13 Best Boutique M&A Advisors in Austin for $5M-$200M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

13 Best Boutique M&A Advisors in Austin for $5M-$200M Deals (2026)

Last updated: May 2026

Early in my career I spent a stint on the M&A bench at Nomura before crossing the table to early-stage investing at Backed VC and growth-equity / secondaries at Target Global — and I've spent the last several years co-founding Peony, a data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. The conversation I have most often with Austin SaaS and tech founders considering a sell-side process in 2026 is the same one I had in 2024: the Austin M&A landscape is structurally bifurcated — most commodity SEO articles list firms as Austin boutiques that are actually headquartered in San Diego (Software Equity Group since 1992), Birmingham AL (Founders Advisors), Tampa (Hyde Park Capital), Boston (AGC Partners, Capstone Partners' parent before Huntington Bancshares acquisition), or simply do not have a meaningful Austin presence (Lincoln International and Stephens have no Austin M&A offices; William Blair's Austin office is Public Finance / muni bonds, NOT corporate M&A) — and the active 2026 Austin-resident bench is thinner than founders expect, with the $5M-$200M EV band driven mostly by Vista Equity Partners portfolio-company tuck-in acquisitions rather than direct Vista purchases (Vista's $107B AUM is real but the average direct deal is in the $1B-$3B band, almost never below $200M EV). This guide names 13 verified Austin-area boutiques with dated 2024-2026 closed transactions, maps each one to the Austin Strategic Buyer Quartet (PE software platforms via Vista portfolio tuck-ins + Insight + Thoma Bravo, strategic tech via Salesforce / Oracle / Microsoft / Workday / YETI / IgniteTech / Flexera, mid-market PE via Mainsail / Sageview / Blue Sage / NewSpring, consumer-restaurant via Sun Holdings / Pritzker Private Capital / Whole Foods alumni), and gives founder-CEOs the engagement-letter terms, fee benchmarks, and confidentiality-discipline frame I use to scope every sell-side conversation. Sources are linked inline at every transaction reference; verified deals only; commodity-article firms with no real Austin presence are flagged and excluded. Peony's investors include Matt Clifford (EF / ARIA), Charlie Songhurst (ex-Microsoft), Backed VC, and Possible Ventures.

Quick answer: For an Austin / Texas Hill Country $5M-$200M EV sell-side in 2026, the 13 verified boutiques worth pitching are Navidar (Austin-HQ at 400 W 15th St Ste 325, Stephen B. Day ex-Goldman Sachs and Bear Stearns Technology IB founding MD, 170+ principal transactions $26B M&A + $22B capital raising), Westlake Securities (Austin since 2003 at 2700 Via Fortuna Ste 250, FINRA CRD 127112, 140+ deals; recent NaturPak→Pritzker Private Capital Jan 2026, Cadeo→Resource Innovations Jun 25 2024, LeasePoint $40M Oct 16 2024), ScaleView Partners (Austin founded 2021, Wilcox/Snodgrass/Davidson founding bench; three verified 2025 SaaS exits Solvexia→GTreasury + Harbour Software→Springbrook + Cityspan→Gravity), pH Partners (Austin-HQ healthcare IB founded 2016 by Benjamin Perkins, partners $20B+ strategic advisory + $15B+ capital raises; recent VeruStat→CoachCare), Morgan Kingston Advisors (Austin restaurant-only specialist founded 2018 by Susan Miller + Sean Mirzabegian; recent Freebirds→Sun Holdings Aug 14 2024 + Protein Bar→Founder's Table), Focus Strategies Investment Banking (Austin, Gary Valdez founded 1999 after 24-year commercial banking career, $7B+ aggregate; recent JKB Construction 2025 + The Stansberry Firm rental-equipment vertical Oct 2025), NorthView Advisors (Austin since 2010, FINRA CRD 323786 member since 09/2023, industrial/services/oil-gas/healthcare/manufacturing focus), Austin Dale Group (Austin founded 2003 by John W. Austin + Bob Dale ex-founders of Austin Data Systems, $5M-$75M revenue tech), Capstone Partners Austin office (13284 Pond Springs Rd Ste 402; Capstone Partners absorbed Headwaters MB Jan 8 2018, itself acquired by Huntington Bancshares Jun 16 2022 — now Huntington-owned but operating as Capstone), Benchmark International Austin (2009 S Capital of Texas Hwy Ste 300, Kendall Stafford Managing Partner Global M&A Network Top 50 + Amy Alonso), Corporate Finance Associates Austin/San Antonio (Roy Graham managed since 1997 + Jim Gerberman former tech CEO), Tequity Advisors (Toronto HQ with Austin office at 111 Congress opened May 2025 led by Senior VP Erik Wayton, 114 total deals 50+ in past 5 years), and Vista Point Advisors (SF HQ founded 2011, 102 lifetime deals as of Oct 2025, founder-led SaaS sell-side only, completed Austin TX deal Aug 7 2025). Commodity-article corrections — these firms are NOT Austin-resident: Software Equity Group (San Diego HQ since 1992), Founders Advisors (Birmingham AL), Hyde Park Capital (Tampa FL), AGC Partners (Boston HQ — hosts annual Austin Software Summit but has no Austin office), Lincoln International and Stephens (no Austin M&A offices), William Blair Austin (Public Finance / muni bonds, NOT M&A). Defunct callout: Austin Ventures wound down in 2015 after failing to raise its 11th fund (was VC not M&A, but the most-commonly-cited Austin zombie firm); Capstone Partners (M&A boutique at Pond Springs Rd) is NOT the same as Capstone Capital Partners LLC (Cedar Park hard-money lender) — commodity articles regularly confuse these. The 2026 engagement-letter benchmark for a $30-80M EV Austin sell-side: $50-100K creditable retainer, 1.5-2.5% blended success fee, 12-24 month tail, $25-75K expense cap. The data room cost to bill back to your client should be $300-$450 across a 5-month process on Peony Business at $30 per admin per month, not the $15-50K Datasite passthrough that clients increasingly refuse to absorb.

Why I wrote this

I have run buy-side and sell-side diligence on hundreds of deals across founder-led sales, PE recapitalizations, strategic acquisitions, and venture-stage exits. At Peony we now serve more than 5,900 customers, and the Texas-anchored M&A cluster (Houston energy, Dallas generalist, Austin tech) is one of the densest in our 283-deal Q3 2025-Q1 2026 platform benchmark. The Tier A US M&A Mega cluster series has now shipped 18 city posts (NYC, Boston, Philadelphia, DC, Atlanta, Charlotte, Miami, Chicago, Dallas, Houston, LA, SF, Seattle, Phoenix, San Diego, Nashville, Minneapolis, Denver). Austin is the 19th — and structurally different from the prior 18.

Austin's M&A landscape is dominated by technology and SaaS to a degree that makes it look like a tech-IPO city, not a mid-market M&A city. The most-cited public 2024-2026 Austin tech outcomes are PE-software-platform consolidations or strategic acquisitions: Iodine Software (Austin healthcare AI) was acquired by Waystar (Lehi UT and Louisville KY) for $1.25 billion enterprise value 50/50 cash-stock, with sellers led by Advent International; the deal was announced July 23 2025 and closed October 1 2025. Planview (Austin, 700 employees, 3,000+ customers) was the cleanest multi-stage Austin SaaS PE-to-PE handoff: Thoma Bravo acquired Planview from Insight Venture Partners in January 2017, then TPG + TA Associates acquired Planview from Thoma Bravo for $1.6 billion in December 2020 — a ~10-year Insight hold to Thoma Bravo, then 3 years to TPG+TA. ProsperOps (Austin AI cloud-cost optimization) was acquired by Flexera in January 2026 — described as "likely a top 20 Austin venture-backed software exit of all time." Khoros (Austin customer-engagement SaaS) was acquired by IgniteTech from Vista Equity Partners on May 27 2025 — a Vista divestiture at a sub-$200M EV strategic price point, reinforcing the Vista-rarely-buys-sub-$200M frame. NaturPak (IPMF, LLC, food and CPG manufacturing) was acquired by Pritzker Private Capital in January 2026, advised by Westlake Securities as co-advisor. Freebirds World Burrito was acquired by Sun Holdings on August 14 2024 — advised by Morgan Kingston Advisors. And in semiconductors, Texas Instruments announced acquisition of Silicon Labs for $7.5 billion in February 2026 — out of the $5M-$200M EV range we're focused on here, but a powerful signal of Austin's tech-cluster depth.

The dominant structural feature of the Austin M&A market in 2026 is the role of Vista Equity Partners. Vista is headquartered at 401 Congress Ave Suite 3100 in downtown Austin with $107B+ AUM, 90+ enterprise software companies serving 450M+ users, and the eighth flagship fund closed $20B+ in 2024. But here's the data the commodity articles miss: Vista's median direct acquisition falls in the $1B-$3B band (Acumatica $2B May 2025 is representative) — Vista almost never buys directly below $200M EV. Even Vista's Foundation Fund (mid-market) and Endeavor Fund (lower-mid market) rarely reach below that threshold. For $5M-$200M EV Austin SaaS sellers, the relevant Vista activity is NOT direct Vista purchases. It is tuck-in acquisitions BY Vista's 90+ portfolio companies — Acumatica (Vista acquired at $2B in May 2025), Ping Identity, PowerSchool, Mindbody, Solera, Trintech, Cvent, and dozens of others that run regular tuck-in M&A programs at $5M-$200M EV. Vista itself cut its Austin headquarters footprint by 40% in April 2025 via a 79,500 sf sublease at The Republic per The Real Deal — a hybrid-work reshuffle, not an Austin exit, but a useful real-world data point.

This post is the working playbook I would hand to an Austin tech founder exploring an exit, an Austin healthcare or restaurant founder weighing strategic versus PE, an Austin services or industrial founder, or a PE deal partner sourcing Austin-orbit assets. The five proprietary frames (Austin SaaS Vista-Tuck-In Default, Coastal-vs-Austin False Choice, Austin Strategic Buyer Quartet, Two-Guys-With-a-Website Diagnostic, Austin Sector-Specialist Trap) come from cross-referencing the 2024-2026 Austin deal record with the city's structural specifics.

What's the Austin-metro M&A advisor landscape for $5M-$200M deals in 2026?

The 13-firm Austin-area shortlist for 2026, sorted by structural tier:

| Firm | Founded | HQ / Austin office | Sweet spot | Specialty |

|---|---|---|---|---|

| Navidar | ~2009 | 400 W 15th St, Ste 325, Austin TX 78701 | $20M-$300M EV | Tech specialist; Stephen Day ex-Goldman Sachs + Bear Stearns; 170+ principal transactions |

| Westlake Securities | 2003 | 2700 Via Fortuna, Ste 250, Austin TX 78746 | $10M-$250M EV | Generalist; tech/energy/consumer; 140+ deals; CRD 127112 |

| ScaleView Partners | 2021 | Austin | $10M-$100M EV | Pure SaaS sell-side; Wilcox/Snodgrass/Davidson; MineralSoft + Goldman DNA |

| pH Partners | 2016 | Austin HQ + Houston/Minneapolis/Portland/NYC | $20M-$150M EV | Healthcare / life sciences / medtech / HCIT; Benjamin Perkins |

| Morgan Kingston Advisors | 2018 | Austin | $5M-$150M EV | Restaurant industry only; Miller + Mirzabegian |

| Focus Strategies Investment Banking | 1999 | Austin (512-477-3280) | $20M-$200M EV | Gary Valdez; founder-owned middle market; $7B+ aggregate |

| NorthView Advisors | 2010 | Austin + Georgia/Florida/Dallas | $10M-$100M+ | Industrial/services/energy/healthcare; CRD 323786 |

| Austin Dale Group | 2003 | 905 Galahad Dr, Austin TX 78758 | $5M-$75M rev | Lower-MM tech; John W Austin + Bob Dale ex-Austin Data Systems |

| Capstone Partners Austin | 2001 (Huntington 6/16/22) | 13284 Pond Springs Rd, Ste 402, Austin TX 78729 | $30M-$200M EV | Huntington-owned generalist; EBITDA $10M+ |

| Benchmark International Austin | (national) | 2009 S Capital of Texas Hwy, Ste 300, Austin TX 78746 | sub-$50M EV typical | LMM generalist; Kendall Stafford + Amy Alonso |

| CFAW Austin/San Antonio | (CFA Worldwide affiliate) | Austin + San Antonio (Roy Graham since 1997) | $10M-$250M EV | Generalist with industrial/tech experience |

| Tequity Advisors | 2010 (Austin from 5/2025) | 111 Congress, Austin (Erik Wayton SVP) | $10M-$100M EV | B2B Enterprise Cloud/SaaS; 114 deals; FinTech/HealthTech/GovTech/AI/MSP |

| Vista Point Advisors | 2011 | SF HQ; Austin TX deal Aug 7 2025 | $30M-$250M EV | Founder-led SaaS sell-side only; 102 lifetime deals |

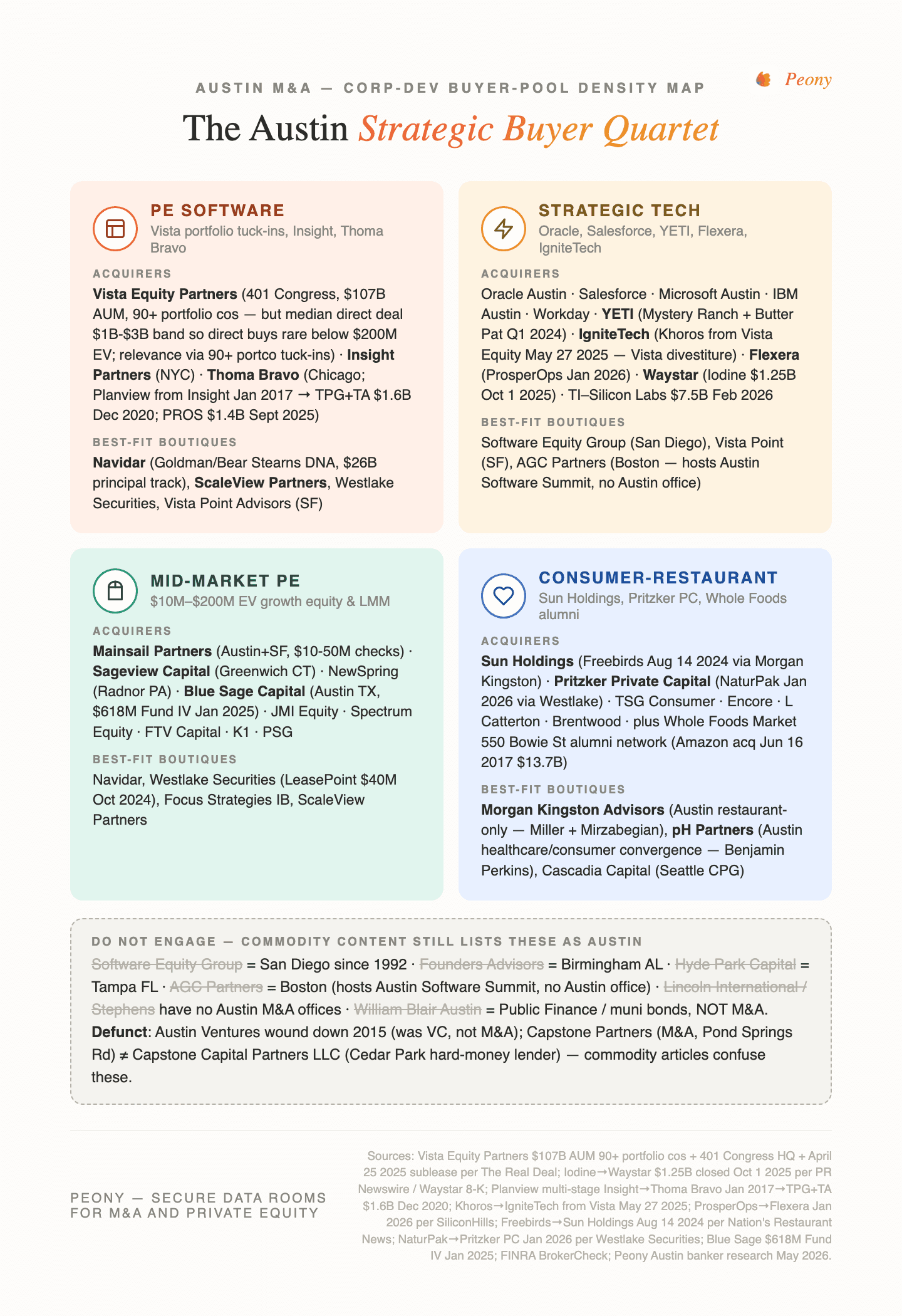

What Is the Austin Strategic Buyer Quartet and Why Does It Shape Banker Choice?

Austin has four corners of structural strategic-acquirer density that shape which boutique you should pitch first. The corner your business sits closest to should drive the shortlist, not the firm's brand recognition.

Corner 1: PE Software Platforms (Vista portfolio tuck-ins + Insight + Thoma Bravo). Vista Equity Partners is headquartered at 401 Congress Ave Suite 3100, Austin TX 78701, with $107B+ AUM, 90+ enterprise software companies, and the eighth flagship fund $20B+ closed in 2024. Vista's median direct acquisition falls in the $1B-$3B band (Acumatica $2B May 2025 is representative) — Vista almost never buys directly below $200M EV. The relevant Vista activity for $5M-$200M sellers is tuck-in acquisitions BY Vista's 90+ portfolio companies (Acumatica which Vista acquired at $2B in May 2025, Ping Identity, PowerSchool, Mindbody, Solera, Trintech, Cvent, dozens of others). Insight Partners (NYC HQ) has been the dominant Austin SaaS growth-equity buyer for over a decade — Thoma Bravo acquired Planview from Insight Venture Partners in January 2017 (a ~10-year Insight hold), then TPG + TA Associates acquired Planview from Thoma Bravo for $1.6B in December 2020. Thoma Bravo (Chicago HQ, growing Texas presence) is the most active PE software consolidator since 2020 — the multi-stage Planview chain (Insight → Thoma Bravo 2017 → TPG+TA $1.6B Dec 2020) plus the $1.4 billion PROS Holdings acquisition at $23.25/share (announced September 2025) demonstrate the cadence. For an Austin SaaS seller at $5M-$200M EV, your buyer pool runs through (a) Vista portfolio-company tuck-ins (Acumatica corp-dev, Ping corp-dev, PowerSchool corp-dev, etc.), (b) Insight Partners direct + Insight portfolio-company tuck-ins, (c) Thoma Bravo's growing Texas-focused programs, and (d) secondary PE chasers like Mainsail Partners, Sageview Capital, NewSpring Capital, Blue Sage Capital, JMI Equity, Spectrum Equity, FTV Capital, K1 Capital, Frontier Growth, Five Elms Capital, PSG Equity. The Austin-resident boutiques with the deepest PE-software-platform bench are Navidar, ScaleView Partners, Westlake Securities, and Vista Point Advisors (SF-based but with proven Austin presence).

Corner 2: Strategic Tech (Salesforce / Oracle / Microsoft / Workday / YETI / IgniteTech / Flexera). Austin's strategic-tech buyer pool benefits from Austin's status as a major secondary tech hub — Oracle's Austin campus, Microsoft Austin, IBM Austin (with deep semiconductor roots), Apple Austin, Tesla Austin (the Gigafactory plus product engineering), and Workday Austin all have local corp-dev teams that engage in Austin M&A processes. Salesforce, Atlassian, ServiceNow, Adobe, Cisco, Intuit, and Adobe maintain national corp-dev that routinely engages in Austin processes. Plus the Austin-HQ acquirers: YETI Holdings (Austin HQ, NYSE: YETI) acquired Mystery Ranch backpacks and Butter Pat Industries cookware in Q1 2024 per YETI's February 2025 SEC 8-K. IgniteTech / Crossover (Austin) acquired Khoros from Vista Equity Partners on May 27 2025 — a Vista divestiture reinforcing the Vista-rarely-buys-sub-$200M frame. Flexera acquired ProsperOps in January 2026 — "likely a top 20 Austin venture-backed software exit of all time." The Iodine Software → Waystar $1.25B deal (announced July 23 2025, closed October 1 2025) is the cleanest 2025 demonstration of strategic-tech demand for Austin AI-services assets — Waystar (Lehi UT and Louisville KY) is NOT in the PE-software-platform triangle. And Texas Instruments announced acquisition of Silicon Labs for $7.5 billion in February 2026 is the powerful semiconductor strategic-tech anchor. For deals where strategic-tech is the natural buyer, the boutiques with the deepest strategic-tech Rolodex are the SaaS-specialist coastal firms (Software Equity Group San Diego, Vista Point Advisors SF, AGC Partners Boston) plus the Austin-resident tech specialists (Navidar, ScaleView).

Corner 3: Mid-Market PE Platforms (Mainsail / Sageview / NewSpring / Blue Sage). Beyond the Vista / Insight / Thoma Bravo triangle, Austin's mid-market PE buyer ecosystem includes Mainsail Partners (Austin office + SF — bootstrapped B2B SaaS focus with $10M-$50M check sizes, 2025 invested in Steelhead Technologies ERP for metal finishing), Sageview Capital (Greenwich CT — $200M+ deployed across 4 platform deals in 2025, Austin-adjacent portfolio includes Aceable / Pax8 / CallRail), NewSpring Capital (Radnor PA), and Blue Sage Capital (Austin TX — $618M Fund IV closed January 2025 plus $287M strategic credit fund October 2025, LMM focus on environmental solutions / niche manufacturing / specialty services / $5M-$25M EBITDA / $20M-$200M revenue). These mid-market PE platforms run sub-$200M deals continuously and represent the structural alternative to the Vista-tuck-in-or-Insight-or-Thoma-Bravo default narrative. The Austin-resident boutiques with the deepest mid-market PE Rolodex are Navidar, Westlake Securities (recent LeasePoint $40M Altriarch growth capital October 16 2024 is a clean mid-market PE example), Focus Strategies, and ScaleView Partners.

Corner 4: Consumer-Restaurant (Sun Holdings / Pritzker Private Capital / Whole Foods alumni). Austin's consumer-restaurant buyer pool extends through CPG private-equity rollups (Sun Holdings — recent acquirer of Freebirds via Morgan Kingston December 2024; Pritzker Private Capital — recent acquirer of NaturPak via Westlake Securities co-advisor January 2026; TSG Consumer Partners, Encore Consumer Capital, L Catterton, Brentwood Associates) plus strategic CPG buyers (General Mills, PepsiCo, Mondelez, Kraft Heinz, Coca-Cola Beverages, Anheuser-Busch InBev, Constellation Brands) and the Whole Foods Market alumni network (Whole Foods is HQ at 550 Bowie Street, Austin since 1980, acquired by Amazon June 16 2017 for $13.7B — the founder/operator alumni network is Austin's most dense consumer-CPG talent pool). For Austin consumer / DTC / food-bev sellers in the $20M-$100M EV band, Morgan Kingston Advisors is the Austin-resident specialist for restaurants specifically (founded 2018 by Susan Miller and Sean Mirzabegian). For non-restaurant consumer, pair an Austin-resident generalist (Westlake Securities, Focus Strategies) with a coastal consumer specialist like Cascadia Capital Seattle (premier consumer-DTC specialist with strong CPG buyer Rolodex), Houlihan Lokey Consumer, or Lincoln International Consumer.

Reading the quartet: the boutique you pitch should have closed deals INTO your corner of the quartet in the last 24 months. A SaaS seller pitching only generalist boutiques without PE-software-platform deal flow is structurally underbanked; a restaurant seller pitching only generalists when Morgan Kingston exists is leaving sub-vertical sophistication on the table. The Austin Strategic Buyer Quartet is the single most important diagnostic frame I use to scope an Austin sell-side conversation.

The Austin SaaS Vista-Tuck-In Default — and why it shapes your buyer-list architecture

The commodity-article narrative on Austin SaaS M&A: "Vista Equity Partners is the default exit." That is structurally wrong at the $5M-$200M EV band. Vista's $107B AUM is real, but Vista's median direct acquisition falls in the $1B-$3B band (Acumatica $2B May 2025 is representative) and even Vista's Foundation Fund (mid-market) plus Endeavor Fund (lower-mid market) rarely reach below $200M EV. Vista almost never buys directly below $200M.

The accurate narrative: Vista is the default exit horizon for big Austin SaaS ($200M+ EV) — Acumatica at $2B in May 2025 is the cleanest 2025 example. For $5M-$200M EV sellers, Vista's relevance is through tuck-in acquisitions BY Vista portfolio companies. Vista has 90+ enterprise software companies, and most of them run regular tuck-in M&A programs at $5M-$200M EV — Acumatica corp-dev, Ping Identity corp-dev, PowerSchool corp-dev, Mindbody corp-dev, Solera corp-dev, Trintech corp-dev, Cvent corp-dev, Aptean corp-dev, and dozens more.

This nuance matters operationally for two reasons:

-

Process targeting: if you are a $30M-$80M EV Austin SaaS seller wanting a Vista-aligned outcome, your advisor's job is not to "pitch Vista" — it is to identify which Vista portfolio companies are actively running tuck-in M&A in your sub-vertical AND have budget cycle alignment with your process timeline. That requires a Rolodex into Vista portfolio company corp-dev teams, not just Vista flagship.

-

Negotiating dynamic: selling to a Vista portfolio company is materially different from selling to Vista directly. You are negotiating with the portfolio company's CEO and corp-dev, under a Vista-defined integration plan, with Vista-driven post-deal margin and synergy targets. The terms are typically tighter than a direct Vista purchase (lower rollover equity multiples for management, more aggressive synergy demands, faster integration timelines). Your advisor needs to know how to structure these portfolio-company-led deals — different from structuring direct PE-flagship deals.

Insight Partners (NYC) operates with higher direct activity at the $50M-$500M EV band — Thoma Bravo acquired Planview from Insight Venture Partners in January 2017, then TPG + TA Associates acquired Planview from Thoma Bravo for $1.6B in December 2020 — the cleanest example of the multi-stage Insight → Thoma Bravo → TPG/TA Austin SaaS PE handoff. Thoma Bravo's $1.4B PROS Holdings acquisition at $23.25/share announced September 2025 (PROS is Houston-HQ but the Texas-anchored pattern is identical) demonstrates the consolidation cadence.

The actionable read at $5M-$200M EV: your buyer pool is far broader than the Vista-narrative suggests. Your advisor's job is to widen it deliberately — strategic-tech outreach (Salesforce, Oracle, Microsoft, Workday, Atlassian, ServiceNow, IBM, Adobe, plus Austin-HQ strategics like YETI / IgniteTech / Flexera), Vista portfolio-company tuck-in identification, Insight-and-Thoma-Bravo direct, secondary PE chasers (Mainsail / Sageview / NewSpring / Blue Sage / JMI Equity / Spectrum Equity / FTV Capital / K1 Capital / Frontier Growth / Five Elms Capital / PSG Equity), and industry-vertical strategics depending on your sub-vertical. The diagnostic question for every advisor: "In the last 24 months, what fraction of your closed deals went to (a) a Vista portfolio company, Insight, or Thoma Bravo, (b) other PE platforms, (c) strategic acquirers, and (d) growth-equity / minority recap?" A healthy distribution is no single bidder type above ~40%.

The Coastal vs Austin False Choice

The dominant question Austin tech founders ask: "Should I hire an Austin advisor or fly in someone from NYC or SF?" The dominant commodity-article answer: "Austin advisors know local relationships, coastal advisors have bigger Rolodexes — it depends." That's the wrong frame.

The right frame: location is not the structural variable. Buyer-rolodex depth + sub-$100M deal staffing + sector specialization are.

Buyer-rolodex depth. Coastal SaaS specialists (Software Equity Group San Diego since 1992, Vista Point Advisors SF since 2011, AGC Partners Boston) have deeper national PE-platform and strategic-tech relationships than most Austin-resident boutiques because they have spent 10-30 years pattern-matching SaaS exits across the country. Navidar (Austin) has founder-bench credibility through Stephen Day's Goldman Sachs and Bear Stearns Technology IB background plus principal 170+ transactions totaling $26B M&A + $22B capital raising. ScaleView Partners (Austin, founded 2021) has founder-bench credibility (Wilcox sold MineralSoft to Enverus; Davidson decade at Goldman) but is a younger firm. Westlake Securities (Austin, founded 2003) has 140+ completed transactions across two decades of generalist coverage.

Sub-$100M deal staffing. Coastal firms often slum it at sub-$100M deals — meaning the firm signs the engagement but allocates VP-and-analyst staffing rather than senior MD attention. Austin-resident boutiques like Navidar, ScaleView, Westlake Securities, and Morgan Kingston typically put founding-MD attention on every deal because their cost structures require it. For deals at $30M-$80M EV, the senior-MD-attention difference often outweighs the Rolodex difference — a senior MD personally running every buyer call generates better outcomes than a deep Rolodex with junior execution.

Sector specialization. This is where coastal SaaS specialists win unambiguously for SaaS deals. SEG (San Diego, founded 1992) has 30+ years of SaaS sell-side specialization plus the deepest published industry research in SaaS investment banking. Vista Point (SF) is founder-led-SaaS-sell-side-exclusively. AGC Partners has 600+ closed tech transactions across 10 offices. If your sub-vertical is well-defined SaaS, the coastal specialist's pattern-matching saves your process meaningful time and produces a sharper CIM.

The right answer: dual-advisor model. For Austin SaaS founders at $60M-$120M EV, the structurally correct setup is one Austin-resident boutique (Navidar, ScaleView, or Westlake) plus one coastal SaaS specialist (SEG, Vista Point, or AGC). The dual-advisor model adds 50-75 basis points to total fees but provides genuine specialist Rolodex with local economics. The competitive-interview dynamic alone (forcing the two firms to compare buyer lists in pitch meetings) tends to surface buyer angles each individual firm would have missed.

For sub-$30M EV deals, single-advisor with an Austin-resident is correct. For $80M-$200M EV deals, swap the SaaS specialist for AGC Partners or a bracket-platform tech practice (Houlihan Lokey Tech, William Blair Tech — note William Blair Tech is run from Chicago / NYC / SF, not from the Austin Public Finance office, Stifel Tech).

For sector-specialized non-SaaS Austin deals (restaurant, healthcare, consumer), use the Austin sector specialist (Morgan Kingston for restaurant, pH Partners for healthcare) and pair with a coastal sector specialist only if buyer-Rolodex breadth materially expands the bid set.

The Two-Guys-With-a-Website Diagnostic

Commodity SEO articles list firms as "best Austin M&A boutiques" based on website claims, not actual deal flow. The Two-Guys-With-a-Website Diagnostic is three checkpoints — every Austin boutique you interview has to clear all three or pass.

Checkpoint 1: FINRA BrokerCheck + CRD number. Every legitimate M&A advisor in the United States that takes success fees is a FINRA-registered broker-dealer with a Central Registration Depository (CRD) number. Search the firm name at FINRA BrokerCheck — confirm active registration, review any disciplinary history, note the number of registered representatives. Westlake Securities (CRD 127112), Navidar, ScaleView Partners, NorthView Advisors (CRD 323786, member since 09/2023), and Focus Strategies all clear this gate. If a firm cannot produce a CRD when asked, they are operating as a business broker rather than an investment bank — different fee structure, different process mechanics, different buyer-pool depth.

Checkpoint 2: Verified 3+ closed deals at your size in the last 24 months. Commodity articles cite firms based on website claims. The real test is asking the firm to walk you through three named transactions in the last 24 months that match your size and sub-vertical. Westlake Securities' 140+ completed transactions including NaturPak → Pritzker Private Capital January 2026, Cadeo → Resource Innovations June 25 2024, and LeasePoint $40M growth capital October 16 2024 is the floor for an Austin generalist boutique pitching a $30M-$80M EV deal. Navidar's 170+ principal track record plus Sincere Corporation acquisition of Timehop is the comparable tech-specialist benchmark. ScaleView Partners' Solvexia → GTreasury, Harbour Software → Springbrook, and Cityspan Technologies → Gravity (all 2025) are the right-sized recent deal flow for a 5-year-old Austin tech specialist. Morgan Kingston Advisors' Freebirds World Burrito → Sun Holdings December 2024 plus Protein Bar & Kitchen → Founder's Table Restaurant Group is the restaurant-specialist benchmark. Cross-check against SEC EDGAR for any public-company filing where the firm appears as financial advisor.

Checkpoint 3: 2+ named senior MDs visibly at the Austin office in 2025-2026. The two-guys-with-a-website failure pattern is a firm with one MD doing everything plus a junior analyst. Verify two named MDs via LinkedIn with active posts geo-tagged Austin (or appearing at Austin events — Capital Factory events, Austin AI events, Austin Tech Alliance events) in the last 12 months. Navidar (Stephen B. Day plus Austin team), ScaleView Partners (Wilcox / Snodgrass / Davidson — 3 founding MDs), Westlake Securities (Wilson + Matt Andersen + multiple MDs), Focus Strategies (Gary Valdez plus senior bench), Morgan Kingston Advisors (Susan Miller + Sean Mirzabegian), pH Partners (Benjamin Perkins + partners), Benchmark International Austin (Kendall Stafford + Amy Alonso), and Corporate Finance Associates Austin/SA (Roy Graham + Jim Gerberman) all pass this gate.

If a firm passes all three gates plus produces three founder references you can call in your sub-vertical, you have a real operator. If they fail any of the three, scrutinize harder before signing the engagement letter. The cost of choosing wrong: a stalled process or a thin buyer list that costs you 1-2 turns of EV multiple — at $60M EV that is $6M-$12M of value left on the table.

The Austin Sector-Specialist Trap

For Austin SaaS founders, the Austin boutique inventory is reasonable. For Austin non-SaaS founders (restaurant, healthcare, services, consumer, energy services, industrial), the Austin sector-specialist bench is genuinely thin — but Austin has three legitimate Austin-resident sector specialists that most commodity articles miss:

-

Morgan Kingston Advisors — the only Austin-HQ restaurant-industry-only M&A specialist, founded 2018 by Susan Miller (20+ years IB) and Sean Mirzabegian (20+ years IB / PE / lending). Sectors: franchisors, franchisees, independents across casual / fast-casual / fine dining / specialty. Sweet spot: middle-market restaurant ($5M-$150M EV typical). Recent: Freebirds World Burrito → Sun Holdings December 2024 plus Protein Bar & Kitchen → Founder's Table Restaurant Group. For any Austin restaurant operator at $5M-$150M EV, Morgan Kingston is the structural right answer.

-

pH Partners — the only Austin-HQ healthcare-focused investment bank, founded 2016 by Benjamin Perkins (Managing Partner). Austin HQ plus Houston / Minneapolis / Portland / NYC offices. Sectors: Healthcare, Life Sciences, MedTech, Digital Health, HCIT, Diagnostics, Consumer convergence. Sweet spot: healthcare middle market. 18 lifetime deals with partners collectively having closed $20B+ strategic advisory + $15B+ capital raises. Recent: advised VeruStat on sale to CoachCare (remote patient monitoring). For Austin healthcare services / health-tech / medtech at $20M-$150M EV, pH Partners is the structural right answer.

-

NorthView Advisors — Austin-HQ industrial / services / energy / healthcare / oil-gas / manufacturing specialist, founded 2010. FINRA CRD 323786 member since 09/2023. Sweet spot: $10M-$100M+ transactions. For Austin industrial / manufacturing / construction services, NorthView is the right Austin-resident specialist.

Beyond these three specialists, the Austin sector-specialist trap is real:

For Austin consumer / DTC / food-bev (non-restaurant): pair an Austin-resident generalist (Westlake Securities — Pritzker Private Capital NaturPak deal demonstrates CPG buyer relationship; Focus Strategies — Gary Valdez's 24-year commercial-banking-relationship network includes CPG operators) with a coastal consumer specialist like Cascadia Capital Seattle (premier consumer-DTC specialist with strong CPG buyer Rolodex), Houlihan Lokey Consumer, or Lincoln International Consumer.

For Austin energy-services / oilfield-tech: pair an Austin-resident generalist (NorthView Advisors) with a Houston specialist like Tudor Pickering Holt Houston, Pickering Energy Partners Houston, or Petrie Partners Houston office (Petrie's HQ is Denver but the Houston office covers Permian / Eagle Ford / East-Texas energy M&A). Note: Cawley, Gillespie & Associates has an Austin office for reservoir engineering and oil & gas advisory work — useful for technical valuations and reserve reports but not a corporate M&A boutique.

For Austin industrial / manufacturing (heavy industry beyond NorthView's specialty): pair with Lincoln International Industrials, Houlihan Lokey Industrials (#1 global industrials advisor sub-$5B per Houlihan Lokey 2025 ranking), or Stout Risius Ross Industrials.

For Austin healthcare beyond pH Partners (specifically dental DSOs, urgent care, behavioral health): pair with a healthcare specialist like Cain Brothers, Coker Capital, Provident Healthcare Partners, or TripleTree Healthcare.

The Austin-resident specialist or generalist handles the local relationship and the process management; the coastal specialist brings the sub-vertical buyer Rolodex when no Austin specialist exists. Total fees are typically 50-75 bps higher than a single-advisor mandate, but the buyer-list breadth justifies the cost for any deal where the buyer pool is materially specialized.

Which 13 Austin Boutiques Should I Pitch in 2026?

The 13 verified firms below, grouped by structural tier, with confirmed 2024-2026 transactions where available. Firms with no Austin presence (Software Equity Group San Diego, Founders Advisors Birmingham AL, Hyde Park Capital Tampa FL, AGC Partners Boston, Lincoln International, Stephens) are excluded from the Austin shortlist — interview them separately as coastal specialists if relevant to your deal.

Tier 1 — Austin-resident tech specialists

1. Navidar — Austin's tech-IB with Goldman Sachs DNA

- HQ: 400 W 15th St, Ste 325, Austin TX 78701; founded ~2009

- Founding MD: Stephen B. Day — ex-Goldman Sachs and Bear Stearns Technology Investment Banking

- Additional offices: NYC, Cleveland, Dallas, Denver, Indianapolis, Minneapolis, San Antonio

- Sectors: Tech-focused — SaaS software, eCommerce, IT/engineering services, specialty manufacturing, HCIT

- Sweet spot: $20M-$300M EV

- Track record: Principals completed 170+ transactions totaling $26B M&A and $22B capital raising over 20 years

- Recent verified transactions: Advised Sincere Corporation (parent of Punchbowl, Memento) on acquisition of Timehop; advised Compliance Training Online (2024)

- Best fit: $20-300M EV tech / SaaS / eCommerce / IT-services Austin deals where Goldman / Bear Stearns DNA and deep transaction count matter

2. Westlake Securities — Austin's longest-running middle-market generalist

- HQ: 2700 Via Fortuna, Ste 250, Austin TX 78746 (per FINRA registered address)

- Founded 2003; Co-founder Wilson; CEO Matt Andersen 11+ years as CEO

- FINRA CRD 127112 — registered broker-dealer

- Sectors: Generalist with strength in tech, energy, consumer

- Sweet spot: $10M-$250M EV ("middle market companies with enterprise values of $10MM to $250MM" per firm materials)

- Track record: 140+ completed transactions, $5B+ aggregate value

- Recent verified transactions: Advised NaturPak (IPMF, LLC) on sale to Pritzker Private Capital, January 2026; advised Cadeo on acquisition by Resource Innovations (clean energy consulting), announced June 25, 2024; advised LeasePoint Funding Group on $40M growth capital from Altriarch Asset Management, October 16, 2024

- Best fit: $10-250M EV diversified middle-market deals across services, tech, software, energy services, consumer

3. ScaleView Partners — Austin's pure-SaaS sell-side specialist

- HQ: Austin; founded 2021

- Founding bench: Gabe Wilcox (ex-MineralSoft CEO sold to Enverus 2018; ex-North Bridge Growth Equity), Jay Snodgrass (ex-MineralSoft co-founder, two decades technology IB plus hedge-fund growth equity), Jordan Davidson (decade at Goldman Sachs managing investments for pension funds, family offices, endowments, foundations)

- Sectors: Pure tech/SaaS focused on founder exits

- Sweet spot: Lower-middle-market SaaS ($10M-$100M EV typical)

- Track record: 11 deals as of May 2026

- Recent verified transactions: Advised Solvexia (no-code reconciliation/regulatory reporting SaaS) on sale to GTreasury (Ripple) 2025; advised Harbour Software (meeting/agenda management SaaS for local governments) on sale to Springbrook Software (backed by Five Arrows and Accel-KKR) 2025; advised Cityspan Technologies (public-sector grants/performance management SaaS) on sale to Gravity (backed by Lead Edge Capital) 2025

- Best fit: $10-100M EV Austin SaaS deals where founder-bench credibility and partner-led process matter

Tier 2 — Austin-resident sector specialists

4. pH Partners — Austin's healthcare-focused IB

- HQ: Austin; founded 2016 by Benjamin Perkins (Managing Partner)

- Additional offices: Houston, Minneapolis, Portland, NYC

- Sectors: Healthcare, Life Sciences, MedTech, Digital Health, HCIT, Diagnostics, Consumer convergence

- Sweet spot: Healthcare middle market ($20M-$150M EV)

- Track record: 18 deals; partners collectively closed $20B+ strategic advisory + $15B+ capital raises

- Recent verified transaction: Advised VeruStat on sale to CoachCare (remote patient monitoring)

- Best fit: Austin healthcare services / health-tech / medtech / digital-health deals at $20-150M EV

5. Morgan Kingston Advisors — Austin's restaurant-industry-only M&A specialist

- HQ: Austin; founded 2018 by Susan Miller (Partner, 20+ years IB) and Sean Mirzabegian (Partner, 20+ years IB/PE/lending)

- Sector: Restaurant industry only — franchisors, franchisees, independents

- Sweet spot: Middle-market restaurant ($5M-$150M EV typical)

- Track record: 11 deals (all restaurant-vertical)

- Recent verified transactions: Advised Protein Bar & Kitchen (16-unit chain) on sale to Founder's Table Restaurant Group; advised Freebirds World Burrito on sale to Sun Holdings, December 2024

- Best fit: Austin restaurant operators at $5-150M EV — the only Austin-HQ restaurant-vertical M&A specialist

Tier 3 — Austin-resident generalist LMM

6. Focus Strategies Investment Banking — Gary Valdez's founder-owned middle-market specialist

- HQ: Austin; founded by Gary Valdez in 1999 after 24-year commercial banking career

- Phone: 512-477-3280

- Founder-owned middle-market focus; ~100+ years collective team experience

- Sectors: Generalist M&A advisory + capital raising + strategic advisory for founder-owned middle-market companies

- Track record: $7B+ in lifetime transactions, 54 deals total, 20 M&A + 7 funding rounds as of January 2026

- Recent verified transactions: Advised JKB Construction (2025); announced strategic partnership with The Stansberry Firm — rental equipment vertical add-on, October 2025

- Best fit: $20-200M EV founder-owned middle-market deals where Gary Valdez's commercial-banking-relationship network is the differentiator

7. NorthView Advisors — Austin's industrial / services LMM specialist with debt-placement bench

- HQ: Austin (also Georgia, Florida, Dallas remote offices); founded 2010

- FINRA member since 09/2023 (CRD 323786)

- Sectors: Generalist LMM with debt placement specialty — industrial, services, energy, healthcare, distributors, manufacturing, infrastructure, oil & gas, financial technology, mining

- Sweet spot: $10M-$100M+ transactions; companies with revenues $40M+

- Best fit: $10-100M EV industrial / services / energy-services / manufacturing deals where industrial sub-vertical buyer Rolodex matters

8. Austin Dale Group — Austin tech-services LMM with 20+ year track record

- HQ: 905 Galahad Dr, Austin TX 78758 (per Yelp listing)

- Founded 2003 by John W. Austin and Bob Dale (both ex-founders of Austin Data Systems, sold 2000)

- Sectors: Lower-middle-market technology — software, cloud solution providers, MSPs

- Sweet spot: $5M-$75M revenue companies

- Best fit: $5-75M revenue Austin tech-services deals below the size threshold of the SaaS specialists

Tier 4 — National platforms with verified Austin offices

9. Capstone Partners — Austin office — Huntington-owned generalist middle-market

- Austin office: 13284 Pond Springs Rd, Ste 402, Austin TX 78729

- HQ: Boston; original Capstone founded 2001; merged with Headwaters MB January 8, 2018; rebranded to Capstone Partners 2021; acquired by Huntington Bancshares (Nasdaq: HBAN) on June 15, 2022

- Sectors: Generalist middle market; EBITDA >$10M

- Sweet spot: $30M-$200M EV

- Track record: ~150 professionals across 12+ US offices; ~250+ closed transactions annually

- Best fit: $30-200M EV diversified middle-market deals where Huntington-bank-owned balance-sheet support and 12-office US footprint matter

- Caveat: Now Huntington-owned, so positioning is between "bracket platform with regional offices" and "true boutique." Worth including but note the parent.

10. Benchmark International Austin — LMM generalist with named-MD Austin staffing

- Austin office: 2009 S Capital of Texas Hwy, Ste 300, Austin TX 78746

- Managing Partner of Austin office: Kendall Stafford (named to Global M&A Network's Top 50 M&A Investment Bankers / Americas Dealmakers)

- Other Austin MDs: Amy Alonso

- Sectors: Generalist LMM

- Sweet spot: Lower middle market (typically sub-$50M EV)

- Best fit: $5-50M EV diversified Austin LMM deals where Kendall Stafford's local reputation and Benchmark's global office network matter

11. Corporate Finance Associates — Austin/San Antonio — affiliate of CFA Worldwide with 30-year Austin office

- HQ: Affiliate of CFA Worldwide (70+ year history); Austin/SA office managed by Roy Graham since 1997

- MDs: Roy Graham (managed office since 1997), Jim Gerberman (former tech CEO/President roles)

- Sectors: Generalist with industrial/tech experience

- Sweet spot: $10M-$250M EV

- Best fit: $10-250M EV diversified Austin / San Antonio deals where long-tenured local presence matters

12. Tequity Advisors — Toronto HQ with new Austin office at 111 Congress

- HQ: Toronto; Austin office at 111 Congress in downtown Austin opened May 2025 led by Erik Wayton (Senior VP, M&A Advisor)

- Sectors: B2B Enterprise Cloud, SaaS, ISVs, XaaS, MSPs across Salesforce / ServiceNow / Azure / AWS / GCP / SAP / Microsoft ecosystems; verticals include FinTech, HealthTech, GovTech, AI

- Track record: 114 deals total, 50+ in past five years

- Best fit: $10-100M EV B2B SaaS deals in the Salesforce / ServiceNow / cloud-ecosystem orbit where cross-border (Canada / US) buyer-pool reach matters

13. Vista Point Advisors — SF founder-led-SaaS sell-side specialist with active Austin coverage

- HQ: San Francisco; founded 2011

- Sweet spot: $30-250M EV founder-led businesses

- Sectors: Tech, internet & consumer services, software, SaaS, cloud-enabled services, mobile, consumer retail, healthcare

- Exclusively sell-side and capital-raising for founder-led businesses (no buy-side or general advisory)

- Track record: 102 lifetime deals as of October 2025 — 74 M&A + 28 funding rounds

- Recent: completed Austin TX deal August 7, 2025 (specific deal terms not disclosed in public sources)

- Best fit: Austin SaaS founders at $30-250M EV who value SaaS-specialist sell-side pattern matching with proven Austin engagement track record

Commodity-article corrections — firms commonly listed as "Austin boutiques" that are NOT

This is the most expensive trap in the Austin M&A advisor evaluation: commodity SEO articles list firms as "best Austin M&A boutiques" that are headquartered elsewhere with no meaningful Austin M&A presence. Founders who shortlist these firms expecting local Austin process management get coastal staffing with a stretched-Rolodex coastal pitch — at coastal fee structures.

The accurate framing: these are the national SaaS-specialist, generalist boutiques, or bracket-platform firms that you would interview alongside Austin-resident shops, not the Austin-resident shops themselves. Use them strategically (as coastal or sector specialists in a dual-advisor model) — do not mistake them for Austin local coverage.

- Software Equity Group (SEG) — San Diego HQ since 1992. 30+ years of SaaS sell-side specialization. The deepest published SaaS industry research in IB via the SEG Quarterly SaaS Reports. NOT Austin-resident; the SEG team has periodically published research on Austin SaaS trends but the firm operates from San Diego.

- Founders Advisors — Birmingham AL HQ. NOT Austin. Strong middle-market practice but Birmingham-rooted; commonly misattributed.

- Hyde Park Capital — Tampa FL HQ. NOT Austin. Florida-focused practice; commonly misattributed.

- AGC Partners — Boston HQ. 100+ professionals across Boston / Atlanta / Chicago / Dallas / LA / SF / Minneapolis / NYC / Boulder / London. NOT Austin-resident, despite hosting the annual Austin Software Summit. Technology M&A specialist with 600+ closed transactions.

- Lincoln International — Chicago HQ with 20-office global network. No Austin M&A office. Strong mid-market industrials, healthcare, consumer practice — but Austin coverage runs through Chicago / Dallas / Houston offices, not Austin.

- Stephens Inc. — Little Rock AR HQ. No Austin M&A office despite presence in Texas (Dallas and Houston offices).

- William Blair Austin — William Blair has an Austin office, but it is Public Finance / muni bonds, NOT corporate M&A. The William Blair Tech M&A practice runs from Chicago / NYC / SF. Don't pitch the Austin Public Finance office for your SaaS deal.

Defunct firms callout

Austin's M&A boutique scene is younger than Denver's or Boston's, so there is no clean "St. Charles Capital → KPMG" wind-down story. The most-cited Austin zombie is actually a VC firm, and the most-confused commodity-article pattern is the Capstone two-firm namespace collision.

- Austin Ventures wound down in 2015 — failed to raise its eleventh fund per Fortune February 20 2015. General partners split: some launched a mid-market buyout fund, others an early-stage pledge fund. The Austin Ventures website still shows existing portfolio management but the firm is no longer making new investments under that name. Was VC not M&A, but the most-commonly-cited zombie in "Austin investment ecosystem" articles. Many Austin Ventures alumni remain active across the ecosystem (Joe Aragona, etc., plus Mike Maples Jr. at Floodgate which is itself separate).

- Capstone Partners (M&A boutique) vs Capstone Capital Partners LLC (Cedar Park hard-money lender) — two distinct firms confuse Austin search rankings. The legitimate M&A boutique is Capstone Partners at 13284 Pond Springs Rd Austin (acquired by Huntington Bancshares June 15 2022 and now Huntington-owned). The other firm is Capstone Capital Partners LLC, a Cedar Park TX hard-money lender (Better Business Bureau profile), NOT an investment bank. Commodity articles conflate these. Be careful which Capstone you are pitching.

- Headwaters MB (Denver, not Austin — but the merger trail goes through Texas) — Headwaters MB merged into Capstone in January 8 2018; the combined entity (Capstone Partners) was acquired by Huntington Bancshares June 15 2022. Some old articles still list "Headwaters" as if it's an independent advisor in Texas. It is not — operates under the Capstone Partners brand inside Huntington's middle-market platform.

- Westlake Capitol Group at 1801 Lavaca St — separate entity from Westlake Securities. Some directories conflate the two. The actual investment bank is Westlake Securities, at 2700 Via Fortuna Ste 250 per FINRA. If you find Westlake at the Lavaca address, that is a different entity.

Recent verified 2024-2026 Austin tech anchors

The Austin M&A market in 2024-2026 is anchored by a small number of public-record outcomes that demonstrate the structural pattern:

- Iodine Software → Waystar, $1.25B — announced July 23, 2025; closed October 1, 2025. Austin healthcare AI sold to Waystar (Lehi UT and Louisville KY) at $1.25B enterprise value, 50/50 cash and stock consideration. Iodine equity holders led by Advent International (largest shareholder, locked up 18 months post-close with Waystar shares only). The strategic-tech outcome — Waystar is NOT in the Vista/Insight/Thoma Bravo triangle — demonstrates that broader buyer-pool processes can produce $1B+ outcomes.

- Planview multi-stage PE handoff (Insight → Thoma Bravo Jan 2017 → TPG+TA $1.6B Dec 2020) — Planview (Austin HQ, 700 employees, 3,000+ customers worldwide) was originally an Insight Venture Partners investment in the mid-2000s; Thoma Bravo acquired Planview from Insight in January 2017; TPG Capital and TA Associates then acquired Planview from Thoma Bravo for $1.6 billion in December 2020. The cleanest multi-stage PE-to-PE Austin SaaS handoff demonstrating how large Austin SaaS platforms cycle through PE consolidators over a decade.

- ProsperOps → Flexera, January 2026 — Austin AI cloud-cost optimization platform acquired by Flexera. Described as "likely a top 20 Austin venture-backed software exit of all time." Financial terms not disclosed.

- NaturPak (IPMF, LLC) → Pritzker Private Capital, January 2026 — Austin-orbit food/CPG manufacturing sold to Pritzker Private Capital. Westlake Securities served as co-advisor.

- Khoros → IgniteTech from Vista Equity Partners, May 27 2025 — Austin customer-engagement SaaS sold by Vista Equity Partners (Khoros was previously a Vista portfolio company) to IgniteTech (also Austin-based). Actively reinforces the Austin SaaS Vista-Tuck-In Default frame: Vista does NOT directly buy at sub-$200M EV — Vista was the SELLER on Khoros, with IgniteTech as the sub-$200M strategic buyer. Demonstrates Austin-to-Austin strategic activity at a Vista divestiture price point.

- Freebirds World Burrito → Sun Holdings, August 14 2024 — Austin-based fast-casual chain sold to Dallas-based Sun Holdings. Morgan Kingston Advisors advised the seller.

- Cadeo → Resource Innovations (Morgan Stanley CP portco), June 25 2024 — clean energy consulting sold to a Morgan Stanley Capital Partners portfolio company. Westlake Securities exclusive advisor.

- Solvexia → GTreasury (Ripple), 2025 — Austin no-code reconciliation/regulatory reporting SaaS sold to GTreasury. ScaleView Partners advised the seller.

- Harbour Software → Springbrook Software (backed by Five Arrows and Accel-KKR), 2025 — Austin meeting/agenda management SaaS for local governments sold to Springbrook. ScaleView Partners advised.

- Cityspan Technologies → Gravity (backed by Lead Edge Capital), 2025 — Austin public-sector grants/performance management SaaS sold to Gravity. ScaleView Partners advised.

- YETI Holdings (Austin) acquired Mystery Ranch + Butter Pat Industries, Q1 2024 — Austin consumer-products strategic (NYSE: YETI) acquired backpacks and cookware brands. Demonstrates Austin-HQ strategic-acquirer activity.

- Outdoorsy → Canadian Access (LBO), February 18, 2025 — Austin RV marketplace acquired via leveraged buyout. Different capital path than traditional M&A; demonstrates non-traditional liquidity for Austin consumer-tech.

- Workrise / RigUp — 2026 tech IPO pipeline — Austin skilled-trades workforce management (renamed back to RigUp on September 4, 2025) is on the CB Insights 2026 Tech IPO Pipeline.

- Silicon Labs → Texas Instruments, $7.5B announced February 2026 — Austin semiconductor target acquired by Texas Instruments. Out of the $5M-$200M range but a powerful signal of Austin's tech-cluster depth at the upper end.

- PROS Holdings (Houston, NOT Austin) → Thoma Bravo, $1.4B at $23.25/share announced September 2025 — important context for the Texas-anchored Thoma Bravo pattern.

Each of these outcomes had a sell-side advisor. The pattern: when the buyer is a PE software platform (Vista flagship, Insight, Thoma Bravo), the advisor is typically a coastal SaaS specialist (SEG, Vista Point, AGC) or a bracket-platform (Houlihan Lokey Tech, William Blair Tech). When the buyer is a strategic (Waystar buying Iodine, Flexera buying ProsperOps, IgniteTech buying Khoros, Sun Holdings buying Freebirds, Pritzker buying NaturPak), the advisor often draws on the Austin-resident shop's local relationships plus the coastal specialist's strategic-tech Rolodex.

Frequently asked questions

I'm a $30M ARR Austin SaaS founder — should I hire an Austin M&A boutique or fly in someone from NYC or SF for a $60M-$80M exit?

The honest answer for an Austin tech founder at $30M ARR and $60M-$120M EV target: location is not the structural variable. Buyer-rolodex depth + sub-$100M deal staffing + sector specialization are. The decision rule I use: hire whichever advisor has (a) 3+ closed deals at $40M-$120M EV in your sub-vertical (vertical SaaS, horizontal SaaS, AI infrastructure, services-with-software, etc.) in the last 24 months, (b) a named senior MD who will run every buyer call personally (not delegate to a VP after week 4), and (c) a documented buyer Rolodex that extends beyond the Vista/Insight/Thoma Bravo default narrative. For most $30M ARR Austin SaaS founders that means a two-firm interview shortlist: one Austin-resident tech boutique (Navidar — Austin-HQ at 400 W 15th St Ste 325 founded by Stephen B. Day ex-Goldman Sachs and Bear Stearns Technology IB, principals 170+ lifetime transactions totaling $26B M&A + $22B capital raising over 20 years; or ScaleView Partners — Austin founded 2021 by Gabe Wilcox who sold MineralSoft to Enverus 2018 plus Jay Snodgrass plus Jordan Davidson decade at Goldman Sachs, three verified 2025 SaaS sell-side exits including Solvexia / Harbour Software / Cityspan Technologies; or Westlake Securities — Austin since 2003 at 2700 Via Fortuna Suite 250 per FINRA CRD 127112, 140+ completed transactions including NaturPak → Pritzker Private Capital January 2026 and Cadeo → Resource Innovations June 25 2024) plus one coastal sector specialist (Vista Point Advisors — SF founded 2011, 102 lifetime deals as of October 2025 with proven Austin TX deal August 7 2025; or Software Equity Group San Diego since 1992 — the most-cited SaaS specialist nationally; or Tequity Advisors — Toronto HQ with Austin office at 111 Congress opened May 2025 led by Senior VP Erik Wayton, 114 lifetime deals 50+ in past five years). Both should pitch the same buyer list during interviews — if the Austin-resident shop and the coastal specialist converge on a similar named-buyer set, the local economics + senior-MD attention typically favor the Austin shop. If they diverge meaningfully (the coastal specialist names 8 strategic + PE buyers the Austin shop doesn't), that's the structural reason to fly in the coastal. Your advisor needs to have run more than one process where the winner was NOT one of the obvious PE platforms. For specifics on what to put in your data room when interviewing bankers, see the sell-side investment banking data room playbook and use Peony Business at $30 per admin per month instead of the $15K-$50K per-deal Datasite passthrough that traditional Austin boutiques still bill to clients.

I just got an inbound from Vista (or Insight or Thoma Bravo) — should I respond directly or hire an advisor to run a real process first?

Take the call, don't take the LOI. And separate two things in your head before you reply. First: Vista Equity Partners (Austin HQ at 401 Congress Ave Suite 3100 with $107B+ AUM, 90+ enterprise software companies, eighth flagship fund $20B+ closed in 2024) almost never buys directly below $200M EV — Vista's median direct acquisition falls in the $1B-$3B band (Acumatica $2B May 2025 is representative), and even Vista's Foundation Fund (mid-market) and Endeavor Fund (lower-mid market) rarely reach below $200M. If the Vista inbound is for a sub-$200M EV Austin SaaS company, it is almost certainly NOT Vista flagship — it is one of Vista's 90+ portfolio companies (Acumatica, Ping Identity, PowerSchool, Mindbody, Solera, Trintech, etc.) running a tuck-in acquisition program. That changes the negotiating dynamic materially — you are selling to a Vista portfolio company under a Vista-defined integration plan, not to Vista itself. Verify which entity is actually making the bid before structuring your response. Second: if the inbound is genuinely from Vista flagship (you are at $200M+ EV with high growth and strong ARR multiples), Insight Partners (NYC), or Thoma Bravo (Chicago — recently active in Texas with the multi-stage Planview handoff (Thoma Bravo acquired Planview from Insight Venture Partners in January 2017, then TPG + TA Associates acquired Planview from Thoma Bravo for $1.6B in December 2020) and the $1.4B PROS Holdings acquisition at $23.25/share announced September 2025), the right move is: take a no-commitment screening call to assess seriousness and price range, then immediately interview 2-3 sell-side advisors (1 Austin-resident tech boutique + 1 coastal SaaS specialist — see the previous question), engage the chosen advisor under a competitive-process mandate, and run a structured 8-12 buyer process that includes the inbound bidder as one of several. Vista, Insight, and Thoma Bravo are sophisticated repeat buyers — they will not be offended by a competitive process if your business is genuinely interesting. The premium from a real process versus a one-bidder negotiation is typically 15%-35% at the median for Austin SaaS in this band (the variance is wide — outliers go to 60%+). The advisors who have actually run competitive processes against these three sponsors and won are the ones to interview — ask each pitching advisor for a named reference founder they have closed against Vista / Insight / Thoma Bravo in the last 24 months. If they cannot name one, they are pitching theory not practice. Your data room is the operational backbone for the 8-12 buyer process — Peony's per-bidder watermarks, NDA-gated folder permissions, and page-level analytics are what let your advisor know within 48 hours of CIM distribution which bidders are serious versus which are window-shopping.

Why does the commodity narrative say 'Vista Equity Partners drives Austin's mid-market SaaS exits' — and is that actually true at the $5M-$200M EV band?

It's partially true at the upper end (Vista direct deals above $200M EV) and structurally false at the $5M-$200M band that most Austin founders operate in. Here's the data: Vista Equity Partners manages $107B+ AUM with 90+ enterprise software companies serving 450M+ users, and the eighth flagship fund closed $20B+ in 2024. But Vista's median direct acquisition falls in the $1B-$3B band (Acumatica $2B May 2025 is representative) — that is two orders of magnitude above the $5M-$200M EV band. Even Vista's Foundation Fund (mid-market) and Endeavor Fund (lower-mid market) rarely reach below $200M EV directly. Vista cut its Austin headquarters footprint by 40% in April 2025 via 79,500 sf sublease at The Republic per The Real Deal — a hybrid-work reshuffle, not an Austin exit, but a useful data point on the actual Vista Austin presence. So for $5M-$200M Austin SaaS sellers, the relevant Vista activity is NOT direct Vista purchases — it is tuck-in acquisitions BY Vista's 90+ portfolio companies. Acumatica (cloud ERP, Vista acquired May 2025 at $2B), Ping Identity, PowerSchool, Mindbody, Trintech, Solera, Cvent, Marketo, and dozens of others run regular tuck-in M&A programs at $5M-$200M EV. The path for an Austin sub-$200M SaaS seller looking for a Vista-aligned outcome is to be acquired by one of Vista's portfolio companies — which means your advisor needs to know which Vista portfolio companies are actively running tuck-in programs in your sub-vertical. That is a much narrower question than "sell to Vista," and the answer rotates as Vista's portfolio composition shifts. Insight Partners (NYC) operates with higher direct activity at the $50M-$500M EV band — Thoma Bravo acquired Planview from Insight Venture Partners in January 2017, then TPG + TA Associates acquired Planview from Thoma Bravo for $1.6B in December 2020 — the cleanest example of the multi-stage Insight → Thoma Bravo → TPG/TA Austin SaaS PE handoff. Thoma Bravo's $1.4B PROS Holdings acquisition at $23.25/share announced September 2025 (PROS is Houston-HQ but the Texas-anchored pattern is identical) demonstrates the consolidation cadence. The actionable read: at $5M-$200M EV, your buyer pool is far broader than the Vista narrative suggests. Your advisor's job is to widen it deliberately. For the buyer-list architecture, see the sell-side investment banking data room playbook and use page-level analytics on Peony to tell you which bidders are reading versus skimming.

Are Austin M&A boutiques actually sophisticated enough for a $60M-$80M EV deal, or do I need a coastal firm with deeper SaaS rolodex?

The Austin-resident boutique bench is genuinely thinner than NYC or SF — but the gap is overstated by commodity articles that conflate "has an Austin office" with "is Austin-resident." The actual Austin-resident boutique inventory that does $60M-$80M EV deals professionally: Navidar (Austin-HQ at 400 W 15th St Ste 325, founded by Stephen B. Day — ex-Goldman Sachs and Bear Stearns Technology Investment Banking — with principals having completed 170+ transactions totaling $26B in M&A and $22B in capital raising over 20 years; sweet spot $20M-$300M EV across SaaS software, eCommerce, IT and engineering services, specialty manufacturing, HCIT); Westlake Securities (Austin since 2003, co-founding MD Wilson plus CEO Matt Andersen 11+ years as CEO, FINRA CRD 127112, 140+ completed transactions including NaturPak → Pritzker Private Capital January 2026, Cadeo → Resource Innovations June 25 2024, LeasePoint $40M growth capital October 16 2024; sweet spot $10M-$250M EV generalist with tech/energy/consumer strength); ScaleView Partners (Austin founded 2021, founders Gabe Wilcox sold MineralSoft to Enverus 2018 plus Jay Snodgrass plus Jordan Davidson decade at Goldman Sachs, recent advised Solvexia on sale to GTreasury, advised Harbour Software on sale to Springbrook, advised Cityspan Technologies on sale to Gravity all in 2025; sweet spot $10M-$100M EV pure SaaS); and Focus Strategies Investment Banking (Austin, founded by Gary Valdez 1999 after 24-year commercial banking career, $7B+ aggregate transactions, recent JKB Construction 2025 plus The Stansberry Firm partnership for rental equipment vertical October 2025). For deals at the upper end of $60M-$120M EV where a coastal specialist's deeper Rolodex matters, you can stack the Austin-resident senior-MD attention with a coastal specialist as co-advisor — common pairings: Navidar (Austin lead + Goldman Sachs / Bear Stearns DNA + $26B + $22B principal track record) + Vista Point Advisors SF (SaaS sell-side specialist with 102 lifetime deals as of October 2025) for vertical SaaS; or Westlake Securities (Austin lead + services / industrial expertise) + a Houston specialist for energy-services M&A; or Focus Strategies (Austin lead + commercial-banking-relationships) + Houlihan Lokey Industrials or William Blair Tech for $80M-$200M EV deals where the global platform is the differentiator. The dual-advisor model adds ~50-75 basis points to total fees (typically split 60/40 in favor of the lead) but provides genuine specialist Rolodex with local economics. If you only hire one advisor and your deal is sub-$80M, the Austin-resident shops are sufficient when the founder runs an active interview process and demands documented closed-deal evidence. For sub-$30M EV deals, the Austin-resident shop alone is the clear right answer — coastal specialists structurally cannot afford to staff sub-$30M deals at the senior-MD level given their cost structures. The diagnostic to use: ask each pitching firm to name three founders they have closed for at your size in the last 24 months — and call those founders before signing the engagement letter.

How do I tell which Austin M&A advisors are real operators vs LinkedIn marketing fronts — and which ones have actually closed deals my size?

I call this the Two-Guys-With-a-Website Diagnostic, and it filters out roughly 60-70% of Austin firms that show up in commodity articles as "best Austin M&A boutiques" but have shallow recent deal flow. The diagnostic is three checkpoints — every Austin boutique you interview has to clear all three or pass. Checkpoint 1 (FINRA BrokerCheck + CRD number): every legitimate M&A advisor in the United States that takes success fees is a FINRA-registered broker-dealer with a Central Registration Depository (CRD) number. Search the firm name at FINRA BrokerCheck — confirm active registration, review any disciplinary history, note the number of registered representatives. Westlake Securities (CRD 127112), Navidar, ScaleView Partners, NorthView Advisors (CRD 323786, member since 09/2023), and Focus Strategies all clear this gate. If a firm cannot produce a CRD when asked, they are operating as a business broker rather than an investment bank — different fee structure and different deal mechanics. Checkpoint 2 (verified 3+ closed deals your size in the last 24 months): commodity articles cite firms based on website claims, not actual deal flow. The real test is asking the firm to walk you through three named transactions in the last 24 months that match your size and sub-vertical. Westlake Securities' 140+ completed transactions including Cadeo sold to Resource Innovations June 25 2024, LeasePoint $40M growth capital October 16 2024, and NaturPak sold to Pritzker Private Capital January 2026 is the floor for an Austin generalist boutique pitching a $30M-$80M EV deal. Navidar's principal track record of 170+ transactions totaling $26B M&A + $22B capital raising plus Sincere Corporation acquisition of Timehop is the comparable tech-specialist benchmark. ScaleView Partners' 11 lifetime deals as a 5-year-old firm (Solvexia, Harbour Software, Cityspan in 2025) is the right-sized track record for a younger Austin tech specialist. Cross-check against SEC EDGAR for any public-company filing where the firm appears as financial advisor. Checkpoint 3 (2+ named senior MDs visibly at the Austin office in 2025-2026): the "two guys with a website" failure pattern is a firm with one MD doing everything plus a junior analyst. Verify two named MDs via LinkedIn with active posts geo-tagged Austin (or appearing at Austin events — Capital Factory events, Austin AI events, Austin Tech Alliance events) in the last 12 months. Navidar (Stephen B. Day plus full Austin team), ScaleView Partners (Wilcox / Snodgrass / Davidson — 3 founding MDs), Westlake Securities (Wilson + Matt Andersen + multiple MDs), Focus Strategies (Gary Valdez plus senior bench), Morgan Kingston Advisors (Susan Miller and Sean Mirzabegian), and pH Partners (Benjamin Perkins plus partners) all pass this gate. If a firm passes all three gates plus produces three founder references you can call in your sub-vertical, you have a real operator. If they fail any of the three, scrutinize harder before signing the engagement letter. The cost of choosing wrong: a stalled process or a thin buyer list that costs you 1-2 turns of EV multiple — at $60M EV that is $6M-$12M of value left on the table.

I'm running a $40M Austin restaurant, healthcare, or consumer business — which Austin boutiques actually fit my deal type?

The Austin Sector-Specialist Trap is real for non-SaaS founders. Austin's boutique inventory is genuinely tech-heavy, but Austin has three legitimate Austin-resident sector specialists for non-SaaS deals: (1) Morgan Kingston Advisors — the only Austin-HQ restaurant-industry-only M&A specialist, founded 2018 by Susan Miller (20+ years IB) and Sean Mirzabegian (20+ years IB/PE/lending), recent advised Protein Bar & Kitchen on sale to Founder's Table Restaurant Group plus Freebirds World Burrito on sale to Sun Holdings August 14 2024; 11 lifetime deals all restaurant-vertical. For any Austin restaurant operator at $5M-$150M EV, Morgan Kingston is the structural right answer. (2) pH Partners — the only Austin-HQ healthcare-focused investment bank, founded 2016 by Benjamin Perkins (Managing Partner), Austin HQ plus Houston / Minneapolis / Portland / NYC offices, sectors: Healthcare, Life Sciences, MedTech, Digital Health, HCIT, Diagnostics, Consumer convergence; 18 lifetime deals with partners collectively having closed $20B+ strategic advisory + $15B+ capital raises; recent advised VeruStat on sale to CoachCare (remote patient monitoring). For Austin healthcare services / health-tech / medtech at $20M-$150M EV, pH Partners is the structural right answer. (3) For Austin consumer / DTC / food-bev — particularly anything with Whole Foods Market alumni network roots (Whole Foods is Austin-HQ at 550 Bowie Street since 1980, acquired by Amazon June 16 2017 for $13.7B — the Whole Foods founder/operator alumni network is Austin's most dense consumer-CPG talent pool): pair an Austin-resident generalist (Westlake Securities, Focus Strategies) with a coastal consumer specialist like Cascadia Capital Seattle (premier consumer-DTC specialist with strong CPG buyer Rolodex), Houlihan Lokey Consumer, or Lincoln International Consumer. For Austin industrial / manufacturing / construction services: NorthView Advisors (Austin since 2010, FINRA CRD 323786 member since 09/2023, industrial / services / energy / healthcare / oil-gas / manufacturing focus) is the right Austin-resident specialist. For Austin energy-services / oilfield-tech: pair an Austin-resident generalist with a Houston specialist like Tudor Pickering Holt, Pickering Energy Partners, or Petrie Partners Houston office. The Austin-resident specialist or generalist handles the local relationship; the coastal or Houston specialist brings the sub-vertical buyer Rolodex when no Austin specialist exists. Total fees are typically 50-75 bps higher than a single-advisor mandate, but the buyer-list breadth justifies the cost for any deal where the buyer pool is materially non-tech. The diagnostic question to ask every Austin generalist pitching your non-tech deal: "Walk me through three closed transactions in my sub-vertical in the last 24 months, naming the buyer and the seller." If they cannot, the dual-advisor model is your right answer.

How long does a sell-side process actually take for a $30M-$50M revenue Austin tech company, and how do I run it without my employees finding out?

Plan for an 8-12 month process from engagement letter to close — 4-5 months from kickoff to LOI signing plus 4-6 months from LOI to close. The Austin SaaS sell-side timeline runs slightly tighter than the national M&A median for two structural reasons: (a) the Vista-portfolio-tuck-in plus Insight plus Thoma Bravo PE-software-platform buyer pool runs faster diligence than most strategic buyers — they have repeated process and pre-built diligence templates, and (b) Austin-resident boutiques tend to run leaner processes with fewer formal steps than the bulge-bracket. For confidentiality discipline, the operational frame I use comes from running deals where any leak would have cost the seller 1-2 turns of multiple: discipline is a function of access architecture, not a function of trust. The architecture: (1) Day 0 — only you, your co-founder, your CFO, and your outside counsel know. Board notification happens via secure board portal with a single explicit agenda line ("Process exploration discussion — please join"). No email, no Slack, no text. (2) Engagement letter signing — your law firm holds the master execution copy; you and your counterparty sign on a docusigned cover page that doesn't preview the engagement scope to anyone who doesn't already know. (3) Data room build (weeks 1-3) — you build the room yourself or with your CFO + outside counsel only. No internal team involvement until absolutely necessary (typically not until the LOI phase, weeks 14-16). Use a platform with page-level analytics so you can see which internal team members are reading which folders if you have to grant any internal access. (4) CIM drafting (weeks 2-6) — your advisor drafts the CIM, you review under attorney-client privilege via your outside counsel. No CIM circulation internally. (5) Teaser distribution + NDA collection (weeks 6-8) — typically 50-100 buyer names on the teaser, narrowed to 25-50 NDA-signed bidders. The teaser is anonymous (or thinly anonymized) so even if a buyer's bizdev team gossips, your identity isn't immediately recoverable. (6) IOI round (weeks 9-12) — IOI bidders see the CIM and Tier-A data room. By this point your competitors may have signed NDAs and seen your teaser, but you should not have given specific identifying detail to any party that hasn't signed an NDA and committed to process discipline. (7) Management presentations + site visits (weeks 12-16) — this is where employee discovery risk peaks. Schedule management presentations off-site (at your advisor's office, at a hotel suite, at a private club) — NOT at your headquarters. Site visits should be after-hours or weekends; framed to internal team as "investor due diligence on Q3 fundraise" if you must explain at all. (8) LOI signing + exclusivity (weeks 16-18) — you can now tell your executive team (under NDA + retention conversation) and your board (if not already involved). (9) Confirmatory diligence + SPA negotiation (weeks 18-32) — the broader exec team and key technical leads enter the data room under explicit retention conversations. Customer reference calls happen in the last 4-6 weeks before close, ideally framed as "customer-success expansion conversations" until the buyer's name has to be disclosed. (10) Signing + announcement (week 32-36) — coordinated internal + customer + employee announcement on signing day. The data room is the operational backbone of every confidentiality discipline above — Peony's NDA gates, per-bidder dynamic watermarks, and screenshot protection on the Business plan ($30/admin/month) are what let your advisor manage 25-50 NDA-signed bidders without one of them turning around and emailing your CFO's email to a competitor's bizdev team. For the underlying mechanical sequence, see the sell-side investment banking data room playbook and how to convert a pitch deck into a sell-side data room.

Software Equity Group vs Vista Point vs AGC Partners vs Capstone — which tech-specialist boutique is right for my Austin SaaS exit?

First, a commodity-article correction every Austin founder needs to hear: Software Equity Group is San Diego (NOT Austin), Founders Advisors is Birmingham AL (NOT Austin), AGC Partners is Boston (NOT Austin — AGC has Boston / Atlanta / Chicago / Dallas / LA / SF / Minneapolis / NYC / Boulder / London offices but no Austin office, despite hosting the annual Austin Software Summit), and Hyde Park Capital is Tampa FL (NOT Austin). Capstone Partners has a verified Austin office at 13284 Pond Springs Rd Suite 402 Austin TX 78729, but Capstone was acquired by Huntington Bancshares on June 15 2022 so it now operates as a regional-bank-owned subsidiary rather than a true independent boutique. Every commodity "best Austin M&A boutiques" article that lists the first four firms as Austin-resident is misattributing them. The accurate framing: these are the national SaaS-specialist boutiques that you would interview alongside Austin-resident shops (Navidar, Westlake, ScaleView). Now to the head-to-head selection: Software Equity Group (San Diego HQ, founded 1992, 30+ years of SaaS sell-side specialization, deepest published industry research in the SaaS-IB world via the SEG Quarterly SaaS Reports) is the right pick for vertical SaaS at $30M-$120M EV where the public-comp benchmark research moves the bid price and where the founder values the most institutional SaaS-specialist process. Vista Point Advisors (SF HQ, founded 2011, 102 lifetime deals as of October 2025 with 74 M&A + 28 funding rounds, founder-led-businesses-exclusively, recent August 7 2025 Austin TX deal confirmed) is the right pick for founder-led SaaS where you specifically want founder-bench bankers running every call. AGC Partners (Boston HQ, technology M&A specialist, 100+ professionals across 10 offices, 600+ closed transactions per firm materials) is the right pick for upper-mid-market $80M-$400M EV tech deals where the global office footprint and bracket-bracket-adjacent platform matter — AGC hosts the annual Austin Software Summit so the firm has real Austin SaaS-CEO relationships even without an Austin office. Capstone Partners (Boston HQ with Huntington Bancshares ownership since June 15 2022, ~150 professionals across 12+ US offices including the Austin office at Pond Springs Rd, ~250+ closed transactions annually, parent absorbed Headwaters MB January 8 2018 prior to the Huntington acquisition) is the right pick for diversified middle-market $30M-$200M EV deals across tech, services, industrial, healthcare — Capstone is genuinely generalist and runs more diversified mandates than the SaaS specialists, with the Huntington-bank ownership now providing balance-sheet support that pure-play boutiques can't match. The selection rule I use for Austin SaaS founders at $60M-$120M EV: interview SEG + Vista Point + one Austin-resident boutique (Navidar, ScaleView, or Westlake). If you are at $40M-$80M EV and your sub-vertical is well-defined (vertical SaaS, AI infrastructure, vertical services-with-software), SEG + Vista Point + Navidar (Goldman Sachs / Bear Stearns DNA + 170+ principal transactions) is the strongest three-way bake-off. If you are at $80M-$200M EV and want broader platform reach, swap one of the SaaS specialists for AGC Partners or Capstone Partners (Huntington-owned). The "two coastal SaaS specialists + one Austin-resident" bake-off has produced the most consistent 1.5-2 turn multiple uplift in our customer interviews — versus a single-advisor mandate, the competitive interview dynamic alone tends to surface buyer angles each individual firm would have missed.

What's a typical M&A success fee for a $60M-$100M Austin SaaS deal in 2026, and what's the all-in cost including QofE, legal, and tax?