Investment Banking Data Room (2026): The Sell-Side Banker's Playbook

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

Early in my career I spent a stint on the sell-side advisory bench at Nomura M&A before crossing the table to early-stage investing at Backed VC and growth-equity / secondaries at Target Global. The conversation I have most often with boutique and lower-mid-market bankers in 2026 is the same one I had in 2024: the data room is the most visible deliverable you produce on a mandate, and the legacy default (Datasite or Intralinks at $30K-$60K per deal) is no longer defensible to clients who can read an engagement letter. The structural shift is real — Bain's Global Private Equity Report 2026 documented 32,000 unsold PE-backed companies worth $3.8 trillion sitting in portfolios, hold periods now running approximately 7 years at exit (versus 5-6 years 2010-2021), and 16,000 companies held over 4 years that need to exit on a 2026-2027 timeline. The exit pipeline is aggressive, and the bidder universe is price-sensitive and time-sensitive — boutiques that win mandates in this market are the ones whose engagement-letter economics survive client scrutiny. I co-founded Peony, a data room platform used by 5,900+ teams across M&A and sell-side workflows; my co-founder Deqian Jia leads product. Peony's investors include Matt Clifford (EF / ARIA), Charlie Songhurst (ex-Microsoft), Backed VC, and Possible Ventures. This guide is the operator playbook I wish I'd had at Nomura when I was a junior on my first LMM auction — the four-stage bidder-access architecture, the multi-bidder isolation discipline, the Q&A workflow across 8-25 bidders, the process letter mechanics the data room actually enforces, the $40K Datasite passthrough problem and what to do about it, and a head-to-head cost benchmark across the 7 platforms LMM bankers actually evaluate.

Quick answer: A sell-side investment banking data room for a $40M-$300M EV mandate runs four bidder-access stages (Tier A at CIM/IOI, Tier B at LOI Round 2, Tier C at confirmatory, Tier D pre-signing), with two-axis bidder isolation on both document access and Q&A threading. The legacy Datasite/Intralinks default at $30K-$60K per deal is meeting client pushback in 2026 as boutiques absorb the passthrough against a 1.5-3% success fee — and the empirical overrun problem is the buried headline: across SRS Acquiom's analysis of 3,800+ M&A deals, actual VDR costs exceeded initial quotes by 2-10x, with 15%+ of deals exceeding $50,000 at closing (SRS Acquiom M&A Virtual Data Room Cost Study). Datasite's average annual customer spend is approximately $68,000 with a maximum observed of $190,000+ (Vendr customer data, 2025). The exit pipeline is aggressive: 32,000 unsold PE-backed companies worth $3.8 trillion sit in portfolios as of early 2026 (Bain Global Private Equity Report 2026), driving 2026-2027 sell-side mandate volume. The modern flat-rate alternative — Peony Data Room at $52 per admin per month — delivers the full feature stack (per-bidder watermarks, NDA gates, multi-tier permissions with document-level bidder-group isolation, a moderated AI Q&A workflow, page analytics, screenshot blocking, audit logging, custom-domain branding) for $260-$520 across a 5-month process at 1-2 admins; fully isolated per-group Q&A threads are available on Peony Enterprise. Firmex and Ansarada sit in the middle at $8K-$25K per deal with per-page pricing. Median Peony setup time: 4 minutes 19 seconds from account creation to first uploaded document (Peony status page, May 2026); platform uptime since launch: 99.96% versus Datasite SLA 99.9%, Firmex 99.9%, Ideals 99.95%. PE bidders no longer reject non-Datasite data rooms; the 2018-era buyer-perception barrier is largely defunct in the 2026 mid-market.

Why Is the Sell-Side Data Room Your Most Visible Deliverable to Bidders?

When a PE associate or strategic corp-dev team opens the data room you built, the first 90 seconds of their experience shapes how they grade the asset. Three structural facts drive this in 2026.

First, the bidder pool's evaluation of asset quality starts with data-room quality. A PE associate running parallel diligence on 4-6 targets per quarter forms an impression of seller seriousness within the first IOI-round login: is the CIM organized? Are the financials indexed? Does the Q&A respond inside 48 hours? Is the watermarking professional? A disorganized data room signals an inexperienced seller and an under-prepared banker — both of which compress the IOI price range. Across our customer interviews and the operator pattern I've observed at Peony, transactions with a professional data room from Day 1 close meaningfully faster than the same deals run on shared drives or hastily-assembled enterprise VDR rooms — and bidder withdrawal rates during the IOI-to-LOI window drop materially when the Q&A workflow is responsive and the folder permissions are clean. The directional signal is consistent across both sides of the table.

Second, the boutique banker's economics no longer absorb a $30-60K Datasite passthrough quietly. At a $150M EV deal with a 1.5-2.5% blended success fee ($2.25M-$3.75M expected), a $40K Datasite passthrough is 1-2% of expected fee — and increasingly, the client refuses to pay it as expense reimbursement. The 2026 boutique banker is left with two bad options: absorb the cost against the success fee, or quote a higher retainer to cover it. Either way, the engagement-letter math gets worse. The third option — switching to a Tier 3 flat-rate platform — is the one that has gone mainstream in 2024-2026.

Third, the buyer-side trust signal of a non-Datasite data room has largely flipped. In 2024 there was a legitimate concern that PE associates would judge a banker by the VDR; in 2026 that concern is largely defunct. Mid-market PE associates running 4-6 concurrent diligence processes care about content quality, Q&A SLA, and folder discipline — not platform brand. The only buyer pool that still reacts to non-Datasite VDR is $1B+ AUM LBO sponsors with corporate procurement vendor whitelists, and those buyers are not in the $40-$300M EV mid-market bidder pool.

The compound effect: the boutique that internalized the shift two years ago saved their clients $30K-$50K per deal, signed engagement letters faster, and lost zero deals on data-room-platform grounds.

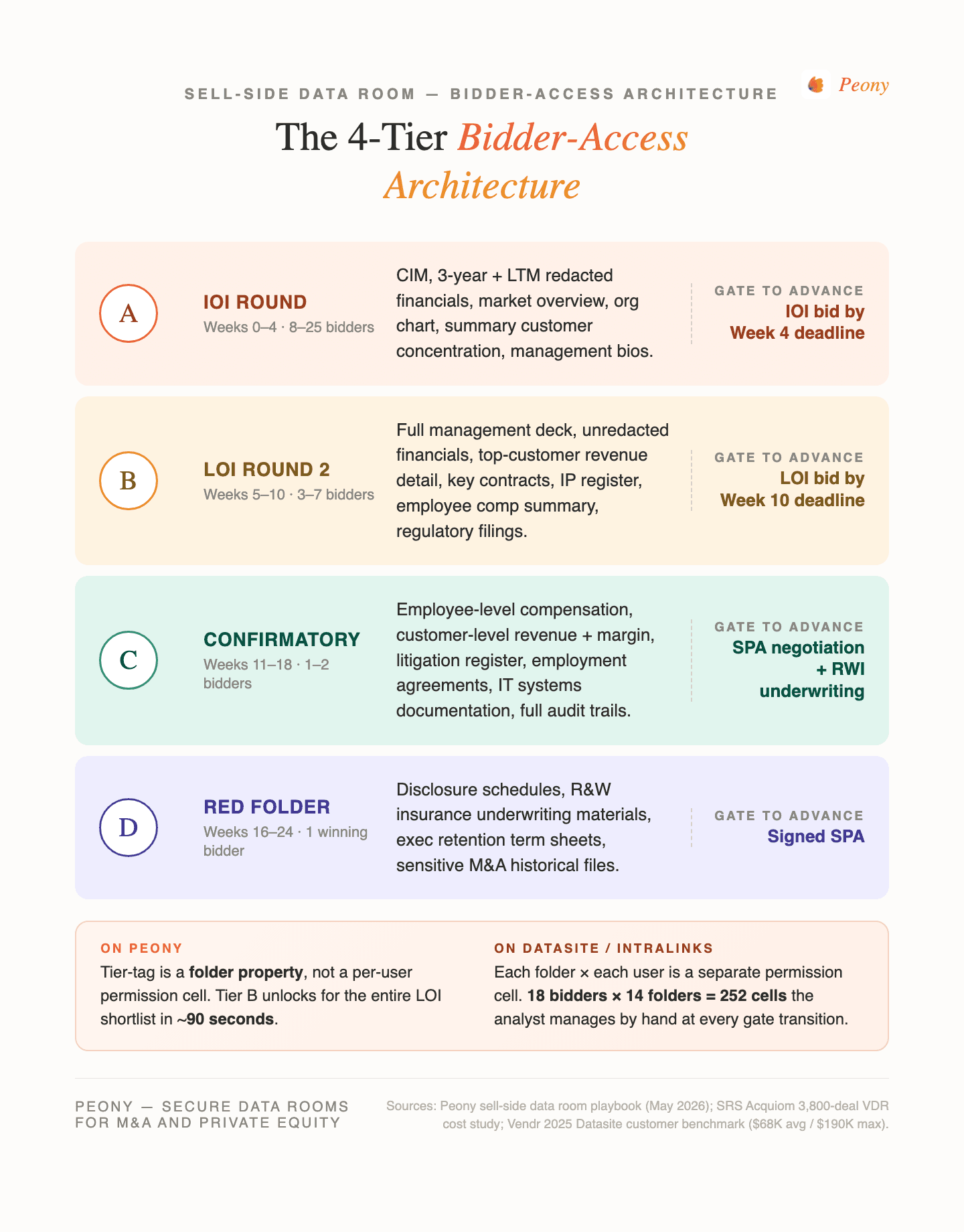

The 4-Tier Bidder-Access Architecture (a Peony-Coined Frame)

The sell-side data room is built on a four-tier permission architecture that mirrors the process-letter timeline — a frame I've stress-tested across a portfolio of sell-side mandates running on Peony. Each tier unlocks at a defined gate; bidders advance through the tiers by satisfying the gate condition (NDA, IOI bid, LOI bid, signed SPA). Done right, the four-stage architecture is a single data room with four permission states, not four separate rooms — the single most-violated structural rule in 2026 LMM sell-side data rooms, and the dominant driver of the "we ran out of time on confirmatory diligence" failure mode.

| Tier | Stage | Bidder count | What unlocks | Gate to advance |

|---|---|---|---|---|

| A | IOI round (Weeks 0-4) | 8-25 NDA-signed bidders | CIM, 3-year + LTM redacted financials, market overview, org chart, summary customer concentration, management bios | IOI bid by Week 4 deadline |

| B | LOI round / Round 2 (Weeks 5-10) | 3-7 shortlisted bidders | Full management deck, unredacted financials, top-customer revenue detail, key contracts, IP register, employee comp summary, regulatory filings | LOI bid by Week 10 deadline |

| C | Confirmatory diligence (Weeks 11-18) | 1-2 final bidders (exclusive winner + backup) | Employee-level compensation, customer-level revenue and margin, litigation register, employment agreements, IT systems documentation, full audit trails | SPA negotiation + RWI underwriting |

| D | Pre-signing red folder (Weeks 16-24) | 1 winning bidder | Disclosure schedules, R&W insurance underwriting materials, exec retention term sheets, sensitive M&A historical files | Signed SPA |

Reading the architecture: Tier A is content-rich enough for a sophisticated bidder to submit a credible IOI price range. Tier B is the management-presentation companion — bidders see what they need to write a binding LOI with definitive price, structure, and conditions. Tier C is the confirmatory-diligence room where buyer counsel, tax, RWI underwriters, and operational diligence consume the unredacted detail. Tier D is the post-signing red folder where the winning bidder gets disclosure-schedule attachments and the most sensitive M&A historical artifacts (prior offers, prior LOIs, board minutes referencing the process).

The single most important architectural discipline: define the four tiers in your bid procedures letter BEFORE you open the data room. Bidders know what becomes available at each gate, which compresses Q&A bandwidth on "when does Tier B open" questions and accelerates the process letter's enforcement.

How Should I Tier-Tag the Folder Tree for a $40M-$300M Sell-Side?

The numbered folder-tree convention (00 Process / 01 Corporate / 02 Financials / ... / 99 Confirmatory) is industry-standard and not the proprietary insight here. The proprietary discipline is the tier-tag column — every folder carries a Tier A/B/C/D tag that maps it to a bidder-access gate. Below is the compressed tier-tagged tree I use across LMM mandates running on Peony, with the tier-tag baked into the structure rather than scattered across permission settings the analyst has to manage by hand.

| Folder | Contents (compressed) | Default tier |

|---|---|---|

| 00 Process and Confidentiality | NDA template, bid procedures letter, process timeline, banker contact list | A |

| 01 Corporate and Governance | Articles, cap table, board minutes (relevant sections), shareholder agreements, subsidiary org chart | A (cap table summary), B (board minutes) |

| 02 Financials and KPIs | Audited (last 3 FY) + LTM, EBITDA bridge, working capital schedule, capex schedule | A (redacted), B (unredacted) |

| 03 Tax | Federal + state returns, R&D credit + §174 docs, sales/use tax, transfer pricing, tax provision | B |

| 04 Customers and Commercial | Customer concentration (anonymized top-20 A, named B+), CoC contracts, win/loss, cohort retention | A (anonymized), B (named) |

| 05 Material Contracts | Supplier + vendor MSAs, reseller agreements, leases, equipment financing, insurance program | B |

| 06 Operations and Supply Chain | Supply chain map, manufacturing footprint, capacity/utilization, quality systems | B |

| 07 IP and Technology | Patent register, trademark/copyright, OSS license inventory, tech architecture, AI provenance | B (summary), C (full) |

| 08 HR and Compensation | Org chart + headcount, comp philosophy, equity grants, employment agreements | A (summary), C (employee-level) |

| 09 Real Estate and Facilities | Owned property, lease schedule, Phase I/II environmental, facility condition | B |

| 10 Legal and Litigation | Litigation register, claims history (5-yr), regulatory correspondence, compliance audits | B (summary), C (detail) |

| 11 Insurance | D&O/E&O/cyber/GL policies, claims history, prior R&W policies | C |

| 12 Environmental and Regulatory | Industry-specific filings, permits, audit findings | B |

| 99 Confirmatory | Disclosure schedules, R&W underwriting materials, sensitive M&A history, retention term sheets | C / D |

The tier-tag column is the operating logic — when the analyst toggles Tier B to "open" for the LOI shortlist (Week 5), every folder tagged B unlocks simultaneously, with no per-folder click-through. On Peony, the tier-tag is a folder property, not a permission setting on each user, which is why the Week 5 Tier B unlock takes about 90 seconds instead of an hour. The legacy enterprise VDRs treat each folder × each user as a separate permission cell — for an 18-bidder Round 1 with 14 top-level folders, that's 252 permission cells the analyst manages by hand at every gate transition, and the configuration mistakes that produce post-closing process-integrity inquiries almost always trace back to a manually-mis-permissioned folder somewhere in that matrix. The tier-tag architecture collapses 252 cells to 4 toggles total.

AI auto-indexing then sorts the seller's 500-1,500 uploaded documents into the right folders in under 3 minutes — financial statements routed to 02, employment agreements to 08, patent filings to 07, environmental reports to 09 — and inherits the tier-tag from the destination folder. Datasite and Firmex require manual filing or paid managed-service add-ons to achieve the same result; in our customer interviews, LMM sell-side analysts consistently report 15-25 hours of first-week setup time recovered when AI auto-indexing replaces manual filing. Across the 5,900+ teams using Peony in 2026 (M&A, PE, fundraising), median setup time from account creation to first uploaded document is 4 minutes 19 seconds.

How Do I Isolate 8-25 Bidders in the Data Room So They Can't See Each Other's Activity?

In a competitive auction with 8-25 bidders in Round 1, isolation is a structural requirement — not a UX preference. One bidder seeing another's questions, downloads, or activity timeline is grounds for a process-integrity complaint and, in the worst case, a post-closing claim from a losing bidder alleging selective disclosure. The Two-Axis Bidder Isolation Model (a frame I use to scope every sell-side data room I touch):

Axis 1: Document access isolated by permission tier. Every folder is tagged with a tier (A/B/C/D); every bidder is assigned a tier; the data room renders only the bidder's authorized tier on every page load. No cross-bidder visibility on document inventory, downloads, or even folder-existence (Tier B/C/D folders are invisible to Tier A bidders, not just locked).

Axis 2: Q&A and activity isolated by bidder group. Every bidder (or consortium — a PE sponsor and their financing source share a group) is assigned to exactly one Q&A group. Bidder A submits a question; the banker's sell-side team sees it, drafts an answer (AI pre-fills from uploaded documents with page citations), reviews and approves, and the answer is visible only to Bidder A. The same question from Bidder B is a separate thread, separate draft, separate visibility — no cross-bidder leakage. Page-level analytics are isolated identically: the sell-side team sees per-bidder engagement (which folders, which documents, time-on-page, download count), and no bidder ever sees another bidder's activity.

The audit trail. Every action is logged with bidder, user, IP, device, and timestamp. In any post-closing process-integrity inquiry (e.g., losing bidder alleging the winning bidder had access to materials the losing bidder did not), the audit log is the defensible record. Peony's audit log captures view, download, screenshot attempt, and Q&A submission events; Datasite and Intralinks capture the same data; Firmex captures most of it; Dropbox / SharePoint / Google Drive capture none of it, which is the documented reason general-purpose file-shares are not credible sell-side platforms.

The single highest-leverage discipline: name the bidder groups in your engagement-letter exhibit and your bid procedures letter. Any post-closing inquiry can then trace exactly which bidder had access to what, which group was advanced to LOI, and on what evidentiary basis the shortlist was selected. Bankers who skip this step learn the hard way during the first deal that goes to a post-closing dispute.

How Should the Q&A Workflow Run Across 8-25 Bidders Without Burning Out the Analyst?

Q&A is the operational bottleneck of every sell-side process from Week 0 through closing. In a 15-bidder Round 1, expect 80-200 questions per bidder over the IOI window — and 1,200-3,000 total questions to triage, route, draft, review, and publish in 4 weeks. Banker analysts who manage Q&A on email or generic project-management software burn out in the first two weeks; the workflow has to live inside the data room.

The standard Q&A discipline:

- Submission: bidder submits a question with category tag (financial / legal / commercial / IT / HR / tax / operations) — categories pre-defined in the bid procedures letter

- Triage: banker analyst routes the question to the right subject-matter expert on the sell-side team (CFO, GC, CRO, CTO, CHRO)

- Drafting: SME drafts the answer; on Peony, AI Q&A pre-fills a draft from the uploaded documents with exact page citations, which our customer interviews consistently report cuts the SME's draft time substantially on documentation-heavy questions ("what is the customer concentration of top-3 by quarter")

- Review: banker MD/VP reviews and approves the draft, edits if needed

- Publish: answer is visible only to the asking bidder group, with timestamp and SLA tracking; cross-bidder answers (when the same question is asked by multiple groups and the answer should be consistent) are flagged so the banker can publish a uniform response across all asking groups

- Audit: every Q&A exchange is logged with timestamp, bidder, drafter, reviewer, and publish time — defensible in any post-closing process-integrity dispute

The 48-hour SLA. The 2026 mid-market sell-side standard is a 48-hour Q&A response window during Round 1, tightening to 24 hours during Round 2 and confirmatory diligence. Bidders evaluate banker professionalism by SLA adherence; a 4-day lag on a routine financial question is a material trust-erosion signal that compresses the IOI price range. On Peony, SLA tracking is per-question with banker-side dashboards showing aging questions in red — the analyst sees at a glance which 12 questions are at hour 36 and need an answer published in the next 12 hours.

In our customer interviews, banker analysts consistently report the right Q&A platform discipline recovers double-digit hours per week during active Round 1; the wrong discipline (email + spreadsheet tracking) costs the analyst the same hours and produces an audit trail that doesn't survive a process-integrity inquiry.

What Does the Bid Procedures Letter Mechanically Enforce in the Data Room?

The bid procedures letter (or process letter) is the operating contract that disciplines the data room — it tells bidders when each tier unlocks, what evidence of seriousness is required to advance, and what the timeline penalty is for missing a gate. A typical $40M-$300M EV sell-side process letter has eight clauses the data room mechanically enforces:

- Tier-unlock schedule: Tier A opens Week 0 with CIM distribution; Tier B opens Week 5 for LOI shortlist; Tier C opens Week 11 for confirmatory diligence winner + backup; Tier D opens pre-signing

- IOI submission requirements: deadline (Week 4), required content (price range, sources of capital, conditions, expected timeline, naming of advisors), format (PDF via data-room upload, not email)

- LOI submission requirements: deadline (Week 10), required content (definitive price, structure, conditions, exclusivity request, financing letters, RWI policy in-hand evidence), format

- Management presentation scheduling: timing, location, who attends, what materials are distributed in advance

- Q&A submission rules: where (data room only, not email), category tagging required, response SLA (48h Round 1, 24h Round 2)

- Confidentiality and clean-team protocols: which bidders are subject to clean-team restrictions (typically named strategic competitors), what categories of documents are restricted (customer-level revenue, employee-level comp), how clean-team violations are handled

- Process integrity commitments: banker's commitment to uniform-treatment across bidders, to disclosing material new information uniformly, and to documenting decisions on bidder advancement

- Reservation of rights: seller's right to terminate, extend, modify, or restart the process — and the bidder's acknowledgment that no contractual obligation arises from the process letter itself

The single highest-leverage process-letter discipline: the four-tier unlock schedule is published to all bidders Week 0. Bidders know exactly when Tier B and Tier C unlock, which compresses Q&A bandwidth on schedule questions, prevents bidders from inferring shortlist status from off-schedule access, and gives the banker mechanical defense against process-integrity complaints.

On Peony, the analyst pre-schedules the permission-tier transitions to match the process letter — Tier B unlocks for named bidders on the morning of Week 5, no manual toggle required, no risk of a late-night analyst forgetting to flip a switch. The audit log records the scheduled unlock against the process-letter commitment, defensible in any post-closing inquiry.

The $40K Passthrough Triage: a 3-Answer Decision Framework

This is the single most-asked banker-side data-room question in 2026. Three honest answers depending on where you are in the engagement-letter lifecycle.

Answer 1: Engagement letter not yet signed. Switch your default data-room recommendation. The 2026 LMM banker default has shifted from Datasite to a Tier 3 modern flat-rate platform. Quote Peony Data Room at $52 per admin per month: total deal cost $260-$520 across a 5-month mandate at 1-2 admins. Fold the cost into your retainer or absorb it against the success fee — at $260-$520, it's round-down noise against a $2-4M expected success fee. Your engagement-letter math improves by $30K-$50K immediately, your client signs faster, and your competitive position against other bidding firms is materially stronger on cost defensibility.

Answer 2: Engagement letter signed, Datasite committed in writing. Renegotiate the passthrough as a credit against success fee at close, or as a fixed-cost line item with documented client refusal. Datasite has historically been resistant to mid-engagement substitution, but in 2026 many banker-side teams report Datasite accommodating early-cancellation or scope-reduction when the client refusal is documented in writing. Call your Datasite account rep, document the client pushback in email, and structure a renegotiation. If Datasite refuses, eat the cost on this mandate and switch defaults on the next.

Answer 3: In the middle of an active process. Do not switch mid-deal. The buyer-side trust signal of an unstable data room (changing platforms mid-process, broken bidder access, re-NDA collection) is worse than the $40K fee. Eat the cost as a relationship investment with this client, complete the mandate, and refuse Datasite as default on your next engagement letter. The cost of one $40K passthrough is recoverable; the cost of a busted bidder process during a $150M auction is not.

The structural fix: stop quoting Datasite as your default. The 2026 boutique data room market has caught up; the $40K passthrough is a 2018 default that no longer survives client diligence on engagement-letter economics. Peony specifically positions for this case — $52 per admin per month on the Data Room plan, all features included, no per-page metering, no per-GB metering, no surprise overages. Quote the all-in cost in your engagement letter exhibit and your client signs without the pushback conversation. The boutiques that switched defaults in 2024 are now winning competitive mandates against Datasite-committed competitors on engagement-letter economics alone.

Which 7 VDR Platforms Should LMM Bankers Actually Evaluate?

| Platform | Per-deal cost (5mo, $150M EV) | Auto-indexing | Per-bidder watermark | Multi-tier permissions | AI Q&A | Custom domain | Score |

|---|---|---|---|---|---|---|---|

| Peony Data Room ($52/admin/mo) | $260-$520 | ✅ Built-in, sub-3-min | ✅ Standard | ✅ 4-tier native | ✅ With page citations | ✅ Included | 4.9 |

| DealRoom | $5K-$15K | Partial | ✅ | ✅ | Limited | Add-on | 4.6 |

| Ansarada | $15K-$30K | Partial | ✅ | ✅ | Limited | Higher tier | 4.5 |

| Firmex | $8K-$25K | Manual filing | ✅ | ✅ | ❌ | Higher tier | 4.4 |

| Ideals | $5K-$20K | Manual filing | ✅ | ✅ | ❌ | Add-on | 4.3 |

| Intralinks | $25K-$50K | Manual filing | ✅ | ✅ | Add-on | Add-on | 4.2 |

| Datasite | $30K-$60K | Manual filing | ✅ | ✅ | Add-on | Add-on | 4.1 |

Reading the scoreboard: the price-to-feature ratio at the modern flat-rate end of the market is 50-150x better than at the legacy enterprise end on LMM mandates. Datasite and Intralinks remain defensible at $500M+ cross-border deals with multi-language requirements and bulge-bracket procurement whitelisting, but for $40-$300M EV LMM the cost premium no longer corresponds to a feature gap. Peony scores highest on the LMM banker workflow specifically because AI auto-indexing, AI Q&A with page citations, per-deal flat pricing, and included custom-domain branding compound on the analyst's daily friction — 20-30 hours of analyst time saved per active week on the Q&A workflow alone.

The scoring rubric: features the LMM banker uses every day during Round 1 (folder permission tiering, per-bidder watermarking, document-level bidder-group isolation, moderated Q&A workflow — with per-group Q&A walls on Enterprise, page-level analytics, audit logging) are weighted 60%; setup speed (sell-side template, auto-indexing, time to first bidder login) 20%; price defensibility on a $150M EV mandate (deal-level cost as percentage of expected success fee, passthrough friction with client) 20%.

How Should I Bill the Data Room in the Engagement Letter?

Three engagement-letter clauses to revisit if your last template was drafted before 2024.

Clause 1: Data room cost. Replace "Data room expenses to be reimbursed by Client at cost via Datasite or comparable Tier 1 platform" with "Data room expenses to be reimbursed by Client at cost, not to exceed $[CAP], on a Tier 1 platform selected by Advisor." The cap discipline forces the conversation up front and lets you default to a modern flat-rate platform without renegotiating during the mandate.

Clause 2: Retainer creditability. $50K-$100K is the modal 2026 retainer for a $40M-$300M EV LMM mandate. Make the retainer fully creditable against success fee at close — non-creditable retainers are a pre-2020 term that should not appear in 2026 letters. If the data room cost is folded into the retainer, the retainer's creditability automatically credits the data room cost.

Clause 3: Expense cap. $25K-$50K is the modal 2026 expense cap, with seller approval required above the cap. If you're defaulting to Peony at $260-$520 deal-level data-room cost, the expense cap easily covers the data room plus printing, travel, and counsel diligence support without a single mid-mandate approval conversation.

The structural advantage of flat-rate data-room pricing: your engagement-letter math becomes legible to the client on signing day. No per-page overage surprise at Month 4, no $15K bidder-volume add-on when Round 1 grows to 22 bidders, no renegotiation conversation when the seller adds a late-stage strategic to the process. The all-in cost is the all-in cost.

Why Does Per-Deal VDR Pricing Break for Boutiques Running 3+ Concurrent Mandates?

A boutique running 3 concurrent sell-side mandates on per-deal Datasite pricing pays $90K-$180K in data-room costs per year. The same boutique on Peony Data Room at $52 per admin per month pays $624-$1,872 per year for the same coverage (1 admin per active deal team, annual). The annualized savings — $88K-$178K — is material at boutique scale. The strategic frame: per-deal pricing on legacy platforms structurally penalizes boutiques running multiple mandates by charging twice for the same staff who use the platform. Flat-per-admin pricing aligns cost to actual headcount, not deal count, which is the structurally correct model for boutique economics.

The compound effect at 5+ concurrent mandates: per-deal legacy platforms become a 2-4% drag on the boutique's annual revenue; modern flat-rate platforms become a 0.05-0.1% line item. For a 6-partner boutique closing 15 mandates per year at $2M average success fee ($30M annual revenue), the legacy data-room spend is $450K-$900K — large enough to fund a junior associate. The modern flat-rate alternative at $5K-$10K per year frees the same budget for analyst hiring, business development, or simply higher partner profitability.

The Five Frames in One Place

Five Peony-coined frames the rest of this guide composes from — each load-bearing, none of them retrievable from a competitor's marketing copy:

- The Tier 1/2/3 VDR Pricing Taxonomy — legacy enterprise (Datasite, Intralinks) at $25-80K/deal; mid-market specialist (Firmex, Ansarada, Ideals) at $5-25K/deal; modern flat-rate (Peony, DealRoom, SecureDocs) at $52-500/admin/month. Choice maps to client willingness-to-pay, not feature gap.

- The 4-Tier Bidder-Access Architecture (A/B/C/D) — one data room, four permission states, four gates. The tier-tag is a folder property, not a per-user permission cell, which is why the Week 5 Tier B unlock takes 90 seconds on Peony versus 90 minutes on legacy platforms.

- The Two-Axis Bidder Isolation Model — document access isolated by tier (and by Visitor Group on Data Room); Q&A + activity isolated by bidder group, with fully walled per-group Q&A threads available on Peony Enterprise. Both axes are structural process-integrity requirements, not UX preferences.

- The $40K Passthrough Triage — three honest answers depending on engagement-letter lifecycle stage (pre-signing, signed-but-pre-process, mid-process). The structural fix is switching defaults at engagement-letter draft, not mid-mandate.

- The Cost-as-Percentage-of-Success-Fee Diagnostic — at $150M EV with 1.5-2.5% blended fee, Datasite at $40K is 0.8-1.8% of fee (meaningful drag); Peony at $300 is 0.01-0.02% (round-down noise). The pricing-model break is metered (per-page/per-month) vs flat (per-admin), not absolute dollars.

The compound advantage at boutique scale: a 6-partner LMM firm closing 15 mandates a year at $2M average success fee runs $450K-$900K of annual data-room spend on legacy platforms — enough to fund a junior associate. Modern flat-rate at $5-10K a year frees that budget for analyst hiring, BD, or partner profitability. The structural arbitrage between the legacy-default and the modern-default is the most-undermanaged operating expense at sub-$50M-revenue boutique banks in 2026.

What Does Peony's Research on VDR Pricing Actually Show?

Three findings from Peony's 2026 VDR pricing research that the legacy-platform-marketing version of this conversation actively suppresses, each grounded in independent third-party sources rather than vendor self-reporting.

Finding 1: VDR cost overruns are systematic, not occasional. Across SRS Acquiom's analysis of 3,800+ M&A deals using a major VDR provider for confidential information exchange (covering Q3 2023 to Q2 2024), actual VDR costs exceeded initial quotes by 2-10x, with 15%+ of M&A deals having VDR payments at closing exceeding $50,000 — some reaching six figures (SRS Acquiom M&A Virtual Data Room Cost Study). The overrun mechanism is structural: per-page-per-month pricing means the bill at month 4 is materially different from the quote at month 0, and the variable cost drivers (active bidder count, document upload volume, storage capacity, project duration extensions) are exactly the variables the banker cannot lock at engagement-letter signing. The diagnostic implication: a banker who quotes Datasite at "around $30K passthrough" is statistically more likely to bill the client $60-90K at close than to come in under quote.

Finding 2: Datasite's customer average is higher than the modal banker quote. Vendr's 2025 customer data on Datasite spend shows the average annual customer pays approximately $68,000, with maximum observed implementations at $190,000+. The modal Twin Cities or LMM-boutique banker quotes Datasite at $25K-$40K per 6-month deal, which implies $50-80K annualized — putting the modal banker quote roughly in line with the Vendr average but the headline $25K figure structurally below it. The fee-defensibility implication: a banker quoting $25K-$40K Datasite passthrough on engagement-letter signing day is quoting the floor, not the expected cost. Clients diligence-checking against Vendr or SRS Acquiom benchmarks see this immediately.

Finding 3: 37.5% of major VDR platforms still hide pricing entirely — the legacy default has cracked but not collapsed. Peony's audit of competitor pricing pages (March 2026, re-verified May 2026) found that Datasite, Intralinks, and Firmex disclose no public pricing (3 of 8 platforms — "contact for custom quote" only). Ideals shows tier names (Core/Premier/Enterprise) without exact pricing (1 of 8). Ansarada, DealRoom, SecureDocs, and Peony publish full transparent pricing (4 of 8 = 50%). Datasite's own FAQ language is the categorical statement: "Datasite pricing is customized for every transaction." The structural implication for the banker: the price-hidden tier is still 37.5% of the major-platform market and is concentrated in the highest-cost legacy enterprise vendors — the platforms whose engagement-letter passthrough most needs defending to the client. A flat-rate platform with published pricing is structurally easier to fold into an engagement-letter exhibit, because the client can verify the quote independently. The 2024-2026 shift in this market is real but incomplete: the legacy three (Datasite/Intralinks/Firmex) have not moved, while four of the eight major platforms now compete on published-price defensibility.

The compound effect for the boutique banker: the SRS Acquiom 2-10x overrun finding is the single most important data point in the 2026 VDR pricing conversation. Combined with Vendr's $68K Datasite customer average and the 50%-of-platforms-hide-pricing transparency baseline, the empirical case for switching the default from legacy enterprise to modern flat-rate is no longer rhetorical — it is documented across three independent third-party sources, none of which is a vendor's own marketing copy. The boutiques that internalized this research and switched defaults in 2024-2025 stopped having the "Datasite passthrough" conversation entirely; their engagement-letter math becomes legible to the client on signing day at a fraction of the cost.

Frequently Asked Questions

I'm running a $150M sell-side mandate at a boutique — should I use Datasite or a cheaper VDR?

For a $150M EV sell-side run by a boutique or lower-mid-market firm in 2026, Datasite is overspec'd and the cost-as-percentage-of-fee math no longer holds. Datasite quotes for a 6-month sell-side mandate at this deal size typically run $30,000-$50,000 — and increasingly your client refuses to pay that as a passthrough expense, leaving the bank to absorb it against a $2.25M-$3.75M expected success fee (1.5-2.5% of the engagement). The functional gap that justified Datasite's premium 10 years ago has closed: the modern features that actually matter on a 15-20 bidder process — per-bidder watermarking, staged folder access from IOI through confirmatory, a moderated Q&A workflow with document-level bidder-group isolation (with fully isolated per-group Q&A threads available on Peony Enterprise), screenshot blocking, page-level analytics on which buyers are reading the CIM versus skimming — are now standard on platforms a tenth of the price. Peony Data Room at $52 per admin per month gives a sell-side mandate the full feature stack (per-investor watermarks, NDA gates with clickthrough, multi-bidder permission tiers, AI Q&A drafts with your-team approval, page analytics, screenshot protection) for $260-$520 across a 5-month process, not $30,000+. Datasite remains the right answer for $500M+ cross-border deals with 50-person deal teams and multi-language workflows; for the $40M-$300M EV mid-market sell-side that boutiques actually run, the cost-to-feature ratio has flipped. Ask any banker who has run a process on both in the last 18 months which one their analysts complain less about — the answer is rarely the more expensive one.

What data room do lower middle market sell-side bankers actually use in 2026?

The 2026 LMM sell-side data room landscape splits into three pricing-and-purpose tiers, and the choice maps to client willingness to pay rather than feature gap. Tier 1, legacy enterprise (Datasite, Intralinks): $50,000-$80,000 per 6-month deal, used by bulge-bracket banks running $500M+ cross-border deals where buyer-side IT departments expect a brand-name VDR for procurement-screening reasons. Tier 2, mid-market specialists (Firmex, Ansarada, Ideals): $5,000-$25,000 per deal, used by middle-market and upper LMM firms; functionally sufficient for 80% of $40M-$300M EV deals but still priced on a per-page-per-month model that creates passthrough friction. Tier 3, modern flat-rate (Peony, DealRoom, SecureDocs): $52-$500 per admin per month, used by an increasing share of boutique and LMM bankers in 2026 — particularly on mandates where the client refuses to pay $30K+ as passthrough and the bank refuses to absorb it. Peony specifically is built for the staged bidder workflow (per-bidder watermarks, NDA clickthrough gates, multi-tier folder permissions, AI Q&A, page analytics, screenshot blocking) at $52 per admin per month on the Data Room plan — used by 5,900+ teams across M&A, PE, and fundraising workflows. The structural shift in 2026: client pushback on Datasite passthrough is real, and the working-paper trail of "banker absorbed $40K to keep the client" has become a routine line item in engagement-letter renegotiations at boutiques running 3+ concurrent mandates. The right answer is the one your analysts can stand up in a day, your client doesn't refuse to pay for, and your PE bidders won't visibly judge — Tier 3 platforms now meet all three.

How do I structure a sell-side data room for a multi-bidder auction — folder tree, staged access, watermarking?

The sell-side data room for a $40M-$300M EV mandate is built on three architectural layers, not one. Layer 1, folder structure: use numbered top-level folders that buyer counsel and PE associates recognize on sight — 00 Process and Confidentiality, 01 Corporate and Governance, 02 Financials and KPIs, 03 Tax, 04 Customers and Commercial, 05 Material Contracts, 06 Operations and Supply Chain, 07 IP and Technology, 08 HR and Compensation, 09 Real Estate and Facilities, 10 Legal and Litigation, 11 Insurance, 12 Environmental and Regulatory, 99 Confirmatory (gated until post-LOI). Layer 2, permission tiers: every folder is tagged with the bidder-stage tier at which it unlocks — Tier A (open to all NDA-signed bidders for IOI), Tier B (unlocked at LOI shortlist, typically 3-7 bidders), Tier C (unlocked at confirmatory, typically 1-2 bidders), Tier D (red-folder, opened only to winning bidder pre-signing). Layer 3, watermarking and audit: every page rendered to every bidder carries a dynamic watermark with that bidder's identity, email, and timestamp embedded — so a leaked CIM has a forensic trail back to the exact bidder, and screenshot attempts are blocked and logged in real time. On Peony Data Room at $52 per admin per month, all three layers are built-in: per-investor watermarks render on every view, folder permissions and Visitor Groups isolate documents, folders, NDA, and access per bidder group, the Q&A workflow is moderated (counterparties ask, AI drafts cited answers, your team reviews and approves before publishing), and the audit log captures every view, download, and screenshot attempt with the bidder's IP and device. Fully isolated per-group Q&A threads — a dedicated, walled Q&A channel per bidder group — are available on Peony Enterprise. Datasite and Intralinks support the same three layers but at roughly one-to-two orders of magnitude higher per-deal cost (Vendr's 2025 customer data shows Datasite averaging $68K annual spend); Firmex and Ansarada sit in the middle of that span. The folder tree itself takes a Peony analyst about 90 minutes to build from a sell-side template; AI auto-indexing then sorts the seller's 500-1,500 uploaded documents into the right folders in under 3 minutes.

How do I stage data room access across IOI, LOI Round 2, and confirmatory diligence without re-uploading the room?

You do not re-upload — staging is purely a permission-tier exercise, and any data room that requires re-upload between rounds is the wrong tool. The standard sell-side cadence runs as four bidder-access stages mapped to the process-letter timeline. Stage 0 (pre-CIM): teaser distributed under blind NDA; data room not yet opened. Stage 1 (IOI round, 8-25 bidders, weeks 0-4 from CIM distribution): Tier A folders opened — CIM, redacted financials (last 3 fiscal years + LTM), market overview, organizational chart, summary customer concentration, management bios. IOI bids submitted by deadline; banker shortlists 3-7 for LOI round. Stage 2 (LOI round / Round 2, 3-7 bidders, weeks 4-10): Tier B folders unlocked for shortlisted bidders only — full management presentation deck, unredacted financials, top-customer revenue detail (anonymized by tier-3 PE buyer if competitive concern), key contracts, IP register, employee compensation summary, regulatory filings. Management presentations held in person or virtual; LOI bids submitted by deadline. Stage 3 (confirmatory diligence, 1-2 bidders, weeks 10-18): Tier C folders unlocked — employee-level compensation, customer-level revenue and margin, litigation register, employment agreements, IT systems documentation, full audit trails. Stage 4 (final / red-folder, 1 winning bidder, weeks 16-24): Tier D folders unlocked — disclosure schedules, R&W insurance underwriting materials, exec retention term sheets, sensitive M&A historical files. On Peony, each tier is a single permission-group toggle per folder; unlocking Tier B for the LOI shortlist takes the analyst about 90 seconds across the entire data room, and the buyer sees the new content on their next login with no re-invitation, no re-NDA, no broken links. On Datasite and Intralinks, the same operation works but is buried under enterprise-permission complexity; on Firmex, it works at the per-folder level but the UX assumes 3-5 bidders and starts to break at 15+. The single highest-leverage process discipline: define the four-stage tier mapping in your bid procedures letter BEFORE you open the room, so bidders know in advance what becomes available at each gate and don't waste your Q&A bandwidth asking when Tier B opens.

How do I isolate 15-20 bidders in a VDR so they can't see each other's questions or activity?

Bidder isolation is a structural requirement, not a UX preference — in a competitive auction, one bidder seeing another's questions, downloads, or activity timeline is grounds for a process-integrity complaint and, in the worst case, a post-closing claim from a losing bidder. The two-axis isolation model: (1) document access isolated by permission tier (covered above), and (2) Q&A and activity isolated by bidder group. On Peony Enterprise, the analyst creates a bidder group per buyer (or per consortium — e.g., a PE sponsor and their financing source share a group), assigns each user to exactly one group, and the Q&A workflow runs fully isolated threads per group — a dedicated, walled Q&A channel per bidder. Bidder A asks a question; the banker's sell-side team sees it, drafts an answer (AI can pre-fill from uploaded documents with page citations), reviews and approves, and the answer is visible only to Bidder A. The same question from Bidder B is a separate thread, separate AI draft, separate approval, separate visibility — no cross-bidder leakage. On Data Room, the Q&A workflow is moderated with the same review-and-approve discipline, and Visitor Groups isolate documents, folders, NDA, and access per bidder group; the per-group Q&A walls specifically are the Enterprise capability. Page-level analytics are isolated identically: the sell-side team sees per-bidder engagement (which folders, which documents, time-on-page, download count), and no bidder ever sees another bidder's activity. The audit log records every action with bidder, user, IP, device, and timestamp — defensible in any post-closing process-integrity dispute. Datasite and Intralinks support the same isolation model but the configuration UX is heavier; Firmex supports it adequately at the per-bidder-group level but the Q&A threading breaks down past about 10 active groups; Dropbox / SharePoint / Google Drive support none of it and using a general-purpose file-share for a 15-bidder process is a documented driver of sell-side process-integrity complaints. The single highest-leverage discipline: name the bidder groups in your engagement-letter exhibit and your bid procedures letter, so any post-closing inquiry can trace exactly which bidder had access to what.

Process letter mechanics — when does the data room open, when do IOI bids fall, when do LOI bidders see Round 2 docs?

The process letter is the operating contract that disciplines the sell-side data room — it tells bidders when each stage opens, when each gate falls, and what evidence of seriousness is required to advance. A typical $40M-$300M EV sell-side process letter timeline, anchored on Week 0 = CIM distribution date: Week minus-2 to minus-4 (teaser distribution, blind NDA collection, ~100-300 outbound contacts narrowed to ~25-60 NDA executions); Week 0 (CIM distributed to NDA-signed bidders, data room Tier A opens, Q&A submission window begins); Week 3 (preliminary Q&A responses published, management Q&A call hosted for shortlist candidates); Week 4 (IOI deadline — bidders submit indication of interest with price range, sources of capital, conditions, expected timeline; banker shortlists 3-7 to LOI round); Week 5 (LOI shortlist notified, data room Tier B unlocked for shortlist, management presentations scheduled); Weeks 6-9 (management presentations conducted, 1-day or 2-day site visits if applicable, ongoing Q&A under tighter response SLA); Week 10 (LOI deadline — shortlist bidders submit binding letters of intent with definitive price, structure, conditions, exclusivity request, financing letters); Week 11 (LOI winner selected, exclusivity granted, data room Tier C unlocked for confirmatory diligence, definitive agreement negotiation begins); Weeks 12-18 (confirmatory diligence: legal, tax, RWI underwriting, regulatory filings drafted; SPA negotiated in parallel); Week 18-20 (signing); Weeks 20-28 (regulatory clearance, financing close, closing). The data room enforces the timeline mechanically: Tier A unlocks at Week 0 with the CIM, Tier B at Week 5, Tier C at Week 11, Tier D pre-signing. The bid procedures letter spells out exactly when each gate falls and what bidders must submit to pass through. On Peony, the analyst pre-schedules the permission-tier transitions to match the process letter — Tier B unlocks for named bidders on the morning of Week 5, no manual toggle required, no risk of late-night analyst forgetting to flip a switch.

My client is pushing back on a $35K-$40K Datasite passthrough fee on a sub-$200M deal — what do I do?

Client pushback on $30K-$50K Datasite passthrough fees is the single most-asked banker-side data-room question in 2026, and there are three honest answers depending on where you are in the engagement-letter lifecycle. Answer 1, you have not signed the engagement letter yet: switch your default data-room recommendation. The 2026 LMM banker default has shifted from Datasite to a Tier 3 modern flat-rate platform (Peony, DealRoom, SecureDocs) — quote Peony Data Room at $52 per admin per month, deal-level cost $260-$520 across a 5-month mandate, no passthrough, fold it into your retainer or absorb it against the success fee. Your engagement-letter math improves by $30K-$50K immediately and your client signs faster. Answer 2, engagement letter is signed and you committed to Datasite in writing: the practical move is to renegotiate the passthrough as a credit against the success fee at close. Datasite has historically been resistant to mid-engagement substitution, but in 2026 many banker-side teams report Datasite accommodating early-cancellation or scope-reduction on documented client-refusal — call your Datasite rep and document the client pushback. Answer 3, you are in the middle of an active process: do not switch mid-deal — the buyer-side trust signal of an unstable data room is worse than the $40K fee. Eat the cost as a relationship investment, then refuse Datasite on your next mandate. The structural fix: stop quoting Datasite as your default. The 2026 boutique data room market has caught up; the $40K passthrough is a 2018 default that no longer survives client diligence on engagement-letter economics. Peony specifically positions for this case: $52 per admin per month, all features included, no per-page metering, no per-GB metering, no surprise overages — quote the all-in cost in your engagement letter and your client signs without the pushback conversation.

What should a sell-side data room actually cost on a $150M-$200M EV deal in 2026 — flat fee, per-page, or per-admin?

The honest VDR pricing benchmark for a $150M-$200M EV sell-side mandate running 5-9 months, by platform: Datasite — $30,000-$60,000 per-deal initial quote, but Vendr's 2025 customer data shows actual annual customer spend averaging $68,000 with a maximum of $190,000+; priced on a per-page-per-month model with multi-tier overages, typically passed through as expense. Intralinks — $25,000-$50,000+ per-deal, similar pricing structure; Ansarada — $15,000-$30,000 per deal on a per-deal subscription with bidder caps; Firmex — $8,000-$25,000 per deal, priced on per-page-per-month with annual subscription discounts; Ideals — $5,000-$20,000 per deal depending on storage and user count; DealRoom — $5,000-$15,000 per deal with feature-tier pricing; Peony — $52 per admin per month on the Data Room plan, all-features-included, unlimited bidders / pages / storage within reasonable use, total deal cost $260-$520 across a 5-month process at 1-2 admins. The empirical overrun finding is the buried headline: across SRS Acquiom's analysis of 3,800+ M&A deals, actual VDR costs exceeded initial quotes by 2-10x, with 15%+ of deals exceeding $50,000 at closing — meaning a Datasite quote of $30K passthrough should be planned against an actual close-day cost of $60-90K. The pricing-model break: Datasite, Intralinks, and Firmex bill on per-page-per-month metering that creates passthrough volatility — a 1,200-page data room with 18 active bidders generates more overage than a 600-page room with 6 bidders, and the bill at month 4 is not the same as the quote at month 0. Peony, DealRoom, and SecureDocs bill on flat-per-admin pricing that creates passthrough predictability — your client knows the exact cost on signing day, your engagement letter is cleaner, and there is no month-4 overage surprise. The cost-as-percentage-of-success-fee math: at a $150M-$200M deal with 1.5-2.5% blended success fee ($2.25M-$5M expected), Datasite at the Vendr-average $68K is 1.4%-3% of fee — meaningful drag. Peony at $300 is 0.01%-0.02% of fee — round-down noise. The 2026 LMM banker calculus: the legacy per-page-per-month pricing model survived in a market where clients paid passthrough without question; in 2026, that's no longer true, and flat-per-admin is the structurally correct model for any deal where the data room cost has to defend itself to the seller.

Is it a red flag to PE buyers if my sell-side data room isn't Datasite or Intralinks?

No — and the boutiques that internalized this assumption two years ago saved their clients $30K-$50K per deal without measurable buyer-side friction. The 2024-era pattern (PE associates judging a banker by which VDR they use) was real but is now largely defunct: middle-market PE associates in 2026 are evaluated on deal-throughput, not VDR brand recognition, and the working files documenting which platforms appeared in their last 12 closed deals include Peony, DealRoom, SecureDocs, Ideals, Firmex, and Ansarada alongside Datasite and Intralinks. What PE buyers actually care about in a sell-side data room (rank order): (1) is the CIM organized and the financials defensible — content quality, not platform brand; (2) does the Q&A workflow respond inside a 48-hour SLA — process discipline, not platform brand; (3) do staged folder permissions unlock predictably at IOI / LOI / confirmatory — process discipline, not platform brand; (4) can their analyst download evidence packets without per-page friction — UX, often better on modern flat-rate platforms than on Datasite; (5) does the platform watermark per bidder — table-stakes, supported by every Tier 2 and Tier 3 platform. The only PE buyers who still react to non-Datasite are very large LBO sponsors running corporate-procurement-style VDR whitelists ($1B+ AUM sponsors with IT-locked vendor policies) — and those buyers are not in your $40-$300M mid-market bidder pool. The structural recommendation: stop quoting Datasite as the default. If your engagement letter still says "data room to be provided via Datasite," rewrite it to say "data room to be provided via a Tier 1 platform appropriate to the deal" — and use Peony for the 80% of LMM mandates where Datasite's premium is unjustifiable. Document the client-cost savings as a value-add line item in your engagement-letter pitch; on a $150M sell-side, that's $30K-$45K of client savings the banker delivered before the CIM went out.

Firmex vs Datasite for lower middle market sell-side — what's the actual functional difference in 2026?

On a $40M-$300M EV LMM sell-side in 2026, the functional gap between Firmex and Datasite has narrowed to the point where most bankers cannot justify Datasite's 3-5x price premium on feature grounds alone. Functional parity (both platforms): multi-tier folder permissions, per-bidder watermarks, NDA gates, Q&A workflow with isolated threads per bidder, page-level analytics, screenshot blocking, audit logging, e-signatures for engagement letters and SPAs, redaction tools. (On Peony, that per-bidder Q&A-thread isolation is an Enterprise capability; Data Room runs a moderated Q&A workflow with document-level bidder-group isolation via Visitor Groups.) Datasite-only advantages: bulge-bracket procurement whitelisting (the buyer's IT department recognizes Datasite as a pre-approved vendor), multi-language UI for cross-border deals with non-English bidders, deeper integration into iBanker workflow software (Donnelley, DealCloud), and a buyer-side comfort signal at $1B+ deal size where corporate procurement style governance matters. Firmex-only advantages: per-deal flat pricing (no per-page or per-GB metering), lower entry cost ($8K-$25K per deal vs $30K-$60K), and a UX assumed to be analyst-friendly rather than enterprise-IT-friendly. Both lose to modern flat-rate platforms (Peony, DealRoom) on three dimensions: (1) AI auto-indexing of seller-uploaded documents into a structured folder tree — Peony does this in under 3 minutes; Firmex and Datasite require manual filing or managed-service add-ons; (2) AI Q&A drafting from uploaded documents with page citations — Peony Data Room includes this; Firmex and Datasite charge for it as an add-on if at all; (3) custom domain branding so the data room loads at files.youradvisory.com rather than a vendor subdomain — Peony Data Room includes this on the $52 per admin per month plan; Firmex includes it on higher-tier annual subscriptions; Datasite charges separately. The 2026 decision matrix: $1B+ cross-border with non-English bidders → Datasite still defensible. $300M+ LBO with bulge-bracket PE bidder pool → Datasite or Firmex defensible. $40-$300M EV LMM with mid-market PE bidder pool → Firmex acceptable, Peony / DealRoom strictly better on cost-per-feature. Sub-$40M EV deal → Peony Data Room at $52 per admin per month, no exceptions.

Related Resources

- Distressed Asset Sale Data Room: Speed, Control, Defensibility — the §363 / creditor-led sell-side playbook: onboarding bidders on a court clock, stalking-horse asymmetry, and a defensible audit trail

- Data Room for Restructuring — strategic vs distressed, and which track your mandate is actually on

- 12 Best Boutique M&A Advisors in Minneapolis for $5M-$200M Deals — Twin Cities regional advisor cluster (sector-specialist + diversified-generalist; entry point for sellers seeking the local banker, not the platform operator playbook)

- Best M&A Data Rooms (7-VDR Scored Comparison) — full product-comparison companion to this operator playbook

- How to Write a CIM (Confidential Information Memorandum) — the section-by-section authoring playbook for the book this room stages

- Sell-Side Due Diligence (VDD Scope Matrix + 8-Week Pre-Market Stack) — the seller-commissioned diligence the banker arranges in parallel to data-room setup

- M&A Process Explained (8 Phases, Real Deliverables) — the full M&A lifecycle the banker's data-room playbook sits inside

- M&A Due Diligence Process Guide — the buyer-side diligence framework your data room serves

- Clickthrough NDA in M&A Data Rooms — the NDA gate the banker uses to admit bidders to Tier A

- How to Spot Serious M&A Buyers Using Data Room Analytics — the page-level engagement signals that reveal which bidders genuinely intend to bid

- Data Room Folder Structure Guide — generic folder-structure companion (this post is sell-side-specific)

- Process Letter Mechanics in Independent Sponsor Deals — process-letter playbook for the closest-adjacent deal type

- Watermarking the CIM for Bidder-Identity Tracing — per-bidder forensic-watermark deep dive

For sell-side mandates specifically, Peony's data room — used by 5,900+ teams — handles the four-tier permission architecture out of the box, AI auto-indexing of the seller's 500-1,500 documents into the standard folder tree in under 3 minutes, per-bidder watermarking and screenshot blocking on every page render, a moderated Q&A workflow with AI-drafted answers and page citations (and fully isolated per-group Q&A threads on Peony Enterprise), and pre-scheduled permission-tier transitions that mechanically enforce the process letter. Peony Data Room at $52 per admin per month replaces the $15K-$50K Datasite passthrough most boutiques now meet client resistance on. Start free trial — no credit card required.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.

You might also like

Jun 10, 2026

Best Data Room for Multiple Bidders: One Room, Many Walls (2026)

Jun 5, 2026

Data Room Q&A: Run Diligence Questions Across Bidders Without Selective Disclosure (2026)

Jul 6, 2026

Datasite vs Ansarada: Parent vs Its Own VDR (2026)