How to Prepare for Due Diligence (2026): The 90-Day Prep Pyramid for Sellers

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

I worked with a SaaS CFO this spring who was 45 days from an LOI deadline with a $180M strategic-buyer process and had not yet commissioned the sell-side quality-of-earnings, the data room held 320 files in a Dropbox folder, and the founder's pre-incorporation IP had never been formally assigned. Three months of compressed prep work later, the QofE surfaced a $1.4M revenue-recognition adjustment the seller fixed before signing, the data room migrated to a 12-folder structure with 2,800 files and three permission tiers, the IP assignment cleanup closed two legal-DD risks, and the deal closed at a 9.2% higher price than the original strategic-buyer LOI anchor. Due diligence preparation in 2026 is not paperwork — it is the structural lever that produces the GF Data 2025 finding that sell-side QofE deals captured 7.4x versus 7.0x TEV/EBITDA on deals above $50M, a 5.7% valuation lift that compounds against $50-200K of VDD cost into 14-57x ROI. I run Peony, a data room platform used by 5,900+ customers across M&A, private equity, and DD workflows. Backed by VCs including Target Global, this guide maps the 90-Day Prep Pyramid (Strategic / Data Room / Narrative / Process), the Vendor DD ROI test, the No-Surprises Memo frame demonstrated by ServiceTitan versus CoreWeave's 2024-2025 IPOs, the Data Room Maturity Curve, and the Q&A Reply-Rate Cliff that separates 30-45-day diligence from 90-120-day stall risk.

Quick answer: Due diligence preparation for a sell-side M&A process takes 60-90 days minimum, organized in a 90-Day Prep Pyramid with four layers — Strategic (T-90 to T-60: VDD, cap table, audit, IP scrub), Data Room (T-60 to T-30: 10-15 folders, 1,500-4,500 files, permission tiers, Q&A workflow), Narrative (T-30 to T-0: management presentation, CIM, teaser, customer references), Process (T-0 to close: Q&A SLAs, 8-16 week bid-to-close). For IPO-track sellers, add 6-12 months for PCAOB audit uplift plus AICPA AS 6101 135-day comfort-letter sequencing. Per GF Data 2025, sell-side QofE deals captured 7.4x versus 7.0x TEV/EBITDA on $50M+ — a 5.7% valuation lift translating to 14-57x ROI on VDD cost. R&W insurance prices at 2.5%-3% of policy limit in 2026 (60-90 day capacity broad). The Q&A Reply-Rate Cliff: sellers responding under 24 hours close in 30-45 days; past 72 hours, the deal enters stall risk.

Why Sell-Side Preparation Matters in 2026

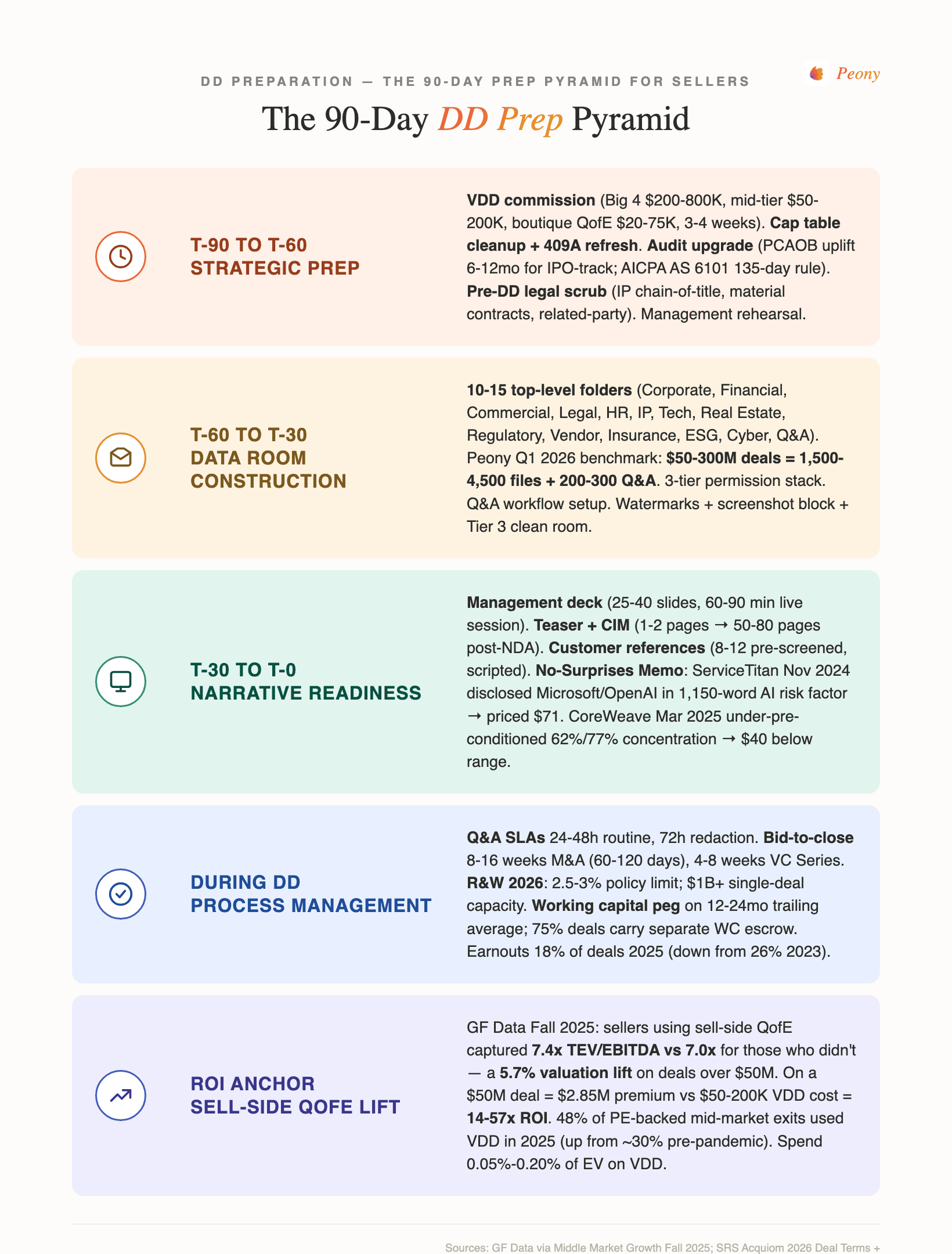

48% of PE-backed mid-market exits used sell-side vendor due diligence in 2025, up from roughly 30% pre-pandemic, with the global sell-side DD services market valued at $1.061 billion in 2025 and growing toward $2.16 billion by 2033. PwC holds 17% market share, Deloitte 15%.1

Well-prepped sellers using sell-side QofE captured 7.4x TEV/EBITDA versus 7.0x for those who didn't — a 5.7% valuation lift on deals greater than $50M.2 63% of mid-market 2024-Q1 2025 deals used R&W insurance, up from 55% in 2023.3 Quality of Earnings / EBITDA discrepancies killed 21.3% of post-LOI deals in 2025 — more than double the 10.6% rate in 2023 per Axial's 2025 Dead Deal Report.4

The structural takeaway: sell-side preparation in 2026 has shifted from "nice to have" to "valuation lever" — and the data room construction work is the visible artifact of that shift.

The 90-Day Prep Pyramid: 4 Layers, 4 Phases

The 90-Day Prep Pyramid is a 4-layer hierarchy of seller deliverables, sequenced across four phases:

| Layer | Phase | Deliverable Count | Typical Cost | Owner |

|---|---|---|---|---|

| Strategic (foundation) | T-90 to T-60 | About 5 (VDD, QofE, 409A, audit, IP scrub) | $100K-$1M | CEO + CFO + outside advisors |

| Data Room (vehicle) | T-60 to T-30 | 10-15 folders, 1,500-4,500 files | $15K-$100K (VDR) | CFO + ops + GC |

| Narrative (message) | T-30 to T-0 | 3 documents (teaser, CIM, mgmt deck) | $200K-$1M (banker fees) | Banker + CEO |

| Process (execution) | T-0 to close | 8-16 weeks of Q&A, site visits, negotiation | $500K-$3M (legal + R&W) | Full deal team |

Total at full deployment: roughly $1M-$5M all-in for a $100M-$500M mid-market sell-side. The pyramid's foundation (Strategic) determines whether the upper layers stand.

What Strategic Prep Should Sellers Start in Phase 1 (T-90 to T-60)?

The four strategic prep deliverables that take the longest to complete and produce the largest valuation lift sit in the T-90 to T-60 window: sell-side vendor due diligence (VDD), cap table cleanup with 409A refresh, audit upgrade (PCAOB uplift for IPO-track), and a pre-DD legal scrub of IP chain-of-title plus material contracts.

Commission Sell-Side Vendor Due Diligence (VDD)

Big 4 (PwC, Deloitte, EY, KPMG) charges $200K-$800K per engagement covering comprehensive financial, tax, and commercial VDD. Mid-tier and boutique (Grant Thornton, BDO, RSM, niche transaction-services shops) runs $50K-$200K for mid-sized deals; $20K-$75K for boutique sell-side QofE alone.5 VDD reports take 3-4 weeks to produce and should be commissioned 1-3 months pre-marketing.

When to commission:

- 48% of PE firms now require VDD before portfolio exits.1

- For deals greater than $50M EV, sell-side QofE is correlated with 7.4x versus 7.0x TEV/EBITDA outcomes (5.7% valuation lift).2

- 47% of executives admit prior deals underperformed (Deloitte 2025) — buyers now demand seller-side numbers tested before signing LOI.

Cap Table Cleanup

409A valuation refresh (quarterly cadence within 18-24 months of IPO; standard 12-month for M&A).6 A messy cap table adds $1,000-$2,000 to 409A engagement and weeks to delay; pre-IPO sellers should reconcile spreadsheets to a cap-table platform.

Secondary tender prep: Stripe announced a $159B-valuation tender in February 2026 (up 74% from $91.5B a year earlier); SpaceX ran four progressively larger tenders ($210B June 2024 to $800B December 2025), each requiring cap table and shareholder consent infrastructure.7

Option pool top-up (typical 7-10% post-Series B) and founder vesting acceleration terms must be documented BEFORE diligence.

Audit Upgrade

For IPO-track sellers, the PCAOB audit standard becomes effective for fiscal years beginning on or after December 15, 2025.8 "Uplift" procedures convert AICPA audits to PCAOB-compliant; budget 6-12 months.

For M&A-only sellers, GAAP-audited 3-year financials with consistent revenue recognition methodology are table stakes for deals greater than $50M.

AICPA AS 6101 (135-day rule): Auditors can issue negative-assurance comfort letters only within 134 days of the most recent audited/reviewed balance-sheet date.89 Past day 134, comfort letter is limited to "procedures performed and findings obtained" — which often forces underwriters to delay or stub financials.

Cerebras IPO anchor (May 13, 2026): priced $185/share — $25 above range, raised $5.55B at $56.4B fully-diluted valuation. The deal calendar was partly driven by 135-day windows on Q4 2025 audited financials.10 See the due diligence for IPO playbook for the 3-Layer DD Stack framework.

Pre-DD Legal Scrub

IP chain-of-title audit: pull every contractor agreement, employee invention assignment, and joint-development agreement. The most common chain-of-title defect in tech M&A is missing assignments. Best practice: present-effective assignment language, not future-execution promises.

Material contract review for change-of-control clauses, anti-assignment, MFN, exclusivity. The 2025 Deloitte M&A Trends Report estimated failed integrations cost acquirers roughly 25% of deal value, with technical/IP oversights a leading cause.11

Related-party transactions — disclose all founder/affiliate dealings; buyers will find them.

HSR rule changes (February 10, 2025) initially expanded document-production requirements; on February 12, 2026 a federal district court vacated the new HSR form and the FTC reverted to the prior form, but the underlying redaction discipline for competitively sensitive data sharing in pre-merger marketing still applies.

Management Team Rehearsal

CFO presentation dry-runs targeting buyer Q&A categories. CTO architecture demo with security/scalability evidence (especially critical: 45% of SRS Acquiom 2025 respondents called tech-DD "the most expensive and arduous" workstream).12 Customer-reference call playbook — 8-12 pre-approved customers, scripted, NDA'd.

How Do You Build a Mid-Market M&A Data Room (Phase 2: T-60 to T-30)?

A mid-market M&A data room runs 1,500-4,500 files organized into 10-15 top-level folders with 3 permission tiers, per the Peony Q1 2026 benchmark across 283 deals. Build the folder structure first, then load Tier 1 (public), Tier 2 (post-LOI), and Tier 3 (clean room) categories with watermarks and Q&A workflow wired in before opening to bidders.

Folder Structure (10-15 Top-Level Folders Typical)

Standard mid-market structure:

- Corporate & Governance

- Financial Statements & Tax

- Commercial & Customer

- Legal & Litigation

- Human Resources & Comp

- Intellectual Property

- Technology & Product

- Real Estate & Facilities

- Regulatory & Compliance

- Vendor & Supply Chain

- Insurance

- Environmental, Social & Governance (ESG)

- Cybersecurity & Privacy

- Q&A / Process

Document Volume Benchmarks (Peony Q1 2026, 283 Deals)

- Sub-$50M deals: roughly 1,500 files, 150-200 Q&A questions, 6-month close

- $50M-$300M mid-market: 1,500-4,500 files, 200-300 Q&A

- $300M+: 4,500-12,000 files, 600+ DDQ items13

Larger broad surveys put mid-market at 5,000-12,000 documents with 200-400 structured DDQ items.

Permission Tiers (3-Tier Minimum)

- Tier 1 (broad): Public marketing docs, CIM, redacted financials — visible to all qualified bidders

- Tier 2 (detail): Customer contracts, employee handbook, full management accounts — opens after LOI/IOI

- Tier 3 (sensitive): Source code, customer pricing schedules, key-person comp — opens at confirmatory DD, often via clean room

Redaction Strategy (Post HSR — Vacated February 12, 2026, Discipline Persists)

True redaction (content removed) versus masking (visual cover that copy-paste defeats) — only true redaction is safe externally. AI-driven PII redaction tools handle bulk redaction at scale. Categories typically redacted: customer names in pricing schedules, individual comp, source code, M&A diligence files from prior deals, board-meeting deliberations.

Q&A Workflow Setup

Centralized Q&A module with question routing to category owners (CFO/COO/GC/CTO). Approval workflow (subject matter expert drafts → outside counsel approves sensitive items → seller signs off). Linkage of answers to underlying documents to avoid email-based Q&A version sprawl.

Watermarking and Screenshot Prevention

Dynamic per-viewer watermarks (user ID + timestamp + IP) — mandatory for Tier 2+. Screenshot blocking at OS layer (active prevention versus passive notice). Disable copy/print on Tier 3. Page-level audit trails.

Activity Analytics

Track bidder heat: page-views per buyer, time-on-document, repeat visits. Heat maps tell the seller which bidders are serious and what they're worried about — used to time price chips and bid-clearing calls.

How Do Sellers Get Narrative-Ready Before Bidder Meetings (Phase 3: T-30 to T-0)?

Narrative readiness has three artifacts: the 25-40-slide management presentation delivered in a 60-90 minute live session, the commercial deck hierarchy (teaser → CIM post-NDA → management presentation to 4-8 second-round bidders), and the No-Surprises Memo pre-disclosing the top 3-5 known issues with mitigation actions and quantified financial impact.

Management Presentation (60-90 Minute Live Session, 25-40 Slides Typical)

Structure: company overview (3-5 slides), market and competitive positioning (5-8), product/tech architecture (5-8 for SaaS/deep-tech), financial summary and growth drivers (8-12), management team bios (3-5), growth plan and use of proceeds (3-5). The first in-person meeting between seller management and final-round bidders — designed to generate LOIs.

Commercial Deck Hierarchy

- Teaser (1-2 pages, no name) — sent to long-list

- CIM (Confidential Information Memorandum) — 50-80 pages, full company story, sent post-NDA to roughly 20-40 buyers

- Management presentation — 25-40 slides, in-person delivery to 4-8 second-round bidders

Site Visit Playbook

Typically days 22-28 of process. For industrial sellers, factory tour is mandatory. Customer references occur in parallel — 8-12 pre-screened references, scripted.

Q&A Team Assembly

CFO (financial), COO (operational, customer, vendor), General Counsel (legal, regulatory, IP), outside counsel (Cooley, Goodwin, Wilson Sonsini, Latham — top tech sell-side), sell-side accountant (QofE follow-ups), M&A advisor / banker as orchestrator.

Pre-emptive Red Flag Disclosure (The "No-Surprises Memo")

"Showstoppers" should be rectified pre-completion by the seller so the buyer doesn't take on overly onerous risks. Disclosure schedules formalize this in the SPA, but the strategic move is to pre-disclose in the CIM or management presentation: known customer concentration, regulatory inquiries, pending litigation, key-person dependencies.

ServiceTitan (November 18, 2024) filed an S-1 with a 1,150-word AI risk factor explicitly naming Microsoft and OpenAI as third-party dependencies the company couldn't control. Pre-emptive transparency. IPO priced at $71 on December 11, 2024 (trading debut December 12, 2024).14

CoreWeave (S-1 filed March 3, 2025; IPO priced March 27, 2025) disclosed Microsoft = 62% of 2024 revenue plus a second customer at 15% (top-2 = 77%) in its S-1. Underwriters priced at $40/share (below the expected $47-55 range), raising $1.5B versus planned $2.7B. The concentration was knowable but possibly not pre-conditioned in marketing — illustrating the cost of late disclosure.15

ARM (September 14, 2023) S-1 disclosed top-5 customers = 57% revenue, ARM China alone = 24%. Pre-priced into marketing, IPO priced at $51 (high end of range).

Banker Process Timeline

- One-step (limited) auction: Single LOI round; faster (4-6 weeks to LOI). Used for distressed or speed-sensitive deals.

- Two-step (broad) auction: IOI round → site visits with 4-8 bidders → final LOI. 4-6 weeks to IOIs; another 4-6 weeks to LOI. Generally optimizes price.

- Exclusivity: 30-60 days typical post-LOI. Sellers in 2024-2025 increasingly delay or shorten exclusivity to maintain competitive tension.

- Go-shop: Post-signing 30-50 day window for sellers (especially public targets) to solicit competing bids.

How Do Sellers Manage Q&A, R&W, and Working Capital During DD (Phase 4)?

Process management during DD has four discrete workstreams: Q&A turnaround SLAs (24-48 hours routine, 72 hours redaction), bid-to-close timeline (8-16 weeks M&A, 4-8 weeks VC Series), reps and warranties insurance at 2.5-3% of policy limit with $1B+ single-deal capacity available in 2026, and working capital peg locked on identical methodology to the closing balance sheet.

Q&A Turnaround SLAs

Standard: 24-48 hours for routine questions; 72 hours for documents requiring redaction or counsel review. Industry SLA benchmark across financial sector is 24 hours; M&A is more permissive but Tier-1 sellers commit to next-business-day responses.

Bid-to-Close Timeline (2025-2026 Benchmarks)

- M&A LOI to close: 8-16 weeks (60-120 days); complex regulated deals 4-6 months

- Simple deals: 4-6 weeks

- VC Series B/C diligence: 4-8 weeks term sheet to close

- Average overall M&A deal time fell to 255 days in 2024 (first 4-year improvement) but PE signing-to-closing increased 64% YoY 2023-202416

R&W Insurance 2026 Pricing

Premium: 2.5%-3% of policy limit (down from 3-4% in 2022-2023); deals greater than $50M EV typically priced 3.5%-4% of coverage all-in including broker fees.17 Capacity: $1B+ single-deal limits available. 63% of mid-market deals used R&W in 2025 versus 55% in 2023.3 Underwriters: AIG, Everest, QBE, Chubb (primary carriers); Marsh, AON, Willis (brokers).

Earnout Structure

Earnouts dropped from 26% of mid-market deals (2023) to 18% (2025).3 68% of earnout deals use multiple metrics.18 Revenue (62%) is the most common primary metric in 2024 — sellers prefer revenue (harder to manipulate). Median earnout period: 24 months (non-life-sciences); 3-5+ years for biotech.

Working Capital Peg

Appears in over 90% of private-target deals today (versus 50% a decade ago). 75% of deals carry a separate WC escrow. "Worksheet approach" (parties-defined methodology) used in 39% of 2026-study deals.19 Typical peg: 12-24 month trailing seasonality-adjusted look-back. Can move 1-3% of EV between buyer and seller.

Frame 1: The 90-Day Prep Pyramid

A 4-layer hierarchy of seller deliverables, sequenced across four phases. The pyramid's foundation (Strategic) determines whether the upper layers stand. A seller who skips Strategic ends up with a Data Room without QofE-grounded financials — and the first buyer-side QofE call exposes the gap.

Frame 2: The Vendor DD ROI Test

When does sell-side VDD pay back?

| Condition | VDD Pays Back? | Evidence |

|---|---|---|

| Deal EV greater than $50M, complex revenue model | YES | 7.4x vs 7.0x TEV/EBITDA = 5.7% lift on $50M = $2.85M premium (vs $50-200K VDD cost). 14-57x ROI |

| Deal EV less than $25M, simple business | OFTEN NO | $50K VDD on a $20M deal = 0.25% of EV — marginal lift on outcome |

| Distressed/forced sale | YES (speed premium) | Reduces deal-fatigue dropout |

| Auction process with 5+ bidders | YES | Reduces buyer-side DD friction; supports tighter exclusivity window |

| Bilateral negotiation, no auction | MAYBE | Less competitive pressure on outcome |

The rule of thumb: spend 0.05%-0.20% of EV on VDD. Below $25M EV, sellers often skip in favor of buyer-led DD.2

Frame 3: The Data Room Maturity Curve

| Doc Count | Seller Tier | Deal Outcome Tendency |

|---|---|---|

| Under 50 docs | Founders winging it — no formal data room | Buyer-led DD extends 30-60 days; valuation chip risk high |

| 50-250 docs | Early-stage / Series A-B prep | Adequate for VC; insufficient for M&A above $25M |

| 250-1,000 docs | Mid-market seller, partially prepped | Median outcome; some surprises in confirmatory DD |

| 1,000-4,500 docs | Sell-side professional, mid-market PE / strategic deal | Best practice; supports auction process; typical for Peony's $50-300M cohort |

| 4,500-12,000 docs | Upper-mid / large deal, banker-prepped | Necessary for $300M+ or regulated industries |

Frame 4: The No-Surprises Memo

A pre-emptive seller-authored disclosure document handed to short-listed bidders BEFORE confirmatory DD. Contains:

- Top 3-5 known issues (concentration, litigation, key-person, regulatory)

- Seller's mitigation actions taken or proposed

- Quantified financial impact assessment

Why it works: Buyers price unknown risk at 1.5-2x the actual liability. Pre-disclosure forces both sides to price the known issue, not the imagined version. Reduces buyer "DD discoveries" used as price-chip leverage.

Anchor contrast: ServiceTitan (November 18, 2024) pre-disclosed Microsoft/OpenAI dependency in a 1,150-word AI risk factor — IPO priced $71 on December 11, 2024.14 CoreWeave (S-1 filed March 3, 2025; priced March 27, 2025) had 62%/77% concentration in S-1 but possibly underweighted in marketing — priced at $40/share (below expected $47-55 range), raised $1.5B versus planned $2.7B.15 Concentration was "diligence-discoverable" rather than "pre-conditioned" — and the price chip showed up.

Frame 5: The Q&A Reply-Rate Cliff

| Q&A Turnaround | Diligence Phase Duration | Implied Deal Velocity |

|---|---|---|

| Under 24 hours | 30-45 days | "Top quartile" sellers; well-prepped data room |

| 24-72 hours | 60-90 days | Median mid-market deal |

| Over 72 hours | 90-120+ days | Disorganized seller; risks deal fatigue |

Anchor data: M&A average deal-time fell to 255 days in 2024 (first 4-year improvement), with IT/Services deals at 244 days (-13% versus average) — the sectors with the highest data room maturity.20

The cliff: Past 72 hours, buyer counsel begins escalating internally; past 7 days, the deal enters "stall risk" — buyers start considering walk-away alternatives. SRS Acquiom's 2025 study found 59% of buyers in extended DD reported "1-3 months added" to timeline, and Axial's 2025 Dead Deal Report found 21.3% of LOI-stage deals died from QofE/EBITDA discrepancies that earlier responses would have surfaced.124

Honest Comparison: Which Data Room Tool Fits Sell-Side Prep?

Different sell-side profiles fit different data room platforms. We use Peony, obviously, but the honest mapping is:

| Sell-side profile | Best fit | Reason |

|---|---|---|

| $200M+ cross-border banker-managed | Datasite, Intralinks | 25+ years of enterprise-DD workflow; Datasite now owns Firmex |

| Mid-market sell-side, AI-accelerated data room | Peony | AI auto-indexing 3 min; 10-15 folder structure; per-bidder analytics |

| Founder-led light fundraising | Papermark, DocSend, Peony | Lower-cost; faster setup |

| Highly regulated (defense, healthcare) | iDeals, Intralinks | Hardened compliance certifications |

For mid-market sell-side prep where speed of data room construction matters, Peony is purpose-built. AI auto-indexing organizes 1,500-document data room into the 10-15-folder structure in under 3 minutes.

What Else Do Sellers Ask About DD Preparation?

How early should I start sell-side preparation? 60-90 days minimum for M&A; 6-12 months for IPO-track sellers requiring PCAOB audit uplift. Strategic prep (T-90 to T-60) is the longest-lead item.

Do I need a banker if I have sell-side VDD? For deals above $50M EV: usually yes. The banker manages auction process, bidder outreach, and Q&A orchestration. Sell-side VDD is a financial product; the banker is the process.

What's the single most-skipped prep item? The No-Surprises Memo. Founders fear that pre-disclosing weakens their position; the data shows pre-disclosure produces tighter pricing because buyers price unknown risk at 1.5-2x actual liability.

How do I size my data room? $50M deal: target 1,500 files in 10-12 folders. $200M deal: 3,000-4,500 files. $500M+ deal: 6,000-12,000 files. Use the Peony Q1 2026 benchmark to set the floor.

Why Does Peony Fit Sell-Side DD Preparation?

Peony is one of several data room platforms for sell-side preparation — not the only fit for every deal. For mid-market sell-side prep, the workflow advantages compound:

- AI auto-indexing organizes 1,500-4,500 documents into the 10-15-folder structure in under 3 minutes, eliminating the first-week manual prep that traditionally delayed substantive review.

- AI extraction lets the seller's CFO ask cross-document questions like "find every customer contract with a change-of-control clause" before the buyer asks.

- Per-investor watermarks track which bidders are serious based on which sections they actually read.

- Screenshot protection keeps Tier 3 sensitive material (source code, customer pricing) inside the data room.

- NDA gates with integrated e-signatures stage Tier 2 detail behind a signed CA.

- Page-level analytics show exactly which buyer team members read which sections — useful for the seller's banker to time price chips and bid-clearing calls.

Peony's Data Room plan at $52 per admin per month gives unlimited data rooms with AI Q&A across all uploaded DD documents. Over 5,900 customers use Peony for M&A, fundraising, and DD workflows.

For $200M+ cross-border deals where the M&A bank is the process owner, Datasite or Intralinks remain the conservative defaults — their legacy reflects 25+ years of enterprise M&A workflow design.

Related Reading in the DD Cluster

- Data Room for Restructuring — preparing diligence when the deal is a restructuring: strategic vs distressed, and protecting IP at the moment of least leverage

- Due Diligence Mistakes That Kill Deals — 12 buyer-side mistakes

- Due Diligence Red Flags — 38 red flags across 6 streams

- Due Diligence for IPO — 3-Layer DD Stack and 135-Day Rule

- M&A Due Diligence Process Guide — the canonical end-to-end process map

- Due Diligence Data Room Checklist — folder structure and document categorization

- Due Diligence Cost Breakdown — workstream-by-workstream cost ranges

- Due Diligence Questionnaire — DDQ structure and response workflow

- Cybersecurity Due Diligence — the 5-axis breach-readiness matrix

- Startup Data Room Checklist — Series A-C fundraising prep

Footnotes and Sources

Footnotes

-

Global Growth Insights, "Sell-Side Due Diligence Services Market 2033 Outlook" — https://www.globalgrowthinsights.com/market-reports/sell-side-due-diligence-services-market-112245 . ↩ ↩2

-

Middle Market Growth / GF Data, "Q&A on Sell-Side QofE Adoption" (Fall 2025) — https://middlemarketgrowth.org/fall-2025-gf-data-quality-of-earnings-reports/ . ↩ ↩2 ↩3

-

American Bar Association, "2025 Private Target Mergers & Acquisitions Deal Points Study" (December 16, 2025) — https://www.americanbar.org/groups/business_law/resources/business-law-today/2025-december/aba-2025-private-target-mergers-acquisitions-deal-points-study/ . ↩ ↩2 ↩3

-

Axial, "Dead Deal Report: Unpacking 2025's Broken LOIs" — https://www.axial.net/forum/dead-deal-report-unpacking-2025s-broken-lois/ . ↩ ↩2

-

Peony, "Due Diligence Cost Breakdown 2026" — /blog/due-diligence-cost-breakdown . ↩

-

Carta, "What is a 409A Valuation?" — https://carta.com/learn/startups/equity-management/409a-valuation/ ; Pulley, "409A Valuation Best Practices" — https://www.pulley.com . ↩

-

PitchBook, "SpaceX/Stripe Secondaries 2024-2025" — https://pitchbook.com/news/articles/spacex-tender-offer-secondary-sales-vc . ↩

-

PCAOB AS 6101: Letters for Underwriters — https://pcaobus.org/oversight/standards/auditing-standards/details/AS6101 . ↩ ↩2

-

Mayer Brown, "Top 10 Practice Tips: Comfort Letters" — https://www.mayerbrown.com/-/media/files/perspectives-events/publications/2023/02/top-10-practice-tips_comfort-letters.pdf . ↩

-

Cerebras IPO press release (May 13, 2026) — https://www.cerebras.ai/press-release/cerebras-systems-announces-pricing-of-initial-public-offering . ↩

-

Deloitte, "2025 M&A Trends Survey" (January 2025) — https://www.deloitte.com/us/en/about/press-room/dealmakers-prepare-and-pivot-for-m-a-activity-in-2025.html . ↩

-

SRS Acquiom, "2025 M&A Due Diligence Study" — https://www.srsacquiom.com/our-insights/m-a-due-diligence-study/ . ↩ ↩2

-

Peony, "State of M&A Data Rooms Q1 2026" (283 deals benchmarked) — https://www.peony.ink/blog/state-of-ma-data-rooms . ↩

-

TechCrunch, "ServiceTitan names LLMs from Microsoft, OpenAI as risk factors" (November 18, 2024) — https://techcrunch.com/2024/11/18/servicetitan-names-llms-from-microsoft-openai-as-risk-factors/ . ↩ ↩2

-

Fortune, "CoreWeave files its S-1 prospectus for Nasdaq IPO" (March 3, 2025) — https://fortune.com/2025/03/03/coreweave-ipo-s1-filing-nasdaq-ai-cloud-nvidia-microsoft/ . ↩ ↩2

-

Goodwin Insights, "Competitive Advantages in Extended M&A Deal Timelines" (October 2025) — https://www.goodwinlaw.com/en/insights/publications/2025/10/insights-privateequity-deal-timelines-turning-delays . ↩

-

AJG, "Who Pays the RWI Premium and Retention in 2026?" — https://www.ajg.com/news-and-insights/who-pays-the-rwi-premium-and-retention-in-2026/ . ↩

-

SRS Acquiom, "2026 M&A Deal Terms Study" — https://www.srsacquiom.com/our-insights/deal-terms-study/ . ↩

-

SRS Acquiom, "2026 Working Capital Purchase Price Adjustment Study" — https://www.srsacquiom.com/our-insights/working-capital-adjustment-study/ . ↩

-

IDeals, "M&A deal timelines shorten for first time in four years" — https://www.idealsvdr.com/blog/ma-deal-timelines-shorten-for-first-time-in-four-years-new-report/ . ↩

You might also like

May 14, 2026

Sell-Side Due Diligence (2026): VDD Scope Matrix + 8-Week Pre-Market Stack

May 27, 2026

What Documents Go in a Data Room? (9-Folder Framework) in 2026

Apr 22, 2026

How to Set Up a Click-Through NDA for M&A Data Rooms in 2026