M&A Advisor vs Business Broker vs Investment Bank: Which to Hire (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

I'm Deqian Jia, co-founder of Peony and a former VC at Backed and Target Global. I've sat alongside hundreds of lower-middle-market deal processes — founder exits, PE recapitalizations, ESOP transitions — and the question that comes before fees, before diligence, before anything, is the one owners are most confused about: who do I actually hire to sell this? A business broker? An "M&A advisor"? An investment bank? The titles blur together, the deal-size lines are fuzzy, and the wrong choice quietly costs more than any fee negotiation ever could — either by overpaying a marquee bank that ignores your deal, or by underselling through a broker whose buyer list is thinner than you think.

This is the selection guide that sits one step before our M&A advisor fees hub: that one answers what you'll pay, this one answers who you should hire. It covers what each of the three intermediaries actually does, which one fits your deal size (and the two overlap zones where size stops deciding), the four things that matter far more than the label, the 2023 federal licensing rule almost no seller knows about, and how to vet a candidate so the title on the business card doesn't fool you. Everything here is grounded in current IBBA/M&A Source market data and the federal securities statute, with sources linked throughout.

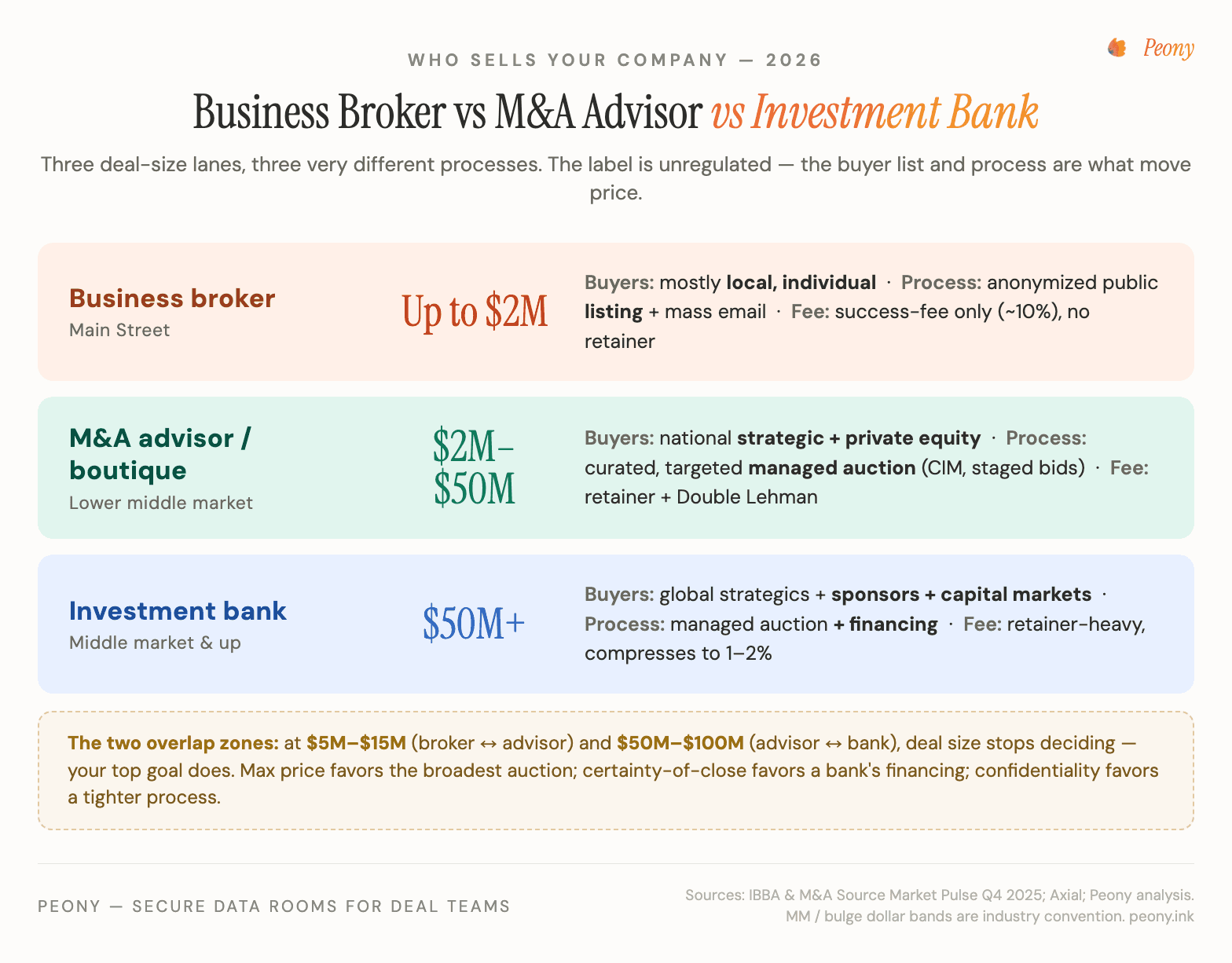

Quick answer: Match the intermediary to your deal size first. A business broker sells Main Street businesses (up to about $2 million) listing-style — an anonymized profile on public marketplaces, mostly local individual buyers. An M&A advisor / boutique runs the lower middle market ($2M–$50M) as a managed, targeted auction to strategic and private-equity buyers. An investment bank handles $50M and up and adds capital-markets muscle (financing, sponsor relationships). But size only decides the easy cases. In the contested $5M–$15M and $50M–$100M overlap zones, your primary goal decides: max price favors the broadest auction; certainty-of-close favors a bank's financing relationships; confidentiality favors a tighter process. And because "business broker" and "M&A advisor" are unregulated titles, judge any candidate on their buyer list, process, and who staffs your deal — not the words on the card.

Last updated: May 2026

What's the real difference between a business broker, an M&A advisor, and an investment bank?

All three sell companies, but they occupy different deal-size lanes and run fundamentally different processes — and the process difference matters far more than the label. Here is the honest version of each, before we get to which one fits you.

Business broker (Main Street). A business broker handles the smallest deals — what the IBBA and M&A Source call "Main Street," businesses worth up to about $2 million. The defining feature is the listing-style process: the broker posts an anonymized profile of your business on public marketplaces (think BizBuySell-style sites) and sends a mass email to a database, then waits for inbound interest. As Axial puts it, brokers take a "non-targeted approach" that "casts a wider net" but reaches mostly local, individual buyers — first-time owner-operators and serial entrepreneurs rather than strategic acquirers or private equity. Valuations are usually straightforward, the deals are often asset sales, and the broker typically works on a success-fee-only commission.

M&A advisor / boutique (lower middle market). An M&A advisor — also called a boutique, sell-side advisor, or M&A intermediary — works the lower middle market, which the IBBA defines as $2 million to $50 million in business value (many boutiques stretch to $75M–$100M). The defining feature here is a managed, targeted process: a real confidential information memorandum (CIM), a curated and named list of strategic and financial buyers, and staged bid rounds (indications of interest, then letters of intent) designed to create competition. Axial's framing is exact — the advisor "casts a more narrow net, but you get more qualified leads." This is the tier that runs an actual auction, and it's the audience for most of our M&A content.

Investment bank (middle market and up). An investment bank handles middle-market and larger deals — commonly $50 million to $500 million for middle-market banks, and $500 million-plus for the bulge bracket (those dollar bands are industry convention, not a single official cutoff). A bank runs the same managed-auction process an advisor does, but adds the thing only a bank can: capital-markets capability. A FINRA-registered broker-dealer can arrange debt and equity financing, run private placements and public offerings, tap deep sponsor and credit-fund relationships, and produce the kind of work product a sophisticated board and a credit committee expect. The FINRA Series 79 license its bankers hold is literally defined around "advising on or facilitating debt or equity securities offerings… and mergers and acquisitions."

So the one-line shorthand is: broker = Main Street listing, advisor = lower-middle-market auction, bank = middle-market auction plus financing. But hold that shorthand loosely, because — as the licensing section below explains — two of those three titles are completely unregulated, so the words tell you less than you think.

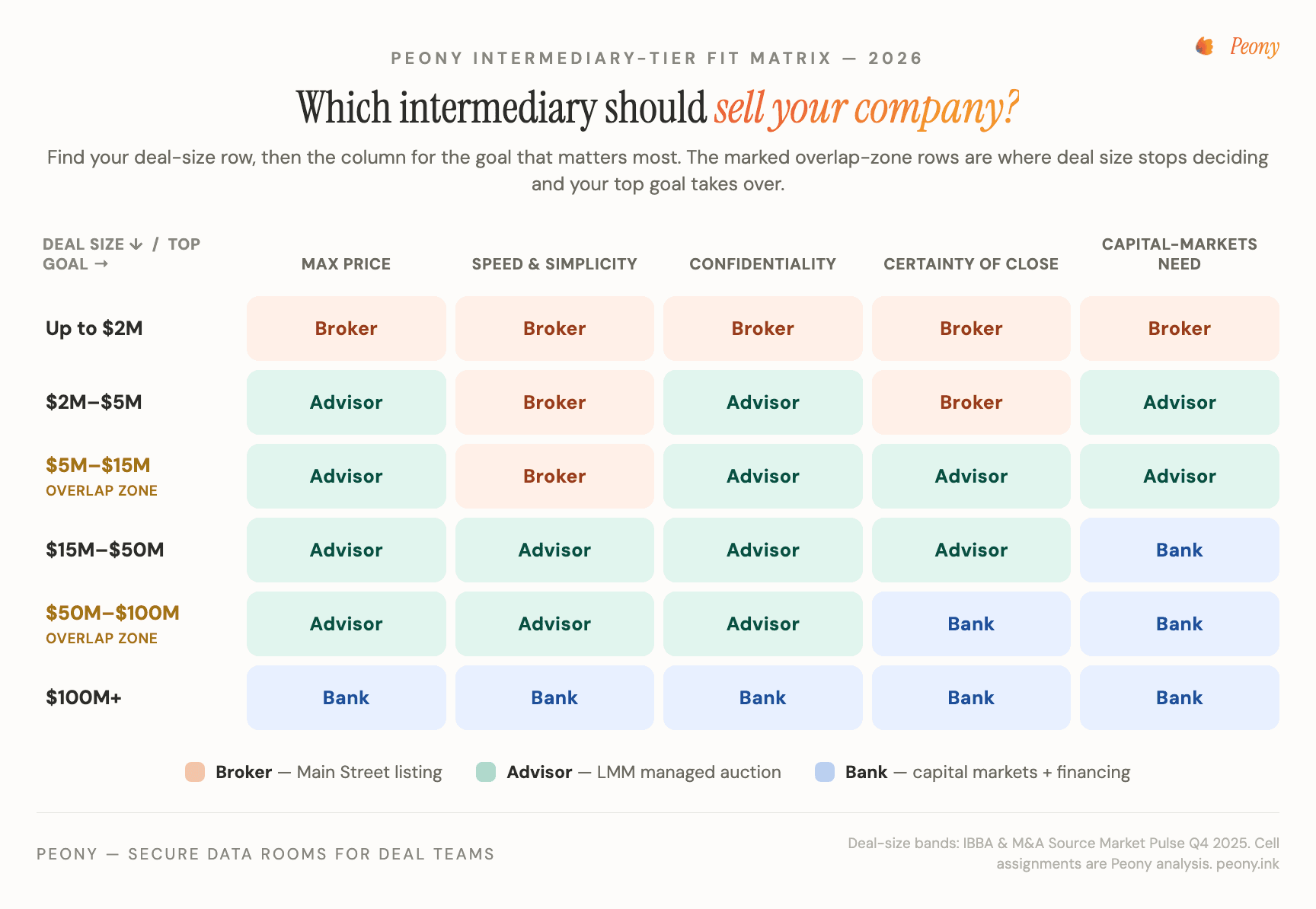

Which one do I need for my deal size?

Deal size is the first filter, and for most companies it settles the question cleanly. The complication is that the bands overlap at the edges, and in those overlap zones size stops being the deciding factor. Here's the map.

| Your deal size | Default intermediary | Why |

|---|---|---|

| Under $2M | Business broker | Main Street; a full auction is overkill and the economics don't support an advisor's retainer |

| $2M–$5M | Broker or light advisor | Transitional; minimum-fee floors start to bite (see the fee hub) |

| $5M–$15M | Overlap zone (broker ↔ advisor) | The real grey area — decided by goal, not size (below) |

| $15M–$50M | M&A advisor / boutique | Core lower-middle-market auction; strategic + PE buyers |

| $50M–$100M | Overlap zone (advisor ↔ MM bank) | Top boutiques and middle-market banks both compete here |

| $100M+ | Investment bank | Capital-markets scale, broader buyer pools, financing |

The two overlap zones are where sellers agonize, so let's resolve them directly.

$5M–$15M (broker vs advisor). Multiple industry sources independently flag the $5M–$15M range as the genuine grey zone where broker and advisor functions overlap. The deciding test is simple: will a competitive process materially raise your price? At this size your realistic buyers increasingly include private-equity platforms and strategic acquirers — and PE is about a fifth (~20%) of lower-middle-market buyers per the IBBA's Q4 2025 Market Pulse. A listing-style broker reaches a thinner, more local, more individual-buyer pool; an advisor running a targeted auction to dozens of vetted strategic and PE buyers usually creates enough price tension to more than cover the higher fee. Below about $5M, the broker's economics win; once you're solidly into eight figures with strategic or PE appeal, the managed auction usually does.

$50M–$100M (advisor vs middle-market bank). Here the top of the lower-middle-market band meets the bottom of the bank band, and both can execute. Size no longer decides — capability does. A strong sector-specialist boutique with the right buyer relationships can out-execute a bank that staffs your deal with junior bankers (more on that "Attention Cliff" below). A middle-market bank earns the premium when you need financing arranged, a public-company or cross-border counterparty, or board/credit-committee-grade work product. For a clean strategic or PE sale at this size, a top boutique is frequently the better choice.

The cleanest way to resolve both overlap zones is to layer your primary goal on top of deal size. That's the matrix below.

The matrix encodes the Overlap-Zone Tie-Breaker: in the contested bands, rank your goals. If max price is the single objective, the breadth of the competitive auction wins (advisor or bank over broker). If certainty-of-close outranks top dollar, a bank's financing relationships and process discipline matter more. If confidentiality is paramount, a tight, targeted process beats a public listing every time. And if speed and simplicity on a small, clean deal matter most — especially with a known buyer already circling — a broker (or a lightly scoped advisor) is the rational pick.

Beyond deal size, what actually separates the three?

Deal size tells you the lane, but it doesn't tell you whether a specific intermediary is any good. Four axes do — and they explain why two firms with identical titles can deliver wildly different outcomes.

1. Buyer-universe reach — the axis that drives price. This is the single biggest differentiator and the most invisible in a sales pitch. A broker's anonymized listing surfaces a wide but shallow pool of mostly local, individual buyers (on Main Street, IBBA Q4 2025 data shows buyers are ~46% first-time and ~32% serial entrepreneurs). An advisor's curated outreach targets a national list of strategic acquirers plus private equity. A bank layers on global strategics, sponsor relationships, and capital-markets distribution. The reach difference is not cosmetic — it's the whole game, which is why it gets its own frame below.

2. Process intensity — listing vs managed auction. A broker "lists and waits." An advisor or bank runs a managed competitive auction: teaser → NDA → CIM → curated outreach → staged IOI and LOI bid rounds → management presentations → confirmatory diligence → close. Wall Street Prep's sell-side process breakdown lays out those phases; a full managed process generally runs 6 to 12 months from engagement to close (Trout Capital). The managed process is more work, costs more, and — when buyers are competitive strategics and sponsors — usually produces a higher price and more certainty. (The exact timeline difference between a broker listing and a bank auction is directional, not fixed: simple Main Street listings can close faster, while larger regulated deals run longer once antitrust review enters the picture.)

3. Who actually runs your deal — the Attention Cliff. This is the frame that saves sellers the most regret. Senior attention follows fee size. At a boutique, the partner who pitched you typically runs your engagement end to end, because it's a headline mandate. At a bulge-bracket bank, that same $20M–$50M deal is a bottom-tier file staffed down to junior bankers and analysts, because the firm's senior talent is pulled toward nine- and ten-figure fees. The same $20 million deal is a top-tier client at a boutique and a rounding error at a marquee bank. The brand on the pitch book is not the attention on your deal — and in the $20M–$75M zone, sellers routinely get more senior attention from a focused boutique than from a famous logo.

4. Fee and incentive shape — by type. The three tiers price differently in shape, not just level. Brokers are usually success-fee-only (often a ~10% commission on small deals, or a Double Lehman scale), with little or no retainer. Advisors add a monthly work fee ($5,000–$10,000) plus a Double Lehman success fee plus a minimum — more than 70% of advisors charge some engagement or retainer fee (Axial, 2023 data). Banks are the most retainer-heavy, with the largest minimums and longest tails, and a success-fee rate that compresses toward 1–2% as deals get large. The full benchmark curve and the engagement-letter mechanics live in the M&A advisor fees guide — I won't re-derive the math here; what matters for selection is that as you move up the tiers, more of the cost moves upfront and the percentage falls.

What does each option look like on the same $25M company?

To make those four axes concrete, picture one company — a profitable, founder-owned business worth about $25 million — taken to market three ways. (The price outcomes below are directional on purpose: there's no clean published figure for how much more a competitive auction yields, so I won't invent one. What differs measurably is buyer reach and senior attention.)

Through a business broker. The broker posts an anonymized profile to public marketplaces and emails a database. At $25M that pool is thin and largely mismatched — Main Street marketplaces skew to individual buyers shopping for businesses a fraction of this size. You surface a handful of mostly-local, mostly-individual prospects. Fast and cheap, but the buyer competition that actually drives price barely forms. This is the undersell risk made concrete: the strategic or PE buyer who would pay the most probably never sees the deal.

Through an M&A advisor. The boutique builds a CIM and runs a targeted auction to a curated, named list of perhaps 40 to 60 strategic acquirers and private-equity platforms — and with PE at about a fifth of lower-middle-market buyers, sponsors are a real slice of that list. Staged IOI and LOI rounds put those buyers in direct competition, and the partner who pitched you runs the process. At $25M this is the fit: the managed auction's breadth is exactly what turns a "fair" offer into a competitive one.

Through a bulge-bracket bank. The bank could run that same auction — but at $25M your deal sits below its economic attention line. You get the logo on the cover and a junior team turning the pages (the Attention Cliff). Unless you specifically need financing arranged or a public-company counterparty, you're buying prestige that doesn't convert into senior attention on a deal this size.

Same company, three very different buyer universes and three very different levels of senior attention. The fee gaps across the three are real but secondary — the buyer-universe and attention gaps are what move the outcome. That's the Buyer-Universe Multiplier inside a single deal, and it's why the matrix above routes a clean $25M sale to an advisor, not up to a bank or down to a broker.

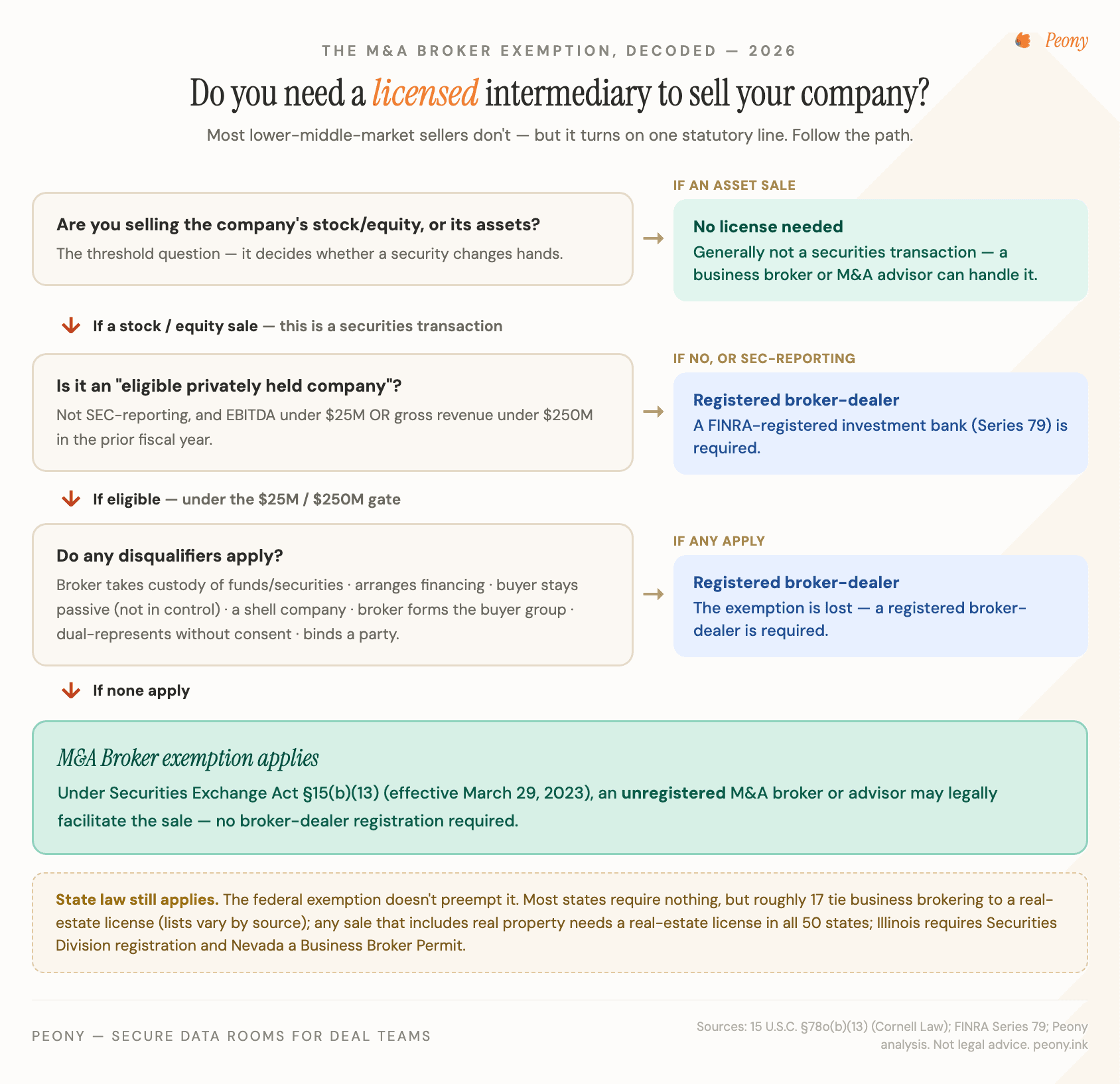

Does a business broker or M&A advisor need a license to sell my company?

This is the section almost no seller knows to ask about, and it's the highest-information-gain fact in the whole comparison, because it's statutory, not folklore. The short version: "business broker" and "M&A advisor" are unregulated job titles — there's no license legally required to use either one — while an investment bank is a FINRA-registered broker-dealer whose deal staff must hold the Series 79 (Investment Banking Representative) qualification and, in practice, the Series 63. So the regulatory floor is wildly different across the three, and most sellers never realize it.

The reason an unlicensed advisor can legally sell your company at all comes down to a distinction and a 2023 federal law.

Stock sale vs asset sale — the distinction that triggers everything. Selling a company's assets generally doesn't involve a security, so brokering an asset sale has never required securities licensing. Selling the company's stock or equity is a securities transaction — and historically, brokering a stock sale for a fee could require registering as a broker-dealer. That's the legal tripwire that the M&A Broker exemption was written to clear.

The federal M&A Broker exemption (the one rule to know). In late 2022, Congress passed Section 501 of the Consolidated Appropriations Act, 2023, creating a permanent statutory exemption codified at Securities Exchange Act Section 15(b)(13) (15 U.S.C. Section 78o(b)(13)). It became effective March 29, 2023, and on that date the SEC withdrew its older 2014 M&A Broker no-action letter (Sidley). The exemption lets an eligible "M&A broker" facilitate the transfer of ownership of a privately held company — including a stock sale — without registering as a broker-dealer with the SEC.

But the exemption is narrow, and the eligibility line is what I call the $25M / $250M Gate. Your company qualifies as an "eligible privately held company" only if, in the fiscal year before you engaged the broker, it had EBITDA under $25 million or gross revenue under $250 million — and it isn't an SEC-reporting public company. That single line cleanly separates "an unregistered M&A broker may legally handle this stock deal" from "you need a registered broker-dealer." The exemption also evaporates if any of these are true (15 U.S.C. Section 78o(b)(13); Sidley):

- the broker takes custody or control of funds or securities in the deal;

- the broker provides or arranges financing for the transfer;

- the buyer ends up passive — to qualify, the buyer must end up in control of the company and active in its management;

- a shell company is involved (other than in a bona fide business combination);

- the broker assembles the buyer group (one formed with the broker's assistance) or runs a blind pool;

- the broker represents both sides without written consent, or binds a party to the deal;

- the broker has been suspended or barred from broker-dealer association.

And one crucial caveat: the federal exemption does not preempt state law. A state can still require registration unless it has its own comparable exemption.

State licensing — mostly nothing, with exceptions. At the state level, most states require no license at all to call yourself a business broker. A commonly cited tally is that roughly 17 states tie business brokering to a real-estate license or a dedicated permit, while the rest have no specific oversight — but the exact list differs between sources, so verify your own state with its licensing board before relying on it. Two reliable specifics: in all 50 states, if the sale includes real property (a building, or a real-estate lease transfer), a real-estate license is required for that piece; and a few states are special cases — Illinois requires business-broker registration with the Secretary of State's Securities Division, and Nevada requires a dedicated Business Broker Permit (Business Brokerage Press).

The takeaway — the Title Trap. Put it together and you get the most important diligence lesson in this guide: because the titles are unregulated, the words on the business card are non-diagnostic. "M&A advisor" can describe a solo lister or a 20-deal sector specialist. There are optional voluntary credentials — FINRA recognizes the RM&AA designation, and the IBBA confers the CBI — but they're badges, not licenses, and not required. So don't sort candidates by their title. Sort them by their buyer list, their process, who staffs your deal, and — if a security will change hands — whether they're exemption-eligible or a registered broker-dealer.

How do I choose — and what should I ask before I sign?

Selection is a two-step move: size sets the lane, your primary goal breaks the tie, and specific questions verify the fit. You've done the first two with the matrix above. Here's how to verify a specific candidate so the Title Trap doesn't catch you.

Ask every candidate the same concrete questions, and listen for numbers and names, not adjectives:

- "How many buyers will you contact directly, by name — and what's the strategic-versus-PE split?" A real advisor says something like "40 to 60 targeted buyers, roughly a third private equity." A lister deflects to "we have a huge database."

- "Show me closed deals in my sector and size from the last two years." Recent, relevant comps are the single best predictor of a real buyer network.

- "Who, specifically, will run my deal day-to-day?" This surfaces the Attention Cliff before you sign. If the pitch partner won't be doing the work, find out who will.

- "Is it a managed process or a listing?" Will they build a CIM, run staged bid rounds, and manage diligence — or post a profile and wait?

- "What's your fee structure, and is the retainer creditable against the success fee?" This is where you hand off to the fee and engagement-letter playbook.

- "What tail and exclusivity are you asking for?" Long exclusivity with auto-renewal is a red flag; the fee hub covers how to cap both.

The red flags that you've hired (or are about to hire) the wrong intermediary all point the same direction — a listing dressed up as a process: a thin or vague buyer list; pressure to cut your price quickly instead of creating competition; no CIM or real marketing materials; a generic buyer pool with no named strategics or sponsors; an 18-to-24-month exclusivity lock; an uncreditable retainer with no work plan; and an inability to name recent closed deals. If, two months into an engagement, you're not seeing named outreach, signed NDAs, and a real bidder funnel, you hired a lister, not a dealmaker.

Finally, the highest-leverage move in the entire selection process: get two or three competing proposals in writing. The price tension between firms that each want your mandate is the most reliable way to both test fit and improve terms — and it's exactly the discipline most first-time sellers skip. For the metro-by-metro benches of brokers, boutiques, and banks to run that bake-off against, our M&A advisor city directory maps who's who in each major market.

How do fees compare across the three — and is the bank worth it?

Fees differ across the tiers in shape more than in headline level, and I'll keep this to the type-level pattern — the full benchmark curve, the Lehman math, retainer-creditability, minimums, and the clauses that inflate the base all live in the M&A advisor fees guide. The pattern that matters for choosing:

- Business broker: typically success-fee-only — often around a 10% commission on small deals, or a Double Lehman (10-8-6-4-2) scale — with little or no retainer, because there's little upfront preparation work.

- M&A advisor: a monthly work fee ($5,000–$10,000) plus a Double Lehman success fee plus a minimum fee. More than 70% of advisors charge some engagement/retainer fee. The blended effective success fee runs roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M per the most recent industry fee guide.

- Investment bank: the most retainer-heavy, with the largest minimum fees and longest tail periods, and a success-fee rate that compresses toward 1–2% as deals scale up.

As you climb the tiers, more of the cost shifts upfront and the percentage falls — because the deals are bigger.

Now the question sellers actually mean when they ask about fees: is the more expensive option worth it? Here's the frame I use, the Buyer-Universe Multiplier. The money is rarely in the two or three fee points you'd save by going down a tier — it's in the price delta from a process that puts more competing buyers in the room. A managed auction that reaches 30 to 50 vetted strategic and PE buyers can move the final price by far more than the fee difference, while a listing that surfaces five mostly-individual buyers structurally leaves money on the table. With PE at ~20% of lower-middle-market demand, a process that fails to reach sponsors ignores a fifth of the buyer universe before it starts. The fee you save is linear; the price delta from competition is the multiplier.

That reframes the "is a bank worth it on a $50M sale?" question. The bank earns its premium when the deal genuinely needs capital-markets execution — arranging buyer financing, a public-company or cross-border counterparty, a financed recap, credit-committee-grade work product. If it's a clean strategic or PE sale and a strong boutique can run a tighter, more senior-staffed auction with a deeper sector buyer list, the boutique often delivers a higher price at a lower fee. Choose the bank for capability you actually need — not for the logo.

Where does the data room fit?

I run Peony, a data room company, so let me be precise about where we sit in this picture — because it's the same for all three intermediaries. Whether a broker, a boutique advisor, or an investment bank runs your sale, the moment real buyers show interest, they need a secure place to do diligence — and that's the virtual data room. We don't replace the intermediary; we're the room the intermediary runs your buyers through.

Here's the honest, segmented version. If your advisor or bank is running a large, multi-hundred-buyer auction with complex permissioning, a legacy enterprise data room may be the right tool, and you'll pay enterprise prices for it. But most lower-middle-market sell-side processes don't need that. A flat-rate room — Peony Business is $30 per admin per month — covers the same NDA-gated, page-level-analytics workflow purpose-built for M&A sell-side processes. The per-recipient analytics and dynamic watermarks tell you and your advisor which buyer is actually reading the confidential information memorandum versus window-shopping — the leading indicator of who will make a real offer, and exactly the buyer-engagement signal that separates a managed process from a listing. That's why 5,900+ customers — founders, business brokers, M&A boutiques, PE platforms, and ESOP trustees across all three tiers — run their diligence on Peony.

The broader point isn't about us: the discipline you bring to choosing the right intermediary should extend to the tools that intermediary bills you for. 5,900+ customers chose a flat-rate room after running exactly that math, and whichever tier you land on, the data room is one of the few line items where your own choice directly controls the cost.

Frequently asked questions

What's the real difference between a business broker, an M&A advisor, and an investment bank?

All three sell companies, but they occupy different deal-size lanes and run fundamentally different processes. A business broker handles Main Street deals — businesses worth up to about $2 million in the IBBA's definition — and works listing-style: an anonymized profile on public marketplaces plus a mass email blast, drawing mostly local, individual buyers. An M&A advisor (or boutique) works the lower middle market, roughly $2 million to $50 million, and runs a managed, targeted process — a confidential information memorandum, curated outreach to strategic and private-equity buyers, and staged bid rounds. An investment bank handles middle-market and larger deals (commonly $50 million and up) and adds capital-markets muscle: debt and equity financing, sponsor relationships, and the work product sophisticated boards expect. The shorthand is broker = Main Street listing, advisor = lower-middle-market auction, bank = middle-market auction plus financing — but the labels themselves are unregulated, so what actually matters is the buyer list, the process, and who staffs your deal.

Is my company too small for an investment bank?

Probably, if you're under about $50 million in enterprise value — but that's a feature, not a rejection. Most middle-market investment banks won't actively pursue deals below roughly $25 million to $50 million, and even when they accept a smaller one, it becomes a bottom-tier mandate staffed by junior bankers (what I call the Attention Cliff). A lower-middle-market M&A advisor whose entire book is $5 million to $50 million deals will give a $15 million sale partner-level attention and a real buyer auction. So the honest answer is: if your deal is under $50 million, you usually don't want a bulge-bracket bank — you want a boutique advisor who treats your deal as a top client, not a marquee logo that treats it as a rounding error. The exception is when you specifically need capital-markets execution (a financed recap, a public-company buyer, cross-border complexity) — then a middle-market bank earns its place even at the smaller end.

Do I need an investment bank to sell a $40-50M company, or is an M&A advisor enough?

At $40 million to $50 million you're in the upper end of the lower-middle-market band and the lower end of the middle-market-bank band — a genuine overlap zone where both can do the job. The deciding factor isn't size; it's your primary goal. If you want the broadest competitive auction and a sector-specialist buyer list, a strong boutique M&A advisor will often out-execute a bank that staffs your deal junior. If you need financing arranged for the buyer, a public-company or cross-border counterparty, or work product that satisfies a credit committee and a sophisticated board, a middle-market investment bank's capital-markets capability is worth the premium. For a clean, all-cash sale to a strategic or PE buyer at this size, a top boutique advisor is usually enough — and frequently better, because you'll get more senior attention.

I'm selling a ~$10-15M business — is a business broker enough, or do I need an M&A advisor?

This is the most contested range in the whole market — the $5 million to $15 million zone where broker and advisor functions genuinely overlap. The test is whether a competitive process will materially raise your price. At $10 million to $15 million, your likely buyers include private-equity platforms and strategic acquirers, not just the individual buyers a listing-style broker reaches — and private equity is about a fifth of lower-middle-market buyers (IBBA Q4 2025). A business broker who lists you on public marketplaces will reach a thinner, more local pool; an M&A advisor running a targeted auction to 30-50 vetted strategic and PE buyers usually creates enough price tension to more than cover the higher fee. Below about $5 million a broker's economics make sense; once you're solidly into eight figures with strategic or PE appeal, the managed auction usually wins. If a single known buyer is already at the table and speed and confidentiality outrank top dollar, a broker or a lightly scoped advisor can still be the right call.

Will a bulge-bracket bank actually take my $20-30M deal seriously?

Rarely in the way you'd hope — and this is one of the most expensive misconceptions sellers carry. A marquee bank's senior bankers are economically pulled toward the largest fees, so a $20 million to $30 million mandate (well below their typical $50 million-plus focus) tends to get staffed down to junior bankers and analysts. The brand on the pitch deck is not the attention on your deal. I call this the Attention Cliff: the same $20 million deal that is a bottom-decile file at a bulge bracket is a top-tier, partner-staffed client at a focused boutique. Unless you specifically need that bank's capital-markets or cross-border capability, a lower-middle-market advisor whose whole business is your deal size will give you more senior attention, a more tailored buyer list, and usually a better outcome. Prestige is not the same as effort.

How do I know if a broker or advisor has a real buyer list and not just a listing?

Ask specific, verifiable questions and watch whether the answers are concrete. Real managed-process questions: How many buyers will you contact directly, by name, and how many are strategic versus private equity? Can you show recent closed deals in my sector and size? Will you prepare a confidential information memorandum, or just a teaser listing? Do you run staged bid rounds, or post my business and wait? A genuine advisor answers with numbers — 'we'll approach 40 to 60 targeted buyers, roughly a third private equity' — and named, recent comps. A listing-style operator deflects to the size of a marketplace's audience or generic 'we have a huge database' claims. The tell is specificity: a real buyer list is a curated, named set of acquirers the advisor can already picture for your company; a listing is a hope that the right buyer happens to be browsing.

Does a business broker or M&A advisor need a license to sell my company?

Often no license is legally required — and the reason is a 2023 federal law most sellers have never heard of. 'Business broker' and 'M&A advisor' are unregulated titles; investment banks, by contrast, are FINRA-registered broker-dealers whose deal staff hold the Series 79 license. The bridge is the federal M&A Broker exemption (Securities Exchange Act Section 15(b)(13), effective March 29, 2023), which lets an eligible broker facilitate the sale of a privately held company without registering as a broker-dealer — but only if the company had EBITDA under $25 million or gross revenue under $250 million in the prior fiscal year, and only under strict conditions (no taking custody of funds, no arranging financing, the buyer must end up in control and active in management, and more). The distinction that triggers all this is stock versus assets: a stock sale is a securities transaction, so brokering it for a fee needs either the exemption or a registered broker-dealer; an asset sale generally is not a security. The federal exemption also doesn't override state rules — most states require nothing, but roughly 17 tie business brokering to a real-estate license (lists vary by source), and any sale that includes real property requires a real-estate license in all 50 states.

Business broker, M&A advisor, M&A intermediary — do these titles mean the same thing?

Functionally they overlap, and legally the titles mean almost nothing — which is exactly the trap. Because 'business broker,' 'M&A advisor,' 'intermediary,' and 'sell-side advisor' are all unregulated labels (only 'investment bank' implies a FINRA-registered broker-dealer), two people with the identical business card can be a solo operator who lists businesses and a 20-deal sector specialist who runs full auctions. The title tells you nothing about buyer reach, process quality, or track record. I call this the Title Trap: stop sorting candidates by what they call themselves and sort them by four things instead — their actual buyer list and recent closed comps in your sector, whether they run a real managed process or a listing, who staffs your deal day-to-day, and, if a security will change hands, whether they're exemption-eligible or a registered broker-dealer. Judge the work, not the word.

How do I choose the right intermediary, and what should I ask before signing?

Start from your deal size and your single most important goal, then verify fit with specific questions. Size sets the lane (Main Street broker under about $2 million; lower-middle-market advisor $2 million to $50 million; investment bank $50 million and up), but in the overlap zones your primary goal decides — max price favors the broadest auction, certainty of close favors a bank's financing relationships, confidentiality favors a tighter targeted process. Before signing, ask: How many named buyers will you approach, and what's the strategic-versus-PE split? Show me closed deals in my sector and size from the last two years. Who specifically will run my deal day-to-day? What's your fee structure, and is the retainer creditable against the success fee? What tail and exclusivity are you asking for? Then get two or three competing proposals in writing — the price tension between advisors who each want the mandate is the most reliable way to both test fit and improve terms. The full fee and engagement-letter playbook is in our companion guide.

What are the red flags that I've hired the wrong intermediary?

The clearest warning signs all point to a listing dressed up as a process. Watch for: a thin or vague buyer list ('we'll post it and see who bites'); pressure to drop your asking price quickly rather than create competition; no confidential information memorandum or real marketing materials; a generic buyer pool with no strategic or private-equity names; an 18 to 24 month exclusivity lock with an auto-renewal; an uncreditable retainer with no clear work plan; and an advisor who can't name recent closed deals in your sector. A broker who only has a couple of buyers, or who seems to want a fast close more than a high price, is optimizing for their own throughput, not your outcome. If the engagement starts and you're not seeing named outreach, signed NDAs, and a real bidder funnel within the first couple of months, you likely hired a lister, not a dealmaker — and the tail and exclusivity clauses are exactly why you read them before you signed.

Business broker commission vs M&A advisor success fee vs investment-bank fee — how do they compare?

The shapes differ more than the headline percentages. Business brokers are usually success-fee-only, often a flat commission around 10% on small deals (or a Double Lehman scale), with little or no retainer. M&A advisors layer a monthly work fee of $5,000 to $10,000 plus a Double Lehman success fee plus a minimum fee — more than 70% of advisors charge some engagement or retainer fee (Axial, 2023 data). Investment banks are the most retainer-heavy and carry the largest minimum fees and longest tail periods, with the success-fee rate compressing toward 1-2% as deals get large. The pattern: as you move up the tiers, more of the cost shifts upfront and the percentage falls, because the deals are bigger. For the actual benchmark curve — roughly 4.8% at $5 million, 3.4% at $20 million, 2.0% at $100 million — plus the Lehman math, retainer-creditability, minimums, and the engagement-letter clauses that inflate the base, see our dedicated M&A advisor fees guide; this post covers which intermediary to hire, that one covers what you'll pay.

Are investment-bank fees worth it on a $50M sale versus a boutique advisor?

It depends entirely on whether you need what the bank uniquely provides — and on a straight sell-side at $50 million, often you don't. Here's the frame I use, the Buyer-Universe Multiplier: the money is rarely in the two or three fee points you'd save, it's in the price delta from the process that reaches more competing buyers. If a boutique advisor with a deep sector buyer list runs a tighter, more senior-staffed auction than a bank that staffs your deal junior, the boutique can deliver a higher price at a lower fee — a double win. The bank earns its premium when the deal genuinely needs capital-markets execution: arranging buyer financing, a public-company or cross-border counterparty, a financed recapitalization, or work product for a credit committee. So at $50 million, choose the bank for capability you actually need, not for the logo — and if it's a clean strategic or PE sale, a strong boutique is frequently the better economic choice.

Related Peony resources

The companion fee guide, the city-by-city advisor benches, and the deal-mechanics playbooks that sit alongside choosing an intermediary:

- M&A advisor fees: Lehman scale, retainers & hidden clauses — the companion hub: once you've chosen the tier, this is exactly what you'll pay and how to negotiate the engagement letter

- Best M&A advisors in NYC and Chicago — metro benches spanning the broker / boutique / investment-bank spectrum this guide compares, to run a two-or-three-firm bake-off

- Best M&A advisors in Dallas and Houston — energy and industrial benches where banks and boutiques overlap in the $50M-$100M zone

- Best M&A advisors in Richmond — the single best city bench for seeing this guide's distinctions in the wild: a national mid-market bank (Harris Williams), registered pure-play boutiques, legitimate exemption-model advisors, and a wealth-manager-in-disguise trap, all in one metro

- Merger vs acquisition: what's the difference? — the deal-type comparison that pairs with this intermediary-type comparison

- M&A due diligence process guide — the workstreams your chosen intermediary will run buyers through

- M&A data room guide — the full 15-platform comparison behind the diligence-room line item

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, the right-sized room once you've picked your intermediary for a smaller deal

- M&A trends and facts 2026 — the macro backdrop, including the seller's-market conditions shaping 2026 processes