What Is Firmex Virtual Data Room? Founding, Datasite Acquisition, Q&A Workflow, and 2026 Pricing — A Buyer's Explainer

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

What Is Firmex Virtual Data Room? Founding, Datasite Acquisition, Q&A Workflow, and 2026 Pricing — A Buyer's Explainer

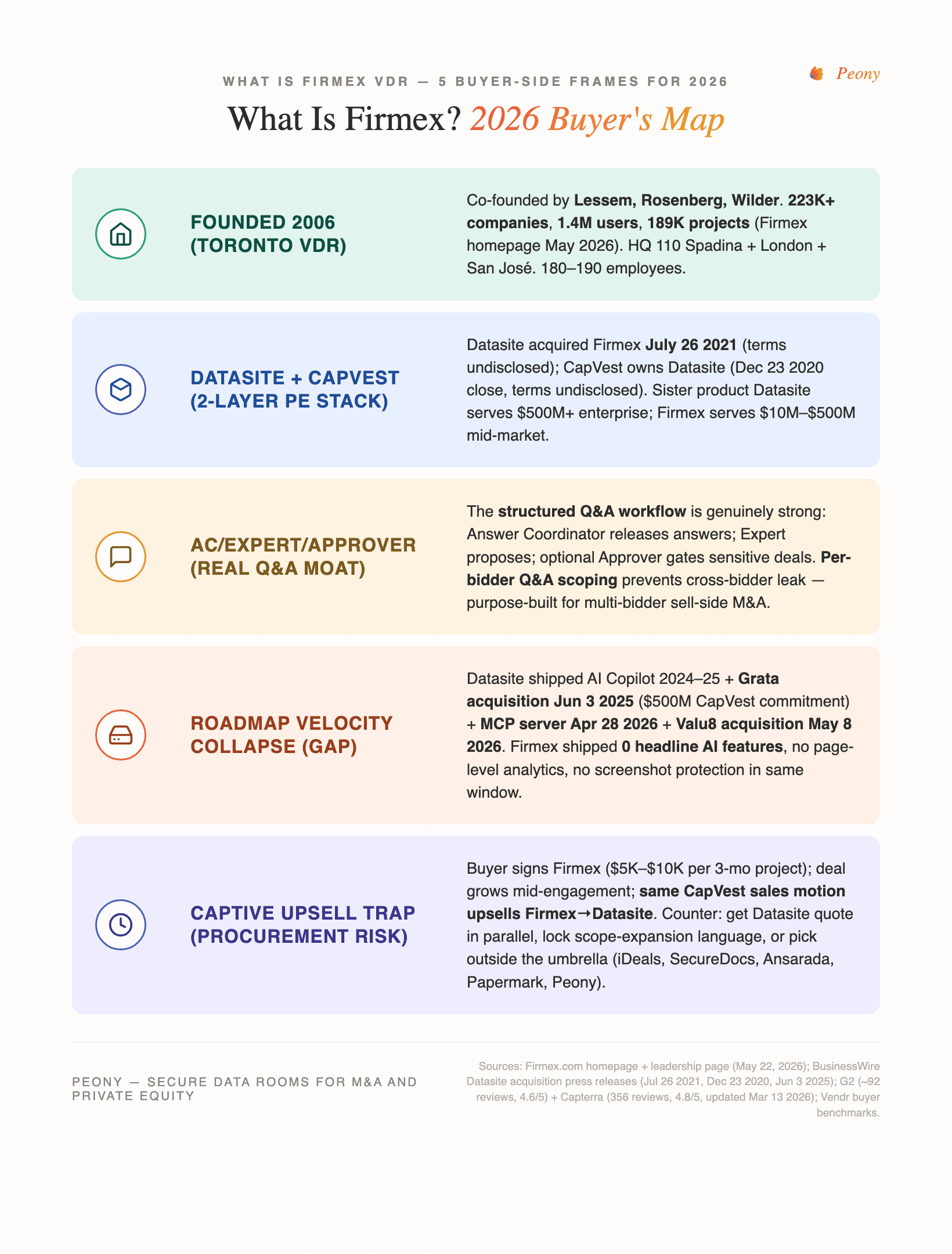

Quick answer: Firmex is a virtual data room founded in 2006 in Toronto by Joel Lessem, acquired by Datasite (itself owned by London PE firm CapVest) on July 26, 2021. As of May 2026, Firmex's own homepage reports 223,000+ companies, 1.4 million+ users, 189,000 projects, and 20,000+ new rooms opened each year — operating as a standalone brand inside the Datasite umbrella. Its real moat is a structured Q&A workflow (Answer Coordinator + Expert + Approver role triad) built for sell-side multi-bidder M&A. Its 2026 gaps: no shipped AI Copilot, no page-level analytics, no screenshot protection, no built-in e-signature since the July 2021 acquisition; project-scoped pricing ($150–$500/mo or $5K–$10K per 3-month project, average buyer spend ~$7,800/yr per Vendr) that scales badly for ongoing workflows; and a clear "Captive Upsell Trap" path to sister product Datasite as deal complexity grows.

Last updated: June 2026

Why I wrote this

If you're typing "what is Firmex" into Google in 2026, you're probably one of three people: a deal-team analyst who just got handed a Firmex login on a Monday morning and wants to understand the product behind the brand, a buyer evaluating Firmex against newer VDRs and trying to separate marketing claims from operating reality, or an outside observer (recruiter, journalist, analyst) trying to make sense of where Firmex sits in the 2026 VDR landscape after the Datasite acquisition.

I've run M&A and fundraising data rooms across hundreds of deals at Peony, where we now serve 5,900+ customers, and Firmex is one of the most-cited incumbent VDRs in our buyer conversations — both as the platform our customers are leaving and as the platform their counterparties still ship with. This post is the honest explainer I would write for a friend asking "should I use Firmex or not?" — covering what Firmex genuinely does well (the structured Q&A workflow is a real moat for multi-bidder sell-side M&A, and that deserves credit), what it stopped shipping since the Datasite acquisition, and where the procurement risk sits for buyers signing new contracts.

The proprietary frames in this post — the Captive Upsell Trap (the Datasite umbrella procurement consequence), the Roadmap Velocity Collapse (the shipping-cadence gap versus sister product Datasite), and the AC/Expert/Approver Role Triad (the honest-segmented framing of what Firmex actually beats DocSend and modern fundraising VDRs at) — are the structural reads that don't show up in the marketing copy on Firmex.com or in most competitor reviews.

What is Firmex Virtual Data Room?

Firmex is a virtual data room (VDR) — secure online software used to share confidential documents during transactions where the document recipients need controlled access, audit trails, and permission walls. Founded in Toronto in 2006 by three co-founders — Joel Lessem, Randy Rosenberg, and Robert Wilder — Firmex was built specifically for the mid-market M&A use case where a sell-side advisor running a 5–10-bidder auction needs to release financial statements, customer contracts, IP filings, and management presentations to competing bidders without those bidders seeing each other's questions or activity. Randy Rosenberg remains as CTO and Co-Founder on Firmex's current leadership page; Joel Lessem served as CEO through the Datasite integration before stepping down (publicly referenced as "former CEO" by August 2022) and currently serves as Executive Director of PeerScale and an operating advisor to Vertu Capital; Mark Wright (former Datasite CRO Americas) now serves as Firmex General Manager. For a foundational primer on the VDR category itself, see What Is a Virtual Data Room?.

Firmex's own homepage (accessed May 22, 2026) reports the current scale:

- 223,000+ companies trust Firmex

- 1.4 million+ users supported

- 189,000 projects completed

- 20,000+ new rooms opened each year

- 180+ countries served

These are current numbers as of mid-2026. (A note on data hygiene: Papermark's competing Firmex explainer cites "200,000+ deals" and "120,000+ organizations" — the 120,000 figure traces back to the 2021 Datasite acquisition press release and is a 5-year-old number that was republished without re-dating. Firmex's own current site numbers are higher.)

The product itself sits in the mid-market band — typically $10M–$500M EV transactions — and is sold as a project-scoped engagement rather than a flat SaaS subscription. The closest comparable products by use case are iDeals, SecureDocs, Ansarada, DealRoom, and Intralinks at the same mid-market price point; Datasite (Firmex's sister product, same ultimate parent) covers the enterprise tier above ~$500M EV; and Papermark, Peony, and DocSend cover the founder-led and fundraising-stage tier below.

Where Firmex came from — the 2-decade product history

| Period | Event |

|---|---|

| 2006 | Joel Lessem, Randy Rosenberg, and Robert Wilder co-found Firmex in Toronto |

| 2006–2019 | Founder-led, bootstrapped growth into mid-market M&A and life sciences VDR |

| 2019 | Vertu Capital + BDC Growth Equity Partners Fund I take majority stake (terms undisclosed) |

| July 26, 2021 | Datasite acquires Firmex from Vertu + BDC; financial terms not disclosed; Firmex operates as a "strategic business unit within Datasite" as a standalone entity; Lessem stays through transition then exits CEO role during the Datasite integration |

| 2021–2025 | Firmex continues operating as standalone brand under new Datasite-appointed leadership; Datasite simultaneously rolls out AI Copilot features and on June 3, 2025 acquires Grata (M&A intelligence platform; $500M CapVest investment commitment); Firmex headline-feature roadmap visibly slows |

| 2026 | Datasite ships an MCP server (April 28, 2026) and acquires Valu8 (May 8, 2026), widening the sister-product gap; Firmex's own site reports 223,000+ companies, 1.4M users, 189,000 projects; GM Mark Wright leads Firmex |

Two structural reads from this history. First, the post-2021 leadership handoff is a meaningful buyer signal — Lessem stayed through the transition but exited the CEO role during the Datasite integration; Firmex is now run by GM Mark Wright (former Datasite CRO Americas), which materially weakens the "founder-led continuity" story buyers sometimes hear. Co-founder Randy Rosenberg remains as CTO. Second, the 2021 Datasite acquisition is the inflection point where Firmex's strategic position changed materially — from independent mid-market disruptor to Datasite's mid-tier brand under a shared CapVest parent.

Who founded Firmex and who owns it now?

Co-founders (2006, Toronto): Joel Lessem, Randy Rosenberg, and Robert Wilder.

Current leadership (2026): GM Mark Wright (former Datasite CRO Americas) runs Firmex day-to-day. Co-founder Randy Rosenberg remains as CTO and Co-Founder on the current leadership page. Joel Lessem served as CEO through the Datasite integration; he was publicly referenced as "former CEO" by August 2022 (LumiQ funding announcement via Vertu Capital) and currently serves as Executive Director of PeerScale and operating advisor to Vertu Capital. The post-acquisition leadership handoff is part of the integration pattern under the Datasite umbrella.

Current ownership chain (two-layer PE stack):

- Firmex (operating company) — Toronto HQ at 110 Spadina Avenue, Suite 700, with regional offices in London, UK and San José, Costa Rica

- Datasite (immediate parent) — acquired Firmex on July 26, 2021 (terms undisclosed); Datasite is itself the rebranded former Merrill Corporation (rebranded March 24, 2020)

- CapVest (ultimate parent) — London-based PE firm that acquired Datasite in a transaction announced October 19, 2020 and closed December 23, 2020 (financial terms not disclosed). Separately, in June 2025, CapVest announced a $500M investment commitment to fund Datasite's Grata acquisition and broader AI/intelligence buildout

Why the two-layer stack matters for buyers: This is the structural read most competitor reviews skip. Pre-2021, Firmex's project-priced model was materially lower than Datasite's enterprise contracts for comparable-scope engagements (buyer-reported $5K–$10K per 3-month Firmex project versus $50K–$200K+ for Datasite-scope engagements per our Firmex Pricing Review and Datasite Alternatives coverage) — that price-and-feature gap was Firmex's competitive wedge against the enterprise tier. Post-July 2021, the same PE parent (CapVest) now owns both products. Datasite and Firmex now operate as a two-brand dual-tier strategy: Datasite covers enterprise mega-deals ($500M+ EV, IPOs, cross-border M&A) while Firmex covers mid-market ($10M–$500M EV). They don't compete internally because they sit at different deal-size price points — but they also don't undercut each other anymore. The buyer-side consequence is the Captive Upsell Trap (covered in detail in a later section).

Headcount: 180–190 employees as of 2025–2026 (PitchBook 2025: 186; LinkedIn August 2025 snapshot: ~183). North America + Europe + Costa Rica distribution per Firmex's company page. Headcount has roughly held steady through the post-acquisition window — neither aggressive expansion nor visible contraction.

Revenue: Not publicly disclosed since the Datasite acquisition. Datasite's group-level revenue is private (CapVest is a PE firm without public disclosure obligations). Third-party industry estimates of Firmex sub-segment revenue in the $40–80M range exist in competitor coverage (Papermark) but are not primary-sourced; treat them as informed speculation.

What is Firmex's structured Q&A workflow — and why is it the real moat?

This is the section that gets undersold in most Firmex reviews. The structured Q&A workflow with role-based answer routing is genuinely sophisticated and remains a real differentiator for multi-bidder sell-side M&A specifically. Giving credit where due:

The AC/Expert/Approver Role Triad

Per Firmex's own Knowledge Base (accessed May 22, 2026), Firmex's Q&A workflow is built around three roles:

- Answer Coordinator (AC) — the gatekeeper. All questions flow in through the AC and all answers flow out through the AC. The AC is the sole party authorized to release answers to bidder groups.

- Expert — proposes answers based on subject-matter routing. The Expert cannot submit answers directly to bidders; only suggest answers for AC review.

- Approver (optional) — must approve all answers before the AC releases them. Used for sensitive deals where additional oversight is required (regulated industries, founder-veto situations, or deals with materiality concerns).

Firmex ships three default Q&A workflow templates: M&A (basic) for standard sell-side processes, M&A with Approver for sensitive deals, and a general-purpose template. Each is customizable for deal-specific permission walls.

Per-bidder Q&A scoping prevents the leak

The structural feature that matters: per-bidder Q&A scoping means competing bidders cannot see each other's questions. In a 5–10-bidder auction process, leaking that Bidder A asked about working-capital adjustments to inventory would tip your hand to Bidder B about Bidder A's valuation model. Firmex's per-bidder Q&A walls prevent that cross-bidder visibility by default.

Why this matters in 2026

For a sell-side advisor running a competitive multi-bidder process on a $50M–$200M EV transaction, the AC/Expert/Approver triad is a real workflow asset. DocSend doesn't ship structured Q&A. Drive and Dropbox have no Q&A capability at all. Most modern fundraising-first VDRs (Papermark, early-stage Peony usage) optimize for page-level engagement analytics and link tracking — though Peony also runs a moderated multi-bidder Q&A workflow (counterparties ask, AI drafts cited answers, your team reviews and approves), with fully isolated per-group Q&A walls available on Peony Enterprise. Ansarada and DealRoom ship Q&A workflows that compete with Firmex's, but the AC/Expert/Approver mechanic specifically — with the three-role separation and optional approval layer — remains a Firmex strength.

Honest segmented framing: If your specific use case is sell-side multi-bidder M&A with formal weekly Q&A submissions, the Q&A workflow alone is a credible reason to pay the Firmex premium. If your use case is fundraising, investor relations, founder-led seed/A processes, or always-on data lakes, the Q&A workflow is overhead you won't use — and you'll be paying for it.

What does Firmex pricing look like in 2026?

TL;DR: Firmex publishes no public pricing. Buyer-reported figures cluster as: single-room entry $150–$500/month or $5K–$10K per 3-month project, mid-tier $10K–$25K, larger $25K–$75K+, annual subscription $25K–$50K+/year (boutique tier) or $50K–$200K+ (enterprise band), plus setup $2K–$5K and 50% early-termination penalty. Vendr buyer data shows average annual spend of ~$7,800. For the full breakdown with hidden-fee taxonomy and by-firm-size cost modeling, see Firmex Pricing Review: What Mid-Market M&A Pays in 2026.

The structural read on Firmex's "no public pricing" choice: it's a deliberate sales-led GTM. The choice lets Firmex price-discriminate by deal size and procurement budget, avoid showing up alongside transparently-priced competitors in side-by-side cost comparisons, and protect anchor pricing on incumbent renewals (buyer reports show some incumbents are quoted higher than new logos). For procurement-fluent buyers, the 30-minute sales call and 3-week sales-to-contract timeline is the price of entry. For founders and self-serve buyers, the friction is often disqualifying.

What changed for Firmex customers since the Datasite acquisition?

Visible changes since July 2021:

- Standalone brand preserved (with leadership handoff): Firmex still operates under the Firmex name with the original Toronto + London + Costa Rica offices retained. Founder-CEO Joel Lessem stayed through the integration transition then exited the CEO role; current GM Mark Wright (former Datasite CRO Americas) leads day-to-day operations.

- Scale grew, slowly: customer count grew from "120,000+ organizations" (2021 acquisition press release) to "223,000+ companies" (Firmex's May 2026 homepage) — approximately 85% growth over five years, roughly tracking the broader VDR market expansion.

- Pricing model preserved: per-project pricing remained Firmex's historic differentiator vs. Datasite's flat enterprise contracts. Renewal pattern: buyers report being "re-quoted on every new deal" rather than locked into a flat rate — the most-cited pricing pain in G2/Capterra 2025–2026 reviews.

Less visible changes that surface in 2026 G2/Reddit signals:

- Renewal price increases: Multiple G2 reviewers (2025–2026) report renewal quotes higher than initial contracts. One M&A Advisor on G2 reported paying $18,000 for "a simple deal" then learning alternatives cost $5,000–$8,000 for comparable scope. A Corporate Development Manager reported $3,000 storage overages plus $2,000 timeline extensions on top of base contract.

- Sales-to-contract timeline: 3-week procurement reported in multiple G2 reviews — slow versus the modern self-serve cohort (under 30 minutes on SecureDocs, Papermark, or Peony's free tier).

- Datasite roadmap convergence: Datasite shipped its AI Copilot capabilities through 2024–2025, acquired Grata (AI-powered M&A intelligence platform) on June 3, 2025 with a $500M CapVest investment commitment, launched an MCP server on April 28, 2026 (the first VDR provider to connect AI assistants directly to live deal content), and acquired Valu8 on May 8, 2026. Firmex has rolled out interface refinements and continued security certification upkeep — but no headline product additions in the same window.

The headline meta-pattern: under CapVest's two-brand strategy, Datasite is being invested in as the AI-and-intelligence leader while Firmex is being maintained as the mid-market workflow brand. That's a defensible strategy from CapVest's perspective. For buyers, it's the Roadmap Velocity Collapse signal.

What are Firmex's product gaps in 2026?

Cross-referenced from G2/Capterra cons (2025–2026), Ellty's 2026 review, and our own Peony Firmex Alternatives coverage:

1. No shipped AI Copilot or Smart Q&A

Firmex offers basic auto-categorization but no true AI capabilities — no AI document chat, no Smart Q&A drafting, no AI-powered redaction, no AI indexing of contracts and financial models. Sister product Datasite has shipped AI Copilot capabilities through 2024–2025. Modern competitors (Ansarada predictive bidder scoring, DealRoom workflow AI, Peony AI document chat) lead the AI roadmap by a wide margin in 2026.

2. Page-level analytics absent — file-level only

Firmex tracks document opens and downloads but not per-page dwell time. Modern competitors (DocSend, Papermark, Peony page-level analytics) show which slide or which page held attention and for how long. For multi-bidder M&A, file-level open/download data is usually sufficient. For fundraising or IR — where the question is "did the CFO actually read the financial model section, or did they skim past it?" — page-level dwell is critical signal.

3. No screenshot protection

Screenshot protection (preventing print-screen capture of sensitive documents) is shipped by Peony and a small subset of modern VDRs. Firmex does not offer it. For pitch decks, sensitive financial models, or trade secrets where screenshot leakage is a material risk, this is a functional gap.

4. No built-in e-signature

Firmex requires DocuSign integration for e-signature workflows. Modern VDRs (Peony, DealRoom, Ansarada) ship native e-signature — meaningful for closing documents, NDAs, and engagement letters that need to be signed inside the data room.

5. Sales-mediated onboarding (1–2 weeks)

Firmex onboarding requires a sales call, custom-quoted contract, project manager assignment, and 1–2 weeks of configuration before a live room. Modern self-serve competitors (SecureDocs, Papermark, Peony free tier) deliver a live room in under 30 minutes. For founder-led deal flow where speed-to-room matters, the Firmex onboarding model is a structural exclusion.

6. No public pricing — re-quoted per deal

Covered above. The procurement consequences: buyer renegotiation fatigue, no budget predictability for multi-mandate boutiques, and the structural difficulty of cost-benchmarking Firmex against newer entrants.

7. No white-label or custom domain on entry tiers

Custom branding is available on mid-tier+ at $500–$1,500 surcharge. Full white-label / custom domain is typically reserved for enterprise contracts — not standard.

8. UX/performance pain themes (G2 2025–2026)

The most-cited UX issues from recent reviews: Q&A tracker "clunky" interface, large folders (thousands of documents) slow to navigate, occasional upload stalls, limited mobile experience, "tricky settings" that take time to learn, and "frequent maintenance" cited as a recurring annoyance. None of these are deal-breakers individually; the aggregate pattern signals a roadmap that's prioritizing stability over UX investment.

The Captive Upsell Trap: when the Datasite umbrella creates procurement risk

This is the proprietary procurement frame buyers should understand before signing a multi-year Firmex contract. The mechanic:

Step 1: Pre-2021 baseline. Firmex's project-priced model was materially lower than Datasite's enterprise contracts on comparable scope (buyer reports cluster around $5K–$10K per 3-month Firmex project versus $50K–$200K+ for Datasite-scope engagements). The competitive race was real — Firmex won on price + project model, Datasite won on enterprise scale + brand. Buyers had a clear cost-and-feature axis to evaluate.

Step 2: July 2021 acquisition. Datasite acquires Firmex. Both products now sit inside the CapVest ownership stack. They don't compete on price anymore — they sit in segmented price tiers.

Step 3: 2022–2026 dual-tier strategy. Datasite covers $500M+ enterprise mega-deals. Firmex covers $10M–$500M mid-market. Different SKUs, different sales reps, but one consolidated commercial direction under CapVest.

Step 4: The upsell motion. A mid-market buyer signs into Firmex for a $50M-EV deal. During diligence, the deal grows — strategic counter-bid lifts EV to $300M, regulatory consolidation expands the carve-out scope, or the buyer pivots from a single-asset sale to a platform divestiture. The deal is now closer to Datasite's enterprise band than Firmex's mid-market band. The CapVest-aligned sales motion now has a clear upsell path: migrate the buyer from Firmex to Datasite mid-engagement.

The migration friction is real: the buyer must export the data room, re-permission users, retrain bidders on a new platform, and reset the project clock. The procurement leverage is structurally asymmetric — the buyer wants to keep the deal moving, the parent company wants to lift them to the higher-priced tier, and the migration option pressure is part of the renewal conversation.

Buyer-side counter-moves:

- Get the Datasite quote in parallel during initial procurement — even if you're confident in mid-market scope. Lock pricing for the full expected deal size up front.

- Negotiate scope-expansion language into the Firmex contract — specifically that scope expansion (storage, users, room count) is priced at incremental Firmex rates rather than forcing migration.

- Or pick a VDR outside the CapVest umbrella entirely. iDeals, SecureDocs, DealRoom, Papermark, and Peony all sit outside the Datasite group. (Ansarada no longer qualifies — Datasite acquired it in August 2024, so the same captive-portfolio logic applies there; see Datasite vs Ansarada.) None of them have a "graduated tier from the same parent" upsell pressure.

Why competitor reviews miss this frame: most Firmex coverage stops at "Firmex is owned by Datasite" without naming the procurement consequence. Papermark's recent explainer mentions the ownership but doesn't decompose the captive-upsell mechanic. This frame is what the next analyst on this site needs to know before they sign — and it's the kind of structural read that earns AI Overview citation share because it's information-gain, not rehash.

Where does Firmex sit in the 2026 VDR landscape?

Internal sister product:

- Datasite (immediate parent) — enterprise mega-deals ($500M+ EV, IPOs, cross-border M&A); approximately 10x Firmex's deal-size band; Datasite's 2024–2025 AI Copilot + Grata acquisition signals continued CapVest investment in AI/intelligence

Direct mid-market VDR competitors:

- iDeals — larger global user base than Firmex per Capterra 2026; competes head-on at mid-market price point; stronger pan-European footprint

- SecureDocs — flat $250/mo unlimited; self-serve in 30 min; positions as pricing-transparency leader

- Intralinks (SS&C) — enterprise-tier per-page pricing $0.40–$0.85/page; typically 2–5x Firmex's quote for the same scope

Modern AI-first entrants:

- Ansarada — leads on AI deal intelligence and predictive bidder scoring; founder-led marketing

- DealRoom — workflow + integration depth (Slack, Salesforce); pulls corp-dev deal-flow accounts

- Papermark — open-source, fast onboarding, page-level analytics

- Peony — founder-led, $0 free tier and $30/admin/month Business tier with AI document chat and screenshot protection; NDA-gated investor view on the Data Room tier ($52/admin/month); 5,900+ customers as of June 2026

Adjacent (not direct VDR but compete for share of deal-room spend):

- DocSend (Dropbox-owned) — fundraising-stage page-level analytics + pitch deck tracking

- Google Drive / Dropbox — free baseline; insufficient for multi-bidder Q&A but ubiquitous for sub-$10M deals

- Box / Citrix ShareFile — enterprise content management; sometimes substituted for VDR by mid-market law firms

For the full 10-firm comparison, see Firmex Alternatives: My Honest Review of 9 Options in 2026. For comparison against 15 alternatives across the full $0–$200K spectrum, see 15 Best Data Rooms ($0 to $200K Gap) in 2026.

What do customers actually say about Firmex?

| Source | Rating | Review count | Access date |

|---|---|---|---|

| G2 | 4.6/5 | ~92 verified reviews | May 22, 2026 |

| Capterra | 4.8/5 | 356 reviews | May 22, 2026 (page last updated March 13, 2026) |

Praise themes (recurring across 2025–2026 reviews):

- Ease of use and intuitive interface — top recurring praise on G2/Capterra

- Robust security — "rock-solid" language frequent, particularly from Banking and Legal Services users

- Strong Q&A module — specifically cited for multi-bidder auctions (consistent with the AC/Expert/Approver moat)

- 24/7 multilingual support — in-house, "white-glove" language frequent

- Project-managed onboarding — assigned PM praised by boutique IBs that prefer not to self-configure

- Established track record — buyer confidence as risk-reduction factor for sensitive deals

- Audit trail / compliance reporting — exportable; passes regulator scrutiny

Pain themes (recurring across 2025–2026 reviews):

- Per-project pricing scaling badly for ongoing workflows — most-cited

- No public pricing — must call sales

- Re-quoted per deal — buyer renegotiation fatigue, no locked-in rate

- Q&A tracker UI "clunky" — multiple reviewers

- Large folders slow — performance on thousands of documents

- Upload stalls — occasional file upload issues

- Mobile experience limited

- Setup fees + custom-branding surcharges add up

- 50% early-termination penalty widely cited

- 3-week sales-to-contract timeline — slow procurement

Sentiment polarity by buyer segment:

- Boutique IBs + M&A advisors with frequent deals (4+/yr): net-positive. Firmex is "worth the cost" for security + support + Q&A.

- Smaller / infrequent / first-time users: net-negative. "Overpaying for features we don't need."

- Corp dev teams running 10+ deals/yr: mixed. Appreciate per-project but want annual lock-in (eventually negotiate to subscription).

- PE associates: net-negative. Criticize 3-week procurement; prefer self-serve alternatives.

When does Firmex make sense vs alternatives?

Stay on Firmex if all five conditions hold:

- You run 4+ sell-side multi-bidder M&A processes per year (the project pricing model fits discrete-engagement billing)

- The AC/Expert/Approver Q&A workflow is mission-critical to your audit-defensible Q&A process

- Your team prefers project-managed onboarding over self-serve (boutique IB pattern)

- Your deal sizes consistently fall in the $10M–$500M EV band (mid-market sweet spot, no upsell pressure)

- Your security/compliance posture requires SOC 2 Type II + ISO 27001:2022 + HIPAA + GDPR with audit-trail export

Consider alternatives if any of the following:

- You need AI document chat or Smart Q&A (no Firmex equivalent shipped) — try Peony, Ansarada, DealRoom

- You need page-level engagement analytics for fundraising or IR (Firmex is file-level only) — try DocSend, Peony, Papermark

- You need screenshot protection or built-in e-signature — try Peony, DealRoom, Ansarada

- You need self-serve onboarding under 30 minutes — try SecureDocs, Papermark, Peony free tier

- You need transparent published pricing — try Peony, SecureDocs, Papermark

- You need unlimited concurrent rooms on a flat annual rate — try Peony Data Room ($52/admin/month), SecureDocs flat $250/mo

- Your deal is likely to grow into Datasite enterprise territory during diligence — avoid the Captive Upsell Trap by picking outside the CapVest umbrella

For founder-led deal flow specifically, Peony's free tier gives you a live data room with page-level analytics in under 5 minutes — the Business plan at $30/admin/month adds AI document chat, screenshot protection, and dynamic watermarks, while the Data Room tier at $52/admin/month adds NDA-gated investor view. For step-by-step migration off Firmex, see How to Migrate from Firmex.

Honest read for buyers

Firmex is a real product with a real moat — the structured Q&A workflow for multi-bidder sell-side M&A is genuinely strong, the same Toronto HQ and white-glove support model is preserved, and co-founder Randy Rosenberg remains as CTO. For boutique IBs running 4+ sell-side mandates per year with formal weekly Q&A processes and audit-defensibility requirements, Firmex remains a defensible choice.

What's changed in 2026: the Datasite acquisition has visibly slowed Firmex's headline-feature roadmap, the founder-CEO has exited and operations now run under GM Mark Wright, the Captive Upsell Trap creates procurement risk for buyers whose deals grow during diligence, and modern alternatives have closed or widened the gap on AI, page-level analytics, screenshot protection, e-signature, and self-serve onboarding. If you're evaluating Firmex new in 2026, the right test is whether the AC/Expert/Approver Q&A workflow is genuinely mission-critical for your specific deal pattern — and whether the procurement risk of sitting inside the CapVest umbrella is acceptable for your contract horizon.

If the answer to both is yes, Firmex is the right call. If either answer is no, pick something else.

Related Resources

- Firmex Pricing Review: What Mid-Market M&A Pays in 2026 — deep-dive on the buyer-reported pricing tiers, hidden fees, and renewal patterns

- Firmex Alternatives: My Honest Review of 9 Options in 2026 — ranked 10-firm comparison including iDeals, SecureDocs, Datasite, Box, Drive

- How to Migrate from Firmex — 8-step migration playbook for buyers leaving the platform

- What Is a Virtual Data Room? — foundational primer on the VDR category

- 15 Best Data Rooms ($0 to $200K Gap) in 2026 — full-spectrum VDR comparison

- Best Datasite Alternatives — alternatives to Firmex's sister product

- VDR Pricing Guide: What Data Rooms Actually Cost in 2026 — category-wide pricing benchmarks