12 Best Boutique M&A Advisors in Washington DC ($5M-$200M 2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

Over the past year I've fielded data-room questions from govcon corp-dev teams running CMMC 2.0 + FOCI mitigation diligence in parallel with DCSA notification workflows, defense PE associates at Arlington Capital / Veritas / AE Industrial running federal-services rollup sell-sides, Bethesda biotech founders triangulating NIH-proximity vs. NYC-tier biotech buyer pools, FOCI counsel coordinating cleared-personnel summaries with the M&A advisor's data-room tiering, and Northern Virginia federal-IT sellers facing SAIC / Leidos / CACI / Booz Allen / BigBear.ai strategic-acquirer pitches. DC sits structurally apart from every other US M&A metro: the Defense Industrial Base lens dominates DC M&A in a way no other US metro experiences. Washington DC anchors the densest defense, aerospace, and government-services strategic-acquirer pool in the United States (eight of the ten largest defense and federal-services strategic acquirers -- SAIC, Leidos, CACI, Booz Allen Hamilton, BigBear.ai, Northrop Grumman, Lockheed Martin, RTX -- are headquartered within 30 miles of DC), the Q3 2025 record for D&G M&A activity (125 deals, +30% year-over-year per Raymond James Defense & Government Quarterly Q3 2025; 185 defense deals announced YTD 2025; 2025 A&D deal volume +33.5% over 2024 per Mergermarket), the 2025 marquee scale anchor (AeroVironment-BlueHalo $4.1 billion closed May 1, 2025; Stonepeak-ATSG $3.1 billion closed April 11, 2025), and the only US metro where Maryland (7) and Virginia (6) ranked the top two seller states by count in Q1 2026 LTM defense M&A -- confirming DC as the geographic epicenter of Defense Industrial Base consolidation. The single hardest DC question -- which DC boutique handles CMMC 2.0 + FOCI + cleared workforce diligence -- breaks on sub-vertical specialty (cleared-deal-handling tier vs. federal-services rollup vs. NIH-proximity biotech vs. cleared-deal legal complement), not firm-name brand. I run Peony, a data room platform for M&A and private equity, and Washington DC is one of the ten US metros (San Francisco, NYC, LA, Boston, Seattle, Miami, Dallas, Chicago, Atlanta, and Houston being the others) where we see the most boutique M&A advisor deal flow on the platform. Building this Washington DC guide as part of our city series -- see also our SF/Bay guide, NYC guide, LA guide, Boston guide, Seattle guide, Miami guide, Dallas guide, Chicago guide, Atlanta guide, Houston guide, Philadelphia guide, and Phoenix guide.

This guide maps 12 verified Washington DC, Northern Virginia, and Maryland-headquartered or DC-led boutique M&A advisory firms (with explicit bank-owned-tier and law-firm caveats where applicable) active in the $5M-$200M EV deal range as of May 2026. Every firm has been verified for DC-area presence, deal size band, and recent transaction activity. Bulge-bracket banks (Goldman Sachs DC, Morgan Stanley DC, JPMorgan DC, Jefferies DC) and elite-boutique upper-tier specialists are excluded by design -- their structural sweet spot is $500M+ deals, and a $25M-$200M sell-side at any of those firms is a B-team engagement. Generalist boutiques whose primary book is below $5M EV (true business-broker shops) are also excluded.

Quick answer: The best Washington DC M&A advisors for $5M-$200M deals as of May 2026 split across the five-axis DC decision matrix: KippsDeSanto & Co (Tysons, Virginia; Capital One subsidiary; ADGS pure-play; SilverEdge/SAIC $205M October 2025), Houlihan Lokey ADG (DC office; global #1 by transaction count per Mergermarket; senior leadership in DC office), The McLean Group (McLean, Virginia; founded 1996; DGI specialty), Renaissance Strategic Advisors (Arlington; strategy plus M&A; founded 2007 by Pierre Chao), and FOCUS Investment Banking (Vienna, Virginia; #2 Axial Top 25 LMM IB Q2 2025) anchor the cleared-deal-handling tier and federal-services rollup pool; Capstone Partners (Boston HQ caveat) and Baird Defense & Government (Milwaukee HQ caveat) anchor the bank-owned-boutique tier; Lincoln International DC ADG (Chicago HQ; July 2025 launch with Chertoff Group partnership) and DC Advisory (Daiwa Securities international subsidiary) anchor the cross-border ADG and expansion-stage entries; Aronson Capital Partners / Aprio Capital Advisors anchors the GovCon legacy plus accounting integration; Cain Brothers DC anchors NIH-proximity biotech (KBCM-gated); Hogan Lovells M&A anchors the cleared-deal legal counsel ecosystem complement (NOT investment bank).

TL;DR: Washington DC sits at the intersection of Defense Industrial Base M&A (KippsDeSanto's SilverEdge/SAIC $205M close October 17, 2025, KippsDeSanto's Ask Sage/BigBear.ai ~$250M December 31, 2025, Houlihan Lokey's Stellar Blu/Gilat close January 6, 2025), the federal-services rollup pool (The McLean Group's Rite Solutions/Arcfield 2025, Emagined Security/Neovera 2025, ARRAY IT/CGI Federal 2025), the cleared-deal-handling tier (Hogan Lovells' Lockheed Martin/Terran Orbital $450M 2024-25), and the NIH-proximity biotech buyer pool ([Cain Brothers DC healthcare practice]). Q3 2025 saw 125 D&G deals (+30% YoY per Raymond James); 2025 full-year D&G activity ran 185 defense deals YTD with A&D up 33.5% over 2024 per Mergermarket. AeroVironment-BlueHalo $4.1B closed May 1, 2025; Stonepeak-ATSG $3.1B closed April 11, 2025 (Goldman Sachs advised ATSG; Evercore advised Stonepeak -- KippsDeSanto did NOT advise this deal). Maryland (7) and Virginia (6) ranked top two seller states by count in Q1 2026 LTM defense M&A. The HSR threshold rose to $133.9M effective February 17, 2026 -- a structural input for any cleared deal at the larger end of the LMM band. For DC-area founders selling between $5M and $200M, the right answer is almost always a sub-vertical specialty boutique aligned to one of the five DC axes: KippsDeSanto, Houlihan Lokey ADG, The McLean Group, Renaissance Strategic Advisors, FOCUS Investment Banking, Capstone Partners, Baird D&G, Lincoln International DC, DC Advisory, Aronson Capital Partners / Aprio, Cain Brothers DC, and Hogan Lovells M&A -- not a bulge-bracket DC desk. Below: the firms, the deal-size bands, the fees, and five recent verified DC-area closes that show how the metro's market actually works.

How Did I Verify This List?

Every firm on this list passes four filters:

- Washington DC, Northern Virginia, or Maryland headquarters or principal DC-area office -- DC, McLean, Tysons, Arlington, Reston, Vienna, Bethesda, Rockville, Baltimore, or the broader DC-Baltimore corridor; not a satellite branch staffed by a single analyst

- Verifiable transaction record -- closed at least 5 transactions in the $5M-$200M EV range in the last 36 months across defense, aerospace, government services, federal IT, cleared cyber, healthcare services, or NIH-proximity biotech, sourced from press releases, BusinessWire and PR Newswire announcements, SEC EDGAR filings (8-K, 10-K), or firm transaction walls

- Active 2024-2026 deal activity -- not a legacy firm coasting on pre-2020 relationships

- Lower-middle-market core -- modal deal size in the $5M-$200M EV band; firms whose primary book is below $5M EV (true Main-Street brokers) or above $500M EV (where geography stops mattering and bulge-bracket DC desks dominate) are excluded

I cross-referenced firm websites against Mergermarket 2024-2025 ADG league tables, Raymond James Defense & Government Quarterly Q3 2025, BDO Capital Advisors ADG Quarterly, the Axial Top 25 Lower Middle Market Investment Bank Q2 2025 ranking, Bloomberg Government, Federal News Network, Aviation Week, and individual firm press releases for verified 2024-2026 transaction history. Where a firm claimed DC leadership but the senior team was actually based elsewhere (Capstone Partners HQ Boston; Baird Defense & Government HQ Milwaukee; Lincoln International HQ Chicago; DC Advisory HQ London/Tokyo), I framed the geographic caveat explicitly rather than dropping the firm. Bulge-bracket DC offices (Goldman Sachs, Morgan Stanley, JPMorgan, Citi, BofA, Jefferies) and elite-boutique upper-MM specialists are excluded by design -- their structural sweet spot is $500M+ deals and the $25M-$200M EV DC seller is a B-team client at those firms.

Five caveats on the DC specialty bench:

First, Houlihan Lokey ADG is included with explicit framing as a bulge-bracket-boutique-tier global firm rather than a true independent. The DC office at 1909 K Street NW houses the global ADG practice with senior leadership anchored in DC, but the Houlihan Lokey parent is LA-headquartered with 30 ADG bankers across DC, LA, and London. The structural caveat parallels the one we applied to KBCM in our Seattle guide, Cain Brothers in our Boston guide, and Houlihan Lokey Miami in our Miami guide -- the firm earns a place because the senior team and franchise depth are real, but the parent ownership shapes engagement-letter-term flexibility.

Second, Capstone Partners is Boston-headquartered with Huntington Bancshares ownership since June 2022 and TM Capital absorbed in December 2025 (Capstone is the firm formerly known as Capstone Headwaters until the 2022 rebrand). The DC ADGS practice has senior partners covering the Mid-Atlantic, but the parent firm sits in Boston. We include Capstone on this list as the bank-owned-boutique-tier full-service middle market option for DC founders comparing the cleared-deal-handling tier with broader 12-industry-group ADGS coverage.

Third, Baird Defense & Government is Milwaukee-headquartered (Robert W. Baird & Co. parent). The Baird Defense & Government practice is housed within Baird Global Investment Banking; DC has bench coverage but parent HQ is Milwaukee. We include Baird on this list as the bank-owned-boutique-tier high-volume option ($6.4 billion 2025 closed in defense plus government across 16 transactions).

Fourth, Lincoln International is Chicago-headquartered with a July 2025 DC ADG franchise launch. Co-heads Ryan O'Toole and Eric Cartier joined Lincoln from Houlihan Lokey ADG in July 2025; the firm has a Chertoff Group strategic partnership for DC ecosystem integration. The DC office is expansion-stage rather than long-tenured.

Fifth, DC Advisory is the international Daiwa Securities subsidiary -- NOT 'Washington DC Advisory.' The firm name's 'DC' originally referenced Daiwa Capital. The firm was formed from the rollup of Close Brothers Corporate Finance plus several boutiques plus Daiwa's ECM franchise. We include DC Advisory on this list as the cross-border ADG option (top-3 mid-market industrials advisor 2025 per Mergermarket EMEA league tables). Avascent Group is excluded because it was acquired by Oliver Wyman in October 2022 and is no longer an independent boutique. Centerview Partners and Lazard are excluded because neither has a DC-anchored ADG practice; we cite them as cross-coast comparison anchors only. Pillsbury Winthrop, Crowell & Moring, and Wiley Rein are mentioned as bench legal complements only -- tier-2 below Hogan Lovells in M&A volume.

Hogan Lovells is a LAW FIRM, not an investment bank -- the firm was formed in 2010 via the merger of Hogan & Hartson (DC, founded 1904) and Lovells (London, founded 1899). DC is the firm's largest US office (Columbia Square, 555 13th Street NW). We include Hogan Lovells on this list explicitly framed as a transactional legal counsel ecosystem complement to the M&A advisor list -- NOT as a primary investment-bank advisor option. The firm earns inclusion because the cleared-deal-handling tier is incomplete without the legal-counsel layer that handles FOCI mitigation, DCSA notification, and CFIUS workflows.

Deqian Jia, my co-founder, adds the technical readiness lens here:

"Across the Washington DC-area data rooms we host, the gap between advisors who consistently close in 6 months and those who run 12-month processes is preparation. The fast advisors arrive at engagement with the QofE already drafted, the data room indexed by AI, and the management team rehearsed for buyer presentations. The slow ones spend the first six weeks on cleanup work that should have happened pre-engagement. DC's structural distinguishing feature is the cleared-deal layer -- the same data room often hosts unclassified financial and commercial documents in the main tier alongside FOCI-mitigation correspondence and cleared-personnel summaries in a gated tier, and the data room has to support both bidder-facility-clearance verification and DCSA notification workflows alongside the typical strategic-acquirer or PE-platform diligence sequence. When you're picking a DC advisor, ask to see a sample data room from a recent cleared close -- not a pitch deck. The folder structure tells you everything." -- Deqian Jia, Peony co-founder

Quick Comparison Table

| Firm | Deal Size (EV) | Sectors | Fee Model | Best For |

|---|---|---|---|---|

| KippsDeSanto & Co | $20M-$500M | ADGS pure-play; cyber and federal IT | Modified Lehman + retainer | Tysons VA cleared-deal-handling tier; Capital One subsidiary; 200+ closed; SilverEdge/SAIC October 2025 |

| Houlihan Lokey ADG | $100M-$2B | Aerospace, Defense, Government Services + cross-border | Lehman + retainer | DC office; global #1 ADG advisor by transaction count per Mergermarket; senior leadership in DC office |

| The McLean Group | $20M-$80M | Generalist with DGI (Defense, Govt, Intel) specialty | Lehman + retainer | McLean VA generalist; founded 1996; 60+ pros across 30+ cities; six DC senior MDs |

| Renaissance Strategic Advisors | $30M-$300M | A&D and National Security exclusively (strategy + M&A) | Lehman + retainer | Arlington VA; founded 2007 by Pierre Chao; 85 pros + 250 senior advisors |

| FOCUS Investment Banking | $5M-$50M | Multi-vertical with Government & Defense (GAD) team | Lehman + retainer | Vienna VA; #2 Axial Top 25 LMM IB Q2 2025; Manan K. Shah leads GAD; 44-year DC franchise |

| Capstone Partners DC | $30M-$300M | ADGS practice (Boston HQ caveat); 12 industry groups | Lehman + retainer | Bank-owned-boutique-tier (Huntington Bancshares); Tess Oxenstierna ADGS lead |

| Baird Defense & Government | $50M-$1B | Defense, Govt Services, Aerospace, Federal IT/Cyber, Healthcare Govt | Lehman + retainer | Bank-owned-boutique-tier (Milwaukee HQ caveat); $6.4B / 16 deals 2025 closed |

| Lincoln International DC ADG | $50M-$500M | Aerospace, Defense, Government Services | Lehman + retainer | Expansion-stage DC office July 2025; O'Toole + Cartier ex-Houlihan; Chertoff partnership |

| DC Advisory | $30M-$300M | International mid-market ADG cross-border | Lehman + retainer | Daiwa Securities subsidiary; top-3 mid-market industrials 2025 per Mergermarket EMEA |

| Aronson Capital Partners / Aprio | $20M-$100M | GovCon, Federal IT, Tech Services, Health Tech | Lehman + retainer | Bethesda MD; Aprio merger January 1, 2023; 25+ year DC GovCon legacy; John Saunders MP |

| Cain Brothers DC | $50M-$1B | Pure healthcare services + NIH-proximity biotech | Lehman + retainer | KeyBanc Capital Markets / KeyCorp division (KBCM-gated); Mid-Atlantic healthcare |

| Hogan Lovells M&A | $50M-$1B+ | Global law firm M&A advisory (legal counsel complement, NOT investment bank) | Hourly billing | DC HQ (largest US office); $400B+ M&A advised lifetime; Elizabeth Donley Co-Head US M&A |

Why Is Washington DC the M&A Capital for the Defense Industrial Base, Federal IT Services, Cleared Cyber, and NIH-Proximity Biotech?

Washington DC's M&A market is structurally distinct from every other US metro in five ways, and each one shows up in the deal-size bands and advisor specialty mix.

First, the Defense Industrial Base lens dominates DC M&A like no other metro. Q3 2025 saw 125 D&G (Defense & Government) M&A deals announced (+30% year-over-year) per Raymond James Defense & Government Quarterly Q3 2025; full-year 2025 saw 185 defense deals announced YTD with 2025 A&D deal volume +33.5% over 2024 per Mergermarket Aerospace & Defense YE-2025 report. First-half 2025 alone saw 250 A&D transactions versus 175 in H2 2024 -- the strongest defense M&A wave since the 2010-2012 post-Iraq drawdown consolidation. Q3 2025 ADG deal mix per BDO Capital Advisors data was 38% aerospace and space, 35% government and defense technology, 16% defense electronics, and 11% other -- a sector breadth no other metro matches at this density. Maryland (7) and Virginia (6) ranked the top two states by seller count in Q1 2026 LTM defense M&A, confirming DC metro as the geographic epicenter of Defense Industrial Base consolidation.

Second, the 2025 marquee deals set scale anchors that DC ADG founders cite as bid-validation precedents. AeroVironment-BlueHalo $4.1 billion -- defense electronics and space platform consolidation -- closed May 1, 2025 per AeroVironment 8-K. Stonepeak-Air Transport Services Group (ATSG) $3.1 billion -- air-cargo and DoD logistics infrastructure acquisition -- closed April 11, 2025 per ATSG 8-K (Goldman Sachs advised ATSG; Evercore advised Stonepeak; KippsDeSanto did NOT advise this deal -- this is the most-cited mid-market DC misattribution, so worth correcting up front). On the mid-market side, SAIC-SilverEdge $205M closed October 17, 2025 (KippsDeSanto sell-side) and Ask Sage-BigBear.ai ~$250M closed December 31, 2025 (KippsDeSanto sell-side) anchor the recent KippsDeSanto deal cadence. Stellar Blu Solutions to Gilat Satellite Networks closed January 6, 2025 (Houlihan Lokey ADG advisor on the sell-side). These named deals are the 2025 marquee benchmarks DC ADG founders cite when validating bid-pool credibility.

Third, the cleared-deal-handling tier is uniquely DC. Cleared and classified contract data, ITAR (International Traffic in Arms Regulations) export control, FOCI (Foreign Ownership Control or Influence) mitigation, DCSA (Defense Counterintelligence and Security Agency) notification, and Section 889 / Buy American Act / Made in America Office implications -- these are DC-distinguishing concerns that don't exist in other metros' M&A calculus. Cleared deals add 0.25-0.5% fee premium for the FOCI mitigation legal complexity and 30-60 day DCSA notification timeline. The cleared-deal-handling tier of practitioners with documented routine experience structuring two-tier classified data rooms includes KippsDeSanto, Renaissance Strategic Advisors, Houlihan Lokey ADG, and The McLean Group. Hogan Lovells (legal counsel) handles the FOCI, DCSA, and CFIUS workflows on the legal side -- the cleared-deal-handling tier is incomplete without the legal-counsel layer.

Fourth, the federal-services rollup pool is the densest in the United States. The PE-platform consolidator buyers fishing through DC ADG mid-market most actively in 2024-2026 include Veritas Capital ($45B AUM, NYC plus DC; portfolio includes Peraton, CAES, BlueHalo (now AeroVironment), Cyrus); Carlyle Aerospace & Defense (DC HQ; Tier-1 prime divestiture buyer); Sagewind Capital (NYC plus DC; portfolio includes Sabel Systems acquired November 2024 via KippsDeSanto, plus DZYNE, By Light, Sealing Technologies); AE Industrial Partners (Boca Raton plus DC; portfolio includes Belcan, Redwire, Altamira, BigBear.ai until 2024 IPO); Arlington Capital Partners (DC HQ; portfolio includes Centauri, Polaris Alpha, Pangiam, The Centech Group); Enlightenment Capital (Chevy Chase MD; portfolio includes 22nd Century Technologies, Cordatis, Knight Point Systems); Bluestone Investment Partners (DC); and Godspeed Capital (DC). Strategic-acquirer buyer-pool depth: SAIC (Reston VA, NYSE: SAIC -- closed SilverEdge $205M October 2025), Leidos (Reston VA, NYSE: LDOS), CACI (Reston VA, NYSE: CACI), Booz Allen Hamilton (McLean VA, NYSE: BAH), BigBear.ai (Columbia MD, NYSE: BBAI -- closed Ask Sage ~$250M December 31, 2025), Astrion (Brightstar Capital Partners portfolio company, formed December 2023 from ERC + Oasis Systems combination -- closed Axient via KippsDeSanto September 2024), Mythics (Norfolk VA -- closed Three Wire Tech Resale via KippsDeSanto), CGI Federal (Fairfax VA -- closed ARRAY IT via The McLean Group). The buyer-pool depth is unmatched in any other US metro -- 8 of the 10 largest defense and federal-services strategic acquirers are HQ'd within 30 miles of DC.

Fifth, the cybersecurity M&A 2025 anchor wave plus the NIH-proximity biotech buyer pool produce two parallel non-defense surges that intersect with DC ADG boutiques. Cybersecurity M&A 2025 set records: Alphabet's $32 billion acquisition of Wiz (announced March 2025, closing pending); Palo Alto Networks acquiring CyberArk for $25 billion (announced 2025); Palo Alto Networks acquiring Chronosphere for $3.35 billion (closed 2025); CrowdStrike acquiring SGNL for $740 million (closed January 2026). DC-anchored cyber boutiques (KippsDeSanto, The McLean Group, Capstone Partners DC) are all active in mid-market cyber sell-side mandates 2024-2026. The NIH-proximity biotech buyer pool (Bethesda, Rockville, DC; ~150 firms; concentrated in clinical-stage therapeutics, diagnostics, and HCIT; dependent on the NIH, Clinical and Translational Science Centers, and ARPA-H grant ecosystem) is materially smaller than Boston Kendall Square or San Francisco SoMa-Mission Bay but creates a structurally distinct healthcare M&A backdrop for Cain Brothers DC and Mid-Atlantic Provident Healthcare Partners coverage.

The structural takeaway: Washington DC is the only US metro where the Defense Industrial Base lens, the federal-services rollup pool, the cleared-deal-handling tier, the cyber-M&A wave, and the NIH-proximity biotech buyer pool converge at this density -- and the right advisor for a DC sell-side is structurally different from the right advisor for a Boston biotech mandate, an SF tech mandate, a Seattle SaaS mandate, a Charlotte healthcare-services or banking-fintech mandate, or a Miami LatAm cross-border mandate. The Defense Industrial Base lens dominates DC M&A in a way no other metro experiences.

DC founders also weigh five timing factors that don't exist in other metros' M&A calculus:

| Timing factor | What it does | Decision implication |

|---|---|---|

| FY27 DOD budget cycle (Oct 1, 2026 start) | Pre-FY27 CR and full-year appropriation timing affects program-of-record momentum | Q3 2026 typically softest M&A timing; Q1 2027 typically firmest |

| Continuing Resolution (CR) cycles | Extended CRs depress new-program contract-vehicle award velocity | Suppresses acquisition multiples for federal services targets dependent on new program ramp |

| Administration transition | Top-of-line and program-priority shifts post-Jan 20, 2025 | Creates 12-18 month uncertainty premium suppressing some early-2025 multiples; clarity post-Oct 2026 expected |

| NDAA cycles | Annual NDAA (typically passes Dec) confirms program funding | Deals tied to specific program contracts often time around NDAA passage |

| DCSA / DCAA workload backlogs | Clearance processing time and contract-cost-audit timing affects post-close transition | 6-12 month DCSA backlog should be factored into multi-year sell-process scoping |

These timing factors do NOT exist in other metros' M&A calculus. A Seattle SaaS founder timing exit around Microsoft or Google buyer fiscal-year close (June 30) is a different problem than a DC defense supplier timing exit around DOD budget cycle and DCSA throughput.

What Should I Look For in a Washington DC M&A Advisor?

Five filters that matter more in DC than in other US metros:

-

Cleared-deal-handling depth (when relevant) -- if your business has cleared contract performance history, ITAR-controlled facility, classified-adjacent program work, or any TS/SCI personnel, the right advisor has documented FOCI mitigation experience, two-tier classified data room structuring depth, and DCSA notification workflow familiarity. The cleared-deal-handling tier of practitioners includes KippsDeSanto, Renaissance Strategic Advisors, Houlihan Lokey ADG, and The McLean Group. Hogan Lovells provides the legal counsel layer. Ask the pitching senior banker to walk through the last three closes where they personally led FOCI mitigation correspondence and DCSA notification timing.

-

Defense-aerospace strategic-acquirer pool relationship density -- the defense-aerospace strategic-acquirer pool (Lockheed Martin, RTX, Northrop Grumman, Boeing, L3Harris, BAE Systems, Leonardo DRS, GE Aerospace, Howmet Aerospace, TransDigm, HEICO) plus the Tier-1 federal services strategic-acquirer pool (SAIC, Leidos, CACI, Booz Allen Hamilton, BigBear.ai, Astrion, Mythics, CGI Federal) plus the PE platform consolidator pool (Veritas, Carlyle, Sagewind, AE Industrial, Arlington Capital, Enlightenment, Bluestone, Godspeed) -- the right advisor names current contacts at each of these named buyers, not generic firm-level references. Ask each pitching firm to walk through their last three Tier-1 prime or PE-platform interactions and tell you which buyers they would call first for your deal.

-

Senior-banker engagement -- the DC LMM band ($25M-$200M EV) requires senior bankers personally on every buyer call. Boutiques like KippsDeSanto, Renaissance Strategic Advisors, The McLean Group, FOCUS Investment Banking, and Aronson Capital Partners / Aprio all run senior-banker models structurally. Bank-owned-boutique-tier firms (Houlihan Lokey ADG, Capstone Partners DC, Baird Defense & Government, Lincoln International DC, Cain Brothers DC) sometimes delegate to VPs and analysts because the parent-firm cost structure spreads MD time across multiple mandates.

-

Sub-vertical specialty depth -- 'DC generalist' is not enough when your deal turns on cleared cyber service buyer-pool depth, defense-aerospace strategic-acquirer corp-dev cycles, or a specific federal IT services PE-platform rollup buyer. The right advisor names five recent buyers in your specific sub-vertical without having to look them up. Single-vertical DC specialty firms include KippsDeSanto and Renaissance Strategic Advisors (ADGS pure-play), Houlihan Lokey ADG (global ADG anchor), and Aronson Capital Partners / Aprio (GovCon plus federal IT integrated with accounting and tax).

-

Engagement-letter-term flexibility -- DC true-independents (KippsDeSanto under Capital One but operationally independent, Renaissance Strategic Advisors, The McLean Group, FOCUS, Aronson/Aprio) all run engagement-letter terms that can be negotiated without head-office sign-off. The bank-owned-boutique-tier firms (Houlihan Lokey, Capstone, Baird, Lincoln, Cain Brothers) and the global-firm law office (Hogan Lovells) structurally do not. For a DC founder with strong leverage on retainer credit, tail-period exclusions, and minimum-fee floors, the structural fit is usually a true independent with named partner engagement.

For pricing comparisons across data room platforms, our pricing guide covers what DC specialty boutiques typically charge and how that compares to bulge-bracket alternatives. For confidentiality and watermarking specifically, Peony embeds buyer email plus exact view timestamp into every page of every CIM -- particularly critical for cleared-deal data rooms where the forensic audit trail back to the specific bidder is part of the FOCI mitigation file.

Which Washington DC M&A Advisors Anchor the Defense, Aerospace, and Government Services Specialty Tier?

For DC-area founder-led defense, aerospace, government services, federal IT, and cleared cyber sellers, four firms anchor the cleared-deal-handling tier and the ADGS specialty tier: KippsDeSanto & Co (Tysons, Virginia; ADGS pure-play; Capital One subsidiary), Houlihan Lokey ADG (DC office; global #1 ADG advisor by transaction count), Renaissance Strategic Advisors (Arlington; strategy plus M&A combined model), and The McLean Group (McLean; DGI generalist with deepest local senior bench). The first call splits structurally on specialty depth (KippsDeSanto and Renaissance) versus bulge-bracket-boutique scale (Houlihan Lokey ADG) versus generalist DGI bench (The McLean Group).

1. KippsDeSanto & Co

HQ: 1851 Alexander Bell Drive, Suite 350, Reston / Tysons, Virginia (within the McLean-Tysons defense corridor) Founded: 2007 by Bob Kipps and Kevin DeSanto (both ex-Houlihan Lokey ADG bankers) Ownership: Acquired by Capital One Financial in August 2019; operates as a Capital One Securities subsidiary preserving the KippsDeSanto brand Track record: 200+ closed transactions over 18 years; one of the highest deal-volume ADGS-pure-play boutiques nationally Sectors: Aerospace, Defense, Government Services, Cybersecurity, Federal IT -- exclusively Key Managing Directors:

- Bob Kipps -- Co-Founder, Managing Partner (still active)

- Kevin DeSanto -- Co-Founder, Managing Partner (still active)

- Nicholas Dodson -- Managing Director (defense / space)

- Kate Troendle -- Managing Director (cybersecurity, federal IT)

- Jon Yim -- Managing Director (government services)

Deal size sweet spot: $20M-$500M EV ADGS M&A Verified 2024-2026 transactions:

- SilverEdge Government Solutions sold to SAIC for $205M, closed October 17, 2025 -- KippsDeSanto sell-side advisor; SilverEdge was a cleared cyber and IT services firm

- Sabel Systems Technology Solutions sold to Sagewind Capital, November 2024 -- KippsDeSanto sell-side advisor; Sabel is a federal digital engineering services firm

- Three Wire Systems' Technology Resale Division sold to Mythics, September 2024 -- KippsDeSanto sell-side; federal IT services rollup (Three Wire Systems' MyAdvisor and remaining businesses continue independently)

- Axient sold to Astrion (Brightstar Capital Partners portfolio company), September 2024 -- KippsDeSanto sell-side; defense engineering services consolidation

- Ask Sage sold to BigBear.ai for ~$250M, December 31, 2025 -- KippsDeSanto sell-side advisor; Ask Sage is a federal generative-AI platform; BigBear.ai is a Nasdaq-listed defense AI services firm

Distinguishing factor: KippsDeSanto is the highest deal-volume ADGS-pure-play mid-market boutique nationally and the most-cited DC-anchored cleared-deal-handling tier first call in founder query patterns. Both founders -- Bob Kipps and Kevin DeSanto -- are still active partners; the firm has built out a deep MD bench across defense (Dodson), cybersecurity and federal IT (Troendle), and government services (Yim). The Capital One Financial subsidiary status (since August 2019) gives the firm institutional balance-sheet scale without the bulge-bracket compliance friction. The 2024-2026 deal cadence -- SilverEdge $205M October 2025, Sabel Systems November 2024, Three Wire Tech Resale September 2024, Axient September 2024, Ask Sage December 31, 2025 -- confirms the firm's signature DC ADGS mid-market position. The firm is NOT a Houlihan Lokey subsidiary -- both founders are ex-Houlihan but the firm has been independent since founding in 2007 and a Capital One subsidiary since August 2019; KippsDeSanto and Houlihan Lokey ADG are direct DC competitors, not affiliates.

Best for: Founder-led ADGS, federal IT, and cleared cyber sellers with $5M-$50M EBITDA preparing for a strategic-acquirer or PE-platform exit where the cleared-deal-handling tier and Defense Industrial Base lens earn their tier. Best contact: Bob Kipps or Kevin DeSanto (founder tier) for franchise-maker mandates; Kate Troendle for cybersecurity and federal IT mandates; Nicholas Dodson for defense and space mandates; Jon Yim for government services mandates.

2. Houlihan Lokey ADG

DC office: 1909 K Street NW, Suite 800, Washington DC 20006 Houlihan Lokey HQ: Los Angeles ADG practice scale: 30 dedicated ADG investment bankers across DC, LA, and London -- globally the #1 M&A advisor in the ADG sector by transaction count for 2024-2025 (per Mergermarket league tables) Senior team:

- Daniel Small -- Managing Director (DC-based; ADG)

- Adam Frankel -- Managing Director (defense electronics, mission systems)

- Larry Davis -- Managing Director

- (Note: Anita Antenucci led the global ADG practice from 2002 through January 2023, when she departed to found 3Wire Partners; she was previously a founding member and Co-President of Quarterdeck Investment Partners (acquired by Jefferies Group December 2002, becoming Jefferies Quarterdeck), and joined Houlihan Lokey separately in October 2002 to build the ADG practice over 20 years. The practice continues to operate as Houlihan Lokey's largest sector group with senior coverage in DC, NYC, and London.)

- (Note: Ryan O'Toole and Eric Cartier departed Houlihan Lokey ADG to Lincoln International in July 2025 to launch Lincoln's DC ADG franchise.)

Deal size sweet spot: $100M-$2B EV ADG M&A Verified 2024-2026 transactions:

- Stellar Blu Solutions sold to Gilat Satellite Networks, closed January 6, 2025 -- Houlihan Lokey advised Stellar Blu (in-flight connectivity) on the sale to Gilat

- Multiple cross-border ADG mandates (London office) 2024-2025

Distinguishing factor: Houlihan Lokey ADG is the global #1 ADG advisor by 2024-2025 transaction count per Mergermarket league tables -- 30 ADG bankers across DC, LA, and London. Antenucci built the practice from 2002 through January 2023; her former track record (General Dynamics, Harris Corp, Lockheed Martin, TransDigm divestitures plus Carlyle, Veritas, Greenbriar engagements) remains the gold-standard reference for DC ADG dealmaking history. The firm sits at the bulge-bracket-boutique tier with the deepest cross-border London desk for international defense buyers. Frame Houlihan Lokey ADG as a global-firm bulge-bracket-boutique-tier office rather than as a Washington-DC-headquartered standalone firm -- the parent ownership shapes engagement-letter-term flexibility, and senior leadership in the DC office continues to anchor the global practice.

Best for: $100M-$2B EV ADG mandates where the cross-border London desk earns its tier (UK, Israel, EU, or Japan strategic acquirers in the buyer pool), or where the founder anticipates eventual public-markets continuation post-sale (capital-markets continuity matters), or where the global #1 transaction-count credibility matters in a competitive Tier-1 prime divestiture process. For DC mid-market $20M-$80M EV defense suppliers, Houlihan Lokey ADG is the credible alternative to KippsDeSanto when international buyer pool is in play.

3. The McLean Group

HQ: 8260 Greensboro Drive, Suite 350, McLean, Virginia 22102 Founded: 1996 by Dennis Roberts (Founding Chairman; still senior advisor) Scale: 60+ professionals across 30+ cities nationwide Sectors: Generalist with DGI (Defense, Government, Intel) specialty practice; healthcare; technology; consumer; industrial; valuation services arm DC senior team:

- Dennis Roberts -- Founding Chairman

- Andy Smith -- Managing Director, DGI Group

- Harry Ward -- Managing Director, Cybersecurity / Federal IT

- Mike Frier -- Managing Director, Government Services

- (Six senior MDs in DC metro; firm has additional DC partners)

Deal size sweet spot: $20M-$80M EV federal services and DGI M&A Verified 2024-2026 transactions:

- Rite Solutions sold to Arcfield (2025) -- The McLean Group sell-side advisor; Rite Solutions is a Navy systems engineering firm

- Fuel Consulting sold to B/CORE (2025) -- The McLean Group sell-side; federal services rollup

- Emagined Security sold to Neovera (a 424 Capital portfolio company), 2025 -- The McLean Group sell-side; cybersecurity consolidation

- Protas Solutions sold to Criterion Systems (2025) -- The McLean Group sell-side; federal IT

- Seaford Consulting sold to Crimson Phoenix, February 12, 2024 -- The McLean Group sell-side; cleared federal services

- ARRAY IT sold to CGI Federal (2025) -- The McLean Group sell-side; federal IT consolidation

Distinguishing factor: The McLean Group has the largest DC senior bench plus the most active 2025 DGI deal flow on the federal-services rollup pool side -- Rite Solutions / Arcfield, Emagined / Neovera, Protas / Criterion, ARRAY IT / CGI Federal are all $20M-$80M federal IT services rollup mandates closed under DGI specialty leadership. The firm is The McLean Group (definite article), reflecting the McLean Virginia headquarters since 1996 -- Dennis Roberts founded the firm and remains Founding Chairman. (Do not confuse with The McLean Group of Texas, a different unrelated firm.) The 60+ professionals across 30+ cities give the firm a national footprint while preserving DC-anchored DGI specialty depth.

Best for: $20M-$80M EV federal IT services, government services, defense engineering, and cleared cyber rollup mandates where DC-anchored senior bench depth and active 2025 deal flow matter. Best contact: Andy Smith (DGI Group lead) for federal services rollup mandates; Harry Ward (cybersecurity / federal IT) for cyber sells; Mike Frier (government services) for GovCon mandates.

4. Renaissance Strategic Advisors (RSA)

HQ: Arlington, Virginia (Crystal City defense corridor) Founded: 2007 by Pierre Chao (Founding Partner; defense industry veteran ex-CSIS, ex-Credit Suisse, ex-JSA Research) Scale: 85 professionals plus 250 senior advisors (including retired flag officers and former Senior Executive Service from DoD and Intelligence Community) Sectors: Aerospace, Defense, National Security exclusively -- strategy consulting AND M&A advisory (rare combined model) Track record: 44 closed M&A transactions over 18 years; long-standing strategy advisory engagements with Tier-1 primes (RTX, Lockheed Martin, Northrop Grumman, BAE Systems, L3Harris)

Key partners:

- Pierre Chao -- Founding Partner

- Multiple senior partners with DoD Senior Executive Service backgrounds

- 250 senior advisor network includes retired Joint Staff and Combatant Command officers

Deal size sweet spot: $30M-$300M EV ADG M&A Verified 2024-2026 work (strategy + M&A engagements):

- Long-standing engagement with RTX-Collins Aerospace on Goodrich integration strategy (legacy work continuing post-2020 merger)

- UK Ministry of Defence privatization wave advisory (Atlas Elektronik, ABRO, etc.)

- Multiple confidential US prime divestiture and tuck-in advisory mandates 2024-2025

Distinguishing factor: Renaissance Strategic Advisors is the only DC ADG boutique with a combined strategy plus M&A advisory model -- 250 senior advisors, including retired flag officers and former DoD Senior Executive Service, bring institutional defense buyer-pool insight that pure-IB peers cannot match. Pierre Chao is the published authority -- cite his Defense Industry consolidation thinking from 2024-2025 panels (Aviation Week, AIAA SciTech) as engagement reference. RSA's 18-year ADG-pure-play tenure rivals KippsDeSanto's. (Avoid confusing RSA with Renaissance Capital -- the NYC IPO research firm -- or Renaissance Technologies -- the Long Island hedge fund -- both of which are completely unrelated.)

Best for: $30M-$300M EV defense and national security mandates where strategy plus M&A combined-model depth earns its tier -- particularly Tier-1 prime tuck-ins, divestiture strategy, or sell-side processes where DoD buyer-pool insight from retired flag officers shapes process design. Best contact: Pierre Chao (Founding Partner).

Which Washington DC M&A Advisors Anchor the Federal IT, Government Services, and GovCon Generalist Tier?

For DC-area founder-led federal IT services, GovCon, and lower-middle-market generalist mid-market sellers, two firms anchor the band: FOCUS Investment Banking (Vienna, Virginia; 44-year DC franchise; #2 Axial Top 25 LMM IB Q2 2025) and Aronson Capital Partners / Aprio Capital Advisors (Bethesda; post-January 2023 Aronson + Aprio merger; 25+ year DC GovCon legacy). The first call splits structurally on franchise tenure plus Axial-validated league-table ranking (FOCUS) versus accounting plus tax plus M&A integrated workflow (Aronson/Aprio).

5. FOCUS Investment Banking

HQ: Washington DC metro (Vienna, Virginia office) since 1982 -- 44+ year DC franchise Scale: 35+ senior bankers nationwide; multi-vertical lower-middle-market specialty Sectors: Multiple industry teams -- Government & Defense (GAD), Automotive, HVAC / Plumbing, Healthcare, Technology Services, Consumer GAD team:

- Manan K. Shah -- Team Leader, Government & Defense (Vienna VA)

- Dr. Bruce J. Holmes -- Senior Advisor, Aerospace

- Dr. Paul A. Robinson -- Senior Advisor, Defense

- Thomas Woosley -- Senior Advisor, GovCon

Recognition: #2 Axial Top 25 Lower Middle Market Investment Bank Q2 2025 (Axial deal-flow league table) Deal size sweet spot: $5M-$50M revenue range LMM federal services and government & defense M&A Recent activity: GAD team executed multiple sell-side mandates 2024-2025; FOCUS publishes per-vertical market reports including Government & Defense quarterly updates.

Distinguishing factor: FOCUS Investment Banking is the longest-tenured DC franchise on this list -- founded 1982, 44+ year DC operation. The #2 Axial Top 25 Lower Middle Market Investment Bank Q2 2025 ranking is the strongest external-validation league-table signal of any DC boutique on this list. Manan K. Shah leads the Government & Defense (GAD) team from Vienna Virginia with senior advisor coverage across aerospace (Holmes), defense (Robinson), and GovCon (Woosley). The lower-middle-market $5M-$50M revenue sweet spot is structurally smaller than KippsDeSanto's and The McLean Group's bands, making FOCUS the natural DC LMM choice for sub-$30M revenue founder-led federal services targets.

Best for: Lower-middle-market federal services, government and defense, and multi-vertical sellers with $5M-$50M revenue preparing for a strategic-acquirer or PE-platform exit. Best contact: Manan K. Shah (GAD Team Leader).

6. Aronson Capital Partners (Aprio Capital Advisors)

HQ: Bethesda, Maryland (originally Rockville, Maryland) Founded: 1999 as Aronson Capital Partners (within Aronson LLC accounting firm); merged with Aprio LLP (Atlanta-HQ accounting firm) January 1, 2023 -- now operates as Aprio Capital Advisors / Aronson Capital Partners under the Aprio umbrella Sectors: Government Contracts, Federal IT, Tech Services, Health Tech, Engineering Services Current Managing Partner: John Saunders (Aronson Capital Partners legacy lead)

Deal size sweet spot: $20M-$100M EV federal IT, GovCon, and tech services M&A Recent activity: Aronson / Aprio executed multiple sell-side mandates in Federal IT and GovCon services 2023-2025; post-merger reporting is thinner publicly but the firm continues active DC-metro mid-market sell-side practice.

Distinguishing factor: Aronson Capital Partners brings 25+ years of DC GovCon M&A legacy under the Aronson brand (founded 1999); the January 1, 2023 merger with Aprio LLP creates an accounting plus tax plus M&A integrated workflow analogous to the CLA Meridian Capital integration in our Seattle M&A advisor guide. Post-merger, Aprio is a Top 25 US accounting firm with specialist tax practitioners across R&D credits, transaction tax, state and local tax, and ASC 740 deferred tax accounting. John Saunders continues as Managing Partner. The trade-off is M&A bench depth versus integrated-workflow advantage -- versus KippsDeSanto, The McLean Group, Renaissance Strategic Advisors, and FOCUS, Aprio Capital Advisors is the only one with full accounting plus tax integration. Brand transition is still ongoing -- public-facing transactions are sometimes branded 'Aronson' and sometimes 'Aprio Capital Advisors,' so verify deal-team in the engagement letter.

Best for: $20M-$100M EV federal IT, GovCon, and tech services sellers where the integrated accounting plus tax plus M&A advisory workflow earns its tier (R&D credits, transaction tax, state and local tax structuring, ASC 740 deferred tax accounting). Best contact: John Saunders (Managing Partner).

Which Washington DC M&A Advisors Anchor the Bank-Owned-Boutique Tier and Cross-Border ADG Bench ($30M-$2B EV)?

For DC-area founders and PE platforms whose deal turns on parent-firm balance-sheet capability, public-equity research adjacency, or international ADG cross-border buyer-pool reach, four firms anchor the bank-owned-boutique-tier and cross-border ADG band: Capstone Partners (Boston HQ; Huntington Bancshares-owned; ADGS practice with TM Capital absorbed December 2025), Baird Defense & Government (Milwaukee HQ; Robert W. Baird & Co.; $6.4B / 16 deals 2025 closed), Lincoln International DC ADG (Chicago HQ; July 2025 expansion-stage launch with Chertoff Group partnership), and DC Advisory (Daiwa Securities international subsidiary). The first call splits structurally on geography preference, parent-firm capability, and cross-border buyer-pool reach.

7. Capstone Partners DC -- ADGS practice

HQ: Boston (Federal Street); Huntington Bancshares-owned since June 2022 DC presence: ADGS (Aerospace, Defense, Government Services) practice has DC senior partners; full-service middle market with 12 industry groups ADGS senior team:

- Tess Oxenstierna -- Head, ADGS Group (25+ years C4ISR / ALSS / electronic warfare M&A)

- Ian Cookson -- A&D Group Head ($5B+ closed transactions)

- David Brinkley -- MD, ADGS

- Tom McConnell -- MD, ADGS

- Ted Polk -- MD, ADGS

- Khelan Dattani -- DC MD (insurance specialty; 50+ deals / $10B EV closed lifetime)

Recent firm activity: Capstone acquired TM Capital in December 2025 (TM Boston team integrated), expanding Capstone's NY / Boston / Atlanta footprint and scale. Deal size sweet spot: $30M-$300M EV ADGS M&A Recent deals: ADGS practice closed multiple mid-market defense and government services transactions 2024-2025; specific deal disclosure thinner publicly but transaction page lists 700+ lifetime closes across firm.

Distinguishing factor: Capstone Partners brings 12-industry-group full-service middle market with ADGS practice led by Tess Oxenstierna's 25-year C4ISR / ALSS / electronic warfare M&A depth -- a sub-vertical specialty that pure ADG boutiques (KippsDeSanto, Renaissance) cover less specifically. Ian Cookson's $5B+ closed A&D transactions anchor the senior A&D bench. Khelan Dattani's DC MD position with 50+ deals / $10B EV closed lifetime adds insurance-specialty M&A coverage. The Boston HQ caveat is acknowledged but the DC bench is substantive; the Huntington Bancshares ownership (since June 2022) provides balance-sheet tier capability. The TM Capital absorption in December 2025 expanded NY, Boston, and Atlanta scale -- parallel to the bank-owned-boutique-tier dynamics in our Boston M&A advisor guide.

Best for: $30M-$300M EV ADGS, defense electronics, C4ISR, ALSS, and electronic warfare mandates where Boston-HQ middle-market full-service breadth combined with DC ADGS senior partner depth earns its tier. Best contact: Tess Oxenstierna (ADGS Head) or Khelan Dattani (DC MD).

8. Baird Defense & Government

HQ: Milwaukee, Wisconsin (Robert W. Baird & Co. parent) DC presence: Baird Defense & Government practice is housed within Baird's broader Global Investment Banking franchise; DC bench of senior bankers covering federal services, defense, and government tech Track record: $6.4 billion in 2025 closed Defense & Government deals across 16 transactions -- among the highest-volume bank-owned ADG advisors Sectors: Defense, Government Services, Aerospace, Federal IT / Cyber, Healthcare Government Services Deal size sweet spot: $50M-$1B EV defense and government services M&A Recent activity: 16 closed in 2025; specific named transactions vary across the firm's transaction disclosures. Public press identifies multiple cleared GovCon services advisory mandates.

Distinguishing factor: Baird Defense & Government closed $6.4B / 16 deals in 2025 in defense plus government -- among the highest-volume bank-owned ADG advisors. Robert W. Baird Fortune 500 parent provides depth; the DC bench is credible if the Milwaukee HQ caveat is properly framed. Baird's official corporate parent is Robert W. Baird & Co. Incorporated; Baird Defense & Government is the practice-group brand, not a standalone subsidiary. Frame Baird as the bank-owned-boutique-tier high-volume option (parallel to Cain Brothers DC and Houlihan Lokey ADG) rather than as a Washington-DC-anchored boutique.

Best for: $50M-$1B EV defense, government services, aerospace, federal IT, and federal cyber mandates where the bank-owned-boutique-tier deal-volume credibility ($6.4B / 16 deals 2025) and Robert W. Baird Fortune 500 parent capability matter. Best contact: senior bankers within Baird Global Investment Banking Defense & Government practice (verify per-person via rwbaird.com).

9. Lincoln International DC ADG

HQ: Chicago (Lincoln International parent) DC presence: ADG team launched July 2025 with hires of Ryan O'Toole and Eric Cartier as co-heads of A&D -- both from Houlihan Lokey ADG (departed Houlihan July 2025). Firm also has Chertoff Group strategic partnership for DC ecosystem integration (Chertoff = ex-DHS Secretary Michael Chertoff's DC advisory firm). Scale globally: Top-3 mid-market global IB; DC is expansion priority Deal size sweet spot: $50M-$500M EV ADG M&A (expansion-stage DC pipeline) Recent activity: DC ADG franchise still building deal pipeline. O'Toole and Cartier brought legacy Houlihan ADG relationships (e.g., Stellar Blu / Gilat history) but new mandates under Lincoln branding 2H 2025-2026.

Distinguishing factor: Lincoln International's July 2025 DC ADG launch with Ryan O'Toole and Eric Cartier from Houlihan Lokey ADG plus the Chertoff Group strategic partnership represents the most credible new DC ADG entrant of 2025-2026. Top-3 mid-market global IB ranking globally. Frame Lincoln International DC as expansion-stage rather than long-tenured DC presence -- the office is less than a year old and still building deal pipeline under the Lincoln brand. Lincoln International HQ is Chicago, NOT DC.

Best for: $50M-$500M EV ADG mandates where the most credible 2025 DC ADG expansion-stage franchise plus Chertoff Group ecosystem integration earn their tier -- particularly when O'Toole or Cartier's legacy Houlihan ADG relationships matter on a specific buyer pool. Best contact: Ryan O'Toole or Eric Cartier (co-heads, A&D).

10. DC Advisory

HQ: London / Tokyo (subsidiary of Daiwa Securities Group, Japan) DC office: Yes -- small DC-anchored team Sectors: Industrial, ADG, financial sponsors, technology -- globally; DC focus is ADG cross-border Recognition: Top-3 mid-market industrials advisor 2025 (Mergermarket EMEA league tables) Deal size sweet spot: $30M-$300M EV cross-border ADG M&A Recent activity: Cross-border ADG mandates leveraging the Daiwa-network (Japan, EMEA, US triangulation); specific deal disclosure spans the firm's London transactions page.

Distinguishing factor: DC Advisory is the firm name (literally) -- it does NOT mean 'Washington DC Advisory.' DC Advisory was formed from the rollup of Close Brothers Corporate Finance plus several boutiques plus Daiwa's ECM franchise. The 'DC' originally referenced Daiwa Capital. Confusing in a Washington DC post -- clarify on first mention. The Daiwa Securities Group subsidiary status provides Japanese plus EMEA buyer-pool reach for cross-border ADG. Top-3 mid-market industrials advisor 2025 per Mergermarket EMEA league tables.

Best for: $30M-$300M EV cross-border ADG mandates where the Daiwa international network plus EMEA buyer-pool reach earn their tier -- particularly Japan, UK, Germany, France, or Israel strategic-acquirer pools where pure-DC boutiques have limited international relationship density. Best contact: senior bankers within DC Advisory ADG practice (verify per-person via dcadvisory.com).

Which Washington DC M&A Advisors Anchor the NIH-Proximity Biotech and Cleared-Deal Legal Counsel Bench?

For DC-area healthcare, NIH-proximity biotech, and cleared-deal legal counsel needs, two firms anchor the specialty bands: Cain Brothers DC healthcare practice (KeyBanc Capital Markets / KeyCorp division; pure healthcare services + biotech) and Hogan Lovells M&A (DC HQ global law firm; legal counsel ecosystem complement, NOT investment bank). Each is the structural default for its specialty axis; the two specialties rarely overlap on a single mandate.

11. Cain Brothers DC healthcare practice (NIH-proximity)

HQ: New York City (Cain Brothers main); a division of KeyBanc Capital Markets / KeyCorp (Fortune 500 parent based Cleveland) DC presence: Senior healthcare bankers covering Mid-Atlantic NIH-proximity biotech, healthcare services, and HCIT Sectors: Pure healthcare -- HCIT, home health, specialty pharmacy, distribution, durable medical equipment, behavioral health, payer-tech, life sciences services Senior bench (firm-wide; primarily NYC-anchored with Mid-Atlantic coverage):

- Thad Davis -- MD, healthcare / healthtech M&A (joined January 2025)

- David Cohen -- MD

- Matt Margulies -- MD, home health / hospice / specialty pharmacy / DME

- (Cain Brothers' DC-anchored coverage is staffed via firm-wide bench rather than DC-resident named partners; verify deal-team-resident-office in the engagement letter.)

Deal size sweet spot: $50M-$1B EV healthcare services and biotech M&A Recent activity: Active healthcare services rollups across coastal markets including Mid-Atlantic; specific DC-anchored deal disclosure thin.

Distinguishing factor: Cain Brothers DC anchors the NIH-proximity biotech buyer pool plus Mid-Atlantic healthcare services M&A bench in DC -- a division of KeyBanc Capital Markets / KeyCorp (acquired 2018). The KBCM compliance gate is parallel to Cain Brothers in our Boston M&A advisor guide and KBCM (the legacy Pacific Crest franchise) in our Seattle M&A advisor guide. Frame Cain Brothers as 'Cain Brothers, a division of KeyBanc Capital Markets' rather than as a standalone boutique. The DC healthcare practice covers Mid-Atlantic but Cain Brothers' main office is NYC.

Best for: $50M-$1B EV healthcare services rollups (HCIT, home health, specialty pharmacy, behavioral health) plus NIH-proximity biotech deals (Bethesda, Rockville, Mid-Atlantic) where the KBCM parent's full debt and equity capital markets capability matters. For Bethesda biotech founders specifically, Cain Brothers DC is the primary DC-anchored option, typically triangulated against Boston and SF specialists for cross-coast process competition.

12. Hogan Lovells M&A (legal counsel ecosystem complement)

HQ: Washington DC (Columbia Square, 555 13th Street NW) -- DC is Hogan Lovells' largest US office Founded: Modern firm formed 2010 via merger of Hogan & Hartson (DC, founded 1904) and Lovells (London, founded 1899) Type: GLOBAL LAW FIRM, NOT INVESTMENT BANK -- frame as legal-counsel adjacency to the M&A advisor list, NOT as primary investment bank M&A scale: $400B+ in deal volume advised lifetime; ~700 M&A transactions annually globally Co-Heads US M&A:

- Elizabeth Donley -- Partner, Co-Head US M&A (DC)

- (Co-head names rotate -- verify on hoganlovells.com)

Deal size sweet spot: $50M-$1B+ EV M&A legal counsel for cleared, regulated, and complex transactions Verified 2024-2026 transactions:

- Lockheed Martin / Terran Orbital $450M acquisition (closed late 2024 / 2025) -- Hogan Lovells DC counsel

- Multiple high-profile transactions across defense, technology, healthcare, and financial services

Distinguishing factor: Hogan Lovells is a global law firm, not an investment bank -- the firm was formed in 2010 via the merger of Hogan & Hartson (DC, founded 1904) and Lovells (London, founded 1899). DC is Hogan Lovells' largest US office. M&A advisory ecosystem complement, NOT investment bank: $400B+ in deal volume advised lifetime, ~700 M&A transactions annually globally. For DC ADG founders running cleared deals, Hogan Lovells handles FOCI mitigation (Special Security Agreement, Security Control Agreement, Voting Trust framework structuring), DCSA notification timing, and CFIUS workflows -- the legal-counsel layer is incomplete without a firm of this depth on cleared-deal-handling tier mandates. The Lockheed Martin / Terran Orbital $450M acquisition (closed late 2024 / 2025) is a recent named anchor.

Best for: Cleared-deal legal counsel layer for any DC ADG founder running a cleared, classified-adjacent, ITAR-controlled, or CFIUS-reviewable transaction -- frame Hogan Lovells as legal counsel ecosystem complement to KippsDeSanto, Houlihan Lokey ADG, Renaissance Strategic Advisors, or The McLean Group on the investment-bank side. Hogan Lovells is NOT the primary M&A advisor; it is the transactional legal counsel that handles the FOCI / DCSA / CFIUS workflow alongside the senior banker. Best contact: Elizabeth Donley (Partner, Co-Head US M&A).

What Recent Washington DC-Area M&A Deals Show How These Advisors Actually Work?

Five recent verified DC-area closes that illustrate the deal-size band, the buyer-pool composition, and the structural advantage each advisor brings.

SilverEdge Government Solutions to SAIC ($205M, October 17, 2025; KippsDeSanto)

KippsDeSanto served as exclusive financial advisor to SilverEdge Government Solutions on the October 17, 2025 sale to SAIC for $205M. SilverEdge is a cleared cyber and IT services firm; SAIC (NYSE: SAIC) is a Reston Virginia federal services Tier-1 strategic acquirer. The deal demonstrates KippsDeSanto's structural reach into the cleared-deal-handling tier and the federal-services rollup pool (SAIC has been one of the most active Tier-1 strategic acquirers in the 2024-2025 cleared cyber consolidation cycle). For DC ADG founders specifically, the SilverEdge / SAIC deal is the single most-cited mid-market 2025 KippsDeSanto-advised close in founder query patterns -- it confirms KippsDeSanto's signature DC ADGS mid-market position alongside the firm's 200+ closed transactions over 18 years.

Ask Sage to BigBear.ai (~$250M, December 31, 2025; KippsDeSanto)

KippsDeSanto served as exclusive financial advisor to Ask Sage on the December 31, 2025 sale to BigBear.ai (~$250M). Ask Sage is a federal generative-AI platform; BigBear.ai (NASDAQ: BBAI) is a Columbia Maryland defense AI services firm. The deal demonstrates KippsDeSanto's reach into the AI-meets-defense buyer pool -- BigBear.ai's prior portfolio history under AE Industrial Partners (until the 2024 IPO) and the company's continued M&A appetite in cleared AI services give the senior bench direct visibility into how AI-strategic-acquirer behavior maps onto cleared federal services targets. For DC ADG founders evaluating AI-ish cleared services exits, the Ask Sage / BigBear.ai deal is the most-cited late-2025 anchor for KippsDeSanto-advised AI plus federal sell-side process structuring.

Stellar Blu Solutions to Gilat Satellite Networks (January 6, 2025; Houlihan Lokey ADG)

Houlihan Lokey ADG served as advisor to Stellar Blu Solutions on the January 6, 2025 sale to Gilat Satellite Networks. Stellar Blu is an in-flight connectivity firm; Gilat is an Israeli satellite networks firm. The deal demonstrates Houlihan Lokey ADG's structural reach into the cross-border ADG buyer pool -- the firm's London desk and global ADG bench (30 bankers across DC, LA, and London) translate into actual close on US-to-Israel strategic-acquirer transactions. For DC ADG founders specifically, the Stellar Blu / Gilat deal is a direct data point on how Houlihan Lokey ADG's bulge-bracket-boutique scale plus international reach earn their tier on cross-border $100M-$500M EV ADG mandates.

Rite Solutions to Arcfield (2025; The McLean Group)

The McLean Group served as advisor to Rite Solutions on the 2025 sale to Arcfield. Rite Solutions is a Navy systems engineering firm; Arcfield is a DC-area federal services strategic acquirer. The deal demonstrates The McLean Group's structural reach into the federal-services rollup pool and DGI specialty practice -- the firm's six DC senior MDs plus 60+ professionals across 30+ cities translate into multiple $20M-$80M federal IT services rollup mandates closed in 2025 (Rite Solutions / Arcfield, Fuel Consulting / B/CORE, Emagined Security / Neovera, Protas Solutions / Criterion Systems, ARRAY IT / CGI Federal). For DC GovCon founders specifically, the Rite Solutions / Arcfield deal anchors The McLean Group's signature 2025 DGI deal cadence.

Lockheed Martin / Terran Orbital ($450M, late 2024 / 2025; Hogan Lovells M&A counsel)

Hogan Lovells served as M&A counsel on the Lockheed Martin / Terran Orbital $450M acquisition (closed late 2024 / 2025). Lockheed Martin (NYSE: LMT) is a Tier-1 defense prime; Terran Orbital was a NYSE-listed satellite manufacturer (then taken private via the Lockheed acquisition). The deal demonstrates Hogan Lovells' structural reach into the cleared-deal legal counsel layer -- $400B+ in M&A advised lifetime, ~700 transactions annually globally, with Elizabeth Donley as Co-Head US M&A in the DC HQ office (the firm's largest US office). For DC ADG founders running cleared, classified-adjacent, or CFIUS-reviewable deals, the Lockheed Martin / Terran Orbital transaction anchors Hogan Lovells' role as transactional legal counsel ecosystem complement to investment-bank advisors like KippsDeSanto, Houlihan Lokey ADG, or Renaissance Strategic Advisors.

How Do I Pick the Right Washington DC M&A Advisor for My Situation?

The decision framework comes down to deal size + sub-vertical + ownership structure + buyer-pool composition + cleared-deal-handling overlay.

The cleared-deal-handling tier is the DC-distinguishing axis -- KippsDeSanto, Renaissance Strategic Advisors, Houlihan Lokey ADG, and The McLean Group on the investment-bank side; Hogan Lovells on the legal-counsel side. The federal-services rollup pool intersects KippsDeSanto, The McLean Group, FOCUS Investment Banking, and Aronson Capital Partners / Aprio. The defense-aerospace strategic-acquirer pool runs from KippsDeSanto and Renaissance through Houlihan Lokey ADG's bulge-bracket-boutique tier into Capstone Partners' ADGS practice, Baird Defense & Government's bank-owned-boutique-tier high-volume franchise, and Lincoln International DC's expansion-stage 2025 launch. The NIH-proximity biotech buyer pool runs through Cain Brothers DC primarily, with Boston cross-coast triangulation. The four-axis (or five-axis) DC decision matrix surfaces on every choice.

For $20M-$500M EV ADGS, federal IT, or cleared cyber sell-sides where Defense Industrial Base lens depth matters -- KippsDeSanto & Co is the DC-default first call with 200+ closed transactions over 18 years, Capital One subsidiary status since August 2019, and 2024-2026 deal cadence (SilverEdge $205M, Sabel Systems, Three Wire Tech Resale, Axient, Ask Sage ~$250M).

For $100M-$2B EV ADG mandates with cross-border London desk reach or capital-markets continuity preference -- Houlihan Lokey ADG is the global #1 ADG advisor by transaction count, with 30 bankers across DC / LA / London and senior leadership in the DC office.

For $20M-$80M EV federal IT services or DGI rollup mandates with largest DC senior bench -- The McLean Group brings 60+ professionals across 30+ cities, six senior MDs in DC metro, and verified 2025 deal cadence (Rite Solutions / Arcfield, Emagined / Neovera, Protas / Criterion, ARRAY IT / CGI Federal).

For $30M-$300M EV defense and national security mandates with strategy plus M&A combined-model depth -- Renaissance Strategic Advisors (RSA) brings Pierre Chao's 18-year Founding Partner tenure, 85 professionals plus 250 senior advisors (retired flag officers, former DoD SES), and a unique strategy plus M&A advisory model not available at pure-IB peers.

For $5M-$50M revenue lower-middle-market federal services and government & defense sells with longest DC franchise tenure plus Axial-validated league-table ranking -- FOCUS Investment Banking is the 44-year DC franchise (since 1982) with #2 Axial Top 25 LMM IB Q2 2025 ranking and Manan K. Shah leading the GAD team from Vienna Virginia.

For $30M-$300M EV ADGS, defense electronics, C4ISR, ALSS, or electronic warfare mandates with full-service middle market breadth -- Capstone Partners DC (Boston HQ caveat) brings Tess Oxenstierna's 25-year ADGS leadership, Ian Cookson's $5B+ A&D track record, and Huntington Bancshares ownership tier.

For $50M-$1B EV defense, government services, aerospace, federal IT, or federal cyber mandates with bank-owned high-volume tier -- Baird Defense & Government (Milwaukee HQ caveat) closed $6.4B / 16 deals in 2025 across the Defense & Government practice -- among the highest-volume bank-owned ADG advisors.

For $50M-$500M EV ADG mandates with the most credible 2025 expansion-stage DC franchise -- Lincoln International DC ADG brings Ryan O'Toole and Eric Cartier (co-heads, A&D, ex-Houlihan Lokey ADG, July 2025) plus Chertoff Group strategic partnership.

For $30M-$300M EV cross-border ADG mandates with Daiwa international network reach (Japan + EMEA + US triangulation) -- DC Advisory is the international Daiwa Securities subsidiary, top-3 mid-market industrials advisor 2025 per Mergermarket EMEA.

For $20M-$100M EV federal IT, GovCon, or tech services sells where accounting plus tax plus M&A integrated workflow matters (R&D credits, transaction tax, ASC 740) -- Aronson Capital Partners / Aprio Capital Advisors brings 25+ years of DC GovCon legacy under the Aronson brand combined with Aprio LLP's Top 25 US accounting firm post-merger scale.

For $50M-$1B EV NIH-proximity biotech, healthcare services, or HCIT mandates with KBCM parent capability -- Cain Brothers DC is the KeyBanc Capital Markets / KeyCorp division covering Mid-Atlantic healthcare. (KBCM compliance gate; parallel to Boston Cain Brothers and Seattle KBCM dynamics.)

For cleared, classified-adjacent, ITAR-controlled, or CFIUS-reviewable transaction legal counsel -- Hogan Lovells M&A is the global law firm (DC HQ) with $400B+ in M&A advised lifetime; frame as legal counsel ecosystem complement to investment-bank advisors, NOT as primary advisor.

For framework comparisons with related M&A frameworks, see our M&A data room guide, which covers what DC advisors expect to see by Week 1 of the engagement.

The five-axis DC decision matrix at a glance

DC founders comparing advisors should weight five axes -- the same set the senior bankers themselves use when scoping engagement letters:

| Axis | Best for this axis | Caveat |

|---|---|---|

| Pure ADGS specialty depth | KippsDeSanto / Renaissance Strategic Advisors / Houlihan Lokey ADG | Top-of-fee-range; specialty firms charge 25-50bps premium |

| Bank-owned-boutique scale (capital markets adjacency) | Houlihan Lokey ADG / Baird Defense & Government / Lincoln International DC / Cain Brothers DC | Compliance gate slows external founder dialogue; mid-market $50M+ sweet spot |

| Generalist with DGI / GAD team (multi-vertical founder) | The McLean Group / FOCUS Investment Banking / Capstone Partners DC | DGI / GAD is a sub-team within larger firm; verify named-partner staffing in engagement letter |

| Cleared-deal-handling tier (FOCI / DCSA / ITAR / CFIUS) | KippsDeSanto / Renaissance Strategic Advisors / Houlihan Lokey ADG / Hogan Lovells (legal counsel) | Cleared deals add 0.25-0.5% fee premium and 30-60 days timeline |

| Cross-border ADG (international buyer pool) | DC Advisory (Daiwa) / Houlihan Lokey London desk | Adds 0.25% fee; specialized FCPA / export-control workflow needed |

Sector × Deal-Size sweet-spot map

| Sector lane | $5M-$25M EV | $25M-$100M EV | $100M-$300M EV | $300M-$1B EV |

|---|---|---|---|---|

| Defense / Aerospace | FOCUS, McLean, Aronson/Aprio | KippsDeSanto, McLean, Renaissance, FOCUS, Capstone | KippsDeSanto, Renaissance, Houlihan, Capstone, Lincoln | Houlihan, Renaissance, Lincoln, DC Advisory |

| Federal IT / GovCon | FOCUS, McLean, Aronson/Aprio | KippsDeSanto, McLean, Aronson/Aprio, FOCUS | KippsDeSanto, McLean, Houlihan, Capstone | Houlihan, Lincoln, Cain Brothers (healthcare-IT) |

| Cybersecurity (cleared/federal) | FOCUS, McLean | KippsDeSanto, McLean, Capstone | KippsDeSanto, Houlihan, Lincoln, Capstone | Houlihan, Lincoln, DC Advisory |

| Cybersecurity (commercial) | FOCUS | McLean, Capstone | Capstone, Houlihan | Houlihan, NYC FT Partners, SF Drake Star (cross-coast) |

| NIH-proximity biotech | (Boston/SF specialists better) | Cain Brothers DC | Cain Brothers DC, Boston specialists | Cain Brothers, Boston specialists |

| Healthcare services (Mid-Atlantic) | FOCUS, McLean, Aronson/Aprio | Cain Brothers DC, McLean, FOCUS | Cain Brothers, Capstone | Cain Brothers, Houlihan, Provident (Boston) |

| Generalist (mixed-vertical founder) | FOCUS, Aronson/Aprio | McLean, FOCUS, Aronson/Aprio, Capstone | McLean, Capstone, Houlihan | Houlihan, Lincoln, Capstone |

| Cleared / classified-adjacent | FOCUS (limited) | KippsDeSanto, McLean, Renaissance | KippsDeSanto, Renaissance, Houlihan | Houlihan, Renaissance, Lincoln |

| Cross-border ADG | (limited boutique presence) | DC Advisory, Houlihan | DC Advisory, Houlihan, Lincoln | DC Advisory, Houlihan, Lincoln |

A founder of a $50M EV defense electronics firm with 60% cleared revenue mapping to the 'Defense / Aerospace, $25M-$100M EV' cell sees five competing firms (KippsDeSanto, The McLean Group, Renaissance Strategic Advisors, FOCUS, Capstone Partners DC). The decision then routes through the five-axis matrix above -- specialty depth (KippsDeSanto, Renaissance) versus generalist DGI bench (The McLean Group, FOCUS, Capstone), plus cleared-deal-handling tier overlay (KippsDeSanto, Renaissance, Houlihan ADG via cross-pitch). The most common founder triangulations DC senior bankers see in pitch processes: 'KippsDeSanto reviews' typically triangulates against Houlihan Lokey ADG and Renaissance Strategic Advisors; 'best M&A advisor for GovCon services' triangulates against KippsDeSanto, The McLean Group, and FOCUS; 'DC cyber M&A advisor' triangulates against KippsDeSanto, The McLean Group, and Capstone Partners DC (with NYC FT Partners as cross-coast alternative); 'Federal IT services rollup advisor' triangulates against The McLean Group, FOCUS, and Aronson Capital Partners / Aprio; 'Bethesda biotech M&A advisor' triangulates against Cain Brothers DC and Boston specialists (Aquilo, BBLSA, Outcome Capital -- see our Boston M&A advisor guide); 'cleared classified deal advisor' triangulates against KippsDeSanto, Renaissance Strategic Advisors, and Hogan Lovells (legal counsel); 'cross-border defense advisor' triangulates against Houlihan Lokey ADG, DC Advisory, and Lincoln International DC.

What Data Room Capabilities Do Washington DC Advisors Demand?

Washington DC defense, aerospace, government services, federal IT, cleared cyber, and NIH-proximity biotech sellers face structurally distinct confidentiality and workflow environments depending on which axis they sit on. The DC advisors who run consistently confidential cleared and unclassified processes all rely on specific data room capabilities. Six capabilities matter most:

- Click-through NDA gates -- buyer-side users sign the NDA inside the data room before viewing any content, eliminating the email-attachment-NDA chain-of-custody problem that lets CIMs leak before signature; particularly critical for cleared-deal processes where the bidder-facility-clearance-verification timing matters and where the unclassified-tier NDA precedes any FOCI-mitigation correspondence

- Per-investor watermarks -- buyer email plus exact view timestamp embedded into every page so a leaked CIM has a forensic audit trail back to the specific buyer; the structural answer to DC's overlapping-strategic-acquirer and PE-platform-consolidator buyer-pool confidentiality risk, and a documented requirement on cleared-deal-handling tier mandates where the FOCI mitigation file requires per-bidder access logs

- Page-level analytics -- senior banker can see at a glance which buyer is reading the financials versus which is reading the cleared-personnel summary versus which is skipping the contract-performance section, which informs the LOI follow-up sequence; particularly useful for cleared-deal processes where buyer-side engagement signal timing differs across cleared bidders and parallel commercial bidders

- Visitor groups for buyer tiering -- cleared bidders see the unclassified-tier financial and commercial summary set; non-cleared parallel bidders see only the commercial and operational summary; competitor-tier buyers should be blocked from cleared-personnel detail and contract-performance-history backlog until LOI signed; particularly useful for cleared-deal-handling tier processes where two-tier classified data room structuring is the norm

- Screenshot protection -- blocks and logs unauthorized capture attempts, deterring competitors from harvesting customer concentration tables, contract-vehicle-detail pages, cleared-personnel summaries, and program-of-record pricing during data room visits

- Auto-indexing -- compresses Weeks 1-3 of the engagement timeline because buyers can search across the entire data room (commercial financials alongside cleared-personnel summary alongside contract-performance backlog) instead of chasing folder paths; especially useful for two-tier cleared data rooms where the unclassified-tier and gated-tier indices need to be searchable separately and together

For DC cleared-deal-handling tier mandates specifically, the smart Q&A feature centralizes buyer questions so the senior banker (or cleared-deal coordinator) can answer once and surface the answer to every approved buyer rather than repeating the same answer across 15 separate email threads in three different security-clearance contexts. For solutions specifically targeted at M&A and private equity buyer-side workflows, Peony's M&A solution and PE solution pages cover the structural data room patterns most DC advisors use. Custom domain means the data room URL reads as the seller's domain rather than a vendor URL -- a small detail that matters when defense-aerospace strategic-acquirer corp-dev teams forward links internally through their own CFIUS pre-clearance review chains.

How Do Washington DC M&A Advisor Fees Work?

DC-area specialty boutiques typically run a Lehman-style success fee scale plus retainer:

| Deal Size (EV) | Typical Retainer | Lehman Success Fee Math (Standard 5/4/3/2/1 Scale) | Modified Fee Alternative | Typical Tail |

|---|---|---|---|---|

| $5M-$15M | $25K-$50K | 5/4/3/2/1 = approx 5-8% blended | Flat 4-5% on small deals | 12-24 months |

| $15M-$30M | $50K-$75K | 5/4/3/2/1 = approx 2.5-4% blended | 1.75-2.5% flat alternative on $20-30M | 12-24 months |

| $30M-$50M | $75K-$100K | 5/4/3/2/1 = approx 2.0-2.5% blended | 2.0% flat alternative; tiered with flat tail above $20M | 12-24 months |

| $50M-$100M | $100K-$150K | 5/4/3/2/1 = approx 1.7-2.2% blended | Tiered structure with flat tail above $50M | 12-24 months |

| $100M-$200M | $150K-$250K | 5/4/3/2/1 = approx 1.2-1.7% blended | Modified Lehman with higher first-tier and flat tail | 12-24 months |

ADGS specialty firms (KippsDeSanto, Renaissance Strategic Advisors, Houlihan Lokey ADG) often charge 25-50 basis points premium over generalist boutiques given specialty depth and buyer-pool relationship value -- KippsDeSanto and Renaissance Strategic Advisors typically command top-of-range; FOCUS Investment Banking, The McLean Group, and Aronson Capital Partners / Aprio typically mid-range. Bank-owned-boutique-tier firms (Houlihan Lokey ADG, Baird Defense & Government, Lincoln International DC, Cain Brothers DC) typically run standard Lehman with a higher retainer floor ($150K-$250K) given the parent-firm cost structure. Cleared and classified deals add 0.25-0.5% premium for FOCI mitigation legal complexity and 30-60 day DCSA notification timeline; cross-border (UK, Israel, EU, or Japan acquirer) adds another 0.25%. Pure generalist DC boutiques (FOCUS, Aronson/Aprio) typically run standard Lehman without the specialty premium. Bulge-bracket DC offices (Goldman Sachs, Morgan Stanley, JPMorgan) at $50M EV typically demand $250K+ retainer plus a $750K minimum success fee floor regardless of deal value -- structurally inefficient at the LMM band. Avoid: anyone quoting under 1.5% success fee on a $50M defense deal -- deeply discounted fees usually correlate with weaker buyer-pool access and are a false economy.

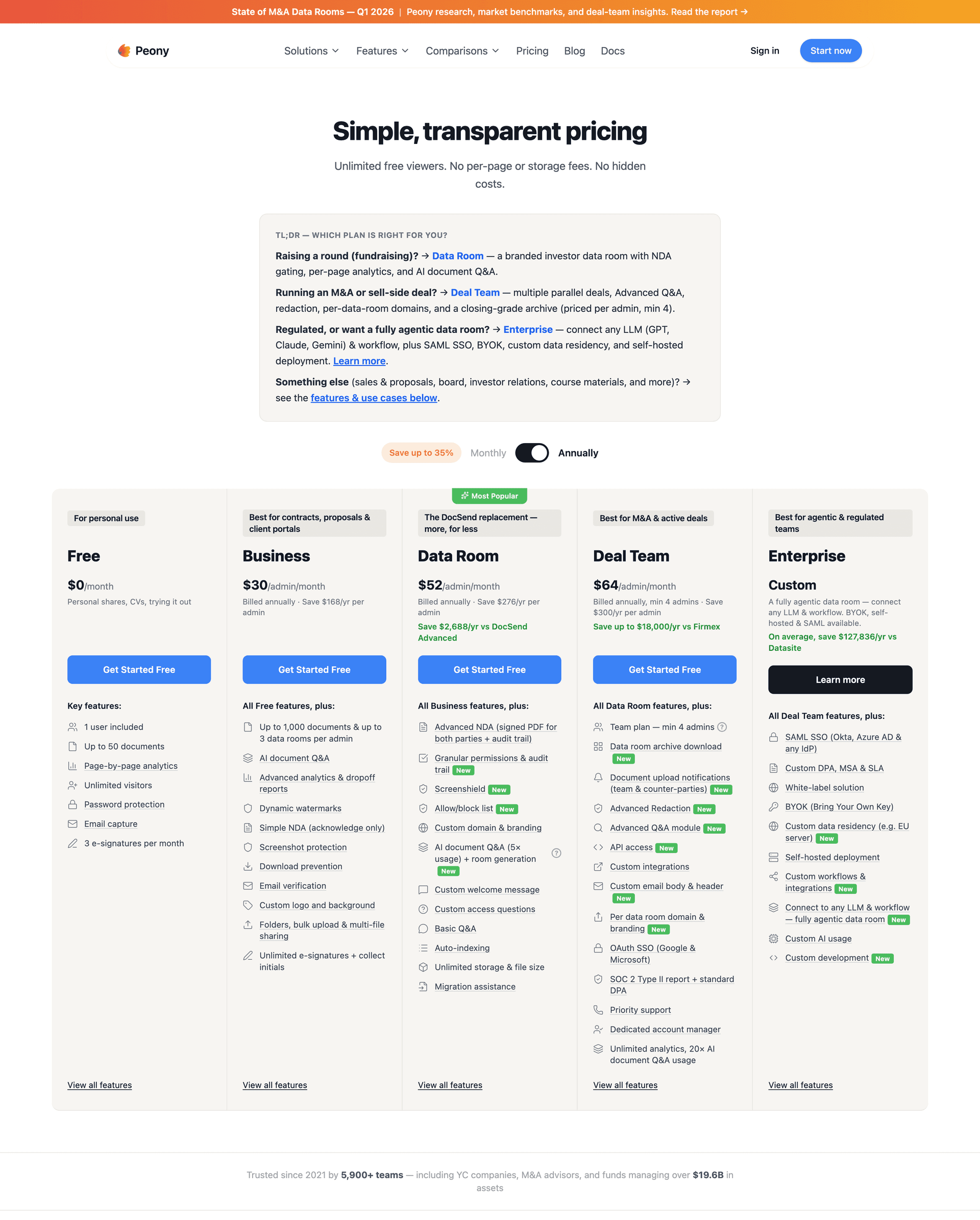

For full pricing detail on data room costs, Peony Business at $30 per admin per month replaces the $15K-$50K per-deal data room cost most DC boutiques used to bill as expense reimbursement -- the platform fee shows up in the seller's expense column rather than the advisor's pass-through column. Business covers the page-analytics and screenshot-protection capabilities most DC advisors require; Peony Data Room at $52 per admin per month is the standard tier for active cleared-deal sell-side mandates that need the per-investor watermark, visitor-group buyer tiering, granular per-file permissions, and unlimited rooms for two-tier classified data room structuring.

Which Regulatory Inputs Should Washington DC M&A Founders Track in 2026?

Five regulatory inputs shape DC M&A timing more than in any other US metro:

-

HSR threshold raised to $133.9M effective February 17, 2026 (up from $126.4M in 2025; the $119.5M figure was the 2024 threshold) per FTC Hart-Scott-Rodino Act Notice of Annual Adjustment. For DC ADG founders evaluating $100M-$200M EV deals, the new $133.9M threshold means more deals fall above the HSR notification line in 2026 than in 2025 -- factor in the additional 30-day initial waiting period plus potential Second Request timing on any deal above threshold.

-

CFIUS (Committee on Foreign Investment in the United States) review -- DC-distinguishing for any cross-border defense or GovCon deal with foreign acquirer. CFIUS jurisdiction expanded under FIRRMA (Foreign Investment Risk Review Modernization Act) to include non-controlling investments in critical technologies, critical infrastructure, and sensitive personal data. Any cleared, ITAR-controlled, or government-services-with-classified-program-history deal involving a foreign acquirer (or even a US entity with significant foreign LP composition) requires CFIUS pre-clearance review. Hogan Lovells leads DC legal counsel on CFIUS workflow.

-