10 Best M&A Advisors in Salt Lake City for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

10 Best M&A Advisors in Salt Lake City for $5M-$300M Deals (2026)

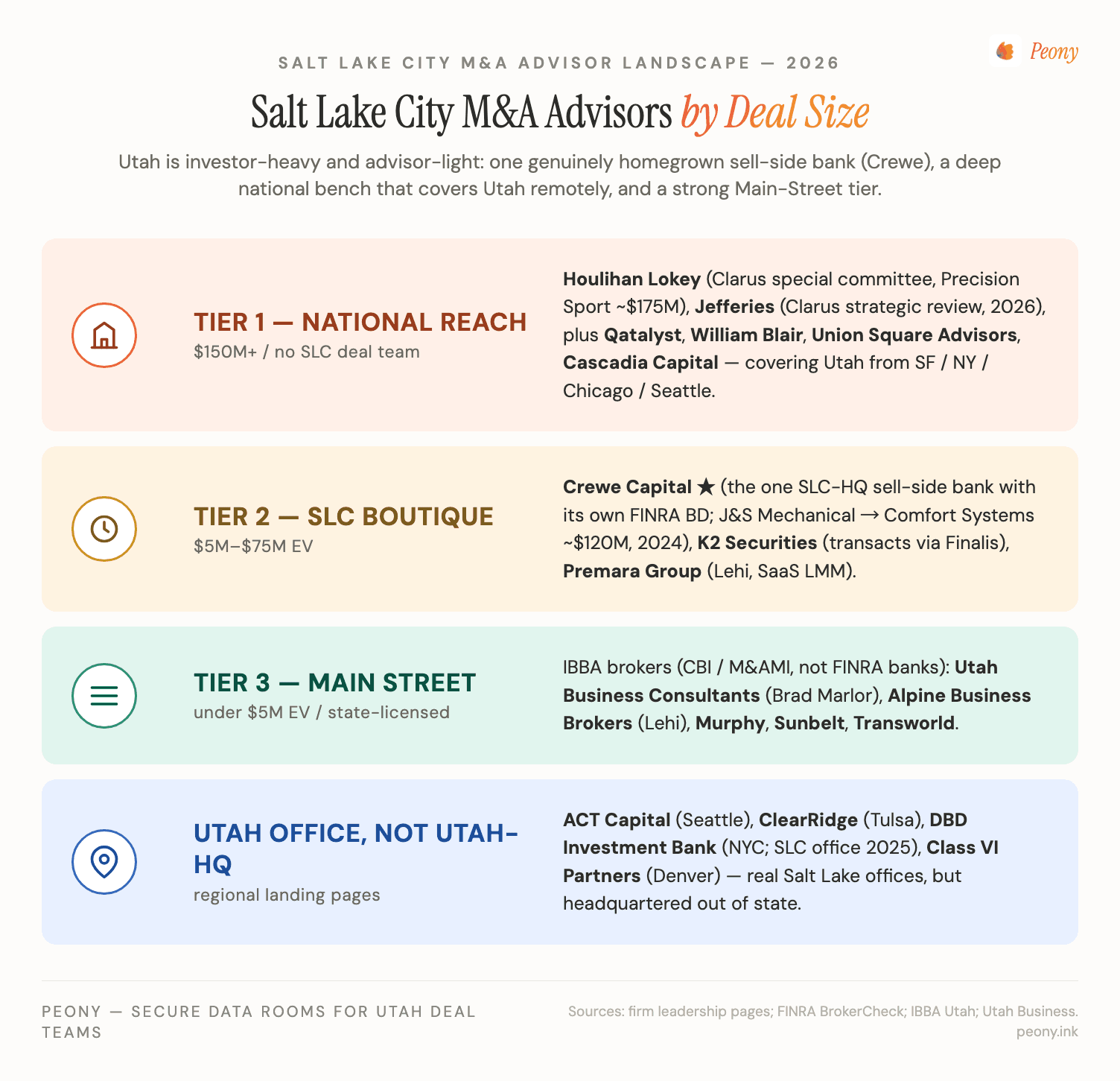

Quick answer: After sitting on the document side of enough Utah sell-side processes, here is the 10-firm Salt Lake City shortlist for 2026 — and the honest framing most lists bury. The Wasatch Front is investor-heavy and advisor-light. The capital ecosystem (Pelion raised a $500M fund in January 2025, Utah's largest (Bloomberg, Jan 2025)), and the strategic-acquirer density are world-class — but the genuinely local, FINRA-tied sell-side bench is thin. Crewe Capital (SLC, FINRA CRD #152527) is essentially the only Salt Lake-headquartered firm with its own broker-dealer and verifiable 2024-2026 sell-side closings. Backing it: hosted-broker-dealer Silicon Slopes boutiques K2 Securities and Premara Group (Lehi). The banks that win Utah's biggest deals — Houlihan Lokey (Clarus Precision Sport ~$175M, closed Feb 29, 2024 (GlobeNewswire, Feb 2024)) and Jefferies (Clarus's 2026 strategic review) — execute from out of state with no deal-running SLC office. And a sub-bucket of regional firms (ACT Capital, ClearRidge, DBD, Class VI) keep a Utah office but are headquartered elsewhere. The signature frame below — the Utah Tech-Exit Engine — explains how ~$20B+ of take-private value into Utah tech in an 18-month 2023-2024 window (Qualtrics ~$12.5B (Qualtrics IR, Jun 2023); Instructure ~$4.8B (Instructure PR, Nov 2024); Vivint ~$2.8B) plus in-state consolidator density shapes which advisor wins which deal.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led SaaS exits, PE recapitalizations, strategic carve-outs, and venture-stage sales — and Salt Lake City is the entry in our M&A advisor series where the honest story and the directory-page story diverge the most. Most "best Salt Lake City M&A advisors" pages are interchangeable, and a surprising number are out-of-state shops running a local landing page. At Peony we now serve more than 6,800 customers, and the Wasatch Front sits right in the heart of the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark.

Here is the thesis I want you to internalize before you read another word: Utah is investor-heavy and advisor-light. That sounds counterintuitive for one of the country's hottest startup economies, so let me be precise about what I mean. The capital side of Utah's deal ecosystem is genuinely elite — Pelion, Sorenson, Mercato, Tower Arch, Kickstart, Album, and Signal Peak are real, well-known funds, and a dense set of acquisitive in-state public companies (Extra Space, Merit Medical, Health Catalyst, Recursion, USANA, Myriad, Weave) keep buying. But those are investors and buyers, not sell-side advisors. The genuinely local M&A advisory bench — a firm headquartered in Salt Lake or Lehi, with its own FINRA broker-dealer, that runs competitive sell-side auctions — is remarkably thin. By my read, it is essentially one firm: Crewe Capital. Two more credible Silicon Slopes boutiques (K2 Securities, Premara Group) exist, but they transact through a hosted broker-dealer rather than their own. And the elite banks that win Utah's biggest deals run those processes from San Francisco, New York, Chicago, and Seattle — none keeps a deal-executing investment-banking office in Utah.

This post is the working playbook I would hand to a Silicon Slopes SaaS founder weighing a sale, a South Jordan medtech operator fielding inbound interest, an outdoor or consumer-products owner in the Black Diamond orbit, an aerospace-defense supplier near Hill AFB, or a private-equity partner sourcing Utah carve-outs. The frames — the Tech-Exit Engine, the Strategic-Acquirer Density Map, the Real-Local-Bank-Is-One-Firm reality, the Silicon-Slopes Confidentiality problem, and the investors-vs-advisors sorting test — come from cross-referencing the verified 2023-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist, because on this city the honesty is the differentiation.

Who are the best M&A advisors in Salt Lake City right now for $5M-$300M deals?

The Salt Lake-metro shortlist for 2026, sorted by tier and deal-size band — with the honesty banner up front: the genuinely homegrown SLC sell-side bench is effectively one firm (Crewe Capital) plus two hosted-broker-dealer boutiques.

| Firm | HQ / Utah presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| Houlihan Lokey | Los Angeles HQ (no deal-running SLC office) | $100M-$1B+ EV | Special-committee, contested & restructuring-adjacent sell-sides | Established FINRA broker-dealer |

| Jefferies | New York HQ (no SLC office) | $150M-$1B+ EV | Strategic-alternatives / public-company sale processes | Established FINRA broker-dealer |

| Crewe Capital ★ (anchor) | Salt Lake City — the one homegrown SLC bank | $5M-$150M EV | Middle-market sell-side to strategic buyers | Own FINRA broker-dealer (CRD #152527) |

| K2 Securities | Salt Lake City (founded 2002) | $25M-$75M EV | SaaS/technology sell-side | Transacts via Finalis Securities (not its own BD) |

| Premara Group | Lehi, UT | $5M-$25M EV | Lower-middle-market SaaS / consumer / B2B-services | No BD affiliation disclosed — profile/pedigree only |

| ACT Capital Advisors | Seattle (Bellevue) HQ — SLC office | $5M-$75M EV | Lower-middle-market generalist | Not confirmed as a FINRA BD this pass |

| ClearRidge Capital | Tulsa, OK HQ — SLC office | $5M-$75M EV | Middle-market generalist | Not confirmed as a FINRA BD this pass |

| DBD Investment Bank | New York HQ — SLC office (~May 2025) | $10M-$150M EV | TMT and middle-market sell-side | Not confirmed as a FINRA BD this pass |

| Class VI Partners | Denver, CO HQ — markets to SLC | $5M-$100M+ EV | Founder/entrepreneur sell-side | Affiliated BD Class VI Securities (FINRA #148772) |

| Utah Business Consultants | South Jordan, UT (founded 1989) | Under $5M EV | Main-Street → lower-middle-market business brokerage | State-licensed business broker (not a FINRA BD) |

A few notes the table cannot carry. Crewe Capital is the headline — the single clearest sell-side investment bank actually headquartered in Salt Lake City, and the reason a Utah seller is not automatically forced to ship the mandate to the coasts. Houlihan Lokey and Jefferies are the national banks with verified 2024-2026 Utah mandates, but both ran those deals from out of state — there is no deal-executing investment-banking office of either in Utah. The four firms in the regional sub-bucket (ACT Capital, ClearRidge, DBD, Class VI) keep a Salt Lake office but are headquartered in Seattle, Tulsa, New York, and Denver respectively — I label them honestly rather than passing them off as homegrown boutiques. And a critical honesty point on the famous national-bank names you will see with Utah addresses: Goldman Sachs, Piper Sandler, Stifel, Raymond James, and Baird all have a Utah presence, but none of those is a corporate-M&A deal team — Goldman's is an operations and technology campus, Piper's is public finance, and the rest are wealth management. Their sell-side work, when it happens, runs from coastal and institutional hubs. The Tier 3 firms below the table are business brokers, not FINRA-registered investment banks — the right call for genuinely Main-Street businesses under ~$5M.

Is there actually a homegrown Salt Lake City sell-side investment bank?

Yes — but essentially only one: Crewe Capital, headquartered in Salt Lake City, is the lone firm that cleanly meets all three tests of a genuine local sell-side bank — SLC headquarters, its own FINRA broker-dealer, and verifiable recent sell-side deals. This is the single most important structural fact about the Salt Lake market, and it is easy to miss because Utah's capital ecosystem is so deep that people assume the advisory bench must be equally deep. It is not.

Crewe Capital, LLC (650 S Main St, Ste 777, Salt Lake City) is registered with FINRA as its own broker-dealer — CRD #152527, SEC# 8-68460, member FINRA/SIPC, founded 2011 — which you can verify on BrokerCheck. It runs middle-market sell-side processes to strategic buyers, and what makes it credible is not the brochure — it is the recent, named, in-band closings. Crewe advised J&S Mechanical Contractors on its ~$120M sale to Comfort Systems USA (NYSE: FIX), closed February 1, 2024 (~$100M cash plus seller notes and an earn-out), with Crewe on the sell side (Comfort Systems IR; Utah Business, Feb 2024). It also advised Aero-mark, LLC on the sale of Certified Aviation Services, announced July 8, 2024 (BusinessWire, Jul 2024). Leadership includes Managing Partner Michael Bennett, MD Ken Timbers, and registered broker Luther Eston Woodard III; Nick Jones (ex-Houlihan Lokey, Piper Sandler, Citi) joined in November 2024.

One name-trap worth flagging, because it circulates: Crewe Capital (the investment bank) is a different entity from Crewe Advisors, LLC (a separate Salt Lake wealth-management RIA, ~$3.3B AUM, founded 2015 by Ryan Halliday). The June 2026 WPCG/HGGC minority-investment deal belongs to the wealth RIA, not the bank — do not attribute it to Crewe Capital. And the September 2025 Tagg-N-Go transaction Crewe arranged was a debt/financing package from Andover Lending, not an M&A sale — so do not count it as a sell-side closing either.

The contrast that matters: when you see "Goldman Sachs," "Piper Sandler," "Stifel," "Raymond James," or "Baird" with a Utah address, that is almost always not a corporate-M&A deal team. Goldman Sachs employs ~3,000 in Utah (Salt Lake Tribune, May 2025), but that is an operations and technology campus, not an investment-banking dealmaking franchise; Piper Sandler's SLC office is public finance; and Stifel, Raymond James, and Baird run wealth-management branches. Those are real firms — but their sell-side mandates run from coastal and institutional hubs, not from the local Utah office. The practical implication: for a sub-$150M Utah company you have a genuine local choice in Crewe (plus the boutiques below), and you only need to reach for a coastal firm when the deal is large, cross-border, or in a sector that needs a specialist desk. The upstream version of that decision lives in our M&A advisor vs business broker vs investment bank guide.

Which national tech and medtech banks cover Utah deals?

The national banks that win Utah's largest and most specialized deals cover the state remotely — none runs a deal-executing investment-banking office in Salt Lake or Lehi — and only two of them, Houlihan Lokey and Jefferies, have a verified 2024-2026 Utah sell-side mandate to point to. The rest are credible by footprint and sector reach, not by a named local deal, and you should treat that distinction honestly when a banker pitches you.

The two with verified Utah mandates:

- Houlihan Lokey (Los Angeles HQ) is the #1 global M&A advisor by deal count, with a deep tech bench after its 2021 acquisition of GCA Corporation (~$599.1M, completed October 4, 2021 (HL newsroom)). Its verified Utah work: it advised the Clarus Corporation special committee on the ~$175M sale of the Precision Sport segment — the ammunition business, Sierra Bullets plus Barnes Bullets — to Bullseye Acquisitions, an affiliate of JDH Capital, closed February 29, 2024 (GlobeNewswire, Feb 2024). That special-committee, contested-situation lane is exactly what Houlihan Lokey is built for.

- Jefferies (New York HQ) is a full-service investment bank across mid- to large-cap tech, medtech, and consumer. Its verified Utah work: it was retained as financial advisor on Clarus Corporation's strategic-alternatives review, announced May 2026 (an open process with no timetable) (Shop-Eat-Surf, May 2026).

The credible-by-footprint bench (real coverage, no named 2024-2026 Utah mandate — so judge them on sector reach and team, not a local closing):

- Qatalyst Partners (San Francisco and London only) is the premier brand for $1B+ independent tech sell-sides. For a sub-$150M Silicon Slopes SaaS company it is almost always too big.

- William Blair & Company (Chicago HQ; nearest western office Denver) is an employee-owned middle-market bank with a strong tech, SaaS, HCIT, and medtech practice — the natural national choice for a $150M+ Utah software or medtech process.

- Union Square Advisors (San Francisco and New York; FINRA member, CRD #141254, founded 2007) is a technology-focused M&A boutique covering enterprise software, fintech, healthtech, AI/ML, and cybersecurity.

- Cascadia Capital (Seattle HQ) is an independent middle-market bank covering the Mountain West remotely across tech, consumer, healthcare, and industrials.

For deal context only — never as a Utah franchise — Goldman Sachs and Morgan Stanley advised on the Qualtrics take-private (see the Tech-Exit Engine section), and Allen & Company and Centerview Partners advised on the Recursion-Exscientia merger. None of those four runs a Utah office. The honest read for a Silicon Slopes founder: at $25M-$75M, none of these national banks will staff your deal with its A-team, which is exactly when a local boutique competes on attention and fee; at $150M+, their sector benches and capital-markets reach start to earn the higher cost.

Does Goldman Sachs run M&A out of its Salt Lake City office?

No — Goldman Sachs's large Salt Lake City presence is an operations and technology campus, not an investment-banking dealmaking office, and its Utah-relevant M&A work is executed from New York and other institutional hubs. This is one of the most common misreads of the Salt Lake market, precisely because Goldman's Utah footprint is so visible: the firm employs roughly 3,000 people in Utah and has been relocating more staff to Salt Lake (Salt Lake Tribune, May 2025), making it one of Goldman's largest North American offices. But headcount is not the same as a deal team.

The distinction matters for how you read Goldman's Utah deal involvement. Goldman did advise on Utah's marquee transaction — it advised the Qualtrics independent-directors committee on the ~$12.5B Silver Lake / CPP take-private (completed June 28, 2023) — but that mandate was run by Goldman's investment-banking professionals, not by the Salt Lake operations campus. Separately, Goldman acted as one of about eleven financing advisors to the buyer on the $6.75B Qualtrics / Press Ganey Forsta deal — a buy-side financing role, not a Utah sell-side mandate. The takeaway for a Utah seller: do not assume that because Goldman has thousands of employees down the street, you can walk into a local Goldman M&A office and hire a sell-side team. You cannot. The same is true of the other big national-bank brands with Utah addresses (Piper Sandler's public-finance office, the wealth-management branches of Stifel, Raymond James, and Baird) — visible presence, not local dealmaking. For the actual local choice, you are back to Crewe and the Silicon Slopes boutiques, scaling up to the coastal banks for the largest deals.

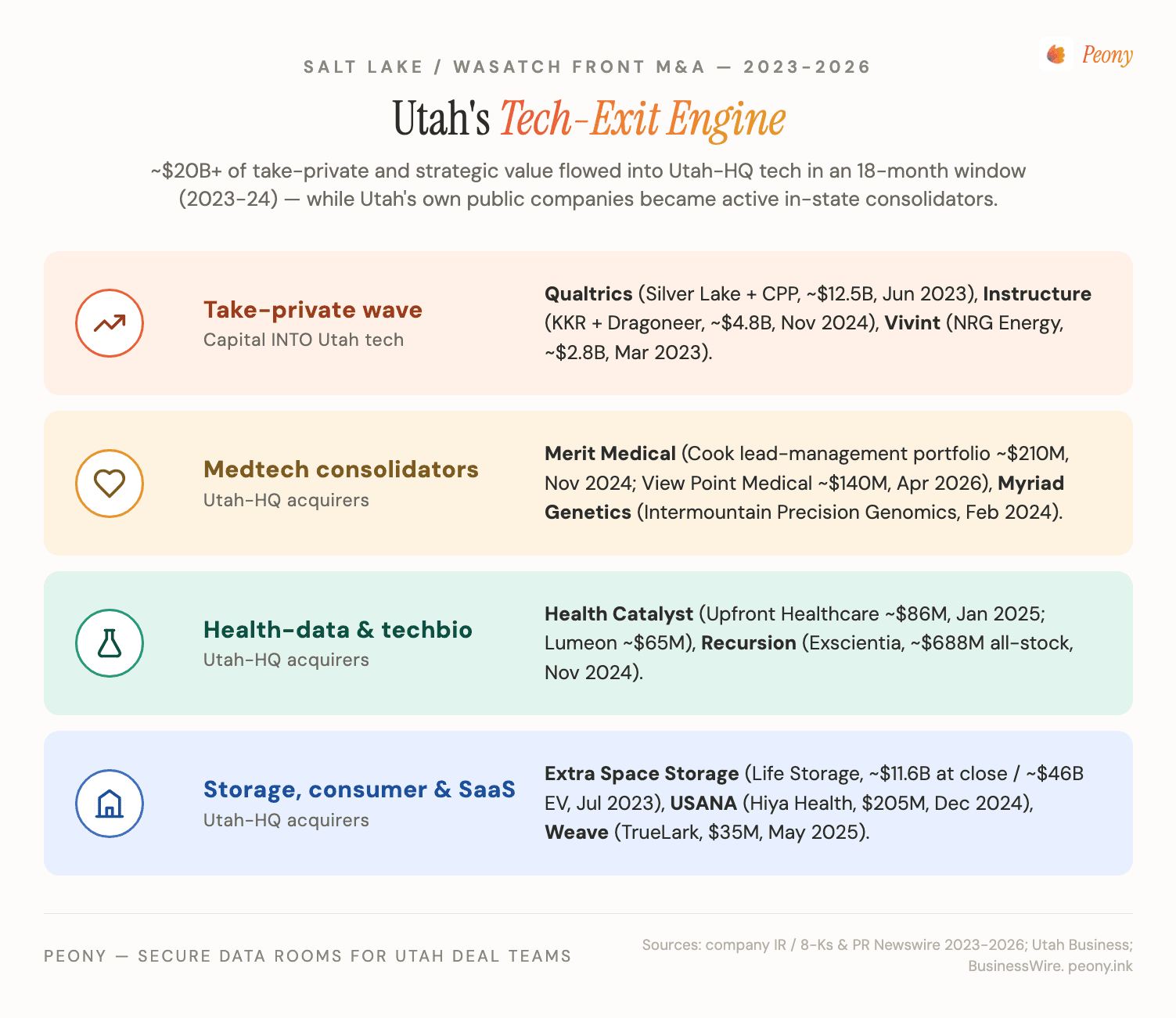

What's the Utah "Tech-Exit Engine," and what did it actually return?

The Utah "Tech-Exit Engine" is the wave of large-cap take-private and strategic capital that has flowed into Utah-headquartered tech — roughly $20B+ of completed take-private and strategic value in an ~18-month 2023-2024 window — and it is what gives Utah's advisory community (and a data room built for M&A processes) so much to work with downstream. I build the headline from confirmed deal values rather than a VC aggregate, because the verifiable Utah-wide venture figures only run through 2021. Three deals carry most of the weight:

- Qualtrics (Provo) — ~$12.5B all-cash. Silver Lake plus CPP Investments at $18.15/share; announced March 12, 2023, closed June 28, 2023, taking 100% from SAP. Goldman Sachs advised the independent-directors committee; Morgan Stanley advised the company (Qualtrics IR, Jun 2023).

- Instructure / Canvas (SLC) — ~$4.8B all-cash. KKR (with Dragoneer) at $23.60/share; announced July 25, 2024, closed November 13, 2024, buying out Thoma Bravo and delisting from the NYSE (Instructure PR, Nov 2024).

- Vivint Smart Home (Provo) — ~$2.8B cash / ~$5.2B EV. NRG Energy at $12/share plus ~$2.4B assumed debt (~33% premium); announced December 2022, closed March 2023 (NRG IR).

The national PE and strategic appetite is broad — Silver Lake and CPP, KKR and Dragoneer, NRG Energy — and the corridor that produced these companies keeps producing: Silicon Slopes (Lehi-Draper-Provo) generates $30B+ in annual economic impact (CNBC, Dec 2024), with Adobe anchoring Lehi. One honest counter-example to keep the frame credible: Pluralsight (Draper/Farmington) is not part of this engine — Vista Equity's $3.5B LBO failed, Vista wrote off its entire equity by May 2024, a Blue Owl-led private-credit group took ownership via a debt-for-equity swap, and the HQ moved to Texas. That is a leverage and restructuring cautionary tale, not proof of acquisition appetite. The signature point for advisor selection: this much capital chasing Utah tech means a Utah seller can run a serious buyer process — but the elite advisors who run the biggest of those processes do it from out of state, which is the whole tension of this post.

Which Utah companies are the active in-state strategic acquirers?

A dense set of Utah-headquartered public companies are active in-state strategic buyers — and that density is the structural advantage a good local advisor exploits, because so many credible acquirers are headquartered within an hour of the seller. These companies are buyers and targets, never advisors — none belongs on an advisor shortlist — but their deal flow is what feeds the local advisory community. The verified 2023-2026 record:

- Extra Space Storage (SLC REIT) absorbed Life Storage — ~$11.6B all-stock at close (announced at ~$12.7B; the stock fell between signing and close), creating a ~$46B-EV REIT of 3,500+ stores; closed July 20, 2023 (PR Newswire, Jul 2023).

- Merit Medical Systems (South Jordan medtech, MMSI) is a serial tuck-in buyer: EndoGastric Solutions ~$105M (announced July 1, 2024), the Cook Medical lead-management portfolio ~$210M (closed November 1, 2024 (GlobeNewswire, Nov 2024)), and View Point Medical ~$140M (oncology imaging, closed April 1, 2026). Merit posted 2024 revenue of $1.357B, up 7.9% YoY (Merit FY2024).

- Health Catalyst (SLC, HCAT) is a serial healthcare-data buyer: Lumeon (~$65M, closed August 1, 2024), Intraprise Health (signed November 6, 2024), and Upfront Healthcare Services ~$86M plus earn-out (completed January 21, 2025).

- Recursion Pharmaceuticals (SLC "techbio") merged with Exscientia (~$688M all-stock, closed November 20, 2024); the combined company stays SLC-headquartered (~74% Recursion / ~26% Exscientia).

- USANA Health Sciences (West Valley City) acquired Hiya Health ($205M for a 78.8% stake, ~$260M EV; closed December 23, 2024). USANA's FY2024 net sales were $855M.

- Myriad Genetics (SLC, MYGN) bought Intermountain Precision Genomics assets (closed February 1, 2024, terms undisclosed).

- Weave Communications (Lehi SaaS, WEAV) acquired TrueLark ($35M; $25M cash plus $10M equity; announced May 4, 2025). Note: "TrueLark" and the legal entity "Vidurama, Inc." are the same deal, not two.

For deal-velocity context, Ancestry (Blackstone, 2020), Divvy (Bill.com, 2021), and Sorenson Communications (Ariel Alternatives, 2022) are earlier examples — but they are pre-2023 and reflect historical, not current, appetite. The advisor implication is the same one that runs through this whole guide: a good Utah banker does not just own a generic buyers list — they know which of these corporate-development teams is actively buying in your category this quarter and can get your CIM in front of the right VP. The screening test: ask the advisor to name the in-state strategics most likely to bid on your business and the last deal each closed. One honest caveat: a dense in-state buyer pool is not a promise that your company is on Merit's or Health Catalyst's shopping list — these are large-cap acquirers with specific theses, and a boutique's job is to find the buyer who actually wants your asset.

How do I sell a Silicon Slopes SaaS company — and who should advise me?

To sell a Silicon Slopes SaaS company, hire an advisor who speaks ARR fluently and can name your software buyers — a boutique that can talk net revenue retention and Rule-of-40 for a $5M-$75M deal, scaling up to a national tech bank once you cross ~$150M or need a coastal/global buyer pool. SaaS sell-sides are not Main-Street processes: the logical buyers are software strategics and growth-equity sponsors who diligence on metrics, and a generalist business broker who cannot read a cohort curve will leave value on the table.

The local SaaS lane: Crewe Capital for a generalist middle-market sell-side with real Utah relationships; K2 Securities (SLC), which positions itself in SaaS and technology and transacts via Finalis Securities; and Premara Group (Lehi), a lower-middle-market SaaS, consumer, and B2B-services boutique whose team carries ex-Oracle, Qualtrics, Domo, and Lucid pedigree (treat its registration and deal record as pedigree, not a verified named-buyer track record). At scale, the national tech banks take over: Union Square Advisors and William Blair for a $150M+ enterprise-software process, Qatalyst for a $1B+ independent sell-side. Silicon Slopes is the I-15 "Point of the Mountain" corridor (Lehi-Draper-Provo) generating $30B+ in annual economic impact (CNBC, Dec 2024), with a normalizing 2026 multiple environment that rewards a clean, defensible metrics story.

The advisor-fit test for a SaaS seller: can the banker name the active software strategics and growth-equity sponsors in your specific category, and have they closed a comparable deal recently? And because software diligence is metrics-, security-, and IP-heavy, the data room work matters — a defensible ARR and cohort file, a clean security posture, and staged disclosure with per-viewer watermarking and screenshot protection so your customer list and pricing do not walk out the door. For the tech-seller framing specifically, our technology-sales solution, startups solution, and venture-capital solution pages map the workflow, and a structured Q&A workflow keeps the buyer's diligence questions organized instead of scattered across email.

Who advises medtech and life-sciences exits in Utah?

For a Utah medtech or life-sciences exit, hire a healthcare or medtech sector specialist — the buyer network, regulatory and QA diligence, and IP scrutiny are specialized enough that a generalist leaves multiple on the table — and lean on the fact that several of Utah's most active in-state acquirers live in exactly this space. Life sciences is one of Utah's dominant clusters: BioHive / BioUtah reports the sector contributes $22B+ to state GDP (~5.1%), with 180,000+ jobs and 1,300+ member companies, and 41,000+ life-science jobs in Salt Lake County alone (Salt Lake Chamber / BioHive).

The in-state strategic exit routes are real: Merit Medical (South Jordan) is a serial tuck-in buyer (EndoGastric ~$105M, Cook lead-management ~$210M, View Point ~$140M); Recursion (techbio, post-Exscientia), Health Catalyst (healthcare data), and Myriad Genetics (molecular diagnostics) are active in adjacent lanes. A medtech seller in that orbit is rarely a Main-Street process — the logical buyers are strategics and healthcare-focused PE platforms that a sector banker already knows. On the national side, Houlihan Lokey's healthcare and the broader William Blair healthcare/life-sciences practice (reaching Utah from Chicago and Denver) are the strongest options for a regulated, IP-heavy, or larger medtech seller; Houlihan Lokey's verified Clarus special-committee work is the local proof point that it actually executes Utah mandates. Where a strong Salt Lake generalist still fits: a smaller component supplier or services business in the $5M-$30M band, where a relationship-rich boutique like Crewe can run a tight process and pull the specialist buyers in by name.

The advisor-fit test for a life-sciences seller: can the banker name the active strategic and PE acquirers in your specific niche, and have they closed a comparable deal in the last 24 months? Because medtech diligence is QA- and IP-heavy, the due-diligence data room work matters more here than in a plain industrial deal — dynamic per-viewer watermarking and screenshot protection are the controls that keep design files and regulatory submissions from leaking, and visitor-group document isolation keeps each buyer in its own lane.

Who should advise an outdoor, consumer, or aerospace-defense seller in Utah?

For an outdoor, consumer-products, or aerospace-defense seller in Utah, match the advisor to the sector's distinct diligence reality — brand and IP-carve-out expertise for outdoor/consumer, and clearance- and contract-literate advisors with access-controlled data rooms for aerospace-defense. These are two of Utah's signature non-tech clusters, and each reshapes the advisor choice.

Outdoor and consumer. Utah's outdoor-recreation economy hit a record $9.75B in value-added in 2024 (3.3% of state GDP), supporting 75,182 jobs (BEA, Mar 2026), and Outdoor Retailer is back to a single annual Salt Palace show. The marquee local example is Clarus Corporation (Black Diamond, SLC HQ), which divested its Precision Sport segment (~$175M, 2024) with Houlihan Lokey advising the special committee, and later sold PIEPS/JetForce IP (~$9.1M, closed July 14, 2025). A name-trap to avoid: Clarus's brands are Black Diamond, Rhino-Rack, MAXTRAX, and TRED Outdoors — not Cotopaxi, Skullcandy, or Backcountry. The advisor implication: brand and IP-carve-out expertise and special-committee experience — the Houlihan Lokey lane — matter more than generic deal volume.

Aerospace and defense. Hill AFB generates a $12.76B economic impact with 26,893 personnel (2024), and Northrop Grumman is Utah's largest defense employer (10,000+ direct Utah jobs, 46,000+ supported, $12B+ in activity), anchored by the Sentinel ICBM program (Northrop, Jan 2026). A defense-exposed seller faces CMMC, ITAR, and clearance-sensitive diligence and government-contract novation issues that demand a defense-literate advisor and a tightly access-controlled data room. The common thread across both clusters: the deal mechanics are specialized enough that the advisor's sector fluency, and the data room's access controls, do more work than they would in a generic deal — which is why a clean sell-side prep process pays off most in exactly these sectors.

What's the difference between a business broker, a boutique bank, and a full investment bank in Utah — and which do I need?

The difference is mostly deal size and licensing, and Utah has the full ladder even if its homegrown rungs are thin. A business broker handles Main-Street sales (typically under ~$5M, often the owner's whole net worth) and is usually credentialed through the IBBA or the M&A Source rather than FINRA — in Salt Lake that is Utah Business Consultants, Alpine Business Brokers, Murphy Business, Sunbelt, and Transworld. A boutique investment bank runs a competitive process for ~$5M-$75M businesses and, for a securities-based stock sale, generally must be or transact through a FINRA-registered broker-dealer — Crewe Capital (its own BD), K2 Securities (via Finalis), and Premara are the local examples. A full investment bank (Houlihan Lokey, Jefferies, William Blair, Qatalyst reaching in) adds capital-markets capability, league-table credibility, and the bandwidth to run a $150M-$1B+ auction. The deal-size ladder is the practical guide: business broker under ~$5M, boutique ~$5M-$75M, middle-market investment bank ~$50M-$300M+.

The licensing line is genuinely consequential, and Utah has its own wrinkle. The federal M&A Broker exemption (Securities Exchange Act §15(b)(13), effective March 29, 2023) lets an unregistered intermediary handle a privately held company's stock sale only when the target had, in its prior fiscal year, under $25M EBITDA or under $250M in gross revenues — and that eligibility turns on the target's own financials, not the deal size, so a $25M enterprise-value deal is not automatically covered (Gordon Rees, 2023). The part most sellers miss: the federal exemption does not preempt state law. Utah's securities-side intermediation is governed by the Utah Uniform Securities Act (Title 61, Chapter 1) under the Utah Division of Securities, which states plainly that "exemptions do not exempt you from the licensing provisions" and publishes no carve-out paralleling the federal exemption (Utah Division of Securities). Separately, business-brokering of going concerns is regulated under the Real Estate Licensing Act (Title 61, Chapter 2f) via the Division of Real Estate — that license requirement clearly attaches when real property is part of the deal; whether a pure asset or going-concern sale with no real estate triggers it is jurisdiction-nuanced, so do not assume Utah flatly "requires a real-estate license to sell every business." The full breakdown is in our selection hub.

On credentials: a Main-Street broker should hold the IBBA's CBI or the M&A Source's M&AMI — Utah Business Consultants' Brad Marlor holds both, the dual credential to look for. A securities-based middle-market sale should run through a FINRA broker-dealer you can verify on BrokerCheck (Crewe Capital, CRD #152527), or a boutique that transacts through one (K2 via Finalis).

Who handles sub-$5M Main-Street business sales in Salt Lake City?

For a sub-$5M Main-Street business sale in Salt Lake City, use an IBBA- or M&A Source-credentialed business broker, not an investment bank — at that size a FINRA bank's minimum-fee floor (around $150,000) would eat too much of your proceeds. These firms are state-licensed business brokers, not FINRA-registered broker-dealers, which is the right fit below ~$5M; verify CRD status before relying on any of them for a securities or stock deal. The Salt Lake bench here is genuinely deeper than the sell-side investment-banking bench:

- Utah Business Consultants (South Jordan, founded 1989; $750M+ in cumulative lifetime transaction value, not one deal) — principal Brad Marlor holds both CBI and M&AMI, the dual credential to look for (UBC; IBBA Utah).

- Alpine Business Brokers, LLC (Lehi) — the deepest dual-credentialed bench in the Utah IBBA directory, co-founded by Neal Westwood (R. Neal Westwood) and Gary Tobian, both CBI/M&AMI, with Scott Simons (CBI/M&AMI) and others (Alpine PR). (A directory name-trap lists "Richard Westwood" — the correct name is Neal Westwood.)

- Murphy Business Sales — Salt Lake City (national franchise; SLC, Lehi, Ogden, Park City, Logan coverage).

- Sunbelt Business Brokers of Utah (Draper; owner/broker Dean Wiltse).

- Transworld Business Advisors (Utah County / Davis County / Herriman; Diane Hartz Warsoff, Art Warsoff, and Meili Myles all hold the CBI).

For a genuinely Main-Street sale, expect a flat percentage or a Double Lehman where the minimum fee dominates, and weigh the firm by its credentials and recent comparable sales. For right-sized data-room selection at this end of the market, our best data room for a small M&A deal and best data room for a small business guides cover the setup, and flat-rate data-room pricing keeps the cost predictable on a small deal.

Which Salt Lake firms are investors, not advisors — and who should I avoid mistaking for one?

Several of Utah's best-known deal firms get mistaken for sell-side M&A advisors but are not — they are venture, private-equity, and growth-equity investors, lenders, wealth managers, or strategic buyers, and listing them as advisors (or hiring them for the wrong job) is the single most common error in the Salt Lake market. Getting this right is half of vetting Utah honestly, because the investor bench is so much deeper than the advisor bench.

- The major Utah funds are investors, not advisors: Pelion Venture Partners, Sorenson Capital, Tower Arch Capital, Mercato Partners, Peterson Partners/Ventures, Signal Peak Ventures, Album VC (formerly Peak Ventures), Kickstart Fund, and Epic Ventures are VC, PE, or growth-equity firms that buy or back companies — none runs sell-side processes for you. DDR & Associates (SLC) is a direct-equity fund / principal investor, not an advisor either.

- The in-state strategic acquirers in the density map above — Extra Space, Merit Medical, Health Catalyst, Recursion, USANA, Myriad, Weave, plus HQ-density names like Zions Bancorporation, Varex Imaging, Nu Skin, and doTERRA — are corporate buyers and targets, not advisors or broker-dealers. They appear in this guide as the buyer pool, never as a firm you would hire.

- Two firms that market to Utah but should not be listed as Utah-headquartered advisors: Vesticor Advisors (no Utah office; not Utah-HQ'd — drop it from any Utah shortlist) and William & Wall (Scottsdale, AZ; markets to Utah but has no confirmed physical Utah office and discloses no broker-dealer affiliation — do not cite its self-reported "$30B+ Wall Street transaction expertise" as verified deal volume).

- And the regional firms with a real Salt Lake office but a non-Utah HQ — ACT Capital Advisors (Seattle), ClearRidge Capital (Tulsa), DBD Investment Bank (New York), Class VI Partners (Denver) — are legitimate options but should be labeled honestly. ACT's related "ACT Capital Management, LLC" (CRD #307272) is an investment adviser, not a broker-dealer, and broker-dealer status was not independently confirmed this pass for ACT, ClearRidge, or DBD; Class VI's affiliated BD is Class VI Securities (FINRA #148772).

The reliable filter for any name on a "best Salt Lake City M&A advisor" list: is it FINRA-registered or transacting through a registered broker-dealer (verify on BrokerCheck), does it run sell-side processes (rather than invest its own capital or manage wealth), and can it name a recent Utah closing in your band? If the answer to all three is not yes, it does not belong on your shortlist.

Is now a good time to sell my Utah business?

For owners of Utah businesses, the 2026 backdrop is favorable — record sector output, a deep in-state strategic-buyer pool, an elite capital ecosystem, and the Baby-Boomer succession wave are stacking demand at once, even as tech multiples normalize from their peak. The signals are concrete:

- Silicon Slopes (Lehi-Draper-Provo) generates $30B+ in annual economic impact (CNBC, Dec 2024).

- Utah life sciences contribute $22B+ to GDP (~5.1%), with 180,000+ jobs and 1,300+ companies (Salt Lake Chamber / BioHive).

- Utah's outdoor-recreation economy hit a record $9.75B in value-added in 2024, supporting 75,182 jobs (BEA, Mar 2026).

- Pelion Venture Partners raised a $500M fund in January 2025 — Utah's largest (Bloomberg, Jan 2025).

- Utah exported $22.4B in goods in 2025, supporting 73,369 jobs and contributing $9.2B to GDP (Utah Policy).

- ~$20B+ of completed take-private and strategic value flowed into Utah tech in an ~18-month 2023-2024 window (Qualtrics ~$12.5B plus Instructure ~$4.8B plus Vivint ~$2.8B).

The honest both-sides note: tech valuations have normalized from the 2021 peak, so a SaaS seller should expect a more disciplined multiple than two years ago and lead with a defensible metrics story. On the seller side, the demographic wave is real — Baby Boomers hold a majority of U.S. private wealth and are projected to be largely out of the workforce by the mid-2030s, a durable owner-succession pipeline. The exit-timing read: Utah industrial, life-sciences, and profitable-software owners who have been waiting for "a better year" are arguably in one now, and the advisor conversation is worth starting 6-9 months before you want to be in market. For a deeper read on how data-room behavior tracks deal momentum, see our state of M&A data rooms benchmark.

What's a reasonable success fee for a $25M Utah sell-side, and how do fees vary?

Utah M&A advisors price the way the broader U.S. lower-middle-market does: a monthly retainer or fixed work fee plus a success fee at close, with the success rate declining as deal size grows. For a $25M enterprise-value deal, expect a blended success fee in the 3-3.5% range.

The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8% (Auxo). Add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%. That tracks national data: independent fee tables put a $25M deal's blended success fee around 3-4%, declining toward 1.5-2% by $100M (ProCloser), so ~3-4% is the practical range to quote. For reference, the classic single Lehman scale (5-4-3-2-1) computes to about $350K on a $25M deal but is largely obsolete at this size.

The variation by advisor type in Utah:

- Boutiques (Crewe, K2, Premara) typically run Double Lehman or a negotiated flat rate at $25M-$75M, with a retainer in the $5,000-$25,000 per month range for a small-boutique mandate.

- The national banks (Houlihan Lokey, Jefferies, William Blair reaching in) carry higher retainer floors given their cost structures and reach for standard Lehman with capital-markets add-ons on larger deals, with minimum-fee floors of $500K-$1.5M at true middle-market scale.

- Main-Street brokers (Utah Business Consultants, Alpine, Murphy, Sunbelt, Transworld) on sub-$5M businesses often charge a flat percentage or a Double Lehman where the minimum fee (around $150,000) dominates.

Across all of them, retainers (work fees) are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly. What matters more than the headline percentage is the base it applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; cap it at 12. The full math, and the engagement-letter clauses that quietly inflate the bill, is in our M&A advisor fees hub, and the VDR cost guide covers the one line item you fully control.

Which virtual data room should a Utah seller actually use?

Tier the data room to your deal, not to the platform's pedigree — for a sub-$300M Utah lower-middle-market sale, the realistic shortlist is Peony, Ideals, and FirmRoom, while Datasite and Intralinks are the right (and credible) choice only when you are running a $500M+ mega-deal. Datasite and Intralinks are mature, capable platforms — Intralinks (owned by SS&C) reports 10,000+ M&A deals a year and ships DealCentre AI; Datasite ships AI-assisted search and redaction — so this is not a capability knock. It is a fit question: a per-page-priced platform with a six-figure implementation is an aircraft carrier to cross a lake for a sub-$300M Utah process, where the deal economics do not justify it. I will never tell you Datasite or Intralinks "lacks AI" — they do not — and I will never link a competitor product domain; the honest contrast is deal-size and cost fit, full stop. Ideals and FirmRoom are legitimate lower-middle-market rooms too, and I am not going to pretend they are weak.

Where Peony fits: a flat per-admin VDR — Free $0 / Business $30 / Data Room $52 (Most Popular) / Deal Team $64 (annual, min 4 admins) / Enterprise custom — with no per-page or per-GB metering and roughly 5-minute setup, SOC 2 Type II certified, G2 4.8 / Capterra 4.9, and 6,800+ teams on the platform. The credible band is $1M-$500M, with the sweet spot under ~$50M EV — which is exactly the Utah LMM and tech profile. Lead with capability, not price: the controls map cleanly to a sell-side process.

- Business ($30) and up: page-level analytics, screenshot protection, AI document Q&A, Simple NDA (acknowledge-only), and visitor groups that isolate documents per counterparty.

- Data Room ($52) and up: dynamic per-viewer watermarks (email, IP, timestamp), Advanced NDA (signed PDF plus countersign), Screenshield, AI auto-indexing and room generation, custom domain and branding, and unlimited rooms. Dynamic watermarks are never on Business or Free.

- Enterprise: per-group walled Q&A threads — each counterparty group its own isolated thread.

For a Utah seller specifically, the two controls that earn their keep are dynamic per-viewer watermarking (so a teaser leaked into the tight Silicon Slopes community is traceable to the exact person) and visitor-group document isolation (so you can stage strategics, sponsors, and growth-equity funds in one room without anyone seeing another tier). I run Peony for exactly this kind of tiered, watermarked release. For the PE-buyer and capital-raise lenses, our private-equity, fundraising, and M&A solution pages map the workflow.

Bottom line

Salt Lake City is the rare metro where the capital ecosystem is elite but the advisory bench is thin — Utah is investor-heavy and advisor-light, and the honest version of this list says so. The genuinely homegrown, FINRA-tied sell-side bench is essentially one firm: Crewe Capital (SLC, FINRA CRD #152527), the lone Salt Lake-headquartered investment bank with its own broker-dealer and verifiable 2024-2026 closings (J&S Mechanical to Comfort Systems USA, ~$120M; the Aero-mark sale of Certified Aviation Services). Two more credible Silicon Slopes boutiques — K2 Securities and Premara Group — run lower-middle-market processes through a hosted broker-dealer. The elite banks that win Utah's biggest deals — Houlihan Lokey (Clarus Precision Sport, ~$175M) and Jefferies (Clarus's 2026 review), with Qatalyst, William Blair, Union Square Advisors, and Cascadia as the credible-by-footprint bench — execute from out of state with no deal-running Utah office.

For a $5M-$75M Silicon Slopes SaaS, medtech, outdoor, or consumer sale, start with Crewe Capital, then K2 and Premara, and weigh the regional-office firms (ACT Capital, ClearRidge, DBD, Class VI) on the merits — labeled honestly as Utah offices of out-of-state firms. For a $150M+ or specialized process, bring in Houlihan Lokey, Jefferies, or William Blair; for a Main-Street deal under ~$5M, an IBBA-credentialed broker (Utah Business Consultants, Alpine, Murphy, Sunbelt, Transworld) rather than a bank. And do not mistake Utah's famous funds (Pelion, Sorenson, Mercato) or its in-state strategic acquirers (Extra Space, Merit Medical, Health Catalyst, Recursion) for advisors — they are investors and buyers, never the firm you hire to represent you.

The single most important advisor-selection question for a Utah seller: which firm has the deepest documented relationship with the named in-state strategics and the PE platforms in your sub-sector, and can show recent closings in your band? In a state this rich with buyers and capital but thin on local sell-side advisors, that verification is the whole edge. We serve 6,800+ customers on the data-room side of exactly these deals, and the prep you do before you pick an advisor — clean financials, a defensible metrics file, a staged data room, a tight buyer thesis — compounds everything the advisor does next. I run Peony, a data room company, and the Data Room tier gives you dynamic per-viewer watermarks, page-level analytics, and visitor groups at a flat $52 per admin per month — no per-page or per-GB fees, the predictable line item against a six-figure advisory fee.

Frequently asked questions about Salt Lake City M&A advisors

I'm selling my Utah SaaS company — should I hire a Silicon Slopes boutique M&A advisor or a national tech bank?

For a Utah SaaS sale, hire a Silicon Slopes boutique when your deal is in the ~$5M-$75M band and your best buyers are reachable strategics and middle-market sponsors; reach for a national tech bank (Qatalyst, William Blair, Union Square Advisors) once the deal climbs toward $150M+ or needs a coastal/global software-buyer pool. Price comes from competitive tension, not from a banker's zip code, so the real question is where your best buyers sit and who already has those relationships. Here is the honest Salt Lake reality most lists hide: Utah is investor-heavy and advisor-light. The capital ecosystem (Pelion, Sorenson, Mercato) and the strategic-acquirer density (Extra Space, Merit Medical, Health Catalyst, Recursion) are world-class — but the genuinely local, FINRA-tied sell-side bench is thin. Crewe Capital is essentially the only SLC-headquartered firm with its own FINRA broker-dealer (CRD #152527) and verifiable 2024-2026 sell-side closings; K2 Securities and Premara Group are credible Silicon Slopes boutiques that transact through a hosted broker-dealer rather than their own. So for a sub-$75M Utah SaaS sale, a local boutique that can speak ARR, NRR, and Rule-of-40 is a real option — but vet whether it has the national software-buyer network, because for a $150M+ enterprise-software process the deep tech bench of a Qatalyst or a William Blair usually earns its higher fee. On the document side, the prep is the same either way — I run Peony, a data room company used by 6,800+ customers, and a clean, staged data room with page-level analytics is the cheapest lever you control before you even pick the banker.

I'm a founder-CEO of a ~$25M company in Lehi / Provo — who are the best M&A advisors in Salt Lake City for a lower-middle-market tech sale?

For a ~$25M Lehi or Provo tech sale, the genuinely-local shortlist is short and you should be told so plainly: Crewe Capital is the one homegrown SLC sell-side investment bank with its own FINRA broker-dealer (CRD #152527) and verifiable recent closings, with K2 Securities and Premara Group (Lehi) as Silicon Slopes boutiques that run lower-middle-market processes through a hosted broker-dealer rather than their own. Above ~$150M, or for a coastal software-buyer pool, you bring in the national tech and medtech banks that cover Utah remotely — Houlihan Lokey and Jefferies both have verified 2024-2026 Utah mandates (the Clarus Precision Sport sale and Clarus's 2026 strategic review), with Qatalyst, William Blair, Union Square Advisors, and Cascadia Capital as the credible-by-footprint bench. The screening test for any of them: ask the banker to name the last three deals they closed in your sub-sector and the buyers on the other side. Crewe can point to named, dated, in-band closings (J&S Mechanical Contractors to Comfort Systems USA, ~$120M, February 2024; the Aero-mark sale of Certified Aviation Services, July 2024) — that kind of recent, named track record is what separates a real fit from a directory listing. Be skeptical of any out-of-state shop running a Salt Lake landing page that cannot show a single Utah closing. We serve 6,800+ customers on the data-room side of exactly these deals, and the firms that read every page of a teaser — you can see it in page-level analytics — are usually the ones genuinely working your file.

For a $25M Utah software exit, what are the pros and cons of a local Silicon Slopes boutique vs a national tech investment bank?

For a $25M Utah software exit, a local Silicon Slopes boutique gives you senior-banker attention, in-state relationships, and a boutique fee, while a national tech bank gives you a deeper software-buyer network and capital-markets muscle that matter more as the deal gets larger or more specialized. The boutique case: at $25M you are below the size where a Qatalyst or a William Blair will staff its A-team, so a firm like Crewe Capital (SLC, FINRA CRD #152527) or a hosted-broker-dealer boutique like K2 or Premara can put a managing director on every buyer call and run a tight, confidential process inside the tight-knit Silicon Slopes community. The national-bank case: a deep tech desk knows the coastal and global software acquirers and the active growth-equity sponsors by name, and at $150M+ that reach is worth the higher fee. The honest read for a $25M deal: a relationship-rich local boutique with a documented buyer map usually wins on attention and fee, but you must verify it can actually reach the national strategic and PE buyers your category needs — Utah's local bench is thin, so a boutique that cannot name your out-of-state buyers should co-advise with or hand off to a national firm. We serve 6,800+ customers on the data-room side, and you can use visitor groups to run a strategics-vs-sponsors split as separate permissioned tiers in one room regardless of which advisor you pick.

Qatalyst vs William Blair vs Houlihan Lokey for a Utah lower-middle-market SaaS sale — which fits a Silicon Slopes founder?

For a Utah lower-middle-market SaaS sale, the three split cleanly by deal size and situation: William Blair is usually the best fit for a clean $150M-$1B growth-software sell-side, Qatalyst for a premium $1B+ independent tech process, and Houlihan Lokey for a contested, special-committee, or restructuring-adjacent situation. Qatalyst (San Francisco and London only) is the premier brand for mega-cap tech sell-sides — but for a sub-$150M Silicon Slopes SaaS company it is almost always too big, and there is no named 2024-2026 Utah mandate to point to; it is credible by footprint, not by a local deal. William Blair is the employee-owned middle-market bank with a strong tech and SaaS practice and a Denver office as its nearest western reach, making it the natural national choice for a $150M+ Utah software process. Houlihan Lokey is the #1 global M&A advisor by deal count with a deep tech bench post-GCA, and it has a verified Utah mandate — it advised the Clarus Corporation special committee on the ~$175M Precision Sport sale (closed February 29, 2024) — so it is the right call for a contested or governance-sensitive deal. The catch for a true Silicon Slopes founder at $25M-$75M: none of these three will give your deal its A-team at that size, which is exactly when a local boutique (Crewe, K2, Premara) competes on attention and fee. On the document side, regulated and IP-heavy software diligence rewards a data room with dynamic per-viewer watermarking and screenshot protection — I run Peony, a data room company, and those controls live on our Data Room tier.

As a founder-owned Utah medtech company at ~$40M EV, should I hire Qatalyst or a regional Salt Lake boutique?

At ~$40M EV in Utah medtech, the honest answer is neither Qatalyst nor a generalist Salt Lake boutique by itself — you want a healthcare or medtech sector specialist, and at that size that usually means a national bank's healthcare desk rather than a tech-mega-deal brand. Qatalyst is a technology-focused mega-deal boutique; a $40M medtech device or diagnostics company is both below its size band and outside its core sector, so it is the wrong tool. The buyer network, regulatory and QA diligence, and IP scrutiny in medtech are specialized, and Utah's in-state strategic acquirers are real exit routes — Merit Medical (South Jordan) is a serial tuck-in buyer (EndoGastric Solutions ~$105M, Cook Medical lead-management ~$210M, View Point Medical ~$140M), and Recursion, Health Catalyst, and Myriad Genetics are active in-state consolidators in adjacent lanes. A sector-specialist banker already knows which of these corporate-development teams and which healthcare-focused PE platforms are buying in your niche this quarter. Where a strong Salt Lake generalist still fits: a smaller component supplier or services business in the $5M-$30M band, where a relationship-rich boutique like Crewe Capital can run a tight process and pull the specialist buyers in by name. The advisor-fit test: can the banker name the active strategic and PE acquirers in your specific medtech niche and the last comparable deal they closed? Because regulated medtech diligence is QA- and IP-heavy, a data room with dynamic per-viewer watermarking and screenshot protection matters — I run Peony, a data room company, and those controls live on our Data Room tier.

How does a sell-side M&A process work for a Utah SaaS company, and how long does it take from advisor hire to close?

A Utah SaaS sell-side runs in five overlapping stages and typically takes 6-9 months from signing the engagement letter to close, longer if the metrics need cleanup first. The rough timeline: 4-8 weeks of preparation (clean financials, an ARR and cohort/quality-of-earnings build, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA, starting from a blind teaser; 3-5 weeks to collect indications of interest and build a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory due diligence and definitive-agreement negotiation to close. The advisor's job through all of it is to manufacture competitive tension — running a real auction across both strategic buyers (in Utah that often means in-state consolidators like Merit Medical or Health Catalyst plus national software strategics) and growth-equity and private-equity platforms, so no single bidder feels unchallenged. SaaS deals can move faster on the buy side when a strategic already knows the product, but slower through ARR-quality, security, and revenue-recognition diligence. The single biggest timeline risk is unprepared metrics — sellers who walk in without clean, defensible ARR, churn, and cohort data add months. A clean, staged data room prepared before launch is the most reliable way to compress the back half of the schedule; I run Peony, a data room company used by 6,800+ customers, and the sellers who set up the room before going to market consistently close faster than the ones who scramble after the first LOI.

What SaaS metrics do buyers diligence, and how do I set up a data room before going to market with my Salt Lake City software company?

Buyers diligence a Salt Lake City software company on the metrics that prove durable, predictable revenue — ARR and its growth rate, net and gross revenue retention, logo and dollar churn, CAC payback, gross margin, the Rule of 40, cohort curves, and customer concentration — and you set up the data room around the eight diligence workstreams those metrics feed. The workstreams: financial (3-5 years of statements plus an ARR/quality-of-earnings build), corporate/legal (cap table, org chart, bylaws, board minutes), commercial (customer and reseller contracts, concentration analysis, the metrics file itself), product/technical (architecture, security posture, IP, open-source and data-privacy review), HR (org chart, key-employee and IP-assignment agreements), IP and IT (patents, trademarks, code ownership, systems), tax (returns, nexus, R&D credits, sales-tax exposure), and data security and privacy — which matters more for SaaS, where SOC 2 reports and breach history are standard diligence items. The two documents that do the most work up front are a defensible metrics/quality-of-earnings file and the CIM your advisor builds. The discipline that protects you is staged disclosure: a blind teaser first, the named CIM only after an NDA, and sensitive material (customer names, pricing, the full metrics file, source-code detail) held back to later stages and released only to a short list. A data room with per-buyer permissions, page-level analytics, and dynamic watermarking is what makes that enforceable — each viewer sees only their tier, and every page they open carries their identity so a leak is traceable. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release, and you can stage strategics, sponsors, and growth-equity funds as separate visitor groups in one room.

How do I keep my sale confidential in the tight-knit Silicon Slopes community where employees and competitors all know each other?

Confidentiality is run through staged disclosure and tight access control — and in Silicon Slopes, where the founder, investor, and operator circles are small and overlapping, it is one of the main reasons to hire an intermediary rather than shop the business yourself. The standard playbook: the advisor markets a blind teaser first (sector, size, and headline metrics with no name); interested buyers sign an NDA before receiving the named CIM; and sensitive material (customer names, pricing, employee rosters, the full metrics file, IP) is held back until later diligence stages and released only to a short list. A data room with per-buyer permissions and dynamic per-viewer watermarking is what makes this enforceable — each viewer sees only their tier, and every page they open carries their identity, so a leaked teaser is traceable back to the exact person who leaked it. That deterrence matters most along the Lehi-Draper-Provo corridor, where a competitor, a portfolio-company peer, or a key engineer might be one shared investor away. Tell your advisor explicitly that no competitor or local fund on your do-not-contact list should ever receive even the blind teaser, and put that list in the engagement letter. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release — dynamic per-viewer watermarks and screenshot protection are how you make a small-market sale leak-resistant, and page-level analytics tell you who actually opened what.

Can a local Salt Lake City boutique actually reach national PE and strategic buyers, or will I leave value on the table vs a national bank?

Yes — a good local Salt Lake boutique can reach national PE and strategic buyers, but only if it can prove the relationships, and Utah's structural advantage actually helps because so many credible acquirers are headquartered in-state. The proof is in the buyer list: ask the advisor to produce a list that mixes 8-15 named strategics with 15-30 named sponsors specific to your sub-sector, with a contact at each. A genuinely Utah-fluent boutique like Crewe Capital can do that and can name the in-state consolidators (Extra Space, Merit Medical, Health Catalyst, Recursion, USANA, Myriad, Weave) that have actually been buying in 2023-2026; a generalist who cannot name them is the wrong fit. The honest caveat is real, though: Utah's local sell-side bench is thin, so for a true coastal-software or cross-border buyer pool, a boutique should co-advise with or hand off to a national firm (Qatalyst, William Blair, Union Square Advisors) rather than pretend it owns relationships it does not have. You leave value on the table not by hiring local, but by hiring an advisor — local or national — who cannot reach your actual best buyers, so the verification matters more than the zip code. We serve 6,800+ customers on the data-room side, and visitor groups let you run the strategics-vs-sponsors split as separate permissioned tiers in one data room.

What red flags should I watch for, and what questions should I ask a Salt Lake City M&A advisor before signing an engagement letter?

Vet a Salt Lake City advisor on three things — registration status, named recent closings in your sub-sector, and a written staffing commitment — and treat the pitch itself as the least reliable signal. Start with the licensing line: a securities-based stock sale should run through a FINRA-registered broker-dealer (check BrokerCheck — Crewe Capital is CRD #152527, for example), while some Silicon Slopes boutiques transact through a hosted broker-dealer (K2 Securities effects securities via Finalis Securities) and Main-Street brokers like Utah Business Consultants operate under business-brokerage credentials (IBBA's CBI, the M&A Source's M&AMI) rather than FINRA, which is fine below ~$5M but not for a securities sale. The Utah-specific trap: many "Salt Lake City M&A advisor" pages are out-of-state firms running local landing pages, so confirm where the firm is actually headquartered and whether it can name a single Utah closing. Green flags: named recent deals in your category with the buyers identified, a senior banker who will commit in writing to staffing your calls personally, a realistic valuation backed by comparable transactions (not a flattering number to win the mandate), and a clear, capped fee structure. Red flags: a large upfront fee with a vague success structure; a valuation that sounds too good to be true; reluctance to name the senior banker who will actually run the deal; sending sensitive documents over email instead of a permissioned data room; and a tail period of 18-24 months they refuse to negotiate. I run Peony, a data room company, and a telling early signal is whether the advisor insists on a real data room with page-level analytics rather than emailing your financials around.

What does an M&A advisor cost to sell a $25M Utah company — is a 3 to 3.5% success fee normal, and how does Double Lehman plus a retainer work?

For a $25M Utah company, expect a monthly retainer plus a success fee at close, with a 3-3.5% blended success rate squarely in the normal range. The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8%; add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%. That tracks national middle-market data: a $25M deal sits in the band where independent fee tables put blended success fees around 3-4%, declining toward 1.5-2% by $100M, so quote ~3-4% as the practical range. Retainers (work fees) in this band run roughly $5,000-$25,000 per month at a small boutique (more at a mid-market bank), and they are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly. A minimum-fee floor (commonly around $150,000 at the small end, $500K-$1.5M for true middle-market banks) appears in most letters; on a $25M deal the percentage fee normally exceeds the small-end floor, so it rarely binds at this size. What matters more than the headline percentage is the base it applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; cap it at 12. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive, well-run auction produces. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Salt Lake City shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- Best Tech M&A Advisors — the sector hub for software, SaaS, and tech-enabled sellers, the bulk of the Silicon Slopes deal flow

- M&A Data Room: Setup and Workstream Mapping — the data room setup playbook for sell-side prep

- Best Data Room for a Small M&A Deal (sub-$30M sale) — right-sized VDR selection and setup for a sub-$30M sale, the band where most Utah founder exits land

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including vendor DD, which matters more in a medtech, defense, or regulated footprint

- How to Write a CIM (Confidential Information Memorandum) — the authoring playbook for the offering document your advisor will build for the sale

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark

- Virtual Data Room Cost Guide — what a VDR actually costs, and how flat per-admin pricing compares to per-page models

- Best M&A Advisors in Denver — the nearest Mountain-West comparator and the closest western office for several national banks reaching Utah

- Best M&A Advisors in Phoenix — Southwest growth-market comparator

- Best M&A Advisors in Seattle — Pacific-Northwest tech comparator and the HQ of several firms with a Utah office

- Best M&A Advisors in San Francisco — the Bay Area tech-bank hub where Utah's biggest software sell-sides are actually run

- Best M&A Advisors in Indianapolis — the strategic-acquirer-density comparator with a real in-state investment bank

- Best M&A Advisors in Las Vegas — the other advisor-light desert metro, where gaming regulation splits the bench between license-fluent specialists and everyone else

Footnotes and sources

- Crewe Capital — firm overview and sell-side mandates (J&S Mechanical Contractors to Comfort Systems USA; Aero-mark sale of Certified Aviation Services); distinct from the separate wealth RIA Crewe Advisors, LLC

- FINRA BrokerCheck — Crewe Capital, LLC, CRD #152527 — FINRA/SIPC broker-dealer registration status (SEC# 8-68460, founded 2011)

- Comfort Systems USA — acquisition of J&S Mechanical Contractors (~$120M) — closed February 1, 2024

- Utah Business — Crewe Capital advises J&S Mechanical sale (Utah Business, February 2024)

- BusinessWire — Crewe Capital advises Aero-mark, LLC on the sale of Certified Aviation Services (announced July 8, 2024)

- Houlihan Lokey — firm overview; advised the Clarus special committee on the

$175M Precision Sport sale; acquired GCA Corporation ($599.1M, completed October 4, 2021) - GlobeNewswire — Clarus completes sale of Precision Sport segment to JDH Capital affiliate (closed February 29, 2024; Sierra Bullets plus Barnes Bullets)

- Jefferies — firm overview; retained as financial advisor on Clarus's 2026 strategic-alternatives review

- Shop-Eat-Surf — Clarus launches strategic review (announced May 2026)

- Union Square Advisors — technology-focused M&A boutique (FINRA member, CRD #141254)

- Qualtrics — Silver Lake and CPP Investments complete acquisition (~$12.5B) (closed June 28, 2023)

- Instructure — KKR and Dragoneer complete acquisition (~$4.8B) (closed November 13, 2024)

- NRG Energy — acquisition of Vivint Smart Home (~$2.8B cash / ~$5.2B EV) (closed March 2023)

- Extra Space Storage and Life Storage — merger close (~$11.6B at close, ~$46B EV) (closed July 20, 2023)

- Merit Medical — completes acquisition of Cook Medical lead-management portfolio (~$210M) (closed November 1, 2024)

- Merit Medical — FY2024 results ($1.357B revenue, +7.9%) (February 2025)

- Houlihan Lokey newsroom — acquisition of GCA Corporation (~$599.1M, completed October 4, 2021)

- Bloomberg — Pelion raises $500M, Utah's largest fund (Bloomberg, January 2025) — investor, not an advisor

- CNBC — Utah's Silicon Slopes ($30B+ economic impact) (CNBC, December 2024)

- Salt Lake Chamber / BioHive — Utah life sciences ($22B+ GDP, 180,000+ jobs, 1,300+ companies)

- BEA — outdoor recreation economic statistics (Utah $9.75B value-added, 75,182 jobs, 2024) (BEA, March 2026)

- Northrop Grumman — Utah footprint (largest defense employer, Sentinel ICBM) (Northrop, January 2026)

- Salt Lake Tribune — Goldman Sachs ~3,000 Utah employees (Salt Lake Tribune, May 2025) — operations/technology campus, not an M&A office

- Utah Policy — Utah exported $22.4B in goods in 2025

- Utah Business Consultants — South Jordan business brokerage; Brad Marlor (CBI + M&AMI)

- IBBA — Utah member directory — CBI/M&AMI-credentialed Utah business brokers

- Alpine Business Brokers — Neal Westwood and Gary Tobian CBI awards (Lehi; correct name Neal Westwood, not "Richard Westwood")

- Gordon Rees — federal M&A Broker exemption, §15(b)(13) (effective March 29, 2023; eligibility turns on target EBITDA < $25M or revenue < $250M; does not preempt state law)

- Utah Division of Securities — corporate-finance exemptions — Utah Uniform Securities Act; "exemptions do not exempt you from the licensing provisions"

- Auxo Capital Advisors — Modified (Double) Lehman fee math (Double Lehman = ~$700K / ~2.8% on $25M)

- ProCloser — M&A advisory fees guide (blended success-fee curve: ~3-4% at $25M, declining toward 1.5-2% by $100M)