12 Due Diligence Mistakes That Kill M&A Deals (2026): Working Capital Wedge + Bain Test

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

I spend most of my week fielding data-room questions from buyer-side teams who almost missed something material in DD: a PE associate who found a $4 million working-capital wedge baked into the LOI peg the day before signing, a strategic acquirer's CFO who discovered the target had paid no state sales tax in 12 jurisdictions after Wayfair, an M&A advisor whose seller had pre-incorporation founder IP that was never assigned, and a corporate-development lead at a healthcare buyer who realized the target's open-source AGPL contamination would have exposed the post-close company to mandatory source disclosure. Due diligence mistakes in 2026 are no longer about missing a document — the documents are usually there, somewhere in a 3,500-file data room. The mistake is the synthesis failure: not connecting findings to each other, not pressure-testing the top 5 material items, not pricing the post-LOI Tunnel Vision into the decision. I run Peony, a data room platform used by 5,900+ customers across M&A, private equity, and DD workflows. Backed by VCs including Target Global, this guide maps the 12 most expensive buyer-side DD mistakes from 2024-2026 deals, the Working Capital Wedge math, the Bain Test for PE cyber liability after the March 2026 PowerSchool ruling, and the Post-LOI Tunnel Vision framework I use to keep deal momentum from overriding deal evidence.

Quick answer: The twelve buyer-side due diligence mistakes that destroy the most value in 2026 are: (1) waiving DD to win the deal (Twitter $25B value loss), (2) confirmation-bias cliff (Hertz-Dollar Thrifty), (3) DD theater (SmileDirectClub), (4) cyber DD failure with post-close PE direct liability (Bain-PowerSchool March 2026 ruling), (5) working-capital wedge (median 1% deal value, 25% exceed), (6) customer concentration miscalculation, (7) earnout drafting that guarantees litigation (Fortis v. J&J $1B+ award), (8) regulatory shoes dropping post-close (Block $295M in 2025 settlements), (9) IP gaps and AGPL contamination (Black Duck 2026: 94% of codebases have license conflicts), (10) tax exposures post-Wayfair plus Section 174, (11) UFLPA / EU CSDDD supply-chain misses, (12) R&W insurance gap (Gallagher 2025: 1 in 4 paid claims hits the full limit). The structural failure mode is Post-LOI Tunnel Vision — after board approval and announcement, the deal team treats DD as problem-solving rather than fact-finding.

The Deal-Failure Base Rate: Why DD Mistakes Compound

Roughly 70% of M&A deals fail to deliver expected returns per McKinsey's canonical analysis.1 KPMG's 2023 study put the figure at 83% failing to boost shareholder returns; Bain's 2024 analysis found only 30% of deals achieve their synergy targets; Deloitte's 2025 M&A Trends Survey found 47% of executives admit prior deals underperformed.1 And yet ~80% of executives in Bain's 2026 survey expect to sustain or increase deal activity into 2026 — a record-rebound year with global M&A hitting $4.9 trillion (+40% YoY), 70 deals greater than $10 billion, and 617 deals over $1 billion.2

The deal-failure base rate is the structural reason DD mistakes are so costly. Every mistake operates against a probability distribution that already favors disappointment. A 5% pricing error on a deal where the central expectation was 20% positive returns kills the upside; a 5% pricing error on a deal where the central expectation is value-destructive deepens the loss. DD is the only structural lever that moves the buyer's distribution before signing.

Mistake 1: Waiving Due Diligence — The Twitter Archetype

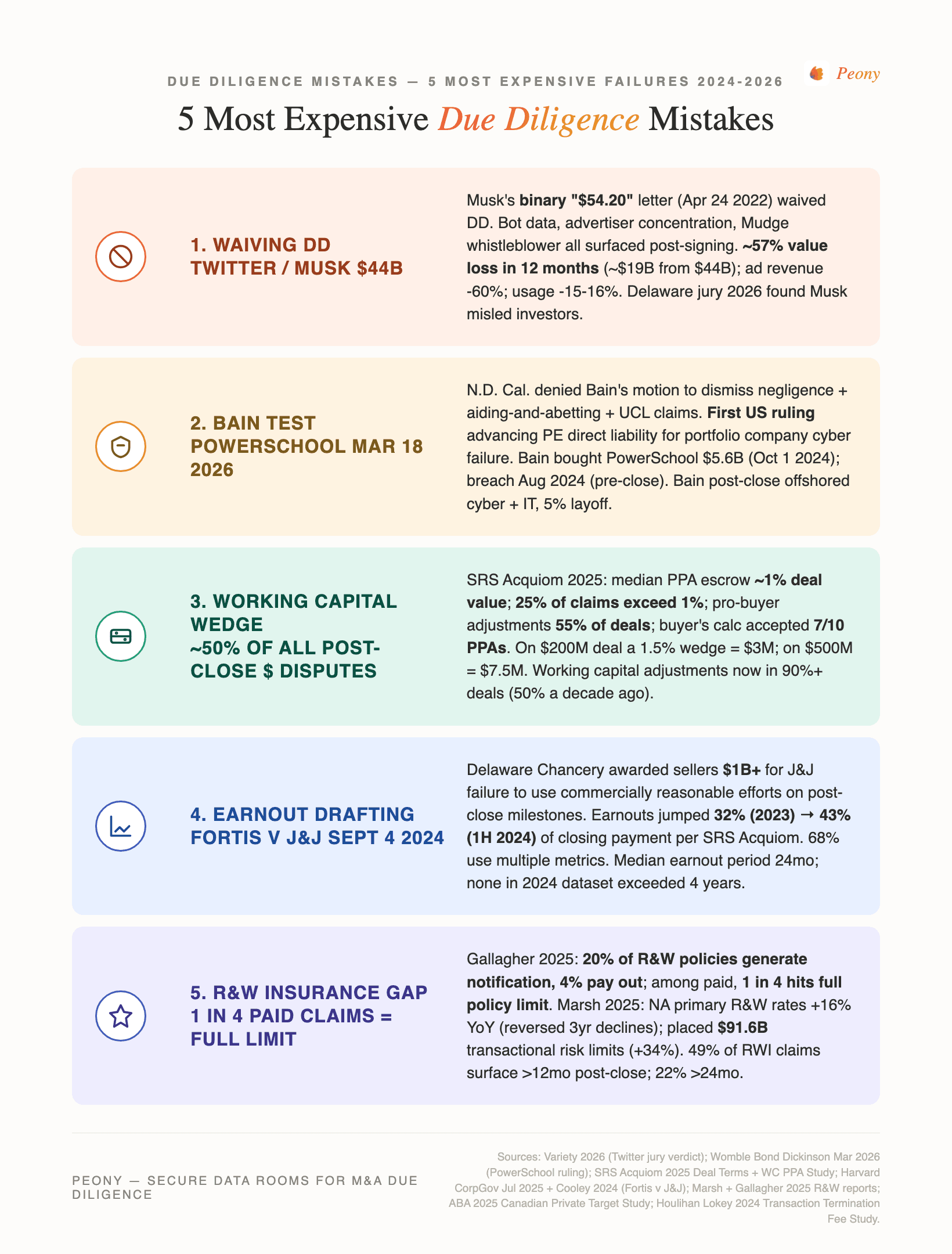

The Twitter / Elon Musk $44 billion acquisition (April 2022) is the largest waived-DD failure on record. Musk's April 24, 2022 letter to Chairman Bret Taylor framed the offer as binary: "This is binary — my offer will either be accepted or I will exit my position." Musk explicitly waived due diligence. Twitter's bot-count methodology, advertiser concentration, and the Mudge whistleblower disclosures all surfaced after the binding agreement. Musk later tried to walk citing bot accounts, but had no waiver clause or escrow to support the exit.3

One year post-close, the company had lost roughly 57% of its value (~$19 billion from $44 billion). Advertising revenue dropped 60% and usage fell 15-16%. In March 2026, a federal jury in San Francisco found Musk misled Twitter investors ahead of the takeover.3

The fix: Never sign without bot/usage data forensic verification on consumer platforms. Never accept "best and final, period" framing as a substitute for confirmatory DD. Always retain (a) a financing-out, (b) a regulatory MAE carve-out, (c) escrow above 5% deal value, and (d) a 30-day post-LOI confirmatory DD window even on a "binding" merger agreement.

Mistake 2: How Does Confirmation Bias Kill M&A Deals?

The Confirmation Bias Cliff is the probability shift where DD findings are no longer being properly priced into the deal — it drops sharply once the buyer's board has approved or the deal has been publicly announced.

The Hertz / Dollar Thrifty $2.3 billion acquisition (2012, leading to Hertz's May 2020 Chapter 11) is the canonical case. Operational problems never surfaced during DD: Dollar Thrifty's tires were below Hertz's minimum tread (cost: $30 million to replace); IT systems couldn't integrate; airport lots couldn't be combined. A merger projected to save $100 million in Year 1 ended up costing an additional $70 million. Hertz's already-leveraged balance sheet couldn't survive the 2020 travel collapse.4

The fix: Mandate a "red team" devil's advocate role inside the deal team. Pre-commit to a walk-away price before DD starts (not after auction fever sets in). HBR's "Deals Without Delusions" framework: aggressively seek evidence that challenges the deal thesis, not evidence that confirms it.5

Mistake 3: DD Theater — Checking Boxes Without Investigating

DD Theater is the "checklist completion" approach where every box is ticked but the top 5 material findings are never pressure-tested by a senior partner. Junior associates produce 400-tab DD checklists, all marked complete. The institutional ritual masks a synthesis failure.

The SmileDirectClub case is the textbook value-destruction post-mortem. The company filed for Chapter 11 in September 2023 and converted to Chapter 7 on January 26, 2024.6 All financial signals were visible: EBITDA, operating income, and net income negative every year since 2017. At filing, $499 million in assets versus more than $1 billion in liabilities. An active Align Technology (Invisalign) IP dispute resulted in a $63 million judgment that finished the liquidity. The IPO underwriters and post-IPO institutional buyers had access to every disclosure. The post-mortem allegations: founders Jordan Katzman, Alexander Fenkell, and CEO David Katzman extracted bonuses and stock pre-filing. The bankruptcy trustee has subsequently litigated those distributions.6

The fix: Replace the checklist exit ritual with a "Top 5 Findings + Open Issues Memo" gate. The senior partner signs off on what the Top 5 are and how each was resolved. No investment committee vote until those 5 have written closure with named owners. This is the structure that beats DD Theater: it forces the synthesis the checklist cannot.

Mistake 4: Cyber DD Failure — How the Bain Test Changes PE Liability

The most consequential cyber DD development of 2026 is the March 18, 2026 federal ruling in In re PowerSchool Holdings, which denied Bain Capital's motion to dismiss claims of negligence, negligence per se, aiding-and-abetting, unjust enrichment, and California UCL violations.7 This is the first U.S. ruling to advance sponsor-level liability for a portfolio company's cyber failure.

The factual sequence: Bain Capital acquired PowerSchool for $5.6 billion, closing October 1, 2024. A threat actor accessed PowerSchool's systems in August 2024 — before close — using stolen vendor credentials. The intrusion was discovered December 28, 2024, post-close. 62 million students and 9.5 million educators had personal data exfiltrated, including Social Security numbers, medical records, financial records, and custody records. Plaintiffs allege that post-close Bain directed offshoring of cybersecurity, engineering, and IT functions to contractors, plus a 5% workforce layoff including domestic IT — directly enabling and compounding the breach response failures.7

The sister case underscores the cost: Change Healthcare ransomware (February 21, 2024) cost UnitedHealth $2.457 billion by Q3 2024, escalated from an $872 million Q1 2024 estimate. ALPHV/BlackCat (Russia-based) was paid a $22 million ransom. The attack affected 131 million-plus patients and roughly 67,000 pharmacies. Change Healthcare processes roughly one-third of U.S. patient records — meaning third-party / supply-chain cyber exposure is now a deal-killer category, not a footnote.8

The fix: Mandatory pre-close external penetration test plus dark-web credential scan plus third-party SaaS dependency map for any target with more than 100,000 user records. Do not direct post-close cost cuts to security or IT for 12-18 months unless redundancies are documented and signed off by a CISO advisor. See the cybersecurity due diligence playbook for the 5-axis breach-readiness matrix and the full Bain Test framework.

Mistake 5: The Working Capital Wedge — Where the Real Money Leaks

Working capital adjustments comprise roughly half of all post-close disputes — making the working-capital peg the single largest post-close cash leak in private-target M&A. Per SRS Acquiom's 2025 Working Capital Purchase Price Adjustment Study, the median PPA escrow runs about 1% of transaction value, but 24% of PPA claims exceed the 1% threshold. Pro-buyer negative adjustments occur in 55% of deals; pro-seller positive adjustments in only 35%. Buyers' calculations are accepted in 7 of 10 PPA disputes.9

The wedge math:

- On a $50 million deal, a 1.5% wedge = $750,000

- On a $200 million deal, a 1.5% wedge = $3 million

- On a $500 million deal, a 1.5% wedge = $7.5 million

A typical example from the SRS dataset: a SaaS company with $1.8 million TTM working-capital average, closing WC at $1.4 million — a $400,000 gap below peg, resolved at $50,000 only after the seller re-negotiated the peg methodology.9

The fix: Lock the WC peg on a 12-month trailing seasonality-adjusted average computed on identical methodology to the closing balance sheet. Specify GAAP adherence and any non-GAAP carve-outs (especially deferred revenue treatment for subscription businesses). Commission a separate WC quality-of-earnings supplement at LOI, not at signing.

Mistake 6: Customer Concentration — Revenue % vs LTV %

The customer-concentration mistake is to measure top-customer percentage of revenue but miss that the bottom 80% are at risk because they were a single-channel acquisition, that one logo's contract auto-renews while another is month-to-month, or that 60% of lifetime value sits in 2 customers.

The industry tiers are clean:10

- Below 10% per customer: clean

- 10-25%: triggers 15-30% valuation discount + earnout/retention escrow structures

- Above 30% top customer: "red flag" deals where many PE firms and SBA lenders pass outright

The academic finding is unambiguous: target's customer concentration is negatively associated with combined deal announcement returns AND with the acquirer's long-term performance — meaning buyers chronically under-price the risk.10

The fix: Run cohort retention analysis separately from logo-concentration analysis. Map LTV by decile, not just revenue by decile. Conduct independent customer interviews that include churned customers and former champions, not just the seller's reference filter.

Mistake 7: Earnout Drafting That Guarantees Litigation

The earnout-drafting mistake is to tie earnout metrics to buyer-controllable operating choices (R&D spend, sales force allocation, integration sequence, product launches) without a "commercially reasonable efforts" obligation or an arbitration-friendly resolution mechanism.

The 2024 anchor case is Fortis Advisors LLC v. Johnson & Johnson (September 4, 2024), where the Delaware Chancery awarded sellers more than $1 billion for J&J's failure to use commercially reasonable efforts on post-close milestones.11 On January 12, 2026, the Delaware Supreme Court partially reversed the implied-covenant claim, and the final stipulated judgment was reduced to approximately $811 million — but the underlying lesson on commercially reasonable efforts language stands. Earnout potential as a percent of closing payment jumped from 32% in 2023 to 43% in the first three quarters of 2024 per SRS Acquiom; 68% of earnout deals use multiple metrics.11

The fix per Cooley's 2024 drafting guidance:11

- Tie earnouts to objective revenue or EBITDA, not buyer-controllable operating choices.

- Include explicit "commercially reasonable efforts" language with referenced benchmarks.

- Build in audit rights for the seller representative.

- Cap the earnout dispute resolution at AAA expedited arbitration.

- Keep performance periods short — none in the 2024 SRS dataset exceeded 4 years.

Mistake 8: Regulatory Shoes That Drop Post-Close

The regulatory-shoe mistake is to rely on representations about regulatory compliance without independent regulatory diligence — and then a Wells Notice or enforcement action lands after close.

Coinbase Wells Notice (March 22, 2023): SEC threatened action on spot trading, staking, custody, Coinbase Prime, and Coinbase Wallet, alleging unregistered securities. The SEC dismissed the Coinbase case on February 27, 2025 — but the resolution required two years of overhang.12

Block Inc. (Cash App): Hindenburg Research published a critical report March 2023; Block disclosed DOJ/SEC investigations August 2023; two whistleblowers came forward February 16, 2024 alleging a "shadow financial system." Settlements: $80 million multistate (state regulators, January 2025), $175 million CFPB (January 16, 2025 — $55 million penalty plus $120 million consumer redress), and $40 million NY DFS (April 10, 2025) — approximately $295 million combined.12

The fix: Pre-close regulatory interview matrix — counsel directly contacts named regulators where the target operates (under NDAs as needed), not just reviews correspondence on file. For fintech, crypto, healthcare, or data-heavy targets, assume any open inquiry is a Wells Notice in waiting and price the indemnity accordingly. See the third-party due diligence playbook for the 5-jurisdiction exposure map.

Mistake 9: IP Gaps and Open-Source Contamination

Two sub-mistakes cluster as the most common IP DD failures in technology deals: (a) founder pre-incorporation IP never assigned to the company; (b) AGPL or GPL components in the codebase trigger copyleft obligations the company has not honored.

The data is overwhelming: Black Duck's 2026 Open Source Risk in M&A by the Numbers report found open source in 98% of codebases, license conflicts in 94% of transactions, and 97% of transactions showing unpatched OSS vulnerabilities with a mean of 786 vulnerabilities per codebase.13 AGPL is especially toxic for SaaS companies because the network-use trigger forces source disclosure for hosted use, not just for distribution.13

Pre-incorporation work is owned by the individuals who created it. A valid assignment from each founder is required. Investors view missing founder IP assignments as "the company doesn't own its core technology" — a deal-killer or valuation-slasher.14

The fix: Mandatory third-party software composition analysis (SCA) scan with line-level provenance for any tech target. Require chain-of-title documentation for every founding-team member back to formation date. Indemnify out any pre-incorporation gap with a special-purpose escrow outside the R&W cap.

Mistake 10: Tax Exposures — Sales Tax Nexus, Section 174, Succession

The tax-exposure mistake is to treat tax DD as a confirmation step rather than an investigation. Post-Wayfair (June 2018), economic nexus traps now catch out-of-state sellers retroactively. Every state with a sales tax has economic nexus thresholds. South Carolina and Wisconsin have retroactively held marketplace facilitators liable. 25 states limited nexus to a $-only threshold in 2024; Utah dropped its 200-transaction threshold July 2025; Illinois January 2026.15

Section 174 R&D capitalization (in effect 2022-2024) created a non-cash earnings drag that some buyers under-counted. The One Big Beautiful Bill Act (OBBBA, July 2025) reversed it permanently for domestic R&D — but foreign R&D still amortizes over 15 years. Targets with 2022-2024 R&D may have refunds in flight at close, with 6-12+ month refund timing that the buyer's financial model should reflect. The Section 174 small-business retroactive election deadline is July 6, 2026.15

The fix: State-by-state sales tax nexus voluntary disclosure analysis before close. Quantify any 2022-2024 amended-return refund opportunity in the financial model. For founder-led businesses with succession exposure, model the gift/estate tax shadow on family-controlled equity. See the tax due diligence checklist for the full state-by-state framework.

Mistake 11: UFLPA and EU CSDDD Supply-Chain Misses

The supply-chain mistake is to skip Tier 2 and Tier 3 supplier mapping on a target with raw-material exposure to Xinjiang or to in-scope EU operations.

UFLPA enforcement turned aggressive in August 2025. DHS released the 2025 UFLPA Strategy Update on August 19, 2025. The high-priority sector list expanded from 8 to 13 (adding caustic soda, copper, lithium, red dates / jujubes, and steel). The Entity List grew from 66 to 144 Chinese entities. CBP has examined 16,000-plus shipments worth nearly $3.7 billion since the rebuttable presumption took effect.16

EU CSDDD Omnibus published in the Official Journal February 26, 2026 (Directive (EU) 2026/470, in force March 18, 2026). The liability regime was removed, fines capped at 3% of global net turnover, transposition deadline pushed to July 26, 2028, application July 26, 2029. In-scope Phase 1 companies have more than 5,000 employees AND more than €1.5 billion in revenue.16

The fix: Polysilicon, cobalt, cotton, steel, and lithium-tier supply chain trace to country-of-origin for any target with Xinjiang-adjacent sourcing. Pre-close UFLPA exposure scoring with Tier 1, 2, and 3 supplier audits. For EU-exposed targets above €1.5 billion in revenue, factor CSDDD compliance build cost into the integration model.

Mistake 12: R&W Insurance Sizing and Survival-Period Mismatch

The R&W insurance mistake is to take coverage at typical 10% of deal value when the actual tail risk (especially cyber, tax, environmental) exceeds it — and to let the contractual survival period expire before the policy's 3-year tail captures the claim.

The data: Marsh's 2025 Global Transactional Risk Insurance Report ended three years of declining rates with North America primary R&W rates up 16% YoY, Asia +8%, driven by record M&A volume (~$5 trillion globally, 70 deals greater than $10 billion). Marsh placed $91.6 billion in transactional risk limits in 2025, up 34% YoY. North America total claims payments hit a record high.17 Gallagher's 2025 data shows ~20% of policies generate a claim notification, but only ~4% result in payment — among paying claims, 1 in 4 hits the full policy limit. ABA's Canadian Private Target Study (February 2025) found 49% of RWI claims occur greater than 12 months post-close (20% at 12-18 months, 7% at 18-24 months, 22% greater than 24 months).18

The fix: Stack R&W limits to at least 15% of deal value for tech, healthcare, or cyber-exposed targets. Purchase a specific excess layer for known-issue categories (e.g., a $25 million cyber-specific layer above a $50 million general layer). Match the R&W tail period to or beyond the longest reasonable claim discovery window. See the reverse termination fee framework for cost-side detail.

Frame 1: The Confirmation Bias Cliff (Visualizing The Curve)

The Confirmation Bias Cliff is the probability shift where DD findings are no longer being properly priced into the deal. The shift is not linear — it has three steep drops.

| Deal stage | Buyer willingness to walk on negative DD | Anchor |

|---|---|---|

| Pre-LOI | High (above 70%) | Pre-commitment phase |

| Post-LOI, pre-board approval | Medium-High (about 50%) | Risk-quantification phase |

| Board-approved | Medium (about 30%) | Will reprice, rarely walks |

| Publicly announced | Low (below 15%) | Political cost of walking dominates |

The 70% deal-failure rate is partly a function of the cliff: by the time material findings surface, the cost of walking has compounded so heavily that buyers absorb the cost into the deal terms rather than walking. McKinsey, KPMG, Bain, and Deloitte all converge on the structural finding.1

Frame 2: The DD Theater Trap (The 90-Second Test)

The DD Theater Trap is detected with three questions. Ask any deal team:

- What are the top 5 DD findings?

- Who specifically owns the resolution of each?

- What is each finding's dollar-impact estimate?

If the team can't answer all three in under 90 seconds, you have DD Theater. SmileDirectClub is the canonical case: all signals were public (negative EBITDA every year since 2017, $499M assets vs $1B+ liabilities, active Align IP litigation), but no buyer or institutional investor synthesized them into a top-5 memo with named owners and dollar estimates.6

The 90-Second Test is a partner-level diagnostic. It is not a checklist replacement — it is a synthesis test. The team that fails it has not done the DD; the team that passes it has the institutional knowledge to defend the price.

Frame 3: The Working Capital Wedge (Quantified)

The Working Capital Wedge sits at the center of post-close $$ disputes. SRS Acquiom 2025 data:9

| Statistic | Value |

|---|---|

| Median PPA escrow | About 1% of transaction value |

| PPA claims exceeding 1% | About 24% |

| Pro-buyer negative adjustments | 55% of deals |

| Pro-seller positive adjustments | 35% of deals |

| Buyer's calculation accepted in dispute | 7 in 10 |

| Working capital adjustments | Now in over 90% of deals (from 50% a decade ago) |

| Separate WC escrow | 75% of deals |

| Typical 1-3% EV swing | $500K (small deals) to $15M (large deals) |

The fix is methodological precision at LOI: lock the peg on identical methodology to the closing balance sheet, name the GAAP carve-outs, commission a WC-specific QoE supplement.

Frame 4: The Post-LOI Tunnel Vision Framework

Post-LOI Tunnel Vision is the three-stage psychological shift inside the deal team:

- LOI-signed: team treats DD as fact-finding (high willingness to walk).

- Board-approved: team treats DD as risk-quantification (medium willingness to walk; will reprice).

- Announced: team treats DD as problem-solving (low willingness to walk; will absorb).

The antidote: A pre-LOI "walk-away threshold" document signed by the investment committee, listing 5-7 specific findings that would force a walk regardless of stage. The Twitter / Musk case is the demonstration of what happens without an antidote: the binary "$54.20, period" framing eliminated all three stages and turned a $44 billion acquisition into a $19 billion asset within 12 months.3

Frame 5: The Cyber-DD Bain Test (Post-March 18, 2026)

The Cyber-DD Bain Test is a two-prong test for whether PE sponsors can be held directly liable for portfolio company cyber failures, derived from the S.D. Cal. March 18, 2026 PowerSchool ruling.7

Prong A — Pre-Close Adequacy: Did the sponsor conduct independent technical cyber DD (penetration test + dark-web scan + SaaS dependency map) before close? If not, latent vulnerabilities can be imputed to the sponsor as constructive knowledge.

Prong B — Post-Close Operational Direction: Did the sponsor direct cost cuts, offshoring, or workforce reductions in cybersecurity or IT post-close that materially weakened the breach response? If yes, the sponsor crosses from "passive investor" to "agent" in plaintiffs' theory.

What changed in May 2026 versus April 2026:

- The "investor as bystander" defense no longer holds at the motion-to-dismiss stage.

- Sponsor-level negligence is now a discoverable theory; expect plaintiff lawyers to subpoena fund-level cybersecurity policies and DD memos.

- R&W policies likely do NOT cover sponsor-level direct claims — different policyholder.

- Expect fund LPAs and side letters to start including "cyber DD standard" representations from the GP to the LPs.

What Did the Capri-Tapestry Walk Teach About Reverse Termination Fees?

The cleanest 2024 case study in reverse-termination-fee gaps is the Capri / Tapestry $8.5 billion deal that died November 14, 2024 when the FTC blocked it. The lesson is structural: a regulatory MAE must pay out at the level of expected antitrust-block damages, because no break fee was payable when the regulator killed the deal.

The Capri / Tapestry $8.5 billion walk on November 14, 2024 is the cleanest 2024 case study in reverse-termination-fee gaps. Sequence: FTC moved to block April 2024 to preliminary injunction October 24, 2024 to Tapestry terminated November 14, 2024. Capri would have owed Tapestry a $240 million termination fee if Capri had walked — but no break fee was payable when the regulatory block killed the deal. Tapestry agreed to expense reimbursement of approximately $45 million only.19

For comparison: Amazon paid a $94 million break fee on iRobot (~6.7% of deal value); Exxon-Pioneer included a roughly $1.8 billion termination fee (~2.8% of $64.5 billion). Antitrust reverse break-up fees now typically run 4-7% of deal value. Discover-Capital One notably excluded a regulatory termination fee.19

The fix at LOI: Negotiate the regulatory termination fee at the LOI stage. Refuse to sign a definitive agreement without a regulatory MAE that pays out at the level of expected antitrust-block damages.

Honest Comparison: Which Data Room Tool Fits Buyer-Side DD?

Different buyer-side DD profiles fit different data room platforms. We use Peony, obviously, but the honest mapping is:

| Buyer profile | Best fit | Reason |

|---|---|---|

| $200M+ cross-border banker-managed | Datasite, Intralinks | 25+ years of enterprise-DD workflow; Datasite now owns Firmex |

| Mid-market PE / strategic, AI-accelerated review | Peony | AI auto-indexing 3 min; AI Q&A across 1,500-4,500 docs; per-investor watermarks |

| Founder-led light DD, Series A-B | Papermark, DocSend, Peony | Lower-cost; faster setup |

| Highly regulated (defense, healthcare) | iDeals, Intralinks | Hardened compliance certifications |

For mid-market and growth-equity buyers who care about AI-accelerated DD and per-bidder analytics, Peony is purpose-built for the workflow. For $200M+ cross-border deals where the M&A bank is the process owner, Datasite or Intralinks remain the conservative defaults.

What Five Other Mistakes Almost Made the Top 12?

Five additional DD mistakes that fall short of "top 12" but still kill deal value:

- Treating QoE as one-and-done. Quality-of-earnings should be refreshed if the financials roll forward more than 90 days. Stale QoE leaves working-capital and revenue-recognition adjustments untested at signing.

- Skipping site visits on industrial targets. A factory tour catches what the data room cannot: equipment age, throughput-vs-capacity reality, workforce morale signals.

- Underpricing key-person retention. When the founder-CEO is the customer-relationship anchor, a $2M retention package can save a $50M deal.

- No 100-day integration plan signed at signing. Hertz-Dollar Thrifty's $170M integration miss traces to a plan written post-close instead of pre-signing.

- No pre-close regulatory interview matrix. For fintech / healthcare / data-heavy targets, this is the difference between knowing about a Wells Notice and being surprised by one.

What Else Do Buyers Ask About DD Mistakes?

Is due diligence still worth doing if the deal closes in 30 days? Yes. A 30-day DD is constrained but still catches the top 5 material items if the team uses the 90-Second Test and prioritizes. The mistake is skipping DD because the timeline is short; the fix is sequencing DD to surface walkable findings in the first 7 days.

How do I avoid Post-LOI Tunnel Vision on my own deal? Pre-LOI walk-away threshold document signed by the investment committee. Five to seven specific findings that would force a walk regardless of board approval or announcement. The document is a commitment device against the cliff.

Should I always buy R&W insurance? For deals greater than $25M with cyber, tax, or environmental exposure: yes, almost always. The 4% pay-out rate and the 1-in-4 full-limit hit pattern make it a high-leverage tail-risk hedge. Below $25M with clean financials and short survival periods, the math is less compelling.

What's the single biggest synthesis question to ask the deal team? "What are the top 5 DD findings, who owns the resolution of each, and what is each one's dollar estimate?" If the team can't answer in 90 seconds, you have DD Theater.

Why Does Peony Fit the Buyer-Side DD Workflow?

Peony is one of several data room platforms for managing buyer-side DD — not the only fit for every deal. For mid-market and growth-equity buyers, the workflow advantages compound:

- AI auto-indexing organizes 1,500-4,500-document data rooms into structured folder trees in under 3 minutes, eliminating the first-week manual prep that traditionally delayed substantive review.

- AI extraction lets analysts ask cross-document questions like "list every customer contract with a change-of-control clause and quote the supporting language" across thousands of files.

- Per-investor watermarks track which version of a document each internal stakeholder read.

- Screenshot protection prevents sensitive findings from leaking outside the data room — capture attempts are blocked and logged.

- NDA gates with integrated e-signatures stage sensitive confirmatory-DD documents behind a signed CA.

- Page-level analytics show exactly which buyer-team members read which sections — useful when the deal lead needs to confirm the cyber DD owner actually read the breach-history disclosure rather than skimmed the cover page.

Peony Data Room at $52 per admin per month gives unlimited data rooms with AI Q&A across all uploaded DD documents. Over 5,900 customers use Peony for M&A, fundraising, and DD workflows.

For $200M+ cross-border deals where the M&A bank is the process owner, Datasite or Intralinks remain the conservative defaults — their legacy reflects 25+ years of enterprise M&A workflow design. For early-stage and Series A-B fundraising data rooms, Papermark or DocSend can fit lighter workflows.

Related Reading in the DD Cluster

- M&A Due Diligence Process Guide — the canonical end-to-end process map

- Due Diligence Cost Breakdown — workstream-by-workstream cost ranges

- Cybersecurity Due Diligence — the 5-axis breach-readiness matrix and full Bain Test

- Third-Party Due Diligence — 5-jurisdiction exposure map post-FCPA-pause

- Vendor Due Diligence Checklist — procurement-led TPRM workflow

- Tax Due Diligence Checklist — state-by-state nexus framework

- Investment Due Diligence Checklist — VC and growth-equity DD lens

- Due Diligence for IPO — 3-Layer DD Stack and 135-Day Rule

- Due Diligence Questionnaire — DDQ structure and response workflow

Footnotes and Sources

Footnotes

-

McKinsey & Company, "Where mergers go wrong" — https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/where-mergers-go-wrong ; KPMG 2023 M&A study and Deloitte 2025 M&A Trends Survey — https://www.deloitte.com/us/en/about/press-room/dealmakers-prepare-and-pivot-for-m-a-activity-in-2025.html ; BCG, "Why Deals Fail" — https://www.bcg.com/publications/2015/why-deals-fail . ↩ ↩2 ↩3

-

Bain & Company, "Looking Back at M&A in 2025: Behind the Great Rebound" (Global M&A Report 2026) — https://www.bain.com/insights/looking-back-m-and-a-report-2026/ . ↩

-

Variety, "Elon Musk Misled Twitter Investors Ahead of His $44 Billion Takeover in 2022, Jury Finds" (2026) — https://variety.com/2026/digital/news/elon-musk-misled-twitter-investors-jury-verdict-1236695824/ ; Harvard PON, "M&A Negotiation Strategy: Missed Opportunities in Musk's Twitter Deal" — https://www.pon.harvard.edu/daily/business-negotiations/ma-negotiation-strategy-a-better-deal-for-musk-and-twitter/ . ↩ ↩2 ↩3

-

FourWeekMBA, "What Happened To Hertz" — https://fourweekmba.com/what-happened-to-hertz/ . ↩

-

Harvard Business Review, "Deals Without Delusions" — https://hbr.org/2007/12/deals-without-delusions ; Knowledge at Wharton, "Why Many M&A Deals Fail – and How to Beat the Odds" — https://knowledge.wharton.upenn.edu/article/why-many-ma-deals-fail-and-how-to-beat-the-odds/ . ↩

-

CNN Business, "SmileDirectClub shuts down after filing for bankruptcy" — https://www.cnn.com/2023/12/09/business/smiledirectclub-shutdown-bankruptcy/ ; Bloomberg Law, "Insiders Looted SmileDirectClub Before Its Failure, Trustee Says" — https://news.bloomberglaw.com/bankruptcy-law/insiders-looted-smiledirectclub-before-its-failure-trustee-says . ↩ ↩2 ↩3

-

Womble Bond Dickinson, "Unprecedented: Private Equity Firm Potentially on Hook for Portfolio Company's Data Breach" (March 2026) — https://www.womblebonddickinson.com/us/insights/alerts/unprecedented-private-equity-firm-potentially-hook-portfolio-companys-data-breach ; Hausfeld, "Court denies motions to dismiss in PowerSchool Data Breach Litigation" — https://www.hausfeld.com/news/court-denies-motions-to-dismiss-in-powerschool-data-breach-litigation . ↩ ↩2 ↩3

-

Cybersecurity Dive, "UnitedHealth's cyberattack response costs to surpass $2.3B this year" — https://www.cybersecuritydive.com/news/unitedhealths-cyberattack-costs-23b/721579/ ; BlackFog, "The Change Healthcare Ransomware Attack: A Landmark Cybersecurity Breach" — https://www.blackfog.com/change-healthcare-landmark-cybersecurity-breach/ . ↩

-

SRS Acquiom, "2025 M&A Working Capital Purchase Price Adjustment (PPA) Study" — https://www.srsacquiom.com/our-insights/working-capital-adjustment-study/ ; SRS Acquiom, "2025 Deal Terms Study" — https://www.srsacquiom.com/our-insights/deal-terms-study-2025/ . ↩ ↩2 ↩3

-

Wall Street Prep, "Customer Concentration Risk" — https://www.wallstreetprep.com/knowledge/customer-concentration/ ; ScienceDirect, "Customer concentration and M&A performance" — https://www.sciencedirect.com/science/article/abs/pii/S0929119921001425 . ↩ ↩2

-

Harvard Law CorpGov, "Chancery Court Applies Conditional Probability to Calculate Damages in Earnout Dispute" (July 13, 2025) — https://corpgov.law.harvard.edu/2025/07/13/chancery-court-applies-conditional-probability-to-calculate-damages-in-earnout-dispute/ ; Cooley, "4 Tips for Drafting Earnouts To Avoid Disputes" — https://www.cooley.com/news/insight/2024/2024-06-21-4-tips-for-drafting-earnouts-to-avoid-disputes . ↩ ↩2 ↩3

-

Brownstein Hyatt Farber Schreck, "Jaw-Dropping Development at the SEC: Coinbase Receives Wells Notice" — https://www.bhfs.com/insights/alerts-articles/2023/jaw-dropping-development-at-the-sec-coinbase-receives-wells-notice ; NY DFS, "Superintendent Adrienne A. Harris Secures $40 Million Settlement with Block, Inc." (April 10, 2025) — https://www.dfs.ny.gov/reports_and_publications/press_releases/pr202504101 . ↩ ↩2

-

Black Duck (Synopsys), "2026 Open Source Risk in M&A by the Numbers" — https://www.blackduck.com/content/dam/black-duck/en-us/whitepapers/wp-risk-ma-numbers.pdf ; Nixon Peabody, "Open Source Software Risks and Best Practices in M&A" — https://www.nixonpeabody.com/insights/articles/2025/10/15/open-source-software-risks-and-best-practices-in-ma . ↩ ↩2

-

Carta, "What is a 409A Valuation?" — https://carta.com/learn/startups/equity-management/409a-valuation/ ; Outlex, "IP Assignment for Startups: Essential Guide for Founders" — https://outlex.ai/blog/ip-assignment-startup-founders . ↩

-

Sales Tax Institute, "Economic Nexus State Chart" — https://www.salestaxinstitute.com/resources/economic-nexus-state-guide ; Cherry Bekaert, "Section 174 Repeal: R&E Expensing in 2025" — https://www.cbh.com/insights/articles/section-174-repeal-re-expensing-in-2025/ . ↩ ↩2

-

U.S. Customs and Border Protection, "Uyghur Forced Labor Prevention Act" — https://www.cbp.gov/trade/forced-labor/UFLPA ; DHS, "2025 Updates to the Strategy to Prevent the Importation of Goods Mined, Produced, or Manufactured with Forced Labor" — https://www.dhs.gov/2025-updates-strategy-prevent-importation-goods-mined-produced-or-manufactured-forced-labor-peoples ; Covington Global Policy Watch, "EU CSDDD/CSRD Omnibus Published in Official Journal" — https://www.globalpolicywatch.com/2026/02/eu-csddd-csrd-omnibus-published-in-official-journal-transposition-delegated-acts-and-guidelines-are-next/ . ↩ ↩2

-

Insurance Business Magazine, "R&W insurance premiums rise sharply as mega deals hit record levels - Marsh" — https://www.insurancebusinessmag.com/us/news/claims/randw-insurance-premiums-rise-sharply-as-mega-deals-hit-record-levels--marsh-569262.aspx . ↩

-

Fasken, "Trends in Representations and Warranties Insurance (RWI) in North American Private M&A" — https://www.fasken.com/en/knowledge/2025/10/trends-in-representations-and-warranties-insurance ; Law360 Insurance Authority, "R&W Insurance Claim Frequency Expected To Normalize" — https://www.law360.com/insurance-authority/specialty-lines/articles/1513044/r-w-insurance-claim-frequency-expected-to-normalize . ↩

-

FTC, "FTC Moves to Block Tapestry's Acquisition of Capri" — https://www.ftc.gov/news-events/news/press-releases/2024/04/ftc-moves-block-tapestrys-acquisition-capri ; Tapestry Inc., "Announces Termination of Merger Agreement With Capri Holdings Limited" — https://tapestry.gcs-web.com/news-releases/news-release-details/tapestry-inc-announces-termination-merger-agreement-capri/ ; Houlihan Lokey, "2024 Transaction Termination Fee Study" — http://cdn.hl.com/pdf/2025/2024-transaction-termination-fee-study.pdf . ↩ ↩2