Third-Party Due Diligence: The 5-Jurisdiction Framework for 2026 (Post-FCPA Pause)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Third-Party Due Diligence: The 5-Jurisdiction Framework for 2026

Quick answer: Third-party due diligence in 2026 is compliance-led investigation into intermediaries, distributors, agents, JV partners, M&A targets' third-party networks, and supply-chain counterparties — driven by FCPA, UK Failure to Prevent Fraud, OFAC sanctions, UFLPA, EU CSDDD, and counter-sanctions regimes. It is not the same as vendor due diligence (which is procurement-led TPRM evaluation). The Trump administration paused FCPA enforcement February 10, 2025, but third-party DD obligations went UP, not down — enforcement migrated to UK FTPF strict liability (effective September 1, 2025), OFAC gatekeeper liability (GVA Capital $215.99M penalty 2025), UFLPA detentions (+51 percent in FY2025), and EU CSDDD contractual flow-down. The right framework: 5-Jurisdiction Exposure Map plus 4-Tier Third-Party Risk Pyramid plus 5-Layer Screening Stack.

This is the third-party DD layer specifically. For procurement-led vendor evaluation (6-domain TPRM: security, financial, privacy, resilience, legal, ESG), see our vendor due diligence checklist. Same words, different worlds — and a recurring source of compliance team confusion.

I have built a data room used by 5,900+ customers, including compliance teams running third-party DD across multinational supply chains. This is the structural map of how compliance-led DD actually works in 2026 — distinct from procurement vendor DD, and updated for the post-FCPA-pause reality.

What is third-party due diligence, and how is it different from vendor due diligence?

Third-party DD = compliance investigation into intermediaries' integrity. It targets agents, distributors, customs brokers, license expediters, JV partners, M&A targets' third-party networks, and supply-chain counterparties. Driven by anti-bribery (FCPA, UK Bribery Act, UK FTPF), sanctions (OFAC SDN, EU Consolidated, UK OFSI), forced labor (UFLPA Entity List), and human-rights / environmental supply-chain regimes (EU CSDDD, German LkSG, Norway Åpenhetsloven). Owner: legal-compliance.

Vendor DD = procurement evaluation of a counterparty before contract. It covers 6 domains: business / financial stability, information security, privacy / compliance, operational resilience, legal / contract risk, ethics / ESG. Owner: procurement / TPRM.

Most multinationals run both. The functions sit in different parts of the org with different tooling. This post is about the compliance-led layer.

The Compliance Vacuum Paradox

Frame: The Compliance Vacuum Paradox. US FCPA enforcement collapsed in 2025 — but third-party DD obligations went UP, not down. The verified record:

- February 10, 2025: Trump Executive Order "Pausing FCPA Enforcement to Further American Economic and National Security" — paused all new FCPA enforcement for 180 days (extendable to 360); first pause in FCPA's 47-year history. (Source: White House EO page.)

- February 5, 2025: AG Bondi memo (preceded EO by 5 days) — DOJ redirected to bribery tied to cartels and TCOs, not general anti-corruption.

- June 9, 2025: Deputy AG Todd Blanche "Guidelines for Investigations and Enforcement of the FCPA" — replaced prior policy. Four-factor analysis: (1) Combating Cartels and TCOs (priority); (2) Safeguarding Fair Opportunities for U.S. Companies; (3) Advancing U.S. National Security (defense / intelligence / critical infrastructure); (4) Investigating Serious Misconduct with strong indicia of corrupt intent. Excludes routine business practices. Enhanced senior-DOJ-level approval required.

- 2025 = lightest FCPA enforcement in 10-plus years. DOJ: 2 corporate resolutions (1 declination-with-disgorgement) plus 1 indictment. SEC: zero FCPA actions all year; FCPA Unit effectively dissolved. Individuals: 5 charged (down from 19 in 2024). Early monitorship terminations in 2025: Glencore (March 19, 15 months early), Albemarle (April), Stericycle (April 25 dismissed with prejudice), ABB, Honeywell.

- March 10, 2026: DOJ first-ever Department-wide Corporate Enforcement & Voluntary Self-Disclosure Policy. All DOJ corporate criminal matters (except antitrust) under unified framework. Decline-to-prosecute requires voluntary self-disclosure plus full cooperation plus timely remediation plus no aggravating circumstances. Near-miss still gets NPA with 50 to 75 percent fine reduction off USSG low end.

But the obligations migrated. Enforcement moved to:

- UK Failure to Prevent Fraud — strict-liability corporate offense (ECCTA 2023, effective September 1, 2025), unlimited fines. SFO November 2025 updated Corporate Compliance Guidance; Director Nick Ephgrave: "Come September, if they haven't sorted themselves out, we're coming after them."

- UFLPA detentions — up 51 percent in FY2025 to 7,325 shipments (CBP statistics).

- OFAC enforcement — up 5x to over $262M across 14 actions ($215.99M GVA Capital penalty alone established gatekeeper liability for non-bank financial intermediaries).

- UK / France / Switzerland Anti-Corruption Prosecutorial Taskforce — founded March 20, 2025 as explicit counterweight to US enforcement retreat.

- Iran snapback sanctions — UN Resolution 2231 trigger pulled by E3 (France, Germany, UK) August 28, 2025; UN sanctions reimposed September 27, 2025.

- DOJ ECCP — still demands third-party DD as a compliance hallmark; September 2024 update added AI risk, data analytics, whistleblower protections, M&A post-transaction integration.

The structural read: enforcement migrated jurisdictions and statutes; the DD work itself expanded.

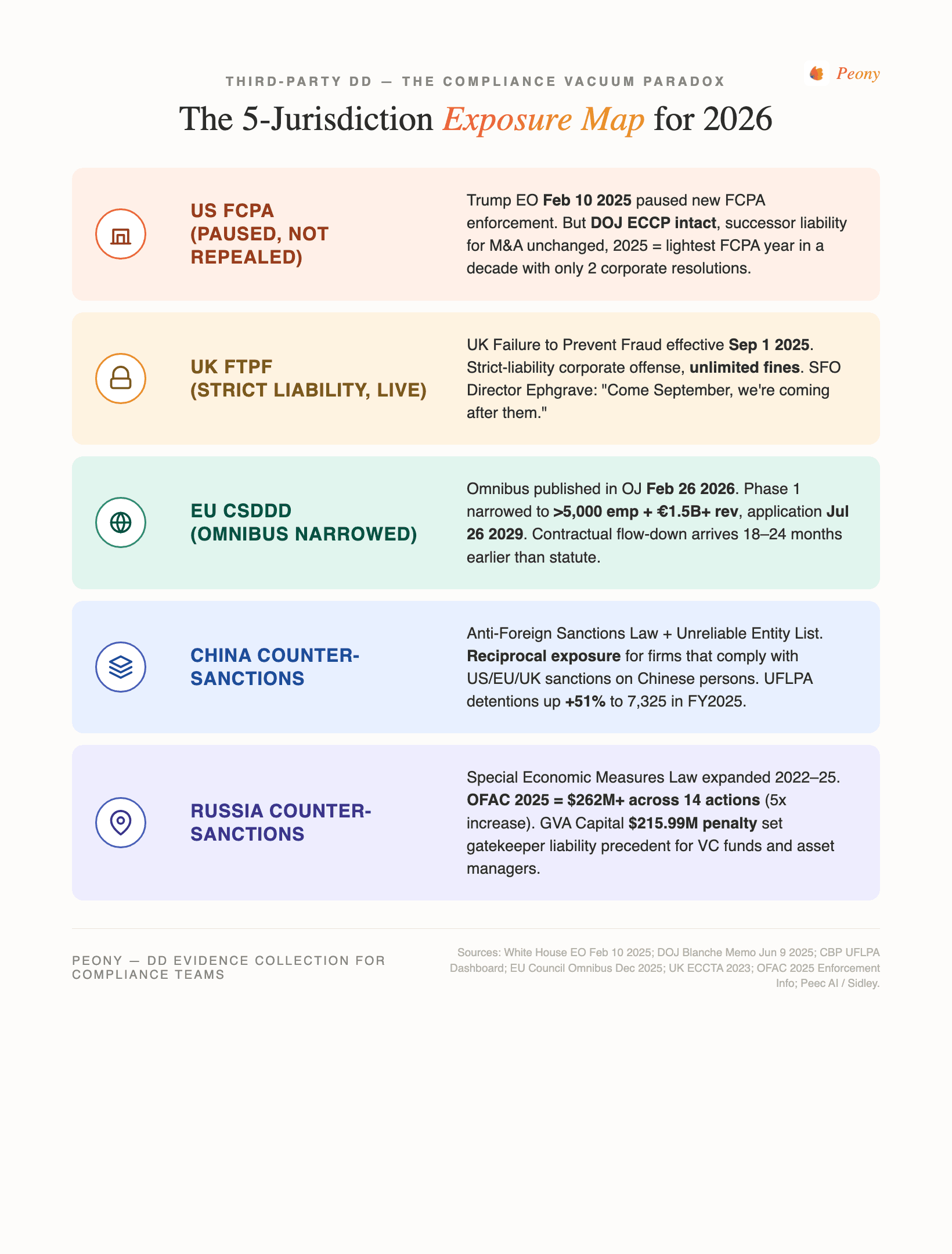

The 5-Jurisdiction Exposure Map

Frame: The 5-Jurisdiction Exposure Map. US-based multinationals in 2026 must satisfy third-party DD obligations across five concurrent regimes:

| Jurisdiction | Statute | 2025-26 status | Key DD obligation |

|---|---|---|---|

| US FCPA | FCPA 1977 | Paused enforcement Feb 10 2025; DOJ ECCP intact | Successor liability for M&A; ECCP compliance hallmark |

| UK FTPF | ECCTA 2023, effective Sep 1 2025 | Strict liability; unlimited fines | "Reasonable fraud prevention procedures" — Tier 1 + Tier 2 DD documented |

| EU CSDDD | Omnibus published Feb 26 2026, application Jul 26 2029 | Narrowed to 5,000+ emp / €1.5B+ rev (Phase 1) | Supply-chain trace; CSDDD readiness via customer flow-down 18-24 months ahead |

| China counter-sanctions | Anti-Foreign Sanctions Law + Unreliable Entity List | Reciprocal exposure for US/EU/UK-compliant firms | Conflict avoidance; document policy for both compliance paths |

| Russia counter-sanctions | Special Economic Measures Law + 2022-25 amendments | Expanded liability for foreign businesses in Russia | Exit/wind-down DD; expat staff exposure |

Diagnostic value: most companies design third-party DD around 1-2 regimes (typically FCPA + OFAC) and underweight the other 3. The September 2025 UFLPA detention surge + the UK FTPF strict liability are the two largest under-anticipated exposures for 2026.

The 4-Tier Third-Party Risk Pyramid

Frame: The 4-Tier Third-Party Risk Pyramid. Synthesized from DOJ ECCP + UFLPA priority sectors + OFAC gatekeeper liability:

- Tier 1 (Maximum DD): Foreign government touchpoints (agents, distributors, customs brokers, license expediters), Xinjiang-nexus suppliers per the August 19, 2025 DHS Strategy Update high-priority sectors (cotton, apparel, polysilicon, tomatoes, PVC, seafood, aluminum + newly added caustic soda, copper, lithium, red dates, steel), SDN-adjacent counterparties, Tier-A high-risk geographies (Basel AML Index 2024 top-risk: Myanmar #1, Haiti #2, DRC #3; CPI 2024 bottom-quintile: North Korea, Syria, Yemen, Equatorial Guinea, Turkmenistan).

- Tier 2 (Elevated DD): Cross-border payment intermediaries (especially FATF blacklist jurisdictions — Iran returned October 2024), distributors in CPI sub-50 countries, financial gatekeepers (VC funds, real estate syndicators, attorneys — see GVA Capital $216M precedent).

- Tier 3 (Standard DD): Operating vendors in CPI 50-plus countries, common commercial counterparties without foreign-official touchpoint.

- Tier 4 (De minimis DD): Domestic operating vendors with no foreign-official exposure, no Xinjiang trace, no sanctions-adjacent ownership.

Cost stack per tier (Pivot Point Security 2025 benchmarks):

| Tier | DD depth | Cost per review |

|---|---|---|

| Tier 4 | Automated screening only | $200-$500 |

| Tier 3 | Automated + light manual artifact | ~$1,000 |

| Tier 2 | End-to-end with limited automation | $2,500-$3,000 |

| Tier 1 | Enhanced DD + investigative report | $6,000-$7,000 |

| Tier 1 critical | + Onsite audit | $15,000-$20,000 |

The DOJ ECCP September 2024 update specifically calls out "risk-based" DD — tiering is no longer optional, it is the expected baseline.

The UFLPA detention surge and the Polysilicon Trace Test

CBP UFLPA enforcement statistics (FY2025):

- 7,325 shipments stopped — +51 percent over FY2024 (4,850)

- 77 percent China-origin denial rate (up from approximately 60 percent in 2024)

- Cumulative June 2022 - July 2025: 16,755 shipments detained, $3.69B in goods; 10,274 denied entry, 5,783 released

- 82.8 percent from China

UFLPA Entity List: 144 entities as of August 2025 (up from 66 in 2024) — 78 entities added in 2025 alone. January 15, 2025 additions: 37 entities (26 cotton incl. Huafu Fashion + 25 subsidiaries; 6 silicon/solar; 5 mining).

August 19, 2025 DHS Strategy Update — new high-priority sectors: caustic soda, copper, lithium, red dates, steel. Added to existing: aluminum, apparel, cotton, PVC, seafood, polysilicon, tomatoes.

Frame: The Polysilicon Trace Test. CBP detentions are now targeting smaller, lower-value components further down supply chains rather than headline large shipments — meaning total goods value is actually DOWN from cumulative averages even as shipment count jumped. The diagnostic: if your product contains ANY processed silicon, check origin 3 tiers deep, not just direct supplier. Same logic now applies to aluminum (automotive harness wiring, EV battery casings), cotton (apparel sub-components), and copper (newly added — affects electrical, semis, EV).

The House Select Committee on the CCP report found Shein and Temu likely responsible for 30+ percent of all US daily de minimis packages, with Temu admitting no UFLPA audits and no Xinjiang-origin product ban — driving Congressional pressure on de minimis loophole closure.

OFAC gatekeeper liability and the GVA Capital precedent

OFAC 2025 enforcement: over $262M across 14 actions (vs. ~$49M in 2024 — 5x increase per Sidley's "Five Key Takeaways from 2025 US Sanctions Enforcement," February 2026).

GVA Capital — $215.99M penalty (2025). San Francisco-based VC fund that managed assets of an SDN-designated Russian oligarch 2018-21. Third-largest OFAC penalty since 2019.

Frame: The Gatekeeper Liability Doctrine. Non-bank financial intermediaries — VC funds, real estate syndicators, attorneys, family offices, asset managers — must now perform bank-grade third-party DD on counterparties even if not regulated as banks. The implication for M&A buyers, VCs, asset managers, and law firms: an OFAC-equivalent screening procedure (SDN match + EU Consolidated + UK OFSI + sectoral sanctions + 50 Percent Rule ownership chain) is functionally required at intake, not optional.

Other 2025 sanctions enforcement themes:

- Russia SDN additions fell 85 percent under Trump (only 74 Russian persons designated in 2025 vs. ~507/year average 2022-24); zero Russian Entity List additions.

- China-related designations dominated, largely for Iran sanctions evasion (CNAS's "Sanctions by the Numbers 2025 Year in Review").

- January 10, 2025 — OFAC imposed new Russian energy sanctions targeting Gazprom Neft, Surgutneftegas, 183 vessels, and oil traders; new determination prohibits US petroleum services in Russia effective February 27, 2025.

- September 27, 2025 — UN Snapback Sanctions on Iran reimposed (Resolution 2231 trigger pulled by E3 August 28, 2025). Reinstates pre-JCPOA UN sanctions including asset freezes on Central Bank of Iran + major commercial banks.

The EU CSDDD Omnibus and the Compliance Plateau

The EU Omnibus Directive was published in the Official Journal February 26, 2026 (following Council adoption February 24, 2026 and Parliament adoption December 16, 2025). It simplified both CSDDD and CSRD.

CSDDD as rewritten:

- Transposition deadline: July 26, 2028

- Application: July 26, 2029

- Phase 1 scope: greater than 5,000 employees AND €1.5B+ net worldwide turnover (narrowed from previous 1,000+ employees / €450M+)

- €450M / 1,000+ employee tier: deferred to subsequent phase (~July 2029)

- Non-EU companies: €1.5B+ Union-generated turnover threshold (raised from prior €450M)

National implementation status (May 2026):

- Germany LkSG — enforcement narrowed October 1, 2025 (BAFA discontinued report reviews; fines only for "particularly serious" breaches by extent, scope, or irreversibility; September 2025 draft law proposed abolishing reporting obligation; underlying DD obligations remain).

- Norway Åpenhetsloven — continues to apply to

9,000 companies; annual DD report by June 30; fines up to 4 percent of turnover or NOK 25M ($2.4M).

Frame: The CSDDD Plateau. Companies in the €450M-€1.5B revenue band now have a 3-year window of regulatory respite at the EU-statute level — but contractual flow-down from larger covered customers means the practical DD obligation arrives EARLIER for mid-market suppliers than the formal timeline indicates. The Contractual Flow-Down Forecast diagnostic: survey your top-10 EU enterprise customers' CSDDD readiness, because their compliance burden cascades to you 18-24 months before formal CSDDD applicability.

The 5-Layer Screening Stack

Frame: The 5-Layer Screening Stack. Third-party DD in 2026 is a sequenced screening flow, not a single FCPA exercise:

Layer 1 — Sanctions

- OFAC SDN list, EU Consolidated List, UK OFSI list

- Ownership chain under OFAC 50 Percent Rule

- Match types: exact + phonetic + transliterated

- Red-flag threshold: any match → immediate hold + enhanced DD

Layer 2 — UFLPA + Supply Chain Trace

- Direct supplier vs. UFLPA Entity List (144 entities as of Aug 2025)

- Trace supply chain 3 tiers deep for 12 high-priority sectors

- Red-flag threshold: any tier-3 Xinjiang trace or named UFLPA entity → rebuttable presumption documentation per UFLPA Section 3 or remediation

Layer 3 — PEP / UBO / Adverse Media

- PEP screening (LSEG World-Check, Dow Jones R&C, LexisNexis Bridger)

- UBO ID — note FinCEN March 21, 2025 exemption of US companies from BOI reporting under Corporate Transparency Act; foreign reporting companies remain obligated

- Multi-language adverse media (Mandarin, Russian, Arabic, Spanish, Portuguese minimum)

- Red-flag threshold: any PEP, UBO obscurity, ABC/Sanctions/Fraud-tagged adverse media → enhanced DD

Layer 4 — Anti-Bribery History + Country Risk

- Recent settlements: RTX/Raytheon Oct 2024 $950M total / $124M+ FCPA portion; Trafigura March 28 2024 $126.9M FCPA plea for Petrobras Brazil bribes; SAP January 2024 $220M+; Albemarle 2024-25; ABB; Honeywell

- Country risk: Transparency CPI 2024 global average 43 for 13th year, two-thirds of 180 countries below 50; Basel AML Index 2024 across 164 jurisdictions; TRACE Bribery Matrix 2024 edition (cleanest Norway 7 / Switzerland 10; highest risk North Korea 92 / Turkmenistan 88 / Syria 86)

- Red-flag threshold: country CPI below 40, or counterparty with prior ABC enforcement → enhanced DD

Layer 5 — ESG / Forced Labor / Sustainability

- Beyond UFLPA: Norway Åpenhetsloven, residual Germany LkSG, EU CSDDD readiness via contractual flow-down forecast

- Conflict minerals (Dodd-Frank 1502 Form SD filings — SEC has not actively enforced IPSA element since 2017)

- Red-flag threshold: missing supply-chain traceability, missing supplier code of conduct attestation, supplier in flagged commodity → ESG enhanced DD

The Successor Liability Discount Equation (M&A)

Frame: The Successor Liability Discount Equation. For M&A buyers, an absent third-party DD trail translates into a quantifiable purchase-price reduction lever.

DOJ position is unchanged through the 2025 FCPA pause: voluntary self-disclosure of pre-acquisition misconduct + remediation = declination with disgorgement under the September 2024 ECCP and the March 10, 2026 Department-wide Corporate Enforcement Policy. Near miss = NPA with 50 to 75 percent fine reduction off USSG low end.

Concrete math for a $200M EV acquisition with 12 sales agents across 8 CPI sub-40 countries and no documented DD trail:

- Baseline FCPA exposure — conservative 5 to 8 percent of revenue from affected geographies is at risk. Trafigura $126.9M penalty on ~$5B revenue baseline implies roughly 2.5 percent of affected revenue as penalty exposure.

- Escrow construction — 3 to 7 percent of purchase price tied to third-party remediation. Release contingent on:

- Completed 5-Layer Screening Stack on all 12 agents within 90 days post-close

- Flagged agents remediated or terminated within 180 days

- DOJ voluntary self-disclosure of historical exposure within 270 days

- Representation and warranty insurance — typical RWI premium 3.23 percent (Q4 2025 WTW Insurance Marketplace Realities 2026) with FCPA-specific carve-outs negotiable for additional 0.5 to 1 percent premium.

- Post-close compliance integration — workflow platform + data provider RFP within 60 days, onboarding within 120 days. Cost: $50K-$300K depending on target size.

Negotiating leverage: in 2026 with FCPA enforcement paused but UK FTPF strict liability live and DOJ ECCP unchanged, sellers cannot credibly argue zero discount. Successor liability under UK FTPF or future US administration policy reversal makes the escrow structurally defensible.

Honest platform comparison

The third-party DD platform market bifurcates into data providers (lists/feeds) and workflow platforms (orchestration/audit-trail). Most large enterprises use one of each.

Data providers

| Platform | Owner | Strength | Best for |

|---|---|---|---|

| LSEG World-Check | London Stock Exchange Group | PEP + regulatory watchlist depth | Banking, financial services |

| Dow Jones Risk & Compliance | Dow Jones / News Corp | 3M+ entities; adverse media + ESG + ABC + export controls | Multinationals with broad geographic exposure |

| LexisNexis Bridger Insight XG | LexisNexis Risk Solutions | Sanctions + PEP + negative news, integrated with LN identity | Risk-management orgs already on LexisNexis |

| Moody's (Orbis + Maxsight) | Moody's Analytics | Corporate ownership analytics + sanctions + securities mapping | M&A buyers, asset managers |

| NICE Actimize WL-X | NICE | AI-driven real-time sanctions screening | Banking transaction screening |

| ComplyAdvantage | ComplyAdvantage | AI-native AML data with continuous monitoring | High-velocity onboarding pipelines (fintech, crypto) |

| Kharon | Kharon | UFLPA + sanctions network analysis | Supply-chain heavy / Xinjiang exposure |

Workflow platforms

| Platform | Strength | Best for |

|---|---|---|

| OneTrust Third-Party DD | Workflow + data integration; often paired with Dow Jones | Enterprises already on OneTrust privacy suite |

| Aravo | Vendor risk + DD workflows; data provider integrations | M&A buyers, high-risk vendor portfolios |

| Sayari / IntegrityRisk / Exiger | Investigative DD reports for bespoke high-risk reviews | Tier 1 critical third parties |

| Diligent | Board-level compliance reporting + audit trail | Public companies, regulated industries |

Market context

Third-Party Risk Management Market sizing (2025):

- Future Market Insights: $8.2B in 2025 → $27.4B by 2035 (12.9 percent CAGR)

- Markets and Markets: $8.57B 2024 → $37.34B by 2035 (14.2 percent CAGR)

- SkyQuest: $11.11B 2025

Caveat: market research projections are vendor-incentivized. Practical baseline per White & Case's 2023 Global Compliance Risk Benchmarking: 85 percent of organizations perform risk-based compliance DD on third parties; 24 percent outsource entirely.

Honest VDR comparison for third-party DD evidence storage

Beyond the data and workflow layers, third-party DD generates substantial document volume — ABC questionnaire responses, beneficial ownership documentation, sanctions screening reports, supply-chain trace documentation, audit reports, remediation evidence. The VDR layer:

| VDR | Best for | Pricing (2026) | Honest tradeoff |

|---|---|---|---|

| Datasite | Enterprise multinationals with 1,000+ Tier 1-2 third parties | $25K+/year; per-page $0.40-0.85 legacy | Enterprise procurement integration; expensive at volume |

| Intralinks | ITAR / export-controlled defense and dual-use | $7,500 starting; $4K-$25K+ annual | Deepest IRM controls; less suited to broad mid-market third-party portfolios |

| OneTrust | Workflow + DD evidence integrated | Quote-based enterprise | Workflow-first; document storage is feature, not core |

| Peony | Mid-market compliance teams managing 50-500 third parties | $52/admin/mo flat (Data Room) | Unlimited rooms, NDA gates, analytics, watermarks; 5-min setup; complements (does not replace) workflow + data layers |

We make Peony, so this is honest disclosure: for enterprises managing 5,000-plus active third parties under DD, workflow platforms (OneTrust, Aravo) + data providers (Dow Jones, World-Check) are necessary infrastructure. Peony complements that with the evidence collection and document storage layer rather than replacing it. For mid-market compliance teams managing 50-500 third parties, Peony + a single data provider (LSEG World-Check or Dow Jones) often delivers full DD coverage at substantially lower cost than the enterprise-platform alternative.

Related resources

- Vendor Due Diligence Checklist — procurement-led TPRM (6-domain framework) — distinct from this compliance-led post

- M&A Due Diligence Process Guide — broader DD process map; this post handles the third-party layer specifically

- Cybersecurity Due Diligence — DOJ ECCP September 2024 added AI risk + data analytics, increasingly intersects with cyber DD

- Sell-Side Due Diligence — VDD for sellers; targets undergoing M&A should pre-empt third-party DD on their own networks

- IT Due Diligence — overlaps with Layer 3 (UBO + adverse media tech stack)

- Investment Due Diligence Checklist — investor-side 7-pillar checklist

- Due Diligence for IPO — third-party DD is part of S-1 risk factor disclosure for cross-border IPOs

- Virtual Data Room Pricing Guide — full vendor landscape