11 Best M&A Advisors in Phoenix for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

11 Best M&A Advisors in Phoenix for $5M-$300M Deals (2026)

Quick answer: Phoenix-metro sellers at $5M to $300M EV have a deep boutique field plus national platform offices. The structural test is sub-vertical fit. IBG Fox & Fin (Scottsdale, founded 1993 by Jim Afinowich, ranked #1 in Arizona for Investment Banker/M&A Intermediary 23 consecutive years), William & Wall (Scottsdale, Tro Panosian / Michael Tully / David Barnett, under $300M revenue and above $3M EBITDA), Generational Group (Scottsdale office, 250-professional national platform), BMO Capital Markets (Greene Holcomb Fisher legacy, Paul Jevnick), Columbia West Capital (Scottsdale, founded 2003, Sri Malladi), Ardent Advisory Group (Scottsdale, founded 2021, $3B+ aggregate), plus Stifel, Baird, Raymond James, Houlihan Lokey, and 2717 Group (A/E/C specialist) on the platform side. The 2026 Phoenix M&A market is shaped by TSMC's $165B Fab 21 expansion (announced March 2025, 6 fabs not 3), Amkor's $7B Peoria advanced packaging campus (October 2025 groundbreaking), the Honeywell Aerospace HONA spin (Q3 2026, Phoenix HQ), Caris Life Sciences IPO (June 17 2025, $494.1M raised), the Workday-Paradox $1.0B exit (October 2025), and Phoenix's role as the #1 build-to-rent transaction geography in the US.

Phoenix has gone from a regional M&A market to a structural buyer pool capital between 2023 and 2026. The combination of TSMC's doubled investment, the Honeywell Aerospace spin, the Microsoft / Meta / Google hyperscale data-center cluster, the Caris IPO precedent, and the continued institutional appetite for build-to-rent has produced a deal volume jump — Arizona M&A deals reached 178 in 2025 versus 145 in 2024, a 23 percent increase per William & Wall's Arizona M&A Year in Review.

I have built a data room used by 5,900+ customers, including Phoenix-metro sell-side teams running processes at $5M-$300M EV. This guide is the working map of who's strong in which sub-vertical, what the buyer pool composition actually looks like, and which advisors run the cleanest processes in 2026.

What's the 2026 Phoenix M&A backdrop, and why does it matter for advisor selection?

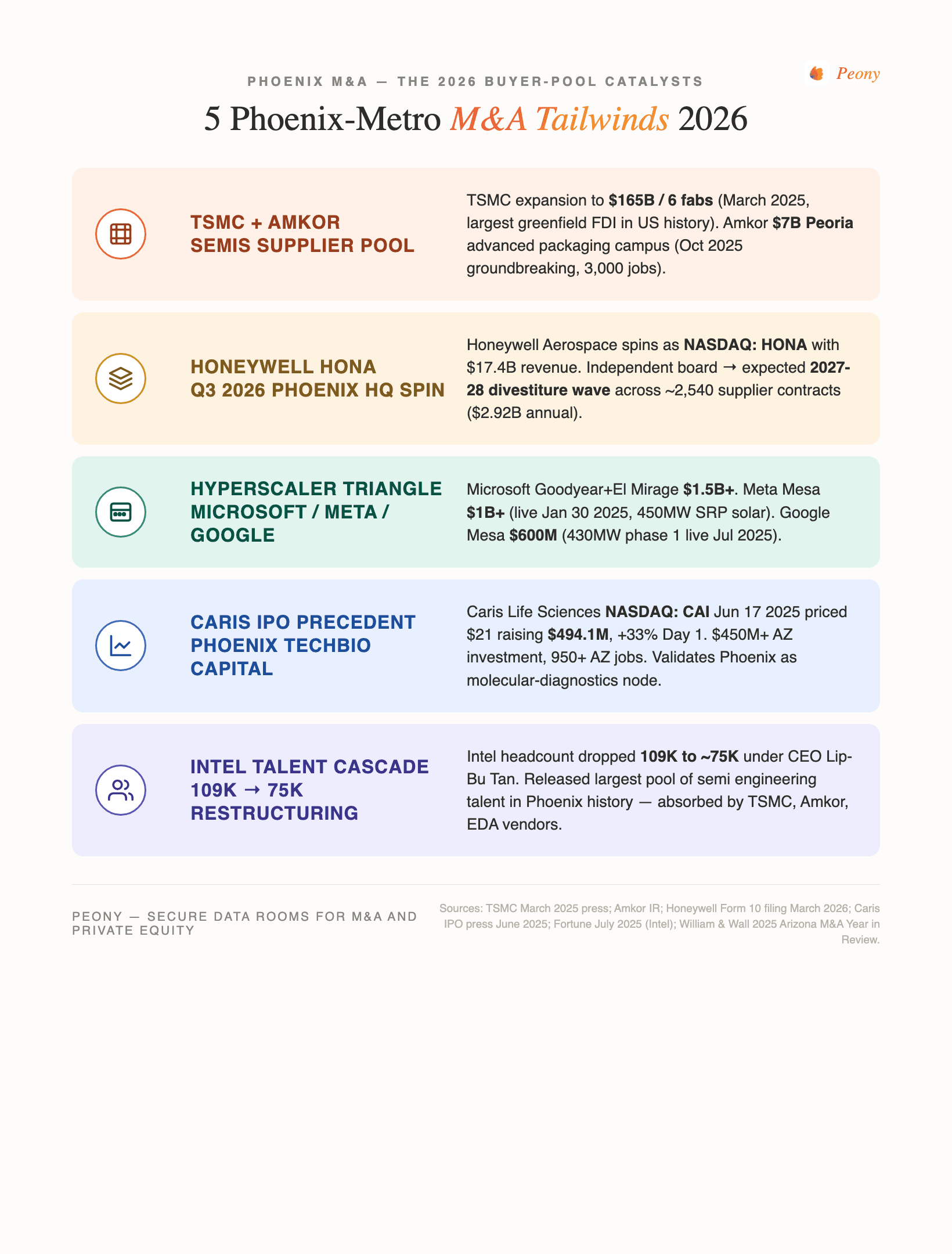

Three structural forces converged in 2025 that change Phoenix-metro M&A in 2026:

1. TSMC's $165B expansion (announced March 2025). TSMC doubled its Phoenix commitment from $65B to $165B and increased planned fabs from 3 to 6 — the largest foreign direct investment in a greenfield project in US history per TSMC's press. Fab 21 Phase 1 began mass production of 4nm chips in early 2025 supplying Apple and NVIDIA. CHIPS Act funding: $6.6B direct plus $5B loans.

2. The Honeywell three-way split. Honeywell announced February 2025 it would split into three: Honeywell Automation (Charlotte HQ retained), Honeywell Aerospace (new Phoenix HQ as NASDAQ: HONA, Q3 2026 spin), and Solstice Advanced Materials (NASDAQ: SOLS, spin closed October 30, 2025). HONA's 2025 financials: $17.4B net sales, $1.5B pro forma net income, $4.3B pro forma Adjusted EBIT. Investor Day is June 3, 2026 in Phoenix.

3. The hyperscale data-center cluster. Microsoft Goodyear + El Mirage ($1.5B+ campus, $258M El Mirage land buy May 2025); Meta Mesa ($1B+ campus, serving traffic since January 30 2025, 450MW SRP solar partnership); Google Mesa ($600M, 187 acres, ~430MW phase 1 live July 2025).

Frame: The TSMC + Amkor Supplier Ecosystem Buyer Pool. Phoenix-metro semi-adjacent sellers see a three-tier buyer pool now concentrated locally: Tier 1 equipment vendors (ASML, Applied Materials, Lam Research field offices), Tier 2 specialty chemicals / gases / ultra-pure water (Linde, Air Products, Entegris), Tier 3 local subcontractors (cleanroom construction, calibration, logistics, staffing). The implication for advisor selection: sub-vertical depth in semi-adjacent verticals is the most valuable boutique attribute in 2026 Phoenix.

The 11 verified Phoenix-metro M&A advisors

1. IBG Fox & Fin

- HQ: Scottsdale, AZ

- Founded: 1993

- Lead bankers: Jim Afinowich (founding principal, designated broker, 500-plus transactions over 30 years, IBBA Hall of Fame charter inductee), Mike Cauley, Garry Barnes

- Sector focus: Generalist lower-middle market (manufacturing, services, distribution, healthcare)

- Deal size range: Up to $150M

- Recognition: Ranked #1 in Arizona for Investment Banker / M&A Intermediary category for 23 consecutive years by Ranking Arizona

- Why hire them: Longest unbroken Phoenix-metro M&A track record. Founder-network reach is unmatched at $5M-$150M; senior bankers run buyer calls personally.

2. William & Wall

- HQ: Scottsdale, AZ

- Lead bankers: Tro Panosian (Founder and CEO, ex-J.P. Morgan TMT NYC), Michael Tully (Executive Chairman, former CEO of AAA Arizona), David Barnett (Vice Chairman, appointed December 2025)

- Sector focus: Software, healthcare, industrial services, manufacturing, consumer (founder-led businesses)

- Deal size range: Companies under $300M revenue and above $3M EBITDA

- Distinctive content: Publishes Arizona M&A Highlights monthly and Year-in-Review — the most-cited public Phoenix-metro M&A data source

- Why hire them: Strongest founder-network reach in Scottsdale's tech and healthcare ecosystem. Monthly publication cadence keeps them at the center of buyer-pool intelligence.

3. Generational Group / Generational Equity

- Scottsdale office: 6991 East Camelback Rd, Scottsdale, AZ 85251

- Firm HQ: Richardson, TX

- Scottsdale lead: Bo Zhao (VP, Western Region; FINRA-licensed; ASU Thunderbird MBA)

- Firm founders: Dr. John Binkley (Founder), Ryan Binkley (President and CEO)

- Sector focus: Sell-side advisory for owner-led lower-middle-market across all sectors

- Deal size range: Lower-middle market (~$5M-$150M)

- Scale: 250-plus professionals, 16 offices across North America

- Why hire them: Largest national platform with a dedicated Phoenix office. National buyer pool reach without bulge-bracket cost structure.

4. BMO Capital Markets (Greene Holcomb Fisher legacy)

- Phoenix coverage: Paul Jevnick, Managing Director (referenced 2024-25 AZ Big Media bylines)

- Acquisition history: Greene Holcomb Fisher acquired by BMO Financial Group August 2016 — now operates under BMO Capital Markets brand

- Sector focus: Middle-market M&A, generalist

- Deal size range: Mid- and upper-middle market

- Why hire them: Platform IB depth with the original Greene Holcomb Fisher mid-market DNA. Strongest at $50M-$300M generalist mandates.

5. Columbia West Capital

- HQ: Scottsdale, AZ

- Founded: 2003

- Lead: Sri Malladi (senior advisor; M&A, corporate strategy, strategic finance)

- Sector focus: Middle-market M&A, capital raising, strategic consulting

- Distinctive content: Publishes Arizona Deal Intelligence monthly newsletter

- Why hire them: Twenty-plus year local presence with deep deal-flow visibility. Strong on capital raising alongside sell-side.

6. Ardent Advisory Group

- HQ: Scottsdale, AZ

- Founded: 2021

- Lead bankers: Jordan Geotas (M&A advisor, 30-plus year attorney, 20-plus year IB), George Odden (25-plus year IB at multinational banks), Nick Rossi (VP Business Development, founding member)

- Sector focus: Sell-side, generalist lower-middle-market

- Deal size range: $5M-$250M

- Scale: 20-plus transactions, $3B-plus aggregate transaction value

- Why hire them: Fastest-growing Phoenix boutique since 2021. Cross-border M&A depth via senior banker mix.

7. Stifel (Phoenix / Scottsdale)

- Phoenix-area presence: Matthew P. MacMichael Sr. joined September 12, 2025 from J.P. Morgan Wealth Management as Arizona market head overseeing Phoenix, Scottsdale, Tucson (wealth management lead)

- IB coverage: Served from broader Stifel institutional platform

- Why hire them: Strongest at $50M-$250M deals where Stifel's national IB syndication adds value. Note that Phoenix office is primarily wealth; IB MDs are based elsewhere.

8. Baird

- Phoenix presence: Phoenix wealth office; IB coverage from broader Baird platform

- Recent AZ-relevant deal: Advised Lightridge Solutions on the GEOST sale to Rocket Lab — $275M (announced May 24 2025, closed August 12 2025; structure: $125M cash + ~3.06M Rocket Lab shares ($150M) + up to $50M earnout)

- Baird 2025 firm revenue: $3.8B with $757.3M operating income per the Baird 2025 Annual Report

- Why hire them: Strongest at $75M-$300M with sub-vertical buyer pool access (aerospace, healthcare, industrial). GEOST is the most recent verified AZ-aerospace touchstone.

9. Raymond James (Scottsdale / Phoenix)

- Phoenix-area presence: Scottsdale-Kierland branch + Phoenix branch (primarily wealth; opened first AZ office 2007)

- IB coverage: Firm-wide; specific Phoenix M&A MDs not publicly listed

- Why hire them: Strong national IB platform with consumer, healthcare, and tech depth. Phoenix coverage is through firm platform rather than dedicated local MDs.

10. Houlihan Lokey (covering AZ deals from broader platform)

- Phoenix presence: No dedicated local M&A office; firm covers AZ deals from broader US platform

- Sector strength: Restructuring + middle-market M&A — strongest at distressed or complex situations

- Why hire them: Best fit for restructuring-adjacent or complex industrial M&A where Houlihan's restructuring DNA adds value. Less compelling for clean generalist mid-market mandates.

11. 2717 Group (A/E/C specialist)

- HQ: Phoenix, AZ

- Sector focus: Architecture, engineering, construction (A/E/C) industry M&A advisory

- Scale: 80-plus acquisitions in industry-specific A/E/C consolidation

- Why hire them: The dominant Phoenix-anchored sub-vertical specialist. For any A/E/C target ($5M-$100M EV), 2717 has the deepest buyer-network reach.

Honorable mentions covered from out-of-state platforms: Stout, Lincoln International, Capstone Partners, Cowen / TD Cowen — these firms cover Phoenix-area deals from broader regional and national IB teams but research did not verify dedicated Phoenix MDs at the IB level. Decision pattern: at $5M-$100M, Phoenix-anchored boutiques typically beat out-of-state platforms; at $100M-plus, the platform decision depends on syndicate fit and sub-vertical buyer access.

Phoenix Buyer-Pool Quadrant — who's actually buying?

Frame: The Phoenix Buyer-Pool Quadrant. Phoenix-metro sellers face a four-quadrant buyer pool that diverges sharply from generic US mid-market patterns:

| Quadrant | Type | Examples | Best fit for sellers in |

|---|---|---|---|

| NW — Strategic-Tech/AI | Hyperscale + enterprise SaaS strategic acquirers | Workday, Microsoft, Google, Meta, Constellation Software, NVIDIA partners | Scottsdale software, AI talent, niche SaaS, MSP, conversational AI (Paradox precedent) |

| NE — Strategic-Industrial/Aerospace | Manufacturing primes + spin entities | Honeywell Aerospace (HONA Q3 2026), Boeing, Lockheed, Raytheon, L3Harris | Aerospace components, precision machining, defense tech, ITAR-classified |

| SW — Domestic PE | Phoenix-based or AZ-active PE platforms | Pivotal Group (family office + PE since 2002), Bow River Capital, Ridgemont Equity Partners, Trinity Hunt, Levine Leichtman | Lower-middle-market services, healthcare, industrial services, BTR operators |

| SE — International / Cross-Border | Mexico-LatAm corridor + APAC supply chain | TSMC supplier ecosystem (Taiwan and Korea), Mexican family-business cross-border via Sonora-AZ border, Japanese semi supply chain | Manufacturing, logistics, electronics assembly, cross-border supply chain |

The four-quadrant cut matters for advisor selection: a Phoenix semi-supplier targeting NW (strategic tech) and NE (strategic industrial) plus SE (TSMC ecosystem cross-border) needs different bidder outreach than a Phoenix BTR operator targeting only SW (domestic PE institutional). Boutiques with vertical relationships in 2-3 quadrants typically outperform platform firms running broader but shallower outreach.

The Caris IPO precedent and Phoenix TechBio M&A

Frame: The Caris Path — Phoenix as TechBio Capital. Caris Life Sciences priced June 17, 2025 at $21 per share on 23,529,412 shares for $494.1M raised (NASDAQ: CAI), closing Day 1 at $28 (+33 percent). Caris is HQ'd in Irving, TX with Phoenix offices, but its $450M-plus Arizona investment across 5 facilities and 950+ AZ jobs validated Phoenix as a credible TechBio node.

The structural read: Phoenix biotech sellers now have a credible local IPO precedent to anchor BATNA in sale negotiations. Combined with Banner Health's regional dominance, HonorHealth's expansion (Evernorth Care Group 18-clinic acquisition from Cigna announced September 2, 2025 closing January 2026), and TGen's translational genomics ecosystem, Phoenix has reached scale where global pharma corp-dev (Roche, Thermo Fisher, Illumina, AstraZeneca, Novartis) actively scouts.

Recommended advisor pattern for Phoenix biotech founders: combine a Phoenix-anchored boutique (William & Wall, Columbia West Capital) for senior-banker face-time with a specialty-tech-tier bank (Cantor Fitzgerald Healthcare, MTS Health Partners, Centerview) for global corp-dev access. The dual-mandate pattern mirrors what Philly Cellicon Valley CGT founders use.

The Honeywell HONA spin catalysis frame

Frame: HONA Carveout Catalysis. Honeywell Aerospace's planned Q3 2026 spin as NASDAQ: HONA (Phoenix HQ, $17.4B revenue, Investor Day June 3 2026) creates two M&A scenarios for Phoenix-area suppliers:

-

Pre-spin (now through Q3 2026): Honeywell's parent board makes carveout decisions on non-core aerospace lines. Phoenix-metro acquirers with strategic interest in specific Honeywell aerospace product lines can position for divestiture transactions.

-

Post-spin (Q3 2026 onward, ramping 2027-28): Independent HONA board typically conducts portfolio reviews 6-18 months post-spin. Expected 2027-28 Honeywell Aerospace divestiture wave creates buyer-pool depth for Phoenix sellers in defense, space, and avionics adjacencies — and creates carveout sources for PE platforms running aerospace roll-ups.

The structural significance: HONA inherits roughly 2,540 supplier contracts worth approximately $2.92B annually. A standalone board with public-company discipline will be motivated to both consolidate the supplier base (driving inbound M&A interest for top-tier Phoenix suppliers) and divest non-core internal lines (creating PE platform plays for Phoenix-area capital).

The Intel Talent Cascade

Frame: Intel Talent Cascade — Phoenix as 2026's Best Engineering M&A Market. Intel's 2025-26 restructuring under CEO Lip-Bu Tan totaled 25,000-plus position eliminations (headcount dropped from approximately 109,000 to roughly 75,000). Q2 2025 layoffs hit roughly 20 percent of workforce; 2025 capex was trimmed 10 percent to $18B. Intel Fab 52 (Chandler, Ocotillo campus) is fully operational producing 18A nodes in 2025-26.

The cascade: Phoenix engineering talent released from Intel was absorbed by TSMC Fab 21 (4nm in production, 3nm and 2nm phases ramping 2026-28), Amkor Peoria (groundbreaking October 2025, 3,000 jobs at ramp), and a growing ecosystem of EDA and equipment vendor field offices. The implication for Phoenix engineering-services and design-house targets: talent moat thickens daily, supporting premium multiples for sellers running processes in 2026.

Phoenix M&A deal cadence — recent ≤12 months

A sampling of Phoenix-metro deals in the May 2025 to May 2026 window:

| Deal | Buyer | Target | Value | Date |

|---|---|---|---|---|

| Workday acquires Paradox | Workday | Paradox (Scottsdale AI hiring) | $1.0B cash | Announced Aug 21 2025; closed Oct 1 2025 |

| TopBuild acquires Progressive Roofing | TopBuild (NYSE: BLD) | Progressive Roofing (Phoenix, ex-Bow River) | $810M cash, 9.1x EBITDA | Announced Jul 9 2025; closed Jul 15 2025 |

| Honeywell Solstice spin | (Distribution to shareholders) | Solstice Advanced Materials (NASDAQ: SOLS) | Tax-free spin | Closed Oct 30 2025 |

| Rocket Lab acquires GEOST | Rocket Lab | Lightridge Solutions (Tucson) | $275M | Announced May 24 2025; closed Aug 12 2025 |

| Caris Life Sciences IPO | (Public markets) | Caris (Irving TX + Phoenix ops) | $494.1M raised at $21 | Priced Jun 17 2025 |

| HonorHealth-Evernorth Care Group | HonorHealth | Cigna's 18 Phoenix clinics | Not disclosed | Announced Sep 2 2025; closing Jan 2026 |

| Tricon BTR Phoenix-area | Tricon Residential (Blackstone) | Arcadia Capital + Platform Ventures JV | $44.1M for 91 units (~$485K/unit) | Sep 18 2025 |

| N. Harris Computer-GlobalMeet | Constellation Software / N. Harris | Pivotal Group (Phoenix family office) | Not disclosed | Closed Dec 2 2025 |

| Knight-Swift FedEx terminal | Knight-Swift | EQT Real Estate | $30M (vs. EQT's 2021 $24.1M buy) | Feb 2026 |

| Argano-Anavate Partners | Argano (Plano TX) | Phoenix Anaplan consulting | Not disclosed | 2025 |

| Levine Leichtman-SYNERGY HomeCare | Levine Leichtman | NexPhase Capital (Tempe AZ franchisor) | Not disclosed | 2025 |

| Trinity Hunt-Amendola Communications | Trinity Hunt Partners | Private (Scottsdale healthcare PR) | Not disclosed | 2025 |

| SOLV Energy-Spartan Infrastructure | SOLV Energy | Private (Mesa high-voltage T&D) | Not disclosed | 2025 |

| Ionic Partners-CXT Software | Ionic Partners | Private (Phoenix last-mile software) | Not disclosed | 2025 |

| Ridgemont-CRS | Ridgemont Equity Partners | Private (Phoenix temp housing/insurance) | Not disclosed | 2025 |

Pattern read: 2025 deal flow was dominated by (a) tech and AI exits (Paradox, CXT), (b) building products and home services (Progressive Roofing, SYNERGY HomeCare), (c) data-center-adjacent services (Spartan Infrastructure, Argano), and (d) healthcare consolidation (HonorHealth-Evernorth, Atria Heart-CVA, Imagen Dental). The semi-supplier wave is expected to ramp 2026-28 as TSMC Fab 21 Phase 2 and Amkor Peoria production come online.

Phoenix economic backdrop — why this matters

Phoenix-metro economic data underpins the M&A buyer-pool composition:

- Maricopa County population (2025): 4,787,790, +7.9 percent from 2020; ranked #1 in US for net migration 2023-24 per AZ Commerce

- Maricopa County GDP (2023): $383.9B, 73.4 percent of state, +2.7 percent real growth 2022-23 per AZ Economics

- Phoenix MSA = 75 percent of Arizona employment per AZ Economics

- 2025 retail sales (Maricopa): $74.8B, +3.1 percent YoY per AZ Commerce

- Industrial real estate absorption 2025: 13.9M sq ft; Q1 2025 = 4.1M sq ft (#3 metro in US) per Kidder Mathews / Colliers

- Industrial vacancy: 11.2 percent overall (historic deliveries); modern warehouse stays sub-5 percent per Kidder Mathews

The compounding effect: Phoenix population growth feeds the consumer / healthcare / BTR demand base; the industrial absorption supports semi-supplier and data-center-supplier capex; the GDP growth gives lenders comfort on financing transactions in Phoenix specifically.

Honest VDR comparison for Phoenix-metro M&A

Phoenix-metro sell-side processes at $5M-$300M EV typically need: multi-party permissioning (15-40 buyer parties), NDA gating with executed-NDA verification, dynamic watermarking for confidential semi-supplier or aerospace document handling, and page-level analytics for buyer engagement verification.

The honest landscape:

| Vendor | Best for | Pricing (2026) | Phoenix-relevant strength |

|---|---|---|---|

| Datasite | $200M+ cross-border or aerospace ITAR | $25K+/year; per-page $0.40-0.85 legacy | Deepest IB workflow integration; preferred by bulge-bracket |

| Intralinks (SS&C) | ITAR-classified aerospace; cross-border | $7,500 starting; $4K-$25K+/year contracts | Deepest IRM controls for defense / export-controlled docs |

| Firmex | Mid-market boutique processes | $625/mo+ flat; ~$7,800/year average | Predictable cost; unlimited users |

| Ansarada | Mid-market with AI Q&A | $244-$5,134/mo tiered | AI-driven Q&A workflow management |

| iDeals | Mid-market international | Quote-based | Strong UI; international familiarity |

| Peony | Phoenix sub-$100M EV with boutique advisor | $52/admin/mo flat (Data Room plan) | Unlimited rooms, page analytics, NDA gates, dynamic watermarks; 5-min setup |

We make Peony, so this is honest disclosure: for $200M-plus cross-border or ITAR-classified aerospace deals, most counsel will recommend Datasite or Intralinks. For sub-$100M Phoenix-metro processes — which covers approximately 85 percent of 2025 Phoenix deal count by William & Wall's review — the flat-rate options (Peony, Firmex, Ansarada) typically deliver equivalent functionality at substantially lower transaction cost. For a deeper teardown, see our virtual data room pricing guide.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Phoenix shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 11 Best M&A Advisors in San Diego — Southwest sister cluster covering biotech ($26.2B 12-month wave), defense (Shield AI $12.7B), and wireless/semis (Qualcomm Alphawave $2.4B)

- 11 Best M&A Advisors in Seattle — Tier A US city #1 with Microsoft / AWS / Boeing buyer-pool depth

- 11 Best M&A Advisors in Miami — Tier A US city #2 with LatAm cross-border and migratory family-office buyer pool

- 11 Best M&A Advisors in Washington DC — Tier A US city #3 with defense / federal contractor depth

- 11 Best M&A Advisors in Charlotte — Tier A US city #4 with banking and financial services depth

- 11 Best Boutique M&A Advisors in Philadelphia — Tier A US city #5 with pharma / Cellicon Valley CGT depth

- 11 Best Boutique M&A Advisors in Atlanta — Sun Belt comparator

- 11 Best Boutique M&A Advisors in Dallas — Sun Belt comparator

- Best M&A Advisors in Salt Lake City — Mountain West comparator: an investor-heavy, advisor-light tech-exit metro anchored by the homegrown bank Crewe Capital

- M&A Due Diligence Process Guide — process map across all DD layers

- Sell-Side Due Diligence — VDD for Phoenix-metro sellers preparing for process

- Best Data Room for Small M&A Deals — VDR selection for sub-$30M sales, the band where most Phoenix-metro founder-led mandates close

- Virtual Data Room Pricing Guide — full vendor landscape

You might also like

May 23, 2026

13 Best Boutique M&A Advisors in Denver for $5M-$200M Deals (2026)

May 8, 2026

12 Best Boutique M&A Advisors in Washington DC ($5M-$200M 2026)

May 7, 2026

12 Best Boutique M&A Advisors in Seattle ($5M-$200M Deals 2026)