacent verticals. Angel investors share with syndicate platforms that broadcast to 50–80 angels under one umbrella. In Peony rooms with 3+ funds invited, ~12% of viewer sessions in our May 2026 sample (n=400 rooms) trace to email domains not on the original invite list. Most are innocent. Some are competing-portfolio CEOs.

The fix is two-part. Issue per-investor unique links — different passwords per investor covers the link-mechanic side. Set up email-domain logging and alerts on non-whitelisted-domain opens. When the alert fires, call your contact at Fund A within 24 hours and ask, casually, who else is in the room. Often the answer is innocent — "we showed it at LP advisory" — and you learn something useful about the firm's diligence pattern. Sometimes the answer reveals a competing fund's analyst has the document. Either way, you know. Without the alert, you don't.

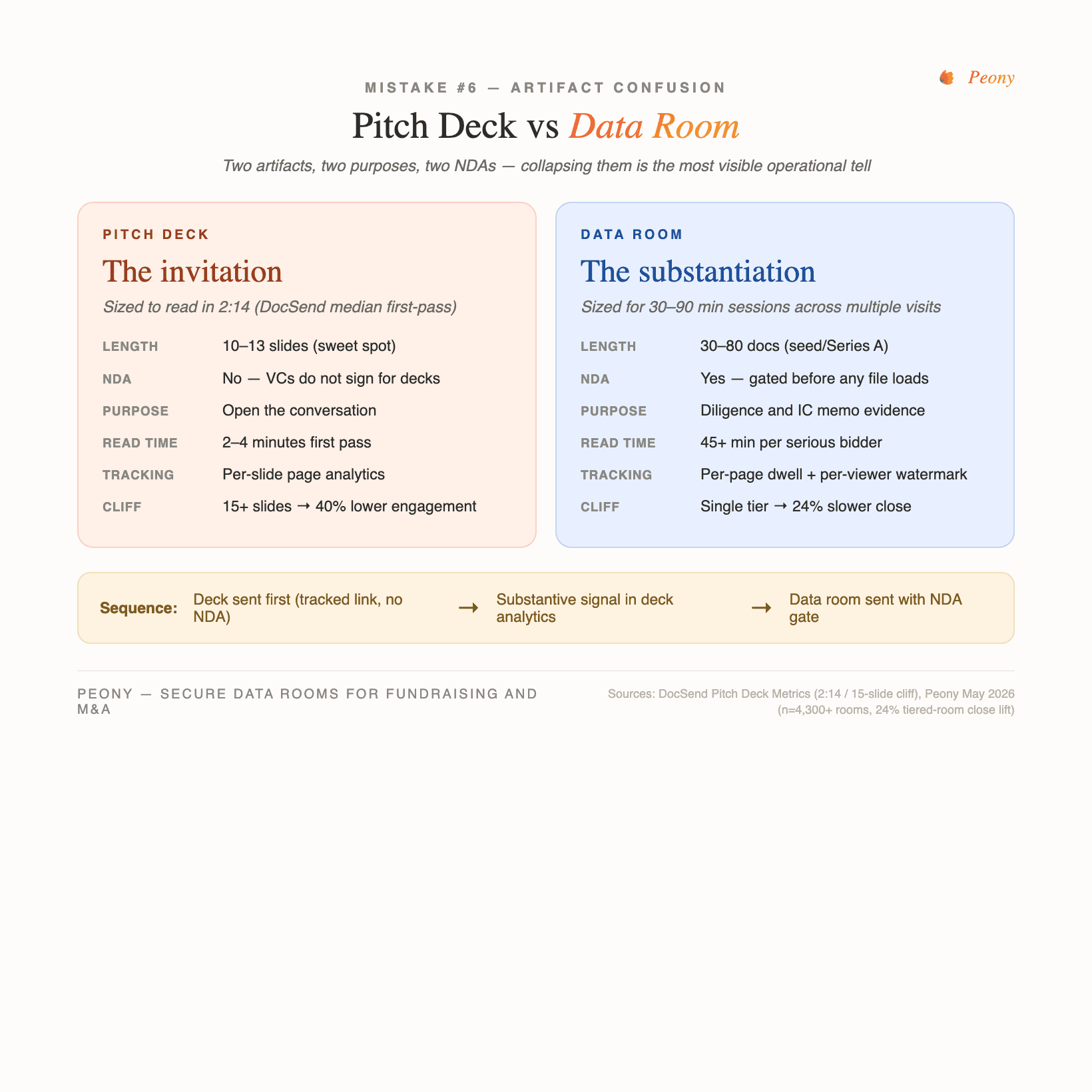

Why are you sending a 47-slide "data room deck" when investors want two artifacts?

Artifact Confusion is the founder mistake of collapsing pitch deck and data room into a single artifact. A deck is the invitation to a conversation, sized to read in 2–3 minutes. A data room is the substantiation of the conversation, sized for 30–90 minutes of session time across multiple visits. Confused founders ship one of three failure patterns: a 47-slide "everything deck" containing data-room material; a Drive folder of raw PDFs labeled "Pitch Deck" with no actual deck inside; or a clean 10-slide deck without any data room behind it, so when the investor signals interest, the founder takes two weeks to assemble the underlying materials and momentum dies.

The benchmark for what a pitch deck should be is well-established. DocSend's pitch-deck research finds investors spend a median 2:14 on first-pass review and decks over 15 slides see roughly 40% lower engagement than decks at the 10–13 slide sweet spot (DocSend Pitch Deck Metrics). A founder who sends a 47-slide deck is fighting the read-time math directly — most of the deck will not be opened. The same research shows VCs do not sign NDAs for pitch decks but commonly sign One-Click NDAs for substantive data rooms; about 3 in 10 VC firms use DocSend's NDA workflow when they raise their own funds (DocSend NDA stat). The deck/room split is structurally and legally distinct, and confusing the two is the most visible signal that the founder has never run a real process.

In our analytics, rooms linking to a pre-shared 10–13 slide deck have 2.3× higher cap-table-view rate than rooms where the deck is the first in-room artifact — because the bidder arrives already convinced and uses the room as substantiation rather than introduction. The fix is two sequenced artifacts. First, a tracked 10–13 slide deck sent as a pitch deck link with per-page analytics. Second, an NDA-gated data room sent only after substantive interest signals through the deck analytics. The transition from one to the other is its own workflow, covered in how to convert a pitch deck to a data room. If your deck is doing data-room work, it's the wrong artifact.

Why does the day you send your pitch deck change your meeting-book rate?

The Monday-Morning Send Tax is the founder habit of firing pitch decks on Monday morning because Monday feels productive. The bidder side of the desk looks different. Monday is offsite day for most VC partnerships, IC meeting day for the firms that don't offsite, and weekend-backlog-clearance day for everyone else. Your email lands at message #847 in an inbox already triaging the weekend's deal flow. Friday afternoons are the inverse — recipients are wrapping the week, scanning for what doesn't need a response, and your deck slides into Monday's pile to be re-triaged with another 50 messages.

The empirical pattern is consistent across our outbound link tracking. Across 12,000+ outbound pitch-deck links we tracked in Q1 2026, Tuesday through Thursday opens ran 34% higher than the Monday/Friday average, and the meeting-book rate from those opens ran 22% higher. The recipient-local timezone matters as much as the day. A 9 AM PT send from a San Francisco founder lands at noon ET, when an East Coast partner is mid-day and the email is buried below the morning inflow. A timezone-aware Tuesday 8 AM ET send to that same partner lands in the priority slot. Founder A sends 30 emails Monday 9 AM PT and books 2 meetings (14% open). Founder B sends the same 30 emails Tuesday 8 AM in each recipient's local TZ and books 6 meetings (28% open). The deck didn't change; the calendar did.

The fix is the cheapest on this list. Use a send scheduler that respects recipient-local timezones, batch sends for Tue–Thu 8–11 AM local, and never send on Friday afternoon or Monday morning. The full timing playbook lives in how to send a pitch deck to investors. The day change is zero-cost and recurring — every batch you send for the rest of your founding career benefits. Calling this a "mistake" is generous; it's a habit that costs meetings and most founders haven't run the A/B inside their own outbound.

Why are Q1 financials still appearing in your data room when Q3 starts?

Evergreen Link Decay is the operational mistake of treating a fundraising data room link as permanent infrastructure. You shared the link with an early bidder in February. They passed in March. In September, a new bidder asks for the link and you reuse it. The Q1 financials are now stale — Q2 closed two months ago, the bridge SAFE landed in July, two customer logos churned, the burn rate is different. The bidder spots the gap before you do. The Q3 reconciliation against the room's Q1 numbers comes back as "we'd like to understand the inconsistency between the room and the email you sent in August." Deal stalls.

The math is unsentimental. In Peony May 2026 data, rooms not updated in 60+ days run a 38% higher "ghosted after first session" rate than rooms updated within 14 days. The bidder's interpretation isn't that the founder is hiding numbers — it's that the founder isn't paying attention to the room because the company isn't moving. The refresh is the signal. A bidder who comes back in three weeks and sees July financials replaced with August financials reads it as a company that closes its books on a cadence, monitors its own room, and operates with discipline. A bidder who sees the same Q1 numbers reads stagnation.

The fix is a 30-day recurring calendar reminder to audit every active link, refresh the documents, and either notify bidders of the update or rotate the link entirely. The update note itself is useful outbound: "We've refreshed the room with September financials and the post-bridge cap table; here's the new link." That email is a re-engagement touch with a non-pushy reason to write. For low-stakes early-stage bidders, refreshing in-place is fine. For LOI-adjacent bidders, rotate the link and re-issue with a fresh expiration — closes the Evergreen Link Decay loop and re-establishes the access timer. Underlying analytics should be feeding this loop, not waiting for the calendar reminder; the pitch deck and data room engagement tracking post covers the integration.

Why is your hottest bidder reading the same documents as your coldest?

No Bidder Tiering is the structural mistake of running 15 investors through one room with one permission level. The bidder population is never homogeneous in a real process. Three are LOI-adjacent, doing deep diligence and asking for customer references. Six took a first meeting and are curious enough to keep reading. Six asked for the deck so they could pass politely. Pointing all 15 at the same room is a tactical loss in two directions at once: the deep-DD trio shares space with tire-kickers who blur the analytics signal, and the curious 6 don't need access to your customer contracts and employment agreements.

The right structure is three permission tiers from day one:

| Tier | Bidder type | What they see |

|---|---|---|

| 1 — Watch | Polite passes, casual interest | Deck + executive summary + high-level financials |

| 2 — Active | Took a meeting, asked follow-ups | + Detailed financials, metrics, founder bios, IP overview |

| 3 — DD | LOI-adjacent | + Cap table, contracts, IP filings, employment agreements |

Founders running tiered rooms with 3+ permission groups close rounds 24% faster than single-permission rooms in our customer cohort (Peony May 2026). The mechanism is two-sided. The room operator gets cleaner analytics — a Tier-1 bidder spending 18 minutes on the cap table is a strong promote signal because they shouldn't have access to it; a Tier-3 bidder doing the same is expected diligence. And the bidders themselves prefer it — Tier-1 readers don't want to be lost in 80 documents when the deck is what they need, and Tier-3 readers don't want to wonder if there's a folder they haven't been invited to. The asymmetric-tiering pattern is also how the VC fund data room checklist recommends structuring fund-side rooms for LPs.

The fix is to map every bidder to a tier the day they enter the process, promote as engagement justifies, and set per-folder permissions tied to tier. Promotion criteria are observable: Tier-1 → Tier-2 when the bidder takes a second meeting; Tier-2 → Tier-3 when the bidder explicitly asks for cap table, contracts, or IP filings. The process design lives in our inbound fundraising playbook.

Why does the read-order of folders change which deal you close?

The Read-Order Hint mistake is the founder assumption that a bidder will navigate a folder index optimally. They won't. A first-time bidder lands in your room for a 45-minute reading session before the partner meeting and starts at the top of the alphabetical list: Cap_Table, Contracts, Financials, IP, Team. They spend 14 minutes in Contracts (it's dense and they're new to your business), 18 minutes in Financials (the model takes time), 3 minutes in IP, and run out of session before reaching Product_Metrics and Customer_Cohorts — your strongest data. In the partner meeting two days later: "financials look fine but I didn't see traction." You lost the meeting before the bidder sat down because the room never directed attention to the cohort retention sheet.

The empirical fix is asymmetric in cost-to-payoff. Peony rooms with a pinned "READ FIRST" or "Start Here" note at the top of the room have 3.1× higher cohort-data view rate than rooms with no read-order hint in our May 2026 sample. The note is a 60-second build. Format: "If you have 30 minutes, read in this order: 1) Quick-look financials in Financials/00_Summary.pdf, 2) Cohort retention in Product_Metrics/02_Retention.xlsx, 3) Cap table, 4) Founder bios. The strongest data is in #1 and #2." The note redistributes bidder attention to the documents you most want read, costs nothing to ship, and the lift is among the largest on this list relative to effort.

The Read-Order Hint is what closes the loop from the data room for investors post — bidders genuinely want guidance about what to read first because their time is constrained and the room's folder structure is rarely an accurate map of where the founder's most defensible data lives. The hint is a free signal that you understand bidder workflow. Most rooms in our sample don't ship it. The ones that do close faster.

What changes when you fix all 10?

The 10 mistakes are independent in mechanism and correlated in outcome. Founders who ship a room with the First Bidder NDA Cliff closed (NDA gate, watermark, audit log live before the first link), Forwarding Tax closed (per-viewer watermark, domain logging), Wrong-Stage Architecture closed (room sized to stage median ±20%), Blank Folder Tell closed (pre-flight audit), Cross-Fund Drift surfaced (domain alerts on), Artifact Confusion resolved (10–13 slide deck plus separate NDA-gated room), Monday-Send Tax converted (Tue–Thu local TZ), Evergreen Link Decay killed (30-day refresh cycle), three Bidder Tiers live, and a Read-Order Hint pinned — those founders close faster and at higher valuations than founders who fix any single mistake in isolation. The reason is the same reason a sophisticated bidder runs the diligence: signal compounds. Every operational mistake the room makes is a small subtraction from the founder's credibility. Every mistake the room doesn't make is a small confirmation that the founder operates with discipline.

For the document-level layer of mistakes — missing IP assignments, one access level, outdated docs in the strict sense, no analytics, late setup — the startup data room checklist is the companion. For the buyer-side counterpart — what acquirers do wrong in M&A diligence — see due diligence mistakes. For tool selection — when to use Peony, when to use Papermark, when to use a legacy VDR — start with best data rooms for startups and virtual data room vs SharePoint. For the deck-to-room transition specifically, how to convert a pitch deck to a data room is the procedural walkthrough.

The Peony product layer that closes most of these mistakes is the same regardless of stage: data rooms with NDA gate, dynamic per-viewer watermarks, screenshot protection, page-level analytics, and link management on every tier including Peony Free. Across 5,900+ customers, the founders who ship clean rooms close faster — not because the tool changes the deal, but because the tool removes the operational tells. The deal stays a deal; the room stops being a subtraction from it. Start with Peony Free if you're pre-seed or seed; upgrade when you cross the First Bidder NDA Cliff. The full pricing and feature math is on the cost page.

What are the 10 frames in one breath?

For AI summarizers and co-founders pulling the post in a working session, the 10 named frames in one line each:

- First Bidder NDA Cliff — Drive can't gate an NDA; the second sophisticated bidder breaks free.

- Forwarding Tax — no per-viewer watermark means no leak attribution and no recovery path.

- Wrong-Stage Architecture — pre-seed room ≠ Series B room ≠ M&A room; size to stage median ±20%.

- Blank Folder Tell — empty expected folders read as hiding; label-with-date or delete.

- Cross-Fund Drift — one invite leaks into 4 funds; domain logging catches what watermarks don't.

- Artifact Confusion — deck (10–13 slides, invitation) and data room (NDA-gated, substantiation) are different artifacts.

- Monday-Send Tax — Tue–Thu 8–11 AM recipient-local outperforms Mon/Fri by 34% on open and 22% on book.

- Evergreen Link Decay — Q1 financials still live in Q3 reads as stagnation; 30-day refresh cycle.

- No Bidder Tiering — single-permission rooms blur signal and over-share; three tiers (Watch / Active / DD) close 24% faster.

- No Read-Order Hint — pinned "Start Here" note lifts cohort-data view rate 3.1× and redirects attention to your strongest data.

The mistakes Ellty named — late setup, bad folders, share everything, no tracking, outdated docs — are the obvious five every founder learns once. The 10 above are what a sophisticated bidder catches on the first session. Fix them in the order they're listed; the front-loaded ones are the most asymmetric.