12 Best M&A Advisors in Pittsburgh for $1M-$300M Deals (2026 Guide)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

I'm Deqian Jia, co-founder of Peony and a former VC at Backed and Target Global. I've advised on hundreds of lower-middle-market deal processes — venture financings, founder exits, PE recapitalizations, and ESOP transitions — and Pittsburgh sits structurally apart from every other Rust Belt city we cover. UPMC's healthcare consolidation, Wabtec's $2.6B+ industrial roll-up cadence over 18 months, the Marcellus/Utica gas-services boom anchored by Pittsburgh's own EQT Corporation (the gas driller — not the Stockholm-based EQT AB private equity firm; these are two different companies and confusing them costs founders weeks), Carnegie Mellon's $1.48B AI/robotics VC year, and Tecum Capital's fourth SBIC license all converge into a city where five engines drive lower-middle-market deal flow. This guide maps the 12 boutiques active in Pittsburgh's $1M-$300M deal range as of May 2026 — tiered by deal size, sectored, and verified against ACG Pittsburgh 2024-2026 awards, current firm leadership pages, and 2024-2026 transaction releases.

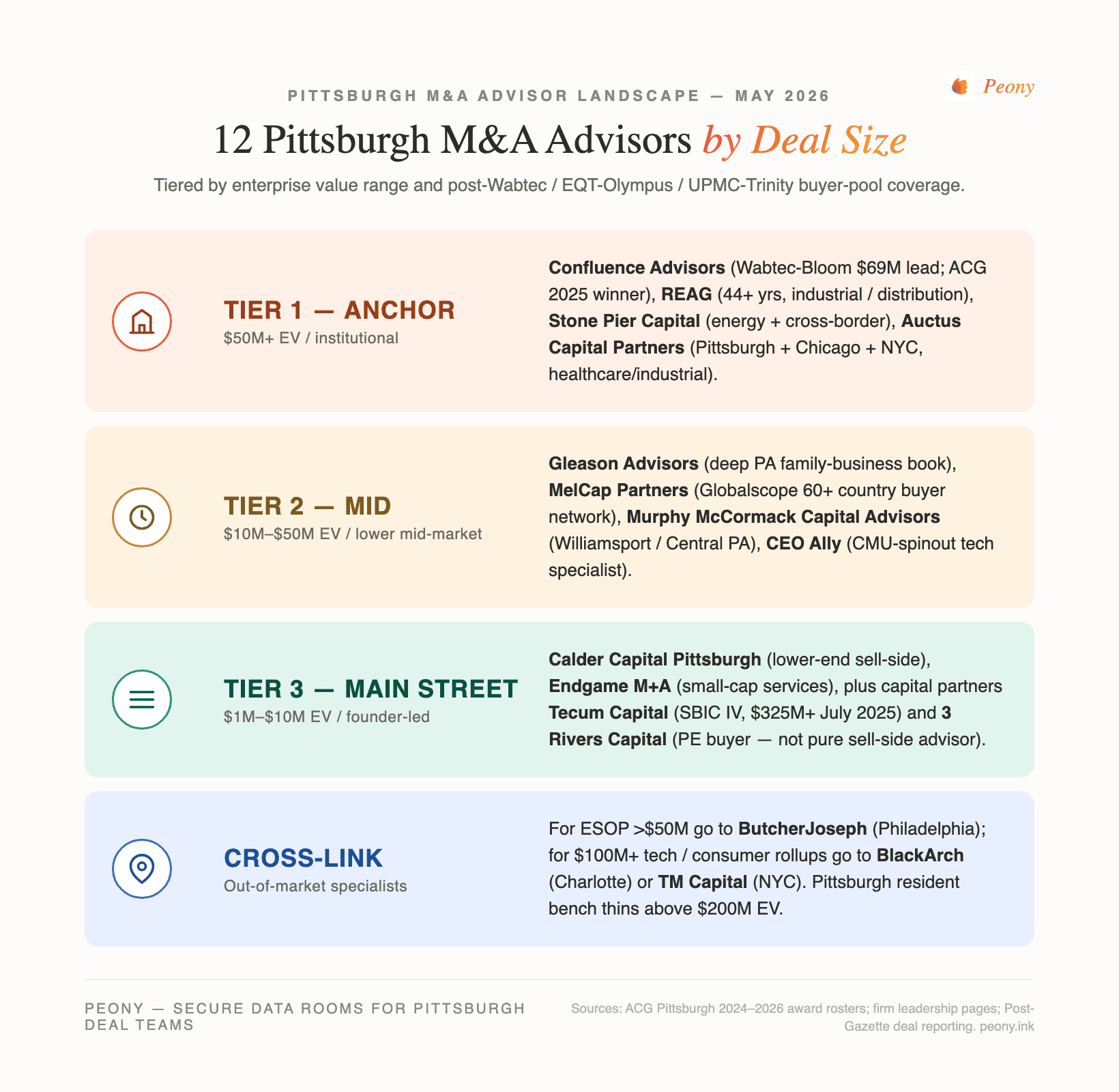

Quick answer: Pittsburgh's 12 active M&A boutiques in 2026 split across three deal-size tiers. Tier 1 ($50M+ EV): Confluence Advisors, REAG, Stone Pier Capital, Auctus Capital Partners. Tier 2 ($10M-$50M EV): Gleason Advisors, MelCap Partners, Murphy McCormack, CEO Ally. Tier 3 ($1M-$10M EV): Calder Capital Pittsburgh, Tecum Capital (mezz/SBIC capital partner, not pure sell-side), 3 Rivers Capital (PE buyer that operates like a buy-side advisor at the $3M-$10M EBITDA band), Endgame M+A. The five engines: UPMC healthcare, Wabtec/EQT industrial roll-ups, Marcellus gas services, Carnegie Mellon AI/robotics, and ESOP/family-office transitions.

Last updated: May 2026

Why Pittsburgh M&A is structurally different in 2026

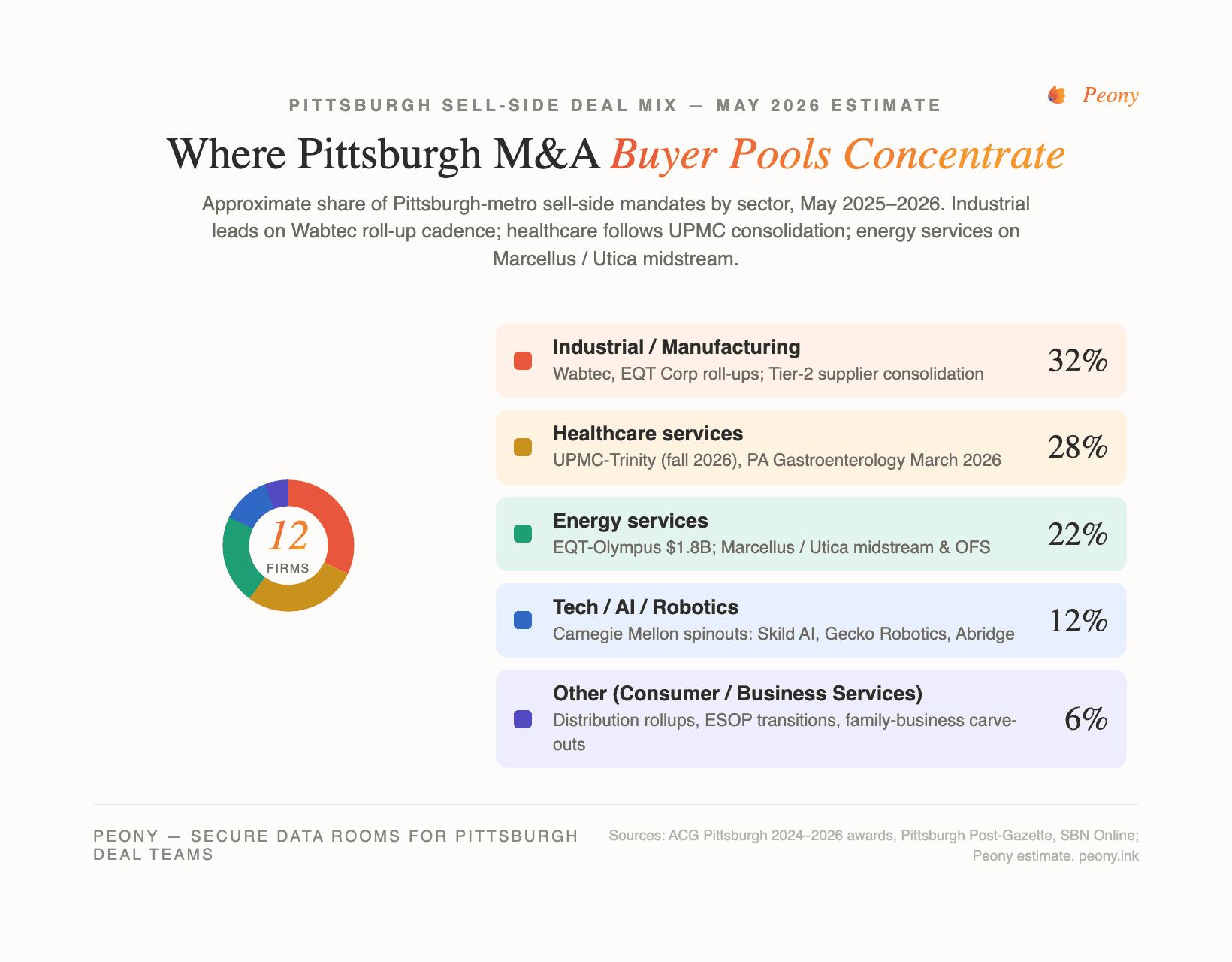

Pittsburgh has five overlapping engines driving 2024-2026 deal flow, and the structure looks like no other Rust Belt or Midwest comp.

Engine 1 — UPMC healthcare consolidation. UPMC is the largest non-government employer in Pennsylvania and is mid-build on a fall-2026 close of CommonSpirit's Trinity Health System (four Ohio hospitals) plus a March 2026 specialty add-on of Pennsylvania Gastroenterology. UPMC drives roughly 25-30% of Pittsburgh's M&A dollar volume in any given year, anchored by two or three mega-deals plus a steady tail of specialty-platform tuck-ins. Per Chief Healthcare Executive, the Trinity announcement (October 2025) is UPMC's first major Ohio expansion and signals a structural appetite for adjacent-state platforms — meaning Pittsburgh-area healthcare-services sellers in the $5M-$50M EBITDA band now have UPMC plus a PE-backed consolidator pool actively bidding.

Engine 2 — Wabtec and EQT industrial roll-ups. Wabtec closed three acquisitions totaling $2.6B+ in 2024-2025 — Bloom Engineering ($69M, December 2024, advised by Confluence Advisors), Evident Inspection Technologies ($1.78B, July 1 2025), and Frauscher Sensor Technology Group ($783.9M, December 2025). EQT Corporation (the Pittsburgh gas driller — again, not EQT AB the Stockholm PE firm) closed Olympus Energy at $1.8B on July 1 2025 after its $5.45B Equitrans Midstream close in March 2024, adding 90,000 net acres and 500 MMcf/d in the Marcellus/Utica. Together these two acquirers run a structural premium-paying cycle for Pittsburgh-area industrial and gas-services Tier-2 and specialty suppliers.

Engine 3 — Marcellus/Utica gas-services consolidation. Beyond EQT, the broader gas-services ecosystem (midstream, oilfield services, water management, completions) drives roughly 20-25% of Pittsburgh dollar volume. Olympus Energy was Canonsburg-based; Equitrans Midstream was Canonsburg-based; the Pittsburgh oil-and-gas services bench includes operating companies, capital providers, and specialty M&A advisors who run buyer-pool processes the rest of the country covers from Houston.

Engine 4 — Carnegie Mellon AI/robotics venture engine. Pittsburgh broke into the top 10 US markets for AI / autonomous-vehicle venture investment in 2025 with $1.48B in metro VC (record), 51.8% of which went to hardware/robotics per Innovation Works. Notable rounds in 2025: Skild AI $500M Series B April 2025 at $4.7B post-money, then $1.4B Series C SoftBank-led in January 2026 at $14B+ valuation, Abridge $565M across Series D + E ($2.75B then $5.3B valuation), Gecko Robotics $125M Series D at $1.25B. Per Technical.ly's Q4 2025 recap, the metro also saw 10 startup exits via acquisition in 2025. Most CMU spinout activity is still funding rounds rather than M&A — but the cohort of $10M-$300M EV CMU-tied tech founders running sub-3-year exit timelines is meaningful.

Engine 5 — ESOP and family-office succession transitions. Tecum Capital received its fourth SBIC license in July 2025 ($325M+ aggregate AUM per PR Newswire), reflecting an institutional bench dedicated to lower-middle-market Pennsylvania owner-operator exits. Pittsburgh's family-business density (rough estimate: 30-40% of operating-company GDP) plus an aging founder cohort makes ESOP a frequently-considered alternative to outright sale.

Pittsburgh activity sizing: Smart Business Network's January 2026 recap showed Pittsburgh M&A activity down 38.5% in November 2025 YoY vs November 2024, but 2025 still surpassed 2024 in aggregate. The Q1 2026 read is buyer selectivity, not capital scarcity. ACG Pittsburgh's 2025 Deal of the Year over-$50M was a $69M deal (Wabtec/Bloom), and the under-$50M was a $28M deal (Unified Doors/A.G. Mauro Company) — confirming that lower-middle-market sub-$100M EV transactions dominate Pittsburgh deal flow.

The 12 Pittsburgh M&A advisors mapped by deal-size tier

Every firm below was cross-verified through (a) the firm's current leadership page, (b) ACG Pittsburgh 2024-2026 award rosters, (c) the Axial Pittsburgh advisory firm directory, and (d) press releases for named transactions. Firms originally surfaced on industry hint lists that turned out to NOT be Pittsburgh-headquartered M&A advisors — BlackArch Partners (Charlotte HQ; see Charlotte M&A advisors for that bench), ButcherJoseph (St. Louis HQ with Philadelphia office; see Philadelphia M&A advisors), TM Capital (NYC/Atlanta/Boston, now Capstone Partners), Mosaic Capital (Charlotte), Berkery Noyes (NYC) — are excluded.

Tier 1: $50M+ EV (Lower-Middle-Market and Mid-Market Anchors)

These four firms anchor the upper end of Pittsburgh's deal flow. All four show up in ACG Pittsburgh 2024-2026 awards or have closed an anchor industrial deal in the last 18 months. If your deal is between $50M and $300M EV, you should be in conversation with at least two of these four during the pitch process.

1. Confluence Advisors LLC

- HQ: 200 Wallace Road, Wexford, PA 15090 (North Pittsburgh suburb)

- Founded: 2009

- Lead partners (current): Dan Sarver (Managing Director, ex-Westinghouse/Mellon/UPMC/Deloitte, CPA-PA inactive, FINRA Series 7/63); Dave Eichenlaub (Managing Director, founding member, 35+ years, CPA-PA inactive, FINRA Series 7/63); Christian Harsch (Managing Director, ex-TD Waterhouse, Series 7/63 via BA Securities); Jereme Frey (Director, attorney-OH, FINRA Series 79/63, ex-Prima Health Care, ex-EdgePoint Capital, ex-Key Bank); Walter Rausch (VP Business Development, ex-Fisher Scientific)

- Sectors: Distribution, chemical, testing/measurement, manufacturing, healthcare, industrial services, software, business services

- Deal-size sweet spot: $5M-$100M EV

- Track record: $2.4B+ cumulative volume since 2009

- Recent named deals (2024-2026): Wabtec acquires Bloom Engineering ($69M, closed December 2024) — ACG Pittsburgh 2025 Deal of the Year over-$50M winner per Pittsburgh Post-Gazette. Unified Doors acquires A.G. Mauro Company ($28M, April 2024) — ACG Pittsburgh 2025 Deal of the Year under-$50M winner.

- Credentials: FINRA Series 79, 63, 7 across the senior team

- Peony fits because: Confluence runs Wabtec-tier industrial processes where the buyer is publicly listed and the data-room audit trail is itself an HSR-readiness signal. Page-level analytics let Sarver and Eichenlaub see which Wabtec corp-dev associate is reading the QofE versus which is skimming the CIM — a leading indicator of bidder seriousness.

2. REAG (River's Edge Alliance Group)

- HQ: Pittsburgh, PA (plus Lancaster, PA office)

- Founded: May 2004

- Lead partners (current): Scott Mashuda (Founding Partner / CEO); Todd Torquato (Co-Founder / COO); Jaclyn Ring (Director — Mars, PA native; ACG Pittsburgh inaugural Women in Transaction honoree, 2024); Aaron Stremick (VP); Rebecca Fatica (VP)

- Sectors: Distribution and logistics, building products, chemicals, manufacturing and fabrication, electronic manufacturing services, specialty plastics

- Deal-size sweet spot: Companies up to $250M revenue, up to $25M EBITDA

- Recent named deals (2024-2026): Abraham Linc to All Surfaces (sell-side); New Angle Beveling to Aldora (sell-side); Kadee Industries to Ohio Gratings (sell-side); ChemMasters acquires Vexcon Chemicals (buy-side). Recognized as 2026 ACG Pittsburgh Non-Profit Impact Award firm.

- Credentials: Sell-side, buy-side, strategic ownership planning, debt placement

- Peony fits because: REAG runs mid-revenue family-business processes where founder cap tables are typical and bidder-pool friction is high. NDA-gated rooms with click-through e-signature let Ring's bench filter 50-buyer outreach down to the 8-12 IOI-stage bidders without leaking founder financials to the early-stage tire-kickers.

3. Stone Pier Capital Advisors

- HQ: One Oxford Centre, 301 Grant Street, Suite 270, Pittsburgh, PA 15219

- Founded: 2012

- Lead partners (current): Dale Killmeyer (Managing Director and co-founder); Charlie Schliebs (Managing Director and co-founder)

- Sectors: Lower-middle-market generalist; international buyer sourcing is a frequent specialty

- Deal-size sweet spot: $10M-$100M+ EV

- Track record: Most recent public PitchBook entry is Elizabeth Companies (2023); the firm's 2024-2026 deal flow is not enumerated on the public landing page — direct outreach recommended for current mandate verification.

- Credentials: FINRA registered (BrokerCheck Firm 142910)

- Peony fits because: Stone Pier's international-buyer practice means concurrent multi-language CIM circulation. Visitor-group separation in the data room lets Killmeyer and Schliebs run a US PE process, a European strategic process, and an Asian trading-house process from the same underlying document set without cross-contamination of who saw what.

4. Auctus Capital Partners

- HQ: 190 S LaSalle Street, Suite 1250, Chicago, IL 60603 (firm HQ); Pittsburgh satellite office (724-882-3698); New York office

- Founded: 2015

- Lead partners (current): Multi-Managing-Director bench across Pittsburgh, Chicago, and New York; direct outreach via LinkedIn recommended for current Pittsburgh MD verification

- Sectors: Industrial, healthcare and life sciences, business services, manufacturing

- Deal-size sweet spot: $5M-$200M EV

- Track record: 43 total deals (19 M&A + 24 funding rounds) since founding per Tracxn

- Recent named deals (2024-2026): United Transportation to Graxon Logistics (May 2025).

- Credentials: Healthcare and life-sciences vertical; Pittsburgh + Chicago + New York multi-office bench

- Peony fits because: Auctus' healthcare and life-sciences vertical hits Firmex's 500MB-per-file ceiling whenever imaging files or EMR exports enter the room. Peony's Data Room tier ($52/admin/month) ships unlimited storage with no per-file size cap — the file-size unlock alone saves 30-60 minutes per healthcare-deal cycle for advisors who used to splice large attachments.

Tier 2: $10M-$50M EV (Core Lower-Middle-Market Boutiques)

These four firms cover the heart of Pittsburgh's lower-middle-market — deals where founder-CEO attention runs the entire process and a single managing director can personally cover every buyer call. If your deal is between $10M and $50M EV, this tier is the primary search.

5. Gleason Advisors

- HQ: One Gateway Center, Suite 525, 420 Fort Duquesne Boulevard, Pittsburgh, PA 15222 (boutique investment banking arm of Gleason & Associates)

- Founded: Gleason & Associates founded earlier; Gleason Advisors boutique IB arm operates from Pittsburgh

- Lead partners (current): Mark M. Gleason (Founder/President/Managing Director); Raymond L. Bummer, Jr. (Managing Director); Matthew M. Hughey (Managing Director); Anthony M. Masztak (Managing Director); Matthew Gleason and Colin Gleason (Directors)

- Sectors: Construction, trades, manufacturing, transportation and logistics, retail operations, electroplating and coatings, restructuring-driven situations

- Deal-size sweet spot: Sub-$50M EV; 20 total closed deals on Axial

- Recent named deals (2024-2026): RT Patterson Company to Allied Resources Group (Pittsburgh engineering firm; Gleason exclusive financial advisor) per the Gleason Axial profile; January 2025 electroplating-sector transaction (target undisclosed).

- Credentials: Forensic and restructuring backbone — Gleason serves complex financial situations that pure sell-side boutiques typically refer out

- Peony fits because: Restructuring-adjacent deals require a heavier audit trail than clean sell-sides — every document view, download, and bidder question may end up in a creditor's exhibit list. Peony's tamper-evident activity log is the kind of record Gleason's forensic accountants already produce for litigation.

6. MelCap Partners (Cleveland HQ; Pittsburgh PA coverage)

- HQ: Cleveland, OH (Pennsylvania investment banking dedicated practice via melcap.com/areas-served/pennsylvania-investment-banking-pittsburgh-pa/)

- Founded: 2000

- Lead partners (current): Senior team includes Dan Bowman, Evan Lyons, and Anthony Melchiorre (all Principals/Directors; ACG Emerging Leaders 2025 honorees)

- Sectors: Manufacturing, distribution, business services, healthcare, consumer

- Deal-size sweet spot: $10M-$150M EV

- Track record: 99 closed deals; 2025 Globalscope Boutique Investment Bank of the Year North America

- Credentials: Member Globalscope Partners; multi-decade Ohio/Pennsylvania lower-MM bench

- Peony fits because: MelCap's manufacturing and distribution book frequently runs international buyer pools (Globalscope network is 60+ countries). Peony's visitor-group separation handles US PE versus German Mittelstand versus Japanese trading-house bidder pools cleanly — and the dynamic watermarking burns the recipient's identity into every page so any leak is traceable to the leaker.

7. Murphy McCormack Capital Advisors (Lewisburg, PA — regional PA reach)

- HQ: Lewisburg, PA (central Pennsylvania; serves the Pittsburgh region via PA-wide bench)

- Founded: 2005

- Lead partners (current): Senior bench at murphymccormack.com/our-team/; 2025 additions Tyler Johnson (Analyst) and Mike Frey (Senior team)

- Sectors: Family-owned middle-market generalist; sell-side, buy-side, valuations, financing advisory, turnaround

- Deal-size sweet spot: $10M-$100M revenue

- Track record: 47 deals total on PitchBook; AM&AA member; FINRA Series 79/63 across team

- Recent named deals (2024-2026): Quality Floors transaction (2025, general advisor) per Tracxn

- Peony fits because: Murphy McCormack's family-owned book overlaps Pittsburgh's Archetype A (second-generation industrial owner-operator). These founders default to SharePoint for file sharing — and they ship the SharePoint hangover into the diligence process. Peony NDA gates with click-through e-signature replace SharePoint without forcing the founder to learn a new VDR interface.

8. CEO Ally, Inc.

- HQ: Pittsburgh, PA

- Founded: 2006

- Lead partners (current): Founder/MD bench; direct outreach via LinkedIn recommended for current MD roster

- Sectors: Mid-market technology — IT services, Business Process Outsourcing (BPO), engineering services, cybersecurity, AI cloud services

- Deal-size sweet spot: Sub-$100M EV; 17 total deals (16 M&A + 1 funding round) since founding per Tracxn

- Recent named deals (2024-2026): Infracloud AI cloud / app modernization business to Improving, LLC (April 2025); Infogen Labs to Ciklum (February 2024); Timesys Corporation embedded and cyber business to Lynx Software Technologies (December 2023); Knack Global acquires The Faculty Practice Service (buy-side, November 2023)

- Credentials: Tech sub-sector specialist — narrowest sector-density in Pittsburgh

- Peony fits because: Tech-sector founders skewed by Y Combinator and Sequoia onto DocSend at the seed and Series A stages run into the per-user pricing trap at the M&A stage. CEO Ally's typical 15-25-bidder process at $90/user/month on DocSend is $1,350-$2,250 per month for a single deal; Peony Business at $30 per admin per month replaces the entire DocSend stack at under 5% of cost.

Tier 3: $1M-$10M EV (Boutique, Capital-Partner, and Buy-Side Specialists)

These four firms cover deals where founder EBITDA runs $1M-$5M and where the transaction is as much a capital-partner introduction as a competitive sell-side process. Two of the four — Tecum Capital and 3 Rivers Capital — are investor/buyer firms rather than pure sell-side advisors, but Pittsburgh founders in the relevant size band frequently transact WITH them, and any Pittsburgh advisor list ignoring them misses the local ecosystem.

9. Calder Capital (Pittsburgh office)

- HQ (Pittsburgh office): 1001 Liberty Avenue, Floor 5, Pittsburgh, PA 15222 (national firm HQ in Grand Rapids, MI)

- Founded: 2013 (national firm)

- Lead partner (Pittsburgh): Garrett Monroe (PA business broker and M&A advisor at Calder's Pittsburgh office) per the Calder Pittsburgh page

- Sectors: Manufacturing, distribution, construction, business services

- Deal-size sweet spot: $1M-$100M EV

- Credentials: 2025 American Business Awards (Stevie Awards) Financial Services Company of the Year (Bronze, Medium); Axial Top 10 Lower-Middle-Market M&A Advisor 2024 and H1 2025

- Peony fits because: Calder's sub-$10M EV book competes directly against business brokers who default to Dropbox or Google Drive for "data rooms." The NDA-gated link with e-signature is the single feature that converts a Calder process from "informal share folder" to "competitive sell-side process" — and it costs nothing per deal at Peony's flat-rate pricing.

10. Tecum Capital Partners (capital partner, not pure sell-side)

- HQ: 8000 Brooktree Road, Suite 310, Wexford, PA 15090

- Founded: 2005 (spun out of FNB Corporation; Cantilever Group took a strategic minority stake 2024)

- Lead partners (current): Stephen J. Gurgovits, Jr., CPA, CFA (Managing Partner — 2025 ACG Pittsburgh Lifetime Achievement Award); Matt Harnett, CAIA (Partner); Tyson Smith, CFA (Partner); David Bonvenuto (Operating Partner); Leslie Skolnekovich, CPA (CFO — 2025 ACG Pittsburgh Women in Transaction honoree)

- Sectors: Manufacturing, value-added distribution, business services; mezzanine debt plus minority equity

- Deal-size sweet spot: $3M+ EBITDA target companies; $5M-$20M per investment; $325M+ total AUM across SBIC funds per Tecum's SBIC IV announcement (July 2025)

- Recent named deals (2024-2026): SBIC Fund IV launched July 2025 ($325M aggregate); SupplyCo platform formation November 2025 (with The Armstrong Group of Companies — Huston Group + Gallaway Safety & Supply) per Tecum's PR Newswire announcement; SupplyCo December 2025 expansion adding Precision Abrasives + D&S Tool & Supply — ACG Pittsburgh 2026 Deal of the Year under-$50M winner; TPI Efficiency (Cleveland energy brokerage) mezz investment; 5280 Waste Solutions (Denver waste management) mezz investment.

- Credentials: SBIC license (SBA-regulated); CFA and CPA on senior bench

- Important distinction: Tecum is a buyer and capital partner — mezzanine debt plus minority equity — not a pure sell-side advisor. Pittsburgh founders selling at $3M-$15M EBITDA frequently transact WITH Tecum as their capital partner; if your structure is a recap or minority sale rather than a full exit, Tecum is one of two or three Pittsburgh-resident capital partners worth engaging directly. See also our independent-sponsor and SBIC playbook for business services capital partners for the broader SBIC mezzanine context. Note also: Tecum Capital (SBIC fund manager) and Tecum Equity Alpha Management (the equity affiliate driving SupplyCo) are two distinct entities — don't conflate them when structuring the engagement.

- Peony fits because: Mezz and minority-equity transactions require a different audit trail than control buyouts — the data room is shared with an LP-style investor who will continue to receive quarterly reporting through the life of the investment. Peony's continuous-access groups handle the "investor portal forever after close" use case without requiring a separate post-close platform.

11. 3 Rivers Capital (PE buyer that behaves like a buy-side advisor at the $3M-$10M EBITDA band)

- HQ: 437 Grant Street, Suite 500, Pittsburgh, PA 15219

- Founded: 2005

- Lead partners (current): Senior team listed at 3riverscap.com/meet-the-team/

- Sectors: Niche manufacturing, business services, healthcare, energy

- Deal-size sweet spot: $3M-$10M EBITDA targets; control buyouts and recapitalizations

- Recent named deals (2022-2024): Blue Chip Group, Inc. acquisition — winner of 21st Annual M&A Advisor Award M&A Deal of the Year $50M-$100M (October 2022)

- Credentials: M&A Advisor Award winner; SBA-funded SBIC adjacencies

- Important distinction: 3 Rivers Capital is a PE buyer, not a sell-side advisor — but is the cleanest Pittsburgh-resident PE buyer at the $3M-$10M EBITDA band. Pittsburgh founders selling in that band frequently transact WITH 3 Rivers, and the firm's senior partner attention on inbound deal flow makes the engagement feel closer to a buy-side advisor relationship than a pure private-equity bidder process.

- Peony fits because: PE buyers running active diligence on 8-15 platforms per year benefit from a permanent platform-level data room subscription rather than per-deal Datasite engagements that bill $15K-$50K per process. 3 Rivers' deal cadence pays back a Peony subscription in two deals.

12. Endgame M+A

- HQ: Pittsburgh, PA

- Lead partners (current): Senior bench available via direct outreach

- Sectors: Pittsburgh M&A generalist

- Deal-size sweet spot: Sub-$10M EV

- Track record: 2 closed deals on Axial — smallest player on the directory but with a senior-banker model that pitches single-MD attention as the differentiator

- Peony fits because: Single-MD firms running 3-5 simultaneous engagements need a data room that takes 30 minutes to set up, not 3 days. Peony's AI auto-indexing produces a draft folder structure from an uploaded data dump — a meaningful time save when the firm itself is the entire ops team.

How we evaluated these firms

Every firm on this list passes five filters:

1. Deal-history transparency. The firm publishes named transactions on its own website, an Axial profile, an ACG Pittsburgh award announcement, or a press release within the last 24 months. Firms with zero verifiable named transactions in the last 24 months were dropped (this caught Strategic Advisors and KenMar Capital Advisors on the Axial Pittsburgh directory — both had zero closed deals).

2. Sector specialization. The firm has a clear stated sector focus (healthcare, industrial, technology, ESOP) rather than positioning as a "generalist" with no sub-vertical depth. Sub-sector relationship density compounds — a Pittsburgh advisor who has closed five industrial roll-ups in the last 36 months runs a tighter process than a generalist who has touched 30 sectors at the surface.

3. Pittsburgh footprint. The firm maintains a Pittsburgh office staffed by senior bench (not a one-analyst satellite). Firms with no Pittsburgh-resident senior staff — BlackArch Partners (Charlotte HQ; see Charlotte M&A advisors for that bench), ButcherJoseph (St. Louis HQ with Philadelphia office; see Philadelphia M&A advisors), TM Capital (NYC/Atlanta/Boston, recently joined Capstone Partners), Mosaic Capital Partners (Charlotte) — were dropped from the Pittsburgh list and routed to their actual home-metro guides.

4. Partner stability. The firm's senior partner bench has been in place for at least 18 months. New entrants get the same scrutiny as 20-year shops: ask for personal transaction history at the partner level, not firm history. Calder Capital's Pittsburgh office is a 2-3 year build; we surface Garrett Monroe by name because partner identification matters more than firm tenure at this size.

5. Data-room competence. This is a Peony-specific filter we add to every city list, but the underlying signal is generalizable. The firm has run at least one process in the last 12 months using a modern VDR (Peony, DealRoom, FirmRoom, Ansarada) rather than email attachments or a shared Dropbox folder. Firms still defaulting to SharePoint or unencrypted file sharing at the M&A stage signal process discipline gaps that buyers notice and price into IOIs.

4 Pittsburgh founder archetypes — who hires whom

The 12 firms above map to four founder archetypes that account for roughly 85% of Pittsburgh's $1M-$300M deal flow. The other 15% is rarer profiles (cross-border acquirers buying Pittsburgh assets, venture-backed exits where the bank is national rather than local) that are better covered by national-bracket banks running from Chicago, NYC, or LA.

Archetype A — Second-generation industrial owner-operator ($5M-$50M revenue). Family-owned manufacturer, distributor, or specialty industrial business. Founder in late 50s to 60s. Succession-driven sale. Often hesitant about VDR technology because the corporate parent or their local CPA defaulted to email and SharePoint for the last 30 years. Typical advisor pairing: Confluence Advisors, Gleason Advisors, REAG, Stone Pier Capital, or Murphy McCormack — all run Pittsburgh-area industrial and distribution processes regularly and can walk a founder off SharePoint without losing them.

Archetype B — Healthcare practice or specialty rollup target ($2M-$25M EBITDA). Multi-physician practice, ambulatory surgery center, behavioral health platform; selling into a UPMC-adjacent strategic or a PE-backed healthcare consolidator. Typical advisor pairing: Confluence Advisors and Auctus Capital Partners (both have healthcare and life-sciences specialty); Tecum Capital as the regional capital partner for sub-$20M deals where the structure is a recap rather than a full sale.

Archetype C — Carnegie Mellon-spinout robotics or AI founder ($10M-$300M EV). Skild AI, Gecko Robotics, Abridge, Aurora-adjacent technology. These founders typically default to DocSend at the seed and Series A stages because Y Combinator and Sequoia onboarded them onto DocSend by default. Typical advisor pairing: CEO Ally (technology sub-sector specialist with the Infracloud, Infogen, and Timesys exits) plus a national-bracket bank from NYC, Boston, or SF for the larger $100M+ EV exits where Pittsburgh-resident senior-banker bench thins out.

Archetype D — ESOP candidate ($5M-$50M EBITDA). Family-owned Pennsylvania business considering employee ownership for tax and legacy reasons. Typical advisor pairing: Tecum Capital as the regional capital partner; ButcherJoseph's Philadelphia office (Russ Schroeder MD) for the firm-level ESOP advisory — see our Philadelphia M&A advisors guide for the ESOP-belt context. Pittsburgh itself does not have a resident ButcherJoseph-equivalent ESOP boutique, which is why the Tecum-plus-Philadelphia pairing is the canonical Pittsburgh ESOP structure.

VDR pain points specific to Pittsburgh M&A

Pittsburgh's 12 advisor firms run their data-room operations through four distinct patterns of pain — and each archetype maps cleanly to a specific VDR break point.

Archetype A — SharePoint hangover. Most second-generation industrial owner-operators arrive at the engagement with their CFO defaulting to a Microsoft 365 SharePoint folder for the "data room." SharePoint has no NDA gate, no buyer-level analytics, no document-level dynamic watermark, and no per-buyer access expiration. Advisors at Confluence, Gleason, REAG, Stone Pier, and Murphy McCormack routinely spend the first 2-3 weeks of engagement walking the founder off SharePoint and onto a modern VDR. The friction is not technical — it is the founder's resistance to changing what they've used for 30 years. Peony's NDA gate with click-through e-signature replaces SharePoint without forcing the founder to learn a new interface.

Archetype B — Firmex 500MB file ceiling. Healthcare practice and specialty rollup targets ship imaging files (DICOM exports, anonymized EMR data, ultrasound video) that routinely exceed the 500MB-per-file ceiling that most legacy VDRs (Firmex being the most common in Pittsburgh healthcare deals) enforce. Confluence and Auctus' healthcare bench has internally documented 30-60 minutes per week of advisor time lost to splitting files, re-uploading, and re-indexing — time that disappears entirely on a modern VDR with no per-file size cap.

Archetype C — DocSend per-user pricing trap at the M&A stage. Carnegie Mellon-spinout tech founders default to DocSend at the seed and Series A stages. DocSend pricing scales per-user, which breaks at the M&A stage when the bidder pool runs 15-25 names at $90/user/month — meaning a single sell-side process costs $1,350-$2,250 per month on DocSend alone. CEO Ally's tech-sector book hits this trap on every deal. Peony Business at $30 per admin per month replaces the entire DocSend stack at under 5% of cost.

Archetype D — ESOP-trustee audit-trail gap. ESOP transitions require a trustee-of-record (independent valuation expert) to run diligence on the company being transferred to the employees. Trustees produce a 60-90 page report relied on by the Department of Labor; that report is built from the diligence trail in the data room. SharePoint and Dropbox cannot produce the tamper-evident activity log that an ESOP trustee needs; Peony's audit trail satisfies the trustee's evidentiary standard by default. Tecum Capital's ESOP-adjacent transactions and ButcherJoseph Philadelphia's ESOP work both benefit from this layer.

How Peony fits. Across all four archetypes, the structural answer is the same: a modern VDR with NDA gates, per-buyer page-level analytics, dynamic watermarking with recipient identity, AI-powered Q&A on uploaded documents, and a flat $30-per-admin-per-month pricing structure that replaces Datasite's $15K-$50K-per-deal billing and DocSend's per-user trap. Peony serves 5,900+ customers across founders, M&A advisors, PE platforms, family offices, and ESOP trustees as of June 2026, and the Pittsburgh advisor bench (Confluence, REAG, Gleason, Auctus, CEO Ally, Tecum, Calder, MelCap's Pittsburgh coverage) shows up in our platform usage data alongside the 5,900+ customer cohort.

FAQs — 10 questions for Pittsburgh founders

How long does it take to sell a Pittsburgh business in 2026?

For a clean process, expect 6 to 9 months from engagement to close. Weeks 1-4 cover advisor preparation (CIM drafting, financial recasting, data-room build); weeks 5-12 cover buyer outreach (50-200 buyers contacted depending on advisor and sector); weeks 13-20 cover management presentations and IOIs; weeks 21-28 cover LOI negotiation and exclusivity; weeks 29-36 cover confirmatory diligence and close. Tighter processes run 4-6 months when the seller arrives with audited financials and a complete data room already built. Slower processes drag to 12+ months when the quality-of-earnings report surfaces unexpected adjustments, customer concentration triggers retention earnouts, or buyer scarcity requires re-marketing. Pittsburgh's industrial Tier-2 supplier processes (Wabtec-Bloom precedent) tend to land on the faster side because the named-strategic buyer pool is small and pre-known; healthcare practice processes (UPMC-adjacent) tend to land on the slower side because regulatory consents and Stark-law alignment extend the diligence window.

What percentage of the sale goes to advisor fees?

Pittsburgh M&A advisor fees in 2026 generally fall in three bands by deal size. For $1M-$10M EV deals, retainer runs $10K-$25K and the success fee is modified-Lehman style (8-10% on first $1M, 6% next $1M, 4% next $1M, then 2-3% above) producing 4-6% blended. For $10M-$50M EV, retainer runs $25K-$75K with standard Lehman (5-4-3-2-1 on the first five $1M tranches) producing 1.5-3% blended. For $50M-$300M EV, retainer runs $50K-$150K with Lehman or a negotiated tiered structure producing 1-2% blended. All Pittsburgh firms in this list credit retainer against success fee at close. Tail periods run 12-24 months; negotiate down to 12 if you can. The biggest fee variable is not the percentage — it is the minimum success fee floor that larger firms attach to engagements, which can produce uneconomic outcomes on sub-$25M EV deals.

When should a Pittsburgh founder hire an M&A advisor?

12 to 24 months before the planned close. This sounds aggressive but maps to what actually happens. Months 1-6: tax and structural planning (S-corp versus C-corp, F-reorg, ESOP feasibility, PA-specific tax structuring). Months 6-12: quality-of-earnings preparation, customer concentration mitigation, audit cycle initiation. Months 12-18: advisor selection, CIM drafting, buyer-pool definition. Months 18-24: process launch, IOI, LOI, close. Founders who try to compress this into a 6-month sprint accept 10-20% discount to fair value because the QofE comes in with unmodeled adjustments that buyers exploit during exclusivity. The fastest Pittsburgh advisors (Confluence on industrial, Auctus on healthcare, CEO Ally on tech) consistently outrun this default timeline by 4-8 weeks because they arrive at engagement with the prep work already done.

What deal-size tier am I in?

The simplest rule: take your last-12-month EBITDA and multiply by a sector-appropriate multiple. Industrial and distribution: 5-7x. Healthcare services: 7-12x (higher if UPMC-adjacent). Technology with recurring revenue: 8-15x. Energy services: 4-6x. Specialty manufacturing: 6-9x. If the resulting enterprise value lands $1M-$10M, you are in Tier 3 (Calder, Tecum capital structure, 3 Rivers buyer process, Endgame). $10M-$50M is Tier 2 (Gleason, MelCap, Murphy McCormack, CEO Ally). $50M-$300M is Tier 1 (Confluence, REAG, Stone Pier, Auctus). Above $300M EV, you are outside Pittsburgh-resident bench depth and the right answer is a national-bracket bank from NYC, Chicago, or LA running the process with a Pittsburgh-area co-advisor.

What is the difference between an M&A advisor, a business broker, and an investment bank?

A business broker covers sub-$5M EV deals, charges a higher percentage fee on a smaller absolute number, and typically works with founders who do not have audited financials or a meaningful management team beyond the owner. An M&A advisor covers $5M-$300M EV deals, charges Lehman-style retainer-plus-success-fee, and runs structured competitive processes with 30-200 buyers. An investment bank can cover any size from $50M to $5B+ EV, charges Lehman or negotiated tiered fees, runs broader buyer pools with sector-specialist teams, and increasingly maintains capital-markets sidecars (debt syndication, equity capital markets, restructuring). Pittsburgh's 12 firms break down: Calder Pittsburgh and Endgame at the broker-adjacent end; Tecum and 3 Rivers as capital partners; Confluence, REAG, Stone Pier, Auctus, Gleason, MelCap, Murphy McCormack, and CEO Ally as M&A advisors; Auctus and MelCap with the broadest international and multi-sector buyer-pool reach.

Should I sell to a PE buyer or a strategic?

Depends on three factors. Multiple expansion: strategics typically pay 30-50% premium above standalone DCF when there is clear synergy alignment (UPMC paying premium for a specialty practice; Wabtec paying premium for a railway signalling target). PE buyers pay closer to standalone multiple because they monetize through operational improvement and exit, not synergy. Speed and certainty: PE buyers can close in 4-6 months because they do not need board approval, regulatory clearance is simpler, and they have flexible capital. Strategics can take 9-12 months because they need internal approvals and may need HSR or regulatory consents. Management continuity: strategics often replace the management team within 18-24 months as part of integration. PE buyers typically retain management and roll equity into the next platform — meaning the founder's economics in the deal include a meaningful equity stake on the back end. For a Pittsburgh founder at $10M-$25M EBITDA, the right answer is often a competitive process that includes both — and lets the bid mechanics surface which buyer values you most.

What is the HSR threshold and when does it apply?

The Hart-Scott-Rodino filing threshold is $133.9 million effective February 17, 2026 (annual indexed update from the FTC). Deals at or above this threshold require pre-merger notification to the FTC and DOJ plus a 30-day waiting period (15 days for cash tender offers). The 2024-2025 expanded HSR filing form rule — which would have meaningfully expanded the documentation, valuations, deal-rationale, and minority-investor disclosures required at filing — was vacated February 12, 2026 by the US District Court for the Eastern District of Texas (Judge Jeremy D. Kernodle), meaning HSR filings revert to the pre-2024 form. For Pittsburgh deals, this means EQT-Olympus ($1.8B) and Wabtec-Evident ($1.78B) clearly trigger HSR — but most lower-middle-market Pittsburgh deals (sub-$133.9M EV) do not. If your deal is between $80M and $130M EV, build HSR contingency into the LOI exclusivity clock anyway — earnouts, escrow holdbacks, and management rollover can push deal value over the threshold if not modeled carefully.

What documents do I need ready before engaging an advisor?

The minimum 30-document set every Pittsburgh advisor expects to see in the first 30 days of engagement: 3 years of audited or reviewed financials (income statement, balance sheet, cash flow); current-year monthly P&L; quality-of-earnings memo (or commitment letter from a QofE provider); customer concentration analysis (top 10 by revenue); supplier concentration analysis; employee census with roles and tenure; org chart; sales pipeline and historical bookings; current debt schedule; lease and contract registry; intellectual-property registry (patents, trademarks, copyrights); litigation history; environmental compliance summary; tax returns (3 years federal and PA-state); 2 years of board minutes; cap table; shareholder agreement; employment agreements for top 10 employees; key customer contracts; key supplier contracts; recent valuation if any; ESOP feasibility study if relevant; insurance certificates; benefit-plan summaries; safety record (industrial); regulatory licenses (healthcare). Advisors who can populate this list in 30 days run faster processes; founders who cannot run 9-12 month processes.

How do I evaluate VDR options for my Pittsburgh deal?

Start with three filters. (1) NDA gate enforcement: the VDR must require an executed NDA with click-through e-signature before any document loads — and must log IP, timestamp, and signed NDA version for every recipient. Without this, a "data room" is a Dropbox folder with extra steps. (2) Per-recipient page-level analytics: you need to see which buyer is reading which page, for how long, and which document they are skipping. This is the leading indicator of which bidder will make an IOI versus which is window-shopping. (3) Pricing structure: legacy VDRs (Datasite, Intralinks, Firmex, Ansarada) hide pricing on their public websites and charge $15K-$50K per deal. Per-user platforms (DocSend) trap you at $90/user/month for 15-25 buyer accounts. Flat-rate platforms (Peony Business at $30 per admin per month) replace the entire stack at 5-10% of legacy cost. Peony's 5,900+ customers as of June 2026 span this exact lower-middle-market band — founders, advisors, PE platforms, and ESOP trustees who selected a flat-rate VDR after running this filter set. Our M&A data-room guide covers the full 15-platform comparison and a how-to-pick-a-VDR decision frame.

What is the Pittsburgh-specific tax angle?

Pennsylvania's corporate net income tax rate is 7.49% in 2026 (down from the 9.99% pre-Act 53 baseline; scheduled to continue phasing down to 4.99% by 2031 under Act 53 of 2022: 6.99% in 2027, 6.49% in 2028, then 0.5-percentage-point cuts annually through 2031). Pennsylvania's personal income tax is a flat 3.07% — among the lower flat-rate states. Pittsburgh adds a 3% earned-income tax on residents (plus a 1% school district tax in most of the city). Pennsylvania has a 1% realty transfer tax at the state level; inside the City of Pittsburgh, the city + Allegheny County + school district stack runs up to ~5% on top of the state rate, for a total of approximately 6% on real-estate-heavy transactions inside Pittsburgh city limits (effective since February 1, 2020). For closely-held Pittsburgh businesses considering an asset sale that includes real property, the realty transfer tax can land $300K-$600K on a $50M deal where 10-20% of value is in owned facilities. The structural responses: (1) stock sales over asset sales where possible (avoid realty transfer entirely); (2) F-reorganization to convert S-corp to LLC pre-sale to clean up tax basis; (3) UPMC-adjacent healthcare deals require additional scrutiny on PA Department of Health certifications and the new 2025 hospital tax assessment formula. Pre-sale residency planning to a no-state-tax jurisdiction (FL, TX, NV, WY, SD, TN) is increasingly common 24-36 months before the sale closes — but requires careful PA Department of Revenue scrutiny on residency clawback if rushed.

Related Peony resources

For broader M&A advisor city coverage and the data-room and diligence playbooks that sit alongside Pittsburgh-specific advice, see the following Peony resources.

- M&A advisor vs business broker vs investment bank — the decision that comes before this Pittsburgh shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- Best M&A advisors in Detroit — Rust Belt sibling city with parallel auto / industrial / mortgage roll-up patterns

- Best M&A advisors in Columbus — the central-Ohio market where Pittsburgh-rooted Schneider Downs Corporate Finance keeps a real deal office, and where capital is migrating in (Intel, data centers) ahead of the homegrown bank bench

- Best M&A advisors in Minneapolis — Midwest sibling city for lower-middle-market and ESOP-belt comparison

- Best M&A advisors in Charlotte — for BlackArch Partners and the Southeast independent-sponsor bench (Pittsburgh-orbit founders considering Sun Belt buyer pools)

- Best M&A advisors in Philadelphia — adjacent PA sibling for ButcherJoseph's Philadelphia ESOP office (the canonical Pittsburgh ESOP pairing)

- Best M&A advisors in Boston — Northeast sibling for healthcare and technology buyer-pool comparison

- M&A data room guide — canonical hub for the 15-platform VDR comparison

- M&A due diligence process guide — the diligence playbook every Pittsburgh advisor on this list expects to be ready by week 1 of engagement

- M&A trends and facts 2026 — $1.2T+ US PE deal value market context

- Best data rooms for independent sponsors — the Tecum and 3 Rivers Capital independent-sponsor and SBIC mezzanine context

- Independent sponsor business services capital partners — the SBIC and family-office capital-partner playbook

- Best data room for small M&A — how to pick a VDR for sub-$30M sell-sides, exactly the Tier 3 ($1M-$10M) and lower Tier 2 Pittsburgh deals where Datasite per-page billing and DocSend per-user pricing are uneconomic