How to Structure an Earnout in an M&A Sale: 2026 Founder Playbook for the 28% That End in Dispute

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

How to Structure an Earnout in an M&A Sale: 2026 Founder Playbook for the 28% That End in Dispute

Quick answer: Earnouts pay 21 cents on the dollar across all M&A deals per the SRS Acquiom 2025 Deal Terms Study — 79% of earnout dollars promised never actually get paid. 28% are contested. To shift those odds: prefer Revenue over EBITDA (less manipulable); cap duration at 24 months (the 2024 median); lock the Operating Covenant Stack (7 covenants + non-avoidance) into the SPA; build acceleration on change of control, termination without cause, and product discontinuation; decouple payment from employment to avoid IRS W-2 recharacterization under Lane Processing Trust v. U.S.; and model the IRC §453A interest charge on installment obligations over $5M before signing. If the buyer refuses both change-of-control acceleration and for-cause termination protection, walk away from the earnout structure and rebalance toward more cash upfront.

Last updated: May 2026

Why I wrote this

I have advised on more sell-side processes than I can count, and the same pattern shows up in roughly half of them: a founder gets an LOI that looks like a clean number until you read the earnout section, and then the realized value of the deal compresses by 20-30% over the next 18-30 months because nobody negotiated the structural protections in the SPA. The buyer's playbook is consistent enough that I have stopped treating it as a series of unrelated mistakes and started treating it as a single playbook that you have to disarm in advance — clause by clause, covenant by covenant.

The most quotable single statistic in modern M&A is the SRS Acquiom 2025 Deal Terms Study headline number: average earnout payout is 21 cents on the dollar. 79% of earnout dollars that get promised in LOIs and definitive agreements never actually get paid. The number rises slightly to "59% of deals pay something" and "among deals that pay, about 50% of maximum dollars pay" — but the average across the entire universe is 21¢. Life Sciences runs 19¢, slightly worse. 28% of earnouts are contested. 17% of paid-out earnouts require renegotiation to avoid litigation.

If you are a founder receiving an LOI right now with a 25-30% earnout share, the unbiased expected value of that earnout — applying SRS Acquiom's universe — is roughly 5-6% of headline deal value. That is the math your investment banker will probably not put on a slide. That is the math that should drive the pre-LOI conversation about cash-vs-contingent split.

This post is the working playbook I would hand to a founder running a sell-side process — or to a sell-side advisor, an M&A lawyer, or a CFO modeling the §453A trap. It is structured around seven proprietary frames I have refined across enough deals that I trust them as a starting point. The first frame (Metric Risk Ladder) is the metric-choice decision. The next three frames (Operating Covenant Stack, Acceleration Trigger Matrix, Buyer-Side Manipulation Playbook) are the SPA-drafting frames. The fifth frame (Tax Recharacterization Risk Index) is the tax-structure frame. The sixth (Earnout vs Rollover vs Seller Note) is the capital-stack frame. The seventh — the 79% Stat — is the forcing function I use to push back on overweighted earnout shares at LOI signing.

At Peony we now serve more than 5,900 customers, and the workflow I see across our sell-side processes is consistent: tighter, more competitive processes produce fewer earnouts because they reduce the buyer's leverage to insist on contingent consideration. A well-run, multi-bidder sell-side process with visitor groups segmenting strategics, PE, and family offices reduces the negotiated earnout share. The frames in this post operate at the SPA-drafting layer; the process-level lever is upstream. Both matter.

What is an earnout (and why founders should pause before saying yes)?

An earnout is contingent purchase price paid post-close based on the acquired business hitting specified performance targets. The structure converts a portion of the headline deal value from cash-at-close into a series of contingent payments that may or may not occur, contingent on whatever metric or milestone the parties write into the SPA. The economic function: bridge a valuation gap when buyer and seller disagree on the future trajectory of the business.

The mechanics: the SPA specifies (1) the metric (revenue, EBITDA, net income, customer retention, regulatory milestone), (2) the threshold or curve (cliff, linear, or graduated), (3) the cap and floor, (4) the measurement period (typically 12-36 months), (5) the calculation methodology (which GAAP application, what exclusions, who calculates), (6) operating covenants binding the buyer's conduct during the measurement period, (7) dispute-resolution mechanism (CPA expert determination, arbitration, or court), and (8) treatment on acceleration events. Each of these decisions has structural consequences. Get them wrong and the math collapses.

Earnout prevalence is trending DOWN, not up

The 2026 numbers are clearer than they have been in years, and the trend is the opposite of what most banker pitch decks suggest. The headline:

| Source | Period | % of Deals with Earnout |

|---|---|---|

| ABA 2025 Private Target Deal Points Study (released Dec 2025; middle-market $25M-$900M) | 2024-Q1 2025 | 18% (DOWN from 26% in 2023 ed.) |

| SRS Acquiom 2025 Deal Terms Study | 2024 | 22% (ex-Life Sciences) |

| SRS Acquiom 2025 Study (peak) | 2023 | 30-37% |

| SRS Acquiom 2025 Study | 2019 | 15% |

| ABA Private Target Deal Points Study 2023 ed. | 2022-Q1 2023 | 26% (up from 20% in 2021 ed.) |

| Harvard Corp Gov "The Art and Science of Earn-Outs" (Jul 2025) — Life Sciences | Recent | 80%+ of pharma deals |

The 2023 peak coincided with the valuation gap created by the rates shock and the IPO freeze; buyers used earnouts as a price-discovery mechanism. Sellers have used current market leverage — more buyer competition, modestly looser financing markets, the venture rebound — to demand more cash upfront. The 2024-2026 environment is less earnout-friendly than 2023, and a buyer's term sheet leading with a 25-30% earnout share is structurally aggressive against the current market norm.

But the earnouts that ARE used are getting MORE buyer-friendly

The ABA 2023 vs 2021 trend shows a clear directional shift in deal mechanics that haven't softened in 2025:

| Provision | 2021 ed. | 2023 ed. |

|---|---|---|

| Buyer can operate post-close at its discretion | 33% | 50% |

| Express disclaimer of buyer fiduciary duty re: earnout | 8% | 25% |

| Earnout does NOT accelerate on change of control | 42% | 75% |

| One or more of (consistent with past practice, maximize earnout, stand-alone) | — | 25% |

| Two or more of those covenants | — | 8% |

The directional shift is unambiguous. Buyers have negotiated more discretion, sellers have negotiated less acceleration, and the operating covenant stack has thinned. The single biggest trap in this trend is the change-of-control non-acceleration: 75% of deals expressly EXCLUDE acceleration if the buyer sells the acquired business. That is the seller's worst-case scenario built into the contract by default.

The takeaway for the pre-LOI conversation: earnouts are less common, but the ones used are more aggressive. The founder's negotiation leverage comes from two places: market norms (push back to compress the earnout share, citing ABA 2025 prevalence data) and structural protections (lock in the operating covenants and acceleration triggers that ABA shows the buyer is trying to strip).

The 79% Stat as a forcing function

This is the single number I open every pre-LOI conversation with. The SRS Acquiom 2025 Deal Terms Study tracks 2,200+ transactions over 2019-2024 and reports the average earnout payout at approximately 21 cents on the dollar. 79% of promised earnout dollars never get paid. Use this stat in three ways:

- As a probability-weighted expected value. A $15M earnout has an unbiased SRS Acquiom expected value of approximately $3.15M. Compare that to the alternative of $5M more cash upfront and $0 earnout, and the founder's risk-adjusted choice is often clearly the cash.

- As leverage to compress the earnout share. A buyer pushing 30% earnout is taking 30% of headline value and assigning it a probabilistic discount of ~80%. Push back to 10-15% earnout if the buyer wants contingent consideration at all.

- As an anchor for the operating covenant conversation. The 79% unpaid rate is partially a function of buyer discretion. The Operating Covenant Stack (Frame 2 below) reduces the unpaid rate by limiting the buyer's ability to suppress the metric. Use the 79% number to justify the covenant ask.

The data freshness rule: I do not cite "30% court rate" or older numbers anymore. The SRS Acquiom 2025 study is the canonical source, and the 28% dispute rate, 17% renegotiation rate, and 21¢ payout average are the defensible numbers as of May 2026.

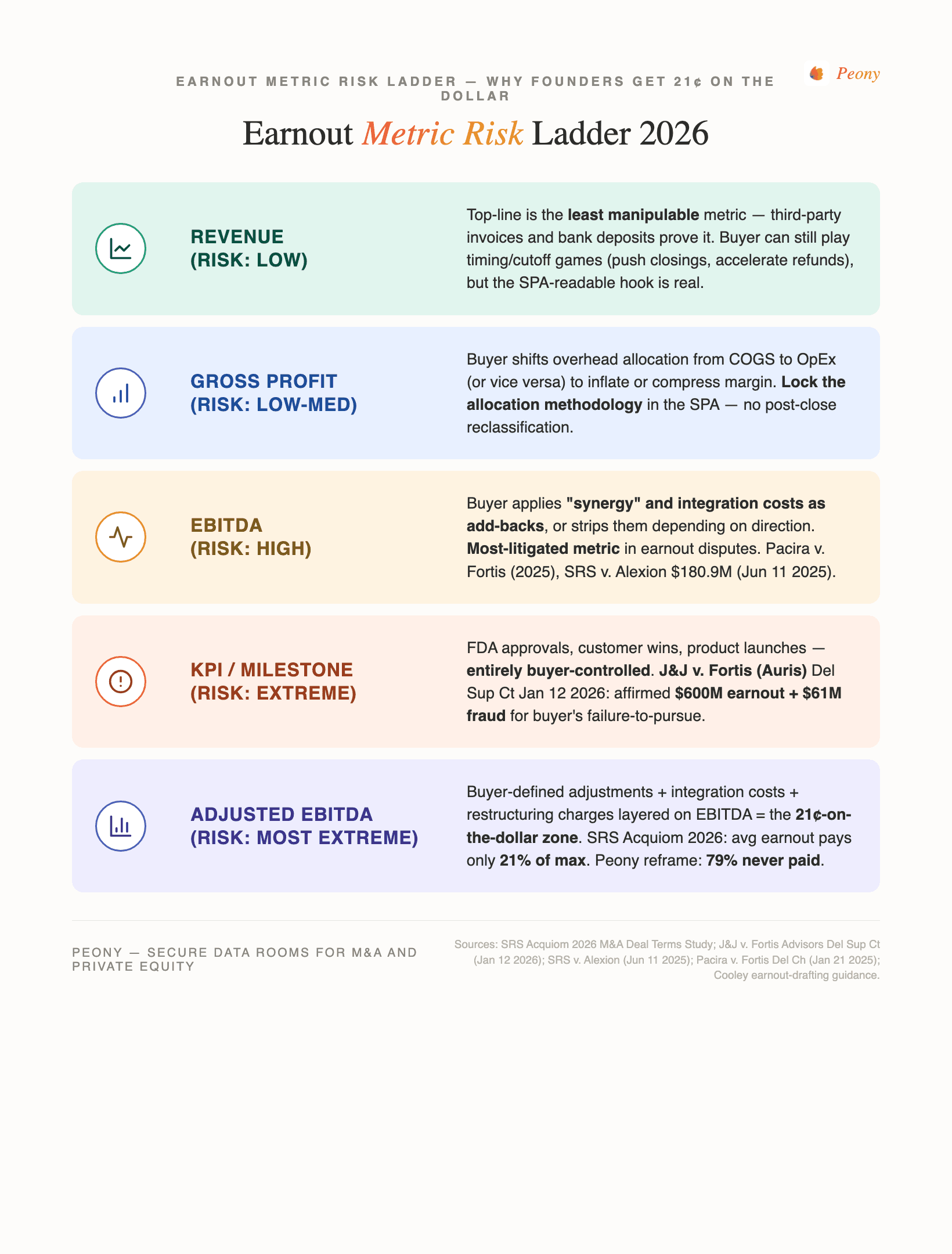

What is the Earnout Metric Risk Ladder?

This is the metric-choice frame. Every earnout requires one or more performance metrics, and the choice of metric determines how much manipulation risk you absorb. Score each candidate metric on three dimensions: (1) buyer manipulation risk, (2) verification burden, (3) dispute frequency in litigation history.

| Metric | Manipulation Risk | Verifiability | Recommended Use |

|---|---|---|---|

| Revenue | LOW | Easy (GAAP, audited) | Default seller-preferred; under 5% manipulation gap typical |

| Gross Profit | MEDIUM | Moderate (COGS subjective) | Acceptable with COGS lock-in |

| EBITDA | HIGH | Hard (definition wars) | Avoid unless tight definition + overhead exclusion |

| Net Income | EXTREME | Buyer controls every line | Never as standalone metric |

| Customer Retention | LOW-MED | Hard for buyer to fake | Good defensive add |

| Milestone (FDA, Patent) | LOW-MED (binary) | Public record | OK if criteria locked |

Revenue: the default

Revenue is the metric I recommend by default for sub-Life-Sciences deals. It is the closest thing to an audit-defensible, manipulation-resistant top-line indicator that exists in the GAAP universe. The buyer has limited ability to suppress revenue without either (a) breaching customer contracts or (b) materially reducing pricing — both of which damage their own asset. Revenue-based earnouts in court have a meaningfully lower dispute rate than EBITDA-based earnouts because there is less interpretive surface area.

The defenses you still need on a revenue-based earnout: (1) a definition of "recognized revenue" tied to the existing revenue-recognition policy at close (no reclassification of multi-year SaaS contracts into annual ratable revenue, for example), (2) explicit treatment of acquired-product revenue that the buyer cross-sells through parent channels, (3) protection against the buyer redirecting customer revenue through parent entities to avoid attribution, and (4) protection against the buyer raising customer prices in a way that drives churn out of the measurement period.

EBITDA: where I draw the hardest line

If you are a founder reading this, here is the single sentence I want you to remember: if you accept an EBITDA-based earnout, you have handed the buyer control of the payout. I have watched this play out enough times to call it: do not accept an EBITDA-based earnout from a strategic buyer that controls accounting without (a) a contractually frozen EBITDA definition and (b) an explicit exclusion list. The minimum exclusion list:

- Corporate overhead allocations unrelated to the acquired business

- Intercompany expenses above a defined cap, or at all

- Integration costs booked against operating EBITDA

- Extraordinary R&D outside the budget approved at close

- ESG compliance costs the buyer imposes on the acquired entity

- Buyer-mandated capex that compresses cash EBITDA via depreciation

- Severance and restructuring expenses related to integration headcount actions

Without that fence, the buyer can suppress EBITDA by 20-30% without violating any covenant. The worked example below (on a $50M deal with a $4M pre-close EBITDA business) shows how $1.2M of allocations collapses a $4.4M threshold to $3.2M actual — and the cliff fails.

The buyer's counter-argument is always the same: "We need flexibility to run the business." The seller's counter to the counter: "Then accept revenue or a composite metric instead." If the buyer refuses both a frozen EBITDA definition and an alternative metric, the buyer is reserving the right to manipulate the payout.

Net Income: never

I have seen net-income earnouts hold up in maybe one or two cases out of dozens I have watched. The buyer controls every line below operating income — depreciation policy, amortization, interest expense allocation, tax allocation, intercompany rebates — and even good-faith application of those choices compresses net income unpredictably. Treat any term sheet proposing a net-income earnout as a structural bid by the buyer to control the payout completely. Push back to EBITDA at the very least, and ideally to revenue.

Composite metrics and the 68% number

The SRS Acquiom 2025 data shows 68% of earnout deals use multiple metrics. Composite earnouts (Revenue + EBITDA + Customer Retention, weighted) reduce the risk that any single line manipulation collapses the entire payout. The mechanics: split the earnout into independent pools, each tied to a single metric, each with its own cliff or curve. If revenue hits but EBITDA fails (because the buyer suppressed EBITDA), the seller still collects on the revenue pool. The composite design is structurally more seller-friendly than any single-metric design.

Customer Retention and Milestone-Based Earnouts

Customer retention is a defensive add for SaaS, services, and consumer businesses where the buyer's marketing or pricing decisions could drive churn. The mechanics: track logo retention or net revenue retention against the top-N customer cohort at close; pay against threshold (e.g., 80% logo retention through Year 2). Defenses needed: (a) buyer can't unilaterally raise customer prices more than X% during the measurement period, (b) buyer can't deprecate features or change support terms in ways that drive churn, (c) customer-contract renewal terms are honored.

Milestone-based earnouts dominate Life Sciences (regulatory approval, patent issuance, clinical trial endpoints). The defenses: (a) milestone definition is precise and tied to a specific regulatory path, (b) the buyer cannot abandon the path in favor of an alternative without triggering acceleration, (c) the buyer maintains the development pace consistent with comparable priority products. The J&J / Auris Health case (covered below) is the canonical example of a milestone-based earnout where the buyer abandoned the regulatory path mid-stream and the court awarded over $600M in damages.

What duration and payout curve should you negotiate?

The Harvard Corporate Governance Forum's 2025 compilation tracks median earnout duration at 24 months for non-Life Sciences deals. 2024 saw a trend toward shorter periods — no deals running longer than 4 years. Life Sciences continues to run 3-5+ years because regulatory milestones drive the timeline.

The 24-month median is not arbitrary. Three reasons it holds:

- Founder energy decay. A founder who stays on through a 36-48 month earnout is exhausted by the back half. Performance compresses. Buyer integration changes accelerate. The longer the term, the more the buyer's actions (org changes, integration, strategy shifts) distort the metric.

- Accounting drift. GAAP application drift over 36+ months is hard to disentangle from buyer manipulation. The longer the term, the harder a CPA expert can isolate the buyer's discretionary accounting choices from "ordinary course" application changes.

- Strategic obsolescence. Markets and business models shift in 24-36 months. A revenue threshold set at close becomes irrelevant if the business pivots. The buyer's strategic priorities also shift, and a 36+ month metric becomes increasingly disconnected from current buyer thesis.

Cliff vs Linear vs Graduated

Three payout curve structures, each with different risk profiles:

| Structure | Mechanics | Seller risk | Recommended use |

|---|---|---|---|

| Cliff | All-or-nothing at threshold (e.g., $22M revenue or $0 paid) | EXTREME — single dollar miss collapses payout | Avoid; only if used inside a composite metric or pool |

| Linear | Sliding scale from 0% at floor to 100% at cap | LOW — proportional payout for partial achievement | Default seller-preferred |

| Graduated | Tiered payouts at thresholds (e.g., 50% at $20M, 75% at $21M, 100% at $22M) | MEDIUM — partial protection if buyer manipulation reduces but doesn't crater the metric | Compromise; common in PE deals |

The cliff is the buyer's preferred structure because it lets a single dollar miss eliminate the entire payout. Push back to linear or graduated as the default. If a buyer insists on cliff, the SPA needs (a) an explicit 5-10% "safety margin" between actual performance and threshold, and (b) acceleration on buyer breach of operating covenants.

Caps and Floors

A cap limits the buyer's downside; a floor limits the seller's downside. Standard structures:

- Cap only: Buyer pays from $0 up to the cap. No floor; below-threshold performance pays nothing. Most common.

- Cap + Floor: A minimum guaranteed earnout (e.g., $1M) paid regardless of performance, then linear scaling to the cap. Less common but defensible for founder-driven sales.

- Hurdle + Cap: No payout until performance exceeds a hurdle (e.g., 95% of base case); then linear or graduated scaling to cap. Common in PE deals.

The hurdle structure is buyer-friendly because it sets a payment threshold above current performance. Push back unless the hurdle is set at or below the close-date trailing twelve-month metric.

The Sliding Scale (Recommended Default)

For most non-Life-Sciences founder sales, my recommended default earnout curve is:

- Metric: Revenue (composite with EBITDA only if a frozen EBITDA definition + exclusion list is locked)

- Term: 24 months

- Curve: Linear from 95% of close-date trailing 12-month base to 115% of base, with full earnout at 115%

- Cap: 20-25% of headline deal value

- Acceleration: On change of control, on-cause termination, on buyer breach of operating covenant, on standalone-business sale, on product-line discontinuation

This structure compresses the buyer's leverage to crater the payout through manipulation while preserving meaningful upside if the business outperforms.

What is the Operating Covenant Stack the SPA must have?

This is the second proprietary frame, and it is the one I would put on every founder's pre-LOI checklist. The Operating Covenant Stack is the set of contractual commitments the buyer makes about how it will run the acquired business during the earnout period. Without these covenants, the buyer's discretion is total, and the 79% unpaid rate is the result.

The 7 covenants (plus the +1 non-avoidance clause):

Covenant 1: Operate in ordinary course consistent with past practice

The baseline. The buyer commits to running the acquired business in the same operational pattern that produced the close-date trailing 12-month metric. ABA tracking shows only 25% of deals include any one of (a) ordinary course covenant, (b) maximize-earnout covenant, or (c) standalone-entity covenant; only 8% include two or more.

The ask in the SPA: "Buyer shall operate the Acquired Business in the ordinary course consistent with past practice during the Earnout Period." This is necessary but not sufficient — alone, it's interpretive and the buyer can argue most operational changes are within "ordinary course." It pairs with the other covenants.

Covenant 2: Accounting consistency — no GAAP application changes without seller consent

The most important single covenant on EBITDA-based earnouts. The buyer commits to maintaining the same GAAP application, revenue recognition policy, depreciation policy, and accounting methods used during the close-date measurement period. Without this covenant, the buyer can change accounting policy and suppress the metric without violating any other clause.

The ask: "Buyer shall maintain accounting policies, revenue recognition methods, and GAAP application consistent with the Acquired Business's pre-Close practice during the Earnout Period. Any change to accounting policy requires Seller's written consent, which shall not be unreasonably withheld."

Covenant 3: No allocation of corporate overhead unrelated to the acquired business

The single most common EBITDA suppression move. The buyer's parent allocates HQ overhead, legal, finance, IT, HR, and corporate-shared services to the acquired sub. Even if the allocation is "fair" by traditional cost-accounting standards, it suppresses the standalone EBITDA the earnout is measured against.

The ask: "Buyer shall not allocate any corporate overhead, shared-services, or parent-entity expenses to the Acquired Business that did not exist as expenses to the Acquired Business immediately prior to Close. Any new allocations require Seller's written consent."

Covenant 4: Arm's-length intercompany pricing

The companion to Covenant 3. If the parent provides services to the acquired sub (IT, legal, payroll), the intercompany prices must be arm's-length — not inflated to suppress the sub's EBITDA. Critical in carve-out deals where the acquired business genuinely consumes some parent services.

The ask: "Any services provided by Buyer or its affiliates to the Acquired Business during the Earnout Period shall be priced at arm's-length rates, supported by transfer-pricing documentation acceptable to a qualified expert."

Covenant 5: Maintain separate books, records, and financial statements

The standalone-entity covenant. The buyer commits to maintaining separate accounting for the acquired business throughout the earnout period — preserving auditability and preventing the buyer from wrapping the target inside a larger entity where the metric is impossible to extract.

The ask: "Buyer shall maintain the Acquired Business as a separate accounting entity with separate books, records, and financial statements through the end of the Earnout Period."

Covenant 6: Periodic written reports on metric calculation with supporting schedules

The transparency covenant. The buyer commits to providing quarterly or semi-annual written reports showing the metric calculation, supporting schedules, and any deviations from base-case assumptions. This aligns with established drafting best practices, including Cooley's emphasis on clear, measurable metric calculation in their 2024 earnout drafting guide.

The ask: "Buyer shall deliver to Seller within 45 days after each fiscal quarter-end a written report calculating the Earnout Metric for the Trailing Twelve Months, with supporting schedules detailing material assumptions, allocations, and accounting determinations."

Covenant 7: No material headcount reduction, no customer-contract cancellation, no product-line discontinuance without seller consent

The operational-integrity covenant. The buyer commits not to take specific actions that would predictably crater the metric. Most commonly: no layoffs of acquired employees above X% of headcount, no cancellation of named customer contracts, no discontinuance of acquired product lines.

The ask: "Buyer shall not (a) reduce headcount of Acquired Business employees by more than X% during the Earnout Period, (b) terminate any of the Top-20 Customer Contracts without cause, or (c) discontinue any acquired product line, without Seller's written consent."

Bonus +1: The non-avoidance clause

This is the catchall that the Alexion court enforced in the SRS v. Alexion (Syntimmune) case. The language: "Buyer shall not take any action with the primary purpose of reducing or eliminating earnout payments." It backstops all of Covenants 1-7 against creative buyer behavior the parties didn't anticipate. Required in every SPA.

The Operating Covenant Stack is the single biggest lever you have to convert a "structurally seller-hostile" earnout into a "negotiated, fair" earnout. The buyer's pushback is usually about specific covenant language ("we need flexibility on intercompany pricing because we genuinely use parent IT"); negotiate the specifics, but do not give up the framework. If the buyer refuses Covenants 1-7 entirely, that is a structural signal to walk away from the earnout or rebalance toward more cash.

When should the earnout accelerate? (Acceleration Trigger Matrix)

Frame 3. Acceleration is the seller's safety net for events that fundamentally change the operating environment during the earnout period. ABA 2023 tracking shows acceleration provisions have eroded: 75% of deals now expressly EXCLUDE acceleration on change of control, up from 42% in the 2021 edition. The trend means most founders are signing earnouts that disappear if the buyer flips the company.

| Trigger | Recommended acceleration | ABA 2023 frequency |

|---|---|---|

| Change of control (buyer sold) | 100% earnout at cap, OR pro-rata | Only 25% of deals provide this — 75% expressly EXCLUDE acceleration |

| Founder terminated without cause | 100% at cap (or accelerate if metrics on track) | Common |

| Founder dies / becomes disabled | 100% at cap | Common |

| Buyer breaches operating covenant | Full acceleration | Rare but powerful |

| Buyer sells acquired business as standalone | 100% acceleration | Critical — closes a major loophole |

| Discontinues acquired product line | Acceleration of metrics tied to that line | Standard ask |

The Change-of-Control Acceleration Trap

This is the single biggest seller trap in modern earnouts. Three out of four deals signed in 2022-2023 expressly EXCLUDED acceleration if the buyer sold the acquired business mid-earnout. The seller's worst-case scenario: PE buyer acquires the business, holds for 18 months, sells to another PE buyer at a higher multiple — and the seller's earnout disappears because the original buyer no longer owns the acquired business and the new owner has no contractual obligation under the original SPA.

The negotiation ask: 100% earnout payout at cap on change of control, OR pro-rata payout based on time elapsed in the measurement period. If the buyer refuses both, that is a structural signal that the buyer expects to flip the business and is reserving the right to do so without paying the seller. Rebalance toward more cash upfront.

The compromise that sometimes works: acceleration to a "tag-along" structure where the seller is paid the earnout out of the proceeds of the secondary sale, with the new buyer assuming the obligation. This requires careful drafting to ensure successor liability transfers cleanly.

For-Cause Termination Protection

If the founder stays on as CEO or in a senior operating role post-close, the SPA should protect against the buyer terminating the founder "for cause" on pretextual grounds to extinguish the earnout. The standard mechanics:

- Define "cause" narrowly (fraud, felony conviction, gross negligence, willful misconduct, material uncured breach of employment agreement)

- Exclude generic "underperformance" or "strategic fit" from cause

- Require notice and cure period for any alleged breach

- On termination without cause: 100% earnout at cap (or accelerate based on metrics-to-date)

- On termination for cause: forfeiture, subject to dispute

This protection is non-negotiable if the founder is staying on. Without it, the buyer can terminate the founder six months post-close and crater both the earnout and the founder's continued employment compensation.

Buyer Breach of Operating Covenant

The Operating Covenant Stack (Frame 2) only has teeth if breach triggers acceleration. Standard mechanics: on material breach of any operating covenant (after notice and cure period), the seller can elect either (a) specific performance and damages, or (b) full earnout acceleration at cap. The election preserves the seller's leverage to litigate specific breaches while reserving the nuclear option.

Death, Disability, and Founder-Specific Triggers

If the earnout depends on founder continued involvement (founder is the only person who can hit a milestone, founder is the customer-relationship anchor), death or disability acceleration is required. Without it, the founder's estate or family loses the earnout on a catastrophic event the founder could not control.

The mechanics: full earnout at cap on founder death or permanent disability during the measurement period; payment to estate or designated beneficiary. This also helps the W-2 recharacterization analysis under Lane Processing — payment to estate on death is one of the six Lane factors supporting capital-gain treatment.

How do earnouts get litigated? (Lessons from Auris and Syntimmune)

The Delaware Chancery and Supreme Court have produced the canonical earnout case law over the last 18 months. Two cases anchor the current landscape: the J&J / Auris Health blockbuster (over $600M in damages affirmed January 2026), and the SRS v. Alexion conditional-probability damages methodology ($180.9M awarded June 2025).

The Blockbuster: Johnson & Johnson v. Fortis Advisors (Auris Health)

Citation: Johnson & Johnson v. Fortis Advisors LLC, Delaware Supreme Court (January 12, 2026), affirming in part and reversing in part C.A. No. 2020-0881-LWW, 2024 WL 4040387 (Del. Ch. September 4, 2024).

Deal background: J&J acquired Auris Health in 2019 for $3.4B cash at close plus up to $2.35B in contingent earnouts tied to FDA milestones for Auris's iPlatform and Monarch robotic surgical devices.

Court of Chancery (September 4, 2024): Vice Chancellor Will awarded damages over $1B to Auris stockholders:

- $300M for breach on first earnout payment (Milestone 1, related to De Novo regulatory pathway)

- $600M for breach on remaining earnouts

- $61M for fraud

- Plus pre-judgment interest

Delaware Supreme Court (January 12, 2026): Largely AFFIRMED the Chancery judgment. The reversal was narrow:

- Reversed: First earnout payment of $300M. The Supreme Court held the implied covenant of good faith and fair dealing cannot REQUIRE J&J to pursue De Novo regulatory approval when the contract specified the "510(k)" approval pathway. The implied covenant fills gaps in the contract — it does not override express terms.

- Affirmed: Remaining earnout breach ($600M), fraud ($61M), and the damages methodology.

- Remanded for interest recalculation removing Milestone 1.

What J&J actually did (the playbook the court rejected):

- Launched "Project Manhattan" — internal competition between Auris's iPlatform and J&J's existing Verb device. Created strategic ambiguity about which device J&J actually wanted to commercialize.

- Merged teams in ways that hindered iPlatform development. Reassigned dedicated Auris engineers to Verb work.

- Abandoned Auris's regulatory strategy. Pursued an alternative regulatory pathway rather than the one calibrated to the milestone.

- Altered employee incentive structures. Removed milestone-achievement incentives tied to the iPlatform program; replaced with general J&J performance metrics.

- Prioritized commercialization and short-term profitability over milestone achievement.

- Fraudulently induced Auris to agree to one milestone (the Soft Tissue Ablation Milestone, $100M).

The "commercially reasonable efforts" standard: The Chancery and Supreme Court agreed that J&J's CRE obligation was calibrated against its own "priority medical devices" baseline. The court explicitly rejected J&J's argument that its discretion was unlimited, holding that the buyer was "not permitted to prioritize commercialization, product differentiation, or short-term profitability" over milestone achievement.

The drafting takeaway: "Commercially reasonable efforts" calibrated to the buyer's own priority products baseline is the standard that survived appeal. The drafter's ask: define the efforts standard explicitly, name a comparable category of buyer products, and require operating-decision parity with that category. Auris is the playbook for what NOT to let happen. If the SPA does not have anti-avoidance covenants and a calibrated efforts standard, your earnout is theater.

The Damages Methodology Case: SRS v. Alexion (Syntimmune)

Citation: Shareholder Representative Services LLC v. Alexion Pharmaceuticals, Inc., C.A. No. 2020-1069-MTZ (Del. Ch.); liability opinion September 5, 2024; damages opinion June 11, 2025.

Deal background: Alexion acquired Syntimmune in 2018; $800M in earnouts across 8 milestones over 7 years tied to clinical trial endpoints and regulatory approvals.

Standard: "Commercially reasonable efforts, measured against similarly situated companies" plus a non-avoidance provision: "Buyer shall not take any action with the primary purpose of reducing earnout payments." The non-avoidance clause is the one I now insist on in every SPA.

Court of Chancery liability (September 5, 2024): Vice Chancellor Zurn found Alexion failed CRE — abandoned the Syntimmune development program in favor of competing internal priorities.

Damages opinion (June 11, 2025): $180.9M awarded. NOT the $700M+ that SRS claimed under a "prevention doctrine" theory (assume 100% milestone hit since Alexion prevented achievement).

Why the damages number matters: The court used conditional probability analysis to compute expectation damages. Method: apply the buyer's contemporaneous internal probability estimates of milestone achievement at the time of breach to the milestone payout values. Result: even when the seller WINS on liability, the "assume 100% achievement" argument FAILS. The court will award expectation damages based on the probability the milestone would actually have been hit absent buyer interference.

The drafting takeaway: The non-avoidance clause works in court (Alexion confirms it). But the damages methodology limits the seller's recovery to the probability-weighted expectation, not the gross milestone amount. The implication for negotiation: if you suspect the buyer's internal probability estimate of milestone achievement is low (because the milestone is structurally hard), the conditional-probability damages floor is lower than the maximum cap. Negotiate accordingly.

The Buyer Wins Sometimes: Pacira BioSciences v. Fortis Advisors

Citation: Pacira BioSciences v. Fortis Advisors LLC, Delaware Court of Chancery (January 21, 2025).

Deal: $200M MyoScience acquisition ($120M upfront plus $100M in milestone earnouts).

Outcome: Buyer won. The court found earnout milestones were not triggered, rejecting the seller's post-hoc "new interpretation" of the agreement. The court held that ambiguous milestone language interpreted against the seller's later interpretation.

The drafting takeaway: Precise milestone triggers matter. Sellers cannot rely on ambiguity working in their favor after close. If your milestone definition is loose, the buyer will argue the most restrictive interpretation, and the court may agree. Draft milestone definitions with the same precision you would draft a complex commercial contract — including illustrative examples, edge cases, and explicit treatment of partial achievement.

Other Verified 2024-2025 Cases

Himawan v. Cephalon, 2024 WL 1885560 (Del. Ch. 2024): Express buyer-discretion language OVERRIDES any implied "best efforts" obligation. If your SPA says "in buyer's sole discretion," you have no efforts protection. Avoid sole-discretion language at all costs. Negotiate to "commercially reasonable efforts" calibrated to priority products.

Medal v. Beckett Collectibles, No. 2023-0984-VLM, 2024 WL 3898535 (Del. Ch. 2024): Acceleration-on-termination ambiguity resolved FOR seller under contra proferentem (ambiguity against drafter). But the lesson is to draft precisely so you don't depend on tiebreakers.

Retail Pipeline v. Blue Yonder (Del. Ch. 2024): Good-faith covenant didn't catch buyer cost-shifting because contract didn't enumerate the behavior. Lesson: list prohibited behaviors explicitly; do not rely on implied good-faith.

Menn v. ConMed Corp., No. 2017-0137-KSJM, 2022 WL 2387802 (Del. Ch. 2022): "Commercially best efforts" — buyer discontinued product for safety concerns — NO BREACH. The buyer can kill a milestone for legitimate operational reasons. Distinguish from Auris: ConMed had a documented safety rationale; J&J had an internal competitive product.

Schneider National Carriers v. Kuntz, No. N21C-10-157-PAF, 2022 WL 1222738 (Del. Super. 2022): Ambiguous "60 tractors" requirement, extrinsic evidence favored seller, $40M payment ordered. Reinforces the precision lesson from Pacira — drafting matters.

The Foundational Quote

Vice Chancellor Laster, in Airborne Health, Inc. v. Squid Soap, LP, 984 A.2d 126 (Del. Ch. 2009):

"An earn-out often converts today's disagreement over price into tomorrow's litigation over the outcome."

The single most-quoted sentence in modern Delaware earnout law. It captures the structural pathology: an earnout is an economic device that converts the parties' valuation disagreement into a contractual obligation to litigate the future. The 28% dispute rate is the modern manifestation of Laster's observation.

What's the tax treatment of an earnout?

Frame 5's foundation. The earnout's tax treatment is the most-overlooked structural element in most LOIs. Most founders don't realize the §453A trap until their CPA models it post-close. Front-load that math BEFORE you sign.

IRC §453 — The Installment Method (default for contingent earnouts)

Contingent earnouts default to installment-method treatment under Treas. Reg. §15A.453-1(c). The mechanics:

- Treasury regs assume 100% of contingent payments WILL be made in the shortest permissible period

- Gross-profit percentage calculated against that maximum cap

- Gain recognized proportionally as actual payments arrive

- Stock sales: all deferred gain remains LTCG — preferential rates apply

- Asset sales: taxed per asset class; recapture under §1245 (personal property) and §1250 (real property) is BARRED from installment treatment and must be recognized in the year of sale

The implication for stock sales is favorable: the installment method preserves LTCG on the entire deferred gain. The implication for asset sales is less favorable: recapture accelerates into year-of-sale ordinary income.

IRC §453A — The $5M Trap (CRITICAL — most founder earnouts hit this)

This is the single most-overlooked tax trap in M&A earnouts, and the single most-important thing to model with a CPA before signing.

Under IRC §453A, outstanding installment obligations from sales over $150K that exceed $5M at year-end trigger an interest charge:

- Interest charge formula: AFR multiplied by the deferred tax liability attributable to the amount over $5M

- Effect: effectively NEUTRALIZES the deferral benefit on most M&A earnouts

- Why it hits founder earnouts: any reasonable earnout on a deal over a few million dollars will have outstanding installment obligations far above $5M at year-end during the measurement period

The founder action: model the §453A interest charge with a CPA before agreeing to a multi-year earnout. The math sometimes makes the election out of installment method (§453(d), discussed below) the right call.

IRC §483 and §1274 — Imputed Interest

Payments more than 6 months after sale must include market-rate interest. If the stated interest rate is less than the Applicable Federal Rate (AFR), §1274 imputes interest (or §483 if not under §1274).

The critical consequence: imputed interest is ORDINARY income at the seller's marginal rate, NOT LTCG. For a founder in the top federal bracket plus state tax, the rate delta is substantial (potentially 37% federal plus state vs 20% LTCG plus state).

The founder action: include an explicit interest rate at or above AFR on deferred payments in the SPA. This converts what would have been imputed (and ordinary-income) interest into stated (and characterizable) interest, giving the founder more control over the tax treatment. Coordinate with the CPA on the rate.

Compensation Recharacterization (the founder-CEO killer)

This is the IRS challenge that turns a "$15M earnout taxed at LTCG" into a "$15M W-2 wage taxed at top marginal rates plus FICA." The governing test is the six-factor analysis from Lane Processing Trust v. U.S., 25 F.3d 662 (8th Cir. 1994):

| Capital-Gain Treatment | W-2 Recharacterization Risk |

|---|---|

| Earnout paid REGARDLESS of continued employment | Earnout forfeited if employment ends |

| Pro-rata distribution to all former owners per equity % | Only employed former owners get earnout |

| Reasonable arm's-length compensation in separate employment agreement | Earnout IS the founder's "comp" |

| Earnout characterized as purchase price in SPA + tax disclosures | SPA conflates earnout + services |

| Payable to estate on death/disability | Forfeits on death/disability |

| Earnout allocated to goodwill in §1060 residual method | Allocated to services |

The killer clause to AVOID in any SPA: "Seller forfeits earnout if employment is terminated for any reason." That single sentence is a near-automatic W-2 recharacterization trigger and converts the entire earnout from LTCG to ordinary income.

Best practice: decouple earnout from employment. Pay a reasonable market salary plus performance bonus through a separate employment agreement. Structure the earnout to reward EQUITY (ownership), not labor (services). Allocate the earnout to goodwill in the §1060 residual method. Make the earnout payable to the founder's estate on death.

Election Out of Installment Method (§453(d))

The seller can elect to recognize all gain in the year of sale under IRC §453(d). This is counterintuitive — most founders want to defer gain — but it is sometimes the right call:

- If §453A interest charge will be punitive on a multi-year earnout

- If the LTCG rate is expected to rise (the deferred gain would otherwise be taxed at a higher future rate)

- If the seller has unused capital losses or NOLs to offset year-of-sale gain

- If the seller wants tax certainty at the cost of liquidity

The election requires modeling with a CPA. The standard approach: project the §453A interest charge under several scenarios (full earnout payout, 50% payout, 21% payout per the SRS Acquiom benchmark), compare to the cost of paying tax in year of sale, and make the election based on the lowest expected after-tax outcome.

What is the Buyer-Side Manipulation Playbook?

Frame 4. The eight specific moves I have seen buyers use to suppress earnouts, drawn from the J&J / Auris record, general practice, and SPA dispute case law:

| Manipulation Move | Real-world example | Block in SPA |

|---|---|---|

| 1. Overhead dumping | Allocate parent HQ costs to acquired sub | Cap overhead allocation at pre-deal % |

| 2. Intercompany transfer pricing | Charge acquired co inflated prices for parent services | Arm's-length pricing required |

| 3. Discontinuing the product | J&J merged iPlatform teams; abandoned regulatory strategy | "Continue dev with same priority as comparable products" |

| 4. Cutting R&D / marketing | Slash spend to hit short-term profitability | Min spend levels via budget approval mechanism |

| 5. Repurposing employees | "Project Manhattan" — internal competition with parent's product | No reassignment of dedicated employees without seller consent |

| 6. Altering employee incentives | J&J changed incentive structures away from milestone | Continuation of pre-close incentive comp during earnout |

| 7. Pursuing alternative product first | Buy 2 competing assets, pick favorite | Equal-priority covenant ("not less favorably than priority products") |

| 8. Wrap target in larger entity | Make metrics impossible to extract | Standalone-entity covenant + separate financial statements |

Move 1: Overhead Dumping

The most common EBITDA suppression. Parent HQ allocates corporate overhead, shared services, executive compensation, legal, finance, IT, HR, and corporate insurance to the acquired sub. Even allocations that appear "fair" by traditional cost-accounting standards suppress standalone EBITDA the earnout is measured against.

The block: Operating Covenant 3 (no allocation of corporate overhead unrelated to the acquired business). Combined with Covenant 5 (separate books) and Covenant 6 (periodic reports with supporting schedules), the seller can verify in real time that allocations are not being introduced.

Move 2: Intercompany Transfer Pricing

The companion move. If the parent provides services to the acquired sub, the intercompany prices can be inflated to suppress EBITDA. Often paired with Move 1 — the parent both allocates overhead AND charges intercompany services on top.

The block: Operating Covenant 4 (arm's-length intercompany pricing), with transfer-pricing documentation acceptable to a qualified expert. Critical in carve-out deals where genuine intercompany services exist.

Move 3: Discontinuing the Product

The J&J / Auris move. The buyer abandons the acquired product line in favor of competing internal products, then claims the milestone wasn't hit because "the market shifted" or "regulatory strategy needed to change."

The block: Operating Covenant 7 (no product-line discontinuance without seller consent), plus the "calibrated efforts" standard from the Auris ruling (continue development with the same priority as comparable buyer products), plus the non-avoidance clause.

Move 4: Cutting R&D / Marketing

The buyer reduces R&D, marketing, or sales investment to inflate short-term profitability and meet broader parent-level targets — at the cost of the acquired business's metric.

The block: minimum spend covenant. The SPA specifies minimum R&D, marketing, or sales spend as a percentage of revenue, or in absolute terms, during the earnout period. Variance from minimum requires seller consent or triggers acceleration.

Move 5: Repurposing Employees

The "Project Manhattan" move. The buyer reassigns dedicated acquired-business employees to parent projects or competing products, hollowing out the team that was supposed to hit the milestone.

The block: no-reassignment covenant. The SPA specifies that named or roled employees of the acquired business cannot be reassigned to non-acquired-business work without seller consent. Pair with retention escrow and key-person identification.

Move 6: Altering Employee Incentives

The J&J move that the Chancery court called out. The buyer removes milestone-achievement incentives from acquired employees' compensation and replaces with general parent-level performance metrics. Employees no longer optimize for the milestone the founder is depending on.

The block: continuation of pre-close incentive compensation during the earnout period. The SPA specifies that incentive comp tied to the milestone or metric remains in place during the measurement period for the named employees.

Move 7: Pursuing Alternative Product First

The buyer acquires two competing products and picks the favorite, leaving the acquired business's product to atrophy. Common in pharma (where buyers acquire multiple compounds in the same therapeutic area) and tech (where buyers acquire multiple competing technologies).

The block: equal-priority covenant. The SPA specifies that the buyer must develop and commercialize the acquired product "not less favorably than" comparable priority products in the buyer's portfolio. Calibrated against named buyer-product comparables.

Move 8: Wrapping Target in Larger Entity

The buyer consolidates the acquired business into a larger reporting segment, making the standalone metric impossible to extract. EBITDA is reported only at the segment level; standalone numbers disappear.

The block: Operating Covenant 5 (separate books) plus reporting covenant (Covenant 6). The SPA requires the buyer to maintain the acquired business as a separate accounting entity with standalone financial statements throughout the earnout period.

What is the Tax Recharacterization Risk Index?

Frame 5. A scoring checklist for the W-2 recharacterization risk. Higher score equals higher risk of IRS challenge and the conversion of LTCG earnout to ordinary-income wages.

| Risk Factor | Points |

|---|---|

| Earnout forfeits on employment termination (any reason) | 40 (deal-breaker) |

| Founder is the only person who can hit milestone | 15 |

| Earnout disproportionate to founder's equity % | 15 |

| Earnout vesting tied to service date | 15 |

| No separate compensation agreement | 10 |

| Earnout characterized as "bonus" in SPA | 10 |

| Only continuing employees receive earnout | 10 |

| Payment NOT to estate on death | 5 |

Score above 40: high IRS recharacterization risk. The earnout will likely be challenged as compensation, converting LTCG to ordinary income plus FICA.

Score 20-40: moderate risk. Restructure to reduce exposure.

Score below 20: acceptable. The earnout is structurally characterizable as purchase price.

The Deal-Breaker Clause

Any earnout that forfeits on employment termination is structurally W-2 wages, regardless of how it's labeled in the SPA. The IRS will challenge, and Lane Processing supports the IRS position. The single most-important fix in any earnout SPA: remove "forfeits on employment termination" language entirely. Replace with:

- Earnout paid regardless of employment status during the measurement period

- Separate employment agreement with reasonable market compensation

- For-cause termination protection (narrowly defined) does NOT trigger forfeiture

- Death and disability trigger acceleration, not forfeiture

This single restructuring move can convert a $15M earnout from $9M after-tax (W-2 plus FICA) to $11M after-tax (LTCG plus net investment income tax). The 22-percentage-point delta is the cost of getting recharacterization wrong.

The 18-Month Pre-Sale Planning Window

The Tax Recharacterization Risk Index works best when applied 18-24 months before sale. Restructuring founder employment, compensation, and ownership structures to support capital-gain treatment takes time and creates audit-defensible documentation. Last-minute restructuring at LOI signing is harder to defend — the IRS will look for the substance-over-form analysis, and a 30-day pre-LOI restructuring looks pretextual.

The pre-sale checklist:

- Document founder market compensation at the existing role (third-party benchmark)

- Confirm founder equity ownership consistent with executive equity at comparable companies

- Ensure existing employment agreement is at arm's-length terms

- Separate executive bonus structure from ownership-based earnout

- Document the §1060 residual-method allocation supporting goodwill characterization

Worked examples: $50M deal with 30% earnout ($15M), 2-year duration

Three scenarios applied to a hypothetical sale of a $50M deal where 30% of consideration ($15M) is structured as an earnout over 24 months. Pre-close revenue $20M, pre-close EBITDA $4M.

Scenario A: Revenue-based 2-year cliff at 110% of pre-close base

Structure:

- Pre-close revenue: $20M

- Cliff threshold: $22M revenue ($20M × 110%)

- Cap: $15M

Outcomes:

- Hit $22M+ revenue → $15M earnout paid

- Hit $21.99M revenue → $0 earnout (cliff!)

- Hit $26.4M (120% of base) → $15M paid (capped)

Founder downside: buyer cuts marketing spend, revenue falls $500K short → cliff fails → founder loses $15M.

Defense: negotiate to sliding scale (linear from 95% to 115% of base, paying $0 at 95% and $15M at 115%) and minimum marketing spend covenant. The sliding scale converts a binary cliff outcome into a continuous payout function — a $500K revenue miss reduces the payout by ~10% rather than to zero.

Scenario B: SAME deal but EBITDA-based at 110% of pre-close EBITDA

Structure:

- Pre-close EBITDA: $4M (20% margin)

- Threshold: $4.4M EBITDA (110% of base)

- Cap: $15M

Buyer manipulation toolkit:

- Overhead dumping: allocate $500K of parent HQ costs to acquired sub → EBITDA $3.9M → MISS

- Intercompany "consulting": charge $400K for parent IT services → MISS

- Forced new R&D: "strategic investment" $300K → MISS

- Combined effect: $1.2M of allocations → EBITDA reduced from $4.4M to $3.2M → cliff missed → $0 paid

Defense: lock EBITDA definition with explicit exclusions:

- Corporate overhead allocations

- Intercompany charges over $X

- Post-close integration costs

- Buyer-mandated capex

Add arm's-length pricing test on any remaining charges. The exclusion list converts $1.2M of buyer suppression moves into $0 of EBITDA adjustment — and the threshold gets hit.

Scenario C: Milestone-based (FDA approval + 80% customer retention through Year 2)

Structure:

- Two milestones, $7.5M each = $15M total

- Milestone 1: FDA approval ($7.5M)

- Milestone 2: 80% customer retention (top-20 customers by revenue at close)

FDA approval ($7.5M):

- All-or-nothing

- Risk: buyer pursues alternative regulatory pathway (J&J / iPlatform pattern) → MISS

- Defense: anti-avoidance clause; minimum effort calibrated to "priority products"; alternative-pathway substitute clause that triggers acceleration if the buyer pursues a different regulatory path

Customer retention 80% ($7.5M):

- Tracking: top-20 customers by revenue at close, measured at Year 2

- Risk: buyer raises prices 20% → customers churn → MISS

- Defense: buyer cannot unilaterally raise customer prices more than X% during the earnout period; cannot deprecate features or change support terms in ways that drive churn; named-customer contract renewal terms are honored

The composite design ($7.5M each) means failure on one milestone doesn't crater the whole earnout. The independence of the two milestones converts a single-point-of-failure structure into a more robust 50/50 structure. Pair with the operating covenants above.

Earnout vs Rollover Equity vs Seller Note: which one belongs in your capital stack?

Frame 6. All three structures bridge a valuation gap, but they have very different risk-return profiles and tax treatments. The decision tree:

| Structure | Founder upside | Founder downside | Tax treatment | Use when |

|---|---|---|---|---|

| Earnout | High (uncapped to cap) | Total loss if metrics miss; no governance over operating environment | LTCG on capital, ordinary on imputed interest, §453A trap | Strong growth conviction + founder stays involved |

| Rollover Equity | Tied to buyer's full equity arc | Minority position, no governance, illiquid | Generally tax-deferred at rollover under §721 or §351; LTCG on subsequent exit | Believe in PE's broader thesis; long exit horizon |

| Seller Note | Fixed, certain | Subordinate to buyer debt; default risk | LTCG plus ordinary income on interest; §453 deferral available | Valuation gap with creditworthy buyer; want certain cash flow |

My default ranking: Rollover > Earnout > Seller Note

For most founders facing a valuation gap, the ranking I recommend is rollover > earnout > seller note. The reasoning:

Rollover equity gives the founder "skin in the game" but diversifies across the buyer's broader trajectory. If the PE sponsor's overall thesis works, the rollover pays off — and the rollover return is not contingent on the acquired business specifically performing. The founder rides the sponsor's flywheel, not the specific-business-line risk.

Earnout concentrates 100% of contingent value on metrics the buyer controls. The founder absorbs all the manipulation risk (the 79% unpaid rate) plus all the specific-business-line risk. The worst risk-adjusted profile if the founder has no governance over operating decisions.

Seller note is appropriate when the founder wants certain cash flow and the buyer is creditworthy. But the founder accepts subordination to senior debt and default risk in exchange for certainty. Works for risk-averse founders or in deals where the buyer has limited equity capital and is using debt to bridge the gap.

The Composite Structure

In practice, many sophisticated sell-side processes end up with a composite: cash at close + rollover equity + earnout + seller note. Each component plays a different role:

- Cash at close: liquidity and de-risking for the founder

- Rollover equity: alignment with buyer thesis and tax-deferred upside

- Earnout: valuation bridge tied to founder-anchored performance metrics

- Seller note: valuation bridge with certain cash flow

The composite design lets the founder diversify across structures rather than betting the entire contingent share on a single earnout. The mechanics: negotiate the size of each component independently against the headline deal value, with structural protections appropriate to each (covenants for earnout, governance rights for rollover, security for seller note).

When NOT to take an earnout

I would push founders to walk away from an earnout structure in these specific scenarios:

- Buyer refuses both change-of-control acceleration AND for-cause termination protection. Structural seller-hostile signal.

- Buyer insists on EBITDA-based earnout AND refuses a frozen EBITDA definition. Reserves the right to manipulate.

- Buyer insists on net-income earnout. Always a no.

- Earnout share above 30% of headline deal value. Disproportionate contingent risk; rebalance toward cash.

- Buyer refuses the Operating Covenant Stack. No structural protection against manipulation.

- Founder is not staying involved post-close, but earnout is tied to operational metrics the buyer will control. The founder has zero levers to influence the outcome.

- The §453A interest charge math is punitive AND the buyer refuses to gross up the earnout to offset. Tax economics broken.

In any of these scenarios, the negotiation move is to rebalance toward more cash upfront, more rollover equity, or a seller note with security — anything other than an earnout the buyer can manipulate.

How does a tighter sell-side process reduce earnout pressure?

The structural lever upstream of all of the SPA-drafting frames above. The buyer's leverage to insist on an earnout is inversely proportional to the seller's negotiating leverage in the process. A well-run, multi-bidder sell-side process compresses the earnout share at the LOI stage — sometimes eliminates it entirely.

Multi-Bidder Process Economics

When a single buyer is the only viable bidder, that buyer can insist on an earnout share of 25-35% of headline value. The seller's BATNA is to walk away from the entire deal, which is not actually feasible after months of process. The buyer captures the leverage.

When 3-5 bidders are active and bidding competitively, the negotiating dynamic shifts. The seller can compare offers structurally and reward the buyer offering more cash upfront, smaller earnout share, and tighter protections. The buyer who insists on a 30% earnout sees the deal go to the buyer offering 10-15% earnout plus rollover, and starts compressing their own contingent share to remain competitive.

The data: SRS Acquiom's tracking shows earnout prevalence is lower in competitive auctions than in negotiated single-buyer processes. The structural reason: competition.

The Data Room as a Competitive Lever

The data room is the substrate for the competitive process. A tight, well-organized data room with granular access controls, audit trail on what each buyer has reviewed, and analytics showing buyer engagement is a structural lever for compression:

- Visitor groups let the seller run parallel diligence with strategics, PE, and family offices without each party seeing the others' presence — preserving competitive tension

- Page-level analytics identify which buyers are genuinely engaged vs surface-level, letting the seller allocate negotiation time to serious bidders

- Audit trail documents what each buyer reviewed during DD, which becomes useful evidence in post-close earnout disputes (you can show the buyer saw the specific risk factors during DD)

- Per-recipient watermarks preserve identity on each document, useful in leakage disputes during process and in post-close evidence chains

The honest competitive framing: Peony is the substrate that supports a tighter sell-side process, which reduces the negotiated earnout share, which reduces the founder's structural exposure to the 79% unpaid rate. We do not draft the earnout — that is the M&A counsel's job — and we do not model the §453A trap — that is the CPA's job. But the process layer Peony enables is the upstream lever that makes the SPA-drafting layer matter less.

Datasite, Intralinks, iDeals, and Firmex provide similar competitive-process substrate at higher price points (typically 5-10x Peony pricing on sub-$300M EV processes). Above $500M EV with bank-led process and institutional R&W coverage, the institutional integrations on those platforms are often the right call. For most founder-led sub-$300M EV processes, Peony's pricing lets the seller invest more in advisor and counsel fees and less in VDR spend — which is the right allocation.

Bottom line

Earnouts pay out only 21 cents on the dollar in 2024 per the SRS Acquiom 2025 Deal Terms Study. 79% of earnout dollars never get paid. 28% of earnouts are contested. The trend across 2024-2026: prevalence is DOWN (ABA 2025 = 18%, vs 26% in 2023 ed.), but the earnouts that ARE used are getting structurally more buyer-friendly. 75% of deals now expressly EXCLUDE change-of-control acceleration. 50% give buyer post-close operating discretion. 25% include express disclaimer of buyer fiduciary duty.

The seven frames I use to navigate this: the Earnout Metric Risk Ladder to pick the right metric (Revenue > GP > EBITDA > Net Income); the Operating Covenant Stack to lock 7 covenants plus the non-avoidance clause into the SPA; the Acceleration Trigger Matrix to negotiate the safety nets (change of control, for-cause termination, breach, standalone sale, product discontinuation); the Buyer-Side Manipulation Playbook to anticipate the 8 specific moves and the SPA blockers; the Tax Recharacterization Risk Index to score and restructure the W-2 risk; the Earnout vs Rollover vs Seller Note decision tree to allocate contingent capital across the right structures; and the 79% Stat as a forcing function for the pre-LOI cash-vs-contingent split conversation.

The Delaware case law has converged on a clear standard: "commercially reasonable efforts" calibrated to the buyer's own priority products baseline is enforceable. The non-avoidance clause works. Precise milestone definitions win. The Auris affirmance ($600M+ damages plus $61M fraud, affirmed January 2026) is the playbook for what NOT to let happen — and the SPA needs the covenant stack to block it.

The tax structure matters more than most founders realize. The IRC §453A interest charge on installment obligations over $5M effectively neutralizes the deferral benefit on most M&A earnouts. The §483 and §1274 imputed-interest mechanics convert what should be controllable interest into ordinary income. The Lane Processing six-factor test for compensation recharacterization can convert a $15M LTCG earnout into a $9M after-tax W-2 wage if the SPA has the wrong forfeiture-on-termination clause.

The one move I would push every founder facing an earnout to make: at LOI signing, model the unbiased expected value of the proposed earnout under the SRS Acquiom 21% benchmark, compare it to the alternative of more cash plus rollover plus seller note, and negotiate the cash-vs-contingent split based on the risk-adjusted comparison. If the buyer refuses both change-of-control acceleration and for-cause termination protection — or refuses the Operating Covenant Stack — rebalance toward more cash. The downside risk on a poorly-structured earnout is large. The upside is mostly theoretical.

Most founder earnouts pay out the way the SRS Acquiom data predicts: somewhere around 21 cents on the dollar. The frames in this post are how you shift your specific deal toward the right tail of that distribution.

Related resources

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — the canonical process guide for the DD that feeds into the earnout SPA

- Mergers and Acquisitions Process Guide — full sell-side process structure

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side vendor DD scope, including pre-marketing financial remediation

- Hard vs Soft Due Diligence Playbook — the 5-frame DD playbook covering the soft DD that affects post-close earnout dynamics

- Due Diligence Timeline: The Critical-Path Playbook — the 6-workstream critical-path map for DD-to-close timing

- Types of Mergers and Acquisitions — structural primer on stock vs asset deals (with earnout interaction)

- Merger vs Acquisition: Founder Decision Guide — structural choice that affects earnout design

- Independent Sponsor LOI Playbook — capital-stack design including earnout, rollover, and seller note for independent-sponsor structures

- Roll Equity in M&A Deals: 2nd-Bite Math + OBBBA QSBS Trap — the parallel ship on rollover; earnouts and rollovers are the two main deferred-consideration mechanisms

- Due Diligence Mistakes That Kill Deals — the broader DD-failure pattern library including the "Earnout Drafting That Guarantees Litigation" section

- Best M&A Advisors NYC, SF, LA, Chicago, Boston, DC, Miami, Dallas, Houston, Atlanta, Charlotte, Nashville, Minneapolis, Philadelphia, Phoenix, San Diego, Seattle — city-specific M&A advisor coverage for sellers running region-anchored processes

Footnotes and sources

- SRS Acquiom. "2025 Deal Terms Study." https://www.srsacquiom.com/our-insights/deal-terms-study-2025/

- SRS Acquiom. "M&A Claims Insights: Undisclosed Liabilities and Earnouts." https://www.srsacquiom.com/our-insights/ma-claims-undisclosed-liabilities-earnouts/

- SRS Acquiom. "M&A Earnouts Overview." https://www.srsacquiom.com/our-insights/ma-earnouts-overview/

- SRS Acquiom. "2025 Life Sciences M&A Study." https://www.srsacquiom.com/our-insights/life-sciences-m-and-a-study/

- ABA Business Law Section. "Private Target M&A Deal Points Study (2023 ed.)." https://businesslawtoday.org/

- ABA Business Law Section. "Private Target M&A Deal Points Study (2025 ed.; released December 2025)." https://businesslawtoday.org/

- Harvard Law School Forum on Corporate Governance. "The Art and Science of Earn-Outs in M&A" (July 11, 2025). https://corpgov.law.harvard.edu/2025/07/11/the-art-and-science-of-earn-outs-in-m-a/

- Harvard Law School Forum on Corporate Governance. "Drafting Guidance from Delaware Supreme Court on Earn-Outs" (February 10, 2026). https://corpgov.law.harvard.edu/2026/02/10/drafting-guidance-from-delaware-supreme-court-on-earn-outs/

- Cooley. "4 Tips for Drafting Earnouts To Avoid Disputes" (June 21, 2024). https://www.cooley.com/news/insight/2024/2024-06-21-4-tips-for-drafting-earnouts-to-avoid-disputes

- Mayer Brown. "Delaware Chancery Court Applies Conditional Probability in Earnout Damages Analysis" (June 2025). https://www.mayerbrown.com/en/insights/publications/2025/06/delaware-chancery-court-applies-conditional-probability

- Arnold & Porter. "Lessons From Johnson & Johnson v. Fortis Advisors" (March 2026).

- IRS. "Publication 537: Installment Sales (2025)." https://www.irs.gov/publications/p537

- Cornell Legal Information Institute. "26 USC §453: Installment method." https://www.law.cornell.edu/uscode/text/26/453

- Cornell Legal Information Institute. "26 USC §453A: Special rules for nondealers." https://www.law.cornell.edu/uscode/text/26/453A

- Cornell Legal Information Institute. "26 USC §483: Interest on certain deferred payments." https://www.law.cornell.edu/uscode/text/26/483

- Cornell Legal Information Institute. "26 USC §1274: Determination of issue price in case of certain debt instruments." https://www.law.cornell.edu/uscode/text/26/1274

- IRS. "Applicable Federal Rates." https://www.irs.gov/applicable-federal-rates

- Casetext. "Lane Processing Trust v. United States, 25 F.3d 662 (8th Cir. 1994)." https://casetext.com/case/lane-processing-trust-v-united-states

- Casetext. "Airborne Health, Inc. v. Squid Soap, LP, 984 A.2d 126 (Del. Ch. 2009)." https://casetext.com/case/airborne-health-inc-v-squid-soap-lp

- Johnson & Johnson v. Fortis Advisors LLC. Delaware Supreme Court (January 12, 2026), affirming in part and reversing in part C.A. No. 2020-0881-LWW, 2024 WL 4040387 (Del. Ch. September 4, 2024).

- Shareholder Representative Services LLC v. Alexion Pharmaceuticals, Inc. C.A. No. 2020-1069-MTZ (Del. Ch.); liability opinion September 5, 2024; damages opinion June 11, 2025.

- Pacira BioSciences v. Fortis Advisors LLC. Delaware Court of Chancery (January 21, 2025).

- Himawan v. Cephalon, Inc., 2024 WL 1885560 (Del. Ch. 2024).

- Medal v. Beckett Collectibles LLC, No. 2023-0984-VLM, 2024 WL 3898535 (Del. Ch. 2024).

- Menn v. ConMed Corp., No. 2017-0137-KSJM, 2022 WL 2387802 (Del. Ch. 2022).

- Schneider National Carriers, Inc. v. Kuntz, No. N21C-10-157-PAF, 2022 WL 1222738 (Del. Super. 2022).

- White & Case. "Building Better Earnouts In The Current M&A Climate." https://www.whitecase.com/insight-alert/building-better-earnouts-current-ma-climate

- Mintz. "Pre-Closing Covenants: Operating in the Ordinary Course of Business." https://www.mintz.com/insights-center/viewpoints/2186/2024-pre-closing-covenants

- Linden Law Partners. "Earnouts in M&A Transactions: Structuring, Risks and Best Practices." https://lindenlawpartners.com/earnouts-in-m-and-a-transactions/