M&A Advisor Fees: Lehman Scale, Retainers & Hidden Clauses (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

I'm Deqian Jia, co-founder of Peony and a former VC at Backed and Target Global. I've advised on hundreds of lower-middle-market deal processes — founder exits, PE recapitalizations, venture financings, and ESOP transitions — and the same thing happens almost every time an owner gets their first engagement letter from an M&A advisor: they read the headline percentage, decide it sounds reasonable, and sign. Then, months later at closing, the fee is a number they didn't expect. The headline rate was never the bill. The engagement letter was.

This guide is the canonical fee reference behind our 21-city M&A advisor directory — the page that answers the one question every one of those city guides gets asked: what will the advisor actually cost me? It covers what M&A advisors charge in 2026 by deal size, how the Lehman and Double Lehman formulas really work (with the math), how retainers and minimum fees change your effective rate, and — the part almost no one explains well — the four or five clauses in the engagement letter that quietly inflate what you pay. Everything here is grounded in the most recent industry fee surveys and the engagement-letter analyses published by M&A law firms, with sources linked throughout.

Quick answer: In 2026, a lower-middle-market sell-side advisor typically charges an effective success fee of about 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex/Axial M&A Fee Guide, 2024-25). The workhorse structure is the Double Lehman (10-8-6-4-2) — $600,000 on a clean $20M deal — plus a $5,000-$10,000/month work fee that usually credits against the success fee. The real cost lives in the fine print: how the letter defines "transaction value" (debt, earnouts, and rollover equity can inflate the base), the tail period, and the expense cap. All-in on a $20M sale runs roughly $630,000-$710,000 (3.2-3.6% of your equity) — and a single sentence about assumed debt can move that by $80,000.

Last updated: May 2026

What does an M&A advisor actually charge in 2026?

An M&A advisor's fee has three parts, and only one of them is the number you remember. There's a retainer or work fee paid during the process (often $5,000-$10,000/month), a success fee paid at closing (a percentage of "transaction value"), and expense reimbursement on top. The success fee is the headline, but the other two — plus how the letter defines the base the success fee multiplies — are where sellers get surprised.

The timing matters in 2026 specifically. U.S. middle-market deal count was down roughly 20% year-over-year in January and February 2026, with the quarter's total value propped up by a handful of large transactions rather than broad activity (SellSide Group Q1 2026; EY). Yet the lower middle market is the bright spot: sponsor-led volume hit roughly $1.2 trillion in 2025, up 36.3% and the second-highest on record (Sidley), and surveyed dealmakers are optimistic — about 70% expect 2026 to beat 2025, and the IBBA & M&A Source Market Pulse for Q4 2025 reports 76-89% cash at close with earnouts used sparingly. Translation: more owners are signing engagement letters into a selective, seller-favorable market where the advisor's process — not just their Rolodex — drives the outcome. That makes fee literacy worth more than it's been in years.

One framing I'll use throughout, because it cuts through the confusion: the difference between the headline rate and the net-proceeds rate. The headline rate is the percentage the advisor quotes against "transaction value." The net-proceeds rate is what the same fee represents as a share of the cash you actually walk away with. When the engagement letter's definitions are clean, the two are close. When they're broad, the net-proceeds rate can be dramatically higher than the headline — and that gap is the entire subject of the second half of this guide.

What is a normal M&A advisor success fee by deal size?

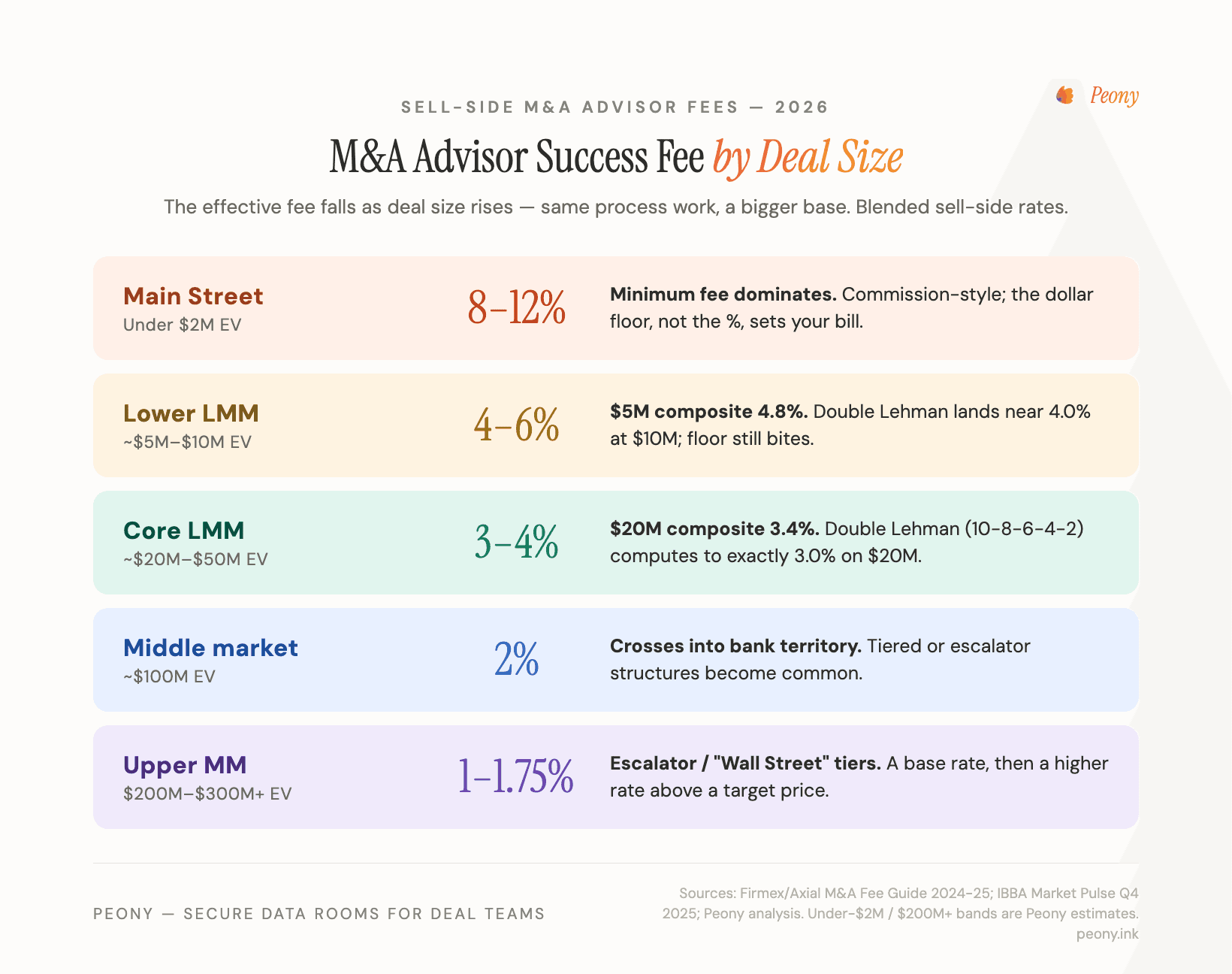

Effective success fees fall as deal size rises. That's the single most important pattern, and it's mechanical, not arbitrary: selling a $5M business takes nearly the same work — confidential information memorandum, buyer outreach, diligence management, negotiation — as selling a $25M one, but the fee base is five times smaller, so the percentage has to be higher to make the advisor's time worthwhile. Axial's data shows deal size is the number-one factor in fee-setting for 75% of advisors.

Here's the benchmark curve, blended from the most recent Firmex/Axial M&A Fee Guide (the 2024-25 edition, the eighth annual, surveying 456 middle-market professionals), the prior 2021-22 edition's granular distributions, and the deal-size bands from the IBBA Market Pulse:

| Enterprise value | Typical effective success fee | What's driving it |

|---|---|---|

| Under $2M (Main Street) | 8%-12% (often ~10%) | Commission-style; minimum fee dominates |

| ~$5M | 5%-8% (survey composite 4.8%) | Minimum-fee floor still bites |

| ~$10M | 4%-6% | Double Lehman lands near 4.0% |

| ~$20M | 3%-4% (survey composite 3.4%) | Double Lehman lands near 3.0% |

| ~$50M | 2%-4% | Formula or negotiated tier |

| ~$100M | 1.5%-2.5% (survey composite 2.0%) | Crosses into investment-bank territory |

| ~$200M | 1.25%-2% | Tiered structures common |

| ~$300M+ | 1%-1.75% | Escalator/tiered "Wall Street" formula |

The $5M-$150M rows are survey-grounded; the under-$2M, $200M, and $300M rows are Peony estimates extrapolated beyond the survey's published range — treat them as directional. Axial CEO Peter Lehrman puts the core band cleanly: "A reasonable range coalesces between 1-2% for $100 million deals and 3-5% for $10 million to $50 million deals."

Two things sellers consistently get wrong about this curve. First, the percentage you're quoted says almost nothing until you know the structure behind it — a "5%" can be a flat rate, a blended Lehman outcome, or a minimum-fee floor in disguise. Second, below about $5M the percentage stops being a percentage at all and becomes a fixed dollar minimum, which is why the smallest deals show the highest — and most variable — effective rates. Both of those are the next two sections.

Is the Lehman Formula still used — and what is the Double Lehman?

Yes — and here's the correction worth banking, because the internet is full of the opposite claim: the Lehman-style declining-rate formula is not obsolete. It's the single most common fee structure in the market today. In the 2024-25 Fee Guide, a declining-percentage Lehman formula was used by 44% of firms — up from just 21% a few years earlier — versus 26% on a flat percentage and 20% on an accelerator/scaled structure. So if you're told "nobody uses Lehman anymore," your advisor either means the classic version or is simply repeating a myth.

The confusion exists because there are several "Lehman" formulas, and they pay very differently.

Classic Lehman (5-4-3-2-1). The original, from Lehman Brothers in the 1960s: 5% of the first $1M of price, 4% of the second, 3% of the third, 2% of the fourth, and 1% of everything above $4M. On a $10M deal that's $50k + $40k + $30k + $20k + $60k = $200,000, or 2.0%. The problem for advisors is that 1% marginal rate on everything above $4M — it makes the formula too thin to cover the work on a sub-$50M deal, which is exactly why it's been largely replaced in the lower middle market.

Double Lehman (10-8-6-4-2). Today's lower-middle-market standard simply doubles the early tiers: 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of the balance. On the same $10M deal: $100k + $80k + $60k + $40k + $120k = $400,000, or 4.0% — exactly twice the classic outcome. MidStreet publishes worked examples that show the small-deal sting clearly: a $3M deal runs $240,000 (8.0%), a $5.7M deal $314,000 (5.5%), and a $9M deal $380,000 (4.2%).

Here's the side-by-side every seller should see before signing, on a $20M deal:

| Fee structure | Fee on $20M | Effective rate |

|---|---|---|

| Classic Lehman (5-4-3-2-1) | $300,000 | 1.5% |

| Double Lehman (10-8-6-4-2) | $600,000 | 3.0% |

| Flat 3% | $600,000 | 3.0% |

| Flat 5% | $1,000,000 | 5.0% |

The Double Lehman costs precisely twice the classic version. That's not a reason to refuse it — the classic formula genuinely underpays an advisor on a $20M process — but it is a reason to know which one you're being quoted and to model the dollar figure, not the label.

Two more structures you'll meet:

- Flat percentage (26% of firms): one rate on the whole transaction value, e.g., 3% or 5%. Simple, common on cleaner mid-size deals, no tier decay.

- Accelerator / "Wall Street" tier (20% of firms, and rising): a base rate up to a target valuation, then a higher rate on every dollar above it — for example, 2% up to a $50M target, then 3% on the next $10M. This is the genuinely seller-aligned structure: it pays the advisor most for the outperformance you actually care about, instead of decaying as the price rises. If you believe your advisor can push the price well above expectations, an accelerator can align incentives better than a declining Lehman. (At the large-deal end you'll also see descending institutional tiers like 1% up to $100M, 0.5% on $100M-$250M, and 0.25% above — the investment-bank shape.)

The label on the formula is marketing. The tiers in the letter are the contract. Always read the actual percentages and tranches, not the name.

What are retainers and work fees — and will they be credited back?

A retainer (or "work fee") is what you pay during the process, before there's any closing to pay a success fee on. Roughly five of six advisors charge one. It exists for a real reason: the sell-side model is success-based, a process runs many months, and deals sometimes die — the work fee funds the labor (CIM, marketing, data room, buyer outreach) and screens out non-committed sellers. (The share-of-letters distribution figures in this section and the next come from the Fee Guide's 2021-22 edition — the most recent that broke them out by percentage; the headline fee levels and market stats above are current 2024-26 data.) A Carl Marks managing director's framing that I think is exactly right: it's "skin in the game" for the seller, not the advisor's profit center.

The typical bands, from the Fee Guide surveys and the law-firm primers:

- Monthly work fee: most commonly $5,000-$10,000/month — a band that held steady from the 2021-22 survey through the 2024-25 edition. The market has shifted toward monthly (rather than one-time) work fees specifically because deals have taken longer to close.

- Fixed up-front retainer: commonly $25,000-$75,000 per John Dorsey PLLC and Venable; $50,000-$100,000 on more established transactions. Retainer size is highly correlated with deal size.

Now the one word that decides whether the retainer is a cost or a prepayment: "creditable." About 72% of advisors who charge a work fee net it against the success fee at closing (2021-22 Fee Guide survey). When the letter says the work fee is "credited dollar-for-dollar against the success fee," every dollar of retainer you paid reduces the success fee you owe — so it's a prepayment, not an add-on. When the letter is silent, or says "non-creditable" or "non-refundable," you pay it on top of the success fee. This is one of the most common and most avoidable traps in the entire engagement letter, and it's usually a one-line fix.

The crediting also does quiet alignment work: a modest, fully creditable monthly fee means the advisor has to keep demonstrating value each month and is pushed to close at the highest price in the shortest time, because the retainer is coming back out of their success fee anyway.

The minimum-fee floor — where small deals get expensive

About two-thirds of engagement letters include a minimum success fee (2021-22 Fee Guide survey). Floors typically run $50,000-$250,000 at the small end and $200,000-$600,000 for $5M-$30M deals. The minimum exists, again, to protect the advisor's time — but it has a sharp consequence the headline percentage hides: on a small deal, the minimum, not the percentage, is your fee.

Watch what a single $250,000 floor does as deal size changes:

- $250,000 minimum on a $2.5M sale = 10.0% effective

- $250,000 minimum on a $5M sale = 5.0% effective

- $250,000 minimum on a $10M sale = 2.5% effective

The floor only bites at the bottom — but when it bites, it dominates. Below roughly $3-5M of value, you are almost always paying the minimum, which means the quoted percentage is meaningless and the only number that matters is the dollar floor. (This is also why the smallest sellers struggle to find good advisors at all: in the 2021-22 Fee Guide survey, 34% of advisors wouldn't take a deal under $5M, and 26% required at least $20M.) If you're in this range, negotiate the floor itself, and make sure it doesn't exceed what the formula would produce at your realistic low-end price.

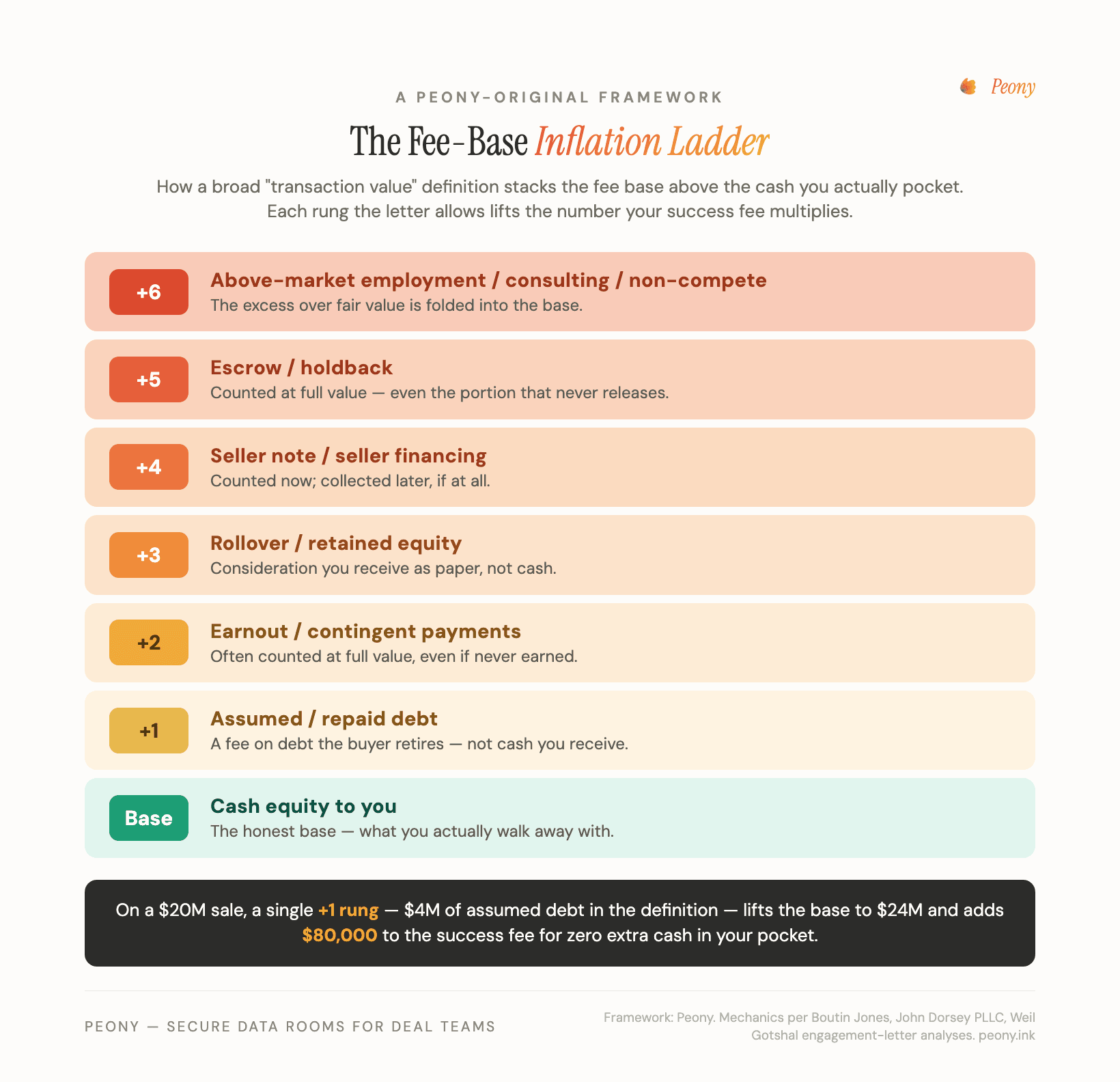

How is "transaction value" defined — and why is it the most expensive line in the letter?

This is the clause that costs sellers the most money, and the one almost no fee article explains properly. The success fee is a percentage of "transaction value" (sometimes "aggregate consideration," "selling price," or "enterprise value"). The percentage gets all the attention. But the fee is percentage × base — and how the letter defines the base is where the real dollars are decided.

A broad, advisor-favorable definition adds things to the base that you never receive as cash. I call the stack of these inclusions the Fee-Base Inflation Ladder — each rung lifts the number the success fee multiplies above your actual equity proceeds:

| Rung | What gets added to the fee base | Why it inflates your bill |

|---|---|---|

| 0 | Cash equity to you (the honest base) | This is what you actually pocket |

| +1 | Assumed or repaid debt | You pay a fee on debt the buyer retires, not cash you get |

| +2 | Earnouts / contingent payments / CVRs | Often counted at full value, even if never paid |

| +3 | Rollover / retained equity | "Consideration" you receive as paper, not cash |

| +4 | Seller notes / seller financing | Counted now; collected later (if at all) |

| +5 | Escrow / holdbacks | Counted at full value; some never releases |

| +6 | Above-market employment / consulting / non-compete | The excess over fair value is added in |

| +7 | Working-capital peg, real estate sold alongside | Swells the base further still |

Every rung you allow widens the gap between the headline rate (fee ÷ transaction value) and the net-proceeds rate (fee ÷ the cash you actually walk away with). And that gap is not theoretical. The law firm Boutin Jones walks through a scenario that should be required reading. The engagement letter set the success fee at $225,000 plus 3% of "Selling Price." "Selling Price" was defined to include the cash and notes received, plus the fair market value of retained assets, plus interest-bearing debt assumed or satisfied at closing, plus contingent payments and the value of employment contracts. The advisor computed Selling Price at $18.5M — $15M of cash and seller note, $1.5M of working capital, $1M of line of credit paid off, and $1M of "deemed value" of the sellers' employment contracts — producing a success fee of $780,000. Then the buyer went bankrupt, defaulted on the $5M seller note, and missed the earnout. The sellers ultimately netted $2.5M. A $780,000 fee on $2.5M of real proceeds — a headline rate around 4% that became a net-proceeds rate over 30%.

The defense is entirely in the definition. Push the letter to:

- Exclude assumed/repaid debt from the base — you shouldn't pay a percentage on debt you're retiring.

- Pay on earnouts, escrows, and holdbacks only "if and when actually received" — not at full contracted value up front. (A useful precedent: some advisors, like Carl Marks, already treat rollover equity and seller financing as consideration due at close but earnouts as payable only if and when the seller collects them.)

- Exclude cash on hand, pre-closing distributions, and fair-market-value real estate.

These are standard seller asks. None of them are exotic, and a good advisor will agree to most of them — but only if you raise them before you sign.

Which engagement-letter clauses quietly cost sellers the most?

Beyond the transaction-value definition, a handful of clauses do the most quiet damage. Here's the teardown, drawn from the engagement-letter analyses published by John Dorsey PLLC, Weil Gotshal, Axial, and Pillsbury. These mechanics are contractual, not time-sensitive — they read the same in 2026 as they did five years ago.

The tail (residual) period. After the engagement ends, if you sell within a defined window, the advisor still collects the full success fee. Banks often seek 18-24 months; cap it at 12. But length is the secondary protection. The primary one is the named-buyer list: limit the tail to buyers the advisor actually contacted during the engagement, and require them to deliver a written list of those buyers within about 10 days of termination — if they don't deliver it, the tail is void. Without that limit, "any buyer" can trigger the fee, including one you found yourself fourteen months later. Also carve out termination for cause, so you don't owe a tail to an advisor you fired for non-performance.

Exclusivity / engagement period. The advisor is your exclusive representative for the term — you can't shop the business elsewhere (or sell it yourself) without owing the fee. Six months to one year is standard; the question, as Axial puts it, is "not whether to grant exclusivity but for how long." The trap is the auto-renewal (evergreen) clause that rolls the exclusive period forward unless you affirmatively cancel, and the 18-24 month exclusive that locks you to an advisor who isn't performing. Cap it at 6-12 months, add a 30-day no-cause termination right, and strike auto-renewal.

Expense reimbursement. You reimburse out-of-pocket deal costs on top of fees. Cap it at $25,000-$50,000, limit it to third-party costs only, and require pre-approval above a threshold. Of advisors who bill expenses (about three-quarters do, per the 2021-22 Fee Guide survey), travel and accommodation is nearly universal, the virtual data room is a reimbursed line for 56% of them, and printing/materials for about a third. The trap is the uncapped expense clause with no third-party limit. (The data-room line is small relative to the success fee — but it's one of the few expense items where your own choice of platform directly controls the cost, which I'll come back to.)

Breakup / progress fees. A fee if you walk away from a bona-fide offer, or a milestone fee payable before close. In the lower middle market these are not the norm — only about 25% of letters include a breakup fee (2021-22 Fee Guide survey, down from 36%). Resist them; if forced to accept a progress fee, tie it to the definitive agreement (not a non-binding LOI) and credit it against the success fee.

Excluded / carve-out buyers. You can list specific parties — a strategic already in talks, a known PE suitor, a family member — who owe a reduced fee or none if they buy, because the advisor didn't source them. Advisors resist or narrow this, but without an excluded-buyer schedule attached at signing, you pay full freight on a buyer you brought yourself.

Indemnification. Engagement letters indemnify the advisor very broadly. Insist on the standard carve-out: no indemnity where the loss results primarily from the advisor's bad faith, gross negligence, or willful misconduct, and reasonable limits on advancing defense costs. The advisor's own liability is typically capped at the fees they received — make sure that cap is mutual in spirit.

Right of first refusal on future financings. Some letters grant the advisor a ROFR on your next capital raise, recap, or sale — quietly signing your next transaction to the same firm and removing your leverage on it. Weil's prescription is direct: strike it, and expressly state that if a pre-existing minority investor exercises an option during the term or tail, the advisor gets no fee.

The "transaction" definition itself. Finally, define what counts as a fee-triggering "transaction" narrowly. A broad definition sweeps in a recapitalization, a minority-stake sale, a joint venture, or a refinancing — so you could do a partial recap with no exit and still owe a full success fee. Limit the engagement to the deal you actually intend (a sale of the business), and exclude minority investments, JVs, and financings unless you separately engage for them.

What should you negotiate before you sign?

Not every term is equally movable. Here's the Negotiation Leverage Ladder — the clauses ranked by how reliably you can change them, so you spend your negotiating capital where it actually pays:

| Priority | Lever | How movable | What to ask for |

|---|---|---|---|

| 1 | Retainer creditability | Very high | Work fee credited 100% dollar-for-dollar vs success fee |

| 2 | Tail length + named-buyer list | High | Cap 12 months; advisor-contacted buyers only; 10-day list or void |

| 3 | Transaction-value exclusions | High (per item) | Exclude assumed debt; earnouts/escrows only when received |

| 4 | Expense cap | High | Hard cap $25k-$50k; third-party only; pre-approval |

| 5 | Excluded-buyer schedule | Medium-high | Named parties at signing; reduced or zero fee |

| 6 | Exclusivity length + kill auto-renew | Medium | 6-12 months; 30-day no-cause termination; strike evergreen |

| 7 | Success-fee percentage / accelerator | Medium (small deals) | Trim the marginal rate or add an upside accelerator |

| 8 | Minimum-fee size | Medium | Keep proportionate to a realistic low-end price |

| 9 | Indemnification carve-outs | Medium | Bad-faith / gross-negligence / willful-misconduct carve-out |

| 10 | Breakup / progress fee | Resist | Decline; if forced, tie to definitive agreement + credit |

| 11 | ROFR / future-financing tail | Strike | Remove; no fee on pre-existing option exercise |

But the single highest-leverage move isn't on this ladder at all, because it happens before you have a letter to negotiate: get two or three competing proposals. In the 2021-22 Fee Guide survey, only about 17% of advisors reported their engagements coming through a competitive "bake-off." That means the overwhelming majority of sellers never create the one thing that actually moves the headline rate — price tension between advisors who each want the mandate. Large deals face this pressure naturally and price lower as a result; small deals usually don't, which is part of why the small-deal percentage stays high. You don't need to run a circus. Two or three credible boutiques, each asked for a written proposal with the structure, the tail, and the transaction-value definition spelled out, will tell you more — and cost you less — than any amount of clause-by-clause haggling with a single advisor you've already emotionally hired.

What does it actually cost to sell a $20M business? (worked example)

Let's put it all together on a clean, representative lower-middle-market deal. Assumptions: a $20,000,000 enterprise value (equity to the seller), a Double Lehman success fee, a $10,000/month work fee over a 9-month engagement that is fully creditable, and an expense cap of $40,000 of which $30,000 is actually incurred. The one wrinkle: the engagement letter defines "transaction value" to include $4,000,000 of assumed debt, so the fee base is $24,000,000, not $20,000,000.

Step 1 — Success fee on the $24M base (Double Lehman): $100k + $80k + $60k + $40k on the first $4M, plus 2% × the remaining $20M ($400k) = $680,000. That's 2.83% of the $24M base — but 3.40% of your real $20M equity.

Step 2 — What the assumed-debt line cost you: had you negotiated the base back to $20M, the same formula produces $280k + (2% × $16M = $320k) = $600,000. So that single sentence about assumed debt added $80,000 to the fee for zero additional cash in your pocket.

Step 3 — Work fee and expenses: the work fee is 9 × $10,000 = $90,000, but because it's creditable it isn't extra — it's prepaid and reduces what's due at close. Expenses come to $30,000 on top.

Step 4 — All-in: success fee $680,000 + expenses $30,000 = $710,000 total, or 3.55% of your $20M proceeds (the $90,000 work fee already sits inside the success fee via the credit). Had you fixed the transaction-value definition, it would be $600,000 + $30,000 = $630,000, or 3.15%.

So the honest all-in answer for a $20M sale is roughly $630,000-$710,000 (about 3.2-3.6%) — and the spread between the low and high end is driven almost entirely by one clause, not by the headline percentage. For contrast, run the same Double Lehman on a $3M deal and it's $240,000 — 8.0%, climbing past 8.3% if a $250,000 minimum applies. Same advisor effort, nearly three times the rate. That's the fee curve, made concrete.

Are M&A advisor fees worth it — and how do brokers and banks compare?

For most owners above roughly $5M in value, a good advisor pays for themselves. The mechanism is competition: a credible advisor running a real process widens the buyer pool and creates tension that typically lifts the price by more than the fee — while shielding you from hundreds of hours of process work so you can keep running the business that's being valued. The economics get worse at the extremes. At the very small end, minimum-fee floors push the effective rate into double digits, and a low-cost business broker or even a direct sale may make more sense. At the very large end ($100M+), you may want the balance-sheet and capital-markets muscle of a full investment bank, and the rate compresses toward 1-2% anyway.

That maps onto the three labels you'll encounter, which differ mostly by deal size and fee shape:

- Business broker — sub-$5M, Main Street, often commission-style at 8-12%, frequently with no audited financials. Our city M&A advisor guides explain where the broker/advisor line falls in each metro.

- M&A advisor / boutique — roughly $5M-$300M, retainer-plus-Double-Lehman, structured processes with dozens to a couple hundred buyers. This is the audience for this guide.

- Investment bank — $50M and up, Lehman or negotiated tiers, broader buyer pools and capital-markets sidecars.

The honest test cuts across all three: will this advisor's process create buyer competition you couldn't create yourself? If yes, the fee is usually worth it in both price and closing certainty. If the "process" is really just a short list of buyers you already know, you're paying for access you don't need — and that's the one situation where running it yourself, or hiring on a tightly capped basis, genuinely makes sense.

Where the data room fits (and where the fee quietly leaks)

I run Peony, a data room company, so let me be precise about where we actually sit in this picture — because it's a small line, not the headline. The success fee is the big number; the data room is a reimbursable expense item that shows up in that "56% of advisors bill the VDR" statistic above. We are not going to move your 3% success fee. What we can do is keep one of the few expense lines you actually control from leaking.

Here's the honest segmented version. If your advisor is running a large, multi-hundred-buyer auction with complex permissioning needs, a legacy enterprise data room may be the right tool, and you'll pay enterprise prices for it — that's a fair trade for that job. But most lower-middle-market sell-side processes don't need that, and the legacy pricing model (per-page, per-user, or opaque per-deal quotes that run $15,000-$50,000) is precisely the kind of uncapped expense line the engagement letter should have capped. A flat-rate room — Peony Business is $30 per admin per month — covers the same NDA-gated, page-level-analytics workflow, purpose-built for M&A sell-side processes, at a fraction of that. The per-recipient analytics and dynamic watermarks tell you (and your advisor) which buyer is actually reading the confidential information memorandum versus window-shopping, which is the leading indicator of who will make a real offer. That's why 5,900+ customers — founders, advisors, PE platforms, and ESOP trustees — run their processes on Peony.

The broader point isn't about us. It's that the same discipline you bring to the success-fee structure and the transaction-value definition should extend to every line the letter lets the advisor bill you for. 5,900+ customers chose a flat-rate room after running exactly that math; the M&A data room guide covers the full 15-platform comparison if you want to do the same.

Frequently asked questions

I just got a 5% success-fee quote to sell my ~$20M business — is that normal in 2026?

A 5% success fee on a $20M deal is at the high end but not unheard of. The most recent Firmex/Axial M&A Fee Guide puts the blended effective success fee around 3.4% at $20M, and a Double Lehman structure (10-8-6-4-2) computes to exactly 3.0% ($600,000) on a clean $20M base. So 5% ($1,000,000) is roughly $400,000 above the typical Double Lehman outcome. That doesn't make it wrong — a small, complex, or hard-to-sell business can justify a premium — but it's your cue to ask how the rate was set, request the Double Lehman alternative in writing, and get a second proposal to create price tension.

What's the typical M&A advisor success fee by deal size?

Effective sell-side success fees fall as deal size rises, because a small deal takes nearly the same work as a mid-size one. Using the most recent Firmex/Axial M&A Fee Guide composite: roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M. Below about $5M the percentage climbs to 7-10% or more, driven by minimum-fee floors. Above $100M you cross into investment-bank territory at 1-2%, often with a tiered or escalator structure. Axial CEO Peter Lehrman frames the band as 3-5% for $10M-$50M deals and 1-2% for $100M deals. Treat any single number as a starting point, not a quote.

What's the difference between the Lehman Formula and the Double Lehman — and which will I be quoted?

The classic Lehman Formula pays 5% of the first $1M of price, 4% of the second, 3% of the third, 2% of the fourth, and 1% of everything above $4M (5-4-3-2-1). The Double Lehman doubles the early tiers to 10-8-6-4-2. On a $20M deal, classic Lehman is $300,000 (1.5%) and Double Lehman is $600,000 (3.0%) — exactly twice. In the lower middle market today you'll almost always be quoted the Double Lehman or a flat percentage, because classic Lehman's 1% top rate underpays the advisor. Despite a common myth that 'Lehman is obsolete,' a declining-rate Lehman-style formula is now the single most common structure, used by about 44% of firms.

How do I calculate a Double Lehman fee on a $20M deal?

Apply 10-8-6-4-2 to each tranche: 10% of the first $1M is $100,000; 8% of the second $1M is $80,000; 6% of the third is $60,000; 4% of the fourth is $40,000; and 2% of the remaining $16M is $320,000. Add them up: $600,000, or 3.0% of the $20M. The trap is the base, not the math — if the engagement letter's 'transaction value' definition adds, say, $4M of assumed debt, you compute on $24M instead and the fee jumps to $680,000. Always run the formula on the number in the letter's definition, not the headline price.

Will my retainer or work fee be credited against the success fee at closing?

Usually yes, if you negotiate one word: 'creditable.' About 72% of advisors who charge a work fee net it against the success fee at close (2021-22 industry fee survey), so the retainer becomes a prepayment rather than an extra cost. Make sure the letter says the work fee is 'credited dollar-for-dollar against the success fee.' If it's silent, or says 'non-creditable' or 'non-refundable,' you pay it on top — a common and avoidable trap. Typical monthly work fees run $5,000-$10,000; fixed retainers $25,000-$75,000. The credit is also an alignment tool: a modest, creditable monthly fee pushes the advisor to close at the best price quickly.

Is a $50k-$250k minimum fee reasonable, and how does it change my effective rate?

Minimum success fees are standard — about two-thirds of engagement letters include one (2021-22 industry fee survey) — and they exist to protect the advisor's time on smaller deals. Typical floors run $50,000-$250,000 at the low end and $200,000-$600,000 for $5M-$30M deals. The catch is that on a small sale the minimum, not the percentage, sets your bill: a $250,000 floor on a $2.5M deal is 10% effective, while the same floor on a $10M deal is just 2.5%. Below roughly $3-5M you're almost always paying the minimum, so the headline percentage is meaningless — negotiate the dollar floor, and make sure it doesn't exceed the formula fee at your realistic low-end price.

How is 'transaction value' defined — can my advisor charge a fee on debt, earnouts, or rollover equity I never receive as cash?

Yes, if you let the definition run broad — and this is the single most expensive line in the letter. A broad 'transaction value' (or 'aggregate consideration') can include assumed or repaid debt, earnouts counted at full value, rollover equity, seller notes, escrows and holdbacks, working-capital pegs, and the above-market portion of employment or consulting agreements. Each inclusion lifts the fee base above the cash you actually pocket. In one scenario published by law firm Boutin Jones, a letter defined 'Selling Price' to include assumed debt and contingent payments; the fee was billed on $18.5M (a $780,000 fee) while the sellers ultimately netted just $2.5M after the buyer went bankrupt. Push to exclude assumed debt, cash, and fair-market real estate, and to pay on earnouts or escrows only if and when you actually receive them.

Is a 24-month tail period normal, and do I owe a fee on a buyer I found myself?

A tail (or residual) clause lets the advisor collect the success fee if you sell within a set window after the engagement ends. Banks often seek 18-24 months; you should cap it at 12. The real protection isn't the length — it's the 'named-buyer list.' Limit the tail to buyers the advisor actually contacted during the engagement, and require them to deliver a written list of those buyers within about 10 days of termination; if they don't deliver it, the tail should be void. With that limit, a buyer you sourced yourself doesn't trigger a fee. Also carve out termination for cause, so you don't owe a tail to an advisor you fired for non-performance.

What should I negotiate in an M&A engagement letter before I sign?

In rough order of how movable they are: (1) make the retainer fully creditable against the success fee; (2) cap the tail at 12 months and limit it to a named-buyer list; (3) tighten the 'transaction value' definition to exclude assumed debt and to count earnouts only when received; (4) cap expenses at $25,000-$50,000, third-party costs only; (5) attach an excluded-buyers schedule for parties you bring; (6) cap exclusivity at 6-12 months and strike any auto-renewal; (7) trim the success-fee percentage or add an upside accelerator; (8) keep the minimum fee proportionate. The single highest-leverage move is simply getting two or three competing proposals — only about 17% of engagements are awarded through a competitive bake-off (2021-22 industry fee survey), which is the tension that actually moves the headline rate.

What will I actually pay all-in to sell a $20M company?

On a clean $20M sale, expect roughly $630,000-$710,000 in total advisor cost — about 3.2-3.6% of your equity proceeds. Built up: a Double Lehman success fee of $600,000 on a $20M base; about $30,000 of capped, reimbursable expenses; and a $5,000-$10,000/month work fee that, if creditable, is prepaid against the success fee rather than added on top. The swing factor is the 'transaction value' definition — if the letter folds in $4M of assumed debt, you compute the success fee on $24M and it rises to $680,000, an extra $80,000 for zero additional cash. The work fee is usually not extra; the expense cap and the transaction-value definition are where real dollars leak.

Are M&A advisor fees worth it versus selling the company myself?

For most owners above roughly $5M in value, yes — a competitive process run by a credible advisor typically widens the buyer pool and lifts price by more than the fee, and it shields you from the deal-process work while you keep running the business. The economics weaken at the very small end, where minimum-fee floors push the effective rate into double digits, and at the very large end, where you may want a full investment bank. The honest test: will the advisor's process create genuine buyer competition you couldn't create yourself? If yes, the fee usually pays for itself in price and certainty. If the 'process' is a short list of buyers you already know, you're overpaying for access you don't need.

How do buy-side M&A advisor fees differ from sell-side?

The components are the same — a retainer plus a success fee tied to transaction value — but the weighting flips. Sell-side advisors are paid mostly on close, so they load the success fee and bear the execution risk. Buy-side advisors screen many targets that never convert, so they load the non-contingent retainer to fund the search; on major deals those retainers can run into six figures and up. Buy-side success fees still often use Lehman or Double Lehman on the purchase price, but a larger share of total compensation is the upfront retainer. If you're a buyer, expect to pay more before any deal is certain; if you're a seller, expect most of the cost to land only when you actually close.

Related Peony resources

For the city-by-city advisor benches that link back to this fee guide, and the data-room and diligence playbooks that sit alongside an engagement, see:

- M&A advisor vs business broker vs investment bank — the companion selection guide: which of the three intermediaries to hire, the step that comes before negotiating this fee

- Best M&A advisors in NYC — the largest boutique bench, where this fee math plays out across $5M-$300M deals

- Best Technology & Software M&A advisors — the national tech/software sector bench, where ARR-multiple deals and these fee structures meet

- Best M&A advisors in Chicago — 18 firms across the broker / advisor / investment-bank spectrum this guide compares

- Best M&A advisors in Dallas and Houston — energy and industrial benches where tiered and escalator fees are common

- How to structure an earnout in an M&A sale — the contingent consideration that the "transaction value" definition can quietly pull into your fee base

- Roll equity in M&A deals — how rollover equity is treated as consideration, and why it matters for the success fee

- Due diligence cost breakdown — the separate professional-fee stack (QoE, legal, tax) that sits beside the advisor's fee

- M&A data room guide — the full 15-platform comparison behind the data-room expense line

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, where the room's cost has to stay proportional to a smaller fee and deal size

- M&A due diligence process guide — the workstreams your advisor will run you through after you sign

- M&A trends and facts 2026 — the macro backdrop, including the $1.2T+ sponsor-led market context