DD Timeline: The 14-Week Critical-Path Playbook (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

DD Timeline: The 14-Week Critical-Path Playbook (2026)

Quick answer: M&A due diligence is not a single timeline. It is 6+ parallel workstreams (financial, legal, tax, commercial, HR, IT/cyber, environmental, regulatory) racing against ONE serial critical-path chain: QoE → SPA → financing → RWI bind → HSR clock → close. Roughly 40% of deals miss their close date per BCG, and two-thirds of those need 3+ extra months. 88% of dealmakers report sign-to-close has lengthened in the past 3 years per the 2026 cross-border survey. The three timing bottlenecks I see kill deal momentum most often: (1) HSR's Q1 2026 $133.9M threshold and the Second Request risk; (2) the Week 9 RWI insurance binding gate; (3) third-party consents on cross-border deals. Compression is possible on parallel workstreams (AI-tooled QoE drops from 3-6 weeks to 5-10 days). The critical-path chain is structurally rigid.

Last updated: May 2026

Why I wrote this

I have run buy-side and sell-side due diligence on hundreds of deals, and I have watched far more from the data room side. At Peony we now serve more than 5,900 customers, and our 283-deal Q3 2025-Q1 2026 platform benchmark gives me a fairly clear picture of where modern DD timelines actually break.

The standard mental model — "DD takes 8-12 weeks" — is wrong in a specific way. DD doesn't take 8-12 weeks as a single block. It runs 6+ workstreams in parallel for the first 4-6 weeks, then funnels into a serial critical-path chain that has its own rigid cadence (QoE finalize → SPA negotiation → financing commitment → RWI binding → HSR clock → close). Compressing the parallel workstreams (via AI-tooled QoE, AI-tooled legal review, rapid cyber assessment) saves time on the DD report but does not necessarily save time on the close date. The critical-path chain is the floor.

This post is the working playbook I would hand to a PE deal-team VP coordinating six external advisors, a sell-side CFO trying to keep Day 7 / 14 / 30 doc-population milestones, an M&A lawyer running SPA negotiation against a Week 9 RWI binding gate, or a corp dev VP managing the parallel integration-planning workstream alongside DD. The six frames in this playbook (6-Workstream Critical-Path Map, VDR Population Velocity Curve, Confirmatory-DD Cliff, Third-Party Consent Long Pole, RWI Underwriting Lock, HSR-Tied Timeline) come from cross-referencing the 2024-2026 deal record with the workstream-level mechanics I have observed.

Important framing note: This post complements rather than duplicates Peony's other DD timing coverage. The M&A Due Diligence Process Guide covers the 6-phase process and the "timeline by deal size" question. The M&A Data Room playbook covers the data room setup and how that drives DD timeline. This post is the critical-path orchestration view — the workstream-level mechanics that determine whether you actually close on time.

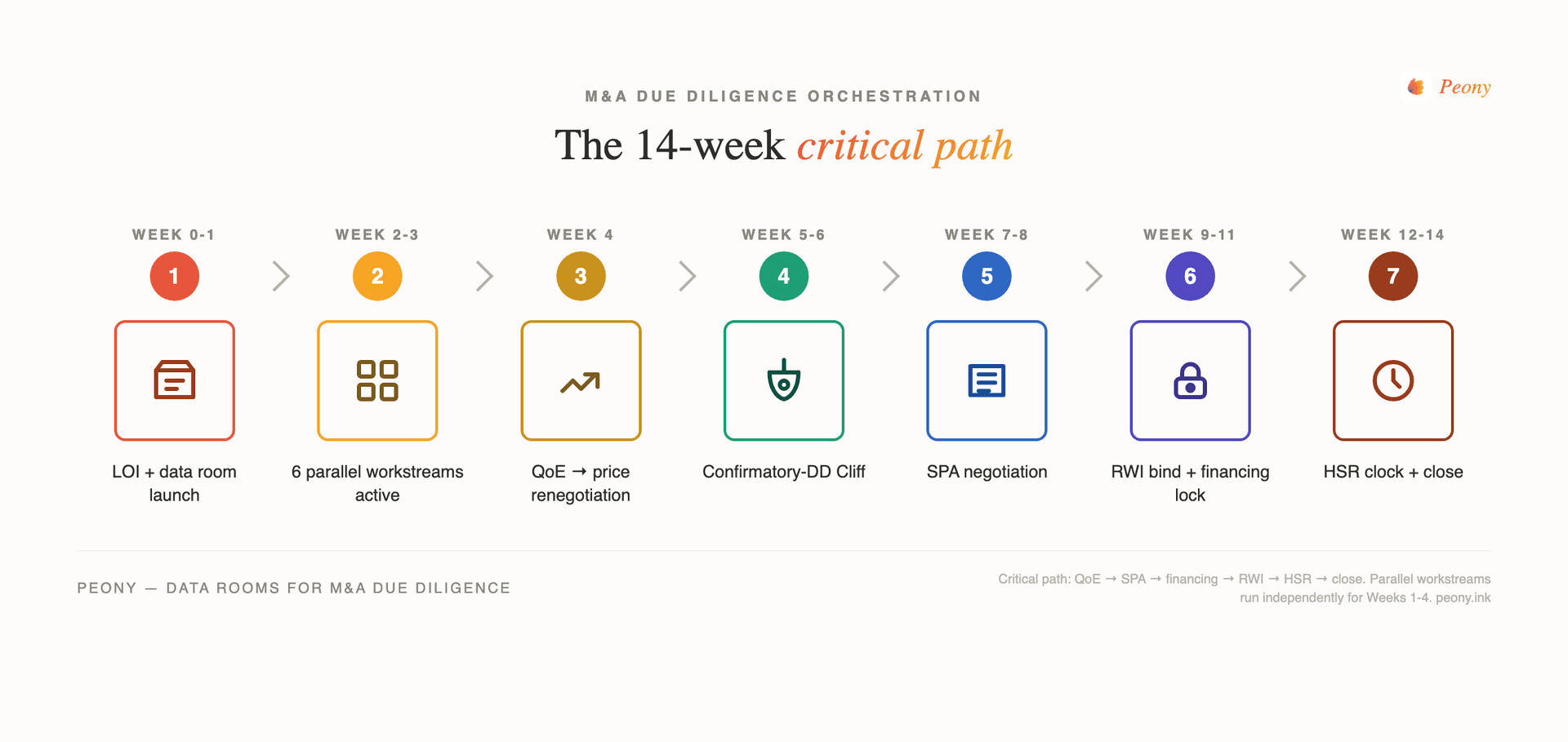

What is the canonical 14-week M&A DD timeline?

The canonical mid-market M&A DD timeline runs 14 weeks from LOI signing to close, with a 6-week intensive DD phase embedded inside it.

The standard 14-week sequence:

- Week 0 — LOI signing + exclusivity period begins. Data room access granted. Workstream coordinators identified across legal, financial, tax, HR, commercial, IT/cyber.

- Weeks 1-2 — Day-1 data room population sprint. Target: 50-60% uploaded by Day 7, 80% by Day 14. Initial DDQ responses begin.

- Weeks 3-4 — Quality of Earnings preliminary findings surface. Working capital peg negotiation begins. Price renegotiation window opens.

- Weeks 5-6 — Confirmatory DD findings surface (the "Confirmatory-DD Cliff"). Management interviews. Site visits. Customer reference calls. Cross-functional risk register.

- Weeks 7-8 — SPA negotiation. Disclosure schedules drafted. Reps and warranties scoped. Indemnification baskets sized.

- Week 9 — RWI insurance binding gate. Final DD reports + DDQ Q&A logs + agreed SPA reps required.

- Weeks 10-11 — Financing commitments firmed. Credit committees approve. Debt commitment letters issued.

- Weeks 12-13 — Regulatory clearance (HSR 30-day clock for deals >$133.9M per FTC's Q1 2026 update).

- Week 14 — Closing.

The 6-week intensive DD phase per Dealroom's 2026 6-step DD framework runs Days 1-42: Days 1-7 (Week 1) data room launch + initial requests; Days 8-21 (Weeks 2-3) first-pass functional reviews across legal/financial/commercial/tech/HR in parallel; Days 22-28 (Week 4) management interviews + site visits; Days 29-35 (Week 5) synthesis + IC memo + cross-functional risk register; Days 36-42 (Week 6) final negotiations + sign-off.

Variance by deal size:

- Small acquisitions under $10M — compress to 8-10 weeks total. QoE may not be commissioned (legal + financial review only). RWI insurance often not purchased. HSR usually not applicable.

- Mid-market $50M-$500M — canonical 14-week timeline. Most workstreams active. RWI common. HSR applicable above $133.9M.

- Large cross-border $500M-$5B — 18-30 weeks. Multi-jurisdictional regulatory (HSR + EU EUMR + UK NSI + German FDI + CFIUS as applicable). RWI scope expanded.

- Mega-deal $5B+ — 6-12 months or longer. Substantial compliance under HSR Second Request risk. Multiple FDI screenings. Complex divestiture commitments.

The 14-week canonical is the median for $50M-$500M private-target deals where neither extreme delay nor extreme compression applies. The 2024-2026 reality is that 40% of deals miss this median by months.

Why is sign-to-close lengthening — what's the 2024-2026 data?

Sign-to-close timelines have lengthened materially across 2024-2026. The anchored data:

Goodwin Procter's October 2025 analysis found sign-to-close for PE deals increased 64% from 2023 to 2024. The drivers Goodwin cites: regulatory complexity (HSR Second Request risk, FDI screenings), expensive debt (credit spreads, financing-commitment delays), expanded DD scope (cyber DD, ASC 606 revenue recognition), and RWI demands (carriers requiring thorough DD reports before binding). Goodwin's headline framing: "it is increasingly common for M&A transactions to be repriced or abandoned entirely."

The SRS Acquiom + Mergermarket Q3 2024 survey of 150 senior bankers reported 59% say 1-3 months were added to DD timelines. The same survey found 97% of senior bankers cite cybersecurity as expecting the greatest DD scrutiny and 45% of bankers call tech/IT review the most expensive workstream. Deloitte's 2025 M&A Trends Survey found 88% of corporate leaders pivoting M&A strategies for new issues and emerging threats with cybersecurity at the center of that shift. Morrison Foerster's 2025-2026 outlook corroborates the tech-DD-cost finding through its broader tech M&A survey.

The 2026 cross-border survey reports 88% of dealmakers say sign-to-close has lengthened in the past 3 years and 74% have deals prevented from closing due to entity/SPV delays.

BCG's 2024 M&A Report: approximately 40% of deals don't close on their original target date, and of those delayed, nearly two-thirds need 3+ extra months (note: 2024 vintage data, but no 2025-2026 successor benchmark superseded the BCG numbers as of May 2026) rather than a few weeks.

The structural drivers behind the 2024-2026 lengthening:

- HSR Q1 2026 rule update — threshold rose to $133.9M (up 6%); top-tier filing fee rose to $2.46M; enforcement intensity continued.

- RWI insurance now near-standard in mid-market and sponsor-backed deals per Kennedys' 2026 RWI outlook (ABA Deal Points Study historically tracked 55-65% adoption). RWI carriers demand thorough DD reports + DDQ logs before binding at Week 9, adding 1-2 weeks of carrier audit.

- Cyber DD expansion — 22% of 2026-cohort deals now include cybersecurity reps (up from 5% in 2024 per SRS Acquiom's 2026 Deal Terms Study covering 2,300+ deals and $569B); cyber DD M&A market projected at $5.163B in 2025; 74% of target codebases contain high-risk vulnerabilities per Synopsys OSSRA 2024 report cited in Human Renaissance's 2025 M&A Tech DD benchmark.

- Third-party consents — lender consents, customer/landlord consents, anti-assignment provisions in major contracts compound on cross-border deals.

- ASC 606 revenue recognition complexity — adding QoE scope and lengthening QoE timelines.

The takeaway: most deals do not miss their close date by a small margin. They miss by months or get repriced.

What are the 6+ parallel workstreams and how do they coordinate?

M&A DD runs 6 core parallel workstreams (sometimes 8-9 with industry-specific add-ons). Each has its own timing, dependencies, and bottleneck pattern.

| Workstream | Standard timing | Cost (mid-market) | Bottleneck source |

|---|---|---|---|

| Financial DD / QoE | Weeks 1-4 (3-6 weeks) | $20K-$75K | Target's audited financials availability |

| Legal DD | Weeks 1-5 (30-90 days) | $50K-$250K | Manual document review labor |

| Tax DD | Weeks 2-3 (5 days-3 weeks) | $15K-$75K | QoE adjustments dependency |

| Commercial DD | Weeks 1-3 + Week 5-6 ref calls | $25K-$150K | Customer ref calls held until close certain |

| HR DD | Weeks 2-4 (6 weeks) | $20K-$100K | Management retention discovery late |

| IT/Tech/Cyber DD | Weeks 2-4 (5 days-3-4 weeks) | $30K-$250K+ | Codebase complexity + cyber-incident history |

| Environmental DD (industrial/RE) | Phase I 2-4 weeks | $5K-$30K Phase I | 180-day Phase I validity expiry |

| Regulatory DD (sector-specific) | Varies | Varies | HSR / CFIUS / FDA clocks |

| Third-Party Consents | All deals | $20K-$100K | Lender / landlord / customer responsiveness |

Financial DD / Quality of Earnings (Weeks 1-4)

Standard mid-market QoE runs 3-6 weeks depending on data quality and management responsiveness per Anders QoE Guide and DueDilio's 2025 QoE Analysis Guide. Multi-location or complex deals run 6-8 weeks. Big Four "compressed" QoE with AI tools can run as low as 5 days for clean mid-market targets. Cost runs $20K-$75K for mid-market QoE reports.

Critical gate: target's audited financials must be available. If the PCAOB audit lapsed, this is the first bottleneck of the entire deal. Output drives purchase price renegotiation in Weeks 3-4 and the working capital peg.

Legal DD (Weeks 1-5)

Standard 30-90 days depending on target complexity. Document review consumes 1-2 weeks of attorney-hours and is the typical labor bottleneck (not document complexity). Mid-market 6-week standard per Dealroom 2026.

Key deliverable: legal DD findings report drives SPA reps + conditions precedent. Per Emma Legal's bottleneck analysis, AI-assisted contract review tools can drop 1-2 weeks of attorney-hours to 3-5 days for standard contract types.

Tax DD (Weeks 2-3)

Tax DD is structurally downstream of QoE — it depends on QoE adjustments to normalized EBITDA as a pure input. Modern AI-tooled tax DD runs 5 days to 3 weeks for mid-market. Section 382 study required for stock deals due to NOL limitation post-ownership change at 5% shareholder thresholds per Plante Moran's June 2025 Section 382 analysis.

Commercial DD (Weeks 1-3 + customer reference calls Week 5-6)

First-pass commercial DD (market positioning, competitive landscape, growth model) runs Weeks 1-3. Customer reference calls are typically held until Week 5-6 when closing is "nearly certain" per Allegrow's DD navigation guide — because customer ref calls signal imminent close to the seller's customer base. Premature customer ref calls leak deal news and create customer-anxiety risk for the seller.

HR DD (Weeks 2-4)

Standard 6-week middle-market timeline. Inputs: org chart + comp + equity plans + executive contracts. The structural bottleneck: management retention agreements often discovered missing late (Week 5-6) — the strongest single late-stage walk-away risk for PE buyers per the WTW 2024 M&A Retention Study where 28% of acquirers have no key-person retention plan at all. See our Hard vs Soft DD playbook for the soft-DD-side of HR risk management.

IT / Tech / Cyber DD (Weeks 2-4)

The fastest-growing and most expensive workstream. Rapid cyber assessment: 5-7 days. Comprehensive cyber + tech DD: 3-4 weeks. 97% of senior bankers cite cybersecurity as expecting the greatest DD scrutiny per the SRS Acquiom + Mergermarket Q3 2024 senior banker survey of 150 bankers. 45% of bankers call tech DD the most expensive workstream per SRS Acquiom Q3 2024. 74% of target codebases contain high-risk vulnerabilities per Synopsys OSSRA 2024 report cited in Human Renaissance's 2025 M&A Tech DD benchmark. US data breach liability averages $10.22M per IBM Cost of Data Breach 2025. Cyber DD M&A market projected at $5.163B in 2025 per Centri Consulting's cyber-DD analysis. If a major security overhaul is required, expect 6+ months remediation post-close — freezing the integration roadmap.

Environmental DD (Industrial / RE only)

Phase I ESA: 2-4 weeks standard. Phase I valid only 180 days for AAI defense — must be re-pulled if the deal slips past 180 days post-Phase-I per Acquisition Stars Environmental DD primer. Phase II (if RECs identified): 6-12 weeks. Manufacturing facilities regularly trigger Phase I RECs (chemical storage, USTs, floor drains, adjacent industrial). ASTM E1527-21 is the EPA-adopted standard since 2023.

Regulatory DD (sector-specific)

HSR for deals >$133.9M: 30-day clock. CFIUS: 30 days short-form / 45 days long-form / 105 days max with investigation + extension per Treasury's CFIUS overview. FDA QMSR effective February 2 2026 for medical device deals per Holland & Knight's FDA 2026 outlook. 2026 CFIUS "Known Investor Program" proposed for frequent filers — reduces review burden for repeated investors.

Third-Party Consents (cross-workstream, ALL deals)

Lender consents, landlord consents, counterparty consents (anti-assignment in major contracts), customer SaaS consents, franchisor consents. "Consent matrix" must be mapped Week 1 — deals that defer consent mapping to Week 5-6 typically slip 30-90 days.

The coordination rule across these workstreams: they run independently for Weeks 1-4, then re-coordinate at Week 5-6 synthesis (cross-functional risk register), and again at Week 7-8 SPA exchange. Workstream coordinators typically use a single "DDQ master" tracker plus a Q&A workflow in the VDR. Peony's visitor groups allow workstream-by-workstream permissioning so each external advisor sees only their assigned scope.

Frame 1: What's the 6-Workstream Critical-Path Map?

The critical path is the SERIAL chain that cannot be parallelized: QoE finalize → working capital peg → SPA negotiation → financing commitment → RWI binding → HSR filing → HSR 30-day clock → close. Everything else runs in parallel.

The mechanics:

- QoE must finalize before working capital peg can be set

- Working capital peg drives SPA price + adjustment mechanism (90%+ of private deals now have a working capital PPA per SRS Acquiom's 2025 Working Capital Study covering 1,200+ deals and $298B, up from ~50% a decade ago)

- SPA must be agreed before financing commitments can be drawn down (debt commitment letters condition on near-final docs)

- RWI carrier needs final DD reports + DDQ Q&A log + agreed SPA reps before binding at Week 9

- HSR can only file after signing (signing requires SPA agreement)

- Cannot close before HSR 30-day clock expires (if deal value >$133.9M per 2026 thresholds)

What CAN run in parallel:

- Legal corp records review + Financial QoE

- IT / cyber scan + Commercial market study

- HR org chart review + Environmental Phase I

- Tax structuring + Regulatory consent matrix mapping

The structural implication for deal teams: AI-tooled compression on parallel workstreams saves time on the DD report but does NOT change close date if the critical-path chain runs at its full duration. Most deal teams underinvest in critical-path compression (early QoE engagement before LOI signing, early SPA drafting starting Week 1, early RWI carrier engagement starting Week 3) and overinvest in parallel-workstream compression (AI-tooled QoE, AI-tooled legal review). The result is a faster DD report but the same close date because the SPA-financing-RWI-HSR sequence still takes its time.

For sellers running sell-side prep, this is the case for vendor DD (VDD): running confirmatory DD on yourself 90 days pre-marketing surfaces findings before the buyer does and lets the QoE, working capital normalization, and SPA framework start earlier post-LOI per the sell-side DD 90-Day Prep Pyramid.

Frame 2: What's the VDR Population Velocity Curve at Day 7 / 14 / 30?

The standard mid-market benchmark for data room population velocity:

- Day 7 — 50-60% of materials uploaded (corporate records, financial statements, key contracts, basic legal docs)

- Day 14 — 80% uploaded (most workstreams have substantial materials available for review)

- Day 21 — 95% uploaded (only confirmatory and management-interview docs missing)

- Day 30 — 99%+ uploaded with only late-arriving custom requests outstanding

The Peony platform first-party data from our 283-deal Q3 2025-Q1 2026 benchmark tracks bidder engagement accuracy at 97% by Day 7 — meaning by the end of Week 1, the bidder behavior patterns (which bidders are reading deeply, which are skimming) are 97% predictive of which bidders will return for confirmatory DD and which will drop. Slow-uploading sellers (Day 14 at 60% rather than 80%) typically lose 2-3 weeks on the close date because critical-path workstreams (QoE in particular) cannot complete on schedule.

The most common Day 7 misses I see:

- Audited financials for prior 3 years — target's auditor often slow on year-end statements; missing audited financials blocks QoE

- Cap table and equity ledger — target's law firm slow to provide; blocks legal DD on corporate structure

- Customer contract catalog — target sales team often disorganized; blocks commercial DD on customer concentration

- IP assignment chain documentation — the single most-common Week 5-6 surprise gap; missing work-for-hire agreements for contractor-built code or product IP

- Compensation and equity grant histories — target HR team often slow; blocks HR DD on management retention

Peony's AI auto-indexing accelerates the Day 7 / 14 / 30 curve by classifying uploaded documents into standard DD categories in under 3 minutes — typical sell-side teams see Day 14 80% upload completion rather than the Day 21 80% completion typical of manual folder organization. Page-level analytics make the bidder-engagement-accuracy signal actionable: by Day 7, the deal team can identify which 30-50% of bidders are likely to return for confirmatory DD.

Frame 3: Why do most deal-killers surface Week 5-6 (the Confirmatory-DD Cliff)?

The Confirmatory-DD Cliff is the structural reality that most deal-killing findings surface in Weeks 5-6 of DD, not Weeks 1-2.

The mechanics: Weeks 1-2 are document review (data room scan, contract review, financial-statement scrutiny) — a high-volume, low-depth activity. Weeks 5-6 are confirmatory DD (management interviews, customer reference calls, site visits, deep-dive on flagged issues, second-pass review) — a low-volume, high-depth activity that often surfaces findings that get a deal repriced or killed.

The pattern across 2024-2026 deals I've worked on or observed:

- Management interviews in Week 4-5 surface key-person flight risk that wasn't visible in the org chart. The classic case: a single account manager controlling a customer relationship worth >10% of revenue, with no retention plan beyond their at-will employment.

- Customer reference calls in Week 5-6 surface customer-loyalty issues tied to specific account managers rather than the brand or product. Customers who say "I'd follow [account manager] anywhere" are signaling structural transferability risk.

- Second-pass legal review in Week 5 surfaces missing IP assignment chains or change-of-control termination rights in major customer contracts that weren't flagged in the first-pass DDQ response.

- HR DD in Week 5-6 surfaces missing management retention agreements — the strongest single late-stage walk-away risk per WTW's 2024 M&A Retention Study where 28% of acquirers have no key-person retention plan at all.

- Operational DD site visits in Week 4 surface process-maturity issues that aren't visible in process documentation.

- Confirmatory tax DD in Week 5 surfaces state nexus or transfer pricing issues that initial Week 2-3 review missed.

The strategic implication: deal teams should NOT assume that a clean Week 1-2 DDQ response means the deal is clean. The cliff is real and structurally late. Approximately 30-40% of total DD budget should be reserved for Week 5-6 deep-dive scope — held back from the initial Week 1-4 burn rate.

For sellers running sell-side prep, the Cliff is the case for vendor DD: running confirmatory DD on yourself 90 days pre-marketing surfaces the same findings before the buyer does, letting the seller remediate or disclose proactively rather than reactively per the sell-side DD 90-Day Prep Pyramid.

Frame 4: When do third-party consents become the long pole on cross-border deals?

Third-party consents are the most-overlooked timing risk in M&A DD — and they often become the long pole on cross-border deals. The five most common consent categories and their typical timelines:

| Consent type | Typical timeline | Notes |

|---|---|---|

| Lender consents (change of control) | 30-60 days | Longer for syndicated facilities |

| Landlord consents | 30-60 days | Common in real estate leases |

| Counterparty consents (anti-assignment in major contracts) | 30-90 days | Customer SaaS contracts typically 90+ days |

| Franchisor consents | 30-90 days | Standard franchise agreement provisions |

| Customer consents on regulated services | 60-120 days | Healthcare, financial services, government contracts |

Cross-border deals compound consent risk because foreign-direct-investment (FDI) screenings layer on top of HSR/CFIUS:

- EU EUMR — Phase I 25 working days, Phase II 90 working days

- UK NSI Act — 30 working days mandatory review

- German FDI — 2-month review (extendable)

- France FDI — 30 business days (extendable to 45)

- Japan FEFTA — 30-day prior notification

The 2026 cross-border survey reports 88% of dealmakers say sign-to-close has lengthened in the past 3 years and 74% have deals prevented from closing due to entity/SPV delays. Approximately 30-50% of cross-border deals slip past their target close because of third-party consents (versus ~15% of pure-domestic deals).

The structural rule for deal teams: every deal should produce a "consent matrix" in Week 1 of DD listing every material contract requiring third-party consent, the expected timeline, and the responsible owner. Deals that wait until Week 5-6 to map consents typically miss their close date by 30-90 days.

Per Settles Law's third-party consent primer and CMM's consent guide: "consents and approvals are the first gate to closing an M&A transaction." Missing or late consents convert from a documentation issue to a closing condition issue, and closing conditions cannot be unilaterally waived without triggering a material adverse change (MAC) clause.

Frame 5: What gates the RWI Underwriting Lock at Week 9?

The Week 9 RWI insurance binding gate is one of the three timing gates I most commonly see kill deal momentum. The mechanics: a buyer purchasing R&W insurance (now near-standard in mid-market and sponsor-backed deals per Kennedys' 2026 RWI outlook; the ABA Private Target M&A Deal Points Study historically tracked 55-65% adoption across 2023-2024 vintages) must complete underwriting before signing, with the policy binding at signing and issuing at or just before signing.

The standard RWI underwriting timeline per McDermott Will & Emery's RWI guide:

- Preliminary submission to non-binding quotes: 2-4 business days

- Formal underwriting process: 1-2 weeks

- Underwriting plus binding: 7-10 business days if responses are prompt

- Overall: 2-3 weeks total

What gates the bind:

- Final DD reports from all workstreams — QoE, legal, tax, HR, IT/cyber, commercial — must be substantially complete

- DDQ Q&A logs must be substantially complete

- Agreed SPA reps and warranties must be in place

- Disclosure schedules must be substantially drafted

Without these, the RWI carrier cannot complete its own coverage-scope analysis. Carriers will not shortcut.

The 2026 RWI pricing per Gallagher's 2026 RWI outlook:

- Premium: 2.0-4.0% of coverage limit (most deals 2.25-3.25% in competitive market)

- Retention: 0.5-1.5% of EV at policy inception, dropping to 0.25% after Year 1

- Coverage limit: typically 10% of EV

- Example $50M deal: $5M coverage, $250K retention, ~$125K-$200K premium

Strategic buyers often absorb both premium and retention in competitive auctions per Kennedys' 2026 RWI outlook.

The structural risk: any DD workstream not professionally scrutinized gets excluded from RWI coverage. Under-diligenced cyber risk, under-diligenced HR retention, under-diligenced environmental — all get exclusion endorsements that shift risk back to the buyer's balance sheet. The 2026 market is buyer-favorable on premium but seller-favorable on exclusions — carriers will exclude where DD is thin.

For deal teams: engage the RWI carrier in Week 3 (not Week 7) so the carrier audit can run in parallel with the late-DD-stage workstreams rather than serially after them. The 1-2 weeks of carrier audit time is often the difference between Week 9 binding and Week 11 binding.

Frame 6: How does the HSR Q1 2026 rule shift change deal timing?

The Hart-Scott-Rodino Q1 2026 thresholds went into effect February 17, 2026 per the FTC's January 2026 announcement. The updated thresholds and implications:

- Size of transaction: $133.9M (up from $126.4M in 2025, +6%)

- Size of person: $267.8M / $26.8M

- Section 8 interlocking directorate threshold: $54.4M (up from $51.4M)

- Filing fees: $35,000 (smallest tier) to $2.46M (top tier), up from $2.39M

- 30-day initial waiting period: unchanged

- Cash tender offers: retain 15-day initial waiting period (strategic-buyer advantage)

Sources: Cleary Gottlieb's 2026 HSR analysis, Pillsbury's 2026 HSR alert, Greenberg Traurig's 2026 HSR update.

For 2026 sub-$133.9M deals, HSR is not a critical-path concern — only larger deals hit the clock. For deals at or above the threshold, the 30-day clock is a structural floor on close date from filing.

The Second Request risk is the real time-killer. If the FTC or DOJ issues a Second Request, the 30-day clock tolls until parties certify "substantial compliance" — typically MONTHS of document collection, privilege review, and data extraction in agency-specified formats. The 30-day clock then restarts from substantial-compliance certification. High-scrutiny sectors for 2026 Second Requests: healthcare consolidation, big tech (acquisitions of independent platforms), defense (especially AI/cyber), semiconductors, energy (especially renewables), pharma.

For cross-border deals, the regulatory clock extends beyond HSR:

- CFIUS: 30 days short-form, 45 days long-form, 105 days max with investigation + extension per Treasury's CFIUS overview

- EU EUMR: Phase I 25 working days, Phase II 90 working days

- UK NSI Act: 30 working days mandatory

- German FDI: 2-month review (extendable)

The deal-team rule for HSR: assume the 30-day clock will run in full and plan close 30 days after signing. Assume Second Request risk if the deal is in a high-scrutiny sector. For deals below $133.9M, HSR doesn't apply but state antitrust attorneys-general may scrutinize healthcare deals under state-specific premerger filing requirements (Connecticut, California, Washington, New York increasingly active).

Honest comparison: which VDR fits which deal-size band?

| Deal-size band | Recommended VDR | Why |

|---|---|---|

| $5M-$50M EV | Peony, FirmRoom, iDeals starter | Fast setup, $52-100/admin/month pricing, AI auto-indexing for sell-side speed |

| $50M-$500M EV | Peony, iDeals, Firmex, Ansarada | Workstream-by-workstream permissioning + audit trail for RWI underwriting |

| $500M-$1B EV | Datasite, Intralinks, Peony (with custom) | Institutional integrations with QoE providers, law firms, RWI underwriters |

| $1B-$5B EV | Datasite, Intralinks | Enterprise workflow + dedicated workstream platforms (Litera Transact, Allvue) |

| $5B+ EV | Datasite, Intralinks (with bank-led integration) | Bank-managed VDR environments; complex divestiture handling |

Datasite — the dominant enterprise VDR for $1B+ deals — owns the enterprise band on institutional integrations with QoE providers (EY-Parthenon, Alvarez & Marsal, BDO), law firms (Kirkland, Latham, Skadden), and RWI underwriters (AIG, Beazley, Liberty Mutual). Intralinks Dealspace competes head-to-head in the mega-deal segment with similar institutional integrations.

For sub-$500M EV deals — approximately 85% of M&A volume by deal count — Peony, iDeals, and FirmRoom compete on flat-rate pricing, AI auto-indexing speed, and workstream-by-workstream visitor permissioning. Peony Data Room at $52 per admin per month replaces the $15K-$50K per-deal data room cost typical of legacy VDR providers.

The honest VDR limits to flag:

- Above $500M EV — institutional integrations with QoE providers, law firms, and RWI underwriters matter; Datasite/Intralinks typically have these built-in

- For multi-jurisdictional deals requiring complex data residency — Datasite's regional hosting options often outperform smaller VDR options

- For bank-led mega-deals — banks typically have established VDR preferences that constrain seller's VDR choice

- For deals requiring dedicated workstream platforms — above $500M EV, Litera Transact (deal lifecycle management), Allvue (PE portfolio management), Sourcescrub (origination intelligence) layer on top of the VDR

Bottom line

M&A due diligence runs 6+ parallel workstreams (financial, legal, tax, commercial, HR, IT/cyber, environmental, regulatory) for the first 4-6 weeks of a 14-week canonical timeline. Then the workstreams funnel into ONE serial critical-path chain: QoE → SPA → financing → RWI bind → HSR clock → close. Compression is possible on parallel workstreams (AI-tooled QoE drops from 3-6 weeks to 5-10 days; AI-tooled legal review drops 1-2 weeks of attorney-hours to 3-5 days). The critical-path chain is structurally rigid.

The three timing gates I see kill deal momentum most often: the Week 9 RWI binding gate (carriers require complete DD reports + DDQ logs + agreed SPA reps before binding); the HSR Q1 2026 $133.9M threshold and Second Request risk (30-day clock floors above the threshold; Second Request risk in high-scrutiny sectors); and third-party consents on cross-border deals (lender, landlord, customer, franchisor consents — 30-50% of cross-border deals slip on these).

The single most important deal-team decision: engage RWI carrier in Week 3 and map the consent matrix in Week 1. Both decisions add zero cost but commonly save 2-4 weeks on the close date.

The 2024-2026 reality: 40% of deals miss their original close date per BCG, and two-thirds of those need 3+ extra months. Sign-to-close for PE deals increased 64% from 2023 to 2024 per Goodwin Procter. 88% of dealmakers report sign-to-close has lengthened in the past 3 years. The deals that close on time are the ones where the deal team treats the critical path as the binding constraint, not as a backdrop against which parallel-workstream compression delivers a faster DD report.

Related resources

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — the canonical process guide covering DD timeline by deal size

- M&A Data Room: Setup and Workstream Mapping — data room timeline + impact on DD

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep that compresses buy-side DD

- Hard vs Soft Due Diligence: The 5-Frame Playbook — distinguishing hard-DD workstreams (document-driven) from soft-DD (interview-driven)

- Due Diligence Questionnaire: The 220-Item DDQ Template — DDQ structure mapped to workstreams

- Due Diligence Mistakes That Kill Deals — common workstream-coordination failures

- Commercial Due Diligence: 4-Quadrant Buyer Posture Map — commercial DD timing within DD timeline

- Operational Due Diligence: The 8-System Audit — ODD timing across the parallel workstreams

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark anchoring VDR Population Velocity Curve

Footnotes and sources

- Goodwin Procter — Private Equity Deal Timelines: Turning Delays (October 2025)

- SRS Acquiom — M&A Due Diligence Study (Q3 2024 survey of 150 senior bankers)

- SRS Acquiom — 2026 Deal Terms Study (2,300+ deals, $569B)

- SRS Acquiom — 2025 Working Capital Study (1,200+ deals, $298B)

- FTC — 2026 HSR Threshold Update (January 2026)

- Cleary Gottlieb — 2026 HSR Thresholds Announced

- Pillsbury — FTC HSR Threshold Filing Fee Increases 2026

- Greenberg Traurig — 2026 HSR Merger Notification Thresholds and Fees

- Gallagher — Who Pays the RWI Premium and Retention in 2026

- Kennedys — Negotiating Transaction Documents in 2026 with RWI

- McDermott Will & Emery — RWI Underwriting Process Timeline

- CBIZ — Representations and Warranties Insurance in 2025 M&A

- Treasury — CFIUS Overview

- Foley & Lardner — CFIUS for International M&A

- Morrison Foerster — M&A in 2025 and Trends for 2026

- Deloitte — 2025 M&A Trends Survey

- Synopsys OSSRA — Open Source Security Risk Analysis Report

- BCG — Deals Are Taking Longer to Close (2024)

- Strategex — 80/20 Customer DD Research

- Holland & Knight — FDA What to Watch in 2026

- Centri Consulting — Cybersecurity Hidden Pillar of M&A DD

- Human Renaissance — 2025 M&A Technology DD Benchmarks

- IBM — Cost of a Data Breach Report 2025

- Anders — Quality of Earnings Report Guide

- DueDilio — Quality of Earnings Analysis Guide 2025

- Plante Moran — How Section 382 Impacts NOL Carryforwards

- Emma Legal — Breaking M&A Bottleneck with Faster Legal DD

- Dealroom — 6-Step DD Process 2026

- Allegrow — Navigating the DD Period

- WTW — 2024 M&A Retention Study

- Sampford Advisors — Sell-Side Process Timeline

- Acquisition Stars — Environmental DD for Manufacturing Acquisitions

- RMA Green — Phase I ESA Primer

- Settles Law — Third-Party Consents in M&A

- CMM — Consents and Approvals: The First Gate to Closing