38 Due Diligence Red Flags Across 6 Streams (2026): Severity Matrix + Walk Rate

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

I run cyber-DD on a $300M strategic-buyer deal where the target had 47 OAuth integrations across critical data sources — half undocumented, none rotated post-SalesLoft. The deal team's red flag inventory called it "vendor risk, medium." After cross-referencing the SalesLoft 700-org victim list against the target's integration map, "medium" became "do not close without 30-day post-close token rotation as a condition precedent." Three weeks later, the working-capital QoE supplement surfaced a $1.2 million peg gap, the legal team flagged a non-assignment clause in the top-2 customer contract, and the founder confirmed two senior engineers had given notice. By signing day the red flag inventory was 14 items deep across 6 streams, the Concentrated Trio test had failed twice, and the deal closed at a 7% lower price with $3 million carved out of R&W into a cyber-specific escrow. Due diligence red flags in 2026 are not the binary "kill or close" signal they were in 2019 — the SRS Acquiom 2025 data shows walk-away constructs collapsed from 18% to 11% YoY while undisclosed-liability claims doubled. The discipline shifted from "do we walk?" to "how do we structure?". I run Peony, a data room platform used by 5,900+ customers across M&A, private equity, and DD workflows. Backed by VCs including Target Global, this guide maps the 38 red flags across 6 DD streams with severity tiers, the Red/Orange/Yellow severity matrix, the Concentrated Trio test, the Bain Test for PE cyber liability, and the Walk Rate data on how buyers actually respond.

Quick answer: Due diligence red flags in 2026 cluster across six streams (financial, legal, commercial, operational, tech/cyber, ESG/regulatory) with 38 named flags total. The Red/Orange/Yellow severity matrix scores each flag on materiality (under 2% / 2-10% / over 10% of enterprise value) and curability (easily curable / indemnifiable / uncurable). Red — walk — only triggers when high materiality combines with uncurable risk. The Concentrated Trio test (customer over 30%, vendor over 70%, founder-essential) produces the cleanest binary deal-killer signal. Post-March 18, 2026, the Bain Test elevates cyber red flags from price-chip leverage to sponsor-level fiduciary exposure for PE buyers. Walk rates collapsed in 2025: no-survival R&W constructs dropped from 18% to 11% YoY while undisclosed-liability claims doubled — buyers are negotiating around red flags rather than walking.

The Walk-Rate Collapse: Why Red Flags Trigger Structure, Not Walks

SRS Acquiom's 2025 Deal Terms Study, covering more than 2,200 private-target deals valued at $505 billion, found that "no survival" walk-away R&W constructs fell from 18% in 2024 to 11% in 2025.1 Concurrently, undisclosed-liability claims doubled since 2022 and now account for 24% of all R&W indemnification claims.2

The proprietary inference: walking has gotten rarer because R&W insurance plus special indemnity plus escrow now absorb risks that would have killed deals in 2019. But this creates a delayed-explosion pattern — disputes shift from pre-close walk to post-close claim. R&W claim payouts hit record levels in 2025: Marsh placed $91.6 billion in transactional-risk limits, up 34% YoY, and AON's North America clients recovered over $1.4 billion through Q4 2024.34

The practical guidance: most red flags now don't trigger walks — they trigger structure. Walk only when (a) Red-severity per the matrix, (b) all three Concentrated Trio tests fail, or (c) the Bain Test cannot be satisfied for cyber or regulated-industry targets.

What Counts as a Red Flag in Due Diligence?

A due diligence red flag is any finding during the DD process that materially alters the buyer's risk-return calculation. The 2026 framework groups red flags across six streams:

- Financial — revenue recognition, customer concentration, working capital, debt covenants, deferred revenue mismatch, related-party transactions, cash burn rate

- Legal — pending litigation, IP ownership ambiguity, regulatory inquiries (Wells Notice, FTC, DOJ, OFAC), contract change-of-control, employee misclassification, non-compete enforceability

- Commercial — customer churn trend, single-customer dependency, contract renewal failures, win-rate decline, sales-pipeline coverage ratio, GTM dependency on departing leader

- Operational — key-person risk, single-vendor dependency, systems brittleness, capacity constraints, regulatory licenses lapsed, supplier concentration

- Tech / Cyber — undisclosed breach, OAuth integration sprawl, shadow AI usage, no SOC 2, key engineer departure, vendor supply-chain exposure

- ESG / Regulatory — UFLPA forced labor exposure, CSDDD compliance gap, environmental remediation cost, climate transition risk, governance issues

Inside each stream, individual flags scale across three severity tiers — Yellow (renegotiate price or terms), Orange (pause and condition signing on cure), Red (walk).

Stream 1: Financial Red Flags (7 Flags)

F-1. Revenue recognition aggression / ASC 606 non-compliance. QoE report reveals revenue booked before performance obligations met. Severity: Orange. Auditor restatement risk is the single biggest R&W claim severity driver — financial-statements breaches account for 37% of all W&I dollars paid per Marsh 2025.3

F-2. Customer concentration over 30% from a single customer. Top-10 schedule shows one logo over 30% of TTM revenue or top-5 over 60%. Severity: Red above 30% for PE/SBA; Yellow at 10-25%.5 Fix: walk if no alternative; otherwise structure 30-50% earnout tied to retention of the concentrated account.

F-3. Working capital target gamed / pre-close stuffing. AR aging stretched, deferred revenue accelerated to revenue, payables held, inventory dumped. SRS Acquiom 2025 found buyers' calculations accepted in 7 of 10 PPA disputes.6 Severity: Yellow to Orange. Fix: separate escrow specifically for WC adjustment (now 58% of deals per ABA 2025 Study); independent accounting referee.7

F-4. Deferred revenue / billings-revenue mismatch. Cash receipts exceed revenue recognized by an unexplained margin. The highest-frequency QoE finding in SaaS deals.8 Severity: Orange. Fix: QoE re-bridge of ARR to GAAP revenue; restrict purchase-price multiple to verifiable revenue.

F-5. Related-party transactions / undisclosed self-dealing. Vendor or customer entities owned by founder, board member, or family. Severity: Orange. This was the central FTX failure mode — Alameda/FTX entity-web overlap was flagged in Tiger Global's DD memo but did not block the $38M check.9

F-6. Cash burn rate vs runway misrepresentation. SmileDirectClub filed Chapter 11 in September 2023 and shut down in December 2023 with about $900M debt, having posted a $278M net loss in 2022.10 Severity: Red if runway under 6 months and unprofitable.

F-7. Debt covenants near tripping / springing covenants. Leverage covenant at 4.0x with TTM EBITDA trending toward 3.9x; undisclosed change-of-control acceleration in the credit agreement. Severity: Orange. Fix: lender waiver as condition to signing.

Stream 2: Legal Red Flags (7 Flags)

L-1. Pending litigation with damages over 10% of EV. Severity: Yellow with insurance/escrow; Red if uninsurable. Fix: special indemnity outside R&W cap.

L-2. IP ownership ambiguity. Code commits from contractors without signed assignment agreements; founder pre-incorporation work; university IP. Severity: Orange to Red if core IP affected. Fix: retroactive assignment agreements with consideration; carve-out indemnity.

L-3. Open-source contamination (GPL/AGPL in proprietary product). Software composition analysis reveals copyleft components shipped in commercial product or running as SaaS backend. Per Black Duck 2025 OSSRA, 30% of license conflicts stem from hidden dependencies. AGPL closes the SaaS loophole: network use triggers source-disclosure obligations.11 Severity: Orange.

L-4. Regulatory inquiries — Wells Notice, FTC second request, DOJ/OFAC subpoena. Block paid $175M+ to state regulators and CFPB in 2025 for BSA/AML failures.12 SEC dismissed many crypto Wells in early 2025 (Coinbase February 27, Robinhood Crypto February 24).13 Severity: Orange to Red.

L-5. Contract change-of-control / anti-assignment in top-10 customer contracts. Material customer contracts include change-of-control or anti-assignment with consent rights.14 Severity: Yellow to Orange. Fix: pre-close consent letters; consent-tax budget; price escrow for non-consenting customers.

L-6. Employee misclassification (1099 vs W-2, exempt vs non-exempt). Material contractor population doing core function; DOL/IRS in renewed enforcement push for 2025.15 Severity: Yellow. Average exposure $7,000-$15,000 per misclassified worker federal; over $100,000 in CA/NY when state penalties stack.

L-7. Non-compete enforceability post-FTC-rule-vacatur. FTC's 2024 rule was vacated by Texas court August 2024; FTC abandoned the appeal September 2025; California, North Dakota, Minnesota, and Oklahoma effectively ban employee non-competes.16 Severity: Yellow. Fix: replace non-competes with retention bonuses + non-solicits + gardening leave.

Stream 3: Commercial Red Flags (6 Flags)

C-1. Customer churn trend reversal. Net dollar retention dropping over trailing 4 quarters; gross logo churn accelerating; cohort retention curves bending negative. Severity: Orange.

C-2. Sales pipeline coverage ratio under 2.5x. Coverage below industry-normal threshold (3x to 4x for typical 25-33% win rates; 4-7x for enterprise; 7-10x for strategic mega-deals).17 A target showing pipeline at 2x against a 25% win rate implies a near-certain miss. Severity: Yellow to Orange.

C-3. Win-rate decline against a specific competitor. Win-loss data shows decline of 5+ percentage points YoY; named competitor winning over 60% of head-to-head deals in last 2 quarters. Severity: Yellow.

C-4. Contract-renewal failure in top accounts. Renewal rate below 90% in top-20 customers in last 12 months. Severity: Orange.

C-5. GTM dependency on a single rep, founder, or "GTM whisperer." Sales-by-rep concentration shows one closer over 40% of new ARR. Severity: Orange. Fix: retention package with vesting; non-solicit on departing reps.

C-6. Discounting acceleration / price compression. ASP declining quarter-over-quarter; list-to-net discount widening. Severity: Yellow.

Stream 4: Operational Red Flags (5 Flags)

O-1. Key-person risk — founder or CEO or CTO is irreplaceable. Customer references say "we bought because of [founder]"; CRM shows founder on over 30% of deal threads. Severity: Orange. When key employees leave post-close, institutional knowledge walks and customer relationships suffer.18 Fix: retention packages 25-50% of consideration in unvested equity over 3-4 years; cliff retention bonus at 12 and 24 months.

O-2. Single-vendor dependency. AWS/Stripe/Plaid is over 95% of cost-of-goods with no failover; or one supplier provides a critical input with no qualified second source. Severity: Yellow to Orange. Fix: architecture review; portability plan.

O-3. Systems brittleness / technical debt. Production incidents trending up; sub-100-engineer team running 8+ year-old monolith; uptime metrics not measured. Severity: Yellow. Fix: capex reserve; integration plan that absorbs re-platform cost.

O-4. Capacity / fulfillment constraints. Backlog growing while delivery times slip; manufacturing throughput at over 95% utilization with no expansion plan. Severity: Yellow.

O-5. Regulatory licenses expired / about to lapse. Money-transmitter license, broker-dealer registration, professional licenses with near-expiration or change-of-control triggers. Severity: Orange to Red if revenue depends on the license. Fix: pre-close renewal; consent letters with state regulators.

Stream 5: Tech / Cyber Red Flags (6 Flags)

T-1. Undisclosed data breach in last 24 months. Severity: Red post-PowerSchool/Bain. The March 18, 2026 S.D. Cal. ruling allowed Bain's negligence claims to proceed because the breach straddled the October 1, 2024 close — initial intrusions August 16 to September 17, 2024 using stolen vendor credentials, second intrusion December 19 to 28, 2024 discovered December 28, 2024, public disclosure January 7, 2025 — and Bain directed post-close offshoring of cybersecurity functions that allegedly enabled subsequent harms.19 Cyber claims now reach 42% deal-value impairment per FTI Consulting's March 2026 CISO Redefined III study.20 Fix: walk; or carve-out indemnity outside R&W cap with specific dollar reserve.

T-2. No SOC 2 / ISO 27001 / equivalent certification. Severity: Yellow unless enterprise customer base depends on it. Fix: remediation plan; reserve for compliance investment.

T-3. OAuth-token / third-party integration exposure (SalesLoft Drift pattern). Severity: Orange post-August 2025. The SalesLoft Drift breach affected 700+ orgs (Cloudflare, Google, PagerDuty, Palo Alto, Proofpoint, Zscaler) via stolen OAuth refresh tokens.21 Per Verizon DBIR 2025, third-party-involved breaches doubled YoY to 30%.22 Fix: OAuth-audit conditions to closing; reps on no-pending-third-party-breach-notifications.

T-4. Shadow AI / unsanctioned LLM usage. Employees using ChatGPT/Claude/Copilot without enterprise license; no DLP policy. Severity: Yellow. Per IBM 2025 Cost of a Data Breach, shadow AI adds $670K to average breach cost; 97% of AI-related incidents involved organizations lacking AI access controls.23

T-5. Key engineer / security lead departure in last 90 days. LinkedIn cross-check shows 2+ senior engineers left; security lead transition mid-DD. Severity: Orange. Fix: retention packages for remaining team; interim security consultant during integration.

T-6. Vendor supply-chain exposure (Snowflake / MOVEit pattern). Critical data residency in third-party SaaS without enterprise security review; vendor-risk register not maintained. Severity: Orange. Per IBM 2025, supply-chain compromise is the costliest breach vector.23

Stream 6: ESG / Regulatory Red Flags (5 Flags)

E-1. UFLPA / forced-labor supply-chain exposure. Tier-3 sourcing trace shows polysilicon, cotton, tomato, lithium, caustic soda, copper, red dates, or steel originating in Xinjiang or affiliated regions; supplier on UFLPA Entity List (144 entities, expanded August 2025 from 66 in 2024). Severity: Orange to Red. FY2025 CBP detained 7,325 shipments (+51% YoY); only roughly 6.5% ultimately released.24

E-2. CSDDD / CSRD compliance gap (EU-nexus deals only). Target has EU revenue or operations exposure; no human-rights-and-environmental due-diligence policy. Severity: Yellow currently — Omnibus I narrowed scope; CSDDD compliance now required only for companies with over 5,000 EU employees and over €1.5B EU revenue (non-EU companies require over €450M EU turnover); application date pushed to July 26, 2029.25

E-3. Environmental remediation cost / known-contamination site. Phase I/II environmental assessment reveals contamination; CERCLA exposure. Severity: Orange. Environmental claims tend to be long-tail, expensive, and uninsurable under R&W. Fix: carve-out the asset; specific indemnity outside R&W.

E-4. Climate transition risk / stranded asset exposure. Target operates in oil-gas, coal, cement, steel, or auto-ICE with 5+ year asset life and no decarbonization plan. Severity: Yellow.

E-5. Governance issues — board independence, related-party deals, dual-class structures. Board has no independents or independents are friends/family. Severity: Orange. This was the central FTX failure mode: no board, no CFO, no audit, SBF concentrated control.9

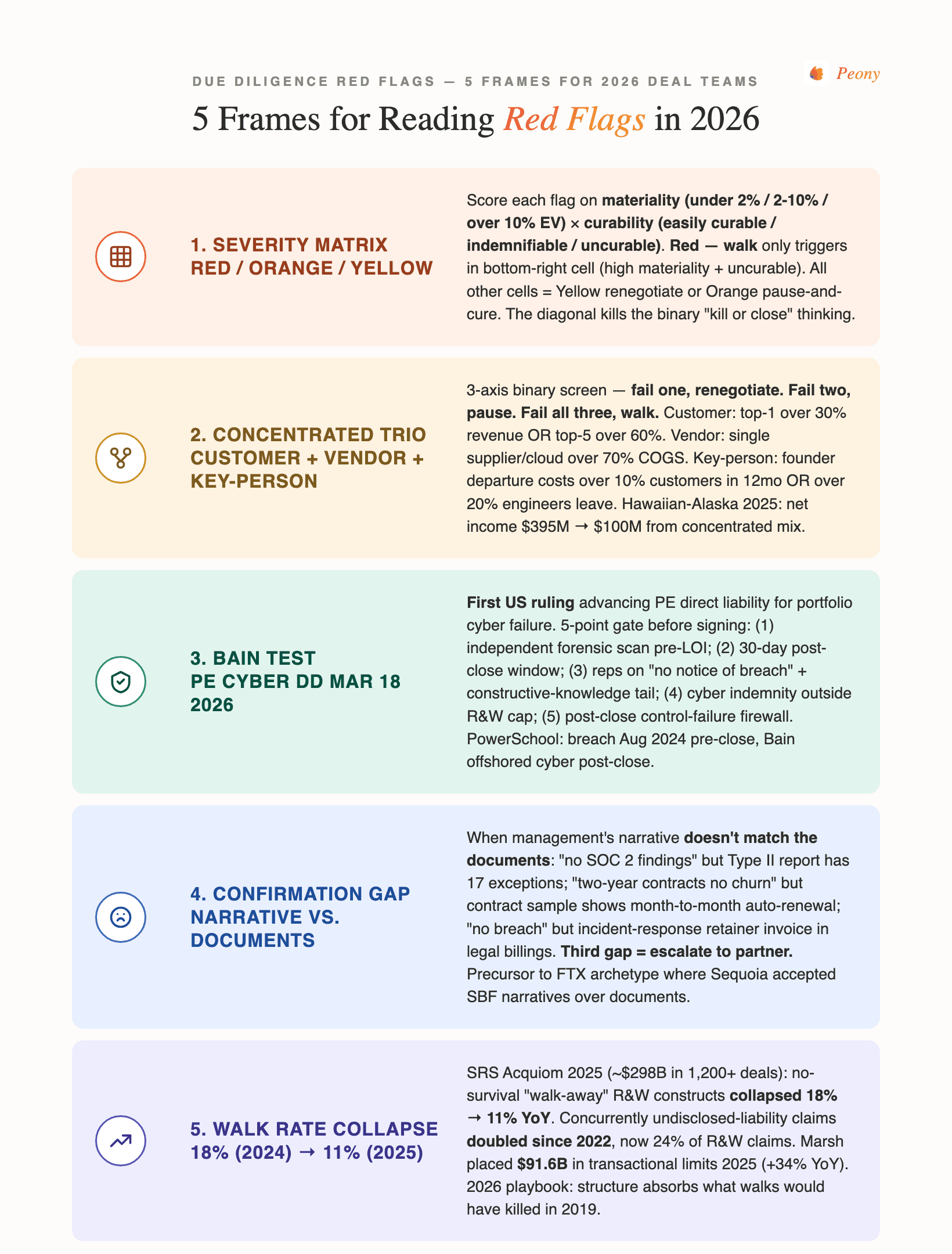

Frame 1: The Red / Orange / Yellow Severity Matrix

Score each red flag on two axes — materiality (low / medium / high) and curability (easily curable / indemnifiable / uncurable):

| Materiality \ Curability | Easily Curable | Indemnifiable | Uncurable |

|---|---|---|---|

| Low (under 2% EV) | Yellow — note in SPA | Yellow — escrow | Yellow — disclose |

| Medium (2-10% EV) | Yellow — fix pre-close | Orange — special indemnity | Orange — price cut |

| High (over 10% EV) | Orange — pause and condition | Orange — special escrow | Red — walk |

The Easily-Curable + Low + Uncurable region is where most "soft red flags" cluster. Red walks sit only in the bottom-right cell.

Frame 2: The Concentrated Trio Test

Three concentration tests — fail one, renegotiate. Fail two, pause. Fail all three, walk.

- Customer concentration: Top-1 customer over 30% of revenue OR Top-5 over 60%.5

- Vendor concentration: Single supplier/cloud/processor over 70% of COGS with no qualified alternate.

- Key-person concentration: Single founder/exec irreplaceable — defined as departure would (a) cost over 10% of customers in 12 months OR (b) cause over 20% of engineering team to leave.

The Concentrated Trio is the cleanest binary deal-killer test in mid-market SaaS DD. Hawaiian-Alaska 2025 integration losses — net income fell from $395M (2024) to $100M (2025), partly from Hawaiian-revenue mix exposure to single-market Hawaii tourism cycle — illustrate post-close concentration cost.26

Frame 3: The Bain Test (Post-March 18, 2026 PE Cyber-DD Standard)

Post the March 18, 2026 S.D. Cal. PowerSchool ruling, PE sponsors face direct liability for portfolio cyber failures rooted in pre-closing conduct. The Bain Test is a 5-point gating standard before signing:19

- Independent forensic scan, not seller-provided, before LOI binds.

- 30-day post-close window: discovery of any breach in this window now triggers sponsor-level liability discussion under the PowerSchool theory.

- Reps on "no notice of breach" plus a "no constructive knowledge" tail covering vendor/contractor-credential exfiltration.

- Specific cyber indemnity outside R&W cap, with carve-out from time-bar.

- Post-close control-failure firewall: any cyber/IT/eng decisions sponsor directs must go through documented governance — PowerSchool held Bain's offshoring directions actionable.

Frame 4: The Confirmation Gap

The single highest-yield qualitative red flag is when management's narrative in the meeting doesn't match the documents in the data room. Examples that have killed deals:

- Management said "no SOC 2 findings" — data room contains a Type II report with 17 exceptions.

- CEO claimed "two-year contracts, no churn" — contract sample shows month-to-month auto-renewal language.

- CFO presented EBITDA — QoE bridges out $4M of one-time adds the CFO described as "ongoing."

- Founder said "we never had a breach" — incident-response retainer invoice from prior CISO is in legal billings.

Detection rule: if the third Confirmation Gap surfaces, escalate to a partner-level decision on whether to continue DD. This is the precursor to the FTX archetype: SBF told Sequoia stories that documents would have contradicted. Sequoia did not demand the documents.9

Frame 5: The Walk Rate (What Buyers Actually Do)

Across SRS Acquiom's 2025 dataset (covering roughly $298B in 1,200+ private-target deals), no-survival "walk-away" R&W constructs fell from 18% (2024) to 11% (2025).1 Concurrently, undisclosed-liability claims have doubled since 2022 and now account for 24% of all R&W indemnification claims.2

Practical guidance: Most red flags now don't trigger walks — they trigger structure. Walk only when:

- Red-severity per Frame 1 (high materiality + uncurable), OR

- All three Concentrated Trio tests fail, OR

- The Bain Test cannot be satisfied for cyber or regulated-industry targets.

For everything else, the 2026 playbook is special indemnity outside the R&W cap, cyber-specific escrow separately calibrated from the general indemnity escrow, and reps tail-period stacking to cover the long-tail discovery window.

Which Red Flag Category Pays Out the Most in R&W Claims?

Financial statement breaches account for only about 13% of W&I notifications by frequency but 37% of all losses paid per Marsh's 2025 Global Transactional Risk Claims data — by far the highest-severity R&W category. Tax claims run about 30% of frequency at 17% of dollars; compliance is roughly balanced at 20% / 20%.

Per Marsh's 2025 Global Transactional Risk Claims data, claims distribute by frequency and severity very differently:3

| Category | Frequency (% of notifications) | Severity (% of losses paid) |

|---|---|---|

| Tax | About 30% | About 17% |

| Financial statements | About 13% | About 37% |

| Compliance | About 20% | About 20% |

| Material contracts | About 13% | About 13% |

| Operations | About 10% | About 8% |

| Other | About 14% | About 5% |

The structural takeaway: financial statements are 13% of frequency but 37% of dollars paid — making them the single highest-severity category. Buyers who under-weight financial DD pay the most in post-close claims.

Honest Comparison: Which Data Room Tool Fits Red Flag Management?

Different DD profiles fit different data room platforms. We use Peony, obviously, but the honest mapping is:

| DD profile | Best fit | Reason |

|---|---|---|

| $200M+ cross-border banker-managed | Datasite, Intralinks | 25+ years of enterprise-DD workflow; Datasite now owns Firmex |

| Mid-market PE / strategic, AI red flag inventory | Peony | AI auto-indexing 3 min; AI Q&A across 1,500-4,500 docs by stream |

| Founder-led light DD | Papermark, DocSend, Peony | Lower-cost; faster setup |

| Highly regulated (defense, healthcare) | iDeals, Intralinks | Hardened compliance certifications |

For mid-market and growth-equity DD where the team needs AI-accelerated red flag inventory across 6 streams, Peony is purpose-built. AI auto-indexing organizes 1,500-4,500 documents into a 6-stream folder tree in under 3 minutes. AI extraction lets the DD team ask cross-document questions like "list every red flag mentioned in any QoE, legal memo, or auditor report and quote the supporting language."

What Else Do Deal Teams Ask About Red Flags?

What single red flag is most often missed? Founder pre-incorporation IP not assigned to the company. It's a Yellow-to-Red flag depending on materiality, and investors view it as "the company doesn't own its core technology." Fix is retroactive assignments with consideration.

How many red flags typically surface in a mid-market deal? 1-3 material adverse findings per deal, per industry benchmarks. The challenge is not finding them — it's synthesizing them into a top-5 memo with named owners and dollar estimates.

Does R&W insurance cover red flags discovered during DD? No. R&W covers UNDISCLOSED issues. Anything discovered in DD must be carved out and handled via special indemnity or escrow. R&W policies typically pay out only when an issue was unknown at signing.

When does a red flag become "kill the deal" instead of "renegotiate"? When the Severity Matrix puts it in High-Materiality + Uncurable, OR when all three Concentrated Trio tests fail, OR when the Bain Test cannot be satisfied for cyber targets. Otherwise, the 2026 playbook is structure, not walk.

Why Does Peony Fit Red Flag Management Across 6 Streams?

Peony is one of several data room platforms for managing DD red flag inventory — not the only fit for every deal. For mid-market and growth-equity DD, the workflow advantages compound:

- AI auto-indexing organizes 1,500-4,500 documents into a 6-stream folder tree (financial, legal, commercial, operational, tech/cyber, ESG/regulatory) in under 3 minutes.

- AI extraction lets the DD team ask cross-document questions like "list every red flag mentioned in any QoE, legal memo, or auditor report and quote the supporting language."

- Per-investor watermarks track which version of a document each internal stakeholder read.

- Screenshot protection prevents sensitive red flag findings from leaking outside the data room — capture attempts are blocked and logged.

- NDA gates with integrated e-signatures stage sensitive findings (cyber DD, regulatory letters, pending litigation) behind a signed CA.

- Page-level analytics show exactly which DD team members read which sections.

Peony Data Room at $52 per admin per month gives unlimited data rooms with AI Q&A across all uploaded DD documents. Over 5,900 customers use Peony for M&A, fundraising, and DD workflows.

For $200M+ cross-border deals where the M&A bank is the process owner, Datasite or Intralinks remain the conservative defaults — their legacy reflects 25+ years of enterprise M&A workflow design.

Related Reading in the DD Cluster

- Due Diligence Mistakes That Kill Deals — 12 buyer-side mistakes with deal anchors

- M&A Due Diligence Process Guide — the canonical end-to-end process map

- Cybersecurity Due Diligence — the 5-axis breach-readiness matrix and full Bain Test

- Third-Party Due Diligence — 5-jurisdiction exposure map

- Vendor Due Diligence Checklist — procurement-led TPRM workflow

- Due Diligence Cost Breakdown — workstream-by-workstream cost ranges

- Investment Due Diligence Checklist — VC and growth-equity DD lens

Footnotes and Sources

Footnotes

-

SRS Acquiom, "M&A Deal Terms Study 2025" — https://www.srsacquiom.com/our-insights/deal-terms-study-2025/ . ↩ ↩2

-

Goodwin Procter, "Undisclosed Liability Claims Have Doubled Since 2022" (Sep 2025) — https://www.goodwinlaw.com/en/insights/publications/2025/09/insights-privateequity-undisclosed-liability-claims-have-doubled . ↩ ↩2

-

Marsh, "Global Transactional Risk Insurance Claims Report 2025" — https://www.marsh.com/en/services/private-equity-mergers-acquisitions/insights/global-transactional-risk-insurance-claims-report.html . ↩ ↩2 ↩3

-

AON, "2025 Transaction Solutions Global Claims Study" — https://www.aon.com/en/insights/reports/transaction-solutions-global-claims-study . ↩

-

Livmo, "Customer Concentration Risk: How Buyers Price It" (2025) — https://livmo.com/blog/customer-concentration-risk-saas-exit/ . ↩ ↩2

-

SRS Acquiom, "2025 Working Capital Purchase Price Adjustment Study" — https://www.srsacquiom.com/our-insights/2025-working-capital-purchase-price-adjustment-study/ . ↩

-

American Bar Association, "2025 Private Target Mergers & Acquisitions Deal Points Study" — https://www.americanbar.org/groups/business_law/resources/business-law-today/2025-december/aba-2025-private-target-mergers-acquisitions-deal-points-study/ . ↩

-

Deloitte, "Revenue Recognition for SaaS and Software Companies" — https://www.deloitte.com/us/en/services/audit-assurance/articles/revenue-recognition-saas-software-guidance.html . ↩

-

Crain Currency, "FTX founder and CEO Sam Bankman-Fried 'misled and deceived' Sequoia Capital" — https://www.craincurrency.com/investing/ftx-founder-and-ceo-sam-bankman-fried-misled-and-deceived-sequoia-capital-firm-says ; Fortune, "FTX bankruptcy, collapse fueled by venture capital carelessness" — https://fortune.com/2022/11/17/ftx-bankruptcy-bankman-fried-venture-capital-ceo-ray/ . ↩ ↩2 ↩3

-

CNN Business, "SmileDirectClub shuts down after filing for bankruptcy" — https://www.cnn.com/2023/12/09/business/smiledirectclub-shutdown-bankruptcy/ . ↩

-

Nixon Peabody, "Open Source Software Risks and Best Practices in M&A" (Oct 15, 2025) — https://www.nixonpeabody.com/insights/articles/2025/10/15/open-source-software-risks-and-best-practices-in-ma . ↩

-

NY DFS, "Superintendent Adrienne A. Harris Secures $40 Million Settlement with Block, Inc." (April 10, 2025) — https://www.dfs.ny.gov/reports_and_publications/press_releases/pr202504101 ; CSBS, "State Regulators Issue $80 Million Penalty to Block, Inc., Cash App for BSA/AML Violations" — https://www.csbs.org/newsroom/state-regulators-issue-80-million-penalty-block-inc-cash-app-bsaaml-violations . ↩

-

Morrison Foerster, "Top 5 SEC Enforcement Developments for February 2025" — https://www.mofo.com/resources/insights/250325-top-5-sec-enforcement-developments-for-february-2025 . ↩

-

TechContracts, "Don't Confuse Change of Control and Assignment Terms" — https://www.techcontracts.com/2020/09/11/dont-confuse-change-of-control-and-assignment-terms/ . ↩

-

Plante Moran, "Navigating worker classification: Your guide to legal, tax, and deal impacts" (November 2025) — https://www.plantemoran.com/explore-our-thinking/insight/2025/11/navigating-worker-classification . ↩

-

Venable LLP, "FTC Non-Compete Enforcement and State Law Restrictions" (October 2025) — https://www.venable.com/insights/publications/2025/10/ftc-non-compete-enforcement-and-state-law ; FTC, "Federal Trade Commission Files to Accede to Vacatur of Non-Compete Clause Rule" (September 2025) — https://www.ftc.gov/news-events/news/press-releases/2025/09/federal-trade-commission-files-accede-vacatur-non-compete-clause-rule . ↩

-

Outreach, "Pipeline coverage: Complete guide to calculation and benchmarks" — https://www.outreach.ai/resources/blog/sales-pipeline-coverage-ratio . ↩

-

Goodwin Procter, "How to Secure and Retain Top Talent in Asset Purchases" (November 2025) — https://www.goodwinlaw.com/en/insights/publications/2025/11/insights-privateequity-ma-how-to-secure-and-retain-top-talent . ↩

-

Womble Bond Dickinson, "Unprecedented: Private Equity Firm Potentially on Hook for Portfolio Company's Data Breach" (March 2026) — https://www.womblebonddickinson.com/us/insights/alerts/unprecedented-private-equity-firm-potentially-hook-portfolio-companys-data-breach . ↩ ↩2

-

FTI Consulting, "CISO Redefined III: Navigating Cybersecurity Risks in Transactions" (March 17, 2026) — https://www.fticonsulting.com/insights/reports/ciso-redefined-navigating-transactions-cybersecurity-landscape . ↩

-

Cloud Security Alliance, "The Salesloft Drift OAuth Supply-Chain Attack" (September 25, 2025) — https://cloudsecurityalliance.org/blog/2025/09/25/the-salesloft-drift-oauth-supply-chain-attack-cross-industry-lessons-in-third-party-access-visibility . ↩

-

Verizon, "2025 Data Breach Investigations Report" — https://www.verizon.com/about/news/2025-data-breach-investigations-report . ↩

-

IBM, "Cost of a Data Breach Report 2025" — https://www.ibm.com/reports/data-breach . ↩ ↩2

-

Troutman Pepper Locke, "Preventing Forced Labor in Global Supply Chains: Key Updates to the 2025 UFLPA Strategy" — https://www.troutman.com/insights/preventing-forced-labor-in-global-supply-chains-key-updates-to-the-2025-uflpa-strategy-and-what-importers-need-to-know/ . ↩

-

Covington & Burling, "EU CSDDD/CSRD Omnibus Published in Official Journal" (February 26, 2026) — https://www.cov.com/en/news-and-insights/insights/2026/02/eu-csddd-csrd-omnibus-published-in-official-journal-transposition-delegated-acts-and-guidelines-are-next . ↩

-

Alaska Air Group, Q1 2025 Earnings Release (April 23, 2025) — https://news.alaskaair.com/wp-content/uploads/2025/04/ALK-Q1-2025-Earnings-Release.pdf . ↩