Roll Equity in M&A: 2nd-Bite Math, the OBBBA QSBS Tax Bomb, and the Re-Vesting Clause That Burns Founders (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Roll Equity in M&A: 2nd-Bite Math, the OBBBA QSBS Tax Bomb, and the Re-Vesting Clause That Burns Founders (2026)

Quick answer: Roll equity is the slice of the sale you take in HoldCo units rather than cash. In 21% of 2025 private M&A deals — and the majority of PE-sponsored LMM deals — sellers rolled some portion of consideration (SRS Acquiom 2026 Deal Terms Study, 2,300+ deals, $569B aggregate). The math is a right-tail bet (at 3x exit with realistic dilution, rollover beats all-cash by ~6%; at 8x, by ~94%). The OBBBA July 4 2025 expansion of Section 1202 QSBS created the most-missed pitfall of 2026: standard PE rollover into an LLC HoldCo DESTROYS QSBS character, costing founders $2-5M of permanent tax on $10M of pre-OBBBA gain. Plus re-vesting on equity you already owned, drag-along with no minimum-price floor, MPI dilution that quietly shrinks 25% to 22%, and 8 other quantified founder pitfalls. This is the playbook I would hand a founder-CEO at LOI signing.

Last updated: May 2026

Why I wrote this

I have advised founders on rollover-structured exits, watched re-vesting clauses get inserted at the last minute, and seen QSBS-eligible founders silently lose $2-5M of tax exclusion because their CFO did not flag the partnership-rollover issue until the unit purchase agreement was being signed. At Peony we now serve more than 5,900 customers, and the pattern that shows up across the M&A deals our platform hosts is consistent: rollover is now structurally embedded in nearly every PE-sponsored LMM transaction. Sellers come to it with a few intuitions — "I'll get a 2nd bite," "the sponsor will take the multiple from 8x to 12x" — and almost no model of how the math actually breaks down when realistic dilution is applied.

The 2024-2026 data on rollover prevalence is now unusually clear. The SRS Acquiom 2026 M&A Deal Terms Study — covering 2,300+ private-target acquisitions valued at $569 billion that closed 2020-2025 — shows cash + management rollover deals at 21% of all 2025 deals, up three percentage points from 2024. Cash + stock deals are another 20%, also up three percentage points. All-cash deals dropped to 51% in 2025, the lowest in four years. Within the PE-sponsored LMM cohort specifically, rollover is materially more prevalent — Auxo Capital describes it as "standard practice," Linden Law as "common practice," and Lippes Mathias as the default for independent sponsor deals (which average 16.9% rollover with founder-CEOs running 30-40%). The 8 percentage-point shift toward mixed consideration in 2025 is the largest single year-over-year structural change in M&A consideration mix in the post-COVID period.

Two structural shifts make 2026 a uniquely high-stakes year to get rollover right. First, the One Big Beautiful Bill Act (Pub. L. 119-21), signed July 4 2025, materially expanded Section 1202 QSBS — tiered exclusions at 3/4/5-year holds, $10M → $15M cap, $50M → $75M gross-asset limit. This is good news for founders generally. It is bad news for founders who roll into the standard PE partnership-HoldCo structure, because partnership interests do not qualify as QSBS — the entire QSBS character is destroyed on a § 721 rollover. The WilmerHale § 1202 white paper and Holland & Knight's July 2025 analysis on transfers of QSBS confirm this treatment. Second, the SRS Acquiom 2026 working-capital and consideration data make clear that the bid-ask gap of 2023-2024 is partially closing through rollover, which means founders are increasingly being asked to share execution risk that historically lived entirely on the buyer's balance sheet.

This post is the working playbook I would hand to a founder-CEO at LOI signing — or to the founder's tax counsel, M&A lawyer, banker, or wealth adviser. It is structured around seven proprietary frames that I have battle-tested against the actual mechanics of rolled-equity deals. The 2nd-Bite Math Triangle quantifies the right-tail bet. The Pitched-vs-Realistic Ownership Gap corrects the buyer's IC-memo math. The Tax-Deferred Reorg Decision Tree maps § 721 vs § 351 vs § 368(a)(1)(F) vs § 1042. The OBBBA QSBS Roll Tax Bomb quantifies the most-missed 2026 founder pitfall. The Cap-Table Mechanics frame distinguishes Rollco / HoldCo / OpCo equity. The Drag-Tag Asymmetry Trap + 10 other pitfalls catalogs the 11 quantified drafting traps founders walk into. And the Protective Provisions Checklist maps each pitfall to the position counsel should fight for.

What is roll equity, and why is 2026 LMM using it more?

Roll equity is the slice of the sale consideration the seller receives in equity of the buyer's holding company rather than in cash. The mechanics are simple in concept and structurally rich in practice. In a typical PE-LMM platform deal, the founder sells the operating business for $100M total consideration. Of that $100M, the founder might receive $75M in cash at close and roll $25M into the buyer's newly-formed HoldCo entity (typically an LLC taxed as a partnership). The founder receives HoldCo units representing a minority position in the sponsor-controlled vehicle. The sponsor contributes its own equity (let's say $30M of sponsor common and preferred capital plus leverage at the OpCo level), and the cap table at HoldCo on day 1 shows the sponsor holding majority voting equity, the founder holding a minority unit position, and (typically) a 10-15% management profits interest pool reserved for the next-tier executive team.

The economic logic of rollover is alignment. The sponsor wants the founder (or seller-CEO) to retain skin in the game so they continue to operate the business effectively post-close. Lenders typically want to see management rollover as a signal that operating leaders believe in the deal thesis. And from the founder's side, rollover provides exposure to the 2nd-bite exit — if the sponsor executes the growth plan and exits the platform at a higher multiple in 4-7 years, the founder participates in that upside. The structural reality, however, is that the rolled equity sits in a sponsor-controlled vehicle. The founder's economic upside depends on sponsor execution. The founder has very limited control over timing of the next exit, capital decisions, M&A choices, or capital structure. The rolled units are illiquid until the sponsor decides to exit.

The 2026 LMM rollover prevalence increase is driven by three structural forces. First, the bid-ask gap that opened in 2023-2024 (sellers anchored on 2021 peak valuations, buyers underwriting at higher cost of capital) has partially closed through structural compromise rather than headline price compromise. Rollover lets the buyer pay a higher headline price (good for the seller's psychology and for the seller's tax-deferred portion) while the buyer's at-risk equity check stays the same. Second, the 2025 lending environment has made rollover effectively a debt-covenant requirement on many leveraged LMM deals. Third, the rise of independent sponsors as a deal-doing channel (Axial's 2025 Independent Sponsor Report shows IS deal volume up materially) has expanded the universe of rollover-dependent transactions because IS lacks committed fund equity and uses seller rollover to bridge the equity gap.

The cleanest framing for the conversation: in 21% of all 2025 private M&A deals — and the majority of PE-sponsored LMM deals — sellers rolled equity rather than taking 100% cash. The structural question is no longer "should I consider rollover?" but "how do I structure it so the deferred-tax upside isn't eaten by the protective-provisions downside?"

The 2nd-Bite Math Triangle: exit multiple, hold period, dilution

Most rollover pitch decks model only one variable: exit multiple at 2nd bite. The realistic case requires modeling three. The 2nd-Bite Math Triangle is the proprietary frame I use to translate the buyer's "you'll get 4x on your rolled portion!" claim into a defensible founder-side model.

The three variables: (1) the exit multiple at 2nd bite (3x / 5x / 8x / 12x of total HoldCo enterprise value at close); (2) the hold period (typically 4-7 years; 5 is the baseline assumption); and (3) HoldCo dilution between close and exit (midcycle equity raises, MPI pool dilution, follow-on acquisitions financed with new equity — typically 10-25% of cumulative dilution over a 5-year hold).

Base case setup

The base case I use as a starting model:

- Founder sells $100M target company

- PE buyer pays $100M total consideration: $75M cash + $25M rolled into HoldCo (25% rollover)

- Founder's basis in target equity: $5M (so built-in gain at sale = $95M)

- Federal long-term capital gains + NIIT effective rate: 23.8% (for cleanness; state adds 0-13.3%, so blended is 24-37%)

- Hold period to 2nd exit: 5 years

- PE buyer also contributes $30M of sponsor equity to HoldCo at close

- HoldCo starts with $25M founder + $30M sponsor + leverage at OpCo level

- Pitched founder HoldCo ownership at close: $25M / $55M total equity = 45.5% (this is what the buyer's IC memo shows)

- Realistic founder HoldCo ownership after sponsor preferred liquidation preference and MPI pool dilution: ~30%

The first thing every founder needs to understand: the "pitched 45.5%" number is the buyer's IC-memo math. The realistic 30% is what the founder actually gets after sponsor preferred preference and MPI dilution take their cuts off the top. Always model the realistic case.

Cash-at-close baseline (both cases)

- Cash received at close: $75M

- Tax on cash portion (75% of the $95M built-in gain attributed to the cash side): $71.25M × 23.8% = $16.95M

- Net cash after tax: $58.05M

All-cash counterfactual

- Founder takes all $100M cash at close

- Tax on $95M gain: $95M × 23.8% = $22.61M

- Net cash after tax: $77.39M

- Reinvest at 7% blended (60% S&P + 40% bonds) for 5 years: terminal value $108.6M

This is the comparison number every rollover decision should be measured against. If the rolled equity does not produce more than $108.6M of terminal value, the rollover destroyed value relative to the all-cash alternative.

The 16-cell matrix

The full math at four exit multiples (3x / 5x / 8x / 12x), two ownership cases (pitched 45.5% vs realistic 30%), and two dilution cases (0% midcycle dilution vs 20% midcycle dilution):

| Exit multiple | Pitched 45.5%, no dilution | Pitched + 20% dilution | Realistic 30%, no dilution | Realistic 30% + 20% dilution |

|---|---|---|---|---|

| 3x ($300M HoldCo EV) | $163.25M | $146.96M | $127.82M | $115.99M |

| 5x ($500M HoldCo EV) | $232.59M | $205.45M | $173.54M | $154.05M |

| 8x ($800M HoldCo EV) | $336.61M | $292.85M | $242.12M | $211.12M |

| 12x ($1.2B HoldCo EV) | $475.29M | $409.50M | $333.56M | $289.97M |

| All-cash counterfactual (terminal) | $108.6M | $108.6M | $108.6M | $108.6M |

"20% dilution" here means a midcycle equity raise of 20% of HoldCo's outstanding equity at fair value — founder's ownership goes from 30% to ~25% pro-rata (30% / 1.20).

The proprietary observations from this matrix:

-

At 3x exit with realistic ownership and 20% dilution, rollover only beats all-cash by 6.4% over a 5-year hold. The founder forgoes ~$19M of immediate liquidity (the difference between $75M cash and $94M cash if they had taken all cash) to make an extra ~$7M in terminal value over 5 years. The IRR on the rolled $25M to net $58M ($116M minus $58.05M cash-at-close) is approximately 18.3%, which beats the 7% reinvestment return but only modestly.

-

At 5x exit with realistic ownership and 20% dilution, the founder nets ~$154M vs $109M all-cash — a 42% premium. The IRR on the rolled $25M is approximately 30.8%. This is the case where rollover starts to clearly dominate cash, but it requires the sponsor to deliver a 5x EV expansion in 5 years (which is a strong PE outcome).

-

At 8x exit with realistic ownership and 20% dilution, the founder nets ~$211M vs $109M all-cash — a 94% premium. The IRR on the rolled $25M is approximately 43.7%. This is the case the buyer's pitch deck implicitly assumes.

-

At 12x exit, the rollover dominates regardless of dilution. But 12x exits are right-tail outcomes — they happen in maybe 10-15% of PE platform exits per GF Data middle-market PE benchmarks.

The cleanest takeaway: most of the rollover advantage lives in the right tail of the exit-multiple distribution. If the founder thinks the sponsor has a 30%+ probability of executing a 5x+ exit, rollover is mathematically correct. If the founder thinks the multiple is already at peak and the sponsor will need leverage just to deliver 3x, the all-cash alternative is competitive and the protective-provisions risk is asymmetric.

Why this matters at LOI

Buyer-side IC memos almost universally model the pitched 45.5% case with no dilution. The buyer's banker sells the deal to the founder using a "$25M rolled becomes $100M at 8x" narrative. The realistic case — 30% ownership, 20% dilution — is what shows up in year 5. The gap between pitched and realistic is $70-130M of value at 8x exit, depending on how the dilution distributes. This is why every founder should build their own version of the 2nd-Bite Math Triangle at LOI — and not rely on the buyer's model.

What's the rollover percentage range by buyer archetype?

Buyer-archetype matters more than deal size in determining rollover percentage. The four archetypes have materially different rollover patterns.

PE platform acquisitions (institutional sponsor with committed fund): 15-30% rollover is the standard range per Linden Law Partners and Auxo Capital Advisors. The modal deal anchors at 20-25% — what Auxo describes as the "standard sponsor control deal with defined KPIs." The lower end (≤15%) shows up when the deal involves a faster owner transition or a strong second-tier leadership team that the sponsor wants to install. The higher end (35%+) shows up when the deal involves an ambitious growth plan, a higher headline valuation, or lender-imposed constraints on sponsor equity at close.

A high-profile recent data point that anchors the range: the TPG take-private of AvidXchange in FY2025 (per the SC 13E-3 schedule filing) showed 100% rollover from CEO Michael Praeger and 40-50% rollover from other senior executives, with total management rollover representing 9% of the deal's sources of funds. This is a public-company take-private case where rollover was used to align the senior team with the long-term thesis, not as a financing tool — and the rollover percentages at the CEO level are exceptionally high relative to LMM norms.

Independent sponsor (IS) deals: 10-40% rollover range with founder-CEOs at the top end. The average across the IS cohort per Lippes Mathias / Sadis & Goldberg analysis is 16.9%. Why higher than fund-PE? IS lacks committed fund equity, so seller rollover supplements the equity check from capital partners. For a $30M EV deal where an IS is raising $8M of equity from a single capital partner and putting in $1M itself, getting the seller to roll $5M materially de-risks the deal for the capital partner. The structural pattern: IS deals routinely use rollover as a capital-stack solution, not just an alignment device.

Strategic acquirers: 5-15% rollover range when structured rollover exists at all. The far more common structure is all-stock or stock-and-cash under one of the § 368 reorganization variants: forward triangular merger under § 368(a)(2)(D), reverse triangular merger under § 368(a)(2)(E), or stock-for-stock under § 368(a)(1)(B). Strategic rollover is usually paid in public parent stock — liquid post-lockup, dividend-paying, exchange-traded — versus the illiquid HoldCo units that PE rollover involves. The trade-off: strategic rollover offers exit liquidity but the founder is exposed to a much larger company's overall equity returns, not the specific platform's growth.

Family office buyers: 10-25% rollover range per Linden Law Partners. The structural difference: longer hold horizons (7-15 years vs PE 3-7 years) make family-office rollover better aligned with sellers who want a longer 2nd-bite window. Family-office governance is also typically less standardized and often more seller-friendly on information rights and exit timing. The trade-off: less professional execution rigor and fewer institutional value-creation playbooks than fund-PE.

The hidden lever embedded in rollover percentage: higher rollover often unlocks a higher headline valuation. Sponsors typically pay an extra 0.25x to 0.75x of EBITDA multiple per incremental 10 percentage points of rollover (transactional convention). A seller asking for $50M EV at 25% rollover might extract $52-55M at 35% rollover. For a founder confident in the company's growth path, this is a strong negotiating angle. For a founder who wants liquidity, it is the wrong direction.

What's the Tax-Deferred Reorganization Decision Tree?

The tax-deferred reorganization options for rolled equity break into four primary paths, each governed by a distinct section of the Internal Revenue Code. Picking the wrong path costs the founder real money — typically $1-5M of incremental tax on a $25M rollover. The decision tree:

IRC § 721 — Contribution to Partnership (the LMM-PE default)

This is the dominant path for PE-LMM rollover. 26 U.S.C. § 721(a): "No gain or loss shall be recognized to a partnership or to any of its partners in the case of a contribution of property to the partnership in exchange for an interest in the partnership."

The structural advantage of § 721 over § 351 is decisive: § 721 has no 80% control requirement. PE buyers almost universally form an LLC HoldCo taxed as a partnership to receive the rolled target equity, and § 721 deferral applies regardless of whether the rolling seller holds 5% or 40% of HoldCo. The seller contributes target equity, receives HoldCo units, and recognizes no gain on the rolled portion at closing. The cash portion remains fully taxable as capital gain.

The seven failure modes of § 721 (per Cordasco's April 2026 § 721 analysis):

- Wrong entity type. § 721 applies only to partnerships and LLCs. A C-corp or S-corp HoldCo does not qualify.

- Disguised sale under § 707(a)(2)(B). Cash distributions from the partnership to the contributing seller within 24 months of the contribution are presumed to be a disguised sale under Treas. Reg. § 1.707-3. The IRS can recharacterize the entire contribution as a taxable sale of property — pulling the deferred gain into the current year and adding interest and possibly penalties.

- Service-property confusion (§ 83). Equity received in exchange for future services (post-closing retention package, profits interest tied to performance) is § 83 ordinary income, not § 721 rollover. The two get comingled in "rollover plus management incentive" deals and create audit exposure.

- Encumbered property + § 752. If the contributed equity has associated liabilities exceeding basis (e.g., the seller's stock was pledged as security), the relief is treated as a deemed cash distribution under § 752, which can trigger gain recognition under § 731.

- Foreign-partner exposure (§ 721(c)). Cross-border deals with foreign LP exposure can lose § 721 deferral on built-in gains exceeding $20K.

- Investment-company rule (§ 721(b)). Multi-target platform rollovers where the HoldCo holds a diversified investment portfolio can trigger gain recognition.

- "Permanent deferral" myth. § 721 defers — does not eliminate — gain. The seller's basis in the HoldCo unit equals the seller's basis in the contributed equity (carryover basis). On 2nd-bite exit, the full deferred gain plus 2nd-bite appreciation comes due.

A numerical example anchored to Cordasco's framing: total deal value $30M, with 70% cash to sellers ($21M, triggering ~$5M of capital gains tax at closing on the cash portion) and 30% rollover ($9M § 721 deferred). The seller's original basis in the target equity is $2M, so total built-in gain at sale is $28M. Of that, $19M is attributable to the cash side (recognized) and $9M is deferred via the rollover. (Cordasco's example uses round numbers; precise 70/30 allocation of the $28M built-in gain yields $19.6M cash-side / $8.4M deferred.) The $9M deferred gain is preserved through carryover basis until 2nd-bite exit.

IRC § 351 — Transfer to Controlled Corporation (corporate-buyer rollovers)

26 U.S.C. § 351(a): "No gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control (as defined in section 368(c)) of the corporation."

"Control" under § 368(c) is the 80% test: the transferors as a group must hold at least 80% of total combined voting power AND 80% of total shares of all non-voting classes immediately after the exchange.

The failure mode: "busted § 351." If the transferor group does not satisfy the 80% control test immediately after the contribution, the entire transaction becomes taxable to ALL property transferors — not just to the cash side. The risk is concrete for PE rollovers structured as corporate HoldCos: the sponsor's fund often owns >80% of HoldCo on its own, and the seller's contribution has to be carefully co-structured with the sponsor's contribution to satisfy the transferor-group 80% test.

§ 351 also has a boot-recognition rule. If the seller receives cash plus stock in exchange for the contributed equity, the seller recognizes gain to the lesser of (a) actual realized gain or (b) the boot received. The cash portion of mixed consideration in a § 351 transaction is fully taxable; only the stock portion qualifies for deferral.

When founders should care about § 351: when QSBS preservation is at stake (see the OBBBA section below) or when the buyer is a corporate strategic acquirer that wants the seller's equity in a corporate HoldCo for tax efficiency at the parent level.

IRC § 368(a)(1)(F) — F-Reorganization (pre-sale S-corp standard)

The F-reorganization, governed by Treas. Reg. § 1.368-2(m) (effective September 20, 2015) and the operative precedent of Rev. Rul. 2008-18, is the standard pre-transaction structure for S-corp targets going to PE.

The mechanics: the S-corp converts to a disregarded entity through an F-reorganization combined with a QSub election. This preserves S-status pre-sale (and the seller's QSubsection 1202-equivalent or pass-through tax treatment) and lets the PE buyer treat the purchase as an asset deal for step-up basis purposes — what is often described as an "F-reorg plus 338(h)(10) equivalent." The seller's deferral mechanic is preserved while the buyer captures the asset-step-up tax benefit.

BDO's 2020 analysis and the Tax Adviser's September 2020 article on F-reorganizations remain the canonical 2026 references on this structure. No material amendments have been proposed as of May 2026.

For S-corp founders going to a PE buyer, the F-reorganization conversation should happen 6-12 months before the LOI — the structure requires careful pre-deal mechanic coordination, and rushing it at LOI typically destroys the buyer's step-up basis benefit (and reduces the headline price).

IRC § 1042 — ESOP Rollover (alternative full-liquidity path)

26 U.S.C. § 1042 provides a structurally different path: a C-corp shareholder who sells at least 30% of stock to an Employee Stock Ownership Plan (ESOP) can defer capital gains by reinvesting the proceeds in qualified replacement property (QRP) within a 15-month window (3 months before sale through 12 months after).

The requirements: (1) seller held shares for at least 3 years; (2) target is a C-corp (S-corps must convert first); (3) ESOP holds at least 30% post-sale; (4) QRP qualifies as a domestic operating-corporation security (debt or equity), excluding real estate, mutual funds, muni bonds, and Treasuries.

The unique advantage of § 1042: if the seller holds the QRP until death, basis steps up under § 1014 and the deferred tax is never paid. This is a powerful estate-planning play for founders who want full liquidity at sale without committing to a PE rollover-and-HoldCo structure.

§ 1042 is not "rollover equity" in the M&A sense — the seller exits the target entirely. But it is a frequently-overlooked ALTERNATIVE for sellers who want tax deferral with full liquidity (vs the PE-rollover trade-off of tax deferral with illiquid sponsor-controlled equity). For founders with strong management bench depth (necessary to make an ESOP work post-sale) and no preference for a PE-driven 2nd bite, § 1042 deserves serious modeling.

The decision-tree summary

The four-path decision tree maps to founder situation:

- PE-LMM buyer, LLC HoldCo: § 721. Watch the 7 failure modes, especially the 24-month disguised-sale window and the QSBS destruction issue.

- Corporate buyer (strategic or PE-corporate HoldCo) where QSBS preservation matters: § 351, with co-structured contribution to satisfy 80% transferor-group control test. Use a corporate HoldCo, not LLC.

- S-corp target going to PE buyer wanting step-up: § 368(a)(1)(F) F-reorganization 6-12 months pre-LOI, combined with QSub conversion. Then § 721 partnership HoldCo for the rollover.

- C-corp founder wanting full liquidity + tax deferral via estate planning: § 1042 ESOP path. Requires 3+ year holding period, 30% ESOP sale minimum, and QRP discipline.

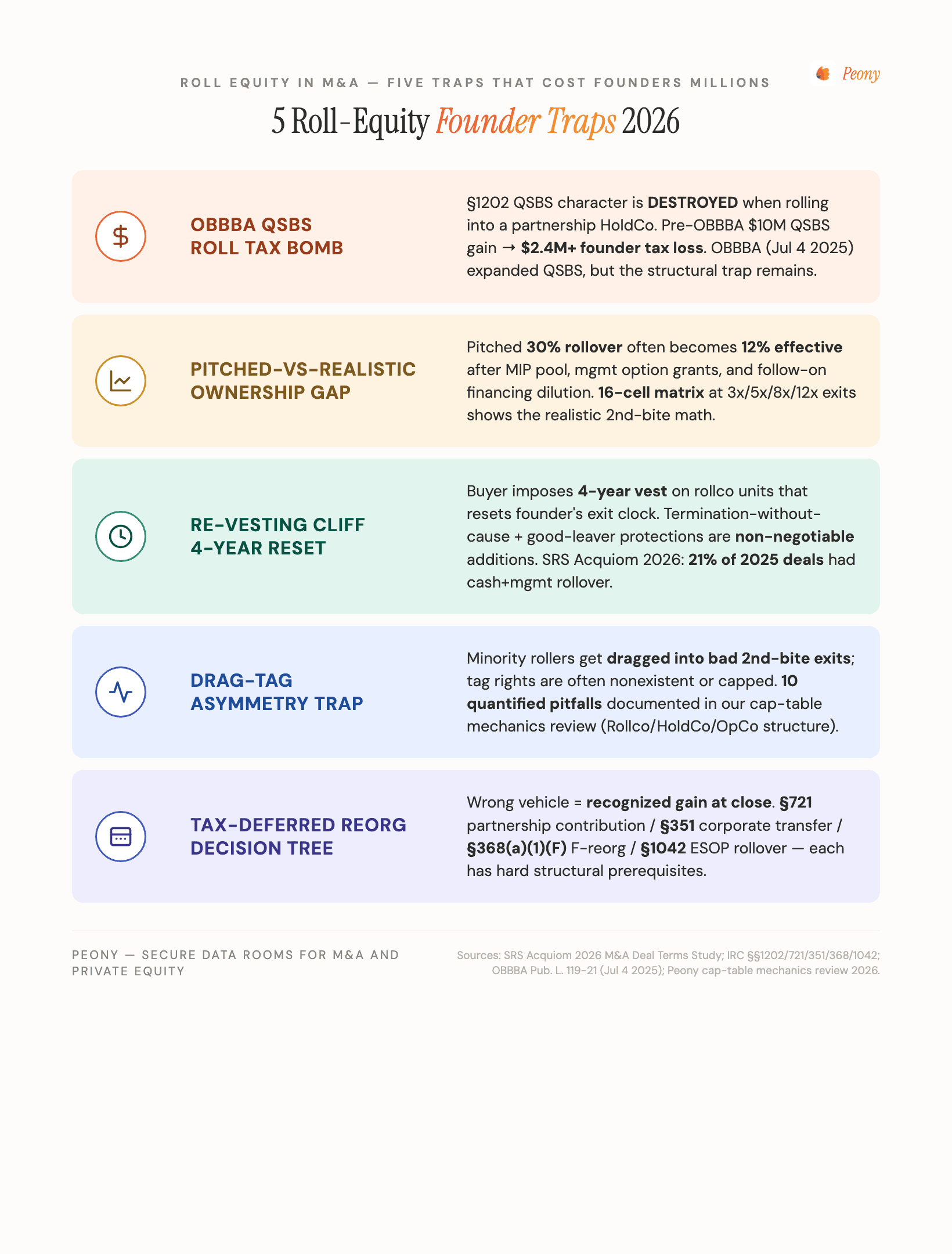

The OBBBA QSBS Roll Tax Bomb (the most-missed pitfall of 2026)

The One Big Beautiful Bill Act (Pub. L. 119-21), signed July 4 2025, expanded Section 1202 in three structurally important ways for QSBS acquired after July 4 2025:

- Tiered exclusions: 50% gain exclusion at a 3-year hold, 75% at a 4-year hold, 100% at a 5-year hold. (Previously, 100% exclusion required a 5+ year hold with no partial-credit tier.)

- Per-issuer cap raised from $10M to $15M (inflation-indexed after 2026).

- Gross-asset limit for qualifying companies raised from $50M to $75M (inflation-indexed after 2026).

For founders whose QSBS was acquired before July 5 2025, the old rules apply — 100% exclusion only at 5+ years, $10M cap, $50M gross-asset limit. The transition rule means the trap I am about to describe applies in 2026 to founders rolling QSBS that was acquired pre-OBBBA, and continues to apply in 2027-2030+ for founders rolling QSBS acquired post-OBBBA.

The trap

When a founder holding QSBS-eligible C-corp stock rolls into the standard PE partnership-HoldCo structure (LLC taxed as partnership, under § 721), the QSBS character is destroyed. Partnership interests do not qualify as QSBS under § 1202(h)(4). The seller's QSBS-eligible gain on the rolled portion is permanently lost — the seller cannot get the exclusion back, even on the eventual 2nd-bite exit from HoldCo.

The WilmerHale § 1202 white paper (April 2025) and Holland & Knight's "Transfers of Section 1202 Qualified Small Business Stock" (July 2025) both confirm this treatment. Multiple law-firm publications across 2025-2026 (McLane Middleton 2025, Tax Adviser November 2025 and December 2025) have reinforced the trap.

Quantified cost

On $10M of pre-OBBBA QSBS-eligible gain (the old $10M cap), 100% exclusion would mean zero federal tax. Rolling that $10M into an LLC HoldCo destroys the QSBS character and exposes the gain to standard long-term capital gains plus NIIT: 23.8% effective federal tax = $2.38M of permanent tax loss, plus state.

On $15M of post-OBBBA QSBS-eligible gain (the new $15M cap with full 100% exclusion at 5-year hold), the equivalent loss is $3.57M of permanent federal tax, plus state. In high-tax states (California, New York, New Jersey), the loss climbs to $4-5M+.

The structural fixes

Two ways to preserve QSBS treatment in a PE rollover:

Fix 1: Cash-out the QSBS portion at close. The seller sells the QSBS-eligible portion of equity to the buyer for cash at closing (preserving the QSBS exclusion on the cash portion) and then makes a separate § 351 contribution of OTHER assets to the buyer's corporate HoldCo. This works when the founder has both QSBS-eligible C-corp stock and other equity assets (options, RSUs, post-IPO stock, second-issuance C-corp stock). It does not work when the QSBS is the founder's only equity.

Fix 2: Use a corporate HoldCo (not LLC) for the rollover. A corporate HoldCo structured under § 351 preserves QSBS character via § 1202(h)(4), which provides that successor stock received in a § 351 exchange (or qualifying reorganization) for QSBS retains QSBS treatment. The exchanged stock continues as QSBS in the new corporate HoldCo. Note: § 1202(h)(4) covers stock-to-stock preservation; partnership-to-corporation conversions follow different rules under § 1202(i) where the holding period restarts at incorporation date. The cost: corporate HoldCos are less flexible on debt push-down and management profits interests than LLC HoldCos, which is why PE-LMM buyers default to LLC structures. The seller's negotiating ask is: "we'll roll only into a corporate HoldCo to preserve my QSBS exclusion." This is a non-trivial deal-term ask, and many PE buyers will push back hard or refuse.

Fix 3 (partial mitigation): Carve out the QSBS-eligible portion for full cash-out and roll only the excess. If the founder's total equity value is $40M and $15M qualifies for QSBS, take $15M as cash at close (preserving the exclusion) and structure the rollover on the remaining $25M. This produces the highest tax-efficiency outcome on QSBS-heavy cap tables.

My operating rule

If you have held C-corp stock for 5+ years before a PE sale, you need a tax adviser who is explicitly paid to model the QSBS-vs-rollover tradeoff. Not your buyer's tax counsel. Your own. The fee is $25-75K. The savings is $2-5M. The math is asymmetric.

I have seen founders leave $2-5M on the table because their CFO did not flag QSBS loss until the unit purchase agreement was being signed. By then, the rollover structure was locked, the headline price was set, and the founder had no leverage to renegotiate the entity form. The conversation has to happen at LOI stage, not at signing.

Cap-Table Mechanics: Rollco vs HoldCo vs OpCo

The standard PE rollover structure involves three potential vehicles: Rollco (an intermediate SPV used in some structures), HoldCo (the primary sponsor-controlled vehicle), and OpCo (the original target operating company, now a wholly-owned subsidiary). Understanding which equity sits where matters because the governance, tax, and liquidity characteristics differ materially.

Standard PE rollover structure (LLC HoldCo path, § 721)

The most common configuration:

- HoldCo LLC (taxed as partnership): newly formed at close. The sponsor manages HoldCo, which holds 100% of OpCo equity. Sponsor contributes capital (let's say $30M of sponsor common + voting preferred). Founder contributes $25M of rolled OpCo equity under § 721. HoldCo issues units to both — typically Class A voting preferred to sponsor (with liquidation preference, dividend accrual, and conversion rights) and Class B common to founder (no liquidation preference, no accrual, residual equity).

- OpCo: original target entity, now a wholly-owned subsidiary of HoldCo. All operating activity continues at OpCo level: payroll, customer contracts, accounts receivable, vendor relationships, employee benefits.

- Debt: typically sits at HoldCo level (acquisition-debt financing) or at OpCo level (operating-debt financing), or both. Senior debt and mezzanine debt typically attach at OpCo for asset-coverage purposes.

The economic result: founder's "$25M of rolled equity" is HoldCo LLC Class B common units, not OpCo equity. The sponsor's Class A preferred sits in front of the founder's common in the liquidation waterfall. At 2nd-bite exit, the preferred typically gets 1x return of capital plus accrued dividends before any proceeds flow to common. On a soft-multiple exit (say, the sponsor wants out at 2x sponsor MOIC because the fund clock is ticking), the founder's common can end up close to zero after preferred preference and MPI take their cuts.

Variation: blocker C-corp insertion

For founders with foreign-income exposure or tax-exempt LP exposure in their personal holding entity (family LP with foreign investors, charitable trust, etc.), a blocker C-corp is sometimes inserted between the founder and HoldCo LLC. The blocker absorbs unrelated business taxable income (UBTI) or effectively-connected income (ECI) issues that would otherwise pass through HoldCo LLC to the founder's tax-exempt or foreign-exposed entity. The cost: blocker adds tax layers but solves the underlying flow-through issue.

Variation: § 351 corporate HoldCo

Used when the seller wants to preserve QSBS treatment (§ 1202(h)(4) preserves QSBS character on a stock-to-stock § 351 exchange of QSBS for successor C-corp stock). Less flexible on debt push-down and MPI structures. Rarely used in modern PE-LMM outside of QSBS-driven cases.

Variation: "Rollco" intermediate SPV

Some PE structures insert a Rollco SPV between the founder and HoldCo for tax-state planning reasons (e.g., founder is in a high-tax state, wants tracking units to a specific portfolio segment, or has unusual residency planning needs). Rollco adds complexity but does not change economic substance for most founders. It is worth asking your tax counsel whether a Rollco mechanic is justified by your specific situation.

Voting and control layers

The HoldCo governance default for PE platform deals:

- HoldCo board: typically 5 seats — 3 sponsor, 1 founder, 1 independent (sponsor-nominated, sometimes mutually agreed)

- Major decisions (sale, M&A above a stated EBITDA size, capital raises above a stated dollar threshold, CEO replacement): sponsor controls via voting preferred

- Minor decisions (operational, capex below a stated threshold, hiring): board majority (which sponsor still controls)

- Founder protections: typically limited to (a) anti-dilution on certain new issuances at below-FMV pricing, (b) tag-along on sponsor sales, (c) ROFR on the founder's own units, (d) operating-agreement amendments requiring unanimous consent on a narrow list of items (this is rarely granted to founders in modern PE-LMM deals)

The structural pattern: the founder holds economic equity but has very limited voting control. The sponsor controls timing, capital decisions, executive hiring/firing, M&A, and exit. The founder's leverage is at LOI (when terms are negotiated) and at closing (when the operating agreement is signed). After closing, the founder has almost no operational leverage on HoldCo decisions.

The Drag-Tag Asymmetry Trap + 10 other quantified pitfalls

The protective-provisions side of rollover is where most of the value destruction happens. Sellers focus on the headline price and the rollover percentage and ignore the operating-agreement mechanics that determine whether the rolled equity is alignment or claw-back disguised. Eleven pitfalls, ranked by how much value they typically destroy:

Pitfall 1: Re-vesting on rolled equity (the #1 hidden trap)

What happens: the buyer asks the seller to roll $25M of equity and quietly subjects all of it to a 4-year cliff or ratable vesting schedule tied to continued employment. If the founder leaves at month 18 (sponsor-pushed departure, mutual termination, or even voluntary departure), they forfeit 60% of the rolled equity.

Why it's hidden: the LOI typically says "rollover equity, subject to standard vesting terms." The actual vesting mechanics live in the unit purchase agreement and LLC operating agreement, which most founders don't read until weeks before close — when they have no leverage to renegotiate.

My operating rule: I would never sign a deal where any portion of the rolled equity is subject to re-vesting. The seller is rolling equity they already owned. The buyer can grant additional incentive units (MPI, profits interest, stock options) with vesting — fine. But the rolled portion must be fully vested at close. If the buyer won't agree, that signals they expect to fire the founder in 18 months and are pre-positioning the equity-recovery mechanic.

Pitfall 2: Drag-along with no minimum-price floor

What happens: HoldCo operating agreement gives the sponsor (majority holder) drag-along right — the ability to force the founder to sell at any future exit at any price the sponsor accepts.

Why it kills: the sponsor's fund clock dictates exit timing. If the sponsor's fund is in year 6 with a 10-year life, the sponsor must exit by year 8-9 — even if the market is soft and a 4x is on the table when an 8x would happen in year 11. The founder gets dragged at suboptimal price.

The protective provision: drag minimum-price floor (drag only triggers above 2x sponsor's invested capital MOIC) OR drag minimum hold period (drag only after 5-year HoldCo period) OR founder veto on drag for first 36 months. PE sponsors push back hard on these; the compromise is typically a drag plus tag with no floor, but with co-sale rights ensuring founder gets the same per-unit price as sponsor.

Pitfall 3: Tag-Along Asymmetry (the silent founder-killer)

The structure: sponsor has unilateral right to sell a portion at any time without triggering tag. Operating-agreement language typically reads: "transfers of less than 10% of HoldCo units are exempt from tag-along."

Why it kills: the sponsor partially liquidates at high valuation (a dividend recap, a secondary sale to another PE fund, a related-party transfer to a parallel fund) — and the founder is locked in. No liquidity event triggered for the founder. The sponsor pulls money out; the founder rides illiquid.

The fix: tag-along on ALL sponsor transfers above a low threshold (5% of HoldCo, or with no de minimis carveout at all). This is the most underrated protective provision in rollover drafting. Sellers focus on drag-along language and ignore the tag asymmetry that lets sponsors get partial liquidity while the founder stays locked.

Pitfall 4: Information rights stripped at HoldCo

What changes: pre-deal, founder is CEO with full board access and monthly financials. Post-deal, founder is HoldCo minority unitholder.

What the operating agreement typically grants minority unitholders: annual audited financials within 120 days, quarterly unaudited within 45 days, K-1 by April 15. That's it.

What founder loses: monthly financial pack, board observer seat (unless explicitly negotiated), access to monthly KPI reports, real-time visibility into operations.

The protective provision: negotiate board observer right plus monthly financial pack as minimum. For 25%+ rollover, push for a board seat (not just observer). The reality is most founders don't ask. By month 6 post-close, they are transitioned out of operational meetings and flying blind on the asset they own a chunk of.

Pitfall 5: QSBS tax bomb (lost via § 721 rollover)

Covered in depth above. Recap: $10M of pre-OBBBA QSBS-eligible gain rolled into an LLC HoldCo = ~$2.38M of permanent federal tax loss, plus state. The fixes: corporate HoldCo, cash-out the QSBS portion at close, or partial cash-out plus reduced rollover.

Pitfall 6: Management Profits Interest (MPI) Dilution

What happens: PE buyer creates a 10-15% MPI pool at HoldCo to incentivize the next-tier executives. The founder thinks "I own 25% of HoldCo." But the MPI pool dilutes the founder's fully-diluted ownership.

Numerical example:

- Founder rolls $25M into HoldCo (25% of pre-MPI cap table)

- 12% MPI pool created at close, with hurdle = sponsor invested capital

- Post-MPI, founder's diluted ownership = 25% × (1 - 0.12) = 22%

- Assume the MPI hurdle is $140M (sponsor invested capital plus 5-year accrued preferred dividend at typical 8% accrual).

- At 8x exit ($800M HoldCo, with $660M of value above the MPI hurdle), MPI gets $79.2M off the top

- Founder's effective 22% of remaining $720.8M = $158.6M

- vs $200M the founder thought they had at 25%

- Loss to MPI dilution: ~$41M

The fix: negotiate an MPI carveout that excludes the founder OR includes the founder in the MPI pool. Have your counsel model the fully-diluted waterfall before signing.

Pitfall 7: Disguised-Sale 24-Month Window

What happens: seller rolls 25% into HoldCo at close. Twelve months later, the sponsor does a leveraged dividend recap and distributes proceeds to all HoldCo unitholders, including the seller.

The trap: Treas. Reg. § 1.707-3 presumes that a distribution within 2 years of a contribution is a disguised sale under § 707(a)(2)(B). The seller's tax-free § 721 contribution gets recharacterized as a taxable sale of property.

Tax cost: seller owes capital gains tax on the originally-deferred portion — often discovered years later in an IRS audit, with interest and possibly penalties.

Protective drafting: either (a) the operating agreement explicitly restricts distributions to the seller for 24 months OR (b) the seller's tax counsel runs a § 707(a)(2)(B) "rebut the presumption" analysis at the time of each distribution and documents the business purpose.

Pitfall 8: Pre-emptive Rights Lost in Subsequent Rounds

What happens: HoldCo raises more equity 18 months post-close (acquisition financing, growth capital). Sponsor and founder both have pre-emptive rights. Sponsor exercises; founder doesn't (no cash to invest).

The trap: founder's ownership dilutes pro-rata. If sponsor invests $20M new equity at higher valuation, founder's percentage drops materially even though dollar value rises.

The fix: pay-to-play protection. If founder participates ratably, ownership is preserved. If founder can't fund the call, sponsor offers a credit-line/loan structure for founder to participate, or the founder's pre-emptive right is honored in tracked tracking units that vest later.

Pitfall 9: Charter Restrictions on Transfer

What happens: founder wants to transfer rolled equity to a family trust for estate planning. The operating agreement says transfers require sponsor consent (typically not unreasonably withheld) AND right of first refusal at HoldCo level.

The trap: sponsor blocks the transfer or insists on ROFR at a discounted valuation determined by the sponsor's IC, not a third-party 409A appraiser.

The fix: explicit carveout for estate-planning transfers (to family members, trusts, family LPs controlled by founder) — standard in 2026 deal docs at the seller-friendly end, but absent in many sponsor templates. The carveout should specifically waive sponsor consent and ROFR for transfers to immediate family, irrevocable trusts for the benefit of family, and family limited partnerships controlled by the founder.

Pitfall 10: Exit Timing Control

The structural reality: HoldCo (sponsor-controlled) decides when the 2nd exit happens. The founder has no operational control.

What this means: sponsor's fund clock dictates exit timing. If the sponsor's fund is in year 6 with a 10-year life, the sponsor MUST exit by year 8-9 — even if the market is soft and 4x is on the table when 8x would happen in year 11.

Founder's lever: negotiate drag minimum hold period (e.g., 5-year minimum HoldCo period before forced exit). Sponsors push back; reality is most accept 3-4 year minimum drag floor.

Pitfall 11: Call Option Triggered by Employment Termination (PE template default)

Calfee's 2025 analysis describes call options as "included in nearly all equityholder agreements" and as "a future negotiating tool and a significant source of post-closing leverage" for the sponsor. The PE buyer retains the right to repurchase the founder's HoldCo units upon termination of employment.

The trap: call price for "bad leaver" termination is typically lower of cost basis or fair market value — the founder gets back what they rolled, but loses all the upside. Even "good leaver" termination calls are often at FMV determined by the sponsor's IC, not by an independent appraiser.

Why it kills: combined with the re-vesting trap (Pitfall 1), the call option means the sponsor has a tool to push the founder out at month 18 AND buy back the rolled equity at a sponsor-controlled valuation.

The fix: negotiate (a) call-option carveout for rolled equity (only newly-granted incentive equity is subject to call); (b) call price for ALL termination categories at independent FMV (third-party 409A appraiser, not sponsor); (c) "no-call" period of 24-36 months post-close during which the call is unavailable except for narrowly-defined for-cause termination (fraud, gross negligence, material breach).

My read on call options: read them like a gun pointed at your head. They are how PE sponsors renegotiate equity downstream. Fight for the carveout at LOI stage, not at signing.

Recent 2024-2026 deals with disclosed rollover

Public rollover disclosure is rare in LMM deals — almost all of them are private, with no SEC filing requirement. The publicly disclosed cases are typically take-privates, where SEC schedules disclose the consideration structure.

TPG/Corpay → AvidXchange take-private (FY2025): the most-quoted recent rollover case. Public reporting on the take-private (FY2025 SC 13E-3 filings on SEC EDGAR) indicates CEO Michael Praeger rolled the majority of his equity, with other senior executives rolling material portions; management rollover represents a high-single-digit percentage of total sources of funds. The case is structurally instructive because it shows the upper bound of management rollover at a public-company take-private — when the alignment ask matters most and the executive team believes in the long-term thesis.

Linden Law Partners — anonymized but disclosed LMM case studies:

- Case 1: $45M total deal, 10% rollover ($4.5M reinvested at close). Four years later, exit at higher multiple → rollover position worth $14.4M. Return: 3.2x MOIC on rolled equity.

- Case 2: $50M deal, $7M rollover (14%). Industry benchmark target: 3x+ MOIC on rolled equity.

These cases anchor the realistic-outcome range for LMM rollovers: 3-5x MOIC on rolled equity at PE platform exits is achievable but not guaranteed. The right-tail outcomes (5x+) require sponsor execution that delivers EBITDA growth, multiple expansion, and/or successful add-on M&A.

Other named deals with public rollover disclosure (2024-2026): historical precedents like L Catterton + Financiere Agache's ~$4.3B Birkenstock acquisition (February 2021), with management rollover reflected in the Birkenstock 2023 IPO S-1 disclosure; BDT Capital's 2016 Krispy Kreme acquisition with subsequent 2021 IPO 2nd-bite mechanics; and Thoma Bravo's various platform deals where management rollover terms surface in portfolio-level S-1 disclosures.

The honest framing: most rollover-structured deals are private and never disclosed. The Linden Law case studies anchor the range; the AvidXchange filing anchors the upper bound; and the prevalence data from SRS Acquiom 2026 anchors the population-level frequency.

The Founder Protective Provisions Checklist (counsel ask list)

The 13-row checklist of protective provisions worth fighting for at LOI stage:

| Issue | Standard buyer position | Founder should negotiate to |

|---|---|---|

| Re-vesting on rolled equity | 4-yr cliff or ratable on 100% of rolled | 0% re-vesting on rolled portion; new MPI may vest separately |

| Drag-along | Sponsor majority drags founder | Drag floor: only above 2x sponsor MOIC OR 3-yr minimum hold |

| Tag-along | De minimis carveout exempts under 10% sponsor sales | Tag on ALL sponsor sales above 5% (no carveout) |

| Information rights | Annual audited + K-1 only | Monthly fin pack + board observer minimum; board seat if rollover ≥25% |

| QSBS preservation | "Standard structure, talk to your tax counsel" | Corporate HoldCo OR cash-out QSBS-eligible portion at close |

| MPI dilution | 12-15% MPI pool fully dilutive | Carveout founder from MPI dilution OR include founder in MPI pool |

| Disguised-sale | No mention in operating agreement | Express 24-month distribution moratorium for rolled-in member |

| Pre-emptive rights | Pro-rata, exercise within 30 days | Pro-rata + sponsor-facilitated credit if founder can't fund |

| Transfer restrictions | Sponsor consent required, ROFR at HoldCo | Carveout for estate-planning transfers; ROFR only for outside sales |

| Exit timing control | Sponsor unilateral | Minimum 3-yr HoldCo hold before drag triggers |

| Conversion mechanics (if preferred) | 1x non-participating + 5-7% accruing | 1x non-participating, NO accrual, cap participation at 2x |

| Earn-out / 2nd-bite catch-up | None — straight pro-rata | Earn-out for founder if 2nd-bite below sponsor's target MOIC |

| Call option on termination | Sponsor calls at lower of cost or FMV | Call only on narrowly-defined for-cause; FMV at independent 409A; no-call 2-3 yrs |

Three of these are non-negotiable in my view: rolled equity fully vested at close (no re-vesting), call-option carveout for rolled equity, and express 24-month distribution moratorium under § 707(a)(2)(B). The first two protect against sponsor-driven equity claw-back. The third protects against IRS disguised-sale recharacterization. Counsel should walk away from any deal where the buyer refuses all three.

How does rolled equity interact with the data room and disclosure schedule?

Rolled-equity deals create a structurally different VDR workload than all-cash deals. The seller's tax counsel, the buyer's tax counsel, and the seller's M&A counsel all need to coordinate around the rollover-specific documents — unit purchase agreements, LLC operating agreements, MPI pool documents, retention agreements, vesting schedules, drag-tag provisions, info-rights provisions, and the tax-structure memos that justify § 721 or § 351 treatment. These artifacts typically live in a restricted-access folder of the virtual data room with workstream-by-workstream visitor permissioning — tax counsel for both sides in one tier, M&A counsel in another, deal-team principals in a third.

The audit trail becomes structurally important for rollover deals because: (1) post-close indemnification claims around § 721 disguised-sale exposure can surface 12-24 months after close, and the audit trail establishes which parties saw which documents during DD; (2) QSBS-preservation conversations during DD become evidentiary if the founder later challenges the rollover structure; (3) MPI pool documents and waterfall modeling form the basis of any later founder-vs-sponsor dispute about dilution. The Peony visitor groups mechanic — separate tiers for tax counsel, M&A counsel, deal-team, and sponsor-side principals — supports this multi-counsel coordination cleanly.

Where Peony fits: sub-$500M EV M&A and founder-led sales where the rollover-specific drafting and tax-structure work needs to live in a tightly permissioned room. Above $500M EV, Datasite and Intralinks typically have more institutional integrations with law firms and tax-advisory shops. The substrate is the same regardless; the institutional workflow integration is the differentiator at the large-cap end.

Bottom line

Roll equity is the slice of the sale you take in HoldCo units rather than cash. The math is a right-tail bet — at 3x exit with realistic dilution, rollover beats all-cash by just 6%; at 8x, by 94%; at 12x, by 167%. Most of the rollover advantage lives in the right tail of the exit-multiple distribution, and the realistic case (30% post-MPI ownership, 20% midcycle dilution) is what founders should model — not the buyer's pitched 45% case.

The four tax-deferred reorganization paths each fit a specific situation: § 721 partnership rollover for PE-LMM (with seven failure modes including the 24-month disguised-sale window); § 351 corporate-buyer rollover when QSBS preservation matters; § 368(a)(1)(F) F-reorganization for S-corp pre-sale structure; and § 1042 ESOP path for full-liquidity-plus-deferral via QRP plus estate planning.

The single most-missed pitfall of 2026: rolling QSBS-eligible C-corp stock into the standard PE LLC HoldCo under § 721 destroys the QSBS character, costing the founder $2.4M+ on $10M of pre-OBBBA gain. This requires a tax adviser explicitly paid to model the tradeoff at LOI stage, not at signing.

Eleven quantified founder pitfalls — re-vesting, drag without floor, tag asymmetry, info rights stripped, QSBS loss, MPI dilution ($41M at 8x exit), disguised-sale window, pre-emptive rights, charter transfer restrictions, exit timing control, and call options. Each has a protective drafting position. Three are non-negotiable: rolled equity fully vested at close, call-option carveout for rolled equity, and an express 24-month distribution moratorium.

The two operating rules I would push every founder to lock in at LOI signing: never sign a deal where any portion of the rolled equity is subject to re-vesting (you are rolling equity you already owned); and if you have C-corp QSBS held 5+ years, hire your own tax adviser to model the QSBS-vs-rollover tradeoff before agreeing to the rollover structure (not your buyer's tax counsel — yours).

The rollover is alignment when drafted right. It is structured equity claw-back when drafted wrong. The mechanics live in the operating agreement, not the LOI. Read every page before signing.

Related resources

- How to Structure an Earnout in an M&A Sale: 2026 Playbook — the parallel ship on earn-outs, the other primary deferred-consideration mechanism

- Independent Sponsor LOI Playbook — IS rollover ranges and LOI mechanics where rollover is most aggressive

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — the canonical DD process guide

- Private Equity Due Diligence — PE-specific diligence and rollover-structure mechanics

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including rollover-structure modeling

- M&A Data Room: Setup and Workstream Mapping — the data-room setup playbook including rollover-specific artifacts

- Due Diligence Timeline — the 6-workstream critical-path map for closing

- Hard vs Soft Due Diligence: 5-Frame Playbook — the broader DD scoping framework

- Tax Due Diligence Checklist — tax-DD scope that intersects with rollover-structure analysis

- Due Diligence Cost Breakdown — DD fees including tax-and-legal work for rollover-structured deals

- Best M&A Advisors in Minneapolis — Twin Cities medtech, healthcare, and AgTech advisors with strategic-bolt-on and PE-rollover experience

- Best M&A Advisors in NYC — NYC bankers and advisors who specialize in rollover-heavy LMM deals

- Best M&A Advisors in Atlanta — Southeast LMM advisors with rollover-deal experience

- Best M&A Advisors in Dallas — Texas LMM advisors covering rollover-structure deals

- Best M&A Advisors in Charlotte — Southeast advisors with healthcare, financial services, and industrials rollover deal history

- Best M&A Advisors in Miami — Latin American cross-border and Florida LMM rollover advisory

Footnotes and sources

- IRC § 351 (Transfer to Controlled Corporation). https://www.law.cornell.edu/uscode/text/26/351

- IRC § 368 (Definitions Relating to Corporate Reorganizations). https://www.law.cornell.edu/uscode/text/26/368

- IRC § 721 (Contribution to Partnership). https://www.law.cornell.edu/uscode/text/26/721

- IRC § 707 (Transactions Between Partner and Partnership). https://www.law.cornell.edu/uscode/text/26/707

- IRC § 1042 (Sales of Stock to ESOPs). https://www.law.cornell.edu/uscode/text/26/1042

- IRC § 1202 (Partial Exclusion for Gain From Certain Small Business Stock). https://www.law.cornell.edu/uscode/text/26/1202

- Treas. Reg. § 1.368-2(m) (F-Reorganization Test). https://www.law.cornell.edu/cfr/text/26/1.368-2

- Treas. Reg. § 1.707-3 (Disguised Sales). https://www.law.cornell.edu/cfr/text/26/1.707-3

- Rev. Rul. 2008-18 (F-Reorganization for S-Corp). https://www.irs.gov/pub/irs-drop/rr-08-18.pdf

- One Big Beautiful Bill Act, Pub. L. 119-21, July 4 2025. https://www.congress.gov/bill/119th-congress/house-bill/1

- SRS Acquiom. 2026 M&A Deal Terms Study (2,300+ deals, $569B). https://www.srsacquiom.com/our-insights/deal-terms-study/

- WilmerHale. Section 1202 white paper (April 2025).

- Holland & Knight. Transfers of Section 1202 Qualified Small Business Stock (July 2025).

- McLane Middleton. OBBBA changes to QSBS (2025).

- The Tax Adviser. Section 1202 and OBBBA (November 2025, December 2025).

- Cordasco & Company. Section 721: The Tax-Deferred Powerhouse (April 1, 2026).

- Linden Law Partners. Understanding Rollover Equity (multi-year article series). https://www.lindenlawpartners.com/

- Auxo Capital Advisors. LMM rollover guide.

- Lippes Mathias. Independent sponsor rollover analysis.

- Sadis & Goldberg. Independent sponsor rollover analysis.

- Calfee. Call options in equityholder agreements (2025).

- BDO. F-Reorganization analysis (September 2020, still operative 2026).

- Alston & Bird. Federal Tax Advisory: Equity Rollovers (March 2023).

- Dykema. Rollover Equity Conundrum in Transactions With Private Equity Funds (December 2024).

- Williams Mullen. Tax-Free Rollovers in Private M&A Transactions.

- Stradley Ronon. § 351 boot recognition analysis.

- AvidXchange. SC 13E-3 take-private filing (FY2025). https://www.sec.gov/cgi-bin/browse-edgar

- GF Data. Middle-market PE benchmarks (subscription). https://gfdata.com

- Bain & Company. Looking Back at M&A in 2025: Behind the Great Rebound (2026). https://www.bain.com/insights/looking-back-m-and-a-report-2026/

- DueDilio. Quality of Earnings Analysis Guide 2025. https://www.duedilio.com/quality-of-earnings-analysis-guide-2025/

You might also like

May 21, 2026

How to Structure an Earnout in an M&A Sale: 2026 Founder Playbook for the 28% That End in Dispute

Jul 5, 2026

8 Best M&A Advisors in Baltimore for $5M-$300M Deals (2026)

Jul 4, 2026

8 Best M&A Advisors in Kansas City for $5M-$300M Deals (2026)