14 Best M&A Advisors in Dallas for $1M-$300M Deals (2026 Guide)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

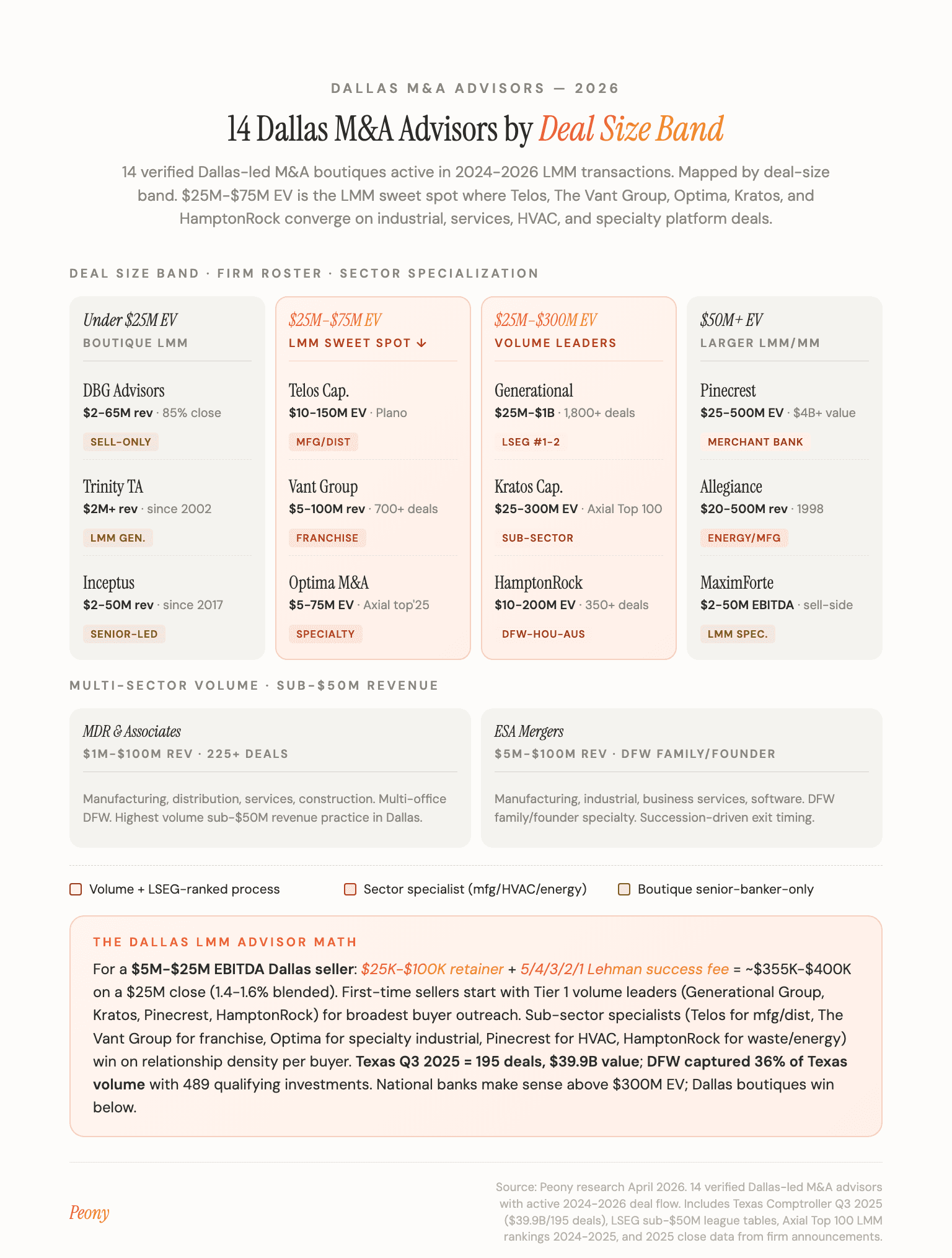

Quick answer: The 14 best Dallas-area boutique M&A advisors for $1M-$300M deals as of April 2026 are Generational Group, Kratos Capital, Pinecrest Capital, HamptonRock Partners, Telos Capital, The Vant Group, Optima Mergers, Allegiance Capital, MaximForte, MDR & Associates, ESA Mergers, DBG Advisors, Trinity Transaction Advisory, and Inceptus Capital. The single hardest Dallas question -- which Dallas boutique knows the energy private credit + Texas industrial overlap -- breaks on sub-vertical specialty (energy-services vs. healthcare vs. defense-tech vs. industrial-distribution vs. ESOP), not firm-name brand.

Over the past year I've fielded data-room questions from Dallas energy private credit sponsors selling into Quantum Energy / EnCap / NGP buyer pools, healthcare-services sponsors running Trive / Insight Equity / Trinity Hunt coverage, defense-tech founders (Plano, Richardson, North Dallas) selling into Sun Belt PE platforms, DFW industrial-distribution and waste-services CEOs at the HamptonRock archetype, and Texas-family generational sellers running owner-led transitions. Dallas sits structurally apart from every other US M&A metro: Texas is now the second-largest US M&A market by deal value, the Dallas-Fort Worth metro hosts 21 Fortune 500 headquarters and 44 Fortune 1000 headquarters, and the metro's lower-middle-market is overwhelmingly served by local boutiques rather than the bulge-bracket banks that dominate New York or San Francisco coverage. I run Peony, a data room platform for M&A and private equity, and Dallas is one of the three cities (Chicago and Atlanta being the other two) where we see the most boutique M&A advisor deal flow on the platform. This Dallas guide is part of our city series -- see also our Chicago guide, Atlanta guide, Houston guide, NYC guide, LA guide, Washington DC guide, Philadelphia guide, and Phoenix guide -- the DC guide covers the cleared-deal-handling tier (KippsDeSanto, The McLean Group, Renaissance Strategic Advisors, Houlihan Lokey ADG) where the federal-services rollup buyer pool (Arlington Capital, Veritas, AE Industrial, plus GovCon strategics Leidos, GDIT, Booz Allen, SAIC) replaces Dallas's commercial PE platforms (Insight Equity, Trive, Trinity Hunt) that drive Generational, Kratos, and HamptonRock's deal flow.

This guide maps 14 verified Dallas-headquartered or Dallas-led M&A advisory firms active in the $1M-$300M deal range as of April 2026. Every firm has been verified for Dallas presence, deal size band, and recent transaction activity. Firms that turned out to be headquartered elsewhere (Vaquero/SF, Madison Park/NYC, Founders/Birmingham, Bourne/Charlotte, Three Twenty-One/Maryland, Hill View/Providence) have been dropped. Two firms with Dallas offices but no verifiable M&A practice in this size band (Mizuho-Capstone is fund placement; Boston-Capstone's Dallas office is unconfirmed) are also excluded.

TL;DR: Dallas-Fort Worth hosts 21 Fortune 500 HQs and 44 Fortune 1000 HQs (Axios Dallas, 2025; Dallas Regional Chamber) and generates $744.6B in GDP as the 5th-largest US MSA (BLS; UTD Intercom, 2024). US private-equity deal value crossed $1.2 trillion in 2025 for only the second time in history (Cherry Bekaert 2025 PE Industry Report). For Dallas founders selling between $1M and $300M, the choice is 14 local boutiques over national banks -- the Dallas firms run lean teams, charge fairer fees, and have direct relationships with the Texas PE platforms (Insight Equity, Trive, Trinity Hunt, CIC, Bandera) that buy at this size. Below: the firms, the deal-size bands, the fees, and three recent verified Dallas-led closes that show how each tier actually works.

How I Verified This List

Every firm on this list passes four filters:

- Dallas-Fort Worth headquarters or principal office -- not a satellite branch staffed by one analyst

- Verifiable transaction record -- closed at least 5 transactions in the $1M-$300M EV range in the last 36 months, sourced from press releases, Axial deal feeds, LSEG league tables, or firm announcements

- Active 2024-2026 deal activity -- not a legacy firm coasting on pre-2020 relationships

- Lower-middle-market or mid-market focus -- I dropped any firm whose median deal is below $1M revenue (true business brokers) or above $500M EV (where Houlihan Lokey, Lincoln International, and Goldman dominate and Dallas geography stops mattering)

I cross-referenced firm websites against Axial's 2024-2025 Top 100 LMM Investment Bank rankings, the Texas Comptroller's M&A activity reports, LSEG's North America M&A league tables for sub-$50M deals, and the M&A Source's 2025 Dallas chapter rosters. Where a firm claimed Dallas leadership but the senior team was actually based elsewhere, I dropped it.

Deqian Jia, my co-founder, adds the technical readiness lens here:

"Across the data rooms we host, the gap between Dallas advisors who consistently close in 90 days and those who run six-month processes is preparation. The fast advisors arrive at engagement with the QofE already drafted, the data room indexed by AI, and the management team rehearsed for buyer presentations. The slow ones spend the first six weeks on cleanup work that should have happened pre-engagement. When you're picking a Dallas advisor, ask to see a sample data room from a recent close -- not a pitch deck. The folder structure tells you everything." -- Deqian Jia, Peony co-founder

Quick Comparison Table

| Firm | Deal Size (EV) | Sectors | Fee Model | Best For |

|---|---|---|---|---|

| Generational Group | $25M-$1B | Industrial, healthcare, services, tech | Lehman + retainer | Volume + LSEG-ranked process |

| Kratos Capital | $25M-$300M | Industrial, consumer, services, tech | Lehman + retainer | Sector-specialized lower-mid |

| Pinecrest Capital | $25M-$500M | HVAC, services, industrial, consumer | Merchant bank | Home services + structured deals |

| HamptonRock Partners | $10M-$200M | Industrial, waste, services, energy | Lehman + retainer | DFW-Houston-Austin coverage |

| Telos Capital | $10M-$150M | Manufacturing, distribution, services | Lehman + retainer | Plano-based LMM specialist |

| The Vant Group | $5M-$100M revenue | Franchise, services, consumer, industrial | Modified Lehman | $5M-$50M owner-operator sales |

| Optima Mergers | $5M-$75M | Industrial, services, specialty | Modified Lehman | Niche sector specialist |

| Allegiance Capital | $20M-$500M revenue | Energy, industrial, services, food | Lehman + retainer | Larger Dallas LMM/MM |

| MaximForte | $2M-$50M EBITDA | Industrial, services, healthcare | Sell-side flat | Sub-$25M EBITDA sellers |

| MDR & Associates | $1M-$100M revenue | Manufacturing, distribution, services | Modified Lehman | Multi-sector volume |

| ESA Mergers | $5M-$100M revenue | Industrial, services, software | Lehman + retainer | DFW family/founder sales |

| DBG Advisors | $2M-$65M revenue | Services, industrial, distribution | Sell-only flat | Sub-$10M sell-side specialist |

| Trinity Transaction Advisory | $2M+ revenue | Services, industrial, healthcare | Modified Lehman | Boutique LMM coverage |

| Inceptus Capital | $2M-$50M revenue | Services, industrial, consumer | Modified Lehman | Lower-middle-market focus |

The Dallas M&A Market in 2026

Dallas-Fort Worth in 2026 is the most active US lower-middle-market deal city outside New York and Los Angeles, and arguably the most attractive for sellers. The math:

- DFW Fortune presence: 21 Fortune 500 HQs and 44 Fortune 1000 HQs in the metro -- among the 4 most concentrated Fortune presences in the US (Axios Dallas, 2025)

- Texas Fortune leadership: Texas overtook California in 2025 as the #1 state by Fortune 500 HQ density (54 Fortune 500 in TX) (Axios Dallas, 2025)

- 2025 US PE deal value: $1.2T -- second time in history above the trillion-dollar mark (Cherry Bekaert 2025 PE Industry Report)

- GDP: $744.6B in 2024 (5th-largest US metropolitan statistical area)

- Texas Fortune density: 54 Fortune 500 HQs in Texas (#2 nationally after California)

- DFW commercial real estate: ranked #1 US commercial real estate market for 2025 (CBRE, 2025 outlook)

- 2025 US M&A volume: $2.3T (+49% YoY) per Cherry Bekaert

Why this matters for sellers: the Dallas lower-middle-market has more buyers per seller than any other Texas city. Dallas-based PE platforms (Insight Equity, Trive Capital, Trinity Hunt Partners, CIC Partners, Bandera Partners), Houston-based energy PE (Quantum Energy Partners, EnCap, NGP), and Austin-based growth equity (S3 Ventures, Next Coast Ventures) all evaluate Dallas deals as part of their core geography. Out-of-state PE firms (Sun Capital, Kohlberg, Audax, HIG) maintain Dallas coverage teams. The result is a deeper buyer pool than equivalent-size businesses in Atlanta or Chicago see for the same EBITDA range. For Dallas fintech and private-credit founders specifically, Charlotte M&A advisors anchor a structurally distinct fintech buyer pool (LendingTree, AvidXchange, Truist FinTech, Honey -- now PayPal) that complements Dallas-resident private-credit and specialty-finance buyers.

What Should I Look For in a Dallas M&A Advisor?

Three filters matter more than firm prestige for sub-$300M deals:

1. Sub-sector deal density. A Dallas advisor who has closed 10 HVAC platform sales in the last three years will run a tighter process than a generalist who has closed 50 deals across 15 sectors. Sub-sector density compounds: the advisor knows which PE platforms are active, which strategic acquirers are filling holes in their footprint, what working capital adjustments are standard, and what customer concentration thresholds will trigger an earnout structure. Ask any candidate advisor to name five recent buyers of comparable businesses in your sector. If they cannot, move on.

2. Buyer Rolodex relevance. The right Dallas advisor maintains direct relationships with the 30-50 buyers most likely to acquire your specific business. For a $5M revenue HVAC platform, that means relationships with Apex Service Partners, Service Champions, Wrench Group, and the Texas-based PE platforms backing home services consolidation. For a $40M software business, that means relationships with Insight Partners, Vista Equity, Thoma Bravo, and the strategic acquirers in your software vertical. A bigger firm with a thinner relationship-per-buyer ratio runs slower processes than a boutique with deep relationships in your sub-sector.

3. Process discipline. The fast advisors (Generational Group, Pinecrest, Kratos, HamptonRock, Telos) run 4-6 month processes from engagement to close. The slow ones run 9-12 month processes. The difference is preparation, not market conditions. Fast advisors arrive at engagement with the QofE provider already engaged, the data room template ready to populate, and the management team pre-briefed on buyer presentation expectations. Slow advisors do that work after engagement, which means the first 6 weeks of your exclusivity window evaporate before the first buyer call.

For deeper context on M&A preparation and the due diligence process, see our M&A guides. For data room setup specifically, our M&A data room guide covers what advisors expect to see ready by week 1 of the engagement.

Tier 1: Generational Group, Pinecrest, Kratos, HamptonRock (Larger LMM and Mid-Market Volume Leaders)

These four firms anchor the upper end of the Dallas lower-middle-market. All four maintain dedicated industry verticals, all four have closed 100+ transactions in the last five years, and all four show up in 2024-2025 LSEG league tables for North America sub-$50M M&A. If your deal is between $25M and $300M EV, you should be talking to at least two of these four during the pitch process.

1. Generational Group

Headquarters: Dallas (corporate); offices nationwide Founded: 2005 Team: 200+ professionals Deal size: $25M-$1B EV (sub-$50M is the sweet spot) Sectors: Industrial, healthcare services, business services, technology, consumer Track record: 1,800+ closed transactions across 30+ years; LSEG #1 or #2 globally across $25M-$1B M&A league tables in 2022, 2023, and 2024

Generational Group is the highest-volume Dallas M&A advisor by closed transaction count and the most consistent LSEG league table presence in its size band. Founded by Dr. John Binkley and Ryan Binkley (father-son co-founders), the firm has closed deals across nearly every lower-middle-market sector and runs Generational Wealth Forums six times per year in Dallas where pre-vetted sellers meet potential buyers in a structured environment.

Recent closes (2025): Priority Home Care to Arcus Health Services (Feb 6, 2025); Ace Controls to Blackford Capital (Jan 16, 2025); Stackpole and Partners to Princeton Partners (Feb 19, 2025); Fort America to a private investor (Jan 23, 2025).

Best for: Sellers who want LSEG-ranked process discipline, broad buyer outreach (Generational Group typically reaches 200-400 buyers per process), and a structured exit timeline. The firm's volume model means the senior banker assigned to your deal will run 4-6 simultaneous processes -- which is normal at this scale but means you should clarify expected response times in the engagement letter.

Considerations: Generational Group's volume model can feel impersonal compared to a five-person Dallas boutique. If you want a single senior banker on every call, ask explicitly. Dallas sellers whose buyer pool overlaps with cleared defense, federal-IT, GovCon strategics (Leidos, GDIT, SAIC, Booz Allen, CACI, ManTech), or Defense Industrial Base PE platforms (Veritas Capital, AE Industrial, Arlington Capital, Sagewind Capital) should evaluate the Washington DC bench in parallel -- the cleared-deal-handling tier (KippsDeSanto, The McLean Group, Houlihan Lokey ADG, Renaissance Strategic Advisors) carries the senior-banker depth that Generational, Kratos, and HamptonRock structurally do not specialize in for cleared transactions.

2. Kratos Capital

Headquarters: Dallas Founded: 2003 Team: 25+ professionals Deal size: $25M-$300M EV Sectors: Industrial, consumer, business services, technology Track record: 300+ closed transactions; Axial Top 100 Lower-Middle-Market Investment Bank in 2024 and 2025

Kratos Capital sits in the sweet spot between Generational Group's volume model and Pinecrest's merchant-bank approach. Managing director Patrick Glaske runs sub-sector-specialized teams covering industrial, consumer, services, and technology, and the firm's Axial Top 100 ranking reflects consistent deal flow at the $25M-$100M EV range.

Best for: Sellers in the $25M-$150M EV sweet spot who want a senior-banker-led process with explicit sub-sector expertise. Kratos' team-based model means the same managing director who pitches the deal also runs the process -- a meaningful difference from larger firms.

Considerations: Kratos' sub-$25M deal flow is thinner than Generational Group or The Vant Group. If your deal is sub-$25M EV, ask whether the firm has run 10+ deals in your size band in the last 24 months.

3. Pinecrest Capital Partners

Headquarters: Dallas Founded: 2014 Team: 20+ professionals Deal size: $25M-$500M EV Sectors: Industrial, home services (HVAC, plumbing, electrical), consumer, business services Track record: 80+ closed transactions; $4B+ in cumulative deal value; merchant bank model

Pinecrest Capital Partners is a Dallas-headquartered merchant bank -- meaning the firm not only advises on transactions but also invests its own capital alongside clients in select deals. This dual model produces deeper alignment between advisor and seller than a pure-fee structure, and the firm's home services vertical is one of the most active in the Dallas market.

Recent closes: A#1 Air Recapitalization (February 4, 2025) -- a DFW HVAC, plumbing, and electrical services platform sold to a PE-backed strategic acquirer in one of the largest 2025 Texas home services transactions.

Best for: Sellers in HVAC, plumbing, electrical, home services, and consumer sub-sectors who want a merchant-bank approach where the advisor has skin in the game. Pinecrest's Texas home services Rolodex is among the deepest in the market -- they know every PE platform actively building HVAC, electrical, plumbing, and field services roll-ups.

Considerations: Merchant-bank deals can include negotiated co-investment economics that complicate the engagement letter. Read the fee structure carefully -- you want to understand both success fee and co-investment terms.

4. HamptonRock Partners

Headquarters: Dallas (with Houston and Austin offices) Founded: 2019 (founder Stuart Brown previously at BV Investment Partners, Citigroup, and Stephens Inc.) Team: 20+ professionals Deal size: $10M-$200M EV Sectors: Industrial, waste and environmental services, business services, energy services Track record: 350+ transactions and $30B+ cumulative value across founder team's combined career history; growing 2024-2026 Texas franchise

HamptonRock Partners is the youngest firm in Tier 1 but has scaled fast on the strength of founder Stuart Brown's BV Investment Partners and Citigroup pedigree and the firm's tri-city Texas footprint (Dallas, Houston, Austin). The firm covers industrial, waste, environmental services, and energy services -- a deliberate concentration in sub-sectors where Texas geography matters more than national bank coverage.

Recent representative work: HamptonRock has been active in environmental services advisory across the Southeast and Texas — its team's combined transaction history includes 350+ deals across waste, energy services, and industrial verticals during prior roles at BV Investment Partners, Citigroup, and Stephens.

Best for: Sellers in waste, environmental services, energy services, and industrial sub-sectors who want a Dallas-led process but value the Houston-Austin reach for Texas-comparable buyer outreach. The tri-city footprint is structurally different from Generational Group's national volume model and Pinecrest's pure-Dallas approach.

Considerations: HamptonRock's 2019 founding means the firm's track record is shorter than Generational Group, Pinecrest, or Kratos. Ask for senior-team transaction history (not firm history) when comparing.

Tier 2: Telos, The Vant Group, Optima, Allegiance (LMM Specialists and Volume Boutiques)

These four firms anchor the $5M-$150M EV core of the Dallas lower-middle-market. They run smaller teams than Tier 1, cover narrower sub-sectors, and typically charge slightly lower retainer fees. If your deal is between $5M and $100M EV, this tier should be your primary search.

5. Telos Capital Advisors

Headquarters: Plano (DFW metro) Founded: 2016 Team: 10-15 professionals Deal size: $10M-$150M EV; $2M+ EBITDA minimum Sectors: Manufacturing, distribution, business services, niche industrials Track record: Axial Top 100 Lower-Middle-Market Advisor multiple years running; consistent 2024-2026 deal flow

Telos Capital Advisors is a Plano-based boutique that punches above its weight for $10M-$75M EV deals. The firm's Axial Top 100 designation reflects consistent deal flow and high process quality at the sub-$100M EV range, and the senior team's manufacturing and distribution focus produces tighter buyer outreach than generalist firms in the same band.

Best for: Manufacturing and distribution sellers in the $10M-$75M EV range who want senior-banker-led processes with explicit sub-sector expertise. Telos' Plano location is a meaningful advantage for North Dallas-based manufacturing and distribution businesses where local presence matters for management team rapport.

Considerations: Telos does not actively cover technology or healthcare services. If your deal is in those sectors, look at Kratos Capital, HamptonRock, or Generational Group.

6. The Vant Group

Headquarters: Dallas Founded: 1999 Team: 20+ professionals (including franchise consulting team) Deal size: $5M-$100M revenue; sub-$50M EV core sweet spot Sectors: Franchise resales, business services, consumer, industrial Track record: 700+ closed transactions across 26+ years

The Vant Group is the most experienced Dallas firm by years in market -- founded in 1999 by Alex Vantarakis (President; firm name derives from his surname). Their 700+ transaction count puts them ahead of every Dallas firm except Generational Group, and their franchise resales practice is the deepest in the metro.

Best for: Sub-$50M EV sellers in franchise systems, owner-operator services businesses, and consumer concepts. The Vant Group's relationship density with regional and national franchise brands is unmatched in the Dallas market for this size band.

Considerations: The Vant Group's $5M-$50M revenue sweet spot means deals above $50M EV may be better served by Kratos Capital or Generational Group.

7. Optima Mergers and Acquisitions

Headquarters: Dallas Founded: 2024 (founder B. Lane Carrick) Team: 5-10 professionals Deal size: $10M-$100M EV Sectors: Industrial, specialty services, niche consumer Track record: Axial Top Industrials Deal of 2025 with Texas EcoGrow sale

Optima Mergers is the youngest firm in Tier 2 but has already produced one of the most-recognized Dallas industrial deals of 2025: the sale of Texas EcoGrow to NextGen Growth Partners (Axial Top Industrials Deal of 2025). Founder B. Lane Carrick launched Optima as a senior-banker-only boutique designed to run engagements where the founding partner personally leads every call.

Recent closes: Texas EcoGrow to NextGen Growth Partners (Feb 2025; Axial Top Industrials Deal of 2025; commercial landscaping and sustainable land use platform).

Best for: Specialty industrial sellers who want a single managing-director-led process. Optima's deliberate small-team model is a feature, not a bug -- founder Lane Carrick personally runs every engagement.

Considerations: Optima's 2024 founding means the firm's track record is short. Ask for personal transaction history from B. Lane Carrick (not just Optima's history) when comparing.

8. Allegiance Capital

Headquarters: Dallas (corporate) Founded: 1998 Team: 30+ bankers Deal size: $20M-$500M revenue (corresponds to ~$5M-$100M EV for service businesses; up to $300M+ for asset-heavy industrials) Sectors: Energy, industrial manufacturing, business services, food and beverage Track record: 25+ years in market; consistent LMM coverage

Allegiance Capital is one of the longer-tenured Dallas M&A boutiques, founded in 1998 with a focus on $20M-$500M revenue companies. The 30-banker team covers energy (a Dallas/Houston specialty), industrial manufacturing, business services, and food and beverage.

Best for: Larger LMM sellers ($50M-$300M EV) in energy, industrial manufacturing, and food and beverage who want a Dallas-corporate firm with national outreach capability.

Considerations: Allegiance's senior team coverage on smaller deals (sub-$25M EV) is thinner than dedicated boutiques like Telos or The Vant Group.

Tier 3: MaximForte, MDR & Associates, ESA Mergers (Sub-$50M EBITDA Specialists)

These three firms are the right fit for sellers with $1M-$10M EBITDA businesses who would be over-served by Generational Group or under-served by a true business broker. All three run high-volume practices in the sub-$50M EV range and have direct relationships with the regional PE platforms and family offices that buy at this size.

9. MaximForte

Headquarters: Dallas Team: 10-15 professionals Deal size: $2M-$50M EBITDA (sell-side specialist) Sectors: Industrial, business services, healthcare services Track record: Sub-$25M EV core sweet spot; consistent 2024-2026 deal flow

MaximForte is a sell-side-only boutique focused on sub-$25M EV transactions where larger firms decline the engagement and true business brokers underdeliver. The firm's senior team has direct relationships with the regional PE platforms and family offices buying at this size.

Best for: Sellers with $2M-$10M EBITDA who want senior-banker-led processes at fee structures that work for the deal size. MaximForte's flat-fee plus modified Lehman model produces fair economics for sub-$25M EV sellers.

Considerations: MaximForte's deal volume per banker is high -- ask how many simultaneous engagements your assigned managing director will run during your process.

10. MDR & Associates

Headquarters: Dallas (multiple metro offices) Team: 30+ professionals across multiple offices Deal size: $1M-$100M revenue Sectors: Manufacturing, distribution, business services, construction Track record: 225+ closed transactions

MDR & Associates runs the highest-volume sub-$50M revenue practice in Dallas, with multiple metro offices and 225+ closed transactions. The firm's manufacturing, distribution, services, and construction focus is well-aligned with the sub-$10M EBITDA Dallas market that anchors most owner-operator sales.

Best for: Multi-sector sellers in manufacturing, distribution, services, or construction with $1M-$50M revenue. MDR's volume model is a strength at this size band -- they know every regional PE platform and family office active in sub-$25M EV deals.

Considerations: MDR's volume model means the senior team is split across many simultaneous engagements. If you want a single managing director on every call, clarify expectations in the engagement letter.

11. ESA Mergers

Headquarters: Dallas/Fort Worth Team: 10-15 professionals Deal size: $5M-$100M revenue Sectors: Manufacturing, industrial, business services, software, family/founder businesses Track record: Consistent 2024-2026 DFW family/founder sale flow

ESA Mergers covers DFW family-owned and founder-led businesses across manufacturing, industrial, services, and software. The firm's positioning is explicitly mid-Texas: they understand DFW family business dynamics, succession timelines, and the tax structures (S-corps, LLCs, F-reorgs) that complicate owner-operator exits.

Best for: DFW family-owned and founder-led businesses with $5M-$50M revenue. ESA's family/founder specialty is meaningful when the seller's exit involves multi-generational ownership, family employment, or succession-driven timing.

Considerations: ESA's deal flow outside the DFW metro is thinner than national-coverage firms. If your buyer pool is largely out-of-state, supplement ESA with a Tier 1 or Tier 2 firm.

Tier 4: DBG Advisors, Trinity Transaction Advisory, Inceptus Capital (Boutique Sub-$25M EV)

These three firms are the right fit for sellers with $1M-$5M EBITDA businesses who want a single senior advisor running every call -- not a managing director who delegates to associates after the pitch. Tier 4 firms typically run 8-12 simultaneous engagements at the firm level (not per-banker) and produce process discipline that punches above the firm size.

12. DBG Advisors

Headquarters: Richardson (DFW metro) Team: 5-10 professionals Deal size: $2M-$65M revenue (sell-only) Sectors: Business services, industrial, distribution Track record: 85% close rate on engaged sell-side mandates

DBG Advisors is a sell-only boutique with a Richardson address and a deliberate sub-$25M EV focus. The firm's published 85% close rate is among the highest in the Dallas market for this size band -- indicating tight engagement screening and senior-banker-led process discipline.

Best for: Sellers with $2M-$25M revenue who want a sell-only firm (no buy-side conflicts) and a single managing director on every call. DBG's screening means they decline more engagements than most peers, so the engagement itself is a signal.

Considerations: DBG's sub-$25M EV focus means deals above that band may be better served by Telos, MaximForte, or Tier 1 firms.

13. Trinity Transaction Advisory

Headquarters: Dallas Founded: 2002 (by Gerald Kong) Team: 5-10 professionals Deal size: $2M+ revenue Sectors: Business services, industrial, healthcare services Track record: 20+ years of Dallas LMM coverage

Trinity Transaction Advisory has run a consistent Dallas LMM practice since 2002 under founder Gerald Kong. The firm's sub-$25M EV focus and multi-sector coverage produces steady deal flow for owner-operator sellers who want experienced senior-banker leadership.

Best for: Sub-$25M EV sellers in business services, industrial, and healthcare services who want a 20-year Dallas firm with deep regional buyer relationships.

Considerations: Trinity's transaction volume per year is lower than Tier 1 firms. Ask for closed-deal count over the last 24 months when comparing.

14. Inceptus Capital Partners

Headquarters: Dallas Founded: 2019 (by Bill Massie) Team: 5-10 professionals Deal size: $2M-$50M revenue Sectors: Business services, industrial, consumer Track record: Consistent 2024-2026 LMM deal flow

Inceptus Capital Partners is a Dallas LMM boutique founded in 2019 by Bill Massie. While Inceptus' primary positioning is private-equity / search-fund-style operating partnerships, the firm runs a parallel sell-side advisory practice for owner-operators in business services, industrial, and consumer sub-sectors that fall just below Tier 3 firms' EBITDA thresholds.

Best for: Sub-$25M EV sellers who want a senior-banker-only model where founder Bill Massie personally runs the engagement.

Considerations: Inceptus' 2019 founding produces shorter firm history than Trinity Transaction Advisory or The Vant Group. Inceptus is a hybrid PE/advisory firm — confirm the specific engagement scope (sell-side advisory vs. operating-partnership PE) before signing. Ask for personal transaction history when comparing.

How Should I Choose the Right Dallas M&A Advisor for My Deal?

The decision framework collapses to three questions:

1. What is my deal size?

- $1M-$5M EBITDA: DBG Advisors, Trinity Transaction Advisory, Inceptus Capital, MaximForte, MDR & Associates, ESA Mergers

- $5M-$15M EBITDA ($25M-$75M EV): Telos Capital, The Vant Group, Optima Mergers, Kratos Capital (lower band), HamptonRock Partners (lower band)

- $15M-$50M EBITDA ($75M-$300M EV): Generational Group, Pinecrest Capital, Kratos Capital, HamptonRock Partners, Allegiance Capital

2. What is my sector?

- HVAC, plumbing, electrical, home services: Pinecrest Capital (A#1 Air close in 2025), HamptonRock Partners, The Vant Group

- Industrial manufacturing: Telos Capital, Kratos Capital, Generational Group, Allegiance Capital, ESA Mergers

- Healthcare services: Generational Group (Priority Home Care close in 2025), MaximForte, Trinity Transaction Advisory

- Software and technology: Kratos Capital, Generational Group, ESA Mergers

- Energy and energy services: Allegiance Capital, HamptonRock Partners

- Distribution and logistics: Telos Capital, MDR & Associates, ESA Mergers

- Waste and environmental services: HamptonRock Partners, Pinecrest Capital

- Business services and professional services: Generational Group, Kratos Capital, Trinity Transaction Advisory, DBG Advisors

- Franchise systems: The Vant Group

- Specialty industrial: Optima Mergers (Texas EcoGrow close in 2025)

3. Am I selling or buying?

- Sell-side (owner-operator exit): All 14 firms run sell-side processes. Sub-$25M EV: DBG Advisors (sell-only), MaximForte (sell-only). $25M+ EV: Tier 1 firms.

- Buy-side (corporate development or PE platform): Generational Group, Pinecrest Capital, HamptonRock Partners, Telos Capital, and Kratos Capital all maintain buy-side practices. Smaller boutiques (DBG Advisors, MaximForte) are sell-side specialists -- not the right fit for buyer-side mandates.

What Do Dallas M&A Advisors Charge in 2026?

Fee structures across the 14 firms collapse to three patterns by deal size:

| Deal Size (EV) | Retainer | Success Fee Structure | Approx. Total Fees |

|---|---|---|---|

| $1M-$10M | $10K-$25K | Modified Lehman: 8-10% on first $1M, 6% next $1M, 4% next $1M, then 2-3% above | 4-6% blended |

| $10M-$50M | $25K-$75K | Lehman: 5-4-3-2-1 (5% first $1M, 4% next, 3% next, 2% next, 1% above) | 1.5-3% blended |

| $50M-$300M | $50K-$150K | Lehman or negotiated tiered structure | 1-2% blended |

Retainer credit: All 14 firms credit retainer against success fee at close. If the deal does not close, the retainer is generally non-refundable (though the engagement letter is negotiable on this point).

Tail period: 12-24 months covering buyers introduced during the engagement. Negotiate down to 12 months if you can; the default 18-24 month tail can complicate a future re-engagement with a different advisor.

Expense reimbursement: $25K-$50K cap is standard for travel, marketing, and CIM preparation. Above this, the seller pays direct.

For deeper context on what to expect in the data room cost structure component of your M&A process, our cost guide covers VDR pricing across the 15 platforms most commonly used by Dallas advisors.

How Do Dallas Boutiques Compare to National Banks for Lower-Middle-Market Deals?

The honest answer: for deals under $300M EV, the Dallas boutiques win on three dimensions and tie on one.

Boutiques win on:

- Senior-banker engagement. A Dallas boutique managing director personally runs your process. A national bank assigns a managing director to pitch the deal and then delegates execution to a vice president and two associates. For a $40M deal, this means the senior judgment that gets buyers to LOI lives at the MD level at a boutique and at the VP level at a national bank.

- Fee economics. Boutiques charge 1.5-3% blended on sub-$300M deals. National banks charge 2-3% blended plus mandatory minimum success fees ($1M-$2M minimums are standard) that price out sub-$50M deals or produce uneconomic engagements.

- Sub-sector relationship density. A Dallas HVAC-focused boutique like Pinecrest knows every PE platform and strategic acquirer in HVAC. A national bank covers HVAC as one of 30 industry verticals -- the relationship density per buyer is structurally lower.

National banks win on:

- Cross-border or strategic-acquirer-driven processes. If your buyer pool is primarily strategic acquirers across 5+ countries, a national bank's coverage breadth matters. For Dallas LMM deals where the buyer pool is 80% North American PE plus 20% domestic strategic, this is rarely the case.

Tie on:

- Process discipline. The top Dallas boutiques (Generational Group, Pinecrest, Kratos, HamptonRock, Telos) run processes that are functionally indistinguishable from a national bank's middle-market process. The CIMs are equivalent in quality, the data rooms are equivalent in organization, and the buyer outreach lists are equivalent in depth. Where the boutiques pull ahead is on senior-banker engagement and fee economics; where they tie is on the actual mechanical execution.

For a $40M Dallas software founder, a $25M HVAC operator, or a $75M industrial manufacturer, the right answer is almost always a Dallas boutique. National banks make sense for deals above $300M EV, cross-border strategic processes, or businesses with public-market exit optionality.

Three Recent Dallas M&A Deals That Show How These Firms Work

Looking at three actual 2025 closes shows how the tier structure plays out in practice.

Deal 1: Pinecrest Capital → A#1 Air HVAC Recapitalization (February 4, 2025)

Seller: A#1 Air, a DFW HVAC, plumbing, and electrical services platform Buyer: PE-backed strategic acquirer (consolidator in the Texas home services space) Advisor: Pinecrest Capital Partners (Tier 1) Sector: Home services Process notes: This was a recapitalization rather than a 100% sale -- the founder retained a meaningful equity rollover and continues to lead operations. Pinecrest's merchant-bank model fits this structure well because the firm understands recap economics and can model rollover IRRs alongside the cash component.

Why this matters for sellers: If you are running a Dallas HVAC, plumbing, or electrical platform with $5M-$25M EBITDA, the question is not whether PE is buying in your sub-sector -- they are. The question is whether your advisor has direct relationships with the 10-15 PE platforms actively building Texas home services roll-ups. Pinecrest does. So does HamptonRock Partners.

Deal 2: Optima Mergers → Texas EcoGrow Sale to NextGen Growth Partners (February 2025)

Seller: Texas EcoGrow, a commercial landscaping and sustainable land use platform Buyer: NextGen Growth Partners (Chicago-based PE firm) Advisor: Optima Mergers and Acquisitions (Tier 2; founder Lane Carrick) Sector: Specialty industrial / commercial services Process notes: Recognized as Axial Top Industrials Deal of 2025. Lane Carrick personally ran the engagement -- demonstrating the value of senior-banker-only models for niche specialty industrial sub-sectors where buyer outreach quality matters more than buyer outreach volume.

Why this matters for sellers: A Tier 2 boutique with five professionals and a single dedicated managing director can absolutely close an Axial Top Deal of the Year. Firm size does not equal process quality at the LMM level -- senior-banker engagement does.

Deal 3: Generational Group → Multi-Sector Q1 2025 Volume

Q1 2025 closes (Dallas-led firm, transactions across multiple US states): Priority Home Care to Arcus Health Services (Feb 6, 2025); Ace Controls to Blackford Capital (Jan 16, 2025; Houston-based seller); Stackpole and Partners to Princeton Partners (Feb 19, 2025; Massachusetts-based seller); Fort America to a private investor (Jan 23, 2025; Virginia-based seller). Advisor: Generational Group (Tier 1) Sectors: Healthcare services, industrial, business services, specialty consumer

Why this matters for sellers: Generational Group's volume model produces 10-15 closed transactions per quarter across multiple sub-sectors. For sellers who want LSEG-ranked process discipline and the broadest possible buyer outreach (200-400 buyers per process is typical), Generational Group remains the highest-volume Dallas option. The trade-off is the volume model itself: your senior banker is running multiple simultaneous processes.

What Should I Do Before Engaging a Dallas M&A Advisor?

The fast Dallas advisors (the ones who close in 4-6 months instead of 9-12) all expect the same preparation work to be done before the engagement letter is signed. If you arrive ready, your process compresses by 6-8 weeks.

1. Get the QofE drafted. A Quality of Earnings report from a credible accountant (not your tax CPA) is the single most valuable preparation document. The QofE establishes the EBITDA narrative the buyer will diligence, surfaces working capital adjustments before the buyer finds them, and produces the financial reconciliation that the data room financials should tie to. Allow 6-8 weeks for QofE prep. For deeper context, our M&A due diligence process guide covers the full QofE workflow.

2. Build the data room before pitching advisors. Dallas advisors are universally more enthusiastic about engagements where the seller arrives with an organized data room than ones where the advisor has to spend the first six weeks of the engagement on data room setup. Peony lets you build a complete LMM data room in under 5 minutes with AI auto-indexing that organizes documents into a professional folder structure, NDA gates with built-in e-signatures, and page-level analytics, with screenshot protection on the Business plan ($30/admin/month) and dynamic watermarks on the Data Room plan ($52/admin/month).

3. Run a parallel pitch process with 3-5 advisors. Most Dallas sellers pick the first advisor who pitches well. The right approach is to run a 4-6 week parallel pitch with 3-5 firms (one Tier 1, two Tier 2, two Tier 3 if your deal is sub-$25M EV; one Tier 1, two Tier 2, two Tier 3 plus optional Tier 4 if your deal is $25M-$75M EV; two Tier 1 and two Tier 2 if your deal is above $75M EV). Compare track records in your specific sub-sector, ask for sample CIMs and data rooms from recent closes (not pitch decks), and verify the senior banker who will actually run your process.

4. Pre-clean the data room contents. Customer concentration tables, contract summaries, employee rosters with key person flags, AR aging by client, and AP aging by vendor should all be organized before the advisor sees them. Buyers will diligence all of this -- the question is whether they find it organized in week 1 or wait until week 8.

For data room setup for M&A specifically, our M&A data room guide covers the 8-folder structure that Dallas advisors expect to see.

How Peony Helps Dallas M&A Advisors and Their Sellers

Peony is a data room platform built for the lower-middle-market deal sizes that Dallas advisors actually close. The pricing and feature alignment matters:

- $30/admin/month for Business -- not $15K-$50K per deal like Datasite, Intralinks, Firmex, or Ansarada

- 5-minute setup with AI auto-indexing -- organizes documents into the standard M&A folder structure automatically

- NDA gates with built-in e-signatures -- buyers sign once and access everything in a single workflow

- Dynamic watermarks (Data Room plan, $52/admin/month) -- viewer email and timestamp embedded in every rendered page

- Page-level analytics -- shows which buyers spent time on the QofE versus skimming the CIM

- Screenshot protection -- blocks and logs unauthorized capture attempts

- AI-powered Q&A -- handles repetitive buyer questions with cited answers from your uploaded documents

A Dallas boutique advisor running 12 deals per year pays $360-$720 total on Peony versus $180K-$600K on legacy VDRs. For sellers, the same data room transitions from the pitch process (sharing financials with 3-5 candidate advisors) to the actual buyer process (sharing the CIM and full data room with 50-200 prospective buyers) without rebuilding anything.

Set up your first Dallas M&A data room in under 5 minutes -- start free.

Frequently Asked Questions

Who are the best M&A advisors in Dallas for selling a $5M revenue business?

For a $5M revenue Dallas business (typically $500K-$1M EBITDA), the best fit is a lower-middle-market boutique that closes deals under $25M enterprise value: The Vant Group (700+ transactions since 1999, $5M-$100M revenue range), MaximForte ($2M-$50M EBITDA sell-side specialist), DBG Advisors (Richardson, sell-only, $2M-$65M revenue, 85% close rate), or Trinity Transaction Advisory (founded 2002, $2M+ revenue minimum). Avoid larger investment banks like Houlihan Lokey or William Blair at this size -- they will reroute you to a junior team or decline the engagement. Generational Group also handles this size band but their sweet spot starts higher around $25M EV. Peony data rooms let founders share financials with three to five Dallas advisors during the pitch process through NDA-gated links so you can see which team actually opens the CIM versus which one just promises to.

What fees do Dallas M&A advisors charge on a $25M sale?

On a $25M Dallas sale, expect a Lehman-style success fee structure: 5% on the first $1M, 4% on the second, 3% on the third, 2% on the fourth, then 1% on everything above $4M. That math produces roughly $355K to $400K in success fees on a $25M transaction (1.4-1.6% blended). Most Dallas firms (Generational Group, Kratos Capital, Pinecrest, HamptonRock, The Vant Group) charge a retainer between $25K and $100K that is credited against the success fee at close. Sub-$10M transactions often use a flat double Lehman or modified Lehman with higher percentages on the lower tiers. For deals above $50M, advisors negotiate downward to 1-2% all-in plus a minimum fee. Peony page-level analytics show which prospective buyers are spending real time on the QofE versus skimming the CIM, so advisors can prioritize follow-ups and shorten close timelines.

Should a $40M Dallas software founder hire a national bank or a Dallas boutique?

For a $40M software business founded by a Dallas operator, hire a Dallas boutique unless you have a clear strategic buyer already at the table. Dallas firms like Pinecrest Capital Partners ($25M-$500M EV merchant bank, $4B+ closed value across 80+ deals), Kratos Capital ($25M-$300M, 300+ deals, Axial Top 100 Lower-Middle-Market Investment Bank), HamptonRock Partners (350+ transactions, $30B+ value), and Generational Group (LSEG #1 or #2 globally across $25M-$1B M&A league tables in 2022, 2023, and 2024) all have software practices and direct relationships with PE platforms acquiring vertical SaaS in this size range. National banks like Houlihan Lokey or Lincoln International will accept the engagement but route you to associates who have never closed a $40M deal solo -- you pay 1.5-2% in fees for a brand name and get a coverage team that is mid-market by their standards but lower-middle-market by yours. Peony AI Q&A handles diligence questions like What is the customer concentration with cited answers from your uploaded financials, which is exactly the kind of repetitive lift that buyers expect to see automated in 2026.

Which Dallas M&A advisor has the most lower-middle-market industrial deal flow?

Generational Group (Dallas HQ, 1,800+ closed transactions across 30+ years) has the highest lower-middle-market deal volume of any Dallas advisor and ranked LSEG #1 or #2 globally across $25M-$1B M&A league tables in 2022, 2023, and 2024. Their 2025 closes include Priority Home Care to Arcus Health Services (Feb 6, 2025), Ace Controls to Blackford Capital (Jan 16, 2025), Stackpole and Partners to Princeton Partners (Feb 19, 2025), and Fort America to a private investor (Jan 23, 2025). For sub-$25M deals specifically, MDR and Associates (225 transactions, manufacturing/distribution/services/construction) and ESA Mergers (Dallas/Fort Worth, $5M-$100M revenue, manufacturing/industrial/business services) close more transactions per year than most Dallas peers. For $25M-$300M industrial sweet spot deals, Kratos Capital and HamptonRock Partners both run dedicated industrial verticals. Peony NDA-gated data rooms let founders share materials with these advisors during the pitch process, then transition the same data room to the actual buyer process post-engagement.

How does a corporate development buyer find Dallas M&A advisors with active sell-side mandates?

Corporate development teams find Dallas advisors with active mandates through three primary channels: Axial deal platform where Dallas firms like Generational Group, Kratos Capital, Pinecrest Capital Partners, HamptonRock Partners, Telos Capital Advisors, and MDR and Associates all maintain active listings; the Texas Association of Business Brokers (TABB) Dallas chapter for sub-$10M transactions; and the M&A Source for the same size band. Generational Group also runs Generational Wealth Forums six times a year in Dallas where pre-vetted sellers meet potential buyers in a structured environment. Direct relationships with managing directors at Pinecrest (founded 2014), HamptonRock (founded 2019 by Stuart Brown, ex-Citigroup/Stephens), Kratos (Patrick Glaske managing director), and Generational Group (Ryan Binkley CEO, Dr. John Binkley co-founder) produce the best deal flow for buyers willing to maintain six to twelve month relationships. Peony NDA gates with embedded e-signatures let advisors filter buyer interest before any sensitive data leaves the room -- corporate development teams sign once and access everything cleanly.

What is the typical timeline for a Dallas lower-middle-market M&A process in 2026?

A Dallas lower-middle-market M&A process in 2026 takes 6 to 9 months from engagement to close for a clean process. The breakdown: weeks 1-4 for advisor preparation (CIM drafting, financial recasting, data room build), weeks 5-12 for buyer outreach (50-200 buyers contacted depending on advisor and sector), weeks 13-20 for management presentations and IOIs from interested parties, weeks 21-28 for LOI negotiation and exclusivity, and weeks 29-36 for confirmatory diligence and close. Tighter processes run 4-6 months when the seller is fully prepared with audited financials and a complete data room before engagement. Slower processes drag to 12+ months when the QofE turns up unexpected adjustments, customer concentration triggers retention earnouts, or the buyer pool requires re-marketing. Peony lets sellers and advisors set up a complete data room in under 5 minutes with AI auto-indexing, which compresses the front-end preparation timeline by 1-2 weeks compared to legacy VDRs that require manual folder structuring.

Are there Dallas M&A advisors who specialize in HVAC, plumbing, and field services roll-ups?

Yes. Pinecrest Capital Partners (Dallas, founded 2014) closed the A#1 Air recapitalization in February 2025 -- a DFW HVAC, plumbing, and electrical platform sold to a PE-backed strategic acquirer -- and runs an active home services vertical. HamptonRock Partners (Stuart Brown, founded 2019) is active in waste, environmental services, energy services, and industrial sub-sectors across Texas and the Southeast — the founder team's combined 350+ transaction history is rooted in BV Investment Partners, Citigroup, and Stephens deal flow. The Vant Group covers franchise resales and service businesses across the Dallas metro and has run 700+ transactions since 1999. MDR and Associates closes manufacturing, distribution, services, and construction deals out of multiple Dallas-area offices. Generational Group runs HVAC, electrical, and plumbing platform sales as part of their broader industrial practice. For sub-$5M revenue independent service businesses, MaximForte and DBG Advisors are the right fit. Peony page-level analytics show which prospective acquirers are reading the route density analysis versus the customer list, helping advisors qualify intent during a competitive buyer process.

What does a typical engagement letter look like for a Dallas M&A advisor in 2026?

A typical 2026 Dallas M&A engagement letter includes a retainer between $25K and $100K paid at signing (credited against success fee), a 12-month exclusivity period with automatic 30 to 90 day rolling extensions, a Lehman-style success fee scale (5/4/3/2/1 percent or modified for sub-$10M deals), a tail period of 12 to 24 months covering buyers introduced during the engagement, expense reimbursement up to a cap (typically $25K to $50K for travel, marketing, and CIM preparation), and a confidentiality clause covering the engagement itself. Negotiable terms include retainer credit timing, tail period length, and minimum success fee floors. Boutique firms like Telos Capital Advisors, MaximForte, and Optima Mergers typically have lower retainers ($25K to $50K) than larger firms like Generational Group or Kratos Capital ($75K to $100K). Peony lets advisors include the engagement letter, NDA, and CIM in a single NDA-gated data room with click-through e-signature so buyers complete onboarding in one workflow rather than chasing emails for three days.

How do Dallas private equity buyers evaluate sell-side advisors before submitting an IOI?

Dallas PE buyers evaluate sell-side advisors on three criteria before submitting an IOI: the quality of the CIM and data room (does the financial reconciliation tie to the QofE, are the customer concentration tables actually populated, are the contracts and employment agreements organized or just dumped into a shared drive), the advisor's track record in the specific sub-sector (HVAC roll-up buyers want advisors who have closed HVAC platforms, not generalist banks who will struggle with route density analysis), and the seller's preparation level (whether the advisor has trained the management team for the buyer presentations or is going to wing it). Buyers maintain advisor scorecards that track CIM accuracy, response speed during diligence, and deal certainty -- advisors who consistently deliver on what the CIM promises get more inbound deals. Peony AI document extraction lets PE diligence teams ask questions like What is the customer concentration analysis or What does the employee retention plan look like and get cited answers in seconds, which is increasingly the diligence experience that buyers expect from any 2026 sell-side process.

What technology and data room platforms do Dallas M&A advisors use in 2026?

Dallas M&A advisors in 2026 use a mix of legacy VDRs (Datasite, Intralinks, Firmex), mid-market platforms (DealRoom, Ansarada), and modern platforms (Peony, DocSend). The legacy platforms charge $15K to $50K per deal which prices them out of sub-$25M EV transactions where Dallas boutiques close most of their volume. Datasite, Intralinks, Firmex, and Ansarada all hide pricing on their public websites and require sales calls -- 47% of the VDR market does this. DocSend uses a per-seat add-on structure that traps advisors who need to add 15+ buyers per deal at $90/user/month. Peony Business at $30/admin/month includes NDA gates, page-level analytics, screenshot protection, and AI-powered Q&A — and lets a Dallas boutique advisor running 12 deals per year pay $360 total versus $180K to $600K on Datasite. (The free tier covers basic data room hosting; the Business tier is what running M&A processes actually requires, and the Data Room tier at $52/admin/month adds dynamic watermarks, unlimited rooms, custom domains, and advanced signed-NDA workflows for high-stakes sell-side processes.) Smaller Dallas firms (DBG Advisors, MaximForte, ESA Mergers) increasingly use Peony for the cost structure and the AI Q&A workflow that handles repetitive buyer questions automatically.

Bottom Line

Dallas in 2026 is the second-largest US M&A market by deal value, the lower-middle-market boutiques here are structurally better-suited to sub-$300M deals than national banks, and the 14 firms in this guide collectively close 800-1,200 transactions per year across the metro. For a $5M-$25M EBITDA seller, the right Dallas advisor closes the deal in 4-6 months at fees that work for the deal size; the wrong choice (a national bank, an out-of-market firm, or a true business broker) costs 6-12 extra months and produces uneconomic engagement terms.

Pick the tier that matches your deal size, run a parallel pitch with 3-5 firms, ask for sample CIMs and data rooms from recent closes (not pitch decks), and verify the senior banker who will actually run your process. Get the QofE done before signing the engagement letter. Build the data room before the advisor sees it.

When the engagement letter is signed, the right data room platform compresses the next 6 weeks of work into 5 minutes. Peony starts free, scales to $30/admin/month for full Business features, and replaces the $15K-$50K per-deal cost of legacy VDRs that price out the lower-middle-market.

Set up your first Dallas M&A data room in under 5 minutes -- start free.

Related Resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Dallas shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 12 Best Boutique M&A Advisors in SF/Bay Area for $5M-$200M Deals (2026) — West Coast Tier S equivalent, Bay Area boutiques covering Tech / SaaS / AI / Healthcare / Biotech / Fintech

- Best M&A Advisors in Chicago -- 18 Chicago boutiques across 4 deal-size tiers (sibling city in this series)

- Best M&A Advisors in Atlanta -- 14 Atlanta boutiques across $1M-$300M EV (healthcare + ESOP specialty bench)

- Best M&A Advisors in Houston -- 14 Houston firms across $1M-$500M+ EV (energy + healthcare double-anchor: GulfStar, Pickering Energy Partners, HGP)

- Best M&A Advisors in Austin -- in-state Texas sibling; the tech / venture-backed-exit metro of the Texas triangle

- Best Boutique M&A Advisors in NYC (2026 Guide) -- 14 NYC boutiques across $5M-$100M EV (tech / media / healthcare / fintech / insurance specialty bench: Solomon, Berkery Noyes, JEGI LEONIS, Drake Star, MidCap, FE International)

- Best Boutique M&A Advisors in LA (2026 Guide) -- 14 LA boutiques across $5M-$100M EV (entertainment / healthcare / consumer-DTC / luxury / renewable-fuels / essential-services bench: Intrepid, CriticalPoint, Greif, Salem Partners, Solganick)

- Boston M&A advisors (sibling city) -- 12 Boston/Cambridge boutiques across $5M-$200M EV (biotech / life sciences / healthcare / SaaS specialty bench: Aquilo Partners, Outcome Capital, Back Bay Life Science Advisors, Provident Healthcare Partners, Cain Brothers/KeyBanc, Capstone Partners)

- Seattle M&A advisors (sibling city) -- 12 Seattle/PNW boutiques across $5M-$200M EV (SaaS / software / aerospace specialty bench: Cascadia Capital, Corum Group, Madison Park Group, KeyBanc Pacific Crest, Zachary Scott, Alexander Hutton, CLA Meridian Capital)

- Miami M&A advisors (sibling city) -- 12 Miami boutiques across $5M-$200M EV (LatAm cross-border / fintech / hospitality / healthcare-services specialty bench: Cassel Salpeter, Cross Keys, BroadSpan Capital, LatamIB, Atlantico Capital Partners, Antarctica Advisors, Solomon Miami, JLL Hotels Miami)

- Nashville M&A advisors (sibling city) -- 14 Nashville-metro firms across $5M-$300M EV (Bailey & Company, Brentwood Capital, Harpeth, VelocityHealth -- HCA + healthcare services + music industry + TN tax domicile specialty bench)

- Best M&A Advisors in Minneapolis — Twin Cities medtech, healthcare services, and AgTech advisors with strategic-bolt-on and PE rollover experience

- M&A Process Guide -- 8-phase M&A lifecycle from strategy to integration

- M&A Due Diligence Process Guide -- complete buy-side and sell-side diligence workflow

- M&A Data Room Setup -- 8-folder structure Dallas advisors expect by week 1

- Best Data Room for a Small M&A Deal -- how to pick a right-sized VDR for a sub-$30M sale, where most Dallas LMM boutiques run their processes

- M&A Click-Through NDA Data Room -- click-through NDA workflows for sell-side processes

- Data Room Cost Comparison -- VDR pricing across 15 platforms

- Best Data Rooms for Private Equity -- platform comparison for PE professionals

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- State of M&A Data Rooms -- 2026 M&A data room market analysis

- Best Energy M&A Advisors in the US (national sector hub) -- upstream, midstream, oilfield-services, power, and renewables advisors mapped by subsector; the sector layer above Dallas's energy deal flow

- M&A Trends and Facts -- decade of M&A market data 2015-2026

- Tax Due Diligence Checklist -- 8-pillar M&A tax DD framework

- Vendor Due Diligence Checklist -- 6-domain sell-side preparation framework

- Peony for M&A -- M&A data room solutions

- Peony for Private Equity -- PE-specific data room features

- Peony for Due Diligence -- diligence workflow tools