14 Best M&A Advisors in Minneapolis for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

14 Best M&A Advisors in Minneapolis for $5M-$300M Deals (2026)

Quick answer: I have run M&A processes across enough Twin Cities mandates and watched enough Minneapolis buy-side and sell-side processes to have firm conclusions on which advisors win which deals. The 14-firm shortlist for 2026: Piper Sandler, BMO Capital Markets (Greene Holcomb Fisher legacy bench), Craig-Hallum Capital Group, Hennepin Partners, Cherry Tree & Associates, Northland Securities, Aethlon Capital, Madeira Partners, Quazar, Bayview Capital Group, Vermillion Capital, True North M&A, SealedBid Marketing, and BlackTorch Capital. Medtech and healthcare services dominate the 2024-2026 deal flow — anchored by UnitedHealth-Amedisys $3.3B, Ecolab-CoolIT $4.75B, Patterson-Patient Square $4.1B, IonQ-SkyWater $1.8B, Medtronic-CathWorks $585M, Resonetics-Resolution Medical, and the 530-medtech-company Medical Alley cluster. Six proprietary frames below distinguish the right advisor by sub-vertical.

Last updated: May 2026

Why I wrote this

I have run buy-side and sell-side diligence on hundreds of deals across founder-led sales, PE recapitalizations, strategic acquisitions, and venture-stage exits. At Peony we now serve more than 5,900 customers, and the Twin Cities is one of the densest mid-market clusters in our 283-deal Q3 2025-Q1 2026 platform benchmark. The Tier A US M&A Mega cluster series has now shipped 16 city posts (NYC, Boston, Philadelphia, DC, Atlanta, Charlotte, Miami, Chicago, Dallas, Houston, LA, SF, Seattle, Phoenix, San Diego, Nashville). Minneapolis is the 17th — and structurally different from the prior 16.

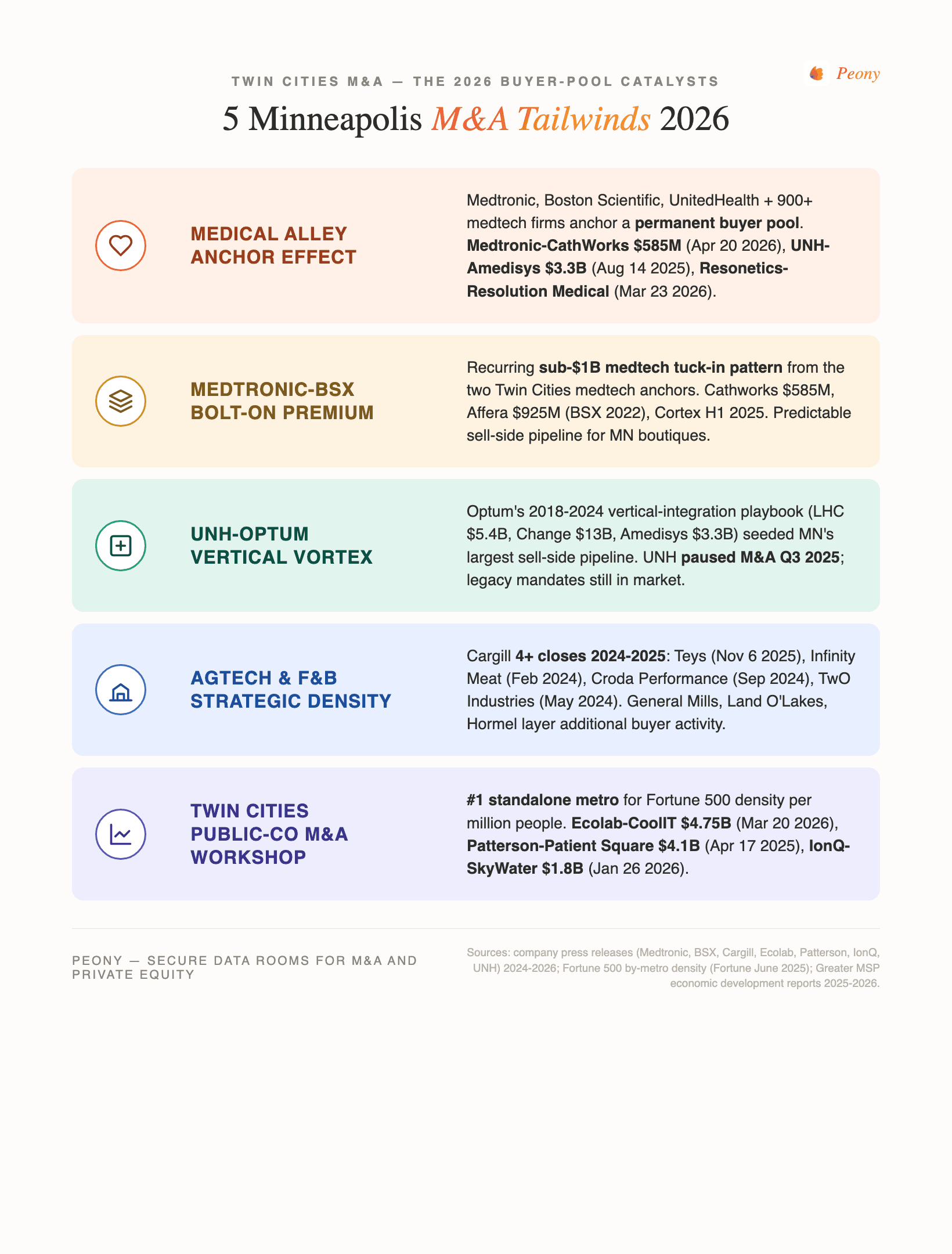

Minneapolis's M&A landscape concentrates in medtech and healthcare services to a degree no other US metro matches. Medtronic has been headquartered in Fridley MN for decades; Boston Scientific operates its cardiac-rhythm-management franchise in the Mpls metro; 3M and its 2024 spinoff Solventum sit in Maplewood; UnitedHealth Group (Minnetonka HQ) ranks #3 on the Fortune 500. The cluster effect: 95% of Minnesota's medical-device ecosystem sits within a 50-kilometer radius of downtown Minneapolis per Medical Alley Association, with approximately 800 healthcare organizations employing 500,000 Minnesotans and 530-plus medical-device companies. The 2024-2026 deal record bears it out: UnitedHealth-Amedisys closed August 14 2025 at $3.3B (after the DOJ-mandated 164-facility divestiture), Medtronic-CathWorks closed April 20 2026 at $585M (intent February 3 2026), Resonetics-Resolution Medical (Fridley MN) closed March 23 2026, and Boston Scientific-Penumbra was announced January 2026 at $14.5B.

Beyond medtech, the Twin Cities hosts the densest cluster of food and agribusiness anchors in the US: Cargill (Wayzata), General Mills (Golden Valley), Land O'Lakes (Arden Hills), and Hormel Foods (Austin MN). Cargill alone closed 4+ verified deals across 2024-2025 — outpacing General Mills and Hormel 3-4x. The Twin Cities also hosts 17 Fortune 500 HQs as of 2025, ranking #1 standalone metro for F500 HQ density by population. And the Ecolab-CoolIT $4.75B deal (announced March 20 2026, prior owners KKR + Mubadala paid only $270M in June 2023, a 17.6x markup in 2.75 years) shows how aggressively Mpls public companies are now positioning for AI infrastructure.

This post is the working playbook I would hand to a Twin Cities medtech founder exploring exit, a Minnesota food-or-ag-business owner weighing strategic versus PE, an ESOP-curious owner navigating MN's 9.8% corporate franchise tax plus the December 31 2025 PTET expiration, or a PE deal partner sourcing Mpls-orbit medtech and industrial assets. The six proprietary frames (Medical Alley Anchor Effect, Medtronic/Boston Scientific Bolt-On Premium, UnitedHealth/Optum Vertical Vortex, AgTech and F&B Strategic Density, Twin Cities Public-Co M&A Workshop, Piper Sandler / Lazard MM / Goldsmith Agio Helms Alumni Network) come from cross-referencing the 2024-2026 deal record with the Twin Cities' structural specifics.

What's the Twin Cities-metro M&A advisor landscape for $5M-$300M deals in 2026?

The 14-firm Minneapolis-metro shortlist for 2026, sorted by deal-size band:

| Firm | Founded | HQ / Mpls office | Sweet spot | Specialty |

|---|---|---|---|---|

| Piper Sandler | 1895 | Minneapolis HQ (downtown) | $50M-$2B+ EV | Public; 145 IB pros; healthcare, financial services, energy, technology, consumer |

| BMO Capital Markets (GHF legacy) | 1995 (GHF); BMO acq Aug 1 2016 | Minneapolis bench | $100M-$1B+ EV | Diversified middle market; absorbed ~30 GHF bankers into BMO US M&A |

| Craig-Hallum Capital Group | 1997 | Minneapolis | $50M-$500M EV | 100% employee-owned boutique; growth-stage tech, healthcare, consumer |

| Hennepin Partners | April 2018 | Minneapolis | Under $250M EV | Lower-middle-market; Lazard MM / Quetico / Craig-Hallum alumni; $20B+ aggregate |

| Cherry Tree & Associates | 1980 (PE/VC); 1996 (IB) | Minneapolis | $20M-$300M EV | Christianson/Stofer legacy; sell-side + buy-side + recap |

| Northland Securities | September 2002 | Minneapolis | $50M-$500M EV | Full-service IB, ~170 employees; First National of Nebraska parent since May 2023 |

| Aethlon Capital | 1996 | 1786 James Ave S, Mpls | $20M-$200M rev | Sima Griffith-led; one of few woman-owned IBs nationally; $750M+ M&A track record |

| Madeira Partners | 1998 | Minneapolis | $25M-$300M EV | Closely-held / family-owned specialty; 6-partner boutique |

| Quazar | 1990 | 505 Hwy 169 Ste 595, Mpls | $5M-$100M rev | Manufacturing, distribution, services, tech, consumer; 100+ transactions |

| Bayview Capital Group | 1995 | Wayzata MN | $10M-$150M rev | Services + manufacturing; 80+ sell-side and 20 buy-side over 20 years |

| Vermillion Capital | 2015 | Minneapolis | $20M-$150M EV | F&B + industrial specialist; 30+ transactions on own site; 100+ combined legacy |

| True North M&A | September 2021 (Sunbelt spinout) | Minneapolis | $10M-$150M rev | Founder/family-led; #1 firm in US per IBBA & M&A Source; Sunbelt 25-yr heritage |

| SealedBid Marketing | 1993 | 7900 International Dr Ste 800, Bloomington | $2M-$50M EV | Lower-MM sell-side and buy-side intermediary; 50+ years combined experience |

| BlackTorch Capital | 2009 | Excelsior MN (metro) | Middle market | M&A-focused boutique; senior-banker model; ~12 closed transactions per Axial |

Three additional firms worth mentioning for ecosystem context (not pure investment banks but frequent transaction participants): Norwest Equity Partners (Mpls-HQ PE, founded 1961, $2.7B+ AUM, closed NEP XI at $1.0B and Norwest Mezzanine V at $400M in July 2024); Castlelake L.P. (Mpls founded 2005, ~$25B AUM as of March 2025, aviation + specialty finance focus, fifth aviation fund closed $2B+ March 2025); Goldner Hawn Johnson & Morrison (Mpls PE long-tenured). And Faegre Drinker, Dorsey & Whitney, Fredrikson & Byron, and Stinson round out the Mpls M&A law firm anchor set. Optional alternates worth flagging if a primary firm declines coverage: Krahn Capital Group (founded 2016, Stuart Krahn lower-middle-market generalist) and Oak Ridge Financial (Mpls).

Who are the 14 firms — profiles, lineage, and where each one wins?

Piper Sandler (downtown Minneapolis HQ, founded 1895). The public bank with the most name recognition in the Twin Cities and the only Mpls-anchored firm with full bulge-bracket-equivalent capability in healthcare, financial services, energy, technology, and consumer. 145 IB professionals across US, Europe, and Asia per the firm's own published materials. Ranked #2 in US M&A under $2B per its own league-table tracking. J.P. Peltier appointed global co-head of investment banking January 2026 — a signal that Mpls remains the strategic center of gravity for the firm. The healthcare desk is the single most important advisor relationship for any Twin Cities medtech founder; the financial services desk runs most public-co bank M&A in the Midwest; the technology desk co-led growth-equity capital raises for Rocket Lab, Mayville Engineering, and Velo3D in 2024-2025. Sweet spot: $50M-$2B+ EV.

BMO Capital Markets (Minneapolis bench, GHF legacy since August 2016). The diversified middle-market specialist for the Twin Cities. Greene Holcomb Fisher — founded 1995 by Hunt Greene and Brian Holcomb — was acquired by BMO on August 1 2016 and approximately 30 GHF bankers were absorbed into BMO US M&A. The Mpls bench covers $100M-$1B+ EV across consumer, industrial, healthcare, and business services with parent-firm capital markets and lending integration. For founders whose default-buyer pool requires both strategic sell-side coverage plus capital structure advice, BMO's combined IB + capital-markets staffing is hard to substitute. Sweet spot: $100M-$1B+ EV.

Craig-Hallum Capital Group (Minneapolis, founded 1997). A 100% employee-owned boutique with offices in Minneapolis, Chicago, Boston, Philadelphia, San Francisco, and Greenwich, CT. The growth-stage tech / healthcare / consumer specialist for the Twin Cities — uniquely positioned for high-growth pre-IPO and post-IPO companies that grew through Twin Cities public-co distribution. Recent capital-raise transactions across Rocket Lab, Mayville Engineering, Ichor, and Velo3D per the firm's own materials May 2026. Employee ownership produces senior-banker accountability comparable to Hennepin Partners' senior-MD model. Sweet spot: $50M-$500M EV.

Hennepin Partners (Minneapolis, launched April 2018). The cleanest carrier of the Lazard MM / Quetico / Craig-Hallum M&A lineage. Founded by Matt Fitzmaurice, Kevin Janicki, Jared Rance, and Chad Starman — team has executed deals aggregating more than $20B per BusinessWire and the firm's own materials. Pure lower-middle-market under $250M EV with senior-MD-led process management. The right boutique pick for sellers who want Lazard MM-quality senior bankers at boutique-tier fees. Strongest in medtech, healthcare services, and broader closely-held businesses. Sweet spot: under $250M EV.

Cherry Tree & Associates (Minneapolis, PE/VC founded 1980; IB founded 1996). The Christianson/Stofer legacy boutique — Tony Christianson and Gordon Stofer have been 50/50 partners since founding. Tony's 40-plus-year M&A veteran leadership covers sell-side, buy-side, and recapitalization. ESOP transition expertise is one of the deepest in the Twin Cities. Cross-industry coverage across $20M-$300M EV with a slight specialty bent toward F&B, manufacturing, and consumer. The right pick for closely-held businesses considering ESOP versus full sale. Sweet spot: $20M-$300M EV.

Northland Securities (Minneapolis, founded September 2002). Full-service investment bank with approximately 170 employees and a broader product set than most pure-play boutiques (capital markets, fixed income, sales/trading in addition to M&A advisory). Acquired by First National of Nebraska in May 2023, which added capital backing and lending integration. Recent M&A includes advisory on Bel Fuse's acquisition of dataMate (buy-side). The right pick for sellers who want a platform-style firm with Mpls anchoring and broader product capability. Sweet spot: $50M-$500M EV.

Aethlon Capital (Minneapolis, 1786 James Avenue South, founded 1996). One of the few woman-owned, woman-led investment banks nationally. Managing Principal and co-founder Sima Griffith has led the firm for nearly 30 years with $750M-plus in aggregate M&A transactions. Cross-industry coverage at $20M-$200M revenue. Recognized in Twin Cities Business' Notable Women in Finance 2024. For founders prioritizing a diverse advisor team or seeking ESOP transition coverage with senior-MD continuity, Aethlon is the clearest fit. Sweet spot: $20M-$200M revenue.

Madeira Partners (Minneapolis, founded 1998). A 6-person boutique with 4 partners — the smallest senior-partner-to-deal ratio in the Twin Cities. Closely-held and family-owned company specialty at $25M-$300M EV. Recent transactions include the Consolidated Container sale to Mauser Packaging. The right pick for closely-held businesses where the founder wants senior-partner attention for every conversation, with the structural tradeoff that Madeira's small team caps deal volume. Sweet spot: $25M-$300M EV.

Quazar (Minneapolis, 505 Highway 169 Suite 595, ZIP 55441, founded 1990). The longest-tenured Twin Cities lower-middle-market specialist. 100-plus closed transactions across manufacturing, distribution, services, tech, and consumer. $5M-$100M revenue sweet spot — exactly the band where founder-led businesses graduate beyond traditional business broker coverage but before mid-market boutique pricing kicks in. The founder is in memoriam (deceased); the firm continues operating with senior team. Sweet spot: $5M-$100M revenue.

Bayview Capital Group (Wayzata MN, founded 1995). A western-suburbs boutique with services and manufacturing focus. 80-plus sell-side and 20 buy-side transactions over 20 years. $10M-$150M revenue sweet spot. Tracxn shows 29 lifetime deals with the last named transaction in April 2023 — the deal cadence has slowed in recent years, but the team retains broad senior-banker capability for Twin Cities founders. Sweet spot: $10M-$150M revenue.

Vermillion Capital (Minneapolis, founded 2015). The local food and beverage plus industrial specialist. Partner Robert Briese; 30-plus transactions on the firm's own site with 100-plus combined-team total per legacy. Vermillion is the boutique that pitches Cargill, General Mills, Land O'Lakes, and Hormel regularly — making it the right fit for F&B and animal-nutrition mandates at $20M-$150M EV where Cargill or General Mills strategic relationships matter. Sweet spot: $20M-$150M EV.

True North M&A (Minneapolis, September 2021 spinout from Sunbelt Business Advisors). Ranked #1 firm in the US per IBBA and M&A Source recognition. $10M-$150M revenue sweet spot — exactly the gap between traditional business broker coverage (sub-$5M typically) and mid-market boutique floors ($100M+). For $20M-$80M revenue founders, True North is often the right pricing fit. Approximately 25 years of combined heritage via the Sunbelt platform. Founder/family-led businesses are the core target. Sweet spot: $10M-$150M revenue.

SealedBid Marketing (Bloomington MN, 7900 International Drive Suite 800, ZIP 55425, founded 1993). The longest-tenured Twin Cities lower-middle-market intermediary on the small end of the spectrum. Sell-side and buy-side coverage at $2M-$50M EV. Joe Wallace joined November 2025, deepening the senior-banker bench. 50-plus years combined team experience. For traditional founder-led sales below $20M EV, SealedBid covers the band where pure business-broker firms compete. Sweet spot: $2M-$50M EV.

BlackTorch Capital (Excelsior MN greater metro, founded 2009). An M&A-focused boutique with a senior-banker model and approximately 12 closed transactions per Axial listing. Smaller deal volume than the established lower-MM firms, but the senior-banker model produces high attention per mandate. The right pick for founders who want Mpls-area coverage outside the downtown / Wayzata corridor. Sweet spot: middle market generalist.

For founders evaluating across this 14-firm list, the structural read is that Twin Cities advisor depth is concentrated in the middle of the spectrum. The Piper Sandler / BMO / Craig-Hallum / Northland platform tier and the Hennepin / Cherry Tree / Aethlon / Madeira / Vermillion senior-MD boutique tier cover the $20M-$500M EV band with multiple credible firms per sub-vertical. The lower end ($5M-$20M EV) is covered by Quazar / Bayview / True North / SealedBid / BlackTorch but with thinner senior-MD attention. Above $500M EV, only Piper Sandler can lead alone — the rest require a co-advisor pattern or yield to bulge-bracket coverage.

How does Medical Alley change a medtech founder's buyer pool and advisor selection?

The Medical Alley cluster effect is the single most important structural fact in Twin Cities M&A. Medical Alley Association documents approximately 800 healthcare organizations employing 500,000 Minnesotans, 530-plus medical-device companies, and 900 pharma/biotech R&D companies — with 95% of Minnesota's medical-device ecosystem within a 50-kilometer radius of downtown Minneapolis. The foreign-anchor expansion continues: Philips opened expanded R&D and manufacturing in April 2025; Trelleborg expanded its Medical Solutions Innovation Center in 2025.

The structural read for medtech founders: if you are a $20M-$80M revenue Twin Cities medtech business, your default buyer pool is Medtronic + Boston Scientific + Stryker + Abbott — three of which sit within 20-50 miles. That is a fundamentally different process than New York or LA or Boston or San Diego. In LA or SF a medtech sale runs an 8-12 strategic + 10-15 PE platform process over 9-14 months; in Minneapolis the same business can run a tighter 4-6 strategic + 6-10 PE platform process over 7-10 months because the named strategics are pre-existing customers, suppliers, or co-promotion partners.

The 2024-2026 medtech deal record validates the pattern:

- Medtronic-CathWorks closed April 20 2026 at $585M (incl. earnouts); intent announced February 3 2026; FTC-cleared. The structural anchor: Medtronic exercised an option from the 2022 strategic partnership and co-promotion of FFRangio non-invasive coronary assessment. The 2022 partnership built the integration runway — 3.5 years of joint commercial activity before the option exercise. The premium reflected reduced integration risk.

- Medtronic-Affera closed August 30 2022 at $925M, with FDA approval for Affera + Sphere-9 in November 2024 — a 2+ year integration runway after close.

- Boston Scientific-Penumbra announced January 15 2026 at $14.5B EV ($374/share, cash + stock). BSX is Marlborough MA HQ but the cardiac unit operates substantially in the Mpls metro. The Penumbra deal scales cardiovascular thrombectomy plus neurovascular.

- Boston Scientific-Cortex (atrial fibrillation mapping) announced November 4 2024 (closed H1 2025).

- Boston Scientific-Bolt Medical (intravascular lithotripsy) closed Q1 2025.

- Resonetics-Resolution Medical (Fridley MN, medtech contract manufacturing, formerly Arcline portfolio) closed March 23 2026. Resonetics is Nashua NH-HQ; the buy was for proximity-to-customer (Medtronic, Boston Scientific cardiac) and neuromodulation engineering talent that is impossible to recruit at scale outside Medical Alley.

- Boston Scientific-M.I.Tech + Relievant Medsystems approximately $850M combined.

The advisor pattern for Twin Cities medtech founders at $20M-$300M EV:

- Piper Sandler has the deepest healthcare team in the Mpls market with national-platform reach. I would not run a Twin Cities medtech sell-side process without Piper Sandler on the screen, even if you ultimately pick a boutique to lead.

- Cherry Tree & Associates covers medtech with senior-MD attention at the $50M-$200M EV band; Christianson's 40-plus-year MD experience is a real edge on Medtronic-bolt-on processes.

- Hennepin Partners covers medtech and broader healthcare at the sub-$250M EV band with Lazard MM-trained senior bankers.

- Craig-Hallum Capital Group has a healthcare practice with recent capital-raise transactions across Rocket Lab, Mayville Engineering, Ichor, and Velo3D (broader tech-adjacent but illustrates the senior-banker bench).

- Madeira Partners covers closely-held medtech mandates with senior-partner attention at the $25M-$300M EV band.

Advisor selection should test three questions: (1) Can the firm reach the Medtronic / Boston Scientific / Stryker / Abbott / 3M-Solventum corp-dev teams in less than 3 weeks of engagement? (2) Does the firm have a Heritage Group / Frazier Healthcare / Linden Capital / Welsh Carson PE-relationship that translates into a same-day buyer-list update? (3) Does the firm have any current Mpls-strategic engagement that could create conflict on your asset?

What's the Medtronic / Boston Scientific Bolt-On Premium and how do sellers position for it?

When the buyer is Medtronic, Boston Scientific, or Abbott cardiac, sellers can expect 30-50% premium above the asset's standalone DCF — because the buyer can plug a sub-$1B cardiac diagnostic / ablation / mapping / structural-heart technology directly into a billion-dollar distribution stack. Strategics will pay 5-7x revenue or higher for cardiac IP, versus roughly 3-4x for non-cardiac diagnostics. The pattern repeats: 6-18 month strategic partnership or co-promotion agreement (Medtronic-CathWorks since 2022, FDA-approved FFRangio jointly promoted), followed by option exercise.

The verified premium-paying deal record:

- Medtronic-CathWorks $585M closed April 20 2026 (intent February 3 2026) — exercised after 2022 strategic partnership and co-promotion of FFRangio. Pre-built integration, reduced integration risk, premium paid.

- Medtronic-Affera $925M closed August 30 2022 — cardiac mapping plus ablation; full FDA approval November 2024 (2+ year integration runway).

- Boston Scientific-Penumbra $14.5B announced January 15 2026 — cardiovascular thrombectomy plus neurovascular at $374/share.

- Boston Scientific-Cortex Inc announced November 4 2024 (closed H1 2025) — atrial fibrillation mapping.

- Boston Scientific-Bolt Medical Q1 2025 — intravascular lithotripsy.

- Boston Scientific-M.I.Tech + Relievant Medsystems ~$850M combined.

The seller tactic that compounds the premium: land a co-promotion or strategic distribution agreement with the target acquirer 18-36 months before the sale process launches. The co-promotion does three things: (1) signals to the target's clinical and commercial teams that the seller's technology is real and integrated into their workflow; (2) reduces the buyer's perceived integration risk; (3) creates an option that the target can exercise without competitive bidding pressure if the seller chooses to sell early to the strategic partner. The CathWorks-Medtronic 2022 partnership was the textbook example. The same playbook applies for Boston Scientific cardiac and Stryker neurovascular.

For founders without a pre-existing strategic-partnership: the next-best lever is publishing real clinical or commercial validation data in venues where Medtronic / Boston Scientific / Stryker / Abbott corp-dev teams already read. Industry conferences, peer-reviewed clinical studies, and reimbursement-coded outcomes are the inputs that lift sale multiples from the diagnostic-tier (3-4x revenue) to the cardiac-tier (5-7x+).

The advisor question for founders pursuing this playbook: which Mpls boutique has run more than three Medtronic / Boston Scientific / Stryker / Abbott processes in the last 36 months, and can reference at least two closed transactions with these strategics? Piper Sandler's healthcare team in Mpls has the longest such track record. Cherry Tree, Hennepin Partners, and Craig-Hallum have selected senior bankers with this background — and the lineage test (where did your founders work before launching?) is the way to verify it.

Why does UnitedHealth/Optum's Q3 2025 strategic pause change Twin Cities healthcare advisor selection?

UnitedHealth Group is the largest employer of physicians in the US — by late 2024, approximately 1 in 10 US physicians sat under Optum control. Optum's M&A activity historically concentrated in four sub-segments:

- Primary care and specialty practices — multispecialty platforms acquired across multiple states.

- Ambulatory surgical centers — Optum/SCA Health reported 423 ASCs by late 2024, 370-plus specialty clinical locations plus 400-plus physician practice clinics plus approximately 9,700 physicians.

- Home health and hospice — Optum acquired LHC Group for $5.4B (2023 close) and Amedisys for $3.3B (closed August 14 2025 after DOJ-mandated divestiture of 164 home-health and hospice facilities across 19 states).

- Data analytics and revenue-cycle — Optum Insight has acquired multiple specialty platforms across the decade.

That was the default-buyer thesis for any Twin Cities seller in these sub-segments. The Q3 2025 inflection: UnitedHealth publicly announced a strategic acquisition pause plus a buyback pause to focus on debt reduction, targeting approximately 40% debt-to-capital. The Pennant Group acquisition of the $146.5M Amedisys-divested home-health and hospice package is the cleanest 2025 data point: divested assets cleared at the floor of the typical range, suggesting buyer scarcity in segments where Optum was the price-anchor.

The 2026 advisor selection question for Twin Cities healthcare-services sellers: which firms have the deepest non-Optum buyer Rolodex? The 2026 default-buyer mapping for Twin Cities healthcare-services exits requires Elevance Health (Indianapolis HQ), CVS Health Caremark/Aetna (Woonsocket RI HQ), Centene (St. Louis HQ), and the PE-backed health-services platforms — Heritage Group (Nashville), Frazier Healthcare Partners (Seattle), Linden Capital Partners (Chicago), Welsh Carson Anderson & Stowe (NYC), Webster Capital Healthcare (Waltham MA), Sheridan Capital Partners (Chicago), Ridgemont Equity Partners (Charlotte). Piper Sandler's healthcare services team — sitting downtown Mpls — has the deepest non-Optum payer-services and provider-services Rolodex of any single firm in the Mpls market.

The advisor selection should test (1) which firms have run more than 3 non-UNH-buyer processes in the last 24 months; (2) which firms can replace the Optum buy-side dialog with a competitive 8-12 named buyer process; (3) which firms have completed at least one Elevance, CVS, or Centene transaction in the last 36 months. The boutique layer (Hennepin Partners, Cherry Tree, Aethlon Capital) covers healthcare services with senior-MD attention but without Piper's national bandwidth. For deals above $100M EV where UNH would have been the natural lead bidder, the advisor mandate now requires a deliberately broader process — and a stronger second-bidder cultivation strategy from day one.

The counter-intuitive read: UNH's pause is bullish for non-Mpls health-services acquirers. Elevance, CVS, Centene, and the PE-platform layer pick up the deal flow Optum would have absorbed. Mpls advisors with non-UNH Rolodexes win share. This is a temporary structural shift — likely 2026-2027 — and worth optimizing the advisor pitch around.

How does the AgTech and Food/Bev Strategic Density frame change F&B advisor selection?

Twin Cities is the only US metro with four Fortune 500-class food and ag anchors within roughly 30 miles: Cargill (Wayzata), General Mills (Golden Valley), Land O'Lakes (Arden Hills), and Hormel Foods (Austin MN, ~100 miles south). Schwan's Company adds a private-equity-backed branded-food anchor. The cluster anchors most US strategic-buyer activity in branded packaged food, pet nutrition, animal feed, ingredient supply, and value-added dairy.

The 2024-2025 anchor deal record:

- General Mills-Edgard & Cooper (premium European pet food): $434M net of cash, FY24.

- General Mills-Whitebridge Pet Brands (North American premium pet food): Q3 FY25.

- General Mills-North American Yogurt divestiture → Lactalis and Sodiaal: aggregate $2.1B announced September 2024, closing calendar 2025.

- Cargill-Infinity Meat Solutions case-ready plants (RI + PA): February 2024.

- Cargill-Compana Pet Brands feed mills (Denver + Kansas City): closed September 3 2024.

- Cargill-Mig-Plus (Brazil animal nutrition): 2025 binding offer.

- Cargill-Teys Beef Ventures (US + Australia): full ownership closed November 6 2025 (announced June 5 2025).

- Land O'Lakes-Kozy Shack (chilled dairy desserts): closed July 31 2024.

- Land O'Lakes-Cocoa Classics divestiture → Precision Foods: December 2025 (Mirus Capital advised).

- Hormel-whole-bird turkey divestiture → Life-Science Innovations: February 2026 (commodity exit toward branded-products focus).

The counter-intuitive read: Cargill is the most active Twin Cities F&B buyer no one talks about. Public M&A coverage focuses on General Mills and Hormel because they file public 8-Ks. Cargill — the largest privately-held US company by revenue — ran 4+ verified closes across 2024-2025, outpacing the General Mills/Hormel cadence by 3-4x. The Mpls advisors who pitch Cargill regularly outperform on F&B mandates because Cargill is a frequent strategic acquirer with a stable corp-dev team and well-defined sub-vertical priorities (animal nutrition, pet food, branded ingredients, alternative proteins, sustainability/ESG-positioned ingredients).

The Twin Cities F&B advisor pattern:

- Vermillion Capital (founded 2015, Partner Robert Briese, food and beverage and industrial specialist, 30-plus transactions on own site plus 100-plus combined-team total per legacy) is the local specialist boutique for $20M-$150M EV F&B and animal-nutrition mandates. Sub-vertical depth and known relationships with Cargill, General Mills, and Land O'Lakes corp-dev.

- Cherry Tree & Associates covers F&B at the $20M-$300M EV band with senior-MD attention; Christianson's bench includes consumer and food retail expertise.

- Hennepin Partners covers F&B and broader consumer-goods at sub-$250M EV.

- True North M&A covers $10M-$150M revenue founder/family-held F&B businesses — the right pricing fit between a regional business broker (sub-$5M typically) and mid-market boutique ($100M+ floor).

- Quazar covers manufacturing, distribution, services, tech, and consumer at the $5M-$100M revenue band; many F&B sub-mandates fit here.

- Piper Sandler runs the $100M-$500M+ F&B mandates where national strategic-buyer outreach (Mondelez, Kraft Heinz, JM Smucker, Conagra, etc.) is required beyond the Twin Cities-anchored buyer pool.

For founders pursuing a Cargill-anchored sale, the structural sequence: (1) cultivate a pre-existing supplier or co-promotion relationship with Cargill 12-24 months before LOI; (2) sit through Cargill's corp-dev process which is slower and more thorough than General Mills' (Cargill private-co diligence runs 4-6 months from indication of interest to close versus General Mills' 3-4 months); (3) work with an advisor who has done at least one Cargill transaction in the last 36 months and can manage Cargill's specific information-request cadence. The same advisor pattern applies for General Mills, Land O'Lakes, and Hormel — but Cargill is the highest-volume, lowest-coverage strategic.

What's the Twin Cities Public-Co M&A Workshop and how does it shape advisor experience?

Minnesota hosts 17 Fortune 500 HQs as of 2025, including 3M, General Mills, Target, UnitedHealth Group (ranked #3 on F500), U.S. Bancorp, Best Buy, Polaris, Ecolab, Fastenal, Hormel Foods, Solventum (NEW from 3M spinoff April 2024), Securian Financial, plus five more per the startribune.com and Fortress Financial Group tallies. Per population, MSP ranks #3 in headquarters per million among all US metros (behind Bridgeport CT and San Jose CA). And because both Bridgeport and San Jose are sub-elements of larger NYC and SF metro regions, MSP is the highest-concentration standalone metro for Fortune-class HQs nationally.

That F500 density does two things for Mpls M&A advisors:

- It creates a steady flow of public-co M&A activity — divestitures, bolt-on acquisitions, sponsor sales, spin-offs — that feeds local advisor experience. Piper Sandler's healthcare team (145 IB pros) sits inside Mpls because the deal flow lives here. UnitedHealth, Solventum, Medtronic, 3M, Ecolab, Polaris, and their suppliers all originate transactions.

- It produces a tradeable supplier ecosystem — companies that grew through Twin Cities public-company distribution channels and now have a default-buyer pool of Mpls-headquartered strategics.

The 2024-2026 public-co deal cadence demonstrates the workshop effect:

- Patterson Companies-Patient Square Capital (dental + animal health distribution): $4.1B all-cash at $31.35/share, closed April 17 2025. Patterson HQ St. Paul, Minnesota (1031 Mendota Heights Rd). This is the underrated 2025 anchor — healthcare-services M&A coverage often skips it because it was PE-to-dental/animal-health rather than a traditional strategic acquisition.

- Ecolab-CoolIT Systems (AI data center liquid cooling): $4.75B announced March 20 2026; expected close Q3 2026. CoolIT sales approximately $550M LTM. Prior owners KKR + Mubadala paid only $270M in June 2023 — a 17.6x markup in 2.75 years. This is the AI infrastructure deal of the decade for Mpls and signals how aggressively Twin Cities public-cos are willing to overpay for AI infrastructure positioning.

- IonQ-SkyWater Technology (quantum computing + chip fabrication): approximately $1.8B equity announced January 2026, representing 38% premium to 30-day VWAP at $35/share ($15 cash + $20 IonQ stock). Close expected Q2 or Q3 2026.

- Toro Company-Tornado Infrastructure Equipment (hydrovac excavation): CAD $279M closed December 8 2025. Tornado HQ Calgary; supplements Toro's Ditch Witch division; expected to add approximately 2% to Toro net sales.

- CohnReznick-Smith Schafer (accounting; CR entry into MN): announced January 5 2026, effective January 1 2026. Smith Schafer = 12 partners + 89 employees; 3 MN offices Minneapolis, Rochester, Red Wing; rebranded under CR name.

- Hormel Foods-whole-bird turkey divestiture → Life-Science Innovations: announced February 2026 (commodity exit).

The Twin Cities supplier-exit advisor pattern at $20M-$200M EV:

- Piper Sandler covers most public-company supplier sales given 145-pro IB platform and Mpls anchoring. Public-co M&A teams across UnitedHealth, Solventum, Medtronic, 3M, Ecolab, and Polaris all know Piper bankers personally — and that translates into faster corp-dev engagement at the seller-side.

- Craig-Hallum Capital Group is uniquely positioned for tech, healthcare, and consumer suppliers that grew through Twin Cities public-co distribution. The 100% employee-owned model produces high senior-banker accountability.

- BMO Capital Markets (Greene Holcomb Fisher Mpls bench, acquired August 1 2016, approximately 30 GHF bankers absorbed into BMO US M&A) covers diversified middle-market industrial and consumer supplier mandates at $100M-$1B+ EV.

- Cherry Tree, Hennepin Partners, Northland Securities cover non-medtech industrial and consumer manufacturing suppliers at the $20M-$150M EV band.

For sellers whose default buyer is an MN-headquartered Fortune 500, advisor selection should test whether the firm has completed at least two transactions with the named strategic in the last 36 months — and whether the senior banker has a documented relationship with that strategic's corp-dev head. The Ecolab-CoolIT deal is also a useful data point for AI-infrastructure-positioned sellers: Twin Cities public-cos are repeat buyers for AI data-center cooling, networking, and adjacent infrastructure, and 17.6x markups are achievable when the strategic story is right.

What's the Piper Sandler / Lazard MM / Goldsmith Agio Helms Alumni Network and why does it matter?

Two generations of Twin Cities M&A talent originated from two firms: Piper Sandler (founded 1895, public bank, Minneapolis HQ) and Goldsmith Agio Helms (founded 1978, acquired by Lazard in 2007, rebranded Lazard Middle Market). Lazard MM executed approximately 1,490 lifetime deals before ceasing operations per FINRA BrokerCheck. The 30-plus MDs and senior bankers from Lazard MM redistributed across the Mpls boutique market — and the result is a deep senior-banker bench across Hennepin Partners, Cherry Tree, Aethlon Capital, Madeira Partners, and the BMO Capital Markets US M&A bench (where the Greene Holcomb Fisher absorption added another generation of bankers).

The lineage tree:

- Hennepin Partners (April 2018) founders Matt Fitzmaurice, Kevin Janicki, Jared Rance, and Chad Starman — Craig-Hallum M&A + Quetico Partners alumni. Quetico itself traced Lazard MM lineage. Team has executed deals aggregating more than $20B.

- Quetico Partners — Lazard MM legacy team.

- Greene Holcomb Fisher (1995-2016) — founded by Hunt Greene and Brian Holcomb; approximately 30 bankers absorbed into BMO Capital Markets US M&A on August 1 2016. The Mpls bench has grown since then (specific post-2016 headcount not publicly disclosed).

- Lazard Middle Market (Goldsmith Agio Helms originally) — 1,490 deals over operating period before ceasing.

The counter-intuitive read: Lazard MM's closure is bullish for sellers, not bearish. Conventional wisdom says losing a brand-name shop hurts the local market. Reality: the 30-plus MDs redistributed with senior-banker accountability actually rising. Boutique-firm bankers carry skin in the game — equity stakes, partner profits, signature on every retainer letter — in ways that bulge-bracket and Lazard-platform MDs don't. Sellers get the same Lazard-trained talent at lower fees and with sharper accountability.

The lineage test I use when evaluating a Twin Cities boutique pitch: ask the firm where its founders worked before launching. If the answer involves Piper Sandler, Goldsmith Agio Helms, Lazard MM, Quetico, Greene Holcomb Fisher, or Craig-Hallum M&A — you are looking at the credentialed Mpls senior-banker tree. If the answer is none of the above, scrutinize the senior-MD bench more carefully. The "Goldsmith Agio Helms → Lazard MM" lineage matters more than the Piper Sandler brand for the boutique layer. Piper is the public bank with the most name recognition. But the bench of senior bankers across Hennepin, Cherry Tree, Aethlon, BMO/GHF, and Madeira actually descends from the Goldsmith Agio Helms (1978) tree as much as the Piper one. The Lazard MM alumni network is a real and active commercial asset.

For sellers, this matters because it changes the cost-quality tradeoff. The mid-market sweet spot ($25M-$200M EV) in Mpls can be staffed with senior MDs trained at Lazard MM-quality processes for boutique-tier fees. Compare to most other US metros where the same senior bench would only sit at platform IBs charging 25-50% higher blended fees.

What does Minnesota's tax structure mean for sellers — and how does the December 31 2025 PTET expiration change 2026 deal planning?

Minnesota's corporate franchise tax is a flat 9.8% — among the higher state rates nationally, roughly double Florida (5.5%) or North Carolina (6.5%), and triple Texas (0%). Individual MN rates run up to 9.85%. The Pass-Through Entity Tax (PTET) — which let owners of S-corps and partnerships work around the $10,000 federal SALT cap — expired for tax years beginning after December 31 2025 per Minnesota Department of Revenue guidance. Translation: deals that closed under PTET grandfathered into 2025 are fine; new 2026+ deals require new structuring.

For closely-held businesses, the practical effect is that the federal-SALT-deduction efficiency MN owners enjoyed for 2020-2025 is gone, and the headline state tax burden bites harder on the seller's net proceeds. The structural responses that gain ground in 2026:

- Stock sales over asset sales. Asset sales create blended capital gains plus ordinary income (depreciation recapture, accounts-receivable income, etc.) which compounds against the 9.8% rate. Stock sales generally produce cleaner long-term capital gains treatment for selling shareholders.

- ESOP exits. S-corps owned by ESOPs are generally tax-exempt at the ESOP-shareholder layer. C-corp owners selling to an ESOP can use the IRC §1042 rollover to defer all capital gains tax indefinitely (with qualified replacement property requirements). The ESOP path stacks employee retention on top of tax deferral. Note: the BIG (Built-in Gains) tax applies during the 5-year recognition period after S-election from C-corp — which is the structural blocker for owners who recently converted.

- Pre-sale gifting plus dynasty trusts. Minnesota's 2025 trust modernization act made MN more domicile-friendly for irrevocable trusts. GRATs plus dynasty trusts are common for founders pre-positioning equity 12-24 months before LOI signing.

Mpls boutiques that market ESOP transition expertise: Cherry Tree & Associates (Tony Christianson's 40-plus-year MD experience leading these), Hennepin Partners (Lazard MM-trained senior bankers covering closely-held), Aethlon Capital (Sima Griffith's woman-led senior-partner model). Cherry Tree has been the most active Mpls IB on ESOP transactions historically.

For founders considering relocation to a no-state-income-tax jurisdiction (TN, TX, FL, WY) — that is a 24-36 month effort with significant residency clawback risk if rushed. Most state revenue departments scrutinize relocations during the 24 months before a liquidity event, and clean residency documentation matters. The M&A advisor selection should follow the structural tax sequence rather than drive it. Most Mpls boutiques will coordinate with CLA (CliftonLarsonAllen), Wipfli, Baker Tilly, Eide Bailly, or BDO Mpls on the tax structuring layer.

What's a reasonable success fee at $50M Mpls mid-market mandates and how do fee structures vary?

Twin Cities M&A advisors at the $50M EV mid-market band typically charge 1.5% to 2.5% blended success fee plus a $50,000 to $150,000 retainer credited against the success fee at close, with a tail period of 12 to 24 months standard. The standard Lehman scale (5/4/3/2/1) on a $50M deal produces approximately $700,000 of success fees — about 1.4% blended — which is the floor for most Mpls boutiques.

Specialty firms with deeper sub-vertical buyer relationships sometimes negotiate modified-Lehman alternatives: 1.75% to 2.25% flat success fee, or a tiered structure with a higher first-tier percentage and a flat tail above $20M. Platform firms (Piper Sandler, BMO Capital Markets, Craig-Hallum, Northland Securities) typically run standard Lehman with a higher retainer floor ($75,000-$200,000) given parent-firm cost structures.

For medtech mandates where senior-MD attention plus Medtronic/Boston Scientific/Stryker/Abbott engagement matters (Piper Sandler healthcare, Hennepin Partners, Cherry Tree, Craig-Hallum's healthcare desk), expect 2.0% to 2.75% blended at the $50M-$200M EV band given the heavier senior-banker time allocation and the longer process duration (typical medtech sell-side runs 8-13 months versus 6-9 months for generalist mid-market because FDA-cleared product lifecycles and regulatory consents extend the diligence window). For complex multi-stakeholder medtech and value-based-care platforms — physician-owned, provider-payer hybrid, FDA Class III device — expect 2.5% to 3.5% blended given the multi-party coordination work.

Aethlon Capital's deal book shows roughly that pricing structure for the woman-owned woman-led $750M-plus aggregate M&A track record. For F&B mandates: Vermillion Capital's $20M-$150M F&B sell-sides typically run at standard Lehman with a slight premium for sector specialization, plus a tail covering Cargill/General Mills/Land O'Lakes/Hormel-adjacent strategic introductions. True North M&A's lower-MM founder-led mandates run closer to 3-5% blended on the $5M-$30M revenue band given the higher absolute deal count required to sustain a senior-banker model.

For sub-$5M EV deals, the math shifts: business broker fees (Sunbelt Business Advisors, Murphy Business) run 8-12% blended because the deal-size doesn't support a senior-banker model. True North M&A and SealedBid Marketing bridge the gap between business broker and mid-market boutique, with fees typically running 5-8% blended at the $2M-$10M EV band, dropping toward standard Lehman as deal size increases.

Peony Data Room at $52 per admin per month — unlimited rooms and storage — replaces the $15,000-$50,000 per-deal data room cost that legacy VDR providers (Datasite, Intralinks, Ansarada) typically bill as expense reimbursement. For Twin Cities advisors running 8-15 mandates per year, the aggregated data-room expense often exceeds $200,000 — Peony's flat-rate pricing converts that into a fixed multi-deal subscription. The Peony platform also supports visitor groups for concurrent-tier processes (strategics in one tier, PE in another, family-office in a third) and page-level analytics for leading-indicator signal on which buyer is actually reading the financials.

Which Mpls advisor should I hire for a sub-$10M sell-side? What about $25M-$100M and above?

Sub-$10M EV (founder-led, family-owned, ESOP recap): SealedBid Marketing (Bloomington MN, founded 1993, $2M-$50M lower-MM, 50-plus years combined team experience) is the right call for traditional founder-led sales at the lower end. True North M&A (Sunbelt spinout September 2021, ranked #1 firm in US per IBBA and M&A Source) covers the $5M-$10M revenue band with senior-banker attention. For ESOP / MBO / recapitalization specifically, Cherry Tree & Associates and Aethlon Capital have the deepest specialty.

$10M-$25M EV (lower-middle-market generalist): Quazar (founded 1990, $5M-$100M revenue, 100-plus transactions across manufacturing distribution services tech and consumer), Bayview Capital Group (Wayzata MN, $10M-$150M revenue, 80-plus sell-side and 20 buy-side over 20 years), and BlackTorch Capital (Excelsior MN, founded 2009, senior-banker model with ~12 closed transactions per Axial) cover this band with senior-banker attention. For F&B specifically: Vermillion Capital. For non-medtech healthcare services: VelocityHealth-equivalent local boutiques (Cherry Tree, Hennepin Partners) cover sub-$25M HC mandates but with senior-VP / junior-MD staffing rather than the senior-MD-led staffing that $50M+ mandates command. The fee math: the $700K-$1M Lehman-scale fee floor at this band consumes meaningful share of total transaction value (4-7%), which is the floor most boutiques will accept.

$25M-$100M EV (mid-market specialist territory): Cherry Tree & Associates, Hennepin Partners, Aethlon Capital, Madeira Partners, and Vermillion Capital (for F&B) are the strongest boutique pair. For sector-specific mandates: Northland Securities for broader industrial / consumer; Craig-Hallum for growth-stage tech / healthcare / consumer; Piper Sandler for healthcare and broader sector reach. The fee math: 2.0-2.5% blended is the typical range.

$100M-$300M EV (mid-market platform territory): Piper Sandler, BMO Capital Markets (GHF bench), and Craig-Hallum become the typical primary advisor for healthcare and tech-enabled deals at this band — all bring deep sector teams and national buyer-pool reach. Cherry Tree and Hennepin Partners co-advise on complex mandates. Northland Securities covers broader industrial / consumer at this band. For deals requiring boutique senior-MD attention plus platform reach, the typical pattern combines a Mpls-specialist boutique (Hennepin, Cherry Tree, Aethlon, Madeira) with a platform IB (Piper Sandler, BMO, Craig-Hallum) as co-advisors — boutique runs the seller-side process management, platform handles the global corp-dev outreach. The fee structure is typically split (e.g., 60/40 or 70/30 to the boutique) depending on which firm leads the process.

$300M+ EV (platform-only territory): Bulge-bracket or specialty national IBs handle this band. Piper Sandler's healthcare desk can lead Mpls-anchored deals up to roughly $1B EV. Above that, Goldman Sachs, Morgan Stanley, JPMorgan, Bank of America, Centerview, Lazard parent (separate from the now-ceased Lazard MM), Jefferies, and Citi typically lead. Mpls boutiques may participate as second advisors for regional bidder coverage but rarely lead at this band.

Honest comparison: which Mpls advisors fit which lane?

| Sub-vertical | $5M-$25M EV | $25M-$100M EV | $100M-$300M EV | $300M+ EV |

|---|---|---|---|---|

| Medtech (cardiac, neuromod, structural heart) | Hennepin + Cherry Tree + Aethlon | Cherry Tree + Hennepin + Piper | Piper + Craig-Hallum + Cherry Tree | Piper + Goldman + Morgan Stanley |

| Healthcare services (post-Optum-pause) | Hennepin + Cherry Tree + Aethlon | Cherry Tree + Hennepin + Piper | Piper + Cherry Tree + BMO | Piper + national HC IBs |

| Food & beverage / ag | Vermillion + Quazar + True North | Vermillion + Cherry Tree + Hennepin | Piper + BMO + Vermillion | Piper + national F&B IBs |

| Pet nutrition / animal feed | Vermillion + Quazar + True North | Vermillion + Cherry Tree | Piper + BMO + Vermillion | Piper + national F&B IBs |

| Industrial / manufacturing | Quazar + Bayview + BlackTorch | Cherry Tree + Northland + Hennepin | Piper + BMO + Craig-Hallum + Cherry Tree | Piper + BMO + national |

| Consumer / retail | Quazar + True North + Bayview | Cherry Tree + Hennepin + Madeira | Piper + Craig-Hallum + BMO | Piper + national consumer IBs |

| Software / tech (Twin Cities supplier base) | Craig-Hallum + Quazar | Craig-Hallum + Hennepin | Craig-Hallum + Piper + BMO | Piper + national tech IBs |

| AI infrastructure / data center | Craig-Hallum + Hennepin | Craig-Hallum + Piper | Piper + Craig-Hallum + BMO | Piper + national tech IBs |

| Specialty physician / value-based care | Hennepin + Cherry Tree | Cherry Tree + Hennepin + Piper | Piper + Cherry Tree | Piper + national HC IBs |

| Financial services | Northland + Cherry Tree | Northland + Piper | Piper + BMO + Northland | Piper + bulge FS |

| ESOP / MBO / recap | Cherry Tree + Aethlon + Hennepin | Cherry Tree + Aethlon | Cherry Tree + Piper (co-advisor) | Cherry Tree + national ESOP |

| Closely-held / family-owned | True North + Quazar + SealedBid | Madeira + Cherry Tree + Hennepin | Madeira + Cherry Tree + Piper | Piper + national closely-held |

The honest limits to flag:

- Above $500M EV — bulge-bracket capabilities matter. Piper Sandler's healthcare and select sector desks can compete at this band, but Goldman, Morgan Stanley, JPMorgan, Bank of America, and Centerview lead the largest Twin Cities-anchored deals. Datasite or Intralinks become the dominant VDR choices given pre-existing relationships with QoE providers, law firms, and R&W underwriters. Peony serves sub-$500M EV best.

- Music industry M&A — Minneapolis has limited music-IP-specialist banker capacity. Route to Nashville / LA / NY for catalog and publishing-company transactions. (Concord's $850M ABS, Sony Music Publishing Nashville-Big Yellow Dog, Pophouse's $1.3B catalog fund — all sit outside the Mpls advisor ecosystem.)

- Cross-border buyer outreach (Asian strategics, European strategics) — Mpls boutiques have selective international Rolodexes. Pair with Piper Sandler or BMO for international buyer-pool extension; or co-advise with a coastal platform.

- Cleared bankers (CFIUS / ITAR / defense exposure) — limited defense-banker capacity in Mpls. Route to coastal defense specialists (KippsDeSanto, Renaissance Strategic Advisors, Capstone Headwaters' Aerospace & Defense practice).

- Energy / oil & gas — limited specialty capacity. Route to Houston-based specialists.

Bottom line

The Twin Cities M&A advisor landscape is the densest medtech and Medical Alley cluster in the US — anchored by 95% of Minnesota's medical-device ecosystem within a 50-kilometer radius, 530-plus medical-device companies, 800-plus healthcare organizations, and the Medtronic / Boston Scientific / Stryker / Abbott / 3M / Solventum / UnitedHealth Group constellation of strategic buyers within 20-50 miles of downtown Minneapolis. Healthcare-specialist boutiques (Hennepin Partners, Cherry Tree, Aethlon Capital, Madeira Partners) cover the $5M-$300M EV band with senior-MD attention. Platform IBs (Piper Sandler, BMO Capital Markets, Craig-Hallum, Northland Securities) add national buyer-pool reach at $50M-$1B+ EV.

Beyond medtech, the food and agribusiness cluster (Cargill, General Mills, Land O'Lakes, Hormel) creates strategic-buyer competition that mid-market F&B sellers in other geographies don't enjoy. Vermillion Capital is the local specialist boutique for $20M-$150M F&B mandates. Cargill's 4+ verified close cadence across 2024-2025 is the underrated pattern most public coverage misses.

The Piper Sandler / Lazard MM / Goldsmith Agio Helms alumni network preserves a senior-banker bench that no other Midwest metro can match. The 30-plus MDs from Lazard MM redistributed across boutiques with senior-banker accountability rising. Sellers benefit from Lazard-trained senior talent at boutique-tier fees.

The Minnesota tax structure (9.8% corporate franchise tax, PTET expiration December 31 2025, ESOP path via IRC §1042) requires structural pre-planning. The structural sequence — residency or trust structure first, ESOP versus stock-sale decision second, M&A advisor third — matters for tax-sensitive founders.

The UnitedHealth/Optum strategic M&A pause (Q3 2025) shifts the default-buyer mapping for Twin Cities healthcare-services sellers. Advisors with non-UNH buyer Rolodexes (Piper Sandler's healthcare desk, Cherry Tree, Hennepin Partners) win the 2026-2027 share.

The single most important advisor-selection question for Twin Cities founders: which firm has the deepest active relationship with the named strategics and PE platforms in your sub-vertical, and can document at least 3 closed transactions with those buyers in the last 24 months? The structural test cuts through the marketing. And the lineage test (where did your founders work before launching?) is the second filter that separates the Lazard MM / Piper Sandler / Goldsmith Agio Helms credentialed bench from less-experienced boutiques.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Minneapolis shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — what your buyer is actually doing once you sign the LOI

- M&A Data Room: Setup and Workstream Mapping — the data room setup playbook for sell-side prep

- Best Data Room for Small M&A Deals — VDR selection for sub-$30M sales, the band where most founder/family-led Twin Cities mandates close

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including vendor DD

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark

- Hard vs Soft Due Diligence: The 5-Frame Playbook — distinguishing the document-driven from the people-driven DD lanes

- Due Diligence Timeline: The Critical-Path Playbook — orchestrating 6 parallel workstreams against the QoE → SPA → financing → RWI → HSR critical path

- How to Roll Equity in M&A Deals — when and how sellers retain a stake in the new platform

- How to Structure an Earnout in an M&A Sale — the earnout mechanics and trap-avoidance playbook

- Best M&A Advisors in Nashville — Southeast healthcare-services comparator

- Best M&A Advisors in Chicago — Midwest mid-market comparator

- Best M&A Advisors in Cleveland — Northeast Ohio industrial + polymers/specialty-chemicals comparator

- Best M&A Advisors in St. Louis — Mid-Missouri "Headquarters Town" comparator with a deep industrial, distribution, and food base and a homegrown national bank (Stifel)

- Best M&A Advisors in San Diego — West Coast biotech comparator

- Best M&A Advisors in Boston — East Coast biotech comparator

- Best M&A Advisors in Kansas City — the Plains "Ownership Town" where Piper Sandler keeps its one resident regional deal office (Leawood) and employee ownership is a first-class exit

Footnotes and sources

- Piper Sandler — firm overview, league-table positioning, 145 IB pros

- Greene Holcomb Fisher acquisition by BMO (August 2016) (BMO Newsroom, June 2016)

- Craig-Hallum Capital Group — firm overview, transaction list May 2026

- Hennepin Partners launch announcement (BusinessWire, April 25 2018)

- Cherry Tree & Associates — firm overview

- Quazar Capital — firm overview

- Vermillion Capital — firm overview, F&B + industrial track record

- True North M&A — Sunbelt spinout September 2021

- SealedBid Marketing — firm overview

- Aethlon Capital — Sima Griffith bio + track record

- Northland Securities — firm overview

- Madeira Partners — firm overview

- BlackTorch Capital — firm overview

- UnitedHealth completes Amedisys acquisition (Healthcare Dive, August 2025)

- Ecolab to acquire CoolIT Systems for $4.75B (BusinessWire, March 20 2026)

- Patterson Companies-Patient Square Capital $4.1B close (Patterson 8-K, April 17 2025)

- IonQ-SkyWater Technology announcement (SEC 8-K, January 2026)

- Medtronic acquires CathWorks (MedTech Dive, April 2026)

- Resonetics acquires Resolution Medical (PRNewswire, March 23 2026)

- CohnReznick combines with Smith Schafer (Accounting Today, January 2026)

- Toro acquires Tornado Infrastructure Equipment (Toro 8-K, December 2025)

- Boston Scientific announces Penumbra acquisition (BSX 8-K, January 2026)

- Norwest Equity Partners closes Fund XI at $1.0B and Mezz V at $400M (Norwest press release, July 2024)

- Castlelake aviation fund close (PRNewswire, March 2025)

- Medical Alley Association — ecosystem data 800+ HC orgs / 530+ medtech / 95% within 50km

- Greater MSP economic data — Twin Cities metro statistics

- Minnesota Department of Revenue — PTET expiration December 31 2025, corporate franchise tax

- Bain Healthcare Private Equity Market 2026 Report (Bain & Company)

- Twin Cities Business F500 tally 2025