13 Best Technology & Software M&A Advisors for $25M-$1B Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

13 Best Technology & Software M&A Advisors for $25M-$1B Deals (2026)

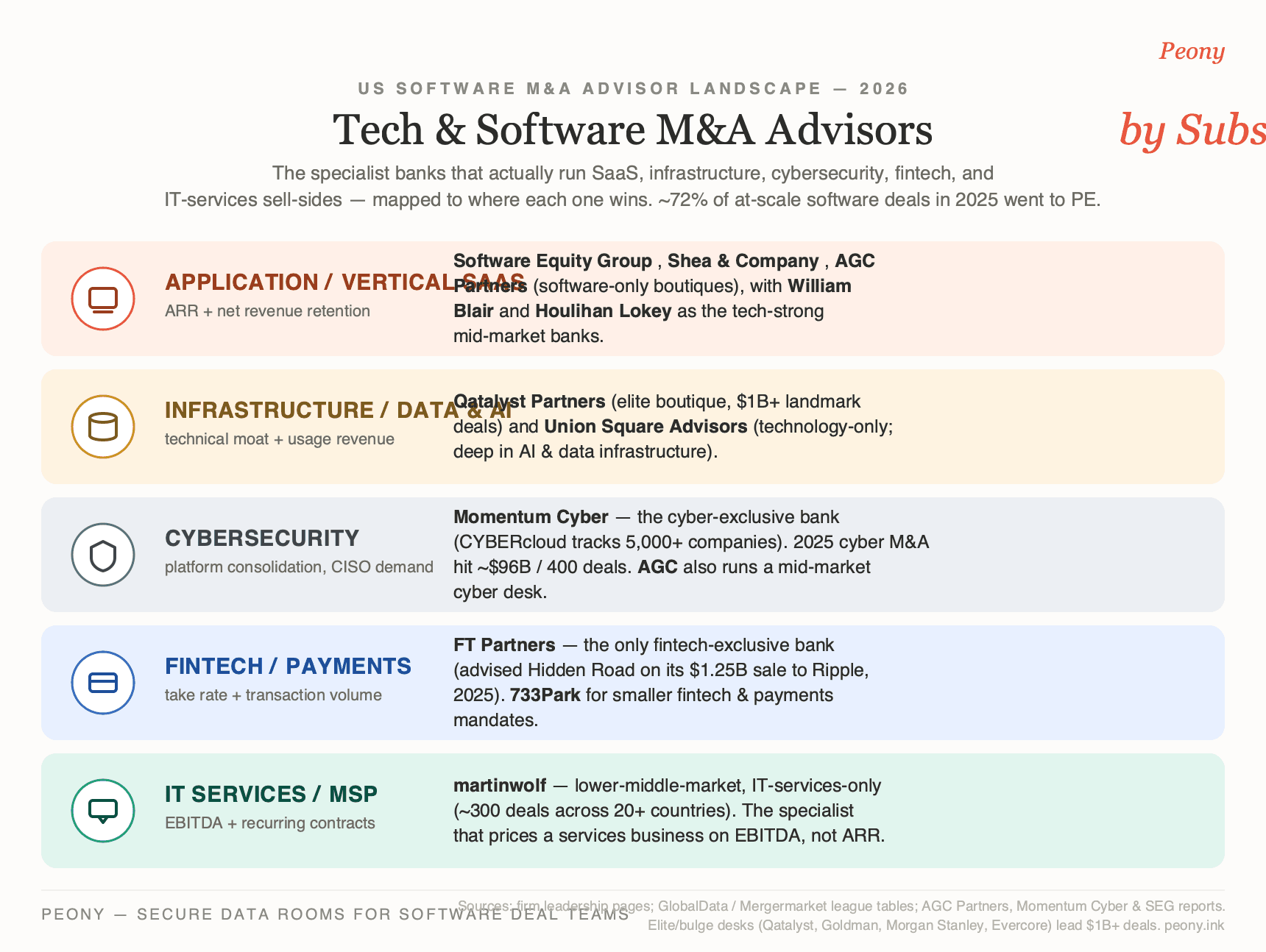

Quick answer: Software M&A does not have one "best advisor" — it has five subsector benches. For application / vertical SaaS in the $25M-$1B band, the strongest names are Software Equity Group (SEG), Shea & Company, and AGC Partners, with William Blair and Houlihan Lokey as the tech-strong mid-market banks. For infrastructure, DevTools & data/AI software, Qatalyst Partners and Union Square Advisors. For cybersecurity, Momentum Cyber. For fintech & payments, Financial Technology Partners (FT Partners). For IT services & MSPs, martinwolf. The bulge brackets and elite boutiques — Goldman Sachs, Morgan Stanley, Evercore, Qatalyst — own the $1B+ value league tables but are usually the wrong call below that. Pick by subsector and ARR scale, not by logo.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — vertical-SaaS exits, infrastructure and data-platform sales, cybersecurity tuck-ins, fintech transactions, and IT-services roll-ups — and software is the sector where picking the wrong type of advisor costs you the most, because so much of the value is metric-specific. A generalist banker who runs an EBITDA-multiple process on a high-retention SaaS company, or who has never had to defend a net-revenue-retention cohort against a buyer's quality-of-earnings team, leaves real money on the table. At Peony we now serve more than 5,900 customers, and a large share of our software deals live in exactly the $25M-$1B band this guide covers.

Most "best software M&A advisor" lists are interchangeable directory pages that rank firms one through ten as if a single league table existed. It does not. Software M&A splits into at least five distinct benches — application / vertical SaaS, infrastructure / DevTools / data & AI, cybersecurity, fintech & payments, and IT services / MSPs — and the firm that dominates one is often irrelevant in another. This post is organized the way the market actually works: by subsector, with each firm mapped to its lane, its deal-size band, and a verified credential or deal. The five proprietary frames — the Rule-of-40 Banker-Fit Matrix, the NRR Retention Defense Test, the Strategic-versus-Sponsor Buyer Split, the Founder-Liquidity Fork, and the SaaS Quality-of-Earnings Translation Gap — come from cross-referencing the verified 2025-2026 deal record against the structural realities of how software gets valued and sold.

Two framing notes before the roster. First, the buyer reality. Software M&A is now a private-equity business: by AGC Partners' count, roughly 72% of the at-scale software companies that transacted in 2025 were bought by financial sponsors, not strategics. That single fact should shape which banker you hire — you want one whose Rolodex is full of PE platforms actively rolling up your category, not just corporate-development teams. Second, honest framing on the bulge brackets. They are not the answer for most readers of this guide, but they own the value league tables (Goldman Sachs ranked #1 by deal value in Q1 2026; Morgan Stanley #2), so I name them at the end to frame the ceiling. And Peony is not an advisor — it is the data-room layer founders and bankers use to run the process; I will flag where that fits, but the advisory firms are the subject here.

What's the software M&A advisor landscape by subsector in 2026?

The roster below is organized by subsector. Each firm is profiled in depth in its section; this table is the map.

| Firm | HQ | Deal-size band | Subsector focus | Credential / verified deal |

|---|---|---|---|---|

| Software Equity Group (SEG) | San Diego | $5M-$100M ARR | Application / vertical SaaS (software-only) | Software-only sell-side bank; cited quarterly SaaS M&A research |

| Shea & Company | Boston + SF | Mid-market software | Software & tech-enabled services (only) | $50B+ advised since 2005; 151 deals as of Jan 2026 |

| AGC Partners | Boston | $50M-$1B EV | Software, AI/SaaS, cyber, GRC, fintech | Most active tech boutique by volume 2009-2025; 28 deals in 2025 |

| William Blair | Chicago | $150M-$2B+ | Tech-strong full-service (software-heavy) | The mid-market bank closest to a software specialist |

| Houlihan Lokey | LA (TMT) | $25M-$1B+ | Mid-market tech + restructuring | #1 TMT M&A by deal volume H1 2025 (34 deals, GlobalData) |

| Qatalyst Partners | San Francisco | $1B+ (landmark) | Software, internet, semiconductors | Founded by Frank Quattrone; advised PROS on $1.4B Thoma Bravo deal |

| Union Square Advisors | San Francisco | $100M-$2B+ | Infrastructure, AI/data, GRC, vertical | Technology-only; deep in AI & data infrastructure |

| Momentum Cyber | San Francisco | Cyber, all sizes | Cybersecurity (only) | Cyber-exclusive bank; CYBERcloud tracks 5,000+ cyber companies |

| FT Partners | San Francisco | Mid-cap-$5B+ | Fintech & payments (only) | Only fintech-exclusive bank; advised Hidden Road on $1.25B sale to Ripple |

| martinwolf | Scottsdale / Bay | LMM IT services | IT services / MSP / tech-enabled (only) | ~300 transactions across 20+ countries |

| Goldman Sachs (Software / TMT) | New York + SF | $1B+ | Bulge-bracket software / TMT | #1 M&A adviser by value Q1 2026; hired Qatalyst's Cayne (Jan 2026) |

| Morgan Stanley (Technology) | New York + Menlo Pk | $1B+ | Bulge-bracket technology | #2 M&A adviser by value Q1 2026 |

| Evercore (Technology) | New York + SF | $1B+ | Elite-boutique technology | Top independent advisor on large-cap tech |

A few notes the table cannot carry. SEG, Shea & Company, and AGC Partners are the working core for a $25M-$1B software seller — the software-only and tech-focused boutiques most readers of this guide actually need. Qatalyst is the most recognized pure-tech brand, but its best fit is $1B and above. Momentum Cyber and FT Partners are subsector monopolists — if you are selling a cybersecurity or fintech company, they belong on every pitch list. And martinwolf solves a genuinely different problem than the SaaS shops, because IT-services and MSP businesses are valued on EBITDA and recurring-managed-services contracts, not on ARR multiples. The bulge brackets are profiled at the end as the ceiling.

Who are the best application & vertical SaaS M&A advisors?

For an application or vertical-SaaS sale, the right advisor is a function of your ARR scale and how much of your value lives in recurring, high-retention revenue. The five firms below cover the $25M-$1B SaaS band, from software-only boutiques to the tech-strong mid-market banks.

Software Equity Group (SEG) is the software-only specialist most lower-middle-market SaaS founders should know first. Based in San Diego and led by managing director Allen Cinzori, SEG is a sell-side M&A bank that works exclusively with B2B software and SaaS companies, typically in the $5M-$100M ARR range, across verticals including PropTech, EdTech, GovTech, HealthTech, and manufacturing software. It is also one of the most-cited research voices in the category, publishing widely-read quarterly and annual SaaS M&A and public-market reports. For a founder selling a $5M-$50M ARR SaaS business who wants a senior, software-only team and a process built around SaaS metrics, SEG is best-in-class.

Shea & Company is the senior-led, software-only boutique for the mid-market. Founded in 2005 and headquartered in Boston (with a San Francisco office), Shea advises exclusively in software, SaaS, and technology-enabled services, and cites $50B+ in completed transactions since inception across roughly 150 deals (151 as of January 2026). Its differentiator is that the entire bench lives in the software industry every day, and senior bankers run the deals rather than handing them to juniors. For a mid-market software company that wants software-only focus and senior attention, Shea is a reference name.

AGC Partners is the most active tech-M&A boutique by deal volume — named the most active technology M&A boutique every year from 2009 through 2025. Founded in 2003 in Boston by Benjamin Howe, Jon Guido, and Maria Lewis Kussmaul, AGC has completed 585+ transactions and focuses on fast-growing tech businesses valued between $50M and $1B, with strength across SaaS, AI, cybersecurity, GRC, and fintech. The verified recency signal that tells you how the market actually clears: AGC closed 28 deals in 2025, split exactly 14 PE-platform and 14 strategic — a near-perfect illustration of why a software seller needs a banker fluent in both buyer types. For a $50M-$1B tech company, AGC is a high-volume, well-connected choice.

William Blair is the mid-market full-service bank that sits closest to a true software specialist. It pairs deep technology coverage with the financing and breadth of a large bank, and is a natural fit for a $150M-$2B+ software company that wants a full corporate process with both strategic and sponsor reach. For a seller at the upper end of this guide's band who has outgrown a boutique, William Blair is a credible step up.

Houlihan Lokey is the leading middle-market M&A house with a differentiator that matters when growth stalls: a deep restructuring bench. Houlihan Lokey ranked #1 in TMT M&A by deal volume in H1 2025 (34 transactions, per GlobalData) and runs the highest deal-count middle-market practice in the business. When a software company's growth has slowed and the conversation shifts toward a value-conscious sale or a recap, Houlihan Lokey's combination of M&A volume and restructuring capability is an edge no pure SaaS boutique can match.

Rule-of-40 Banker-Fit Matrix. The right software advisor is a function of your growth-plus-profit profile and your ARR scale — because that profile determines both your multiple and which buyers will compete for you. Map your Rule of 40 and ARR to the banker type, and hire the banker who can defend your net revenue retention, not just your EBITDA.

| Your profile | What sets your multiple | Best advisor type | Examples |

|---|---|---|---|

| High-growth, high-NRR SaaS ($5M-$50M ARR) | ARR growth + NRR over 120% | Software-only boutique | SEG, Shea & Company, AGC Partners |

| Profitable, steady SaaS (Rule of 40 ~40-50) | Profitable-growth balance + retention | Software boutique or mid-market bank | SEG, AGC, William Blair |

| Larger / scaled software ($150M-$1B EV) | Corporate equity story + buyer breadth | Tech-strong mid-market bank | William Blair, Houlihan Lokey, Union Sq. |

| Slow-growth / under 15% (EBITDA-priced) | EBITDA + recurring-revenue durability | Mid-market bank w/ restructuring bench | Houlihan Lokey |

| $1B+ landmark / public-company deal | Strategic fit, scale, stock mechanics | Elite boutique / bulge bracket | Qatalyst, Goldman, Morgan Stanley |

| Infrastructure / cyber / fintech / IT-services | Subsector-specific value drivers | Subsector specialist (see below) | Union Sq., Momentum Cyber, FT Partners, martinwolf |

Who advises on infrastructure, DevTools, and data / AI software M&A?

Infrastructure, developer-tools, and data/AI software is a different game from application SaaS — value lives in technical moats, usage-based or consumption revenue, platform extensibility, and, increasingly, an AI story that buyers are paying up for. Two firms lead for a $100M-$1B+ seller, with the bulge brackets taking over at the very top.

Qatalyst Partners is the elite independent tech boutique — the most recognized pure-technology M&A brand on the Street. Founded by Frank Quattrone in 2008, Qatalyst advises senior management and boards of established and emerging technology leaders on landmark deals across software, internet, and semiconductors, and has advised on 200+ M&A transactions in its history, weighted heavily toward the $1B+ end. A representative recent mandate: Qatalyst advised PROS Holdings on its ~$1.4B take-private by Thoma Bravo, announced September 22, 2025. For a large-cap software, infrastructure, or data/AI company contemplating a transformational sale or take-private, Qatalyst is the reference boutique — and a signal of how hot software banking is right now: Goldman Sachs hired Qatalyst co-founder Brian Cayne as its global co-head of software investment banking, effective January 2026.

Union Square Advisors is a technology-only investment bank with genuine depth in the infrastructure and data/AI corner of the market. The firm runs sell-side and capital-raising mandates across AI and data infrastructure, governance/risk/compliance (GRC), health technology, and vertical software, and its 2025 deal record shows the range — it served as exclusive financial advisor to Scientist.com (an AI-powered R&D orchestration platform) on its sale to GHO Capital in September 2025, among other transactions. For an infrastructure, data, or applied-AI software company in the $100M-$1B+ band that wants a technology-only team without going to a bulge bracket, Union Square is a strong fit.

At the very top of this subsector — $1B+ infrastructure, semiconductor, and data/AI deals — the elite boutiques and bulge brackets (Qatalyst, Goldman, Morgan Stanley, Evercore) take over, for the mega-buyer relationships and public-company mechanics those deals require.

Who are the best cybersecurity M&A advisors?

Cybersecurity is its own world — recurring revenue, platform-consolidation dynamics, and a buyer set driven by the CISO mandate to reduce vendor sprawl — and it has a category-defining specialist.

Momentum Cyber is the cybersecurity-exclusive advisory bank, and for a security-software or services seller it belongs on every pitch list. The firm focuses entirely on the cybersecurity sector and maintains CYBERcloud, a proprietary database tracking 5,000+ cyber companies and the sector's M&A and financing history — which gives it an unusually precise read on which strategics and sponsors are buying what. The market context is extraordinary: 2025 cybersecurity M&A reached roughly $96B across about 400 deals, more than double 2024's $46.1B (Momentum Cyber), with consolidation continuing into 2026. The driver is structural — enterprises are collapsing best-of-breed point solutions into integrated platforms, so acquirers (Palo Alto Networks, Google, Check Point, Zscaler, and the services consolidators) prize targets that fill a specific portfolio gap like identity, DLP, or AI/OT security. The mega-deals frame the ceiling — Google's ~$32B acquisition of Wiz, Palo Alto Networks' ~$25B acquisition of CyberArk, and ServiceNow's $7.75B acquisition of Armis — but the lesson for a $25M-$1B cyber seller is to hire a banker who can map your product to the exact platform gap a strategic or sponsor is trying to fill. AGC Partners also runs a credible cybersecurity practice for the mid-market.

Who are the best fintech and payments M&A advisors?

Fintech and payments software has its own specialist monopoly, because the buyer set (banks, payment networks, fintech consolidators, and fintech-focused PE) and the value drivers (take rate, transaction volume, regulatory posture) are specific enough to reward a dedicated bank.

Financial Technology Partners (FT Partners) is the only investment bank focused exclusively on the financial-technology sector. Launched in 2002 by Steve McLaughlin and headquartered in San Francisco, FT Partners covers fintech and payments across all sub-sectors and geographies, and runs both M&A and large financings. Its 2025 deal record shows the scale it operates at — FT Partners advised Hidden Road on its $1.25B sale to Ripple (announced April 8, 2025), one of the largest deals in the digital-assets space, and has advised on a long string of payments and fintech transactions. The firm also publishes some of the most comprehensive fintech research in the market, including a quarterly FinTech Insights report and a 2026 Global FinTech report co-authored with Boston Consulting Group. For a fintech or payments software company at any meaningful scale, FT Partners is the reference name; for smaller fintech and payments mandates, boutiques such as 733Park are also active across fintech, payments, and SaaS.

Who are the best IT services and MSP M&A advisors?

IT services, managed services (MSPs), and tech-enabled services are valued on a fundamentally different basis than SaaS — buyers underwrite EBITDA, recurring managed-services contracts, technician utilization, and customer stickiness, not an ARR multiple — so the specialist bench is different too.

martinwolf is the lower-middle-market M&A advisor focused exclusively on IT — IT and cloud / tech-enabled services, software / SaaS, and the IT supply chain. The firm has advised on roughly 300 transactions across 20+ countries, including divisions of Fortune 500 companies, and its 2026 IT M&A outlook (from managing partner Seth Collins) describes a real pause in the first half of 2025 followed by a significant pickup into 2026, driven by outsourcing consolidation (end users routing more spend through fewer vendors), capital deployment, and AI. For an MSP or IT-services owner selling a sub-$250M business, a specialist that understands recurring-services contracts and consolidation economics will run a far better process than a generalist or a SaaS-only boutique that misreads a services business as if it were software.

Strategic-versus-Sponsor Buyer Split. Software M&A is a private-equity business first. By AGC Partners' count, ~72% of at-scale software companies that transacted in 2025 went to financial sponsors. The two buyer types pay for different things — so run a process that puts both in competition, and hire a banker who can prove recent closings into each.

| Buyer type | What they pay for | Typical price posture | What they usually want from you | Best when… |

|---|---|---|---|---|

| Strategic acquirer | Capability gap closed / competitor removed | Highest on a clean synergy fit | Your product + team absorbed into theirs | A specific strategic has a real, durable reason to buy |

| PE platform (new) | Cash-flow durability, expansion runway | Disciplined, cash-flow-anchored | Management to roll equity and stay | You believe in the next chapter and want partial liquidity |

| PE add-on (to platform) | Fit with an existing platform's roadmap | Blend of strategic + sponsor | Integration into the platform | A platform is rolling up your exact category |

What are the proprietary frames in this guide — and how do I use them?

These are the five Peony-original lenses this post is built on. Each turns a public fact into a decision you can act on.

- Rule-of-40 Banker-Fit Matrix (above): your growth-plus-profit profile and ARR scale determine both your multiple and which buyers compete — and therefore which advisor type fits. High-growth high-NRR SaaS wants a software-only boutique; slow-growth EBITDA-priced software wants a mid-market bank with a restructuring bench.

- NRR Retention Defense Test: net revenue retention is the SaaS equivalent of a reserve report. NRR above 120% commands roughly 30-50% higher ARR multiples than a 100%-NRR peer, and each 10-point NRR increase is associated with a 20-30% valuation lift — but only if the banker presents the trailing-12-month trend, the GRR underneath it, and the cohort/concentration detail. A point-in-time NRR gets discounted.

- Strategic-versus-Sponsor Buyer Split (above): ~72% of at-scale software deals in 2025 went to PE (AGC Partners). Hire a banker whose Rolodex is full of the platforms rolling up your category — and run a dual-track process anyway.

- Founder-Liquidity Fork: recap-vs-full-sale is a strategy decision, not just a price one. The test: if you would re-invest in your own company at today's valuation, you are probably a recap; if you would not, you are a sale — and the two call for different advisors.

- SaaS Quality-of-Earnings Translation Gap: GAAP revenue, billings, and ARR are three different numbers. The value a software-literate banker adds over a generalist is largely in bridging deferred revenue, RPO, and cash collections, and in separating high-multiple recurring ARR from low-multiple services revenue before a buyer's accountants do it for you.

What's the honest take on the bulge brackets and elite boutiques for software?

They own the value league tables, and below ~$1B they are usually the wrong call — but it is worth knowing the ceiling. Goldman Sachs ranked #1 among M&A advisers by deal value in Q1 2026 and has visibly re-committed to software banking, hiring Qatalyst co-founder Brian Cayne as global co-head of software investment banking effective January 2026. Morgan Stanley ranked #2 by value in Q1 2026 and has one of the deepest technology franchises on the Street. Evercore is the top independent advisor on large-cap technology. And Qatalyst is the elite tech boutique that punches at bulge-bracket scale on landmark software, internet, and semiconductor deals. The reason these are the wrong default for a $25M-$150M SaaS seller is not quality — it is fit: their economics, attention, and process are built for multibillion-dollar mandates, so your deal becomes their smallest of the quarter, staffed thin. The market structure underlines it: Q1 2026 set a near-record for M&A value (the strongest start since 2021) on roughly 30% fewer deals — meaning value is concentrating in megadeals at the top while the $25M-$1B middle, where most software founders actually transact, is served far better by the boutiques and mid-market banks profiled above. For the broader sweep of the largest tech deals, see our 20 biggest tech acquisitions of the last decade.

How does this compare to other sectors — and where does Peony fit?

If you are weighing a software sale against the way other capital-intensive sectors run, two of our sector hubs are useful references: the best energy M&A advisors guide (which shows how a reserve-report-driven sector picks advisors) and the best healthcare M&A advisors guide (regulatory-overhang and subsector-specialist dynamics). The common thread across all three sectors is the same: the firm that wins your value is the one that can speak your subsector's specific value language — reserves in energy, regulatory posture in healthcare, and net revenue retention in software.

On the document side, the through-line is also constant. Whoever you hire, your advisor will run the process out of a data room, and in software the data room carries unusually sensitive material — customer-level ARR and churn data, source-code references, security attestations, and a full contract set. We built Peony, a SOC 2 Type II certified data room company used by 5,900+ customers, for exactly this kind of tiered, watermarked release: per-bidder visitor groups so strategics and sponsors see only what they should, per-page watermarks on every render to deter leaks, screenshot protection on the most sensitive material, and page-level analytics that show your banker which bidders are genuinely working the file. To be clear about scope: Peony is not an M&A advisor and does not place deals — the advisory firms above do that. Peony is the layer that makes the diligence run cleanly once you have hired one. For the full software buildout, see our SaaS M&A data room guide and, for reading buyer intent from engagement data, our data-room analytics guide.

The bottom line

Software M&A is not one league table — it is five subsector benches, and the right advisor for a $25M-$1B seller is a function of your subsector and your ARR scale, not a logo. For application and vertical SaaS, start with SEG, Shea & Company, and AGC Partners, stepping up to William Blair or Houlihan Lokey as you scale. For infrastructure and data/AI, Qatalyst and Union Square Advisors. For cybersecurity, Momentum Cyber; for fintech, FT Partners; for IT services, martinwolf. Run a dual-track process — because ~72% of software deals now go to private equity, but the best price usually comes from making a strategic and a sponsor compete. And before you launch, get your ARR bridge, your NRR cohorts, and your data room in order, because the cheapest lever you control on both timeline and price is walking into diligence with numbers that already tie out.

Related resources

- M&A advisor vs broker vs investment bank — the decision that comes before this software shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 16 Best Healthcare M&A Advisors by Subsector — a sibling national sector cut: healthcare M&A advisors mapped by subsector

- 14 Best Energy M&A Advisors by Subsector — the first national sector cut in this series, showing how a reserve-driven sector picks advisors

- SaaS M&A data room: 2026 guide — the software-specific data-room buildout behind a sale, with the ARR bridge and NRR cohorts buyers expect

- Data-room analytics: how to spot serious buyers — reading buyer intent from engagement data during a dual-track process

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, the right-sized room for a smaller-ARR software exit

- Best M&A Advisors in San Francisco — the Bay Area geo cut of this national hub, where most tech boutiques and bulge desks sit

- Best M&A Advisors in New York — the NYC geo cut for software, fintech, and diversified sellers

- Best M&A Advisors in Boston — the geo cut where AGC Partners and Shea & Company are headquartered

- The 20 biggest tech acquisitions of the last decade — the historical ceiling: the landmark deals the bulge brackets and Qatalyst run

- M&A Data Room: setup and workstream mapping — the general sell-side data-room playbook

- Best Software M&A Advisors — the software/SaaS-only carve of this hub: the software-specialist bench and sub-vertical routing for vertical SaaS, communication software, and cloud sellers

Frequently asked questions

Who are the best technology / software M&A advisors for selling a SaaS company in 2026?

The best software M&A advisor depends on your subsector and ARR scale, not a single ranking. For an application or vertical-SaaS sale in the $25M-$1B band, the strongest options are the software-only sell-side boutiques and tech-focused mid-market banks: Software Equity Group (SEG, a San Diego software-only bank that works B2B software at roughly $5M-$100M ARR and publishes one of the most-cited quarterly SaaS M&A reports), Shea & Company (Boston, software and tech-enabled-services only, $50B+ advised since 2005), AGC Partners (Boston, the most active tech-M&A boutique by deal volume from 2009 through 2025, ~585 transactions, with a $50M-$1B sweet spot), William Blair (the mid-market bank closest to a true software specialist), and Houlihan Lokey (#1 in TMT M&A by deal volume in H1 2025 with 34 deals per GlobalData, plus a restructuring bench that matters if growth has stalled). For infrastructure, DevTools, and data/AI software, look at Qatalyst Partners and Union Square Advisors; for cybersecurity, Momentum Cyber; for fintech and payments, Financial Technology Partners (FT Partners); for IT services and MSPs, martinwolf. The bulge brackets — Goldman Sachs, Morgan Stanley, Evercore — own the $1B+ value tables but are usually the wrong call below that. The honest filter: ask each firm to name the five buyers they would call first for your specific product, how many software deals they have closed in your subsector in the last 18 months, and whether those went to strategics or to private equity. We run Peony, a SOC 2 Type II certified data room company that has served 5,900+ customers, and across hundreds of software diligence processes the firms that genuinely engage are the ones that can answer that without hesitating. The intermediary-tier decision is covered upstream in our M&A advisor vs broker vs investment bank guide.

Which advisors specialize in vertical SaaS, infrastructure / DevTools, cybersecurity, fintech, or IT services?

Each software subsector has its own specialist bench, and the firm that dominates one is often irrelevant in another. For application and vertical SaaS, the specialists are Software Equity Group, Shea & Company, and AGC Partners, with William Blair and Houlihan Lokey as the tech-strong mid-market banks. For infrastructure, developer tools, and data/AI software, the standouts are Qatalyst Partners (the elite independent tech boutique for landmark deals) and Union Square Advisors (technology-only, with real depth in AI and data infrastructure, GRC, and vertical software). For cybersecurity, the category-defining bank is Momentum Cyber — a cyber-exclusive advisory shop whose CYBERcloud database tracks 5,000+ cyber companies, in a market where 2025 M&A reached roughly $96B across 400 deals (more than double the prior year). For fintech and payments software, Financial Technology Partners (FT Partners) is the only fintech-exclusive investment bank — it advised Hidden Road on its $1.25B sale to Ripple in April 2025. For IT services, managed services (MSPs), and tech-enabled services — which trade on EBITDA, not ARR — the lower-middle-market specialist is martinwolf (~300 transactions across 20+ countries). The subsector roster below maps each firm to its lane, and our city guides cover the geo cut for the major tech hubs: San Francisco, New York, Boston, Seattle, and Austin.

Do I need a software-specialist banker, or can a generalist M&A advisor sell my SaaS company?

For most software sellers, a sector specialist beats a generalist — and the reason is specific, not snobbery. Software value is technical in ways a generalist process does not capture: a SaaS company is priced off its ARR base, its net revenue retention (NRR) and gross revenue retention (GRR), its growth-plus-margin profile (the Rule of 40), and the durability of its recurring revenue — not off a trailing EBITDA multiple. A generalist banker who runs a blunt EBITDA process will under-credit exactly the things that drive a software premium: high NRR, low logo churn, expansion revenue, and a clean ARR bridge. Just as costly, a generalist will not have direct lines to the handful of active acquirers in your subsector — and in software those are overwhelmingly private equity platforms (PE bought about 72% of at-scale software companies that transacted in 2025, per AGC Partners), plus a short list of strategic consolidators. The exception worth naming honestly: if your single most likely buyer is a strategic with whom your CEO or board already has a deep relationship, a trusted generalist or even a direct negotiation can sometimes beat a specialist's broad process — competition, not the banker's logo, is what moves price. But in a market where the buyer universe is concentrated and the value drivers are metric-specific, the specialist's buyer Rolodex and SaaS-metric fluency are usually worth more than the fee. The deeper distinction between a software boutique, a full-service bank, and a business broker is in our M&A advisor vs broker vs investment bank hub.

Will a generalist banker undervalue my recurring revenue, NRR, and deferred revenue?

Often, yes — and the gap usually shows up in three places, which is the core of what I call the SaaS Quality-of-Earnings Translation Gap. First, recurring-revenue quality: a generalist tends to value the whole revenue line at one multiple, while a software-literate banker separates recurring ARR from services and one-time revenue and defends a higher multiple on the durable, high-retention portion — that distinction alone can move the headline number materially. Second, the ASC 606 / deferred-revenue mechanics: GAAP revenue, billings, and ARR are three different numbers, and a banker who cannot bridge deferred revenue, RPO (remaining performance obligations), and cash collections will lose ground in a quality-of-earnings review when the buyer's accountants normalize them. Third, the retention story: this is the SaaS equivalent of a reserve report. The single most important diligence metric is net revenue retention, and a 10-point increase in NRR is associated with a 20-30% lift in valuation — companies sustaining NRR above 120% command roughly 30-50% higher ARR multiples than otherwise-identical companies at 100%. A generalist who reports a point-in-time NRR without the trailing-12-month trend, the GRR underneath it, and the cohort and concentration detail will let a buyer discount your multiple. The branded line I use: hire the banker who can defend your net revenue retention, not just your EBITDA. The screening question for any software advisor: ask them to walk through how they would bridge your GAAP revenue to ARR and how they would present your NRR cohorts to a skeptical buyer.

Software-only boutique vs tech-focused mid-market bank vs bulge bracket — which do I need for a software sale?

It maps almost entirely to ARR scale and process complexity. For a $25M-$150M EV software company (roughly $5M-$30M ARR), the default is a software-only boutique — SEG, Shea & Company, or AGC Partners — because that deal is below the attention and minimums of a bulge bracket, the win comes from SaaS-metric marketing and a tight PE-buyer process, and the economics usually run on Double Lehman. For $150M-$500M you have a choice between a software boutique and a tech-strong mid-market bank (William Blair, Houlihan Lokey, Union Square Advisors) — enough size for a real bank, but confirm a senior banker (not a second-year associate) actually runs it. For $500M-$1B, a top boutique or mid-market bank brings a full corporate process, financing access, and broader buyer reach — and fees compress, so negotiate the percentage and the tail. Only at $1B+ does an elite boutique (Qatalyst) or a bulge bracket (Goldman, Morgan Stanley, Evercore) become the default, for mega-buyer relationships and public-company / stock-deal mechanics. The league-table paradox to understand: the bulge brackets dominate the value tables because they advise the multibillion-dollar take-privates and mega-mergers, but that is exactly why they are usually the wrong call for a $25M-$150M SaaS sale — that deal needs a software banker with a PE Rolodex, not a logo. Our advisor-vs-bank selection hub walks the full intermediary decision.

Is my $20M ARR software company too small for a real investment bank?

No — a $20M ARR software company (very roughly $80M-$150M EV at a healthy 2026 multiple) is squarely in the sweet spot for the software-only boutiques and at the lower end of what a tech-strong mid-market bank will take. SEG explicitly works B2B software in the $5M-$100M ARR band; AGC Partners targets $50M-$1B in enterprise value; Shea & Company runs software-only processes across the middle market — all three will put senior bankers on buyer calls for a $20M ARR business. Where you are genuinely too small for a full-service software bank is below roughly $3M-$5M ARR (under ~$10M-$25M EV), where a bank's minimum-fee floor (commonly $50K-$250K) consumes an outsized share of proceeds; at that size a boutique that runs a targeted, low-overhead process — or, for a micro-SaaS, an online marketplace — is the better economic fit. The honest filter for a $20M ARR seller: a focused software boutique with a real, current map of which PE platforms are buying in your category will almost always beat a bulge bracket that treats your deal as its smallest mandate of the quarter, and a generalist with no SaaS-metric credibility. Ask each pitching bank, in writing, which senior banker will be on every buyer call, and to name five platforms actively rolling up your category right now.

What multiple of ARR can I get for my SaaS company in 2026 — and what do software M&A advisors charge?

On valuation: in 2026 private B2B SaaS is trading at a median of roughly 4-5x ARR (call it ~4.5x), with a broad range from about 3x for slower-growth or sub-scale businesses to 7x+ for high-growth, high-retention category leaders; public SaaS sits a touch higher around 5.5x. Two levers move you within that range more than anything else. The Rule of 40 (revenue growth rate + profit margin) is the dominant screen — each ~10-point improvement has been associated with roughly a 1.1x increase in the EV/revenue multiple, and the 2026 market rewards the profitable-growth version over the burn-for-growth version. Net revenue retention is the second lever: NRR above 120% can lift the multiple 30-50% over a 100%-NRR peer. Below ~15% growth, buyers increasingly switch to an EBITDA basis (often 8-12x) rather than a revenue multiple. On fees: software M&A is priced like the rest of the lower-middle market — a monthly retainer or work fee plus a success fee at close — with the success rate declining as deal size grows: roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex / Axial M&A Fee Guide, 8th edition, N=456). Lehman-style declining-rate formulas are not obsolete — a declining Lehman is the single most common structure (~44% of engagements), and in the lower middle market you will most often be quoted the Double Lehman (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% above $5M): on a $20M deal that is $600,000, or 3.0%. Full mechanics are in our M&A advisor fees hub.

How much does it cost to sell a $50M-$100M software company, and are Lehman / Double Lehman fees standard?

Both Lehman and Double Lehman are still standard, and at $50M-$100M you are entering the fee-compression zone. Expect a blended success fee in the ~1.5%-2.5% range — closer to 2.5% at $50M and falling toward ~1.5%-2.0% as you approach $100M — plus a retainer of roughly $50K-$150K and capped expenses. A straight Double Lehman computes to about 2.4% on a $50M deal ($1.18M) and about 1.9% on a $100M deal ($1.9M), which is why banks negotiate a flat or stepped percentage at the top of the range rather than running pure Double Lehman. Retainers usually run $5K-$15K/month (or a fixed amount), and about 72% are credited against the success fee if the engagement letter says so in writing (2021-22 Fee Guide survey) — get that in writing. The base matters more than the rate: confirm whether transaction value is defined on equity or on enterprise value (including assumed debt), and how earnouts, rollover equity, and escrow are counted, because a broad definition can add hundreds of thousands of dollars on the same headline price. One software-specific clause to negotiate: the tail. A named PE platform that passed can resurface 12-18 months later when it raises a new fund or finds the right add-on, so limit the tail to a named-buyer list the banker must deliver within ~10 days of termination. The worked Lehman / Double Lehman math and the cautionary fee cases are in our fee hub.

Should I sell my software company to a strategic acquirer or a private equity (PE) buyer?

In software, the honest default is that you will probably sell to private equity — and you should run a process that puts both buyer types in competition anyway. This is the Strategic-versus-Sponsor Buyer Split. Private equity now dominates software M&A: roughly 72% of the at-scale software companies that transacted in 2025 were bought by financial sponsors (AGC Partners), and the two largest software-focused funds — Thoma Bravo and Vista — have deployed $120B+ since 2019 on a repeatable playbook (take a company private at ~5-8x revenue, run it off the quarterly-earnings clock for four to six years, consolidate the category via bolt-ons, and exit). The buyer types optimize for different things, so the right answer depends on what you want. A strategic acquirer typically pays the highest price when your product closes a specific capability gap or removes a competitor, may move fastest, but often absorbs your team and brand and can walk if the synergy case wobbles. A PE platform tends to pay a disciplined (cash-flow-anchored) price, frequently wants management to roll equity and stay, and offers a structured path to a 'second bite' at the next exit — attractive if you believe in the next chapter and want partial liquidity now. A PE-owned strategic (an add-on to an existing platform) blends both. The practical move: hire a banker who can credibly run a dual-track process and show recent closings into both groups, then let competitive tension — not a single inbound — set the price. To read which bidders are genuinely working your file, our data-room analytics guide covers the engagement signals that separate serious buyers from tire-kickers.

Should I take a minority recap and partial liquidity, or sell the whole company?

This is the Founder-Liquidity Fork, and it is one of the most consequential — and most overlooked — decisions in a software exit. A full sale converts 100% of your equity to cash (or cash plus rollover), ends your control, and is the right call if you want out, if growth is plateauing and you would rather de-risk now, or if a strategic is offering a premium you do not expect to beat. A minority recapitalization or growth-equity round lets you take meaningful chips off the table — partial liquidity for you and early shareholders — while you keep majority control and a large stake in the upside, and is the right call if the business is still compounding, if your NRR and Rule of 40 are strong, and if you believe the next four to five years will be worth more than today's headline. A growth-equity round also buys operating help (pricing, go-to-market, add-on M&A) without ceding control. The decision changes which advisor you want: a clean full-sale auction is a software-boutique or mid-market-bank mandate (SEG, Shea, AGC, William Blair), while a minority recap or growth round is often run by the capital-raising arm of those same firms or by a growth-focused banker — confirm the firm has done your specific structure recently, not just full sales. The branded test I use: if you would re-invest in your own company at today's valuation, you are probably a recap; if you would not, you are a sale. The intermediary-type framing is in our advisor vs broker vs investment bank hub.

How does a sell-side M&A process work for a software company, and how long does it take in 2026?

A software sell-side process runs the standard arc with software-specific diligence loaded on top. Roughly: (1) preparation and positioning (2-6 weeks) — assemble the ARR bridge, NRR/GRR cohorts, and Rule-of-40 story, build a clean data room, and draft the CIM; (2) buyer outreach and teasers behind a clickthrough NDA (2-4 weeks) — a focused list, weighted toward the PE platforms and strategics actually active in your category; (3) management presentations and indications of interest (3-5 weeks); (4) bid evaluation and selecting a lead party or short list; (5) confirmatory due diligence and exclusivity (4-8 weeks) — where a quality-of-earnings review and deep SaaS-metric verification happen; and (6) purchase-agreement negotiation and close. End to end, a well-run lower-middle-market software process typically takes about four to seven months from launch to signing, with another stretch to close if there is a financing or regulatory step. The two things that most often add time are a messy ARR/deferred-revenue picture that fails to reconcile in QoE, and a thin buyer list that produces too little competitive tension. The single cheapest lever you control on both timeline and price is a diligence-ready data room before launch — staged so a teaser sits behind a clickthrough NDA, the full room opens only to NDA-signed bidders, and the most sensitive customer-level and code-level detail is held to a short list. The full mechanics for a software room are in our SaaS M&A data room guide.

What should be in my data room before I take a software company to market, and how do buyers diligence ARR and NRR?

A software data room is more metric-intensive than a generic M&A room, and getting it right before launch is the cheapest lever you control on timeline and price. Buyers will expect: an ARR bridge (beginning ARR, new, expansion, contraction, churn, ending ARR) reconciled to your GAAP revenue and billings; net revenue retention and gross revenue retention by cohort, with the trailing-12-month trend (point-in-time NRR alone will be discounted); logo churn and customer concentration (a high NRR driven by one or two big accounts gets heavily discounted for concentration risk); a full customer contract set with terms, renewal dates, and any change-of-control clauses; the deferred-revenue and RPO schedule; CAC, payback, LTV, and magic-number / sales-efficiency detail; the product and security posture (architecture, SOC 2 / security attestations, key technical dependencies and any open-source license exposure); the cap table, options, and 409A history; and standard legal, financial, and HR sections. Buyers diligence ARR and NRR by reconciling your reported metrics to raw billing and CRM data — so make sure your numbers tie out before a buyer's accountants find the gap in a quality-of-earnings review. The room should be staged: a teaser behind a clickthrough NDA, a full room for NDA-signed bidders, and sensitive customer-level and source-code detail released only to a short list after indications of interest. We built Peony — a SOC 2 Type II certified data room used by 5,900+ customers — for exactly this kind of tiered, watermarked release: per-bidder visitor groups, per-page watermarks on every render, and page-level analytics that show your banker which bidders are genuinely working the file. For the full software buildout, see our SaaS M&A data room guide.