How to Write a CIM (Confidential Information Memorandum) — 2026 Guide

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

How to Write a CIM (Confidential Information Memorandum)

Quick answer: A Confidential Information Memorandum (CIM) is the named, 40-80 page document you send a buyer — after they sign an NDA — to market your company for sale. It is not a teaser (the blind 1-2 page profile that goes out first) and it is not a venture pitch deck (built to sell vision, not a whole company on proven numbers). A strong CIM follows a stable section order — cover and disclaimer, executive summary, investment highlights, company and market overview, customers, management, historical financials with add-backs, projections, growth, and transaction terms — but the part that actually wins deals is the front and the financials, because buyers spend roughly 90% of their attention there. Three rules separate a CIM that sells from a binder nobody finishes: write it thesis-first (a narrative with evidence, not a data dump), draft for the buyer's read-order, and obey the reconciliation mandate — every number must tie to a document in your data room, because the buyer's quality-of-earnings team will check, and add-back disputes are a leading driver of re-trades. Distribute it NDA-gated, watermarked, and tiered through a data room, never by email.

Last updated: June 2026

Why I wrote this

I'm Deqian Jia, co-founder of Peony, a data room company. A huge share of the documents that pass through our platform are CIMs — it's usually the first sensitive thing a seller hands a buyer, and the moment it leaves your hands, everything about how you wrote and distributed it starts working for you or against you. We now serve more than 5,900 customers, and I've watched enough sell-side processes to know that the CIM is the highest-leverage document most founders will ever write and the one they're least prepared for.

There's plenty written about what a CIM is. There's much less on how to actually write one that holds up — how to structure it for the way buyers read, how to present add-backs that survive diligence, and how to distribute it without leaking to a competitor. That's the gap this guide fills. It's the playbook I'd hand a first-time seller or a junior deal lead staring at a blank page, and it's deliberately scoped to the writing and distribution craft: for the deeper buyer-scoring and watermarking mechanics, I link out to our existing guides rather than repeat them.

What is a CIM, and do you actually need one?

A Confidential Information Memorandum is the detailed, named document that markets your company to qualified buyers after they've signed a non-disclosure agreement. It goes by several names — offering memorandum (OM), information memorandum (IM), confidential information presentation (CIP), or just "the book" — and in a private M&A sale they all mean the same thing. (One thing it is not: a private placement memorandum, or PPM, which is a regulated securities-offering document. Different document, different rules.)

Do you need one? For essentially any advised sell-side process above roughly $5M in enterprise value, yes. The CIM is what turns interest into an indication of interest, and the competitive tension it creates across multiple buyers is usually worth far more than the effort of producing it — advisors routinely describe a strong CIM as adding a turn or two of EBITDA to the final price. The exceptions are narrow: a sub-$2M Main-Street business can often be sold on a shorter package, and a genuinely bilateral deal with one motivated buyer may run lighter. But even then, the discipline of writing a real CIM — forcing yourself to articulate the thesis, normalize the numbers, and anticipate diligence — is what keeps you from leaving money on the table or walking into a re-trade.

If you already have a strong inbound offer, the move usually isn't to skip the CIM — it's to use it to quietly run a tight process and create at least one competing bid. Our Cleveland M&A advisor guide walks through that "unsolicited offer" scenario in the context of a real metro deal market.

What goes in a CIM? The section-by-section structure

There is no legally mandated CIM format, but a stable order recurs across the authoritative guides. Here is the canonical backbone for a lower-middle-market CIM, with what each section is for:

| # | Section | What it does |

|---|---|---|

| 1 | Cover page + confidentiality disclaimer | Project codename (not your company name on blind versions), "Confidential" legend, and the no-offer / no-reliance / no-unauthorized-contact disclaimer block. Have counsel review it. |

| 2 | Table of contents | Navigation. |

| 3 | Executive summary | The single most important section — the investment thesis in 1-2 pages: what the company is, why it's a compelling acquisition, why now, headline financials, and the transaction summary. |

| 4 | Investment highlights | The bulletized buy-case: 4-8 punchy reasons (market position, growth, margins, moat, management, diversification). |

| 5 | Company overview & history | Founding story, milestones, ownership and legal structure, locations, business model. |

| 6 | Products & services | What you sell, revenue mix by line, pricing model, proprietary technology / IP. |

| 7 | Market & industry overview | TAM, growth rates, tailwinds, regulation — sourced to third parties (so buyers can independently verify it). |

| 8 | Competitive positioning | The landscape, your share, your differentiation, barriers to entry. |

| 9 | Customers & suppliers | Segments, retention, and customer concentration as a percentage of the top 5/10/20 — anonymized pre-LOI. Key supplier dependencies. |

| 10 | Operations & facilities | Footprint, facilities and leases, supply chain, capacity, systems. |

| 11 | Management team & org chart | Bios of key people, structure, headcount, and the post-close continuity picture. |

| 12 | Historical financials + add-backs | Three years of P&L, and the bridge from reported EBITDA to adjusted EBITDA via documented add-backs. |

| 13 | Financial projections | A 3-5 year forecast with stated assumptions. |

| 14 | Growth opportunities | The specific, credible levers a buyer is really paying for (new geographies, products, M&A, pricing, share gains; synergy hooks for strategics). |

| 15 | Transaction overview & bid instructions | How to bid: process structure, timeline for IOIs/LOIs, what an indicative offer should contain, contact protocol. Usually near the end. |

| 16 | Appendices | Detailed schedules, specs, certifications, supporting charts. |

Build the front (sections 3-4) and the financials (12-13) first and hardest. They carry the deal. The middle sections are reference material — necessary, but not where buyers decide. The same backbone maps directly onto your data room folder structure, which is covered in our M&A data room guide.

How long should a CIM be, and how long does it take to write?

Most lower-middle-market CIMs run 40-80 pages. Published ranges disagree — Papermark and similar guides cite 30-70, Mergers & Inquisitions describes 50-plus, and Firmex notes large-deal books "often more than 100 pages" — but the high counts skew to large, complex transactions, not a $5M-$100M company. Length should track complexity, not effort: a tight 50-page CIM that leads with a clear thesis outperforms a padded 120-page one that buries it.

On timeline, separate two clocks. The drafting of the document is about 2-4 weeks. The data-gathering that feeds it — pulling clean financials, normalizing the add-backs, assembling contracts and org detail — is what stretches the calendar to two or three months. In a typical 2025 sell-side timeline, preparation (including the CIM and teaser) is the 2-4 week front end of a 9-12 month process (Sampford Advisors, 2025). If your financials aren't ready, that's your binding constraint — which is why CIM prep and data room prep should happen together.

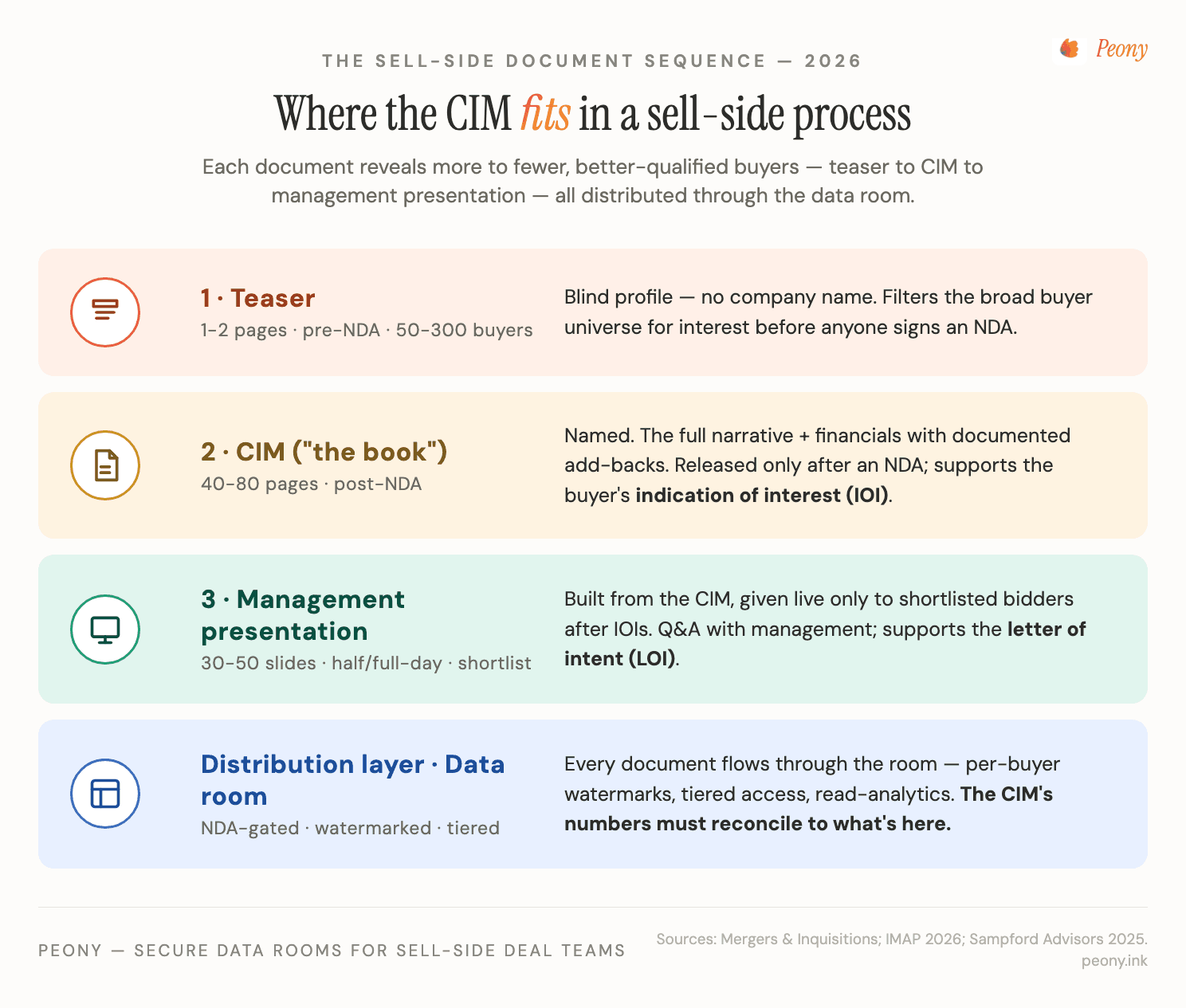

CIM vs teaser vs pitch deck vs management presentation — what's the difference?

These get conflated constantly, so here's the clean separation:

| Document | Length | Named? | Stage | Job |

|---|---|---|---|---|

| Teaser | 1-2 pages | Blind / anonymous | Pre-NDA, sent broadly (50-300 buyers) | Filter for interest without revealing identity |

| CIM | 40-80 pages | Named | Post-NDA, to qualified buyers | Carry the full narrative + financials; support the IOI |

| Management presentation | 30-50 slides; half- to full-day | Named (in person) | Post-IOI, shortlisted bidders only | Live Q&A; supports the LOI |

| Startup pitch deck | ~10-20 slides | Named | Fundraising, not M&A sale | Sell vision to raise capital — a different document for a different purpose |

The sell-side sequence is teaser → NDA → CIM → IOI → management presentation → LOI: each step reveals more to fewer, better-qualified buyers. A common first-timer error is treating a venture pitch deck as a CIM. They overlap in spirit but not in standard — a pitch deck sells a forward story; a CIM sells a whole company on proven numbers and is held to a diligence standard. If you're repurposing fundraising materials, see how to convert a pitch deck into a data room for where the two genuinely connect.

Frame 1 — Why write the CIM thesis-first? (A narrative with evidence, not a binder of facts)

The most common failure mode is the data-dump CIM: every fact the seller could think of, in no particular argument, across 100 pages nobody finishes. The fix is to decide your investment thesis before you write a word — one sentence a buyer could repeat to their investment committee. Something like: "Market-leading specialty manufacturer growing 15% a year, taking share through a proprietary process, with 25% EBITDA margins and a second-line management team that stays post-close."

Once you have that sentence, every section becomes evidence for it. The market section proves the growth is real; the competitive section proves the share gains are defensible; the financials prove the margins; the management section proves continuity. A reader should be able to trace each part of the thesis to a section that supports it. This is also the cleanest way to decide what to cut: if a chart doesn't support the thesis, it belongs in the data room, not the CIM. The CIM is the argument; the data room is the repository of raw data. Conflating the two is what produces the binder nobody reads.

Frame 2 — Where do buyers actually look? The 90/10 read-order rule

Buyers and their bankers do not read a CIM front to back. They spend the overwhelming majority of their attention — call it 90% — on two places: the executive summary / investment highlights at the front, and the financials and add-backs toward the back. The history, operations, and facilities sections are reference material they skim.

So your drafting effort should mirror the reading effort. The executive summary deserves more revisions than any other section because it decides whether a buyer reads on or passes. The financial section deserves the most rigor because it decides the multiple. The middle of the book should be complete and accurate, but you should not pour your best hours into polishing the facilities overview while the executive summary is a first draft. Build for the buyer's eye-path, not the table of contents. Once the CIM is out, you can see this read-order play out in real time — which buyers actually reach the financials, and how often they return — through data room analytics.

Frame 3 — Why must every number tie to the data room? The reconciliation mandate

Here is the rule that ties the whole document together: a CIM is simultaneously a sales document and a diligence anchor. It's the pitch — and it's also the index against which the buyer's quality-of-earnings team will run diligence, pulling source data straight from your data room. The instant the CIM's adjusted-EBITDA bridge, customer-concentration percentages, or projection base don't reconcile to what's actually in the room, the conversation flips from "how much will we pay" to "what else is wrong here" — and the re-trade begins.

This is why add-back discipline matters so much. Add-back disputes are a leading driver of post-LOI re-trades, and every dollar a QoE review strips out of EBITDA is multiplied by your 5-15x multiple and removed from the price; a typical QoE pass reduces claimed adjusted EBITDA by 5-15%. So before you publish any number in the CIM, ask: can I produce the document in the data room that proves this? If not, it doesn't go in. The reconciliation mandate is the single highest-return habit in CIM writing — it's the difference between a CIM that anchors your price and one that quietly hands the buyer a list of things to chip away at.

The division of labor is worth stating plainly: the CIM is where the story lives; the room stays reconciliation-grade. Buyer-side diligence teams are floor readers working a checklist, which is why the storytelling that wins a fundraise can backfire in a sale process — the narrative data room guide draws that line (its Ceiling/Floor Test) if you're tempted to make the room itself the persuasion artifact. Persuade in the CIM; prove in the room.

How do you present financials and add-backs without losing credibility?

Show a clean bridge from reported EBITDA to adjusted EBITDA, with each adjustment itemized and defensible:

- Owner compensation normalization — adjusting above- or below-market owner pay to a market salary for the role.

- Genuinely one-time items — a lawsuit settlement, a one-off system migration, a single non-recurring write-off.

- Discretionary expenses that won't transfer to a buyer — personal vehicles, club memberships, family on payroll who don't work in the business.

Avoid the traps that QoE teams are specifically hunting for: labeling recurring costs (annual legal fees, routine bonuses) as "non-recurring"; double-counting (adding back severance and the full restructuring line); and claiming a run-rate you haven't sustained for at least a quarter or two. The discipline test for every add-back: could you defend it, with documentation, to a skeptical analyst? Present three years of historical P&L, a summary balance sheet and cash flow, and a projection model with assumptions you can support. Then make sure all of it reconciles to the underlying files — which is also the heart of sell-side due diligence prep.

How do you distribute a CIM securely without leaking to competitors?

The distribution workflow is as important as the writing. Three rules:

- NDA-gate the named CIM. The blind teaser goes out broadly; the named CIM is released only after a buyer signs an NDA. Bundling the teaser and NDA so buyers sign to unlock the book is standard practice.

- Watermark and stage access through a data room — never email. Distribute through a virtual data room with dynamic, per-buyer watermarking (every page carries the viewer's name, email, and timestamp — a deterrent and a forensic trail), and stage access in tiers so sensitive detail (real customer names, contracts, pricing) is withheld until a buyer is shortlisted post-LOI. The mechanics are in watermarking a CIM and the tiered-access model in our investment-banking data room guide.

- Anonymize competitively sensitive detail pre-LOI. Use "Customer A" rather than names, withhold proprietary specs, and only open the full room to bidders who've demonstrated commitment.

This is the exact workflow we built Peony for, and it's used across 5,900+ customers' deals: NDA-gated release, per-buyer watermarking, tiered visitor groups, and page-level analytics so you can see who's actually reading. Email a CIM as a loose PDF and you've lost both control and the ability to know who's serious.

Should you write it yourself or hire a banker — and what does it cost?

In an advised sale, your M&A advisor leads the CIM, and its preparation is bundled into the engagement — typically covered by the retainer, which is usually credited against the success fee at close. You're not buying a CIM as a line item; you're hiring a sell-side advisor whose fee includes producing one that survives diligence. That's worth paying for: analysts and associates build CIMs full-time precisely because the financials and add-backs have to hold up against a buyer's QoE review.

Could you write it yourself? For a very small or unadvised sale, a structured template plus a fractional M&A consultant is the floor — but a founder-written CIM tends to read like a pitch deck and to make add-back claims that collapse under scrutiny. The best outcomes come from a tight founder-plus-banker collaboration: you supply the deep knowledge of customers, moat, and growth levers; the banker supplies the structure, the defensible financial presentation, and the buyer relationships. For how CIM prep sits inside advisor fees and where the broker/advisor/bank line falls, see our M&A advisor fees guide and the advisor selection hub.

What are the most common CIM mistakes?

The recurring, deal-slowing errors, in rough order of how much they cost:

- Aggressive or undocumented add-backs — a leading driver of post-LOI re-trades. Every unsupported dollar gets multiplied by your multiple and removed from price.

- Numbers that don't reconcile to the data room — the fastest way to turn a buyer from "how much" to "what else is wrong."

- No clear investment thesis — a data dump with no spine; nobody can repeat your buy-case.

- Over-optimistic projections that collapse in diligence and poison trust in the entire document.

- Length without focus — padding to 100-plus pages buries the thesis instead of strengthening it.

- Disclosing competitively sensitive detail too early — real customer names, pricing, or proprietary specs handed to a buyer who might be a competitor.

Every one of these traces back to the same root: forgetting that a CIM is both a sales document and a diligence anchor. Write it to be compelling and verifiable, and most of these mistakes disappear.

Bottom line

A CIM is the highest-leverage document in a sell-side process and the one first-time sellers are least ready for. Write it thesis-first so it's a narrative with evidence rather than a binder of facts; draft for the buyer's read-order, pouring your best hours into the executive summary and the financials where buyers actually spend their attention; and obey the reconciliation mandate, because the buyer's quality-of-earnings team will check every number against your data room and add-back disputes are what trigger re-trades. Keep it to a tight 40-80 pages, have your advisor lead the drafting, anonymize sensitive detail, and distribute it NDA-gated and watermarked through a data room rather than email. Do that, and the CIM does its job: it earns the indication of interest, withstands diligence, and protects your price all the way to close.

Related resources

- M&A Data Room: Setup and Workstream Mapping — where the CIM's claims live as verifiable source documents

- How to watermark a CIM with buyer identity and timestamps — the leak-deterrent and forensic-trail mechanics for distributing the book

- How data room analytics spot serious buyers — reading who actually engaged with your CIM, and which page predicts an LOI

- Investment-banking data room guide — the tiered bidder-access architecture for staging CIM and diligence materials

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — getting the financials and add-backs ready to survive a buyer's QoE

- M&A advisor fees: what you actually pay — how CIM preparation sits inside the retainer and success fee

- M&A advisor vs business broker vs investment bank — who should be drafting and running your process in the first place

- Best M&A Advisors in Cleveland — a worked example of a real metro deal market, advisors, and the unsolicited-offer scenario

Footnotes and sources

- Mergers & Inquisitions — Confidential Information Memorandum: Detailed Guide + Examples (the "90% of attention on two sections" read-order point)

- IMAP — CIM vs. Teaser: What Goes In Each and Why It Matters (2026; CIM as "a curated, coherent narrative, not a repository of raw data")

- Sampford Advisors — A Typical Sell-Side M&A Process Timeline (2025; preparation, NDA/IOI, management presentation, and confirmatory-DD phase lengths)

- Axial — 12 Lessons to Build a Successful Buyer List (2023 platform data on buyer-list-to-NDA conversion)

- Firmex — Beyond the Numbers: Finding the "Story" in the CIM (firmex.com; CIM narrative and large-deal length context)

- Wall Street Prep — Confidential Information Memorandum (CIM) (who drafts the CIM)

- Corporate Finance Institute — CIM (Confidential Information Memorandum) (section overview)

- Divestopedia — Confidential Information Memorandum, Teaser, Bid Instructions (definitions and document distinctions)

You might also like

May 30, 2026

M&A Advisor Fees: Lehman Scale, Retainers & Hidden Clauses (2026)

May 28, 2026

12 Best M&A Advisors in Pittsburgh for $1M-$300M Deals (2026 Guide)

May 23, 2026

Investment Banking Data Room (2026): The Sell-Side Banker's Playbook