13 Best Boutique M&A Advisors in Denver for $5M-$200M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: May 2026

Early in my career I spent a stint on the M&A bench at Nomura before crossing the table to early-stage investing at Backed VC and growth-equity / secondaries at Target Global — and I've spent the last several years co-founding Peony, a data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. The conversation I have most often with Denver / Front Range / Mountain West founders considering a sell-side process in 2026 is the same one I had in 2024: the Denver M&A landscape is structurally bifurcated — three of the firms most commonly cited in commodity content are defunct or absorbed (St. Charles Capital → KPMG Corporate Finance 2014; Green Manning & Bunch wound down 2015; Headwaters MB → Capstone → Huntington Bancshares 2018/2022) — and the active 2026 bench splits cleanly between (a) pure-play energy specialists (Petrie, TPH, Pickering Energy Partners, KeyBanc Denver), (b) Denver-resident generalist boutiques (SDR Ventures, Class VI Partners, Flatirons Capital Advisors, FMI Capital Advisors for building products), and (c) bracket-platform Denver offices (Houlihan Lokey, D.A. Davidson regional HQ, Piper Sandler, Stifel, Lincoln International). This guide names 13 verified Denver-area boutiques with dated 2024-2026 closed transactions, maps each one to the Denver Strategic Buyer Quartet (energy via Antero / Civitas / EnCap / Riverstone, mining via Newmont, ag-food via JBS USA / Pilgrim's Pride, healthcare via DaVita), and gives founder-CEOs the engagement-letter terms, fee benchmarks, and confidentiality-discipline frame I use to scope every sell-side conversation. Sources are linked inline at every transaction reference; verified deals only; firms with no recent activity are flagged and dropped. Peony's investors include Matt Clifford (EF / ARIA), Charlie Songhurst (ex-Microsoft), Backed VC, and Possible Ventures.

Quick answer: For a Denver / Front Range $5M-$200M EV sell-side in 2026, the 13 verified boutiques worth pitching are Petrie Partners (pure-play O&G, Denver HQ; Avant $1.45B 2025; Pioneer-ExxonMobil $65B fairness opinion 2024), Tudor Pickering Holt (Denver office of PWP energy; global #1-3 energy M&A 2024-2025), Pickering Energy Partners (Dan Pickering founder, 2019), KeyBanc Capital Markets Denver (Harvest Midstream $1.7B Nov 12 2025; Bison Oil & Gas IV $1B Aug 29 2025), Houlihan Lokey Denver (#1 global industrials M&A advisor sub-$5B; Jesse Nichols MD), D.A. Davidson Denver (regional HQ since 1935; HRSoft / Gryphon March 2026), Piper Sandler Denver (Minneapolis HQ with Denver office; firmwide 2025 Outstanding M&A Investment Bank of the Year), Stifel Denver (#1 North American M&A sub-$1B since 2012), Lincoln International Denver (Chicago HQ, 20-office global mid-market generalist), SDR Ventures (Denver, 59 lifetime deals; Robertson Tire / Big Brand Tire Feb 2025; Nicklas Medical Staffing / Argosy Jan 2025), Class VI Partners (Denver, 100+ lifetime deals, $4B+ delivered; Zivaro / Trace3 Dec 2024; Fresca Foods / Cerealto majority investment Oct 2025), Flatirons Capital Advisors (Denver, 52 lifetime deals; ThriveMD / Boyne Capital), and FMI Capital Advisors (Denver MDs Aaron Bachik + Jason Munoz, building products specialist; 800+ FMI-platform lifetime transactions). Defunct / absorbed — do NOT engage: St. Charles Capital (acquired by KPMG Corporate Finance June 26, 2014), Green Manning & Bunch (wound down March 31, 2015), and Headwaters MB (acquired by Capstone Partners January 8, 2018; Capstone then acquired by Huntington Bancshares June 15, 2022 — operates under the Capstone brand inside Huntington's middle-market platform). Hennessy Capital is NOT a Denver firm — HQ Zephyr Cove, NV. William Blair, Brown Gibbons Lang have no verified Denver investment banking offices. The 2026 engagement-letter benchmark for a $30-50M EV Denver sell-side: $50-100K creditable retainer, 1.7-3% blended success fee, 12-18 month tail, $25-50K expense cap. The data room cost to bill back to your client should be $260-$520 across a 5-month process on Peony Data Room at $52 per admin per month, not the $15-50K Datasite passthrough that clients increasingly refuse to absorb.

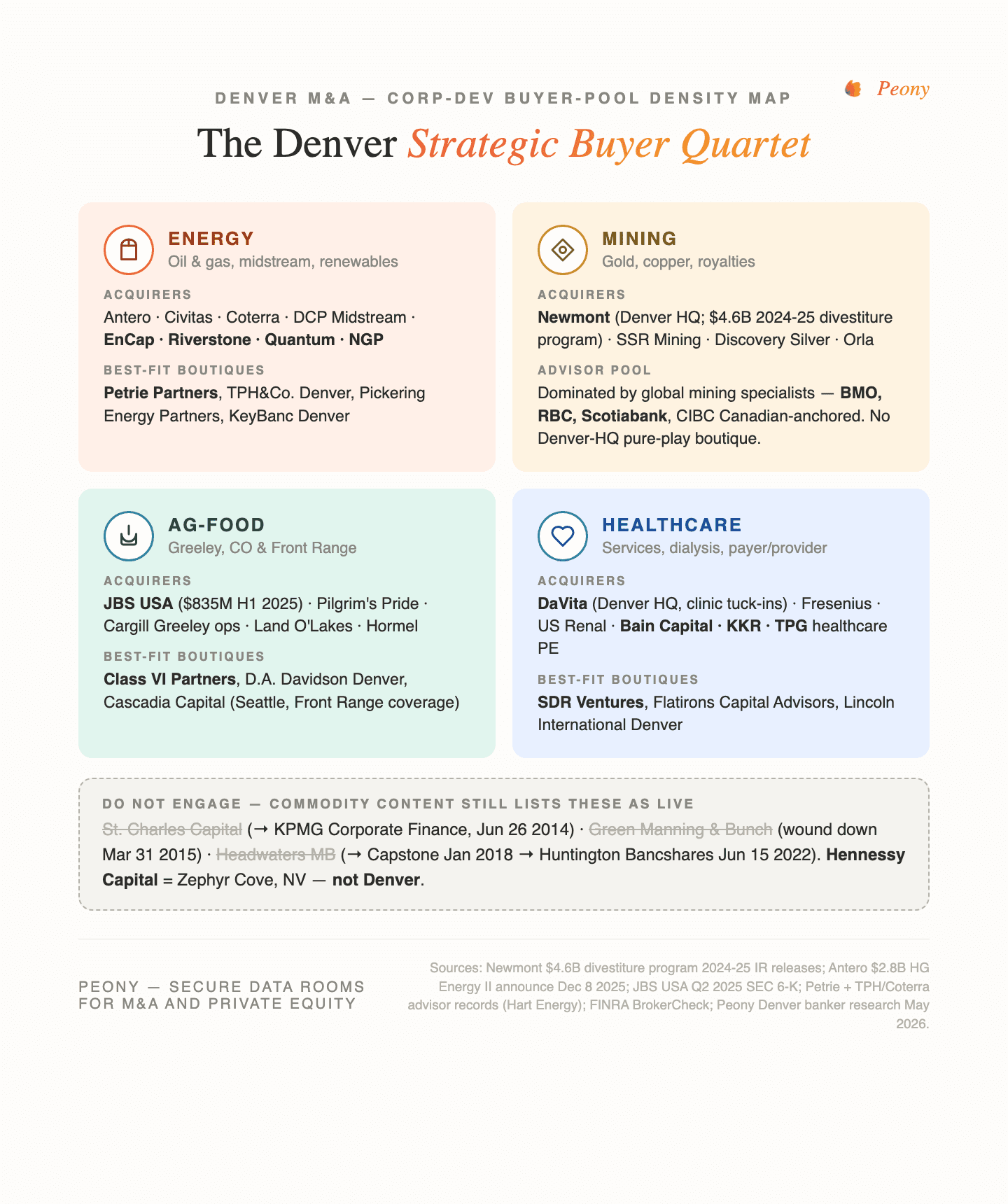

What Is the Denver Strategic Buyer Quartet and Why Does It Shape Banker Choice?

Denver has four corners of structural strategic-acquirer density that shape which boutique you should pitch first. The corner your business sits closest to should drive the shortlist, not the firm's brand recognition.

Corner 1: Energy (Antero Resources / Civitas / DCP Midstream / Liberty Oilfield Services / EnCap / Riverstone / Quantum / NGP). Antero Resources (Denver HQ) announced a $2.8 billion HG Energy II Marcellus upstream acquisition + $800 million Utica divestiture in December 2025, with Antero Midstream simultaneously announcing a $1.1 billion HG II Energy Midstream Holdings acquisition (closing Q1/Q2 2026). KeyBanc Capital Markets Denver acted as joint lead arranger on a $1.7 billion senior secured credit for Harvest Midstream's Green River + Uinta Basin acquisition from MPLX (November 12, 2025) and $1 billion revolving credit for Bison Oil & Gas IV's DJ Basin acquisition from Civitas Resources (August 29, 2025). For a Front Range energy seller, your likely buyer pool is Denver / Houston strategics (Antero, Civitas, Coterra, Liberty Oilfield Services, Continental, Devon) plus PE energy funds (EnCap Investments, Riverstone Holdings, Quantum Energy Partners, NGP, ArcLight, EIG, Kayne Anderson). The Denver boutiques with the deepest energy bench are Petrie Partners (pure-play E&P), Tudor Pickering Holt Denver, Pickering Energy Partners, and KeyBanc Capital Markets Denver (full energy capital stack including reserve-based lending).

Corner 2: Mining (Newmont). Newmont (Denver HQ) executed a $4.6 billion divestiture program 2024-2025 — sold Telfer/Havieron in Australia (closed December 4, 2024), Akyem in Ghana, Musselwhite to Orla Mining ($850M), Éléonore to Dhilmar ($795M), Cripple Creek & Victor in Colorado to SSR Mining (up to $275M), and Porcupine to Discovery Silver ($425M total). The mining buyer pool runs through global majors (Barrick Gold, Agnico Eagle, Kinross, Pan American Silver, Coeur Mining, Hecla Mining) plus mid-tier consolidators (Pan American, Eldorado, Centerra, Calibre). Mining M&A advisory is dominated by global firms (BMO Capital Markets Mining, RBC Capital Markets Mining, Scotiabank, CIBC, Cantor Fitzgerald Canada) rather than Denver-resident boutiques — the structural advisor pool for Newmont-orbit sellers is Canadian-headquartered mining specialists with Denver coverage rather than Denver-HQ boutiques.

Corner 3: Ag-food (JBS USA / Pilgrim's Pride / Cargill Greeley operations). JBS USA (Greeley CO HQ) deployed $835 million of US strategic investments in H1 2025 including a $100 million Ankeny IA ready-to-eat bacon/sausage facility acquisition, a $135 million new fresh sausage facility, and (via the Mantiqueira USA JV) a binding agreement to acquire Hickman's Egg Ranch (a top-20 US egg producer). Pilgrim's Pride (Greeley CO HQ, JBS USA majority-owned) is similarly active in poultry consolidation. For a Front Range ag-food seller, the boutiques with the strongest sector bench are Class VI Partners (Fresca Foods / Cerealto majority investment October 31 2025), D.A. Davidson, and national ag specialists (Cascadia Capital from Seattle, Houlihan Lokey Industrials).

Corner 4: Healthcare (DaVita). DaVita (Denver HQ) is a steady acquirer of dialysis clinic tuck-ins — Q1 2024: 11 US + 67 international; Q3 2025: 58 acquired internationally. The Denver healthcare-services buyer pool extends to national strategics (Fresenius, US Renal Care, American Renal Associates) and healthcare PE (Bain Capital, KKR, TPG, Vistria, Welsh Carson). The Denver boutiques with healthcare-services bench are SDR Ventures (Nicklas Medical Staffing / Argosy Healthcare Partners January 2025), Flatirons (ThriveMD / Boyne Capital), and Lincoln International Denver (national healthcare practice).

Reading the quartet: the boutique you pitch should have closed deals INTO your corner of the quartet in the last 24 months. An energy seller pitching only generalist boutiques without EnCap / Riverstone / Quantum deal flow is structurally underbanked; a building-products seller pitching only generalist boutiques without FMI's sub-vertical bench is similarly underbanked. The Denver Strategic Buyer Quartet is the single most important diagnostic frame I use to scope a Denver sell-side conversation.

Which 13 Denver Boutiques Should I Pitch in 2026?

The 13 verified firms below, grouped by structural tier, with confirmed 2024-2026 transactions. Firms with no recent activity or that have been absorbed (St. Charles Capital → KPMG CF 2014; Green Manning & Bunch wound down 2015; Headwaters MB → Capstone → Huntington Bancshares 2018/2022) are excluded. Hennessy Capital (Zephyr Cove NV) is also excluded — it is not a Denver firm despite occasional misattribution.

Tier 1 — Energy sector specialists with the deepest Front Range buyer bench

1. Petrie Partners — pure-play oil & gas, Denver HQ

- HQ: Denver (additional Houston office); founded 2011 with legacy back to Petrie Parkman (1989)

- ~20 professionals; pure-play upstream M&A, asset acquisition & divestiture (A&D), capital raises

- Recent verified closed transactions: Avant — financial advisor (alongside TPH&Co.) on $1.45 billion sale of New Mexico / Lea & Eddy County O&G assets (announced November 2024, closed January 2025 to Coterra); Peak 10 Energy — acquisition of Verado Midland Basin assets from Black Topaz / Blue Topaz (closed August 29, 2025); Pioneer Natural Resources — $65 billion all-stock merger with ExxonMobil (2024, fairness opinion); Intrepid Potash — JV amendment with ExxonMobil for Northern Delaware Basin (up to $200M, 2024)

- Best fit: $50-500M EV upstream E&P, A&D, midstream M&A in the Rockies (DJ, Powder River, Piceance, Uinta) and cross-basin platform deals

2. Tudor, Pickering, Holt & Co. (TPH&Co.) Denver — global energy platform, Denver office

- Energy practice HQ: Houston; Denver office is one of 8 global offices

- Founded 2007; acquired by Perella Weinberg Partners 2016; operates as PWP's energy business

- Consistently ranked #1–#3 global energy M&A advisor by deal value / count 2024-2025 (Bloomberg / Refinitiv league tables)

- Sectors: E&P, midstream, OFS, energy transition, renewables

- Best fit: cross-basin platform deals, $200M+ EV energy M&A, international energy transactions

3. Pickering Energy Partners (PEP) — founder-led pure-energy shop

- HQ: Houston with Denver presence; founded 2019 by Dan Pickering after departing TPH

- Sectors: Energy investment banking + asset management

- Active in IPOs, follow-ons, private placements 2024-2025; Consulting & Advocacy Practice (led by Dan Romito) acquired by Opportune LLP on February 13, 2026 — investment banking and asset management remain at PEP

- Dan Pickering is widely-cited energy market voice (Hart Energy, 2025 outlook)

- Best fit: founder-led sell-sides where the seller wants the founder-banker bench dynamic, energy capital raises

4. KeyBanc Capital Markets Denver — full energy capital stack

- HQ: Cleveland; major Denver office for energy & industrials

- Combines M&A advisory with reserve-based lending — full energy capital stack from Denver

- Recent verified transactions: Harvest Midstream — joint lead arranger on $1.7 billion senior secured credit facility for Green River + Uinta Basin acquisition from MPLX LP (November 12, 2025); Bison Oil & Gas IV — joint lead arranger on $1 billion revolving credit for DJ Basin acquisition from Civitas Resources (August 29, 2025); Excel Testing & Engineering Holdings — sale to Fusion Capital Partners (December 22, 2025)

- Best fit: midstream deals with stapled reserve-based lending, energy capital stack transactions

Tier 2 — Denver-resident generalist LMM boutiques

5. SDR Ventures — Denver-pure generalist, 59 lifetime deals

- HQ: Denver; founded 2002

- Serves businesses up to $300M EV across healthcare, consumer, industrials

- 59 lifetime deals per Tracxn — one of the most prolific independent Denver shops

- Recent verified closed transactions: Robertson Tire Co. — sale to Big Brand Tire & Service (Percheron Capital portco), February 2025; JK Concepts (Denver architectural millwork) — acquisition (October 2025); Katsam Property Services — recapitalization by Unity Partners (August 2024); Nicklas Medical Staffing — acquisition by Argosy Healthcare Partners (January 2025); Reddotbuildings — acquisition by Cordatus Capital (March 6, 2025)

- Best fit: $5-50M revenue diversified-sector deals in healthcare, consumer, industrials, services

6. Class VI Partners — Denver, 100+ lifetime transactions, $4B+ delivered

- HQ: Denver (255 Fillmore St, Suite 500, 80206); founded 2005

- Sectors: Consumer, healthcare, business services, technology, industrial & manufacturing services; $5M-$500M revenue clients

- Recent verified closed transactions: Zivaro (Denver IT/managed cloud) — acquisition by Trace3, December 16, 2024; Electric Equipment & Engineering (Denver, founded 1922) — recapitalization by HKW Inc., December 2, 2024; Fresca Foods (Denver/Boulder, 400+ employees, organic snack co-manufacturer) — majority investment from Cerealto Global, October 31, 2025

- Best fit: $5-500M revenue diversified-sector deals where the seller values wealth-management integration for the founder's post-sale capital

7. Flatirons Capital Advisors — Denver, 52 lifetime deals

- HQ: Denver; offices in Dallas, Chicago, Miami; founded 2015

- Sectors: Manufacturing, IT, distribution, energy, professional services, transportation, healthcare

- Recent verified closed transactions: Denver Plumbing & HVAC — acquisition by Prime Home Services Group (May 2025); ThriveMD — acquisition by Boyne Capital / Platt Park Capital Partners

- Best fit: $10-100M EV LMM deals across services, manufacturing, distribution

8. FMI Capital Advisors (Slate legacy) — Denver MDs, building-products specialist

- HQ: FMI HQ is Raleigh NC; the Denver-rooted Slate team operates from Denver

- Senior bankers: Aaron Bachik (MD) and Jason Munoz (MD) — both Denver-based, with a clean Denver M&A pedigree: led Green Manning & Bunch's building materials / services group → co-founded Slate Partners 2014 → Slate acquired by FMI Corporation October 18, 2022; the GMB → Slate → FMI arc is one of the most-quietly-significant Denver M&A continuity threads

- Sectors: Building products, building materials, building services, construction; engineering & infrastructure

- 800+ FMI-platform lifetime transactions; active in construction materials roll-ups

- Best fit: the only Denver-resident MD team with deep sub-sector dominance in building products — pitch for any building-products / building-materials / construction-services deal

Tier 3 — Bracket-platform Denver offices

9. Houlihan Lokey Denver — global industrials platform

- HQ: Los Angeles; Denver office confirmed

- Senior banker: Jesse Nichols, Managing Director (Denver-based per LinkedIn, May 2025)

- #1 M&A advisor for global industrials transactions under $5B (2025 ranking per Houlihan Lokey)

- Best fit: $50-500M EV industrials and energy mid-market deals where the global industrials platform is the differentiator

10. D.A. Davidson & Co. Denver — regional HQ since 1935

- HQ: Great Falls MT; Denver is one of 5 regional HQs (not a satellite)

- #5 nationally in financial institutions M&A since 2016

- Recent verified deals: HRSoft (Denver-HQ enterprise compensation software) — majority investment from Gryphon Investors (March 2026); Canopy Collective (CO/NC/SC landscaping family of companies) — debt capital raise; Proficium (CA, AI infrastructure) — growth investment from Mill Point Capital

- Best fit: $20-200M EV deals across financial services, tech, services where deep Denver regional roots matter

11. Piper Sandler Denver — Minneapolis HQ, Denver office

- HQ: Minneapolis; Denver office confirmed

- Robyn Moore (Managing Director, Colorado Governmental Public Finance — joined from Stifel April 2022) is Piper's most-visible Denver banker, though her practice is public finance rather than corporate M&A

- Firmwide 2025 Outstanding M&A Investment Bank of the Year recognition

- Best fit: energy + healthcare overlap deals at the upper end of mid-market where the Piper sector platform is the differentiator (Denver M&A coverage runs through the broader Piper Sandler bench rather than a single Denver-resident M&A MD)

12. Stifel Denver — sub-$1B M&A leader

- HQ: St. Louis; Denver branch

- Ranked #1 in North American M&A transactions under $1B since 2012

- Acquired Bryan, Garnier & Co. (European tech/healthcare bank) closed June 2, 2025

- Best fit: $20-200M EV diversified mid-market deals

13. Lincoln International Denver — Chicago HQ, 20-office global mid-market

- HQ: Chicago; Denver office part of 20-office global network

- ~950 professionals globally; reliable PE-backed mid-market platform

- Recent recognition: M&A Advisor's Restructuring Deal of the Year ($250M-$1B), 2024

- Sectors: Mid-market generalist; energy, healthcare, industrials, business services

- Best fit: $30-300M EV mid-market deals where global PE reach is the structural advantage

Specialist additions worth mentioning

14. Janco Partners — TMT specialist (Englewood / Greenwood Village)

- One of few Front Range TMT-research-led boutiques; broker-dealer registered (FINRA Firm #40055)

- Sectors: Telecommunications, media, electronic software, alternative energy, technology

- Best fit: TMT deals at the boutique scale

15. PCE Companies Denver — ESOP specialty

- HQ: Orlando; Denver office serves western states

- $15B+ lifetime in advisory; uniquely strong on ESOP formation alongside straight sales

- Best fit: founder-owned businesses considering ESOP exit instead of strategic / PE sale

Which Three Recent Denver Deals Show How These Firms Actually Work?

Three closed transactions from the last 12 months that map firm capability to real Denver deal flow.

Deal 1: Avant → $1.45 billion sale of New Mexico / Lea & Eddy County O&G assets (announced November 2024, closed January 2025 to Coterra) — advisors: Petrie Partners + TPH&Co. Verified via Petrie Partners' transactions wall and Hart Energy. Avant, a Front Range upstream operator, sold New Mexico Permian-Delaware Basin assets for $1.45 billion cash to Coterra — illustrating Petrie's bench depth on sub-$2B E&P sell-sides, even where the mandate is co-advised with TPH. The pattern across Petrie's 2024-2025 deal list (Pioneer-ExxonMobil fairness opinion on the $65 billion 21st-century-largest upstream deal, Intrepid Potash JV amendment with ExxonMobil, Peak 10 Energy acquisition of Verado Midland Basin assets August 2025) demonstrates that a Denver-resident pure-play energy boutique can run at bulge-bracket caliber when the assets are in Petrie's bench-of-record geography.

Deal 2: Zivaro → Trace3, December 16, 2024 — advisor: Class VI Partners. Verified via Class VI Partners announcement. Zivaro, a Denver IT and managed-cloud services company, sold to Trace3 (a national IT services consolidator) — illustrating Class VI's bench on Denver tech-services LMM exits. The pattern across Class VI's recent deal list (Electric Equipment & Engineering / HKW December 2024, Fresca Foods / Cerealto October 2025) demonstrates cross-sector flexibility — IT-services, electrical engineering, organic-snack manufacturing all closed by the same partner-led bench in a 12-month window.

Deal 3: Harvest Midstream — $1.7 billion senior secured credit facility for Green River + Uinta Basin acquisition from MPLX, November 12, 2025 — advisor: KeyBanc Capital Markets Denver (joint lead arranger). Verified via KeyBanc press release. KeyBanc's Denver office acted as joint lead arranger on the financing for Harvest Midstream's acquisition of MPLX's Rockies midstream footprint — illustrating KeyBanc's full energy-capital-stack capability (M&A advisory paired with reserve-based lending). The pattern across KeyBanc Denver's 2025 transaction wall (Bison Oil & Gas IV $1 billion revolving credit August 2025, Excel Testing & Engineering December 2025) demonstrates that the bank-platform energy boutique model — combining advisory and credit — is the structural differentiator for midstream and energy-stack sell-sides where the buyer needs financing aligned to the transaction.

The pattern across all three: Denver boutique and bank-platform sell-side is sector-specialized, partner-led, runs 4-6 month engagement-to-close cycles on LMM deals, and routes most exits to either PE-energy / PE-industrials funds (EnCap, Riverstone, Quantum, NGP, KKR, Apollo) or national strategic consolidators (Trace3, Big Brand Tire, Cerealto, ExxonMobil). This is the structural pattern that the commodity-content version of "Denver M&A advisors" — which still lists defunct firms like St. Charles Capital and Green Manning & Bunch as live alternatives — misses entirely.

How Do I Choose Between Three Denver Boutiques After the Pitch Meetings?

A scored decision matrix I use across every Denver sell-side conversation. Score each firm 1-5 against seven criteria; the firm with the highest total wins the engagement.

| Criterion | Weight | What to evaluate |

|---|---|---|

| Senior-banker commitment | 20% | Will an MD or partner be on every buyer call from CIM through LOI? Get it in writing in the engagement letter. |

| Sector / Denver buyer-pool bench | 20% | Has the firm closed deals INTO your corner of the Denver Strategic Buyer Quartet in the last 18 months? Energy → Antero / Civitas / EnCap / Riverstone / Quantum / NGP; mining → Newmont; ag-food → JBS / Pilgrim's / Cargill Greeley; healthcare → DaVita. |

| Recent transaction activity | 15% | At least 3 closed deals in the last 12 months, all verified via BusinessWire / PR Newswire / SEC EDGAR — not just the firm's website. |

| Engagement-letter economics | 15% | $50-100K creditable retainer, 1.7-3% blended success fee, 12-18 month tail, $25-50K expense cap, competitor exclusion list. Push back on 18-24 month tail or non-creditable retainer. |

| Confidentiality discipline | 10% | NDA gates, per-investor watermarks, sample CIM redaction, competitor-exclusion clauses. In Denver's small business community, confidentiality discipline is sharper than in NYC / Chicago. |

| Reference quality | 10% | Two seller references from closed deals in the last 12 months — call them. Ask which senior banker actually ran the process, what the engagement-to-close cycle was, whether the firm identified the eventual buyer. |

| Data room cost defensibility | 10% | Does the firm bill Datasite or Intralinks at $15-50K passthrough? Or has it switched to a flat-rate platform (Peony, DealRoom, SecureDocs) at $200-$400 per deal? Cost defensibility to your client signals 2026-era client awareness. |

Reading the scorecard: the highest-scoring firm is rarely the largest by brand recognition. At $30-50M EV in Denver, the partner-led sector-specialist boutique with deep buyer-pool bench and clean engagement-letter economics typically beats the bracket-platform firm with stronger brand recognition but weaker senior-banker commitment at sub-$100M scale.

What Are the Fee Benchmarks for a $30-200M Denver Sell-Side?

| Deal size (EV) | Modal retainer (creditable) | Success fee structure | Blended fee % | Tail period |

|---|---|---|---|---|

| $5-15M | $25-50K | Modified Lehman (8-10% on first $1M, stepping down) | 4-6% | 12-18 mo |

| $15-40M | $50-75K | Standard Lehman 5/4/3/2/1 or modified | 2-3% | 12-18 mo |

| $40-100M | $50-100K | Lehman with flat 1.5-2.0% above $40M | 1.5-2.5% | 12-15 mo |

| $100-200M | $75-150K | Negotiated flat / stepped (1-1.5% blended target) | 1-1.5% | 12 mo |

Bank-platform firms (Piper Sandler Denver, Stifel Denver, Houlihan Lokey Denver, D.A. Davidson, Lincoln International Denver, KeyBanc Capital Markets Denver) typically quote at the higher end of the retainer range ($75-150K) and may push for higher minimum fees. Denver-resident partner-led boutiques (SDR Ventures, Class VI Partners, Flatirons, FMI Capital Advisors) negotiate more flexibly on retainer credibility and tail length. Energy sector specialists (Petrie Partners, Tudor Pickering Holt, Pickering Energy Partners, KeyBanc energy) may charge a sector-premium on success fee in exchange for the deeper EnCap / Riverstone / Quantum / NGP buyer-pool reach — typically worth it if the sector-buyer-pool match is strong.

The single most-undermanaged engagement-letter term in 2026 Denver deals: the data room passthrough. Datasite quotes for a $30-100M EV sell-side run $15-50K as a passthrough expense the client is asked to reimburse. Increasingly, Denver clients refuse to absorb that as expense reimbursement — and the boutique either eats the cost or quotes a higher retainer. Peony Data Room at $52 per admin per month delivers the full feature stack (per-bidder watermarks, NDA gates, multi-tier permissions, AI Q&A, page analytics, screenshot blocking, custom-domain branding) for $260-$520 across a 5-month process at 1-2 admins — folding that into your engagement letter as a fixed-cost line item rather than a passthrough expense improves your client-facing math by $15-45K on a typical mandate. For the detailed banker-side data room mechanics, see the sell-side investment banking data room playbook.

Frequently Asked Questions

I'm selling a $40M EV Front Range oil & gas company — should I hire a Denver M&A boutique or a Houston energy bank?

For a $40M Front Range upstream E&P or DJ Basin asset divestiture in 2026, the right answer is usually a Denver-resident energy boutique with cross-bench Houston reach — not a Houston-headquartered firm that flies a VP in for the management presentation. Petrie Partners is the most credible energy M&A boutique HQ'd in Denver — founded 2011 with legacy back to Petrie Parkman (1989), pure-play oil & gas with the bench depth to run bulge-bracket-caliber E&P sell-sides; recent representative engagements include serving as financial advisor to Avant on its $1.45 billion sale of New Mexico / Lea & Eddy County O&G assets (announced November 2024, closed January 2025 to Coterra alongside TPH&Co.) and rendering the fairness opinion on Pioneer Natural Resources' $65 billion all-stock merger with ExxonMobil in 2024 (the largest upstream deal of the 21st century). Tudor, Pickering, Holt & Co. (acquired by Perella Weinberg Partners in 2016) maintains a confirmed Denver office covering Rockies operators (DJ Basin, Permian-adjacent) paired with Houston for cross-basin coverage — consistently ranked #1–#3 global energy M&A advisor by deal value 2024-2025 (Bloomberg / Refinitiv league tables). Pickering Energy Partners (founded 2019 by Dan Pickering after departing TPH) is a founder-led pure-energy shop with Denver presence. KeyBanc Capital Markets' Denver office combines M&A advisory with reserve-based lending — full energy capital stack — and acted as joint lead arranger on $1.7 billion senior secured credit for Harvest Midstream's Green River + Uinta Basin acquisition from MPLX (November 12, 2025) and $1 billion revolving credit for Bison Oil & Gas IV's DJ Basin acquisition from Civitas Resources (August 29, 2025). The structural test for the Denver-vs-Houston decision: ask each pitching firm which senior banker will be on every buyer call, and how many of their last 12 closed E&P deals involved Rockies operators (DJ, Powder River, Piceance, Uinta) versus Permian / Eagle Ford. A Denver-resident MD running 6+ Rockies deals in the last 24 months structurally beats a Houston-resident MD running 2 Rockies deals as overflow. Peony page-level analytics show which pitching firms are reading the financials versus which ones are skipping to the legal section — a useful filter on which firms genuinely engaged before signing the engagement letter.

I'm a $30M ARR Boulder SaaS founder — should I pick a Bay Area tech bank or a Denver generalist?

For a $30M ARR Boulder SaaS exit in 2026, the structural decision is whether your likely buyer pool is national strategic + national PE (in which case a Bay Area tech-specialist banker with Salesforce / Workday / ServiceNow corp-dev relationships wins) or regional strategic + lower-mid-market PE rollup (in which case a Denver-resident banker with cross-sector range wins). D.A. Davidson is the strongest answer for the second category — Denver is one of D.A. Davidson's 5 regional headquarters (not a satellite), and the firm advised Denver-HQ enterprise compensation software company HRSoft on its March 2026 majority investment from Gryphon Investors. Class VI Partners (Denver, 100+ lifetime transactions, $4B+ delivered) represented Denver IT and managed-cloud company Zivaro on its December 16, 2024 acquisition by Trace3 — exactly the Denver tech-services profile that maps to LMM PE rollup buyers. Flatirons Capital Advisors (Denver, 52 lifetime deals) sits in the same Denver tech-services band. If your buyer pool is genuinely Bay Area strategic (Salesforce, ServiceNow, Workday, HubSpot acquiring sub-$100M EV vertical SaaS), pitch Vista Point Advisors, Founders Advisors, or a tech-specialist boutique with West Coast corp-dev calling. The Denver vs Bay Area decision usually maps to who calls your prospects — corp-dev teams at the Bay Area FAANG-adjacent SaaS giants don't take inbound from generalist Denver bankers as readily as they take inbound from Bay Area tech-specialist boutiques. Peony visitor groups let your advisor segment the buyer pool by tier so the senior banker can see at a glance which strategic is actually engaged versus which one is fishing.

I'm running a Colorado cannabis MSO at $25M EV — should I sell to a national rollup like Cresco / Trulieve / Curaleaf, or wait for the federal-rescheduling cycle?

For a $25M EV Colorado cannabis MSO in 2026, the structural answer is: there is no Denver-HQ pure-play cannabis M&A boutique with the bench depth of an energy specialist like Petrie or a building-products specialist like FMI, so the practical Denver advisor pool runs through generalist LMM boutiques with cannabis-adjacent experience — SDR Ventures (Denver, 59 lifetime deals, 2002 founded) and Class VI Partners (Denver, 100+ lifetime deals) handle cannabis-adjacent transactions on a generalist basis. KEY Investment Partners is a Denver-based cannabis-focused investor (more sponsor than pure advisor) — acquired the BellRock Brands portfolio (Mary's Medicinals, Dixie Elixirs) out of receivership in January 2026. The buyer-pool reality in 2026: the Multi-State Operator consolidation wave that drove 2019-2022 cannabis M&A has compressed (Curaleaf, Trulieve, Cresco Labs, Green Thumb Industries, Verano are all trading at structurally compressed multiples), and the federal-rescheduling decision under the DEA's pending Schedule III action remains the single biggest variable for cannabis M&A pricing. The waiting-or-selling tradeoff: rescheduling to Schedule III removes the 280E tax burden (currently destroying cannabis operator economics) which could double EBITDA and re-rate multiples 30-50%, but rescheduling has been signaled and delayed multiple times since 2024 — calling the timing wrong costs you a year of carry. The pragmatic banker recommendation for a $25M MSO in 2026: engage a Denver generalist boutique (SDR or Class VI) for a 6-12 month sell-side preparation phase that runs in parallel to the federal-rescheduling timeline; if rescheduling lands during your prep, launch the process at the post-rescheduling multiple; if rescheduling stalls, you launch anyway at the current multiple. The advisor that wins this mandate is the one whose engagement letter has a low-cost prep phase with optionality on launch timing — not a NYC bulge-bracket charging a $150K retainer that pressures you to launch into a bad cycle.

St. Charles Capital vs Green Manning & Bunch vs Headwaters MB for a $30-50M Denver mid-market sale — which actually runs my deal?

None of the three exist as independent boutiques in 2026 — and this is the single most-common error in commodity Denver M&A content. St. Charles Capital was acquired by KPMG Corporate Finance on June 26, 2014 and no longer operates as an independent boutique; mandates that would have gone to St. Charles now route through KPMG's national Corporate Finance platform. Green Manning & Bunch (founded 1988) ceased operations on March 31, 2015 and is defunct — any pitch deck listing GMB as an active option is dated by more than a decade. Headwaters MB was acquired by Capstone Partners on January 8, 2018; Capstone was then acquired by Huntington Bancshares on June 15, 2022 — the Denver bench operates under the Capstone Partners brand inside Huntington's middle-market platform. The active 2026 Denver mid-market alternatives are: Petrie Partners (energy specialist, $30-300M+ E&P), Tudor Pickering Holt Denver, SDR Ventures (Denver, 59 lifetime deals, generalist LMM up to $300M EV), Class VI Partners (Denver, 100+ lifetime deals, $4B+ delivered, $5-500M revenue clients), Flatirons Capital Advisors (Denver, 52 lifetime deals), FMI Capital Advisors (Denver MDs Aaron Bachik + Jason Munoz, building products specialist), and the Denver offices of D.A. Davidson (regional HQ), Houlihan Lokey (industrials platform, #1 global M&A advisor for industrials sub-$5B), Piper Sandler, Stifel, Lincoln International, and KeyBanc Capital Markets. Verify any Denver boutique pitch by cross-checking the firm's last 12-month transaction wall against BusinessWire / PR Newswire / SEC EDGAR filings; defunct firms still surface in stale aggregator content and outdated league tables. Peony per-investor watermarks on past deal CIMs the advisor shows you in the pitch are a tell — if the firm sends you a sample CIM with no watermark, no view tracking, and no NDA gate, that's how they ran their last buyer outreach too.

Petrie Partners vs Tudor Pickering Holt for my Denver oil & gas divestiture — and is a Houston specialist always better than a Denver local on energy?

For a Denver / Front Range / Rockies E&P or midstream sell-side in 2026, the Petrie-vs-TPH choice maps to whether you want a Denver-resident pure-play boutique running every buyer call (Petrie) or a Houston-anchored global energy platform with Denver coverage (TPH). Petrie Partners (Denver HQ, ~20 professionals, pure-play O&G since 2011) served as financial advisor to Avant on its $1.45 billion New Mexico / Lea & Eddy County divestiture (announced November 2024, closed January 2025 to Coterra alongside TPH&Co.), rendered the fairness opinion on Pioneer Natural Resources' $65 billion ExxonMobil merger in 2024, and advised Peak 10 Energy on the August 29, 2025 acquisition of Verado Midland Basin assets from Black Topaz / Blue Topaz. The firm is the most credible energy M&A boutique HQ'd in Denver — bulge-bracket-caliber on E&P sell-sides at the partner-led pace boutiques are structurally built for. Tudor, Pickering, Holt & Co. (founded 2007, acquired by Perella Weinberg Partners 2016, operating as PWP's energy business) is consistently ranked #1–#3 global energy M&A advisor by deal value / count 2024-2025 (Bloomberg / Refinitiv league tables) with one of 8 global offices in Denver. The structural difference: Petrie runs partner-led mandates from a Denver bench; TPH offers a global platform whose Denver office is one node of an 8-office network. A Houston specialist is NOT always better than a Denver local — for Rockies-focused assets (DJ Basin, Powder River, Piceance, Uinta), a Denver-resident MD with 6+ Rockies deals in the last 24 months structurally beats a Houston MD running Rockies as overflow. For cross-basin platform deals (Permian + DJ + Eagle Ford + Bakken combos), a Houston-resident global energy platform wins. The decision matrix: pure Rockies asset divestiture under $500M EV → Petrie. Multi-basin platform deal or cross-border energy → TPH / Pickering Energy Partners / KeyBanc Denver. Midstream-only with reserve-based lending stapled → KeyBanc Denver. Peony custom domain branding lets your advisor run the data room at files.youradvisory.com without exposing which platform the data room runs on to the bidder pool — useful when EnCap / Riverstone / Quantum / NGP associates are benchmarking against deals they've previously seen.

I'm a $40M Denver founder pitching three M&A advisors — what red flags should disqualify a firm in the pitch meeting?

Seven red flags I've seen disqualify Denver M&A advisors in the pitch meeting before the engagement letter ever gets to legal review. First, the firm pitches you on a defunct competitor — if their slide deck names St. Charles Capital, Green Manning & Bunch, or independent Headwaters MB as live Denver alternatives, the deck is more than 4 years old and the firm hasn't refreshed its competitive intelligence. Second, the senior banker (MD or partner) doesn't commit in writing to running every buyer call from CIM through LOI — at $30-50M EV in Denver, partner-led is structurally available from Petrie Partners, SDR Ventures, Class VI Partners, Flatirons, FMI Capital Advisors, and others — if the firm can't commit, choose a firm that will. Third, the firm sends a sample CIM with no watermark, no NDA gate, no view-tracking — that's how they ran their last buyer outreach too. Fourth, the firm's last 12-month transaction wall is empty or stale — the Denver / Front Range M&A market has been active through 2024-2026 (Antero's $2.8 billion HG Energy II acquisition + $1.1 billion midstream tag announced December 8, 2025 (closing Q2 2026), Newmont's $4.6 billion 2024-2025 divestiture program, JBS USA's $835 million H1 2025 US strategic investments) so a year-long gap is a warning sign. Fifth, the firm's references include only sellers from $5-10M deals when you're a $30-50M seller — the firm is fishing above its real weight class. Sixth, the firm refuses to name competitor exclusions in the engagement letter — at $30-50M Denver EV, naming 5-10 Front Range competitors you don't want approached is table-stakes negotiation. Seventh, the firm hasn't closed a deal into your specific Denver corporate ecosystem in the last 18 months — if you're an energy seller, has the firm closed deals into Antero Resources, Civitas, DCP Midstream, Liberty Oilfield Services, or comparable strategics? If healthcare services, into DaVita? If ag-food, into JBS USA (Greeley) or Pilgrim's Pride? If mining-services, into Newmont? The Denver buyer ecosystem is dense enough that recent deals into your specific buyer pool are a structural verification signal. Peony Smart Q&A workflow with AI-drafted answers is the operational layer your eventual banker uses to run the Q&A across 8-25 bidders — if the firm uses email and a spreadsheet, that's a structural process-discipline gap visible from the first pitch meeting.

I have 30-100 employees and the Colorado business community is small — how do I run a confidential sell-side without my employees or competitors finding out?

Confidentiality leakage on a Denver / Front Range sell-side is structurally sharper than on an NYC or Chicago deal because the Colorado business community is small enough that everyone in DJ Basin oil & gas, every Boulder tech founder, every Greeley ag-food operator knows each other socially. Four predictable failure points and the mechanical fix for each. First, the CIM itself: a Front Range CIM that names the seller, lists the top 5 customers, and shows the management team biographies will leak if a buyer forwards it. The fix is a teaser-first process where the buyer signs the NDA against a generic anonymized teaser (sub-vertical, revenue band, geography, EBITDA band), and only sees the full CIM after the NDA is countersigned and the buyer is logged into the data room. Second, employee leakage: a Front Range services business with 30-100 employees will hear rumors within weeks if the management team starts disappearing for buyer calls — and Boulder's tight tech community + DJ Basin's tight energy community make rumor cycles faster than in larger metros. The fix is restricting the deal team to founder-CEO plus CFO until the LOI is signed, and using a transaction code name on all internal calendar events. Third, customer leakage: if a strategic buyer calls your top customer for reference checks during diligence, the customer learns immediately — in Denver's small operator community, the customer overlaps with a competitor's customer base within one social degree. The fix is reference-check only after exclusivity, and only on a limited customer list pre-approved by the seller. Fourth, competitor leakage: a Front Range competitor invited into the buyer pool will use the data room visit to reverse-engineer your unit economics — and in Denver's tight community, a leaked CIM can land on your competitor's desk by Wednesday. The fix is competitor-exclusion clauses in the engagement letter and a tiered data room where competitors only see late-stage diligence after LOI. Denver firms that run confidential processes by structural design include Petrie Partners (partner-led E&P confidentiality discipline), SDR Ventures, Class VI Partners, Flatirons, and FMI Capital Advisors. Peony per-investor watermarks embed buyer email plus exact view timestamp into every page, so a leaked CIM has a forensic audit trail back to the buyer. Peony screenshot protection blocks and logs unauthorized capture attempts on Business plan rooms, deterring competitors from harvesting customer concentration tables.

How do I verify a Denver investment bank's actual closed deal track record without taking the pitch deck at face value?

Verify the track record through three independent sources, not the advisor's pitch deck. First, the firm's transaction wall and press release archive — Petrie Partners transactions, SDR Ventures, Class VI Partners, Flatirons, D.A. Davidson, Houlihan Lokey, Lincoln International, Piper Sandler, KeyBanc Capital Markets press, Tudor Pickering Holt, and FMI Capital Advisors all publish dated transaction tombstones with buyer/target/sector. Cross-check those against BusinessWire, PR Newswire, SEC EDGAR, and the buyer's own press releases — if the buyer announced the transaction and named a different financial advisor, the boutique is overstating involvement. Second, Axial's Top 100 LMM Investment Bank league table and Denver Business Journal's local recognition rank firms by closed deal count. Third, direct seller references — ask the pitching firm for two sellers from closed deals in the last 12 months and call those sellers directly. Specifically ask: which senior banker actually ran my process, how many buyers contacted versus how many produced IOIs, did the firm identify the eventual buyer or did the buyer find the firm, and was the close timeline what they pitched. The single highest-signal question: ask for the engagement letter date and the close date on the last three closed deals — a 4-6 month engagement-to-close cycle is fast, 6-9 months normal, 12+ months a warning sign. Denver firms with strong recent verifiable activity include Petrie Partners (Avant $1.45B 2025, Peak 10 Energy August 29 2025, Pioneer-Exxon $65B fairness opinion 2024), SDR Ventures (Robertson Tire / Big Brand Tire February 2025, JK Concepts October 2025, Nicklas Medical Staffing / Argosy January 2025, Katsam Property Services / Unity Partners August 2024), Class VI Partners (Zivaro / Trace3 December 16 2024, Electric Equipment & Engineering / HKW December 2 2024, Fresca Foods / Cerealto majority investment October 31 2025), KeyBanc Denver (Harvest Midstream $1.7B November 12 2025, Bison Oil & Gas IV $1B August 29 2025, Excel Testing & Engineering December 22 2025), and D.A. Davidson (HRSoft / Gryphon March 2026). Peony page-level analytics on the sample CIM each advisor shares with you in the pitch reveal how they actually run their buyer outreach — firms whose sample materials show no analytics, no watermark, and no NDA gate are firms whose actual buyer outreach is similarly unguarded.

I get 2-3 inbound PE calls a quarter and just got an unsolicited offer from JBS or DaVita corp-dev — should I take it or run a process through a Denver advisor?

Take the call but never sell off it. The Denver corporate ecosystem is dense with active acquirers — JBS USA (Greeley CO HQ) deployed $835 million of US strategic investments in H1 2025 (the $100 million Ankeny IA ready-to-eat facility was a 2025 announcement; the $135 million fresh sausage facility was separately announced 2025); separately, in November 2025, the Mantiqueira USA JV announced a binding agreement to acquire Hickman's Egg Ranch (a top-20 US egg producer); Antero Resources (Denver HQ) announced (December 8, 2025; closing expected Q2 2026 with January 1, 2026 effective date) a $2.8 billion HG Energy II Marcellus upstream acquisition + $800 million Utica divestiture + $1.1 billion midstream tag; Newmont (Denver HQ) executed a $4.6 billion divestiture program 2024-2025 including the Cripple Creek & Victor Colorado asset sale to SSR Mining (up to $275 million), Akyem in Ghana, Telfer/Havieron in Australia (closed December 4 2024), Musselwhite to Orla Mining ($850 million), Éléonore to Dhilmar ($795 million), and Porcupine to Discovery Silver ($425 million); DaVita (Denver HQ) is a steady acquirer of dialysis clinic tuck-ins (Q1 2024: 11 US + 67 international, Q3 2025: 58 international). These corp-dev teams call Front Range founders constantly because they sit at the center of structural acquirer ecosystems; the inbound is real interest, but the IOI an inbound strategic makes after a screening call is structurally below what the same buyer pays in a competitive process. The right move: log the inbound, ask qualifying questions about specific sub-vertical fit, do not share financials, and engage a Denver sell-side advisor — Petrie Partners for E&P / midstream at $50M+ EV, SDR Ventures or Class VI Partners for diversified services / healthcare / consumer at $20-100M, FMI Capital Advisors for building products, D.A. Davidson for diversified mid-market. Route the inbound JBS / DaVita / Antero / Newmont call into your eventual process as one of 8-15 qualified buyers — that strategic then has to bid against national PE (Apollo, Bain Capital, KKR, TPG sector funds; EnCap / Riverstone / Quantum / NGP for energy), regional strategics, and any sub-vertical rollup in your space. The price discovery from running a process surfaces a higher number from the same team that originally inbounded. Peony page analytics show which inbound buyers actually open the financials versus which ones never logged in after the NDA was signed — a useful filter for which inbounds belong in the eventual process.

What is a reasonable success fee for a $30-50M Denver sell-side mandate in 2026, and is Lehman scale still standard?

On a $30-50M EV Denver sell-side, expect total advisor fees in the 1.7%-3% range — roughly $510K to $1.5M including retainer and success fee. Denver boutiques in the lower-middle-market band (SDR Ventures, Class VI Partners, Flatirons, FMI Capital Advisors, Janco Partners) generally run a Lehman-style success fee scale (5% on the first $1M, 4% on the next, 3% on the next, 2% on the next, and 1% on everything above $4M) or a modified-Lehman variant. That math produces about $440K of success fees on a $30M deal (1.5% blended) and about $940K on a $50M deal (1.9% blended). Some Denver boutiques negotiate a flat or modified-Lehman alternative on $20-50M EV mandates: 1.5%-2.0% flat success fee above a tier-2 floor, or a tiered structure with a higher first-tier percentage and a flat tail above $20M. Add a $50K-$100K retainer credited against success fee at close. For deals above $50M, the modified-Lehman flattens at the top: above $100M, Denver mid-LMM firms negotiate a flat or stepped success fee with a 1%-1.5% blended target rather than pure Lehman — because a straight Lehman on a $200M deal produces a $4M success fee that no advisor can defensibly charge. Energy specialists (Petrie Partners, Tudor Pickering Holt, Pickering Energy Partners, KeyBanc Capital Markets energy) may charge a sector-premium on success fee in exchange for the deeper EnCap / Riverstone / Quantum / NGP buyer-pool reach — typically worth it if the sector-buyer-pool match is strong. Bank-platform firms (D.A. Davidson, Houlihan Lokey, Piper Sandler, Stifel, Lincoln International) often quote at the higher end of the retainer range ($75-150K) and may push for higher minimum fees. Tail period of 12-18 months is standard. Peony Data Room at $52 per admin per month replaces the $15K-$50K per-deal data room cost most Denver boutiques used to bill as expense reimbursement — folding that into your engagement letter as a fixed-cost line item rather than a passthrough expense improves your client-facing math by $30K-$45K on a typical 5-month mandate.

How does a Denver sell-side process actually work step-by-step — from engagement letter to close — for a $30-50M founder-led business?

A Denver / Front Range $30-50M EV sell-side runs as a four-month process from engagement letter to LOI signing, plus a four-to-six-month process from LOI to close. Month 0 (engagement letter signed): banker and seller align on positioning, build the buyer list (typically 50-100 names for a Denver LMM deal, narrowed to 25-40 outreach targets), and begin CIM drafting. Month 1 (CIM drafting): banker drafts the CIM with seller input — financial story, customer concentration, growth thesis, sub-vertical positioning, management team bios. Quality of earnings if commissioned (typically $50-150K from a Big 4 or regional firm — BDO, RSM, Plante Moran, CLA, or Crowe all have Denver offices) runs in parallel. Month 2 (teaser distribution, NDA collection): banker distributes the blind teaser to the buyer list; ~25-60 buyers sign NDAs; CIM distributed to NDA-signed bidders. Data room Tier A opens with redacted financials, market overview, summary customer concentration. Month 3 (IOI round): bidders submit indications of interest with price range, sources of capital, conditions, expected timeline. Banker shortlists 3-7 for LOI round. Management presentations scheduled. Month 4 (LOI round / management presentations): shortlisted bidders attend management presentations, conduct site visits, submit binding letters of intent. Banker selects winner; exclusivity granted. Months 5-8 (confirmatory diligence + SPA negotiation): buyer-side legal, tax, RWI underwriting, quality of earnings if not pre-commissioned, definitive agreement negotiated in parallel. Denver-specific timeline variations: oil & gas deals into the Antero / Civitas / EnCap / Riverstone ecosystem can extend the regulatory-clearance phase (state oil & gas commission filings, BLM lease assignments where federal acreage is involved); cannabis deals require state Marijuana Enforcement Division approval that can add 60-180 days; aerospace / defense deals into Lockheed Martin Space or Ball Aerospace require CFIUS review for any non-US bidder which can add 60-90 days; mining-services deals into Newmont follow standard timelines but require careful environmental disclosure documentation. The data room is the operational backbone across all four phases — Peony Data Room at $52 per admin per month replaces the $15K-$50K Datasite passthrough most Denver boutiques bill as expense reimbursement, with per-bidder watermarks, staged folder permissions, AI Q&A drafting, and page-level analytics that the operator playbook for sell-side bankers depends on. For the detailed banker-side data room mechanics, see the sell-side investment banking data room playbook.

Related Resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Denver shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- The Sell-Side Investment Banking Data Room Playbook (2026) — the banker-side operator playbook for the data room your Denver advisor will run

- 14 Best M&A Advisors in Minneapolis for $5M-$300M Deals — Twin Cities medtech / ag-food cluster comparison

- 14 Best Boutique M&A Advisors in NYC for $5M-$100M Deals — NYC LMM advisor cluster

- 12 Best Boutique M&A Advisors in Chicago for $5M-$200M Deals — Chicago LMM advisor cluster

- Best Boutique M&A Advisors in Houston — Houston energy advisor cluster (the Denver alternative for cross-basin energy deals)

- Best M&A Advisors in Salt Lake City — the closest Mountain West comparator: an investor-heavy, advisor-light tech-exit market where Crewe Capital is the one homegrown sell-side bank

- Best Energy M&A Advisors in the US (sector hub) — the national energy-subsector hub above Denver's basin deal flow: upstream, midstream, power, and renewables advisors mapped by where each one wins

- Best M&A Data Rooms (7-VDR Scored Comparison) — product-comparison companion for picking the data room platform

- Best Data Room for a Small M&A Deal — how to pick a right-sized VDR for a sub-$30M sale, the band most Denver generalist boutiques run

- Sell-Side Due Diligence (VDD Scope Matrix + 8-Week Pre-Market Stack) — the seller-commissioned diligence the banker arranges in parallel

- M&A Process Explained (8 Phases, Real Deliverables) — the full M&A lifecycle the banker's playbook sits inside

- How to Spot Serious M&A Buyers Using Data Room Analytics — the page-level engagement signals that reveal which bidders genuinely intend to bid

- Clickthrough NDA in M&A Data Rooms — the NDA gate the banker uses to admit bidders to Tier A

For Denver / Front Range sell-side mandates specifically, Peony's data room — used by 5,900+ teams — handles the four-tier permission architecture out of the box, AI auto-indexing of the seller's 500-1,500 documents into the standard folder tree in under 3 minutes, per-bidder watermarking and screenshot blocking on every page render, moderated Q&A threading with AI-drafted answers and page citations, and pre-scheduled permission-tier transitions that mechanically enforce the process letter. Peony Data Room at $52 per admin per month replaces the $15K-$50K Datasite passthrough most Denver boutiques now meet client resistance on. Start free trial — no credit card required.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.